CBRE Craiova Real Estate Report A4 Bleed 5 v3

18

CRAIOVA Real-Estate Overview CBRE RESEARCH Photo source: Craiova City Hall

-

Upload

hoangquynh -

Category

Documents

-

view

218 -

download

0

Transcript of CBRE Craiova Real Estate Report A4 Bleed 5 v3

CRAIOVAReal-Estate Overview

CBRE RESEARCH

Photo source: Craiova City Hall

Craiova is the Romania's 6th largest city and capital of Dolj County, situated in the Southern part of the country. Craiova is the most important city of Oltenia region.

With its population of 293,567, Craiova is one of the largest cities in Romania.

The city is an important educational centre: 20,088 students are attending one of the 120 specializations of the Craiova University. The university has a very good Faculty of Automation, Computers and Electronics.

FIGURE 1: CRAIOVA HIGHLIGHTS

Craiova, a secret resource of specialised talent

293,567

Student Population

20,088

6th

Largest City in Romania

30,000 sq m

GDP per Capita6,346

EUR

Retail Stock

CraiovaPopulation

704,097DoljPopulation

83,000 sq m

3CBRE - Craiova Real Estate 2015

CITY 2012 2013 2014 2015 (F) 2016 (F) 2017 (F)

Romania

Bucharest

Craiova

Iasi

338 EUR

496 EUR

307 EUR

308 EUR

357 EUR

531 EUR

318 EUR

329 EUR

373 EUR

555 EUR

332 EUR

346 EUR

397 EUR

581 EUR

347 EUR

362 EUR

422 EUR

603 EUR

360 EUR

375 EUR

443 EUR

626 EUR

372 EUR

387 EUR

FIGURE 2: AVERAGE MONTHLY NET INCOME EVOLUTION

CITY 2012 2013 2014 2015 (F) 2016 (F) 2017 (F)

Bucharest

Craiova

Iasi

15,774 EUR

5,160 EUR

5,070 EUR

16,717 EUR

6,022 EUR

5,388 EUR

17,530 EUR

6,800 EUR

6,024 EUR

18,660 EUR

6,800 EUR

6,024 EUR

19,696 EUR

7,232 EUR

6,376 EUR

20,917 EUR

7,750 EUR

6,809 EUR

FIGURE 3: GDP PER CAPITA

Source: National Committee of Prognosis

Craiova is a candidate to become European Capital of Culture in 2021 and in the run-up to the selection process several investment programs have been initiated. In 2007, Sibiu, another Romanian city was European Capital of Culture. The city benefited greatly from the investments tied to its successful candidacy. Most investments, including significant infrastructure upgrades have contributed to sustainable economic growth in the city in the years a�er it was European Capital of Culture.

Craiova is Romania's 6th largest city and capital of Dolj County, situated in the Southern part of the country. Craiova is the most important city of Oltenia region. The population of Craiova, Romania is 307,022 according to the National Institute of Statistics.

Craiova is an important educational center, with 20,088 students attending one of the 120 specializations of Craiova University every year. The university has a very good Faculty of Automation, Computers and Electronics, thus providing qualified workforce for the IT sector. Foreign languages, in particular English, Spanish and French are widely spoken in Craiova.

It is very important to notice that with the current plans of improving road infrastructure, Craiova has the right ingredients to become a viable destination. Available workforce,

University with technical specialisations, international airport, existing ring road and the know how in different industries are the ingredients that make Craiova attractive.

Apart from the possible automotive suppliers which could come in the region, Craiova could attract companies from the aeronautical segment thus taking advantage of local knowledge in this field.

Craiova can be reached easily by air: the city is served by Craiova Airport with scheduled flights to amongst others London, Barcelona Bologna, Milano, and Rome, but Bucharest and the Sibiu airports are not very far away either. The city has a good road connection with Bucharest (cc. three hours drive) and the Western border town of Arad, and there are plans for building a highway between Bucharest and Calafat: in this case, Craiova could be reached from Bucharest by car in less than two hours, connecting Romania border crossing with Serbia and Bulgaria. There is also train and bus connection to the city and daily trains with service from Craiova to: Bucharest (3 hours), Brasov (6 – 8 hours - via connecting service), Cluj-Napoca (8 – 10 hours - connecting service), Sibiu (4 – 7 hours), and Timisoara (5 hours).

