Capital Flows to Emerging Markets MAY 28, 2015

38

iif.com © Copyright 2015. The Institute of International Finance, Inc. All rights reserved. Capital Flows to Emerging Markets MAY 28, 2015 MAY 28, 2015 MAY 28, 2015 MAY 28, 2015 After a slow start to the year, private capital inflows to EMs are projected to cool to $981 billion in 2015, their lowest level since 2009. For 2016, we project a pickup to $1,158 billion. The projected drop in inflows in 2015 reflects disappointing EM growth, a challenging global interest rate outlook, and country-specific factors such as the Russia-Ukraine conflict. The acceleration in inflows in 2016 assumes a gradual Fed exit, a pickup in EM growth, and reduced political uncertainties. Resident capital outflows are projected to stabilize in 2015—with a continued shift towards private sources and away from official reserve accumulation. We stress downside risks to our capital flows outlook related to (1) continued stagnation in global growth and (2) more aggressive Fed rate increases that could be prompted by further U.S. labor market tightening. In these scenarios, capital flows to EMs would be even weaker in 2015 and would not experience the marked rebound in 2016 that we project in our baseline case. Fallout from a potential EM stress event would be exacerbated by a lack of secondary market liquidity and increased corporate indebtedness across EMs. The outlook for 2015 EM capital inflows has deteriorated since our January report. We now forecast private non-resident inflows to decline from $1,048 billion in 2014 to $981 billion this year, which would be the weakest outcome since the global financial crisis. Moreover, inflows are projected to slide to 3.5% of EM GDP, the lowest level since 2002. In part, the weakness in flows projected for 2015 reflects developments that have already occurred as we estimate that capital inflows reached a six-year low in 2015Q1 in the context of weak EM GDP growth (Chart 1). Table of Contents Overview 1 Growth Acceleration Delayed 5 Alternative Scenarios 8 Spike in Global Risk Aversion 10 EM Reserve Slowdown 13 EM Corporate Debt Risks 15 EM Liquidity—How Bad? 20 Emerging Asia 25 Emerging Europe 27 Latin America 29 Middle East 31 Sub-Saharan Africa 33 Tables and Annex 34 Chart 1 Chart 1 Chart 1 Chart 1 GLOBAL MACROECONOMIC ANALYSIS Felix Huefner CHIEF ECONOMIST [email protected] Robin Koepke ECONOMIST [email protected] Arpitha Bykere ASSOCIATE ECONOMIST [email protected] Scott Farnham RESEARCH ANALYST [email protected] Litia Shaw SENIOR PROGRAM ASSISTANT [email protected] CAPITAL MARKETS & EMERGING MARKETS POLICY Sonja Gibbs DIRECTOR [email protected] Emre Tiftik FINANCIAL ECONOMIST [email protected] Fiona Nguyen SENIOR RESEARCH ANALYST [email protected] Khadija Mahmood RESEARCH ANALYST [email protected] Charles Collyns CHIEF ECONOMIST [email protected] Hung Tran EXECUTIVE MANAGING DIRECTOR [email protected] 150 175 200 225 250 275 300 3.0 3.5 4.0 4.5 5.0 12Q4 13Q2 13Q4 14Q2 14Q4e 15Q2f 15Q4f 16Q2f 16Q4f EM GDP Growth 4-Quarter MA Total Capital Inflows 4-Quarter MA IIF Forecast Source: IMF, National Sources, IIF. $ billion EM EM EM EM GDP Growth and Total EM Capital Inflows GDP Growth and Total EM Capital Inflows GDP Growth and Total EM Capital Inflows GDP Growth and Total EM Capital Inflows percent, q/q, saar

Transcript of Capital Flows to Emerging Markets MAY 28, 2015

iif.com © Copyright 2015. The Institute of International Finance, Inc. All rights reserved.

Capital Flows to Emerging Markets MAY 28, 2015MAY 28, 2015MAY 28, 2015MAY 28, 2015

� After a slow start to the year, private capital inflows to EMs are projected to cool to

$981 billion in 2015, their lowest level since 2009. For 2016, we project a pickup to

$1,158 billion.

� The projected drop in inflows in 2015 reflects disappointing EM growth, a challenging

global interest rate outlook, and country-specific factors such as the Russia-Ukraine

conflict.

� The acceleration in inflows in 2016 assumes a gradual Fed exit, a pickup in EM growth,

and reduced political uncertainties.

� Resident capital outflows are projected to stabilize in 2015—with a continued shift

towards private sources and away from official reserve accumulation.

� We stress downside risks to our capital flows outlook related to (1) continued

stagnation in global growth and (2) more aggressive Fed rate increases that could be

prompted by further U.S. labor market tightening.

� In these scenarios, capital flows to EMs would be even weaker in 2015 and would not

experience the marked rebound in 2016 that we project in our baseline case.

� Fallout from a potential EM stress event would be exacerbated by a lack of secondary

market liquidity and increased corporate indebtedness across EMs.

The outlook for 2015 EM capital inflows has deteriorated since our January report. We

now forecast private non-resident inflows to decline from $1,048 billion in 2014 to $981

billion this year, which would be the weakest outcome since the global financial crisis.

Moreover, inflows are projected to slide to 3.5% of EM GDP, the lowest level since 2002.

In part, the weakness in flows projected for 2015 reflects developments that have already

occurred as we estimate that capital inflows reached a six-year low in 2015Q1 in the

context of weak EM GDP growth (Chart 1).

Table of Contents Overview 1 Growth Acceleration Delayed 5 Alternative Scenarios 8 Spike in Global Risk Aversion 10 EM Reserve Slowdown 13 EM Corporate Debt Risks 15 EM Liquidity—How Bad? 20 Emerging Asia 25 Emerging Europe 27 Latin America 29 Middle East 31 Sub-Saharan Africa 33 Tables and Annex 34

Chart 1Chart 1Chart 1Chart 1

GLOBAL MACROECONOMIC ANALYSIS

Felix Huefner CHIEF ECONOMIST [email protected]

Robin Koepke ECONOMIST [email protected]

Arpitha Bykere ASSOCIATE ECONOMIST [email protected]

Scott Farnham RESEARCH ANALYST [email protected]

Litia Shaw SENIOR PROGRAM ASSISTANT [email protected]

CAPITAL MARKETS & EMERGING MARKETS POLICY

Sonja Gibbs DIRECTOR [email protected]

Emre Tiftik FINANCIAL ECONOMIST [email protected]

Fiona Nguyen SENIOR RESEARCH ANALYST [email protected] Khadija Mahmood RESEARCH ANALYST [email protected]

Charles Collyns CHIEF ECONOMIST [email protected]

Hung Tran EXECUTIVE MANAGING DIRECTOR [email protected]

150

175

200

225

250

275

300

3.0

3.5

4.0

4.5

5.0

12Q4 13Q2 13Q4 14Q2 14Q4e 15Q2f 15Q4f 16Q2f 16Q4f

EM GDP Growth 4-Quarter MA

Total Capital Inflows 4-Quarter MA

IIF Forecast

Source: IMF, National Sources, IIF.

$ billionEMEMEMEM GDP Growth and Total EM Capital InflowsGDP Growth and Total EM Capital InflowsGDP Growth and Total EM Capital InflowsGDP Growth and Total EM Capital Inflowspercent, q/q, saar

iif.com © Copyright 2015. The Institute of International Finance, Inc. All rights reserved.

page 2 CAPITAL FLOWS TO EMERGING MARKETS | MAY 28, 2015

Chart 4Chart 4Chart 4Chart 4

Looking ahead, a key assumption is that the Fed tightening trajectory is broadly in line

with current economist consensus expectations—i.e. liftoff later this year and 4 hikes of

25 basis points each over the course of 2016. In this case any fallout should be limited

and concentrated on the more vulnerable EMs. However, it is important to highlight the

high degree of uncertainty surrounding market reactions to actual Fed hiking of policy

rates. Even if the Fed's schedule and trajectory of rate hikes are consistent with current

expectations, markets can become jittery on the occasion of actual rate hikes to the

detriment of EMs. Moreover, the two main risk scenarios to our baseline point to further

weakness in capital flows to EMs, rather than the revival we project for 2016 in our

baseline (pages 8-9). First, there could be a protracted slowdown in both emerging and

mature economy growth that would reduce incentives for cross-border investment, even

with lower interest rates. Second, the Fed may raise policy rates by more than expected,

perhaps in response to tightening conditions in labor markets even in the face of

moderate growth due to a weakening on the supply side of the U.S. economy.

