CASE NO. SC05-168 SUPREME COURT OF FLORIDA VECTOR PRODUCTS ... · supreme court of florida _____...

42

14341682v1 833598 CASE NO. SC05-168 _________________ IN THE SUPREME COURT OF FLORIDA _________________ VECTOR PRODUCTS, INC. D/B/A VECTOR MANUFACTURING LTD. APPELLANT, VS. HARTFORD FIRE INSURANCE COMPANY APPELLEE. ___________________ ON CERTIFICATION FROM THE UNITED STATES COURT OF APPEALS FOR THE ELEVENTH CIRCUIT ____________________ ANSWER BRIEF OF APPELLEE, HARTFORD FIRE INSURANCE COMPANY ____________________ HINSHAW & CULBERTSON, LLP RONALD L. KAMMER (BAR NO. 360589) ANDREW E. GRIGSBY (BAR NO. 328383) MAUREEN PEARCY (BAR NO. 0057932) SINA BAHADORAN (BAR NO. 523364 9155 S. DADELAND BLVD., SUITE 1600 MIAMI, FL 33156 PHONE: (305) 358-7747 FAX: (305) 577-1063 ATTORNEYS FOR APPELLEE, HARTFORD FIRE INS. COMPANY

Transcript of CASE NO. SC05-168 SUPREME COURT OF FLORIDA VECTOR PRODUCTS ... · supreme court of florida _____...

14341682v1 833598

CASE NO. SC05-168

_________________

IN THE SUPREME COURT OF FLORIDA

_________________

VECTOR PRODUCTS, INC.

D/B/A VECTOR MANUFACTURING LTD.

APPELLANT,

VS.

HARTFORD FIRE INSURANCE COMPANY

APPELLEE.

___________________

ON CERTIFICATION FROM THE UNITED STATES COURT OF APPEALS FOR THE ELEVENTH CIRCUIT

____________________

ANSWER BRIEF OF APPELLEE, HARTFORD FIRE INSURANCE COMPANY

____________________

HINSHAW & CULBERTSON, LLP RONALD L. KAMMER (BAR NO. 360589) ANDREW E. GRIGSBY (BAR NO. 328383) MAUREEN PEARCY (BAR NO. 0057932) SINA BAHADORAN (BAR NO. 523364 9155 S. DADELAND BLVD., SUITE 1600 MIAMI, FL 33156 PHONE: (305) 358-7747 FAX: (305) 577-1063

ATTORNEYS FOR APPELLEE, HARTFORD FIRE INS. COMPANY

i 14341682v1 833598

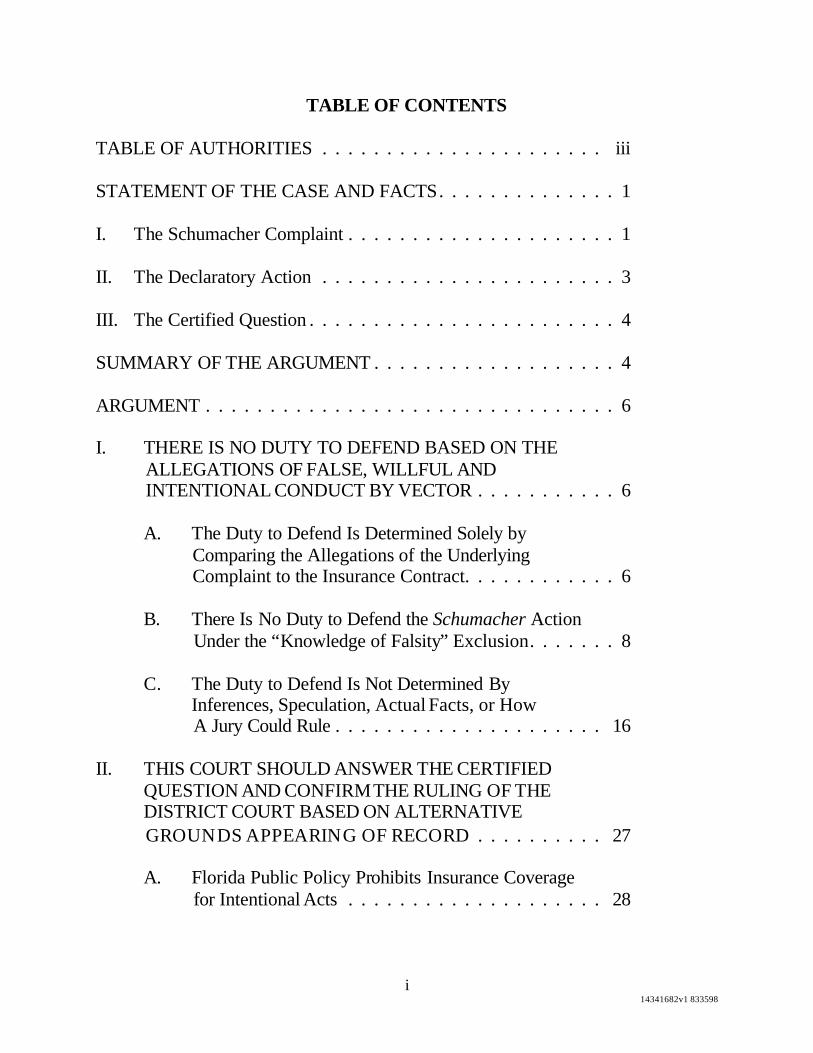

TABLE OF CONTENTS TABLE OF AUTHORITIES . . . . . . . . . . . . . . . . . . . . . . iii STATEMENT OF THE CASE AND FACTS. . . . . . . . . . . . . . 1 I. The Schumacher Complaint . . . . . . . . . . . . . . . . . . . . . 1 II. The Declaratory Action . . . . . . . . . . . . . . . . . . . . . . . 3 III. The Certified Question . . . . . . . . . . . . . . . . . . . . . . . . 4 SUMMARY OF THE ARGUMENT . . . . . . . . . . . . . . . . . . . 4 ARGUMENT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6 I. THERE IS NO DUTY TO DEFEND BASED ON THE ALLEGATIONS OF FALSE, WILLFUL AND INTENTIONAL CONDUCT BY VECTOR . . . . . . . . . . . 6 A. The Duty to Defend Is Determined Solely by Comparing the Allegations of the Underlying Complaint to the Insurance Contract. . . . . . . . . . . . 6 B. There Is No Duty to Defend the Schumacher Action Under the “Knowledge of Falsity” Exclusion. . . . . . . 8 C. The Duty to Defend Is Not Determined By Inferences, Speculation, Actual Facts, or How A Jury Could Rule . . . . . . . . . . . . . . . . . . . . . 16 II. THIS COURT SHOULD ANSWER THE CERTIFIED QUESTION AND CONFIRM THE RULING OF THE DISTRICT COURT BASED ON ALTERNATIVE GROUNDS APPEARING OF RECORD . . . . . . . . . . 27

A. Florida Public Policy Prohibits Insurance Coverage for Intentional Acts . . . . . . . . . . . . . . . . . . . . 28

ii 14341682v1 833598

B. The Claim Is Excluded from Coverage Under the “Intent to Injure” Exclusion . . . . . . . . . . . . . . . 30 C. The Underlying Claim Is Not a Covered “Advertising Injury”. . . . . . . . . . . . . . . . . . . . 31 CONCLUSION. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32 CERTIFICATE OF SERVICE . . . . . . . . . . . . . . . . . . . . . 33 CERTIFICATE OF COMPLIANCE . . . . . . . . . . . . . . . . . . 34

