CCH Federal Taxation 4 Major Types of Federal Taxes 1.Income taxes Individual income tax and...

26

CCH Federal Taxation 4 Major Types of Federal Taxes 1. Income taxes Individual income tax and corporate income tax . 2. Employment taxes FICA Social Security, FICA Medicare and FUTA. 3. Estate and gift taxes Taxes on transfers of property 4. Excise and custom taxes Taxes on transactions (taxes on the purchase of alcohol)

-

Upload

morgan-mcbride -

Category

Documents

-

view

227 -

download

3

Transcript of CCH Federal Taxation 4 Major Types of Federal Taxes 1.Income taxes Individual income tax and...

CCH Federal Taxation

4 Major Types of Federal Taxes

1. Income taxes Individual income tax and corporate income tax.

2. Employment taxes FICA Social Security, FICA Medicare and FUTA.

3. Estate and gift taxes Taxes on transfers of property

4. Excise and custom taxes Taxes on transactions (taxes on the purchase of alcohol)

CCH Federal Taxation

Tax Avoidance v. Tax Evasion

Tax avoidance—Saving tax dollars through specific actions to avoid the tax liability prior to the time it would have occurred according to the law.

Tax evasion—The taxpayer does not properly report income and expenses even though the taxpayer already has a tax liability and all actions are definitely complete.

CCH Federal Taxation

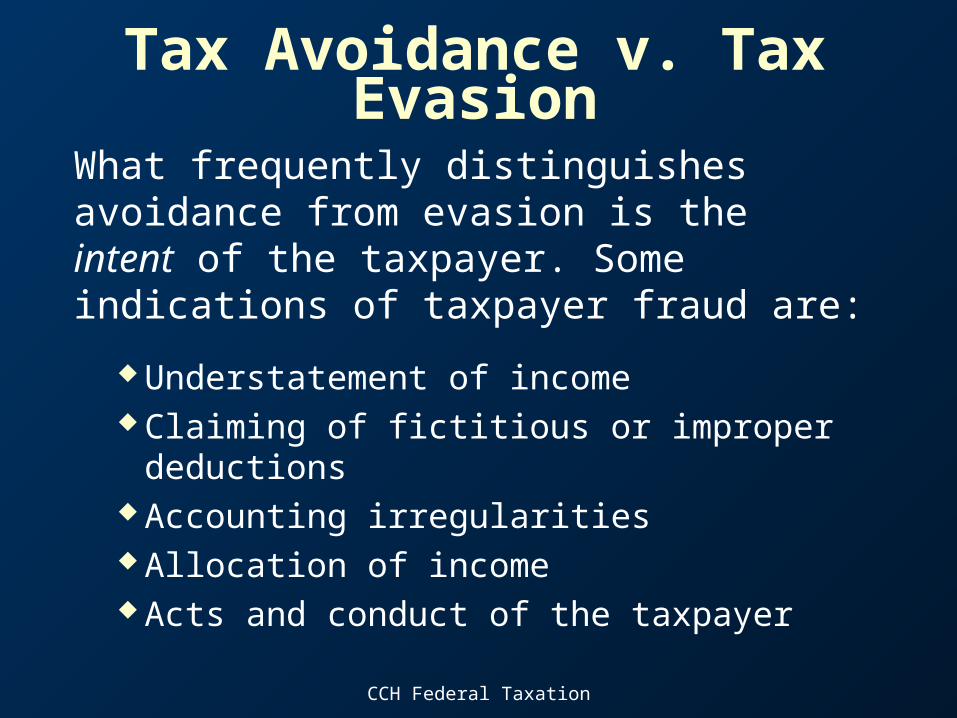

Tax Avoidance v. Tax Evasion

What frequently distinguishes avoidance from evasion is the intent of the taxpayer. Some indications of taxpayer fraud are:

Understatement of income Claiming of fictitious or improper deductions Accounting irregularities Allocation of income Acts and conduct of the taxpayer

CCH Federal Taxation

Tax Legislative Process

1. The Constitution requires that all revenue legislation start in the House Ways and Means Committee.

2. The tax bill is sent to the House of Representatives for approval. The House debates the bill under a “closed rule”

procedure (all amendments must be approved by the House Ways and Means Committee).