Portfolio flows have continued to be volatile over the past few months. Introduction of

QE by the ECB and a shift in market expectations towards a slower Fed exit supported

portfolio flows in the first few months of 2015 (Chart 2). Subsequently, portfolio flows

suffered a retrenchment in May in the context of a sharp increase in mature economy

bond yields, led by a jump in bund yields that seems to have been related to a

stabilization in global oil prices and some alleviation of disinflation concerns. According

to our new Flows Alert, which aims to identify episodes of flow surges and reversals on a

real-time basis, the reversal episode lasted 18 days and was widespread across countries.

We estimate that total EM portfolio outflows in this episode may have amounted to

around $10-15 billion, compared to $35-50 billion during the taper tantrum of 2013

(Chart 3).

For 2015 as a whole, we project portfolio equity flows to climb to around $130 billion, a

30% increase from 2014 (Table 1), helped by improving EM economic prospects as the

year progresses and relatively attractive valuations (Chart 4). Portfolio debt flows will

Chart 2Chart 2Chart 2Chart 2

-30

-20

-10

0

10

20

30

40

50

Jan 14 May 14 Sep 14 Jan 15 May 15

Debt

Equity

Total

TotalTotalTotalTotal NonNonNonNon----Resident Portfolio Flows to Emerging MarketsResident Portfolio Flows to Emerging MarketsResident Portfolio Flows to Emerging MarketsResident Portfolio Flows to Emerging Markets$ billion

Source: IIF.

2010-14 Average: $22 bn

Chart 3Chart 3Chart 3Chart 3

6

8

10

12

14

16

18

2005 2008 2011 2014

Forward P/E RatiosForward P/E RatiosForward P/E RatiosForward P/E RatiosMSCI indices, price-to-12Mforward earnings estimates, dotted line=period average

Developed Markets

Emerging Markets

Source: MSCI, Datastream, IIF.

-1.6

-1.2

-0.8

-0.4

0.0

0.4

0.8

1.2

1.6

Apr 13 Oct 13 Apr 14 Oct 14 Apr 15

Confidence Band7-Day MA28-Day MA

Daily EM Equity and Bond FlowsDaily EM Equity and Bond FlowsDaily EM Equity and Bond FlowsDaily EM Equity and Bond Flows$ billion, all available countries (7)

Taper Tantrum

Oil Price and Ruble Collapse

Spring 2014 Surge

January 2014 Correction

Taper DelayRally

Flows Alerts (Selection)

Bund Bund Bund Bund TantrumTantrumTantrumTantrum

Source: IIF.

AAAA key assumption key assumption key assumption key assumption is that the Fed is that the Fed is that the Fed is that the Fed tightening tightening tightening tightening trajectory is trajectory is trajectory is trajectory is broadly in line broadly in line broadly in line broadly in line with current with current with current with current economist economist economist economist consensus consensus consensus consensus expectationsexpectationsexpectationsexpectations

iif.com © Copyright 2015. The Institute of International Finance, Inc. All rights reserved.

page 3 CAPITAL FLOWS TO EMERGING MARKETS | MAY 28, 2015

continue to be dampened by nervousness about rates in advance of Fed exit and less

favorable valuations compared to asset classes like U.S. high yield bonds (Chart 5).

Overall, we forecast these flows to be flat at around $170 billion.

Foreign direct investment (FDI) accounts for a large portion of the decline in capital flows

projected for 2015 (Table 1). We project FDI inflows to fall to $530 billion this year from

$580 billion in 2014, led by reduced inflows to China and Russia. Nonetheless, FDI

remains by far the largest (and most stable) source of external financing, and is likely to

account for around half of total non-resident inflows this year.

On a regional basis, a major factor behind the marked decline in total capital inflows in

2014/15 is the conflict between Russia and Ukraine (Chart 6). The slump particularly

affected non-bank lending to Russia (including bond flows), which fell from inflows of $85

billion in 2013 to outflows of $72 billion in 2014. For total non-resident flows to Russia,

we project a further retrenchment to the tune of $33 billion this year, led by bank lending

and portfolio debt flows. In addition, net debt-related inflows to China have turned

negative as Chinese corporates have sought to reduce dollar exposure in the face of

dollar strength, monetary policy easing, and more two-way movement in the RMB.

Resident capital outflows by emerging market investors are projected to stabilize at just

under $1.2 trillion in 2015. We expect the composition of EM outward investment to shift

Chart 5Chart 5Chart 5Chart 5

0

75

150

225

300

375

2010 2012 2014

Differential Between U.S.Differential Between U.S.Differential Between U.S.Differential Between U.S. HY HY HY HY Spread and CEMBI SpreadSpread and CEMBI SpreadSpread and CEMBI SpreadSpread and CEMBI Spreadbasis points

Source: Bloomberg, BAML, IIF.

2000-2015 Average

Table 1Table 1Table 1Table 1

Emerging Market Economies: Capital FlowsEmerging Market Economies: Capital FlowsEmerging Market Economies: Capital FlowsEmerging Market Economies: Capital Flows

$ billion 2013 2014 2015 2016

NonNonNonNon----Resident Capital Inflows Resident Capital Inflows Resident Capital Inflows Resident Capital Inflows 1301130113011301 1090109010901090 1049104910491049 1202120212021202

Private InflowsPrivate InflowsPrivate InflowsPrivate Inflows 1269126912691269 1048104810481048 981981981981 1158115811581158

Equity Investment 666 687 657 725

Direct Investment 582 586 529 561

Portfolio Investment 84 101 128 164

Private Creditors 603 361 325 433

Commercial Banks 172 175 119 184

Nonbanks 431 186 206 248

Official Inflows 33 42 68 44

International Financial Institutions -3 12 34 20

Bilateral Creditors 36 30 34 24

Resident Capital OutflowsResident Capital OutflowsResident Capital OutflowsResident Capital Outflows ----1518151815181518 ----1164116411641164 ----1179117911791179 ----1351135113511351

Private Outflows -978 -1054 -1105 -1065

Equity Investment Abroad -418 -397 -388 -406

Resident Lending/Other -560 -657 -716 -659

Reserves (- = Increase) -540 -110 -74 -286

----217217217217 ----74747474 ----130130130130 ----149149149149

Memo:

Net Errors and Omissions -3 -146 0 0

Current Account Balance 220 220 130 149

Source: IIF. See backcover page for guidance on how to interpret these data.

Net Capital FlowsNet Capital FlowsNet Capital FlowsNet Capital Flows

iif.com © Copyright 2015. The Institute of International Finance, Inc. All rights reserved.

page 4 CAPITAL FLOWS TO EMERGING MARKETS | MAY 28, 2015

further towards private sources of capital and away from official reserve accumulation.

Indeed, reserve accumulation is projected to slow to only $74 billion this year from $110

billion in 2014 and an average of $600 billion during 2004-2013. As discussed on pages

13-14, this reduction reflects three main factors: (1) declining oil revenues by major oil

exporters (see page 32), (2) weaker capital inflows mainly in Asian EMs, and (3) a

continued rise in outflows by Chinese corporates (see page 25). Thanks to China,

emerging markets on aggregate remain net exporters of capital (Chart 7). China is

projected to invest $540 billion overseas in 2015 (up $38 billion), of which over 50%

would be resident lending abroad and over a quarter in the form of FDI.

Chart 7Chart 7Chart 7Chart 7

-2000

-1500

-1000

-500

0

500

1000

1500

1995 1998 2001 2004 2007 2010 2013 2016f

"Private" Resident Outflows

Official Reserve Accumulation

Non-Resident Inflows

Net Flows

EM Capital Flows by Residency of InvestorsEM Capital Flows by Residency of InvestorsEM Capital Flows by Residency of InvestorsEM Capital Flows by Residency of Investors$ billion

Source: IIF.

