Card vs Mobile Who Wins in Nigeria

25

Cards vs. Mobile Payment vs. Mobile Money Who will Win? Presented by David Olatilo * Presented at InterSwitch Nigeria on May 09 2012 Victoria Island, Lagos

-

Upload

david-olatilo -

Category

Documents

-

view

201 -

download

2

Transcript of Card vs Mobile Who Wins in Nigeria

Cards vs. Mobile Payment vs. Mobile Money

Who will Win?

Presented by David Olatilo

* Presented at InterSwitch Nigeria on May 09 2012 Victoria Island, Lagos

OutlineCard Payment In Nigeria

Opportunities

Our Present State (Achieved)

Why we are here (Challenges)

Positioning Card to Win (Way Forward)

Mobile Payment/Money In Nigeria Opportunities

Our Present State (Achieved)

Why we are here (Challenges)

Positioning Mobile to Win (Way Forward)

Who Wins (Verdict)

Conclusion

Electronic payment are becoming an increasingly important part of our daily life worldwide –consumers, businesses and governments.The Nigerian e-payment industry has grown significantly over the last two decades, resulting in a fair penetration of ATM usage within the economy, as well as card payments and the entrance of mobile payments. These developments and progress are exemplified by the following facts:

MasterCard, one of the most notable e-payment brands globally has identified Nigeria as a top market in its report on top 10 sub-Saharan markets

Impressive growths in deployment of POS terminals as well as ATM machines around the Country

The Central bank’s redoubled emphasis on electronic payments through issuance of guidelines and policies to facilitate transactions also the cash-lite project.

However, all this notwithstanding the Industry remains underdeveloped relative to where it ought to be given its market potential.

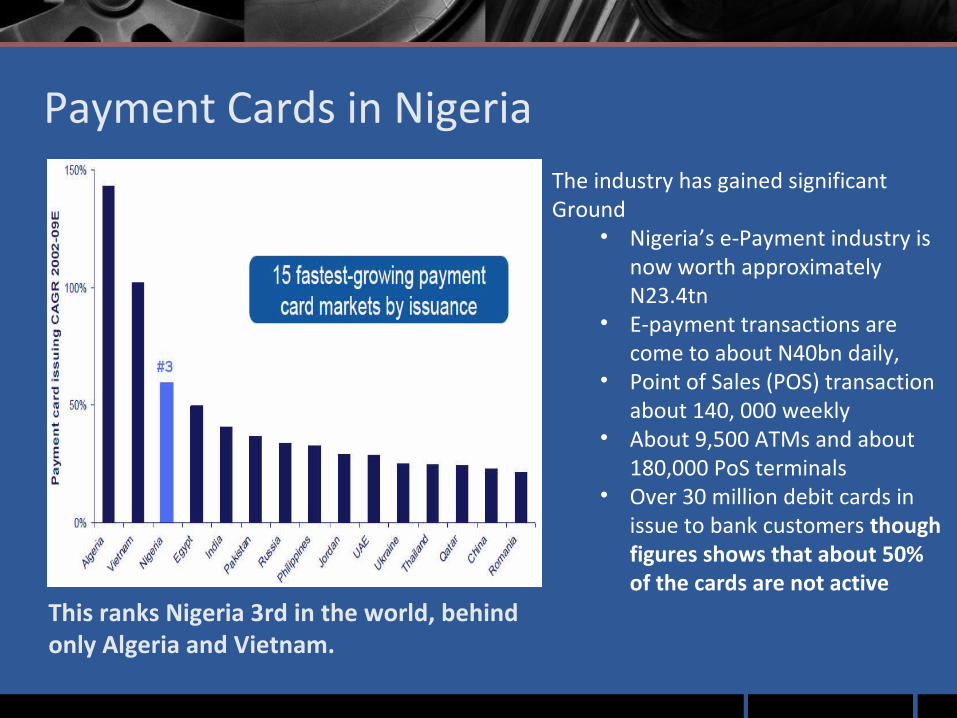

Payment Cards in Nigeria

This ranks Nigeria 3rd in the world, behind only Algeria and Vietnam.