iii 14341682v1 833598

TABLE OF AUTHORITIES

Federal Cases: ABC Distrib., Inc. v. Lumbermens Mut. Ins. Co., 646 F.2d 207, 209 (5th Cir. 1981) ………………………………………………………………….7 Adolfo House Distrib. Corp. v. Travelers Prop. & Cas. Ins. Co., 165 F.Supp.2d 1332, 1341 (S.D. Fla. 2001) ……………………………….12, 16 Aerosonic Corp. v. Trodyne Corp., 402 F.2d 223, 231 (5th Cir. 1968) ………….31 Allstate Ins. Co. v. Travers, 703 F.Supp. 911, 913 (N.D. Fla. 1988) …………25, 27 American Home Assur. Co. v. United Space Alliance, LLC, 378 F.3d 482 (5th Cir. 2004) ………………………………………………………………….22 American States Ins. Co. v. Pioneer Elec., 85 F.Supp.2d 1337, 1343 (S.D. Fla. 2000) ……………………………………………………………….25 Amerisure Ins. Co. v. Laserage Tech. Corp., 2 F.Supp.2d 296, 302 (W.D.N.Y. 1998) …………………………………………………………..11, 12 Auto Owners Ins. Co. v. Travelers Cas., & Sur. Co., 227 F.Supp.2d 1248, 1258 (M.D. Fla. 2002) …………………………………………………..17 Bay Elec. Supply, Inc. v. Travelers Lloyds Ins. Co., 61 F.Supp.2d 611 (S.D. Tex. 1999) ……………………………………………………………….12 Boosey & Hawkes Music Publishers, Ltd. v. Walt Disney Co., 145 F.3d 481, 493 (2d Cir. 1998) ……………………………………………9, 19 Cent. Mut. Ins. Co. v. Stunfence, Inc., 292 F.Supp.2d 1072 (N.D. Ill. 2003) …………………………………………………………….11, 12 Cincinnati Ins. Co. v. Eastern Atl. Ins. Co., 260 F.3d 742 (7th Cir. 2001) …………………………………………………………………21 Davidoff & CIE, S.A. v. PLD Int'l Corp., 263 F.3d 1297, 1301 (11th Cir. 2001) ………………………………………………………………..29

iv 14341682v1 833598

Ekco Group, Inc. v. Travelers Indem. Co. of Ill., 2000 WL 1752829, at *3 (D.N.H. Nov. 29, 2000)……………………………………………….11, 12 Elcom Tech., Inc. v. Hartford Ins. Co. of the Midwest, 991 F.Supp. 1294, 1295-96, 1298 (D. Utah 1997) …………………………………………..12 Finger Furniture Co. v. Travelers Indem. Co. of Conn., 2002 WL 32113755 (S.D. Tex. 2002) ……………………………………………………13 Lime Tree Vill. Cmty. Club Ass'n v. State Farm Gen. Ins. Co., 980 F.2d 1402 (11th Cir. 1993) …………………………………………..22, 23 Mulberry Square Prod., Inc. v. State Farm Fire & Cas. Co., 101 F.3d 414 (5th Cir. 1996)……………………………………………………10 Ohio Cas. Co. v. Cont'l Cas. Co., 279 F.Supp.2d 1281, 1284 (S.D. Fla. 2003) ………………………………………………………………..30 Park Place Entm't Corp. v. Transcon. Ins. Co., 225 F.Supp.2d 406, 411-12 (S.D.N.Y. 2002) ……………………………………………………….21 Planetary Motion, Inc. v. Techsplosion, 261 F.3d 1188, 1193 (11th Cir. 2001) ………………………………………………………………..15 Porous Media Corp. v. Pall Corp., 110 F.3d 1329, 1332-33 (8th Cir. 1997) ………………………………………………………………9, 19 Union Ins. Co. v. The Knife Co., Inc., 897 F.Supp. 1213, 1217 (W.D. Ark. 1995) ………………………………………………………..11 Utica Mut. Ins. Co. v. David Agency Ins., Inc., 327 F.Supp.2d 922 (N.D. Ill. 2004) ………………………………………………………………..21 Vector Products, Inc. v. Hartford Fire Ins. Co., 397 F. 3d 1316, 1321 (11th Cir.

2005) ………………………………………………………………………….....4 Wackenhut Servs., Inc. v. Nat'l Union Fire Ins. Co. of Pittsburgh, 15 F.Supp.2d 1314 (S.D. Fla. 1998) ………………………..10, 14, 15, 16, 17, 27

v 14341682v1 833598

State Cases: Allstate Ins. Co. v. Novak, 313 N.W. 2d 636 (Neb. 1981) ………………………..21 Allstate Ins. Co. v. Shofner, 573 So.2d 47, 50 (Fla. 1st DCA 1990) ……………..30 Amerisure Ins. Co. v. Gold Coast Marine Distrib., Inc., 771 So.2d 579, 580 (Fla. 4th DCA 2000) …………………………………………………..4 Baron Oil Co. v. Nationwide Mut. Fire Ins. Co., 470 So.2d 810, 814-15 (Fla. 1st DCA 1985) ……………………………………………….25, 27 Barry Univ., Inc. v. Fireman's Fund Ins. Co. of Wis., 845 So.2d 276, 278 (Fla. 3d DCA 2003) ……………………………………………………22, 26 Broadhead v. Scott, 497 So.2d 1081 (La. Ct. App. 1987)………………………...21 Capoferri v. Allstate Ins. Co., 322 So.2d 625, 627 (Fla. 3d DCA 1975) …………………………………………………………7, 26 Chicago Title Ins. Co. v. CV Reit, Inc., 588 So.2d 1075, 1075-76 (Fla. 4th DCA 1991) …………………………………………………….7, 17, 18 Cosser v. One Beacon Ins. Group, 789 N.Y.S.2d 586, 587-88 (N.Y. App. Div. 2005) ……………………………………………………..11, 12 Deni Ass'n of Fla., Inc. v. State Farm Fire & Cas. Ins. Co., 711 So.2d 1135, 1140 (Fla. 1998) ……………………………………………..22 Dade County Sch. Bd. v. Radio Station WQBA, 731 So.2d 638, 644-45 (Fla. 1999)……………………………………………………………6, 27 Estate of Bombolis v. Cont'l Cas. Co., 740 So.2d 1229, 1230 (Fla. 4th DCA 1999) ………………………………………………………….30 Fed. Ins. Co. v. Appelstein, 377 So.2d 229, 230 (Fla. 3d DCA 1979) …….7, 22, 25 Ferguson v. Birmingham Fire Ins. Co., 460 P.2d 342 (Or. 1969) ……………….21 Fun Spree Vacations v. Orion Ins. Co., 659 So.2d 419, 421

vi 14341682v1 833598

(Fla. 3d DCA 1995) …………………………………………………….7, 17, 19 Gray v. Zurich Ins. Co., 419 P.2d 168 (Cal. 1966) ……………………………….21 Lindheimer v. St. Paul Fire & Marine Ins. Co., 643 So.2d 636, 639 (Fla. 3d DCA 1994) ……………………………………………………………28 Mason v. Fla. Sheriff's Self-Ins. Fund, 699 So.2d 268 (Fla. 4th DCA 1997) ……………………………………………………………28 Nat'l Union Fire Ins. Co. v. Lenox Liquors, Inc., 358 So.2d 533, 536 (Fla. 1977) ………………………………………………..5, 7, 17, 22, 25, 26 PG Ins. Co. of N.Y. v. S.A. Day Mfg. Co., Inc., 251 A.D.2d 1065, 674 N.Y.S.2d 199 (N.Y. App. Div. 1998) …………………………………11, 12 Popp v. Cash Station, Inc., 613 N.E.2d 1150, 1156-57 (Ill. App. Ct. 1992) ……..29 Posigian v. American Reliance Ins. Co., 549 So.2d 751, 753-54 (Fla. 3d DCA 1989) …………………………………………………………….17 Quick v. State Farm Fire & Cas. Co., 488 So.2d 909, 910 (Fla. 1st DCA 1986) …………………………………………………………..30 Ranger Ins. Co. v. Bal Harbour Club, Inc., 549 So.2d 1005, 1008-09 (Fla. 1989) …………………………………………………………………28, 29 Reliance Ins. Co. v. Royal Motorcar Corp., 534 So.2d 922, 923 (Fla. 4th DCA 1988), rev. denied, 544 So.2d 200 (Fla. 1989) ………………7, 17 S.M. Brickell Ltd. P'ship v. St. Paul Fire & Marine Ins. Co., 786 So.2d 1204 (Fla. 3d DCA 2001) ………………………………………19, 20 State Farm Fire & Cas. Co. v. Compupay, 654 So.2d 944, 946-47 (Fla. 3d DCA 1995) 29 State Farm Fire & Cas. Co. v. Tippett, 864 So.2d 31, 36 (Fla. 4th DCA 2004) ……………………………………………………………28 Sunshine Birds & Supplies, Inc. v. U.S. Fid. & Guar. Co., 696 So.2d 907,

vii 14341682v1 833598

909-10 (Fla. 3d DCA 1997) …………………………………………………7, 17 Valencia v. Citibank Int'l, 728 So.2d 330, 330 (Fla. 3d DCA 1999) ……………..25

Federal Statutes: 15 U.S.C. §1125 …………………………………………………………………..1 28 U.S.C. §636 ……………………………………………………../…………….13

State Statutes: 815 ILCS 510/2(7), Ill. Unif. Deceptive Trade Practices Act ……………………..1

1 14341682v1 833598

STATEMENT OF THE CASE AND FACTS

This appeal involves the important question of whether this Court should

abolish the present test that an insurer’s duty to defend is determined solely by the

allegations of the complaint, and create a new standard requiring insurers to look

outside the four corners of the complaint and to consider mere speculation and

inferences. As demonstrated below, the Court should reject this ill-advised effort

to destabilize decades of established Florida law.

