Carol Tomé - The Home Depotir.homedepot.com/~/media/Files/H/HomeDepot-IR/reports-and... · Diane...

19

Diane Dayhoff Vice President, Investor Relations Carol Tomé Executive Vice President, Corporate Services & Chief Financial Officer Europe June 2017

Transcript of Carol Tomé - The Home Depotir.homedepot.com/~/media/Files/H/HomeDepot-IR/reports-and... · Diane...

Diane DayhoffVice President, Investor Relations

Carol ToméExecutive Vice President, Corporate Services & Chief Financial Officer

EuropeJune 2017

Forward Looking Statements and Non-GAAP Financial Measurements

2

Certain statements contained in today’s presentations constitute "forward-looking statements" as defined in the Private Securities Litigation Reform Act of 1995. Forward-looking statements may relate to, among other things, the demand for our products and services; net sales growth; comparable store sales; effects of competition; state of the economy; state of the residential construction, housing and home improvement markets; state of the credit markets, including mortgages, home equity loans and consumer credit; demand for credit offerings; inventory and in-stock positions; implementation of store, interconnected retail, supply chain and technology initiatives; management of relationships with our suppliers and vendors; the impact and expected outcome of investigations, inquiries, claims and litigation, including those related to the 2014 data breach; issues related to the payment methods we accept; continuation of share repurchase programs; net earnings performance; earnings per share; dividend targets; capitalallocation and expenditures; liquidity; return on invested capital; expense leverage; stock-based compensation expense; commodity price inflation and deflation; the ability to issue debt on terms and at rates acceptable to us; the effect of accounting charges; the effect of adopting certain accounting standards; store openings and closures; guidance for fiscal 2017 and beyond; financial outlook; and the integration of Interline Brands, Inc. into our organization and the ability to recognize the anticipated synergies and benefits of the acquisition. These forward-looking statements are based on currently available information and current assumptions, expectations and projections about future events, and actual results could differ materially from our expectations and projections. You should not rely on our forward-looking statements as they speak only as of the date hereof, and we undertake no obligation to update these statements to reflect subsequent events or circumstances except as may be required by law. Additionalinformation regarding risks and uncertainties is described in Item 1A, "Risk Factors," and elsewhere in our Annual Report on Form 10-K for our fiscal year ended January 29, 2017 and our subsequent Quarterly Reports on Form 10-Q.

Today’s presentations are also supplemented with certain non-GAAP financial measures. We believe these non-GAAP financial measures better enable management and investors to understand and analyze our performance by providing them with meaningful information relevant to events of unusual nature or frequency that impact the comparability of underlying business results from period to period. However, this supplemental information should not be considered in isolation or as a substitute for the related GAAP measures. Reconciliations of the supplemental information to the comparable GAAP measures can be found on our Investor Relations website at ir.homedepot.com.

Discussion Overview

Financial Results & Targets

Our View of the U.S. Home Improvement Market

Strategic Framework

3

First Quarter Fiscal 2017 Results

4

16% Earnings Per Share Growth in Q1 2017

($ Millions USD, except per share data)

Q1 2017 Q1 2016 V%Sales $23,887 $22,762 4.9%Comp Sales 5.5% 6.5%

Gross Profit $8,154 $7,791 4.7%Gross Profit Margin 34.14% 34.23% -9 bps

Total Operating Expenses $4,805 $4,714 1.9%

Operating Profit $3,349 $3,077 8.8%Operating Profit Margin 14.02% 13.52% 50 bps

Net Earnings $2,014 $1,803 11.7%

Diluted Earnings Per Share $1.67 $1.44 16.0%

Fiscal 2017 Outlook

5

New store openings ~6

Sales growth ~4.6%

Comp store sales growth ~4.6%

Diluted EPS growth ~11.0% to $7.15

Capital expenditures ~$2 billion

(1)

(As of May 16, 2017)

(1) All guidance based on GAAP

(2) EPS growth guidance includes ~$5 billion of share repurchases using excess cash in FY 2017

(2)