The industry has gained significantGround

• Nigeria’s e-Payment industry is now worth approximately N23.4tn

• E-payment transactions are come to about N40bn daily,

• Point of Sales (POS) transaction about 140, 000 weekly

• About 9,500 ATMs and about 180,000 PoS terminals

• Over 30 million debit cards in issue to bank customers though figures shows that about 50% of the cards are not active

Penetration of Card in Nigeria

Card issuance viewed in terms of levels of adoption relative to total population size, it may be seen that the levels of penetration remain quite low in Nigeria

When compared to other nations, there is significant opportunity to improve the level of card penetration in Nigeria

Country Number of Cards* (millions)

Adult Population(15-64 years)

GDP(estimate)

Card Penetration(per 100,000 adults)

Brazil 424 134,337,024 $2.041 trillion $315,624

Spain 49 31,345,019 $1.379 trillion 156,325

South Africa 36 32,313,792 $512.2 billion 111,408

India 154 754,308,456 $3.736 trillion 20,416

China 1,999 959,031,874 $8.95 trillion 208,439

Ghana 0.32 14,409,184 $36.53 billion 2,241

Mexico 38 72,654,880 $1.485 trillion 52,302

USA 1174 207,856,018 $14.33 trillion 564,814

UK 168 41,835,808 $2.154 trillion 401,570

Nigeria 30*** 90,480,624 $506.2 billion 16,572

Data Sources: EuromonitorInternational, CIA World Factbook(July 2012 estimate)

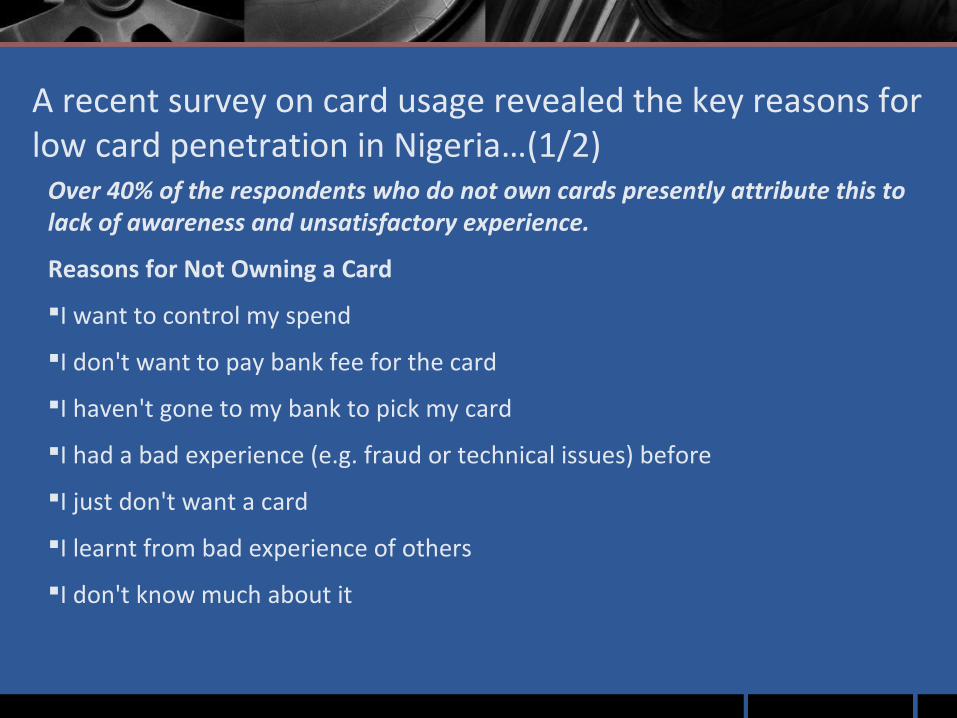

A recent survey on card usage revealed the key reasons for low card penetration in Nigeria…(1/2)

Over 40% of the respondents who do not own cards presently attribute this to lack of awareness and unsatisfactory experience.