3. If approved by the House of Representatives, the bill is sent to the Senate Finance Committee. The Finance Committee may make amendments to the

House bill.

Exhibit 1 page 1-18

CCH Federal Taxation

Tax Legislative Process Cont…4. The bill is sent to the Senate for approval.

Any senator may offer amendments from the floor of the Senate.

Bill may be sent to a Joint Conference Committee if the House and Senate differ. The bill would then be sent back to House and Senate for consideration. At this point, no further amendments can be made.

5. Approved or vetoed by the President

6. Incorporated into the Code if approved by President or if veto is overridden.

Exhibit 1 page 1-18

CCH Federal Taxation

Classification of Materials Primary or “authoritative”

Internal Revenue Code (statutory authority) Treasury Regulations (administrative authority) Internal Revenue Service Rulings (administrative authority) Judicial Authority

Secondary or “reference” Looseleaf tax reference services Periodicals Textbooks Treatises Published papers from tax institutes Symposia Newsletters

Chapter 2, Exhibit 1

CCH Federal Taxation

Judicial Authority

The three courts of original jurisdiction are: U.S. Tax Court U.S. District Court U.S. Court of Federal Claims

Chapter 2, Exhibit 2a

CCH Federal Taxation

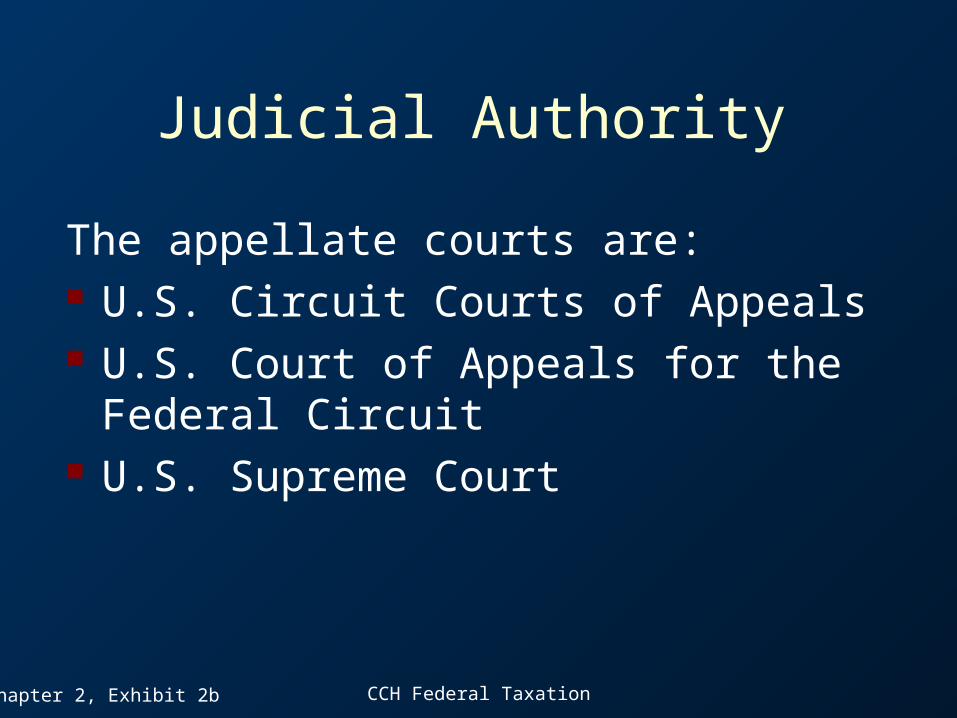

Judicial Authority

The appellate courts are: U.S. Circuit Courts of Appeals U.S. Court of Appeals for the Federal Circuit U.S. Supreme Court