IIF Forecast

Chart 6Chart 6Chart 6Chart 6

-1.5

0.0

1.5

3.0

4.5

6.0

7.5

9.0

10.5

-200

0

200

400

600

800

1000

1200

1400

2000 2004 2008 2012 2016

EM Europe Latin America

MENA EM Asia ex. China

China

Private NonPrivate NonPrivate NonPrivate Non----Resident Capital Inflows to Emerging MarketsResident Capital Inflows to Emerging MarketsResident Capital Inflows to Emerging MarketsResident Capital Inflows to Emerging Markets$ billion percent of EM GDP

Total, Percent of EM GDP

Source: IIF.

IIF Forecast

Thanks to China, Thanks to China, Thanks to China, Thanks to China, emerging markets emerging markets emerging markets emerging markets on aggregate on aggregate on aggregate on aggregate remain net remain net remain net remain net exporters of exporters of exporters of exporters of capitalcapitalcapitalcapital

iif.com © Copyright 2015. The Institute of International Finance, Inc. All rights reserved.

page 5 CAPITAL FLOWS TO EMERGING MARKETS | MAY 28, 2015

GLOBAL GROWTHGLOBAL GROWTHGLOBAL GROWTHGLOBAL GROWTH————ACCELEACCELEACCELEACCELERATION DELAYEDRATION DELAYEDRATION DELAYEDRATION DELAYED

Underlying our projections for reduced flows this year and a pick-up in 2016 is a global

macro outlook where growth is led by an acceleration in mature economies, with weaker,

but regionally differentiated growth in EMs. Fed policy rates are expected to be raised

gradually from later this year, but the ECB and BoJ continue their QE programs.

Relative to our January Capital Flows report, global activity has clearly disappointed so

far this year. We now estimate mature economy growth in the first quarter to have been a

mediocre 1.3%, and only 2.6% in EMs—the lowest rate since the global financial crisis

(Chart 8). While activity in Europe and Japan has gathered some momentum, growth

faltered in both the U.S. and China. More broadly, the global impact of lower oil prices

on consumption was less favorable than previously thought. Also, any beneficial

consumption effect was offset to varying degrees by cutbacks in investment (particularly

in the U.S.) and government spending (in EM oil exporters).

We still expect an acceleration of growth in the remainder of 2015 and 2016, as

temporary factors weighing on U.S. activity unwind, as stimulus measures have an impact

in China, and as conditions improve in a number of other EMs that have been very weak,

notably Brazil and Russia. Nonetheless, as reported in our April Global Economic

Monitor, we have reduced our 2015 global GDP forecasts by around 1/3 percentage

point, with lower annual growth in Latin America, the MENA region and in the U.S.

(Chart 10). Lower EM growth particularly affects FDI and banking inflows, which are

expected to suffer as a result (Chart 9).

DIVERGENT DIVERGENT DIVERGENT DIVERGENT MONETARY POLICY MONETARY POLICY MONETARY POLICY MONETARY POLICY ---- UNEASY BACKUNEASY BACKUNEASY BACKUNEASY BACKDROP DROP DROP DROP FOR PORTFOLIO FLOWSFOR PORTFOLIO FLOWSFOR PORTFOLIO FLOWSFOR PORTFOLIO FLOWS

Prospects for EM portfolio flows hinge crucially on prospects for increases in Fed policy

rates. Since January, expectations for Fed tightening have been pushed backwards,

0

2

4

6

8

10

2010 2012 2014

IIF EM Coincident IndicatorIIF EM Coincident IndicatorIIF EM Coincident IndicatorIIF EM Coincident Indicatorpercent change

SourceSource

EMCI, 3m/3m, saar

Source: IIF.

EM GDP, q/q, saar

Chart 8Chart 8Chart 8Chart 8

Chart 9Chart 9Chart 9Chart 9

Figure 1: Drivers of EM Capital Flows by Major Component Figure 1: Drivers of EM Capital Flows by Major Component Figure 1: Drivers of EM Capital Flows by Major Component Figure 1: Drivers of EM Capital Flows by Major Component

DriverDriverDriverDriver Portfolio EquityPortfolio EquityPortfolio EquityPortfolio Equity Portfolio DebtPortfolio DebtPortfolio DebtPortfolio Debt Banking FlowsBanking FlowsBanking FlowsBanking Flows FDIFDIFDIFDI

Global risk aversion

PushPushPushPush Mature economy interest rates

Mature economy output growth

Domestic output growth

PullPullPullPull Asset return indicators

Country risk indicators

Strong evidence for negative relationship

TypeTypeTypeType

Strong evidence for positive relationship

Some evidence for positive relationship

Mixed evidence, no clear relationship

Some evidence for negative relationship

Source: IIF Working Paper “What Drives Capital Flows to Emerging Markets?”, April 2015.

iif.com © Copyright 2015. The Institute of International Finance, Inc. All rights reserved.

page 6 CAPITAL FLOWS TO EMERGING MARKETS | MAY 28, 2015

reflecting the sluggish U.S. growth performance, even though the U.S. labor market has

continued to heal. While at the beginning of the year, a June 2015 rate hike seemed on

the cards, the first rate hike now seems unlikely to occur before September and then

only if the U.S. economy regains momentum in coming months. In addition, the

expected trajectory of rate increases has become less steep, helped by a downward shift

in the FOMC’s own interest rate projections (Chart 12). On the other side of the Atlantic,

sovereign QE by the ECB has delivered a substantial reduction in European bond yields

and expectations for future ECB policy rates, albeit partly reversed during the first half of

May (Chart 13).

We estimate that lower policy rate expectations in both the U.S. and the Euro Area have

had a positive direct impact on portfolio flows to EMs, in particular this year (Chart 11).

In the past, shifts in perceptions about Fed rates have been the dominant factor, but

ECB actions have risen in importance recently. In addition to this direct effect, lower

European bond yields were one factor weighing on U.S. rates (in part because portfolio

substitution effects coming from the ECB’s QE program drove down the term premium

-1.6

-1.2

-0.8

-0.4

0.0

0.4

0.82015 2016

Forecast Revisions to GDP GrowthForecast Revisions to GDP GrowthForecast Revisions to GDP GrowthForecast Revisions to GDP Growth Relative to January CFRRelative to January CFRRelative to January CFRRelative to January CFRpercentage points

Source: IIF.

Chart 10Chart 10Chart 10Chart 10

-20

-16

-12

-8

-4

0

4

8

12

16

2013 2014 2015

Fed

ECB

Estimated ContributionsEstimated ContributionsEstimated ContributionsEstimated Contributions to EM Portfolio Flowsto EM Portfolio Flowsto EM Portfolio Flowsto EM Portfolio Flows$ billion, cumulative contributions since 1/1/2013

Source: Bloomberg, IIF.

Taper Tantrum

Bund Tantrum

Chart 11Chart 11Chart 11Chart 11

Chart 12Chart 12Chart 12Chart 12 Chart 13Chart 13Chart 13Chart 13

Lower policy rate Lower policy rate Lower policy rate Lower policy rate expectations in expectations in expectations in expectations in both the U.S. and both the U.S. and both the U.S. and both the U.S. and the Euro Area the Euro Area the Euro Area the Euro Area have had a have had a have had a have had a positive direct positive direct positive direct positive direct impact on impact on impact on impact on portfolio flows to portfolio flows to portfolio flows to portfolio flows to EMsEMsEMsEMs

0

1

2

3

Jan 14 Apr 14 Jul 14 Oct 14 Jan 15 Apr 15

10101010----YearYearYearYear Govt. Bond YieldsGovt. Bond YieldsGovt. Bond YieldsGovt. Bond Yieldspercent

Germany

U.S.

Source: Haver.

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2015 2016 2017 2018

Market Expectations as of 5/22/2015

Market Expectations as of 1/8/2015

FOMC as of 12/2014

FOMC as of 3/2015

Outlook for Federal Funds RateOutlook for Federal Funds RateOutlook for Federal Funds RateOutlook for Federal Funds Ratepercent, based on fed fund futures and Eurodollar contracts, FOMC = Median FOMC projection

Source: Bloomberg, Federal Reserve, IIF.

iif.com © Copyright 2015. The Institute of International Finance, Inc. All rights reserved.

page 7 CAPITAL FLOWS TO EMERGING MARKETS | MAY 28, 2015

in U.S. bond yields and in part because of the damping impact on the U.S. economy of

the US dollar appreciation against the Euro), supporting portfolio flows to EMs.