Reasons for Not Owning a Card

I want to control my spend

I don't want to pay bank fee for the card

I haven't gone to my bank to pick my card

I had a bad experience (e.g. fraud or technical issues) before

I just don't want a card

I learnt from bad experience of others

I don't know much about it

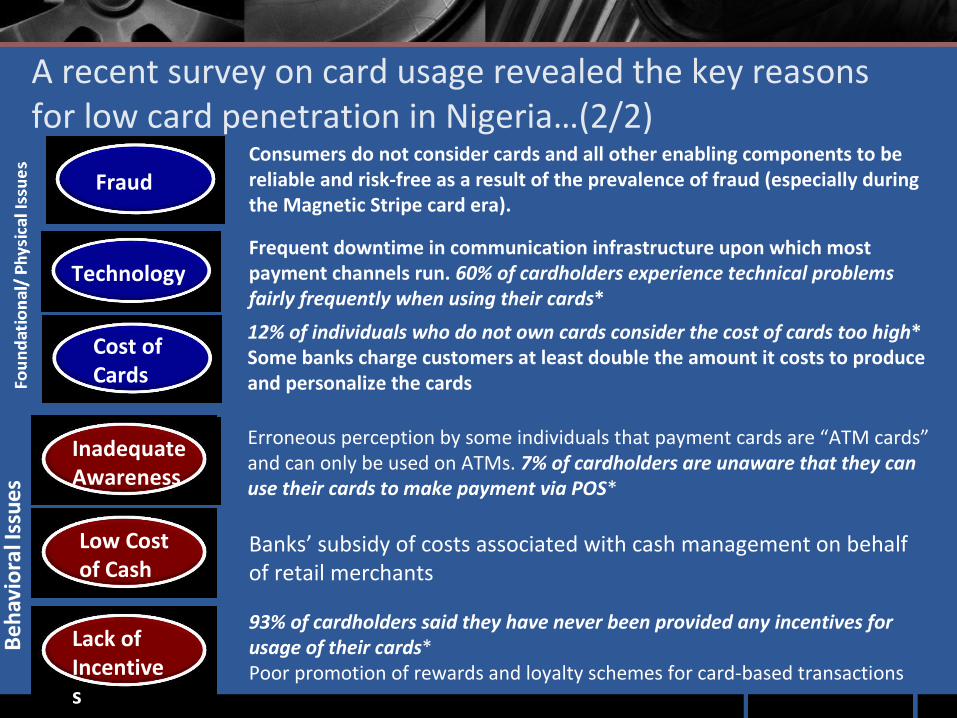

A recent survey on card usage revealed the key reasons for low card penetration in Nigeria…(2/2)

Fraud

Technology

Cost ofCards

InadequateAwareness

Low Costof Cash

Lack ofIncentives

Consumers do not consider cards and all other enabling components to be reliable and risk-free as a result of the prevalence of fraud (especially during the Magnetic Stripe card era).

Frequent downtime in communication infrastructure upon which most payment channels run. 60% of cardholders experience technical problems fairly frequently when using their cards*

12% of individuals who do not own cards consider the cost of cards too high*Some banks charge customers at least double the amount it costs to produce and personalize the cards

Erroneous perception by some individuals that payment cards are “ATM cards” and can only be used on ATMs. 7% of cardholders are unaware that they can use their cards to make payment via POS*

Banks’ subsidy of costs associated with cash management on behalf of retail merchants

93% of cardholders said they have never been provided any incentives for usage of their cards*Poor promotion of rewards and loyalty schemes for card-based transactions

Credit Card Penetration against Market Potential in Developing Market

It is very evident that there is huge opportunity in our market and a lot need to be done to achieve this