I. The Schumacher Complaint

Plaintiff, Vector Products, Inc. was sued by Schumacher Electric

Corporation (“Schumacher”) for “false advertising in violation of Section 43(a) of

the Lanham Act, 15 U.S.C. §1125(a) and the Illinois law prohibiting deceptive

trade practices and unfair competition.” Schumacher Electric Corp. vs. Vector

Products, Inc., No. 03C4410 (N.D. Ill.) (R. 85-175). The Schumacher complaint

sought injunctive relief and damages based on Vector’s “false representations of

fact” about the quality and performance of Vector’s product (R. 87- 88 ¶¶ 13-14).

Count I specifically alleged: “Vector has made such false statements

willfully and intentionally and with full knowledge of the falsity of such

statements” (R. 88 ¶ 15). This allegation was adopted in each count (R. 89 ¶¶ 20,

24). Count II alleged violation of the Illinois Uniform Deceptive Trade Practices

Act, 815 ILCS 510/2(7), incorporated the allegation of intentional conduct in

2 14341682v1 833598

paragraph 15, and further alleged: “Vector has undertaken these wrongful acts

willfully maliciously, and intentionally” (R. 89 ¶ 23). Count III alleged common

law unfair competition, incorporated paragraphs 15 and 23, and reiterated that

“Vector has undertaken these wrongful acts willfully maliciously, and

intentionally” (R. 90 ¶ 27).

The amended complaint1 repeated the theme that Vector intentionally made

statements it knew to be false. Again, Count I alleged that Vector “made such

false statements willfully and intentionally and with full knowledge of the falsity

of such statements” (R. 203 ¶ 16). Count II adopted the prior paragraphs,

including paragraph 16, and further alleged:

29. Vector’s representations in its promotional materials that the Vector Product is compliant with Part 15 of the FCC Rules is a false representation of a material fact.

30. Vector has made such false claim willfully and intentionally and with full knowledge of the falsity of such statement.

(R. 204, 206 ¶¶ 16, 29, 30, emphasis added). Count III again adopted all prior

paragraphs and further alleged in paragraph 38: “Vector has undertaken these

wrongful acts willfully, maliciously, and intentionally” (R. 207 ¶ 38). Last, Count

IV also adopted and realleged the prior paragraphs, and in paragraph 42 repeated

1 Reference to the “Schumacher complaint” from this point on refers to both

the original complaint and the first amended complaint.

3 14341682v1 833598

the allegation in paragraph 38 that “Vector has undertaken these wrongful acts

willfully maliciously, and intentionally” (R. 208 ¶¶ 38, 42).

As the complaints make clear, Schumacher only alleged that Vector engaged

in intentional, willful and malicious conduct and that Vector’s statements were

made with full knowledge that they were false (R. 85, 200). Schumacher did not,

for example, allege in the alternative that Vector’s conduct was unintentional or

that Vector knew or should have known that its statements were false.

Furthermore, each of the legal theories actually pled by Schumacher were solely

predicated on intentional conduct. Schumacher could have sought damages for

false advertising based on unintentional violations of the Lanham Act, but did not

(R. 85, 200).

II. The Declaratory Action

Vector notified defendant Hartford Fire Insurance Company (“Hartford”) of

the Schumacher action (R. 16, 178 ¶ 14). Hartford declined to defend

because the complaint did not allege an advertising injury, and also because

the allegations fell squarely into both the “knowledge of falsity” and “intent

to injure” exclusions. (R. 176). Vector filed this lawsuit against Hartford,

seeking a declaration of its rights and obligations under the insurance

policies and alleging breach of contract (R. 11-20). Hartford answered and

filed a counterclaim (R. 176-89). Hartford contested that the claims were

4 14341682v1 833598

covered under the polic ies (R. 179-81 ¶¶ 4-19), in part, due to the

“knowledge of falsity” and “intent to injure” exclusions (R. 179-80). The

district court granted Hartford’s motion for summary judgment, finding that

Hartford did not have a duty to defend Vector in the Schumacher litigation

because of the “knowledge of falsity” exclusion.

III. The Certified Question

Vector appealed the district court’s ruling to the Eleventh Circuit Court of

Appeals, which certified the following question to this Court:

Whether the Lanham Act § 43(a) claim, as pleaded in the Schumacher complaint, triggers either the intent to injure exclusion or the knowledge of falsity exclusion provided for in the Policies.

Vector Products, Inc. v. Hartford Fire Ins. Co., 397 F. 3d 1316, 1321 (11th Cir.

2005). In the certification, the Eleventh Circuit emphasized that “[o]ur phrasing of

the certified questions [sic] is merely suggestive and does not in any way restrict

the scope of the inquiry by the Supreme Court of Florida.” Id.

SUMMARY OF THE ARGUMENT

Florida law is clear. The duty to defend is determined strictly by comparing

the allegations of the complaint to the insurance policy. Despite Vector’s novel

attempts to the contrary, the duty to defend is not determined by inferences, actual

facts, speculation, theoretical claims, hypothetical damages, or how a jury could

rule. Amerisure Ins. Co. v. Gold Coast Marine Distrib., Inc., 771 So. 2d 579, 580

5 14341682v1 833598

(Fla. 4th DCA 2000); National Union Fire Ins. Co. v. Lenox Liquors, Inc., 358 So.

2d 533, 536 (Fla. 1977).

Vector’s new test has no basis in Florida law and would forever disrupt the

way insurers presently evaluate their defense obligation under insurance contracts

issued in this state. The district court properly granted summary judgment in favor

of Hartford. Hartford has no duty to defend Vector in the Schumacher litigation

based on the “knowledge of falsity” exclusion.

Although not required to do so under the Lanham Act, Schumacher clearly

and specifically pled purely intentional and knowing conduct by Vector.

Allegations of intent by a defendant in a Lanham Act claim may go to the issue of

whether the plaintiff is entitled to treble damages. Such allegations are also

relevant to the issue of deception or confusion of the public, one of the elements of

a Lanham Act claim. The Schumacher complaint alleges that Vector made false

statements and that such statements were made intentionally and willfully.

Accordingly, Hartford has no duty to defend Vector in the Schumacher action

because of the knowledge of falsity exclusion.

This Court should recognize that adopting Vector’s position would : (1)

abolish long-standing Florida law on the duty to defend, (2) eliminate the

“knowledge of falsity” and “intent to injure” exclusions from the insurance

contracts, and (3) require insurers to defend any action where an insured demands

6 14341682v1 833598

a defense on a theoretical, yet unasserted, legal theory. This Court should uphold

the established test for determining the duty to defend and answer the certified

question in the affirmative because Hartford has no duty to defend the Schumacher

complaint under the “knowledge of falsity” exclusion.

This Court should further find that Hartford has no duty to defend the

Schumacher litigation based on alternative grounds appearing of record. A court

may affirm on any basis appearing of record, despite the reasoning of the lower

court. Dade County Sch. Bd. v. Radio Station WQBA, 731 So. 2d 638, 644-45 (Fla.

1999). In this case, the district court’s judgment was correct on a number of

alternative grounds. First, because the complaint alleged knowing, willful and

intentional conduct, Florida public policy prohibits coverage for the action.

Second, the duty to defend was excluded by the “intent to injure” exclusion (R.

179-80). Last, the complaint does not allege an “advertising injury” covered under

the policy.

ARGUMENT

I. THERE IS NO DUTY TO DEFEND BASED ON THE ALLEGATIONS OF FALSE, WILLFUL AND INTENTIONAL CONDUCT BY VECTOR

A. The Duty to Defend is Determined Solely by Comparing the Allegations of the Underlying Complaint to the Insurance Contract.

