cargovision-0206

17

cargo vision QUARTERLY MAGAZINE AIR FRANCE-KLM CARGO VOLUME 21 ˆ NUMBER 25 ˆ JUNE 2006 Preparing for Change People Make a Difference Under One Roof PANDORA’S BOX

Transcript of cargovision-0206

cargovisionQUARTERLY MAGAZINE AIR FRANCE-KLM CARGO VOLUME 21 ˆ NUMBER 25 ˆ JUNE 2006

Preparing for ChangePeople Make a DifferenceUnder One Roof

PANDORA’S BOX

We are in the midst of a global contest, with people everywhere making products that theyhope we will buy. You see this in the supermarket: which country grew the fruit you are aboutto purchase? In your home: was your TV set built by Hungarians or Koreans? And on the street: just look at the international content in the auto you drive.

Interestingly, the competition for your money began long before these products appeared inour local stores. Someone believed you might buy his product because you liked the look ofthe box. But which box? Yes, that’s a good box, but will it still look good when it gets to thestore? And how many of them will fit on an aircraft pallet? Uh-oh, we need to stack themhigh to keep the landed cost acceptable. What’s that? You can’t stack them any higher orthey’ll crush?

With these dilemmas in mind, we decided to devote this issue to packaging. It has broad yetsubtle cost implications for all participants in the supply chain. And because regulators playa large part in deciding how you package your pharmaceuticals or fresh produce, we decid-ed to discuss that topic as well.

An even more familiar issue is the competition for cheap manufacturing labor and supplies.The epicenter of this struggle keeps shifting to new regions. China has led the manufacturingrace for some time. In this issue, we learn why some manufacturers are finding love inEastern Europe.

The role of AF-KL Cargo in these multilayered struggles is to provide effective transportationfor various participants. Although our forwarding partners usually plan their customers’ logis-tics, we can now offer them a wider range of options via our aligned networks, operatingthrough Charles de Gaulle and Schiphol. Our progress in collocating customer service func-tions under one roof is a topic that we believe will offer you a first taste of what lies ahead forthe customers of AF-KL Cargo.

JEAN CHARLES FOUCAULTSenior Vice President Sales & DistributionAir France Cargo-KLM Cargo

4 PANDORA’S BOXPackaging sells products once they are on the shelf. But it also facilitates freight handling, reduces damage and pilferage, and ultimately controls unit costs. Several industries are developing packaging that does it all.

14 PREPARING FOR CHANGEBangkok’s new airport, Suvarnabhumi, is due to replace Don Muang airport later this year.Cargovision spoke with Kovit Thanyarattakul, chairman of Multi Air Services in Bangkok, about the prospects for Thai airfreight and Bangkok’s new airport.

19 U-TURNSearching for leaner logistics and lower landed costs, auto builders found China. Now they likeEastern Europe. Cargovision explores this change and its effect on the air cargo business.

20 PEOPLE MAKE A DIFFERENCEPhilippe Gallon manages AF-KL Cargo in Abidjan. He understands the subtle nature of Africa’sbusiness climate. It irritates him when people explain a service failure with the comment, “Well, this is Africa.”

24 UNDER ONE ROOFWhat exactly does integrating local customer service teams involve? Cargovision spoke with Jan Krems who is overseeing the integration of customer service offices throughout AF-KL Cargo’s network.

08 news & datelines22 Carsten Pellicaan26 country file28 market monitor30 postscript31 information and colophon

COVER IMAGE Pears being harvested

© Peter Titmuss/Alamy

2 cargovision | JUNE 06 cargovision | JUNE 06 3

Suvarnabhumi

Developing packaging, page 4

Jan Krems

SHELF LIFE

cargovision editorial cargovision contents

© R

icha

rd L

evin

e/A

lam

y

© Jochen Tack/Alamy

■ Packaging serves multiple purposes, but theprimary goal is to sell what’s inside the box.However, few companies consider how effectivepackaging can reduce airfreight handling andcosts. After all, optimal packaging protects thecontents and can affect the profitability of a com-pany’s entire supply chain. “Depending on howfar a company wants to go with quality packag-ing, it can generate more reliable logistics sys-tems and greater profit,” says Rogier van Beu-gen, commercial director of Fresh Logistics atAF-KL Cargo. Many products are affected by theway packaging helps or hinders airfreight han-dling and costs: fresh produce, high tech goodsand pharmaceuticals, for example. Each has itsown circumstances and requirements based onits supply chain model.

FRESH FLIGHTS

In the food industry, the UK firm Blue Skies ofPitsford, Northamptonshire, finds that by slicing,dicing and packaging foods at the source, theycan prepare and ship certain perishables by airand deliver them into the hands of wholesale andretail customers in Europe within 36 hours of har-vest. Workers in Ghana, South Africa, and Egyptfirst process food items and then seal and packthem in custom-made plastic tubs stored in chillrooms. Next, they pack the tubs into cardboardboxes and load them into aircraft containers fortheir journey in the plane’s temperature-con-

cargovision | JUNE 06 5

Packaging sells products once they are on the shelf. But it serves other purposesbefore that: it facilitates freight handling, reduces damage and pilferage, and ultimate-ly controls unit costs. Several industries that rely on airfreight are developing packag-ing that does it all.

BY KAREN E. THUERMER

© J

. M

arsh

all-

Trib

aley

e Im

ages

/Ala

my

© R

icha

rd L

evin

e/A

lam

y

PANDORA’S

BOX

trolled cargo hold. “The fruit needs to be shippedin a controlled environment,” says GeorgeHutton, operations manager at Blue Skies. “Weused the Envirotainer units before, but foundthem too expensive and difficult to handle.” Costis a critical component of Blue Skies’ businessmodel, and every expense is scrutinized. “Ourpockets are only so deep,” Mr. Hutton says.“And airfreight is expensive.” When fresh produce travels in individual pack-ages, it takes up more room in an aircraft than itdoes when flown loose in large boxes. “But if youship an entire pineapple, 70% is thrown away lat-er as waste,” Mr. Hutton explains. “Instead, wethrow away that 70% in Ghana and ship just thebits and pieces.” The labor cost to process perishables is muchcheaper in Africa than in Europe, and the ready-to-eat product commands a higher price. Bothpackaging and airfreight are major cost items forall shippers of time-sensitive perishables. Freshfish, in particular, requires delicate handling.Frozen salmon, shellfish, sushi-grade tuna andother expensive seafood commonly travels inEnvirotainers, but the less expensive varieties arepacked in Styrofoam boxes with wet ice andstacked onto pallets. “The Styrofoam boxes have a lifespan of about 2or 3 days,” Mr. van Beugen says. “Norway, thesource of many salmon shipments, generally uti-lizes the best boxes. The business from Africainvolves less expensive fish. It is not as well

6 cargovision | JUNE 06

organized and the box types vary. This candiminish the quality of the product.”

FIT TO FLY

Fierce competition in the consumer electronicsbusiness makes speed to market a paramountconcern. Manufacturers face constant pressureto meet the replenishment demands of theirretailers. “Today it’s hot, tomorrow it’s not,” saysHans van Wijngaarden, business manager forPhilips Applied Technologies, the supply chainarm of Royal Philips Electronics in Eindhoven. “Ifmovement within the supply chain takes morethan three months, price erosion can be morethan 30%, particularly for new digital productssuch as LCDs.” Consequently, electronics manu-facturers carefully consider how to ship theirproducts. Given the industry’s tight margins, costis important. Packaging density can have a majoreffect on cost. “We can identify the reasons whyhigh-end customers need to prevent damages,”says Wim Lagendijk, quality manager at AF-KLCargo. They use consumer packaging increas-ingly as a controlled way of achieving the short-est time to market. They plan deliveries to limitstocks and reduce both costs and out-of-datearticles. Some firms produce on a just-in-timeschedule so they can replenish their stock levelsfrequently. Others ship single orders that werebought on the Internet or were sent as test sam-ples. “It is clear that any damage, partial loss, orpilferage will immediately affect their revenue,”says Mr. Lagendijk.

PAPER THIN

End-user packaging is the trend occupying theattention of most electronics makers today. “Thismeans the boxes are thinner and not as robustas they once were,” says Johan Schreuders, AF-KL team member. “Many boxes are made offiberboard. On top of that, shipments are movingvery fast. This means consolidators must loadpallets quickly. Cargo handlers may not alwaysgive full attention to how they stack products ontop of one another. Heavy industrial shipmentsand personal goods are often loaded on palletsalong with electronics in order to optimize aircraftloads and volume.” Stacking shipments on pallets is an art in itself,with the smallest and lightest packages generallygoing on top. However, the quality of the boxesis not always calculated to withstand the forces

at play in this environment. “We need a betterexchange of information at the onset of packagedesign,” Mr. Lagendijk says. “If the packaging isfit for flying, it will reduce costs.” AF-KL Cargodeem this point so critical that it has implement-ed a Fit-for-Flying initiative that applies to manycommodities that move by air. “Packaging is veryimportant and must be secured in such a way toprotect merchandise from both damage andtheft,” Mr. Lagendijk adds. “It doesn’t pay to bepenny wise and pound foolish.”