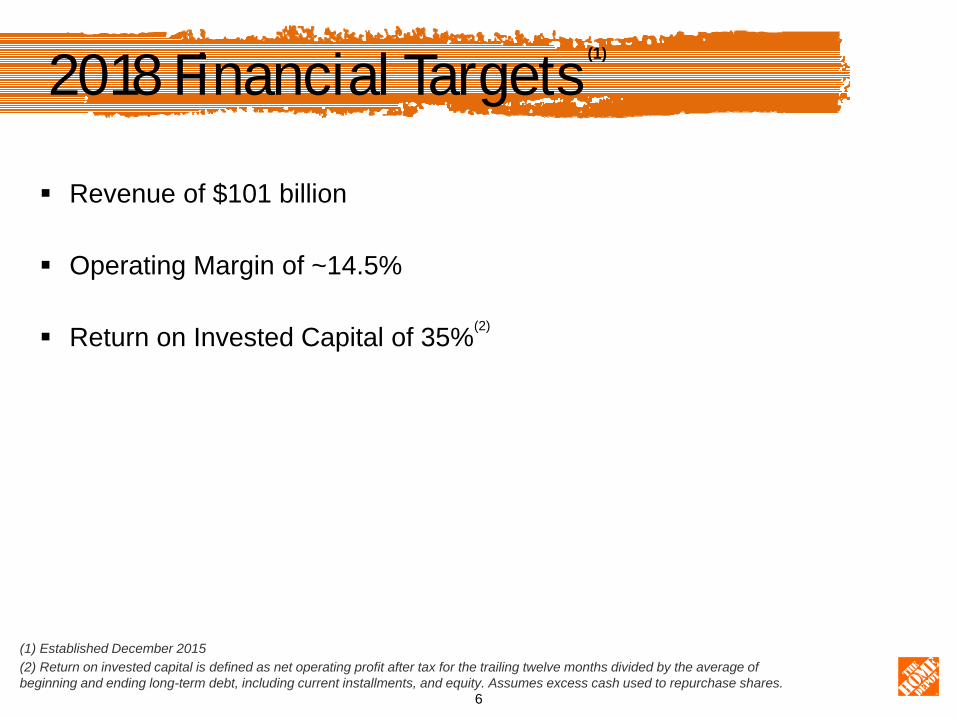

2018 Financial Targets

Sales

6

Revenue of $101 billion

Operating Margin of ~14.5%

Return on Invested Capital of 35%

(1) Established December 2015(2) Return on invested capital is defined as net operating profit after tax for the trailing twelve months divided by the average of beginning and ending long-term debt, including current installments, and equity. Assumes excess cash used to repurchase shares.

(1)

(2)

Solid Liquidity and Conservative Financial Risk Profile

7

We continue to generate strong cash flow Debt Maturity Profile ($B)

FYE 2015 Net DebtIssuance

Dividends FYE 2016CashFlow from the

Business

CapEx

ShareRe-

purchases

0.5

1.21.0

1.8

2.4

1.3

1.01.11.1

2.3

3.0

0.5

1.0 1.01.01.0

1.6

0.81.0

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

2038

2039

2040

2041

2042

2043

2044

2045

2046

2047

2048

2049

2050

2051

2052

2053

2054

2055

2056

Fixed Floating

Weighted Average Maturity: 14.3 yearsWeighted Average Coupon: 3.66%

$2.2

$9.8

$2.5 $1.6

$3.4

$7.0

$2.5

$0.95 $1.04 $1.16

$1.56

$1.88

$2.36

$2.76

$3.56

2010 2011 2012 2013 2014 2015 2016 2017F

Committed to Dividend Payout

Annualized Dividend Paid

Increased Targeted Dividend Payout Ratio from 50% to 55% in February 2017

8

Shareholder Return Principals

9

Return on Invested Capital Principle Maintain high return on invested capital, benchmarking all uses of excess

liquidity against value created for shareholders through repurchases

Adjusted debt/EBITDAR ratio not to exceed 2x

Dividend Principle Targeting payout at approximately 55% of earnings. Intend to increase

dividend every year

Share Repurchase Principle After meeting the needs of the business, use excess liquidity to

