Cash and marketable securities

42

CASH AND MARKETABLE SECURITIES

-

Upload

lyka-gemima-ganancias -

Category

Business

-

view

206 -

download

1

Transcript of Cash and marketable securities

CASH AND

MARKETABLE

SECURITIES

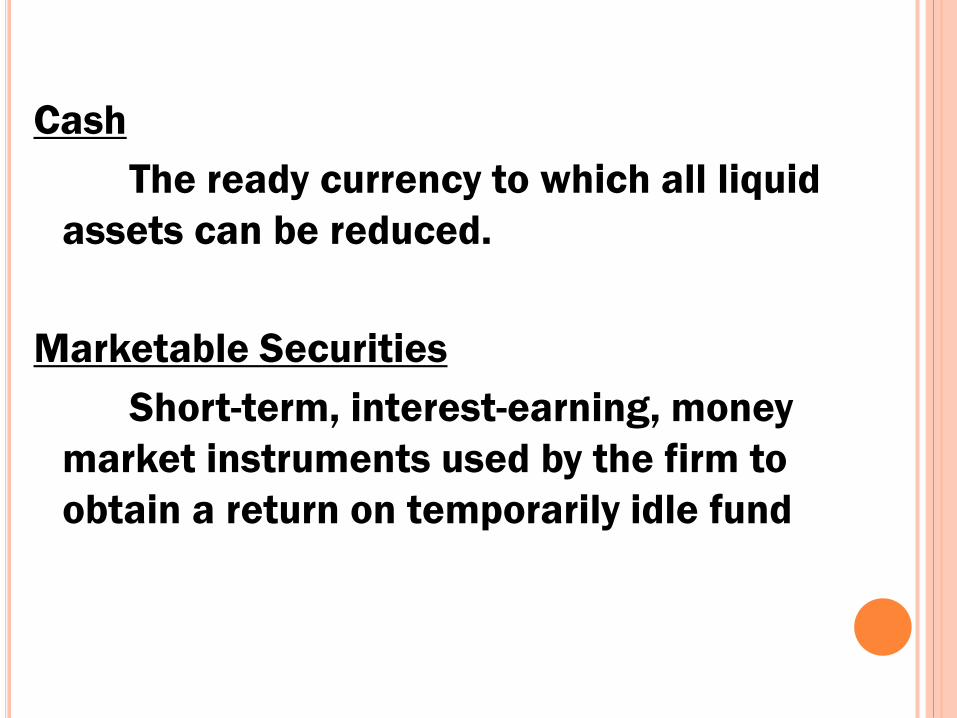

Cash

The ready currency to which all liquid

assets can be reduced.