Chapter 2, Exhibit 2b

CCH Federal Taxation

Five-Step Research Method

1. Gather the facts and identify the tax issues.

2. Locate and study the primary and secondary authorities relevant to the enumerated tax issues.

3. Update and evaluate the weight of the various authorities.

4. Re-examine various facets of the research.

5. Arrive at conclusions; communicate these conclusions to the client.

Chapter 2, Exhibit 3

CCH Federal Taxation

Authoritative Documents

Research Source

Authorship Binding Persuasive

16th Amendment Constitution Congress

Internal Revenue Code

CCH, RIA, and West tax services

Congress

Chapter 2, Exhibit 4a

Research Sources for Legislative Authority

CCH Federal Taxation

Authoritative

Documents

Research Source Authorship Binding Persuasive

Tax Treaties(to render mutual assistance between the U.S. and foreign countries in tax enforcement and to avoid double taxation.)

• Tax Treaties (CCH)• Worldwide Tax Treaty Library (Tax Analysts)• International Tax Treaties of All Nations (Oceana Publications)

Congress (overrides

Code if more

recent)

Chapter 2, Exhibit 4b

Research Sources for Legislative Authority

CCH Federal Taxation

Research Sources for Legislative Authority

Authoritative Documents

Research Source Authorship Binding Persuasive

Committee Reports (useful for determining Congressional intent when Code and Regs. are unclear)

Cumulative Bulletins [CB] (U.S.

Government.).

Internal Revenue Bulletin [IRB] if written within 6 months

House Ways and Means Committee Senate Finance Committee Joint Conference Committee

(no legal effect; only guidance)

Bluebook (interprets new legislation)

Bluebook (a government-issued, blue-covered book)

Joint Committee on Taxation

(no legal effect; only guidance)

Chapter 2, Exhibit 4c

CCH Federal Taxation

Authoritative Documents

Research Sources Authorship Binding Persuasive

Final Regulations (Treasury Decisions)

Federal register (U.S. Government.) Tax services (CCH, RIA and West).

U.S. Treasury Department

Temporary Regulations (issued without opportunity for public comment because timing is critical)

Federal Register (U.S. Government) Cumulative Bulletin (U.S. Government) Tax services (CCH, RIA, and West).

U.S. Treasury Department

(binding if < 3 years old)

(nonbinding if over 3 years old)

Proposed Regulations

Federal Register (U.S. Government) Cumulative Bulletin (U.S. Government) Tax services (CCH, RIA, and West).

U.S. Treasury Department

(nonbinding preview or final Regs.)

Research Sources for Administrative Authority

Chapter 2, Exhibit 5a

CCH Federal Taxation

Authoritative Documents

Research Sources Authorship Binding Persuasive

Revenue Rulings (interprets tax laws)

Cumulative Bulletins (U.S. Government)

National office of IRS

(not approved by the Treasury)

Revenue Procedures (addresses internal procedures of IRS)

Cumulative Bulletins(U.S. Government)

National office of IRS

(not approved by the Treasury)

Letter Rulings (explains how IRS will treat a proposed transaction for tax purposes; issued to taxpayers)

IRS Letters Rulings Reports (CCH) Private Letter Rulings (RIA) Daily Tax Reports (BNA)Tax Analysts & Advocates, TAX NOTES

National office of IRS

(only precedent value is for the taxpayer addressed in letter)

