CE 466 FE Exam Review Engineering Economics Spring 2013.

69

CE 466 FE Exam Review Engineering Economics Spring 2013

-

Upload

aisha-gillins -

Category

Documents

-

view

249 -

download

11

Transcript of CE 466 FE Exam Review Engineering Economics Spring 2013.

CE 466 FE Exam Review

Engineering Economics

Spring 2013

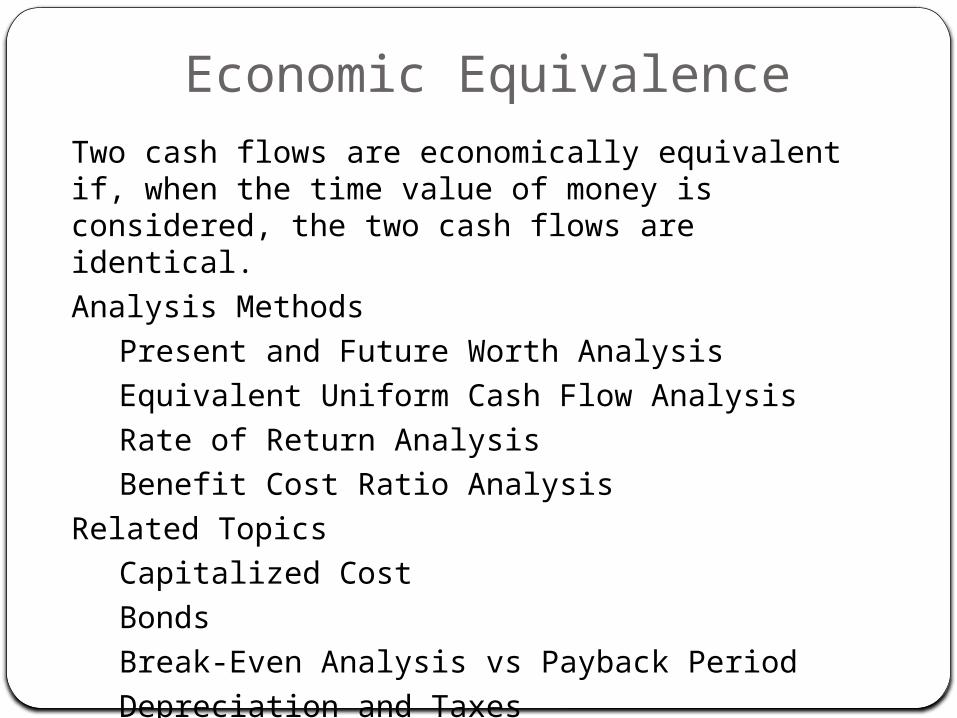

Economic Equivalence Two cash flows are economically equivalent if, when the time value of money is considered, the two cash flows are identical.Analysis Methods

Present and Future Worth AnalysisEquivalent Uniform Cash Flow AnalysisRate of Return AnalysisBenefit Cost Ratio Analysis

Related TopicsCapitalized CostBondsBreak-Even Analysis vs Payback PeriodDepreciation and TaxesInflation

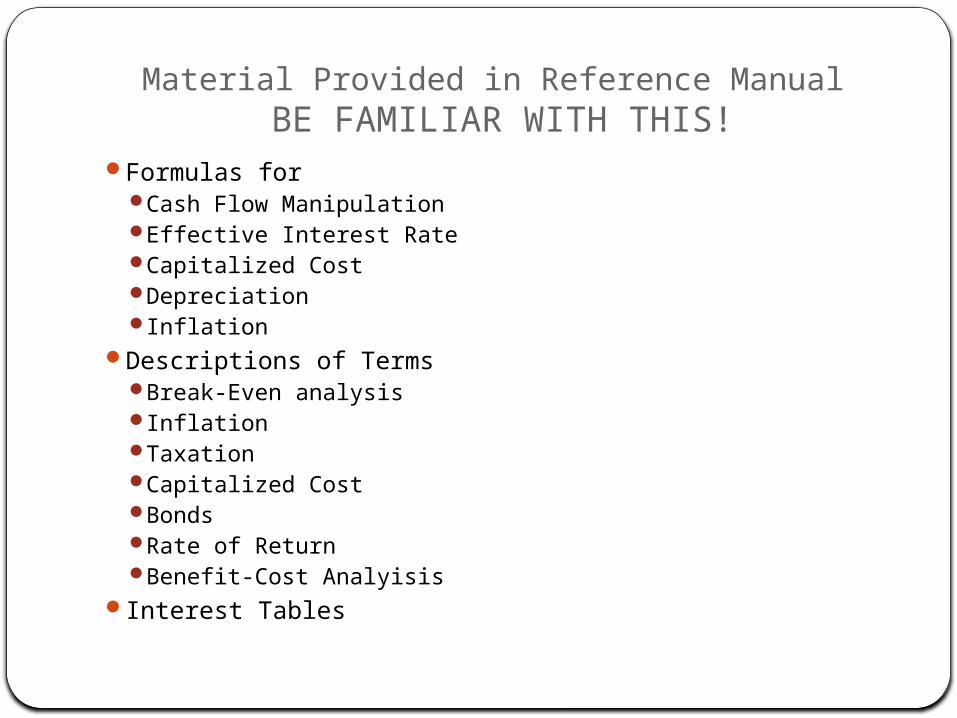

Material Provided in Reference Manual BE FAMILIAR WITH THIS!

Formulas for Cash Flow ManipulationEffective Interest RateCapitalized CostDepreciation Inflation

Descriptions of TermsBreak-Even analysis InflationTaxationCapitalized CostBondsRate of ReturnBenefit-Cost Analyisis

Interest Tables

Cash Flow Formulas – from Reference Handbook, p. 114

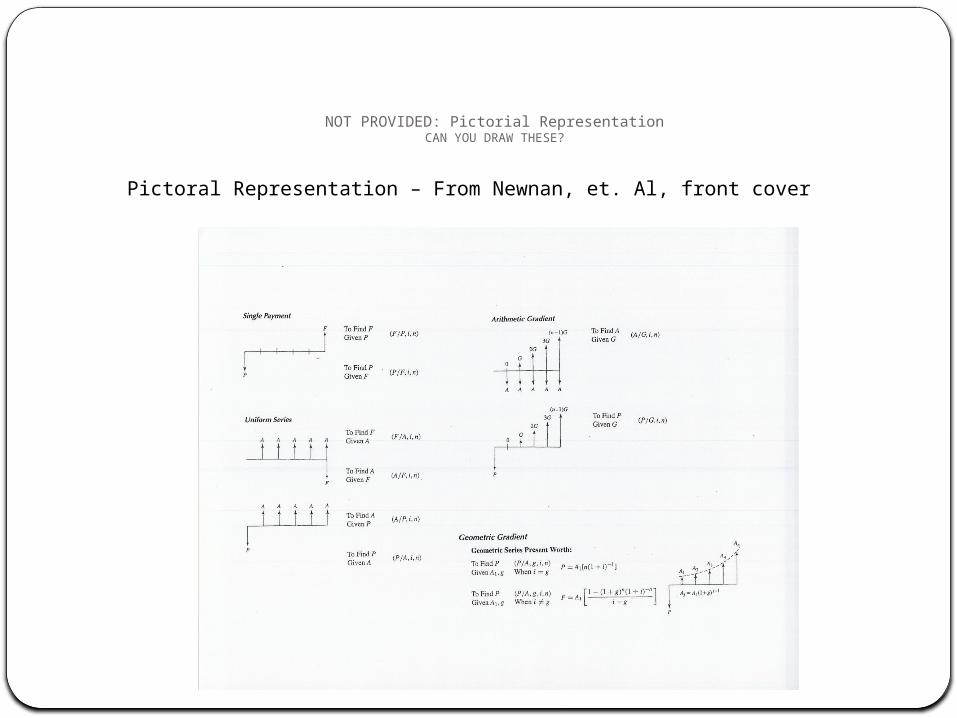

NOT PROVIDED: Pictorial RepresentationCAN YOU DRAW THESE?

Pictoral Representation – From Newnan, et. Al, front cover

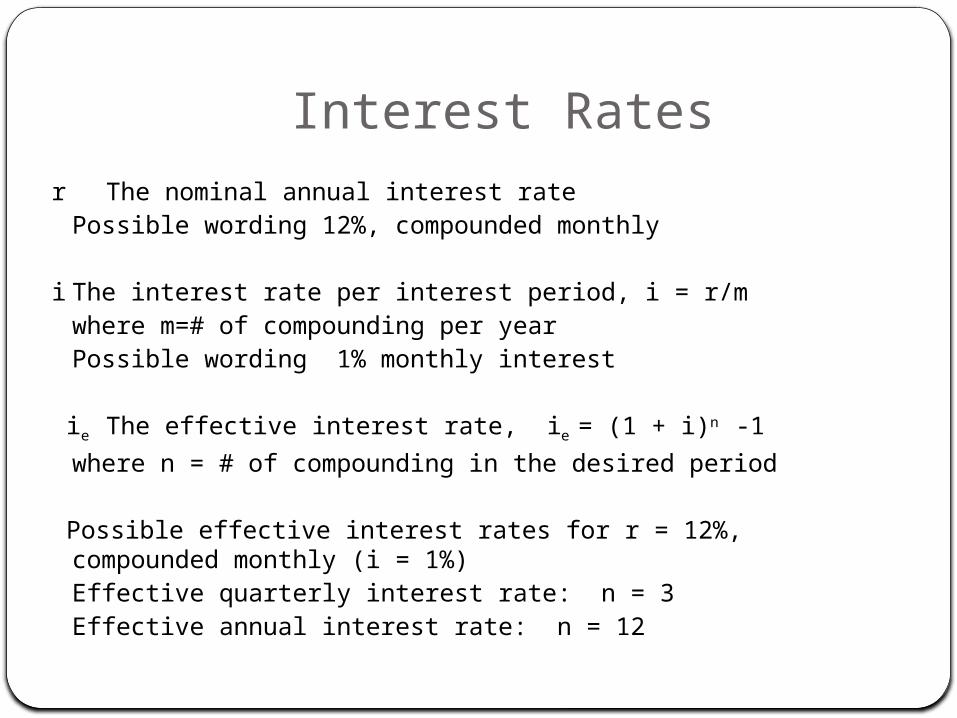

Interest Ratesr The nominal annual interest rate

Possible wording 12%, compounded monthly

i The interest rate per interest period, i = r/m where m=# of compounding per yearPossible wording 1% monthly interest

ieThe effective interest rate, ie = (1 + i)n -1

where n = # of compounding in the desired period

Possible effective interest rates for r = 12%, compounded monthly (i = 1%)Effective quarterly interest rate: n = 3Effective annual interest rate: n = 12

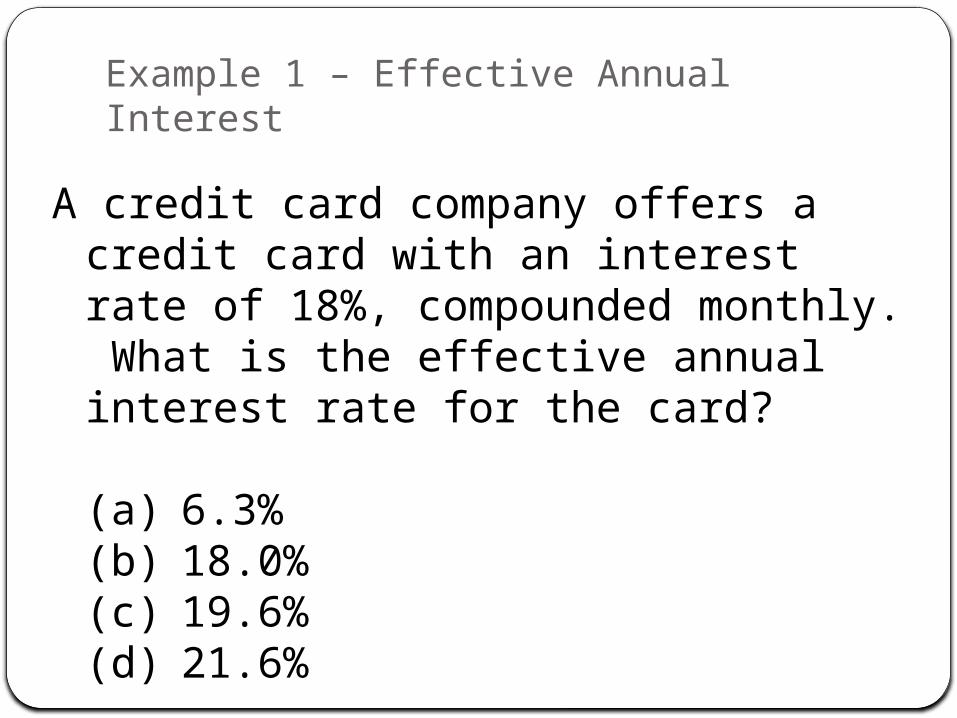

Example 1 – Effective Annual Interest

A credit card company offers a credit card with an interest rate of 18%, compounded monthly. What is the effective annual interest rate for the card?

(a) 6.3%(b) 18.0%(c) 19.6%(d) 21.6%

Solution to example 1

ie = (1 + r/m)m – 1 = (1 + 0.18/12)12 – 1 = 0.1956 = 19.56%

Answer: (c)

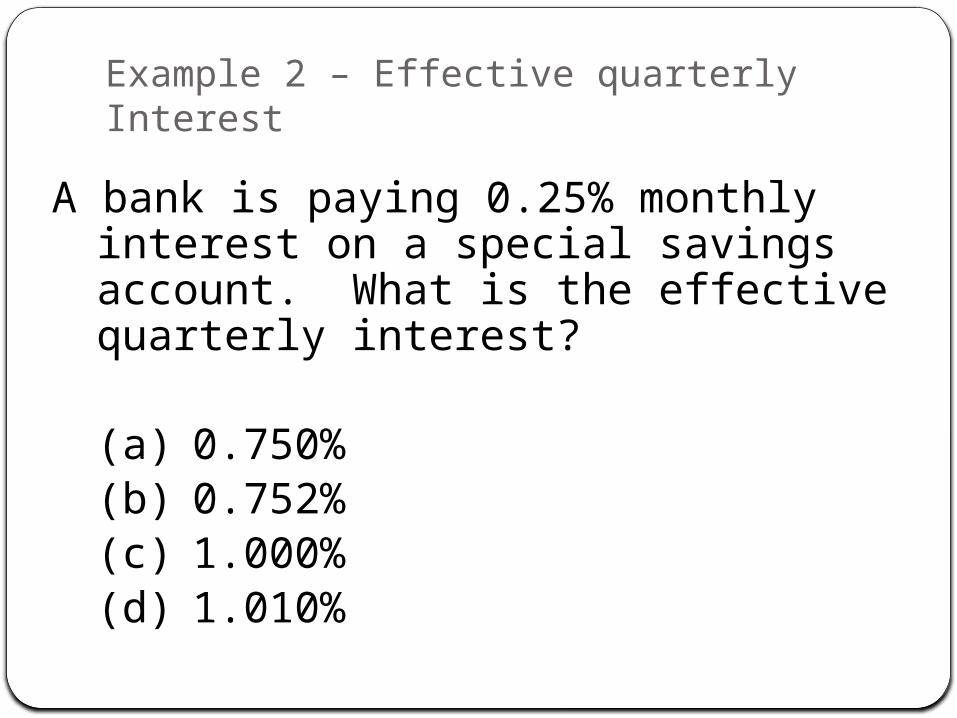

Example 2 – Effective quarterly Interest

A bank is paying 0.25% monthly interest on a special savings account. What is the effective quarterly interest?

(a) 0.750%(b) 0.752%(c) 1.000%(d) 1.010%

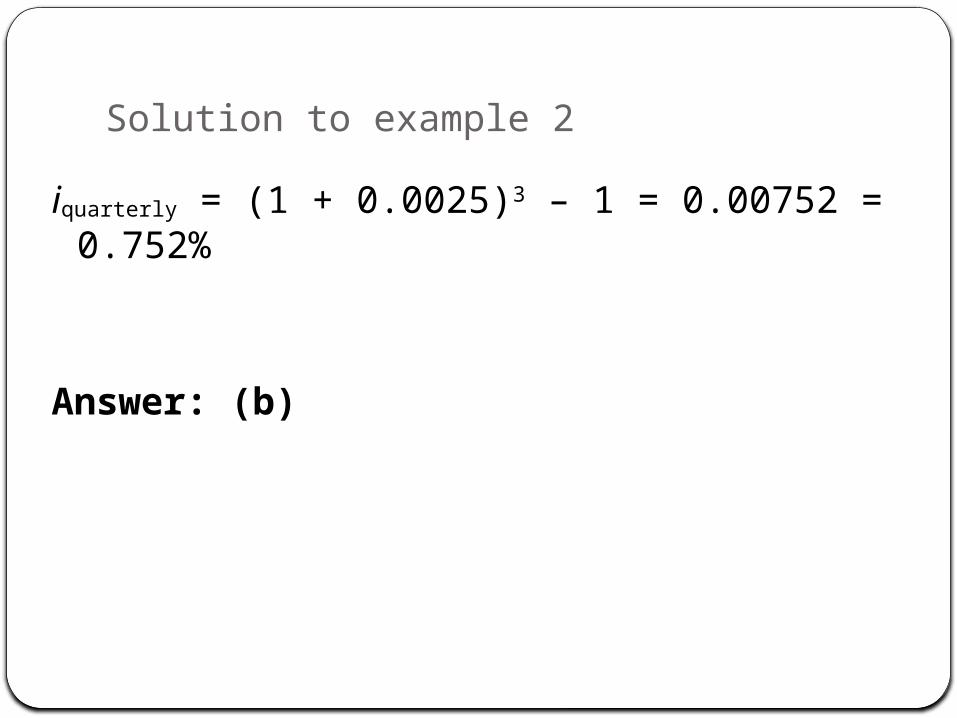

Solution to example 2

iquarterly = (1 + 0.0025)3 – 1 = 0.00752 = 0.752%

Answer: (b)

Present, Future Worth, and Equivalent Uniform Cash Flow Analyses

Three Possible GoalsMaximize BENEFITS orMinimize COSTS orMaximize the NET WORTH (BENEFITS – COSTS)

Present Worth or Future Worth – Move each cash flow to a single point in time.

Equivalent Uniform Cash Flow – Convert each to an equivalent uniform cash flow over the SAME TIME INTERVAL.

