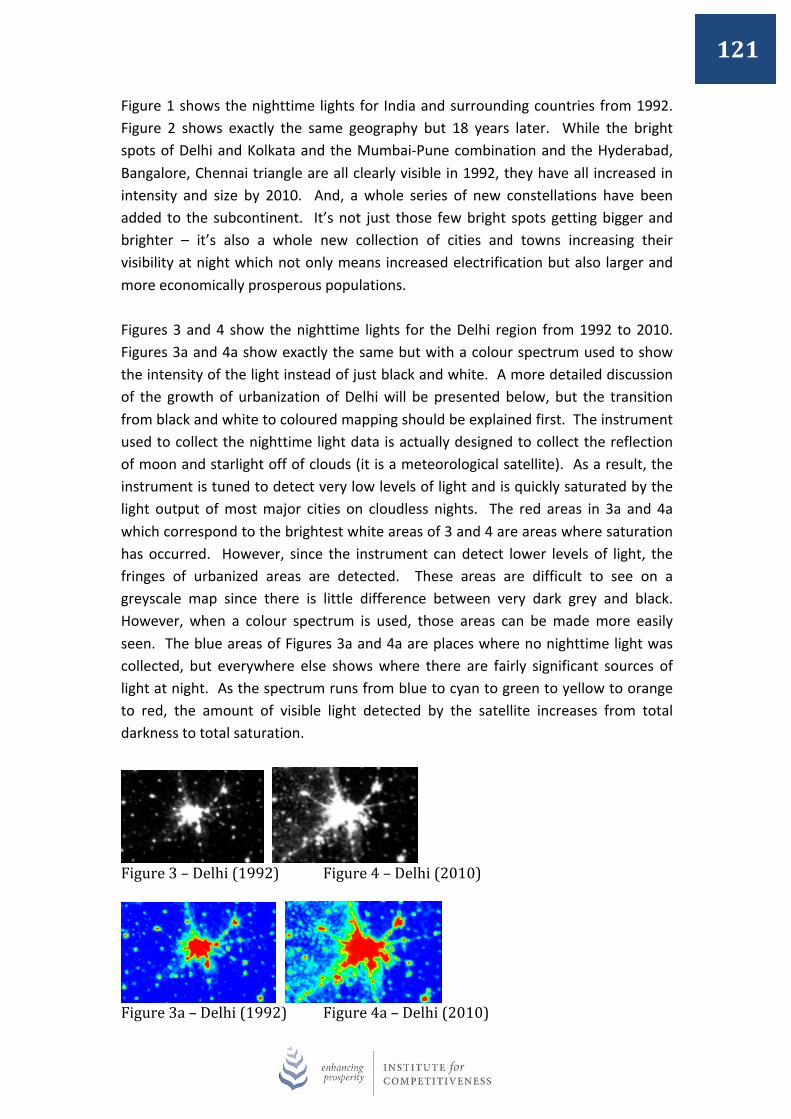

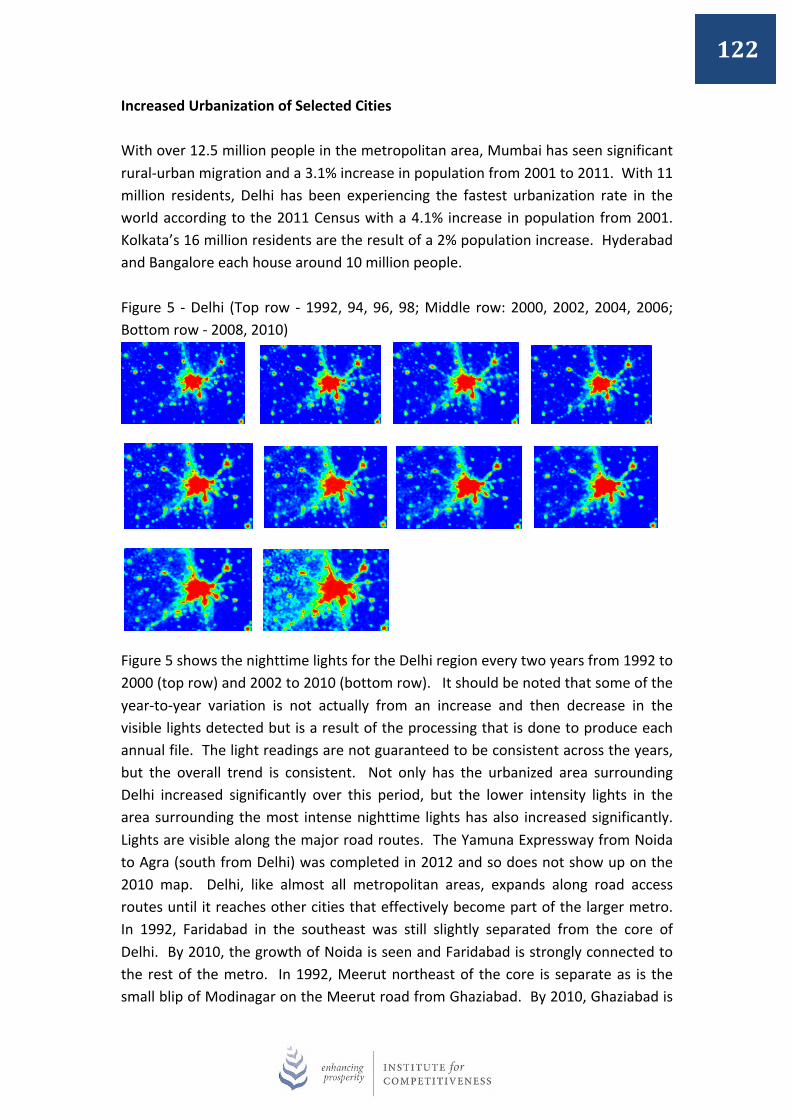

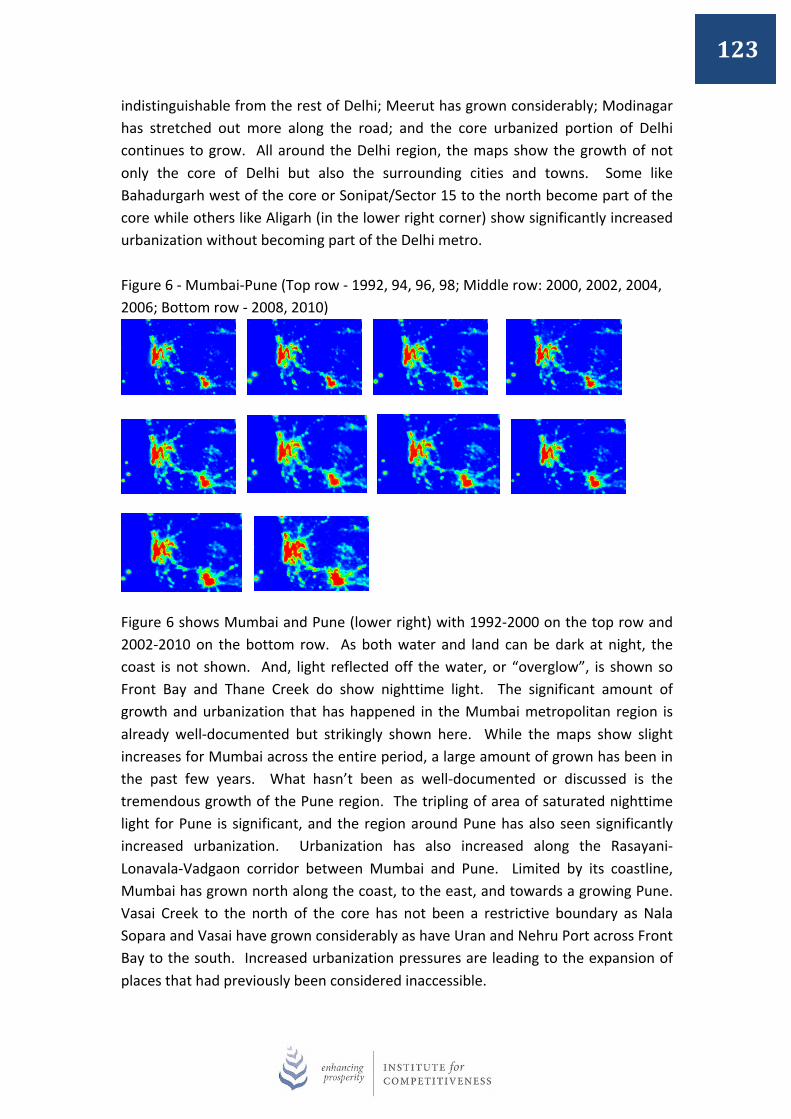

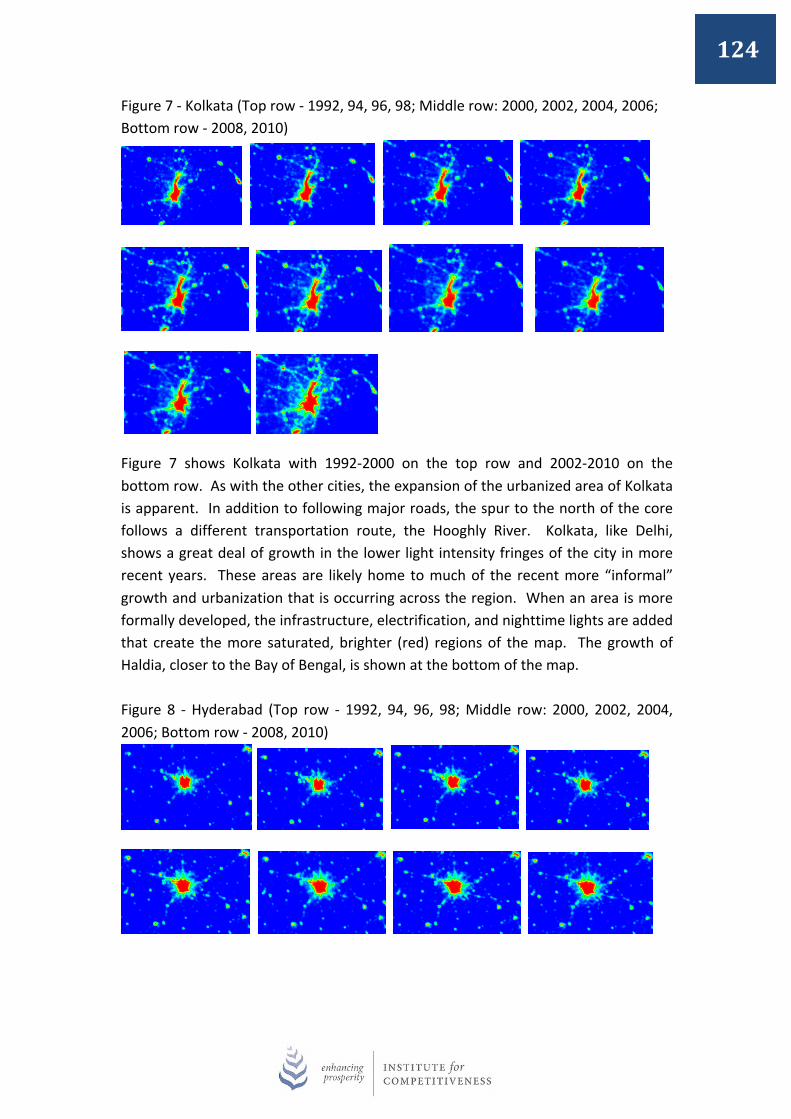

CCR2013 Final Edited - Martin Prosperity...

144

India City Competitiveness Report 2013

Transcript of CCR2013 Final Edited - Martin Prosperity...

India City Competitiveness Report 2013

India City Competitiveness Report 2013

PREFACE The India City Competitiveness Report (ICCR) has being in publication since 2008, and we are happy to release the Sixth Edition of the Report in November 2013. Similar to the previous years, the report evaluates the 50 Indian cities. The report deeply studies, understands and highlights the strong and weak areas of these cities via its city competitiveness index. It also provides an understanding of their present performance with respect to their previous year competitiveness levels. The report offers broad recommendations for government officials, corporations, investors and residents to steer the future of cities with timely action. The report begins with an introduction on competitiveness, explaining about the framework and touching upon India’s competitiveness levels. This was followed by methodological framework used to analyse the data points and ranking of 50 Indian cities on individual pillars and sub-‐indices. The remaining chapters provide insights about the lesser-‐known facts about the Indian cities in terms of their positives and negatives and then, address the attractiveness level of Indian cities on an international platform. Lastly, it also underlines the steps required to redefine the future of the Indian cities.

EXECUTIVE SUMMARY The India City Competitiveness 2013 report evaluates the competitiveness level of 50 Indian cities, which are the building blocks of the nation. The Microeconomic Competitiveness – Diamond Model given by Michael E. Porter, a renowned Harvard Business School Professor has been the basis of the competitiveness index. It consists of four major pillars used to assess the cities from different and various dimensions to establish the imperatives for growth. The set of 50 Indian cities were evaluated on the above pillars and sub pillars to comprehensively understand their domains and accordingly come up with amicable and practical solutions. According to the city competitiveness index, Delhi is the most competitive city in the country. It has been stable on the numero uno position since 2010 because of few obvious reasons such as good governance, high GDP and better infrastructure. Like last year, Mumbai is constant on its 2nd position further followed by Chennai on 3rd, Hyderabad on 4th, Kolkata on 5th, Gurgaon on 6th, Noida on 7th, Bengaluru on 8th, Pune on 9th and Ahmedabad on 10th position. Much more is now expected from the small Indian cities classified as ‘Y’ (according to the sixth central pay commission). Some of cities like Kochi, Surat, Nashik, Jaipur and Indore have performed well on the city competitiveness index and are fast running upwards on the index. They have exhibited good functioning on some crucial pillars. As a result, they are way ahead with good competitiveness rankings in comparison to other cities of the same nature. It is thus vital to enhance the local competition existent in between the cities. It will not only make them more stable and unique but will also help them to join the league of international cities. Hence the city competitiveness index comes into the picture. It serves as a tool to help the cities grow in a sustainable manner, complementing their own inherent strengths and developing a clear vision for their future.

TABLE OF CONTENTS PREFACE EXECUTIVE SUMMARY 1.0 SUMMARIZING THE VITAL CONCEPTS OF COMPETITIVENESS……………………1

1.1 Overview…………………………………………………………………………………………..2 1.2 Factors of Competitiveness……………………………………………………………….3 1.3 Some of the salient features……………………………………………………………..5 1.4 India’s Competitiveness…………………………………………………………………….7 1.5 A look at the Competitiveness of regions & cities in India………………….9 1.6 Urbanization: A Phenomenon w.r.t. India……………………………..…………10 1.7 Classification of Indian cities…………………………………………………………….13 1.8 Increase in the number of Metropolitan areas…………………………………14

2.0 METHODOLOGICAL FRAMEWORK………………………………………………………..…19

2.1 Unit of Analysis……………………………………………………………………………….20 2.2 Data sources & their quality……………………………………………………………23 2.3 About City Competitiveness Index 2013……………………………………….…24 2.4 Analysis the data indicators………………………………………………………..…..25 2.5 Steps undertaken………………………………………………………………………..….25 2.6 The 50 Indian cities addressed…………………………………………………..……27

3.0 RANKINGS…………………………………………………………….…………………………………...28

3.1 The top achievers: Most competitive cities in India………………………...29 3.2 The 11-‐20 positions: Holding immense potential…………………………….30 3.3 The 21-‐30 positions: On the growth path………………………………………..30 3.4 The 31-‐40 positions: Seeking new opportunities……………………………..31 3.5 The 41-‐50 positions: In a developing state……………………………………….31 [Tables] ………………………………………………………………………………………………...32

4.0 PROFILE OF 50 INDIAN CITIES……………………………………………………………………49

5.0 THRIVING INDIAN CITIES: FACE OF THE COUNTRY…………………………………..100

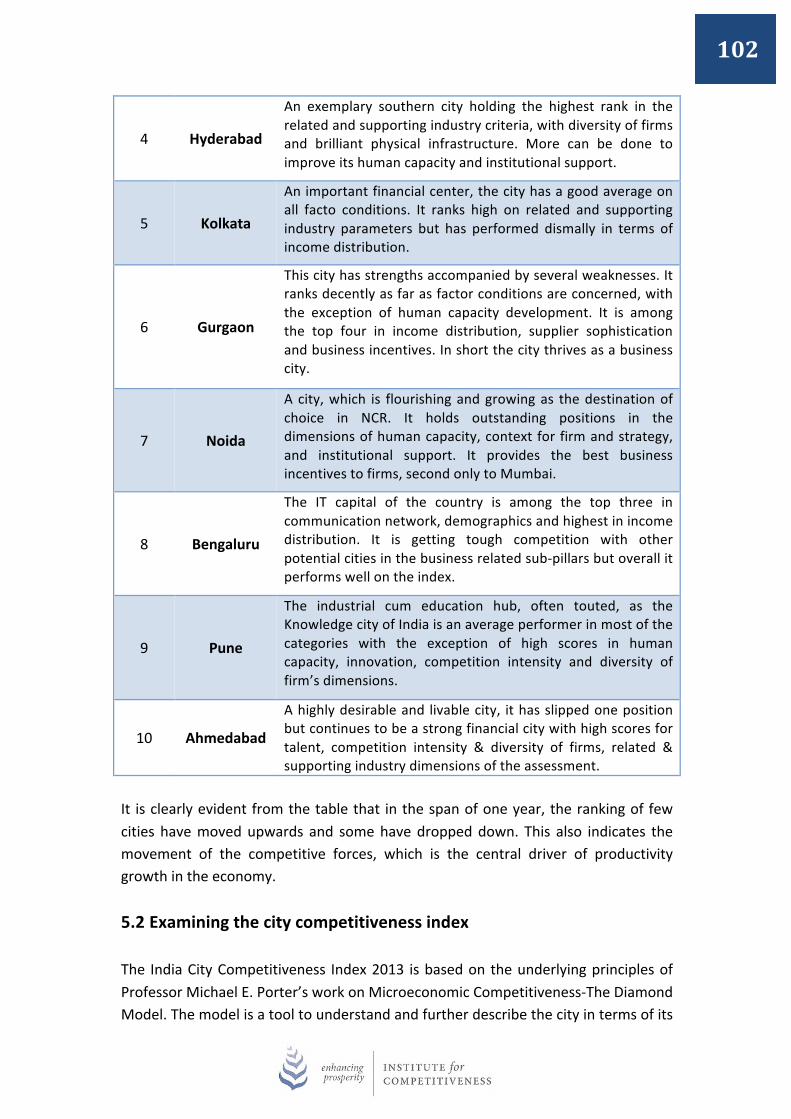

5.1 Unfolding the lesser known facts of the most competitive cities of India……………………………………………………………………………………………….101

5.2 Examining the city competitiveness index………………………………………102 5.3 Potential of small cities classified as ‘Y’ & ‘Z’…………………………………..104 5.4 Poverty in urban India…………………………………………………………………....105 5.5 Doing Business in India……………………………………………………………………106 5.6 Growth of Urban clusters in India…………………………………………………..107

5.7 Urban Mobility System…………………………………………………………………..108 5.8 Smart and Sustainable cities…………………………………………………………..109

6.0 WAYS TO ENHANCE THE CITY COMPETITIVENESS……………………………………111

6.1 The role of governance & inclusive issues……………………………………….112 6.2 Key areas of focus for future Indian cities……………………………………….113 6.3 Critical success factors for city competitiveness………………………………115 6.4 A note on Urban agglomeration, cities and regions………………………..116 6.5 Ideas to shape Indian cities for future…………………………………………….117

7.0 CONTRIBUTIONS……………………………………………………………………………………..119

8.0 REFERENCES…………………………………………………………………………………………….134 APPENDIX

Boxes Box 1: Confusion around the concept of competitiveness……………………………….3 Box 2: Success story of the Indian IT City Bengaluru…………………………………….….9 Box 3: Population density: Urban Change turning into an urban challenge…….11 Box 4: Boundless NCR…………………………………………………………………………………….16 Box 5: A different side of Kolkata – Slums and misery…………………………………...105 Box 6: Ecocabs: Dial-‐A-‐Rickshaw Scheme……………………………………………………….108 Box 7: Delhi Metro: The lifeline of the city and nearby area…………………………..109 Box 8: PPPs in India’s Infrastructure Development -‐ Airport project……………...114

Graphs Graph 1: India on Global Competitiveness Index…………………………………….……….8

Diagrams Diagram 1: Influences of Competitiveness…………………………………………………..…3 Diagram 2: Microeconomic Competitiveness: The Diamond Model…………..…..4 Map Map 1: Snapshot of urban India in 2011……………………………………………………….12 Map 2: Automobile cluster in India………………………………………………………...…..107

Tables Table 1: Population of UAs/Towns as per Census of India 2011…………………...22 Table 2: Number of UAs, Towns, Out Growths (OGs) and villages…………….…..23 Table 3: Classification of pillar and sub-‐indices……………………………………….…….24

1

1.0 SUMMARIZING THE VITAL CONCEPTS OF COMPETITIVENESS

2

1.1 Overview During the financial year 2012-‐13, Indian economy grew at the slowest pace for the first time in a decade. Even the current year does not seem to be much promising. There are talks and discussions amongst intellectuals that India will soon regain its lost glory, but some of the people also have certain apprehensions. Now, one of the world’s fastest growing developing country looks in a state of turmoil with various missing elements of growth. Undoubtedly, India has a very important role to play in the global economy, and it has to realize the fact sooner than later. India with a population base of 1.2 billion can do wonders if it finds ways to improve its competitiveness levels. It has to work upon creating job opportunities and better infrastructure, building social capital, providing basic amenities and implementing a stable policy environment. In other words, Competitiveness is defined as ‘the set of institutions, policies and factors that determine the level of productivity in a country.’

Today the poor infrastructure, investment barriers and lack of innovative ideas are acting as a caveat in the growth of the country. So the drivers of competitiveness should be reconsidered in order to create more business opportunities, enhance the social infrastructure and become more competitive. Thus, India has a long way to go to enter the league of competitive countries of the world. The Institute for Competitiveness, India is thus trying to illustrate the true picture of the country by mapping its ‘powerhouse’ cities and with the help of competitiveness index and analysis. The index is a robust and credible tool to study the competitiveness of Indian cities as it is based on the work of Professor Michael E.

What Determines Competitiveness? Competitiveness depends on the productivity with which a location uses its human, capital, and natural resources.

§ Productivity sets the sustainable standard of living (wages, return on capital, returns on natural resources)

§ It is not what industries a nation competes in that matters for prosperity, but how it competes in those industries

§ Productivity in a nation is a reflection of what both domestic and foreign firms choose to do in that location. The location of ownership is secondary for national prosperity.

