CASE Network Report 41 - Currency Crises in Emerging Markets - Selected Comparative Studies

146

Marek D¹browski (ed.) Warsaw, 2001 No. 41 Currency Crises in Emerging Markets – Selected Comparative Studies

-

Upload

case-center-for-social-and-economic-research -

Category

Economy & Finance

-

view

422 -

download

5

description

This volume presents seven comparative studies of currency crises, which happened in the decade of 1990s in Latin America, South East Asia and in transition countries of Eastern Europe and the former USSR. Authored by: Rafal Antczak, Monika Blaszkiewicz, Marek Dabrowski, Malgorzata Jakubiak, Malgorzata Markiewicz, Wojciech Paczynski, Artur Radziwill, Marcin Sasin, Mateusz Szczurek Published in 2001

Transcript of CASE Network Report 41 - Currency Crises in Emerging Markets - Selected Comparative Studies

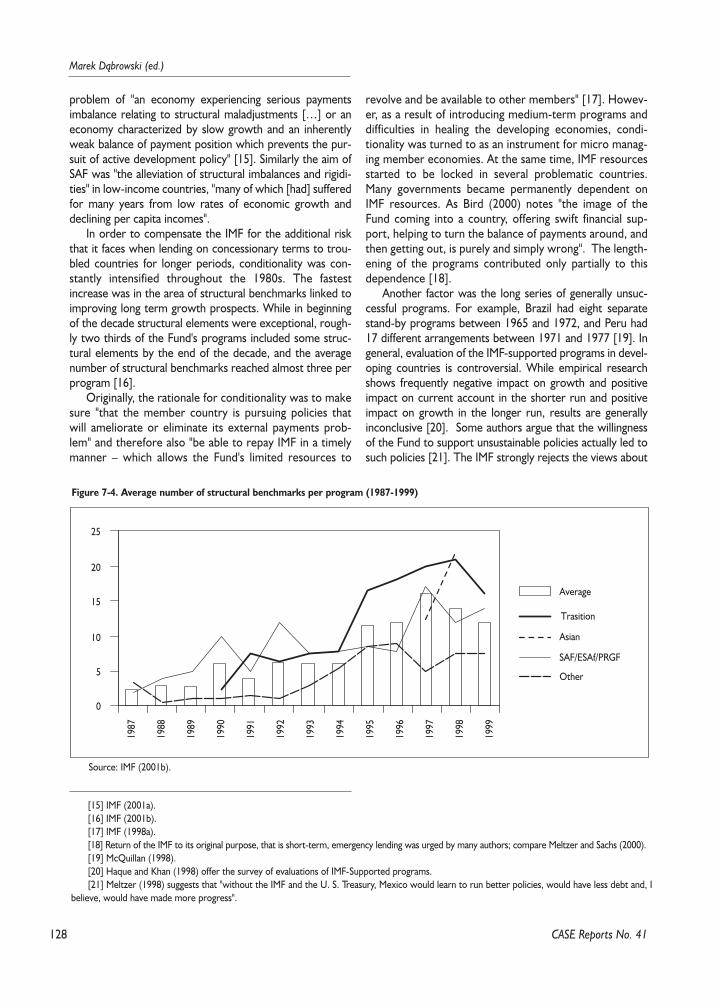

M a r e k D ¹ b r o w s k i ( e d . )

WW aa rr ss aa ww ,, 22 00 00 11 NNoo.. 4411

Currency Crises

in Emerging Markets

– Selected Comparative

Studies

The views and opinions expressed in this publication reflectAuthors’ point of view and not necessarily those of CASE.

Materials prepared for the conference summing up theresearch project No. 0144/H02/99/17 entitled "Analizaprzyczyn i przebiegu kryzysów walutowych w krajach Azji,Ameryki £aciñskiej i Europy Œrodkowo-Wschodniej: wnios-ki dla Polski i innych krajów transformuj¹cych siê" (Analysisof the Causes and Progress of Currency Crises in Asian,Latin American and CEE Countries: Conclusions for Polandand Other Transition Countries) financed by the StateCommittee for Scientific Research (KBN) in the years1999-2001.

The publication was financed by KBN and WestdeutscheLandesbank Polska S.A.

Key words: financial crises, currency crises, IMF, financialsystems, exchange rate regime, transition economies

DTP: CeDeWu Sp. z o.o.

Graphic Design – Agnieszka Natalia Bury

© CASE – Center for Social and Economic Research, Warsaw 2001

All rights reserved. No part of this publication may bereproduced, stored in a retrieval system, or transmitted in anyform or by any means, without prior permission in writingfrom the author and the CASE Foundation.

ISSN 1506-1647 ISBN 83-7178-259-4

Publisher:CASE – Center for Social and Economic Research ul. Sienkiewicza 12, 00-944 Warsaw, Polande-mail: [email protected]://www.case.com.pl

3

Currency Crises in Emerging Markets – Selected Comparative ...

CASE Reports No. 41

Contents

Introduction - Marek D¹browski . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .7

Part I. The Importance of the Real Exchange Rate Overvaluation and the Current Account Deficitin the Emergence of Financial Crises - Marcin Sasin . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .91.1. Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .91.2. Overvaluation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .9

1.2.1. Theory . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .91.2.2. How to Calculate a Real Exchange Rate . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .101.2.3. Overvaluation and Currency Crises, an Empirical Evidence . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .111.2.4. Trade-link Contagion: Competitive Devaluations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .13

1.3. Current Account . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .141.3.1. Evolution of the Point of View on the Current Account . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .14

1.3.1.1. The Early Views: the Trade/Elasticity Approach . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .141.3.1.2. Intertemporal Approach: the Irrelevance of the Current Account Deficit

and the Lawson Doctrine . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .141.3.1.3. Surge in Capital Inflows: from the 5% Rule of Thumb to "Current Account Sustainability"15

1.3.2. Models of the Current Account . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .161.3.2.1. Exchange Rate and Elasticity Approach . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .161.3.2.2. Portfolio Approach . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .161.3.2.3. Intertemporal Choice Approach . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .17

1.3.3. How to Calculate A Sustainable Current Account Deficit . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .191.3.3.1. Underlying Current Account Balance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .191.3.3.2. Model-based Calculations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .191.3.3.3. Different Method for Different Types of Economies . . . . . . . . . . . . . . . . . . . . . . . . . . . .21

1.3.4. Empirical Evidence . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .221.3.4.1. Determinants of Current Account and its Empirical Distribution over Time

and Countries . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .221.3.4.2. The Links Between Current Account and Crises . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .22

1.4. Conclusions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .25References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .26

Part II. Choice of Exchange Rate Regime and Currency Crashes - Evidence of some Emerging Economies - Ma³gorzata Jakubiak . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .292.1. Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .292.2. Old Dilemma: Fixed or Flexible? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .292.3. Costs of a Sudden Shift to a More Flexible Arrangement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .302.4. Why Emerging Markets Peg Their Currencies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .312.5. Choices Faced After a Currency Collapse . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .322.6. Empirical Evidence - Case Studies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .32

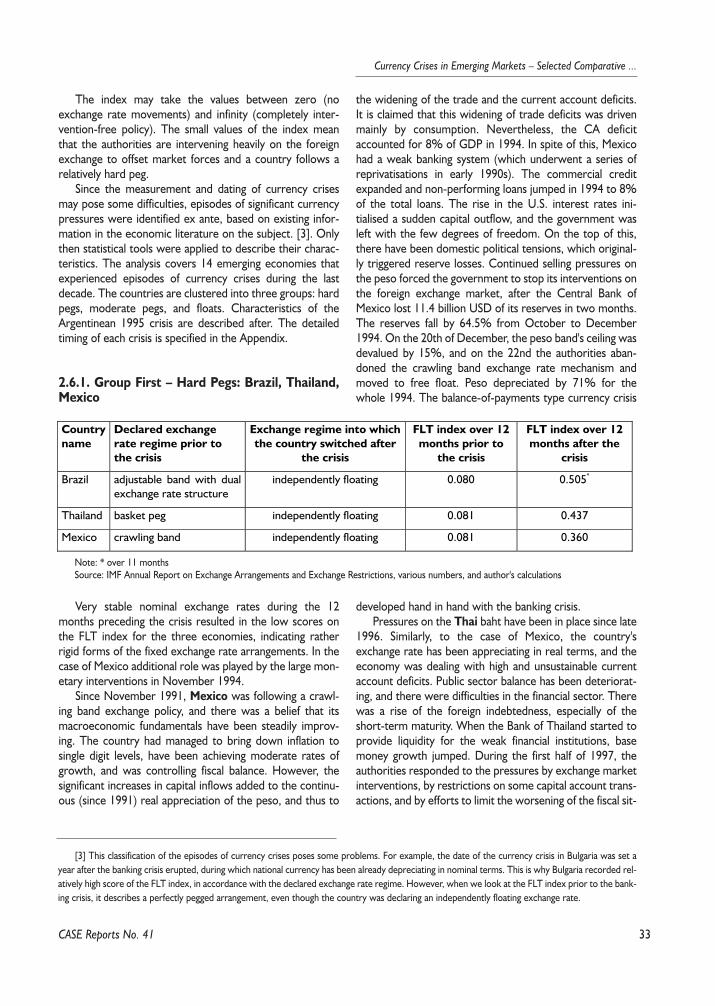

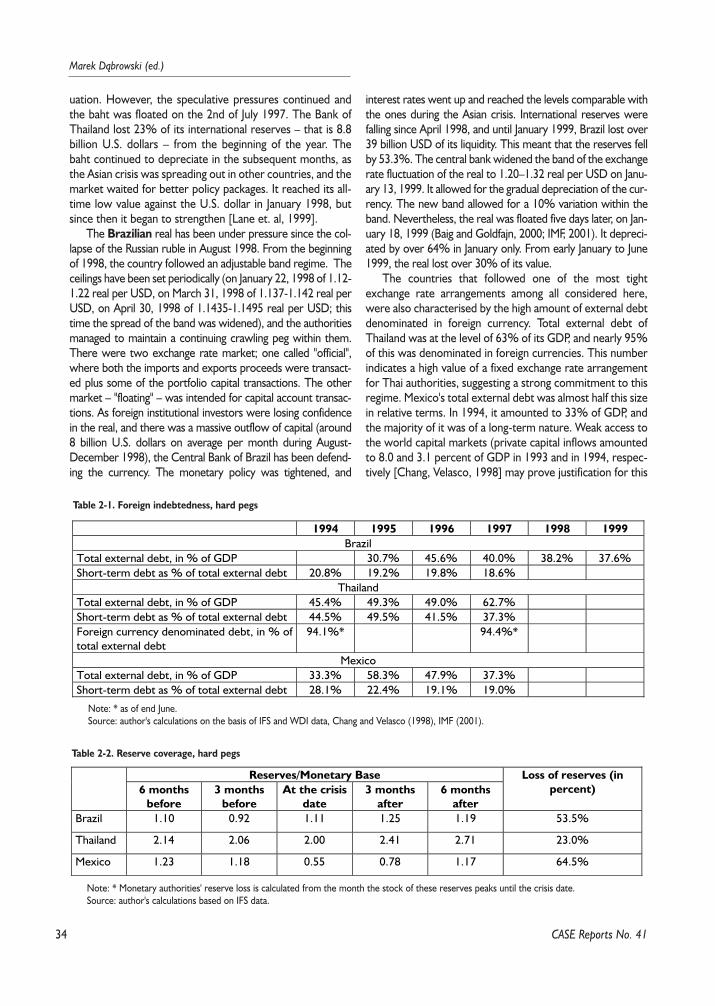

2.6.1. Group First - Hard Pegs: Brazil, Thailand, Mexico . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .332.6.2. Group Second - Moderate Pegs: Russia, Georgia, Ukraine, Korea, Indonesia,

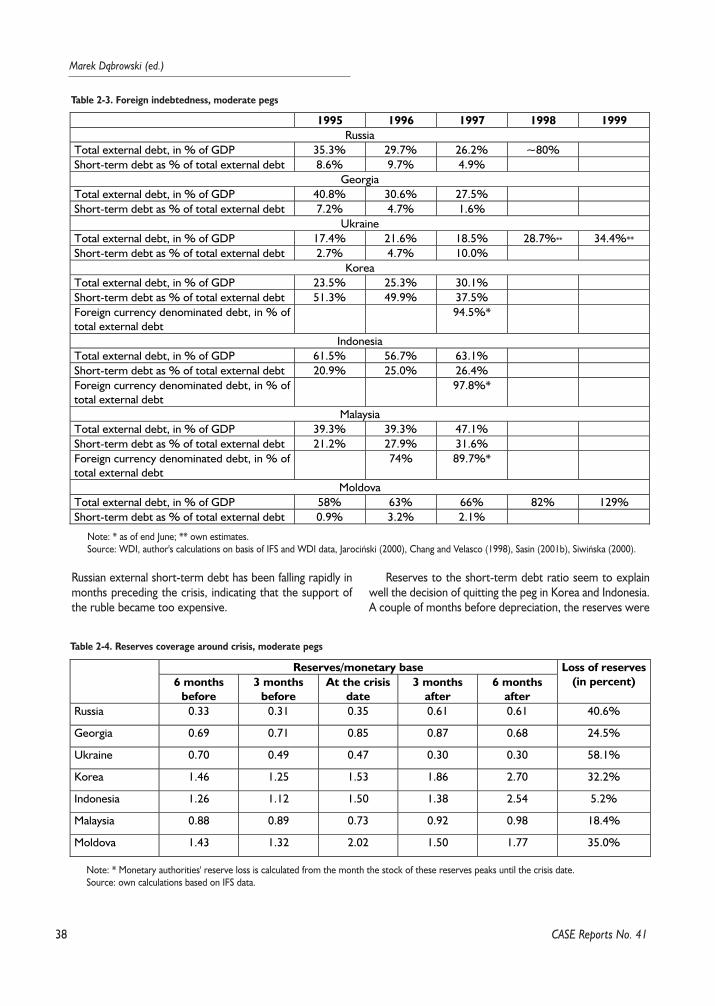

Malaysia, Moldova . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .35

4

Marek D¹browski (ed.)

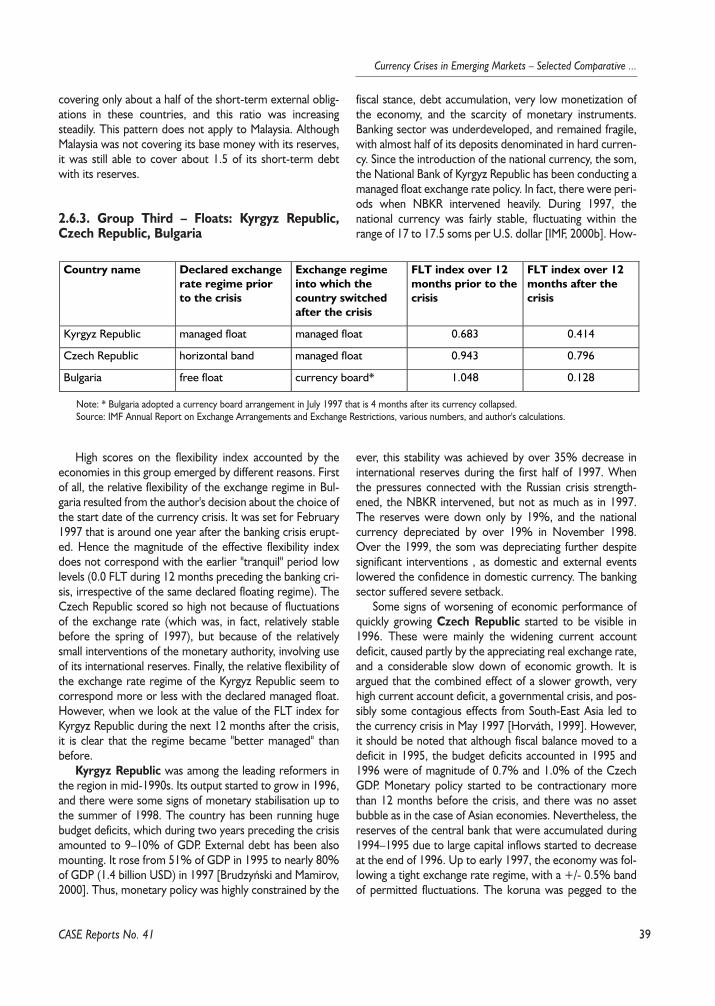

2.6.3. Group Third - Floats: Kyrgyz Republic, Czech Republic, Bulgaria . . . . . . . . . . . . . . . . . . . . . . . . .392.6.4. Currency Board: Argentina in 1995 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .41

2.7. Probability of Ending a Peg. Logit Estimation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .412.8. Conclusions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .42Appendix: Crisis Dates . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .44References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .45