THE WHOLE TRUTH

Philips Applied Technologies and AF-KL Cargorecently organized a workshop for high-techcustomers in Europe, so that shippers and trans-portation providers could discuss aspects ofpackaging that relate to airfreight and to theirown costs. Participants discussed and exploredthe limitations of the air cargo industry and waysto create packaging for the entire supply chain. The packaging of pharmaceuticals is subject tothe same issues as electronics. The differencebeing that lives depend on pharmaceuticals.Product integrity is the primary consideration.Packaging these products is clearly not a one-size-fits-all business. To being with, pharmaceuticals range broadlyfrom vaccines to medicines. International rulesgovern the temperatures for shipping each ofthem. When a company designs packages forthese goods, it must integrate the regulations in

order to maintain the integrity of the contents intransit. “A growing number of companies areworking on packaging to achieve this,” saysSerge Alezier, AF-KL Cargo’s international salesmanager of pharmaceutical logistics forSouthern Europe. However, pharmaceuticalpackaging again serves a dual purposes: to pro-tect and sell the product, and to ensure that itmeets government regulations and industrystandards while in transit. The decisive factor in striking a balance betweenthese purposes is the type of pharmaceuticalproduct, says Stephane Lemaire, director forpharma industry at AF-KL Cargo. “The packag-ing is always linked to what’s inside.” Eventhough companies in this industry have numer-ous packaging options available, many of themuse expanded polyurethane Styrofoam, bothstandard and customized, in conjunction with gelpacks. The more expensive alternative is vacu-um-inflated insulated panels. “There is a lot of research being done on newpackaging materials,” says Ira Smith, senior vicepresident for Pharmaceutical & Healthcare atKuehne+Nagel. For many companies, the goal isto ship products cheaper, better, and faster byclosing the gap in the distribution channel andsaving on packaging costs. “Many firms want toturn a 72-hour package into a 48-hour package.While a lot of packaging has been developed,there has been no magic bullet so far.” One challenge with pharmaceuticals is to ensureintegrity throughout transit. However, as withelectronics, the cost of transportation frequently

overshadows the importance of good packag-ing. “The first thing pharmaceutical companiesdo is use a cheaper box or drum that is lessvoluminous and often too flimsy,” says Arthur vanOlst, senior product manager of PharmaceuticalLogistics for AF-KL Cargo. “In that case, they arebound to have problems.” Both pharmaceuticaland healthcare companies also ship packages incommercial boxes designed to be opened easilyby patients, Mr. Van Olst adds. “If these boxesare accepted for transport and something is thenstacked on top of them, they will collapse.”

ALL WRAPPED UP

High-value products, such as pharmaceuticalsand electronics, often face another problem: highpilferage rates. “Much of the pilferage is simplydue to the poor quality of packaging,” Mr. vanOlst says. As these issues become more widelyknown, companies have begun to collaboratemore with carriers and freight forwarders in orderto develop packaging that suits their transporta-tion needs and meets the requirements of theauthorities and of their trade associations. “The challenge for the logistic partners is toensure that the shipper, the pharmaceuticalcompany, asks for procedures developed withintheir partnership,” says Mr. Smith ofKuehne+Nagel. As a solution for many packaging issues, AF-KLCargo developed the AirModule, a container thatincreases protection of the contents and facili-tates its journey through the supply chain.AirModule is designed to use less packing mate-rial yet offer greater protection against damageand theft. It can be moved easily from door todoor, with lower handling costs and shorter tran-sit times. It does not require the use of woodenpallets or skids. Still, while the AirModule offers apartial solution, it does not change the need formanufacturers to plan their packaging in coordi-nation with their transportation vendors, so thattheir products withstand the rigors of the jour-neys to their individual markets.

cargovision | JUNE 06 7

cargovision pandora’s box

© H

olt

Stu

dio

s/A

lam

y

© H

olla

ndse

Hoo

gte

© E

nigm

a/A

lam

y

4.000 t 20%

15%

10%

5%

0%

-5%

3.500 t

3.000 t

2.500 t

2.000 t

1.500 t

1.000 t

500 t

0 t

2.120t2.233t

3.408t

2.016t1.836t 1.834t

1.629t1.601t

1.443t 1.443t1.301t 1.281t

1.172t1.071t

10%

-3.4%

1%

8%8%

3%

0%-0.6%

18%

-1.5%

-2.0%12%

7%

HONG

KONG

TOKYO

SEOUI

ANCHORAG

E

FRANKFU

RT

SINGAPO

RE

TAIP

EI

SHANGHAI

AMSTE

RDAM

MIA

MI

LONDO

N

DUBAI

NEW Y

ORK

BANGKO

K

2%

AIRPORTS General

LONDONDepending on your satisfaction with handling services at any of theseven British airports owned by BAA, you would be pleased or anx-ious about the ongoing takeover efforts of Ferrovial. The UK is theFerrovial’s second-largest market. About half of its EUR7 billionturnover comes from it’s construction business. However, infrastruc-ture development is its most profitable segment and accounts forover half of its EUR17 billion in assets. BAA owns and operates sevenBritish airports, including Heathrow, Gatwick and Stansted (servingLondon), Southampton, and three Scottish airports at Glasgow,Edinburgh, and Aberdeen.

CARRIERS Asia

TOKYOAmid poor financial results and concerns that maintenance incidentshave compromised safety, JAL SVP Haruka Nishimatsu replacesCEO Toshiyuki Shinmachi in June. Mr. Shinmachi served 10 years inthe carrier’s airfreight division, most recently as a VP, before he waspromoted in 1997 to JAL’s board of directors as an SVP and in 2004as President. Mr. Nishimatsu is JAL’s SVP of finance and purchasingand has worked in finance since 1991. Top-level management changes don’t often affect a carrier’s airfreightbusiness, but in JAL’s case they could. Since April 2004, JapanAirlines International Co. and Japan Airlines Domestic Co. have beenunder the wings of the holding company, JAL. Mr. Nishimatsu over-saw the assimilation of the two airlines and is regarded by both com-panies as a neutral participant. His task is to return JAL to profitabilityby overcoming cultural differences that remain within the two carriers;reducing JAL’s interest-bearing liabilities, which are nearly the sameas its gross sales of ¥2 trillion (EUR14 billion) and withdrawing fromunprofitable international routes. On the last point, Mr. Nishimatsusays that JAL remains firmly determined to make money from itsinternational flights.

BERLIN In mid-March, good business reconciled withgood life after a federal administrative court inLeipzig approved a EUR2.5 billion project toremake Berlin’s Schoenenfeld Airport into Berlin-Brandenburg International. About 4,000 local resi-dents kept this development on hold with protestsand lawsuits over its potentially adverse impact ontheir environment. In consideration, the court’s rul-ing restricts landings after 10 pm and noise pollu-tion. It will also require developers to compensateaffected residents. However, the landing restric-tions won’t help airlines attract business travelersand cargo that often leave Asia at convenienttimes in the afternoon and arrive in Europe in lateevening. Berlin’s Tegel Airport will close onceBrandenburg International opens in late 2011.Tempelhof is expected to close in 2007.

ATHENSAthens International Airport and the Piraeus PortAuthority agreed in March to establish a sea-aircargo link. The authorities will accelerate offloadprocedures at the seaport and move freight tothe airport using a direct truck-shuttle service.They are promoting favorable cost and handlingterms. Connections were to begin in April, withrail links to be added in the future.

AIRPORT TRAFFIC 2005

WORLDShanghai and Dubai topped the growth chartslast year for cities handling over 1 million tonnesof freight. Tokyo and New York sank to the bot-tom. Still, Shanghai’s tonnage was less than ahalf and Dubai’s less than a third of that handledby the largest airport, Hong Kong.

KUALA LUMPURMASKargo got a new B747-400 freighter in Marchand plans to use its range and capacity to servetriangular routes, such as Kuala Lumpur-Dubai-Amsterdam. According to Datuk J J Ong,Malaysia Airlines senior general manager of cargo,the 747-400 freighters could eventually replaceMASKargo’s fleet of six leased B747-200freighters. MAS management expects Mr. Ong touse the new plane to more than tripleMASKcargo’s operating profit in 2006 to RM107million (EUR24 million), up from RM31 million(EUR7 million) in 2005. Results like that should seemany new freighters arriving in Malaysia.

HONG KONGCathay Pacific Airlines wants more of China thanBeijing and Xiamen. It wants Dragonair, or at leastDragonair’s access to the mainland China marketsCathay relinquished, after it bought control of theupstart carrier in 1991. For the moment, Air Chinaholds 29% of Dragonair and controls a further43% of its shares through a Hong Kong sub-sidiary. It would like fifth-freedom rights beyondHong Kong. To sort out routes and shares,Cathay, Air China, and Dragonair began talks inApril. At press time, the prognosticators thoughtthat Cathay would increase its 18% share inDragonair to improve its access to mainlandChina, while Air China would buy into Cathay and

8 cargovision | JUNE 06 cargovision | JUNE 06 9

cargovision news around the worldcargovision news around the world

Our quarterly review ofindustry news keeps youabreast of developmentsin key sectors around the world.

Kuala Lumpur, the new B747-400 freighter

2005 International Feight & Growth

© S

tefa

n Lo

upat

ty

10 cargovision | JUNE 06 cargovision | JUNE 06 11

Technolgy RFID

AMSTERDAMFunny stuff that radio frequency interference. First,researchers at the Amsterdam’s Free Universitycreated a radio frequency identity (RFID) chipinfected with a virus to prove that RFID systemsare vulnerable despite their low memory capacity.Their announcement came at a conference inPisa, in the form of a technical paper entitled, “Isyour Cat Infected with a Computer Virus?”Concern spread quickly that such a virus couldmigrate to the industrial databases connected toRFID scanners and from there to other tags, cor-rupting entire systems. Fortunately, no technologyin recent memory has had the monetary supportof so many government agencies and technolo-gists as RFID. The very next day, Dan Mullen,president of the AIM Global trade group leapt tothe rescue. “Those researchers built a system withweaknesses and then showed how they could beexploited,” Mr. Mullen said. “Poor system design,whether capturing RFID tag, bar code or keyboarddata will create vulnerabilities.” Well, now you canrest easy knowing that your cat is safe.