Going forward, we project that the Fed will start to tighten in September, and then raise

rates by an average of 25 basis points a quarter through 2016, in line with FOMC

projections and the current economist consensus. Market expectations for Fed rate hikes

would edge gradually higher and closer towards the FOMC’s own projected trajectory

(Chart 12) as the date of liftoff comes closer, assuming that U.S. growth recovers

momentum over the summer months and labor markets continue to tighten. It is

important to note, however, that the assumed Fed policy trajectory in this scenario does

not rely on strong U.S. growth outcomes – we assume quarterly growth rates in the range

of 2.5-3 percent from Q3 onwards—but instead is linked to growing evidence for a

closing output gap and a weakening of the supply side of the U.S. economy. This

weakening has occurred across several dimensions.

One is that U.S. productivity performance has been lackluster in the post-crisis period:

growth in real output per hour has been less than half of the pre-2008 average (Chart

14). In addition, labor force participation rates have failed to pick up from their post-crisis

lows and the matching function of the labor market has deteriorated as illustrated by an

outward shift of the Beveridge curve in recent years (Chart 15). This is likely to reflect

continued problems in the housing market, which weigh on labor mobility as well as

continued skills mismatches.

Under the baseline scenario, the drag on EM portfolio and banking flows from gradually

increasing U.S. interest rates would be offset to some extent by the moderate pickup in

mature economy growth. Nonetheless, the uncertainty surrounding the transition to Fed

liftoff and associated adjustment of market expectations is likely to lead to some volatility

of portfolio flows, notably for those EMs with vulnerable macro fundamentals and policy

frameworks. The beginning of this year gave some flavor of the effects of such an

adjustment in rate expectations as markets brought forward their expected timing of the

first rate hike against the background of strong employment data in the U.S. (only to shift

them back again from mid-March onwards).

-2

-1

0

1

2

3

4

5

6

1990 1995 2000 2005 2010 2015

Period averages

U.S. BusinessU.S. BusinessU.S. BusinessU.S. Business Sector ProductivitySector ProductivitySector ProductivitySector Productivitypercent, oya; real output per hour

Source: Haver, BLS.

Chart 14Chart 14Chart 14Chart 14

1.5

2.0

2.5

3.0

3.5

4.0

4 5 6 7 8 9 10 11unemployment rate, percent of labor force

2008H2

20112012

2009

2010

U.S. Beveridge Curve (2001U.S. Beveridge Curve (2001U.S. Beveridge Curve (2001U.S. Beveridge Curve (2001----2014 Data)2014 Data)2014 Data)2014 Data)job openings rate in percent of total jobs (filled and vacant)

2013

Source: BLS, IIF.

2014

2001-2008H1

Chart 15Chart 15Chart 15Chart 15

We project that We project that We project that We project that the Fed will start the Fed will start the Fed will start the Fed will start to tighten in to tighten in to tighten in to tighten in September, and September, and September, and September, and then raise rates by then raise rates by then raise rates by then raise rates by an average of 25 an average of 25 an average of 25 an average of 25 basis points a basis points a basis points a basis points a quarter through quarter through quarter through quarter through 2016201620162016

iif.com © Copyright 2015. The Institute of International Finance, Inc. All rights reserved.

page 8 CAPITAL FLOWS TO EMERGING MARKETS | MAY 28, 2015

WHAT IF REALITY DOES NOT FOLLOW THE BASEWHAT IF REALITY DOES NOT FOLLOW THE BASEWHAT IF REALITY DOES NOT FOLLOW THE BASEWHAT IF REALITY DOES NOT FOLLOW THE BASELINE SCENARIO?LINE SCENARIO?LINE SCENARIO?LINE SCENARIO?

Our baseline scenario is arguably a relatively benign one in current circumstances with a

pick-up in global growth, supporting a recovery of capital flows to EMs. However, after

years of post-crisis disappointments, there are rising doubts about global economic

performance. Here we consider how different scenarios for mature economy GDP growth

and U.S. policy tightening could affect EM growth and capital flows in various ways

(Chart 16).

The best outcome would be robust demand combined with improved supply side

performance and only moderate labor market tightening. This could be seen as a “return

to normal” or “sweetspot” case whereby U.S. growth potential is sufficiently high that

spare capacity is absorbed only slowly despite strong output growth—the best of all

worlds for EM capital flows. Compared to this, our baseline scenario is somewhat more

pessimistic as it combines weaker growth with the same degree of labor market and

policy tightening.

However, there are two alternative scenarios that would have much less benign

implications for EMs. In both cases, capital flows to EMs would remain under pressure,

rather than rebound markedly in 2016 as projected in our baseline scenario.

The first scenario would be a “secular stagnation” scenario, in which mature economy

aggregate demand growth continues to turn out weaker than projected. In these

circumstances, labor market tightening would occur much more gradually and price

inflation would remain well below central bank targets. This could occur as continuing

disappointment with growth outcomes feeds into rising concerns about prospects,

dampening both consumer confidence and business sentiment. This could be reinforced

by a sense that policymakers were running out of instruments to push economies against

strong secular drags, including aging populations, less productivity kick from

Chart 16Chart 16Chart 16Chart 16

FDI Bank Portfolio

Sweetspot

Baseline

Secular Stagnation

U.S. Supply Shock

Note: dark red denotes very adverse impact, dark green denotes

very positive impact.

EM GDP growth

U.S. labor market tightening /Fed policy rate hikes / global risk aversion

Sweetspot

Baseline

Secular Stagnation

EM Capital Flows EM Capital Flows EM Capital Flows EM Capital Flows ---- Different ScenariosDifferent ScenariosDifferent ScenariosDifferent Scenarios

U.S. Wage Shock

EM Capital Flows Scenarios Impact by Type of FlowEM Capital Flows Scenarios Impact by Type of FlowEM Capital Flows Scenarios Impact by Type of FlowEM Capital Flows Scenarios Impact by Type of Flow

We consider how We consider how We consider how We consider how different scenarios different scenarios different scenarios different scenarios for mature for mature for mature for mature economy GDP economy GDP economy GDP economy GDP growth and U.S. growth and U.S. growth and U.S. growth and U.S. policy tightening policy tightening policy tightening policy tightening could affect EM could affect EM could affect EM could affect EM growth and capital growth and capital growth and capital growth and capital flows flows flows flows

iif.com © Copyright 2015. The Institute of International Finance, Inc. All rights reserved.

page 9 CAPITAL FLOWS TO EMERGING MARKETS | MAY 28, 2015

technological progress, and slower convergence by EMs. This would lead the Fed to

signal that it will wait longer to start liftoff (thus more or less validating current market

rate expectations) and then raise rates very gradually with the end-point for rate

increases lower as expectations for longer term growth and equilibrium real rates come

down.

The lower trajectory for Fed rates would benefit portfolio flows thanks to lower global

interest rates than otherwise. However, EM growth would also turn out weaker due to

less demand from mature economies, which would weigh on capital flows, notably FDI.

Overall, we would expect capital flows to EMs to be stagnant in this scenario.

The second scenario—arguably an even more negative one from an EM perspective—

would be a negative U.S. wage shock, whereby even with U.S. demand growing only

moderately according to our baseline, wage pressures pick up more rapidly than

envisaged. This could be the case if the U.S. labor market supply response to rising labor

demand remains weak, implying that even meagre aggregate demand growth leads to a

pick-up in wage pressures. In this case, the Fed would tighten policy quicker than even

their own current projections suggest and market expectations could adjust quite

abruptly, triggering a “super taper tantrum.” Such an adjustment would likely be

accompanied by rising risk aversion.

For EM capital flows, this would be the worst of all worlds with higher global interest

rates, less favorable financing conditions and lackluster mature economy growth.