Source: Michael E. Porter, 2008

3

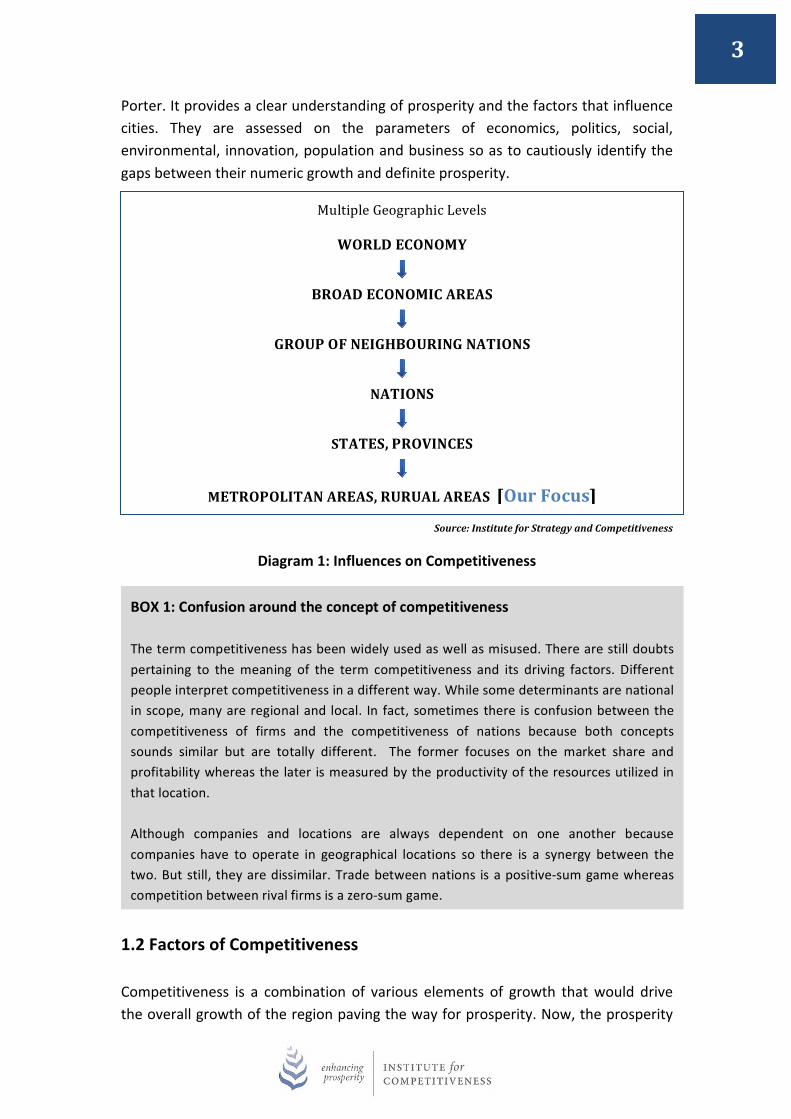

Porter. It provides a clear understanding of prosperity and the factors that influence cities. They are assessed on the parameters of economics, politics, social, environmental, innovation, population and business so as to cautiously identify the gaps between their numeric growth and definite prosperity.

Source: Institute for Strategy and Competitiveness

Diagram 1: Influences on Competitiveness

1.2 Factors of Competitiveness Competitiveness is a combination of various elements of growth that would drive the overall growth of the region paving the way for prosperity. Now, the prosperity

BOX 1: Confusion around the concept of competitiveness The term competitiveness has been widely used as well as misused. There are still doubts pertaining to the meaning of the term competitiveness and its driving factors. Different people interpret competitiveness in a different way. While some determinants are national in scope, many are regional and local. In fact, sometimes there is confusion between the competitiveness of firms and the competitiveness of nations because both concepts sounds similar but are totally different. The former focuses on the market share and profitability whereas the later is measured by the productivity of the resources utilized in that location. Although companies and locations are always dependent on one another because companies have to operate in geographical locations so there is a synergy between the two. But still, they are dissimilar. Trade between nations is a positive-‐sum game whereas competition between rival firms is a zero-‐sum game.

Multiple Geographic Levels

WORLD ECONOMY

BROAD ECONOMIC AREAS

GROUP OF NEIGHBOURING NATIONS

NATIONS

STATES, PROVINCES

METROPOLITAN AREAS, RURUAL AREAS [Our Focus]

4

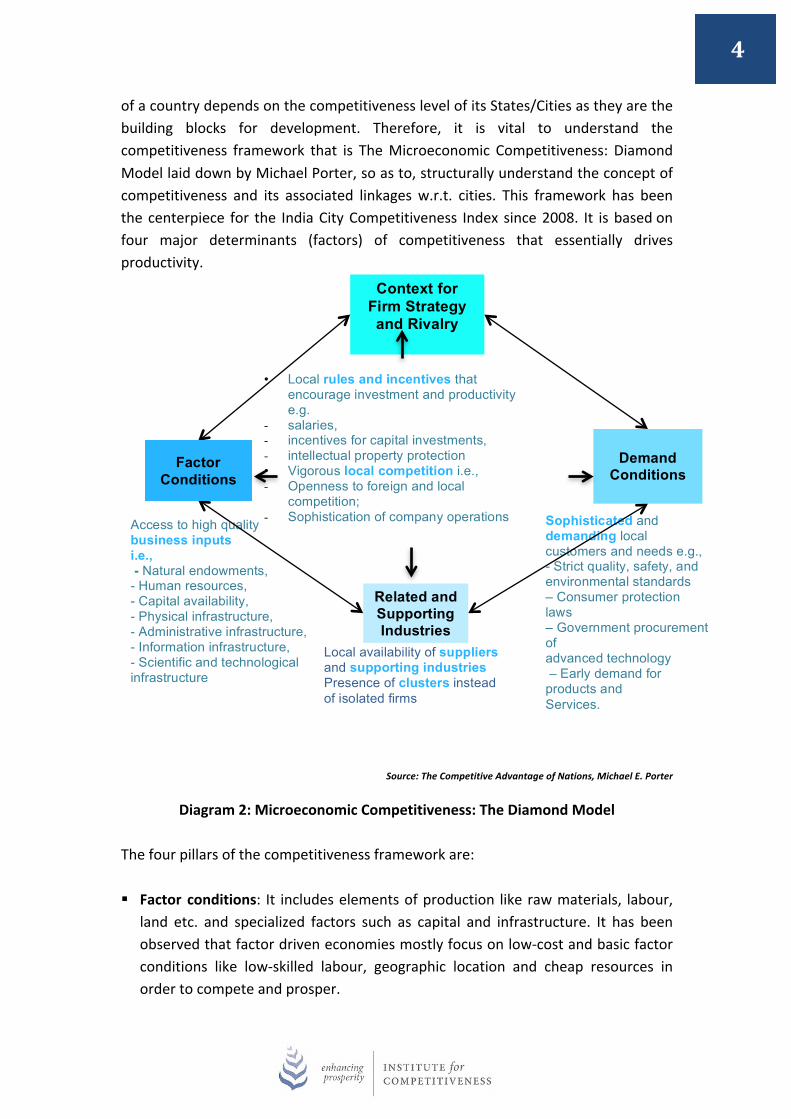

of a country depends on the competitiveness level of its States/Cities as they are the building blocks for development. Therefore, it is vital to understand the competitiveness framework that is The Microeconomic Competitiveness: Diamond Model laid down by Michael Porter, so as to, structurally understand the concept of competitiveness and its associated linkages w.r.t. cities. This framework has been the centerpiece for the India City Competitiveness Index since 2008. It is based on four major determinants (factors) of competitiveness that essentially drives productivity.

Source: The Competitive Advantage of Nations, Michael E. Porter

Diagram 2: Microeconomic Competitiveness: The Diamond Model The four pillars of the competitiveness framework are: § Factor conditions: It includes elements of production like raw materials, labour,

land etc. and specialized factors such as capital and infrastructure. It has been observed that factor driven economies mostly focus on low-‐cost and basic factor conditions like low-‐skilled labour, geographic location and cheap resources in order to compete and prosper.

Context for Firm Strategy and Rivalry

Related and Supporting Industries

Demand Conditions

• Local rules and incentives that encourage investment and productivity e.g.

- salaries, - incentives for capital investments, - intellectual property protection • Vigorous local competition i.e., - Openness to foreign and local

competition; - Sophistication of company operations

Local availability of suppliers and supporting industries Presence of clusters instead of isolated firms

Sophisticated and demanding local customers and needs e.g., - Strict quality, safety, and environmental standards – Consumer protection laws – Government procurement of advanced technology – Early demand for products and Services.

Access to high quality business inputs i.e., - Natural endowments, - Human resources, - Capital availability, - Physical infrastructure, - Administrative infrastructure, - Information infrastructure, - Scientific and technological infrastructure

Factor Conditions

5

§ Demand conditions: These take into consideration the needs, preferences and demands of consumers in an economy. In other words, what product or service does consumers want and what is their affordability ratio in terms of income etc. So the firms, those are better able to understand their consumer in sync with their increasing or decreasing demand for better and innovative product or services that would eventually become more competitive.

§ Context for firm strategy and rivalry: In this competitive environment, firms are

driven to work by increasing their productivity and invention in and around the area. Today, the market is inundated with many local and international companies, which are competing to gain profits, and remain sustainable in the long run. Although, nurturing domestic clusters of competition and encouraging healthy international competition is always a difficult balance. The local rules of taxation and incentives can be beneficial for the growth and prosperity of the businesses. On top of that, role of regulation and industry promotion is also important for sustainable growth.

§ Supporting and related industries: The Diamond model supports a value chain

perspective where the presence of supporting clusters facilitates the exchange of resources and knowledge. Certainly, cluster of firms would exhibit improved productivity levels than isolated firms. It offers better proximity to upstream as well as downstream industries, impacting the dynamism of business activities.

All the four pillars are not mutually exclusive instead they are closely knitted with one another, so there is a high level of dependency among all. For instance, literacy levels in a city (in factor conditions) and population (in demand conditions) influence the talent capacity of firms and its operation (in the context for firm strategy and rivalry) and the sophistication of demand and market potential. Each pillar is a weighted average of many different variables wherein each variable evaluates a different dimension of competitiveness. So, the Diamond model integrates all the determinants and brings a holistic approach to understand and measure the concept of competitiveness.

1.3 Some of the salient features

President and Distinguished Professor of the Santa Fe Institute, Geoffrey West with his team had founded that the all cities share common underlying dynamics. They can be believed as scaled versions of one another. In addition, according to his results a city starts doubling when there is an increase in the economic productivity of a person by nearly 15%. Clearly, indicating that cities are wealth creators, social

6

accelerators and innovation bedrock. Cities keep on competing and collaborating simultaneously to meet he future targets. Even the Indian cities are growing rapidly, and the aggregation of their impact is acting as a growth booster for the Indian economy. Some of the leading Indian cities such as Delhi, Mumbai, and Bengaluru etc. have changed the entire outlook of the country. It has helped India to emerge as the desirable destination on the parameters like, economical stability, human capital, cultural diversity and physical capital. Therefore, it is important to track them, understand them and measure their current performance levels. Now the work becomes easy with the competitiveness rankings of Institute for Competitiveness, India. The India City Competitiveness rankings are vital in nature because they highlight the strengths that should be build and the challenges that must be addressed.

The India City Competitiveness Report 2013 focuses on the concepts that is known to many but understood by few. They are Moving towards urbanization: Indeed, India is urbanizing fast. More than 30% of the Indian population is today residing in urban areas, and if estimates have to be believed then close to 600 million people will reside in the Indian urban areas by 2031. However, there lies a huge demand supply gap between expectations and

Would interest: § Government: It includes government officials in different ministries, policy makers,

municipal corporations etc. who would like to assess their current implemented strategies and make new plans with more feasible and sustainable solutions for their cities and adjacent regions.

§ Corporations: It includes business houses, foreign and local firms that are willing to capture the Indian cities markets but are not aware about their real scenario. It will act as a guidebook for their huge investments.

§ Indian Citizens: It will give a better understanding to the citizens of the respective

cities to make their personal choices w.r.t. their business and social life. It will also guide people who are planning to migrate to assess the regions across a variety of metrics.

§ Others: Comprises of researchers, NGO’s etc. working in the field of urbanization or

cities who are working or willing to work in this area. People who want to understand the nitigrities of the subject and come up with feasible solutions to help the city authorities across the country.

7

reality. Thus to move up the competitiveness levels, the potential of the urban areas should be harnessed resourcefully.

Reality of Indian cities: Indian cities are fascinating. They are the real game changer and the prospering ground for the country to boom further. Although, they seem to be well equipped from a distance, but they are scathing from inside. They lack certain important qualities such as inadequate infrastructure, dearth of basic amenities, poor governance etc. If we take care of these parameters then, undoubtedly they can emerge as one of the best cities of the world and compete with the international cities.

Role of Government: Government is the key authority that is responsible for the development of a region in all dimensions. It plays an inevitable role at all levels (central, state and district) so as to look after the prosperity levels of a region. Although due to complex hierarchy, physical implementation of rules and regulation takes time. Thus affecting the operations of a region and slowing down its progress.

Competitiveness leading to holistic growth: Competitiveness is a complex concept and is understood differently by different people. In simpler terms, it determines the efficiency between two entities by gauging their productivity levels through different parameters. Thus, it is a holistic approach to assess the growth of a region.

Mutual efforts needed: There is an urgent need for strong collaboration between government at all levels, institutions, corporate organizations and public. Active participation is required from all players that directly or indirectly influence the development of the region. Now, building competitiveness should be their primary concern, so as to, not only become competitive w.r.t. Indian cities but also have a footprint on a global platform.

1.4 India’s Competitiveness

India is losing its charm on the global front as every year it is scoring low on the Global Competitiveness Index (GCI). Clearly, demonstrating its low level of competitiveness w.r.t. other countries. From 2009 to 2012, the ranking of India has dropped by ten. This ranking transformation illustrates the poor performance of the country on several pillars. If the decline of the country is traced frontward on the Global Competitiveness Report 2012-‐13, then India stood on 49 rank in 2009-‐10, moved to 51 in 2010-‐11, 56 in 2011-‐12 and finally touched 59 in 2012-‐13. It is still stuck in its first stage of development and is tagged as one of the factor-‐driven economies.

8

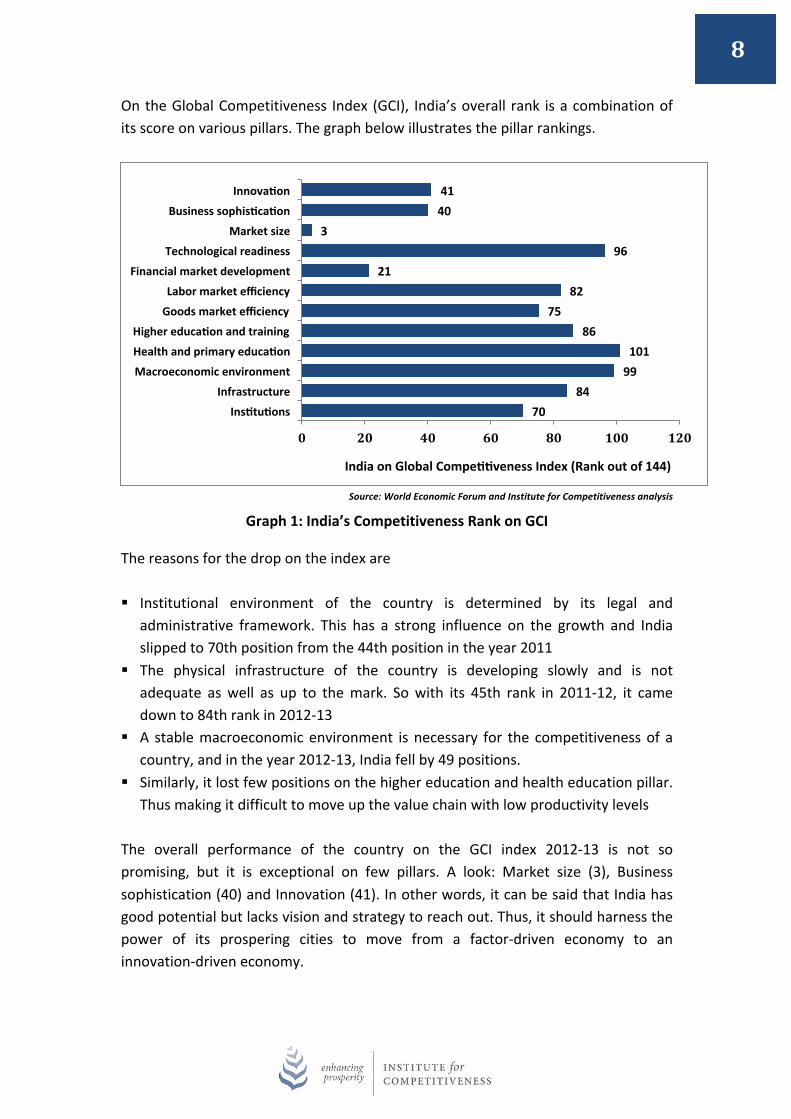

On the Global Competitiveness Index (GCI), India’s overall rank is a combination of its score on various pillars. The graph below illustrates the pillar rankings.

Source: World Economic Forum and Institute for Competitiveness analysis

Graph 1: India’s Competitiveness Rank on GCI

The reasons for the drop on the index are

§ Institutional environment of the country is determined by its legal and administrative framework. This has a strong influence on the growth and India slipped to 70th position from the 44th position in the year 2011

§ The physical infrastructure of the country is developing slowly and is not adequate as well as up to the mark. So with its 45th rank in 2011-‐12, it came down to 84th rank in 2012-‐13

§ A stable macroeconomic environment is necessary for the competitiveness of a country, and in the year 2012-‐13, India fell by 49 positions.

§ Similarly, it lost few positions on the higher education and health education pillar. Thus making it difficult to move up the value chain with low productivity levels

The overall performance of the country on the GCI index 2012-‐13 is not so promising, but it is exceptional on few pillars. A look: Market size (3), Business sophistication (40) and Innovation (41). In other words, it can be said that India has good potential but lacks vision and strategy to reach out. Thus, it should harness the power of its prospering cities to move from a factor-‐driven economy to an innovation-‐driven economy.

70 84

99 101

86 75

82 21

96 3

40 41

0 20 40 60 80 100 120

Insatuaons

Infrastructure

Macroeconomic environment

Health and primary educaaon

Higher educaaon and training

Goods market efficiency

Labor market efficiency

Financial market development

Technological readiness

Market size

Business sophisacaaon

Innovaaon

India on Global Compeaaveness Index (Rank out of 144)

9

1.5 A look at the competitiveness of regions & cities in India

The importance of the role played by regions and its associated factors in the development of the country has been documented long back. Urban regions and cities share a mutual relationship in influencing the prosperity of the national economy. The developmental pace of a country depends on the economy of its regions and cities as successful ‘regional drivers’ and not the other way round. Many indispensable levels of competitiveness exist at the regional level. They not only contribute economically but also provide better quality of life via product and service innovation and technology. To exemplify, the cities of Gujarat have attracted a large number of people because they are providing better residential space, more industrial opportunities and have good governance structure. Cities like Ahmedabad and Surat are acting as most desirable destinations for citizens and investors. They are also competing and collaborating consequently to become highly competitive which is evident by the growth of the State. It is thus necessary that regions and cities compete with each other to improve the overall competitiveness of the nation.

Building up competitiveness is a solution to the various challenges that are encountered by Indian cities. If worked upon vigilantly and prudently then these future cities might also become the best cities of the world.

There is no single policy or step to achieve competitiveness. It is a step-‐by-‐step process, which might take a number of years to build upon and improve.

BOX 2: Success Story of the Indian IT city Bengaluru Preeminent pace with which Bengaluru has risen aloft and emerged as one of the most vibrant, important and successful city is incredible. The Silicon Valley of India has come a long way from being just an education hub in South India to appear as the technology center of the country, centered with the best talent pool. Forbes magazine has titled the city as one of the “Next Decade’s Fastest-‐Growing Cities” because of its phenomenal economic growth of 10.3%, good infrastructure and for being the business center for various kinds of enterprise and trade purposes. It is a city which is packed with good economic growth, fitted with multicultural society, provide steady infrastructure facilities and a lot of opportunities to study and work further. It is also apt for business alliances and has a rich green environment. In the words of Harvard University’s Edward Glaeser – “Bangalore is a model of how an urban agglomeration can bring prosperity to a poor country.” In spite of facing the same set of problems like other cities, the city has projected itself as a successful city. The city is a true urban face of India which has and will constantly make the country proud in future.

10

Each parameter including, education, infrastructure, efficient capital markets, skilled workforce and favorable environment are crucial and required to improve the competitiveness of the region.

1.6 Urbanization: A Phenomenon in context to India Urbanization is a continuous and an inevitable part of the economic development and social change. In India, urbanization is taking place mainly because of the rapid increase in population and partially due to the increase in migration of people from rural to urban areas. These people are coming to cities in search of better opportunities, to have good living conditions and working environment. According to the urban growth statistics of India, the pace of urbanization has slowed during the past 20 years. The urban growth rate was 46% in between the period of 1971 and 1981, which fell to 36% from 1981 to 2001 and then moved to 31.8% from 2001 to 2011. It might look a bit confusing, but the average urban growth rate of the country has increased in comparison to its average growth rate of the rural population, which is a good sign. The urban-‐rural divide in India was 31.16% and 64.84% as measured by the Government of India in Census 2011.

The pace of urbanization in India has been relatively slow when compared to many other developing countries. Only 31.16% of India’s population can be classified as urban. Also, the populous country of the world, China has 45% of its population under the bracket of urbanization. Still, the country is clearly trying its limited

Definition: ‘Urban areas’ in India All the statutory places with a Municipal Corporation, Cantonment Board, or Notified town Area Committee, and all places satisfying the following three criteria simultaneously:

(i) A minimum population of 5000 (ii) At least 75% of male working population engaged in non-‐agricultural; pursuits (iii) A population density of at least 400 per sq. km (1000 per sq. mile)

In addition, some areas falling in the vicinity of city or town are also considered as urban areas if they are treated as the out growths (OGs) of the main urban unit. Such OGs are shown as urban agglomerations. As per the census definition, Urban Agglomeration is a continuous urban spread constituting a town and its adjoining urban outgrowths (OGs) or two or more physical contiguous town together and any adjoining urban out growths of such towns.

Source: Census of India 2011 Press Release: Rural – Urban distribution of Population

11

resource base and trying to fill the existent gap between the demand and supply of resources. It is a proven fact that cities are the drivers of urbanization, so they are affected with the positive as well as with the negative side of this phenomenon. Cities with their charismatic features such as accessibility of resources and easy availability of opportunities help them to accelerate their density levels and growth trajectory. In short, attracting a pool of people and further creating problems, especially in reference to India because in conjunction with people, comes pool of challenges. Even small problems like water supply, roads, transportation system, street lighting etc. create additional challenges for the citizens and the authority of the region.

BOX 3: Population density: Urban change turning into an urban challenge While India accounts for a meager 2.4% of the world surface area, it supports and sustains a whopping 17.5% of the world population. In other words, with a surface area of just 135.79 million square km it is a home for 1.241 billion which makes the population density (per sq. km) of the country to 382 per sq. km in 2011. Comparing with the figures of 2001, it was observed that there was an increase of 57 people on every square kilometer. As evident, India is reckoned as one of the most populous countries of the world. In terms of population density, it is only second to Bangladesh which is the country with the highest population density. In Bangladesh, nearly 964 people reside on every square kilometer as reported by Bangladesh Bureau of Statistics in 2011. The increasing population density of the country is certainly a matter of concern for many people. It adversely affects the entire country in terms of degrading the quality of life and by putting pressure on the natural resources and existing infrastructural services. It is especially problematic for the authorities in the urban areas where managing resources and people become a huge challenge. Densely populated cities are a common feature in India. The top five densely populated cities have a population of 10,000 and above. In the sequence they can be listed as Chennai, (26903), Kolkata (24252), Mumbai (20925), Hyderabad (18480) and Delhi (11297). These cities are bedrocks of prosperity that continuously attract people from rural areas and thus leading to rapid population boom. As a result, majority of the people living in these cities are born in their native places but brought up in these populated cities. Thus, cities with high densities can act as a blessing or a curse wherein the bad effects are known to all. If the resources are in abundance and policies are in place, then the planned structure of the city can lead to the growth of prosperous regions.

