Casualty & Theft Losses

28

Transcript of Casualty & Theft Losses

Anita Robinson has been in the accounting and tax preparation business for over 20 years. AnEnrolled Agent since 1996 and Advanced Certified QuickBooks Pro Advisor since 2007. Anita hasbeen a member of Intuit’s Advisor & Customer Council and has served as a Writing CommitteeMember for the Oregon Licensed Tax Consultants, Oregon Licensed Tax Preparers, as well as,the IRS Enrolled Agent exams.

Anita has taught tax classes for several local and nationwide organizations. Since January of2012 Anita has been organizing a networking group for accounting and tax professionals in theVancouver, WA area. These meetings encourage education on tax and accounting topics, aswell as, practice management and data security issues.

Casualty & Theft Losses

Course Description

This course will review current tax law regarding casualty and theft losses. This course will showexamples of how to calculate different types of casualty losses.

Learning Objectives

Be able to understand when and how to deduct casualty and theft losses.

Disclaimer

Seminar materials are intended to stimulate thought and discussion and to provide attendees withuseful ideas and guidance in the areas of federal taxation. These materials, as well as, the commentsof the instructor do not constitute and should not be treated as tax advice regarding the use of anyparticular tax procedure, tax planning technique, or suggestion or any consequences associated withthem. This information is provided for educational purposes only.

Although the author has made every effort to ensure the accuracy of the materials, neither the author,nor the presenter assumes any responsibility for any individual's reliance on the written or oralinformation presented during the presentation. Each attendee should verify independently allstatements made in the materials and during the seminar presentation before applying them to aparticular fact pattern and should determine independently the tax and other consequences of usingany particular technique or suggestion before recommending the same to a client or implementing the

same on a client's or on his or her own behalf.

These materials are the property of Anita Robinson and may not be used orcopied without her express written permission.2021

Table of Contents

I. Casualty & Theft Losses. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

A. Definitions. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

B. Deductible Losses. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

C. Nondeductible Losses. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

D. Disaster Losses. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

E. Losses on Deposits. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

F. Insurance Reimbursements. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

II. Reporting of Losses. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

A. Personal Use Property. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

B. Business & Income Producing Property. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

C. Theft Losses for Ponzi Schemes. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

D. Timing. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

III. Calculation of Losses. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

A. Reduction in FMV. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

B. Appraisals. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

IV. Casualty Gains. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

A. Gains on Casualty Losses. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

B. Postponing Gain on Casualty Losses. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

V. Examples. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

VI. Reconstruction of records. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

VII.References. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

These materials are accurate at the time of writing. Congress may make changes that might

invalidate these materials. Be sure to check irs.gov for the most current information.

I. Casualty and Theft Losses

A. Definitions

1. A casualty loss is damage, destruction or loss of property that results from anidentifiable event such as a

a. Hurricane

b. Fire

c. Flood

d. Storm, including hurricanes, tornadoes and straight‐line winds

e. Accident

f. Mine cave‐in

g. Shipwreck

h. Sonic boom

i. Terrorist attack

j. Vandalism

k. Volcanic eruption

2. The event must be

a. Sudden,

b. Unexpected, or

c. Unusual

3. Theft Losses occur when something is taken with the intent to deprive theowner of it. It must be illegal under state or federal laws, and done with criminalintent. A conviction is not necessary. Theft includes taking money or property byany of the following:

a. Blackmail (demanding payment or another benefit from someone in returnfor not revealing compromising or damaging information about them)

b. Burglary (entry into a building illegally with intent to commit a crime,especially theft)

c. Embezzlement (theft or misappropriation of funds placed in one's trust orbelonging to one's employer)

Page 4 of 28

d. Extortion (the practice of obtaining something, especially money, throughforce or threats)

e. Kidnapping for ransom

f. Larceny (Theft and larceny are related terms, but not identical. Generally,theft is an umbrella term that includes all types of stealing activity, while, toconstitute larceny, the theft must be of personal property)

g. Robbery (Burglary occurs when someone “intentionally enters [a place]without the consent of the person in lawful possession and with intent tosteal or commit a felony.” Robbery occurs when someone “takes propertyfrom the person or presence of the owner by either… using force…or bythreatening the imminent use of force)

h. Fraud or misrepresentation

4. There are three types of casualty losses:

a. Federal Casualty Losses apply to the loss of personal‐use property thathappened due to a federally‐declared disaster. The loss must occur in a statethat receives a federal disaster declaration.

b. A Disaster loss is a loss that occurred in a federally‐declared disaster areaand the area is eligible for federal assistance. The loss must occur in a countythat is eligible for public or individual assistance. Disaster losses may beclaimed for personal‐use and income‐producing property. Losses may beclaimed by individuals, C‐corporations, S‐corporations and partnerships.

c. A Qualified Disaster loss is a loss of personal‐use property in an area thatwas declared as a major disaster by the President under §401 of the StaffordAct (Instructions to Form 4684, Rev 2/2020).