Movements in EM asset prices could be quite sharp, exacerbated by reduced market

liquidity. In such circumstances, the broad EM asset class could be affected by wide

outflows that would be less differentiated, as liquid markets could suffer quite heavy

withdrawals, at least until market stress subsides. Overall, EM flows could be substantially

lower, mainly because of weaker portfolio flows.

Chart 18Chart 18Chart 18Chart 18

0

10

20

30

40

50

60

70

0

1

2

3

4

5

6

7

8

9

2000 2002 2004 2006 2008 2010 2012 2014

U.S. BBBU.S. BBBU.S. BBBU.S. BBB----Rated Corporate Bond Spread and VIXRated Corporate Bond Spread and VIXRated Corporate Bond Spread and VIXRated Corporate Bond Spread and VIXpercent per annum

Source: Bank of America/ Merrill Lynch, CBOE.

U.S. Corp BBB Spread

VIX

Chart 17Chart 17Chart 17Chart 17

0.1

0.2

0.3

0.4

0.5

0.6

0.7

2008 2009 2010 2011 2012 2013 2014 2015

Pre-2008Crisis Average

Post-2008Crisis Average

Source: IIF, Bloomberg.

Correlation Across EM ExchangeCorrelation Across EM ExchangeCorrelation Across EM ExchangeCorrelation Across EM Exchange RatesRatesRatesRatesaverage 30-day rolling correlation between percentage change in MSCI EM FX index and USD/LC exchange rate for 22 EMs

A U.S. wage shock A U.S. wage shock A U.S. wage shock A U.S. wage shock would be the would be the would be the would be the worst scenario for worst scenario for worst scenario for worst scenario for EM capital flows.EM capital flows.EM capital flows.EM capital flows.

iif.com © Copyright 2015. The Institute of International Finance, Inc. All rights reserved.

page 10 CAPITAL FLOWS TO EMERGING MARKETS | MAY 28, 2015

WHO’S AT RISK FROM A SPIKE IN GLOBAL RISWHO’S AT RISK FROM A SPIKE IN GLOBAL RISWHO’S AT RISK FROM A SPIKE IN GLOBAL RISWHO’S AT RISK FROM A SPIKE IN GLOBAL RISK AVERSION K AVERSION K AVERSION K AVERSION

If history is any guide, global risk aversion would increase sharply, at least temporarily,

under a scenario in which market expectations for Fed policy shift abruptly. Recently,

most broad measures of global risk aversion have remained at relatively low levels, at

least when compared to historical averages (Chart 17). An increase in global risk aversion

would likely introduce additional volatility into capital flows to EMs. A structural decline

in market liquidity increases the degree of concern with volatility spikes (see pages 20-

24).

Not all EMs would be hit equally. In fact, markets have continued to differentiate

significantly across EMs, with cross-country correlations for different asset markets

remaining significantly lower than in the years prior to 2013 (Chart 18). To calibrate the

impact of risk shocks across EMs, we have estimated risk responsiveness betas for some

major EMs, which again supports the differentiation story (see Box).

Our IIF Heatmap of EM vulnerabilities attempts to compare macro fundamentals across

EMs. The country ranking identified in the Heatmap correlates well with market

performance across EMs (Chart 19; see also the discussion in our April Global Economic

Monitor). Much of the focus ever since the 2013 taper tantrum has been on external

vulnerabilities and more recently on policy vulnerabilities. Specifically, EMs with large

current account deficits, such as South Africa, Turkey and Brazil, have tended to

underperform. By contrast, India has used the time since the taper tantrum to reduce its

current account deficit and has been more resilient to market pressures in recent months.

The sharp decline in oil prices relative to its highs in early 2014, notwithstanding the

recent rebound, has tended to reduce external vulnerabilities of oil importers, but hurt oil

exporters. India, for example, clearly is a beneficiary and also took advantage of lower oil

prices to reduce fuel subsidies. While Turkey benefits from a lower oil import bill, much

BR

CLCN

CO

HU

IN

ID

MY

MX

PE

PH

PLRO

ZA

TRRU

-40

-20

0

20

40

60

80

100

0.3 0.4 0.5 0.6 0.7

average of domestic, external and policy vulnerability indices*

*A higher value implies higher vulnerability and vice-versa. Source: IIF, Bloomberg.

IIF Heat MapIIF Heat MapIIF Heat MapIIF Heat Map Vulnerability Measures Vulnerability Measures Vulnerability Measures Vulnerability Measures vs. EMBIG Spreadsvs. EMBIG Spreadsvs. EMBIG Spreadsvs. EMBIG Spreads

change in EMBIG spreads since Aug 2014

Chart 19Chart 19Chart 19Chart 19

AnAnAnAn increase in increase in increase in increase in global risk global risk global risk global risk aversion would aversion would aversion would aversion would likely introduce likely introduce likely introduce likely introduce additional additional additional additional volatility into volatility into volatility into volatility into capital flows to capital flows to capital flows to capital flows to EMsEMsEMsEMs

iif.com © Copyright 2015. The Institute of International Finance, Inc. All rights reserved.

page 11 CAPITAL FLOWS TO EMERGING MARKETS | MAY 28, 2015

Chart 20Chart 20Chart 20Chart 20

BOX: CALIBRATING THEBOX: CALIBRATING THEBOX: CALIBRATING THEBOX: CALIBRATING THE IMPACT OF A RISK SHIMPACT OF A RISK SHIMPACT OF A RISK SHIMPACT OF A RISK SHOCKOCKOCKOCK

A bumpy Fed exit could prompt a spike in global risk

aversion that would spill over into emerging markets. In a

recent research note, we estimate how responsive various

emerging markets’ asset prices are to changes in global risk

aversion. We refer to this relationship as the “EM risk beta,”

analogous to the relation between individual stock prices

and the overall stock market in the Capital Asset Pricing

Model (CAPM) framework. We cover 10 major EM

economies during the period from 2000–2015, and focus on

the MSCI EM stock market index and the U.S. corporate BBB

spread, which have been strongly correlated in recent years

(Chart 20). In addition, we consider other EM asset price

variables like EM bond spreads over U.S. Treasuries and the

exchange rate vis-à-vis the U.S. dollar. We also cross-check

our results by using an alternative measure of global risk

aversion (the VIX).

A useful estimate of the responsiveness of EM stocks to

changes in risk aversion can be obtained by running a simple

regression of the daily percent change in the MSCI EM on

the daily percent change in the BBB spread, plus a constant

term: %EM Asset Pricest = c + β * %BBBt

The coefficient β provides a measure of the elasticity of the

response to shifts in global risk aversion. Within the last 15

years, we look at three sample periods—the pre-crisis period

(2000-2007), the crisis years (2008-2009), and the most

recent years (2012-2015). It is notable that the estimated risk

betas have increased since as EMs have become more

interconnected with global markets (Chart 21).

Countries with high risk betas tend to be those that score

highly on two dimensions: greater vulnerability according to

our EM heat map, and greater openness. On the

vulnerability scale, external financing requirements as

measured by current account deficits shows a particularly

close relationship (Chart 22).

Aside from country vulnerabilities, higher risk betas may also

reflect greater openness, making countries more responsive

to changes in global investor sentiment. A related factor is

the degree to which domestic securities are owned by

foreign investors. We find that risk betas tend to be higher

when foreign investors own a sizeable share of a country’s

securities.

-7

-6

-5

-4

-3

-2

-1

0

1

2

3

0 1 2 3 4

Current Account Balance

Risk Betas EstimatedRisk Betas EstimatedRisk Betas EstimatedRisk Betas Estimated Using Bond Spreads Using Bond Spreads Using Bond Spreads Using Bond Spreads vs. CAvs. CAvs. CAvs. CA BalanceBalanceBalanceBalancepercent of GDP, IIF forecast for 2015 current account balance

Estimated % Response to 1% Increase in Global Risk Aversion

TurkeySouth Africa

China

BrazilIndonesia

PolandMexico

IndiaChile

Source: Bloomberg, IMF, IIF.

