CAPITAL MARKETS BSC/BBA III Winter Semester 2010 Lahore School of Economics.

56

CAPITAL MARKETS CAPITAL MARKETS BSC/BBA III BSC/BBA III Winter Semester 2010 Winter Semester 2010 Lahore School of Economics Lahore School of Economics

-

Upload

ethan-arnold -

Category

Documents

-

view

220 -

download

1

Transcript of CAPITAL MARKETS BSC/BBA III Winter Semester 2010 Lahore School of Economics.

CAPITAL MARKETSCAPITAL MARKETS

BSC/BBA IIIBSC/BBA IIIWinter Semester 2010Winter Semester 2010

Lahore School of EconomicsLahore School of Economics

Chapter 3Chapter 3

Depository InstitutionsDepository Institutions

Depository InstitutionsLearning Objectives

What is a depository institution?

How a DI generates income?

What is the Asset/Liability problem for DI’s?

What is Funding Risk?

What are DI’s funding sources?

What are Reserve Requirements?

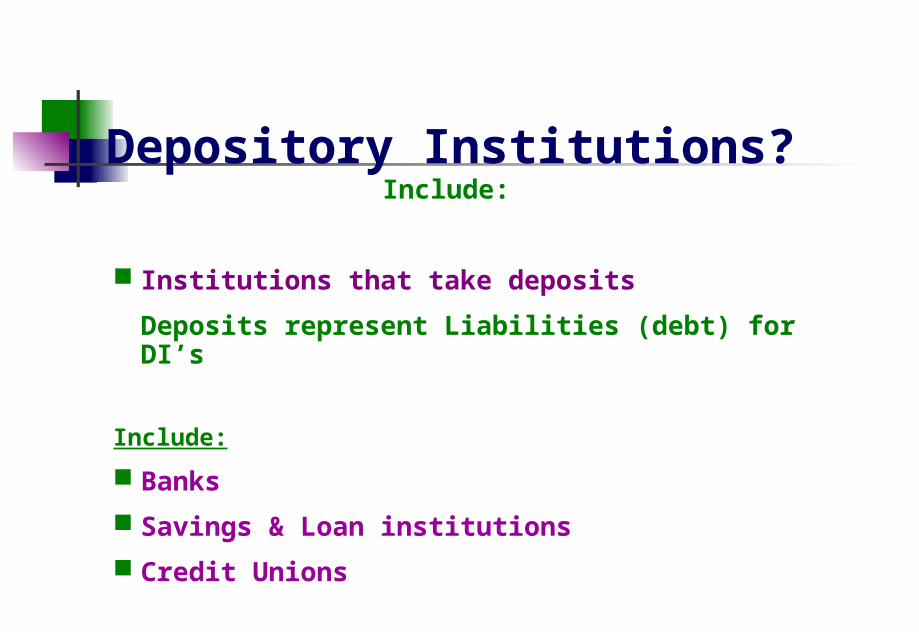

Depository Institutions?

Include:

Depository Institutions?Include:

Institutions that take deposits

Deposits represent Liabilities (debt) for DI’s

Include:

Banks

Savings & Loan institutions

Credit Unions

How do DI’s make money?

3 ways:

How do DI’s make money?3 ways:

LoansMake direct loans to entities

Securities investmentsInvesting in securities & holding portfolios

FeesCharged to their customers

Importance of DI’s?

Heavily regulated because:

Importance of DI’s?

Heavily regulated because:

Their role in financial system

a) Creating the financial playing field

Principal means of making payments

a) Individuals & Businesses use for payments

Vehicle for Govt monetary policy

a) MP implemented through banking system

Special Privileges

Access to Federal Deposit Insurance

Provision of liquidity in emergencies

Govt has interest in DI’s stability & survival…

Asset-Liability Management 2 Main problems:

Funding Risk

Liquidity Risk

Asset-Liability Management

Funding Risk:Illustrate using 100MM, 7% 1 & 10 yrs

Use of Spreads (DI’s make money)

Difference between bid/ask or charging premiums

Gaps

Open positions created due to duration differences

Interest rate exposure

Funding activity resulting in interest rate risk

Asset-Liability Management

Opportunities:

Asset-Liability ManagementOpportunities:

Interest Rate view Managers who have expectations of interest rate

changes will seek to profit from funding!