B. For tax years beginning after 12/31/2017 and ending before 1/1/2026 a personalcasualty loss is only deductible if it occurred in a qualified federally‐declareddisaster area. Federally declared disaster areas that occurred January 1, 2018through January 19, 2020 are all qualified disaster areas. The current listing offederally declared disaster areas can be found at https://www.fema.gov/disasters

1. The taxpayer must file a timely insurance claim to deduct any losses.

2. A personal casualty loss that did not occur in a federally declared disaster areacan offset any gain from a personal casualty.

Page 5 of 28

3. Generally, NOLs apply to businesses only, however, a casualty loss can result inan NOL for an individual without a business. This NOL must be taken back fiveyears for any NOL arising in tax years 2018 through 2020.

C. Nondeductible Losses

1. In some circumstances the taxpayer cannot deduct a loss

a. Money or property that was lost or misplaced

b. Breakage of items under normal circumstances, such as, china, glassware,furniture, etc.

c. Damage from willfully set fires

d. Car accident damage due to willful negligence

e. Progressive damage to property caused by termites or other insects ordisease.

f. A decline in value of stock due to accounting or other illegal misconduct ofthe officers or directors of the company issuing the stock. This may bedeductible as a capital loss if the stock is sold at a loss or it becomesworthless.

2. Related expenses such as treatment of injuries or rental car are not deductible.Expenses for protection against future casualties are not deductible. Theseshould be capitalized as improvements. For example the cost of a levee to stopflooding is not deductible, it adds to the basis of the property.

3. Victims of fraudulent schemes, such as Ponzi schemes may deduct a theft loss.

Page 6 of 28

D. Deductible Disaster losses are losses that occur in an area that the president of theUnited States has declared as a federally‐declared disaster area. Disaster losses maybe claimed for personal‐use property, as well as business and income‐producingproperty.

1. The disaster year is either the year in which the loss occurred or a later year, ifthere is a reasonable chance of recovery and the taxpayer is reimbursed in alater year.

Example

a. A taxpayer’s vehicle was destroyed in a fire in 2019. The taxpayer filed aclaim with his insurance company and was reimbursed for a portion of thevalue of the vehicle in 2020. The loss year is 2020 and he can deduct the lossin 2020 or make an election to deduct the loss in the preceding tax year.

b. Taxpayers have until the due date of the return, including extension to makethe election to deduct the loss in the prior year.

c. This election may be revoked within 90 days of filing.

2. If the taxpayer’s home in a disaster area has to be moved or torn down becauseit is no longer safe to use, the loss in value is a disaster loss. The governmentorder to move or tear down the residence must be issued within 120 days of thedisaster declaration. The fair market value of the home before the moving ortearing down is considered the fair market value after the casualty.

3. In the case of a qualified disaster loss the $100 limit per casualty is increased to$500 and the 10% of AGI limitation does not apply. The standard deduction isincreased by the loss.

E. Losses on Deposits occur when a financial institution becomes insolvent or goesbankrupt. For tax years 2018 through 2025 these losses are not deductible, unlessthey can offset personal casualty gains. A loss on deposits may be deducted as anon‐business bad debt, see IRS Publication 547, Casualties, Disasters, and Thefts, formore information.

1. To deduct a non‐business bad debt the taxpayer must wait until the year theactual loss is determined. A non‐business bad debt is reported on Form 8949 andthen flows to Schedule D. See also Publication 525, Taxable and NontaxableIncome, on how to treat recoveries.

Page 7 of 28

F. Any insurance reimbursementmust be subtracted from the loss, even if thereimbursement is not received until after the year of the loss.

1. If the taxpayer is insured for the property, but does not file a claim, he cannotdeduct the full amount of the loss. Any potential reimbursement must besubtracted from the loss.

2. Funds received from an employer’s emergency disaster fund reduce the loss byany amount that is used to replace and/or repair the lost property.

3. Cash gifts do not reduce the casualty loss. There are no restriction on what giftscan be used for.

4. Insurance reimbursements for living expenses do not reduce the casualty loss ifthe taxpayer’s main home is lost or if government authorities do not allowaccess to the home due to a casualty or threat of one. In the case that insurancereimbursements exceed the temporary increase in living expenses, then theexcess is included in income on Schedule 1, line 8, Additional Income andAdjustments to Income.

Example:

a. A taxpayer’s home was destroyed and is now being rebuilt. During that timethe taxpayer lived in a hotel and had to eat out. Total living expenses for themonth were $1,600. Normally the taxpayer spends only $750 per month. Theinsurance company reimbursed him $1,200 for each month that the taxpayercould not return to his home.

