Carabao Group Public Company...

28

0 Strictly Private & Confidential Carabao Group Public Company Limited Opportunity Day FY17 Mar 2018

Transcript of Carabao Group Public Company...

00

Strictly Private & Confidential

Carabao Group Public Company LimitedOpportunity Day FY17

Mar 2018

11

DisclaimerThe provision herein does not constitute legal advice or investment opinions of any kind, neither is it intended as anoffer, solicitation for Carabao Group PCL. (“CBG” or “The Group”). The information presented within this material isintended to indicate the Group’s operational and financial position at a given period of time and to be used,downloaded, and distributed for analyst briefings, and general meetings with CBG, and to be used for educationalmaterial in order to understand CBG’s operation only. The Group makes no representation that all information iscomplete and accurate for the purpose of producing a projection of CBG’s operations, performance, or financial positionand may be susceptible to uncertainty and important changes based on political, economic, strategic, and other suchuncontrollable factors. Forward looking statements in this presentation are based on the management’s assumption inlight of information currently available and obtainable, as well as the aforementioned/unmentioned risks anduncertainties. CBG’s actual results may vary materially from those expressed or implied in its forward-lookingstatements, and no assurance is made as to whether such future events will occur. The Group accepts no liabilitywhatsoever for any loss arising directly or indirectly from the use or endorsement of any information contained hereinby any users and/or third parties.

22

2017 Business Highlights &2018 Looking Forward

33

2017 Performance Analysis: With VS Without ICUKICUK and Global Football Sponsorship: a strategic investment to build our footprint in global stage

Ex-ICUK & football sponsorship vsIncl. ICUK (Proportionate to 51% CBG’s stake holdings) & CBG’s portion of sponsorship

44

Non-ICUK profitability –domestic business (1/3)Portfolio expanded and new product groups took turn serving as the key driver to domestic sales growth in 2017• New product groups i.e. other branded products and 3rd-party products led the way to an 18.6%

increase yoy, accounting for 22.3% of domestic sales

• Wider range of 3rd-party products alone pushed sales up THB 310mn yoy, thanks to the white spirit

• Channel-wise, cash van turned in a powerhouse where most of the growth and pricing upside are driven through

Non-ICUK profitability –domestic business (1/3)

2015

Domestic

Sales

Energy

Drinks

Sports

Drinks

Other

Branded

Products

3rd-party

Products

2016

Domestic

Sales

5,477

614 51 238 195

6,576

By Products as a % of FY2015 Domestic Sales

100.0% 11.2% 0.9% 4.3% 3.6% 120.1%

Branded

OWN,

93.4%

Branded

OEM,

3.6%

3rd-party

Products,

3.0%

2016

Domestic

Sales

Energy

Drinks

Sports

Drinks

Other

Branded

Products

3rd-party

Products

2017

Domestic

Sales

6,576

41

(99)

699 606

7,822

By Product as a % of FY2016 Domestic Sales

100.0% 0.6% -1.5% 10.6% 9.2% 119.0%

Branded

OWN,

77.8%

Branded

OEM,

12.0%

3rd-party

Products,

10.3%

Note: Pie charts represent annual sales derived from individual product groups as a % of domestic sales in respective finanical reporting period

55

Non-ICUK profitability –domestic business (2/3)Strategic diversification and growth potential are the two compelling factors weighed positively against possible drop in near-term gross profits margin• Fast growing products namely coffee and white spirit came to shoulder our own energy drinks that

had been faced with rising production costs over the year

• 3rd-party products were blended with differing margin and their return are considered accretive

37.0% 31.3%38.8% 39% 28% 16% 16% 37% 28% 13% 12%

2015

Domestic

GP

Energy

Drinks

Sports

Drinks

Other

Branded

Products

3rd-party

Products

2016

Domestic

GP

2,123

221 18 38 31

2,430

By Products as a % of FY2015 Domestic Gross Profits

100.0% 10.4% 0.8% 1.8% 1.4% 114.5%

2016

Domestic

GP

Energy

Drinks

Sports

Drinks

Other

Branded

Products

3rd-party

Products

2017

Domestic

GP

2,430

(97) (28)

79 63

2,447

By Product as a % of FY2016 Domestic Gross Profits

100.0% -4.0% -1.2% 3.3% 2.6% 100.7%

Energy

Drinks

95.5%

Sports

Drinks 1.7%

Branded

OEM 1.5%

3rd-party

Products 1.3%

Energy

Drinks

90.9%

Sports

Drinks 0.6%

Branded

OEM 4.8%

3rd-party

Products 3.8%

Note: Pie charts represent annual gross profits from individual product groups as a % of total gross profits in respective finanical reporting period