If Interest rates rise

What position should you have?

If interest rates fall

What position should you have?

Asset-Liability ManagementOpportunities:

Interest Rate view Managers who have expectations of interest rate

changes will seek to profit from funding!

If Interest rates rise

DI will benefit if it has borrowed long & lent short because when interest rates will rise its cost will remain unchanged but will be able to lend at a higher rate!

If interest rates fall

DI will benefit if it has borrowed short & lent long!

Asset-Liability Management

Threats of positioning:

Asset-Liability Management Threats of positioning:

Adverse financial consequences

If expectations are not realized, Huge losses can occur

No one can predict interest rates consistently

Highly risky

Becomes same as gambling

Long run losses highly likely

Asset-Liability Management

Main goal of Mgmt:

Asset-Liability Management

Main goal of Mgmt:

Try Locking in the spread

Minimize interest rate exposure

Various financial instruments used to manage risk

Asset-Liability Management

Main goal of Mgmt:

Try Locking in the spread

(By not trying to bet on interest rate movements, focus should solely be on earning from the spread not on interest rate movements)

Minimize interest rate exposure

(By investing in assets & Liabilities of similar maturity ranges)

Various financial instruments used to manage risk

(Examples include interest rate options, swaps & forwards)

Liquidity Concerns of DI’s?

Balancing two activities?

Liquidity Concerns of DI’s?

Balancing two activities:

Satisfy Withdrawals of customers (Liquidity Concerns)

Liquidity required

Provide Loans to customers (Earnings)

Liquidity Concerns of DI’s?

4 ways to solve liquidity issues?

Liquidity Concerns of DI’s?

4 ways to solve liquidity issues:

Attract deposits

Borrowing from Federal Agency or other Financial Institutions (using security collateral)

Sell Securities on hand

Raise Funds in Money Markets

Liquidity Concerns of DI’s?

Increase Borrowing using securities:

Discount window borrowing at Fed

Liquidity Concerns of DI’s?

Sell securities it owns:

DI must invest in ST, liquid securities with little Price Risk and keep these in its inventory

E.g: stocks?... No, Bonds? …. No

Solution: ?

Liquidity Concerns of DI’s?

Sell securities it owns:

DI must invest in ST, liquid securities with little price risk and keep these in its inventory

E.g stocks?... No, Bonds? …. No

Solution: Short term, Money Market instruments like Treasury Bills, Commercial Papers etc

Liquidity Concerns of DI’s?

SECONDARY RESERVES?

Securities held by a DI for the purpose of satisfying withdrawals or loans.

Disadvantage?

Lower yield

% of assets as secondary reserves depends on DI’s risk/return appetite

Liquidity Concerns of DI’s?

One more reason for holding liquid assets?

Liquidity Concerns of DI’s?

One more reason for holding liquid assets?

To fulfill Govt regulation!

In form of Reserve Requirements (discussed later)

Commercial Banks

3 Main Types of services:

3 Main Types of services:

Individual Banking

Institutional Banking

Global Banking

Commercial Banks

Individual Banking

Consumer Lending

Residential Mortgage

Credit Card financing

Car & Boat Financing

Brokerage services

Student Loans

Commercial Banks

Institutional Banking:

Loans to Corporations

Loans to Insurance companies

Loans to Government

Commercial Financing & Leasing

Commercial Banks

Global Banking:

Foreign Exchange products

Capital Markets products

Corporate financing products

Commercial Banks

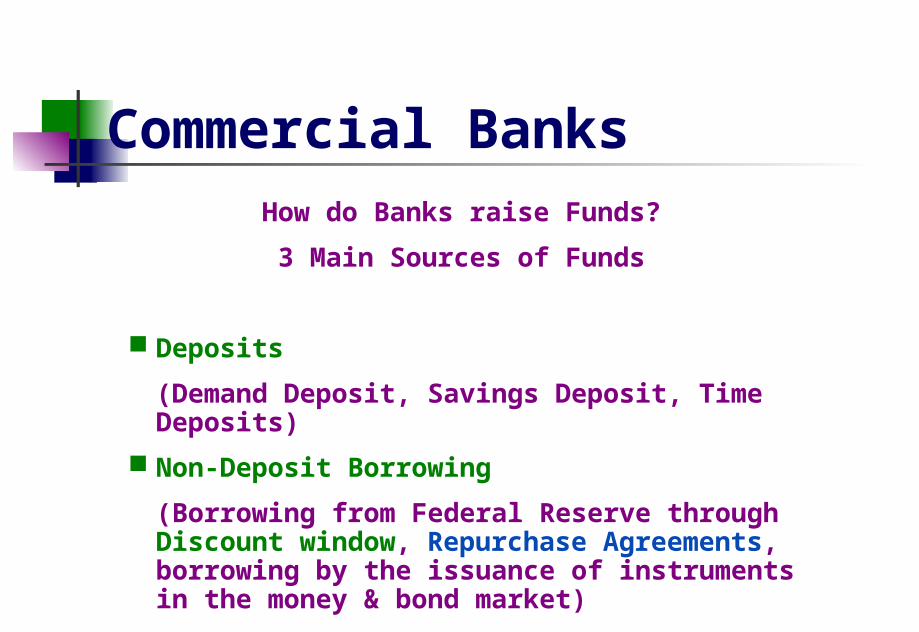

How do Banks raise Funds?

Commercial Banks

How do Banks raise Funds?

3 Main Sources of Funds

Deposits

Non-Deposit Borrowing

Common Stock & Retained Earnings

Commercial Banks

How do Banks raise Funds?

3 Main Sources of Funds

Deposits

(Demand Deposit, Savings Deposit, Time Deposits)

Non-Deposit Borrowing

(Borrowing from Federal Reserve through Discount window, Repurchase Agreements, borrowing by the issuance of instruments in the money & bond market)

Common Stock & Retained Earnings

Commercial Banks

Reserve Requirement &

Borrowing at the Fed Funds Market?

Banks must maintain a %age of deposits with Federal Reserve called Reserve Ratio.

The cash kept with Fed is called Required Reserve.

Commercial Banks

Reserve Requirement

Type of Deposits:

Transaction Deposits Non-transactions Deposits

Reserve Ratios are higher for transaction Deposits relative to non transaction deposits!

Reserve Requirements Reserve maintenance period

2 Week period where the average of the daily total of each type of deposit is taken to get RR (THR-WED)

Actual Reserves

Average Amount of Reserves held at the close of business at the Federal Reserve Bank during each day of a two week reserve maintenance period.

Excess Reserves

If bank reserves exceed the RR at the Fed

Fed Funds Market & Fed Funds

Banks short of RR borrow from Excess Reserves of other Banks at Fed Funds rate.

Fed Discount Window:

Fed is the Banker’s Bank – last resort

Charges DISCOUNT RATE

Collateral

Treasury securities, Govt securities etc.