1) Insurance reimbursement. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $1,200

2) Actual expenses. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $1,600

3) Normal living expenses. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 750

4) Temporary increase in living expenses. . . . . . . . . . . . . . . . . . . . . $ 850

5) Amount includible in income (diff between 1) & 4)). . . . . . . . . $ 350

b. Taxable insurance reimbursements for living expenses are included in theyear the taxpayer is able to use his home again or the year thereimbursement is received, whichever is later.

5. Disaster relief in the form of food, medical supplies and other assistance do notreduce the casualty loss, unless it is a replacement for lost or destroyed property

6. Disaster relief grants under the Stafford Act are not taxable income for amountsused to cover necessary expenses, such as housing, medical, transportation orfuneral expenses.

Page 8 of 28

7. Disaster relief grants to businesses under state programs are taxable income.The business may postpone any gain from the grant if qualifying property hasbeen replaced in a timely manner. Rev. Rul. 2005‐46. The replacement periodbegins on the date the property was destroyed or stolen and ends two yearsafter the close of the first tax year in which a gain is realized.

Example:

a. While on vacation several valuable items, that originally cost $2,500, werestolen from the taxpayer’s property. The theft was discovered upon hisreturn on July 7, 2019. The insurance company finally settled the claim onJanuary 22, 2020 and paid $3,000. The gain of $500 is realized in 2020, so thetaxpayer has until December 31, 2022 to replace the property.

II. Reporting of Losses

A. Casualty and theft losses for non‐business property are reported on Form 4684,Section A. The loss for each item equals the lesser of the taxpayer’s basis in theproperty, or the reduction in fair market value due to the casualty minus anyinsurance reimbursement that the taxpayer could have received.

1. The loss is calculated separately for each item

2. Subtract $100 per event

3. Subtract 10% of AGI from the total of all events

4. Report the net loss on Schedule A line 15

5. Report gains on Schedule D line 4 or line 11. Gains from a casualty loss occurwhen the insurance reimbursement exceeds the casualty loss.

B. Casualty and theft losses for business and income‐producing property is reportedon Form 4684, Section B, Part I. (Income producing property is property that is heldfor investment, such as stocks, bonds, precious metals, vacant land, works of art,etc.) The loss is the lesser of the taxpayer’s adjusted basis (cost less depreciation) orthe reduction in FMV due to the casualty minus any insurance reimbursementreceived or expected to receive.

1. The loss is calculated separately for each item, without the $100 or 10% of AGIreductions.

2. If the property is stolen or completely destroyed the loss is calculated bysubtracting the salvage value and insurance reimbursement from the adjustedbasis of the property.

Page 9 of 28

3. Property that has been held for more than one year may have depreciationrecapture that is reported as ordinary income and calculated on Form 4797.

C. Theft losses due to Ponzi‐type investment schemes are reported on Form 4684,Section C. There are two methods to deduct these types of losses.

1. The safe harbor method, is reported in Section C and then transferred to SectionB, Part II. Rev Proc 2009‐20 has more information on the safe harbor method.The entire loss is claimed in Section C, however, only 95% of the loss is deductedif the taxpayer does not pursue potential recovery. The taxpayer may deduct75% of the loss if he intends to pursue recovery. By deducting less than the fullamount of the loss any recovery in a later year will not be taxable.

2. If the taxpayer chooses not to use the safe‐harbor method or does not qualify touse it, the theft loss is reported in Section B. The entire amount of the loss willbe claimed by filling out lines 19 to 39. The loss for either method will transfer toSchedule A, line 16.

D. Form 4684, Section D is used to elect to deduct a federally‐declared disaster loss ina preceding year. The election to claim a loss in the year immediately preceding theloss must be made within six months of the due date of the original return for theloss year, without extensions. For example, a calendar year taxpayer has untilOctober 15, 2021 to make the election for a 2020 disaster loss.

1. Section D, Part I is the election statement and Section D, Part II is where therevocation of the election is made.

2. Losses are deducted either in the tax year they occurred or the tax year that anyreimbursement can be determined, or the taxpayer knows that he will notreceive any further reimbursement. Reg §1.165‐1(d)

Page 10 of 28

III. Calculation of Losses

A. In order to figure a deductible loss the taxpayer needs to

1. determine the adjusted basis in the property before the loss,

2. determine the decrease in FMV due to the casualty, and

3. subtract any insurance reimbursement from the smaller of the adjusted basis orthe decrease in FMV.

B. Generally, an appraisal is needed to determine the reduction in FMV. In certainsituations the taxpayer may use safe harbor methods instead. (Rev Proc 2018‐08)

1. For casualty losses of $20,000 or less the taxpayer may obtain repair estimatesfrom at least two contractors and use the lesser of the two.

2. The taxpayer may obtain a written good‐faith estimate if the repair cost is$5,000 or less.

3. The taxpayer may use the report of estimated loss that the insurance companyprepared.

4. For federally‐declared disasters, the taxpayer may use the contract price for anyrepairs if he has a signed and binding contract.