SEATTLEMeanwhile, Boeing says it will revolutionize theworkings of the logistics sector for the aerospaceparts business. The plane maker hired IntelleflexCorp. to supply RFID tags for parts of the forth-coming B787 in order to reduce its maintenanceand inventory costs.

WILMINGTONAfter nine years of testing RFID, DHL began aseries of pilot projects in March to see how thetags could improve its efficiency and tracking. One test, in partnership with IBM, will monitor the movement of consumer electronics repairsthrough DHL’s Express network. All other tests will take place in the US and, if successful, couldlead to wider implementation next year.

ALONG THE A-1Autos are prime candidates for RFID installations,everything from immobilizers to tire pressure moni-tors. Using RFID to aid the processes of manufac-turing and distributing autos is Asia, according toan ABI Research report out in March. Europe fol-lows, with cash-poor automakers in NorthAmerica picking up the rear.

ONLINE General

BEIJINGAir China gave Unisys a five-year contract to hosta system to manage its air cargo. It is expected togo online in March 2007. The Chinese carrier nowflies about 700,000 tonnes annually to about 20countries. Things could work out well for Unisys,because Air China Cargo and China Cargo Airlinesformulated a merger plan in April, according toSingapore’s Singtao Daily. The two carriers willhold equal shares of a new company along withCITIC Pacific (please see Carriers: HONG KONG),which vowed to divest itself of the air cargo busi-ness.

HONG KONGIf you know someone who is still filing paper mani-fests for their ocean and river entries into HongKong, please remind them that they must file elec-tronically over the Internet as of June 16.

ALGIERSAir Algerie hired CHAMP Cargosystems to auto-mate its cargo operations on a five-year contract.The carrier mostly operates B737s, but also flies five A330s internationally, and two LockheedC-130s wherever they are needed. It plans toexpand cargo operations.

INDUSTRY Europe

BRUSSELSIn February, the European Commission proposed that supply chainoperators who adhere to minimum European security standardscould be designated as secure operators, a status that would givethem fast-track treatment at security checks at both internal andexternal EU borders and distinguish them from less secure competi-tors. About half a million companies now operate transport and ancil-lary services in the European supply-chain sector. The scheme couldbenefit operators who want to invest in security, but hesitate for fearof wasting valuable assets.

PARISAéroports de Paris SA filed for an initial public offering in April and israising fees to fund EUR1 billion in infrastructure improvements.Airlines are not happy with CDG’s 5% annual increases of the pastfive years, or of the next five years. They want the European Union toregulate airport charges. EU transport commissioner Jacques Barrotsuggested in early April that airports might increase landing fees forairlines at peak hours and lower them at less congested times. Hehad not addressed the issue of Paris as of press time.

TRIVANDRUMAirlines from the Far North buy software from the Far South. Cargojetof Toronto and Northern Air Cargo of Anchorage both signed up forIBS Software’s reservations and ground handling software calledSmartCargo. Cargojet operates B727 Advance freighters and trucksbetween 13 Canadian cities. Northern Air Cargo flies DC-6s, B727freighters and ATR-42s to just about anywhere in Alaska, and toSeattle and Siberia.

HOUSTONIn March, EGL Eagle Global Logistics began using Inforwarding’s AirFreight Rates Application in Europe, the Middle East, and Africa. Theprogram displays cargo rates online and enables agents to searchand compare them.

HOOFDDORPTNT Freight Management joined Cargo 2000 in January.

REDWOOD SHORESOracle added G-Log to its list of acquisitions in transport manage-ment software that already includes Siebel, J.D. Edwards, andPeopleSoft. Oracle has enterprise resource planning software andplans to transportation management software to third-party logisticsproviders. Using G-Log’s Global Command Center product, Oraclewill try to provide another choice for providers who want to reducecycle times and lower total costs.

cargovision news around the world cargovision news around the world

© J

ohn

T. F

owle

r/A

lam

y© A

NP

Fot

o

Cargojet of Toronto

possibly achieve greater international access. If this is too easy to fol-low, let us add that Citic Pacific Ltd, a Chinese conglomerate with29% of Dragonair and 25% of Cathay and a pivotal player in this bar-gain, says it wants to sell its non-core holdings (everything exceptproperty, steel, and power) yet retain a significant share of Cathay.

WELLINGTONA grey drizzle welcomed the Rolling Stones to Wellington Airport fortheir April 18 concert at Westpac Stadium. The city fathers hadgranted permission for the stadium to host a certain number of con-certs each year that could exceed standard noise limits. However,they did not look as favorably upon a proposed Air New Zealand-Qantas codesharing arrangement for air services across the TasmanSea. The Wellington Chamber of Commerce fears that such a pactwill slash flights to Sydney and Melbourne. Nearly 20% of New Zealand’s live lobster exports fly from Wellington,as well as other seafood, flowers, and high-value goods. Wellingtonis located on the southern tip of New Zealand’s North Island and isthat nation’s second largest economic region. So, Mick, enjoy yourlobster in Wellington. ‘Cause you won’t get no satisfaction when youhit Sydney.

72%

80%

60%

40%

20%

0%

-20%

-40%

39%

27% 25% 23%19% 17% 15%

11% 6% 4%

-7%

-23%

8%8%8%

5%

14%

20%

17%

3% 3%

3%

11%

2%13%

Fedex

80%

60%

40%

20%

0%

-20%

-40%

UTI

Exped

itors

Deutsc

he P

ost W

orld

Net

Kuehn

e + N

agel

UPSEGL

John

Men

zies

Si notr

a ns

Panalp

ina TNT

Nippon

Exp

ress

Norbe

rt de

ntre s

angle

Operating income

Operating income

12 cargovision | APRIL 06 cargovision | JUNE 06 13

INTERMEDIARIES Consolidation

WORLDThe market share of the top 10 freight forwarders has increased from25% in 1985 to 40% in 2005. Much of it resulted from ongoing con-solidation. In the last few months, we’ve seen DFDS Transport GroupA/S acquire 99% of Frans Maas Group NV. Fiege, a German logisticscompany bought TTS Group and its sister company, Rewico LogistikInternational, adding to its consumer products and presence inEastern Europe. Another German Logistics firm, Dachser, hasexpanded into Korea and China through joint ventures.Kuehne+Nagel bought E.M. Trans AS in Estonia. John Menziesbought Aeroground, a ground handler operating in the western US.Bibby Distribution in the UK, Azkar in Spain, Bartolini in Italy, MGFLogistique in France, and Rhenus Group in Germany all joinedtogether to form the Logistics World Alliance operating from theRhenus headquarters in Holzwickede. UTi Worldwide Inc. acquiredPortland-based Market Industries, Ltd., a third-party logistics firm.Now, when is UPS going to break down and buy TNT?

INTERMEDIARIES Result

WORLD2005 was a very good year for most forwarders.The operating margins for Kuehne+Nagel andPanalpina led the field and were three to five timesgreater than for most airlines. A number of largefirms saw exceptional year-over-year growth.

OUTLOOK South Africa

JOHANNESBURG2005 was a particularly nasty year for airline safety in Africa, said JeffRadebe, South Africa’s Transport Minister. Addressing an aviationsafety conference in January, Mr. Radebe said that, with one third ofall fatal aviation accidents and less than a 20th of the traffic, Africahad 10 times more accidents than the rest of the world. Still, the air-line business on the continent is thriving. The number of airline com-panies last year reached 372, up from 300 in 2004. Passengergrowth was up 11%, and cargo nearly 8%.

CAPETOWNSouth Africans who import machinery, mechanical appliances, orelectrical equipment from Germany will see their airfreight rates beginto drop. ABX Turner negotiated special rates with airlines that shouldhelp stimulate local industry. Germany supplied R45 billion (EUR6 bil-lion) worth of imports to South Africa last year, compared to R25 bil-lion (EUR3 billion) each from China and the US, and R 21 billion(EUR3 billion) each from Japan and the UK.

JOHANNESBURGIn March, the ocean shipping company Grinrod went on a spendingspree in South Africa, buying the shares it didn’t already own in twodistribution specialists: Auto Carriers Transport and GrinrodPerishable Cargo Agents. Auto Carriers performs vehicle distributionand logistics for South African car manufacturers, where it has about35% of the market. Perishable Cargo Agents has been South Africa’slargest freight forwarder for 25 years..