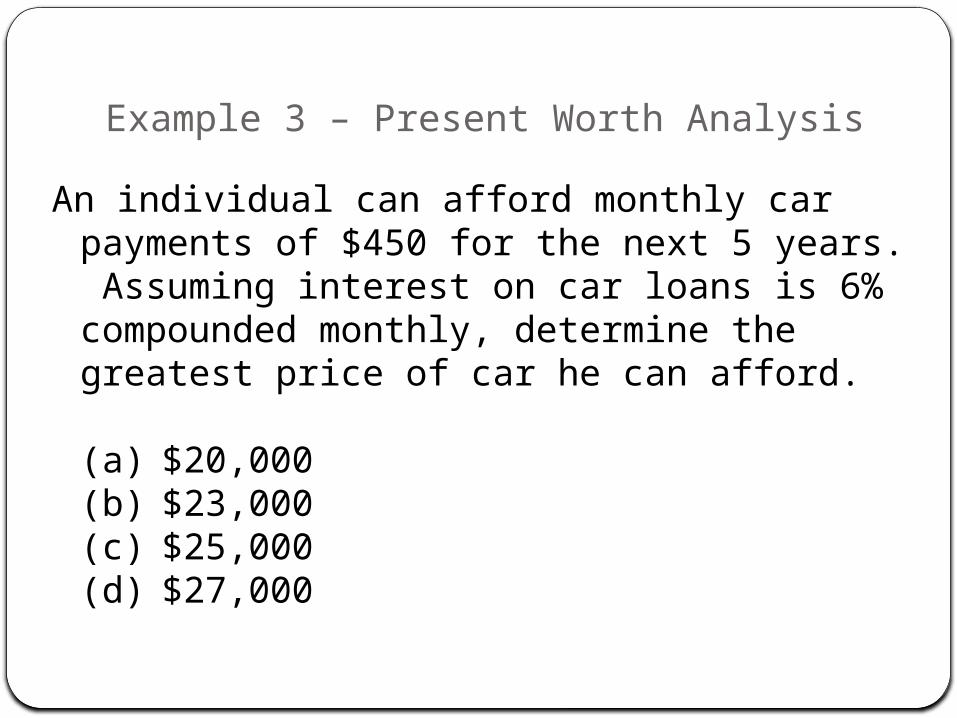

Example 3 – Present Worth Analysis

An individual can afford monthly car payments of $450 for the next 5 years. Assuming interest on car loans is 6% compounded monthly, determine the greatest price of car he can afford.

(a) $20,000(b) $23,000 (c) $25,000 (d) $27,000

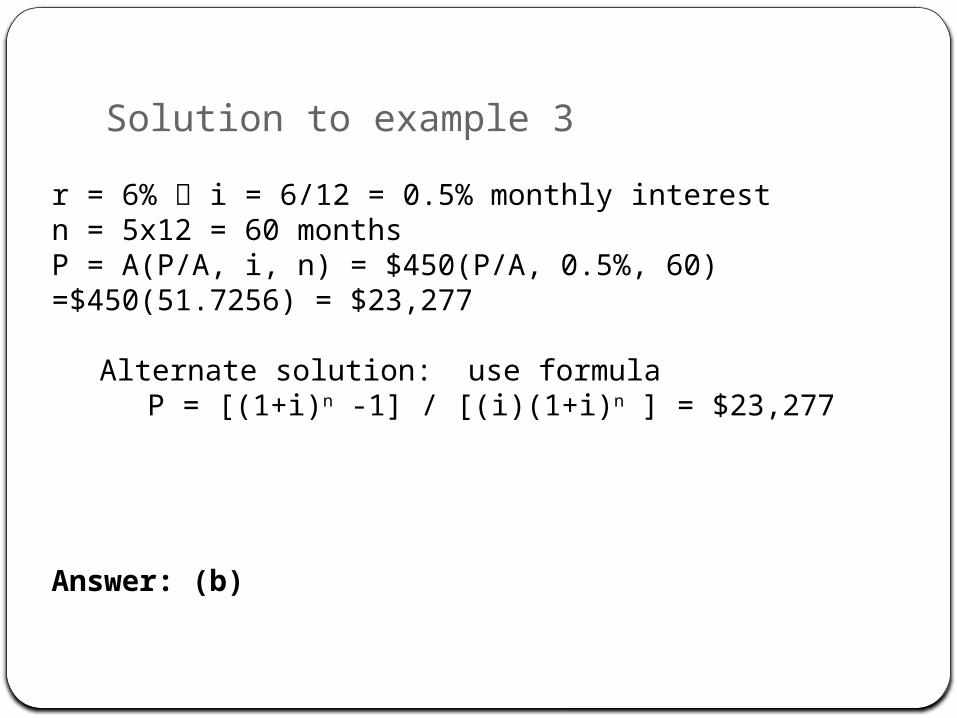

Solution to example 3

r = 6% i = 6/12 = 0.5% monthly interestn = 5x12 = 60 monthsP = A(P/A, i, n) = $450(P/A, 0.5%, 60) =$450(51.7256) = $23,277

Alternate solution: use formulaP = [(1+i)n -1] / [(i)(1+i)n ] = $23,277

Answer: (b)

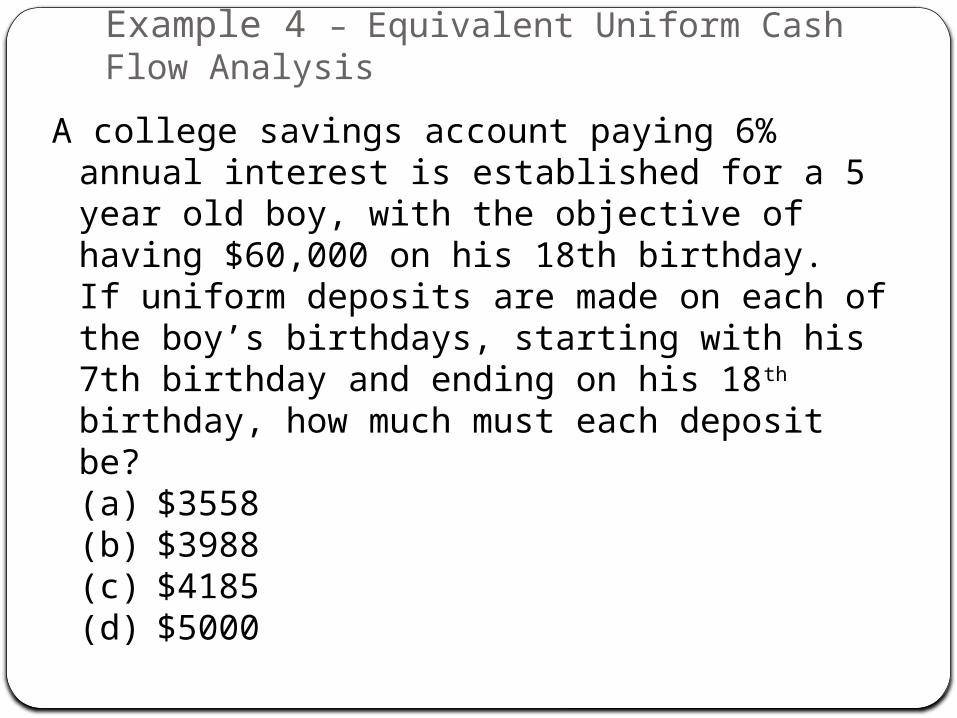

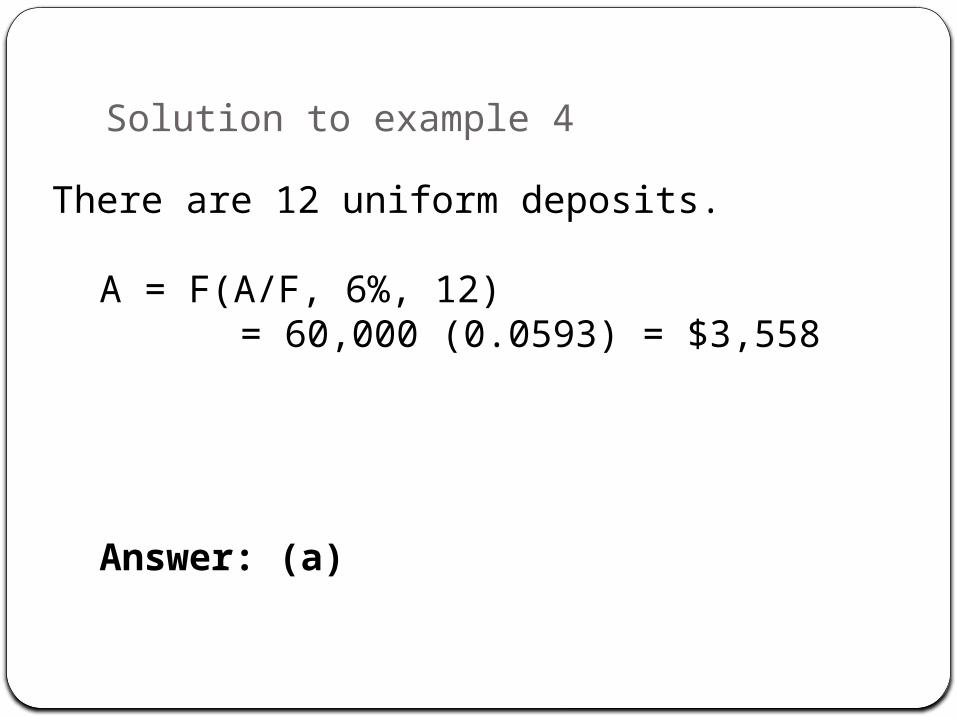

Example 4 – Equivalent Uniform Cash Flow Analysis

A college savings account paying 6% annual interest is established for a 5 year old boy, with the objective of having $60,000 on his 18th birthday. If uniform deposits are made on each of the boy’s birthdays, starting with his 7th birthday and ending on his 18th birthday, how much must each deposit be?(a) $3558(b) $3988(c) $4185(d) $5000

Solution to example 4

There are 12 uniform deposits.

A = F(A/F, 6%, 12) = 60,000 (0.0593) = $3,558

Answer: (a)

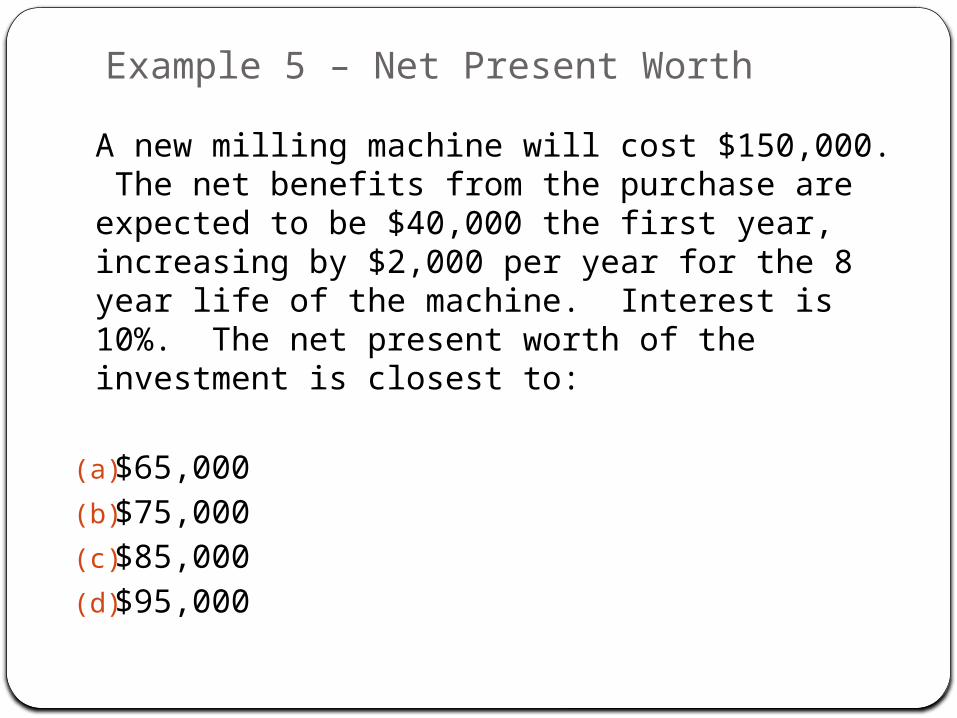

Example 5 – Net Present Worth

A new milling machine will cost $150,000. The net benefits from the purchase are expected to be $40,000 the first year, increasing by $2,000 per year for the 8 year life of the machine. Interest is 10%. The net present worth of the investment is closest to:

(a) $65,000

(b) $75,000

(c) $85,000

(d) $95,000

Solution to example 5NPW = -150,000 +

(40,000+2000(A/G,10%,8))(P/A,10%,8) = -150,000+(40,000*2000(3.0045))

(5.3349) = $95,453

Answer: (d)

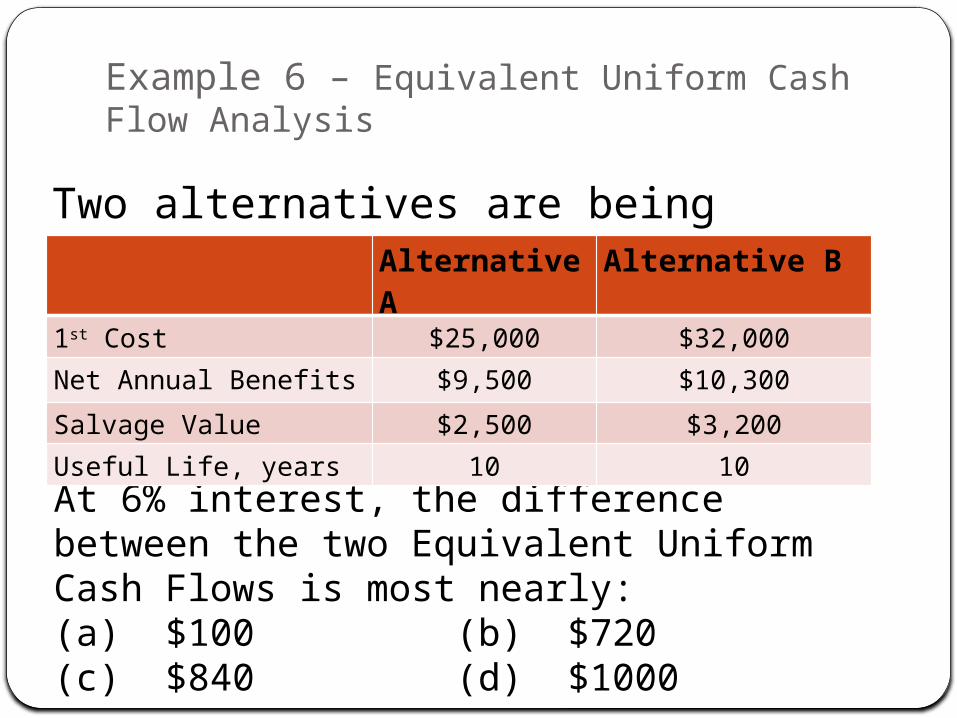

Example 6 – Equivalent Uniform Cash Flow Analysis

Two alternatives are being considered:

At 6% interest, the difference between the two Equivalent Uniform Cash Flows is most nearly: (a) $100 (b) $720 (c) $840 (d) $1000

Alternative A

Alternative B

1st Cost $25,000 $32,000

Net Annual Benefits $9,500 $10,300

Salvage Value $2,500 $3,200

Useful Life, years 10 10

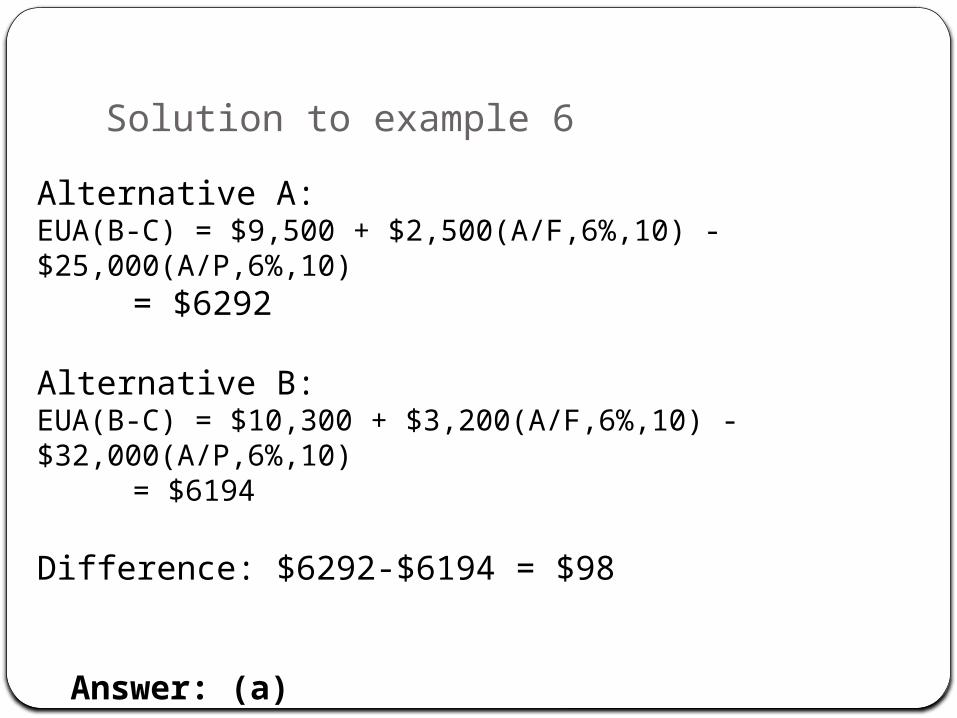

Solution to example 6

Alternative A: EUA(B-C) = $9,500 + $2,500(A/F,6%,10) - $25,000(A/P,6%,10)

= $6292

Alternative B: EUA(B-C) = $10,300 + $3,200(A/F,6%,10) - $32,000(A/P,6%,10)

= $6194

Difference: $6292-$6194 = $98

Answer: (a)

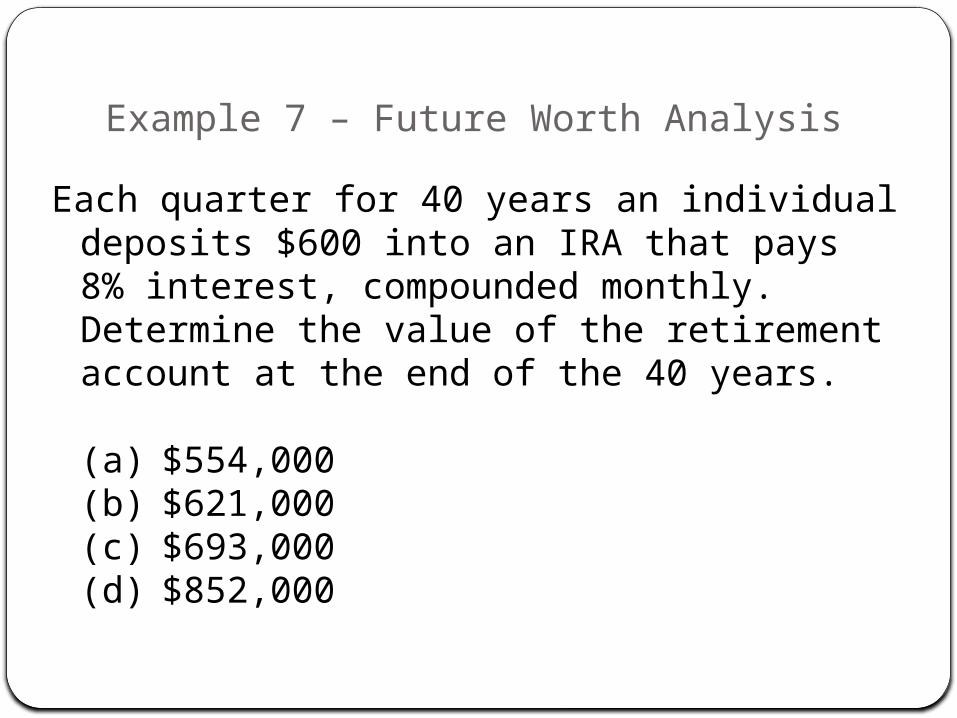

Example 7 – Future Worth Analysis

Each quarter for 40 years an individual deposits $600 into an IRA that pays 8% interest, compounded monthly. Determine the value of the retirement account at the end of the 40 years.

