Case Study Techcombank - Banking Software Systems ... Summary V ietnam Technological and Commercial...

20

Sustained IT Investment For Sustained Competitive Outperformance. Case Study Techcombank

Transcript of Case Study Techcombank - Banking Software Systems ... Summary V ietnam Technological and Commercial...

Sustained IT Investment For Sustained Competitive Outperformance.

Case StudyTechcombank

Executive Summary

Vietnam Technological and Commercial Joint Stock Bank (Techcombank), a Temenos customer since 2001, has always held technological innovation to be critical to the success

of its business. This progressive attitude towards technology has underpinned Techcombank’s consistently high IT investment and has provided the source of enduring competitive advantage that, in turn, has seen Techcombank grow revenue, loans and profits faster than its competitors, while continuing to improve efficiency, customer service and risk management.

This case study aims to demonstrate in practical and quantifiable terms the impact that Techcombank’s sustained investment in TEMENOS T24 (T24), its core banking application, has made in the areas of customer satisfaction, product innovation, operational efficiency and risk management. Throughout the study, we also aim to benchmark Techcombank’s performance against its domestic and international peers to illustrate its comprehensive outperformance in recent years.

Temenos Case Study01

03 About Techcombank06 Partnering With Temenos For Core Banking Software06 • The Need For A New System06 • Initial Selection And Implementation07 • Sustained Investment08 Where Techcombank Has Outperformed And How Technology Has Facilitated This08 • Overview08 • Product Innovation10 • Some Recent Products11 • Customer Service12 • Operational Efficiency14 • Risk Management15 Summary16 Appendix16 • Glossary Of Abbreviations17 • Authors, Further Contact, About Temenos17 • Disclaimer

Contents

Temenos Case Study02

• SincegoinglivewithT24in2003,Techcombankhasbeenthefastest-growing bank in Vietnam, recording a revenue CAGR of 87% over the period.

• ThecustomercentricnatureofT24hasenabledTechcombanktotailor its service to individual customers, translating into the highest customer rating of any Joint Stock Bank and more than 25% annual growth in revenue per customer over the last two years.

• TheflexibilityinT24toconfigurenewproductshasseenTechcombank out-innovate and out-manoeuvre competitors and in doing so grow its deposit base at a CAGR of 72% over the last five years, more than twice the rate of the overall market.

• TheinherentscalabilityofT24,coupledwithitsgrowingusagethroughout the bank, has led to significant economies of scale in IT. IT cost to income, for instance, is 84% below the industry average.

• Despiteitsexceptionalgrowth,acompleteviewofthebank’sriskexposure at both the client and aggregate bank level has allowed Techcombank to control risk successfully: while loans grew by 199% between 2006 and 2008, the percentage of non-performing loans actually fell.

• Between2003and2008,Techcombank’soperatingprofitgrewata compound annual rate of 111%, also faster than any other bank in Vietnam.