JUNE 14-17Third Annual Sino-International FreightForwarders Conference, Dong Fang Hotel,Guangzhou, China. Contact: [email protected]

JUNE 17-2345th Farnborough International Airshow,Farnborough Aerodrome, Farnborough,Hampshire, UK. Tel: +44 (0) 20 7976 3330www.farnborough.com

JUNE 26-28Fourth eyefortransport 3PL Summit, 26-28June, Intercontinental Buckhead, Atlanta.Contact: Izabela Janecka (Event Director),Tel: US +1 800 814 3459 ext. 252. Tel: UK +44 (0) 207 375 7564. [email protected]

AUGUST 2-3The Evolution of Logistics & Supply ChainManagement in China, Pudong Shangri-LaHotel, Shanghai. Tel: +1 630 574-0985 x320. [email protected]

SEPTEMBER 10-13Airport Cities World Conference andExhibition, Sky City, Hong [email protected]. www.airportconference.com

SEPTEMBER 12-14 23rd International Air Cargo Forum andExposition, Calgary, Canada. Contact: TIA-CA Secretariat. Tel: +1 786 265-7011. [email protected]. www.tiaca.org

SEPTEMBER 17-21FIATA World Congress 2006, ShanghaiNew International Expo Centre, Shanghai,China. www.fiata.org

SEPTEMBER 19-22Air Cargo China 2006, Shanghai NewInternational Expo Centre, Shanghai,China. Email: [email protected]

OCTOBER 15-18Council of Supply Chain Management andProfessionals (CSCMP) AnnualConference, Henry B. GonzalesConvention Center, San Antonio, Texas.Tel: +1 630 [email protected]. www.cscmp.org

cargovision datelinescargovision news around the world

© S

tefa

n Lo

upat

ty

© S

kysc

an P

hoto

libra

ry/A

lam

y

Control Tower Johannesburg

Income Change (”04-”05) and Margin (”05)

Suvarnabhumi is the name of the new Bangkokairport 30 kilometers east of the city. The “GoldenPeninsula” or “Golden Land” is due to replace DonMuang airport, 30 kilomeers later this year, aftermany delays and cost overruns. The new airportwill handle 1.5 million tonnes of freight per year,roughly double the capacity of Don Muang.

Will the cargo facilities at Bangkok’s newairport accommodate Thailand’s growth?

I’m very, very positive because the new airport willcertainly allow for more tonnage. The governmentwants the airport to open soon. We expect that tohappen by the end of the year and we believe thecutover will go smoothly.

Will the airport have a cargo village and a customs-free zone?

Yes, but the demand will go far beyond the spaceallocated by the authorities, so a private operatormight find an opportunity there. Thai AirportsGround Services Co, Ltd. will operate the customs-free zone and the cargo terminal will have twooperators, Thai Airways and Bangkok Airways.

What about the lack of airside expressfacilities?

No problem. The Big Four express operators(FedEx, UPS, DHL and TNT) have negotiated withBangkok Airways to use part of the terminal facingairside and this will facilitate express operations.

14 cargovision | JUNE 06 cargovision | JUNE 06 15

Will operators use radio-frequency ID tags orother new technology at Bangkok’s newairport for locating and tracking cargoes?

If airlines and terminal operators want to introducenew technologies that would increase confidence inBangkok’s capabilities, I would fully support them.

Are you surprised that Thai Air Cargo, the cargo airline planned by Qantas and CTI Holding, has been shelved?

Not at all. Our market has lots of exports and fewimports. We know the difficulties they were having.Without a proper network, it’s impossible to runfreighter aircraft profitably.

Didn’t Thai Airways and a freight forwarderalso plan a joint venture?

That is also on hold. If Thai operated bothfreighters and passenger aircraft, it would improveBangkok’s cargo throughput. Nevertheless, theproblem is poor backhaul loads. In spite of theirgood route network, Thai Airways is conservative.

Do airlines and forwarders suffer because ofThailand’s imbalanced flow of air cargo?

Yes, weak inbound and strong outbound flows area real problem. The Thai government needs to pro-mote our airport as a regional hub. Singapore hasbeen doing it successfully for a long time. We justneed action from our government. The authoritiesmust help to create confidence among logisticsproviders that Bangkok is a good cargo center. It is

a matter of trust. We have more flights than mostairports, but less but less cargo throughput. Wecan do repackaging, reassembly, and transship-ment. These services just need more investment inpromotions to build confidence among providers.

What types of cargo flow to and from Thailand?

The growth trend in electronic goods is obviousnow and we are seeing more high-fashion gar-ments. Many factories buy fabric from Italy andmake high-value garments here for export toEurope and America. Our government is promot-ing the car industry and foreign manufacturershave built plants here. We also have very steadygrowth in perishables: orchids and fruit. If thesecan become tax-free under Free-Trade Agree-ments, we can be more competitive. General car-go is growing at about 10% per year.

Has Thailand lost cargo business to other places such as China?

We did lose some of the garment business to

China and our neighboring countries. Vietnam,Cambodia and China all have the advantage oflower wages. Thailand must produce more of thehigh-fashion, high-value garments, as Hong Kongdid years ago.

Do you find benefits in collaborating with specific cargo airlines?

As an independent, we like to deal with all cargoairlines. However, in this era of logistics services,we must generate the confidence that we can pro-vide one high standard of service anywhere.Therefore, we must have close cooperation withsome airlines that, in turn, choose strategic part-ners from among the logistics providers, so theycan offer door-to-door services like the Big Four.

PREPARING FOR CHANGEBY MICHAEL WESTLAKE

Kovit Thanyarattakul is aman with a positive view ofThailand’s airfreightprospects. He is chairmanand managing director ofMulti Air Services (MAS) inBangkok, an air and seafreight forwarder and logis-tics provider that has toppedthe IATA league table forThailand several times andhas been in the top five forthe past 10 years.

Khun Kovit, 55, started withAir Siam after obtaining auniversity degree in market-ing. He founded MAS in1978. He is a former secre-tary of the Thai AirfreightForwarders Association andwas later its adviser. Heserved twice as president ofExpress TransportOrganization, a truckingcompany owned by the ThaiMinistry of Transport.Khun Kovit spoke withCargovision about theprospects for Thai airfreightand Bangkok’s new airport.

COMPANY PROFILE

Multi Air Services was foundedin 1978, focusing in airfreightbusiness. It kept growing suc-cessfully. Multi Freight SystemCo., Ltd. was established in1989 to concentrate in oceanfreight, and Multi Logistics Co.,Ltd. was founded in 1999 toprovide the logistics services inthe globalization era.

Multi Air Services has been oneof the IATA top 5 agents in theexport annual sales volume forthe past 10 years in Thailand. In2004, it has gained the top IATAranking at the sales volume ofUS$64.12 million. Multi canprovide all kinds of airfreightservices. The company hasgained special recognition asone of the very best handlers ofperishable and fresh cargo.

Mr. Kovit Thanyarattakul, theChairman and MD of Multigroup, is now the Chairman ofThai Airfreight ForwardersAssociation (TAFA), which is theonly airfreight association rec-ognized by the ThaiGovernment and the airfreightindustry. He has strong inten-tion to build the airfreight indus-try in Thailand and fully sup-ports the vision of the ThaiGovernment to promoteBangkok’s new SuvarnabhumiAirport as a key airfreight transithub in South East Asia.

■ Suvarnabhumi is the name of the newBangkok airport 30 kilometers east of the city.The “Golden Peninsula” or “Golden Land” isdue to replace Don Muang airport later thisyear, after many delays and cost overruns.The new airport will handle 1.5 million tonnesof freight per year, roughly double the capaci-ty of Don Muang.

© J

. M

arsh

all-

Trib

aley

e Im

ages

/Ala

my

© A

ndre

w W

ood

ley/

Ala

my

© ANP Foto

© R

icha

rd S

tam

per

/Ala

my

Searching the world for leaner logistics and lower landed costs,auto builders found China. That worked for a while. Now, they likeEastern Europe. We explore this change and its effect on the aircargo business, where 8% of traffic is automotive related.

BY MARK W. LYON

■ Just when Chinese laborers had convincedus that resistance was futile, up pops MichaelBomann, general manager of worldwide distribu-tion for BMW, AG. “The promise of China as aninexpensive source of components is not beingdelivered to the auto industry,” Mr. Bomann toldautomotive professionals gathered at a logisticsconference in Montreux in March. The quality ofChinese-made auto parts is unsatisfactory, Mr.Bomann continued. Not only did they take six toeight weeks to arrive by sea freight, but any sub-standard parts then had to be replaced using air-freight at additional cost.China will not become the primary maker of autoparts for European and American auto produc-tion during the next five years, Mr. Bomann pre-dicted. Why auto builders are unimpressed by amanufacturing prowess that makes otherWestern industries quake in their boots, is notonly surprising, but could prove troubling for theairfreight industry if they decide to relocate pro-duction to other regions. The early signs suggestthey will.“The Chinese government saw electronics com-panies as strategic assets, but not auto compa-nies,” explains Thomas Cullen, author ofAutomotive Logistics Europe 2006, published byTransport Intelligence Ltd. This oversight retard-ed the evolution of China’s car industry and theparticipation of its component builders in theUS$19-billion market for global auto parts. It alsoproduced a supply chain infrastructure for elec-tronics components that is highly efficient andanother one for auto parts that is still primitiveand plagued with chronic problems.”When China opened its arms to electronicsfirms, many of them, even some who had movedinto Eastern Europe only a few years before,packed their bags and headed to Asia, leavingbehind a slew of underutilized factories and askilled (and now hungry) workforce. A number ofthese facilities have now reinvented themselvesas neighborhood repair stations for electronics

consumers in Western Europe. Still, vehicle man-ufacturers soon discovered they could opencomponent factories and assembly plants atbargain-basement prices in Eastern Europe.Thus, Poland, the Czech Republic, Slovakia,Hungary, and Romania all became importantsites for auto production, Mr. Cullen explains.More than 10 plants have opened or beenacquired there by Western vehicle manufacturinggroups during the last decade, while no large-volume car plants have opened in WesternEurope.