Heavily Discourages its use

Will investigate if use becomes frequent

Reserve Requirements

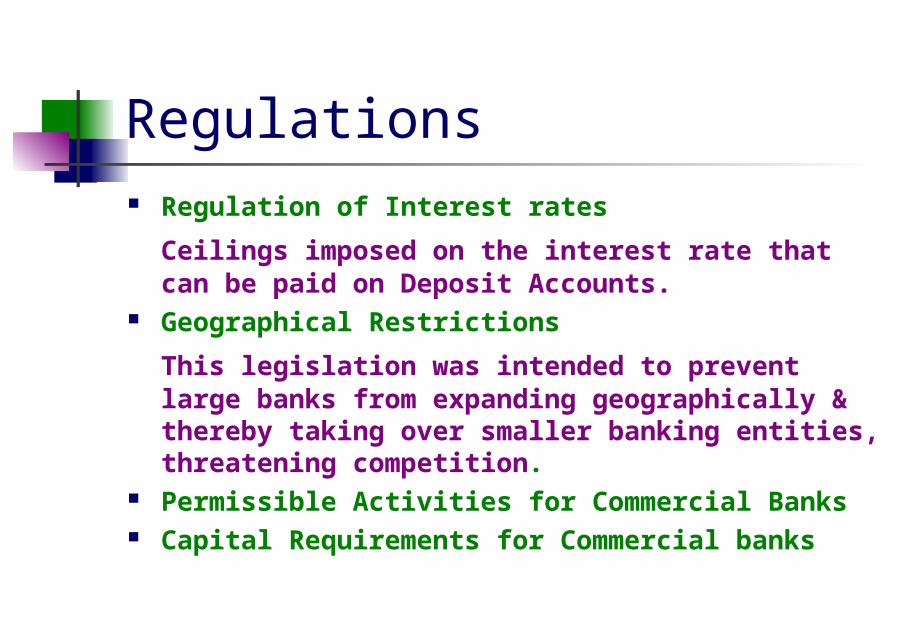

Regulations

Regulation of Interest rates Geographical Restrictions Permissible Activities for Commercial

Banks Capital Requirements for Commercial

banks

Regulations Regulation of Interest rates

Ceilings imposed on the interest rate that can be paid on Deposit Accounts.

Geographical Restrictions

This legislation was intended to prevent large banks from expanding geographically & thereby taking over smaller banking entities, threatening competition.

Permissible Activities for Commercial Banks Capital Requirements for Commercial banks

Permissible Activities for Commercial Banks

The permissible activities of banks are limited to those that are viewed by the Fed as closely “related to banking”.

Banks can neither underwrite securities & stocks, nor can act as dealers in the secondary market.

Banking act of 1933 Prohibits any depository institution from engaging in the securities business.

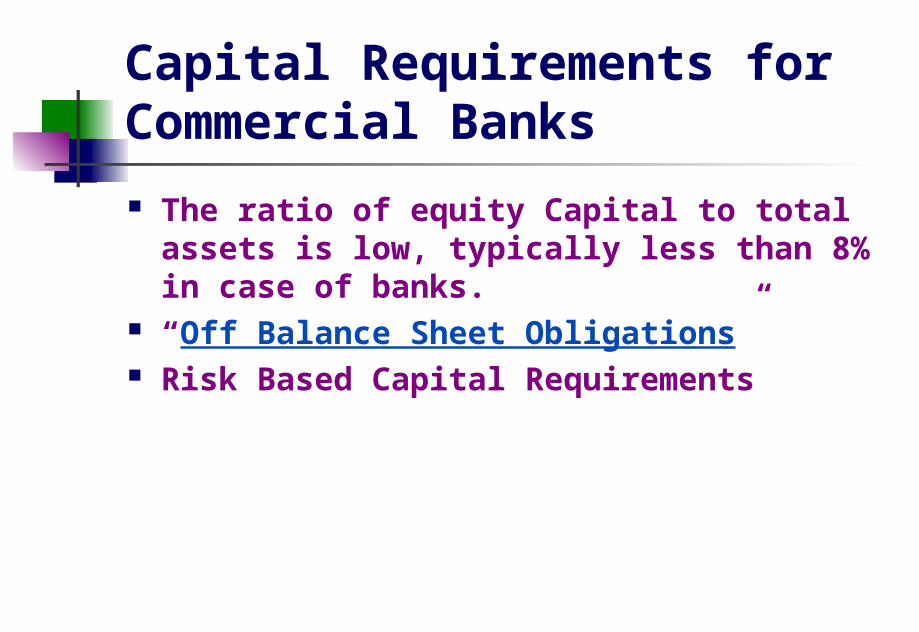

Capital Requirements for Commercial Banks

The ratio of equity Capital to total assets is low, typically less than 8% in case of banks.