Highlights

Temenos Case Study03

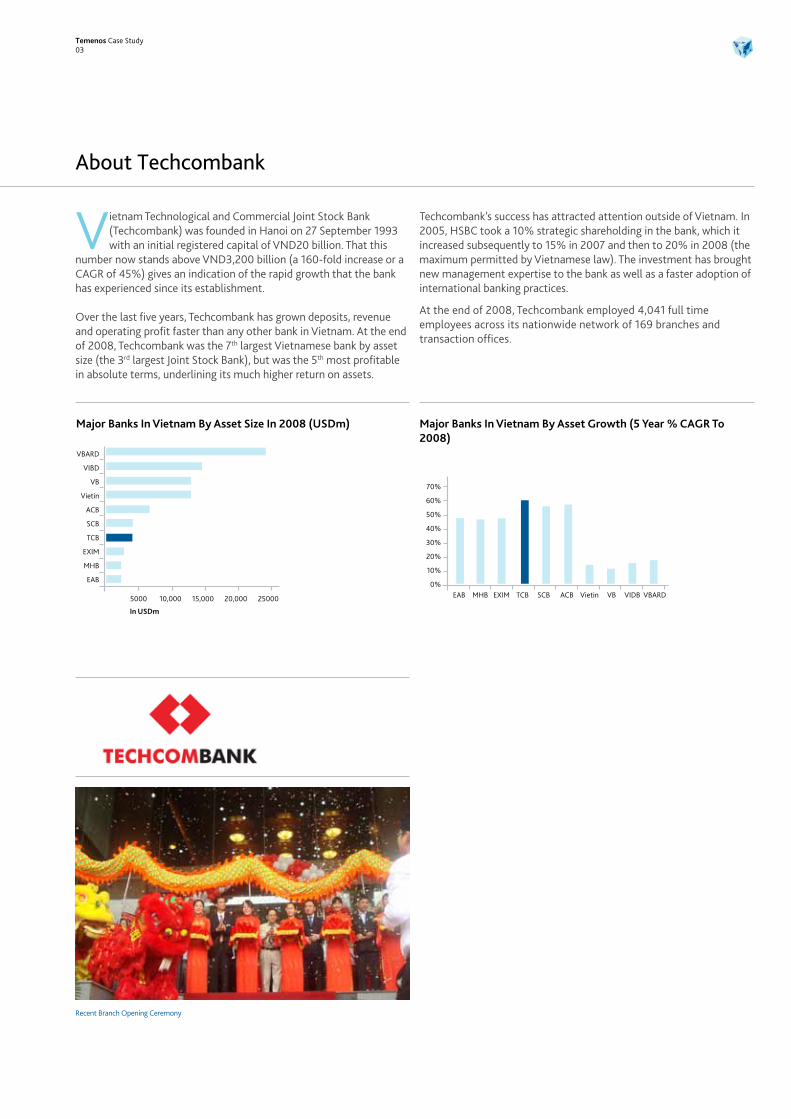

Vietnam Technological and Commercial Joint Stock Bank (Techcombank) was founded in Hanoi on 27 September 1993 with an initial registered capital of VND20 billion. That this

number now stands above VND3,200 billion (a 160-fold increase or a CAGR of 45%) gives an indication of the rapid growth that the bank has experienced since its establishment.

Over the last five years, Techcombank has grown deposits, revenue and operating profit faster than any other bank in Vietnam. At the end of 2008, Techcombank was the 7th largest Vietnamese bank by asset size (the 3rd largest Joint Stock Bank), but was the 5th most profitable in absolute terms, underlining its much higher return on assets.

Techcombank’s success has attracted attention outside of Vietnam. In 2005, HSBC took a 10% strategic shareholding in the bank, which it increased subsequently to 15% in 2007 and then to 20% in 2008 (the maximum permitted by Vietnamese law). The investment has brought new management expertise to the bank as well as a faster adoption of international banking practices.

At the end of 2008, Techcombank employed 4,041 full time employees across its nationwide network of 169 branches and transaction offices.

About Techcombank

VBARD

VIBD

VB

Vietin

ACB

SCB

TCB

EXIM

MHB

EAB

5000 10,000 15,000 20,000 25000

In USDm

Major Banks In Vietnam By Asset Size In 2008 (USDm)

70%

60%

50%

40%

30%

20%

10%

0%EAB MHB EXIM TCB SCB ACB Vietin VB VIDB VBARD

Major Banks In Vietnam By Asset Growth (5 Year % CAGR To 2008)

Recent Branch Opening Ceremony

Temenos Case Study05

Techcombank - Selected Milestones

1993 Techcombank established in Hanoi.

1998 Head office moved to larger location in Hanoi; branch network expanded to cover three main regions in Vietnam.

2001 Signs agreement with Temenos for core banking software.

2004 A rebranding exercise, started the year before, is completed and new logo is launched.

2005 HSBC takes a 10% strategic stake.

2006 Wins several awards, including the international award for payments from Bank Of New York, Citibank and Wachovia.

First Joint Stock Bank to receive Moody’s rating.

A series of new products launched, including first multifunctional savings product.

2007 HSBC increases stake in Techcombank to 15%.

Wins award for “Top Trade Services 2007” from the Ministry of Industry and Commerce.

2008 HSBC increases its stake to 20%.

Diversifying into asset management, with the launch of Techcombank AMC (Asset Management Company).

A series of innovative products released, including collaborative ventures with Vietnam Airlines and Bao Viet Insurance.

Wins several awards, including “the Most Satisfied Services in 2008” voted by readers of Sai Gon Tiep Thi magazine; “The Top Joint Stock Company of Vietnam” given by the securities committee; and, the “Golden Start Award” from the Association of Young Enterprises.

Techcombank ran a very detailed selection process, which lasted for one year and which considered both local and foreign vendors.Even though Temenos, like the other international vendors invited to participate, had little experience in Vietnam – Temenos had just one Vietnamese customer at the time, compared to 11 now – Techcombank wanted a solution that incorporated deep international banking know-how and was prepared to overlook lack of local market references.

What impressed Techcombank about Temenos and T24 (then named Globus) and the reason the solution was ultimately selected ahead of the competing products was the following:

• As a single domain company, Temenos was felt to have the best banking knowledge.• Temenos spends more on R&D than its peers, channelled into an annual release programme. Techcombank valued this commitment to the product (and its clients).• T24 was considered the most flexible solution and Techcombank wanted to be able to make the customisations necessary to meet local requirements without modifying the core code, so that the system would be easily upgradeable.• Techcombank was impressed with the user interface, which it felt was intuitive and easy to navigate.

Before making its final decision, Techcombank visited Temenos’ development centre in Chennai to meet developers and understand more profoundly how the system worked.

The decision to take T24 was made late in 2001, the implementation project began in March 2002 and the product was live across all branches by the 12th December 2003.

Techcombank has always had big ambitions. In its mission statement, it sets out its intention of being the number one bank in Vietnam across a range of metrics – trust, quality, effectiveness. Techcombank has furthermore, always had a

very progressive attitude towards technology. As its name suggests, technology is an integral part of the bank’s make-up and it has always understood the importance of technological innovation as a means of differentiating its business and, by extension, as a source of competitive advantage.

It was this combination of ambition and technological vision that resulted in Techcombank making the decision to replace its core banking system with a packaged solution from a foreign vendor, even though at this time such solutions were largely untested in the Vietnamese market.