12

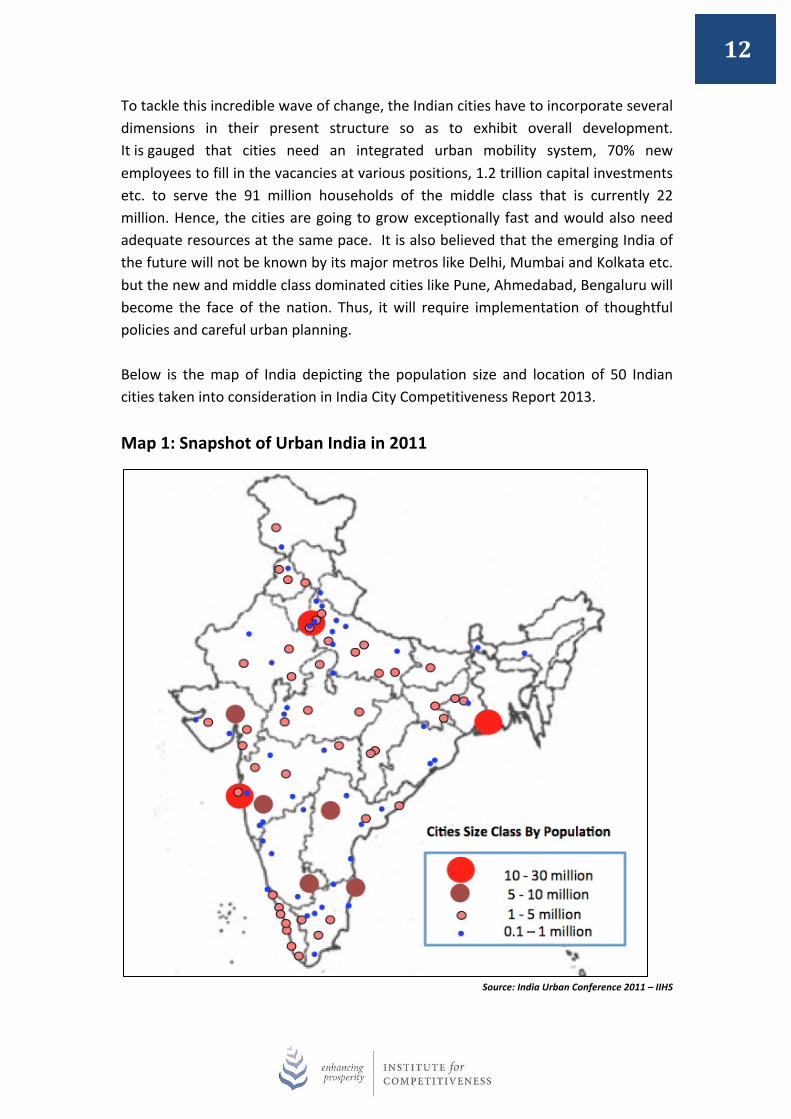

To tackle this incredible wave of change, the Indian cities have to incorporate several dimensions in their present structure so as to exhibit overall development. It is gauged that cities need an integrated urban mobility system, 70% new employees to fill in the vacancies at various positions, 1.2 trillion capital investments etc. to serve the 91 million households of the middle class that is currently 22 million. Hence, the cities are going to grow exceptionally fast and would also need adequate resources at the same pace. It is also believed that the emerging India of the future will not be known by its major metros like Delhi, Mumbai and Kolkata etc. but the new and middle class dominated cities like Pune, Ahmedabad, Bengaluru will become the face of the nation. Thus, it will require implementation of thoughtful policies and careful urban planning.

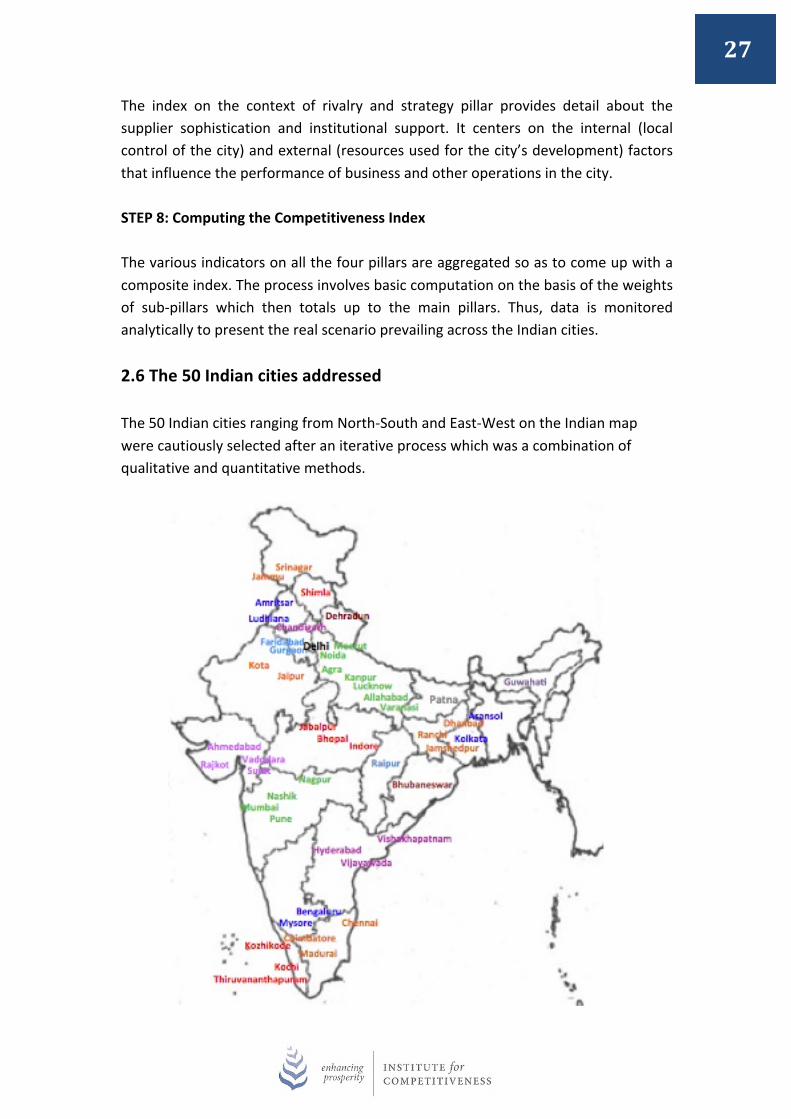

Below is the map of India depicting the population size and location of 50 Indian cities taken into consideration in India City Competitiveness Report 2013. Map 1: Snapshot of Urban India in 2011

Source: India Urban Conference 2011 – IIHS

13

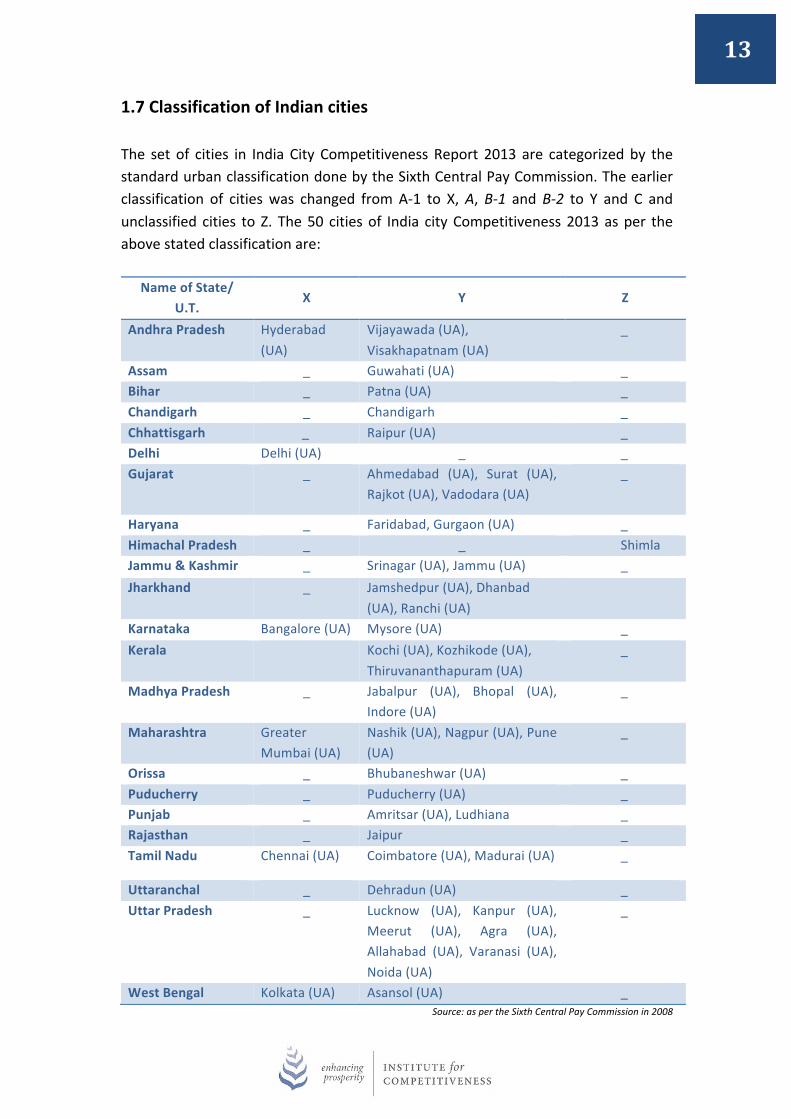

1.7 Classification of Indian cities

The set of cities in India City Competitiveness Report 2013 are categorized by the standard urban classification done by the Sixth Central Pay Commission. The earlier classification of cities was changed from A-‐1 to X, A, B-‐1 and B-‐2 to Y and C and unclassified cities to Z. The 50 cities of India city Competitiveness 2013 as per the above stated classification are:

Name of State/ U.T.

X Y Z

Andhra Pradesh Hyderabad (UA)

Vijayawada (UA), Visakhapatnam (UA)

_

Assam _ Guwahati (UA) _ Bihar _ Patna (UA) _ Chandigarh _ Chandigarh _ Chhattisgarh _ Raipur (UA) _ Delhi Delhi (UA) _ _ Gujarat _ Ahmedabad (UA), Surat (UA),

Rajkot (UA), Vadodara (UA) _

Haryana _ Faridabad, Gurgaon (UA) _ Himachal Pradesh _ _ Shimla Jammu & Kashmir _ Srinagar (UA), Jammu (UA) _ Jharkhand _ Jamshedpur (UA), Dhanbad

(UA), Ranchi (UA)

Karnataka Bangalore (UA) Mysore (UA) _ Kerala Kochi (UA), Kozhikode (UA),

Thiruvananthapuram (UA) _

Madhya Pradesh _ Jabalpur (UA), Bhopal (UA), Indore (UA)

_

Maharashtra Greater Mumbai (UA)

Nashik (UA), Nagpur (UA), Pune (UA)

_

Orissa _ Bhubaneshwar (UA) _ Puducherry _ Puducherry (UA) _ Punjab _ Amritsar (UA), Ludhiana _ Rajasthan _ Jaipur _ Tamil Nadu Chennai (UA) Coimbatore (UA), Madurai (UA) _

Uttaranchal _ Dehradun (UA) _ Uttar Pradesh _ Lucknow (UA), Kanpur (UA),

Meerut (UA), Agra (UA), Allahabad (UA), Varanasi (UA), Noida (UA)

_

West Bengal Kolkata (UA) Asansol (UA) _ Source: as per the Sixth Central Pay Commission in 2008

14

X, Y and Z are more commonly known as Tier-‐I, Tier-‐II and Tier-‐III cities respectively. Please note that the basis of classification of cities/towns into the above stated three categories, as suggested by the Sixth Central Pay Commission is as follows:

Classification of Cities/Towns

Rate of House Rent Allowance as a percentage of (Basic pay + NPA where applicable)

X 30% Y 20% Z 10%

1.8 Increase in the number of Metropolitan Areas According to the official definition, an area having a population of ten lakh or more, comprised in one or more districts and consisting of two or more Municipalities or Panchayats or other contiguous area, specified by the Governor by public notification is said to be a Metropolitan area.

A metropolitan is a combination of densely populated core city and its adjoining territories, which share industry, infrastructure, employment opportunities etc. Metropolitan areas are a result of the migration of people to the peripheral areas or outskirts of the city/mega city because people find it difficult to afford the basic facilities of the core city. However, people living in these peripheral areas do avail and enjoy almost all the facilities of the central city.

It is being anticipated that in the coming years, the number of metropolitan cities will increase progressively. It is necessary that they function efficiently so, a well-‐staffed municipal corporation should be in place so as to take care of the expansion of business and infrastructure in the region. The major metropolitan areas of India are National Capital Region (NCR) Central city: Delhi City Population: 1,10,07,835 Urban Metropolitan Population: 4,60,50,000 Comprises of NCT-‐Delhi (National Capital Territory of Delhi), Districts of Haryana -‐ Gurgaon, Sonipat, Panipat, Faridabad, Rohtak, Bhiwadi and Mahendragarh, Districts of Uttar Pradesh – Meerut, Baghpat, Bulandshahr, Ghaziabad, Gautam Buddha Nagar District (Noida and Greater Noida) and Districts of Rajasthan – Alwar and Bharatpur.

15

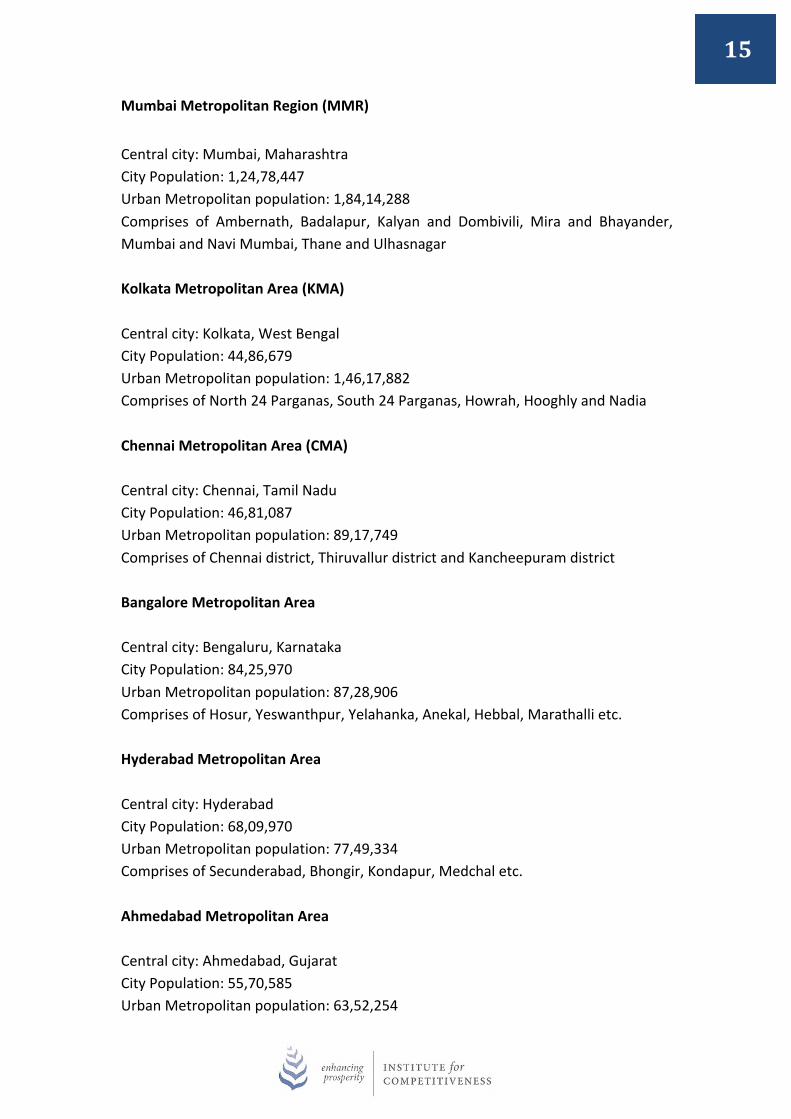

Mumbai Metropolitan Region (MMR) Central city: Mumbai, Maharashtra City Population: 1,24,78,447 Urban Metropolitan population: 1,84,14,288 Comprises of Ambernath, Badalapur, Kalyan and Dombivili, Mira and Bhayander, Mumbai and Navi Mumbai, Thane and Ulhasnagar Kolkata Metropolitan Area (KMA) Central city: Kolkata, West Bengal City Population: 44,86,679 Urban Metropolitan population: 1,46,17,882 Comprises of North 24 Parganas, South 24 Parganas, Howrah, Hooghly and Nadia Chennai Metropolitan Area (CMA) Central city: Chennai, Tamil Nadu City Population: 46,81,087 Urban Metropolitan population: 89,17,749 Comprises of Chennai district, Thiruvallur district and Kancheepuram district Bangalore Metropolitan Area Central city: Bengaluru, Karnataka City Population: 84,25,970 Urban Metropolitan population: 87,28,906 Comprises of Hosur, Yeswanthpur, Yelahanka, Anekal, Hebbal, Marathalli etc. Hyderabad Metropolitan Area Central city: Hyderabad City Population: 68,09,970 Urban Metropolitan population: 77,49,334 Comprises of Secunderabad, Bhongir, Kondapur, Medchal etc. Ahmedabad Metropolitan Area Central city: Ahmedabad, Gujarat City Population: 55,70,585 Urban Metropolitan population: 63,52,254

16

Comprises of Gandhinagar, Anand, Kheda, Kadi, Jambusar, Viramgam with other towns and villages Pune Metropolitan Area Central city: Pune, Maharashtra City Population: 31,15,431 Urban Metropolitan population: 50,49,968 Comprises of Pune city and Pimpri-‐Chinchwad town Surat Metropolitan Area Central city: Surat, Gujarat City Population: 44,62,002 Urban Metropolitan population: 45,85,367 Comprises of Surat and its satellite towns

BOX 4: Boundless NCR

National Capital Region (NCR) was constituted under the National Capital Region Planning Board (NCRPB) Act 1985 to promote balanced and harmonized development of the region. The idea was to control the haphazard growth of the region by routing the flow and direction of economic growth and other crucial elements along nearer, prosperous and potential paths. Delhi, which constitutes 16.75 million people in the area of 1,483 sq. km, with the effect of NCR has transformed into a region spread over nearly 33,578 sq. km with 23 million population. The National Capital Region as notified covers Delhi, Haryana, UP and Rajasthan in its territory.

S. No. Constituent Sub-‐regions/Districts of the State Area (in sq Kms)

% of the region

1 Haryana Faridabad, Gurgaon, Mewat, Rohtak, Sonepart, Rewari, Jhajjhar, Panipat,

Palwal 13413 40

2 Uttar Pradesh Meerut, Ghaziabad, Gautam Budha Nagar, Bulandshahr, Baghpat 10853 32

3 Rajasthan Alwar 7829 23

4 NCT of Delhi -‐ 1483 5

Source: National Capital Region Planning Board

17

This central part of the country is the home to more than 4 crore people living in 108 towns of which 17 are class I cities and more than 7500 rural settlements. The obvious reason is the plethora of opportunities available in and around the area in terms of employment, business, education etc. The area attracts a large number of migrants from other states. As per official figures, Delhi alone witnessed nearly 20 lakh in-‐migrants in the last decade.

Today National Capital Region is one of the largest urban agglomerations in the world made up of 1.06% of India’s total size that is equivalent to the combined area of three States of India that is, Tripura, Nagaland and Sikkim. In 2012, it became the largest residential market in the country, and the area to create more than a fifth of jobs of the country. It is also the first choice of retail companies entering the Indian domain due to the strong and large scale of shopping mall development culture in the area. It also comprises of 54 Special Economic Zones (SEZs).

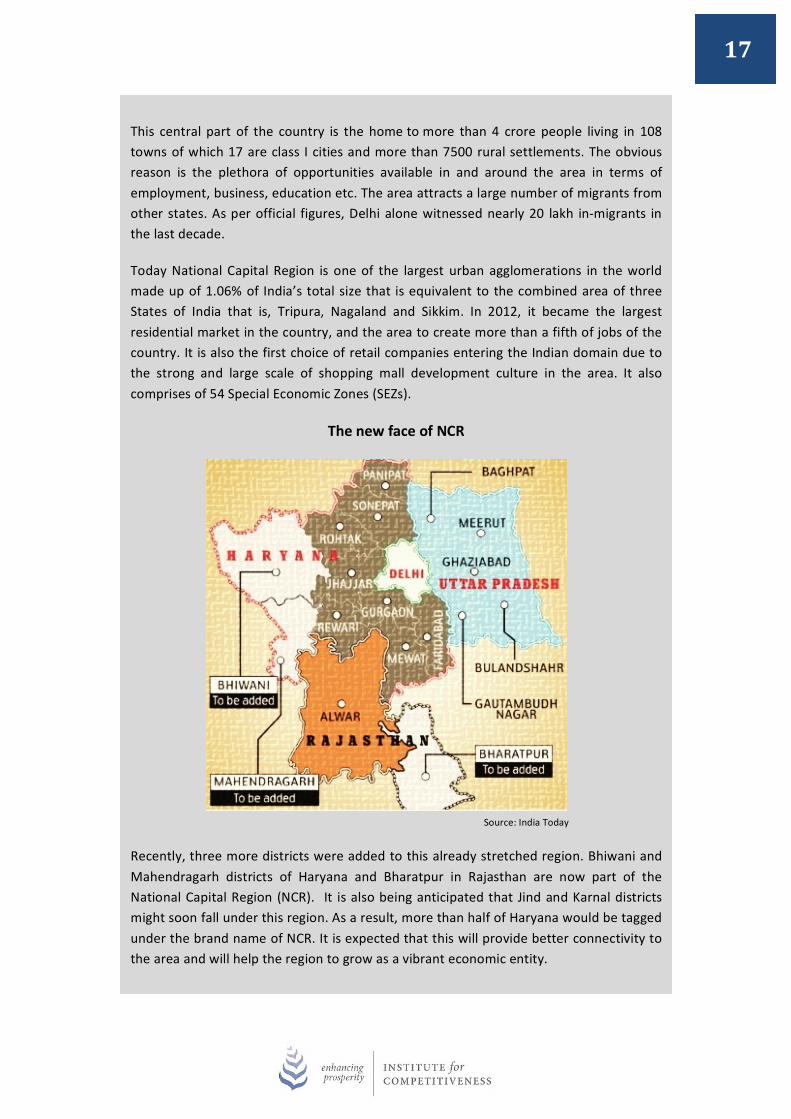

The new face of NCR

Source: India Today

Recently, three more districts were added to this already stretched region. Bhiwani and Mahendragarh districts of Haryana and Bharatpur in Rajasthan are now part of the National Capital Region (NCR). It is also being anticipated that Jind and Karnal districts might soon fall under this region. As a result, more than half of Haryana would be tagged under the brand name of NCR. It is expected that this will provide better connectivity to the area and will help the region to grow as a vibrant economic entity.

18

It is noted that the NCR region is doing fairly well on many economical parameters. The per capita income, rate of growth of both GDP and per capita income have consistently been higher in comparison to the rest of the country. In other words, NCR can be labeled as a crucial hub of economic activity in the country.

Although the capital of the country, Delhi, which is the locus of the entire region, is said to be bearing all the load. People in NCR rely more on the facilities of the capital because their cities/regions are not yet well versed and are in a developing stage. Delhi is always under pressure for better health, education and economic infrastructure even though when it is getting better with every passing year. The dependency of the nearby regions on the capital city is unknowingly affecting the prosperity levels of the city. It is being said that NCR is getting bigger so that the infrastructure pressure on Delhi can be reduced. However, it is an indirect invitation to people living in adjoining districts of NCR to come and settle in this boundless region.

Population acceleration of the region

Region Population (in 2011) Projected Population (in 2021)

Delhi 1,10,07,835 2,02,60,000

NCR 4,60,50,000 6,17,30,000

Source: India Today

It is being projected in the Regional Plan 2021, prepared by the NCRPB, would help the region to grow fairly better such that regions would be developed equitably. This will make the region as the highest urbanized area of the country by 2021 with 73% urbanization rate which is 62% in 2011. Specific attention would be paid to address the infrastructural and environmental challenges. Thus making it as one of the best region to live in the country by developing NCR in a more equitable, efficient and sustainable manner.