Part III. International Liquidity, and the Cost of Currency Crises - Mateusz Szczurek . . . . . . . . . . . .473.1. Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .473.2. Foreign Exchange Reserves in Crisis Models . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .48

3.2.1. A Survey of Literature . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .483.2.2. A Survey of Empirical Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .50

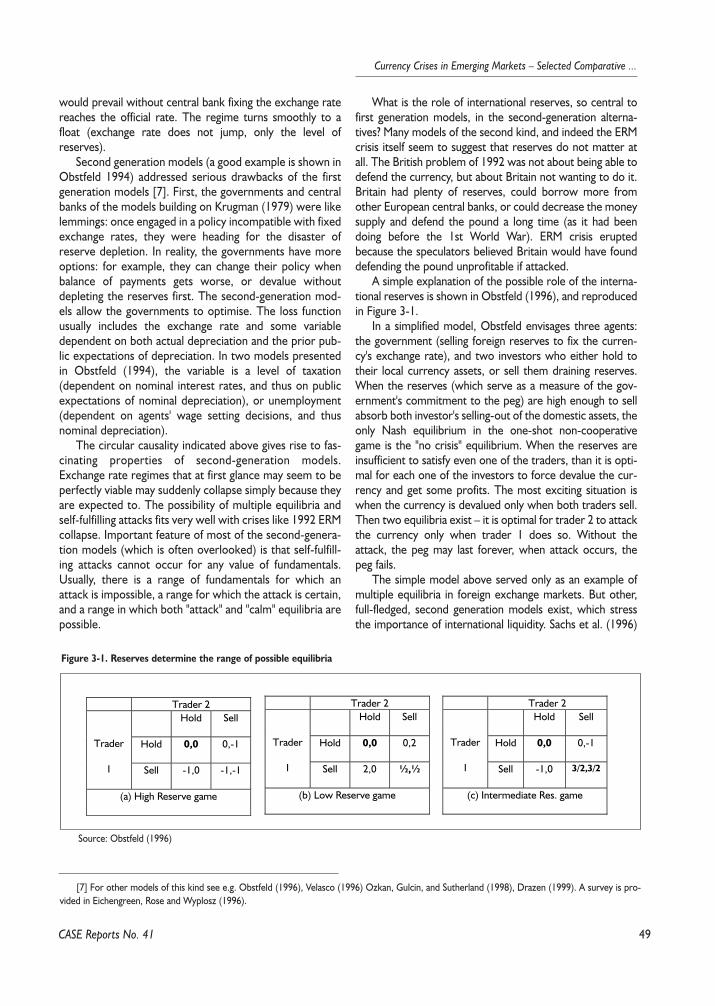

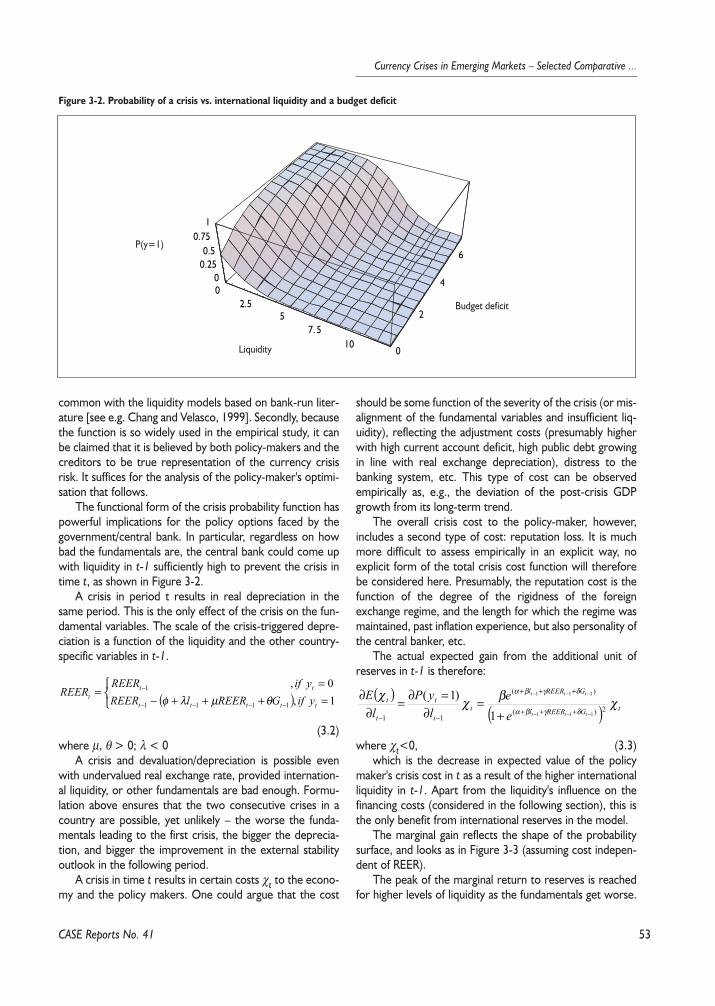

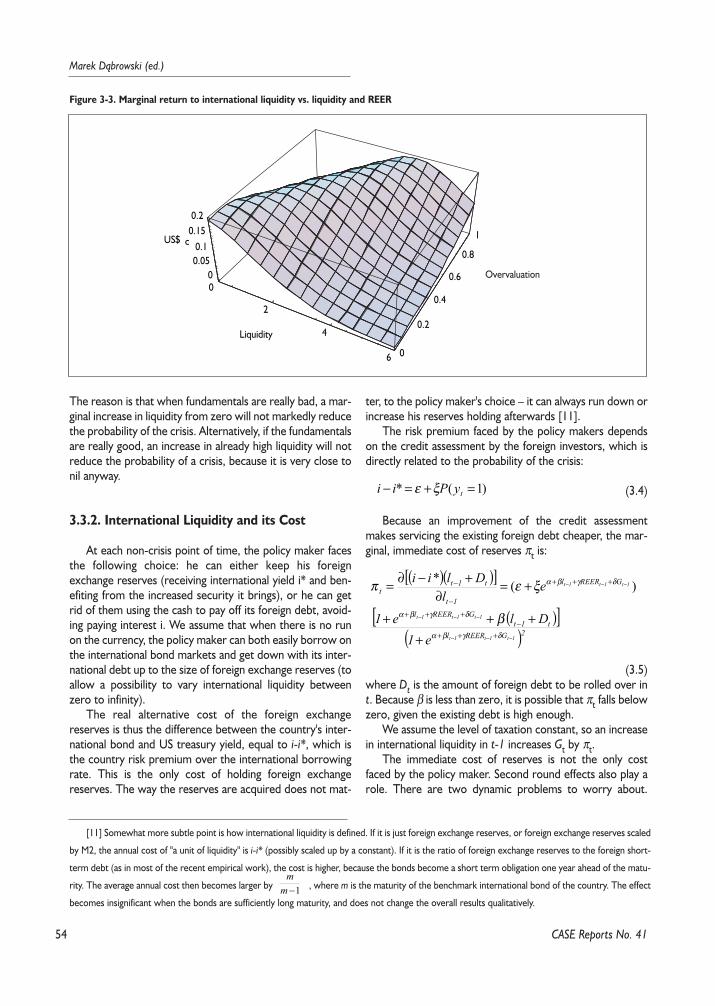

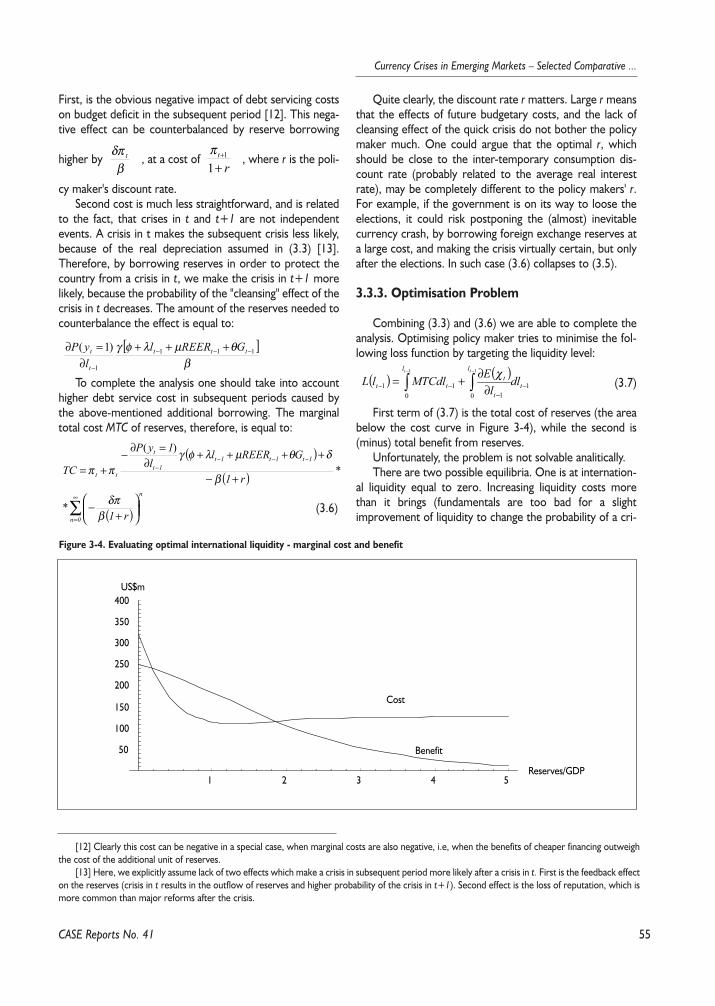

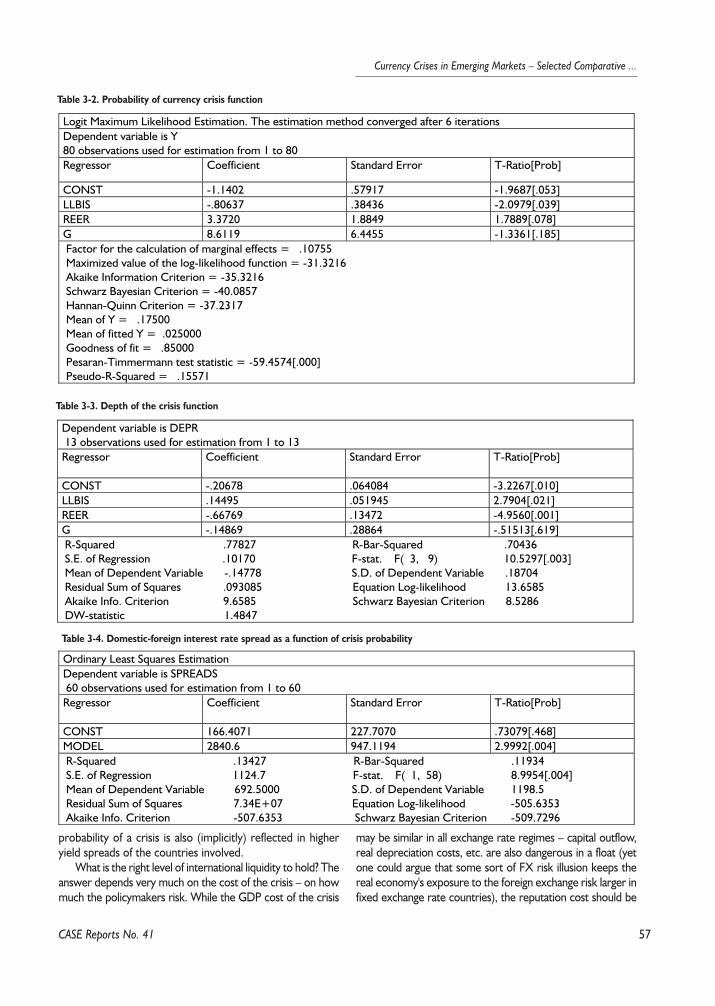

3.3. International Liquidity: Simple Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .523.3.1. Crisis and its Cost . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .523.3.2. International Liquidity and its Cost . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .543.3.3. Optimisation Problem . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .55

3.4. Empirical Application . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .563.4.1. Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .563.4.2. The Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .563.4.3. How Much the Policy Makers Fear the Crisis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .58

3.5. Conclusions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .60Appendix . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .60References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .61

Part IV. Financial Systems, Financial Crises, Currency Crises – Marcin Sasin . . . . . . . . . . . . . . . . . . .634.1. Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .634.2. Theoretical Aspects of Banking and Financial Crises . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .634.2.1. Definitions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .63

4.2.2. The Relationship between Banking and Currency Crises . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .644.2.3. The Theory and Practice of a Banking System Crisis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .64

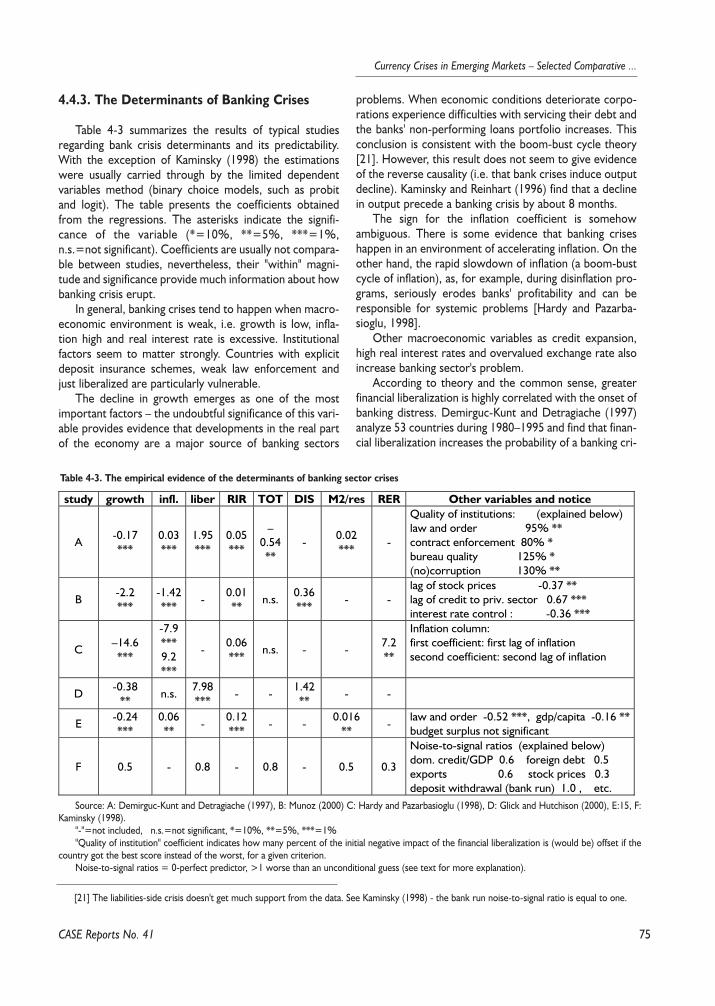

4.3. Assessing the Condition of a Banking System . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .714.4. Empirical Evidence and the Determinants of Banking and Currency Crises . . . . . . . . . . . . . . . . . . . . . . . .72

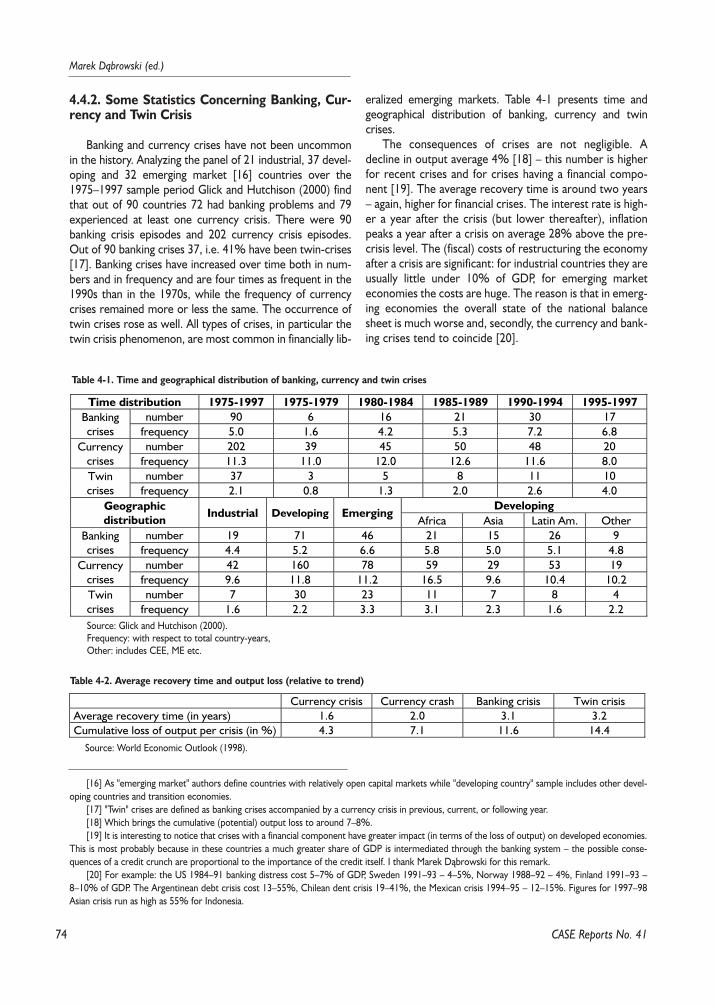

4.4.1. Banking Crises in the Real World . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .724.4.2. Some Statistics Concerning Banking, Currency and Twin Crisis . . . . . . . . . . . . . . . . . . . . . . . . . . .744.4.3. The Determinants of Banking Crises . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .754.4.4. The Empirical Evidence on the Interrelation between Currency and Banking Crises . . . . . . . . . . .76

4.5. Conclusions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .77References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .78

Part V. Propagation of Currency Crises – The Case of the Russian Crisis£ukasz Rawdanowicz . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .795.1. Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .795.2. Definitions of Contagion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .805.3. The Channels of Crises Propagation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .805.4. Measuring Crises Propagation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .82

CASE Reports No. 41

5

Currency Crises in Emerging Markets – Selected Comparative ...