Before running T24 from Temenos, Techcombank used an in-house developed solution that, while adequate for its needs at the time, would have inhibited its ambitious future growth plans.

Techcombank’s legacy solution consisted of 12 separate instances of a Foxpro-based accounting system - one at each branch - which was used for manually recording all transactions and was supported by a separate SWIFT and Local Clearing House system (CITAD).

The first significant problem with this decentralised system was the quality and timeliness of management information. Because each branch had its own separate system, each branch had a separate close of day reconciliation. Management would only (and could only) see a complete view of the business once a month, when consolidated management accounts were prepared.

The second major problem with the system, and which precipitated Techcombank’s decision to replace it, was that it only offered single-branch banking for customers. That is, a customer with an account in one branch could only access the account in that same branch: trying to withdraw money or pay a bill at a different Techcombank branch was impossible.

Temenos Case Study06

Partnering With Temenos For Core Banking Software

“T24 has both facilitated and cemented our technological leadership in this market”Mr Le Xuan VU - CIO - Techcombank

The Need For A New System

Initial Selection And Implementation

Temenos Case Study07

EDM

SWIFT Visa / Mastercard Interbank Clearing

ACH

Stock Exchange

Statement / Report Printing

EFTPOS Information FeedsT 24

InternetCall

CentreCredit Cards

EDI ATMVoice Unit

Home/ Office

POSMobile

UnitPalm Units

External Access External Servicing Remote Acess

T24 Applications Interfaces Ancillary Applications

Current IT System

T24 Is Supported By Just 3 Ancillary Applications: Transware Card, Avaya Call Centre And A Content Management System

Since going live with T24 in 2003, Techcombank has made multiple additional investments to the platform, to upgrade its technology and functionality and to extend its usage.

• In 2004, Techcombank upgraded to the latest version of Globus, G13. This took a team from Techcombank 4 months.• In 2005, Techcombank upgraded to the latest release of the software, which had been renamed to T24. This took a joint team from Temenos and Techcombank 2 months.• In 2006, Techcombank upgraded to the next release of T24, R05. As Techcombank had by this time developed greater expertise on the product, they were able to manage the upgrade using only internal resources and in just 2 months.• In 2007, Techcombank – again without assistance from Temenos – upgraded to R07, which also included taking an additional module, for management reporting.• In 2009, Techcombank installed T-Risk, Temenos’ solution for the Basel II regulations.• Techcombank’s next project, which will start by the end of 2009 and run into 2010, is to upgrade from R07 to R09 and, at the same time, move from Temenos Internet Banking (TIB) to ARC Internet Banking.

“Techcombank is a sophisticated Temenos customer. They have developed a very high level of internal competence on T24, which enables them to upgrade without outside assistance and, in addition, allows them to exploit the existing functionality to run ever greater parts of the bank.”Mr Chris Longden - Regional Director Asia Pacific - Temenos