Florida law is clear. Florida applies the bright-line test that the duty to

defend is determined strictly by comparing the allegations of the complaint to the

7 14341682v1 833598

insurance policy. See, e.g., Lenox Liquors 358 So. 2d at 535; Sunshine Birds &

Supplies, Inc. v. United States Fid. & Guar. Co., 696 So. 2d 907, 909-10 (Fla. 3d

DCA 1997); Fun Spree Vacations, 659 So. 2d at 421; Reliance Ins. Co. v. Royal

Motorcar Corp., 534 So. 2d 922, 923 (Fla. 4th DCA 1988), rev. denied, 544 So. 2d

200 (Fla. 1989); Chicago Title Ins. Co. v. CV Reit, Inc., 588 So. 2d 1075, 1075-76

(Fla. 4th DCA 1991); Capoferri v. Allstate Ins. Co., 322 So. 2d 625, 627 (Fla. 3d

DCA 1975); ABC Distrib., Inc. v. Lumbermens Mut. Ins. Co., 646 F.2d 207, 209

(5th Cir. 1981). To that end, “[n]o obligation to defend the action, much less to pay

any resulting judgment, arises when the pleading in question shows either the non-

existence of coverage or the applicability of a policy exclusion.” Federal Ins. Co.

v. Appelstein, 377 So. 2d 229, 230 (Fla. 3d DCA 1979) (citing Battisti v. Cont.

Cas. Co., 406 F.2d 1318, 1321 (5th Cir. 1969) (collected cases)).

In an effort to avoid the clear allegations of the complaint, Vector misstates

Florida law regarding the duty to defend and asks this Court to adopt a new test

which would require insurers to defend suits whenever claims that are not alleged

might some day create a potential for coverage. To adopt Vector’s test would

require a reversal of established precedent that the allegations of the complaint

determine an insurer’s duty to defend. Vector is requesting insurers to defend any

time an insured demands a defense, regardless of the allegations of the complaint

and based simply on the future possibility of amendment or proof. This Court

8 14341682v1 833598

should reject Vector’s invitation and continue to follow the reasoned approach that

an insurer’s duty to defend is determined by comparing the allegations of the

complaint to the insurance contract.

B. There Is No Duty to Defend the Schumacher Action Under the “Knowledge of Falsity” Exclusion.

Applying the test on the duty to defend to this case, and comparing the

Schumacher complaint with Hartford’s polic ies, it is clear that the claims are

excluded from coverage. Like the district court, this Court should also give

meaning to the “knowledge of falsity” exclusion and rule that Hartford does not

have a duty to defend Vector based on the controlling allegations of the complaint.

The Hartford policies expressly exclude coverage for “personal and

advertising injury” “arising out of oral, written or electronic publication of

material, if done by or at the direction of the insured with knowledge of its falsity.”

Significantly, in each count of the Schumacher complaint, the underlying plaintiff

expressly alleges that Vector made false representations of material fact and that

Vector made those false claims “intentionally and with full knowledge of the

falsity of such statement[s]” (R. 88 ¶¶13-15, 20, 23, 24, 27). Conversely, the

Schumacher complaint does not allege and does not seek relief based on any

purported unintentional act or any act that was done without knowledge of its

falsity. Thus, the allegations of the complaint fall squarely within the Hartford

policies’ “knowledge of falsity” exclusion.

9 14341682v1 833598

Both the original and amended complaints make it clear that Vector is

accused of false, willful and intentional conduct. In each count of the amended

complaint, Schumacher alleges that “Vector has made . . . false statements

willfully and intentionally and with full knowledge of the falsity of such

statements” (R. 203, 204, 207-08 ¶¶ 16, 21, 35, 39). Count II further alleges (and

these allegations are adopted in Counts III and IV):

29. Vector’s representations in its promotional materials that the Vector Product is compliant with Part 15 of the FCC Rules is a false representation of a material fact.

30. Vector has made such false claim willfully and intentionally and with full knowledge of the falsity of such statement.

(R. 206-07 ¶¶ 29-30, 35, 39) (emphasis added). In Counts III and IV, Schumacher

alleges: “Vector has undertaken these wrongful acts willfully, maliciously, and

intentionally” (R. 207 ¶¶ 38, 42, emphasis added).

Vector contends that allegations of intentionally conduct only address the

issue of punitive damages. However, allegations of intentional, willful and

knowing conduct by Vector can serve as a basis for establishing deception or

confusion of the consumer, one of the elements of a Lanham Act claim. Porous

Media Corp. v. Pall Corp., 110 F.3d 1329, 1332-33 (8th Cir. 1997) (recognizing

that a rebuttable presumption of deception is created where the jury finds that the

defendant acted deliberately to deceive); Boosey & Hawkes Music Publishers, Ltd.

v. Walt Disney Co., 145 F.3d 481, 493 (2d Cir. 1998) (holding in order for a

10 14341682v1 833598

plaintiff to obtain damages, he must prove actual consumer confusion or deception,

or that defendant acted intentionally to deceive raising rebuttable presumption of

confusion).

Unable to find any Florida court to support its novel position, Vector offers a

string of citations to suggest that the Court should disregard allegations of

intentional conduct in the complaint, ignore the knowledge of falsity exclusion and

instead, consider, conjecture, speculation and other materials outside the four

corners of the complaint (see Vector Brief at pp. 7-8 and note 5, pp. 15-17).

Vector claims that the cases it relies upon represent the majority position that

allegations of intent do not negate the duty to defend despite the “knowledge of

falsity” or “intent to injury” exclusions. Certainly five states is not the majority

position.

In its treatment, Vector notably fails to mention Wackenhut Servs., Inc. v.

National Union Fire Ins. Co. of Pittsburgh, 15 F. Supp.2d 1314 (S.D. Fla. 1998)

which, unlike its other cases, was decided under Florida law. The “knowledge of

falsity” exclusion precludes coverage where the complaint alleges willful and

intentional conduct by the insured. See, e.g., Mulberry Square Produc., Inc. v.

State Farm Fire & Cas. Co., 101 F.3d 414 (5th Cir. 1996) (finding no duty to

defend because “knowledge of falsity” exclusion precludes coverage for

11 14341682v1 833598

“intentional” conduct and allegations in the complaint specifically alleged that

insured “knew and intended” that its actions would result in certain consequences).

Many of the cases Vector cites apply a totally different rule of law than

Florida in determining an insurer’s duty to defend. In these states, unlike Florida,

courts are permitted to look outside the four corners of the complaint. See Central

Mutual Ins. Co. v. Stunfence, Inc., 292 F. Supp.2d 1072 (N.D. Ill. 2003) (applying

Illinois law which allows the court to go beyond the complaint and consider the

actual facts); Ekco Group, Inc. v. Travelers Indem. Co. of Ill,. 2000 WL 1752829,

at *3 (D.N.H. November 29, 2000) (considering New Hampshire law which

permits court to “decide whether ‘by any reasonable intendment of the pleadings

liability of the insured can be inferred’”); Amerisure Ins. Co. v. Laserage Tech.

Corp., 2 F. Supp.2d 296, 302 (W.D.N.Y. 1998) (applying Illinois law); Union Ins.

Co. v. the Knife Co., Inc., 897 F. Supp. 1213, 1217 (W.D. Ark. 1995) (under

Arkansas law, the court stated, “[i]f injury or damage within the policy could result

from the lawsuit, there is a duty to defend); Cosser v. One Beacon Ins. Group, 789

N.Y.S.2d 586, 587-88 (N.Y. App. Div. 2005) (New York, unlike Florida, allows

consideration of the underlying facts); PG Ins. Co. of N.Y. v. S.A. Day Mfg. Co.,

Inc., 251 A.D.2d 1065 (N.Y. App. Div. 1998) (applying New York law). Vector’s

reliance on these cases is completely misplaced. None of these cases conform with

Florida’s long-established rule that the duty to defend is determined strictly by