“Off Balance Sheet Obligations” Risk Based Capital Requirements

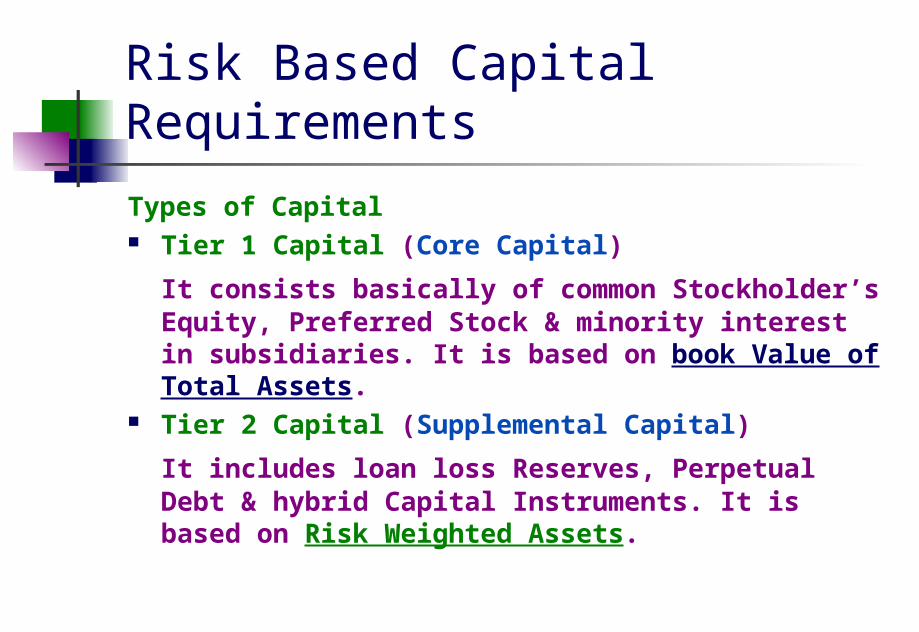

Risk Based Capital Requirements

Types of Capital Tier 1 Capital (Core Capital)

It consists basically of common Stockholder’s Equity, Preferred Stock & minority interest in subsidiaries. It is based on book Value of Total Assets.

Tier 2 Capital (Supplemental Capital)

It includes loan loss Reserves, Perpetual Debt & hybrid Capital Instruments. It is based on Risk Weighted Assets.

Risk Based Capital Requirements

Risk Weight

Examples of Assets included

0% U.S Treasury Securities, MBS issued by GNMA

20% Municipal general Obligation bonds, MBS issued by Govt. Associations

50% Municipal Revenue Bonds, Residential Mortgages

100% Commercial loans & mortgages, Corporate Bonds.

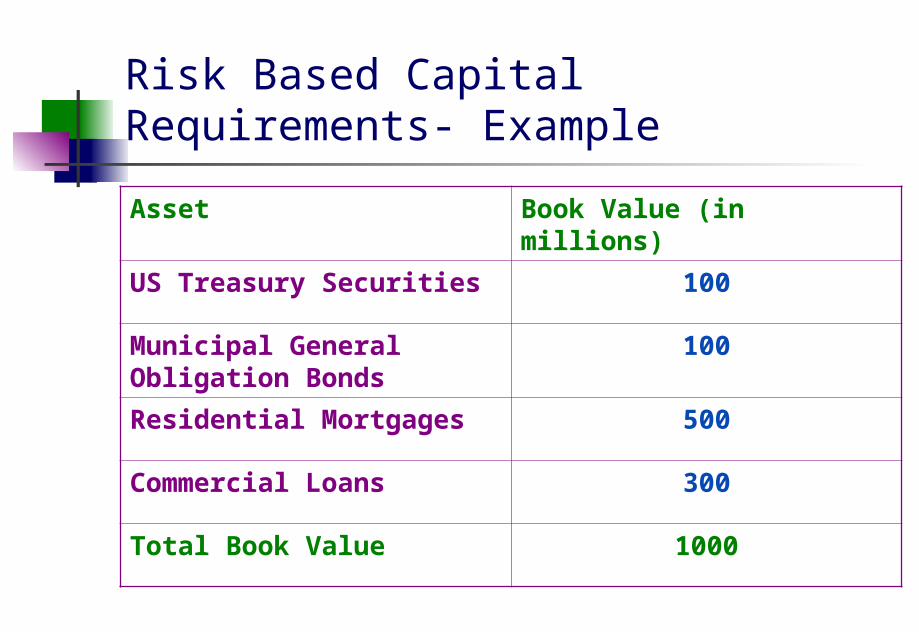

Risk Based Capital Requirements- Example

Asset Book Value (in millions)