Permanent Resident Population:• County: 704,097• Craiova: 293,567

COMPARISON WITH SIMILAR CITIES:

The unemployment in Craiova is 9% (versus 6.5% in Romania). Whilst the western part of Romania is increasingly facing labour shortages, investors are increasing looking to secondary cities such as Iasi and Craiova, where ample and cheaperlabour is still available.

4 CBRE - Craiova Real Estate 2015

Photo source: Boldir Victor Catalin

5CBRE - Craiova Real Estate 2015

OFFICE MARKET:

Romania holds its position as home to more offshore and nearshore centers than any other SEE country, thanks to offering a perfect balance between cost and quality, a flourishing technology hub and abundance of professional and multilingual labour pool.

CRAIOVA - A NEW DESTINATIONFOR OUTSOURCING COMPANIES

With competition for talent on the rise in cities like Bucharest, Timisoara and Cluj, which were initial targets of this sector, other university centers such as Craiova increasingly come into the spotlight.

Craiova is a talent pool generator for the southern part of the country, thanks to its higher education institutes. The city is a more affordable alternative for investors to either Bucharest or Timisoara, benefiting from good transport routes from all main business areas of the country.

The demand for office space in Craiova is generated especially by financial-banking sector, BPO (Business Process Offshoring), SSC (Shared Services Center) and automotive

CraiovaOffice Market

companies. Some of the most renowned companies present in Craiova are Star Storage, Telus International, IT Six Global Services, Iquest Technologies, Comdata, E-mag Pirelli, Netdania, Keppler Rominfo. Such tenants are looking for A and B class office schemes with a very good IT infrastructure.

The number of people employed in the IT&C companies is expected to increase in the next period; today almost 3,000 of employees are working in Craiova for this segment.

The Craiova Office Market has a relatively new history of around 5 years, with substantial development happening in the period 2010 – 2013. The modern office stock is estimated to be 30,000 sq m of class A and B, which is equivalent to almost 1% of the Bucharest office stock – with 14% of Bucharest’s population. The gross rentable area of the biggest office building is 7,000 sq m, while the majority of the office buildings have a rentable area which varies between 1,000 – 2,000 sq m. The development and growth of tenants in Craiova is curbed by the lack of sufficient Class A and B office stock.

For this year and next year there are over 7,000 sq m under construction in the

semi-central area all developed by local entrepreneurs/local private investors.In 2013 the local authorities delivered Centrul Multifunctional, with a rentable area of 12,600 sq m and 220 parking spaces. Centrul Multifunctional covers: exhibition area indoor and outdoor, a conference hall and office space. This year 3 other buildings will be delivered in the same project with a total rentable area of 4,200 sq m and 131 parking spaces.

The overall vacancy rate for class A and B in Craiova stands at around 18%, whereas the vacancy rate for class A office buildings is estimated at 6%.

Prime office asking rents in Craiova vary from 10 to 12 EUR/sq m/month for Grade A and stand between 6 to 10 EUR/sq m/month for Grade B office buildings.

2015 started off with more intense feedback from international companies looking to expand their current operations in Craiova, as well as new companies looking at opening SSC or BPO divisions. Qualified, professional and cheap labour, attractive state incentives for IT segment and real-estate costs are motivating business growth in this area and increasing investors’ interest.

6 CBRE - Craiova Real Estate 2015

1 Modern Office Stock (sq m)

Vacancy Rate

Headline rent – Class A

Headline rent – Class B

Service charge

2

3

4

5

30,000 sq m

18%

10 - 12 (EUR/ sq m/ mth)

6 - 10 (EUR/ sq m/ mth)

3 (EUR/ sq m/ mth)

FIGURE 4: LOCAL REAL ESTATE INDICATORS

Source: CBRE Research

Source: Malmo

7CBRE - Craiova Real Estate 2015

FIGURE 5: EXAMPLE OF EXISTING OFFICE BUILDINGS IN CRAIOVA

8 CBRE - Craiova Real Estate 2015

“The sixth largest city of Romania, Craiova, has the greatest development potential in top 10. With a strong industrial history and two universities, Craiova has a diversified and skilled workforce, but also a job market which is still unable to absorb it. Recently, local authorities put great efforts in developing the city infrastructure and creating facilities for investors. This policy is meant to reverse the unemployment trend, to retain the local talents, but also to exploit the workforce potential of the entire Oltenia region.”