5. For federally‐declared disasters, an appraisal to obtain a loan for federal fundsmay be used.

6. Factors to consider in the calculation of the reduction in FMV can include thecost of cleaning up and making repairs if

a. the repairs are required to restore the property to the condition it was inbefore the casualty, and repairs are actually made,

b. the repairs are not excessive and are only for damages caused by thecasualty, and

c. the value of the property is not increased after making the repairs.

d. Restoration of landscaping to its original condition may indicate a decrease inFMV. The loss would be for removing damaged vegetation and replacing itwith new plants.

Page 11 of 28

7. Some costs cannot be used in the calculation for determining the reduction infair market value for personal use property. Some of these items may bedeductible as an expenses for business use and/or income‐producing property.

a. Expenses for security to protect from looting,

b. medical treatment, rental cars, temporary housing,

c. the actual replacement cost for destroyed items,

d. any sentimental value these items might have,

e. a decline in market value in the area due to the casualty, and

f. the cost of appraisals.

IV. Casualty Gains

A. A taxpayer may have a gain on a casualty if the reimbursement is more than theadjusted basis in the destroyed property (IRC §1033). The gain is computed bysubtracting the amount of the reimbursement received, from the adjusted basis inthe property at the time of the casualty or theft. If the result is a positive number,the taxpayer has a gain.

1. There is no gain on any insurance reimbursements for unscheduled personalproperty that was part of the contents of the home.

a. Unscheduled personal property includes belongings that may be covered byyour standard personal property coverage, but that have not beenspecifically itemized on your policy.

b. Scheduled personal property is a supplemental insurance policy that extendscoverage beyond the standard protection provided in a homeowner’sinsurance policy.

2. A casualty gain will offset any casualty losses, whether or not it is related to afederally‐declared casualty.

B. Reporting of a casualty gain may be postponed if

1. the taxpayer receives property that is similar to the destroyed property asreimbursement, or

2. the taxpayer opts to postpone reporting the gain until he has purchased similarproperty within two (2) years after the end of the first year in which a gain isrealized and within four (4) years for a gain on a personal residence. Example:

A taxpayer’s main home and its contents were completely destroyed in 2019by a wildfire in a federally‐declared disaster area. In 2019 he received

Page 12 of 28

insurance proceeds of $200,000 for the residence, $25,000 for personalproperty, $5,000 for jewelry and $10,000 for several race bikes that werekept in the garage. The jewelry and the race bikes were scheduled propertyon the insurance policy. No gain is recognized on the $25,000 reimbursementfor unscheduled property. The home, jewelry and bikes are considered oneitem of property. Replacement property can include scheduled orunscheduled property and a home. Any gain is postponed if at least $215,000of replacement property is purchased by the end of 2023. (200,000 + 25,000+ 5,000 + 10,000 = 240,000 ‐ 25,000 = 215,000)

3. Gain cannot be postponed if the replacement property is acquired from a relatedperson. This applies to

a. C‐corporations

b. Partnerships that are owned more than 50% by a C‐corporation

c. Any other taxpayer who realized more than $100,000 of gain on all destroyedor stolen properties during the year.

4. The election to postpone the gain is made at the entity level.

a. A statement must be attached to the return stating the following:

i. Date and details of the casualty

ii. Reimbursement received

iii. Gain calculation

b. If the replacement property is acquired before filing the tax return for theyear of the gain, the statement should also include the following:

i. Description of the replacement property

ii. Amount of the postponed gain

iii. Basis adjustment to the replacement property

iv. Any remaining gain that is reported as income

Page 13 of 28

V. Examples

Taxpayer is single, has wages of $80,000 and qualified dividend income of $1,000 andtakes the standard deduction