CASE Reports No. 41

5.4.1. Cross-Market Correlation Coefficients . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .825.4.2. Limited Dependent Variable Models . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .82

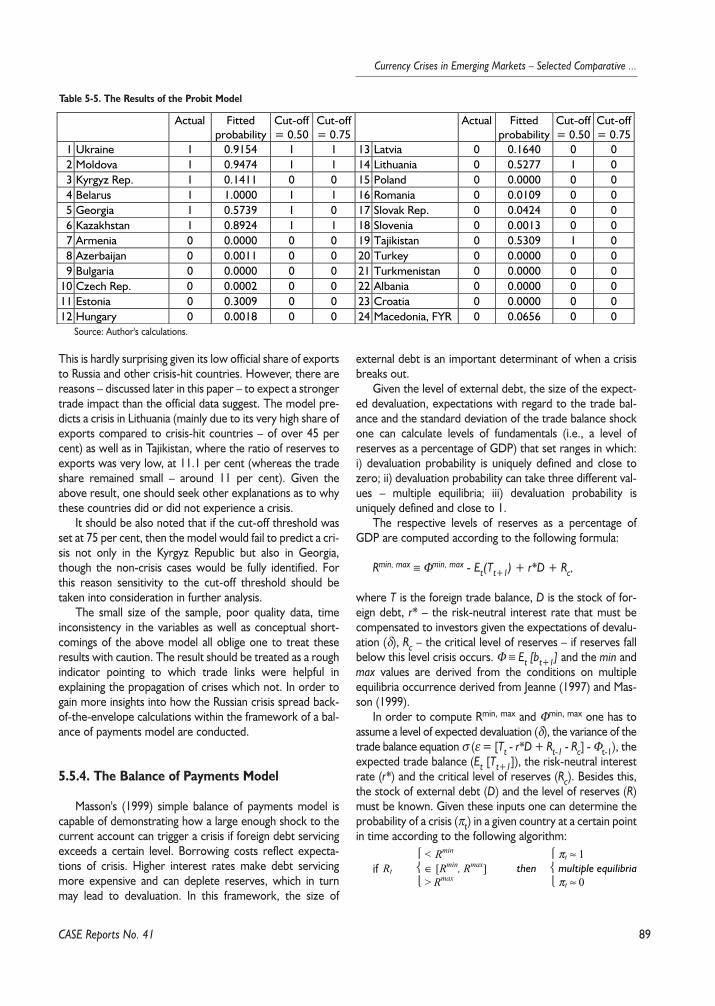

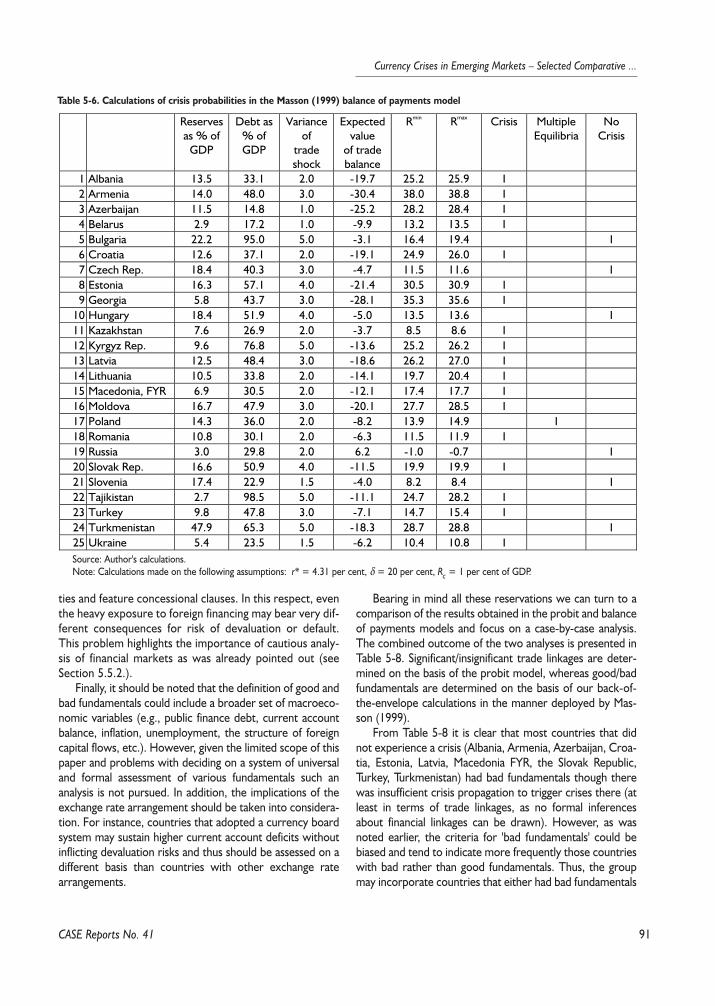

5.5. Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .835.5.1. Definition of a Crisis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .835.5.2. The Russian Crisis – Stylised Facts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .845.5.3. The Probit Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .885.5.4. The Balance of Payments Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .89

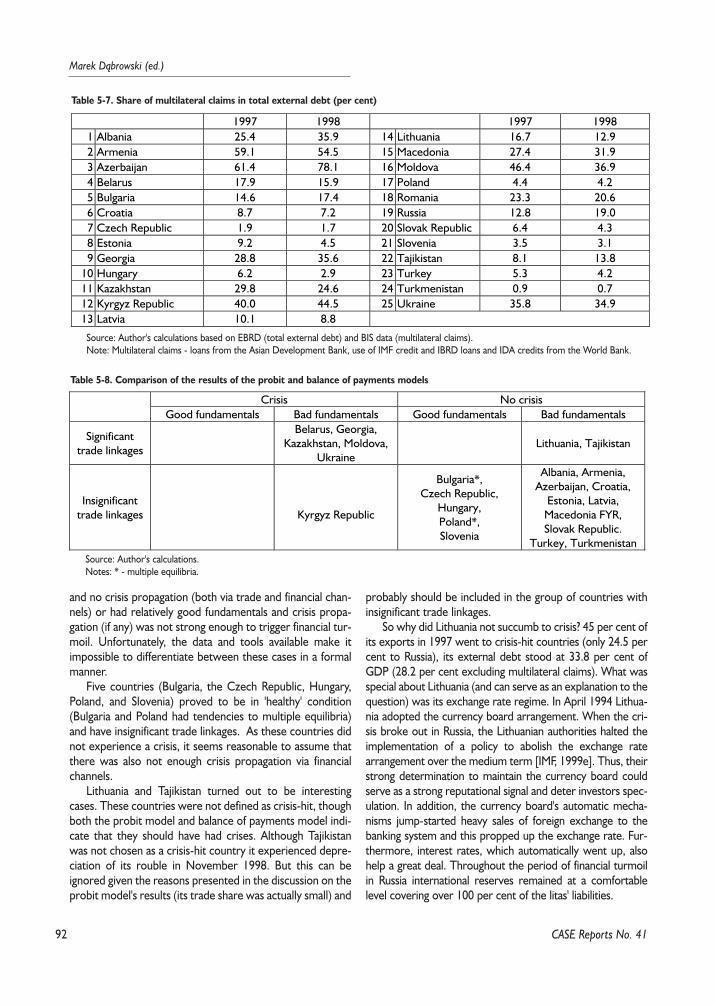

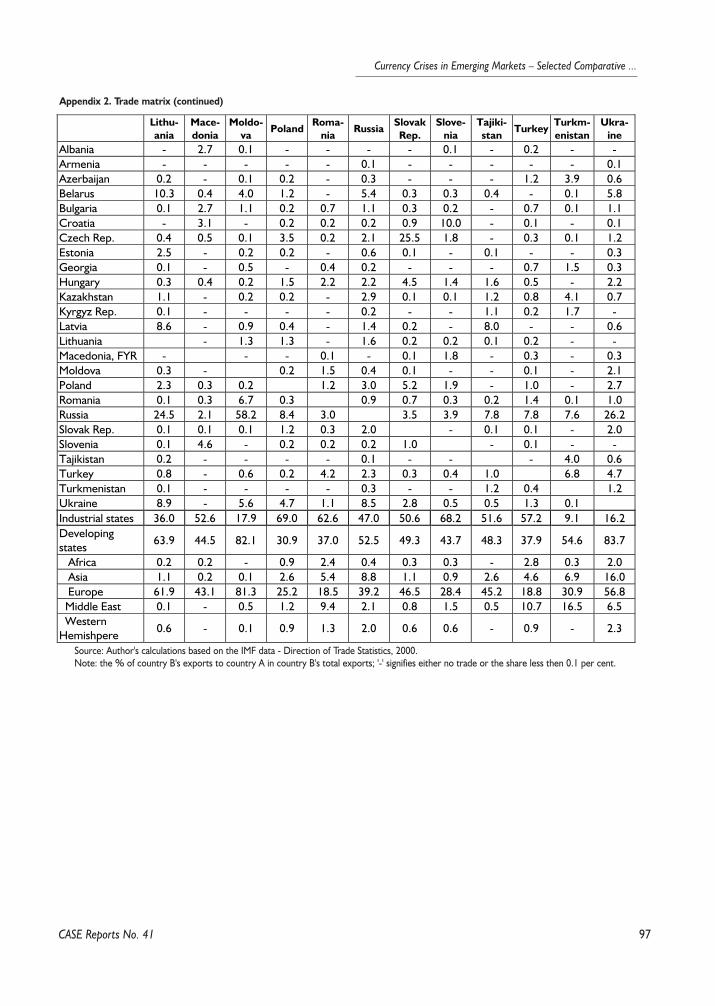

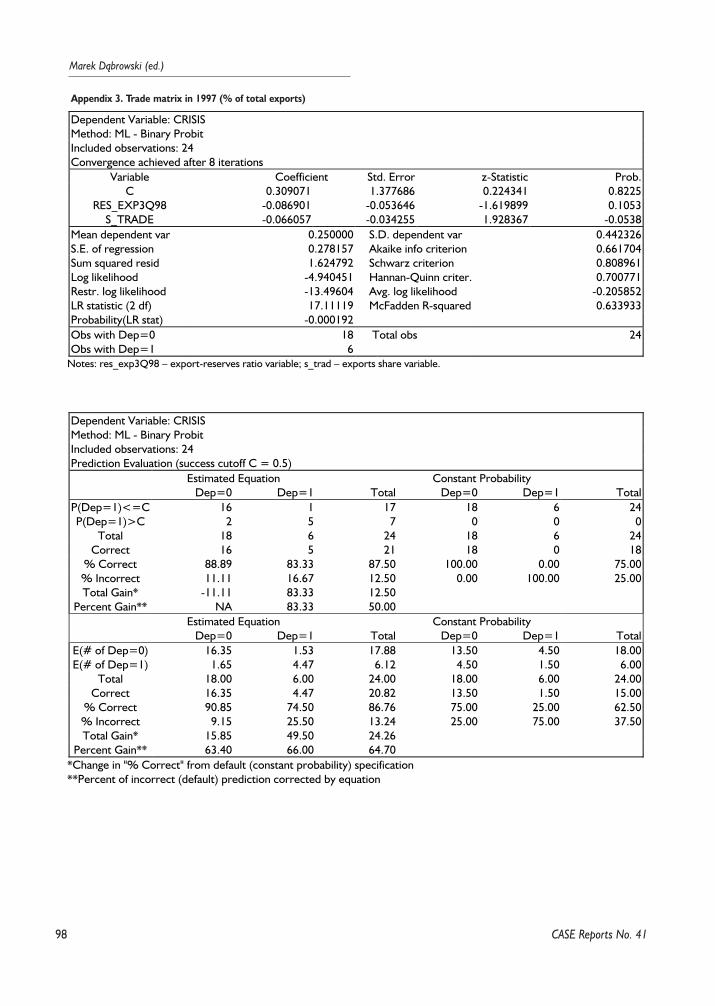

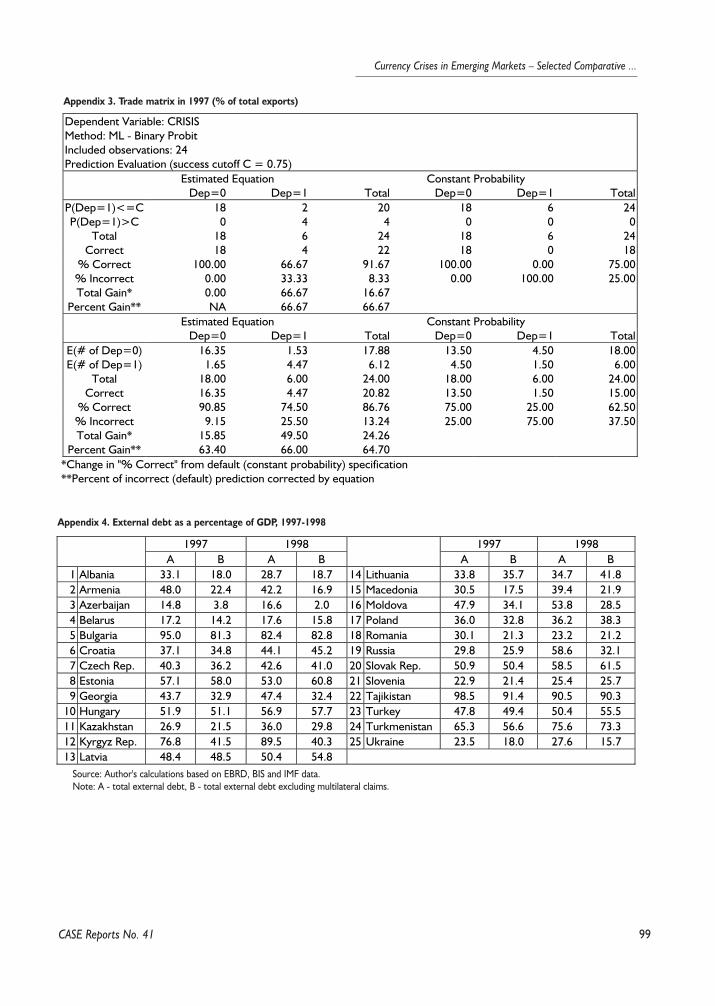

5.6. Conclusions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .93Appendix . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .95References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .100