George Paunescu, Branch ManagerManpower Romania

INDUSTRIAL HERITAGE

Oversized industrial areas were constructed during the communist period in Craiova municipality and Dolj County, nowadays 25% of urban land area is being occupied by industrial units.

A�er the year 1990, the transition to a market economy and the investors’ reluctance to develop projects inside the industrial areas has gradually led to the emergence of some derelict industrial areas. The brownfields areas with redundant infrastructure and buildings continue to be in place, currently the single reconversion worth mentioning is the Electroputere Parc Craiova set in a former production facility of Electroputere, which is a train engine and tram factory.

Previously Dolj County was the centre of railway and automotive industry, but also an important agricultural producer. Currently, these sectors continue to dominate the local economic image of this county, but not at the same scale. Secondary industries are: aeronautics, food and beverages, textile, chemical.

9CBRE - Craiova Real Estate 2015

INDUSTRIAL HERITAGE

Oversized industrial areas were constructed during the communist period in Craiova municipality and Dolj County, nowadays 25% of urban land area is being occupied by industrial units.

A�er the year 1990, the transition to a market economy and the investors’ reluctance to develop projects inside the industrial areas has gradually led to the emergence of some derelict industrial areas. The brownfields areas with redundant infrastructure and buildings continue to be in place, currently the single reconversion worth mentioning is the Electroputere Parc Craiova set in a former production facility of Electroputere, which is a train engine and tram factory.

Previously Dolj County was the centre of railway and automotive industry, but also an important agricultural producer. Currently, these sectors continue to dominate the local economic image of this county, but not at the same scale. Secondary industries are: aeronautics, food and beverages, textile, chemical.

CraiovaIndustrial

NOWADAYS INDUSTRIAL SECTOR

The largest industrial occupier in Dolj county is Ford, which manufactures engines in Craiova and assembles B-Max model. In 2014 the American car manufacturer contributed nearly 24% to the county’s car turnover. In total there are nearly 17,000 companies active in the county.

Ford had recently announced it might launch in the second half of 2017 a second assembly line in Craiova for the SUV EcoSport, a Craiova Industrial decision is expected to be taken in the coming months.

They will take into account the highway infrastructure improvements and also a possible new state aid scheme. The automotive suppliers present in Dolj county are: Automotive Prod Service, BBB Fasteners, Cooper Standard, Electrical Mechanical Wirings, Faurecia, Craiova, H&L, Hella Romania, Craiova, Johnson Controls Romania, Kautex Textron, Kirchhoff Automotive, Magna, Micar, Siemens-Yazaki, Yazaki Caracal. Railway industry in Craiova tradition is continued today by Sofronic, a company controlled by Romanian entrepreneurs

who produce locomotives and electric trains.

As seen before, one of Dolj’s county major problems is the lack of road connectivity, this is why Ford is not producing at full capacity at the moment and automotive suppliers are not too eager to invest here. The only few suppliers present here are producing exclusively for Ford, they have located their production facilities inside Ford’s platform by refurbishing some of the buildings there. They chose not to invest into a greenfield facility, but took into consideration a short term, in sincronicity with the strategy of the American company. Considering the lack of interest from manufacturers, major industrial developers were not eager to invest here.

The only existing private industrial park is Cassia Park Craiova, a small B class distribution platform where small companies based their distribution or storage centres. Dolj county council decided in 2004 to create a state owned industrial park which could offer SME and major companies the right and attractive conditions for building their own facilities. Parc Industrial Craiova is now being fully occupied.