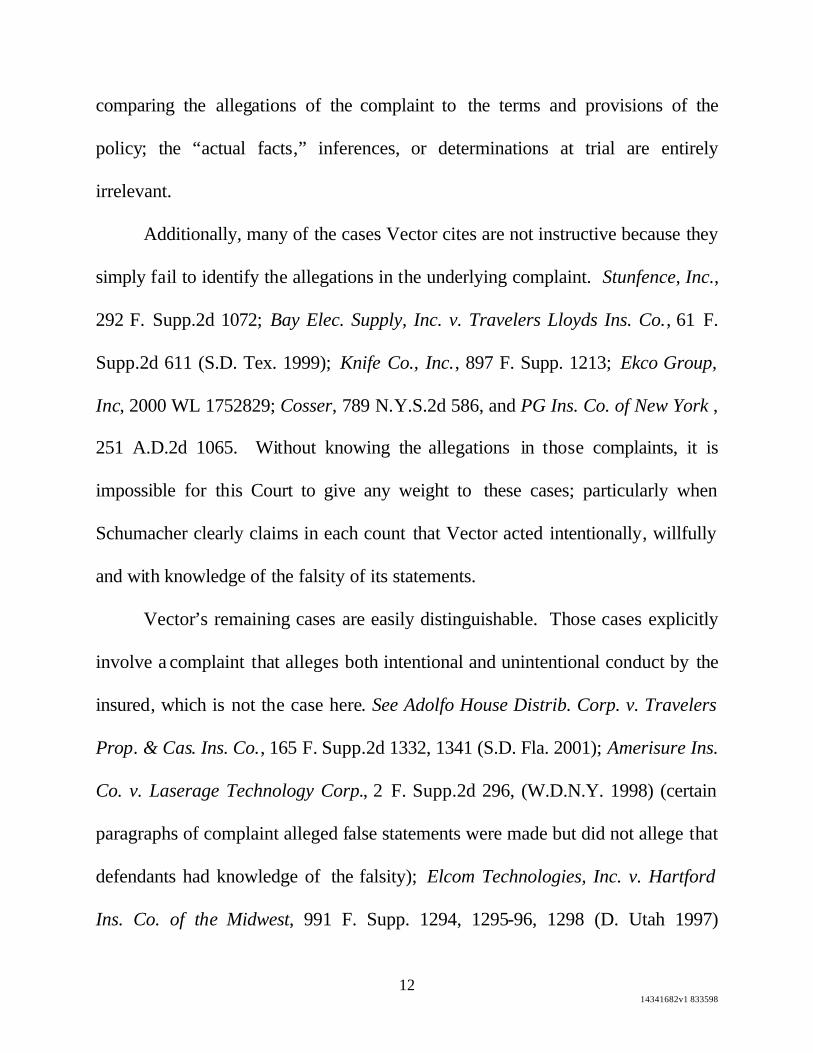

12 14341682v1 833598

comparing the allegations of the complaint to the terms and provisions of the

policy; the “actual facts,” inferences, or determinations at trial are entirely

irrelevant.

Additionally, many of the cases Vector cites are not instructive because they

simply fail to identify the allegations in the underlying complaint. Stunfence, Inc.,

292 F. Supp.2d 1072; Bay Elec. Supply, Inc. v. Travelers Lloyds Ins. Co., 61 F.

Supp.2d 611 (S.D. Tex. 1999); Knife Co., Inc., 897 F. Supp. 1213; Ekco Group,

Inc, 2000 WL 1752829; Cosser, 789 N.Y.S.2d 586, and PG Ins. Co. of New York ,

251 A.D.2d 1065. Without knowing the allegations in those complaints, it is

impossible for this Court to give any weight to these cases; particularly when

Schumacher clearly claims in each count that Vector acted intentionally, willfully

and with knowledge of the falsity of its statements.

Vector’s remaining cases are easily distinguishable. Those cases explicitly

involve a complaint that alleges both intentional and unintentional conduct by the

insured, which is not the case here. See Adolfo House Distrib. Corp. v. Travelers

Prop. & Cas. Ins. Co., 165 F. Supp.2d 1332, 1341 (S.D. Fla. 2001); Amerisure Ins.

Co. v. Laserage Technology Corp., 2 F. Supp.2d 296, (W.D.N.Y. 1998) (certain

paragraphs of complaint alleged false statements were made but did not allege that

defendants had knowledge of the falsity); Elcom Technologies, Inc. v. Hartford

Ins. Co. of the Midwest, 991 F. Supp. 1294, 1295-96, 1298 (D. Utah 1997)

13 14341682v1 833598

(Lanham Act count did not allege intentional conduct by insured and insurer did

not claim knowledge of falsity exclusion). Those cases which identify allegations

of unintentional conduct by the insured do not apply here, where each and every

count in the Schumacher complaint specifically and clearly alleges that Vector

acted willfully, intentionally, knowingly, maliciously, and with full knowledge of

the falsity of its statements. There is no allegation that Vector acted negligently or

unintentionally. These cases simply do not advance Vector’s position.

Vector’s reliance on Finger Furniture Co. v. Travelers Indem. Co. of Conn.,

2002 WL 32113755 (S.D. Tex. 2002), is equally misplaced. This is a report and

recommendation by a magistrate judge, which was never ruled on by an Article III

court. Before objections were ruled upon by the court, the case settled and was

dismissed (Dft.App. A7, Dkt.#43). This report and recommendation is not a

decision, binding or otherwise, unless the parties agree, 28 U.S.C. §636(c), which

they did not (Dft.App. A7, Dkt.#43, http://pacer.txs.uscourts.gov).

Even if the magistrate’s report and recommendation were a “decision,” it is

distinguishable. First, it does not apply Florida law. Id. at *5. Second, the

magistrate found that as long as the underlying “allegations leave open the

possibility that the insured acted without knowledge of falsity of its conduct, the

[knowledge of falsity] exclusion does not apply.” Id. at *13. That possibility does

not exist here as the complaint unequivocally alleges that Vector intentionally

14 14341682v1 833598

made false statements “with full knowledge of the falsity of such statements” (R.

88 ¶ 15, R. 203 ¶ 16).

Vector further takes the unfounded position that the holding in Elcom put

Hartford on notice that the “knowledge of falsity” exclusion does not apply to

intentional Lanham Act violations. What Vector fails to recognize is that Elcom

involved a complaint that alleged both intentional and unintentional conduct by the

insured. 991 F. Supp. at 1295-96, 1298. Contrary to Vector’s assertions, Elcom

does not create a blanket preclusion of the knowledge of falsity exclusion to

Lanham Act claims.

This Court should follow Wackenhut. 15 F. Supp.2d at 1321. In that case,

the insured claimed that the “knowledge of falsity” exclusion did not apply

because the complaint did not expressly allege actual knowledge of falsity. Id. The

district court, applying Florida law, flatly rejected that position.

In Wackenhut, the complaint alleged the following causes of action: “(1)

Intentional and Improper Interference with Continuing and Prospective Contractual

Relations; (2) Unfair Competition; (3) Civil Conspiracy; (4) Restitution; and (5)

Unfair Trade Practices.” Id. at 1318. The Wackenhut court properly confined its

inquiry to the actual allegations of the complaint. The court ruled the specific

allegations that the insured (a) “continued to scheme,” (b) “determined it would

supply false information,” and (c) “supplied false information,” could not be read

15 14341682v1 833598

as anything other than intentional behavior. Unlike the cases Vector cites, the

Wackenhut court refused to read the underlying complaint to allege negligent

misrepresentation, where (as here) the complaint was replete with allegations of

intentional and knowing conduct by the insured. Id.;

Importantly, the court made this determination even though some of the

underlying claims did not require a showing of intent. Cf. Planetary Motion, Inc. v.

Techsplosion, 261 F.3d 1188, 1193 n.4 (11th Cir. 2001) (identifying elements of

trademark infringement claim and stating that same can be used to determine

whether state law unfair competition claim is stated). The court concluded that the

allegations fell squarely into the knowledge of falsity exclusion. Wackenhut, 15 F.

Supp.2d at 1318. To reach this conclusion, the court reasoned: “[E]ven if, in the

underlying suit, the plaintiff could have recovered on a theory of negligence, the

insurer still has no duty to defend if the acts alleged are clearly described as

intentional.” Id. (citing Lumbermens, 646 F.2d at 208-09).

The facts in this case are even more compelling than in Wackenhut since the

Schumacher complaint expressly alleges Vector acted intentionally and with

complete knowledge of the falsity of its statements, claims and representations. As

repeatedly reiterated, every count alleges that Vector acted intentionally and with

knowledge. Like Wackenhut, the knowledge of falsity exclusion precludes

coverage for the Schumacher action.

16 14341682v1 833598

Adolfo, which Vector cites, is inapposite. Although Adolfo questioned

whether the knowledge of falsity exclusion applies to all advertising injuries or

only libel, slander and invasion of privacy, the district court never ruled on this

issue. 165 F. Supp.2d at 1341. Instead, the court concluded that regardless of

whether the exclusion applied to all advertising injuries, the exclusion was

inapplicable because the underlying complaint alleged both intentional and

unintentional grounds for relief, unlike the complaint here. Id. As a result, Adolfo

concluded that “where the complaints allegations leave open the possibility that

[the insured] might be liable for unintentional acts . . ., it may be said that the

complaint contains allegations which ‘fairly and potentially bring the case’ within

the policy coverage, thus requiring the insurer to defend the entire claim.” Id.