US Treasury Securities 100

Municipal General Obligation Bonds

100

Residential Mortgages 500

Commercial Loans 300

Total Book Value 1000

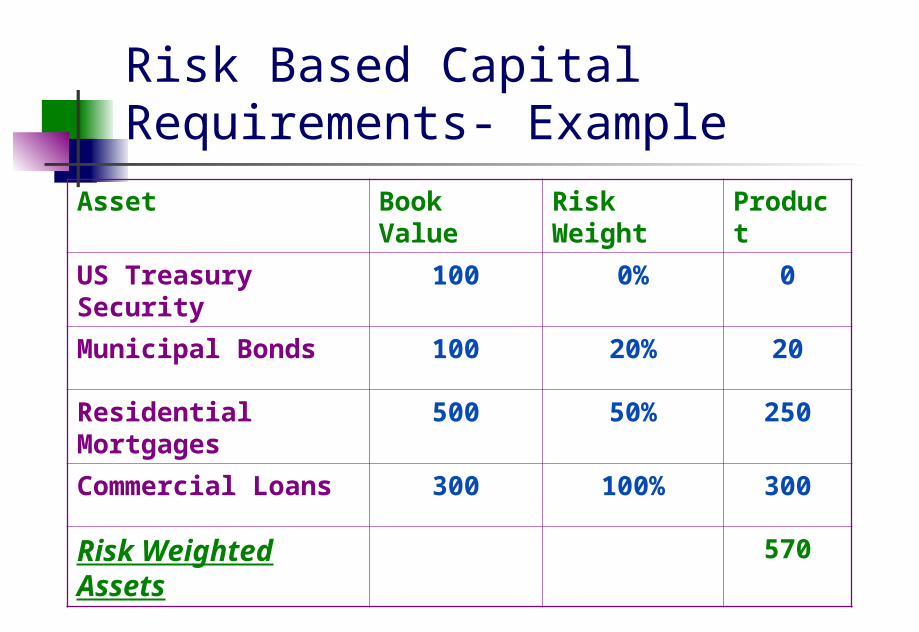

Risk Based Capital Requirements- Example

Asset Book Value

Risk Weight

Product

US Treasury Security

100 0% 0

Municipal Bonds 100 20% 20

Residential Mortgages

500 50% 250

Commercial Loans 300 100% 300

Risk Weighted Assets

570

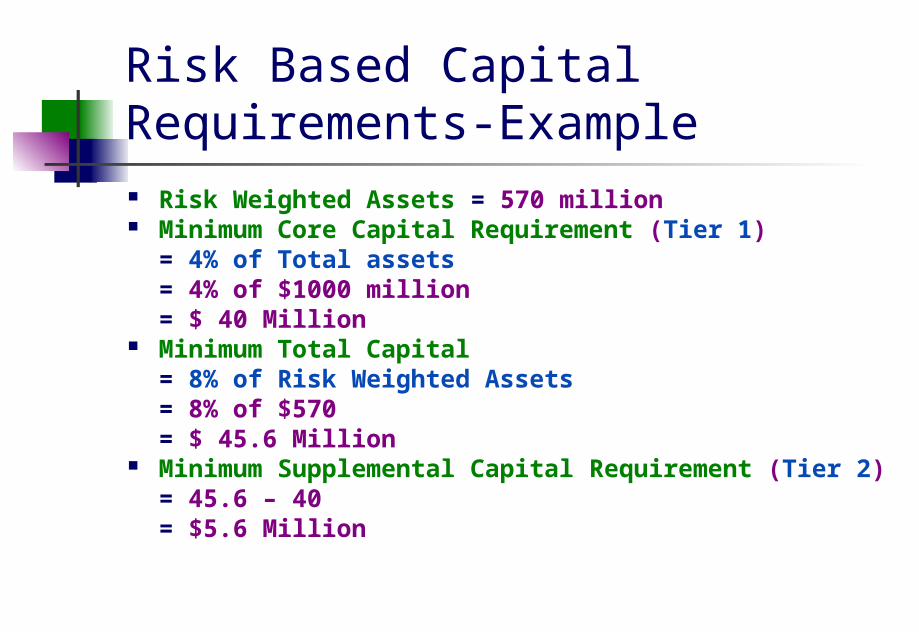

Risk Based Capital Requirements-Example Risk Weighted Assets = 570 million Minimum Core Capital Requirement (Tier 1)

= 4% of Total assets= 4% of $1000 million= $ 40 Million

Minimum Total Capital= 8% of Risk Weighted Assets= 8% of $570= $ 45.6 Million

Minimum Supplemental Capital Requirement (Tier 2)= 45.6 – 40= $5.6 Million

Depository Institutions

Summary

What is a depository institution?

How a DI generates income?

What is the Asset/Liability problem for DI’s?