Sustained Investment

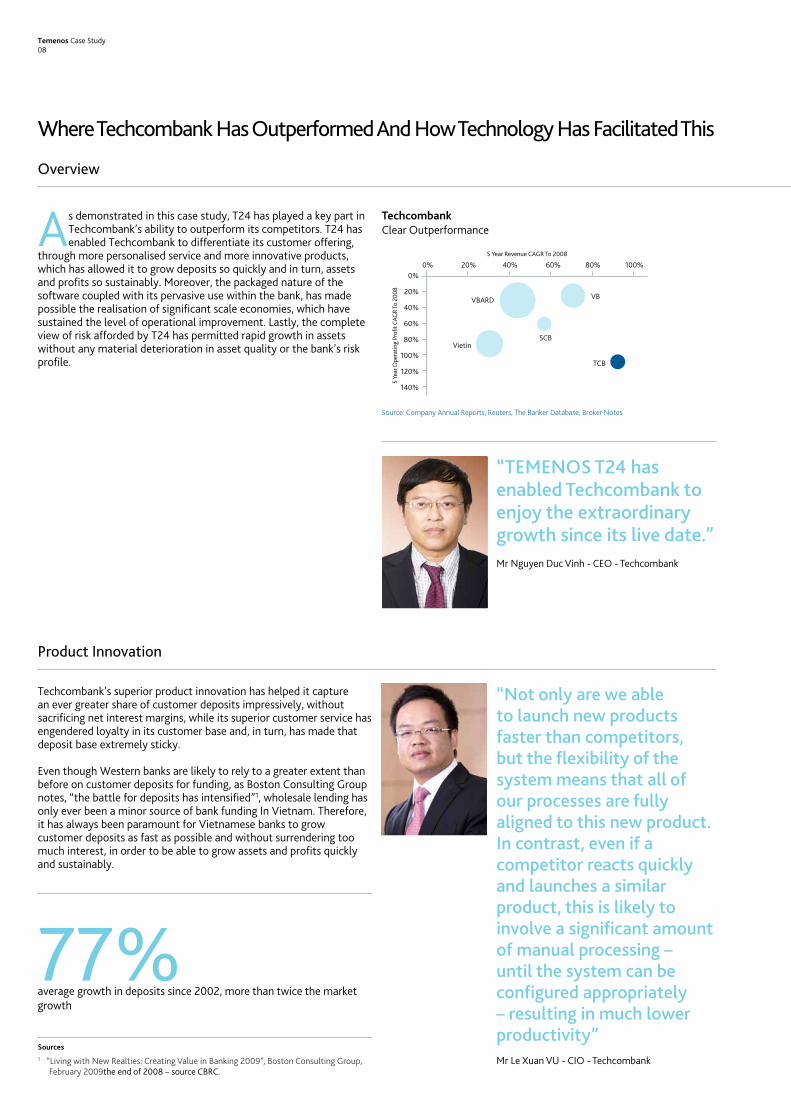

As demonstrated in this case study, T24 has played a key part in Techcombank’s ability to outperform its competitors. T24 has enabled Techcombank to differentiate its customer offering,

through more personalised service and more innovative products, which has allowed it to grow deposits so quickly and in turn, assets and profits so sustainably. Moreover, the packaged nature of the software coupled with its pervasive use within the bank, has made possible the realisation of significant scale economies, which have sustained the level of operational improvement. Lastly, the complete view of risk afforded by T24 has permitted rapid growth in assets without any material deterioration in asset quality or the bank’s risk profile.

Techcombank’s superior product innovation has helped it capture an ever greater share of customer deposits impressively, without sacrificing net interest margins, while its superior customer service has engendered loyalty in its customer base and, in turn, has made that deposit base extremely sticky.

Even though Western banks are likely to rely to a greater extent than before on customer deposits for funding, as Boston Consulting Group notes, “the battle for deposits has intensified”1, wholesale lending has only ever been a minor source of bank funding In Vietnam. Therefore, it has always been paramount for Vietnamese banks to grow customer deposits as fast as possible and without surrendering too much interest, in order to be able to grow assets and profits quickly and sustainably.

Where Techcombank Has Outperformed And How Technology Has Facilitated This

Sources1 “Living with New Realties: Creating Value in Banking 2009”, Boston Consulting Group,

February 2009the end of 2008 – source CBRC.

Temenos Case Study08

0%

20%

40%

60%

80%

100%

120%

140%

0% 20% 40% 60% 80% 100%

Vietin

VBARD VB

TCB

SCB

5 Year Revenue CAGR To 2008

5 Ye

ar O

pera

ting

Profi

t CAG

R To

200

8

Techcombank Clear Outperformance

Source: Company Annual Reports, Reuters, The Banker Database, Broker Notes

“TEMENOS T24 has enabled Techcombank to enjoy the extraordinary growth since its live date.”Mr Nguyen Duc Vinh - CEO - Techcombank

“Not only are we able to launch new products faster than competitors, but the flexibility of the system means that all of our processes are fully aligned to this new product. In contrast, even if a competitor reacts quickly and launches a similar product, this is likely to involve a significant amount of manual processing – until the system can be configured appropriately – resulting in much lower productivity”Mr Le Xuan VU - CIO - Techcombank

77%average growth in deposits since 2002, more than twice the market growth

Product Innovation

Overview

The root of Techcombank’s success in growing deposits faster than competitors has been product innovation. While growth in branches has also been vital (and T24 has facilitated this branch expansion in that it has allowed the bank to leverage its existing IT infrastructure), most of the Joint Stock Banks have been growing their branch network at rates similar or higher than Techcombank.

Techcombank has taken advantage of the flexibility and parameterisation of T24 to build innovative products and launch products quickly. The highly parameterised nature of the system allows Techcombank to create products without any assistance from Temenos while the flexibility of the system enables the IT department to align processes very quickly to fit the product specifications. Techcombank has acted to reduce further the time it takes to launch new products by establishing a very tight working relationship between the product management team and the product implementation team. Now, it is possible for Techcombank to configure, test and launch a new product within 24 hours, although in practice, with User Acceptance Testing, the fastest a product has been launched to date is within two and half days.

It is possible for Techcombank to configure, test and launch a new product within 24 hours

Many of the products or promotions that Techcombank has launched have either been truly pioneering – like “Life Insurance Savings”, a product that incentivised savers to make long-term deposits by offering free life insurance for the whole period of the deposit- or have been faster to market and so captured a larger share of opportunities thrown up by market changes. As an example of the latter, in response to the Central Bank doubling the reserve requirements for short-term deposits in June 2007, competition for deposits intensified further and Techcombank launched, within 8 working days, its “Deposit at Techcombank, Win a Mercedes” product, which boosted depositor numbers significantly. In fact, within 1 month, this product alone had increased total depositor numbers by about 5% and within 6 months, by nearly 20%, helping contribute to the 156% growth in deposits in 2007 (compared to the aggregate market growth of 50%)3.

Temenos Case Study09

What is more, this growth in deposits was not achieved by expensive promotions or by offering above-market interest rates, as can be evidenced by the fact that the net interest margin (NIM) has been relatively stable over the period and, moreover, the existence of a government-imposed ceiling rate for deposits and loans also limits this kind of aggressive or promotional activity.