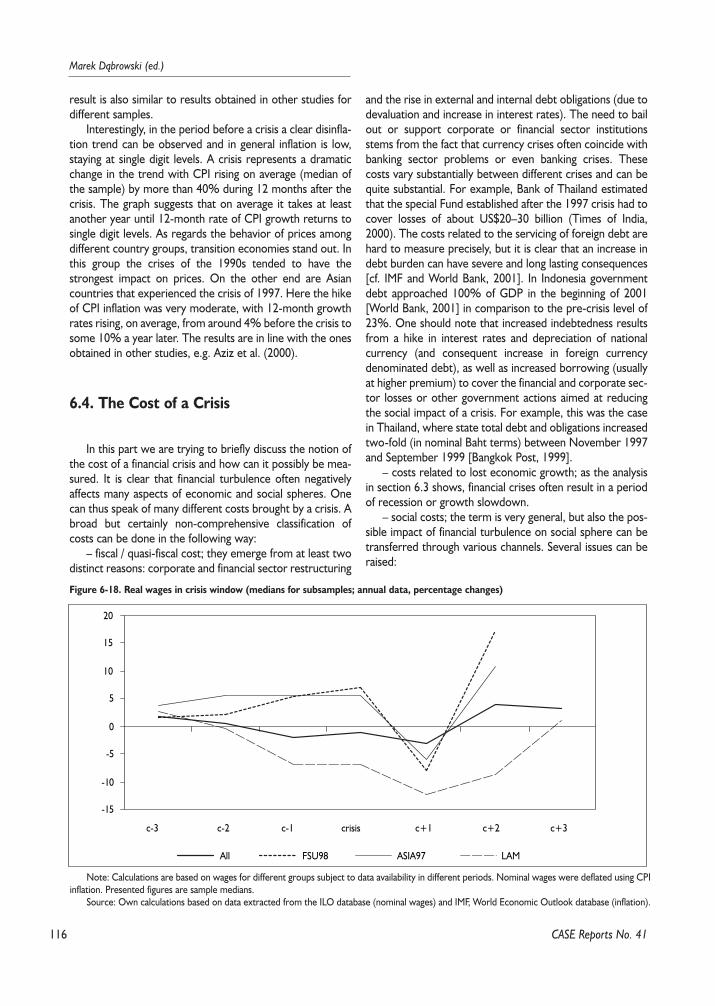

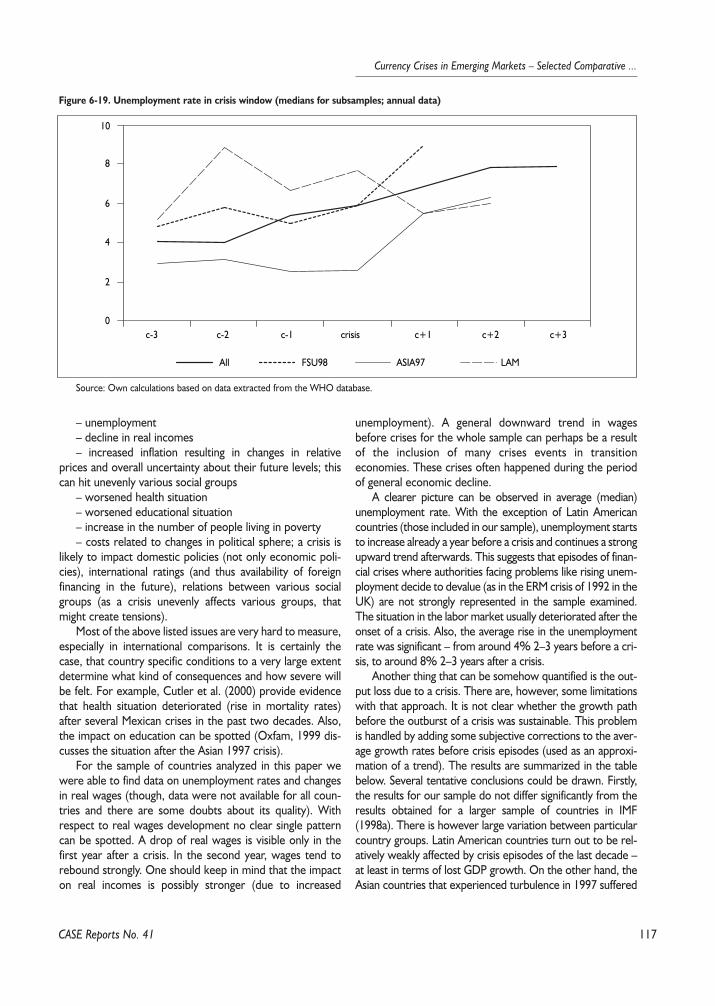

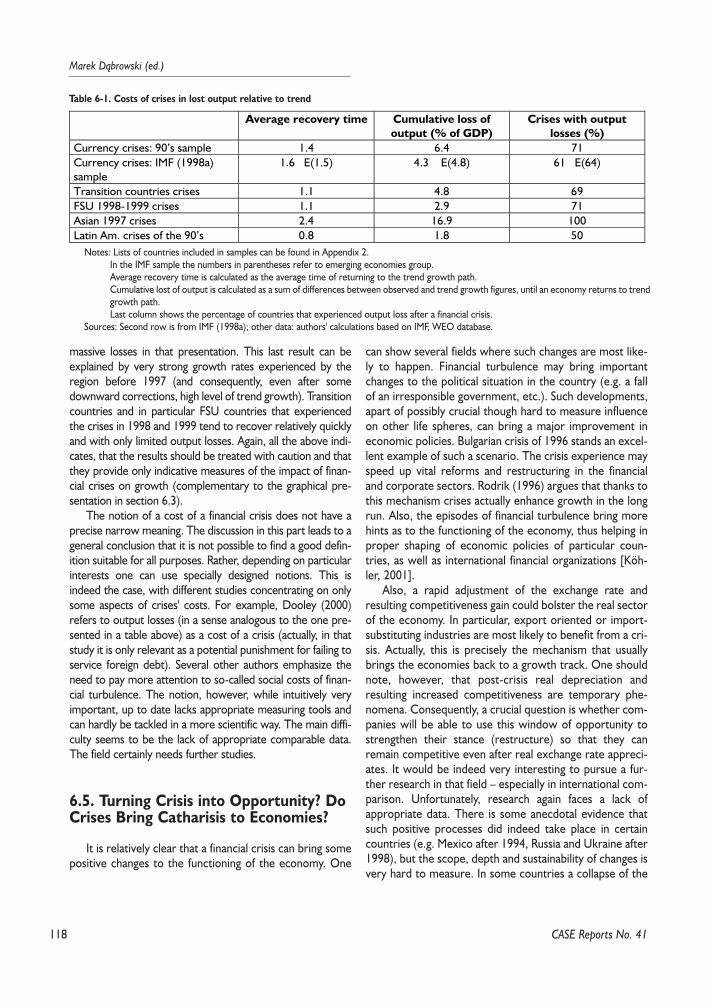

Part VI. The Economic and Social Consequences of Financial CrisesMonika B³aszkiewicz, Wojciech PaczyñskiPart VI. The Economic and Social Consequences of Financial Crises - Monika B³aszkiewicz, Wojciech Paczyñski1036.1. Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1036.2. Review of the Literature . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1046.3. Some Statistical Exercises . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1046.3.1. The Definition of a Crisis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1046.3.2. The Sample . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1056.3.3. Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1056.3.4. Economic Performance Before and After the Crisis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1056.4. The Cost of a Crisis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1166.5. Turning Crisis into Opportunity? Do Crises Bring Catharisis to Economies? . . . . . . . . . . . . . . . . . . . . . . .1186.6. Conclusions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .119Appendix. The Definition of a Crisis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .120References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .121

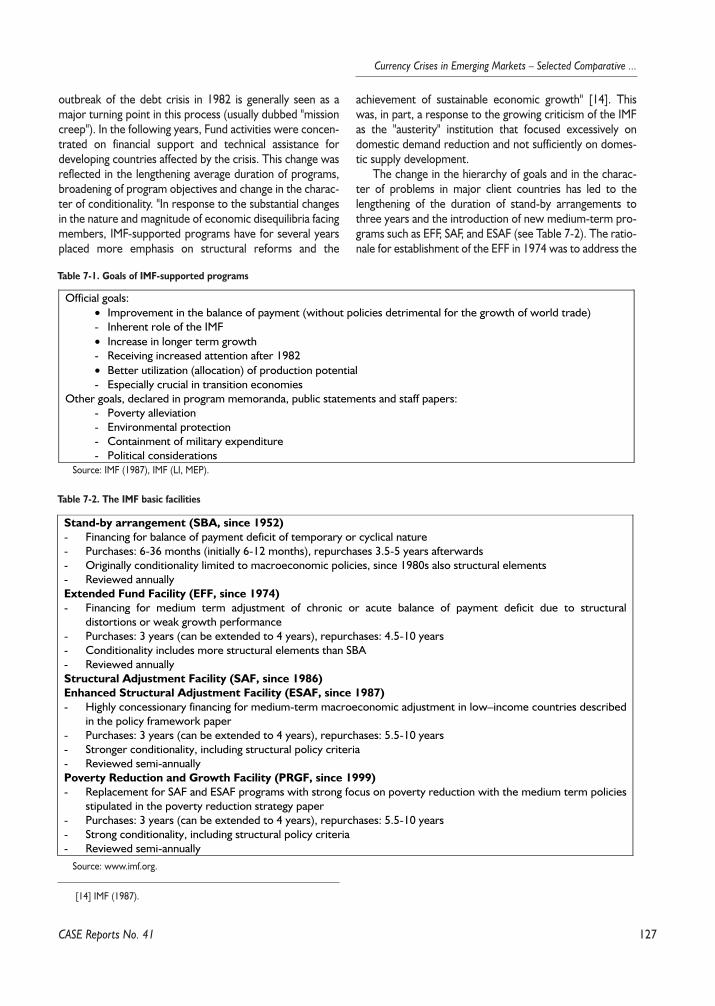

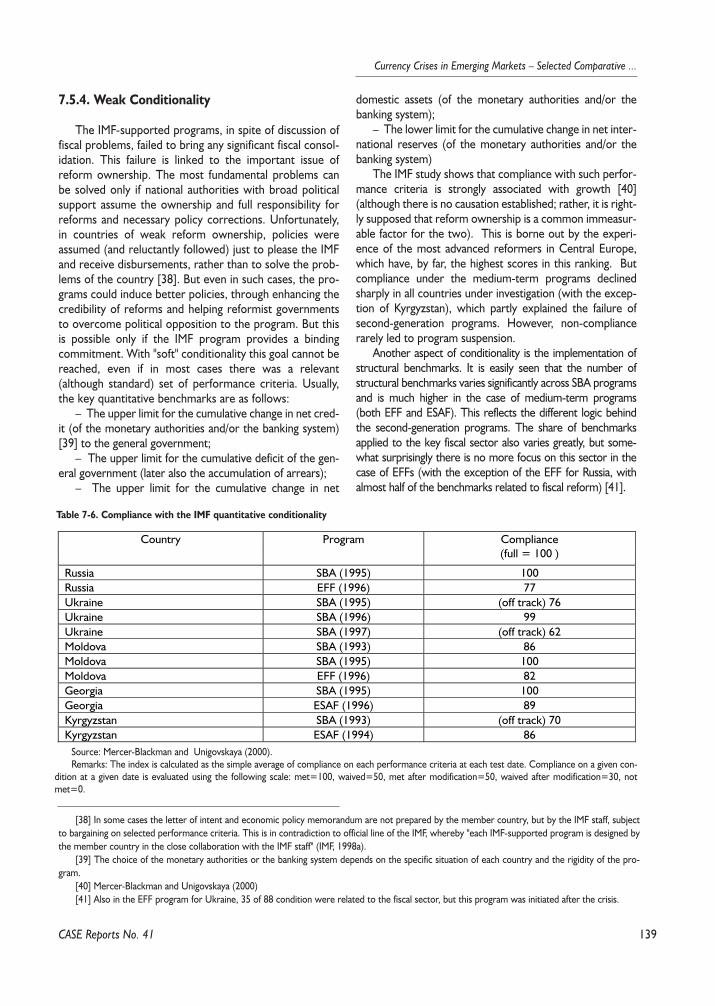

Part VII. Part VII. Financial Crises in FSU Countries: The Role of the IMFRafa³ Antczak, Ma³gorzata Markiewicz, Artur Radziwi³³ . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1237.1. Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1237.2. The Nature of Financial Crisis in FSU Countries . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1247.3. The Role of the IMF . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1267.4. IMF Programs in FSU Countries . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1297.5. Program Deficiencies and Consequences . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .131