66

Non-ICUK profitability –domestic business (3/3)Energy drinks were put under margin pressure due to rising costs of amber glass container and sugar content despite our modest gain from the new excise tax regime

• New excise tax regime booked us with cost saving of 0.11 THB for every bottle sold domestically at least until 2 years from now

• Our cluster of vertically integrated manufacturing units in Bangpakongintended to reduce energy and operating costs going forwards

• Sugar price set free in line with global market mechanism has tendency to benefit us

• Amber glass bottle became more costly due in large part to increased price of cullet and hit gross profits margin by 1-2%

• We expect depreciations to total +500 THBmn in 2018, up from 263 THBmn in 2017

+

-

+

-

+

77

Export Business ProfitabilityExport sales made a further jump on the back of both existing and new markets• CLMV soared a further 29.4% growth, led by Cambodia that broke record high during the last quarter

with volume sold up from 28 to 40 million cans sold in Dec

• China market shining out with a total of 1,019 THBmn in export sales this year is expected to play a vital role tin and by all means

2016 Export Sales CLMV China Other Existing

Markets

Export by CBD Export by ICUK 2017 Export Sales

3,356

747

1,019

(286)

187

5,024

By country as a % of FY2016 Export Sales

100.0% 22.3% 30.4% -8.5% 5.6% 149.7%

1,481

44.1%

CBD

96.0%ICUK

4.0%

CLMV

65.6%

China

20.3%

Afghanistan

& Yemen

9.6%

UK and Outside

Asia 4.0%Others,

0.5%

Note: Pie charts represent annual sales derived from key export markets as a % of export sales in respective finanical reporting period

88

2017 SG&A Analysis - Conso

Marketing (THBmn)Sponsorship +413 (Non-ICUK THB 30mn, ICUK THB 393mn)

Above-the-line Mktg +40 (due to initial launch of branded coffee products = 68 THBmn)

Listing Fee (ICUK) +54

Other marketing expenses (ICUK) +156

Selling (THBmn)Cash Van Expenses +c.100

Admin (THBmn)Services & Fees Expenses +54 (due to Consulting Fees 15 THBmn)

Moving & re-installation production lines 40 THBmn

99

China Looking-forward: 2018 Market Stimulus PlanPOS and Marketing Plan

Business Status:

26 Branches (Up by 2 Branches)

c. 900 Staffs

Marketing Timeline

1010

China Looking-forward: 2018 Focusing Strategy8-3-3-3 Strategy

1. Fuzhou

3. Putian

2. Nanping

Fujian

1111

2017 UK Development

Current Customers

Increasing visibilities prompt us to move on to the next step

Q1 2017 Q2 2017

Q3 2017 Q4 2017

2016

More facings in modern trade channels

1212

UK Looking-forward: 2018 Investment Phase to create fansPotential Customers

2018

- Listed in Jan’18

- To be on-shelf in Apr’18

- In negotiation

on shelf (F)

2Q2018

Product Differentiations

Continue our distinguish position of successful flavours initiation

Mandarin Orange

Engaging Marketing Campaign:

To match digital-lifestyle consumers with reasonable expenses

The Bonkers Drink for Bonkers Lives

- To be listed in Jul’18

NEW

1313

UK Looking-forward: Driving Stronger Sales with Push & PullPUSH

Retail Wholesales

1414

UK Looking-forward: Driving Stronger Sales with Push & PullPULL

1515

Global Marketing Platform

Looking-forward: 2018 Continue to utilize our global asset investments

Potential Export Countries

Windows of opportunity are widening thanks to Carabao Cup

Status: Done

Australia

KSA (Arabian Region)

Received Interest

Philippines

From CBD

Status: Early Negotiation

Turkey

Nigeria

India

Honduras

Nepal

Status: Done

Azerbyjan

Ghana

France

Peru

Received Interest

Macedonia

From ICUK

Status: Early Negotiation

Germany

Belgium/Netherland

Balkans Region

(Slovenia, Croatia, Bosnia)

Denmark

Romania

Switzerland/ Austria

Senegal

1616

Production facilitiesready for larger sales of Carabao energy drink in both domestic and export markets