70,000

60,000

50,000

40,000

30,000

20,000

10,000

0 1 2 3 4 5 6

Months Since Launch

Cum

ulat

ive

Cus

tom

er N

umbe

rs

Take Up Of “Win Mercedes” Savings Product Cumulative Growth In Customer Contracts By Month Following Launch

Source: Techcombank Data

Sources2 “Banking Industry Analysis Report”, Bao Viet Securities Joint-Stock Company, dated July 2008 3 ibid

According to Bao Viet Securities2, aggregate customer deposits grew at an average rate of 34% over the period 2002-2008. Over the same period, Techcombank grew its customer deposits by an average of 77%, more than twice the rate of the total market and significantly faster than most of its main competitors - see adjoining graphic.

40,000

35,000

30,000

25,000

20,000

15,000

10,000

5,000

8.0%

7.0%

6.0%

5.0%

4.0%

3.0%

2.0%

1.0%

0.0%

5.3%

6.7%

6.6%

6.3%

7.5%

FY 04 FY 05 FY 06 FY 07 FY 08

Deposits NIM

VN

D b

n

Increase In Techcombank Deposits In Aboslute Terms (LHS) And NIM (RHS)

Source: Techcombank Annual Reports

TCB

VIB

SCB

HB

EXIM

ACB

VBARD

MHB

Vietin

VCB 6%

13%

28%

37%

48%

55%

59%

64%

66%

86%

6%

Deposit Growth Techcombank Vs Selected Competitors, 5 Year CAGR To 2008

Source: Company Annual Reports, Reuters, The Banker Database, Broker Notes

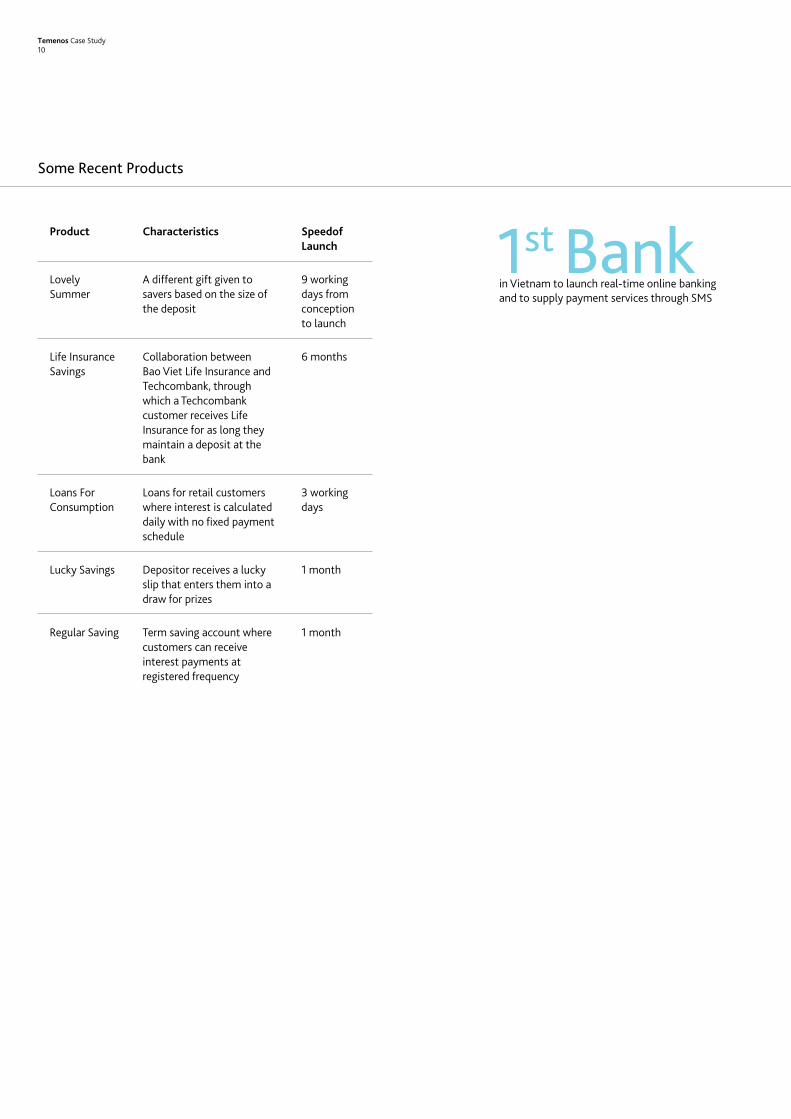

Some Recent Products

Temenos Case Study10

Product Characteristics Speedof Launch

Lovely Summer

A different gift given to savers based on the size of the deposit

9 working days from conception to launch

Life Insurance Savings

Collaboration between Bao Viet Life Insurance and Techcombank, through which a Techcombank customer receives Life Insurance for as long they maintain a deposit at the bank

6 months

Loans For Consumption

Loans for retail customers where interest is calculated daily with no fixed payment schedule

3 working days

Lucky Savings Depositor receives a lucky slip that enters them into a draw for prizes

1 month

Regular Saving Term saving account where customers can receive interest payments at registered frequency

1 month

1st Bank in Vietnam to launch real-time online banking and to supply payment services through SMS

Customer Service

Sources4 “Business as Usual? The Future of IT Investment in Retail Banking”, Datamonitor, March 2009

Temenos Case Study11

As with its products, Techcombank has taken advantage of the flexibility and customer centricity of T24 to launch cutting edge improvements in customer service. For instance, Techcombank

was the first bank in Vietnam to launch an authentic real-time online banking service for individuals, F@st i-Bank, while it was also the first bank in Vietnam to supply payment services through SMS. In fact, the range of mobile phone services offered by Techcombank – balance statement, money transfer, bill payment, account notifications (when salary paid, for example) and payment confirmations – is superior to that offered by most Western banks.