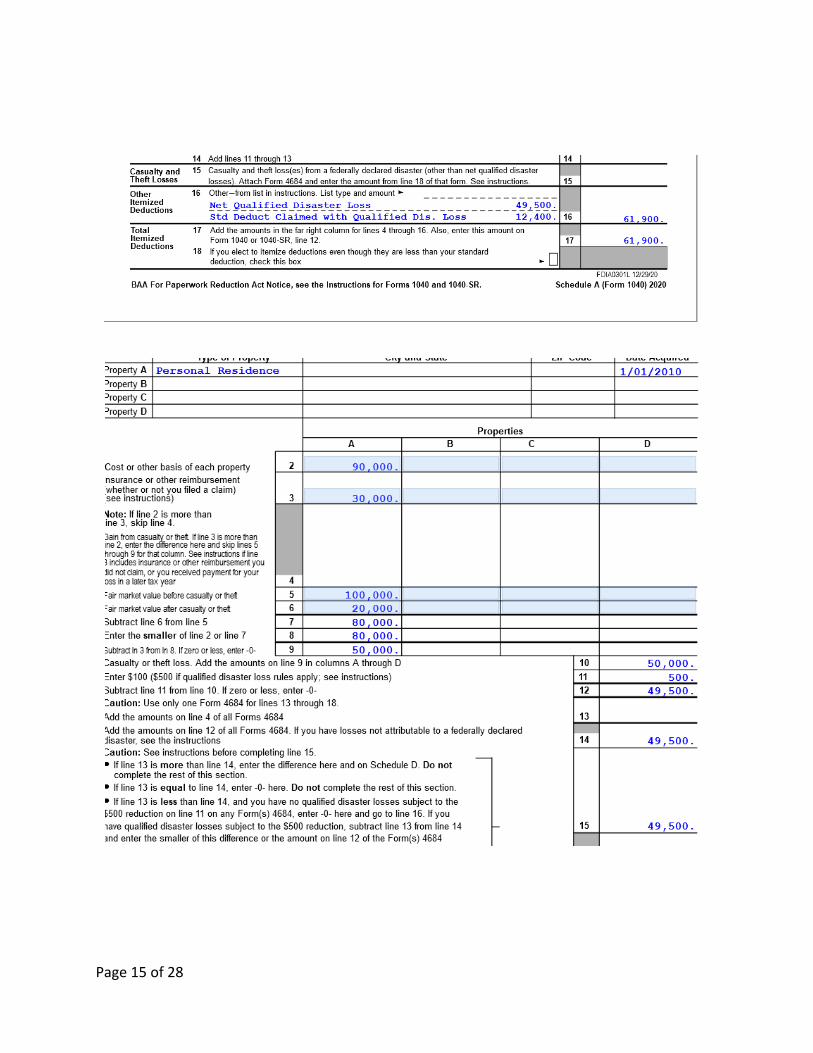

1. Example 1

a. Taxpayer’s personal residence is destroyed by a forest fire in a qualified disasterarea. Cost basis is $90,000 and he received $30,000 insurance reimbursement.

b. The FMV before the casualty was $100,000 and after the fire it was $20,000.

c. The reduction in FMV is $80,000.

Page 14 of 28

Page 15 of 28

1. Example 2

a. Income producing property with a cost of $90,000 and accumulated depreciationof $32682. Net adjusted basis is $57,318. Land value is $20,000. Taxpayerreceived insurance reimbursement of $30,000

b. FMV before the fire is $100,000

c. FMV after the fire is $20,000

d. The reduction in FMV is $30,000

Page 16 of 28

Page 17 of 28

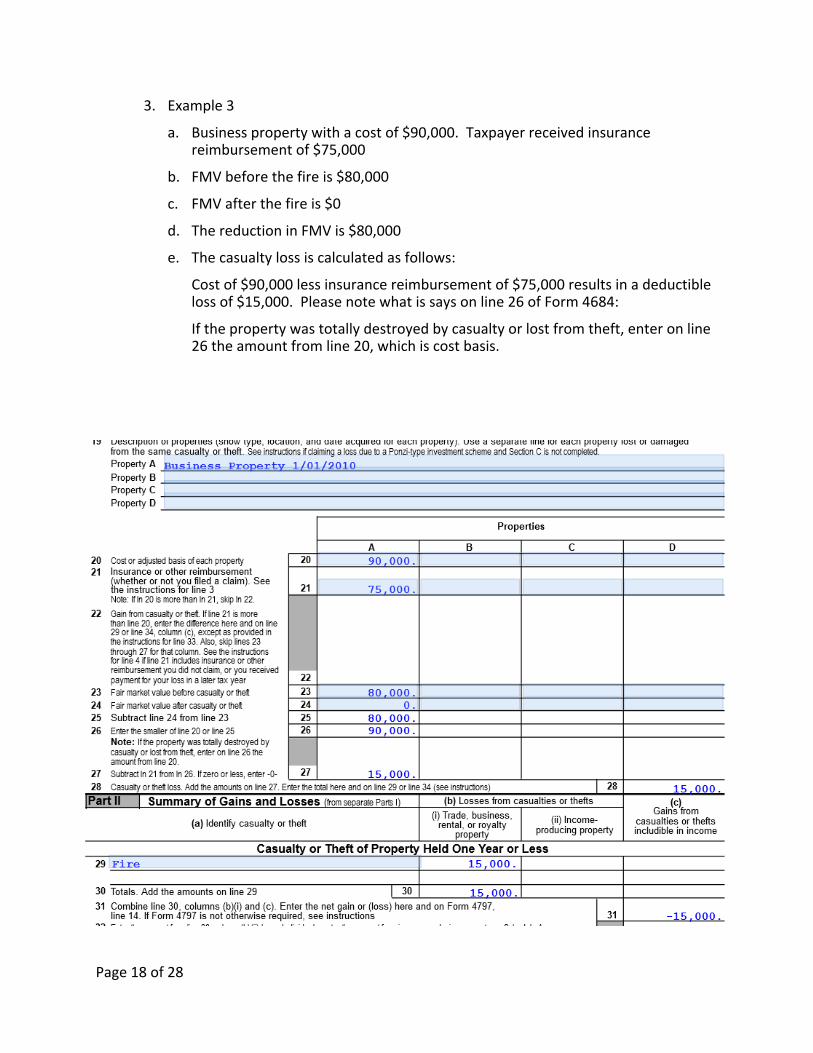

3. Example 3

a. Business property with a cost of $90,000. Taxpayer received insurancereimbursement of $75,000

b. FMV before the fire is $80,000

c. FMV after the fire is $0

d. The reduction in FMV is $80,000

e. The casualty loss is calculated as follows:

Cost of $90,000 less insurance reimbursement of $75,000 results in a deductibleloss of $15,000. Please note what is says on line 26 of Form 4684:

If the property was totally destroyed by casualty or lost from theft, enter on line26 the amount from line 20, which is cost basis.

Page 18 of 28

Page 19 of 28

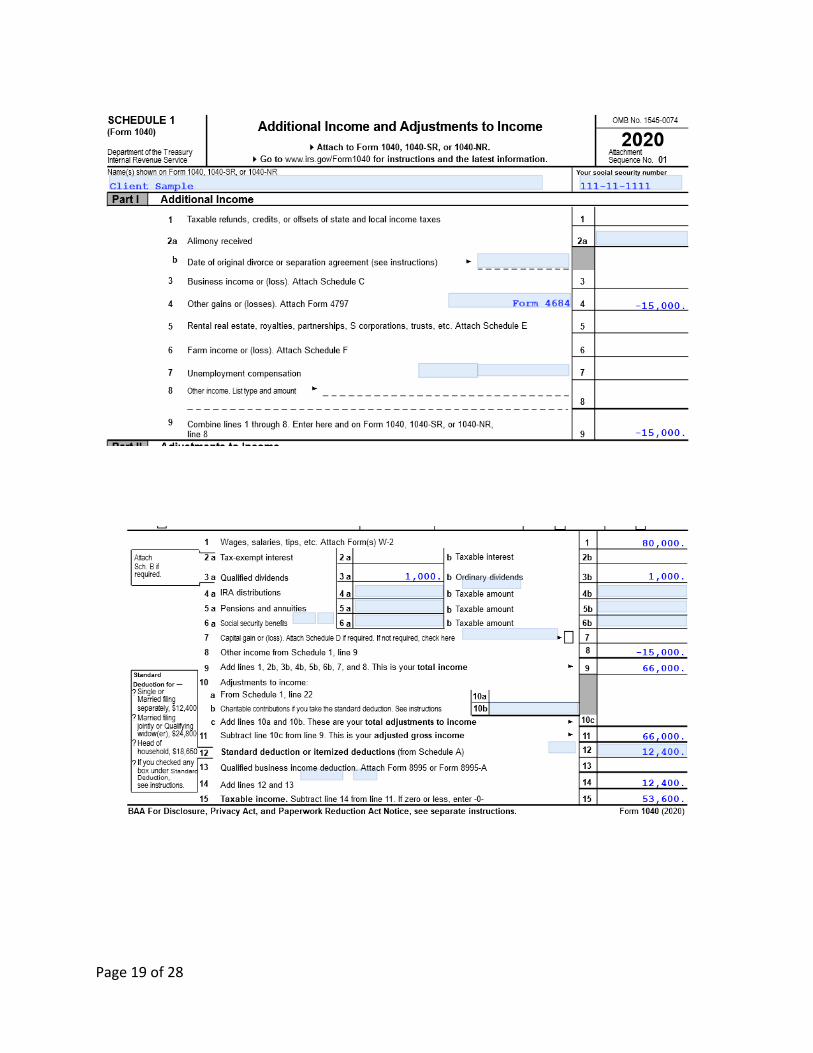

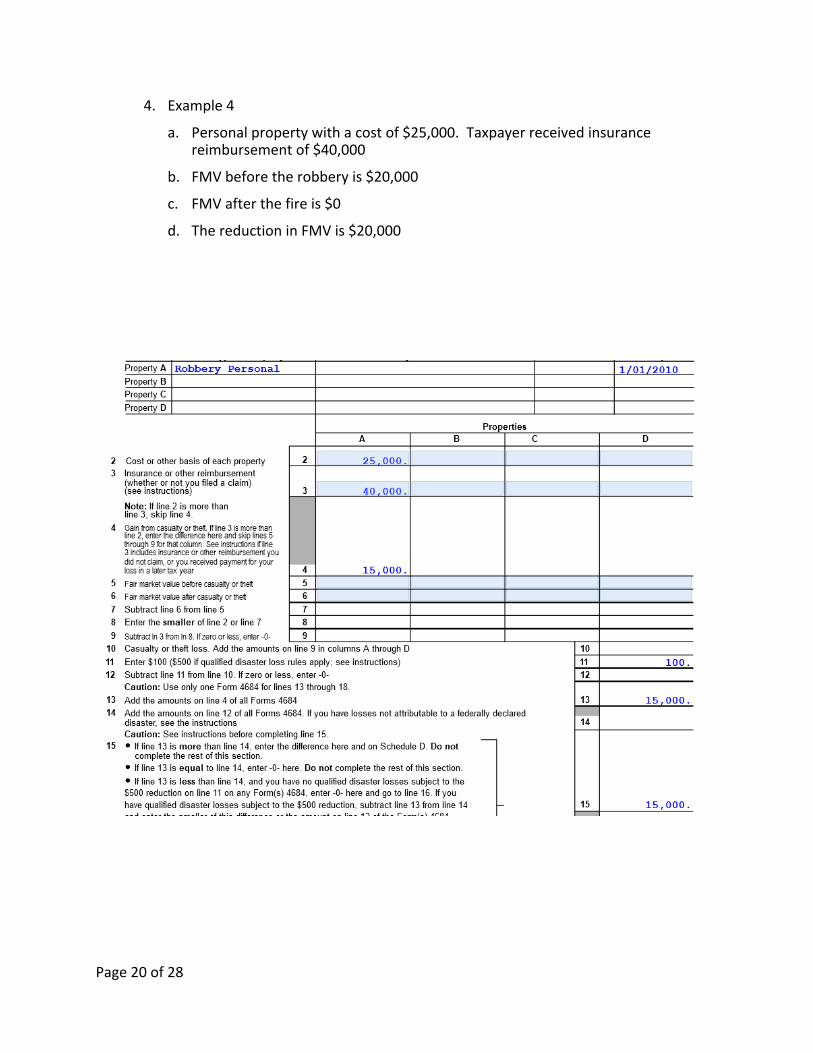

4. Example 4

a. Personal property with a cost of $25,000. Taxpayer received insurancereimbursement of $40,000

b. FMV before the robbery is $20,000

c. FMV after the fire is $0