(a) $554,000(b) $621,000(c) $693,000(d) $852,000

Solution to example 7

r = 8% i = 0.6667%iquarterly = (1.006667)3 -1 = 0.02013 o4 2.013%n = 40*4 = 160Using the formula, F = $600[((1.02013)160 -1)/(.02013)] = $693,280.81

Answer: (c)

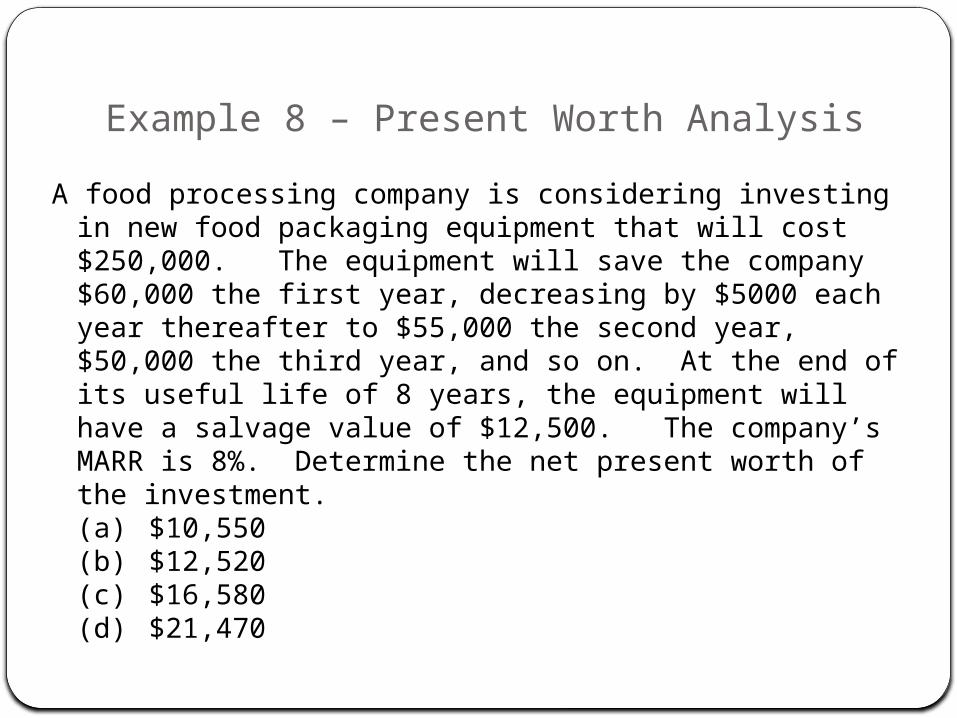

Example 8 – Present Worth Analysis

A food processing company is considering investing in new food packaging equipment that will cost $250,000. The equipment will save the company $60,000 the first year, decreasing by $5000 each year thereafter to $55,000 the second year, $50,000 the third year, and so on. At the end of its useful life of 8 years, the equipment will have a salvage value of $12,500. The company’s MARR is 8%. Determine the net present worth of the investment.(a) $10,550(b) $12,520(c) $16,580(d) $21,470

Solution to example 8

NPW = -250,000 + 60,000(P/A, 8%,8)

– 5,000(P/G, 8%,8) + 12,500(P/F, 8%,8)

= -250,000+60,000(5.7466)-5000(17.8061)+12,500(.5403)

= $12,520

Answer: (b)

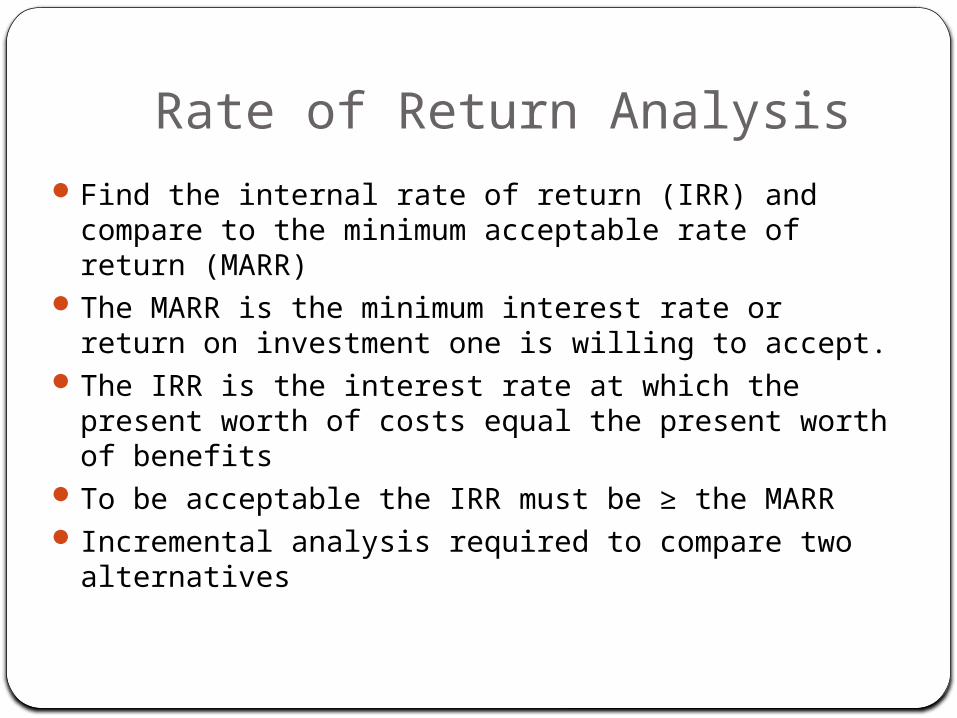

Rate of Return AnalysisFind the internal rate of return (IRR) and compare to

the minimum acceptable rate of return (MARR)The MARR is the minimum interest rate or return on

investment one is willing to accept.The IRR is the interest rate at which the present worth

of costs equal the present worth of benefitsTo be acceptable the IRR must be ≥ the MARR Incremental analysis required to compare two

alternatives

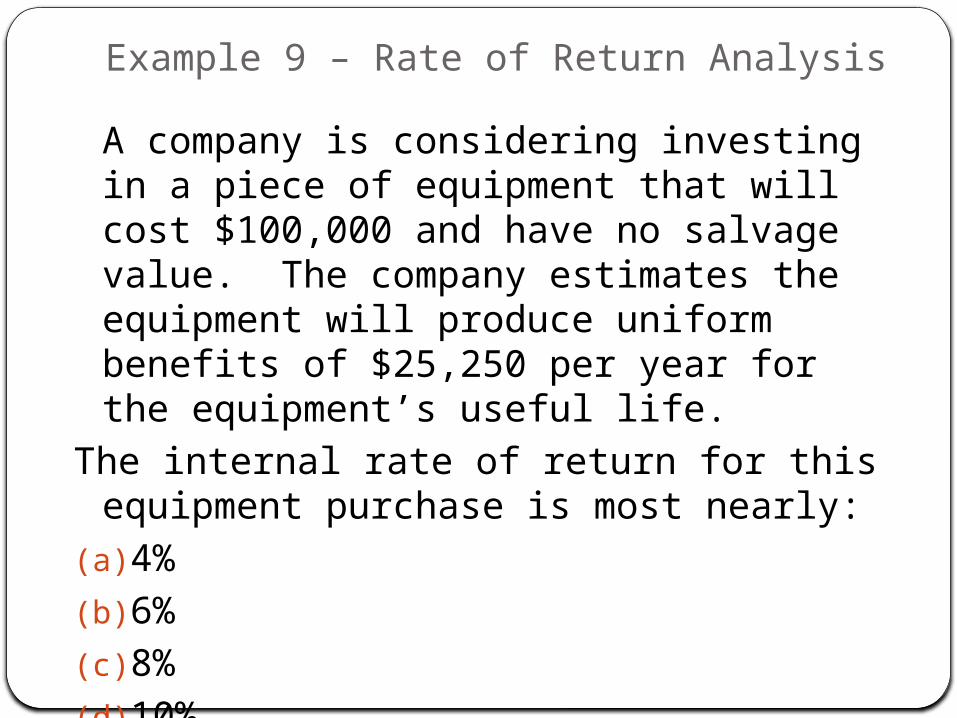

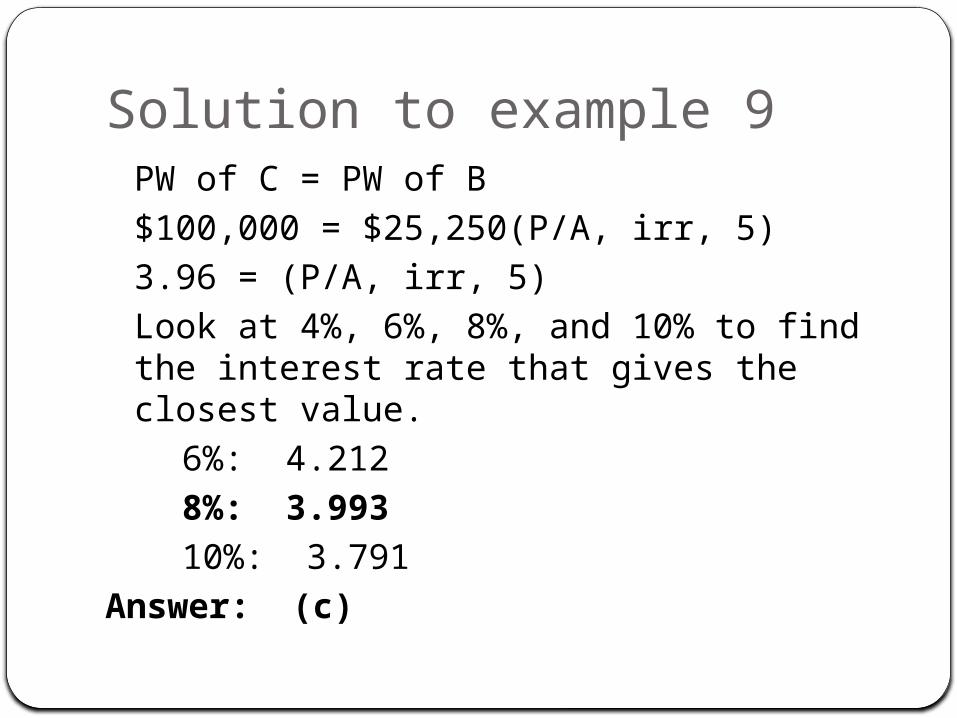

Example 9 – Rate of Return Analysis

A company is considering investing in a piece of equipment that will cost $100,000 and have no salvage value. The company estimates the equipment will produce uniform benefits of $25,250 per year for the equipment’s useful life.

The internal rate of return for this equipment purchase is most nearly:

(a) 4%

(b) 6%

(c) 8%

(d) 10%

Solution to example 9 PW of C = PW of B$100,000 = $25,250(P/A, irr, 5)3.96 = (P/A, irr, 5)Look at 4%, 6%, 8%, and 10% to find the interest rate that gives the closest value.

6%: 4.2128%: 3.99310%: 3.791

Answer: (c)

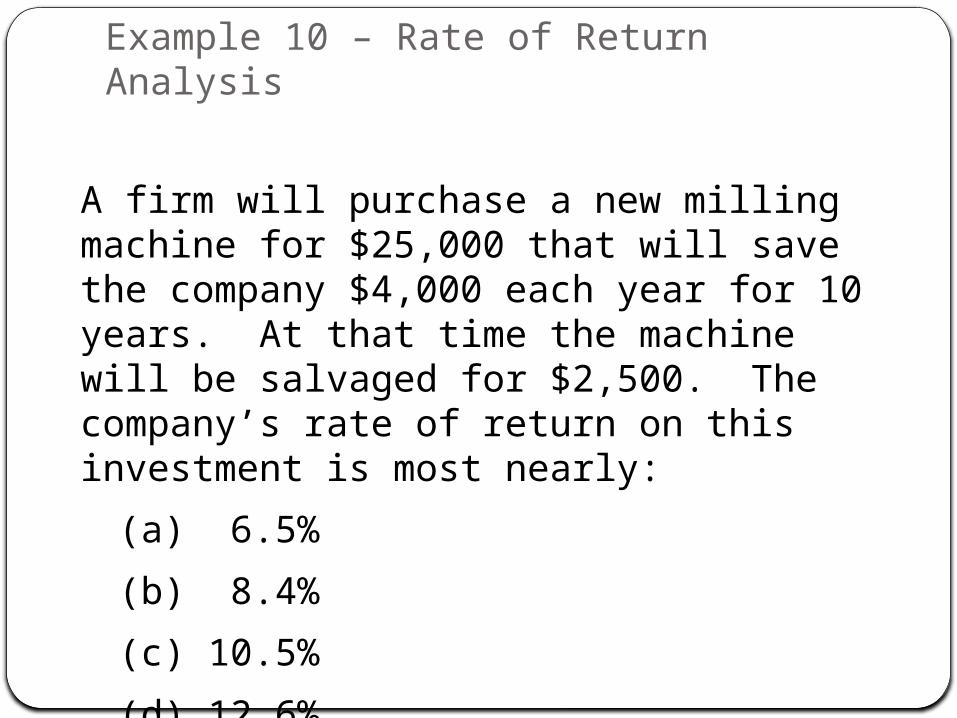

Example 10 – Rate of Return Analysis

A firm will purchase a new milling machine for $25,000 that will save the company $4,000 each year for 10 years. At that time the machine will be salvaged for $2,500. The company’s rate of return on this investment is most nearly:

(a) 6.5%

(b) 8.4%

(c) 10.5%

(d) 12.6%

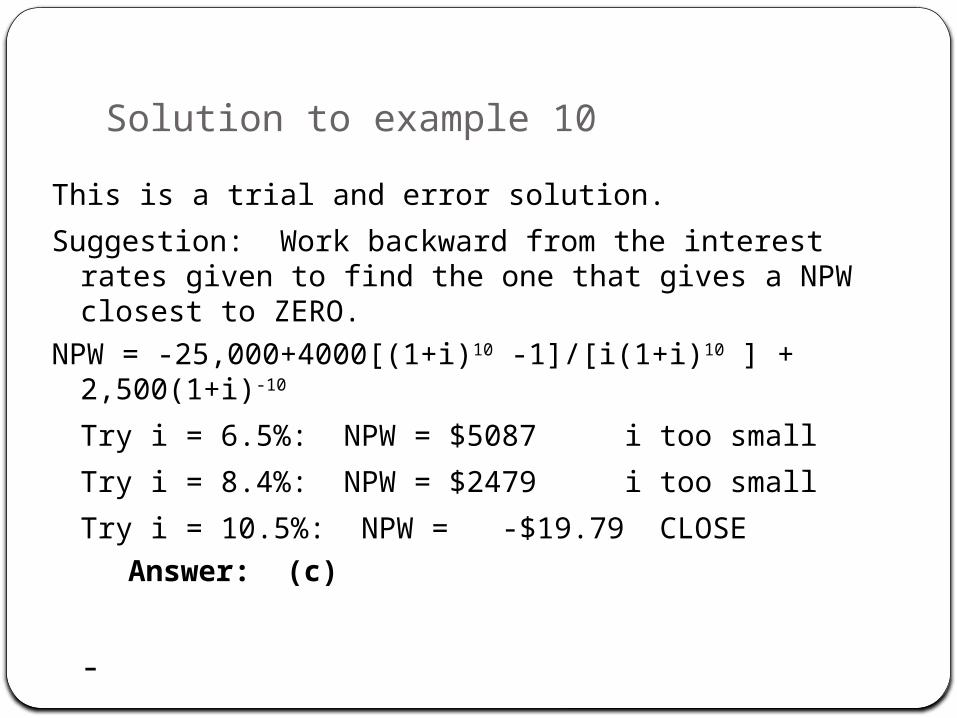

Solution to example 10

This is a trial and error solution.

Suggestion: Work backward from the interest rates given to find the one that gives a NPW closest to ZERO.