10 CBRE - Craiova Real Estate 2015

No Industrial Park Developer/Owner

1 Modern Industrial Stock-Developer led

Vacancy Rate

Prime headline rent

Office space rent

Service charge

2,400 sq m

0%

4 (EUR/ sq m/ mth)

6 (EUR/ sq m/ mth)

0.5 (EUR/ sq m/ mth)

2

3

4

5

FIGURE 6: LOCAL REAL ESTATE INDICATORS

Source: CBRE Research

Source: 4Tuning

11CBRE - Craiova Real Estate 2015

Photo source: WDP Romania

FIGURE 7: MAJOR INDUSTRIAL PARKS IN CRAIOVA

CBRE - Craiova Real Estate 201512

„When planning a new production facility in Europe, Ford selected Craiova mainly because of the availability of a qualified labour force with a long tradition of automotive production (initially Oltcit was produced in the city later Daewoo) at very competitive terms compared to other European markets.

Our choice has proven to be the right one as our Craiova factory is very efficient and competitive in Europe. This major proven competitiveness together with the availability of a competent and low cost labour market offers major opportunities for growing in the near future by adding new product and related investment, generating additional supplier investment and other indirect business investment in the Craiova region.’’

Jan Gijsen,President Ford Romania

13CBRE - Craiova Real Estate 2015

RETAIL MARKET

Although Craiova is the largest city in Southern Romania not taking into account Bucharest, the modern retail was until the recent years represented mainly by big box units located throughout the city. The development of the retail sector in Craiova followed the same pattern as in other similar cities with approx. 300,000 inhabitants with big box retail first and shopping centers opened a�erwards.

HIGH-STREET

A larger part of the on street retail stock is located at the ground floor of old historical buildings located mainly in the city center (bordered in the North by A. I. Cuza Street, in East by Aries Street, in the South by Mihail Kogalniceanu Street and in the West by Unirii Avenue. Other important arteries in terms of on street retailing are Bucuresti and Severinului avenues. The refurbishment of the old city center is almost completed and that is likely to boost the high street retail especially on Lipscani and Romania Muncitoare streets as well as on the neighbouring pedestrian streets.

SHOPPING CENTERS

The local market includes various types of shopping centers: from one raised back in 1975 and refurbished in 2002 - Mercur, located in the city center, to a hypermarket-led scheme - Auchan

CraiovaRetail

Craiovita, located in the Western part of the city (2006) and a modern scheme - Electroputere Parc (approx. 70,000 sq m, late 2011), located in the Central-Eastern part of the city. The total modern shopping center retail stock in Craiova is of only 83,000 sq m, resulting some 300 sq m / 1,000 inhabitants lower even than in Brasov that has some 460 sq m / 1,000 inhabi-tants. The occupancy rate is high (over 95%) with only two operational schemes in Craiova. The rents are in range with the levels registered for similar cities in size and potential.

Among the most important retailers present in Craiova we can name: Zara, Stradivarius, Bershka, Pull&Bear, Deichmann, C&A, LC Waikiki, Flanco, Domo, Media Glaxy, Decathlon, dm,

Douglas, H&M, Intersport, McDonald’s, KFC. Food retailing is well represented: Auchan, Billa, Lidl, Penny Market, Kaufland, Carrefour Market. DIY sector: Praktiker, Dedeman, Leroy Merlin.

OUTLOOK

Due to its size and location Craiova has the potential to attract new retails and investors. During the booming years two other centers were announced in the city (Westgate and Adora Mall). Both schemes were abandoned when Auchan decided to choose for Electroputere Parc. As Electroputere Parc is well located and has a dominant size combined with extension potential, it is unlikely that a new shopping center development will materialize in the near future.