d. The reduction in FMV is $20,000

Page 20 of 28

Page 21 of 28

5. Example 5

a. Personal property with a cost basis of $40,000. Taxpayer received insurancereimbursement of $20,000

b. FMV before the robbery is $30,000

c. FMV after the robbery is $0

d. The reduction in FMV is $30,000

e. The casualty loss is the difference between the FMV before the robbery and theinsurance reimbursement.

Page 22 of 28

Page 23 of 28

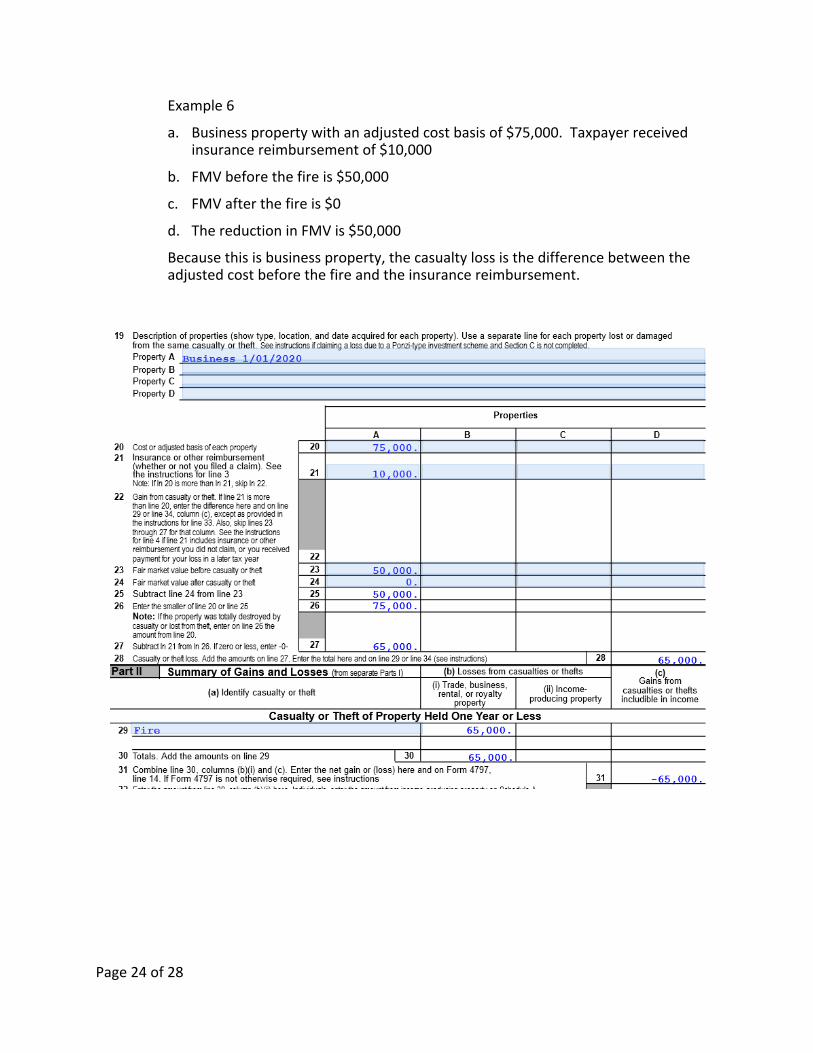

Example 6

a. Business property with an adjusted cost basis of $75,000. Taxpayer receivedinsurance reimbursement of $10,000