Marketable Securities

Short-term, interest-earning, money

market instruments used by the firm to

obtain a return on temporarily idle fund

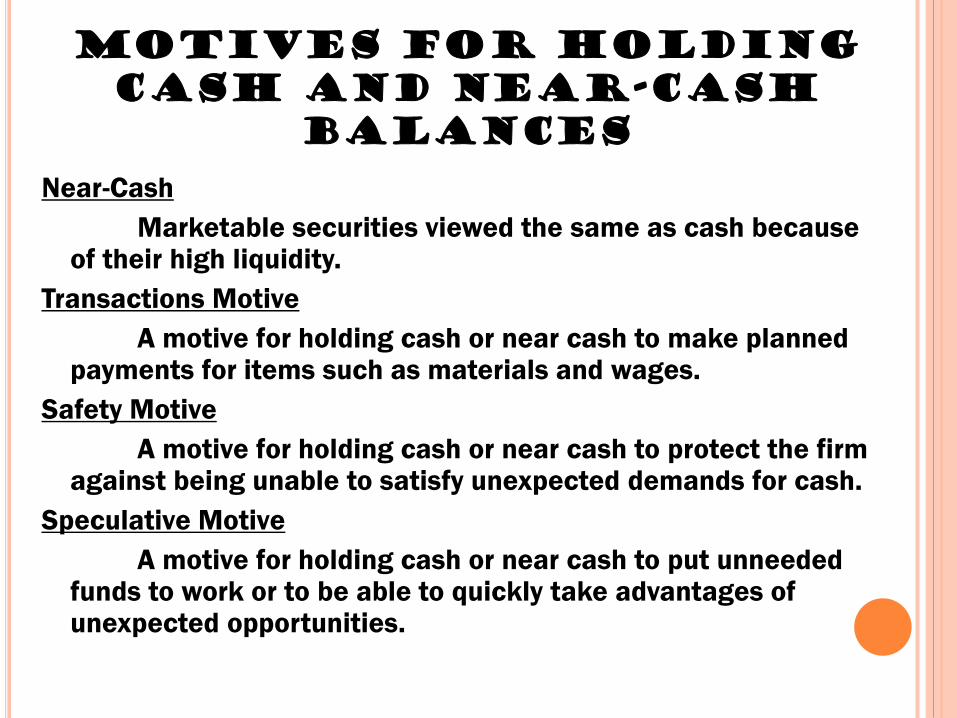

MOTIVES FOR HOLDING

CASH AND NEAR-CASH

BALANCES

Near-Cash

Marketable securities viewed the same as cash because of their high liquidity.

Transactions Motive

A motive for holding cash or near cash to make planned payments for items such as materials and wages.

Safety Motive

A motive for holding cash or near cash to protect the firm against being unable to satisfy unexpected demands for cash.

Speculative Motive

A motive for holding cash or near cash to put unneeded funds to work or to be able to quickly take advantages of unexpected opportunities.

Operating Cycle (OC)

The amount of time that elapses from the

point when the firm begins to build inventory to

the point when cash is collected from sale of the

resulting finished product.

CASH CONVERSION CYCLE

(CCC)

The amount of time the firm’s cash is tied up

between payment for production inputs and

receipt of payment from the sale of the

resulting finished product.

Calculated as the number of days in the

firm’s operating cycle minus the average

payment period for inputs to production.

FORMULA IN GETTING CCC

CCC= OC – APP

Where:

OC – Operating Cycle

APP – Average Payment Period

MANAGING THE CASH

CONVERSION CYCLE

A positive cash conversion cycle means that the firm

use nonspontaneous (i.e., negotiated) forms of

financing such as unsecured short-term loans or

secured sources of financing, to support the cash

conversion cycle.

Ideally, a firm would like to have a negative cash

conversion cycle. A negative CCC means the average

payment period (APP) exceeds the operating cycle (OC).

THE

BASIC STRATEGIES

Turn over inventory as quickly as possible, avoiding stock

outs (depletions of stock) that might result in a loss of

sales.

Collect accounts receivable as quickly as possible

without losing future sales because of high-pressure

collection techniques. Cash discounts, if they are

economically justifiable, may be used to accomplish this

objective.

Pay accounts payable as late as possible without

damaging the firm’s credit rating, but take advantage of

any favorable cash discount.

EFFICIENT INVENTORY –

PRODUCTION MANAGEMENT

One strategy available to MAX is to increase

inventory turnover. To do so, the firm can increase

raw materials turnover, shorten the production

cycle, or increase finished goods turnover.

ACCELERATING THE

COLLECTION OF ACCOUNTS

RECEIVABLE

Another means of reducing the cash conversion

cycle (and the negotiated financing need) is to

speed up, or accelerate, the collection of accounts

receivable.

STRETCHING ACCOUNTS

PAYABLE

A firm pays its bills as late as possible without

damaging its credit rating. Although this approach

is financially attractive, it raises an important

ethical issue.

COMBINING CASH

MANAGEMENT STRATEGIES

Firms typically do not attempt to implement just one cash management strategy; they attempt to use them all to reduce their reliance on negotiated financing.

Firms should take care to avoid having a large number of inventory stock outs to avoid losing sales.

CASH MANAGEMENT

TECHNIQUES

FLOAT

• refers to funds that have been dispatched by a

payer but are not yet in form that can be spent by

the payee.

• It also exists when a payee has receive funds in a

spendable form but these funds have not been

withdrawn from the account of the payer.

TYPES OF FLOAT

Collection Float

The delay between the time when a payer or customer deducts a payment from its checking account ledger and the time when the payee or vendor actually receives the funds in a spendable form.

Disbursement Float

the lapse between the time when a firm deducts a payment from its checking account ledger (disburses it) and the time when funds are actually withdrawn from its account.