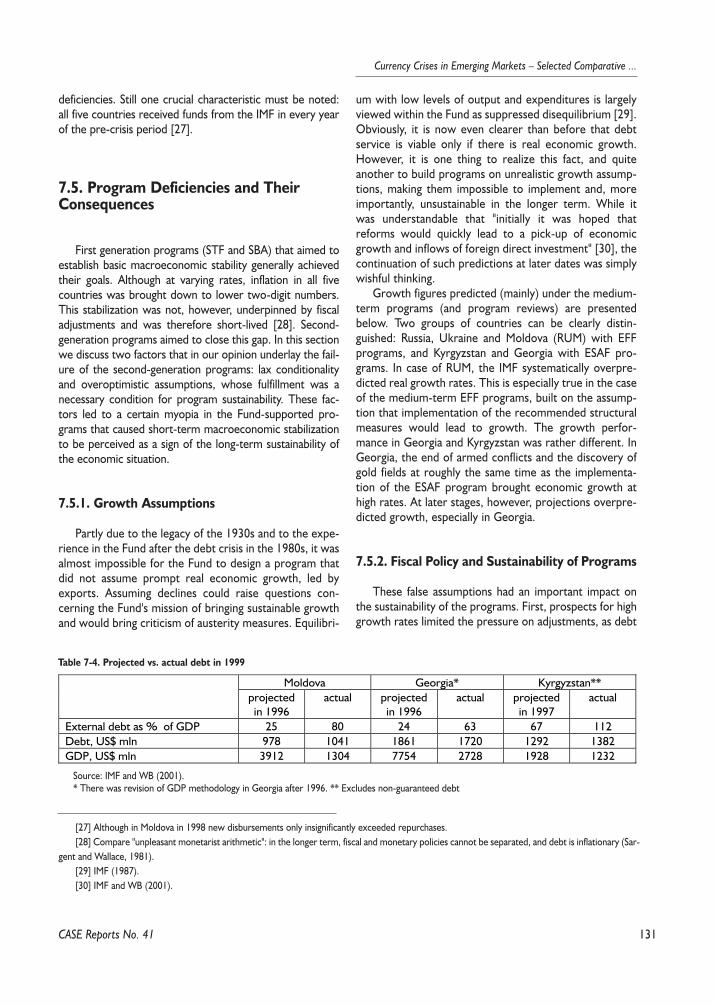

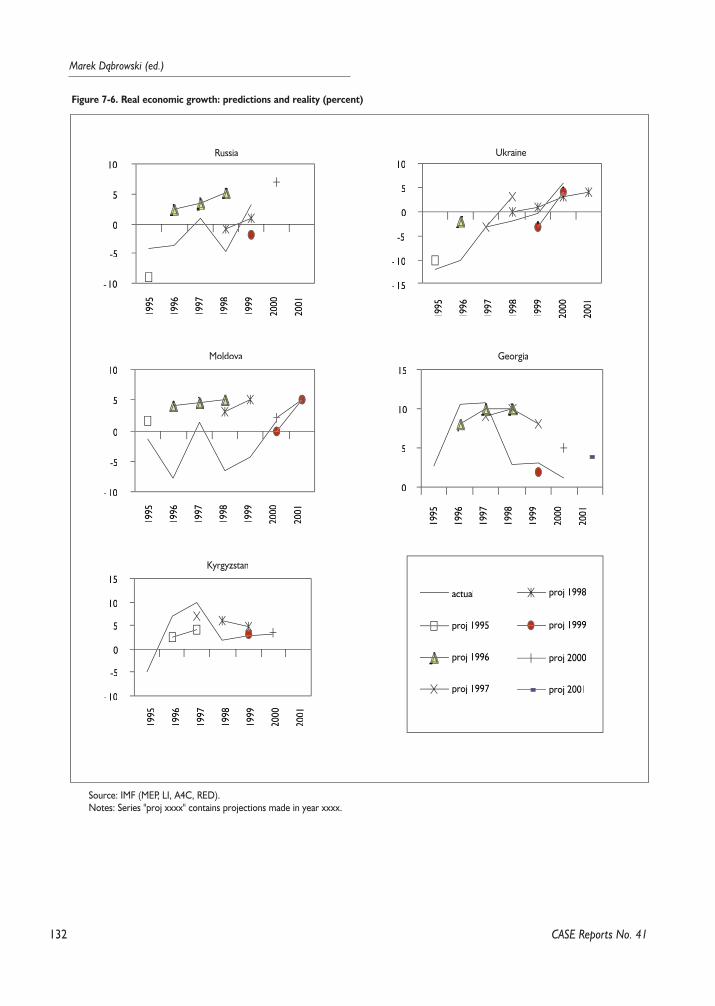

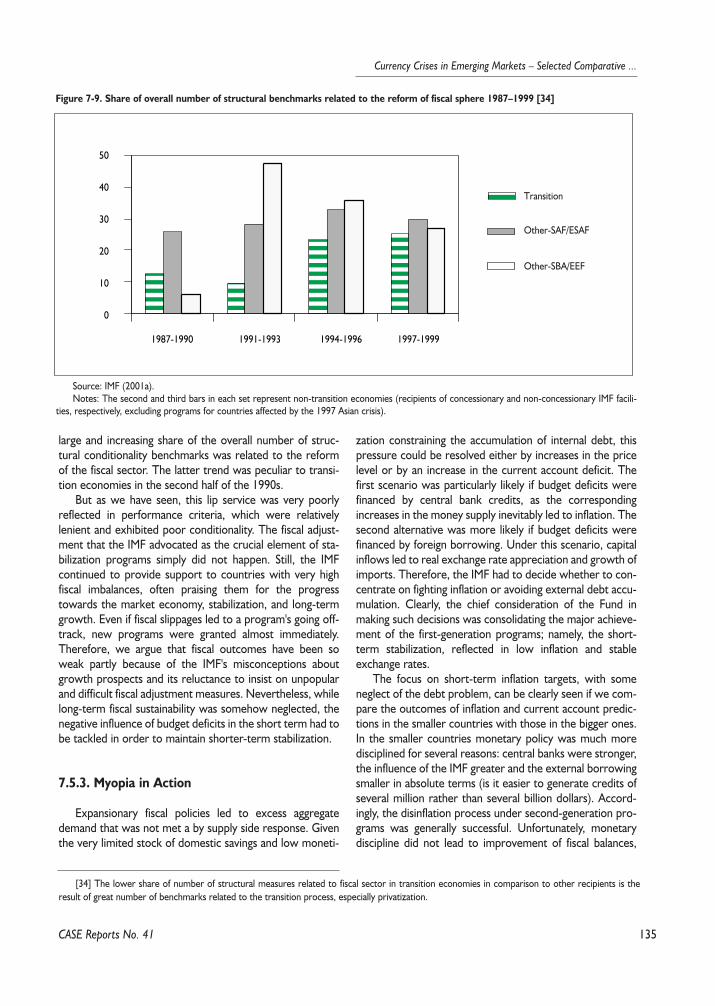

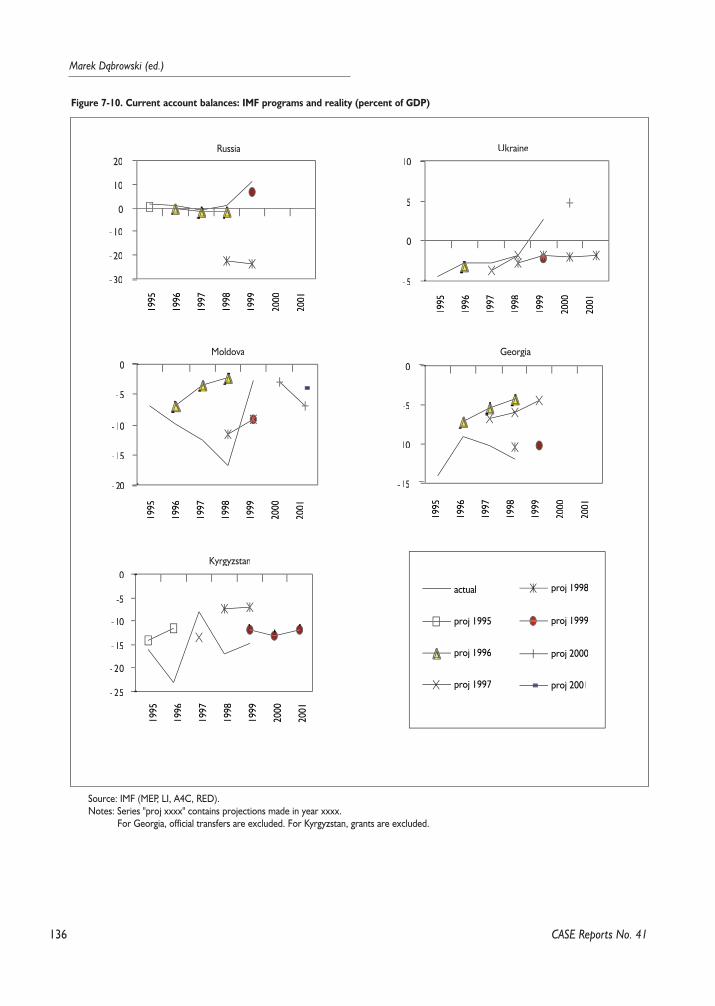

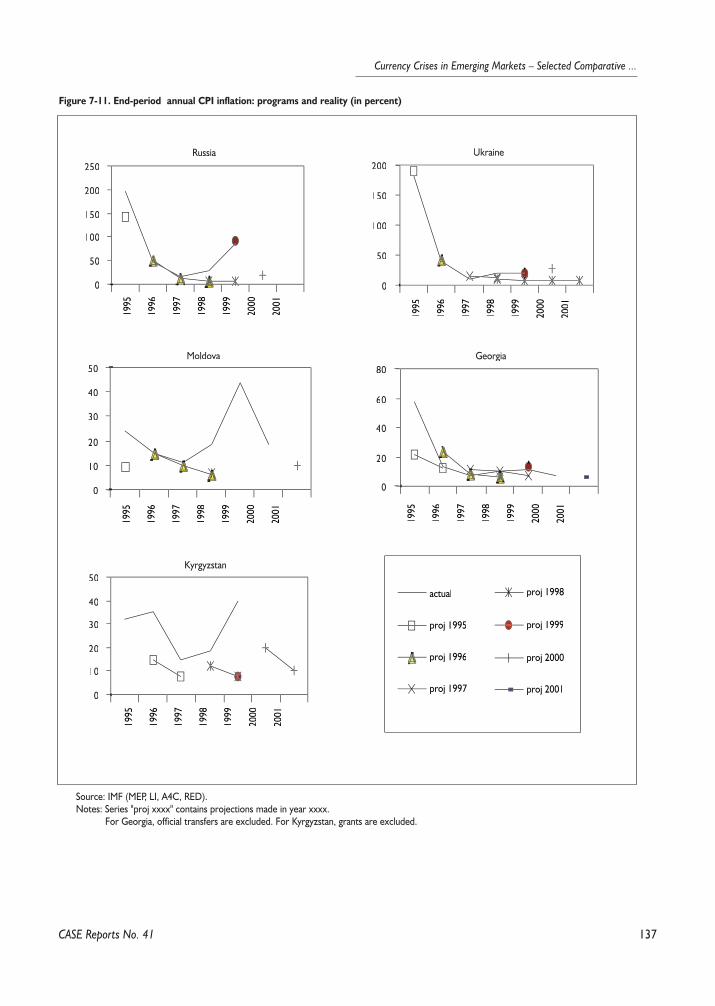

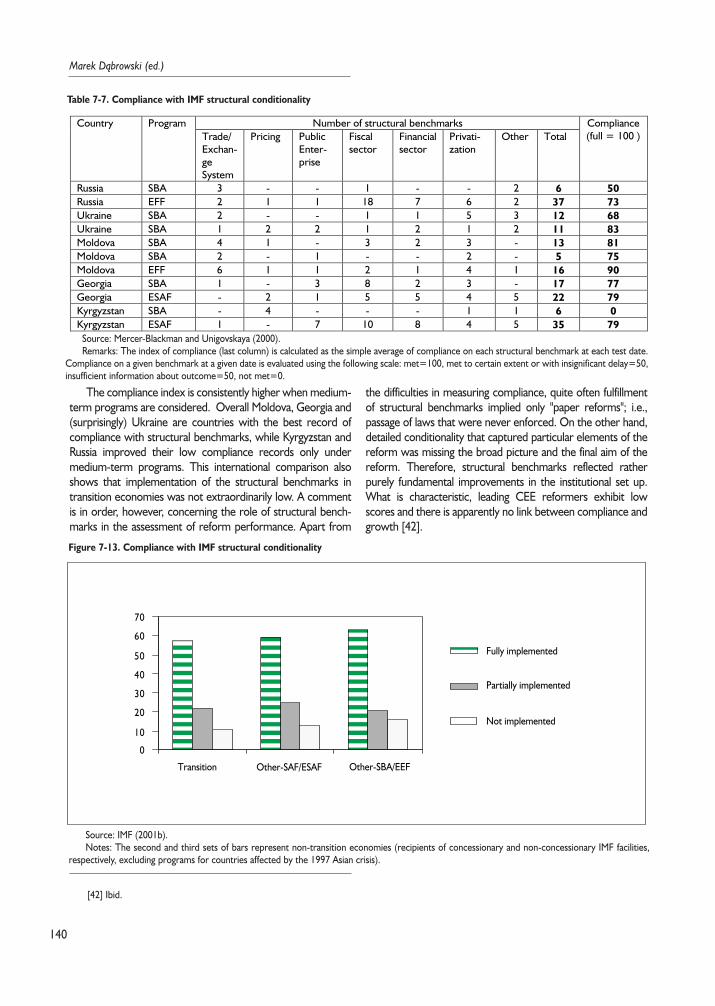

7.5.1. Growth Assumptions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1317.5.2. Fiscal Policy and Sustainability of Programs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1317.5.3. Myopia in Action . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1357.5.4. Weak Conditionality . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1397.5.5. Soft Financing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .145

7.6. Conclusions: Political and Institutional Considerations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .147

6

Marek D¹browski (ed.)

CASE Reports No. 41

Marek D¹browski

Marek D¹browski, Professor of Economics, V-Chairman and one of the founders of the CASE – Center for Social and Eco-nomic Research in Warsaw; Director of the USAID Ukraine Macroeconomic Policy Program in Kiev carried out by CASE;from 1991 involved in policy advising for governments and central banks of Russia, Ukraine, Kyrgyzstan, Kazakhstan, Geor-gia, Uzbekistan, Mongolia, and Romania; 1989–1990 First Deputy Minister of Finance of Poland; 1991–1993 Member of theSejm (lower house of the Polish Parliament); 1991–1996 Chairman of the Council of Ownership Changes, the advisory bodyto the Prime Minister of Poland; 1994–1995 visiting consultant of the World Bank, Policy Research Department; from 1998Member of the Monetary Policy Council of the National Bank of Poland. Recently his area of research interest is concen-trated on macroeconomic policy problems and political economy of transition.

Rafa³ Antczak

Rafa³ Antczak is an economist at the Center for Social and Economic Reasearch. The advisor to: the government of Ukraineand National Bank of Ukraine in 1994–1998, the government of the Kyrgyz Republic in 1995, and the President of Kaza-khstan in 1995. The research activities included also visits to Russia and Belarus. The main areas of activity combine macro-economic problems of transformation, monetary policy, and foreign trade.

Monika B³aszkiewicz

The author received MA in International Economics from the University of Sussex, UK ( 2000) and the Department of Eco-nomics at the University of Warsaw (2001). Presently, Monika B³aszkiewicz works for the Ministry of Finance at the Depart-ment of Financial Policy, Analysis and Statistics. Her main interest lies in short-term capital flows to developing and emerg-ing market economies and the role this kind of capital plays in the process of development and integration with the globaleconomy. In every day work she deals with the problem related to Polish integration with EU, in particular in the area ofEconomic and Monetary Union.

Ma³gorzata Jakubiak

Ma³gorzata Jakubiak has collaborated with the CASE Foundation since 1997. She graduated from the University of Sussex,UK (1997) and the Department of Economics at the University of Warsaw (1998). Her main areas of interest include for-eign trade and macroeconomics of open economy. She has published articles on trade flows, exchange rates, savings andinvestments in Poland and other CEE countries. During 2000–2001 she was working at the CASE mission in Ukraine as res-ident consultant.

Ma³gorzata Markiewicz

Ma³gorzata Markiewicz graduated from the Department of Economics at the Warsaw University. She has collaborated withthe CASE Foundation since 1995. She participated in advisory projects in Kyrgyzstan (1996, 1997), Georgia (1997) andUkraine (1995, 1998–2000). She has been an advisor to government and central bank representatives. Her main areas ofinterest include macroeconomic policies with a special emphasis put on fiscal problems and the correlation between fiscaland monetary policies.

7

Currency Crises in Emerging Markets – Selected Comparative ...

CASE Reports No. 41

Wojciech Paczyñski

Economist at the Centre for Eastern Studies, Ministry of Economy, Warsaw.Graduated from the University of Sussex (1998, MA in International Economics) and University of Warsaw (1999, MA inEconomics; 2000, MSc in Mathematics). Since 1998 he has been working as an economist at the CES. In 2000 started co-operation with CASE. His research interest include economies in transition, political economy and game theory.

Artur Radziwi³³

Artur Radziwi³³ is a researcher at the Center for Social and Economic Research (CASE) and a junior expert at the Interna-tional Economic Advisory Group in Moldova. He obtained his undergraduate education within the Columbia University Pro-gram. He received his MA in Economics at Sussex University, UK and at Warsaw University (summa cum laude).

£ukasz Rawdanowicz

£ukasz Rawdanowicz graduated from Sussex University in 1998 (MA in International Economics) and Warsaw University –Department of Economics in 1999 (MA in quantitative methods). His main area of interest is econometrics and macroeco-nomics (in particular issues on international economics, foreign trade, balance of payments, and forecasting). He is a co-author and editorial assistant of the quarterly bulletins Polish Economic Outlook and Global Economy. He was also involvedin the project on the development of a macro-model in the Kyrgyz Republic.

Marcin Sasin

Marcin Sasin has joined CASE Foundation in 2000. He is an economist specializing in international financial economics andmonetary policy issues. He obtained Master of Science at the Catholic University of Leuven, Belgium in 2000. He also holdsMA in Oriental Studies at the Warsaw University.

Mateusz Szczurek

Mateusz Szczurek is an economist at ING Barings covering Polish macroeconomics and fixed income analysis. He is also aPhD student at the University of Sussex, preparing the thesis on international liquidity and foreign exchange crises. He holdsMA in international economics from the University of Sussex, MA ineconomics from the University of Warsaw, as well as BA joint honours degree from Columbia University and Warsaw Uni-versity. He is a member of Polish Society of Market Economists, Polish Association of Business Economists, and the presi-dent of University of Sussex Polish Alumni group.

8

Marek D¹browski (ed.)

CASE Reports No. 41

This volume presents seven comparative studies of cur-rency crises, which happened in the decade of 1990s in LatinAmerica, South East Asia and in transition countries of East-ern Europe and the former USSR. All the studies were pre-pared under the research project no. OI44/H02/99/17 on"Analysis of Currency Crises in Countries of Asia, LatinAmerica and Central and Eastern Europe: Lessons forPoland and Other Transition Countries", carried out byCASE and financed by the Committee for ScientificResearch (KBN) in the years 1999–2001. They will be sub-jects of public presentation and discussion during the semi-nar in Warsaw organized by CASE on June 28, 2001, underthe same research project. This is a continuation of twoother issues of CASE Reports containing eleven countries'monographs related to currency crises episodes in thesethree regions and a couple of other comparative studiespublished in the CASE Studies and Analyzes series.

Three first studies in this volume deal with broad issueof current account, exchange rate and international reservesof a central bank.

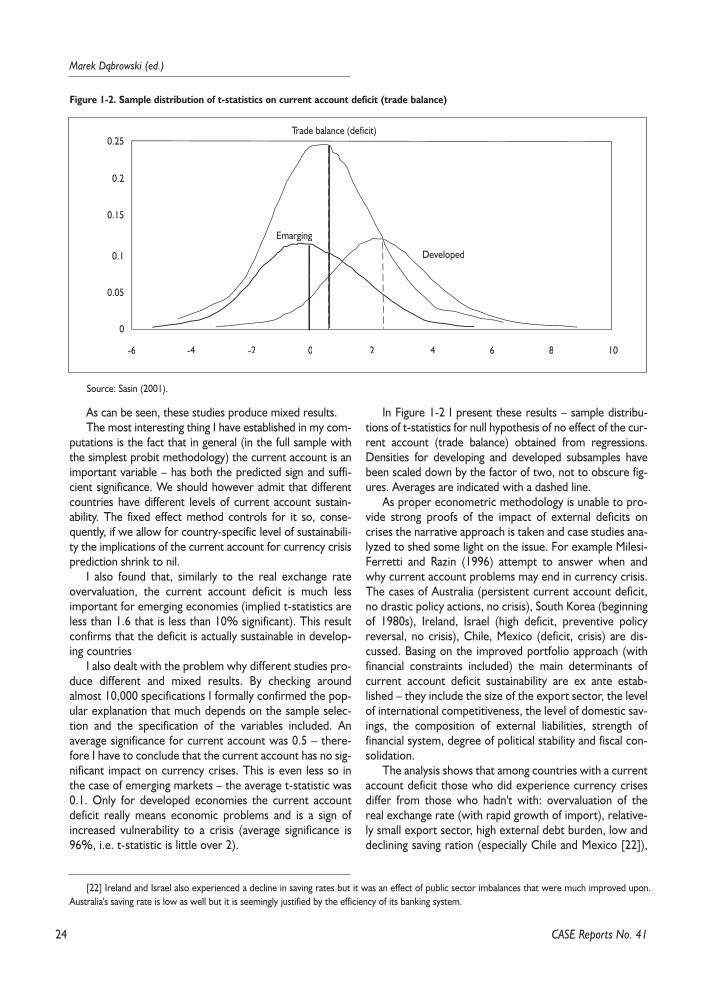

Marcin Sasin discusses the importance of the realexchange rate overvaluation and the current account deficit,which are usually considered as the main causes of currencycrises. While generally confirming the importance of the firstfactor, author shows that question of sustainability of currentaccount deficit has a very individual country characteristic.