Research Sources for Administrative Authority

Chapter 2, Exhibit 5b

CCH Federal Taxation

Authoritative Documents

Research Sources Authorship Binding Persuasive

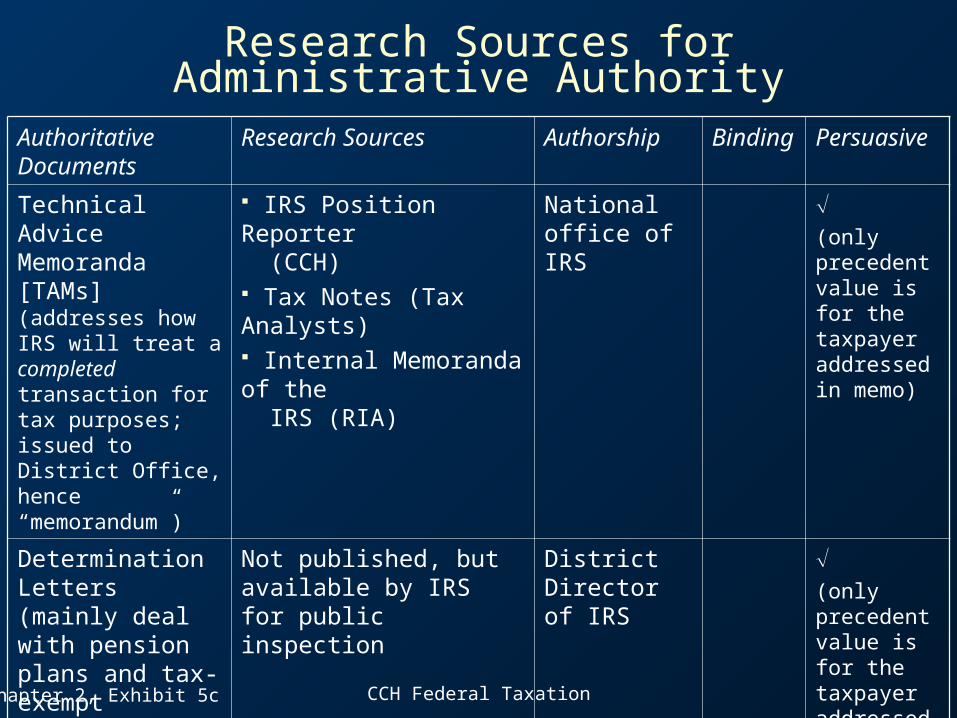

Technical Advice Memoranda [TAMs] (addresses how IRS will treat a completed transaction for tax purposes; issued to District Office, hence “memorandum”)

IRS Position Reporter (CCH) Tax Notes (Tax Analysts) Internal Memoranda of the IRS (RIA)

National office of IRS

(only precedent value is for the taxpayer addressed in memo)

Determination Letters (mainly deal with pension plans and tax-exempt organizations)

Not published, but available by IRS for public inspection

District Director of IRS

(only precedent value is for the taxpayer addressed in letter)