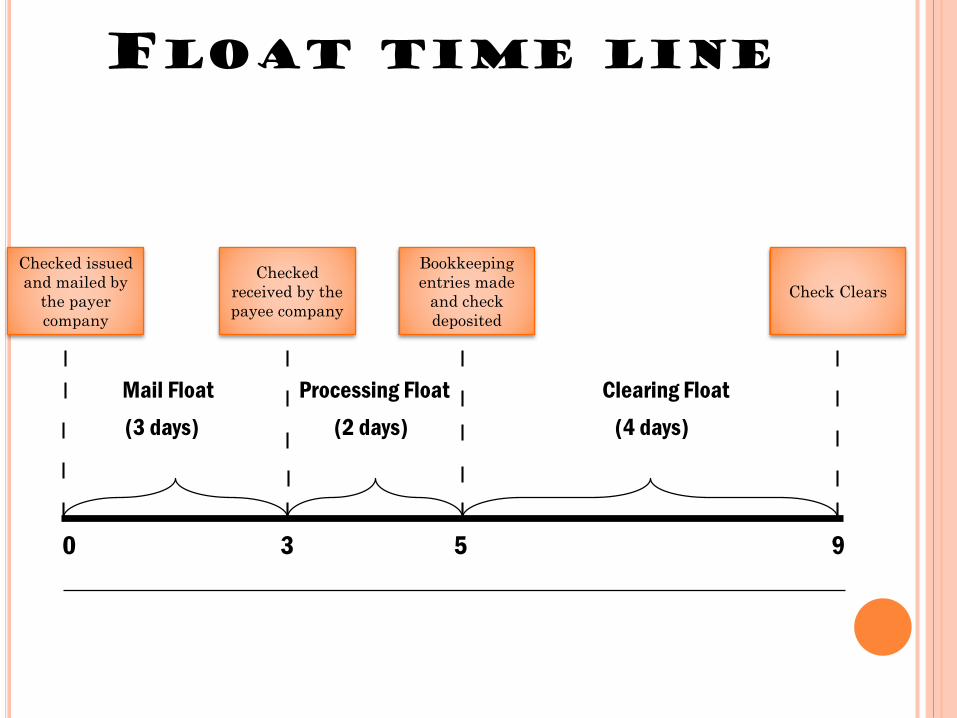

COMPONENTS OF FLOAT

Mail Float

the delay between the time when a payer mails a

payment and the time when the payee receives it.

Processing Float

the delay between the receipt of a check by the payee

and its deposit in the firm’s account.

Clearing Float

the delay between the deposit of a check by the payee

and the actual availability of the funds.

FLOAT TIME LINE

Checked issued

and mailed by

the payer

company

Checked

received by the

payee company

Bookkeeping

entries made

and check

deposited

Check Clears

Mail Float Processing Float Clearing Float

(3 days) (2 days) (4 days)