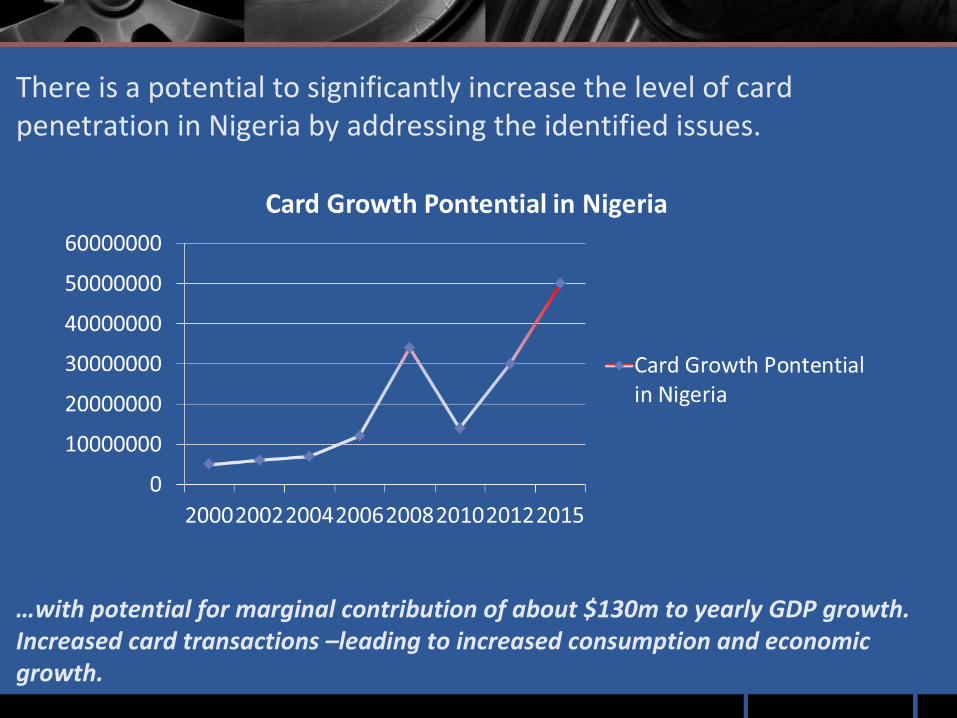

There is a potential to significantly increase the level of card penetration in Nigeria by addressing the identified issues.

…with potential for marginal contribution of about $130m to yearly GDP growth. Increased card transactions –leading to increased consumption and economic growth.

Areas of Business Potential for Cards Micro-Finance Banks and Institutions

Transport, Insurance and Education

Credit and Prepaid Cards

Fleet Card (gasoline, diesel and vehicle maintenance)

Contactless functionality Cards/Technology

Drive Online transaction (very low in Nigeria)

Market research need to be carried out tounlock more market potentials/opportunities

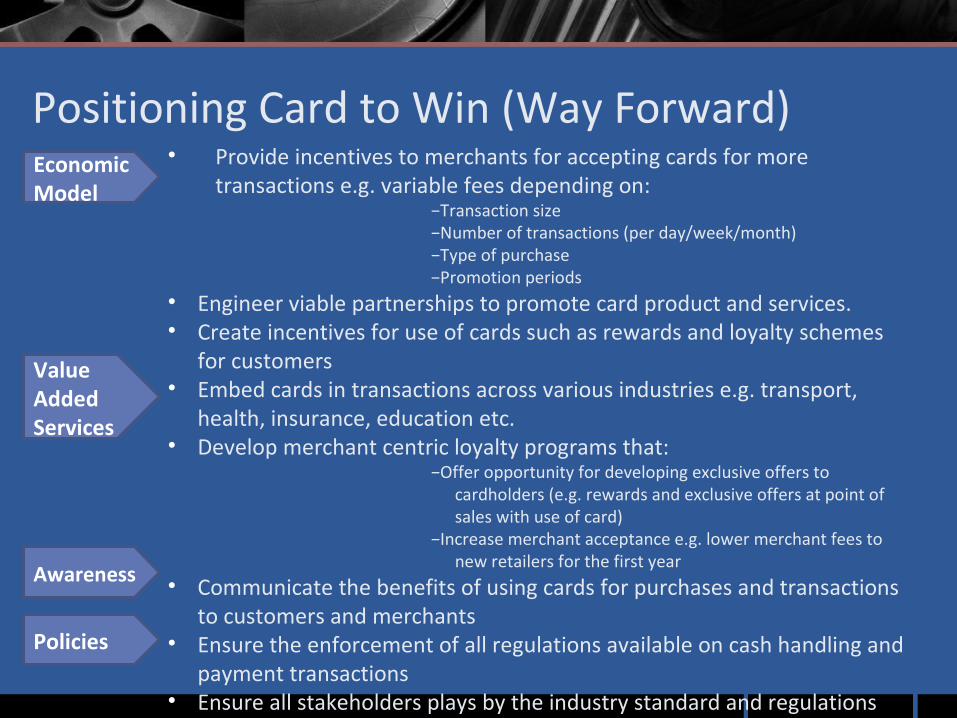

Positioning Card to Win (Way Forward)• Provide incentives to merchants for accepting cards for more

transactions e.g. variable fees depending on:−Transaction size−Number of transactions (per day/week/month)−Type of purchase−Promotion periods