What is Funding Risk?

What are DI’s funding sources?

What are Reserve Requirements?

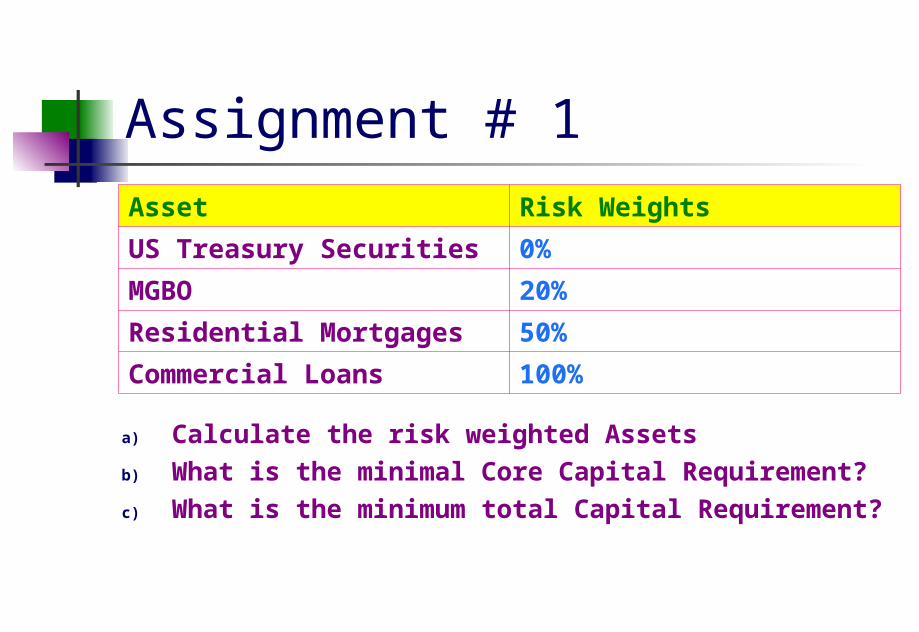

Assignment # 1

Q1: The following is the book value of the assets of a bank:

Asset Book Value (in millions)

US Treasury Securities $50

MGBO 50

Residential Mortgages 400

Commercial Loans 200

Total Book Value 700

Assignment # 1

a) Calculate the risk weighted Assetsb) What is the minimal Core Capital Requirement?c) What is the minimum total Capital

Requirement?

Asset Risk Weights

US Treasury Securities 0%

MGBO 20%

Residential Mortgages 50%

Commercial Loans 100%

Assignment # 1Q2: What is meant by individual Banking?

Institutional Banking? Global Banking?Q3: Explain: Reserve Ratio, Required

Reserves, Excess Reserves.Q4: Are higher or lower interest rates

beneficial to institutions that borrow short & lend long? Explain!

Thank you for your Time & Patience