Cash Flow Management for Small- to Medium-Sized Businesses e-book

12

Cash Flow Management for Small- to Medium- Sized Businesses By James Price, BBM

-

Upload

jeremy-frew -

Category

Business

-

view

507 -

download

1

Transcript of Cash Flow Management for Small- to Medium-Sized Businesses e-book

Cash Flow Management for Small- to Medium-

Sized Businesses

By James Price, BBM

2 jpabusiness.com.au +61 2 6360 0360

Table of Contents

Cash Flow Management for Small-‐ to Medium-‐Sized Businesses ........................... 3 What is cash flow and what does it mean for your business? ........................................................ 3 The truth about cash flow .............................................................................................................................. 4 Why cash flow is so important in a post-‐GFC world .......................................................................... 5 How to improve cash flow with customers ............................................................................................ 7 How to improve cash flow with suppliers .............................................................................................. 8 13 top tips for managing your cash flow ................................................................................................. 9

Disclaimer: The information contained in this e-book is general in nature and should not be taken as personal, professional advice.

jpabusiness.com.au +61 2 6360 0360 3

Cash Flow Management for Small- to Medium-Sized Businesses By James Price, BBM

In this e-book we take a look at Cash Flow:

• The truth about cash flow • Cash flow in a post-GFC world • How to improve cash flow with customers • How to improve cash flow with suppliers • 13 top tips for maintaining a positive cash flow

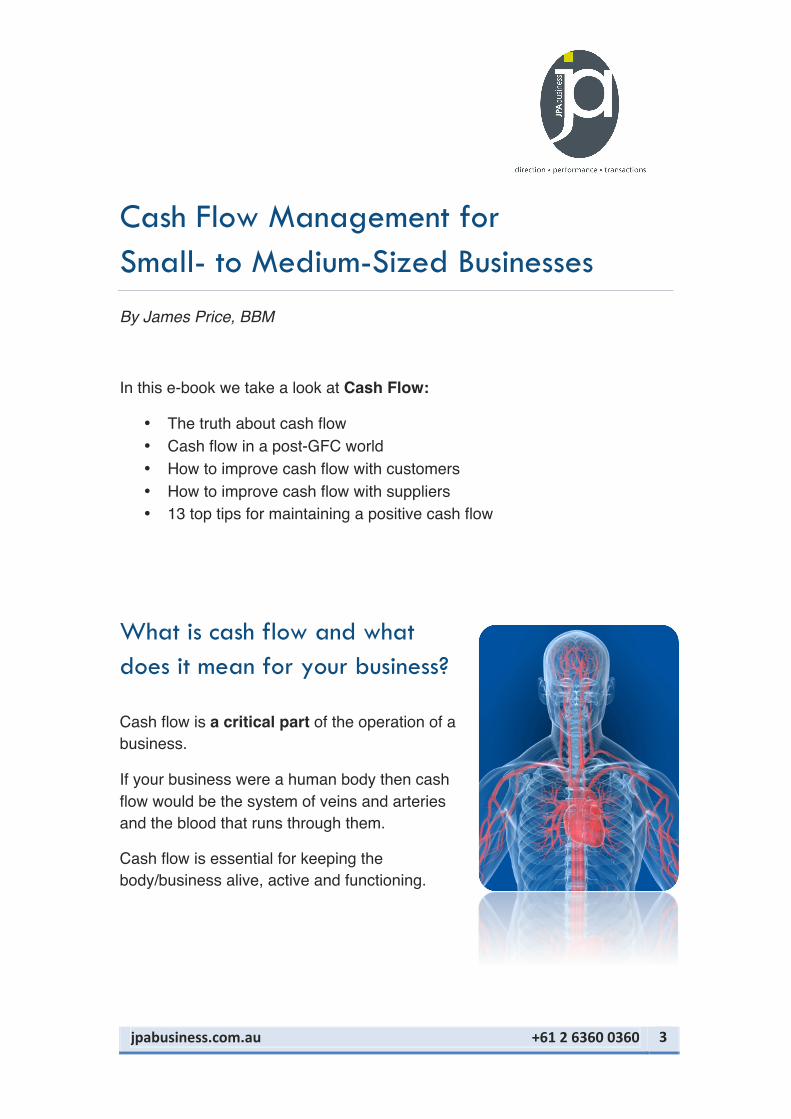

What is cash flow and what does it mean for your business?

Cash flow is a critical part of the operation of a business.

If your business were a human body then cash flow would be the system of veins and arteries and the blood that runs through them.

Cash flow is essential for keeping the body/business alive, active and functioning.