STABILITY AUGMENTATION

Although China overtook South Korea andFrance to become the world’s fourth-largest automanufacturer last year, with nearly 5 million vehi-cles produced, recent developments in westernmarketing are hindering its success with compo-nents:Mechatronics. Mechanical-electronic hybrid sys-tems, such as chassis stabilization and ABSbrakes are found in growing numbers of modelsevery year. Mechatronic parts require sophisti-cated production skills, more so than DVD play-ers, and different supply routes. Workers inEastern Europe have thus far outclassed theirChinese rivals in building mechatronics.Shorter lifecycles. Some new auto models lastfour to six years in the market, says VolkmarHerrscher, SVP for automotive atKuehne+Nagel’s corporate headquarters. Carbuilders used to change models every six toeight years. “With such a short lifecycle, you can-not waste time and money in lengthy supplychains. We saw this previously in electronics.Now, something similar is happening in autos,and the more expensive parts are moving by air.”Build to Order. These programs, offered byRenault and BMW for example, let customerschange the specifications of their car as late as

16 cargovision | JUNE 06 cargovision | JUNE 06 17

DYNAMICS

■ Auto related equipment is8% of total airfreight and 3% ofthe auto industry’s total ship-ping weight. ■ Supply base is dispersedand individual lanes lack suffi-cient volumes.■ High transport costs drivestandardization of packagingto optimize resource utilization.■ Suppliers are on a steeplearning curve.■ Complex supply chainsrequire end-to-end manage-ment.

U-TURN

Participants 2006 Participants 1986

• 5,000 Suppliers • 30,000 Suppliers• US$ 800 billion • US$ 250 billion

AUTOLOGISTICS

SUPPLY-CHAINSTRUCTURE

■ Regionally-based. Automak-ers, wanting to avoid possiblelosses when buying parts in aforeign currency, historicallypreferred suppliers from theirown region, making auto sup-ply chains less global thanthose in electronics, Mr. Cullensays. ■ Regional differencesbetween Central and EasternEurope. Auto plants in CentralEurope are proper manufactur-ing sites with wide-ranginglogistics requirements, whilethose in Eastern Europe areusually CKD plants whereworkers assemble finishedvehicles from completeknocked-down (CKD) kits thatarrive as containers of theparts for a single car.■ Undefined in the East.Poland is well covered bytransportation vendors in theWest and in Eastern Europe.The Baltic States have inferiorservices and competition in theUkraine is intense.

© G

etty

Imag

es

Car manufacturing plant, mechanic working on engine

PEOPLE MAKE A DIFFERENCE

costs. Although container rates from China com-pare favorably to those from Europe andAmerica, airfreight rates from China are oftenthree times higher. To avoid paying thesecharges, he may postpone switching delayedshipments from sea to air until he has no otherchoice. At this point, the failure can wipe out anyprofit his company gained by moving productionto China. Under the same pressure, supply chain man-agers are constantly factoring the minimum tran-sit times required for stable materiel flows. “Takethe minimum everywhere, and when somethinggoes wrong, you will fly more than expected,” Mr.Herrscher says. “We are seeing more of theseemergencies today and are flying more freightthan ever.”Using airfreight for high-value components canlower packaging costs, residual damage, insur-ance premium and lifecycle costs, Mr. Herrschersays. When it comes to high-tech and electron-ics in cars, airfreight becomes increasinglyimportant. It is often the most economicalanswer, but only when companies plan andbudget for it. Auto companies have been reluc-tant to do so, but seem more willing today underthe powerful pressure to reduce cost andincrease productivity. Meanwhile, for the short term, logistics providersmay see the large flows of auto-related trafficnow moving into China replaced by truck move-ments to Eastern Europe. In the longer term, car-riers can expect to fly fewer finished cars fromAsia to Europe. Local parts production in Chinawill begin to grow more in line with local car salesas Central and Eastern Europe component mak-ers take a larger share of the European market.

Philippe Gallon understands the subtle nature of Africa’s business climate. As the local manager for AF-KL Cargo in Abidjan, he hashelped more than a few forwarders get effective results for their customers in West Africa’s Gulf of Guinea region.

BY PHILLIP HASTINGS

18 cargovision | JUNE 06 cargovision | JUNE 06 19

It irritates Philippe Gallon when people explain aservice failure with the comment, “Well, this isAfrica.” As AF-KL Cargo's market manager forWest Africa’s Gulf of Guinea region, he insiststhat being in Africa is no excuse for not meetinginternational standards for air cargo perform-ance. “Basic infrastructure can be a problem,” Mr.Gallon says. “A sudden power cut or a brokentelephone link to your handling company. Or astation suddenly has no aviation fuel and youhave a flight due for takeoff. But these are prob-lems you must resolve. Customers don’t want toknow about your internal difficulties. They justwant their cargo delivered.”In the Gulf of Guinea, those customers includeconsignees receiving cargo from all over theworld, as well as African shippers of time-sensi-tive perishables, such as French beans and man-goes. Meeting their expectations in Africa oftenmeans going the extra mile and sometimes morethan one. “To achieve European or North American servicestandards here,” Mr. Gallon says, “You needthree times as much time and energy. I believemy job is my life. If someone phones at oddtimes with a problem, you must respond posi-tively. But it’s a very exciting life. Something newis happening all the time, and there are so manyopportunities.”

Born in Lomé, the capital of Togo, Mr. Gallonjoined Air France in 1979 and worked in mainte-nance before moving to cargo in the early 1990s.His work has taken him to Europe, Asia, andmany parts of Africa. He arrived in Abidjan lastOctober from South Korea and now managesGhana, Togo, Benin, Nigeria, Niger, BurkinaFaso, and the Ivory Coast. “I’m always on aplane,” he says.A local presence is vital to the company’s suc-cess, Mr. Gallon believes. “Everyone in the Gulfof Guinea market knows that the AF-KL Cargomanager is based in Abidjan. He visits you andthen he returns to Abidjan, not Europe. Thatearns you trust and respect as a man. After that,people respect you in business.”

Phil ippe Gallon, [email protected]

six days before delivery. This can save US$1,500per vehicle compared to keeping it in inventory.The trend is on the rise because customers aremore satisfied, less capital is committed, andmanagement needs fewer inventory controls andpays lower incentives. Jeff Gaudiano, of BMWGroup’s structural planning, production control,and distribution division says, “After changingour IT systems, the most difficult part of introduc-ing build-to-order was managing the change. Wespent hours educating our suppliers to convincethem they don’t need inventory.”

LANE CHANGE

Within China, rising incomes for auto industryworkers along the Eastern Seaboard have man-ufacturers searching inland for lower-cost sites,although most component builders still preferShanghai, with its transportation infrastructureand skilled labor. Yet, they must weigh theseadvantages against an environment that isunderpowered and over-polluted. “According to some OEMs in the Shanghai area,they were asked by authorities to reduce pro-duction in the summer months in order to saveenergy during that period,” Mr. Herrscher says.“They are now trying to force companies intoneighboring provinces, but the workers andtransportation there are lacking.”Western manufacturers also know that exportingnew automotive technologies to China exposesthem to theft and a quick loss of market advan-tage to new competitors. These trends all complicate life for the purchas-ing manager who is trying to lower transportation

cargovision interviewcargovision U-turn

EASTWARD BOUND

■ BMW said it will expand toEastern Europe.■ GM negotiating to build its firstCKD factory in St. Petersburgand in Kaliningrad, locatedbetween Poland andLithuanian.■ Hyundai and Daewoo haveCKD operations in Ukraine.■ Hyundia-Kia will increaseproduction by 50% in Slovakiain 2007.■ Hyundai will open a EUR1 billion plant in theMoravia-Silesia region ofCzech Republic in 2008.■ Johnson Controls - producerof automotive componentsand provider of automationsystems, has announced plansto build a car componentfactory in Siemianowice, in theKatowice Special EconomicZone.■ PSA Peugeot-Citroen isbuilding two manufacturingplants at a cost of EUR1,057 inTrnava in the ZazpadneSlovensko region of Slovakia.■ Renault is reviving Daciaproduction in Pitesti, Romania.■ Toyota, Peugeot, Citroën willstay in Bohemia, CzechRepublic.■ VW took over Skoda in CzechRepublic and will beginproduction in Russia in 2008.

© G

etty

Imag

es

Worker at car assembly line

■ Ask 20 people what they mean by the term“customer service” and you will get 20 differentanswers, says Jan Krems, AF-KL Cargo vicepresident of customer service. “Look how 20companies structure their customer serviceorganizations and you’ll find 20 different solu-tions.” Mr. Krems is overseeing the process ofintegrating customer service offices throughoutAF-KL Cargo’s network. It is a fundamental partof coordinating the AF-KL Cargo strategy forbringing one face to the customer. With AF-KLCargo offices located around the world, culturaldifferences could have posed a problem. Butthat did not happen. Since the project began lastOctober, the organization has made consider-able progress towards unifying customer serviceteams in the cities where they had previouslyoperated as Air France Cargo and KLM Cargo.

GOLD RUSH

“We started this project by agreeing on a visionfor customer service that would apply through-out our organization at the end of the integrationprocess,” Mr. Krems says. “We call this the ‘GoldStandard.’ We also drew up a plan to achieve it.We call that the ‘Gold Rush.’”Although AF-KL Cargo has customer serviceoffices at 160 stations, the partners offer dupli-

cate services at only 64 of them. “Since lastOctober, we have brought the Air France Cargoand KLM Cargo customer service people togeth-er under one roof at 35 of these 64 stations,” Mr.Krems explains. “They work separately, with theirown telephone numbers, but they can see andlearn from each other. By this November, we planto establish co-locations at 29 other stations.”Customers may not notice the difference imme-diately, because their local Air France Cargo orKLM Cargo service representatives continue touse separate telephone numbers and systems,Mr. Krems says. “However, slowly but surely those operations willmerge into one. Then, one office will handle allbooking requirements with one team of peopleand one system. Over time, customers will seethey are working with a single voice for all of theAF-KL Cargo business.”