In stark contrast to Adolfo, the Schumacher complaint does not allege

alternative relief for unintentional acts. As in Wackenhut, the Schumacher

complaint alleges purely intentional conduct by the insured, bringing it squarely

within the knowledge of falsity exclusion. Hartford accordingly has no duty to

defend Vector under Florida law.

C. The Duty to Defend Is Not Determined By Inferences, Speculation, Actual Facts, or How a Jury Could Rule

Under Florida law, the duty to defend is determined solely by comparing the

allegations of the complaint to the insurance policy. “It is improper for the court to

consider the actual facts, the insured’s version of the facts, or inferences in

17 14341682v1 833598

deciding whether there is a duty to defend.” See, e.g. Sunshine Birds, 696 So. 2d at

909-10; Fun Spree, 659 So. 2d at 421 (cannot consider reasonable inferences);

Chicago Title, 588 So. 2d at 1076 (insured’s conclusions based on a theory of

liability that was not pled is irrelevant); Lumbermens, 646 F.2d at 208-09; Auto

Owners Ins. Co. v. Travelers Cas. & Surety Co., 227 F. Supp.2d 1248, 1258 (M.D.

Fla. 2002) (“actual facts” developed in discovery or otherwise do not affect a duty

to defend); Wackenhut, 15 F. Supp.2d at 1321-22 (no duty to defend even if

plaintiff in underlying suit could recover on negligence theory when plaintiff only

alleges intentional conduct by insured); see also Lenox Liquors, 358 So. 2d at 535-

36 (stipulation in underlying litigation that case would be tried on negligence

theory did not create a duty to defend); Reliance Ins. Co., 534 So. 2d at 923

(holding stipulation of facts should not be considered in determining duty to

defend); Posigian v. American Reliance Ins. Co., 549 So. 2d 751, 753-54 (Fla. 3d

DCA 1989) (affirming dismissal with prejudice of coverage dispute where

complaint alleged only intentional conduct but consent judgment averred that

insured acted negligently). Vector’s new test would require future Florida courts

to speculate about what hypothetical facts and legal theories could be alleged to

determine an insurer’s duty to defend and ignores decades of Florida

jurisprudence.

18 14341682v1 833598

In Chicago Title, the underlying lawsuit alleged claims for breach of several

agreements related to a real estate development where the insured was a mortgage

holder. 588 So.2d at 1075. The insured requested a defense under a title policy,

claiming “that ‘it is evident’ that the club and homeowners association are

asserting an equitable lien superior to” the insured’s lien. Id. Finding no duty to

defend, the court reasoned:

We do not find it “evident” at all that such relief has been requested. Furthermore, whether or not a duty to defend exists arises from the allegations of the complaint itself [citation omitted], not on some conclusions drawn by the insured based upon a theory of liability which has not been pled. [citation omitted].

Id. Florida law is clear; the duty to defend is strictly limited to comparing the

allegations of the underlying complaint to the insurance contract.

Vector’s proposed test asks this Court to ignore the actual allegations of the

Schumacher complaint, and, instead to consider the possible (but unpled) outcome

of trial, including all conceivable and theoretical (but unpled) amendments to

pleadings to determine whether Hartford has a duty to defend. If the Court accepts

Vector’s invitation, this Court will have to discard reasoned and long-standing

Florida law that the allegations of the complaint control the duty to defend.

In an attempt to circumvent the allegations of intentional and knowingly

false statements asserted in every count of the Schumacher complaint, Vector

shifts the focus to the elements and recoverable damages of a Lanham Act claim.

19 14341682v1 833598

Vector fails to recognize that a claim of intentional conduct by a defendant in a

Lanham Act case goes to the issue of deception or confusion of the consumer.

Porous Media Corp, 110 F.3d at 1332-33; Boosey & Hawkes, 145 F.3d at 493.

The intentional allegations are relevant to both establishing the claimed Lanham

Act violations and Schumacher’s claim for treble damages.

Additionally, it is contrary to Florida law to consider the potential outcome

at trial. The proper test in Florida is to consider only the allegations of the

complaint. Vector’s attempt to dismiss S.M. Brickell Ltd. Partnership v. St. Paul

Fire & Marine Ins. Co., 786 So. 2d 1204 (Fla. 3d DCA 2001), and Fun Spree, 659

So. 2d. at 421 is unpersuasive.

In Fun Spree, the complaint alleged both negligent and intentional

misrepresentations that damaged plaintiff’s reputation, credit and recognition in the

travel industry and destroyed plaintiff’s business. 659 So. 2d at 420-21. The

complaint did not allege that the insured disparaged or defamed the plaintiff. The

insured’s policy included coverage for “the publication or utterance of a libel or

slander or of other defamatory or disparaging material.” Id. at 420. The court

rejected the insured’s argument that there was a reasonable inference that could be

drawn from the underlying complaint that statements by the insured discredited the

plaintiff’s reputation, holding “[i]nferences are not sufficient” to create a duty to

20 14341682v1 833598

defend. Id. at 421. Accordingly, the court found no duty to defend based solely on

the allegations in the complaint. Id. at 421-22.

In SM Brickell, the insured was sued in two separate actions. The first suit

(Hansen), only alleged the defamatory statements “were false and known to be

false when made.” 786 So. 2d at 1205. In the second suit (Puig), the fourth

amended complaint alleged both “intentional wrongdoing and negligent

defamation.” Id. The plaintiff pled in the alternative, alleging that the insured

acted “intentionally, recklessly, and/or negligently” in disseminating false and

defamatory communications. Id. at 1205 n.1. The plaintiff further alleged that the

insured “knew and/or should have known that [the statements] were false when

made.” Id. Once the negligence claim was asserted, the court found a duty to

defend. Id. The court, however, did not find that St. Paul had a duty to defend the

Hansen suit since that suit, like the Schumacher complaint, alleged the statements

were false and known to be false when made.

Vector argues that Hartford’s position would result in a potential duty to

indemnify, depending on the jury verdict in the Schumacher litigation even though

Hartford owed no duty to defend. Vector invites this Court to abandon its test that

the duty to defend is solely determined by comparing the allegations of the

complaint to the terms of the insurance contract, and adopt Illinois, Louisiana, New

York, Nebraska, or Oregon law, all of which permit the court to consider

21 14341682v1 833598

information outside the complaint to determine if there is a duty to defend.

Cincinnati Ins. Co. v. Eastern Atl. Ins. Co., 260 F.3d 742 (7th Cir. 2001) (applying

Illinois law which permits courts to go beyond allegations of the underlying

complaint in considering defamation claim, while ignoring allegations of

intentional conduct); Utica Mut. Ins. Co. v. David Agency Ins. Inc., 327 F. Supp.2d

922 (N.D. Ill. 2004) (applying Illinois law to defamation claim); Park Place

Entert. Corp. v. Transcon. Ins. Co., 225 F. Supp.2d 406, 411-12 (S.D.N.Y. 2002)

(applying New York law which allows the court to look to the actual facts in

determining whether there is a duty to defend defamation claim); Broadhead v.

Scott, 497 So. 2d 1081 (La. Ct. App. 1987) (going beyond allegations of complaint

when considering application of Louisiana law to claim of trespass and intended

acts exclusion); Allstate Ins. Co. v. Novak, 313 N.W. 2d 636 (Neb. 1981)

(discussing Nebraska law which directly conflicts with Florida law in allowing

court to go beyond allegations of the complaint where assault and battery alleged);

Ferguson v. Birmingham Fire Ins. Co., 460 P.2d 342 (Or. 1969) (considering

information outside the allegations of the complaint under Oregon law regarding

trespass claim). Because Vector’s cases conflict with long-standing Florida law,

they should not be considered by this Court.

Vector also relies on a California case that applies the “reasonable

expectations” doctrine. Gray v. Zurich Ins. Co., 419 P.2d 168 (Calif. 1966) (relying

22 14341682v1 833598

on the reasonable expectations doctrine, and going beyond the pleadings to hold

that the intended acts exclusion did not preclude coverage for a claim of assault).