19

2.0 METHODOLOGICAL FRAMEWORK

20

Edward Glaeser, an urban economist at Harvard in his book “The triumph of the cities” has stated “Urban density offers the shortest route from misery to prosperity as a result, cities are growing at a high rate in developing countries. Indeed, cities today play a vital role for humans. They have always been an epicenter for economic growth and for technological innovations. They are a reason behind the prosperity of a region as they offer all essential commodities for survival, though with certain constraints. In addition, they are productive, fitted with better opportunities, have higher GDP and are happier than corresponding less urban regions”. Similar is the scenario in India. Indian cities such as Delhi, Mumbai etc. have turned out to be advanced cities that are also the major contributors in the Indian economic growth. Following their footsteps, every decade new set of cities are emerging in the country which might be unnoticed right now but are all packed to create their identity in the Indian arena. Every year, the India City Competitiveness Report, takes into consideration 50 prosperous Indian cities to gauge their competitiveness levels with respect to one another. The rankings on the competitiveness index provide a snapshot of their overall performance and information w.r.t. their financial, social, business performance. 2.1 Unit of Analysis It is frequently observed that there exists a lack of clarification in between the terms such as city, urban agglomeration etc. A common man is not well versed with the difference between these terms. Thus, it is crucial to understand the terms and their definitions firstly in order to get a clear picture of India City Competitiveness 2013. The explanation of the terms as per the Government of India, Census 2011: Towns According to the Government of India, Census 2011, it is:

1. All places with a municipality, corporation, cantonment board or notified town area committee, etc.

2. All other places which satisfied the following criteria: a) A minimum population of 5,000 b) At least 75 per cent of the male main working population engaged in non-‐agricultural pursuits c) A density of the population of at least 400 persons per sq. km. etc.

21

The first category of urban units is known as Statutory Towns. These towns are notified under the law by the concerned State/UT Government and have local bodies like municipal corporations, municipalities, municipal committees, etc., irrespective of their demographic characteristics as reckoned on 31st December 2009. Examples: Vadodara (Municipal Corporation), Shimla (Municipal Corporation) etc. The second category of Towns (as in item 2 above) is known as Census Town. These were identified on the basis of Census 2001 data. City According to the Census of India, a city is essentially a town that constitutes a population of nearly 1,00,000 or above. So, essentially city can be defined in terms of town as well. Urban Local Body The city body appointed by the government and responsible for maintaining and resolving the governance issues in the city is termed as Urban Local Body (ULB). It is also known as Municipal Corporation (MC). ULBs are appointed for those cities that are huge in size and are constantly growing such that, the nearby areas are also flourishing and mistaken as a part of the region. MC is only responsible to take care of the planned area of the city. It also varies from one city to another. To exemplify, Mumbai and Suburban Mumbai are two separate areas adjacent to one another but are taken care by the same governance body. Urban Agglomeration (UA) An urban agglomeration is a continuous urban spread constituting a town and its adjoining outgrowths (OGs), or two or more physically contiguous towns together with or without outgrowths of such towns. An Urban Agglomeration must consist of at least a statutory town and its total population (i.e. all the constituents put together) should not be less than 20,000 as per the 2001 Census. In varying local conditions, there were similar other combinations which have been treated as urban agglomerations satisfying the basic condition of contiguity. Examples: Greater Mumbai UA, Delhi UA, etc.

22

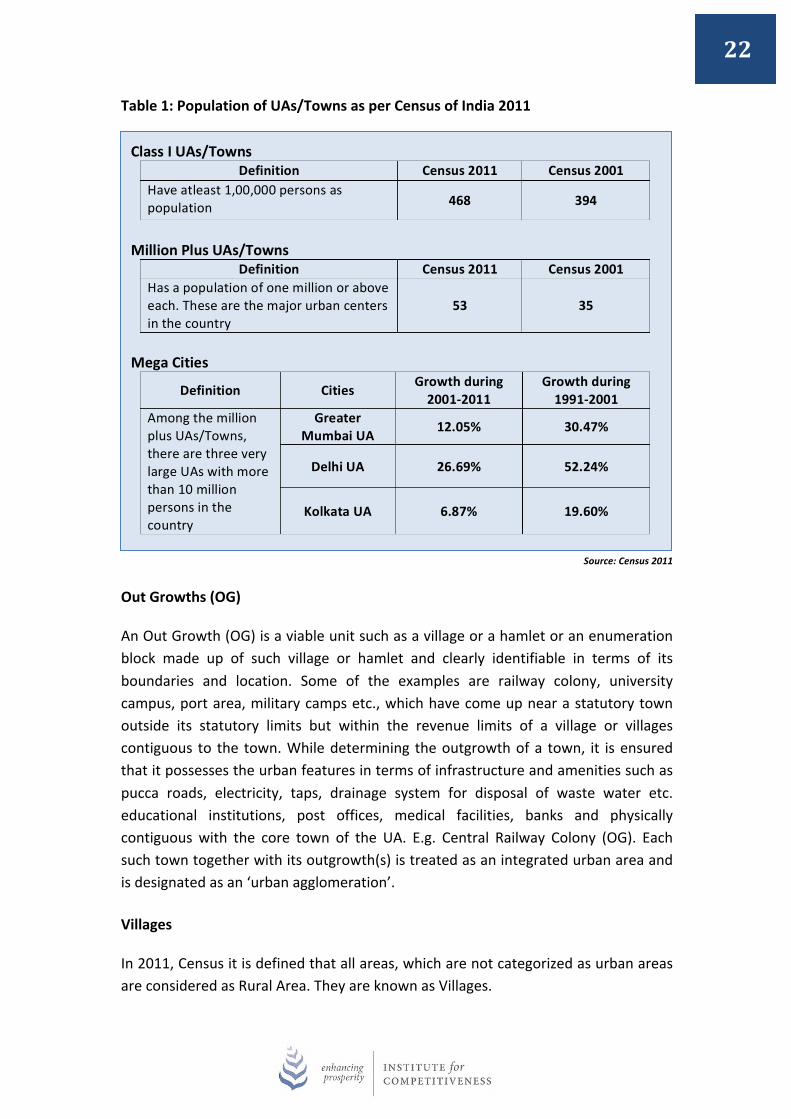

Table 1: Population of UAs/Towns as per Census of India 2011

Source: Census 2011

Out Growths (OG)

An Out Growth (OG) is a viable unit such as a village or a hamlet or an enumeration block made up of such village or hamlet and clearly identifiable in terms of its boundaries and location. Some of the examples are railway colony, university campus, port area, military camps etc., which have come up near a statutory town outside its statutory limits but within the revenue limits of a village or villages contiguous to the town. While determining the outgrowth of a town, it is ensured that it possesses the urban features in terms of infrastructure and amenities such as pucca roads, electricity, taps, drainage system for disposal of waste water etc. educational institutions, post offices, medical facilities, banks and physically contiguous with the core town of the UA. E.g. Central Railway Colony (OG). Each such town together with its outgrowth(s) is treated as an integrated urban area and is designated as an ‘urban agglomeration’. Villages In 2011, Census it is defined that all areas, which are not categorized as urban areas are considered as Rural Area. They are known as Villages.

Class I UAs/Towns Definition Census 2011 Census 2001

Have atleast 1,00,000 persons as population 468 394

Million Plus UAs/Towns

Definition Census 2011 Census 2001 Has a population of one million or above each. These are the major urban centers in the country

53 35

Mega Cities

Definition Cities Growth during 2001-‐2011

Growth during 1991-‐2001

Among the million plus UAs/Towns, there are three very large UAs with more than 10 million persons in the country

Greater Mumbai UA 12.05% 30.47%

Delhi UA 26.69% 52.24%

Kolkata UA 6.87% 19.60%

23

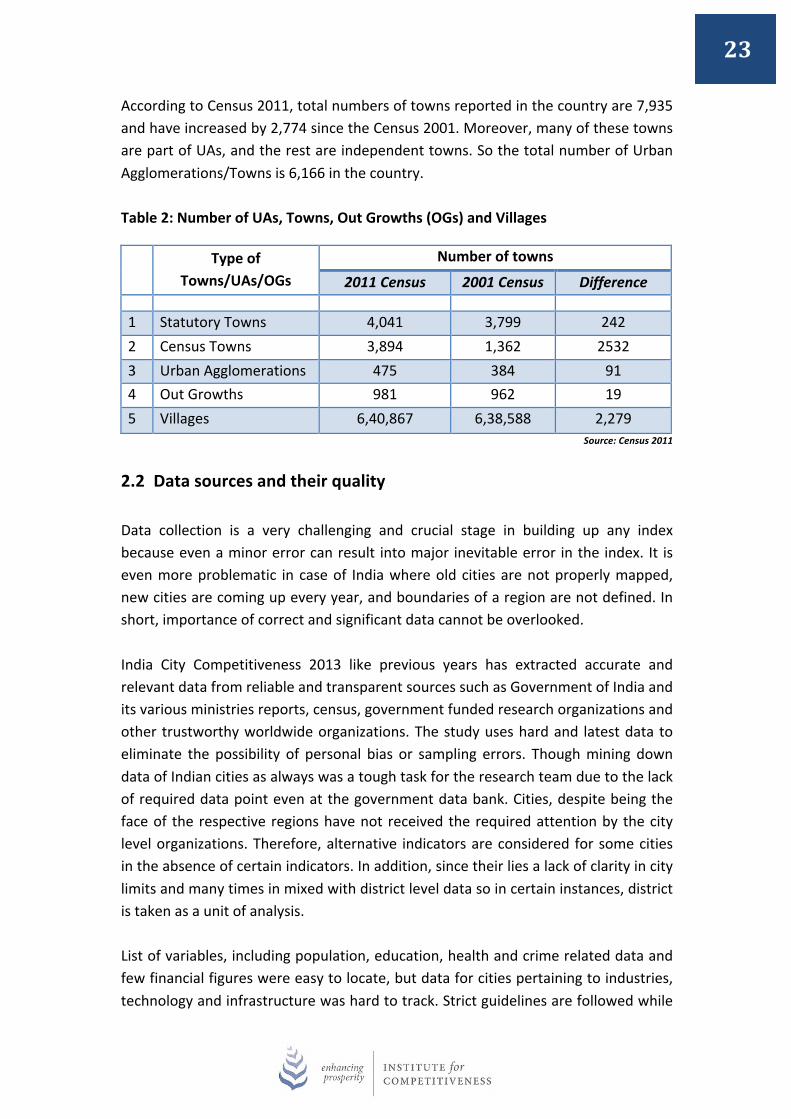

According to Census 2011, total numbers of towns reported in the country are 7,935 and have increased by 2,774 since the Census 2001. Moreover, many of these towns are part of UAs, and the rest are independent towns. So the total number of Urban Agglomerations/Towns is 6,166 in the country. Table 2: Number of UAs, Towns, Out Growths (OGs) and Villages

Type of Towns/UAs/OGs

Number of towns

2011 Census 2001 Census Difference

1 Statutory Towns 4,041 3,799 242 2 Census Towns 3,894 1,362 2532 3 Urban Agglomerations 475 384 91 4 Out Growths 981 962 19 5 Villages 6,40,867 6,38,588 2,279

Source: Census 2011

2.2 Data sources and their quality Data collection is a very challenging and crucial stage in building up any index because even a minor error can result into major inevitable error in the index. It is even more problematic in case of India where old cities are not properly mapped, new cities are coming up every year, and boundaries of a region are not defined. In short, importance of correct and significant data cannot be overlooked. India City Competitiveness 2013 like previous years has extracted accurate and relevant data from reliable and transparent sources such as Government of India and its various ministries reports, census, government funded research organizations and other trustworthy worldwide organizations. The study uses hard and latest data to eliminate the possibility of personal bias or sampling errors. Though mining down data of Indian cities as always was a tough task for the research team due to the lack of required data point even at the government data bank. Cities, despite being the face of the respective regions have not received the required attention by the city level organizations. Therefore, alternative indicators are considered for some cities in the absence of certain indicators. In addition, since their lies a lack of clarity in city limits and many times in mixed with district level data so in certain instances, district is taken as a unit of analysis. List of variables, including population, education, health and crime related data and few financial figures were easy to locate, but data for cities pertaining to industries, technology and infrastructure was hard to track. Strict guidelines are followed while

24

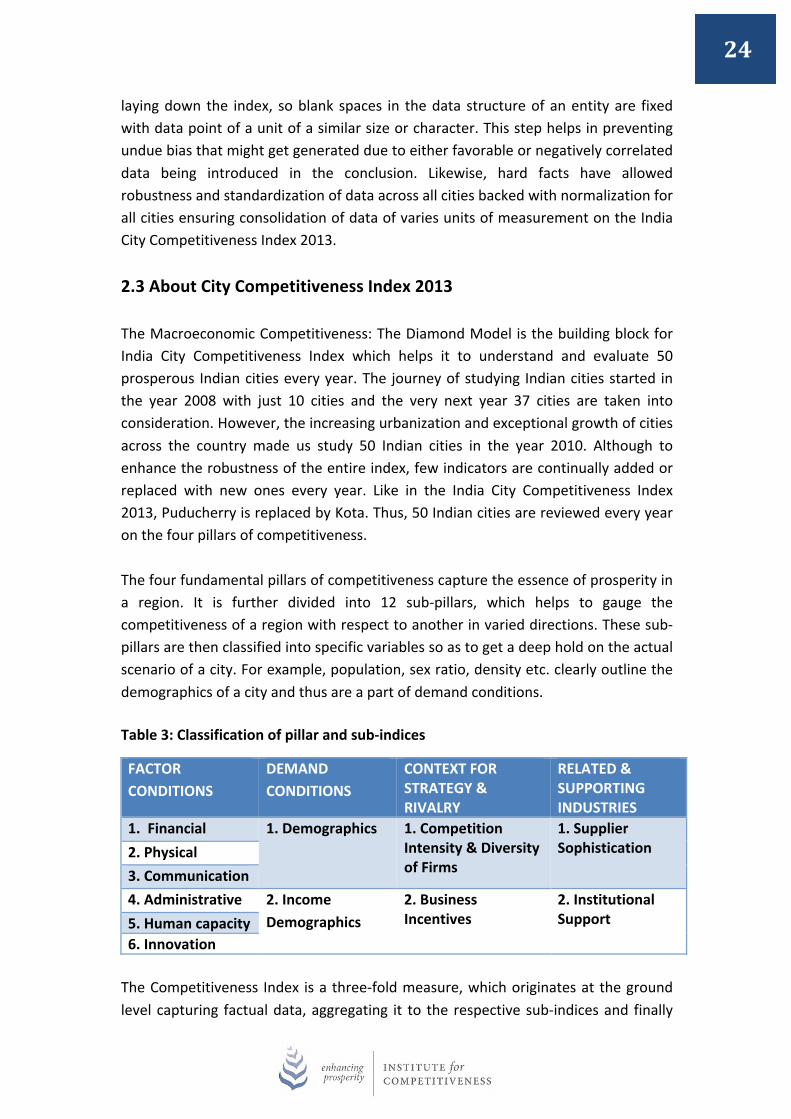

laying down the index, so blank spaces in the data structure of an entity are fixed with data point of a unit of a similar size or character. This step helps in preventing undue bias that might get generated due to either favorable or negatively correlated data being introduced in the conclusion. Likewise, hard facts have allowed robustness and standardization of data across all cities backed with normalization for all cities ensuring consolidation of data of varies units of measurement on the India City Competitiveness Index 2013. 2.3 About City Competitiveness Index 2013 The Macroeconomic Competitiveness: The Diamond Model is the building block for India City Competitiveness Index which helps it to understand and evaluate 50 prosperous Indian cities every year. The journey of studying Indian cities started in the year 2008 with just 10 cities and the very next year 37 cities are taken into consideration. However, the increasing urbanization and exceptional growth of cities across the country made us study 50 Indian cities in the year 2010. Although to enhance the robustness of the entire index, few indicators are continually added or replaced with new ones every year. Like in the India City Competitiveness Index 2013, Puducherry is replaced by Kota. Thus, 50 Indian cities are reviewed every year on the four pillars of competitiveness. The four fundamental pillars of competitiveness capture the essence of prosperity in a region. It is further divided into 12 sub-‐pillars, which helps to gauge the competitiveness of a region with respect to another in varied directions. These sub-‐pillars are then classified into specific variables so as to get a deep hold on the actual scenario of a city. For example, population, sex ratio, density etc. clearly outline the demographics of a city and thus are a part of demand conditions. Table 3: Classification of pillar and sub-‐indices

FACTOR CONDITIONS

DEMAND CONDITIONS

CONTEXT FOR STRATEGY & RIVALRY

RELATED & SUPPORTING INDUSTRIES

1. Financial 1. Demographics 1. Competition Intensity & Diversity of Firms

1. Supplier Sophistication 2. Physical

3. Communication 4. Administrative 2. Income

Demographics 2. Business Incentives

2. Institutional Support 5. Human capacity

6. Innovation The Competitiveness Index is a three-‐fold measure, which originates at the ground level capturing factual data, aggregating it to the respective sub-‐indices and finally

25

shaping the data structure in the form of a composite index at the city level. So, the step-‐by-‐step integration of data points provides a holistic picture of Indian cities.

2.4 Analysis of data indicators Similar to the data collection, data analysis, which is apparently the last stage of indexing, is crucial because it can distort the composite index and produce meaningless results with false numbers. The database consists of variables from varied socioeconomic dimensions so a good understanding of analysis, and a methodical approach has to be followed to run the analysis. It then gets possible to gain a better realization about the Indian cities and their competitiveness level.

The variables are synchronized and validated with the Microeconomic Competitiveness – The Diamond Model pillar and sub-‐pillars to arrive at the final index for competitiveness. Weights are assigned to each indicator (variable) after a comprehensive and meticulous research. To prevent multicollinearity among different indicators in the index, the concept of Principal Component Analysis is applied. The modified analysis clearly explains the relationship of one indicator with another and also its overall impact on the competitiveness index. The measure also determines the reliability and transparency enabling and aiding strategy formulation and policy execution.

India City Competitiveness Report 2013 thus combines all the significant information about the selected 50 Indian cities and brings the competitiveness ranking. It presents the actual situation of Indian cities; identifies individual city’s strong and weak areas and their respective level of supremacy on different dimensions of competitiveness. It is not merely a report; instead it is a guide which can allow its readers to curate new scenarios, identify and modify settings for each city for further discovery.

2.5 Steps Undertaken

While preparing India City Competitiveness Report, we at the Institute for Competitiveness, India follows a very methodological and standardized process. It is described as follows:

STEP 1: Developing a framework

Following the systematic guidelines, the first step is to understand and use the Microeconomic Competitiveness: The Diamond Model to measure the

26

competitiveness of different regions. It is a well-‐known and accepted model to measure the regional competitiveness.

STEP 2: Identifying the relevant variables

Competitiveness is a broad term, comprising of several factors that in a particular way impact the state of an entity. Therefore, depending on the respective sub-‐pillar, the indicators are chosen so as to come up with feasible result. In the index, the central variables are interpreted with quantitative data so that the city can be accurately portrayed and assessed reasonably.

STEP 3: Collection of data points

Building the data bank for the index is a difficult but critical task, especially in the case of Indian cities. So, data is collected cautiously from reliable sources such as government sources. Special attention is paid on making the data set more robust by incorporating recent updates so as to build an authentic index that represents the true nature of a city.

STEP 4: Analyzing Factor Conditions

The factor conditions are mainly defined by sub-‐indices such as financial market, physical conditions, communication modes, administration process, human capacity of the region and degree of innovation. These should be carefully reviewed to understand the cross-‐linkages between them and to measure the level of influence.

STEP 5: Exploring Demand Conditions

The sub-‐pillars of demand conditions are demographics and the distribution of income within the region. It is useful for many investors seeking to understand the patterns of changes in a set time frame.

STEP 6: Examining Business Opportunities

Business opportunities are mainly defined by the context for rivalry and firm level strategy. This information is of vital use for the business houses to identify competition intensity and business incentives of a region, which would eventually benefit the residents of the city directly or indirectly in the long run.

STEP 7: Investigating the scope of Threat and Opportunities

27

The index on the context of rivalry and strategy pillar provides detail about the supplier sophistication and institutional support. It centers on the internal (local control of the city) and external (resources used for the city’s development) factors that influence the performance of business and other operations in the city.

STEP 8: Computing the Competitiveness Index The various indicators on all the four pillars are aggregated so as to come up with a composite index. The process involves basic computation on the basis of the weights of sub-‐pillars which then totals up to the main pillars. Thus, data is monitored analytically to present the real scenario prevailing across the Indian cities. 2.6 The 50 Indian cities addressed

The 50 Indian cities ranging from North-‐South and East-‐West on the Indian map were cautiously selected after an iterative process which was a combination of qualitative and quantitative methods.