ROOM MATES

Forwarders will gradually be able to sourcecapacity and book cargo on any AF-KL Cargoflight with a single phone call. They will speakwith one contact in a common office, using acommon system. The objective of AF-KL Cargois to combine the best assets of both carriers’commercial organizations into a single service.

How this works will become apparent later thisyear when AF-KL Cargo rolls out its unique voiceportal (UVP). This utility will display informationabout AF-KL Cargo customers, allocations,rates, spot rates, allotments, and air waybilldetails. It is a shell program that creates a singleview of the information in the existing orderingand booking systems of Air France Cargo andKLM Cargo for customer service staff at eachco-location.Mr. Krems explains: “Suppose an Air France rep-resentative in Singapore receives a call request-ing 1,000 kg for New York. The rep checks theUVP system and finds there is no space availableon any Air France flight. The same system willthen show whether there is capacity on a KLMflight. If so, and the customer likes that option,they can book the space.”AF-KL Cargo intends to establish UVP shells for allof its local operations by the end of October.“Then we will slowly migrate into a single order-taking system for both carriers,” Mr. Krems says. “We combined customer service offices accordingto their suitability,” Mr. Krems says. “We always tryto be close to the market, but we take the localcircumstances into account. Some of our officesare at the airport and some are in the city. Often itwas a question of whether the Air France Cargo orKLM Cargo offices had enough space.Sometimes we had to move to new offices.”

FOUR CATEGORIES

Apart from putting people together in the sameoffice what, in practice, does integrating localcustomer service offices actually involve? “Weare managing the AF-KL Cargo integration underfour categories,” explains Mr. Krems. “Management organization, people develop-ment, services & processes and infrastructure. “We are already achieving some of our objec-tives,” Mr. Krems continues. “For example, withinour infrastructure we have established 35 co-locations. And now we are moving ahead. Bycreating our initial vision of customer service, theGold Standard, we could share our ideas andplans and were able to align ourselves within theAF-KL Cargo organization.” In principle, AF-KL Cargo wants to complete thetotal integration of its local customer serviceoperations by the end of 2007, Mr. Krems says.“We stress the ‘in principle.’ We don’t want toput a firm deadline that could leave people feel-ing frustrated if there is a delay. The crucial thingis to get this right, so everyone is happy. Thehuman touch, rather than tools and systems, willultimately decide the measure of success.”

Apart from gathering people under one roof, whatexactly does integrating local customer service teamsinvolve? Jan Krems explains.

BY PHILLIP HASTINGS

20 cargovision | JUNE 06 cargovision | JUNE 06 21

UNDER ONE

ROOF

© C

apita

l Pho

tos

Mr. Krems says:“We call this the ‘GoldStandard’. We alsodrew up a plan toachieve it and we callthat the ‘Gold Rush’.”

MONDAYHOOFDDORP AND PARISAlthough I am based in Brussels, my office is actually inHoofddorp near Schiphol Airport. I usually do two trips a weekand spend one day in the office. Today, I have a 08:00 flight toParis. I am not a morning person and find it tough to get up at06:00. In Paris, I go to the DHL office and straight into aninternal meeting, where we analyze the best way to move acustomer’s airfreight into the US and Canada. Should we usea hub and spoke with one or two entry points, or direct flightsto all locations? Customs clearance is part of the calculationand so are rates. In the afternoon, we meet with our customerto discuss the solutions. In the evening, I fly back to Schiphol.

TUESDAY HOOFDDORPIn the office, going through my email. I get about 80 a day,and ditch 30 of them straight away. I have to read the rest anda few involve serious work. Since my colleagues are alwaystraveling, it is always interesting to see who is in the office andto share the pleasures and frustrations of our jobs. Next, Ihave conference calls with a customer, followed by a weeklyconference call with my counterparts in Asia and America.The early afternoon timing for me coincides with the Asianevening and the American morning. Later that evening, I ridemy mountain bike. Because I’m always traveling, I can’t par-ticipate in organized sports.

WEDNESDAYBUDAPEST AND BEYONDAfter a morning in the office, I fly to Budapest. I worked here forfive years and love Hungarian people and culture. It’s alwaysgood to come back, but it has changed so much in just a fewyears. Today, I take a new highway from the airport to the cityfor the first time. Fortunately, the mentality of the people hasnot changed so much, and that is comforting to me. We drivefor three hours that afternoon, to the east of Hungary, wherewe will meet our customer the following morning.

THURSDAY HUNGARY AND THE UKRAINEI spend the morning inspecting a rail terminal where our cus-

tomer will be loading ocean containers. Then we drive to theUkrainian border and leave our car. Since Kiev held theEurovision Song Contest last year, EU citizens no longer needvisas, but the border crossing is still difficult and even morecomplicated if you drive. Our customer picks us up on theother side. The Ukraine is still very poor. You see houses with-out windows and horses in the street. With Eastern Europeancountries now in the EU, Ukraine is a new frontier for high-tech manufacturing. Because customs clearance is majorhurdle, we use Budapest as a hub for our customer. It is actu-ally closer than Kiev. In the evening, I return to Budapest tomeet friends, but our late arrival leaves time for only one beer.

FRIDAYHOOFDDORPI fly to Amsterdam in the morning. In the afternoon, betweenthe emails and conference calls, I take time to think about myjob. My role lets me draw on the varied resources of the DHLorganization. After two years, I am pretty familiar with the dif-ferent parts of the company. But I still bring a local managerwith me to meetings, because they are the specialists. I alsoenjoy sitting with a customer, mapping out their supply chain,and then suggesting a solution that might entail forwarding forone leg and express for another. Since customers don’talways know their own supply chains, it is usually an eye-opening exercise for them, too. Whether they accept creativesolutions is another matter.

SATURDAY HOOFDDORPI do my best to keep weekends free. I don’t mind workinglate during the week, but on Saturday and Sunday, I turn offmy computer. My girlfriend and I will marry in September andwe spend the day planning the wedding, and shopping. Wework on our new house and go out in the evening for dinnerwith friends.

SUNDAY HOOFDDORPWe always keep this day completely free. We have a nice latebreakfast, go for a long walk, or a bike ride, or we visit friends.Tomorrow, I am off on another trip, this time to Barcelona.

CARSTEN PELLICAANCarsten Pellicaan is part of a team that helps DHL’s top 100 customers make the most of the company’s fourbusiness units: forwarding, trucking, contract logistics, and express. Mr. Pellicaan has been a member of theGlobal Customer Solutions Team since 2004 and worked in Central and Eastern Europe for Danzas and AEI. Of the mergers, he jokes, “I changed companies three times, without ever leaving the company I worked for.”

WITH PETER CONWAY

cargovision week in the life of

cargovision | JUNE 06 23

© C

orb

!no

24 cargovision | JUNE 06 cargovision | JUNE 06 25

■ “U.S. Food and Drug Administration (FDA)dictates the temperature regulations and guide-lines for shipping pharmaceuticals,” says Arthurvan Olst, senior project manager for Pharmaceu-tical Logistics at AF-KL Cargo. Other countrieshave adopted the US standards and some, suchas Canada and Ireland, have expanded therequirements to include additional temperaturemonitors. “These regulations have little flexibility, “ Mr. vanOlst adds. “Wherever we go, we must consider amultitude of variables. For example, if you shipvials of vaccine from the United States to theNetherlands, the temperature must be between2°C and 8°C throughout the entire journey.”Vaccines are more sensitive to temperaturechanges than medicines, Mr. Olst adds. FDA guidelines say that temperature controlledpackaging should be validated. This means thatpackaging experts must consider various proto-cols in their designs. For example:Is the pharmaceutical shipment going to a coldor hot climate?Is it traveling during summer or winter?What outside temperatures will it encounter whilein transit? How long will the product be in traveling? Will the shipment take 24, 48 or 72 hours toreach its destination? If it arrives on a holiday, Kuwait on Friday orDallas on Saturday, will the packaging maintainthe required conditions throughout the week-end? “Maintaining a proper and constant temperature

level is paramount in ensuring integrity through-out the supply chain,” says Mr. van Olst.

HEAT SYNCH

Logistics providers have four service optionswhen they use AF-KL Cargo, depending onwhether their customers’ products need to flyfrozen, refrigerated, or at room temperature:Pharma 1. Product must remain frozen at a temperaturebetween -20°C and +20°C. “This is a closed cool-chain concept,” Mr. vanOlst says. Most shipments moving this way useEnvirotainers with active temperature controlsystems. These allow the shipper to stipulateexact temperatures and to keep the producttemperature stable despite fluctuations in theambient temperature. An added benefit,Envirotainers are so secure that they also protectagainst theft and pilferage. “While this is the most secure way to ship tem-perature-sensitive products, it is also the mostexpensive,” Mr. van Olst adds. Pharma 2.Product must remain between 2°C and 8°C.“This is not a closed cool-chain concept, Mr. VanOlst notes. “ It is used more frequently thanPharma 1, because it is cheaper.” These ship-ments may be palletized or stacked in theAirModule system developed by AF-KL Cargo.They are transported in the temperature con-trolled cargo compartment of an aircraft, or atemperature controlled truck, or stored in a tem-

perature-controlled warehouse. “The only time the shipment is not in a controlledenvironment is when being delivered to the air-craft,” Mr. van Olst says. Pharma 3.Product must travel at room temperaturebetween 10°C and 25°C. Products include pills,creams, and other over-the-counter drugs.Pharma 4.Products shipped with dry ice coolant. “AF-KL Cargo offers these solutions to pharma-ceutical shippers based on their temperaturerequirements,” Mr. van Olst says. “They are also

based on the Good Distribution Practices of theFDA.” Where airports do not provide tempera-ture-controlled warehousing, AF-KL Cargoarranges for local ground handling agents to pro-vide temperature-controlled service and ware-housing capabilities, Mr. Olst adds. “Not everystation in the AF-KL Cargo networks can handlepharmaceutical shipments. Based on a cus-tomer’s product requirements, we look at ourworldwide system to see which ones can fulfillthem. This network is audited every year toensure they maintain the quality needed to han-dle pharmaceutical shipments.”