Research Sources for Administrative Authority

Chapter 2, Exhibit 5c

CCH Federal Taxation

Research Sources for Judicial Authority

Authority Research Source Binding Persuasive

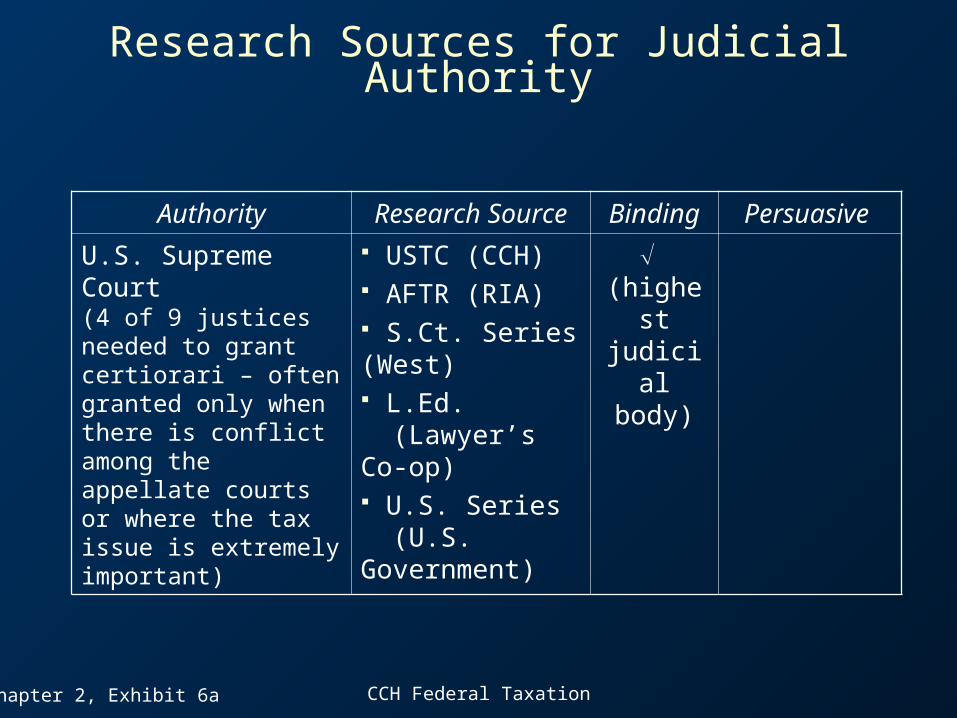

U.S. Supreme Court (4 of 9 justices needed to grant certiorari – often granted only when there is conflict among the appellate courts or where the tax issue is extremely important)

USTC (CCH) AFTR (RIA) S.Ct. Series (West) L.Ed. (Lawyer’s Co-op) U.S. Series (U.S. Government)

(highest judicial body)

Chapter 2, Exhibit 6a

CCH Federal Taxation

Research Sources for Judicial Authority

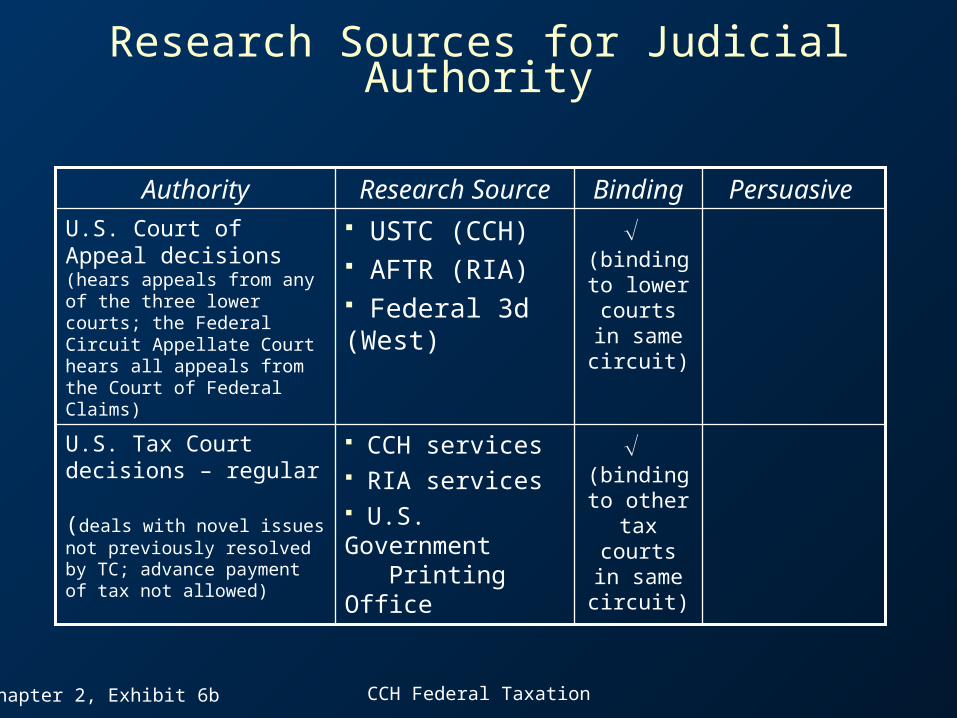

(binding to other tax courts in

same circuit)

CCH services RIA services U.S. Government Printing Office

U.S. Tax Court decisions – regular (deals with novel issues not previously resolved by TC; advance payment of tax not allowed)

(binding to

lower courts in same circuit)

USTC (CCH) AFTR (RIA) Federal 3d (West)

U.S. Court of Appeal decisions(hears appeals from any of the three lower courts; the Federal Circuit Appellate Court hears all appeals from the Court of Federal Claims)