28

3.0 RANKINGS

29

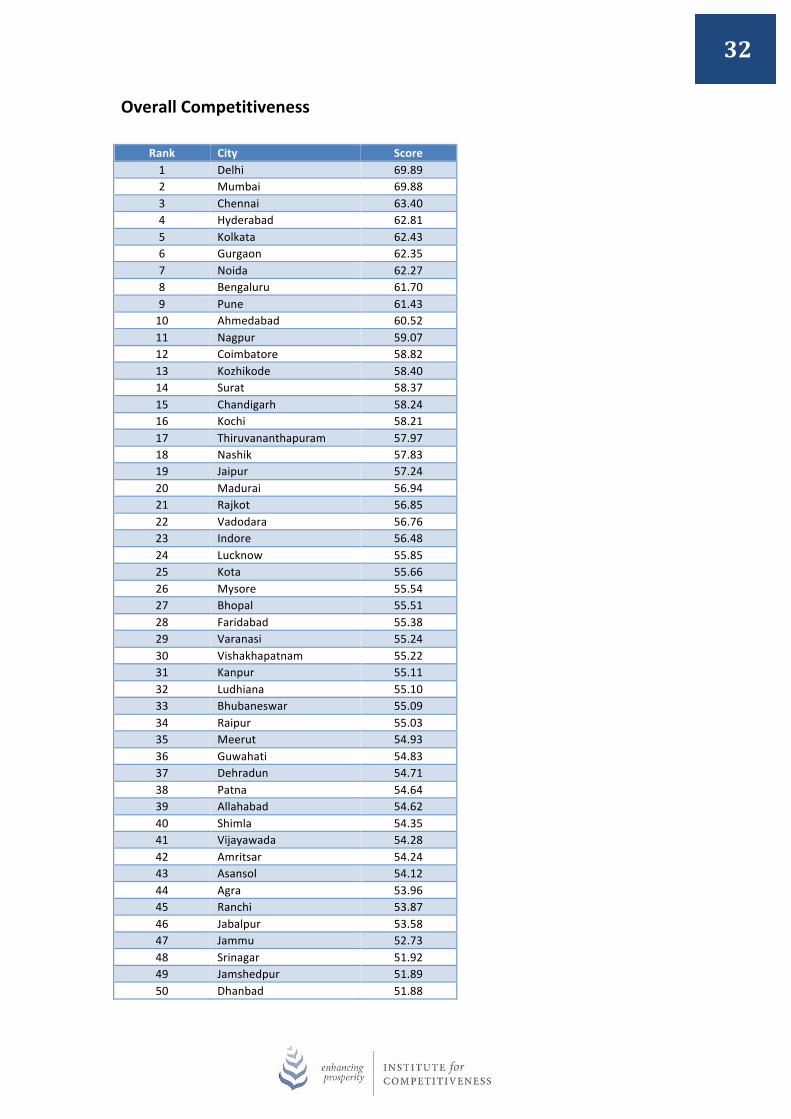

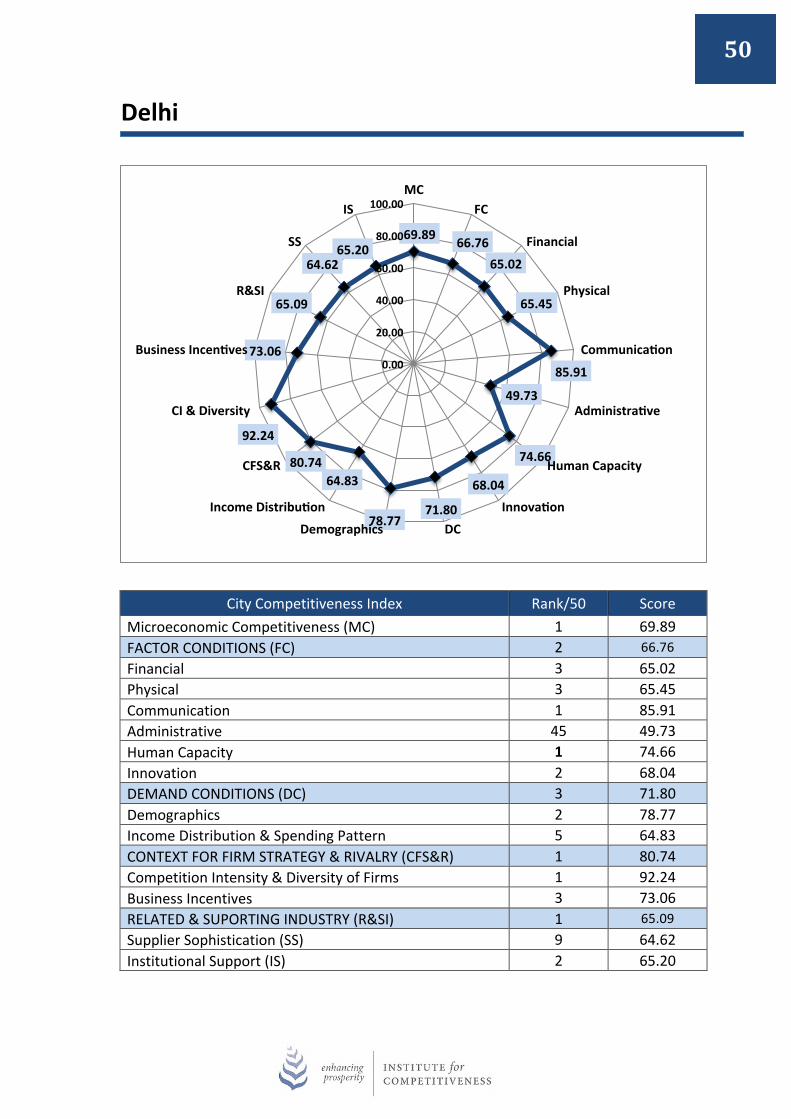

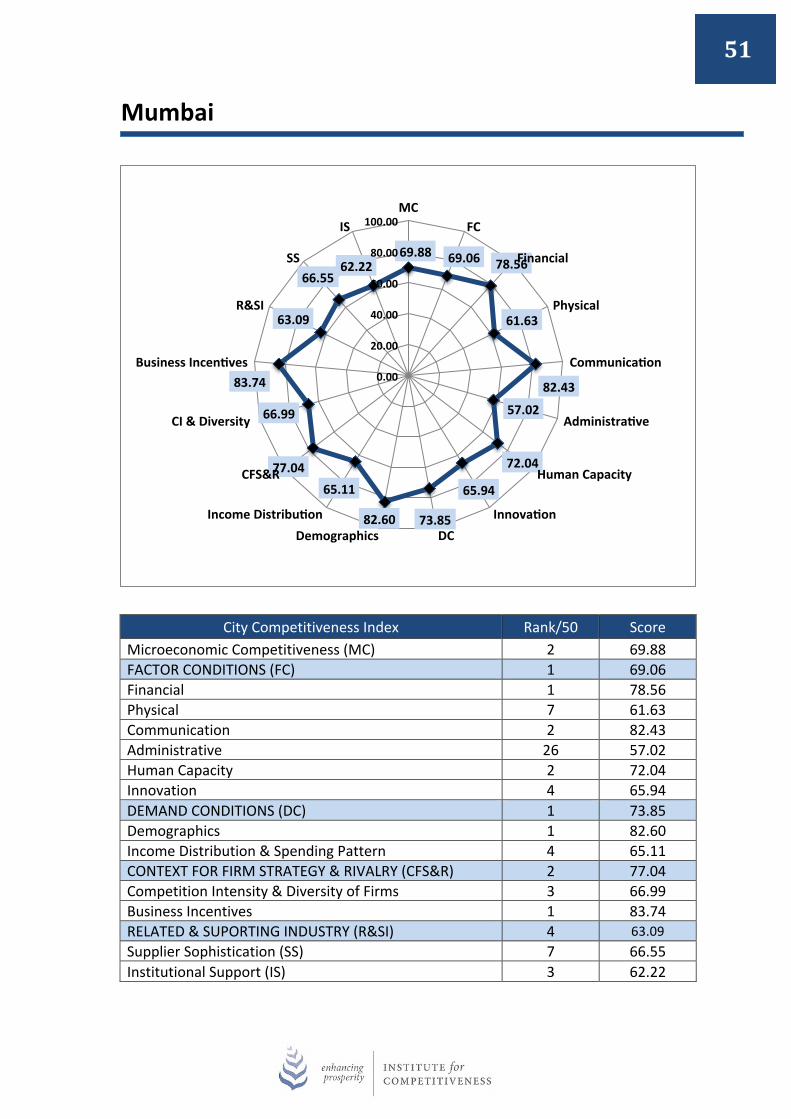

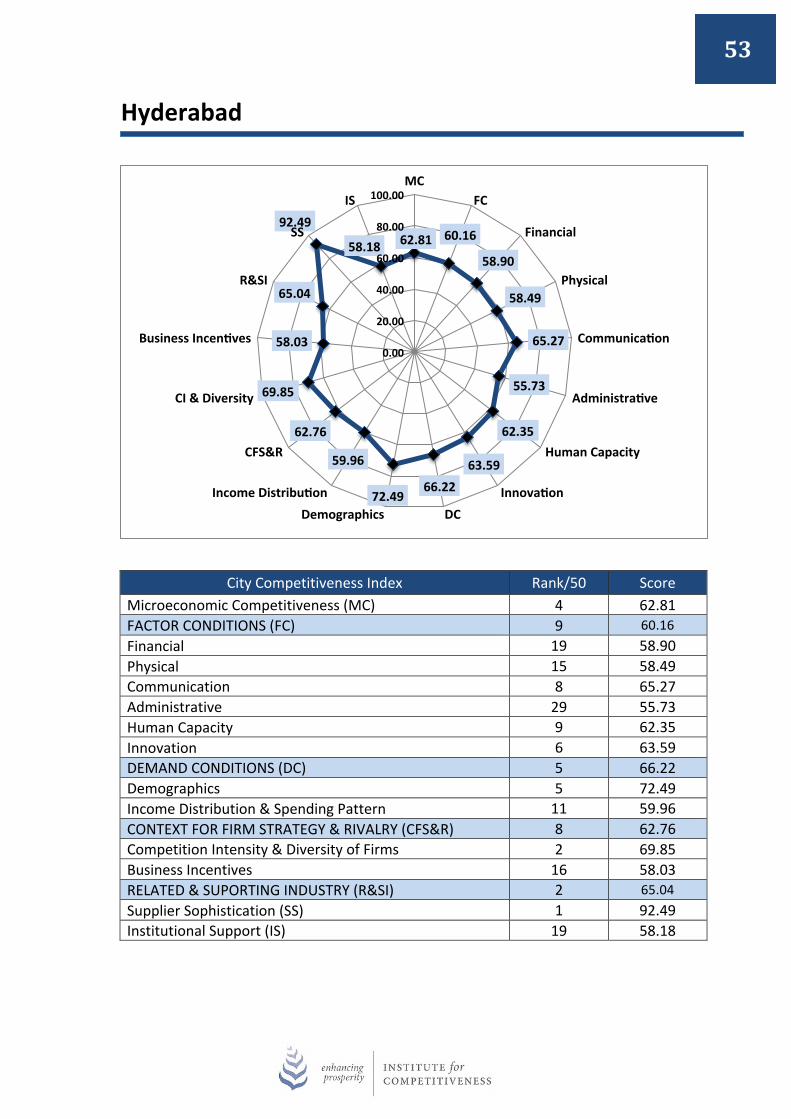

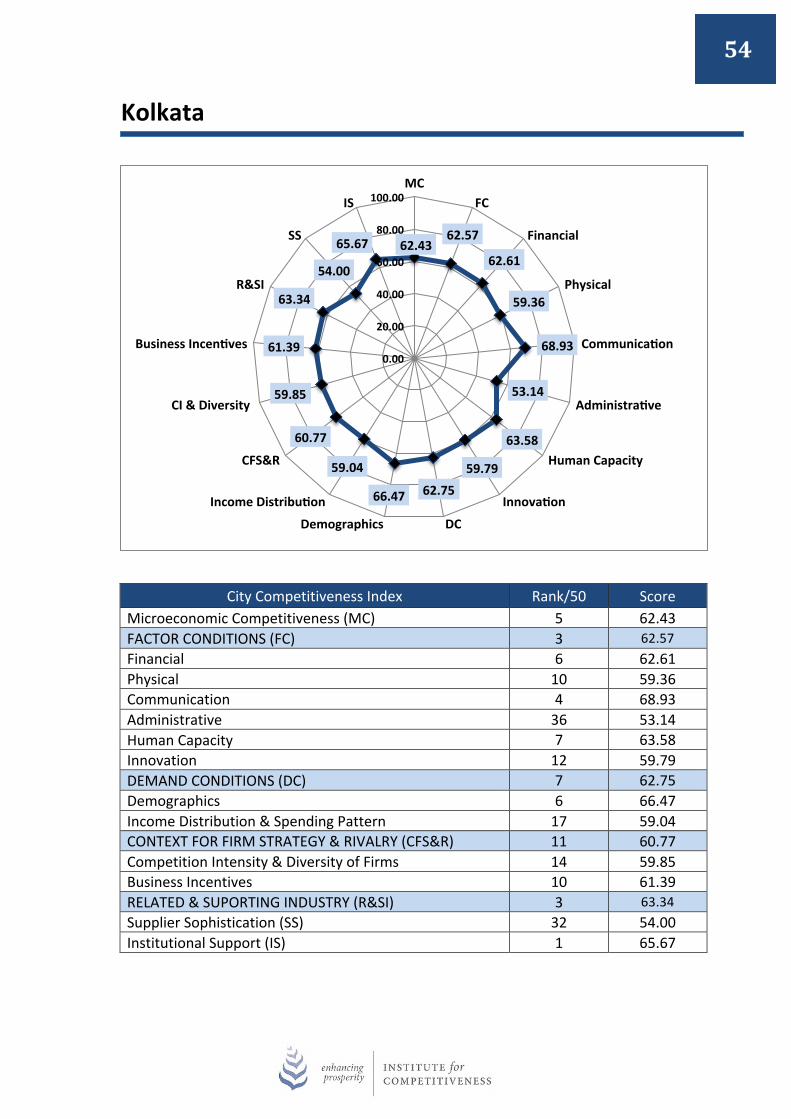

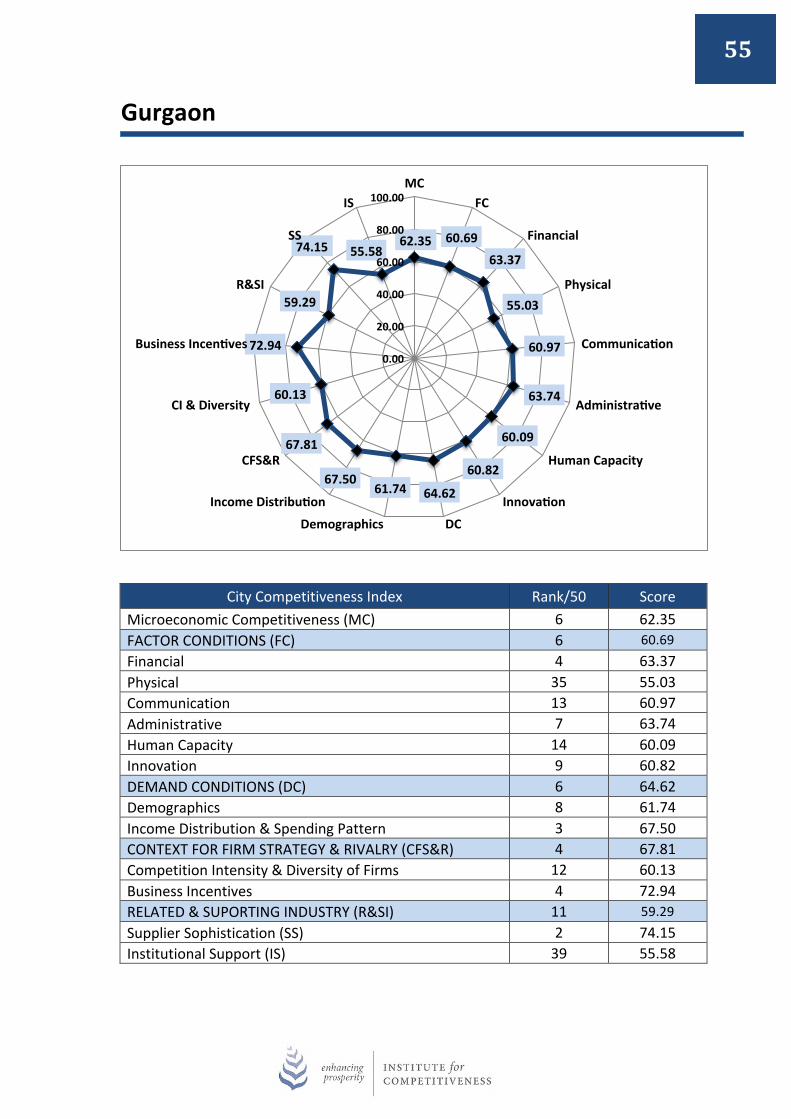

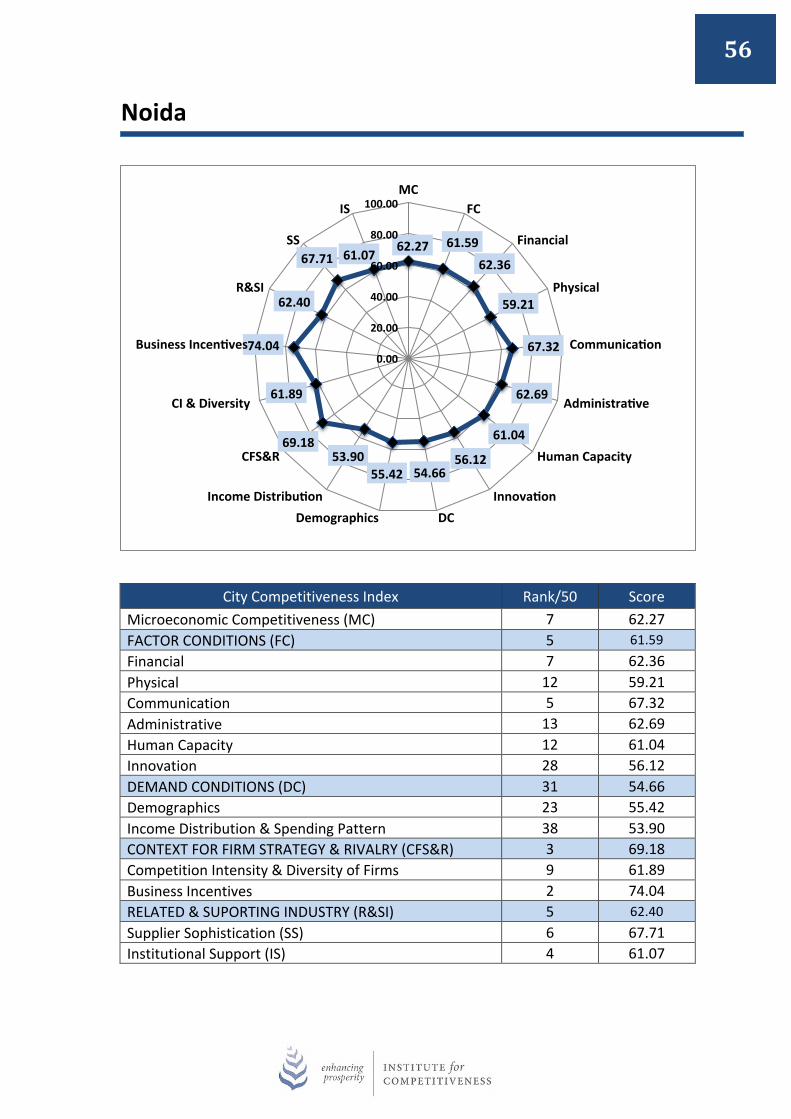

Earlier cities were merely cited as the engines of national growth, but now they have become the hotspots of talent, innovation and prosperity. They play a crucial role in influencing the development and competitiveness of their national economies and are of utmost importance. Therefore, it is important to keep in mind that cities have their own limits and should not be pressurized beyond a certain level, instead, work should be done on their weak areas. Resources should be equally made accessible to other cities. Developmental policies should be put in place so as to connect the missing links of these cities and then, giving them more space to grow. It thus becomes imperative to assess the present state of these cities and nurture them accordingly. The India City Competitiveness Report 2013 thus makes the task easy and brings the competitiveness rankings of 50 Indian cities. According to the competitiveness Index 2013, Delhi has emerged as the most competitive city in the country. It is closely followed by Mumbai, which has successfully maintained its last year’s position. However, there are small changes in the rankings of the rest of the cities, in comparison to their rankings on competitiveness index in 2012. Thus, reflecting the growth of one city with respect to another. 3.1 The Top 10 achievers: Most Competitive cities in India As expected, New Delhi has again emerged as the most competitive city. It is stable on the numero UNO position since the last four years. Even Mumbai maintained its position by capturing the title of the second most competitive city in India. It has retained its 2nd position consecutively for three years now (in 2011, 2012 and 2013). Chennai holds the 3rd position and is stable at its place as it was in the city competitiveness index 2012. The much talked about the city of this year Hyderabad is spotted at the 4th place. Kolkata is stable at 5th position on the index. Followed by, Gurgaon at the 6th position as it was in the city competitiveness index 2012. One shift evident in the top ten ranking is, Noida and Bengaluru have swapped their positions. Noida has moved one position upwards and is spotted at 7th position, and Bengaluru has slipped one place and is now at 8th position. Pune is also stable with its 9th position on the competitiveness index 2013. Similarly, The Manchester of East, Ahmedabad is steady at 10th position. In order of merit, the following cities are India’s top ten: Delhi, Mumbai, Chennai, Hyderabad, Kolkata, Gurgaon, Noida, Bengaluru, Pune, and Ahmedabad. These cities are also the most livable and desirable for work, live, play and learn. These cities are the most competitive with high growth potential and micro-‐economic resilience. All of them influence their respective States both economically and politically. Certainly, they will contribute significantly in enhancing the prosperity of the nation and