b. FMV before the fire is $50,000

c. FMV after the fire is $0

d. The reduction in FMV is $50,000

Because this is business property, the casualty loss is the difference between theadjusted cost before the fire and the insurance reimbursement.

Page 24 of 28

Page 25 of 28

VI. Reconstruction of Records

A. Tax Records and return transcripts, as well as wage and income transcripts can beobtained immediately using

1. the Get Transcript Tool (https://www.irs.gov/individuals/get‐transcript), or

2. by phone, 800‐908‐9946.

3. Taxpayers with a smartphone can get transcripts via the IRS2Go app.(https://www.irs.gov/newsroom/irs2goapp)

4. Taxpayers should write the appropriate disaster designation in red letters acrossthe top of Forms 4506‐T or 4506 to expedite processing and to waive the fee.

B. Basis of a Personal Residence and Real Property can be reconstructed using thefollowing resources.

1. Taking photos or videos as soon as possible after the disaster. If possible useprior photos to help establish the extent of the damage.

2. The title or escrow company that handled the purchase of the home will havecopies of closing documents.

3. The county tax assessor has purchase records.

4. The current property tax statement can be used for land versus building ratios.These are usually available online from the county tax assessor’s office.

5. Establish fair market value by getting an appraisal or reviewing comparable salesin the area.

6. The mortgage company might have copies of the original appraisal.

7. Copies of insurance policies from the insurance company usually list the value ofany buildings to establish a base figure for replacement value.

8. If improvements were made to the home, contact the contractor who did thework for statements.

a. Friends and relatives who saw the house before and after any improvementscan give written affidavits of the improvements

b. If there was a home improvement loan the lender will possibly have anappraisal or other useful documents.

9. For inherited property check court records or get in touch with the attorney whohandled the estate for basis information.

Page 26 of 28

C. Vehicle records can be reconstructed by using

1. Kelley Blue Book https://www.kbb.com/

2. National Automobile Dealers Association https://www.nada.com/

3. Edmunds https://www.edmunds.com/

4. The dealer where the vehicle was purchased should have sales records

5. If there is a loan on the vehicle the lender will have documentation

D. Personal Property

1. Check cell phones for pictures that were taken in and around the house.

2. Check websites for the cost and fair market value of the items (Amazon.com forreplacement cost and Ebay.com or Craigslist.com for FMV).

3. Check for receipts, canceled checks, credit card statements, etc. If purchased atan online retailer, invoices and receipts should be available going back at leastone year.

4. Draw a floor plan showing where each piece of furniture was located, includingshelving and what was on it. Include the garage, basement and attic, and alsoclosets and items hanging on the walls.

E. Business Records

1. Copies of invoices from suppliers and vendors, at least one calendar year back

2. Check cell phones for pictures taken of office furniture, buildings, etc

3. Bank statements, canceled checks or online images

4. Copies of tax returns, including federal, state, excise, payroll and sales taxreturns

5. Sketch an outline of the inside and outside of the business location and fill inwhere items were located, including shrubs, signs, inventory location, awnings,etc

6. If the business was purchased from someone else, ask for a copy of the purchaseagreement

7. If the building was constructed, get invoices from the builder

Page 27 of 28

VII.References

Reconstructing Records After a Natural Disaster or Casualty Loss

https://www.irs.gov/newsroom/reconstructing‐records‐after‐a‐natural‐disaster‐or‐casualty‐loss‐irs‐provides‐tips‐to‐help‐taxpayers

FAQs for Disaster Victims ‐ Casualty Loss (Valuations and Sections 165 (i))

https://www.irs.gov/businesses/small‐businesses‐self‐employed/faqs‐for‐disaster‐victims‐casualty‐loss‐valuations‐and‐sections‐165‐i

Topic No. 515 Casualty, Disaster, and Theft Losses

https://www.irs.gov/taxtopics/tc515

Presidentially Declared Disaster Areas

https://www.irs.gov/newsroom/around‐the‐nation

Form 4684, Casualties and Thefts

IRS Pub. 547, Casualties, Disasters, and Thefts

IRS Pub. 584, 584‐A, 584‐B, Casualty, Disaster, and Theft Loss Workbook

IRS Pub. 976, Disaster Relief

IRS Pub. 2194 Disaster Resource Guide

IRC §165, Losses

Page 28 of 28