• Engineer viable partnerships to promote card product and services.• Create incentives for use of cards such as rewards and loyalty schemes

for customers• Embed cards in transactions across various industries e.g. transport,

health, insurance, education etc.• Develop merchant centric loyalty programs that:

−Offer opportunity for developing exclusive offers to cardholders (e.g. rewards and exclusive offers at point of sales with use of card)

−Increase merchant acceptance e.g. lower merchant fees to new retailers for the first year

• Communicate the benefits of using cards for purchases and transactions to customers and merchants

• Ensure the enforcement of all regulations available on cash handling and payment transactions

• Ensure all stakeholders plays by the industry standard and regulations

Economic Model

Policies

Awareness

Value Added Services

Positioning Card to Win (Way Forward)• All POS terminals and ATMs and other channels should be configured to

become EMV compliant or other best security standard available

• Strict security and safety measures should be ensured at all levels of transactions

• Payment infrastructure must be given adequate attention in terms of provision and maintenance

• Deploy contactless technology (i.e. POS equipment and contactless capable cards) to fasten payment process and improve customer experience

• Use of Innovative technology that conforms with our unique market requirement

Security

Technology/Infrastructure

Mobile Payment/Money Services

In Nigeria

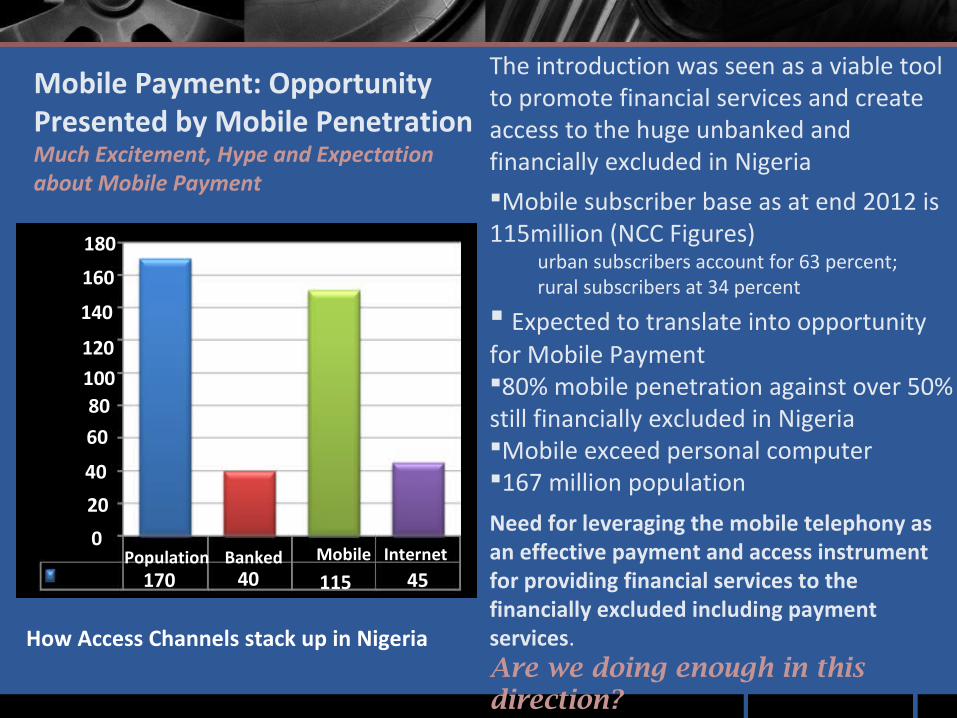

Population 170

Banked 40

Mobile

115 Internet

45

How Access Channels stack up in Nigeria

180

160

140

120

0

20

40

60

80100

Mobile Payment: Opportunity Presented by Mobile PenetrationMuch Excitement, Hype and Expectation about Mobile Payment

The introduction was seen as a viable tool to promote financial services and create access to the huge unbanked and financially excluded in NigeriaMobile subscriber base as at end 2012 is 115million (NCC Figures)

urban subscribers account for 63 percent;rural subscribers at 34 percent

Expected to translate into opportunity for Mobile Payment80% mobile penetration against over 50% still financially excluded in NigeriaMobile exceed personal computer 167 million population

Need for leveraging the mobile telephony as an effective payment and access instrument for providing financial services to the financially excluded including payment services. Are we doing enough in this direction?