30

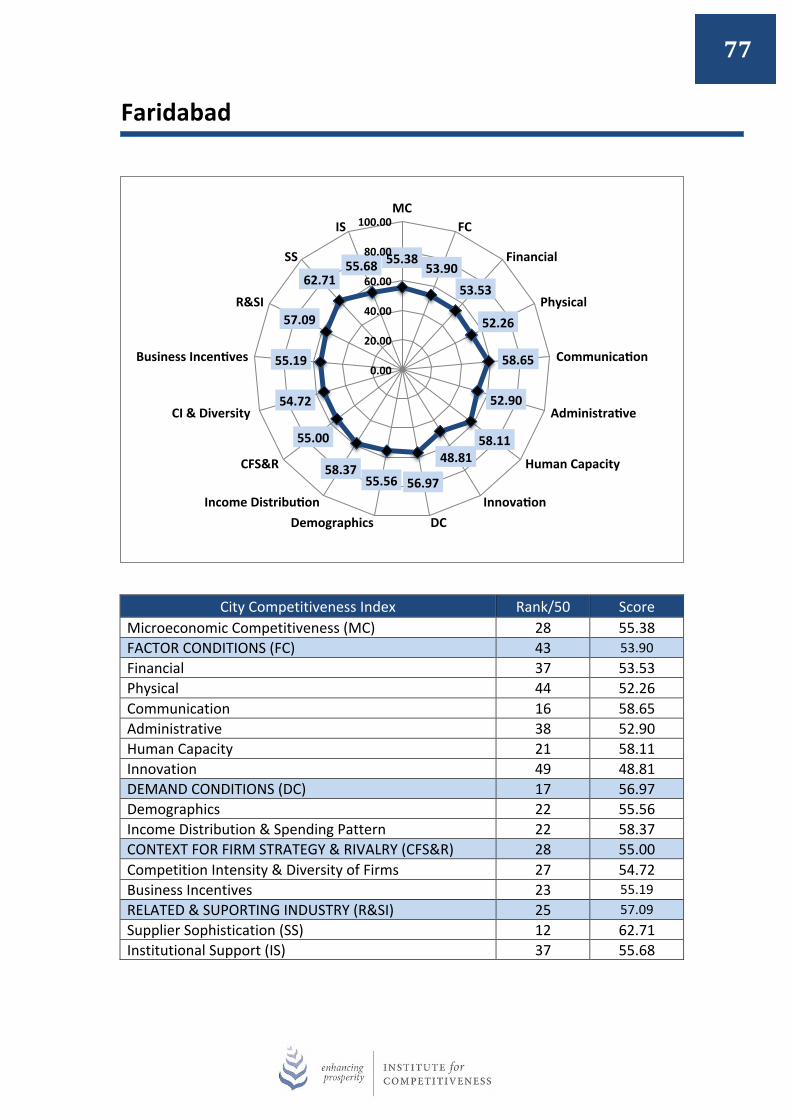

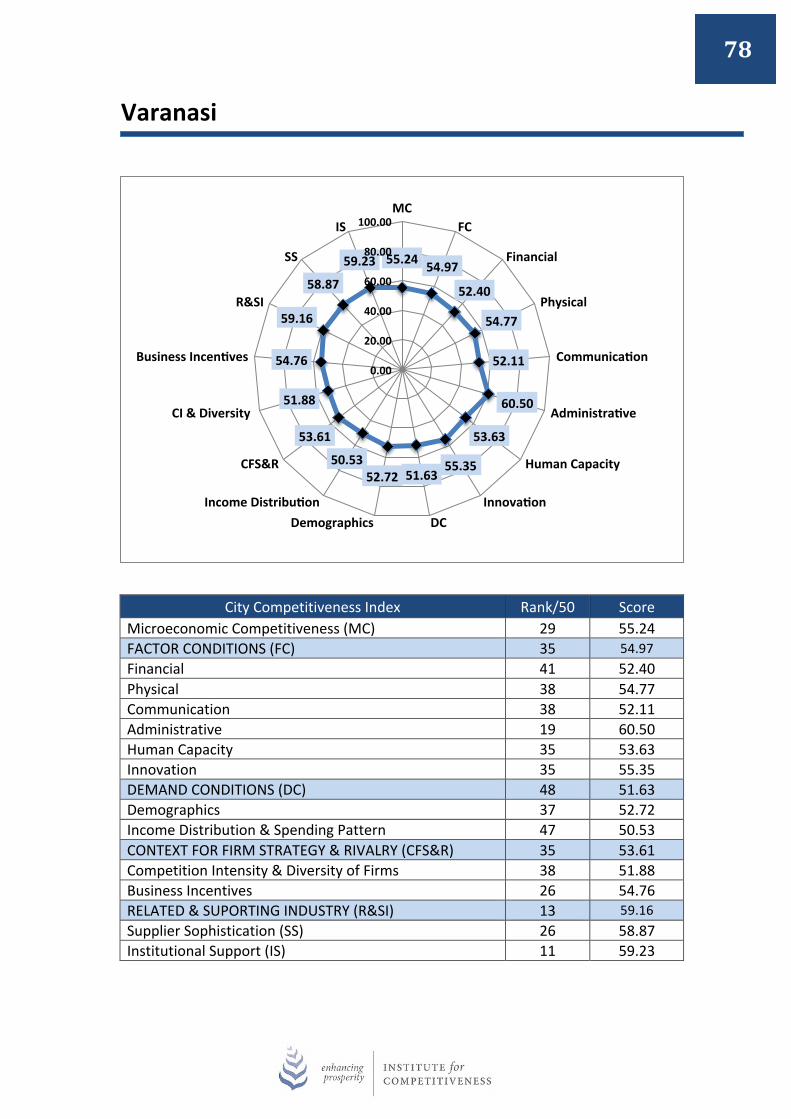

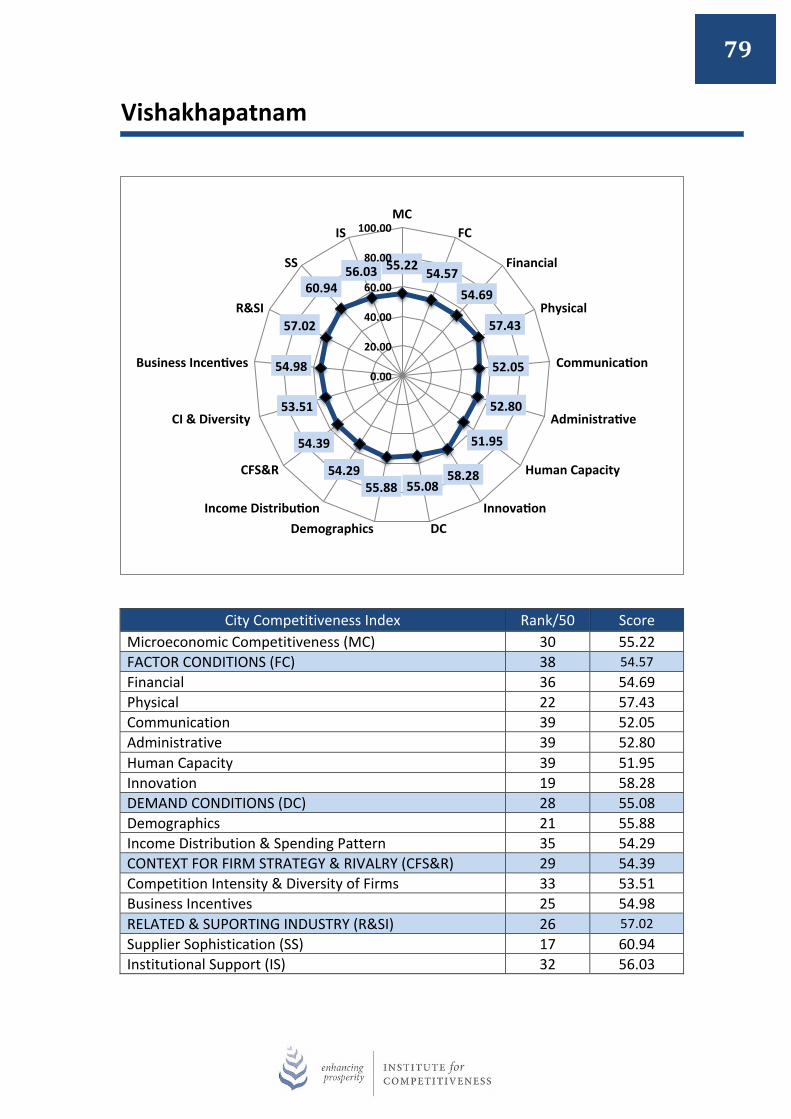

the overall competitiveness. 3.2 The 11-‐20 Positions: Holding immense potential This slot is dominated by the so-‐called small cities. The city at the 11th position is Nagpur and is stable at its position since last year. Coimbatore has moved two places upward and is spotted at the 12th position. Two cities of Kerala, Kozhikode and Thiruvananthapuram were successful in moving up the competitiveness index at 13th and 17th position respectively. On the other hand, Kochi another city from Kerala has dropped one position and is now at 16th position. The city known for its diamonds, Surat has jumped two places and holds the 14th position. Chandigarh has dropped three places and is now at 15th position. Nashik has dropped one place and is at 18th position. Jaipur has moved down to 19th position. Madurai at 20th position is a new entrant in the top 20 competitiveness rankings. Competition in this tier of Indian cities is highly intensive as they are constantly seeking to outdo each other in the category. While competing with one another in this league, these cities benchmark against the first ten and are indeed challenging the achiever cities. The growth potential of these cities attracts younger talent and a new breed of stakeholders. The cities in order of their rankings are Nagpur, Coimbatore, Kozhikode, Surat, Chandigarh, Kochi, Thiruvananthapuram, Nashik, Jaipur and Madurai. These cities have the capacity to succeed if they deploy the right strategy that capitalizes on their resources, flaws and limits. 3.3 The 21-‐30 Positions: On the growth path The city that holds the number one rank in this slot (21-‐30) is Rajkot. It has jumped three places upwards to grab the 21st position. Vadodara is spotted at 22nd position. Followed by Indore at the 23rd position. The capital city of Uttar Pradesh, Lucknow has moved one place upwards and is at 24th position. The new city included in the competitiveness index 2013, Kota is spotted at 25th position. Mysore has dropped five places since last year and is now at 26th position. Bhopal is stable at 27th position. Faridabad has moved upward to 28th position. Two new cities have entered this slot of cities moving on the growth path. Varanasi has grabbed the 29th position, and Vishakhapatnam has grabbed the 30th position. These cities may seem to be lacking in some fundamentals, but they have just embarked their journey towards the 21st century and therefore open to new ideas and external investment. These cities may develop the “x factor”, which will help them to ascend the ladder of competitiveness in the future. The cities in this category in order of their merit are Rajkot, Vadodara, Indore, Lucknow, Kota,

31

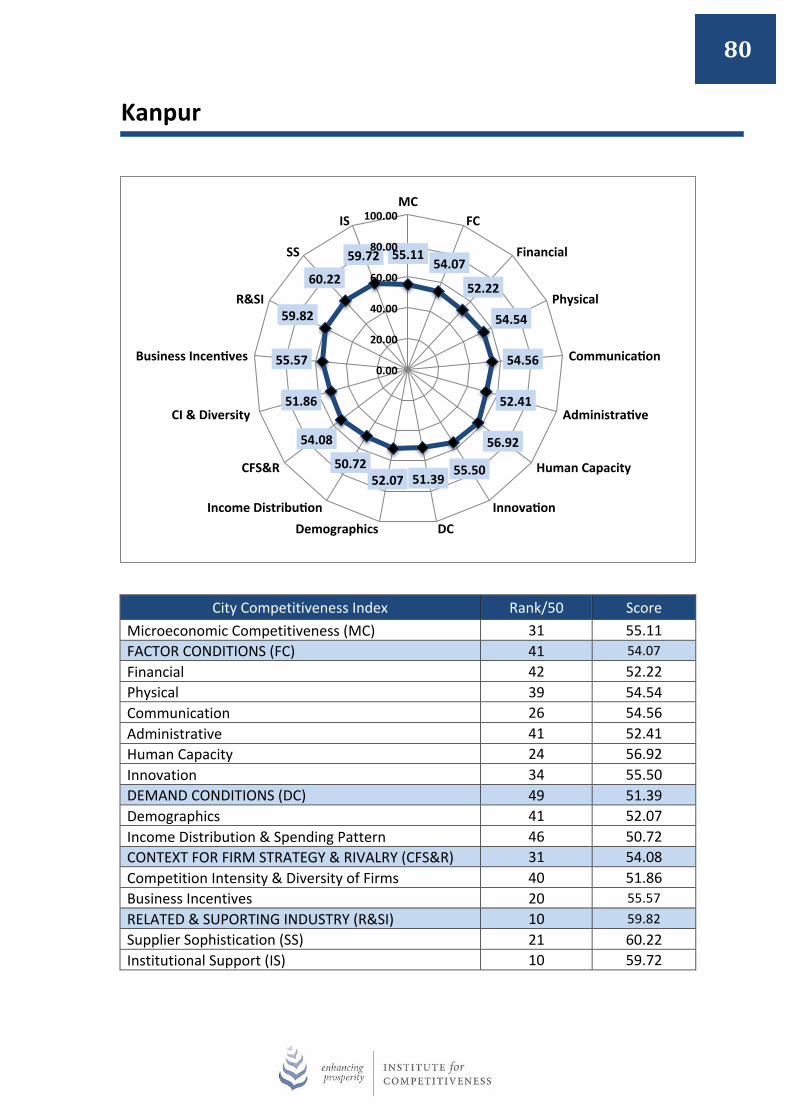

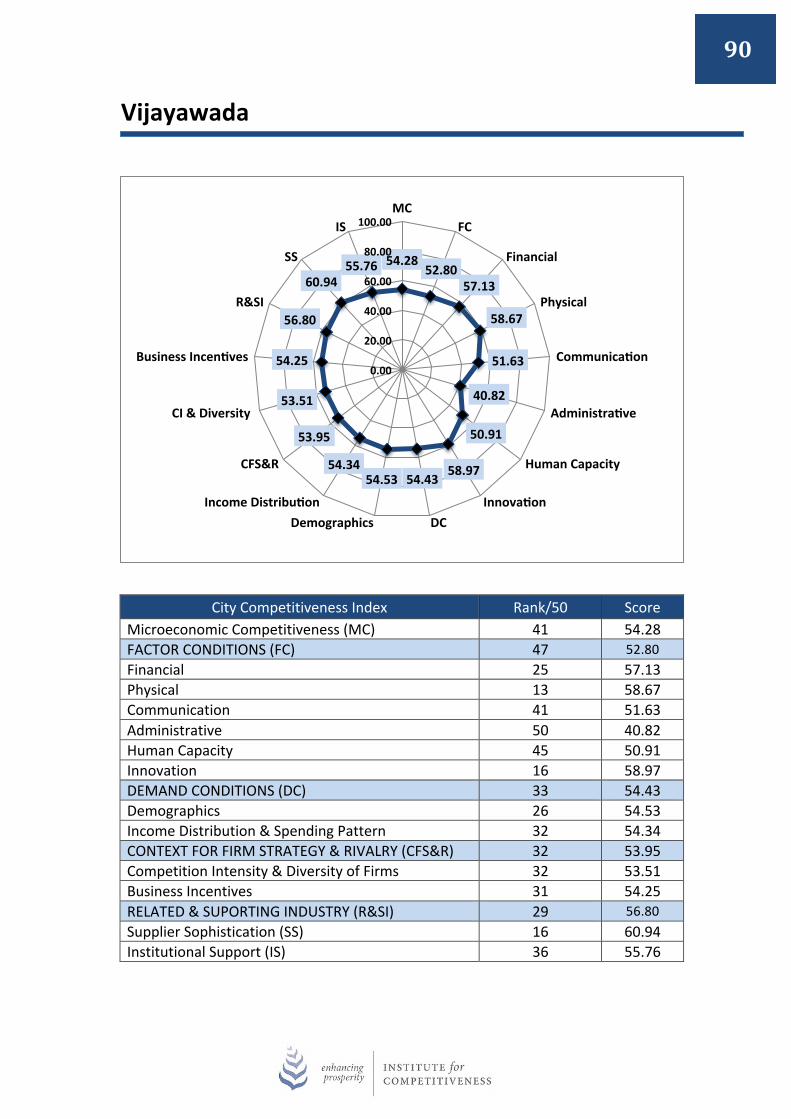

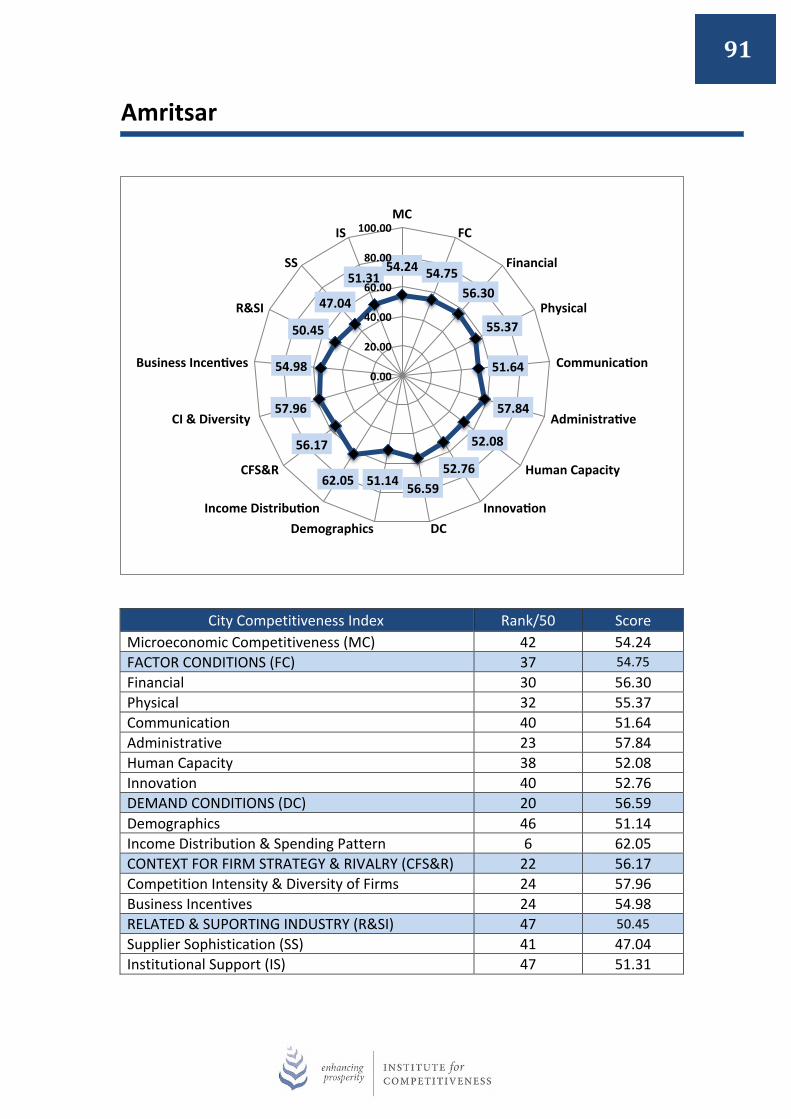

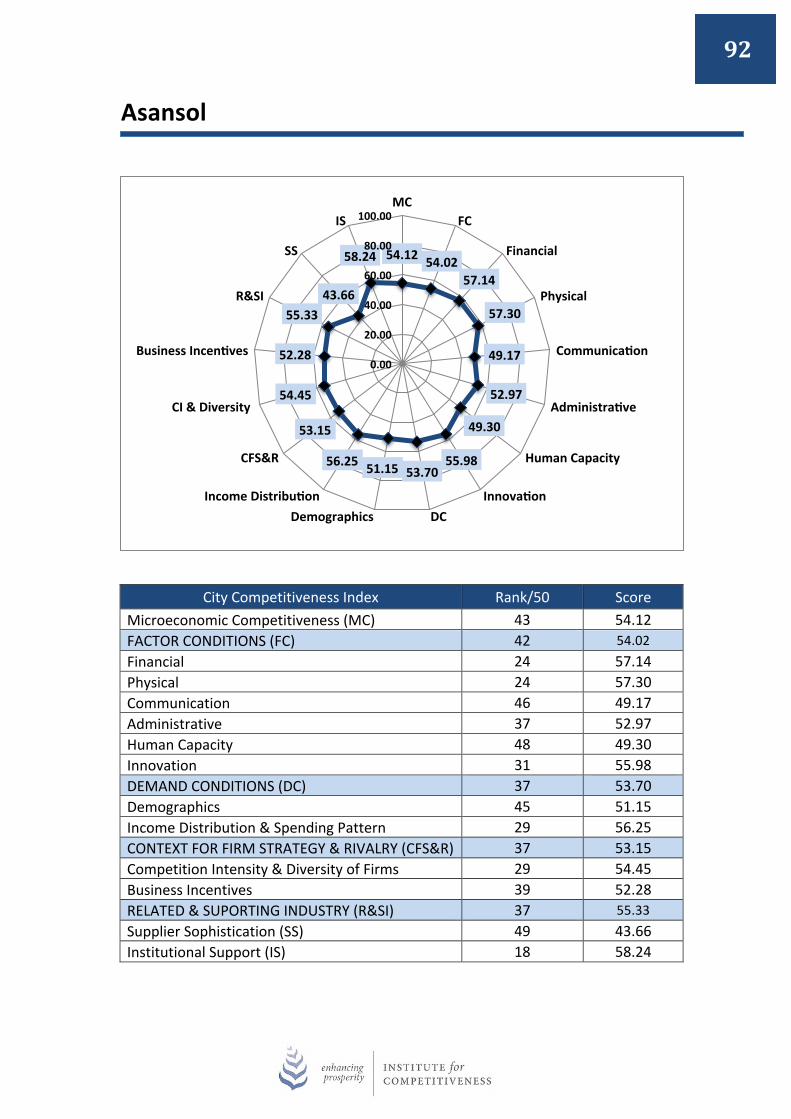

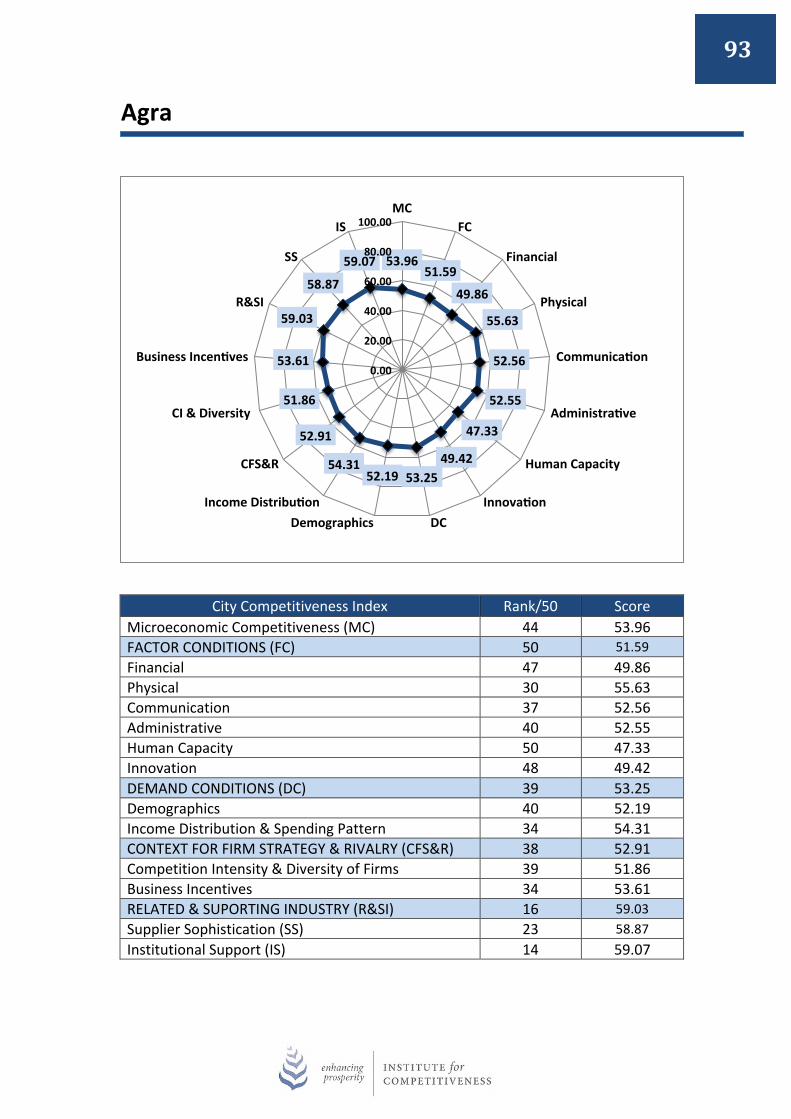

Mysore, Bhopal, Faridabad, Varanasi and Vishakhapatnam. 3.4 The 31-‐40 Positions: Seeking new opportunities Kanpur holds the top position in this slot and holds the 31st position. Followed by Ludhiana at 32nd position and Bhubaneswar at 33rd position, both the cities dropped from their last year’s rank. Raipur is spotted at 34th position. Meerut moved four places upwards and is at 35th position. Guwahati has dropped and is now at 36th position. Dehradun moved upwards to 37th position. Patna at 38th dropped three places. Allahabad and Shimla entered this slot (31-‐40) and are spotted at 39th and 40th position respectively. These cities while locally popular are hardly known internationally. This category consists of Groundfield (old cities with significant legacy infrastructures) and Greenfield cities (newly planned cities). Some cities have stagnated and so continue in this category. Others are new cities that have slower growth rates and are bidding their time move up to the next league. Cities in this category would need to identify strengths and pursue a consistent direction to achieve better results. The list of cities in this category includes Kanpur, Ludhiana, Bhubaneswar, Raipur, Meerut, Guwahati, Dehradun, Patna, Allahabad and Shimla. 3.5 The 41-‐50 Positions: In a developing state Vijayawada is the city at 41st position has drastically dropped from its last year’s position. Amritsar has gained four places and now holds the 42nd position. Asansol has dropped and is at 43rd position. Similarly, Agra declined to 44th position, Ranchi to 45th position and Jabalpur to 46th position. Jammu is stable and holds the 47th position. Srinagar has beaten Dhanbad to grab the spot of 48th position. Thus, Dhanbad now is at 50th position and Jamshedpur at 49th position. It is perceived that cities that have secured lower scores are less competitive, not so prosperous and lagging behind in the growth race. However all cities have their unique strengths and are part of the overall urban ecosystem in India. They are Vijayawada, Amritsar, Asansol, Agra, Ranchi, Jabalpur, Jammu, Srinagar, Jamshedpur and Dhanbad. All cities in India contribute towards India’s national competitiveness and are inter-‐networked. The geospatial distribution of cities and their international linkages become critical both to the region and the world.