0 3 5 9

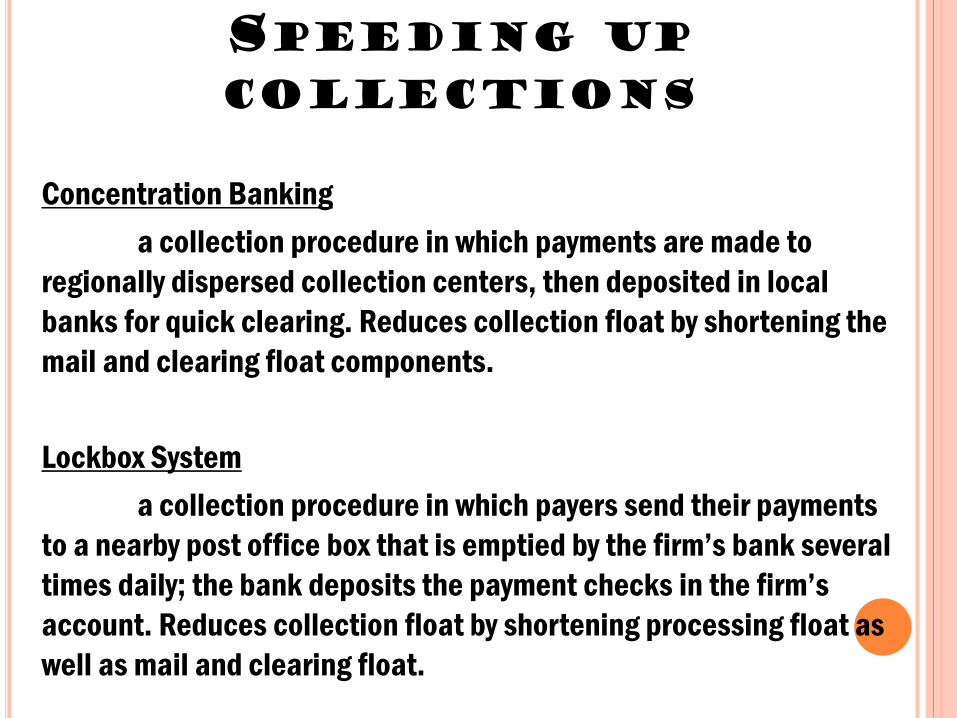

SPEEDING UP

COLLECTIONS

Concentration Banking

a collection procedure in which payments are made to

regionally dispersed collection centers, then deposited in local

banks for quick clearing. Reduces collection float by shortening the

mail and clearing float components.

Lockbox System

a collection procedure in which payers send their payments

to a nearby post office box that is emptied by the firm’s bank several

times daily; the bank deposits the payment checks in the firm’s

account. Reduces collection float by shortening processing float as

well as mail and clearing float.

Direct Send

a collection procedure in which the payee

presents checks for payment directly to the banks

on which they are drawn, thus reducing clearing

float.

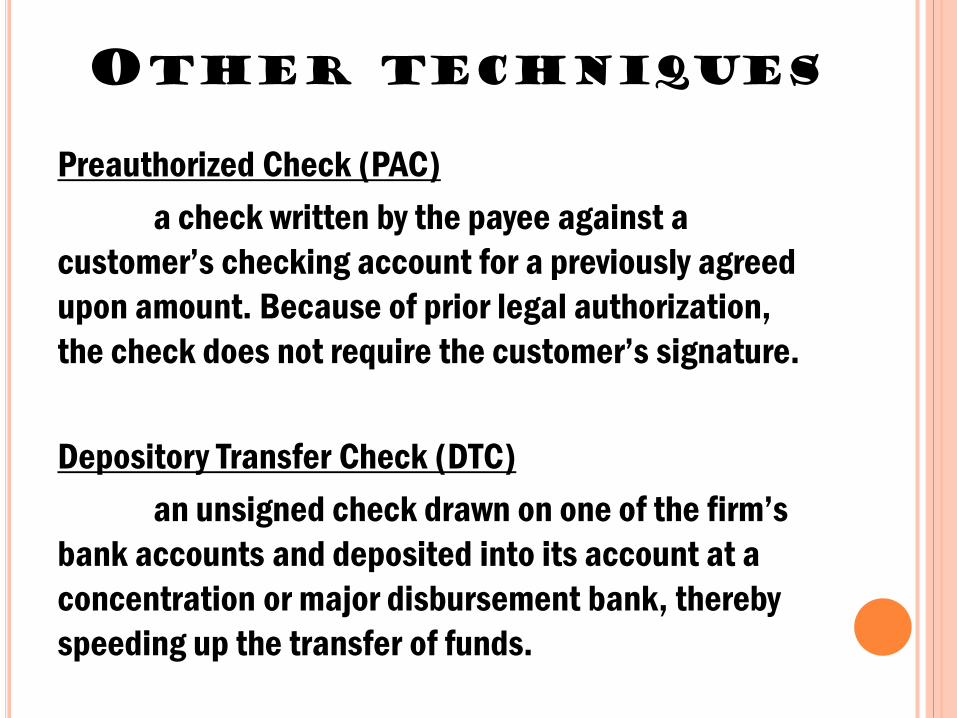

OTHER TECHNIQUES

Preauthorized Check (PAC)

a check written by the payee against a

customer’s checking account for a previously agreed

upon amount. Because of prior legal authorization,

the check does not require the customer’s signature.

Depository Transfer Check (DTC)

an unsigned check drawn on one of the firm’s

bank accounts and deposited into its account at a

concentration or major disbursement bank, thereby

speeding up the transfer of funds.