Techcombank has also capitalised on the complete customer view afforded by T24 to give better and more tailored customer service. For instance, it tailors its retail customer pricing to take account of individual customer profitability. So, if the net interest margin for a particular retail customer is more than 7% (across his or her entire portfolio of products), then the account manager is empowered to give discounts to this customer on future products (within certain parameters). This, therefore, serves as a very effective means of retaining and rewarding the bank’s best customers, as well as fostering cross-selling, which along with customer referrals (for which we have no statistics) are the highest sources of marginal profitability. In fact, while we know this is not the case at Techcombank, Datamonitor estimates that for most banks, it is only cross-selling and customer referrals that generate marginal profitability, since the cost of capture is so high if a customer is not referred and the cost to serve any customer is so high if not spread over many products4.

Techcombank tailors its retail customer pricing to take account of individual customer profitabilityOn a more basic level, having a single view of the customer should result in better (and more efficient) handling of all customer queries and greater cross-selling potential – since the bank employee is aware of all products the customer holds and the customer’s full history of correspondence, etc - and Techcombank has invested heavily in staff training to ensure that this is the case. So, for example, there is an increasingly blurred line between teller and account manager, branches are set out in such a way that allows for more comfortable interaction with the bank’s employees who are knowledgeable about the products available and so can perform both sales and service. Similarly, when a customer calls the bank’s 24-hour call centre, the staff have been trained to be able to deal with most queries, including the completion of complicated documentation, like certificates of origin for export.

Independent market research confirms that Techcombank consistently scores higher than its rivals in customer service

The innovative, personalised and efficient customer service offered by Techcombank has clearly translated into high customer satisfaction levels. In addition to the awards that Techcombank has won for its customer service – such as “the Most Satisfied Services in 2008” voted by readers of Sai Gon Tiep Thi Magazine – independent market surveys confirm that Techcombank scores consistently higher than its main rivals, Joint Stock Banks like Asia Commercial Bank (ACB) and East Asia Commercial Bank (EAB).

More personalised and efficient customer service has also resulted in growth in profitability per customer. In 2007 and 2008, Techcombank increased absolute customer numbers by 94% and 83%, respectively, but increased pre-tax profitability faster - by 148% and 125% in 2007 and 2008, respectively. This means that profitability per customer has grown on average more than 25% in the last two years.

70

60

50

40

30

20

10

0 Q3 2008 Q4 2008 Q1 2009

ACB

SCB

EAB

TCB

Source: Cimigo, Independent Market Researchers

Data From Customer Satisfaction Surveys Held Between Q3 2008 And Q1 2009

25%average growth in revenue/customer in the last two years

“Having a customer-centric, rather than product-centric, banking system allows us to tailor our service for individual customers”Mr Nguyen Duc Vinh - CEO - Techcombank

Temenos Case Study12

Economies Of Scale

Over recent years, Techcombank has been able to extract significant IT synergies by leveraging its modern, integrated core banking infrastructure. Despite the significant and sustained investment that Techcombank has made in its IT systems (see earlier section) and despite its clear technology leadership in the Vietnamese market, the fact is that investment in IT, as a percentage of both revenues and costs, has been falling.

As already explained, Techcombank has built up the expertise on T24 to be able to launch new products in a day, configure the IT systems for a new branch in an hour and upgrade themselves to the latest release of the software (without external help) in two months. In this context, it has not been necessary to increase IT headcount as the same rate as, for example, customer-facing branch staff and, accordingly, the ratio of IT staff/all staff has fallen from 5% in 2006 to 3% in 2008.

Similarly, various other measures of IT efficiency have also improved considerably over the last few years. For example, IT cost to income – which is a fairer measure of efficiency than IT staff/all staff in that it also captures spend on local contractors who maintain hardware at branches more than 100km from Hanoi - has fallen to 1.5%. This is 84% lower than the European industry average of 9.5%5.

Perpetual Improvement In Efficiency And Productivity

Techcombank runs a continuous improvement programme aimed at raising the level of process automation within the bank’s operations centre by building interfaces between T24 and ancillary applications to allow immediate and automatic data transfer or by removing manual intervention in process workflows. In 2008, the Operations Center undertook 75 initiatives to improve efficiency and productivity, which resulted in a 3% reduction in staffing levels. In the first half of 2009, the Operations Center completed 21 initiatives leading to a 60% reduction in error rates compared with 2008.