NPW = -25,000+4000[(1+i)10 -1]/[i(1+i)10 ] + 2,500(1+i)-10

Try i = 6.5%: NPW = $5087 i too small

Try i = 8.4%: NPW = $2479 i too small

Try i = 10.5%: NPW = -$19.79 CLOSE

Answer: (c)

-

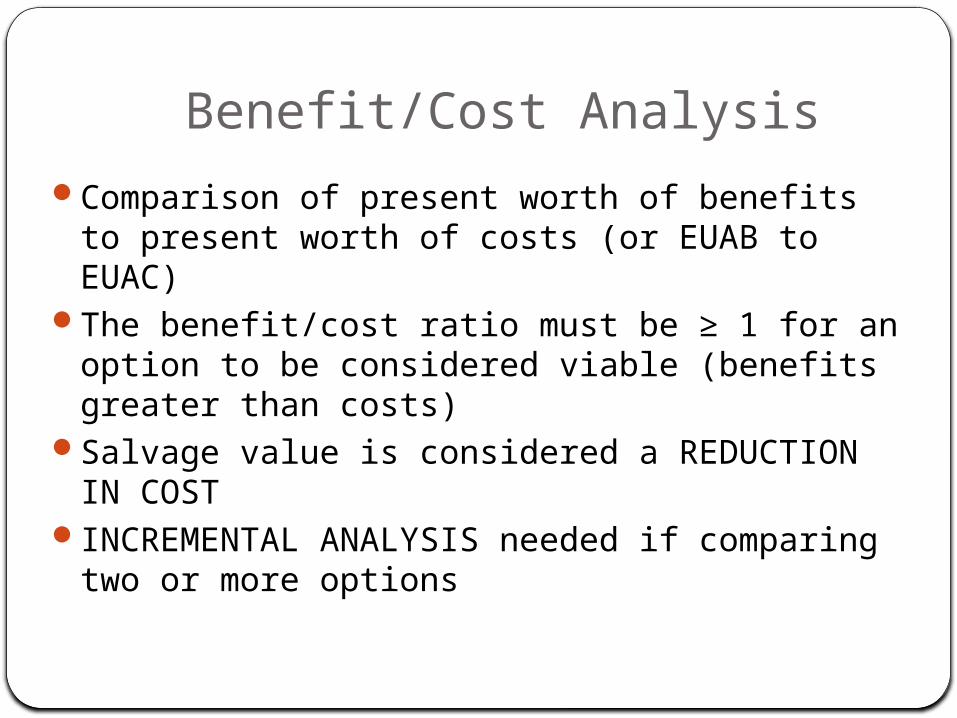

Benefit/Cost Analysis

Comparison of present worth of benefits to present worth of costs (or EUAB to EUAC)

The benefit/cost ratio must be ≥ 1 for an option to be considered viable (benefits greater than costs)

Salvage value is considered a REDUCTION IN COST

INCREMENTAL ANALYSIS needed if comparing two or more options

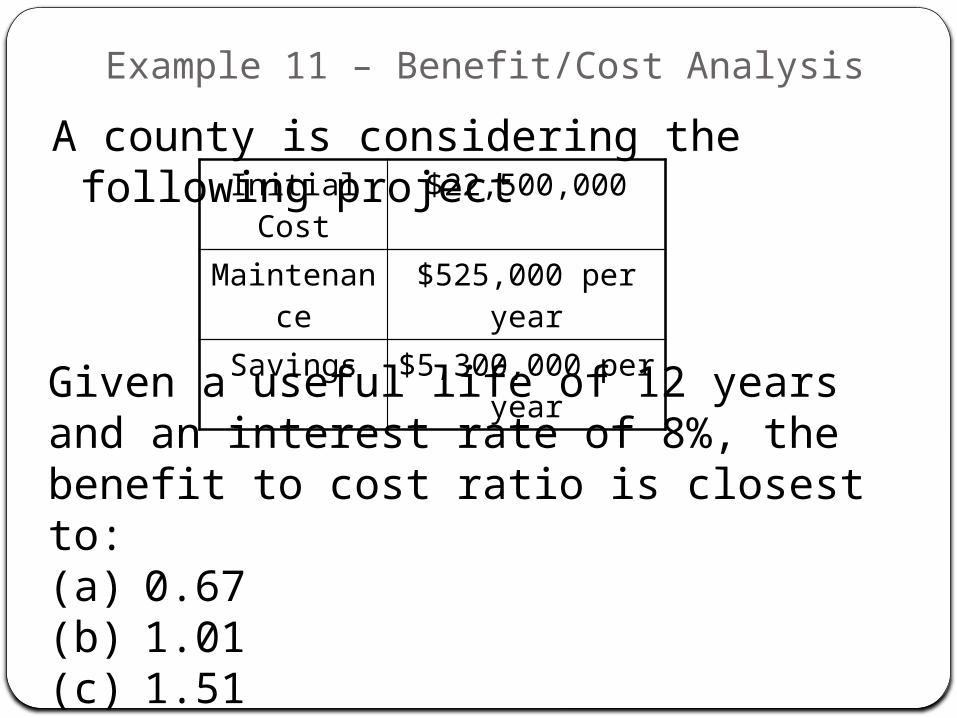

Example 11 – Benefit/Cost Analysis

A county is considering the following projectInitial Cost $22,500,000

Maintenance $525,000 per year

Savings $5,300,000 per year

Given a useful life of 12 years and an interest rate of 8%, the benefit to cost ratio is closest to:(a) 0.67(b) 1.01(c) 1.51(d) 1.67

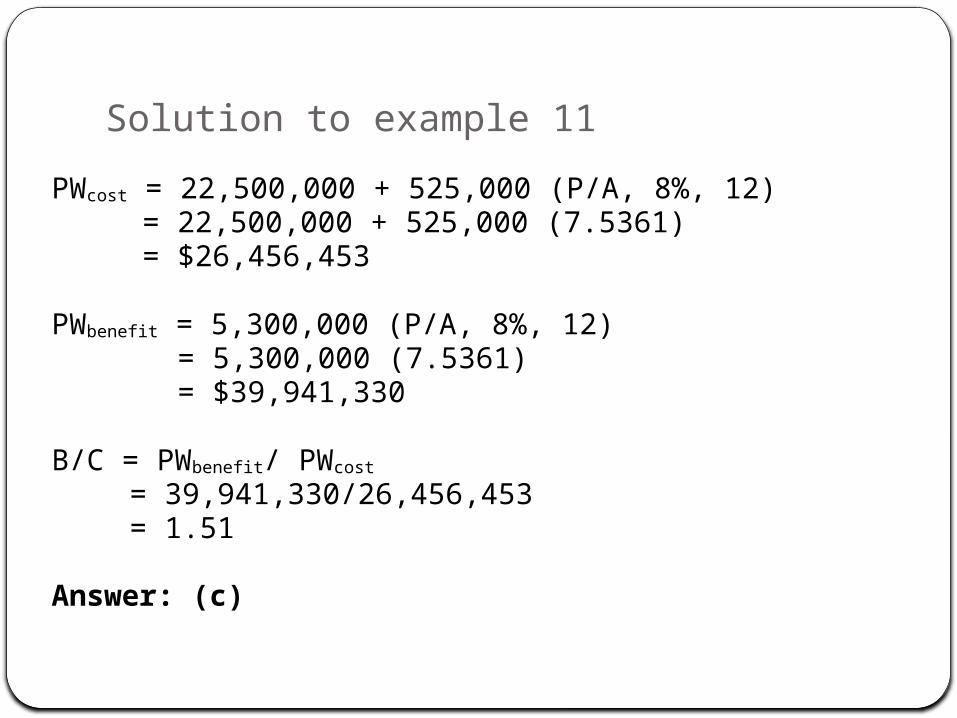

Solution to example 11

PWcost = 22,500,000 + 525,000 (P/A, 8%, 12) = 22,500,000 + 525,000 (7.5361) = $26,456,453

PWbenefit = 5,300,000 (P/A, 8%, 12) = 5,300,000 (7.5361) = $39,941,330

B/C = PWbenefit/ PWcost

= 39,941,330/26,456,453 = 1.51

Answer: (c)

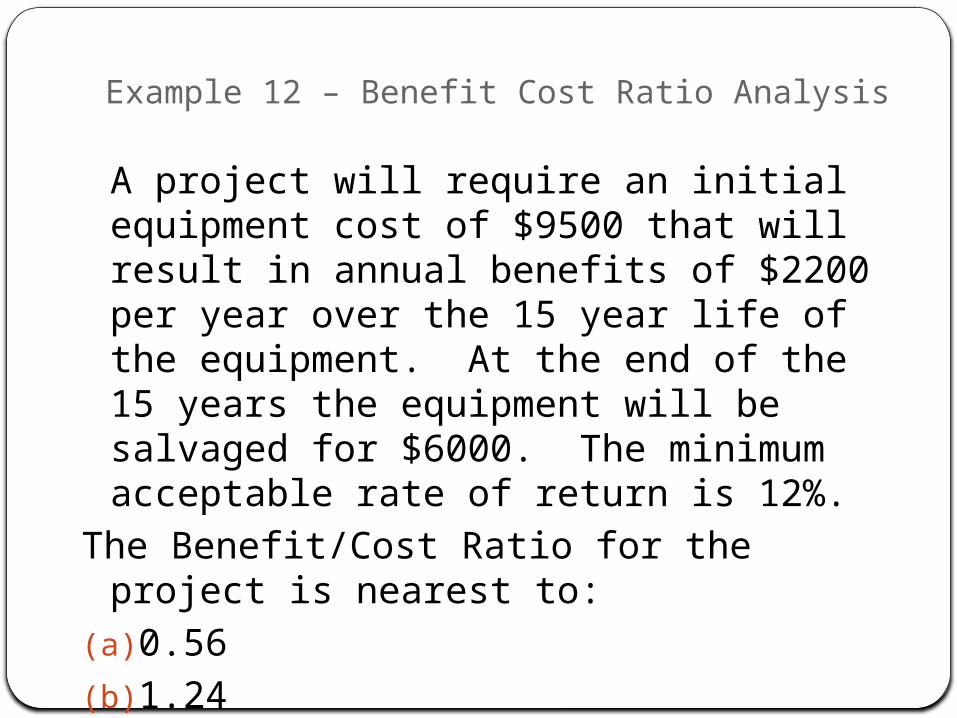

Example 12 – Benefit Cost Ratio Analysis

A project will require an initial equipment cost of $9500 that will result in annual benefits of $2200 per year over the 15 year life of the equipment. At the end of the 15 years the equipment will be salvaged for $6000. The minimum acceptable rate of return is 12%.

The Benefit/Cost Ratio for the project is nearest to:

(a) 0.56

(b) 1.24

(c) 1.78

(d) 2.21

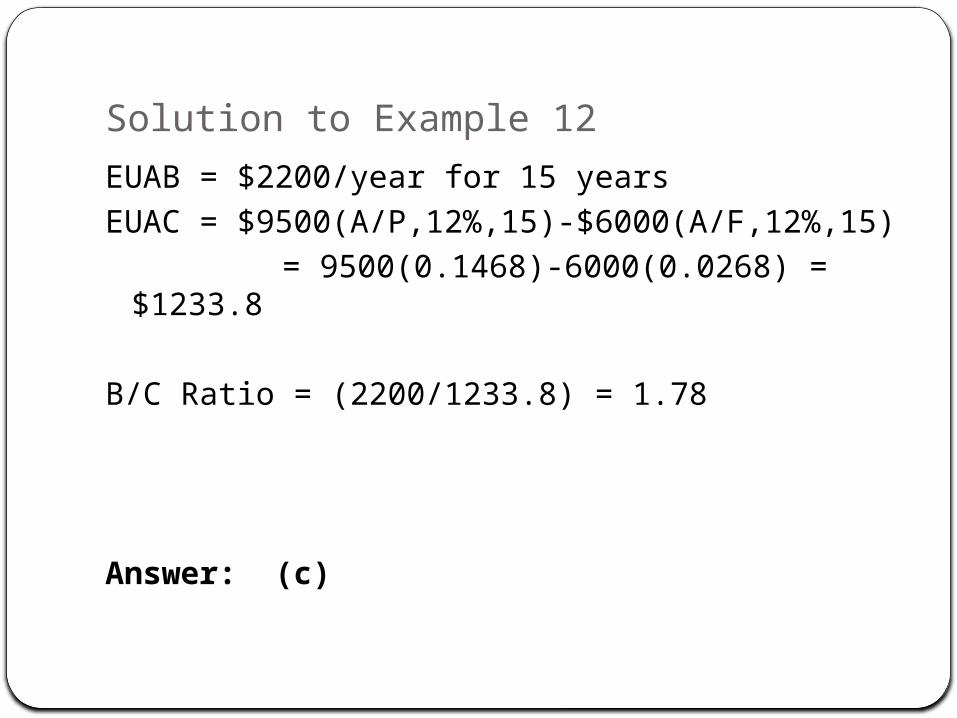

Solution to Example 12

EUAB = $2200/year for 15 yearsEUAC = $9500(A/P,12%,15)-$6000(A/F,12%,15)

= 9500(0.1468)-6000(0.0268) = $1233.8

B/C Ratio = (2200/1233.8) = 1.78

Answer: (c)

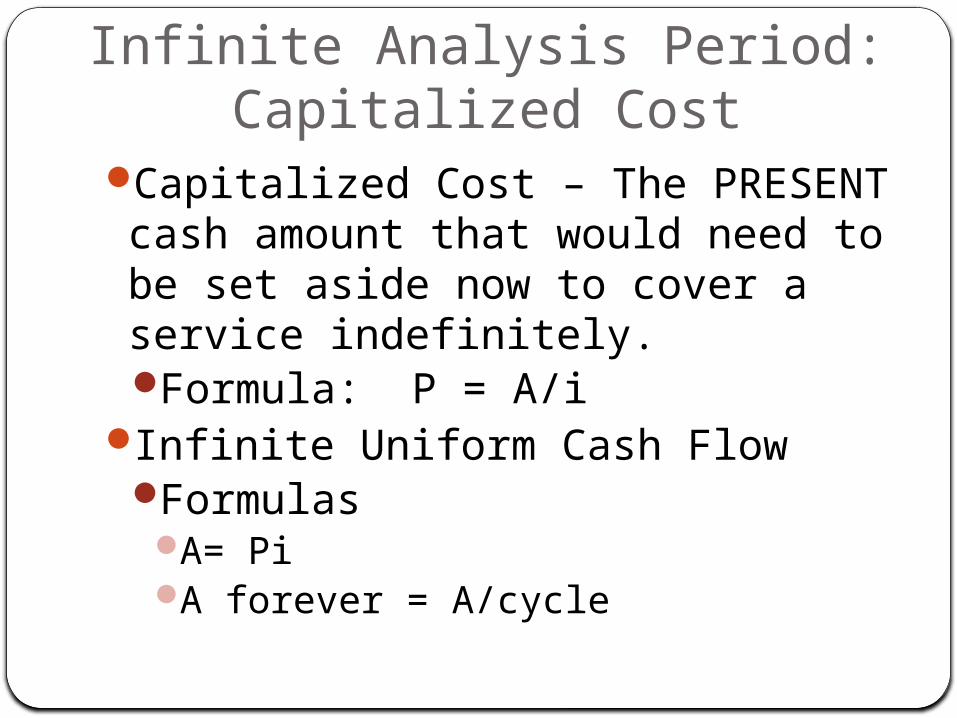

Infinite Analysis Period:Capitalized Cost

Capitalized Cost – The PRESENT cash amount that would need to be set aside now to cover a service indefinitely. Formula: P = A/i

Infinite Uniform Cash FlowFormulas

A= Pi A forever = A/cycle

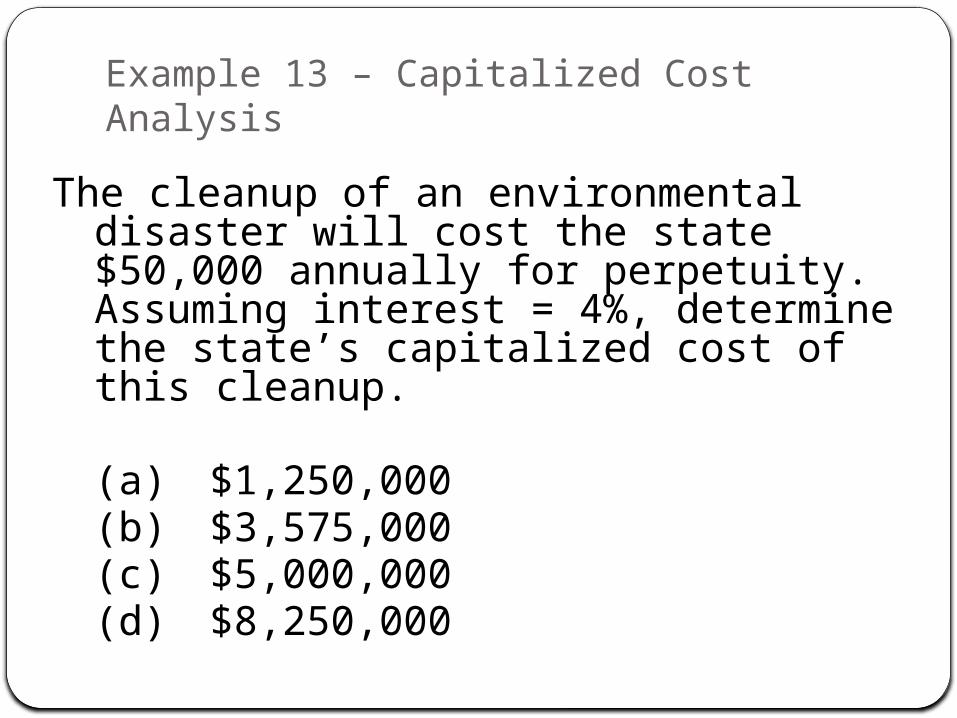

Example 13 – Capitalized Cost Analysis

The cleanup of an environmental disaster will cost the state $50,000 annually for perpetuity. Assuming interest = 4%, determine the state’s capitalized cost of this cleanup.