2017 Business Highlights

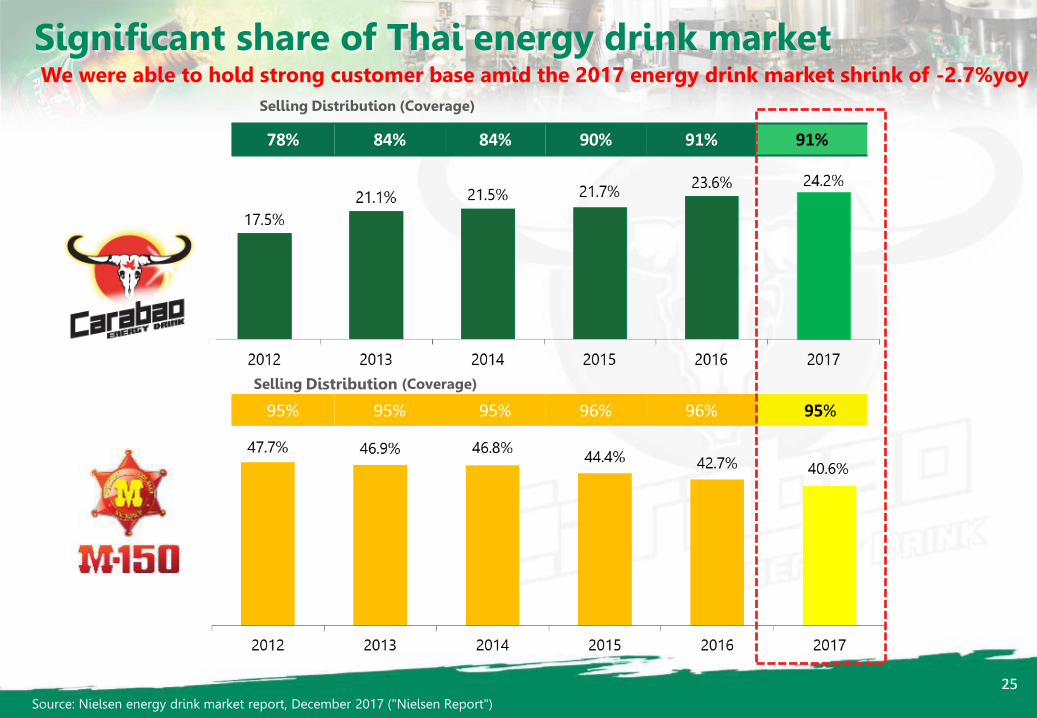

Carabao Dang hold a strong customer base (+0.3%YoY) amid the Thai energy drink market shrink of -2.7%YoY

RTD Coffee received overwhelming demand reaching maximum production capacity of OEM supplier at c.8-9 million cans per month

3rd Party Productsdriven by new key product i.e. Spirits – 1st time sold in Apr’17)

Export marketsCLMV: +29% sales growth

New market: China 1st time export in Feb’17, now contributing to c. 20% of total Overseas Revenue in FY2017

ICUK Increasing visibilities in nationwide modern trades; reaching c. 20,000 POS vs 8,000 POS in FY2016

Expansion Updates:

Bottling Capacity: c.1,800 mn bottles/ year (1Q18)

Canning Capacity: c.1,400 mn cans/ year (since Dec’17)

Amber Glass Bottle Capacity: c. 1,300 mn bottles/year (since Dec’17)

Reaping Carabao Group’s Assets

Assets of CBG

Strong Brand Quality Product

Cash Van Extensive Internal

Distribution SystemBaoDang

Ladies Girls

Product Differentiation

Global Marketing Platform

1717

2018 Growth Driver

(1) According to Spirits revenue of a key player in Thailand market

Production facilitiesACM: Aluminum cans production facilities to be ready for test run by 3Q2018

Carabao DangIntegrating marketing incentives with distribution coverage

RTD Coffee new capacity of OEM supplier at c.13 million cans per month; increase market share

3rd Party Productsdriven by potential growth of key product i.e. Spirits of which the market size is THB c.80k-100k million per year(1)

Export marketsCLMV: effective consumer marketing activities implemented by the local importer and strong brand recognition

China: Increasing brand awareness to drive volume sold

New markets: Australia

ICUKNew flavours: Mandarin Orange

Increasing POS & brand recognition

New export opportunities into European, Africa and Asia regions

1818

Appendix:Detail Financial

1919

Statement of comprehensive income

Remark: G&A excludes Other Expenses

Unit: THB million 2015 2016 2016 2017 2017 Change 4Q2016 4Q2017 4Q2017 Change%sales %sales YoY %sales YoY