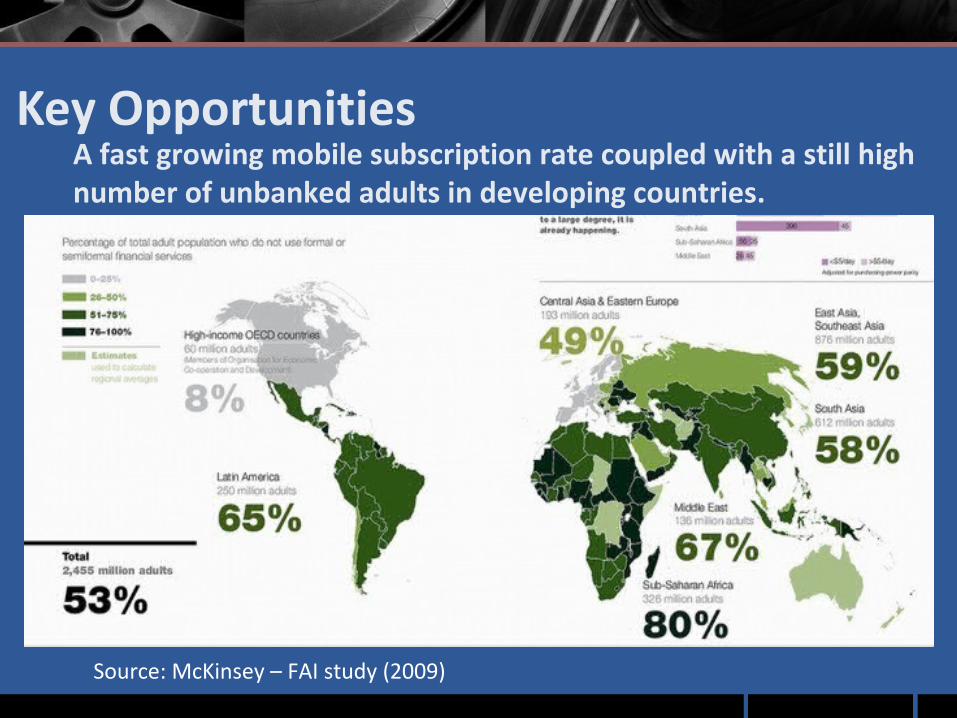

Key Opportunities

Source: McKinsey – FAI study (2009)

A fast growing mobile subscription rate coupled with a still high number of unbanked adults in developing countries.