(a) $1,250,000(b) $3,575,000(c) $5,000,000(d) $8,250,000

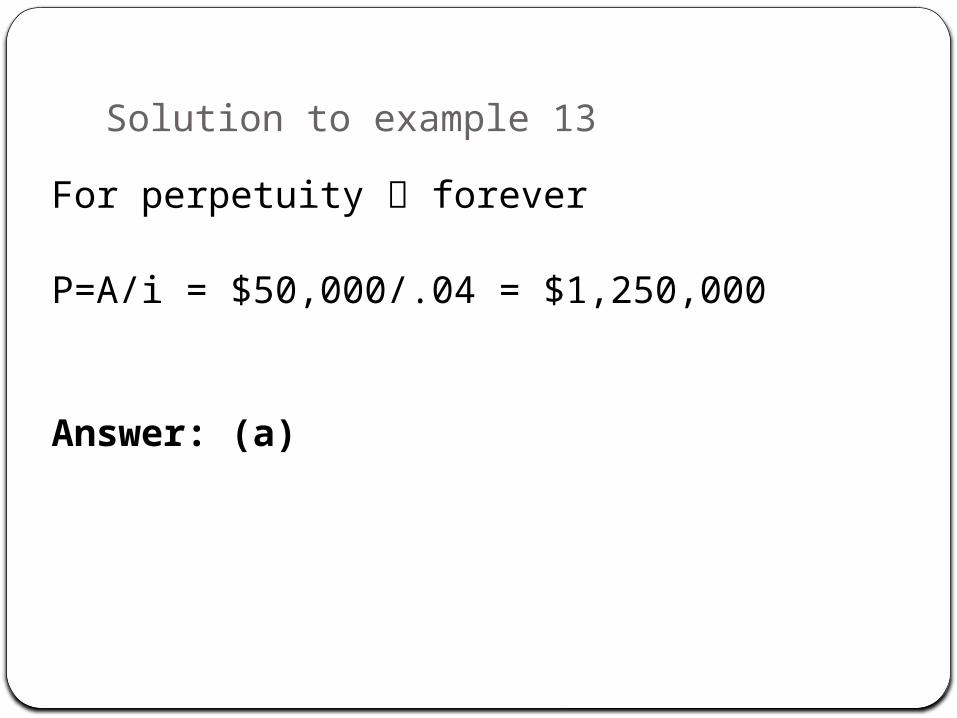

Solution to example 13

For perpetuity forever

P=A/i = $50,000/.04 = $1,250,000

Answer: (a)

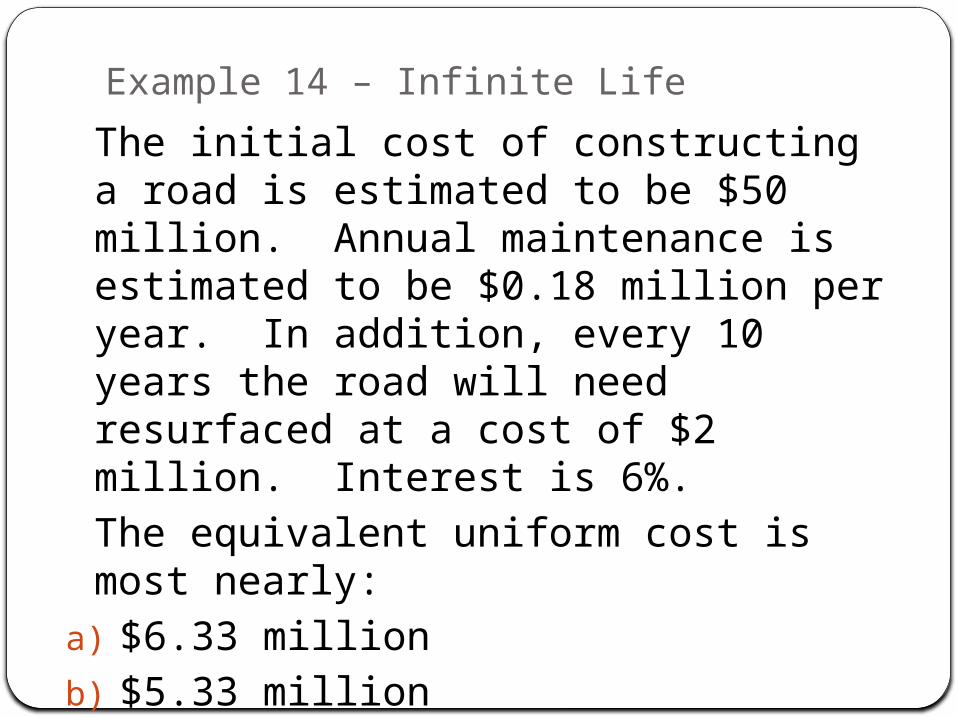

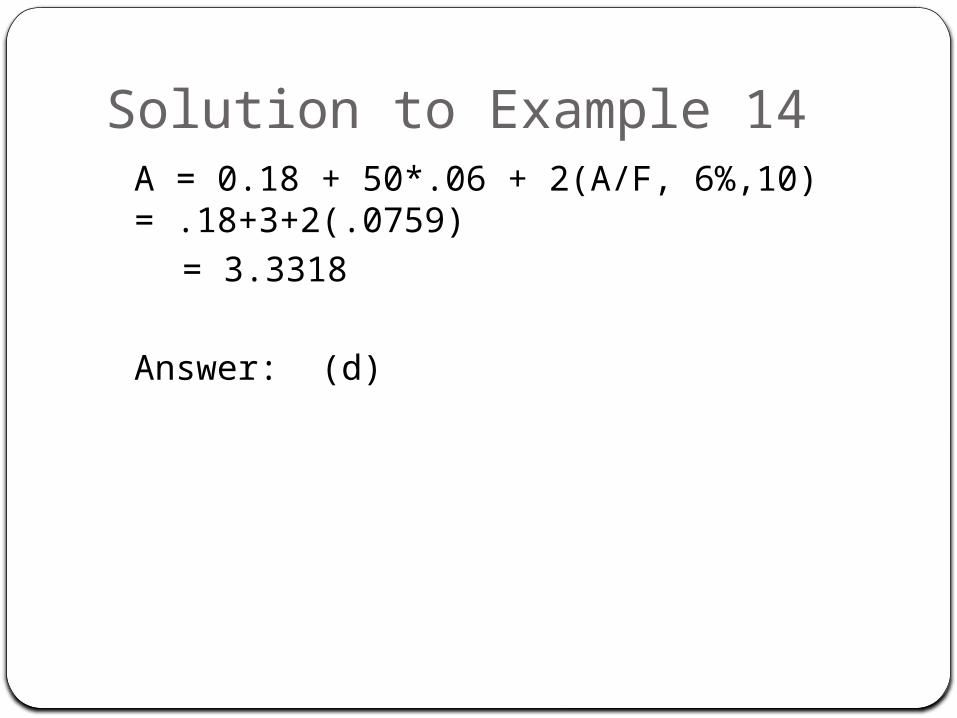

Example 14 – Infinite Life

The initial cost of constructing a road is estimated to be $50 million. Annual maintenance is estimated to be $0.18 million per year. In addition, every 10 years the road will need resurfaced at a cost of $2 million. Interest is 6%.

The equivalent uniform cost is most nearly:

a) $6.33 million

b) $5.33 million

c) $4.33 million

d) $3.33 million

Solution to Example 14A = 0.18 + 50*.06 + 2(A/F, 6%,10) = .18+3+2(.0759)

= 3.3318

Answer: (d)

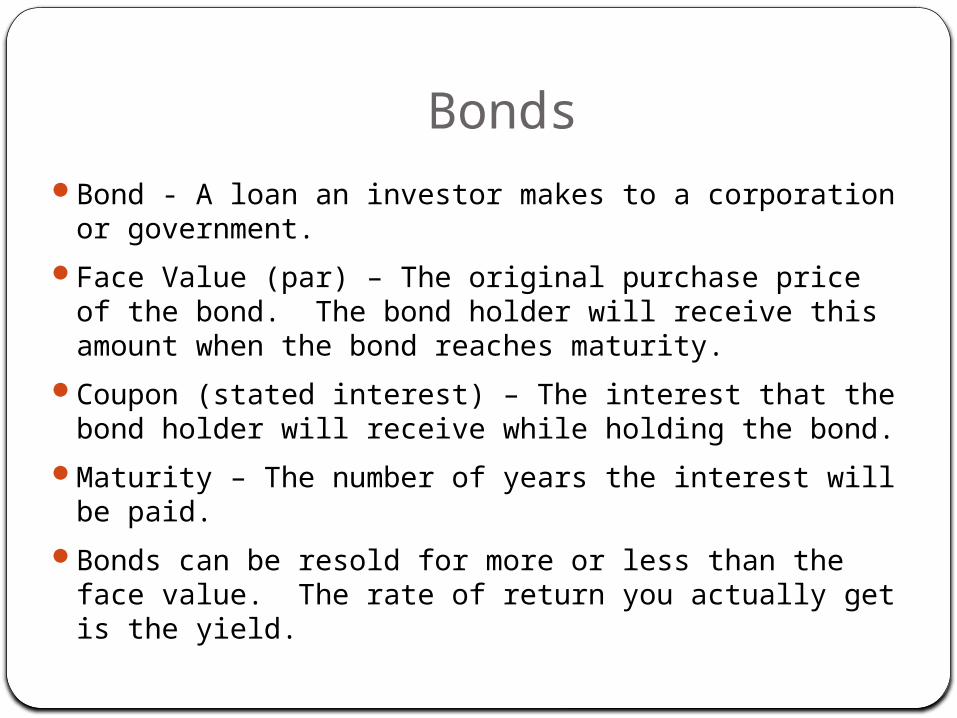

BondsBond - A loan an investor makes to a corporation or

government.

Face Value (par) – The original purchase price of the bond. The bond holder will receive this amount when the bond reaches maturity.

Coupon (stated interest) – The interest that the bond holder will receive while holding the bond.

Maturity – The number of years the interest will be paid.

Bonds can be resold for more or less than the face value. The rate of return you actually get is the yield.

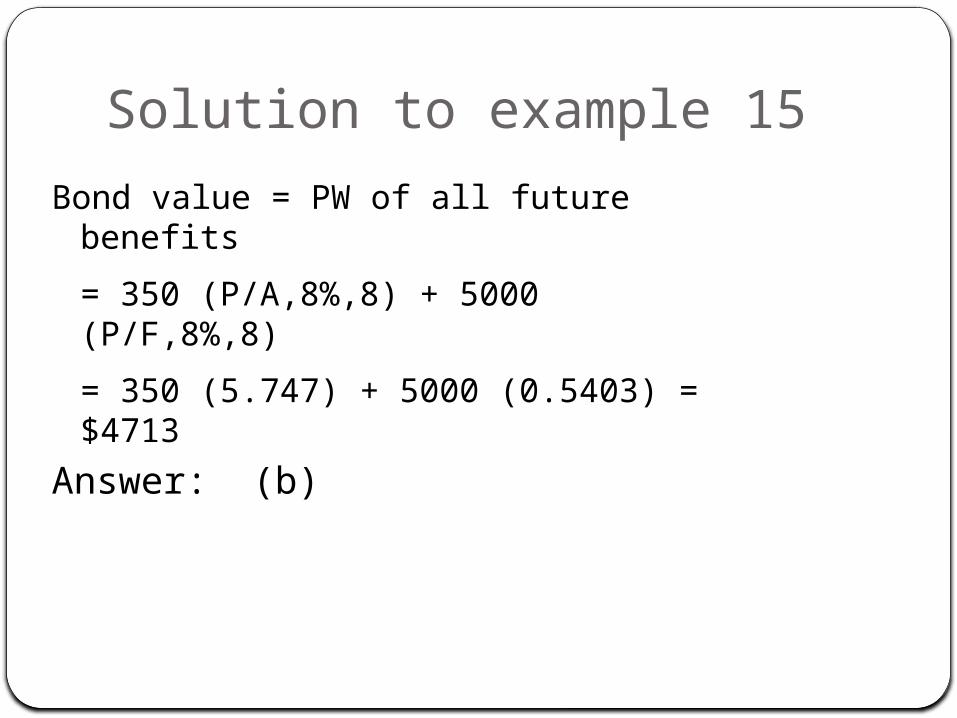

Example 15 – Bonds

A $5000 bond is being offered for sale. It has a stated interest rate of 7%, paid annually ($350 each year). The $5000 debt will be repaid at 8 years along with the last interest payment. If you want an 8% return on this investment (the bond yield), what is the most you would be willing to pay for the bond (the bond value)?

(a) $3500

(b) $4700

(c) $5000

(d) $5200

Solution to example 15

Bond value = PW of all future benefits

= 350 (P/A,8%,8) + 5000 (P/F,8%,8)

= 350 (5.747) + 5000 (0.5403) = $4713

Answer: (b)

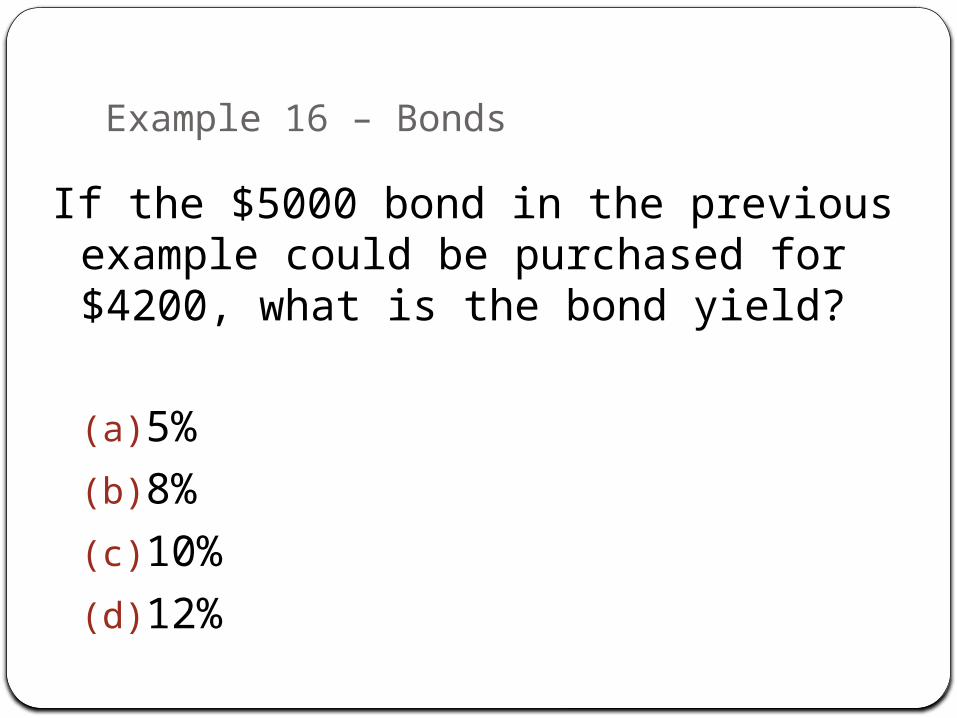

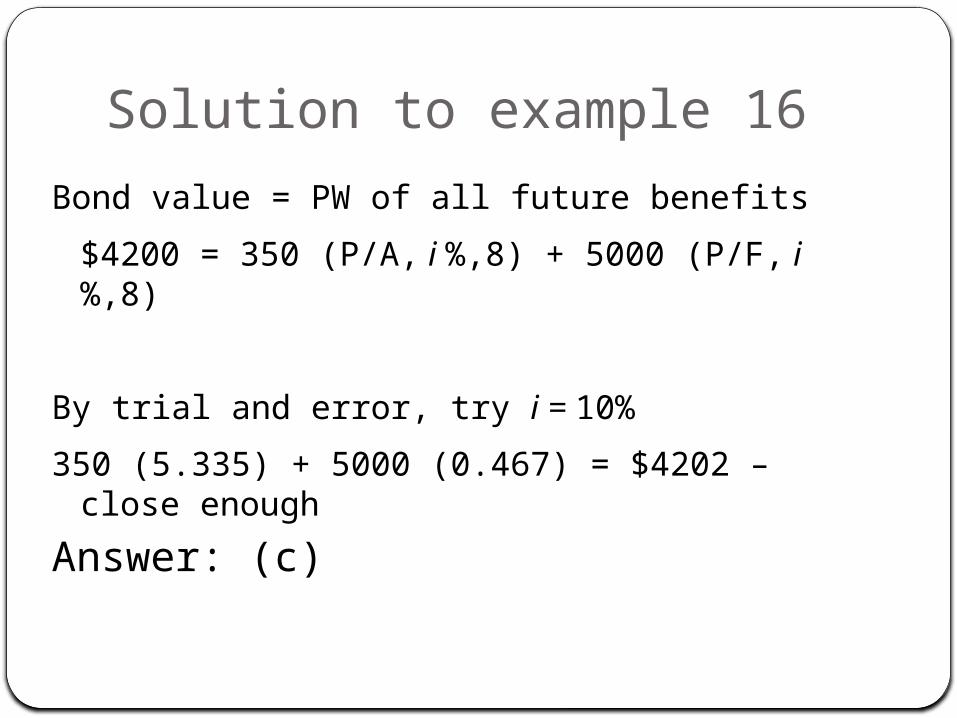

Example 16 – Bonds

If the $5000 bond in the previous example could be purchased for $4200, what is the bond yield?