32

Overall Competitiveness

Rank City Score 1 Delhi 69.89 2 Mumbai 69.88 3 Chennai 63.40 4 Hyderabad 62.81 5 Kolkata 62.43 6 Gurgaon 62.35 7 Noida 62.27 8 Bengaluru 61.70 9 Pune 61.43 10 Ahmedabad 60.52 11 Nagpur 59.07 12 Coimbatore 58.82 13 Kozhikode 58.40 14 Surat 58.37 15 Chandigarh 58.24 16 Kochi 58.21 17 Thiruvananthapuram 57.97 18 Nashik 57.83 19 Jaipur 57.24 20 Madurai 56.94 21 Rajkot 56.85 22 Vadodara 56.76 23 Indore 56.48 24 Lucknow 55.85 25 Kota 55.66 26 Mysore 55.54 27 Bhopal 55.51 28 Faridabad 55.38 29 Varanasi 55.24 30 Vishakhapatnam 55.22 31 Kanpur 55.11 32 Ludhiana 55.10 33 Bhubaneswar 55.09 34 Raipur 55.03 35 Meerut 54.93 36 Guwahati 54.83 37 Dehradun 54.71 38 Patna 54.64 39 Allahabad 54.62 40 Shimla 54.35 41 Vijayawada 54.28 42 Amritsar 54.24 43 Asansol 54.12 44 Agra 53.96 45 Ranchi 53.87 46 Jabalpur 53.58 47 Jammu 52.73 48 Srinagar 51.92 49 Jamshedpur 51.89 50 Dhanbad 51.88

33

Factor Conditions Rank City Score 1 Mumbai 69.06 2 Delhi 66.76 3 Kolkata 62.57 4 Chennai 62.48 5 Noida 61.59 6 Gurgaon 60.69 7 Bengaluru 60.52 8 Ahmedabad 60.42 9 Hyderabad 60.16 10 Kozhikode 60.01 11 Pune 59.88 12 Shimla 59.63 13 Thiruvananthapuram 59.12 14 Coimbatore 59.11 15 Chandigarh 58.70 16 Surat 58.58 17 Dehradun 57.96 18 Raipur 57.84 19 Indore 57.80 20 Vadodara 57.23 21 Mysore 57.09 22 Guwahati 57.05 23 Kochi 56.88 24 Rajkot 56.87 25 Madurai 56.68 26 Bhopal 56.66 27 Bhubaneswar 56.56 28 Jaipur 56.47 29 Jammu 56.10 30 Nagpur 55.99 31 Kota 55.87 32 Nashik 55.84 33 Ludhiana 55.42 34 Allahabad 55.14 35 Varanasi 54.97 36 Lucknow 54.90 37 Amritsar 54.75 38 Vishakhapatnam 54.57 39 Ranchi 54.46 40 Patna 54.42 41 Kanpur 54.07 42 Asansol 54.02 43 Faridabad 53.90 44 Srinagar 53.28 45 Meerut 53.26 46 Jabalpur 53.16 47 Vijayawada 52.80 48 Dhanbad 52.44 49 Jamshedpur 51.84 50 Agra 51.59

34

Financial Rank City Score 1 Mumbai 78.56 2 Pune 65.77 3 Delhi 65.02 4 Gurgaon 63.37 5 Ahmedabad 62.67 6 Kolkata 62.61 7 Noida 62.36 8 Thiruvananthapuram 61.65 9 Kochi 61.60 10 Shimla 61.13 11 Indore 61.11 12 Coimbatore 60.29 13 Rajkot 59.77 14 Chennai 59.57 15 Nashik 59.50 16 Raipur 59.26 17 Kota 59.10 18 Vadodara 59.04 19 Hyderabad 58.90 20 Surat 58.14 21 Mysore 57.93 22 Chandigarh 57.28 23 Bengaluru 57.17 24 Asansol 57.14 25 Vijayawada 57.13 26 Kozhikode 56.71 27 Patna 56.49 28 Ludhiana 56.46 29 Dehradun 56.44 30 Amritsar 56.30 31 Bhopal 56.24 32 Bhubaneswar 56.09 33 Nagpur 55.72 34 Jammu 55.48 35 Jaipur 54.82 36 Vishakhapatnam 54.69 37 Faridabad 53.53 38 Jabalpur 53.31 39 Madurai 53.23 40 Lucknow 53.17 41 Varanasi 52.40 42 Kanpur 52.22 43 Meerut 52.19 44 Allahabad 51.07 45 Guwahati 51.03 46 Ranchi 50.34 47 Agra 49.86 48 Jamshedpur 49.83 49 Dhanbad 48.22 50 Srinagar 45.25

35

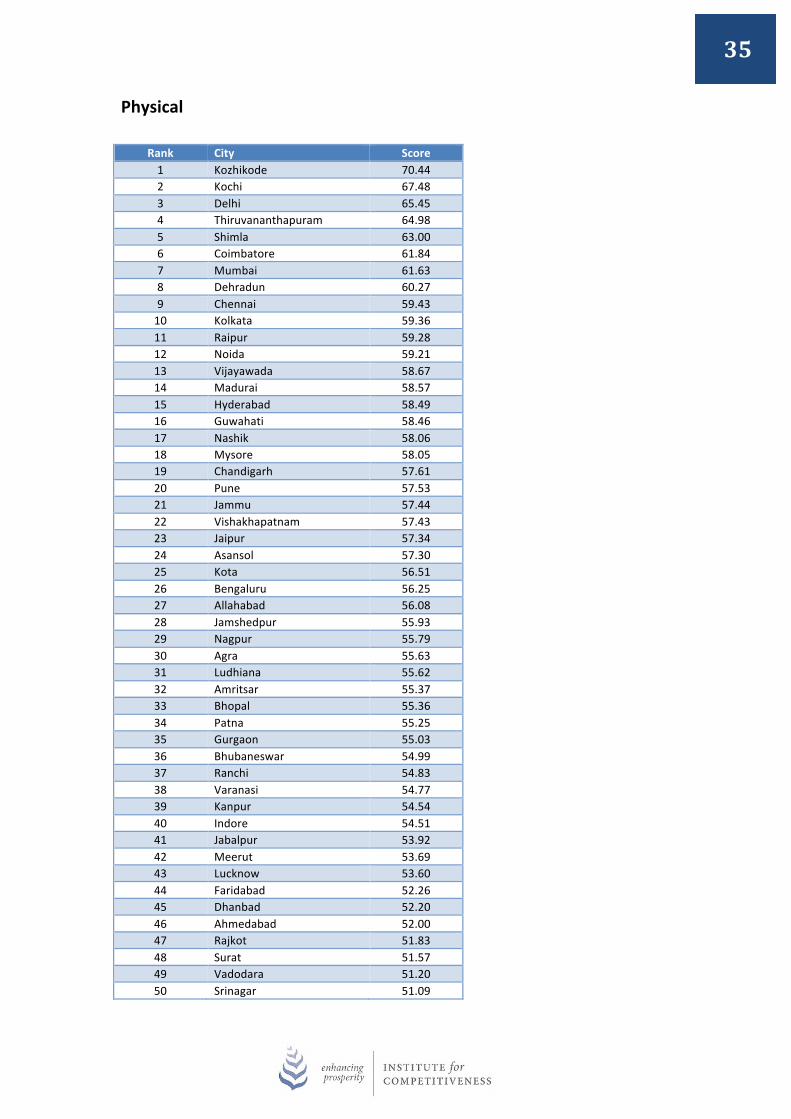

Physical Rank City Score 1 Kozhikode 70.44 2 Kochi 67.48 3 Delhi 65.45 4 Thiruvananthapuram 64.98 5 Shimla 63.00 6 Coimbatore 61.84 7 Mumbai 61.63 8 Dehradun 60.27 9 Chennai 59.43 10 Kolkata 59.36 11 Raipur 59.28 12 Noida 59.21 13 Vijayawada 58.67 14 Madurai 58.57 15 Hyderabad 58.49 16 Guwahati 58.46 17 Nashik 58.06 18 Mysore 58.05 19 Chandigarh 57.61 20 Pune 57.53 21 Jammu 57.44 22 Vishakhapatnam 57.43 23 Jaipur 57.34 24 Asansol 57.30 25 Kota 56.51 26 Bengaluru 56.25 27 Allahabad 56.08 28 Jamshedpur 55.93 29 Nagpur 55.79 30 Agra 55.63 31 Ludhiana 55.62 32 Amritsar 55.37 33 Bhopal 55.36 34 Patna 55.25 35 Gurgaon 55.03 36 Bhubaneswar 54.99 37 Ranchi 54.83 38 Varanasi 54.77 39 Kanpur 54.54 40 Indore 54.51 41 Jabalpur 53.92 42 Meerut 53.69 43 Lucknow 53.60 44 Faridabad 52.26 45 Dhanbad 52.20 46 Ahmedabad 52.00 47 Rajkot 51.83 48 Surat 51.57 49 Vadodara 51.20 50 Srinagar 51.09

36

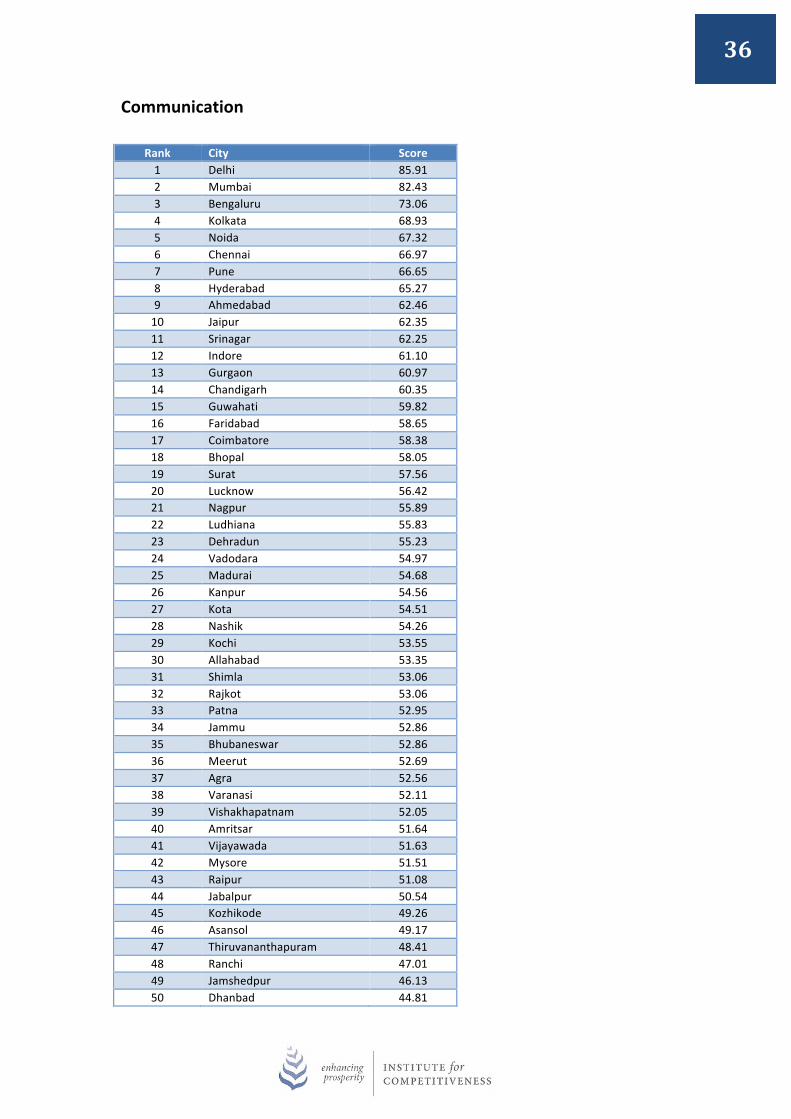

Communication Rank City Score 1 Delhi 85.91 2 Mumbai 82.43 3 Bengaluru 73.06 4 Kolkata 68.93 5 Noida 67.32 6 Chennai 66.97 7 Pune 66.65 8 Hyderabad 65.27 9 Ahmedabad 62.46 10 Jaipur 62.35 11 Srinagar 62.25 12 Indore 61.10 13 Gurgaon 60.97 14 Chandigarh 60.35 15 Guwahati 59.82 16 Faridabad 58.65 17 Coimbatore 58.38 18 Bhopal 58.05 19 Surat 57.56 20 Lucknow 56.42 21 Nagpur 55.89 22 Ludhiana 55.83 23 Dehradun 55.23 24 Vadodara 54.97 25 Madurai 54.68 26 Kanpur 54.56 27 Kota 54.51 28 Nashik 54.26 29 Kochi 53.55 30 Allahabad 53.35 31 Shimla 53.06 32 Rajkot 53.06 33 Patna 52.95 34 Jammu 52.86 35 Bhubaneswar 52.86 36 Meerut 52.69 37 Agra 52.56 38 Varanasi 52.11 39 Vishakhapatnam 52.05 40 Amritsar 51.64 41 Vijayawada 51.63 42 Mysore 51.51 43 Raipur 51.08 44 Jabalpur 50.54 45 Kozhikode 49.26 46 Asansol 49.17 47 Thiruvananthapuram 48.41 48 Ranchi 47.01 49 Jamshedpur 46.13 50 Dhanbad 44.81

37

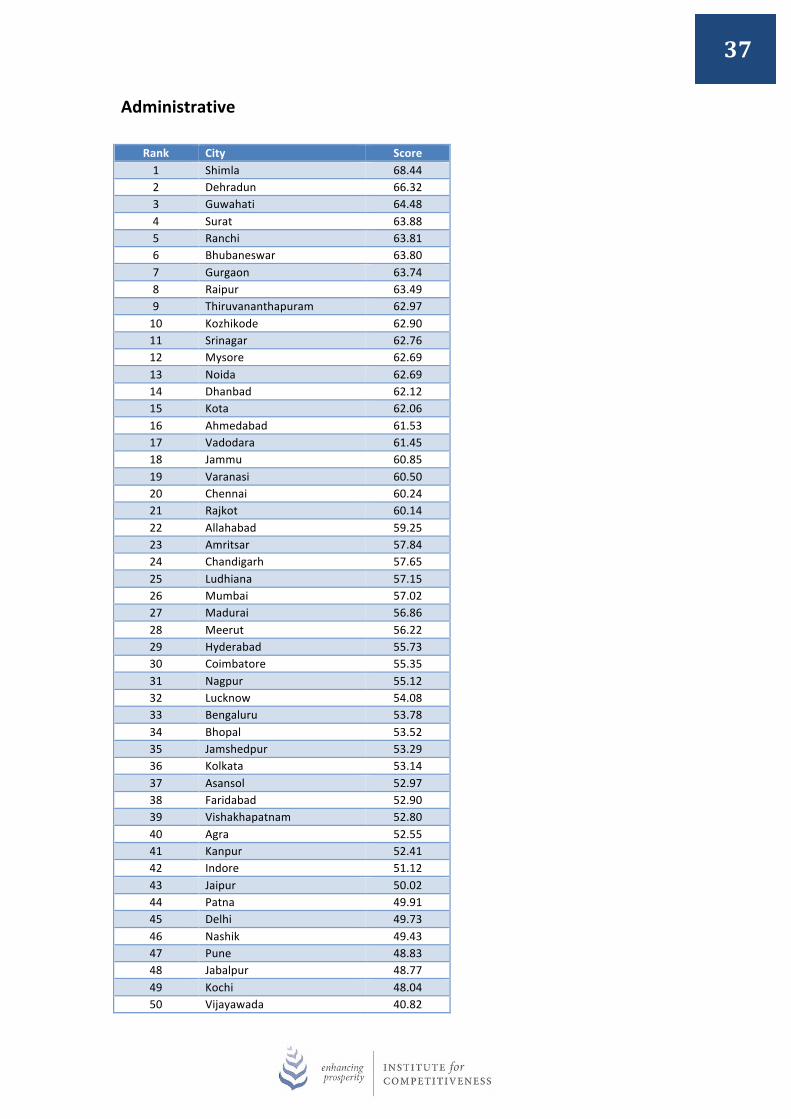

Administrative Rank City Score 1 Shimla 68.44 2 Dehradun 66.32 3 Guwahati 64.48 4 Surat 63.88 5 Ranchi 63.81 6 Bhubaneswar 63.80 7 Gurgaon 63.74 8 Raipur 63.49 9 Thiruvananthapuram 62.97 10 Kozhikode 62.90 11 Srinagar 62.76 12 Mysore 62.69 13 Noida 62.69 14 Dhanbad 62.12 15 Kota 62.06 16 Ahmedabad 61.53 17 Vadodara 61.45 18 Jammu 60.85 19 Varanasi 60.50 20 Chennai 60.24 21 Rajkot 60.14 22 Allahabad 59.25 23 Amritsar 57.84 24 Chandigarh 57.65 25 Ludhiana 57.15 26 Mumbai 57.02 27 Madurai 56.86 28 Meerut 56.22 29 Hyderabad 55.73 30 Coimbatore 55.35 31 Nagpur 55.12 32 Lucknow 54.08 33 Bengaluru 53.78 34 Bhopal 53.52 35 Jamshedpur 53.29 36 Kolkata 53.14 37 Asansol 52.97 38 Faridabad 52.90 39 Vishakhapatnam 52.80 40 Agra 52.55 41 Kanpur 52.41 42 Indore 51.12 43 Jaipur 50.02 44 Patna 49.91 45 Delhi 49.73 46 Nashik 49.43 47 Pune 48.83 48 Jabalpur 48.77 49 Kochi 48.04 50 Vijayawada 40.82

38

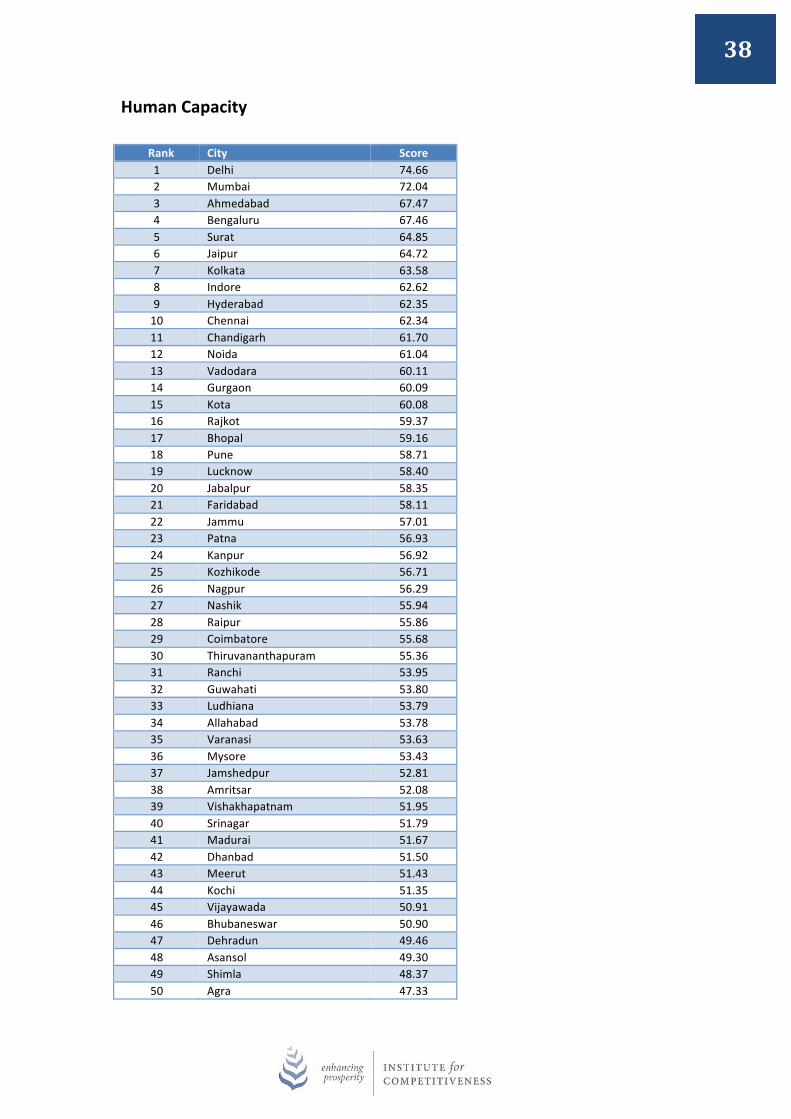

Human Capacity

Rank City Score 1 Delhi 74.66 2 Mumbai 72.04 3 Ahmedabad 67.47 4 Bengaluru 67.46 5 Surat 64.85 6 Jaipur 64.72 7 Kolkata 63.58 8 Indore 62.62 9 Hyderabad 62.35 10 Chennai 62.34 11 Chandigarh 61.70 12 Noida 61.04 13 Vadodara 60.11 14 Gurgaon 60.09 15 Kota 60.08 16 Rajkot 59.37 17 Bhopal 59.16 18 Pune 58.71 19 Lucknow 58.40 20 Jabalpur 58.35 21 Faridabad 58.11 22 Jammu 57.01 23 Patna 56.93 24 Kanpur 56.92 25 Kozhikode 56.71 26 Nagpur 56.29 27 Nashik 55.94 28 Raipur 55.86 29 Coimbatore 55.68 30 Thiruvananthapuram 55.36 31 Ranchi 53.95 32 Guwahati 53.80 33 Ludhiana 53.79 34 Allahabad 53.78 35 Varanasi 53.63 36 Mysore 53.43 37 Jamshedpur 52.81 38 Amritsar 52.08 39 Vishakhapatnam 51.95 40 Srinagar 51.79 41 Madurai 51.67 42 Dhanbad 51.50 43 Meerut 51.43 44 Kochi 51.35 45 Vijayawada 50.91 46 Bhubaneswar 50.90 47 Dehradun 49.46 48 Asansol 49.30 49 Shimla 48.37 50 Agra 47.33

39

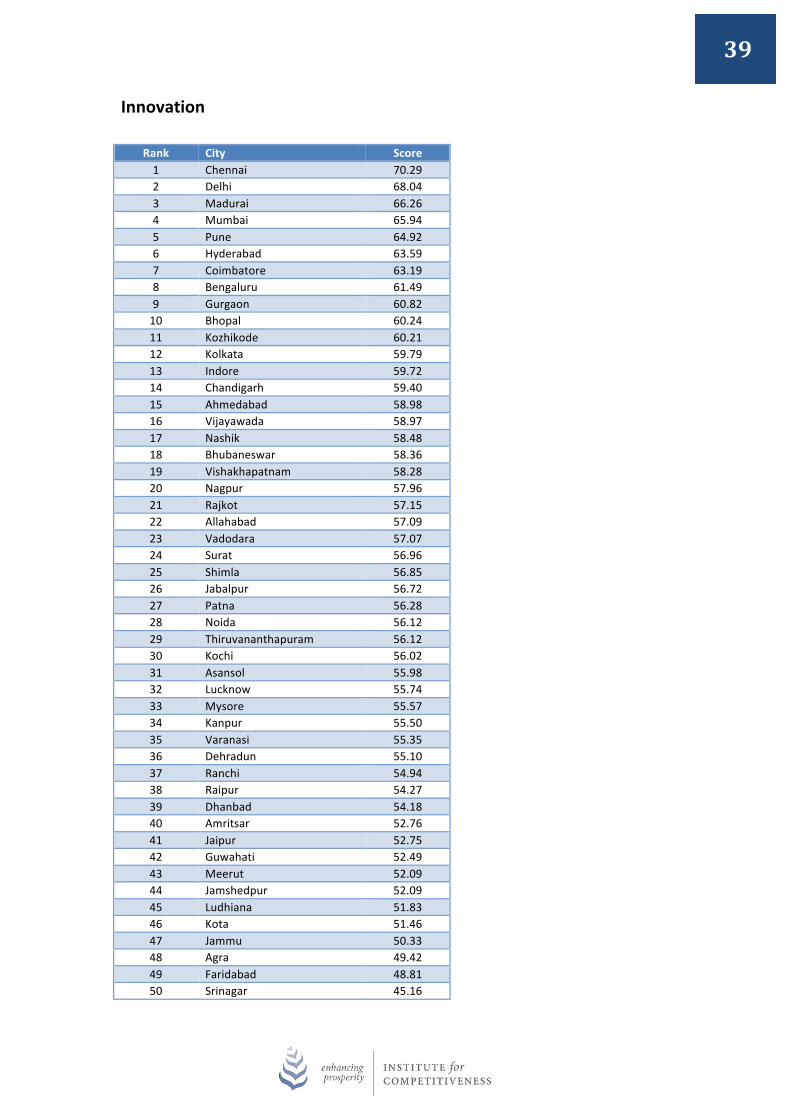

Innovation Rank City Score 1 Chennai 70.29 2 Delhi 68.04 3 Madurai 66.26 4 Mumbai 65.94 5 Pune 64.92 6 Hyderabad 63.59 7 Coimbatore 63.19 8 Bengaluru 61.49 9 Gurgaon 60.82 10 Bhopal 60.24 11 Kozhikode 60.21 12 Kolkata 59.79 13 Indore 59.72 14 Chandigarh 59.40 15 Ahmedabad 58.98 16 Vijayawada 58.97 17 Nashik 58.48 18 Bhubaneswar 58.36 19 Vishakhapatnam 58.28 20 Nagpur 57.96 21 Rajkot 57.15 22 Allahabad 57.09 23 Vadodara 57.07 24 Surat 56.96 25 Shimla 56.85 26 Jabalpur 56.72 27 Patna 56.28 28 Noida 56.12 29 Thiruvananthapuram 56.12 30 Kochi 56.02 31 Asansol 55.98 32 Lucknow 55.74 33 Mysore 55.57 34 Kanpur 55.50 35 Varanasi 55.35 36 Dehradun 55.10 37 Ranchi 54.94 38 Raipur 54.27 39 Dhanbad 54.18 40 Amritsar 52.76 41 Jaipur 52.75 42 Guwahati 52.49 43 Meerut 52.09 44 Jamshedpur 52.09 45 Ludhiana 51.83 46 Kota 51.46 47 Jammu 50.33 48 Agra 49.42 49 Faridabad 48.81 50 Srinagar 45.16