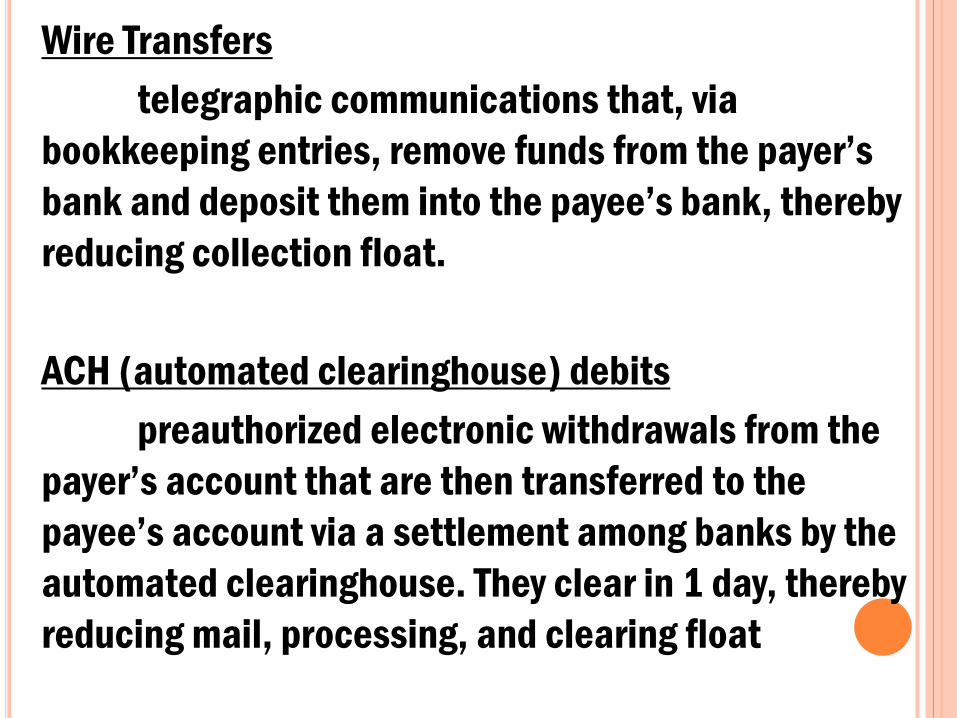

Wire Transfers

telegraphic communications that, via

bookkeeping entries, remove funds from the payer’s

bank and deposit them into the payee’s bank, thereby

reducing collection float.

ACH (automated clearinghouse) debits

preauthorized electronic withdrawals from the

payer’s account that are then transferred to the

payee’s account via a settlement among banks by the

automated clearinghouse. They clear in 1 day, thereby

reducing mail, processing, and clearing float

SLOWING DOWN DISBURESMENT

Controlled Disbursing

The strategic use of mailing points and bank accounts to lengthen mail float and clearing float, respectively.

Playing the float

A method of consciously anticipating the resulting float, or delay, associated with the payment process and using it to keep funds in an interest-earning form for as long as possible.

Staggered Funding

A way to play the float by depositing a certain

proportion of a payroll or payment into the firm’s

checking account on several successive days

following the actual issuance of a group of checks.

Payable-through draft

A draft drawn on the payer’s checking

account, payable to a given payee but not payable

on demand; approval of the draft by the payer is

required before the banks pays the draft.

OVER DRAFT,ZERO-BALANCE,AND ACH CREDITS

Overdraft System

Automatic coverage by the bank of all checks

presented against the firm’s account, regardless of

the account balance.

Zero-balance account

A checking account in which a zero balance

is maintained and the firm is required to deposit

funds to cover checks drawn on the account only as

they are presented for payment.

ACH (automated clearinghouse)credits

Deposits of payroll directly into the payee’s

(employees) accounts. Sacrifices disbursement

float but may generate goodwill for the employer.

THE ROLE OF STRONG

BANKING RELATIONSHIPS

Establishing and maintaining strong banking relations

are among the most important elements in an effective

cash management system.

Banks have become keenly aware of the profitability of

corporate accounts and in recent years have developed a

number of innovative services and packages designed to

attract various types of businesses.

These packages deal w/ everything from basic

accounting and budgeting to complex multinational

disbursement and centralized cash control.

Banks prefer the compensating balance approach giving credit against bank service charges for amounts maintained in the customer’s checking account.

INTERNATIONAL CASH

MANAGEMENT

Differences in Banking System

GIRO SYSTEM

system through which retail transactions are handled in

association with a foreign country’s national postal

system.

VALUE DATING

a procedure used by non-U.S. banks to delay, often for

days or even weeks, the availability of funds deposited

with them.