(a) 5%

(b) 8%

(c) 10%

(d) 12%

Solution to example 16

Bond value = PW of all future benefits

$4200 = 350 (P/A, i %,8) + 5000 (P/F, i %,8)

By trial and error, try i = 10%

350 (5.335) + 5000 (0.467) = $4202 – close enough

Answer: (c)

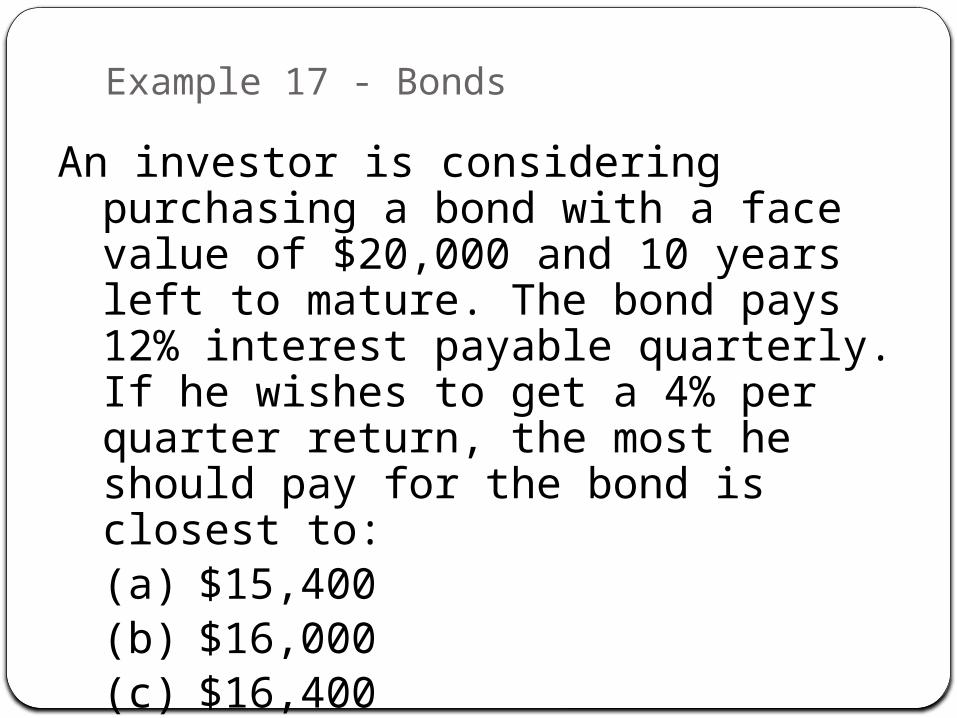

Example 17 - Bonds

An investor is considering purchasing a bond with a face value of $20,000 and 10 years left to mature. The bond pays 12% interest payable quarterly. If he wishes to get a 4% per quarter return, the most he should pay for the bond is closest to:(a) $15,400(b) $16,000(c) $16,400(d) $16,800

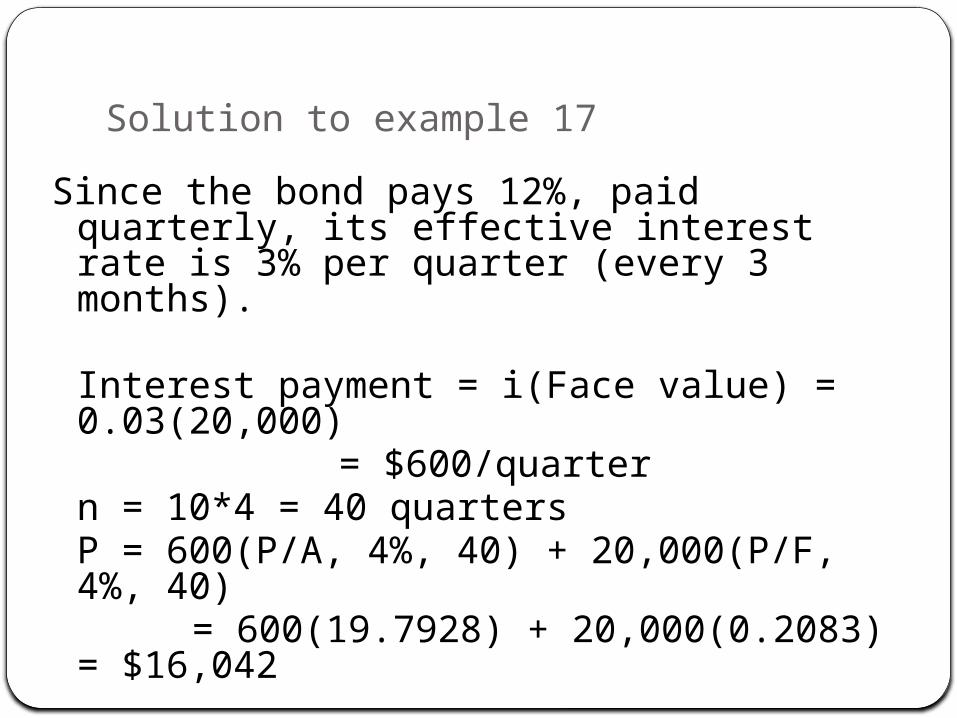

Solution to example 17

Since the bond pays 12%, paid quarterly, its effective interest rate is 3% per quarter (every 3 months).

Interest payment = i(Face value) = 0.03(20,000) = $600/quarter

n = 10*4 = 40 quartersP = 600(P/A, 4%, 40) + 20,000(P/F, 4%, 40)

= 600(19.7928) + 20,000(0.2083) = $16,042

Answer: (b)

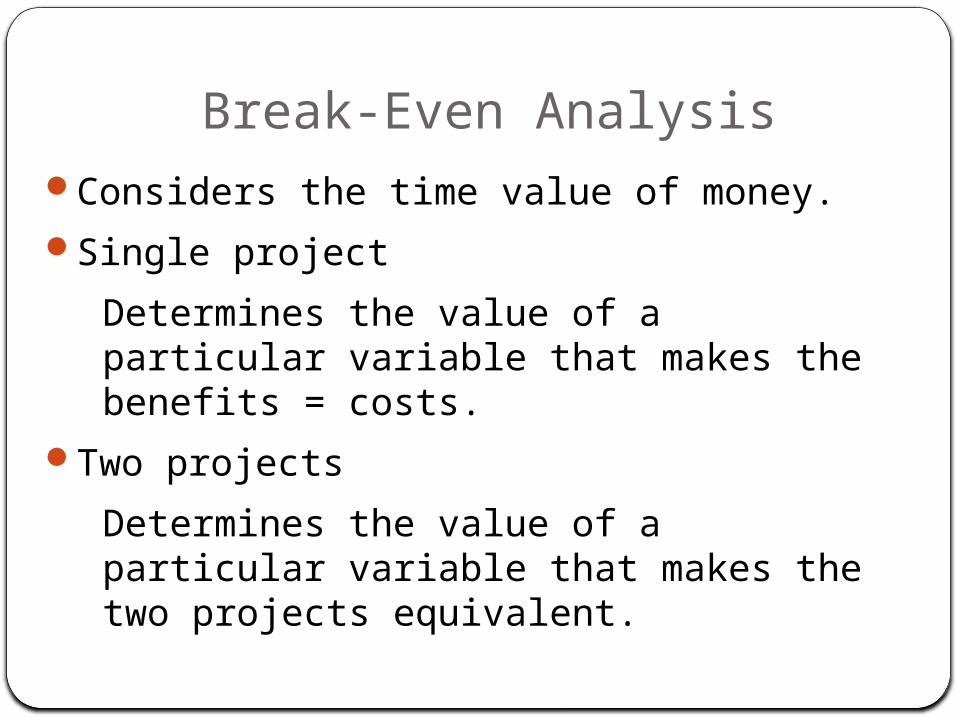

Break-Even Analysis

Considers the time value of money.Single project

Determines the value of a particular variable that makes the benefits = costs.

Two projects

Determines the value of a particular variable that makes the two projects equivalent.

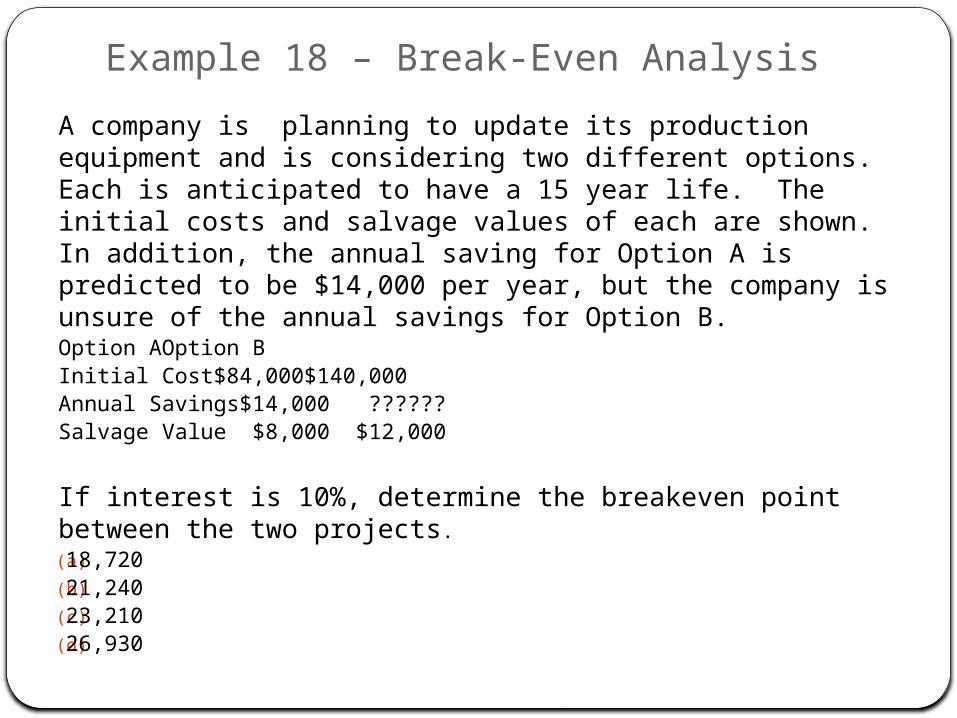

Example 18 – Break-Even Analysis

A company is planning to update its production equipment and is considering two different options. Each is anticipated to have a 15 year life. The initial costs and salvage values of each are shown. In addition, the annual saving for Option A is predicted to be $14,000 per year, but the company is unsure of the annual savings for Option B.

Option A Option BInitial Cost $84,000 $140,000Annual Savings $14,000 ??????Salvage Value $8,000 $12,000

If interest is 10%, determine the breakeven point between the two projects.

(a) 18,720(b) 21,240(c) 23,210(d) 26,930

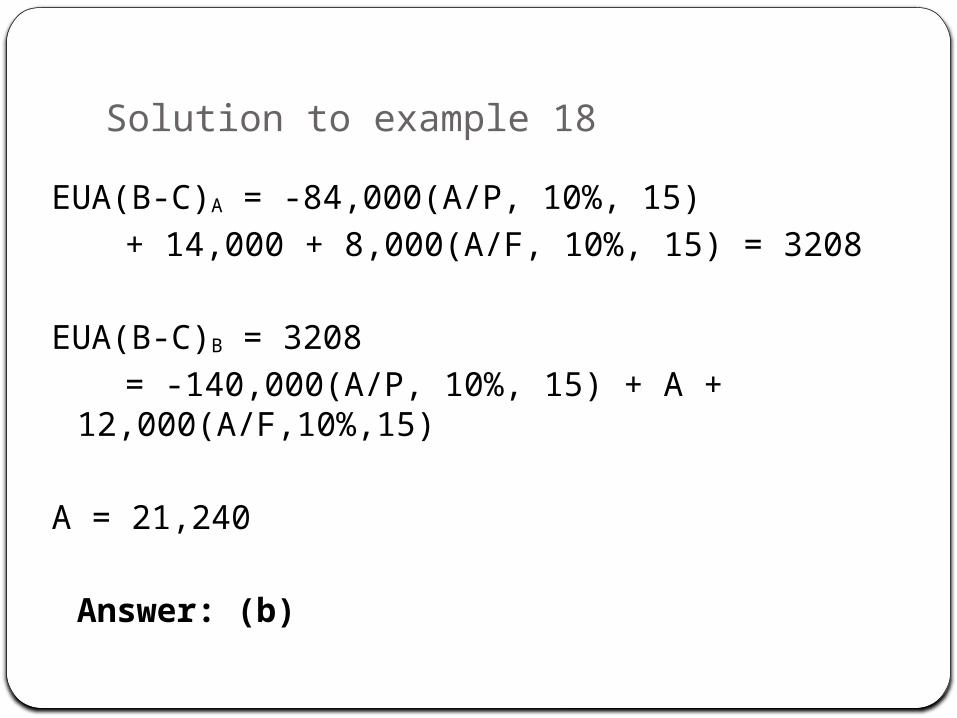

Solution to example 18

EUA(B-C)A = -84,000(A/P, 10%, 15)

+ 14,000 + 8,000(A/F, 10%, 15) = 3208

EUA(B-C)B = 3208

= -140,000(A/P, 10%, 15) + A + 12,000(A/F,10%,15)

A = 21,240

Answer: (b)

Example 19 – Break-Even and Benefit /Cost Analyses

A proposed change to highway design standards is expected to reduce the number of vehicle crashes by 9,200 per year, but have initial cost of $150,000,000 and annual costs of $25,000,000. Given an interest rate of 10% and a study period of 8 years, the average cost of each vehicle crash in order that the benefit-to-cost ratio be 1.0 is closest to:

(a) $5700

(b) $6700

(c) $8700

(d) $9700

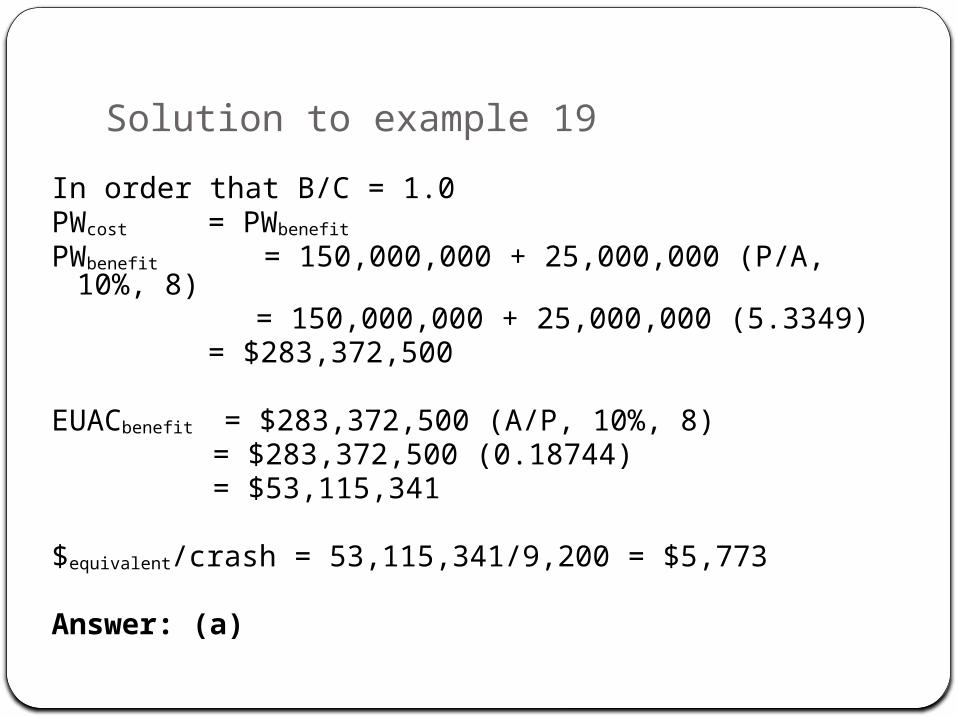

Solution to example 19

In order that B/C = 1.0PWcost = PWbenefit PWbenefit = 150,000,000 + 25,000,000 (P/A, 10%, 8)

= 150,000,000 + 25,000,000 (5.3349) = $283,372,500

EUACbenefit = $283,372,500 (A/P, 10%, 8) = $283,372,500 (0.18744) = $53,115,341

$equivalent/crash = 53,115,341/9,200 = $5,773

Answer: (a)

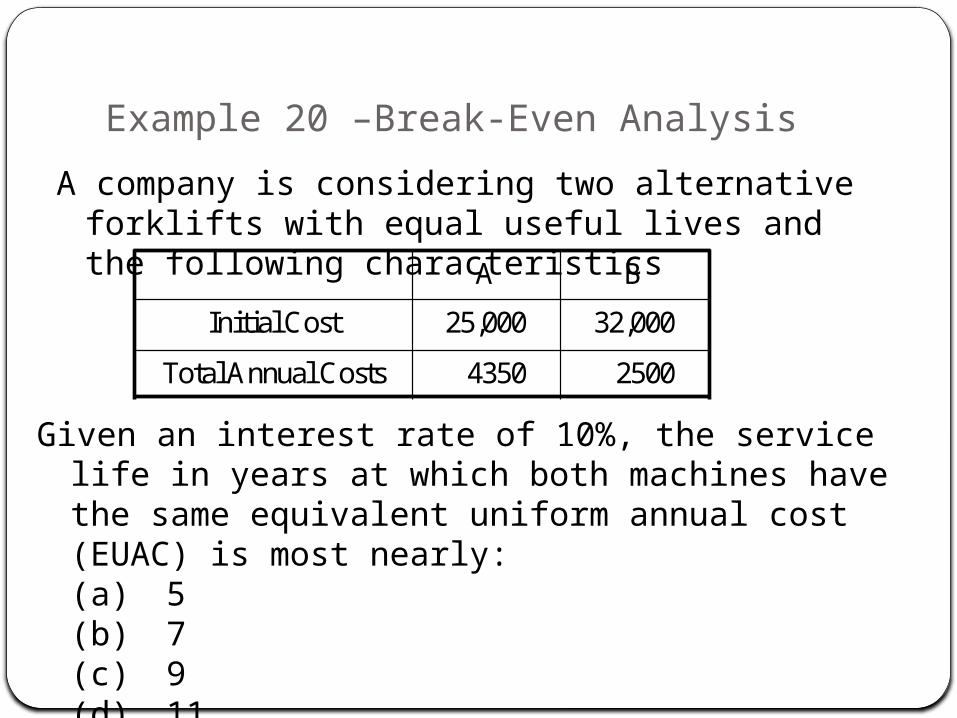

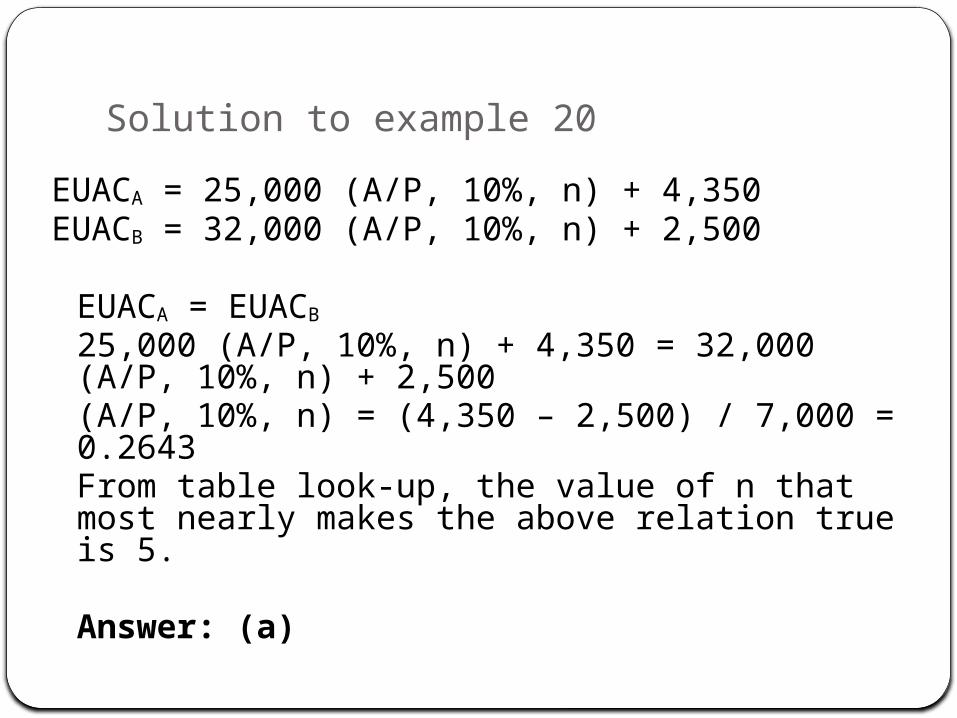

Example 20 –Break-Even Analysis

A company is considering two alternative forklifts with equal useful lives and the following characteristics

A B

Initial Cost 25,000 32,000

Total Annual Costs 4350 2500

Given an interest rate of 10%, the service life in years at which both machines have the same equivalent uniform annual cost (EUAC) is most nearly:(a) 5(b) 7

(c) 9 (d) 11

Solution to example 20

EUACA = 25,000 (A/P, 10%, n) + 4,350EUACB = 32,000 (A/P, 10%, n) + 2,500

EUACA = EUACB

25,000 (A/P, 10%, n) + 4,350 = 32,000 (A/P, 10%, n) + 2,500(A/P, 10%, n) = (4,350 – 2,500) / 7,000 = 0.2643From table look-up, the value of n that most nearly makes the above relation true is 5.