That doctrine was expressly rejected by this Court. Deni Assoc. of Florida, Inc. v.

State Farm Fire & Cas. Ins. Co., 711 So. 2d 1135, 1140 (Fla. 1998).

Another case Vector cites is American Home Assurance Co. v. United Space

Alliance, LLC, 378 F.3d 482 (5th Cir. 2004), which applied Texas law. The court

there failed to set forth the specific allegations of the complaint but noted “some of

the causes of action and allegations of conduct, such as breach and repudiation of

contracts, as well as disparagement, are not types based on and do not involve

knowingly fraudulent statements.” 378 F.2d at 488. The court opined that, under

Texas law, the analysis focuses on the factual allegations which show the origin of

the damages, rather than focusing on the alleged legal theories alleged. Id. The

court, in dicta, proceeded to go far beyond the allegations of the complaint and

speculated on the potential outcome at trial. Id. The court’s analysis is directly

contrary to established Florida precedent which limits the inquiry solely to the

allegations of the complaint. See, e.g., Lenox Liquors, 358 So. 2d at 534; Barry

University, 845 So. 2d at 278; Appelstein, 377 So. 2d at 231-32.

For its novel proposition that the Court must find a duty to defend because

there is a possibility of a duty to indemnify, Vector cites only one federal case that

applies Florida law. Lime Tree Village Cmty. Club Ass’n v. State Farm Gen. Ins.

23 14341682v1 833598

Co., 980 F.2d 1402 (11th Cir. 1993). Vector’s reliance on Lime Tree is misplaced.

In Lime Tree, the Eleventh Circuit properly recognized that it “cannot speculate as

to the nature or merit of the claims; it may only look to the factual allegations of

the underlying complaint” in determining whether there is a duty to defend. Id. at

1406. The complaint contained claims that were covered (slander, breach of

covenant, and restraint of trade) because they were “wrongful acts” under the

policy, as well as claims that were expressly excluded (discrimination). Id. at

1406. The court noted “[t]his is not a case where there is only a single cause of

action based wholly on acts expressly excluded by the policy.” Id. at 1405.

Tellingly, the court acknowledged that there were no allegations that the insured

intended the resulting harm. Id. at 1407. The court ruled: “Based on the facts

alleged in the complaints, if the suits had proceeded to trial, the Lime Tree officers

and directors could have been found not to have acted maliciously or in violation

of any civil rights law, but to have committed an error or a breach of a duty in

passing and recording the amendment to the Covenants and Restrictions.” Id. at

1406.

Here, in contrast, there are direct allegations of intentional conduct. The

Schumacher complaint alleges that all of Vector’s actions and false statements

were done “willfully” and “intentionally,” “with full knowledge of the falsity” (R.

24 14341682v1 833598

88-90 ¶¶ 13-16, 23, 27; RE202-08 ¶¶ 14, 16, 21, 29-30, 35, 38, 39, 42). It is based

on those facts and legal theories that the case would have proceeded to trial.

What Schumacher might possibly allege or prove in the future has no

bearing on Hartford’s duty to defend Vector right now. The duty to defend is

determined from the allegations of the complaint, not the ultimate result of the

litigation. Both the original and amended complaints unequivocally allege that

Vector knowingly made false statements. No duty to defend arises based on

possible - but never pleaded - facts or theories. Vector’s speculation about what a

jury might find in the future and the possibility that an award would somehow be

based on unpled unintentional conduct or some other theory is not a proper

consideration for deciding whether Hartford has a duty to defend. Vector’s

proposed test would require insurers to defend an insured based upon possible

legal theories and theoretical claims, which somewhere down the line may be

included in an amended pleading. Make no mistake, Vector is asking this Court to

create a new rule of law in Florida.

Moreover, Vector’s argument regarding a possible jury verdict is made

without explaining how a jury could reach that result. The only way a jury can be

instructed on an unintentional violation of the Lanham Act is if Shumacher

amended its complaint. If the complaint was amended to include non-intentional

conduct, Vector could then tender that complaint to Hartford and request a defense.

25 14341682v1 833598

Then the duty to defend could arise. Baron Oil Co. v. Nationwide Mut. Fire Ins.

Co., 470 So. 2d 810, 814-15 (Fla. 1st DCA 1985); Allstate Ins. Co. v. Travers, 703

F. Supp. 911, 913 (N.D. Fla. 1988); American States Ins. Co. v. Pioneer Elec., 85

F. Supp.2d 1337, 1343 (S.D. Fla. 2000).

For example, in Appelstein, the underlying complaint asserted claims for

libel, slander, and intentional infliction of emotional distress. 377 So. 2d at 230.

With respect to each count, the plaintiff alleged that Appelstein “‘made said

allegations in bad faith, with malice, with reckless and wanton disregard’” for

plaintiff’s rights and with the specific intent to discredit plaintiff. Id. The plaintiff

also sued the trust for Appelstein’s actions, alleging in each count that his actions

were taken with full approval and ratification of the trust. Id. at 230. Even though

intent is not an element for a libel or slander claim, Valencia v. Citibank Int’l, 728

So. 2d 330, 330 (Fla. 3d DCA 1999), the court found that the intentional acts

exclusion precluded coverage for those claims. Id. at 231. With that decision, that

Florida court expressly rejected the precise argument Vector makes here:

The appellees contend that, even though the face of the fourth amended complaint alleges otherwise, Federal nonetheless was required to defend because the “actual facts” as developed in the subsequent discovery process, showed that the liability of the defendants, particularly the trust, may not have been excluded from the coverage of the policy. We need not consider whether this argument represents an accurate view of the record, because the legal proposition upon which it is based is unsound.

Id. at 232 (citing Lenox Liquors, 358 So. 2d at 534).

26 14341682v1 833598

The Fifth Circuit applied the same reasoning in Lumbermens. Lighting

Systems sued ABC for trademark infringement and related causes of action. 646

F.2d at 208. Lumbermens refused to defend ABC because the complaint alleged

that ABC’s actions were intentional. Id. Acknowledging that the duty to defend

under Florida law is determined strictly from the allegations of the complaint, the

Fifth Circuit recognized that the complaint was “replete” with allegations of

intentional conduct by ABC and that the “overall scheme” alleged in the complaint

was “clearly intentional.” Id. at 209. Again, the court, applying Florida law,

expressly rejected the exact argument that Vector is making here:

Even if Lighting Systems could have gone to trial on a theory of unintentional trademark violation, just as the minor in Lenox Liquors could have gone to trial on a theory of a negligent shooting, under Florida law the insurance company had a right to rely on the averments of the complaint that ABC’s actions had been intentional.

Id.

Florida courts and federal courts applying Florida law consistently follow

this rule and refuse to speculate on theoretical amendments to pleadings which

may never occur. See, e.g., Barry Univ., 845 So. 2d at 278 (“no fair reading of the

complaint alleges facts which create coverage” where complaint alleges intentional

conduct by university asserting claims for breach of contract, fraud in the

inducement, and violations of Florida Deceptive and Unfair Trade Practices Act);

Capoferri, 322 So. 2d at 627 (where only intentional acts alleged, there is no duty

27 14341682v1 833598

to defend even if insured claims acts were not intentional); Wackenhut, 15 F.

Supp.2d at 1321-22 (ruling no duty to defend exists, even is the plaintiff could

have recovered on a negligence claim in the underlying action where the complaint

only alleged intentional acts).

The correct analysis under Florida law is as follows:

[W]here the original complaint fails to allege facts within the policy coverage, if it later becomes apparent from an amended pleading that claims not originally within the scope of the pleadings are being made which are within the insurance coverage, the insurance carrier, upon notification, would become obligated to defend.

Baron Oil Co., 470 So. 2d at 814-15 (and cases cited); see also Travers, 703 F.

Supp. at 913 (applying Florida law). What Vector is asking this Court to do is

make assumptions that directly contradict the factual allegations of the complaint

in order to find a duty to defend. Vector’s proposed test is clearly contrary to

Florida law and should be rejected.

II. THIS COURT SHOULD ANSWER THE CERTIFIED QUESTION AND CONFIRM THE RULING OF THE DISTRICT COURT BASED ON ALTERNATIVE GROUNDS APPEARING OF RECORD.

A Florida court may affirm a decision of a lower tribunal as long as “there is

any basis which would support the judgment in the record.” Dade County Sch. Bd.,

731 So. 2d at 644-45. In this case, Hartford sought summary judgment on other

grounds in addition to the “knowledge of falsity” exclusion. The district court’s

ruling was correct and can be affirmed on these alternative grounds.