0

200

400

600

800

1,000

1,200

Suce

ava

Pite

sti

Sibi

u

Targ

u M

ures

Con

stan

ta

Ploi

esti

Ora

dea

Buch

ares

t

Iasi

Ara

d

Bras

ov

Clu

j Nap

oca

Cra

iova

Brai

la

Tim

isoa

ra

Sq m

/ 1

,000

inha

bita

nts

FIGURE 8: RETAIL DENSITY PER CITY

14 CBRE - Craiova Real Estate 2015

No Retail Scheme GLA (sq m) Type Owner

Electroputere Parc

Auchan Craiovita

Mercur

1

2

3

70,000

13,000

20,000

Shopping Center

Shopping Center

Shopping Center

K&S Development

Immochan

Local businessmen

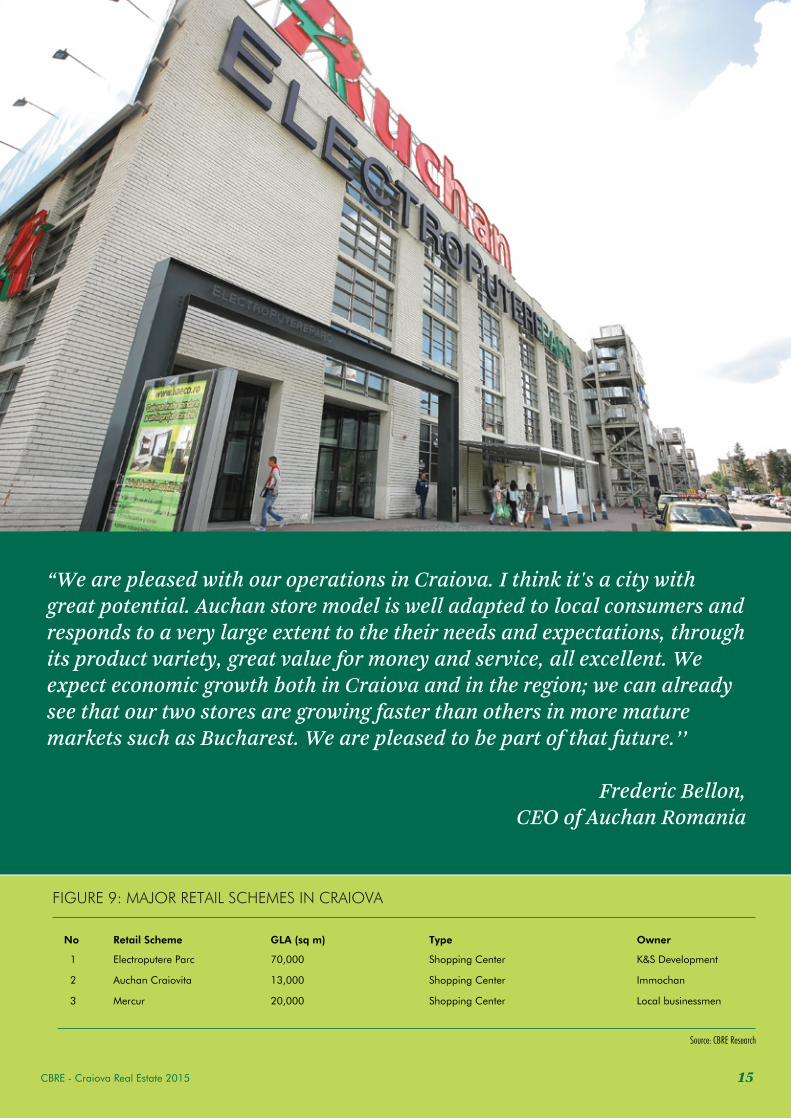

FIGURE 9: MAJOR RETAIL SCHEMES IN CRAIOVA

Source: CBRE Research

Source: electroputeremall.ro

“We are pleased with our operations in Craiova. I think it's a city with great potential. Auchan store model is well adapted to local consumers and responds to a very large extent to the their needs and expectations, through its product variety, great value for money and service, all excellent. We expect economic growth both in Craiova and in the region; we can already see that our two stores are growing faster than others in more mature markets such as Bucharest. We are pleased to be part of that future.’’

Frederic Bellon, CEO of Auchan Romania

15CBRE - Craiova Real Estate 2015

FIGURE 10: EXISTING RETAIL SCHEMES IN CRAIOVA

16 CBRE - Craiova Real Estate 2015

‘‘Electroputere Park is the shopping destination in Craiova with an existing rentable area of almost 70,000 sq m that is currently expanding successively with further 5,000 sq m and 25,000 sq m. The expansion is the result of the highly performant business of the center so far, of the request from tenants to either increase the sales area or to enter the center and of the request from consumers for more retail offer. We are happy to say that Electroputere has a regional span, attracting people from all over the county. Electroputere hosts more than one million people every month.’’