CASH MANAGEMENT

PRACTICES

The cash management practices of multinational

corporations are made more complicated by the need to

both maintain local currency deposit balances in banks in

every country in which the firm operates and to retain

centralized control over cash balances and cash flows

that, in total, can be quite large.

INTRACOMPANY NETTING TECHNIQUE

a technique used by subsidiaries of multinational firms to

minimize their cash requirements by transferring across

national boundaries only the net amount of payments owed

between them. Sometimes bookkeeping entries are

substituted for international payments.

CLEARING HOUSE INTERBANK PAYMENT SYSTEM(CHIPS)

the most important wire transfer service; operated by

international banking consortia.

Marketable securities- are short term, interest-earning,

money market instruments that can easily be converted

into cash.

2 GROUPS:

- government issues

- non government issues

Characteristics of Marketable Securities

2 basic characteristics:

-a ready market

-safety of principal

Breadth of a market

a characteristic of a ready market, determined by the

number of participants (buyers) in the market.

Depth of a market

a characteristic of a ready market, determined by its

ability to absorb the purchase or sale of a large dollar

amount of a particular security.

Safety of Principal

the ease of salability of a security for close to its initial value.

Treasury Bills

are obligations issued weekly on an auction basis, having varying maturities, generally under 1 year, and virtually no risk.

Treasury Notes

are obligation with initial maturities of between 1 and 10 years, paying interest at a stated rate semiannually, and having virtually no risk.

Federal Agency Issues

Low risk securities issued by government agencies but not guaranteed by the US treasury, Having generally Short maturities, and offering slightly higher yields than comparable US treasury issues.

Negotiable certificates of Deposits

negotiable instruments representing specific cash deposits in

commercial banks, having varying maturities and yields based on size,

maturity and prevailing money market conditions. Yields are generally

above those on US treasury Issues and comparable to those on

commercial paper with similar maturities.

Commercial Paper

a Short-term unsecured promissory note issued by a corporation

that has a very high credit standing, having a yield above that paid on

US treasury Issues and comparable o that available on negotiable CDs

with similar maturities.

Bankers Acceptance

short-term, low-risk marketable securities arising from bank

guarantees of business transactions: are sold by banks at a discount

from their maturity value and provide yields slightly below those on

negotiable Cds and commercial paper, but higher than those on US

treasury Issues.

Eurodollar Deposits

deposits of currency not native to the country in which

the bank is located; negotiable, usually pay interest at

maturity, and are typically denominated in units of $1

million. Provide yields above nearly all other marketable

securities with similar maturities.

Money Market Mutual Funds

Professionally managed portfolios of various popular

marketable securities, having instant liquidity, competitive

yields and often low transactions costs.

CASH CONVERSION

MODELS

Cash Conversion Models balance the relevant costs

and benefits of holding cash versus investing in

marketable securities to determine the

economically optimum cash conversion quantity.