28 14341682v1 833598

A. Florida Public Policy Prohibits Insurance Coverage for Intentional Acts.

The lower court’s judgment that Hartford owes no duty to defend should be

affirmed based on Florida public policy. The Schumacher complaint alleges only

intentional conduct by the insured. Florida public policy precludes coverage.

Ranger Ins. Co. v. Bal Harbour Club, Inc., 549 So. 2d 1005, 1008-09 (Fla. 1989)

(holding no insurance coverage permitted for allegations of intentional

discrimination); State Farm Fire & Cas. Co. v. Tippett, 864 So. 2d 31, 36 (Fla. 4th

DCA 2004) (reiterating long-standing public policy precluding coverage for

intentional acts of sexual assault); Mason v. Florida Sheriff’s Self-Insurance Fund,

699 So. 2d 268 (Fla. 4th DCA 1997) (applying public policy prohibition for battery

claim); Lindheimer v. St. Paul Fire & Marine Ins. Co., 643 So. 2d 636, 639 (Fla.

3d DCA 1994) (finding Florida public policy prohibits insurance for intentional

acts where insured sexually assaulted a patient).

There are two factors to consider to determine if public policy bars

coverage: (1) whether the conduct of the insured is a type that will be encouraged

by insurance; and (2) what purpose is served by imposition of liability for that

conduct, i.e., whether it is to deter wrongdoers or compensate victims. Ranger Ins.

Co., 549 So. 2d at 1007. In this case, Schumacher alleged Vector made false,

knowing and intentional misstatements about its battery charger and falsely

represented that it was in compliance with the FCC rules on radio emissions, which

29 14341682v1 833598

“present[s] a serious potential for harmful interference to licensed radio services”

(R. 200-07 ¶27). Both the Lanham Act and the Illinois law which Schumacher

invoked in its original and amended complaint are designed to protect business

competitors and prevent confusion or deception of consumers. See Davidoff &

CIE, S.A. v. PLD Int’l Corp., 263 F.3d 1297, 1301 (11th Cir. 2001); and Popp v.

Cash Station, Inc., 613 N.E.2d 1150, 1156-57 (Ill. App. Ct. 1992). If Vector was

permitted to simply pass the cost of its intentional, false statements about a

competitor on to Hartford, this would serve to encourage, not deter, this type of

conduct at the expense of both consumers and competitors.

As emphasized throughout this brief, the Schumacher complaint allegations

of intentional wrongful conduct by Vector in each and every count. (R. 203 ¶¶16,

30, 38, 42). In Counts I and II of the First Amended Complaint Schumacher

alleges that Vector made false statements about its products “willfully and

intentionally and with full knowledge of the falsity of such statements.” (R. 203

¶¶16, 30). In Counts III and IV, Schumacher alleges that Vector made the

“wrongful acts willfully, maliciously and intentionally.” (R. 203 ¶ 38, 42).

Schumacher could not be any clearer. Schumacher never alleges negligent or

unintentional conduct. Insurance coverage for these actions violates Florida public

policy. Ranger, 549 So. 2d at 1006, 1009. There is no coverage under the

Hartford policy.

30 14341682v1 833598

B. The Claim Is Excluded from Coverage Under the “Intent to Injure” Exclusion

The polic ies exclude coverage for personal and advertising injury “arising

out of an ‘offense’ committed by, at the direction or with the consent or

acquiescence or the insured with the expectation of inflicting ‘personal and

advertising injury’” (R. 81 ¶I(1)). An examination of the clear language of the

exclusion evidences that it applies to the Schumacher complaint. Deni, 711 So. 2d

at 1138 (citing State Farm Mut. Auto. Ins. Co. v. Pridgen , 498 So. 2d 1245 (Fla.

1986)).

Florida courts have consistently held that the phrase “arising out of” is

unambiguous when used in policy exclusions. See Estate of Bombolis v. Cont.

Cas. Co., 740 So. 2d 1229, 1230 (Fla. 4th DCA 1999) (explaining that court should

look to entire language of exclusion); Allstate Ins. Co. v. Shofner, 573 So. 2d 47,

50 (Fla. 1st DCA 1990) (considering a homeowners’ policy); Quick v. State Farm

Fire & Cas. Co., 488 So. 2d 909, 910 (Fla. 1st DCA 1986) (regarding general

liability policy); Ohio Cas. Co. v. Cont. Cas. Co., 279 F. Supp.2d 1281, 1284 (S.D.

Fla. 2003) (automobile policy).

“Expectation” is “the act or state of expecting; . . .something expected; a

thing looked forward to; the degree of probability that something will occur.”

Webster’s Encyclopedic Unabridged Dictionary of the English Language 680

(Deluxe ed. 1996). Webster’s further defines “expect” to imply “confidently

31 14341682v1 833598

believing, usually for good reasons, that an event will occur.” Id. “Inflict” is

defined as “to impose as something that must be borne or suffered to impose

(anything unwelcome); to deal or deliver.” Id. at 979.

This exclusion clearly applies to the allegations of the Schumacher

complaint. For example, the Schumacher complaint alleges that Vector’s

advertisements for its products contained false representations which where made

“willfully and intentionally” and “maliciously.” (R. 202-08 ¶¶ 16-17, 21, 29-30,

35, 39, 42). These allegations are premised entirely on intentional conduct on the

part of Vector. Hartford has no duty to defend.

C. The Underlying Claim is Not a Covered “Advertising Injury”

To trigger a duty to defend, the underlying complaint must allege a

qualifying offense that falls within potential coverage under the Hartford policies.

Although the Hartford polic ies list multiple offenses which can form the basis for a

“personal and advertising injury,” the only potential coverage for the Schumacher

complaint would be for “oral or written publication of material that ... disparages a

person’s or organization’s goods, products or services.” Black’s Law Dictionary

(6th ed. 1996) defines disparagement of goods as “a statement about a competitor’s

goods which is untrue or misleading and is made to influence or tends to influence

the public not to buy.” See also Aerosonic Corp. v. Trodyne Corp., 402 F.2d 223,

231 (5th Cir. 1968) (“[b]asically, actionable disparagement is a statement about a

32 14341682v1 833598

competitor’s goods which is untrue or misleading and which is made to influence

or tends to influence not to buy”).

There are no allegations in the Schumacher complaint that Vector said

anything disparaging about Schumacher or its products. Likewise, none of the

exhibits attached to the Schumacher complaint contain any comparison between

the products of Vector and Schumacher. In the absence of such allegations, there

is no basis for finding a disparagement offense under the Hartford polic ies. The

Schumacher complaint accordingly does not trigger a duty to defend and Hartford

is entitled to summary judgment.

CONCLUSION

For the foregoing reasons, this Court should answer the certified question in

the affirmative, find, like the district court, that Hartford has no duty to defend

Vector in the Schumacher action, and for such other relief as this Court deems

proper.

33 14341682v1 833598

CERTIFICATE OF SERVICE

I hereby certify a true and correct copy of the foregoing Answer Brief of

Appellee, Hartford Fire Insurance Company was served on June 1, 2005 by mail,

upon Major B. Harding, Kenneth P. Abele, 227 South Calhoun Street, Post Office

Box 391, Tallahassee, Florida 32302, and Stephen E. Marshall, Venable, LLP,

1800 Mercantile Bank & Trust Building, 2 Hopkins Plaza, Baltimore, Maryland

21201, Co-counsel for Appellant, Vector Products, Inc..

HINSHAW AND CULBERTSON, LLP __________________________ Ronald L. Kammer Florida Bar No. 360589 Maureen G. Pearcy Florida Bar No. 0057932 Andrew E. Grigsby Florida Bar No. 328383 Sina Bahadoran Florida Bar No. 523364 P.O. Box 569009 9155 South Dadeland Boulevard Suite 1600 Miami, FL 33256-9009 Telephone: 305-358-7747 Facsimile: 305-577-1063

34 14341682v1 833598

CERTIFICATE OF COMPLIANCE

The undersigned counsel hereby certifies that this answer brief complies

with Rule 9.210, Fla.R.App.P., and is typed in Times New Roman 14-point font.

______________________________ Ronald L. Kammer Fla. Bar No. 360589 Maureen G. Pearcy Fla. Bar No. 0057932 Andrew E. Grigsby Fla. Bar No. 328383 Sina Bahadoran Fla. Bar No. 523364