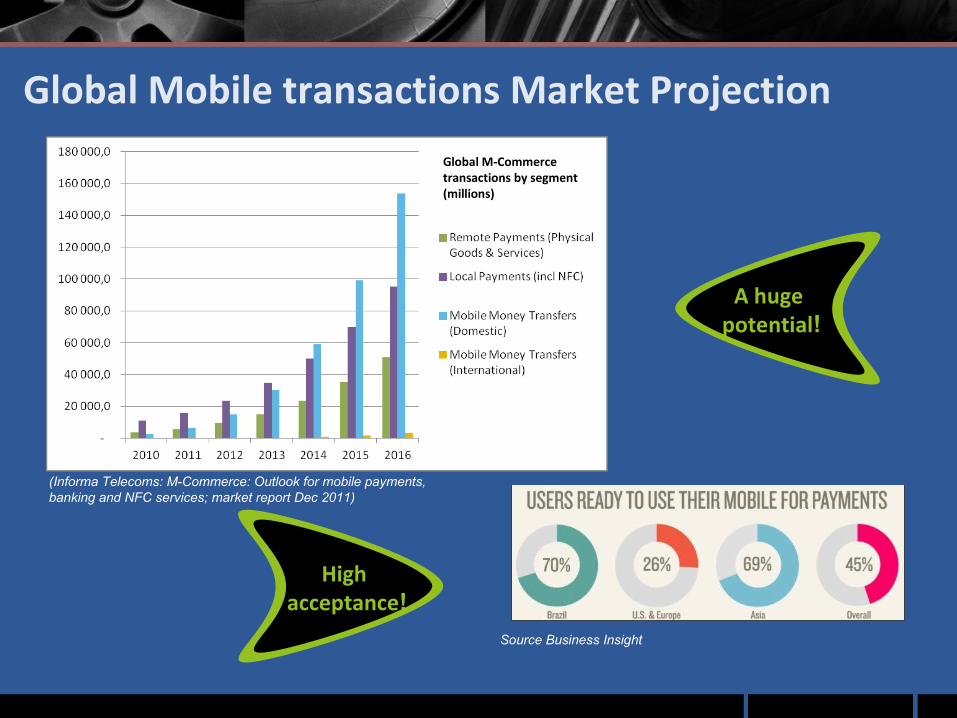

Global Mobile transactions Market Projection

(Informa Telecoms: M-Commerce: Outlook for mobile payments, banking and NFC services; market report Dec 2011)

Global M-Commerce transactions by segment (millions)

Source Business Insight

High acceptance!

A huge potential!

Mobile Payment Now Where We Are:

Slow Adoption Services are yet to achieve significant traction. Most of the licensed operators not in the market Only 4 operators active in the market According to EFIna since launched just 400,000

users against over 100m mobile users 3,000 Agent against 250, 000 needed (One

Network) Mobile Payment /Money services amongst this

huge base of subscribers is, however, very low. Less than 1% of existing bank customers use

mobile payment services High expectation without proper strategy for

penetrating the market. Much emphasis on M-Pesa success while

forgetting that MP is not Cut & Paste for success Failure of market research or pilots prior to

implementing MPS.

Challenges to Mobile Payment in Nigeria Regulatory and Policy Issues

Lack of Awareness

Interoperability

Poor Agent Network

Lack of Value Proposition

Infrastructure

MNOs Apathy

Faulty Business Model and Inadequate Market understanding

Lack of Industry Cooperation

Guiding Principles to Win

Have all 10 on the same screen and give talking points. No two market environments are exactly the same

Business models are not always easily transferable

What works in a particular country at a particular point in time is not necessarily replicable in another

Do not copy & pasteDo not copy & paste

Understand your market environmentUnderstand your market environment

Communicate, communicate, communicateCommunicate, communicate, communicate

Choose your implementing partner wiselyChoose your implementing partner wisely

Have all 10 on the same screen and give talking points. No two market environments are exactly the same

Business models are not always easily transferable

What works in a particular country at a particular point in time is not necessarily replicable in another

Invest time in developing your distribution networkInvest time in developing your distribution network

Test your productTest your product

Monitor your productMonitor your product

Collaborate with regulatorsCollaborate with regulators

Guiding Principles to Win

Who Wins? (Verdict)

“The best way to predict the future is to invent it’’

Alan Kay

Who Wins?Much Expectation, Hype and Speculation in the Industry of late on Mobile Payment, Financial Inclusion, Cash-lite Project etc.

Fact:

Much yet to be achieved

Opportunities (earlier highlighted) still huge

My Submission is that:

It is far too early to be looking for a winner

Much attention should be on addressing the issues impeding our market

Service providers must put in place effective market driven strategies which will ensure business objectives success (win)

Conclusion Stakeholders must agree that the market potential will not be achieved if

the industry is left to grow naturally, without some conscious efforts to drive growth

WIN – WIN STRATEGIES for Service Provider (InterSwitch)

Conscious effort to be competitive and sustain LEADERSHIP

Innovative, Dynamic, Market Driven, Best Practice and Strategic

WIN – WIN STRATEGIES for the INDUSTRY Government and Private sector driven policy directions to encourage e-payment

Conscious change in psychology among industry players to adopt a posture of Coopetition rather than competition

Improving Value propositions to e-payment users

Conscious effort to drive awareness in the market place

Focused drive to reverse infrastructure gap vis a vis ePayments

Business and Operational Strategies