Answer: (a)

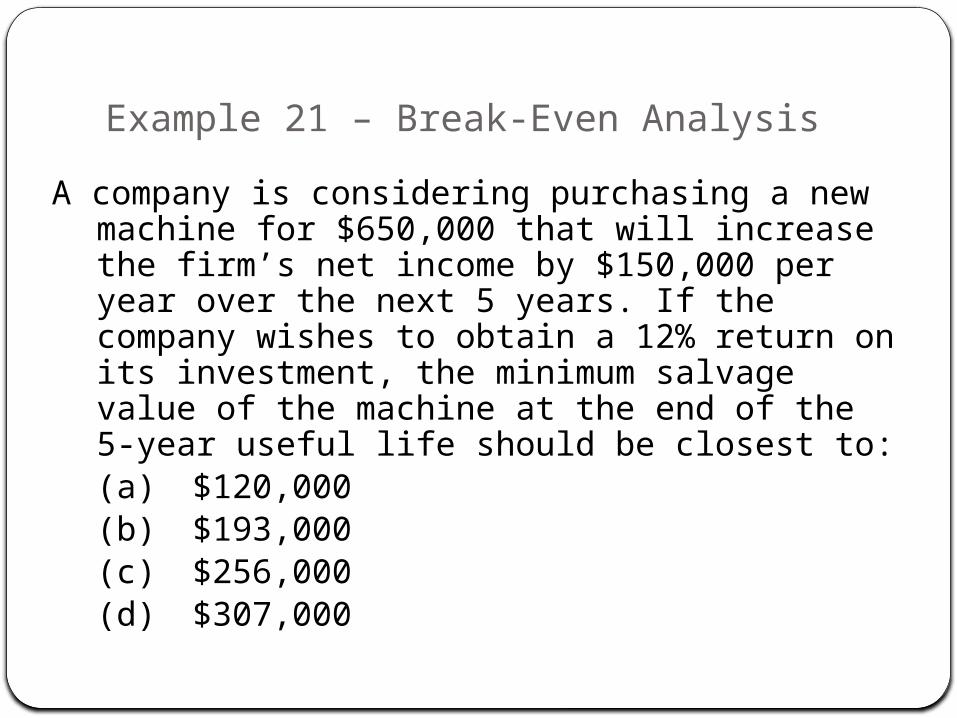

Example 21 – Break-Even Analysis

A company is considering purchasing a new machine for $650,000 that will increase the firm’s net income by $150,000 per year over the next 5 years. If the company wishes to obtain a 12% return on its investment, the minimum salvage value of the machine at the end of the 5-year useful life should be closest to:(a) $120,000(b) $193,000(c) $256,000(d) $307,000

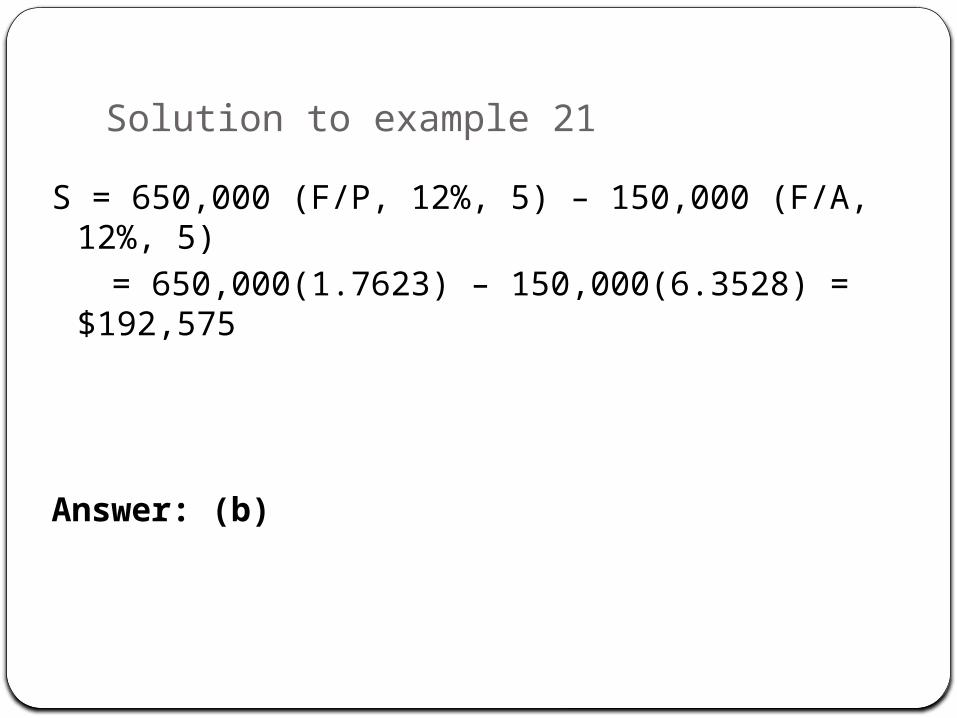

Solution to example 21

S = 650,000 (F/P, 12%, 5) – 150,000 (F/A, 12%, 5)

= 650,000(1.7623) – 150,000(6.3528) = $192,575

Answer: (b)

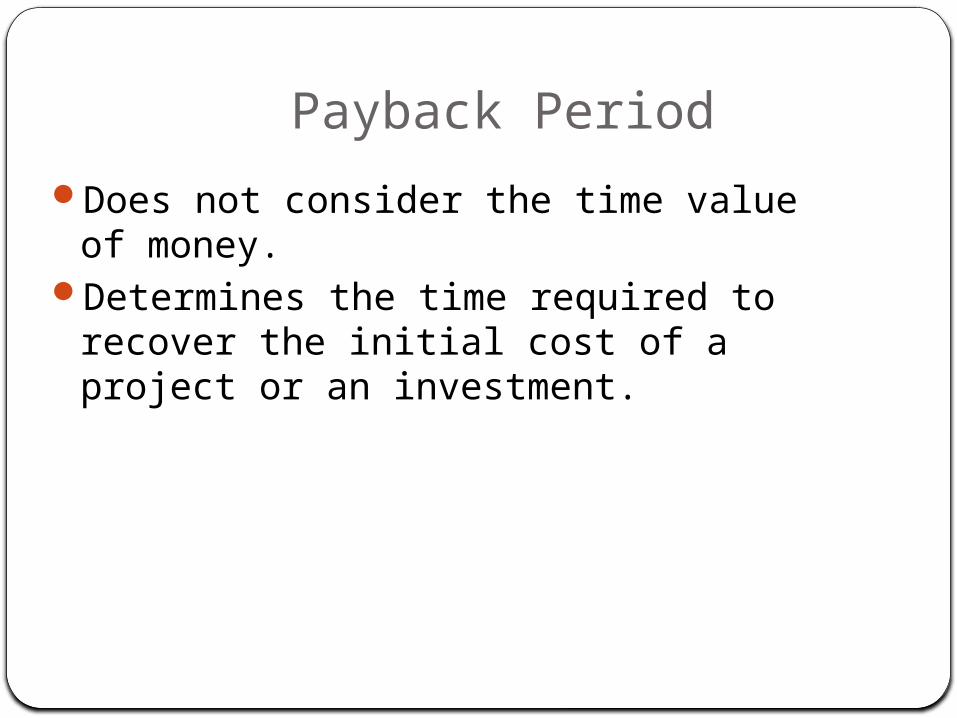

Payback Period

Does not consider the time value of money.

Determines the time required to recover the initial cost of a project or an investment.

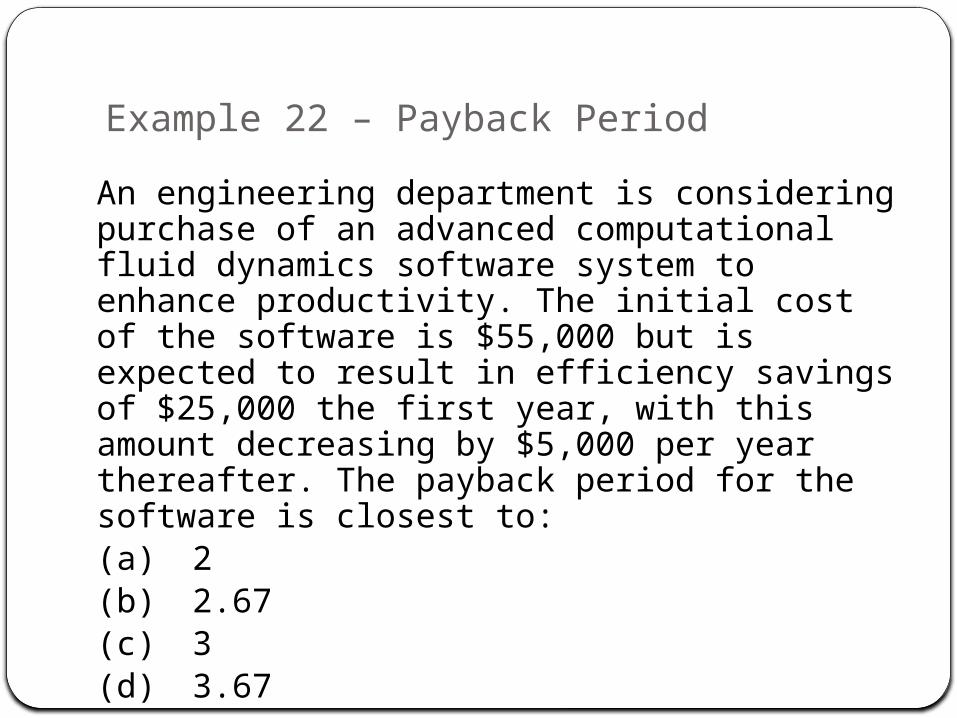

Example 22 – Payback Period

An engineering department is considering purchase of an advanced computational fluid dynamics software system to enhance productivity. The initial cost of the software is $55,000 but is expected to result in efficiency savings of $25,000 the first year, with this amount decreasing by $5,000 per year thereafter. The payback period for the software is closest to: (a) 2(b) 2.67(c) 3(d) 3.67

Solution to example 22

Costs = 55,000 The payback period is the time when total income to date is equal to the total costs.

Costs - Income = 055,000-25,000-20,000=10,000 to pay back at end of year 2. Since the income is stated as $25,000 per year, one can assume that savings occur uniformly throughout the year.15,000 comes in during year 3. Therefore: Payback period =2 + (10,000/15,000) = 2.67

Answer: (b)

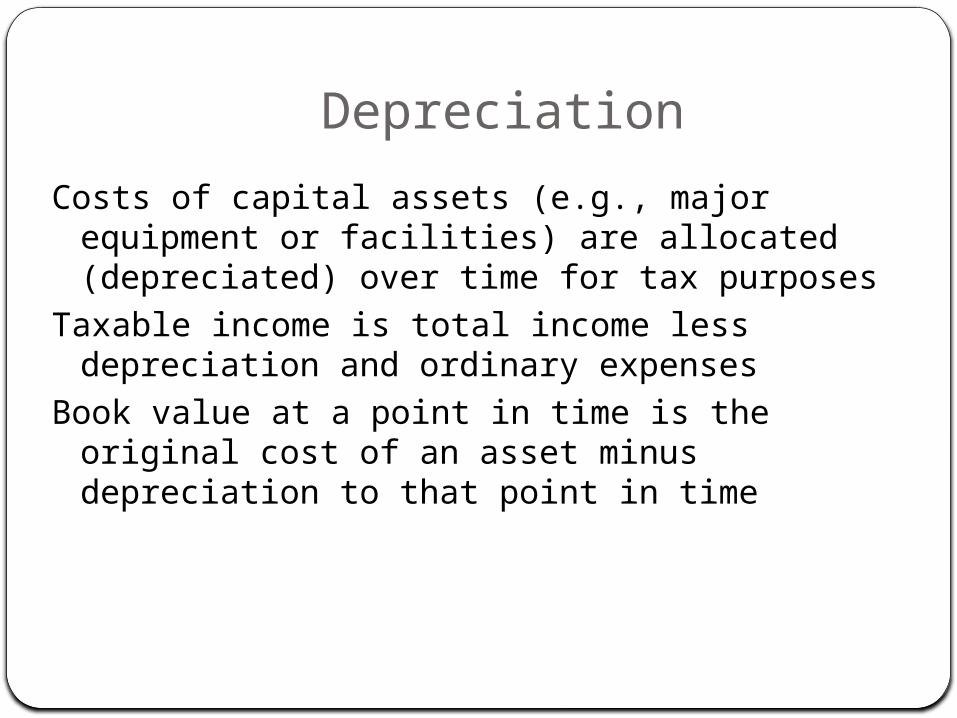

Depreciation

Costs of capital assets (e.g., major equipment or facilities) are allocated (depreciated) over time for tax purposes

Taxable income is total income less depreciation and ordinary expenses

Book value at a point in time is the original cost of an asset minus depreciation to that point in time

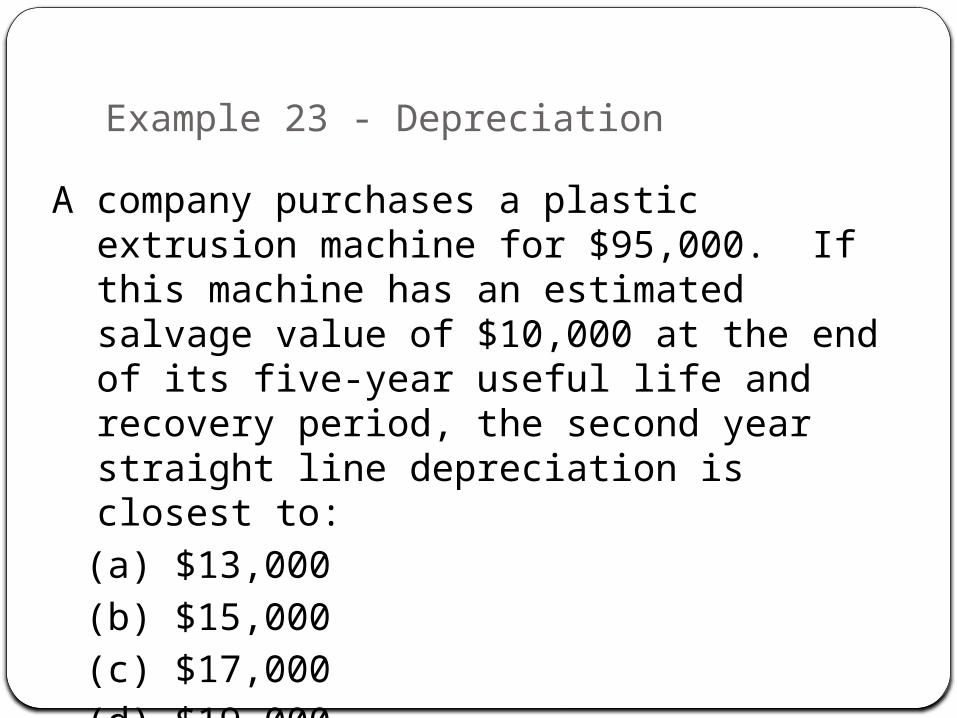

Example 23 - Depreciation

A company purchases a plastic extrusion machine for $95,000. If this machine has an estimated salvage value of $10,000 at the end of its five-year useful life and recovery period, the second year straight line depreciation is closest to:

(a) $13,000

(b) $15,000

(c) $17,000

(d) $19,000

Solution to example 23

Dt = D2 = (95,000 – 10,000)/5 = $17,000

Answer: (c)