Rules and regulations often influence the design and construction of packagingfor air transportation. The pharmaceutical industry is a good example. Its tem-perature sensitive products need methods that can protect against damage andtheft and still temperature-sensitive maintain proper temperature.

BY KAREN E. THUERMER

“Maintaining a properand constant tempera-ture level is paramountin ensuring integritythroughout the supplychain” says Mr. van Olst

TEMPERATURE MATTERS©

Cor

b!n

o

© Corb!no

26 cargovision | JUNE 06 cargovision | JUNE 06 27

YIELDS IMPROVINGAndrea Hricova, airfreight manager,Schenker spol, s.r.o.

“Expansion in our Czech Republic activities hasbeen on the back of the German or Austrianmanufacturers setting up local joint ventureplants. Some 60% of our traffic goes directly byroad to our main hub at Frankfurt where it headsfor Hong Kong, New York, Shanghai, or Tokyo.Rates are negotiated by manufacturer headoffices. I see yields improving on outbound traf-fic, which has moved traditionally on a collectbasis. Key to being successful in this market is tohave a strong network with multiple choices fordelivery.”

FILM RUSHESCtibor Liska, export manager,ATS-Air Transport Service

“The Czech air freight market is becoming morecompetitive from offline carriers that solicit aircargo to be trucked to Vienna and Frankfurt. Asa local forwarder routinely handling 100-kg to500-kg consignments, from vaccines to spareparts, I prefer Prague uplift where possible. I look

to carriers to give good price, reliability, flexibility,and communication. AF-KL Cargo tops that withcommitment, especially for the Equation expressproduct. This benefits the flourishing local filmindustry. Typically, we dispatch film rushes toLondon or America. Even parts of the re-make ofthe James Bond movie Casino Royale were shot inthe country in February. Afterwards, a MonarchAirlines charter ferried 12 tonnes of film equipmentfrom Prague to Nassau. Looking to the future,Prague is thinking big. It could become an air car-go gateway to Central and Eastern Europe.Compared to Vienna, its nearest rival, there isalready little difference in service standards.”

EFFICIENT, COMPACT, ECONOMICRenata Zasmetova, export manager,Delta International Cargo s.r.o.

“Prague Ruzyne Airport is efficient, compact andeconomic. However, it is unlikely to take on therole as a regional hub to Central and EasternEurope soon as long as it is served by smaller air-craft with only limited capacity. We will continue totruck large air shipments to Amsterdam, Frankfurt,London and Paris, en route to destinations suchas Los Angeles and Miami.”

CONSIGNMENT PLANNING 24-7Vaclav Koula, air export manager,cargo-partner CR, s.r.o.

“It is no longer a problem for us to truck across EUborders to airport hubs such as Amsterdam,Brussels, Frankfurt, and Paris. While we work withmost of the airlines serving Prague, the now unifiedAF-KL Cargo management in Prague gives ship-pers round-the-clock service for consignment plan-ning. This is a first in this market by any airline. As aresult, depending on the urgency of shipments orthe client’s choice of service level, we can splitcapacity between the two carriers. We can buyspace for a better rate and even consolidate in ourVienna head office, particularly for the large volumeof automotive parts to the US, Japan and Mexico.”

THRIVING ECONOMYVladimir Blazek, customer service manager for Central and Eastern Europe, AF-KL Cargo, Prague

“Since the Czech Republic joined the EU, the chal-lenge for AF-KL Cargo in Prague has been tomaintain and expand its market share in the faceof growing truck competition to other EU airports.Under a unified Prague management, we retainproduct consistency and selling practices, butshippers now enjoy greater choice in capacity allo-cation between the Air France and KLM networks.This includes using local SkyTeam Cargo partner,

CSA, to connect with Delta flights to JFK fromBerlin and Athens. We are known as the “Detroit ofEurope.” Czech-produced automotive parts,machinery, lighting, electronics, and crystal glass-ware are our key exports. We prefer to board car-go at Prague, but tend to truck it to Paris andAmsterdam via consolidation at Hahn (Air France)and Linz (KLM). A local community of 150,000Vietnamese and Chinese has created a substantialtwo-way market for Equation and time-sensitiveitems. These people were factory workers in thecommunist era, but today have become tradersand entrepreneurs, contributing to the thrivingCzech economy. Prague will likely grow as a trans-shipment hub for small and express imports feed-ing CSA’s Eastern European network.”

MARKET ADVANTAGEHans Korbijn, director - AF-KL Cargo Central and Eastern Europe, Budapest

“The integration of AF-KL Cargo in Prague resultedfrom the enthusiasm of local teams from both air-lines. They wanted this to be one of the first stationsto gather local offices under one roof. This tookplace after the Czech Ministry of Finance allowedboth airlines to sell each other’s air waybills. It hasgiven us a significant market advantage.”

THE CZECH REPUBLIC BY GERRY BROWN

NEED TO KNOW

■ The Czech Republicjoined the EU on May 1,2004.■ Population: 10.2 mil-lion. Czech men refer tothe national drink, beer,as ‘liquid bread’ consum-ing more than 150 liters ayear, the highest in theworld.■ General: A member ofthe OECD, NATO, WTO,IMF, and EBRD, thecountry is a parliamen-tary democracy with anopen market economyand a strong currency. ■ Economy: Real GDP5.5% in 2006; 4.5%expected in 2007. Nearly60% of exports go toEU15 (Germany takes36%), mainly machineryand transport equipment,intermediate manufac-tured goods, and chemi-cals.■ Financial Rating:Moody’s, A1 grade;Fitch, A grade, Stable forlong-term foreign curren-cy obligations.■ Foreign Investment:Favorable laws attracted1,200 foreign companies,including Volkswagen,Daewoo, Hyundai,Siemens, Danone, CocaCola, Pepsi Cola, andTesco.

TRAVEL TIPS

■

Czech companies tend tostart work earlier than09:00 and finish earlier than17:00.■

Meetings can take longerthan expected and can bevery formal.■

Czech business peopleincreasingly use English,but misunderstandings canand do occur. If in doubt,use an interpreter.■

Business people should beopen and expect directlyexpressed opinions.■

Punctuality is expected andappreciated, and businessdress should be smart andclean.■

It is best to use a person’stitle, such as Doctor.■

Shaking of hands is cus-tomary when meeting andleaving people.■

Bring a plentiful supply ofbusiness cards, as the useof business cards is com-mon.■

Some of the old communistattitudes still prevail, butthe new generation of busi-ness leaders is developingall the business skills rec-ognizable in the West.■

The Czechs rightly resentbeing treated as if they area developing country.Therefore avoid statementssuch as “the way we do it inour country is...”

cargovision country file

Prag Museum fur Moderne Kunst Lichthof

Orangery Prague Castle Exterior

© R

ober

t H

ard

ing/

Ala

my

© B

ildar

chiv

Mon

heim

/Ala

my

© A

lam

y

© Arcaid/Alamy

2005

A TROUGH BETWEEN PEAKS?