Steven Van Den Bossche, Managing Partner BelRom

17CBRE - Craiova Real Estate 2015

Source: electroputeremall.ro

INDUSTRIALMETHODOLOGY & DEFINITIONS

Prime headline rent (in Euro per sq m) represents the top open-market tier of rent that could be expected for a unit of standard size commensurate with demand in each location, of highest quality and specification and in the best location in a market at the survey date. For the purposes of this report, a unit of standard size is assumed to be around 2,000 sq m GLA.

Vacancy Rate - (in sq m) represents the total net lettable (or rentable) floor space in existing properties, which is physically vacant and being actively marketed at the survey date. Prime headline rent (in Euro per sq m) represents the top open-market tier of rent that could be expected for a unit of

standard size commensurate with demand in each location, of highest quality and specification and in the best location in a market at the survey date. For the purposes of this report, a unit of standard size is assumed to be around 2,000 sq m GLA. Effective rent – an average rent over the whole lease period which includes tenant’s incentives.

Build-to-suit (BTS) – a non-standard warehouse or industrial scheme designed according to specific tenant’s requirements regarding size, location and building standards. The design is based on the client’s technology process. The projects are usually dedicated for one tenant, newly built or a�er general refurbishments. BTS

projects are more and more popular, especially for production companies. Clients preferring BTS investments over constructing their own buildings, limit the risk by choosing an experienced developer, shorten the time necessary for the development process and reduce the development cost by using the developer’s resources. Lease agreements are more advantageous than the construction of a company’s own facilities, mainly because such projects do not require the involvement of their own capital and provide flexibility for future extension or relocation.

OFFICEMETHODOLOGY & DEFINITIONS

Prime Rent - represents the top open-market tier of rent that could be expected for a unit of standard size (commensurate with demand in each location), of the highest quality and specification and in the best location in a market at the survey date. The Prime Rent should reflect the level at which relevant transactions are being completed in the market at the time, but need not be exactly identical to any of them, particularly if deal flow is very limited or made up of unusual one-off deals. If there are no relevant transactions during the survey period, the quoted figure will be more hypothetical, based on an expert opinion of market conditions.

Vacancy Rate - represents the percentage ratio of total vacant space to stock.

Total Stock – represents the total completed space (occupied and vacant) in the private and public sector at the survey date. Includes owner occupied space.

Business Process Outsourcing (BPO) – a specialized organization that provides specific business functions (or processes), usually non-production ones to third parties.

Shared Service Centre (SSC) – a separated part of an enterprise that

provides a service to an organization or group where that service had previously been found in more than one part of the organization or group. The funding and resourcing of the service is shared and the providing department effectively becomes an internal service provider.

Knowledge Process Outsourcing (KPO) – a form of outsourcing, in which knowledge-related and information-related work is carried out by workers in a different company or by a subsidiary of the same organization, which may be in the same country or in an offshore location to save cost. This typically involves high-value work carried out by highly skilled staff.

18 CBRE - Craiova Real Estate 2015

CBRERazvan IorguManaging Director+40 21 313 10 [email protected]

Gjis KlompHead of Capital Markets+40 21 313 10 [email protected]

Contacts

Disclaimer: Information contained herein, including projections, has been obtained from sources believed to be reliable. While we do not doubt its accuracy, we have not verified it and make no guarantee, warranty or representation about it. It is your responsibility to confirm independently its accuracy and completeness. This information is presented exclusively for use by CBRE clients and professionals and all rights to the material are reserved and cannot be repro-duced without prior written permission of CBRE.

Daniela Gavril Research Analystt: +40 21 313 10 20e: [email protected]

Tudor MunteanResearch Analyst t: +40 21 313 10 20e: [email protected]

Laura Dumea-BenczeHead of Research Romania & CEE Research Analystt: +40 21 313 10 20e: [email protected]

Walter WolflerSenior DirectorHead of Retail CEE CBRE GmbHt: +43 1 533 40 80 97e: [email protected]

Joerg KreindlSenior DirectorHead of Industrial CEEt: +48 22 544 8006e: [email protected]

Mike AtwellSenior DirectorHead of Capital Markets CEEt: +48 22 544 8070e: [email protected]

CBRE - Craiova Real Estate 201520