Even though Techcombank has made very significant improvements in profitability by customer, the improvement in profitability by employee is even more impressive. In 2007, profitability per employee increased by 34% (compared to a 28% increase in profitability per customer), while in 2008, profitability by employee grew by 64%, compared to a 23% increase in profitability per customer.

140

120

100

80

60

40

20

0TCB Raffeissen BP Erste BCP Natixis Postbank

2008 Cost/Income Ratio Techcombank vs Selected International Retail Banks

Source: Company Annual Reports, Reuters, The Banker Database, Broker Notes

80

70

60

50

40

30

20

10

0HB TCB ACB EXIM SCB Average STB Vietin VBARD VIB An Binh

2008 Cost/Income Techcombank Compared To Vietnamese Peers

Source: Company Annual Reports, Reuters, The Banker Database, Broker Notes

Sources5 See Boston Consulting Group’s Third Annual IT Cost Benchmarking Study from May 2006

“At Techcombank, we are committed to a culture of perpetual improvement in efficiency and productivity.”Mr Trung Van Nguyen - Director of Operations Centre - Techcombank

Operational Efficiency

“Having a centralised and modern IT infrastructure allows us to gain significant economies of scale as we grow” Mr Le Xuan Vu - CIO - Techcombank

84%lower Techcombank’s IIT cost/income compared to industry average

64%the increase in profitability per employee in 2008

Temenos Case Study13

Improved Management Information

As part of its ongoing investment programme, Techcombank has carried out several projects to enhance the quality and timeliness of management reporting by making better use of T24’s integrated data set and structure. These projects have ranged from minor, incremental enhancements, like using the T24 end-user tools to define new value adding reports, to the implementation in 2007 of the T24 management reporting module.

With the introduction of this management reporting module, Techcombank is able to get much more granular information, in particular regarding profitability, to inform decision-making. For example, Techcombank now tracks profitability by customer, by product, by line of business (treasury, corporate, retail) and by branch and, as already discussed, the bank is actively making use of this information to determine its customer pricing. It also uses the information to influence its risk strategy (see later), its product promotions and investments, any variations in regional pricing and its divisional investment decisions. In order for this information to be valuable, it has to be precise, so in generating these marginal profitability figures, Techcombank uses more than 20 drivers for each. In the case of profitability by product, for instance, Techcombank allocates costs on the basis of number of transactions, channel mix of transactions (and costs of the same) and processing time.

Techcombank is currently undertaking a project to be able to generate profitability by Relationship Manager.

IT Cost as % of Income

1.5%

9.5%

5.5%

13%

8 bps

23 bps

IT Cost as % of Cost

IT Cost as % of Assets

TCB

TCB

TCB

IND

UST

RY

IND

UST

RY

IND

UST

RY

Source: Techcombank, BCG

IT Efficiency Techcombank Compared To European industry Average For Several Metrics

“At Techcombank, we have a conservative approach to risk, which, to a certain extent, T24 has helped us to embed across the company. But, where T24 really adds value is by giving us a global view of risk, both at the customer level and the total bank level.”Ms Ly Huong Thi Le - Manager - Credit Risk Department - Techcombank

Temenos Case Study14

As already mentioned, Techcombank has grown revenues and profits faster than any other bank in Vietnam, but not at the expense of risk management.

Comparing Techcombank to peers, it is clear that its loan book grew faster than the market average over recent years, at a compound annual rate of 65% vs. we estimate 52.5% for the overall market. However, because of its success in growing deposits, its ratio of loans to deposits, a key measure of risk, has actually been falling for the last 3 years.

Furthermore, the percentage of non-performing loans in 2008 was marginally down on 2006 levels, reflecting Techcombank’s conservative lending practices, anchored in detailed assessments of credit scoring, customer payment history and the quality of collateral.

Where T24 has helped Techcombank, in addition to helping to speed up and automate many of its risk assessment processes, is by giving a complete view of risk. This is true both at the macro, bank level – where producing reports of total loan exposure, for example, takes less than hour – as well as at the micro customer and counterparty level – where total individual client exposure can be seen in real-time, while assessing risk to any one counterparty takes less than 15 minutes.

There abound cases of where Techcombank has capitalised on this global view of risk. For instance, Techcombank has been able to use its complete view of loans and deposit arrangements to establish a better match of the time duration of the same. As an example, it recently began to offer better time deposit rates to customers in Southern Vietnam to incentivise them to make bigger and longer duration deposits in order to match the typically longer duration loans taken in Southern Vietnam compared to provinces in the North.

Risk Management

Vietin

VBARD

VB

MHB

SCB

Average

TCB

VIB

0% 50% 100% 150% 200 %

Loan Growth Techcombank Vs Selected Domestic Peers, 5 Year CAGR To 2008

Source: Company Annual, Reuters, Broker Notes

2008 Ratio Of Loans To Deposits Techcombank Vs Selected Domestic And International Peers

Source: Company Annual Reports, Reuters, The Banker Database, Broker Notes

SBITSCB

EXIM TCBACB

Post HB VID

B VB

VBARD

Vietin

Erste

Natixis

MHB BCP

BP

1.4 1.4 1.3

1.11.1

1.0 1.0 0.9 0.9 0.9 0.9 0.80.7 0.7 0.7

0.5

Temenos Case Study15

T echcombank has always been an ambitious bank with a clear understanding of the value that technology can bring in differentiating and growing its business.