Persuasive BindingResearch SourceAuthority

Chapter 2, Exhibit 6b

CCH Federal Taxation

Research Sources for Judicial Authority

Chapter 2, Exhibit 6c

No precedent authority

Not publishedSmall Cases Division of Tax Court (informal hearing for disputes of $50,000 or less; appeals process not available)

TCM (CCH) T.C. Memo (RIA)

U.S. Tax Court decisions—

Memorandum (deals with factual issues necessitating application of established principles of tax law; advance payment of tax not allowed)

Persuasive BindingResearch SourceAuthority

(binding to other tax courts in

same circuit)

CCH Federal Taxation

Research Sources for Judicial Authority

Authority Research Source Binding Persuasive

U.S. District Court(jury trial available for factual issues but not for legal issues)

USTC (CCH) AFTR (RIA) F. Supp. Series (West)

(binding to courts in

same district)

U.S. Court of FederalClaims (hears any claims against U.S. that is based onthe Constitution,an Act of Congress, or aRegulation of anyexecutive department)

USTC (CCH) AFTR (RIA) Federal Claims Reporter (West)

(binding to same court)

Chapter 2, Exhibit 6d

CCH Federal Taxation

Commercial Publishers of Comprehensive Services

Service Description

Standard Federal Tax Reporter (“Standard”), CCH

Comprehensive, self-contained reference service. 25 coordinated and cross-referenced loose-leaf volumes that provide comprehensive coverage of the income tax law. Compiles legislative, administrative, and judicial aspects of the income tax law, arranged in Code section order. Also contains weekly supplements concerning current legislative, administrative, or judicial changes in tax law.

United States Tax Reporter, RIA

Comprehensive, self-contained reference service. 18 coordinated loose-leaf volumes organized by Code sections and updated weekly. Similar to CCH. RIA is known for its willingness to take a stand on controversial issues not covered by legislation or tax law.

Federal Tax Service, CCH

Contains several volumes of compilation material organized by topic. The Code, Regulations, and Committee Reports are contained in separate volumes. The chapters are prepared by over 250 practitioners.