The next analysis of Ma³gorzata Jakubiak concerns thechoice of exchange rate regimes from the point of view ofboth avoiding and efficient managing currency crises. Authorcompares advantages and disadvantages of the fixed versusfloating exchange rate regimes from the point of view ofcredibility of monetary policies, preventing currency crisisand coping with its consequences. She demonstrates, basingon an empirical analysis, that the most costly are changes ofexchange rate regimes (usually abandoning the peg) underthe pressure of speculative attack.

Mateusz Szczurek provides the additional insight to thisdiscussion estimating the size of optimal international liquid-ity taking into consideration potential costs of the crisis, onthe one hand, and costs of maintaining the internationalreserves, on the other.

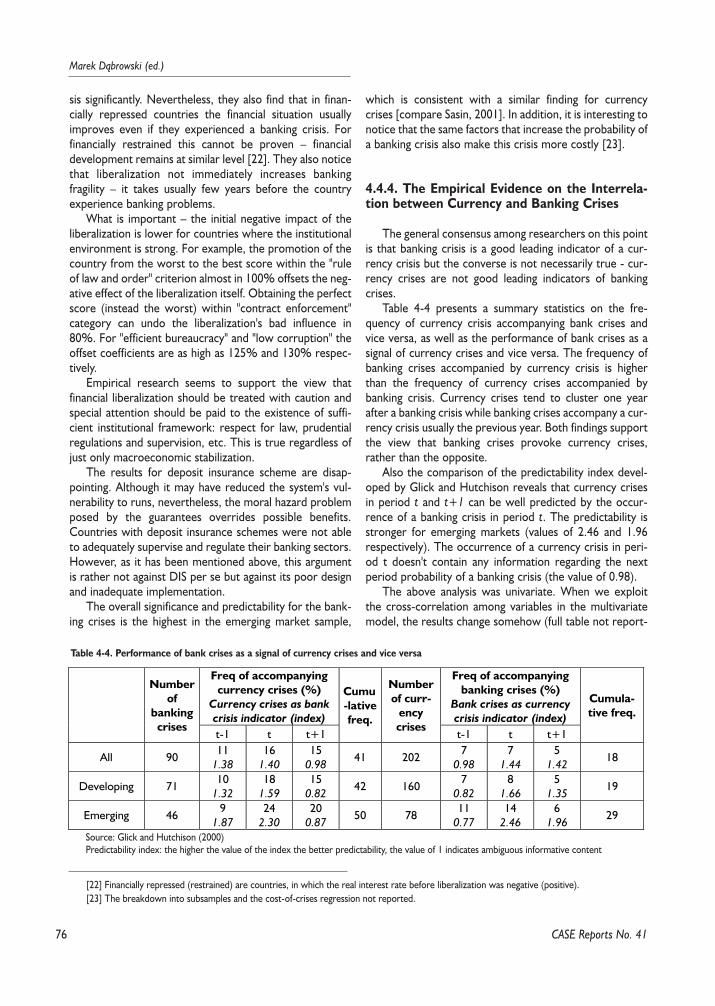

The next study concerns interrelations between bankingand currency crises basing on extensive review of an eco-nomic literature. Marcin Sasin analyzes the institutional andstructural sources of instability of the banking sector inemerging markets. One of them is the direct and indirectvulnerability of banks in relation to sudden interest rate andexchange rate changes. On the other hand, collapse of thesome big banks must lead to credibility crisis of a domesticcurrency.

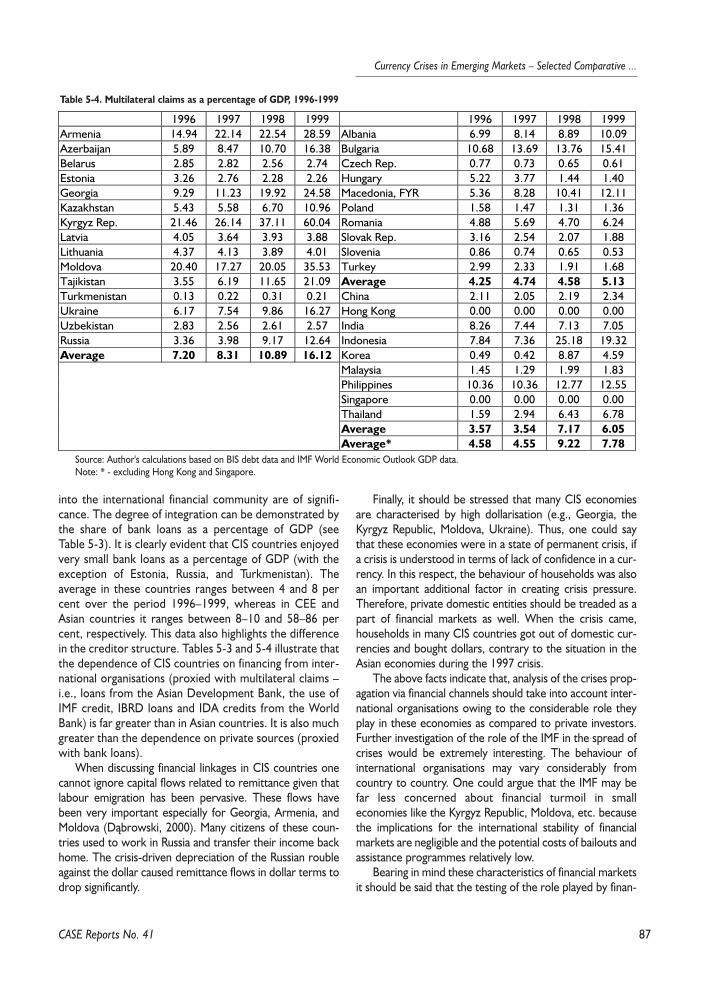

Lukasz Rawdanowicz addresses another hot issue in theeconomic debates of the last decade, i.e. contagion effect ofa crisis in one country on the macroeconomic stability of itsclose and more distant neighbors. He analyzes the impact ofthe Russian 1998 crisis on the situation of CIS countries tak-ing into consideration both trade and financial channels.

Monika B³aszkiewicz and Wojciech Paczyñski try toassess the economic and social consequences of currencycrises in the last decade. The main question discussed bythem is to what extent crisis plays a role of self-correctingmechanism of previously unsustainable policies.

Finally, Rafa³ Antczak, Ma³gorzata Markiewicz and ArturRadziwi³³ analyze the role of the IMF in preventing the cur-rency crises in five selected CIS countries – Russia, Ukraine,Moldova, Georgia and Kyrgyzstan, identifying the mainsources of Fund's failures.

Warsaw, June 13, 2001

IntroductionMarek D¹browski

9

Currency Crises in Emerging Markets – Selected Comparative ...

CASE Reports No. 41

1.1. Introduction

This paper investigates the links between real exchangerate overvaluation, current account deficit and currencycrises. Particularly an attempt is made to answer the ques-tion whether and to what extent overvaluation and currentaccount deficit is a cause of crises and how useful it is in cri-sis prediction.

Overvaluation and current account deficit are, ofcourse, interrelated variables. As for real exchange rate mis-alignment there is little disagreement that, indeed, it is awarning signal against possible distress – the empirical reg-ularities are presented along with a theory brief. The evi-dence on the current account is much more complicated.Not only there are various theories on how the currentaccount balance behaves and how sustainable it is but alsothe empirical research produces contradictory results onthe role of current account deficits as crisis cause or its earlyindicator. For this reason the current account issue obtainsmore extensive treatment.

1.2. Overvaluation

1.2.1. Theory

Law of one price states that, abstracting from trans-portation costs etc., prices of identical goods when con-verted from one currency to another should be the same.Otherwise an arbitrage would take place, the currencydemand/supply condition would change and finally equalityrestored through a change in the exchange rate to its equi-librium value.

s+ pi*=pi (1.1)

where pi is a (log) price of a good i, * indicates foreign vari-able and s is a (log) nominal exchange rate. Because pricesfor all goods are not observed (recorded) one can only useaggregate price levels.

s+p*=p (1.2)

which brings the notion of purchasing power parity (PPP)and real exchange rate

q=s-p+p*+k (1.3)

where q is a (log) real exchange rate and k is a constant.Because consumption bundles are not identical and pricesof goods of which they consist can relatively change andbecause aggregate price levels are only index numbers (notreal, direct prices), the "base year problem" arises – theabove expression holds only up to a constant k. In otherwords, one have to explicitly state in what point of time thereal exchange rate is in equilibrium, set q to zero andrespectively calibrate the constant.

Another problem is that there are various price indexesout of which popular are: consumer price index (CPI), pro-ducer price index (PPP), wholesale price index (WPI),export unit value (EUV). They, of course imply different val-ues for the real exchange rate. Composition of the sameindexes vary over countries making them imperfect mea-sures of overall price level and at the same time distortingthe meaning of the real exchange rate index.

It is well known that PPP doesn't hold continuously, itprobably even doesn't hold for quite long periods. There-fore a key question is whether there is any average valueof (such computed) real exchange rate, or put differentlywhether it is mean reverting (stationary). If yes, then ifthe rate is overvalued it will certainly depreciate in thefuture (sometimes through a currency crisis), if not (if theRER is nonstationary) than its level tells nothing about itsfuture development. The standard framework to test thestationarity of time series is Augmented Dickey-Fullertest.

(1.4)

where α, ϕ are parameters and ε is a disturbance term and∆ is a backward difference operator. This test has, howev-er, very low power against local alternatives, this is the rea-son why it is very hard to detect mean reversion (or reject

Part I.The Importance of the Real ExchangeRate Overvaluation and the Current Account Deficit in theEmergence of Financial Crisesby Marcin Sasin

t

k

iititt qqq εαϕα +∆++=∆ ∑

=−−

110

10

Marek D¹browski (ed.)

CASE Reports No. 41

nonstationarity) in the RER [1]. Soehow better alternative isto use Johansen's approach and test for cointegrationbetween s, p and p*.

On the other hand, the CPI-based RER can indeed benonstationary. Since there is a considerable share of non-tradable goods in the consumer's basket and since the PPPapplies only to tradable goods it can happen that if there isa different rate of productivity improvement in tradablegoods sectors between countries [2] the so-called Balassa-Samuelson effect arises. This effect refers to an apparentovervaluation of the CPI-based exchange rate: the price ofnon-tradable goods must increase to assure equal wagesacross sectors, this implies a (relative) rise in CPI in thecountry where the productivity gains are higher. Since com-petitiveness is not affected the (nominal) exchange rateremains unchanged; hence CPI-based RER becomes over-valued. This effect introduces a nonstationary trend in theCPI-based RER, which means, that the RER would never(systematically) come back to its historical average and theappreciation can continue indefinitely. In this case the level(overvaluation) of the RER would be almost meaningless,and (theoretically) should not contain any (or not enough)information for currency crisis prediction. Actually the caseis made, that the Balassa-Samuelson effect is present in mostemerging economies. Consequently, as evidence show, it isindeed harder to prove CPI-based RER mean reversion. Theevidence of PPI- and WPI-RER nonstationarity is moreample.

Another way of determining the real exchange rate is toderive it from the theoretical model of exchange rate (amonetary model). For example we can start from themoney demand function

m-p = φy - λi (1.5)

where φ, λ are parameters and m is money demand, y isoutput, i is nominal interest rate. Together with purchasingpower parity (2) we obtain

st = (mt-m*t) - φ (yt-y*t) + λ (it-i*t) (1.6)

where m is money supply. In this model, by construction,the real exchange rate is always in equilibrium. It is reason-able to introduce rigidities in the goods market. When inresponse to the shock prices adjust slowly the exchangerate behaves the following way

Et(st+1)-st = -θ (st-st) + Et(πt+1-π*t+1) (1.7)

which implies regressive expectations [3]; Et is an expecta-tion operator basing on the knowledge available at time t;the last term on the right represents structural differencesin inflation rates. After some algebra model yields a Dorn-busch-type equation (a Frankel model)

(1.8)where r is real interest rate. Now, in response to the shocksthe nominal exchange rate overshoots its equilibrium value,hence the RER becomes over- (under-) valued.

Until 1983, i.e. before tremendously influential paper ofMeese and Rogoff (1983), monetary models were believedto be valid [4]. After that, the research on exchange rate hasbeen paralyzed and only resumed since MacDonald and Tay-lor (1994) and Mark (1995) who has shown, using neweconometric tools, that monetary factors affect exchangerates and that these models hold in the long-run. It meantthat the exchange rate actually comes back to its model-predicted equilibrium value.

1.2.2. How to Calculate a Real Exchange Rate

When the mean reversion of the RER is established itmakes sense to estimate the over- (under-) valuation of theexchange rate. This is generally done in two ways:

The first approach (fundamental equilibrium exchangerate or FEER approach) is based on the assumption thatequilibrium RER implies balanced current account. Itexplores the general identity

current account = savings minus investment = change indebt = capital account

In the beginning the long run sustainable level ofdomestic savings and investment is estimated, then thenormal capital flows (at long run equilibrium interest ratedifferential, growth rate of the economy, etc.) are deter-mined. If the two sides are very different it means that thereal exchange rate is not in balance [5]. Afterwards, theequilibrium value that would equate the two sides isassessed basing on estimated coefficients of exchange rateelasticities of various macroeconomic variables. Subtract-ing prevailing exchange rate from the equilibrium onegives the RER overvaluation.

[1] The above reasoning should as well incorporate trend-reversion, which is even harder to detect than mean reversion.[2] The growth in productivity in non-tradable sector (usually services) is assumed to be the same across countries (e.g. zero).[3] With rational expectations derivation would be somehow more complicated but yield the same results.[4] Meese and Rogoff established that a simple random walk model performed better than monetary models in predicting exchange rate move-

ments.[5] It can also mean that the current government policy is unsustainable. The procedure is explained in more detail in section 1.3.3.1.

)(1

)()1

()()( ****tttttttttt rrEyymms −−−++−−−=

θππ

θλφ

∧

11

Currency Crises in Emerging Markets – Selected Comparative ...

CASE Reports No. 41

The second approach uses the econometric and statisti-cal tools and rather abstracts from detailed country-specificknowledge. The easiest way is to explicitly use the notion ofpurchasing power parity. One selects the price index (CPI,WPI, PPI) and a period of time, and then decides that theaverage of index-based RER over the chosen period consti-tutes an equilibrium rate. Subtracting that average from thecurrent index-based RER gives the RER overvaluation.Other popular method – the behavioral equilibriumexchange rate or BEER approach – is slightly more demand-ing and requires empirical estimation of the real exchangerate determinants what is usually done through one-equa-tion regression. Basing on the common knowledge and var-ious models relevant theoretical fundamentals are selected(these usually include the terms of trade, degree of open-ness, government expenditures, etc.) and included in theregression. Afterwards the fundamentals are decomposedinto permanent and temporary components – the perma-nent components are included in the estimated realexchange rate equation and equilibrium (fitted) rate isinferred. Even more sophisticated method requires anunderlying model of the exchange rate – it is usually a mon-etary model, like given by equation (1.6). First there is aneed to estimate parameters φ and λ what is done using his-torical data. Then the parameters together with domesticand foreign values for money supply, output, interest rateand price levels are substituted to the model. If we are(however unjustified) satisfied with a flexible model (6) thesubtraction of the result of (6) from a current exchange rategives the overvaluation measure. If we prefer the (morerealistic) sticky price model (7)-(8) by subtracting the resultof predicted exchange rate (8) from the current one, again,we obtain RER overvaluation [6].

In practice the values obtained for RER are obviously notprecise. This happens primarily because of: differentmethod used, different composition of price indexes andmeasurement errors. For example, Table 1-1 presents ananswer to the question whether the currencies of a countryin question were overvalued (before a crisis if applicable),given by various authors and produced with various meth-ods.

Although implications are quantitatively different, quali-tatively they are similar. So, there is a point in estimating theovervaluation, especially in light of a finding, that in generalthe overvaluation helps predicting currency crises – asexplained in the next section.

1.2.3. Overvaluation and Currency Crises,an Empirical Evidence

To fully understand the implications of the real exchangerate overvaluation one has to analyze its sources. Generallyspeaking, the overvaluation can arise as a consequence of:

– changes in the external environment: e.g. a change inthe terms of trade or a depreciation (devaluation) of majortrade partners' currencies. If these changes are temporarythe overvaluation is usually sustainable, if not (as in the caseof other currencies devaluation) they are the reason for anadjustment;

– a change in domestic situation (e.g. supply-sideshocks), particularly and most interestingly macroeconomicpolicy related causes. An exchange-rate-based disinflationprogram, when economic agents fail to believe the authori-ties about their targeted inflation and refuse to abandontheir (old) inflation expectations is one example. In suchcases inflation continues while the exchange rate is fixedwhat results in real exchange rate overvaluation – a signal,that the policy might have become unsustainable;

– financially related causes, most notably (excessive) for-eign capital inflows which put an upward pressure on theexchange rate.