Here we consider two of the best-known cash

conversion models: The Baumol Model and the

Miller-Orr Model

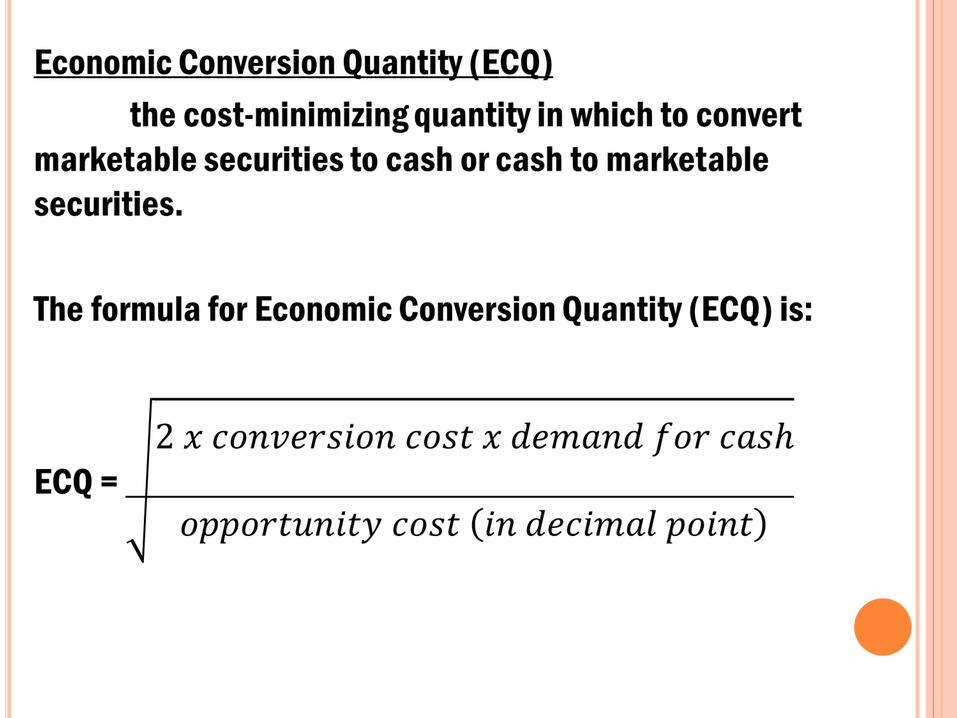

BAUMOL MODEL

A model that provides for cost-efficient transactional cash

balances; assumes that the demand for cash can be

predicted with certainty and determines the economic

conversion quantity (ECQ).

The firm manages this cash inventory on the basis of the

cost of converting marketable securities into cash and

vice versa (the conversion cost) and the cost of holding

cash rather than marketable securities (opportunity cost).

CONVERSION COST

Includes the fixed costs of placing and receiving an

order for cash in the amount of ECQ.

OPPORTUNITY COST

The rate of interest that can be earned on marketable

securities.

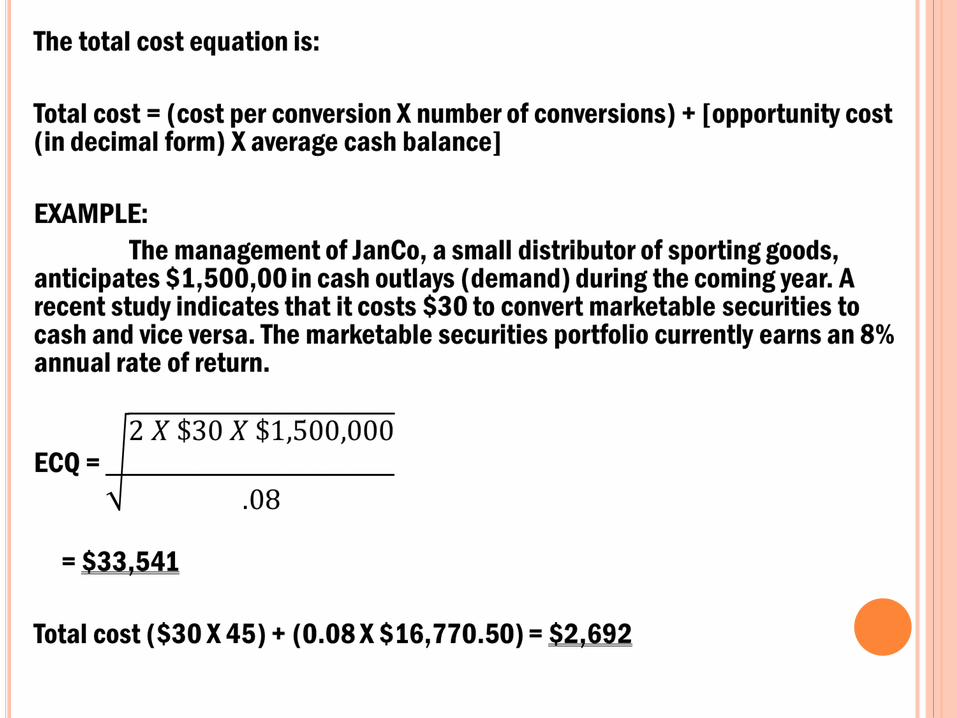

TOTAL COST

The sum of the total conversion and total opportunity

costs.

The number of conversions per period can be found by

dividing the period’s cash demand by the economic

conversion quantity (ECQ)

The average cash balance is found by dividing ECQ by 2.

MILLER – ORR

MODEL

UPPER LIMIT

The upper limit for the cash balance is three times

the return point.

CASH BALANCE REACHES THE UPPER LIMIT

When the cash balance reaches the upper limit, an

amount equal to the upper limit minus the return point is

converted to marketable securities:

Cash converted to marketable securities = upper limit -

return point

CASH BALANCE

FALLS TO ZERO