repurchase shares, as long as value creating

Discussion Overview

Financial Results & Targets

Our View of the U.S. Home Improvement Market

Strategic Framework

10

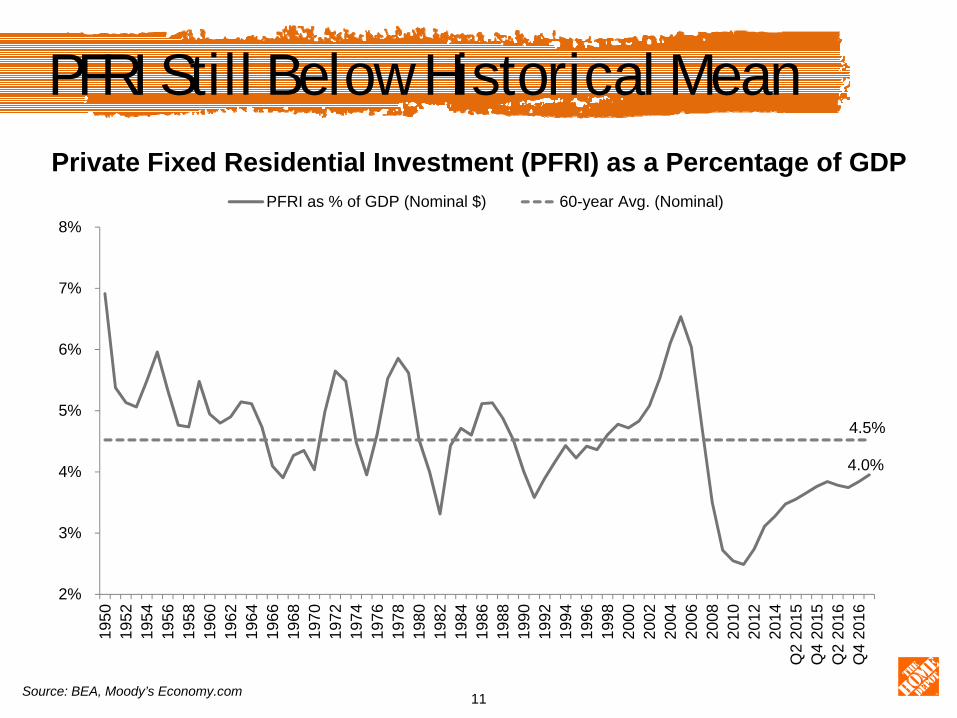

PFRI Still Below Historical Mean

11

Private Fixed Residential Investment (PFRI) as a Percentage of GDP

Source: BEA, Moody’s Economy.com

4.0%

4.5%

2%

3%

4%

5%

6%

7%

8%

1950

1952

1954

1956

1958

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

Q2

2015

Q4

2015

Q2

2016

Q4

2016

PFRI as % of GDP (Nominal $) 60-year Avg. (Nominal)

Home Price Recovery

12Source: S&P Case-Shiller, Moody’s Economy.com (Hist.)

Home Price Index by City

(65%)

(55%)

(45%)

(35%)

(25%)

(15%)

(5%)

5%

15%

25%

35%

Q2

2006

Q3

2006

Q4

2006

Q1

2007

Q2

2007

Q3

2007

Q4

2007

Q1

2008

Q2

2008

Q3

2008

Q4

2008

Q1

2009

Q2

2009

Q3

2009

Q4

2009

Q1

2010

Q2

2010

Q3

2010

Q4

2010

Q1

2011

Q2

2011

Q3

2011

Q4

2011

Q1

2012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

Q3

2013

Q4

2013

Q1

2014

Q2

2014

Q3

2014

Q4

2014

Q1

2015

Q2

2015

Q3

2015

Q4

2015

Q1

2016

Q2

2016

Q3

2016

Q4

2016

Mar

-17

National Index 20-City Composite 10-City Composite Atlanta, GABoston, MA Charlotte, NC Chicago, IL Cleveland, OHDallas, TX Denver, CO Detroit, MI Las Vegas, NVLos Angeles, CA Miami, FL Minneapolis, MN New York, NYPhoenix, AZ Portland, OR San Diego, CA San Francisco, CASeattle, WA Tampa, FL Washington, DC