Revenue from sales 7,753 9,943 100.0% 12,904 100.0% 29.8% 2,837 3,181 100.0% 12.1%Costs of goods sold 4,893 6,388 64.2% 8,840 68.5% 38.4% 1,889 2,286 71.9% 21.0%Gross profits 2,860 3,555 35.8% 4,065 31.5% 14.3% 947 895 28.1% -5.6%Selling expenses 1,120 1,462 14.7% 2,379 18.4% 62.7% 500 571 18.0% 14.3%G&A expenses 395 553 5.6% 741 5.7% 33.9% 213 217 6.8% 2.0%Operating profits 1,380 1,540 15.5% 945 7.3% -38.6% 235 107 3.3% -54.6%Other incomes 121 147 1.5% 164 1.3% 11.4% 27 34 1.1% 25.6%EBIT 1,466 1,687 17.0% 1,109 8.6% -34.3% 262 140 4.4% -46.4%EBITDA 1,702 1,914 19.2% 1,372 10.6% -28.3% 319 219 6.9% -31.2%Interest expenses 2 4 0.0% 48 0.4% 1196.7% 1 19 0.6% 1277.9%EBT 1,465 1,683 16.9% 1,061 8.2% -36.9% 260 121 3.8% -53.4%Income tax expenses 209 278 2.8% 261 2.0% -6.3% 64 42 1.3% -33.5%Net profits for the period 1,256 1,405 14.1% 801 6.2% -43.0% 197 79 2.5% -59.9%

1,256 1,490 15.0% 1,246 9.7% -16.4% 282 209 6.6% -25.7%Equity Holder of the Company

2020

ASSETS Dec-16 Dec-17 Change LIABILITIES Dec-16 Dec-17 ChangeCurrent Assets Current LiabilitiesCash, Cash Equivalents 745 147 (598) Bank overdrafts&short-term loans from financial institutions 750 845 95 Current Investments 604 7 (597) Trade and other payable 1,365 1,897 532 Trade and other receivable 562 960 398 Current portion of long-term loans from financial institution - 300 300 Inventories 434 656 223 Other current liabilities 210 164 (46) Other current assets 110 389 279 Total Current Liabilities 2,325 3,207 881 Total Current Assets 2,455 2,159 (296) Long-term loan from financial institutions 250 2,190 1,940

Other non-current liabilities 104 118 14 Total non-current liabilities 354 2,308 1,954 Total Liabilities 2,679 5,515 2,836

Non-Current Assets SHAREHOLDERS' EQUITYLong-term Investment - - Issued and fully paid up share capital 1,000 1,000 - Investment Properties 104 103 (1) Premium on shares 3,963 3,963 - Property, plant & equipment 6,627 9,609 2,982 Retained earnings 1,478 1,775 297 Intangible Assets 15 67 52 Other components of shareholders' equity 433 376 - Deferred Tax Assets 34 31 (2) Equity attributable to owners of the Company 6,873 7,114 241 Other non-current assets 8 15 7 Non-controlling interests of the subsidiary 226 (108) (334) Goodwill 536 535 (1) Total Non-Current Assets 7,324 10,361 3,037 Total shareholders' equity 7,099 7,005 (94) Total Assets 9,778 12,520 2,741 Total liabilities and Equity 9,778 12,520 2,742

STATEMENT OF FINANCIAL POSITION Unit: THB million

Statement of financial position

2121

BREAKDOWN OF DOMESTIC AND EXPORT SALES

Total revenue from salesFY17 Sales growth delivered our target

2222

Breakdown of our domestic sales

DOMESTIC SALES CHANNEL CONTRIBUTION FROM CASH VAN STRATEGY

DOMESTIC: Increasing sales driven by growth of RTD coffee and 3rd party products for distribution

2323

THB mn FY15 FY16 %YoY FY16 FY17 %YoY 4Q16 3Q17 4Q17 %YoY %QoQCambodia 1,547 2,074 34% 2,074 2,489 20% 599 605 739 23% 22%Myanmar 223 279 25% 279 422 51% 99 69 126 27% 83%Vietnam 98 173 77% 173 356 106% 68 142 74 9% -48%Yemen 167 202 21% 202 225 11% 71 70 112 59% 62%Afghanistan 164 481 193% 481 257 -46% 160 62 - -100% -100%China - - - - 1,019 N/A - 407 - N/A -100%Others 77 153 99% 137 80 -42% 25 21 17 -32% -18%Sales from Thailand 2,276 3,362 48% 3,346 4,847 45% 1,022 1,375 1,068 5% -22%Sales from ICUK - - - 16 203 1179% 16 97 34 117% -65%Total 2,276 3,362 48% 3,362 5,050 50% 1,038 1,472 1,103 6% -25%