In 2001, after a detailed selection process involving local and international vendors, Techcombank selected T24 as its core banking platform.

Since T24’s installation at the bank, Techcombank has made significant incremental investments in the system, extending the usage of the product across more parts of the bank, while taking new releases to ensure its functionality and technology remain up-to-date.

The selection and subsequent sustained investment in T24 has facilitated Techcombank’s extraordinary growth of recent years.

The ability to launch more innovative products than peers and more quickly has enabled Techcombank to grow its deposits faster than any other bank in Vietnam, at a CAGR of 72% over the last five years.

The ability to tailor services to individual customer requirements has translated into the highest customer satisfaction of any Joint Stock Bank as well as strong cross-selling and repeat business: revenue per customer has increased by more than 25% on average over the last two years.

Having a modern and scalable system has allowed Techcombank to extract significant operational efficiencies as it has grown: IT cost/income stands at 1.5%, 84% below the industry average.

Lastly, having a robust system with a complete view of risk has allowed Techcombank to grow revenues without sacrificing risk management. The percentage of non-performing loans in 2008 was 3% lower than in 2006 despite a 199% growth in loans over the same period.

Summary

Raffeissen

BCP

Erste

POST

TCB

MHB

EXIM

Vietin

VB

ACB

SCB

0% 5.0% 10.0% 15.0% 20.0 % 25.0% 30.0% 35.0%

Source: Company Annual Reports, Reuters, The Banker Database, Broker Notes

2008 Return On Equity Techcombank Vs Selected Domestic And International Peers

Temenos Case Study16

Glossary Of Abbreviations

ACB Asia Commercial BankBCP Banco Commercial PortuguesBP Banco PopulareCAGR Compound Annual Growth RateEAB Eastern Asia Commercial BankEXIM Vietnam Eximbank (Export – Import JS Commercial Bank)HB Habubank (Hanoi Building JS Commercial Bank)MHB Housing Bank Of MekongNIM Net Interest MarginPost Deutsche PostbankSBIT Saigon Bank For Industry And TradeSCB Sacombank (Saigon Thuong Tin Commercial Bank)STB Saigon Hanoi Commercial BankTCB TechcombankVB Joint Stock Bank For Foreign Trade Of VietnamVBARD Vietnam Bank For Agriculture And Rural Development VIDB Vietnam Investment And Development BankVietin Vietnam International Bank

Appendix

Temenos Case Study17

AuthorBen Robinson is Director of Strategic Planning at Temenos, based in the Geneva Headquarters. He can be contacted by email at [email protected]

Nathan Pillai is a senior financial analyst, based in Temenos’ offices in Chennai.

Further ContactFor more information about Temenos’ products or to arrange a product demonstration, please contact [email protected]

For information regarding re-use of this publication or to obtain other recent studies, please contact [email protected]

For general enquiries, please visit our website www.temenos.com

About TemenosFounded in 1993 and listed on the Swiss Stock Exchange (SIX: TEMN),Temenos Group AG is a global provider of banking software systemsin the Retail, Corporate & Correspondent, Universal, Private, Islamicand Microfinance & Community banking markets. Headquarteredin Geneva with 67 offices worldwide, Temenos serves over 1100customers in more than 120 countries. Temenos’ software productsprovide advanced technology and rich functionality, incorporatingbest practice processes that leverage Temenos’ experience in over600 implementations around the globe. Temenos’ advanced andautomated implementation approach, provided by its strong ClientServices organisation, ensures efficient and low-risk core bankingplatform migrations. Temenos is top of the IBS Sales League Table2009; winner every year since its launch of the Best Core BankingProduct in Banking Technology magazine’s Readers’ Choice Awardsand ranks 26th in the American Banker top 100 FinTech companies.Temenos customers are proven to be more profitable than theirpeers: data from The Banker – top 1000 banks shows that Temenoscustomers enjoy a 54% higher return on assets, a 62% higher returnon capital and a cost/income ratio that is 7.2 points lower than non-Temenos customers.

Disclaimer - Temenos This case study is based on selected information available in the public domain and provided by the bank, upon which we have placed reasonable reliance. In arriving at our conclusions regarding Bank of Shanghai’s performance compared to domestic peers, we have analysed the data from more than 20 Joint Stock Banks and City Commercial Banks, whom we judged to have similar absolute asset bases and, accordingly, whose performance we believe is directly comparable.

www.temenos.com

TEMENOS™, TEMENOS ™, TEMENOS T24™ and ™ are registered trademarks of Temenos Headquarters SA

©2011 Temenos Headquarters SA - all rights reserved.

Warning: This document is protected by copyright law and international treaties. Unauthorised reproduction of this document, or any portion of it, may result in severe and criminal penalties, and will be prosecuted to the maximum extent possible under law.

Temenos Headquarters SA

2 Rue de l’Ecole-de-ChimieCH - 1205 GenevaSwitzerlandTel: +41 22 708 1150Fax: +41 22 708 1160

201108002