MarketIndexed to Q2 2006

(Mar 2017)Dallas, TX 42.3%Denver, CO 41.7%Seattle, WA 25.5%Portland, OR 23.2%Charlotte, NC 17.8%Boston, MA 13.1%San Francisco, CA 9.8%Atlanta, GA 3.2%National Index 2.7%20-City Composite (3.8%)Los Angeles, CA (4.7%)San Diego, CA (5.0%)Cleveland, OH (5.7%)10-City Composite (6.2%)Minneapolis, MN (7.2%)Detroit, MI (9.5%)Washington, DC (11.8%)New York, NY (12.3%)Chicago, IL (16.0%)Tampa, FL (19.5%)Miami, FL (20.3%)Phoenix, AZ (26.4%)Las Vegas, NV (32.7%)

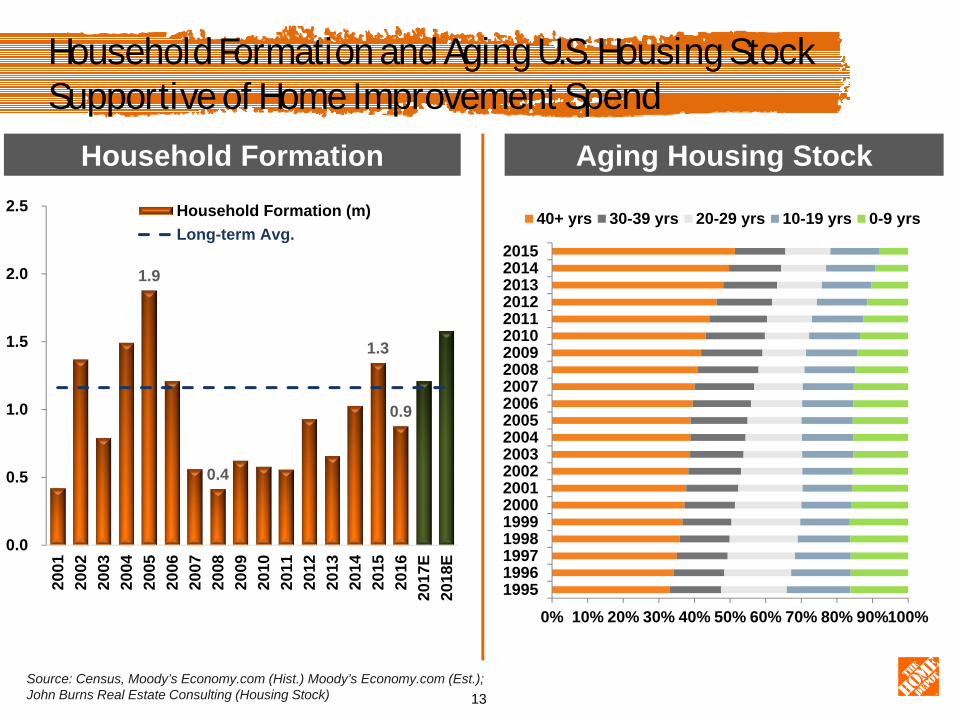

Household Formation and Aging U.S. Housing Stock Supportive of Home Improvement Spend

Household Formation Aging Housing Stock

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%100%199519961997199819992000200120022003200420052006200720082009201020112012201320142015

40+ yrs 30-39 yrs 20-29 yrs 10-19 yrs 0-9 yrs

1.9

0.4

1.3

0.9

0.0

0.5

1.0

1.5

2.0

2.5

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

E20

18E

Household Formation (m)Long-term Avg.

Source: Census, Moody’s Economy.com (Hist.) Moody’s Economy.com (Est.); John Burns Real Estate Consulting (Housing Stock) 13

Discussion Overview

Financial Results & Targets

Our View of the U.S. Home Improvement Market

Objectives & Strategy

14

Our Objectives

Deliver Shareholder Value

Grow Market Share – Pro and Consumer

15

The Power of The Home Depot

Customer Experience Connect Associates to

Customer Needs Interconnected

Experience: Store to Online, Online to Store

Capital Allocation Driven By Productivity And Efficiency Innovate Our Business

Model and Value Chain

Product Authority Connect Products and Services

to Customer Needs Connect Product to Shelf, Site

and Customer

16

Opportunities for Growth

17Sources: 2014 HIRI Reference Guide; 2015 Harvard University “Emerging Trends in the Remodeling Market”; NAICS; and external market analysis

Growth: Professional Customer

18

Growth: Interconnected Retail

19