Overseas sales by key export countriesEXPORT: 4Q17 Overseas sales soften due to winter effect

2424

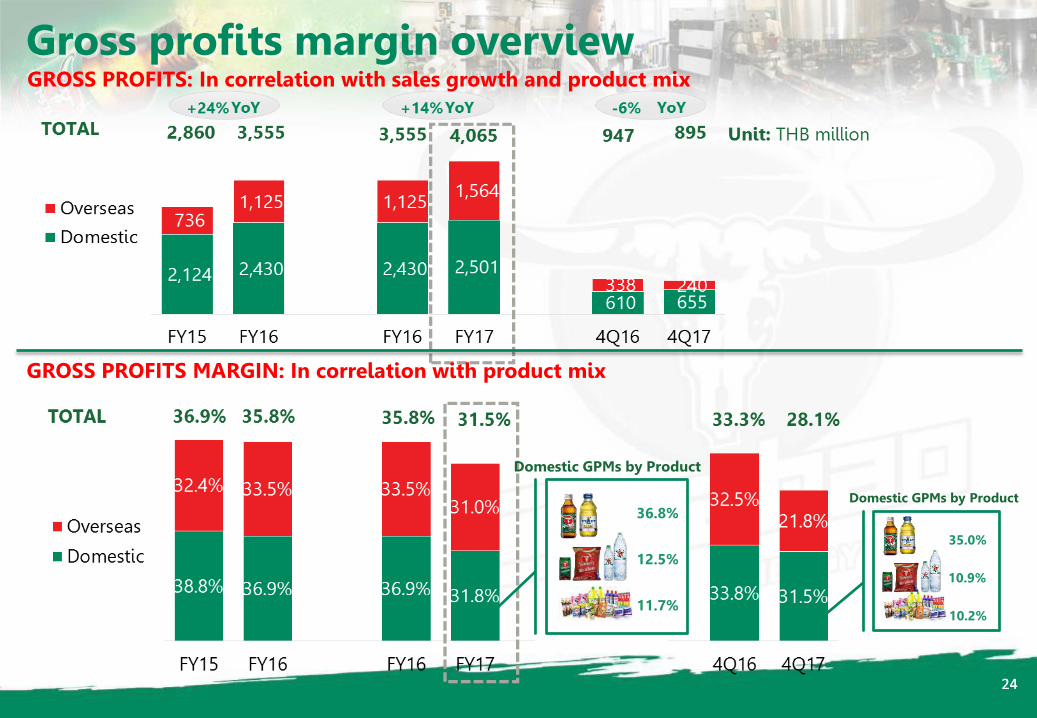

Gross profits margin overview

35.0%

10.9%

10.2%

Domestic GPMs by Product

GROSS PROFITS: In correlation with sales growth and product mix

GROSS PROFITS MARGIN: In correlation with product mix

Domestic GPMs by Product

36.8%

12.5%

11.7%

2525Source: Nielsen energy drink market report, December 2017 ("Nielsen Report")

78% 84% 84% 90% 91% 91%

Selling Distribution (Coverage)

Selling Distribution (Coverage)

Significant share of Thai energy drink market

95% 95% 95% 96% 96% 95%

We were able to hold strong customer base amid the 2017 energy drink market shrink of -2.7%yoy

2626

Thai energy drink and its geographical segmentations

Source: Nielsen energy drink market report, December2017 ("Nielsen Report")

Thai energy drink marketby geographical segmentation

Central Region

Northeast Region North Region

We successfully continued to stay ahead on the Central Region while taking steps closer to bridging the gap of share for the Northeast Region

Greater BKK,

11.8%

Central, 27.9%North,

19.7%

Northeast, 31.2%

South, 9.4%

2727

WORLD CLASS WORLD CLASS

Carabao Group Public Co., Ltd.

Tel: +66 2636 6111 Ext.882

Email : [email protected]

www.carabaogroup.com/en PRODUCT BRAND

Investor Relations