40

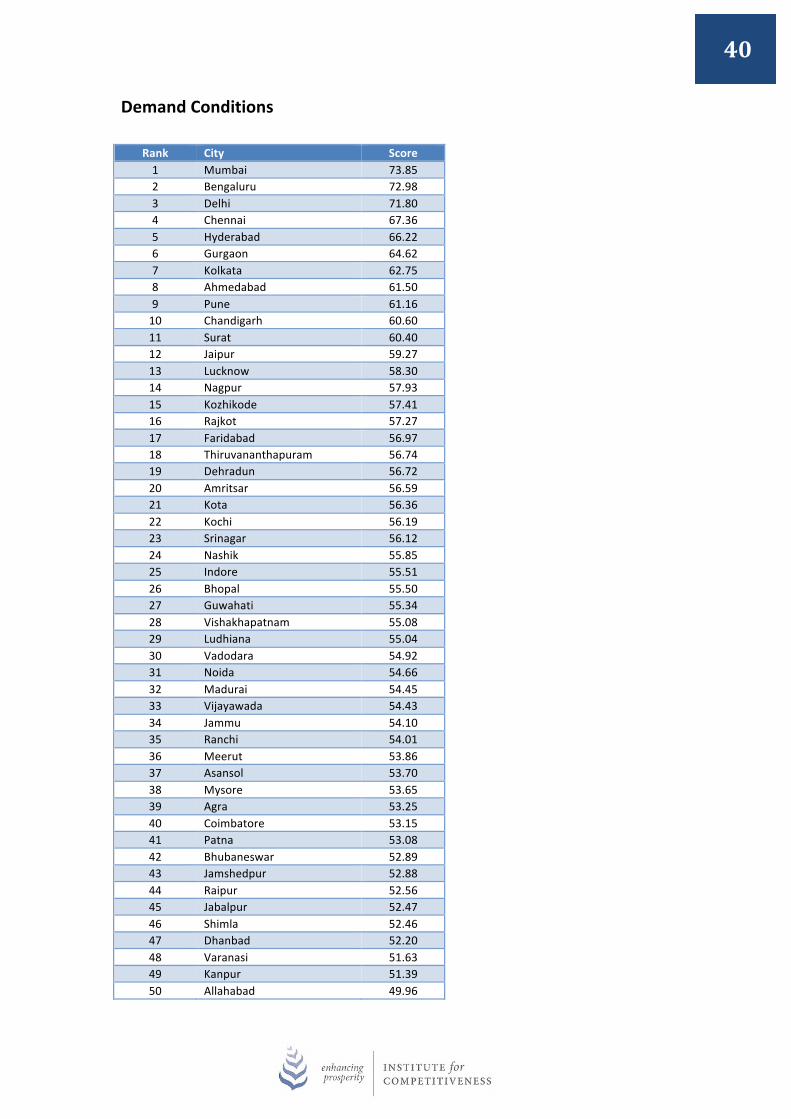

Demand Conditions Rank City Score 1 Mumbai 73.85 2 Bengaluru 72.98 3 Delhi 71.80 4 Chennai 67.36 5 Hyderabad 66.22 6 Gurgaon 64.62 7 Kolkata 62.75 8 Ahmedabad 61.50 9 Pune 61.16 10 Chandigarh 60.60 11 Surat 60.40 12 Jaipur 59.27 13 Lucknow 58.30 14 Nagpur 57.93 15 Kozhikode 57.41 16 Rajkot 57.27 17 Faridabad 56.97 18 Thiruvananthapuram 56.74 19 Dehradun 56.72 20 Amritsar 56.59 21 Kota 56.36 22 Kochi 56.19 23 Srinagar 56.12 24 Nashik 55.85 25 Indore 55.51 26 Bhopal 55.50 27 Guwahati 55.34 28 Vishakhapatnam 55.08 29 Ludhiana 55.04 30 Vadodara 54.92 31 Noida 54.66 32 Madurai 54.45 33 Vijayawada 54.43 34 Jammu 54.10 35 Ranchi 54.01 36 Meerut 53.86 37 Asansol 53.70 38 Mysore 53.65 39 Agra 53.25 40 Coimbatore 53.15 41 Patna 53.08 42 Bhubaneswar 52.89 43 Jamshedpur 52.88 44 Raipur 52.56 45 Jabalpur 52.47 46 Shimla 52.46 47 Dhanbad 52.20 48 Varanasi 51.63 49 Kanpur 51.39 50 Allahabad 49.96

41

Demographics

Rank City Score 1 Mumbai 82.60 2 Delhi 78.77 3 Bengaluru 77.22 4 Chennai 74.17 5 Hyderabad 72.49 6 Kolkata 66.47 7 Ahmedabad 63.24 8 Gurgaon 61.74 9 Pune 61.59 10 Lucknow 59.13 11 Surat 58.95 12 Jaipur 58.61 13 Indore 58.55 14 Raipur 57.71 15 Kozhikode 57.69 16 Nagpur 57.23 17 Coimbatore 56.98 18 Bhopal 56.83 19 Madurai 56.71 20 Thiruvananthapuram 56.09 21 Vishakhapatnam 55.88 22 Faridabad 55.56 23 Noida 55.42 24 Mysore 55.40 25 Dehradun 54.63 26 Vijayawada 54.53 27 Ranchi 54.51 28 Kochi 54.42 29 Patna 54.37 30 Vadodara 53.86 31 Nashik 53.83 32 Guwahati 53.78 33 Rajkot 53.33 34 Srinagar 53.32 35 Kota 52.97 36 Jabalpur 52.79 37 Varanasi 52.72 38 Meerut 52.67 39 Chandigarh 52.67 40 Agra 52.19 41 Kanpur 52.07 42 Jamshedpur 51.76 43 Bhubaneswar 51.46 44 Allahabad 51.35 45 Asansol 51.15 46 Amritsar 51.14 47 Dhanbad 50.95 48 Ludhiana 50.57 49 Jammu 49.80 50 Shimla 45.26

42

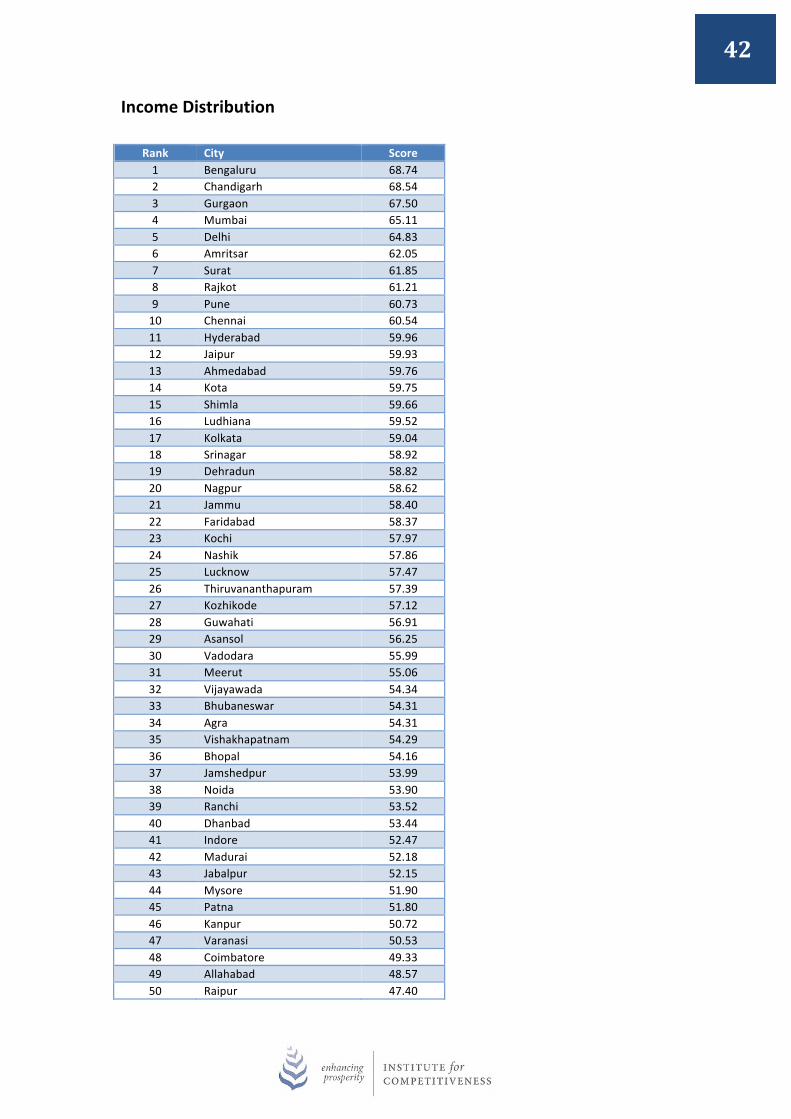

Income Distribution Rank City Score 1 Bengaluru 68.74 2 Chandigarh 68.54 3 Gurgaon 67.50 4 Mumbai 65.11 5 Delhi 64.83 6 Amritsar 62.05 7 Surat 61.85 8 Rajkot 61.21 9 Pune 60.73 10 Chennai 60.54 11 Hyderabad 59.96 12 Jaipur 59.93 13 Ahmedabad 59.76 14 Kota 59.75 15 Shimla 59.66 16 Ludhiana 59.52 17 Kolkata 59.04 18 Srinagar 58.92 19 Dehradun 58.82 20 Nagpur 58.62 21 Jammu 58.40 22 Faridabad 58.37 23 Kochi 57.97 24 Nashik 57.86 25 Lucknow 57.47 26 Thiruvananthapuram 57.39 27 Kozhikode 57.12 28 Guwahati 56.91 29 Asansol 56.25 30 Vadodara 55.99 31 Meerut 55.06 32 Vijayawada 54.34 33 Bhubaneswar 54.31 34 Agra 54.31 35 Vishakhapatnam 54.29 36 Bhopal 54.16 37 Jamshedpur 53.99 38 Noida 53.90 39 Ranchi 53.52 40 Dhanbad 53.44 41 Indore 52.47 42 Madurai 52.18 43 Jabalpur 52.15 44 Mysore 51.90 45 Patna 51.80 46 Kanpur 50.72 47 Varanasi 50.53 48 Coimbatore 49.33 49 Allahabad 48.57 50 Raipur 47.40

43

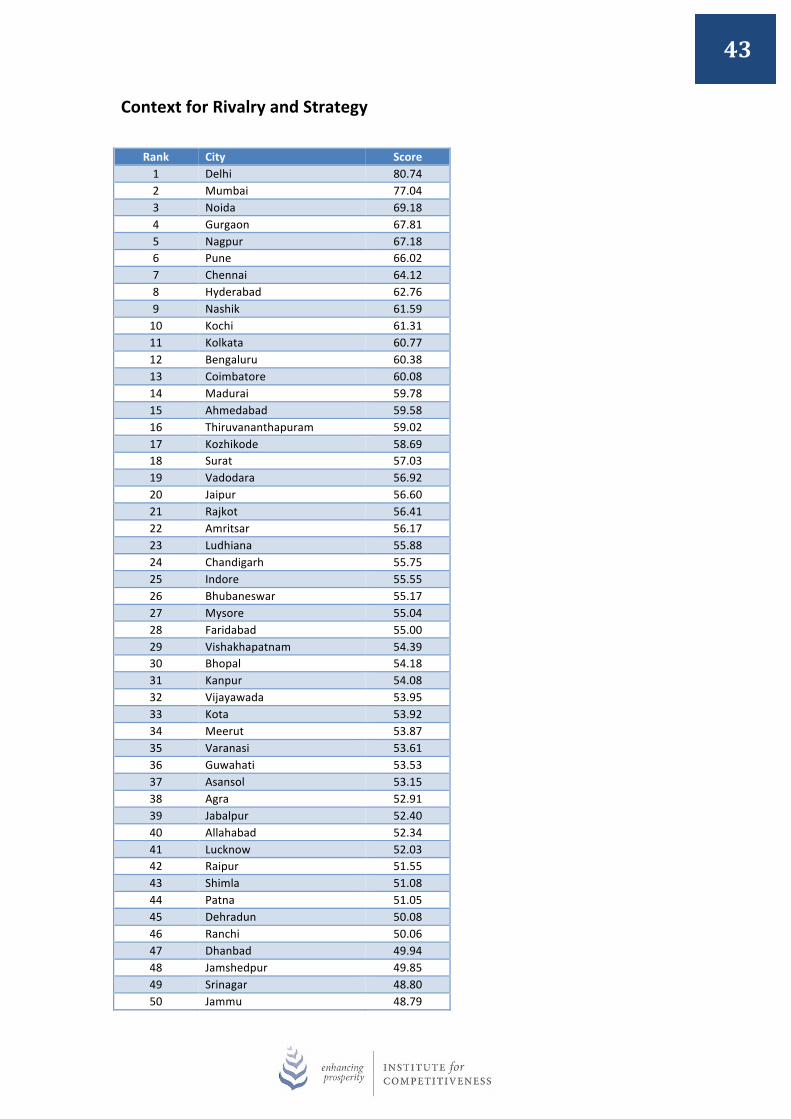

Context for Rivalry and Strategy Rank City Score 1 Delhi 80.74 2 Mumbai 77.04 3 Noida 69.18 4 Gurgaon 67.81 5 Nagpur 67.18 6 Pune 66.02 7 Chennai 64.12 8 Hyderabad 62.76 9 Nashik 61.59 10 Kochi 61.31 11 Kolkata 60.77 12 Bengaluru 60.38 13 Coimbatore 60.08 14 Madurai 59.78 15 Ahmedabad 59.58 16 Thiruvananthapuram 59.02 17 Kozhikode 58.69 18 Surat 57.03 19 Vadodara 56.92 20 Jaipur 56.60 21 Rajkot 56.41 22 Amritsar 56.17 23 Ludhiana 55.88 24 Chandigarh 55.75 25 Indore 55.55 26 Bhubaneswar 55.17 27 Mysore 55.04 28 Faridabad 55.00 29 Vishakhapatnam 54.39 30 Bhopal 54.18 31 Kanpur 54.08 32 Vijayawada 53.95 33 Kota 53.92 34 Meerut 53.87 35 Varanasi 53.61 36 Guwahati 53.53 37 Asansol 53.15 38 Agra 52.91 39 Jabalpur 52.40 40 Allahabad 52.34 41 Lucknow 52.03 42 Raipur 51.55 43 Shimla 51.08 44 Patna 51.05 45 Dehradun 50.08 46 Ranchi 50.06 47 Dhanbad 49.94 48 Jamshedpur 49.85 49 Srinagar 48.80 50 Jammu 48.79

44

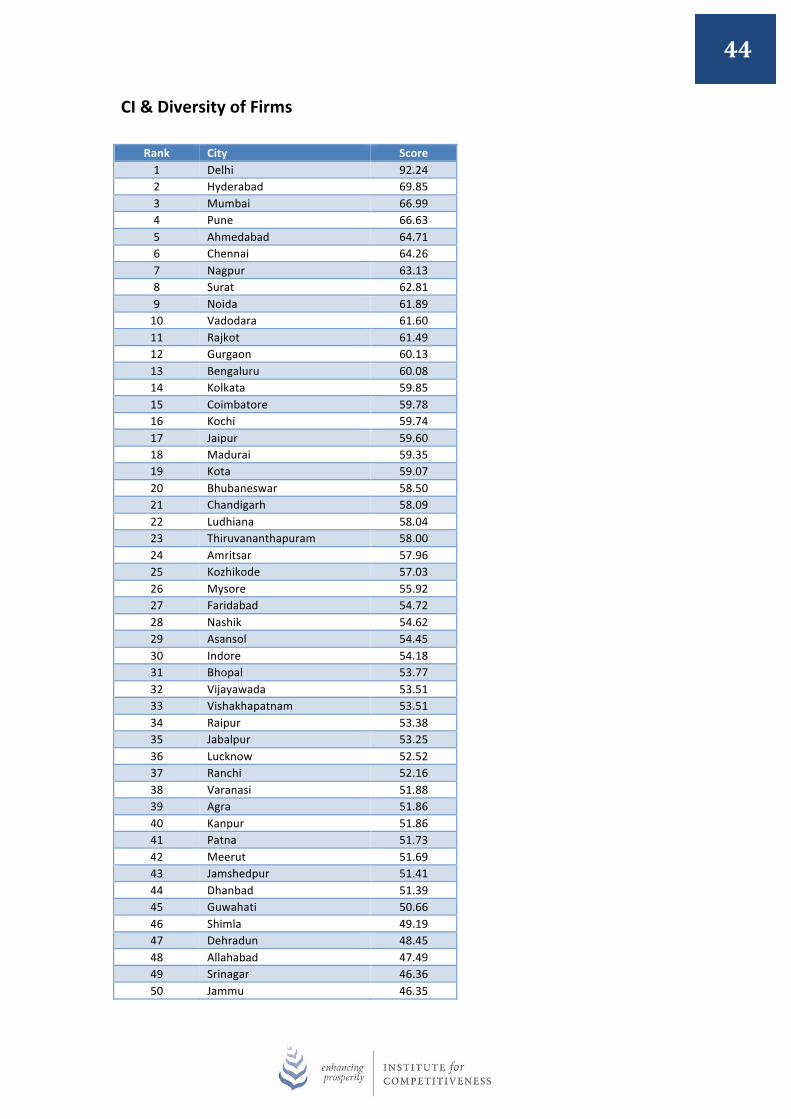

CI & Diversity of Firms Rank City Score 1 Delhi 92.24 2 Hyderabad 69.85 3 Mumbai 66.99 4 Pune 66.63 5 Ahmedabad 64.71 6 Chennai 64.26 7 Nagpur 63.13 8 Surat 62.81 9 Noida 61.89 10 Vadodara 61.60 11 Rajkot 61.49 12 Gurgaon 60.13 13 Bengaluru 60.08 14 Kolkata 59.85 15 Coimbatore 59.78 16 Kochi 59.74 17 Jaipur 59.60 18 Madurai 59.35 19 Kota 59.07 20 Bhubaneswar 58.50 21 Chandigarh 58.09 22 Ludhiana 58.04 23 Thiruvananthapuram 58.00 24 Amritsar 57.96 25 Kozhikode 57.03 26 Mysore 55.92 27 Faridabad 54.72 28 Nashik 54.62 29 Asansol 54.45 30 Indore 54.18 31 Bhopal 53.77 32 Vijayawada 53.51 33 Vishakhapatnam 53.51 34 Raipur 53.38 35 Jabalpur 53.25 36 Lucknow 52.52 37 Ranchi 52.16 38 Varanasi 51.88 39 Agra 51.86 40 Kanpur 51.86 41 Patna 51.73 42 Meerut 51.69 43 Jamshedpur 51.41 44 Dhanbad 51.39 45 Guwahati 50.66 46 Shimla 49.19 47 Dehradun 48.45 48 Allahabad 47.49 49 Srinagar 46.36 50 Jammu 46.35

45

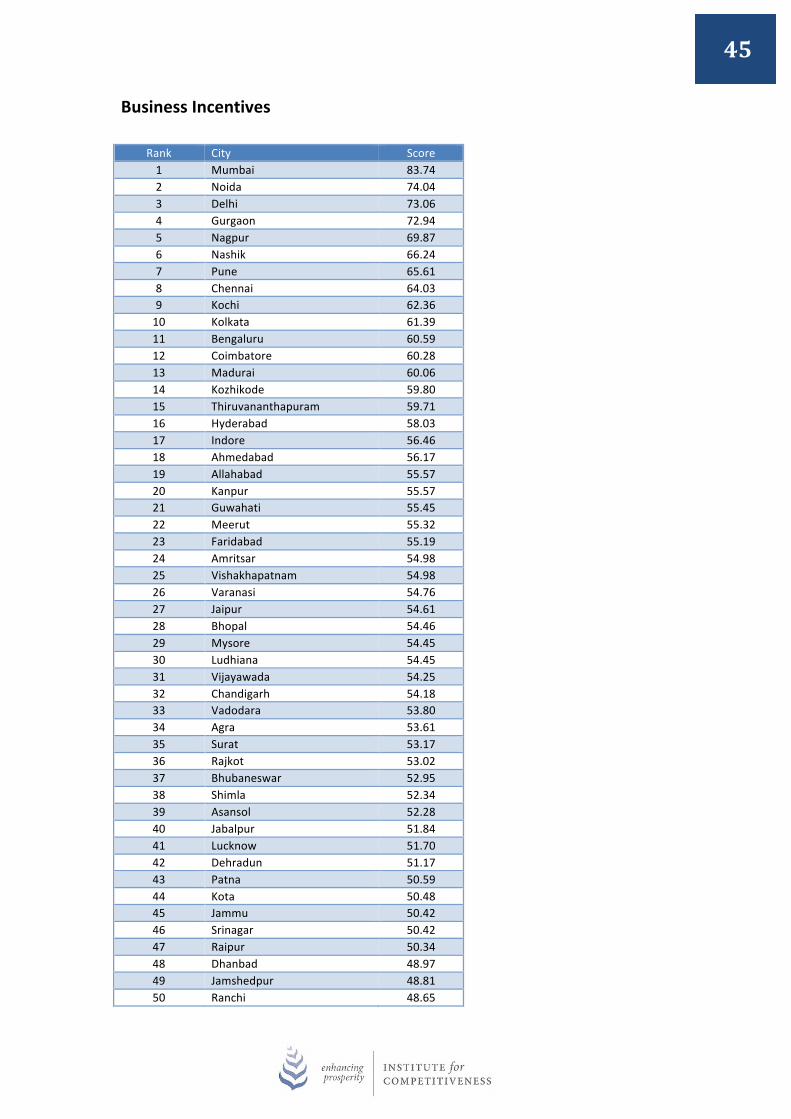

Business Incentives Rank City Score 1 Mumbai 83.74 2 Noida 74.04 3 Delhi 73.06 4 Gurgaon 72.94 5 Nagpur 69.87 6 Nashik 66.24 7 Pune 65.61 8 Chennai 64.03 9 Kochi 62.36 10 Kolkata 61.39 11 Bengaluru 60.59 12 Coimbatore 60.28 13 Madurai 60.06 14 Kozhikode 59.80 15 Thiruvananthapuram 59.71 16 Hyderabad 58.03 17 Indore 56.46 18 Ahmedabad 56.17 19 Allahabad 55.57 20 Kanpur 55.57 21 Guwahati 55.45 22 Meerut 55.32 23 Faridabad 55.19 24 Amritsar 54.98 25 Vishakhapatnam 54.98 26 Varanasi 54.76 27 Jaipur 54.61 28 Bhopal 54.46 29 Mysore 54.45 30 Ludhiana 54.45 31 Vijayawada 54.25 32 Chandigarh 54.18 33 Vadodara 53.80 34 Agra 53.61 35 Surat 53.17 36 Rajkot 53.02 37 Bhubaneswar 52.95 38 Shimla 52.34 39 Asansol 52.28 40 Jabalpur 51.84 41 Lucknow 51.70 42 Dehradun 51.17 43 Patna 50.59 44 Kota 50.48 45 Jammu 50.42 46 Srinagar 50.42 47 Raipur 50.34 48 Dhanbad 48.97 49 Jamshedpur 48.81 50 Ranchi 48.65

46