Chart 22Chart 22Chart 22Chart 22

Chart 21Chart 21Chart 21Chart 21

-1.2

-1.0

-0.8

-0.6

-0.4

-0.2

0.0

India

Poland

Indonesia

South Africa

China

Chile

Turkey

Mexico

Brazil

Russia

2000-2007

2008-2009

2012-2015

EM Risk Betas Estimated Using EM MSCI and U.S. EM Risk Betas Estimated Using EM MSCI and U.S. EM Risk Betas Estimated Using EM MSCI and U.S. EM Risk Betas Estimated Using EM MSCI and U.S. BBB SpreadBBB SpreadBBB SpreadBBB Spreadestimated % response to 1% increase in global risk aversion

Source: Bloomberg, IIF.

1.0

1.5

2.0

2.5

3.0

3.5800

900

1,000

1,100

1,200

2010 2011 2012 2013 2014 2015

MSCI EM and U.S. Corporate BBB SpreadMSCI EM and U.S. Corporate BBB SpreadMSCI EM and U.S. Corporate BBB SpreadMSCI EM and U.S. Corporate BBB Spreadindex percentage points

BBB Spread

MSCI EM

Source: Bloomberg, IIF.

iif.com © Copyright 2015. The Institute of International Finance, Inc. All rights reserved.

page 12 CAPITAL FLOWS TO EMERGING MARKETS | MAY 28, 2015

of the benefit for growth has been eaten up by the fall in the lira. Oil exporters in general

have suffered, seeing a worsening of their external positions and reductions in

government spending weighing on growth, raising particular concerns for countries like

Venezuela with weak macropolicy frameworks.

On the policy side, vulnerabilities are larger for EMs where central banks do not have

firmly established inflation targeting credentials, as reflected in inflation expectations

consistently above target. Turkey is one example of an EM that has lost ground in terms

of monetary policy credibility, as it cut policy rates even as inflation expectations remain

elevated. By contrast, India has benefitted from steps to strengthen its monetary policy

framework.

Going forward, we expect differentiation to focus increasingly on domestic

vulnerabilities, such as credit growth and debt burdens, not least because rising U.S.

policy rates will make refinancing this debt more challenging, in particular when coupled

with further dollar appreciation (see pages 15-19). EMs where corporate debt has risen

sharply, including a significant share in USD-denominated debt include Brazil, Hungary,

Mexico, Russia, and Turkey.

Overall, and based on external, policy and domestic vulnerabilities, EMs that we remain

most concerned in the event of a sharp rise in global risk aversion include Brazil,

Indonesia, Russia, South Africa and Turkey.

On the policy side, On the policy side, On the policy side, On the policy side, vulnerabilities are vulnerabilities are vulnerabilities are vulnerabilities are larger for EMs larger for EMs larger for EMs larger for EMs where central where central where central where central banks do not have banks do not have banks do not have banks do not have firmly established firmly established firmly established firmly established inflation targeting inflation targeting inflation targeting inflation targeting credentials. credentials. credentials. credentials.

iif.com © Copyright 2015. The Institute of International Finance, Inc. All rights reserved.

page 13 CAPITAL FLOWS TO EMERGING MARKETS | MAY 28, 2015

THE GREAT EM RESERVE SLOWDOWN THE GREAT EM RESERVE SLOWDOWN THE GREAT EM RESERVE SLOWDOWN THE GREAT EM RESERVE SLOWDOWN

EM reserve accumulation has moderated substantially since the global financial crisis, and

in 2014 slowed to the weakest pace since 2001 amidst weaker non-resident capital

inflows and higher private resident outflows (Chart 23). Moreover, overall EM current

account balance eased slightly, as a decrease in the current accounts of oil exporters

offset the increase in the current accounts of oil importers (Chart 24). Due to these two

factors, oil exporters’ FX reserves declined and oil importers’ reserve growth halved.

Most dramatically, FX reserves plunged in EM Europe for a second year (Chart 25). The

decline was largely driven by Russia, where non-resident capital inflows declined

significantly in the context of uncertainty associated with the Ukraine conflict. Unfavorable

non-resident capital inflow and private resident capital outflow dynamics also reduced

reserves in Ukraine, Turkey and Romania and slowed reserve accumulation in Hungary

and Poland. However, current account balances improved in most countries, including in

Russia (as lower oil exports were accompanied by demand compression) and Turkey.

In EM Asia, reserve accumulation was cut in half led by weaker capital flows even as

current account balances improved. The key driver was China, where reserve

accumulation slowed significantly amidst the largest private resident outflows since at

least 1983, causing the central bank to intervene towards the end of the year in order to

contain RMB depreciation. Non-resident capital inflows moderated as well as the Chinese

economy slowed. FX reserves declined in Thailand and oil-exporter Malaysia—where

increased risk aversion halved non-resident capital inflows from 2013—and in Philippines

where private resident outflows jumped.

The marked deceleration in reserve growth in Middle East & Africa was driven by

narrowing trade and current account surpluses among oil exporters Saudi Arabia, UAE

and Nigeria. Nigeria also witnessed weaker capital inflows. Reserve accumulation in

South Africa continued to slow rapidly amidst private resident outflows, even though

current account balance and non-resident capital inflows picked up from 2013.

-1200

-800

-400

0

400

800

1200

1600

2000

2000 2002 2004 2006 2008 2010 2012 2014 2016

Resident Private Outflows

Non-Resident Inflows

Current Account Balance

Reserve Accumulation

Source: IIF.

Drivers of EM Reserve AccumulationDrivers of EM Reserve AccumulationDrivers of EM Reserve AccumulationDrivers of EM Reserve Accumulation$ billion

IIF Forecast

Chart 23Chart 23Chart 23Chart 23

-200

0

200

400

600

800

1,000

1,200

2000 2002 2004 2006 2008 2010 2012 2014 2016

EM Asia

Middle East/Africa

Latin America

EM Europe

EM

EM FX Reserve Accumulation by RegionEM FX Reserve Accumulation by RegionEM FX Reserve Accumulation by RegionEM FX Reserve Accumulation by Region$ billion

Source: IIF.

IIF Forecast

Chart 25Chart 25Chart 25Chart 25

-200

-100

0

100

200

300

400

500

600

2003 2009 2015

Oil Importers

Oil Exporters

Source: IIF.

IIF Forecast

EM Current Account BalanceEM Current Account BalanceEM Current Account BalanceEM Current Account Balance$ billion

Chart 24Chart 24Chart 24Chart 24

EM reserve EM reserve EM reserve EM reserve accumulation has accumulation has accumulation has accumulation has moderated moderated moderated moderated substantially since substantially since substantially since substantially since the global financial the global financial the global financial the global financial crisis.crisis.crisis.crisis.

iif.com © Copyright 2015. The Institute of International Finance, Inc. All rights reserved.

page 14 CAPITAL FLOWS TO EMERGING MARKETS | MAY 28, 2015

By contrast, Latin America witnessed an increase in FX reserves following a drop in 2013

led by Brazil, Argentina and Venezuela as a deterioration in current account balances was

financed by higher capital inflows and/or reduced private resident outflows.

Looking ahead, we expect EM reserve accumulation to slow further in 2015. Current

account balances are projected to weaken in aggregate, as a decline in oil exporters’

current accounts will more than offset an improvement in oil importers’ current accounts.

Non-resident capital inflows are likely to moderate among most oil exporters as well as in

over half of oil importers. Overall, we expect oil exporters’ FX reserves to decline in

aggregate and to be only marginally offset by an improvement in oil importers’ FX

reserves (Chart 26).

In fact, monthly FX reserves data adjusted for valuation changes indicate a decline in EM

FX reserves in 2015Q1, in line with our projections for a decline in reserves this year in

countries like Saudi Arabia, Malaysia, Russia, South Africa and Nigeria and weaker reserve

accumulation in China but a further pick up in reserve accumulation in countries like Korea

(Chart 27). Data for Venezuela’s reserves have not been published, but are estimated to

have declined further.

In this environment, a number of countries with a low reserve coverage ratio based on FX

reserve holdings at the end of 2014 and large external financing needs for 2015 will be

vulnerable to periods of stress since the central bank’s ability to intervene to limit currency

depreciation will be constrained (Chart 28). Many of these countries are expected to

witness a decline in FX reserves (Venezuela, Argentina, Lebanon, Malaysia and South

Africa) or a slowdown in non-resident inflows (Indonesia, Malaysia, South Africa, Turkey,

Lebanon and Ecuador) during 2015. Countries like Argentina, Turkey and Czech Republic

also received large portfolio equity and debt inflows during 2009-13 relative to their FX

reserve holdings, thus making them susceptible to risk shocks. South Africa, Indonesia and

Turkey have been on our watch list for a while.