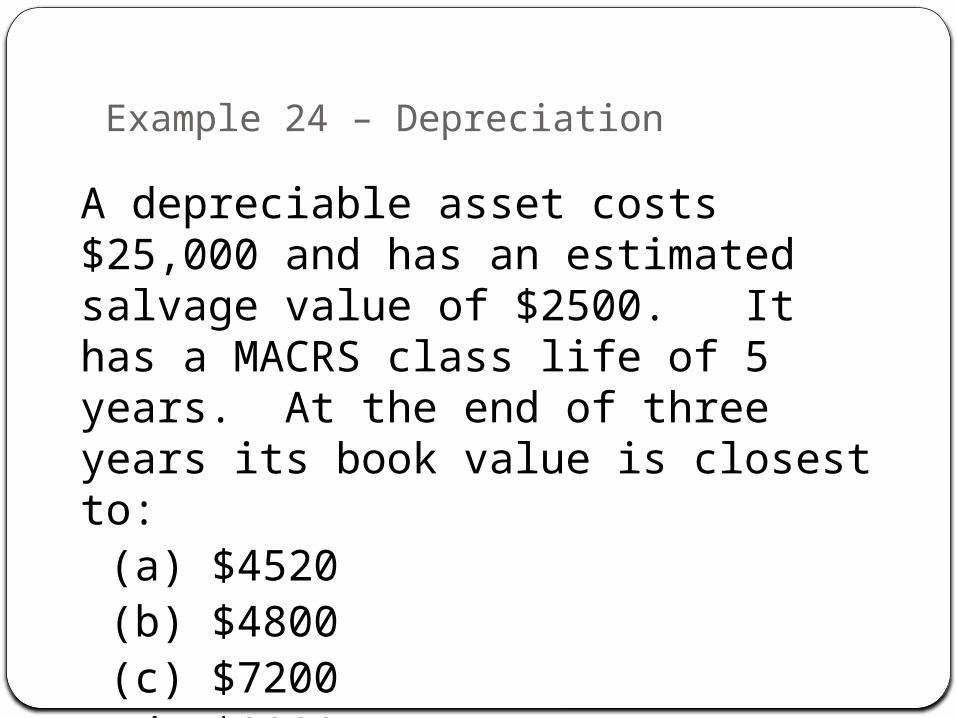

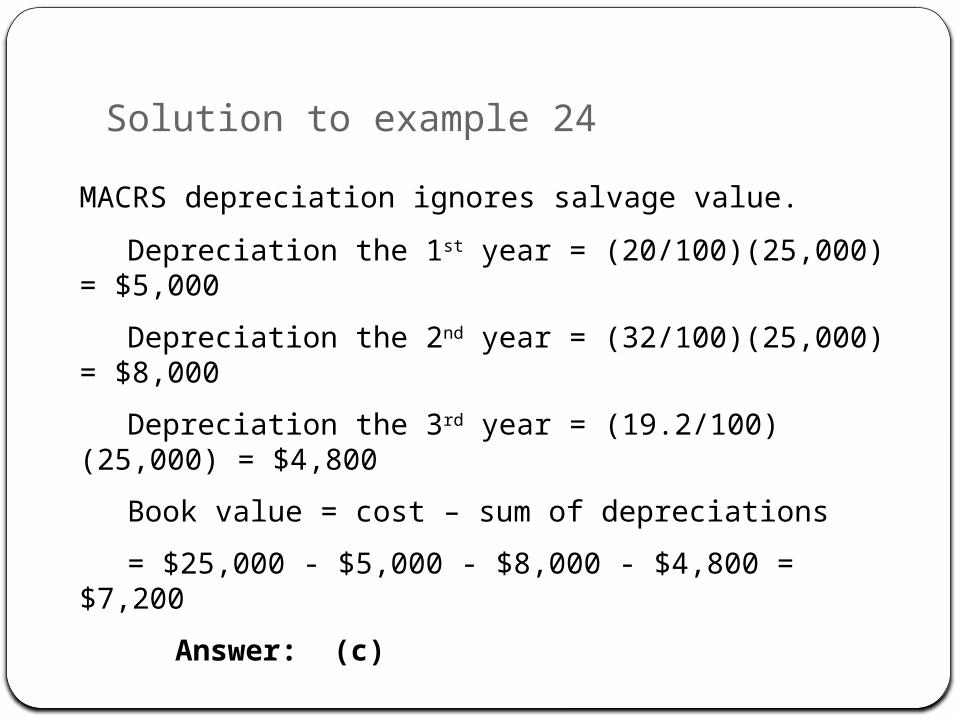

Example 24 – Depreciation

A depreciable asset costs $25,000 and has an estimated salvage value of $2500. It has a MACRS class life of 5 years. At the end of three years its book value is closest to:

(a) $4520(b) $4800(c) $7200(d) $8980

Solution to example 24

MACRS depreciation ignores salvage value.

Depreciation the 1st year = (20/100)(25,000) = $5,000

Depreciation the 2nd year = (32/100)(25,000) = $8,000

Depreciation the 3rd year = (19.2/100)(25,000) = $4,800

Book value = cost – sum of depreciations

= $25,000 - $5,000 - $8,000 - $4,800 = $7,200

Answer: (c)

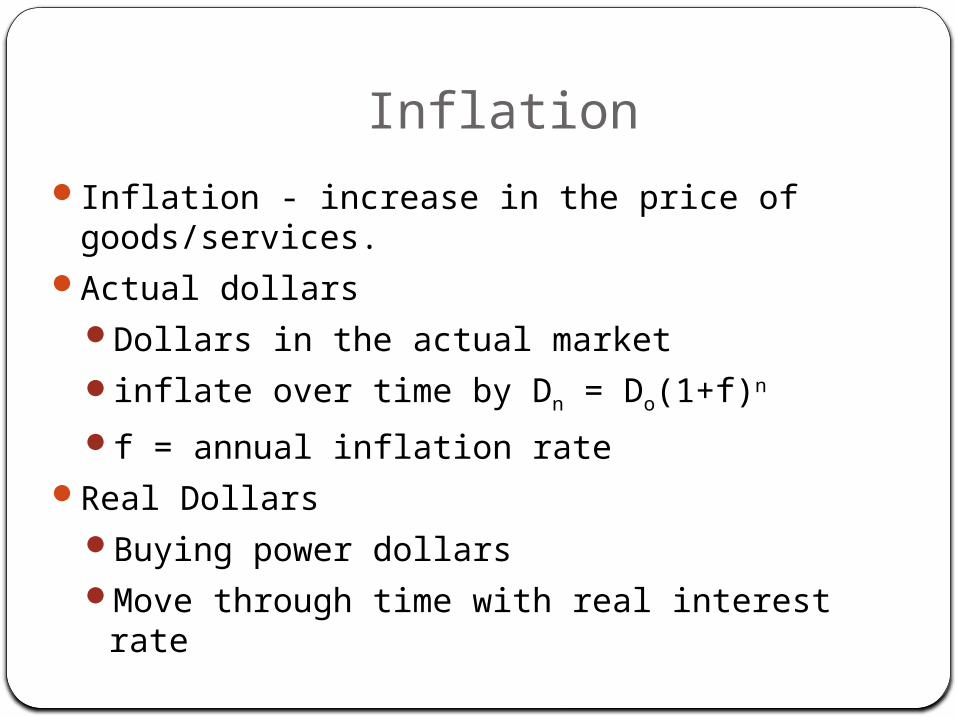

Inflation

Inflation - increase in the price of goods/services.Actual dollars

Dollars in the actual marketinflate over time by Dn = Do(1+f)n

f = annual inflation rateReal Dollars

Buying power dollarsMove through time with real interest rate

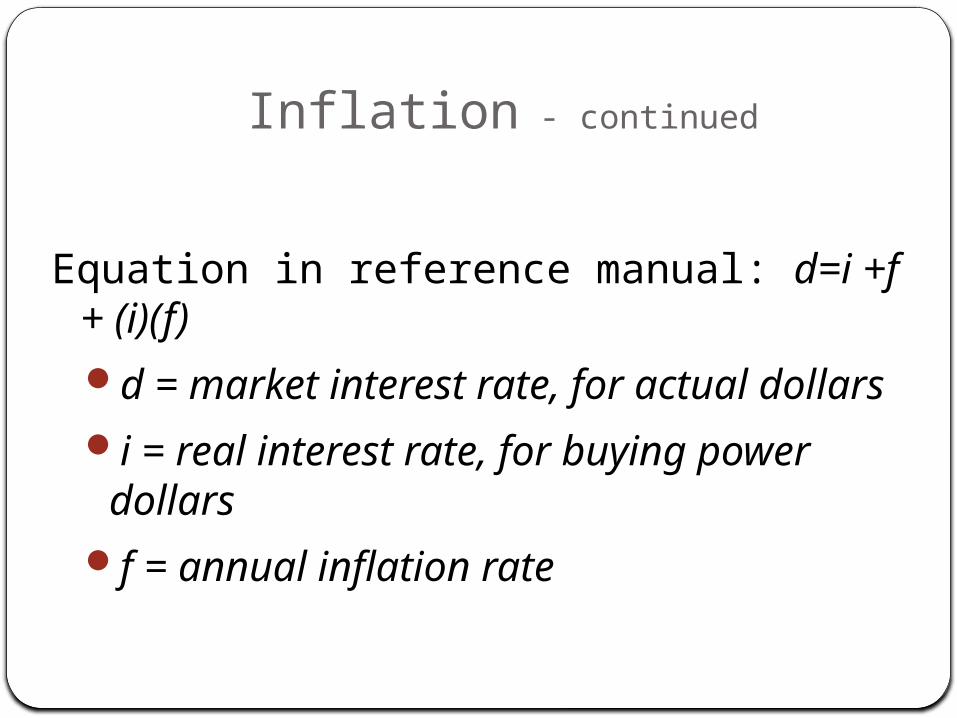

Inflation - continued

Equation in reference manual: d=i +f + (i)(f)d = market interest rate, for actual dollars

i = real interest rate, for buying power dollars

f = annual inflation rate

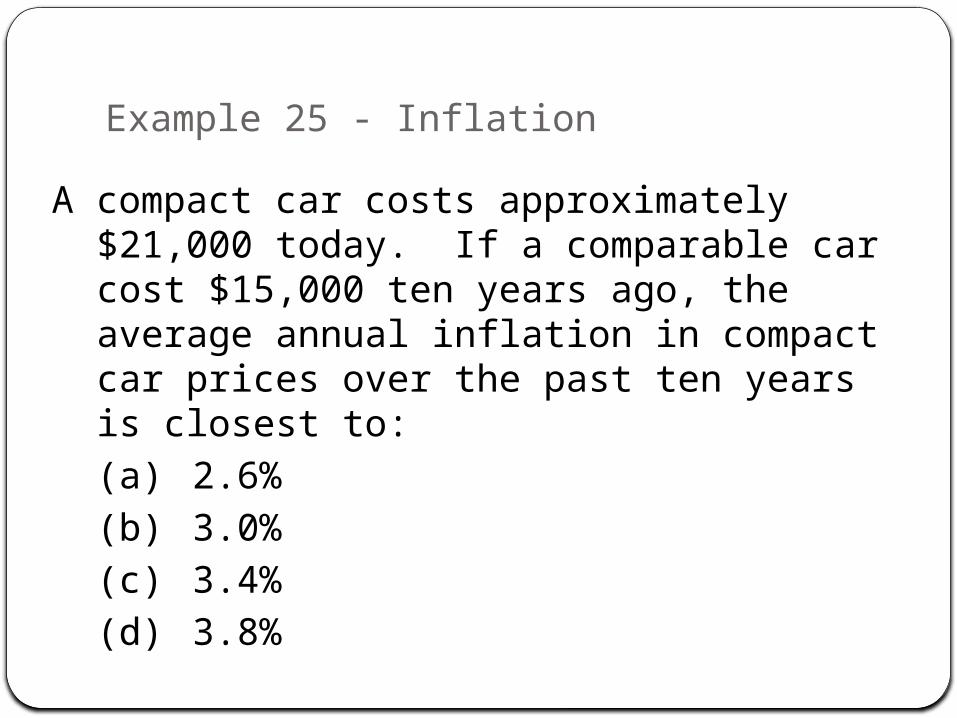

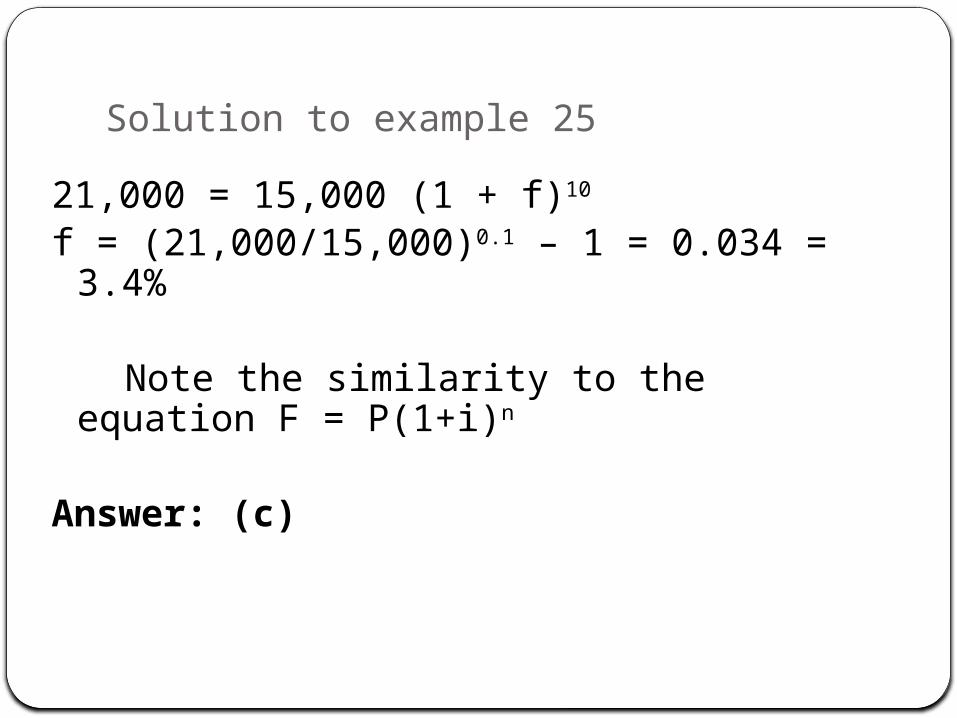

Example 25 - Inflation

A compact car costs approximately $21,000 today. If a comparable car cost $15,000 ten years ago, the average annual inflation in compact car prices over the past ten years is closest to:

(a) 2.6%

(b) 3.0%

(c) 3.4%

(d) 3.8%

Solution to example 25

21,000 = 15,000 (1 + f)10

f = (21,000/15,000)0.1 – 1 = 0.034 = 3.4%

Note the similarity to the equation F = P(1+i)n

Answer: (c)

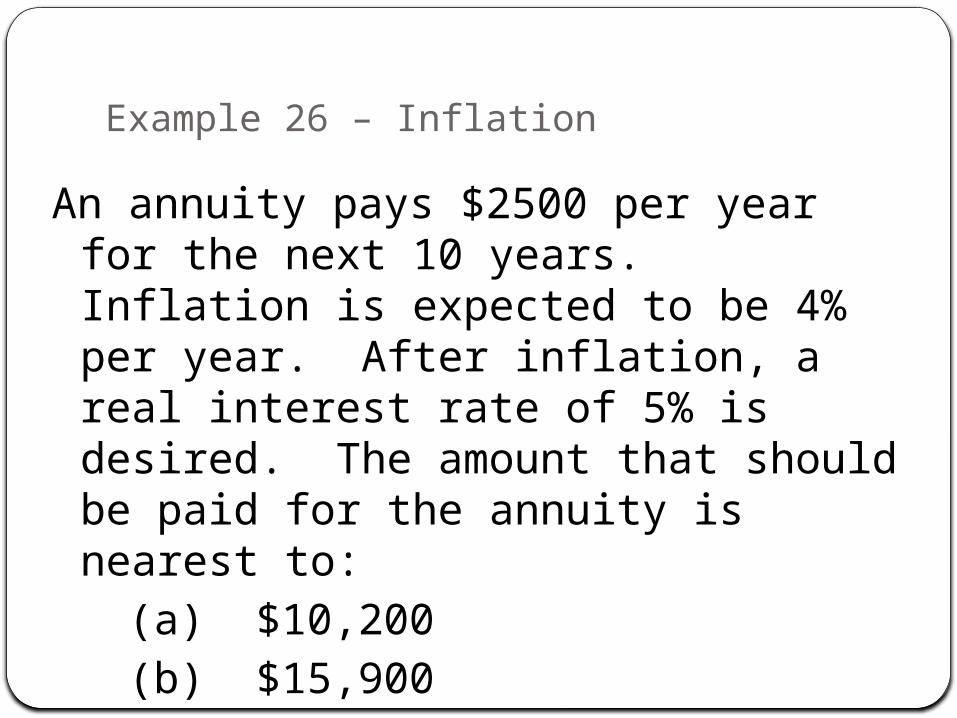

Example 26 – Inflation

An annuity pays $2500 per year for the next 10 years. Inflation is expected to be 4% per year. After inflation, a real interest rate of 5% is desired. The amount that should be paid for the annuity is nearest to:

(a) $10,200(b) $15,900(c) $18,600(d) $25,000

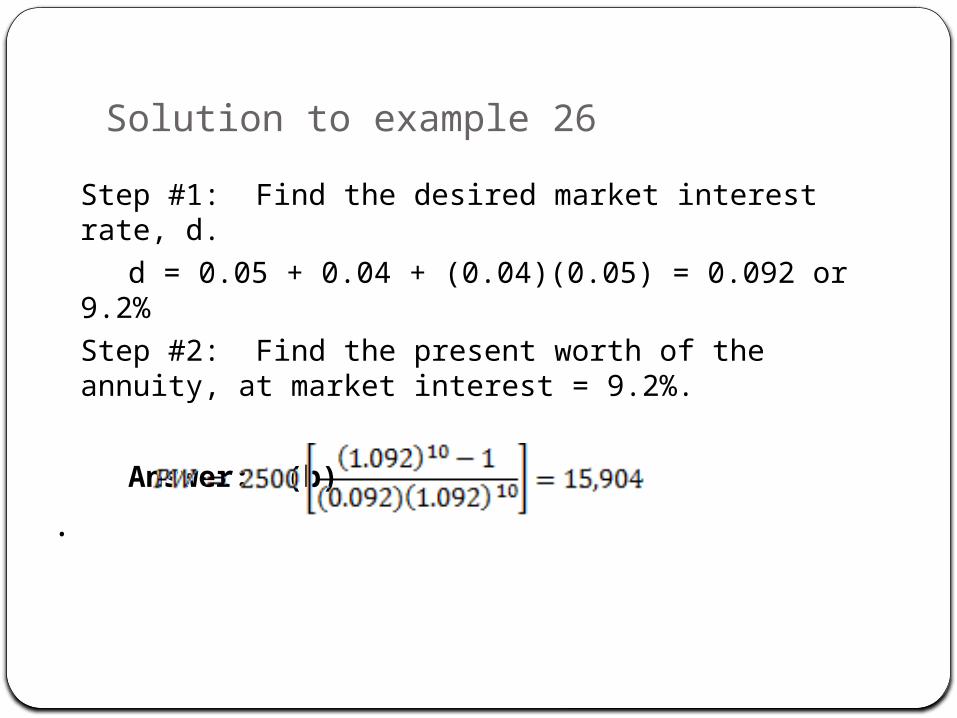

Solution to example 26

Step #1: Find the desired market interest rate, d.

d = 0.05 + 0.04 + (0.04)(0.05) = 0.092 or 9.2%

Step #2: Find the present worth of the annuity, at market interest = 9.2%.

Answer: (b)

.

SourcesFundamentals of Engineering Supplied-Reference

Handbook, 8th Edition, Revised – pg. 114-120Engineering Economic Analysis, 11th Edition, D.G.

Newnan, J.P Lavelle, & T.G. Eschenbach, Oxford University Press, 2012

![[Shinobi] Bleach 466](https://static.fdocuments.in/doc/165x107/568c4a721a28ab4916982d2e/shinobi-bleach-466.jpg)