The overvaluation can be undone basically by the exact-ly opposite processes to the above-mentioned. However, inpractice, it seems more difficult to arrange a smooth realdepreciation (restore the equilibrium) than to allow the realappreciation. This issue is tackled, for example, in Goldfajnand Valdes (1996). They assume that, after controlling forother macroeconomic fundamentals, the real exchange rateovervaluation can be undone in two ways: by cumulativeinflation differentials and by devaluation (among which acurrency crisis). Afterwards they calculate the probability

Table 1-1. The percentage overvaluation of currencies, as given by various studies.

Asia in 1997 MA PH TH IN KO SI Latin America MX BR AR CH CO PE VEChinn (PPI) ‘97 8 19 7 -5 -9 -6 STV 29Chinn(WPI) ‘97 17 24 13 30 -2 12 G-S 16Monetary ‘97 2 -25 2 2 -12 35

1994Dornbusch 30

G-S ‘97 mo mo mo mo mo mo G-S 22 -11 7 5 -4 -2 44Corsetti et.al.‘97 12 16 7.6 5.4 -13 18 JPM 3 1 13 -8 0 -5 9Sachs 1990-97 10 30 10 20 - 10

2000DB -2 5 17 0 10 5 -

mo- "moderately overvalued"; STV-Sachs, Tornell, Velasco (1995); G-S - Goldman and Sachs, G-S (2000); Chinn (1998), Monetary - Chinn (1998), mon-etary model; JPM - JP Morgan; DB - Deutsche Bank; Dornbusch (2001), Corsetti et.al. (1998), Sachs (1997)

[6] On top of an (justified and sustainable) "overvaluation" (overshooting) predicted by the model itself.

12

Marek D¹browski (ed.)

CASE Reports No. 41

that the overvaluation would end smoothly without a sharpdevaluation (crisis) for a large set of countries over the peri-od 1960–1994. They find that the probability of revertingthe prolonged (over six month) overvaluation successfully is32% for an appreciation not exceeding 15%. For 20% themisalignment the probability drops to 24%, for 25% itstands at 10%, for 30% overvaluation it is only 3%, whilethere is no undisturbed return from overvaluation morethan 35%. Goldfajn and Valdes also estimate the timing of acurrency collapse. Figure 1-1 presents their results – forvarious levels of initial overvaluation it depicts the probabil-ity that a devaluation (a crisis) would come within a givenperiod of time.

There is ample evidence that the real overvaluation canexplain currency crises. The simplest reasoning is: if theexchange rate is up it must come down (with or withoutgovernment approval) – just because it is mean reverting. Ithas also its indirect impact – first, if it stays high for a longtime this means that the authorities do not (want to) takeappropriate measures to bring it down, so, most probablytheir policy is unsustainable. Second it has a negative impacton the current account and if the deficit prolongs this intro-duces nervousness among investors about the prospects of

debt repayment – they might cut off their credit to thecountry forcing it to depreciate.

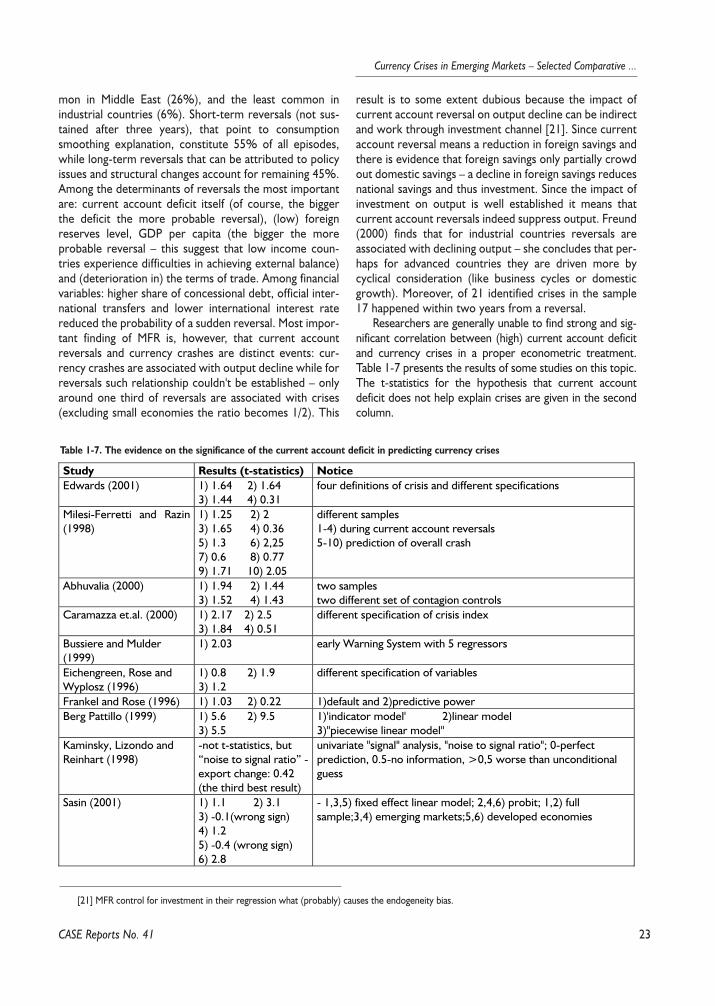

It may sound tautological but since the overvaluation is aleading indicator of devaluation, it should be also a predictorof a sharp devaluation, i.e. a currency crisis. Indeed, the eco-nomic research provides strong support for that view. Table1-2 presents the summary of various attempts to predictcurrency crises – these papers usually included realexchange rate overvaluation as one of explaining variables.In the second column the t-statistics for the null hypothesisthat the overvaluation is irrelevant in crisis prediction is pre-sented [7]. Whenever author tests more than one specifica-tion additional t-statistics are presented. The result present-ed in the table indicate strong support for the hypothesisthat real overvaluation is linked to currency crises.

In my study the real exchange rate turned out to be themost powerful crisis indicator. This result holds true evenwhen the model specification is changed. Both methods Iuse – i.e. a normal probability binary choice method (probit)and a panel fixed effect linear regression – produce similar,significant results with respect to that variable.

The advocates of the opposite view have only few argu-ments. The most often raised is the (above-mentioned) Bal-assa-Samuelson effect. According to it, real overvaluation(as revealed by price index) shouldn't matter in emergingeconomies because it does not impair competitiveness(tradable goods sector productivity rise is higher).

The results I obtained confirm that view to some extent.I established that the significance of the real exchange rateto currency crisis prediction is much lower for the emergingeconomies which would indicate that this effect is presentand the exchange rate is usually only apparently overvaluedwhile the external situation is actually sustainable. On theother hand, as Dornbusch (2001) argues, the Balassa-Samuelson model is often used to justify the sustainability ofovervaluation in the presence of large current accountdeficits, while, according to this model the apparent over-valuation shouldn't cause an external deficit.

Some researchers, skeptical about the econometricmethodology prefer to use "before-after analysis" which isusually done in graphs and depicts the stylized facts associ-ated with currency crises. Aziz, Caramazza and Salgado(2000) provide a recent example. They categorize crisesinto subgroups: crises in industrial countries, in emergingeconomies, crises characterized by currency crashes [8], byreserve losses, "severe" crises, "mild" crises, crises accom-panied by banking sector problems, crises with fast and slowrecoveries. Afterward, they analyze how the given variable(real exchange rate) behaves on average in the neighbor-hood of an average crisis.

[7] Values over 1.9 indicate that, in about 95% confidence, the real overvaluation has an impact on the emergence of currency crises. For around1.6 the confidence level is 10%.

[8] Crises in which currency depreciation accounts of more than 75% of a crisis index.

Figure 1-1.

Degree of appreciation (in %)

Prob

abilit

y of

col

lapse

in x

mon

ths

0.9

0.8

0.7

0.6

0.5

0.4

0.3

0.2

0.1

0.05 10 15 20 25 30 35

48 months

24 months

12 months

6 months

3 months

1 months

Source: Goldfajn, Valdes (1996).

13

Currency Crises in Emerging Markets – Selected Comparative ...

1.2.4. Trade-link Contagion: CompetitiveDevaluations

This section explores interrelation between realexchange rate, current account balance and one specificissue that connects them to currency crises, i.e. trade-link-induced contagion.

When other currencies depreciate (devalue), while thedomestic currency remains unchanged it actually undergoesovervaluation. The impact of these devaluations on thegiven country is the stronger, the stronger are links withdevaluing countries. Particularly trade links seem to play themajor role. If the country belongs to the same trade blockas countries with depreciated currencies, or if they com-pete on third countries' markets for an export share, thedevaluation of its partners may be a signal that the countrymight have to arrange a devaluation as well. Unless its part-ner's (real) devaluation is not undone by inflationary conse-quences in sufficiently short time the country's competitive-ness would be impaired and external situation becomeunsustainable. Investors understand it and launch a specula-tive attack on the given currency in anticipation of its deval-uation. As a result the authorities are immediately forced todevalue. After one country has devalued speculators attackanother, the most closely linked to the former one. Thisresults in the chain of competitive devaluation. Above-

described pattern is the essence of so-called trade-link con-tagion.

Economists differ on the issue whether trade links areimportant in the spread of crises. On one hand, theoreti-cal models allow for it, for example Gerlach and Smets(1994) build a model, which they then calibrate to fit thecase of Scandinavian countries. They show in simulationthat the devaluation of Sweden forces Finland in a shorttime to devalue as well. The competitive devaluation phe-nomenon was used as one explanation of recurrent deval-uations within European Monetary System in the period1992–1994.

The empirical evidence is, however, mixed but to theadvantage of the trade-link contagion. Eichengreen, Roseand Wyplosz (1996a) is one of the first papers to deal withthe issue – the authors find strong support for the view thattrade links play an important role in the spread of crises.Similarly Glick and Rose (1999), using different methodolo-gy, try to explain why currency crises tend to be regional –they find that the trade link is the most (or even the only)important factor that can explain the coincidence of crisesin regional blocks. The phenomenon that during (recent)crises stock market indexes tended to move together couldbe given as a proof of contagion. This fact is explored byForbes (2000) – she finds that, although trade connectionsdo not fully explain stock market returns during crises they

CASE Reports No. 41

Table 1-2. The evidence on the significance of real exchange rate overvaluation in predicting currency crises

Study Results (t-statistics) NoticeEdwards (2001) 1) 0.03 2) 1.05

3) 0.59 4) 0.12four definitions of crisisovervaluation as deviations from PPP

Milesi-Ferretti and Razin(1998)

1) 4.75 2) 4.93) 3.8 4) 3.045) 3.25 6) 3.757) 6 8) 5.69) 6 10) 2.8

different samples1-4) during current account reversals5-10) prediction of overall crash

Ahluvalia (2000) 1) 2.7 2) 33) 1.46 4) 2.48

two samplestwo different set of contagion controls

Caramazza et.al. (2000) 1) 2.17 2) 1.703) .62 4) 1.07

different specification of crisis index

Bussiere and Mulder(1999)

1) 1.9 early Warning System with 5 regressors

Frankel and Rose (1996) 1) 1.51 2) 2.53 1)default 2)predictive powerBerg and Pattillo (1999) 1) 15,9 2) 13,5

3) 3,351)'indicator model' 2)linear model3)"piecewise linear model"

Goldfajn and Valdes(1996)

1) 1.69 2) 1.533) 2.63 4) 1.51

different models and nominal vs. real devaluation

Kaminsky, Lizondo,Reinhard, (1998)

not t-statistics, but“noise to signal ratio”1) 0.19 (the best result)

univariate "signal" analysis, "noise to signal ratio"; 0-perfectprediction, 0.5-no information, >0,5 worse than unconditionalguess

Sasin (2001) 1)4.7 2)5.43)1.6 4)2.85)4.1 6)2.6

-1,3,5)fixed effect linear model; 2,4,6) probit; 1,2)full sample;3,4)emerging markets; 5,6)developed economies -ActuallySasin checks around 10,000 specifications and concludes thatan average significance for RER is 4 with standard deviation ofabout 2.

14

Marek D¹browski (ed.)

are undoubtfully economically and statistically important.What is worth to notice is the fact that in the above-men-tioned analyses other macroeconomic variables are more orless insignificant with respect to contagion. Sasin (2000), inturn, constructs an index of vulnerability to trade-link con-tagion and proves that this index is highly significant in crisisprediction.

On the other hand, Masson (1998) argues that trade(which he categorizes as a "spillover") cannot explain thecoincidence of speculative attacks on Latin America's andAsian currencies during, respectively, Mexican peso andThai baht crises. Baig and Goldfajn (1998) also reject theimportance of trade links in the spread of crises.

Finally several authors [e.g. Caramazza et. al., 2000] takean intermediate attitude and claim that trade effects areactually important but are usually overshadowed by other(notably financial) factors. Apart from the evidence obtainedfrom econometric estimations, the pattern of competitivedevaluation is very appealing. This point of view, especiallywhen financial investors subscribe to it, can, of course,become a self-fulfilling prophecy

1.3. Current Account

1.3.1. Evolution of the Point of View on the Current Account

It is interesting to notice that over past decades therehave been important changes in the way the economist viewthe current account – a throughout survey is included inEdwards (2001), on which this section draws. It can be saidthat with respect to policy implications and/or currencycrises this evolution came from "current account deficit mat-ters" through "current account deficit is irrelevant as long asthe public sector is balanced" and, again, "deficit matters"finally to "deficit may matter".

1.3.1.1. The Early Views: the Trade/Elasticity Approach

The 1950s up to mid-1970s discussion on country'sexternal position was dominated by the "elasticity approach"and stressed issues like trade flows or terms of trade. Dur-ing this period most developing countries used to run largeand persistent current account deficits – the usual remediesto counteract the problem were recurrent devaluations.Economists, convinced that the external position should bebalanced, focused on issue whether devaluations brought animprovement to the situation – the improvement, in turn,depended on export and import price (exchange rate) elas-ticities. These studies resulted in a so called "elasticities pes-simism" – the inferred elasticities were small meaning that

the country had to arrange a large exchange rate adjustmentto improve its external position. Nevertheless, after exam-ining 21 major devaluations during 1958–1969 Cooper(1971) argued that on average devaluation succeeded inbringing the current account back to balance. On the otherhand, other authors claimed that since developing countriesexported mainly commodities and since there was noprospect for a surge in demand for such goods in the worldmarket – the devaluations were ineffective and broughtabout only recession and income contraction. The answerwas not to devalue (one time after another) but to encour-age industrialization through import substitution policies.The view – advocated, among others, by prominent UNofficials – turned out to be totally wrong.

1.3.1.2. Intertemporal Approach: the Irrelevance ofthe Current Account Deficit and the Lawson Doctrine

During the second part of the 1970s the world experi-enced an oil shock and, partially because of that, most coun-tries' current account worsened dramatically – between1973 and 1979 the aggregate developed countries' externalposition moved from an US$11 bln surplus to an US$28 bil-lion deficit (reflected, of course, in enormous OPEC coun-tries' surplus). These developments forced economists totake a closer look on the determinants of a current accountand its further sustainability. The most important progresswas dropping the trade-flow/elasticity approach and focus-ing on intertemporal dimension of the current account. Thefact that from the national accounting perspective the cur-rent account is just equal to national savings minus invest-ment was rediscovered. On the other hand, both savingsand investment decisions are based on intertemporal factors– such as permanent income, expected return on invest-ment project, etc. – so, as a consequence, the currentaccount is an intertemporal phenomenon. The (policy)implication was that as long as (large) current account deficitreflected new investment perspectives but not falling savingrates there was no reason to be concerned about it. Thedeficit meant only, that economic agents, expecting futureprosperity brought by new investment opportunities, wereonly smoothing their consumption paths – the consumptionwas moved from the future to the present and financed byforeign sector (i.e. by debt accumulation), which would berepaid later, when growth prospects materialize. The influ-ential paper by Sachs (1981) insisted on this view.

In the beginning of 1980s, the intertemporal approachalso gave answers to concerns about mounting debt prob-lem. Sachs (1981) claimed that because this debt reflectedincrease in investment in the presence of rising (or stable)saving rates it should not pose a problem of repayment. Inaddition, the new approach made a distinction between thedeficits that result from fiscal imbalances and those reflect-ing private sector decisions. The public sector was thoughtto act rather on political than on economic and rational

CASE Reports No. 41

15

Currency Crises in Emerging Markets – Selected Comparative ...

grounds, so the current account deficit induced by the bud-get deficit was "bad", while private sector's decisions wereassumed rational and the current account deficit respondingto them was optimal, i.e. "good" – in the future the privatesector would be able to make necessary corrective actions(while public sector most probably not). The argument thata large current account deficit is not a cause of concern ifthe fiscal accounts are balanced is associated with formerChancellor of the Exchequer, Nigel Lawson, and thereforeit is known as "Lawson's Doctrine" [9]. It has also becamewidely accepted paradigm for the external situation analysis– for example, in 1981, when Chile's current account deficitexceeded 14% of GDP senior IMF officials assured that aslong as the "twin deficits" do not coincide there is absolute-ly no reason to be concerned.