Chapter 2, Exhibit 7a

CCH Federal Taxation

Commercial Publishers of Comprehensive Services

Service Description

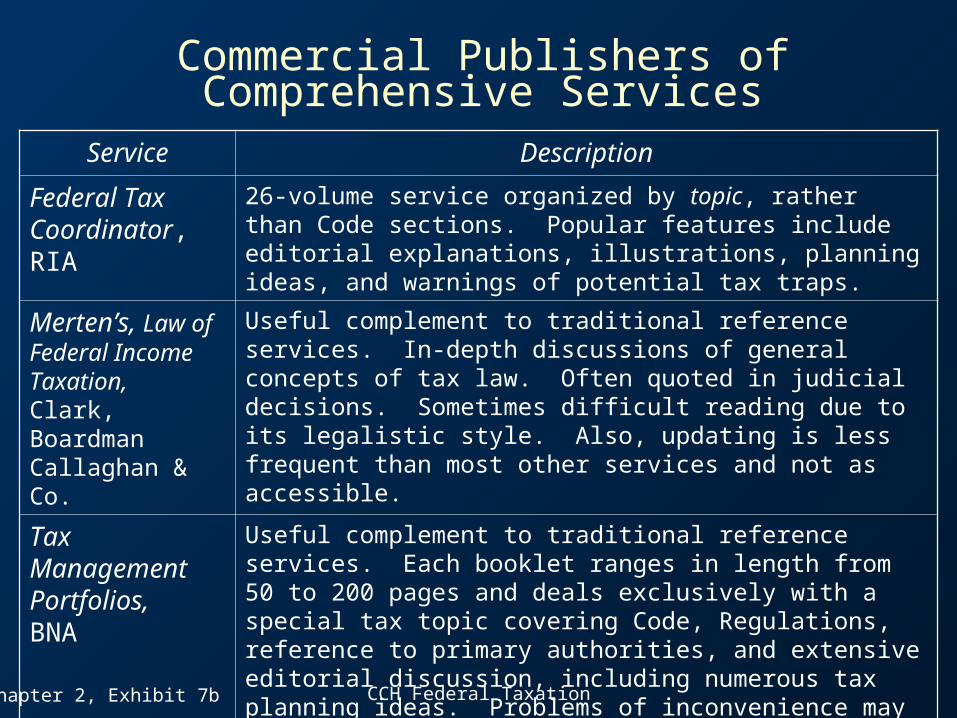

Federal Tax Coordinator, RIA

26-volume service organized by topic, rather than Code sections. Popular features include editorial explanations, illustrations, planning ideas, and warnings of potential tax traps.

Merten’s, Law of Federal Income Taxation, Clark, Boardman Callaghan & Co.

Useful complement to traditional reference services. In-depth discussions of general concepts of tax law. Often quoted in judicial decisions. Sometimes difficult reading due to its legalistic style. Also, updating is less frequent than most other services and not as accessible.

Tax Management Portfolios,BNA

Useful complement to traditional reference services. Each booklet ranges in length from 50 to 200 pages and deals exclusively with a special tax topic covering Code, Regulations, reference to primary authorities, and extensive editorial discussion, including numerous tax planning ideas. Problems of inconvenience may develop when there is no one portfolio squarely on point and the research effort requires reference to many portfolios. Updates are convenient though not extensive.

Chapter 2, Exhibit 7b

CCH Federal Taxation

Commercial Publishers of Comprehensive Services

Service Description

CCH ONLINE An electronic research service. Incorporates practitioner-oriented access methods to successfully located the desired tax information and to retrieve documents of special interest. Available in many different “libraries” addressing tax and nontax topics.

LEXIS/NEXIS, Reed Elsevier, Inc.

An electronic research service. LEXIS accesses federal statutes, regulations, IRS rulings, and judicial decisions. NEXIS contains the full text of over 500 publications.

WESTLAW, West Publishing Co.

An electronic research service. Provides much of the same data as Lexis. Available online or CD-ROM.

Chapter 2, Exhibit 7c

CCH Federal Taxation

Commercial Publishers of Judicial Decisions

Service Description

CCH Citator, CCH

Two-volume, loose-leaf reference service. Contains alphabetical listing of Tax Court (formerly Board of Tax Appeals, “BTA”) and federal court decisions since 1913. Indicates a paragraph reference where each case is digested in the Compilation Volumes of the Standard Federal Tax Reporter. Each listing outlines the judicial history of a selected case beginning with the highest court to have ruled on that issue.

Chapter 2, Exhibit 8a

CCH Federal Taxation

Commercial Publishers of Judicial Decisions

Service Description

Federal Tax Citator, RIA

Seven-volume citator service organized in a manner consistent with CCH Citator. Provides an alphabetical list of court cases followed by a descriptive legislative history of each case.

U.S. Tax Cases (USTC),CCH

Series of volumes that cover Supreme Court, Courts of Appeals, District Courts, and Court of Federal Claims cases since 1913.

Chapter 2, Exhibit 8b

CCH Federal Taxation

Commercial Publishers of Judicial Decisions

Service Description

American Federal Tax Reports (AFTR), RIA

Comparable to USTC above.

Tax Court Memorandum Decisions (TCM), CCH

Publishes memorandum decisions of the Tax Court.

TC Memorandum Decisions (TC Memo),RIA

Similar to TCM above.

Chapter 2, Exhibit 8c

CCH Federal Taxation

Penalties

Delinquency penalties Accuracy-related and

fraud penalties Negligence penalty Substantial

understatement of tax liability

Substantial valuation misstatement penalty

Substantial overstatement of pension liabilities

Estate of gift tax valuation understatements

Penalty for aiding understatement of tax liability

Civil fraud penalty Criminal fraud penalty Estimated taxes and

underpayment penalties Failure to make deposits of

taxes Tax preparer penalties

Chapter 2, Exhibit 16