Chart 27Chart 27Chart 27Chart 27

ARPLBG

ZA

BR

MY

RO

RU

CO

KR

LB

MO

ID

CL

HU

PEPH

CZ

MX

IN

NG(9.1, 1.7)

TH

TR

VEUKEC

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0

reserve coverage ratio in 2008*

CN(5.9, 5.1)

EG

EM Reserve AdequacyEM Reserve AdequacyEM Reserve AdequacyEM Reserve Adequacyreserve coverage ratio in 2015* (threshold=1.0)

FX reserves at end of previous year/(Current account deficit + short-term external debt + amortization payments due in current year). Source: IIF.

Chart 28Chart 28Chart 28Chart 28

-200

0

200

400

600

800

1,000

1,200

2003 2009 2015

Oil ImportersOil Exporters

Source: IIF.

IIF Forecast

EM FX ReservesEM FX ReservesEM FX ReservesEM FX Reserves$ billion

Chart 26Chart 26Chart 26Chart 26

-50

-40

-30

-20

-10

0

10

20

30

40

CN SARU

MY

NG

RO ZA

MO PECL

CO TR

AR

EG ID CZ

TH

BG

HU

UK

PH PL

LB BR

MX

KO IN

Valuation AdjustedValuation AdjustedValuation AdjustedValuation Adjusted Change in EM FX Reserves in 2015Q1Change in EM FX Reserves in 2015Q1Change in EM FX Reserves in 2015Q1Change in EM FX Reserves in 2015Q1$ billion

Source: IMF IFS, IIF Calculations.

We expect EM We expect EM We expect EM We expect EM reserve reserve reserve reserve accumulation to accumulation to accumulation to accumulation to slow further in slow further in slow further in slow further in 2015. 2015. 2015. 2015.

iif.com © Copyright 2015. The Institute of International Finance, Inc. All rights reserved.

page 15 CAPITAL FLOWS TO EMERGING MARKETS | MAY 28, 2015

EMERGING MARKET CORPORATE DEBTEMERGING MARKET CORPORATE DEBTEMERGING MARKET CORPORATE DEBTEMERGING MARKET CORPORATE DEBT————WHERE ARE THE RISKS? WHERE ARE THE RISKS? WHERE ARE THE RISKS? WHERE ARE THE RISKS?

A striking phenomenon in recent years has been the speed of growth in EM corporate bond

markets. This growth has been driven both by the hunt for yield as global investors look

further afield, and by the ongoing development of EM bond markets more broadly. Since

2008, total corporate bonds outstanding have almost doubled, surpassing $6.8 trillion at end

-2014, significantly outpacing the growth of bank credit. While both financial and non-

financial corporate bonds have contributed to this sharp increase, the rise has been more

pronounced in the EM non-financial corporate bond market, which now totals more than $2.6

trillion—almost triple its level in 2008 (Chart 29).1 With hard currency (mainly USD) corporate

issuance at or near record levels in 2013-14 (Charts 30 and 31), total EM international (hard

currency) debt securities outstanding now total over $1.8 trillion, i.e. one fourth of the total.

Of this, some $520 billion is non-financial corporate, $575 billion is financial corporate, and

about $750 billion is government bonds.

As a result of this rapid growth, outstanding debt of the emerging market non-financial

corporate sector is now over 80% of GDP on average, up from about 60% in 2008; China,

Singapore and Hungary now have corporate debt well over 80% of GDP. A significant part of

this debt has been denominated in foreign currencies, about 25-30% in USD, prompting

concerns about vulnerabilities in many EM countries given recent dollar strength and

widespread anticipation of higher U.S. rates. Many EM firms have “natural hedges,” i.e. dollar

revenue streams, or may have hedged their USD exposure in derivatives markets. However,

those that have limited or no protection against currency risk are likely to face a higher

degree of credit and refinancing risk over the next few years.

Shift towards more bond marketShift towards more bond marketShift towards more bond marketShift towards more bond market----based borrowingbased borrowingbased borrowingbased borrowing

Strong growth in EM bond markets has contributed to a notable shift towards non-financial

corporate financing in most emerging market countries. For example, the share of bond

financing in total non-financial corporate debt financing has increased more than 20

percentage points in Korea and Mexico. Other countries, including Hungary, South Africa,

Indonesia, and Brazil have also witnessed a marked shift towards bond financing (Chart 32).

Chart 29Chart 29Chart 29Chart 29 Chart 30Chart 30Chart 30Chart 30

Our thanks to Elif Aksoy for insights and contributions to this section based on her work on EM corporate debt markets.

1 The BIS statistics by residence of issuer underestimate the size of the EM non-financial corporate sector, as they don’t include issuance via overseas

and offshore subsidiaries—this is particularly true for Brazilian, Chinese and Russian corporates.

0

25

50

75

100

125

2007 2011 2015

Non-fin

Fin

USDUSDUSDUSD Bond IssuanceBond IssuanceBond IssuanceBond Issuance$ billion

Source: Thomson One, IIF.

15

20

25

30

35

40

45

0

100

200

300

400

500

600

700

800

2007 2009 2011 2013 2015ytd

Other foreign currencyEURUSDLocal currencyShare of FC (rhs)

EMEMEMEM Corporates: Bond Issuance, by CurrencyCorporates: Bond Issuance, by CurrencyCorporates: Bond Issuance, by CurrencyCorporates: Bond Issuance, by Currency$ billion

Source: Thomson One, IIF. Data contain financial and non-financial EM30 corporate bond issuances

0 2 4 6

Fin. Corp. LC

Fin. Corp. HC

Non-fin. Corp. HC

Non-fin. Corp. LC

Sov HC

Sov LC

2014

2007

EM Corporate and Sovereign BondEM Corporate and Sovereign BondEM Corporate and Sovereign BondEM Corporate and Sovereign Bond MarketsMarketsMarketsMarkets$ trillion

Source: BIS, IIF.

Chart 31Chart 31Chart 31Chart 31

iif.com © Copyright 2015. The Institute of International Finance, Inc. All rights reserved.

page 16 CAPITAL FLOWS TO EMERGING MARKETS | MAY 28, 2015

While the majority of this bond financing has been in local currency (65-75%) over the past

few years) , the share of the issuance in foreign currency was over 50% in the first five

months of 2015— a fresh record high (Chart 33). While a shift toward more bond market

financing is part of the structural development of EM capital markets—as such a welcome

development—the speed of the increase in non-financial corporate debt in some

emerging markets is a cause for concern.

CrossCrossCrossCross----border bank lending also rose sharply in 2008border bank lending also rose sharply in 2008border bank lending also rose sharply in 2008border bank lending also rose sharply in 2008----13131313

While the focus has been on the rise in bonded debt, growth in cross-border bank lending

to the corporate sector has also been strong in recent years. Indeed, data on BIS-

reporting banks’ international claims on the EM non-bank private sector suggest a

sustained pickup in cross-border bank lending in the aftermath of the 2008 crisis to nearly

$3 trillion in 2014 (Chart 34), driven mainly by non-EU banks—notably, U.S., Japan, and

China. While almost all countries in our sample have increased reliance on cross-border

bank credit, firms in EM Asia and in oil-exporting countries have recorded the largest

buildup in cross-border banking liabilities.

Although some 8-9% of the outstanding stock of international EM loans is denominated in

euro (and would thus be less exposed to a strengthening USD), most of the remainder—

nearly $3 trillion—is USD-denominated.2 While the share of EUR-denominated bank

lending has been broadly stable—and Japanese and Chinese banks are becoming

increasingly important as a source of cross-border credit, primarily in yen and RMB—over

45% of new cross-border lending to EM borrowers was denominated in USD in 2013-14.