The debt crisis of 1982 exposed the obvious inadequacyof prevailing views on the current account. In fact, the crisiserupted in countries, of which most were running large cur-rent account deficits simultaneously with balanced fiscalaccounts and/or increasing investment rates. The crisis hadrather profound implications. In Latin America, for example,the net transfer of resources swung from more than US$12billion yearly inflows between 1976 and 1981 to the averageUS$24 billion a year outflows in the following five year peri-od. The forced adjustment brought about through import(of capital and intermediate goods) and investment contrac-tion resulted in a serious recession. During much of the1980s most developing countries were cut from the inter-national capital market and running external surpluses ormoderate deficits. The Lawson Doctrine was (by majority)abandoned and emphasis put again on the current accountand the (real) exchange rate (overvaluation). The reasoningwent, again, that large current account deficits were (often)a sign of troubles and a rationale for devaluation.

1.3.1.3. Surge in Capital Inflows: from the 5% Rule ofThumb to "Current Account Sustainability"

The end of 1980s and the beginning of 1990's witnessedsome major changes in the world economy, of which themarket oriented reforms in developing countries as well asrapid development in the international financial market andsurge in capital flows were the most pronounced. Unprece-dented amount of these flows was directed into emergingmarkets, which were apparently not prepared to absorbsuch a capital overabundance. The surge in inflows induceda real exchange rate appreciation, loss of competitivenessand, again, a current account deficit. Another problem wasthat capital inflows in the presence of insufficient investmentopportunities crowded out domestic savings to some

extent. These processes were readily visible in Mexico; thecurrent account deficit during 1992–1994 averaged 7% ofGDP and, as the World Bank (1993) estimated, about two-thirds of the widening of the current account deficit in 1992could be ascribed to lower private savings. Eventually Mex-ico experienced a currency crisis in 1994–1995 [10].

The importance of external balances in limiting country'svulnerability to currency crisis was reiterated after the cri-sis. The prevailing view was that large current accountdeficits were likely to be unsustainable, regardless of theunderlying factors. The US Secretary of the Treasury LarrySummers explicitly stated that close attention should bepaid to any current account deficit in excess of 5% of GDP.This number has been, and still is, very popular in assessinga vulnerability to a crisis. Indeed, studies show [11] that onaverage a 4% of GDP is a threshold over which currentaccount deficit becomes a concern to private sector ana-lysts. On the basis of this rule of thumb, warning has beenaddressed to Malaysia and Thailand that they should containtheir deficits, which in the second part of 1990s wentbeyond the safe line.

The overabundance of capital created a problem of itsefficient intermediation and in many cases problems ofspeculation and moral hazard. In addition, as opposed to1970s capital flows that took form of syndicated bank loans,in the 1990s the capital streamed into equity and bondinstruments. Since portfolio flows are quite volatile anapparently underestimated threat of (possible) suddenreversals emerged. The focus on current account deficitwas not only with respect to its existence but also to how itwas financed. In contrary to short-term flows, the FDI flowswere thought to be desirable way of sustaining the deficit.

It is still a controversial and unresolved issue whethercurrent account deficits were a primary cause of the 1997Asian crisis. Corsetti et.al. (1998) find some support for thishypothesis and argue that a group of countries that cameunder attack in 1997 appear to have been those with largecurrent account deficit throughout the 1990s. But this sup-port is very limited – for five main Asian countries during1990–1996 the deficit exceeded an arbitrary 5% only 12out of 35 possible times, for two years preceding crises thisratio even comes down to 3 out of 10 possible times.

The relatively balanced fiscal and external position ofAsian countries before the crisis only confused economistsand researchers. I try to distinguish between (generallyspeaking) two ways of understanding the importance of cur-rent account for currency crises. Both are connected witheach other and can be described as "current account deficitmay matter".

CASE Reports No. 41

[9] As will be discussed later, the Lawson Doctrine is not (directly) implied by the intertemporal model.[10] Mexican officials still claim that large current accont deficit was not a main cause of the crisis because, what's interesting, the public sector

finances were under control.[11] See, for example, Ades and Kuane (1997).

16

Marek D¹browski (ed.)

CASE Reports No. 41

First, many economists argue that the nature of curren-cy crises has changed overtime. Dornbusch (2001), forexample identifies, that the old-style crises involved a cycleof overspending and real appreciation that worsened thecurrent account – usually the external deficit was a counter-part of a budget deficit. The debt rose, foreign reservesdeclined and finally country had to arrange a devaluation. Inthis respect they were current-account-crises. The new-style crises are centered on doubts about the solvency ofthe balance sheet of a significant part of the economy andthe exchange rate. The balance sheet may be underminedby the large portfolio of non-performing loans or by maturi-ty (or currency) mismatches. The crisis is triggered by sud-den capital flight. This view recognizes that capital marketsrather than current account dominate exchange rate issues.The role for real overvaluation and current account deficit issecondary rather – it can act as a focal point in inviting cur-rency crises to the country already having a balance sheetproblem. Dornbusch (2001) speculates that it is safe to saythat a rapid real appreciation amounting to 25% or moreand an increase in the current account deficit to exceed 4%of GDP, without prospects of correction, take a country intothe red zone.

Secondly, various authors, suspicious of one-for-all 4%threshold and believing that the current account deficit is abasis and deeply underlying cause for external crises, try todefine the notion of "current account sustainability".Because of the lasting improvement in capital marketaccess, persistent terms of trade improvement and pro-ductivity growth emerging economies can, as it is predict-ed by the intertemporal models, finance moderate currentaccounts on an ongoing basis. The weakest notion of sus-tainability implies that the present value of the (future) cur-rent account deficits (plus debt) must equal the presentvalue of the (future) surpluses, or in other words that acountry will (in infinity) repay its debt. This criterion is cer-tainly not satisfactory – the debt repayment prospect maybe too distant and it says nothing about the appropriate-ness of a present deficit – virtually any present deficit canbe (somehow) undone by sufficiently large surplus in the(unspecified) future. According to the stronger notion ofsustainability, the deficit is sustainable if it can be revertedinto sufficient surplus in the foreseeable future and debtrepaid on an ongoing basis (in a sense of non-increasingdebt/GDP ratio) without drastic policy changes and/or acrisis. This definition is a starting point for a calculation ofa sustainable current account – if the actual deficit lastslonger above sustainable level and a country doesn'tundertake corrective measures (devaluation or domesticdemand restrain) it can perhaps expect an externallyforced adjustment.

1.3.2. Models of the Current Account

1.3.2.1. Exchange Rate and Elasticity Approach [12]It is natural to analyze the current account in the context

of (real) exchange rates, that is in the framework of mone-tary models (variations of the quantity theory of money).For example, it can be shown that in Dornbusch-type mod-els (including covered interest rate parity, money marketclearing immediately and slow adjustment of goods market)expansionary monetary shock results in so-called "over-shooting", and until the price of domestic goods fully offsetthe shock the real exchange rate is effectively overvalued –the current account is in deficit.

In terms of elasticity, it is quite easy to derive the so-called Marshall-Lerner condition saying that devaluationbrings an improvement to the current account only if a sumof the elasticity of a foreign demand for domestic export andthe elasticity of a domestic demand for import is larger thanone.

1.3.2.2. Portfolio ApproachAccording to standard portfolio theory, agents are will-

ing to hold a constant share of each asset and this sharedepends only on agent's risk aversion and asset's perfor-mance (mean return and risk). We can transpose this rea-soning to current account context. The net internationaldemand for country's liabilities is then given by

(1.9)

where D is a stock of country's gross foreign liabilities, FX isa stock of country's gross foreign assets (for example foreignexchange reserves), W* and W denote respectively worldand domestic wealth, α* and α denote world's desired hold-ings of country's assets and country's desired holdings ofworlds assets as a share of respective wealths.

Assuming that the country's wealth is proportional to its(potential) GDP (denoted Y) with proportionality factor θand that the country's wealth is a δ-proportion of totalworld's wealth we can write

(1.10)

where the complex (but constant) expression adjacent to Yis shorten to λ. It is important to notice, that λ can be inter-preted as a net world desired holdings of country's assets asa ratio to GDP or simply debt/GDP ratio.

Taking first differences, dividing by the GDP we obtain

(1.11)

[12] I don't include here the Mundell-Fleming model, which is a common tool to obtain (only) qualitative guidance on how the balance of paymentis going to behave depending on the exchange rate regime and capital mobility.

( ) WWWFXD αα −−=+ **

YYFXD λαδ

δαθ =

−

−=+

1*

1

1

1

1

1

1

−

−

−

−

−

− −=

−+

−

t

tt

t

tt

t

tt

YYY

YFXFX

YDD

λ

17

Currency Crises in Emerging Markets – Selected Comparative ...

CASE Reports No. 41

which, after and moving foreign exchange to the right handside, is equivalent to

(1.12)

where cad is a current account deficit (as a share of GDP),fx is a foreign reserves to GDP ratio, γ is a growth rate ofGDP. This simple equation says that in equilibrium the cur-rent account deficit (corrected for foreign exchangereserves accumulation) is a constant fraction of GDPgrowth. In other words, it means that country, other thingskept constant, can run a deficit to a tune of its growth. Twothings should be made more precise. First, it is reasonableto assume that the economy might want to hold a constantforeign-reserves-to-import ratio (not a constant foreign-reserves-to-GDP ratio). We can write

(1.13)

assuming a constant import growth η. Second, improve-ment takes into account the difference in real exchangerates. Due to world inflation or for example the Balassa-Samuelson effect, the (emerging) country's real exchangerate can get overvalued. Increase in the domestic currency(real) value reduces both debt and foreign reserves, so wehave to make respective changes in the equation, whichnow becomes

(1.14)

where ε is the real exchange rate overvaluation. The equa-tion is ready for estimation and/or calibration and inferencesabout steady state sustainable current account deficit. Themain message of (1.14) is that sustainable current accountdeficit vary across countries and depend on the variablesthat affect portfolio decision as well as economic growth.

1.3.2.3. Intertemporal Choice ApproachThis model is based on a consumption smoothing and

permanent income theory and is a straight adaptation ofindividual choices to the economy as a whole.

Consider a representative consumer that maximizes thediscounted value of (lifetime) utility given by

(1.15)

subject to

(1.16)

where β is the domestic discount factor, u is the utility func-tion [13], B is economy's stock of foreign assets, r is the

fixed world interest rate, Y is GDP, C is consumption, I isinvestment and G is government spending. This infinite opti-mization problem has no closed solution in general, but ifwe assume that the utility function u(C) is quadratic and thatthe world and domestic discount factors are equal (i.e.β(1+r)=1) the solution for consumption path is given by

(1.17)

where Y-I-G i.e. GDP net of investment and governmentexpenditures can be referred to as the net output. Theequation states that along optimal path the consumption isequal to the annuity value of expected future stream of netoutput, or that it is proportional to the permanent incomerather than the income at any instant.

Using (1.16) we obtain the result for the currentaccount (CA=Bt-Bt-1, i.e. positive values indicate a surplus)

(1.18)

This links the current account position to the expecta-tions of future (net) output changes. In other words when acountry's economic prospect is bright, or if the investmentopportunities exceed saving propensity, its residents preferto move the consumption from the future to the presentand finance it externally, being sure of their ability to repayit later – the current account imbalances, consequently,reflect optimal and rational intertemporal decision of eco-nomic agents, they are sustainable and should not be a mat-ter of concern.

The second version of the model can be obtain by max-imizing (1.15) under assumption that the utility function u(C)has constant elasticity of substitution σ, i.e.

(1.19)

and that the worlds interest rate is a random variable. Thecurrent account balance can be presented as

(1.20)

where βw is a world discount factor (from time t to time s)and tilded variables indicate a "permanent" level of a vari-able for example

fxcad ∆−= λ γ

fxfxfxfxdesiredγ

γη

γ

η

+

−=−

+

+=∆

111

)(

( ) fxcadγ

γεηεγλ

+

−+−+=

1

∑∞

=

=0

)(t

tCuU

tttttt GICYBrB −−−++= −1)1(

∑∞

=−+++

− +−−++

=0

1)()1(1 j

tjtjtjtj

tt rBGIYrEr

rC

∑∞

=+++

− −−∆+−=1

)()1(j

jtjtjttj

t GIYErC A

[13] So called felicity or Bernoulli utility funtion to distinguish from overall lifetime utility U.

1

1

1)(

1

−

−

−=

−

σ

σCCu

)~~~~

)~~

(

11)

~()

~(

)~

()~

()~(

1

1

tttt

tt

w

tttt

tttttttt

GICYt

ArGGII

CCYtArtrCA

−−−+

−−−−−

−−−+−=

−

−

βββ

−

+

18

Marek D¹browski (ed.)

CASE Reports No. 41

(1.21)

where

(1.22)

is a market discount factor.The equation (1.20) states, that the current account is

primarily driven by the deviation of key variables (net outputand the world interest rate) from their permanent levels.The last expression on the right hand side represent a "con-sumption-tilting" effect: when the domestic impatience rate(1/β) is larger than the world's one residents want to con-sume their (permanent) income earlier, so they move con-sumption from the future to the present causing currentaccount deficit to rise [14]. But the main conclusion of (1.20)is that a country can run a current account deficit inresponse to exogenous shocks that affect present and/orfuture growth prospects as well as changes in the rest of theworld (reflected in changes of the world's interest rate).Table 1-3 summarizes these implications.

First, net debtor countries in the presence of temporar-ily low worlds interest rate [15] should save some of bene-fits from lower debt payment and move (smooth) the con-sumption into the future. A rise in the rate of savings willimprove current account. The opposite is a case for netcreditor countries. Consequently, if net debtor countriesrise their consumption in response to the temporary drop inthe world interest rate they destabilize their optimal con-sumption paths. Investment is unaffected – only permanentchanges in output growth can increase it to assure optimalcapital/output ratio. Second, the response to shock improv-ing growth prospects depends crucially on the expectations

whether the improvement is transitory or permanent. Thetransitory surge in country-specific productivity (growth)induces savings as agents save part of temporarily highincome for the future. Investment remains unchanged, sothe current account improves. The permanent rise in coun-try-specific growth prospects rises permanent income andinduces higher investment. Consumption also increases, sothe country moves into a current account deficit. The tran-sitory rise in global productivity increases (total) world sav-ings and put a downward pressure on the world interestrate, which decreases temporarily below average, withabove-explained consequences. The permanent rise in glob-al productivity rises the permanent income and gives incen-tives to consume more in present, but at the same time, thepermanent world interest rate goes up. Because the worldis a closed economy the current account can't change simul-taneously in all countries – the world interest rate rise is suf-ficient to squeeze (back) consumption in debtor countriesand induce saving necessary to pay increased debt service inthe future – and do the opposite in creditor countries.

Intertemporal models were further refined by incorpo-rating other relevant variables in order to study policy impli-cations of various shocks. For example Obstfeld and Rogoff(1996) build a model in which demographic factors (fluctua-tions in the labor force) play role. Their model (after somesimplifications) yields

(1.23)

where L is a labor force. The implications of the modelhave been used to explain the current account deficit afterIsrael has, during 1989–1997, incurred a demographicshock – a large inflow of (former Soviet Union) immi-grants amounting to 800.000 people or almost 20% of thepopulation.

Overlapping generations models have been analyzed incontext of the current account deficit to correct for life-cycle considerations, establish its link with labor force com-position, etc.

∑

∑∞

=

∞

==

tsst

tssst

t

R

YRY

,

,~

∏+=

+

= s

tuu

st

rR

1

,

)1(

1

Table 1-3. Current account reaction to various shocks as predicted by the intertemporal approach

Temporary PermanentShock

Saving Investment Curr. acc. Saving Investment Curr. acc.debtor countries + 0 +World interest

rate belowmean creditor counties - 0 -

not applicable

country's + 0 + - + -debtor + 0 + + + 0

Rise inproductivity global

creditor - 0 - - - 0Note: + at current account position means improvement.Source: Reisen (1998), extended by the author.

[14] There is evidence that this is a case with emerging economies.[15] Permanent drop below the average is, of course, nonsense.

)~

()~~( ttttt GGLwwLCA −−−=

19

Currency Crises in Emerging Markets – Selected Comparative ...

CASE Reports No. 41