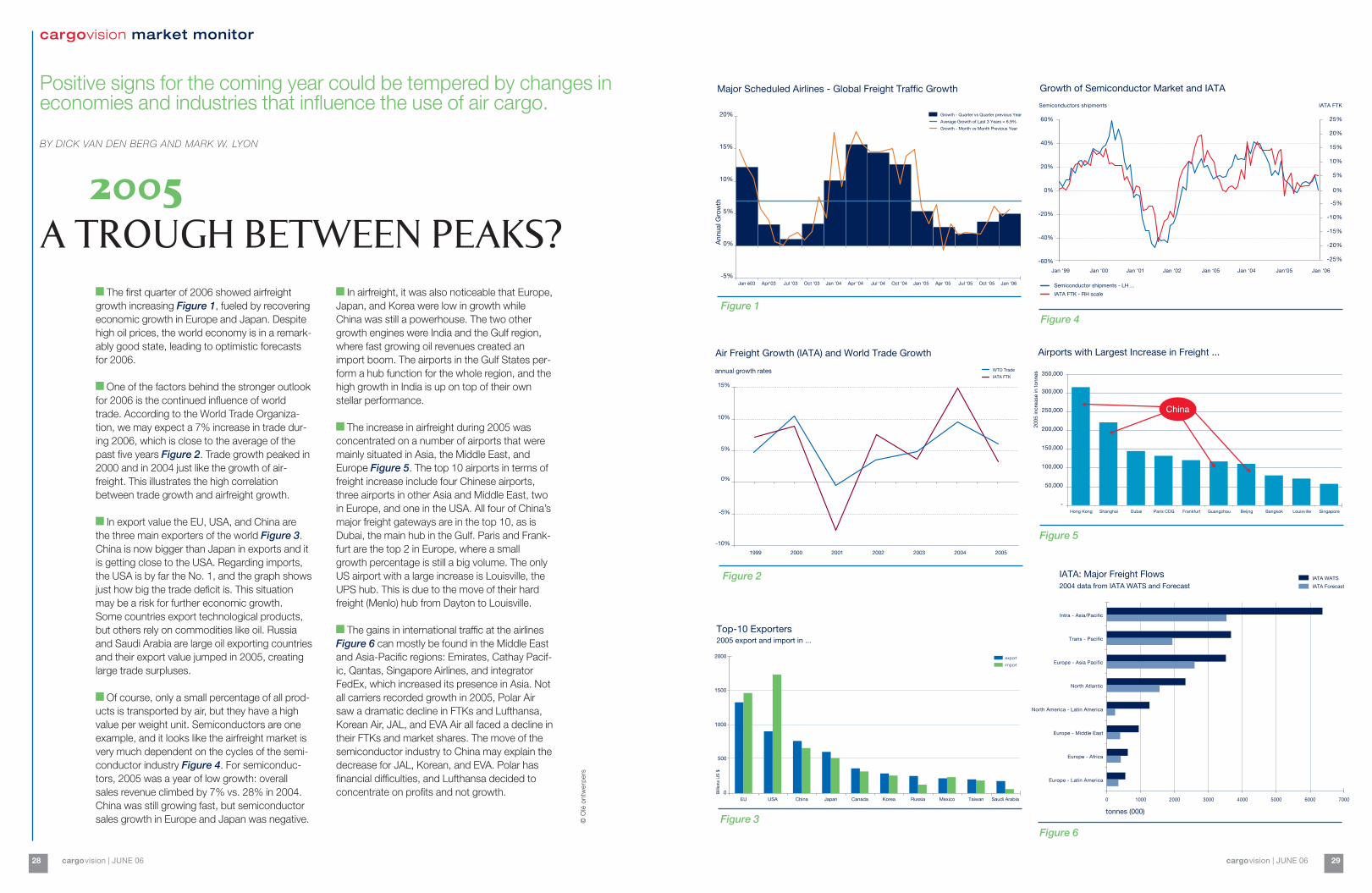

■ The first quarter of 2006 showed airfreightgrowth increasing Figure 1, fueled by recoveringeconomic growth in Europe and Japan. Despitehigh oil prices, the world economy is in a remark-ably good state, leading to optimistic forecastsfor 2006.

■ One of the factors behind the stronger outlookfor 2006 is the continued influence of worldtrade. According to the World Trade Organiza-tion, we may expect a 7% increase in trade dur-ing 2006, which is close to the average of thepast five years Figure 2. Trade growth peaked in2000 and in 2004 just like the growth of air-freight. This illustrates the high correlationbetween trade growth and airfreight growth.

■ In export value the EU, USA, and China arethe three main exporters of the world Figure 3.China is now bigger than Japan in exports and itis getting close to the USA. Regarding imports,the USA is by far the No. 1, and the graph showsjust how big the trade deficit is. This situationmay be a risk for further economic growth. Some countries export technological products,but others rely on commodities like oil. Russiaand Saudi Arabia are large oil exporting countriesand their export value jumped in 2005, creatinglarge trade surpluses.

■ Of course, only a small percentage of all prod-ucts is transported by air, but they have a highvalue per weight unit. Semiconductors are oneexample, and it looks like the airfreight market isvery much dependent on the cycles of the semi-conductor industry Figure 4. For semiconduc-tors, 2005 was a year of low growth: overallsales revenue climbed by 7% vs. 28% in 2004.China was still growing fast, but semiconductorsales growth in Europe and Japan was negative.

■ In airfreight, it was also noticeable that Europe,Japan, and Korea were low in growth whileChina was still a powerhouse. The two othergrowth engines were India and the Gulf region,where fast growing oil revenues created animport boom. The airports in the Gulf States per-form a hub function for the whole region, and thehigh growth in India is up on top of their ownstellar performance.

■ The increase in airfreight during 2005 wasconcentrated on a number of airports that weremainly situated in Asia, the Middle East, andEurope Figure 5. The top 10 airports in terms offreight increase include four Chinese airports,three airports in other Asia and Middle East, twoin Europe, and one in the USA. All four of China’smajor freight gateways are in the top 10, as isDubai, the main hub in the Gulf. Paris and Frank-furt are the top 2 in Europe, where a smallgrowth percentage is still a big volume. The onlyUS airport with a large increase is Louisville, theUPS hub. This is due to the move of their hardfreight (Menlo) hub from Dayton to Louisville.

■ The gains in international traffic at the airlinesFigure 6 can mostly be found in the Middle Eastand Asia-Pacific regions: Emirates, Cathay Pacif-ic, Qantas, Singapore Airlines, and integratorFedEx, which increased its presence in Asia. Notall carriers recorded growth in 2005, Polar Airsaw a dramatic decline in FTKs and Lufthansa,Korean Air, JAL, and EVA Air all faced a decline intheir FTKs and market shares. The move of thesemiconductor industry to China may explain thedecrease for JAL, Korean, and EVA. Polar hasfinancial difficulties, and Lufthansa decided toconcentrate on profits and not growth.

28 cargovision | JUNE 06 cargovision | JUNE 06 29

cargovision market monitor

© O

lé o

ntw

erp

ers

Positive signs for the coming year could be tempered by changes ineconomies and industries that influence the use of air cargo.

BY DICK VAN DEN BERG AND MARK W. LYON

Major Scheduled Airlines - Global Freight Traffic Growth

-5%

0%

5%

10%

15%

20%

Jan ë03 Apr ‘03 Jul ‘03 Oct ‘03 Jan ‘04 Apr ‘04 Jul ‘04 Oct ‘04 Jan ‘05 Apr ‘05 Jul ‘05 Oct ‘05 Jan ‘06

Ann

ual G

row

th

Growth - Quarter vs Quarter previous Year

Average Growth of Last 3 Years = 6.9%

Growth - Month vs Month Previous Year

-10%

-5%

0%

5%

10%

15%

1999 2000 2001 2002 2003 2004 2005

Air Freight Growth (IATA) and World Trade Growth

annual growth rates WTO Trade

IATA FTK

Top-10 Exporters2005 export and import in ...

0

500

1000

1500

2000

EU USA China Japan Canada Korea Russia Mexico Taiwan Saudi Arabia

export

import

Bill

ions

US

$

Growth of Semiconductor Market and IATA

60%

40%

20%

0%

-20%

-40%

-60%

Jan ‘99 Jan ‘00 Jan ‘01 Jan ‘02 Jan ‘04Jan ‘05 Jan‘05 Jan ‘06

Semiconductor shipments - LH ...

IATA FTK - RH scale

25%

20%

15%

10%

5%

0%

-5%

-10%

-15%

-20%

-25%

Semiconductors shipments IATA FTK

Airports with Largest Increase in Freight ...

350,000

300,000

250,000

200,000

150,000

100,000

50,000

-Hong Kong Shanghai Dubai Paris CDG Frankfurt Guangzhou Beijng Bangkok Louisville Singapore

2005

incr

ease

in t

onne

s

China

IATA: Major Freight Flows2004 data from IATA WATS and Forecast

Europe - Latin America

Europe - Africa

Europe - Middle East

North America - Latin America

North Atlantic

Europe - Asia Pacific

Trans - Pacific

Intra - Asia/Pacific

IATA WATS

IATA Forecast

tonnes (000)

0 1000 2000 3000 4000 5000 6000 7000

Figure 1

Figure 2

Figure 3

Figure 4

Figure 5

Figure 6

SO, YOUWANT TO

BUY APORT, EH?

in the US;Security of China operating port terminals in theUS;Security of Emirates Airlines operating a cargo ter-minal at JFK.The legislators also seem to have overlookedInchcape Shipping Service, which provides foodand fuel to US Navy Ships at ports around theworld under a US$50-million, five-year contract. Itis owned by Istithmar PJSC, an investment housebased in the UAE..

UNA BUONA IDEA?

Why not give the US ports back to the mafia? AsksDeanne Stillman in a blog on The Huffington Post.“In World War II, the feds handed security for thePort of New York over to Lucky Luciano. So what ifthey had to spring him from the joint in exchangefor protection? The plan worked - German U-boatsnever landed at Battery Park and if they tried - well,fuhgeddaboutit. Now is not the time to break withtradition. Let’s keep homeland security in lafamiglia.Someone quickly reminded Deanne that it took the

Published by

AF-KL Cargo Communication

P.O. Box 7700

1117 ZL Schiphol

The Netherlands

Christelle Dufour Theuws

Kirsten Hemmer

Concept & Realization

vdBJ Communicatie Groep,

Bloemendaal

The Netherlands

www.vdbj.nl

Editor in Chief

Mark W. Lyon

Project Manager

Urtha Ririhatuela

Art Direction

Sok Visueel Management

Amsterdam, the Netherlands

Editorial Office

Vijverweg 18

2016 GX Bloemendaal

The Netherlands

Tel.: +31(0) 23 541 17 01

Fax: +31(0) 23 541 18 01

Circulation Manager

Herman Brijssinck

Tel.: +32 2752 90 51

Fax: +32 2751 77 59

AF-KL Cargo © June 2006

Volume 21 Number 25

30 cargovision | JUNE 06 cargovision | JUNE 06 31

Cargovision is the management magazine of AF-KL Cargo. Its function is

to disseminate information on transport, distribution, logistics, informa-

tion services, and general business developments. The editorial opinions