4 jpabusiness.com.au +61 2 6360 0360

The truth about cash flow

Cash flow is not profit and it’s not loss, although a business can build cash or burn cash.

Even in large businesses there’s often a misconception that ‘if I’m profitable I have a sound cash flow’. Often businesses that are profitable or are going through growth spurts can have very, very serious cash flow problems.

The other misconception is ‘if I increase my turnover I will have a positive cash flow’.

Many businesses, particularly in recent years, have had a strategy of increasing their turnover. But what matters for cash flow is the extent to which there is a positive margin earned on that turnover, after your ongoing fixed and operational expenses.

The other critical factor is the timing of receiving those funds.

For example, you sell a service today and you incur labour and materials costs on that service. You pay for the labour and materials now, but you’re customer doesn’t pay you for the service for 30 to 120 days.

There’s a gap and someone has to fund it – you!

There has to be enough cash flow – or working capital – in the business to cover the gap, whether it be in the form of debt, equity or retained earnings.

jpabusiness.com.au +61 2 6360 0360 5

Why cash flow is so important in a post-GFC world

Cash flow has always been important, but it has become even more so in the five years since the global financial crisis.

In the GFC money was hard to come by, so smart companies looked at their total business operations and asked ‘where do I have money tied up that I can use more efficiently?’

If you look at a simple business, there are a number of areas where money is tied up:

• Inventory or stock – the value of your inventory and the degree to which

you turn it over represents funds that are tied up.

• Debtors – money that customers owe you. At any one time if you look at a

company’s debtors list there is money outstanding.

• WIP (Work in Progress) – if you’re part way through fulfilling a contract,

you will have cash flow tied up in WIP that may not yet be billed to your

customer. • Creditors – money you owe others.

During the GFC smart companies looked at those areas and asked:

• How can we tweak this to better control those money flows?

• How can we rearrange our payment terms with creditors, and also better

manage our payment terms with customers?

• How can we manage our stock better – can we order just-in-time or leave

some stock with the supplier, rather than buying it now and tying up

capital?

• How can we more aggressively manage older or slower-moving stock?

6 jpabusiness.com.au +61 2 6360 0360

Lending in a post-GFC world Some companies operate and fund their business based on debt, some on equity and debt.

Through the GFC banks became very cautious about lending money and typically post-GFC banks are focusing more closely on cash flow factors before lending.

So if a company has a strong surplus cash flow, it’s not only creating profit but it’s creating sustainable cash earnings.

A bank is much more interested in lending to a company with strong sustainable cash earnings, than in lending to a company where they have a cash flow deficit or are marginal in generating cash flow.

jpabusiness.com.au +61 2 6360 0360 7

How to improve cash flow with customers

New business is not necessarily good business Often in business the biggest focus is to win a new customer, but it’s important that you understand any new customer’s credit worthiness i.e. to what extent they pay their bills on time.

Be sure to do your homework up front and ask the hard questions of a new customer regarding their payment history.

Some business owners prefer to tighten their payment terms with new customers, until they’ve established a positive track record.

There are a number of credit rating agencies where, for a small fee, you can run a report that gives you a feel for a new customer’s likely payment performance, and of course don’t be afraid to ask for a trade referee or two.

Take a disciplined approach to invoicing A business needs to have a disciplined invoicing process.

Some businesses will work away at servicing their customers for many months before sending them an invoice. The administration should work in parallel with the service or product, rather than following delivery.

Document and agree on your payment terms (‘terms of trade’) Often, invoices are very unclear about the expected payment terms. Many invoices don’t even have payment terms documented on them.

In many business environments it’s a handshake and an expectation, but this makes it very hard to fall back on something should payment terms be out of order.

In the post-GFC environment, clear documentation and expectations are critical.

8 jpabusiness.com.au +61 2 6360 0360

How to improve cash flow with suppliers

Extend your payment terms with your suppliers If you have a track record and a relationship, then look for opportunities to extend your payment terms.

That often involves deliberate discussions and negotiations about what might work for both parties. Remember there needs to be a bit of give and take, but make sure you document and agree a fair arrangement upfront.

Closely manage stock and inventory Managing stock and inventories is often the great hidden cash flow trap.

There is a philosophy that stock is worth money because you sell it eventually, and if you haven’t got it, you won’t be able to sell it.

That’s correct in principal.

But I would rather say that a business has to have access to stock in a timely fashion.

By running just-in-time, you don’t have to carry the risk on it. Rather, you carry the delivery risk and need to manage your customers’ expectations.

Be smarter about stock levels There are many businesses which, if asked what their stock level is today and what it’s worth, wouldn’t know within 10 per cent.

That suggests they aren’t managing their cash flow.

Businesses need to have a deliberate, robust and constant focus on stock management.

They need to look at individual item stock levels and ask:

• How much do we really need to hold? • What are the trigger points for re-ordering • How do we shift slow-moving or obsolete stock?

jpabusiness.com.au +61 2 6360 0360 9

13 top tips for managing your cash flow

1. Create a calendar Have a monthly calendar and agree – either as the business owner, the finance or administration department – on trigger points for cash flow management.

2. Set standard timing for invoicing Agree on the timing of invoicing and slavishly focus on meeting it.

Design your internal business processes and information collection and verification procedures to deliver to that time frame.

3. Clearly state payment terms on your invoice Make sure your invoice clearly states your expectations about payment terms.

Get some business or legal advice to ensure your invoice and terms of trade measures up in the event you have a defaulting payment that necessitates recovery action.

4. Instigate a calling program If you send out invoices with 14-day payment terms, then on day 13 make sure there is a calling program.

Call all your key customers due for payment the next day and speak to the decision maker or accounts person responsible.

Let them know it’s ‘a friendly call just to indicate that your invoice is due tomorrow....just confirming that we can expect payment in our terms of trade’ and, if you wish, follow up with an email.

This will help you keep in touch with your customers and understand if there are any issues at their end – it’s better to understand earlier than later!

10 jpabusiness.com.au +61 2 6360 0360

5. Monitor payment Make sure there are processes in place to monitor payment as per the payment terms.

This can simply mean checking your bank account to see if the flow of funds is happening.

If the funds aren’t happening the day following when invoices are due, then follow up and get clarity with the customer regarding their intention to pay or not, and when.

6. Resolve disputes quickly Often, poor payment is not due to the customer’s lack of ability to pay, but because they disagree with what they’ve been invoiced for.

The business owner/manager needs to ensure there is a discussion between the person in their business responsible for providing the service or product, and the customer, as soon as a dispute is identified.

The issues need to addressed, the dispute resolution agreement documented and the invoice addressed.

Deal with disputes quickly, because you want a clean debtor ledger at all times.

7. Talk to your creditors As a business we all go through stresses and strains around cash flow.

If you have cash flow issues then talk ahead of time to your creditors and suppliers and see if you can structure another payment arrangement.

Most business owners do not communicate cash flow issues to their suppliers, customers or financiers, and then have to deal with it once payment is overdue.

It’s much better to talk ahead of time.

jpabusiness.com.au +61 2 6360 0360 11

8. Directors have responsibilities As directors of an incorporated body associated with running a business, one key director responsibility is to ensure the company can meet its short-term commitments – its current liabilities.

Cash flow is inextricably linked to meeting those commitments.

Clearly monitor your business’ position with respect to these commitments, raise ‘red flags’ early and implement corrective action if things aren’t on track.

9. Take a close interest in your cash flow Oversight your cash flow day to day, rather than letting the person responsible for dispatching invoices manage it in isolation. This is critical for a business owner.

If you’re focused on it day to day you will spot potential gaps looming in your cash flow. You will be in a much better position to negotiate additional working capital or carry-on finance with your bank if you are foreseeing potential problems and talking to your bank, customers and suppliers ahead of time.

10. Unless you’re a bank, don’t act like one Some businesses have payment terms that state ‘the payment period is X days – if the account is not paid in X days the customer will be charged interest at a daily rate of Y per cent’.

It’s important to have that trigger there for poor payers, but the reality is that interest being charged doesn’t necessarily help your cash flow!

The cash flow gap still exists because the payment remains outstanding.

12 jpabusiness.com.au +61 2 6360 0360

11. Tackle the taboo subject: money! Often in business, particularly private business, payment and cash flow are taboo subjects.

Many business owners feel embarrassed or nervous to approach a customer and ask why they haven’t paid. In managing cash flow well, business owners need to get over those inhibitions.

12. Going legal No one likes to go legal to recover payment – it’s usually an expensive and frustrating exercise.

Business owners/managers, finance and administration departments need to set the trigger time for when an outstanding invoice is put through a recovery process.

13. Communicate, communicate, communicate The most important cash flow tip for any business owner/manager, large or small, is to make sure expectations are clear and lines of communication are explicitly open.

If you are talking openly to your customers, financiers, partners, investors and suppliers about payment and cash flow issues, whether invoices are outstanding to a creditor or outstanding from a debtor, or it’s simply a tight period of cash generation in the business, you can usually sort them out.

Documentation is important, but be careful not to substitute an email for a straight-forward, simple discussion.