A closer look at the USD exposure of EM nonA closer look at the USD exposure of EM nonA closer look at the USD exposure of EM nonA closer look at the USD exposure of EM non----financial firmsfinancial firmsfinancial firmsfinancial firms

To identify specific countries and sectors that would be particularly vulnerable to a

stronger USD and higher U.S. rates, it is worth looking more closely at both the stock of

EM non-financial corporate debt relative to GDP, and at its breakdown by currency and

sector. China is the clearly the elephant in the room—non-financial corporate debt has

grown by more than 50 percentage points since 2008 to around 150% of GDP. However,

Chart 32Chart 32Chart 32Chart 32 Chart 34Chart 34Chart 34Chart 34

2 The series on the currency decomposition of the cross-border bank lending is based on Bloomberg data.

Chart 33Chart 33Chart 33Chart 33

0

10

20

30

40

50

2007 2011 2015

NonNonNonNon----Fin.Fin.Fin.Fin. Corporate Bond Corporate Bond Corporate Bond Corporate Bond Issuance in Foreign Currency Issuance in Foreign Currency Issuance in Foreign Currency Issuance in Foreign Currency percent

Share of USD

Share of EUR

Source: Thomsone One, IIF.

0 10 20 30 40 50

Turkey

Hungary

China

Indonesia

Russia

Brazil

Thailand

South Africa

Korea

Mexico

2014

2008

ShareShareShareShare of Bond Financing for EM Nonof Bond Financing for EM Nonof Bond Financing for EM Nonof Bond Financing for EM Non----financial Corporatesfinancial Corporatesfinancial Corporatesfinancial Corporatespercentage of total debt financing

Source: BIS, IIF.

0.0

0.8

1.6

2.4

3.2

1996 1999 2002 2005 2008 2011 2014

Government

Banks

Nonbank Private Sector

International Claims of BIS reporting Banks in EM30International Claims of BIS reporting Banks in EM30International Claims of BIS reporting Banks in EM30International Claims of BIS reporting Banks in EM30$ trillion

Source: BIS-CBS, IIF.

iif.com © Copyright 2015. The Institute of International Finance, Inc. All rights reserved.

page 17 CAPITAL FLOWS TO EMERGING MARKETS | MAY 28, 2015

other EM countries have also seen a notable increase in non-financial corporate sector

indebtedness, including Turkey, Brazil, and Russia (Charts 35). While a number of

countries, notably Korea, China and Russia, now have less USD exposure relative to GDP

than in 2008 (in some cases due to deliberate efforts to reduce such exposure), for many

EM countries USD exposure continues to be a significant proportion of overall debt

(except in a number of Central and East European countries, where euro-denominated

borrowing has been more prevalent). Across the emerging market countries in our

sample, USD borrowing exposure of the non-financial corporate sector stands at over

10% of GDP on average (Chart 36).3

Which emerging marketsWhich emerging marketsWhich emerging marketsWhich emerging markets————and sectorsand sectorsand sectorsand sectors————are most at risk from USD liabilities?are most at risk from USD liabilities?are most at risk from USD liabilities?are most at risk from USD liabilities?

In an environment of rising global interest rates, Fed tightening, EM currency

depreciation (Chart 37) and slowing economic growth and capital flows, USD-

denominated debt may become increasingly difficult for EM non-financial corporate

borrowers to repay. Some of these firms also suffer from significant reduction in oil and

commodity prices as well as a general slowdown in growth of global trade. Indeed, for

EM-30 countries, maturing USD non-financial corporate bonds and cross-border loans

total around $375 billion for the 2016-18 period (Chart 38)—a period when U.S. rates are

likely to be higher, making roll-over of credits more difficult. Against this backdrop, a key

question is how well EM corporates are hedged against potential currency mismatches

during stress episodes.

To identify vulnerabilities for specific countries and sectors, it is helpful to look both at

the stock of EM non-financial corporate debt relative to GDP, and at its breakdown by

currency and sector. Looking at specific sectors, a key question is to what extent

currency risk may be hedged—either via a natural hedge such as export revenues, or via

derivatives markets. Some corporate borrowers may also maintain significant foreign

currency assets on their balance sheets to offer a degree of protection for FX liabilities.

Chart 35Chart 35Chart 35Chart 35

Chart 38Chart 38Chart 38Chart 38

Chart 37Chart 37Chart 37Chart 37

Chart 36Chart 36Chart 36Chart 36

-10 0 10 20 30 40 50 60

South AfricaKorea

Saudi ArabiaIndia

ThailandMexicoPoland

HungaryCzech Rep.Indonesia

RussiaBrazilTurkeyChina

ChangeChangeChangeChange in EM Nonin EM Nonin EM Nonin EM Non----Financial Corporate DebtFinancial Corporate DebtFinancial Corporate DebtFinancial Corporate Debt----totototo----GDP RatioGDP RatioGDP RatioGDP Ratio

percentage point change since 2008

Source: BIS, IIF.

3 Underlying data in Chart 8 cover international and domestic debt securities as well as domestic and cross-border bank credit provided by the BIS.

Data on currency breakdown is based on IIF estimates.

95

100

105

110

115

120

125

130

135

2013 2014 2015

USD vs DM

USD vs EM

U.S. DollarU.S. DollarU.S. DollarU.S. Dollar

index, end-2012=100

U

USD Appreciates

Source: Bloomberg, IIF.

020406080100120140160

2015 2018 2021

USD Loans

USD Bonds

EMEMEMEM----30303030 USD denominated USD denominated USD denominated USD denominated Debt Maturity ProfileDebt Maturity ProfileDebt Maturity ProfileDebt Maturity Profile$ billions

Source: Bloomberg, IIF.

0 20 40 60 80 100 120 140 160

Indonesia

Mexico

South Africa

Brazil

Turkey

Thailand

Russia

Hungary

Korea

China

LC

USD

Others

EMEMEMEM NonNonNonNon----Financial Corporate Debt in 2014Financial Corporate Debt in 2014Financial Corporate Debt in 2014Financial Corporate Debt in 2014percent of GDP

Source: BIS, IIF estimates.

iif.com © Copyright 2015. The Institute of International Finance, Inc. All rights reserved.

page 18 CAPITAL FLOWS TO EMERGING MARKETS | MAY 28, 2015

Looking across the diverse range of EM countries and taking into account both the level of

corporate external debt and the structure of the economy, the impact of a stronger U.S. dollar is

likely to vary considerably:

■ More protected: More protected: More protected: More protected: commodity producers and exporters of manufactured goods typically have

a natural hedge as their revenues are primarily USD-denominated. Within the internationally

tradable EM corporate bond universe, these sectors (energy and basic metals) account for

around 30% of total outstanding bonds (Chart 39). However, it is important to note that

many such “hedged” EM corporates—oil and commodity producers in particular—have

seen prices of their exports fall substantially over the past year, reducing the value of their

natural hedges.

■ Indirect exposureIndirect exposureIndirect exposureIndirect exposure: Financial corporates are typically adequately hedged against currency

risk via derivatives markets, mainly due to regulatory requirements that limit the extent to

which banks can have currency mismatches. However, as some non-financial corporates are

not hedged against this risk, their FX risk may translate into credit risk for banks at times of

market stress. For example, Turkish banks have relatively small net open foreign currency

positions (around 3% of bank capital). However, the Turkish non-financial corporate sector

has FX liabilities of over $250 billion, and over $140 billion of this accounts for domestic FX

loans.

■ Little direct impactLittle direct impactLittle direct impactLittle direct impact: For others, a rising U.S. dollar may have little impact. Countries with

managed and pegged currencies, like China, Hong Kong and GCC, would be better

protected from higher debt service costs due to currency depreciation (Chart 40), though

rising global rates would affect their refinancing costs. The flip side, however, is that where

a currency peg proves to be unsustainable, corporates may be exposed to a sharp and

unexpected rise in their foreign currency liabilities in local currency terms when its peg

breaks down.

■ Limited vulnerabilityLimited vulnerabilityLimited vulnerabilityLimited vulnerability: Some countries/sectors face fewer risks, either because corporate

USD exposure is modest, and/or because there is some degree of hedging in place.

Although reliable data on hedging activities are limited, corporate sectors in countries such

as Mexico and Korea have relatively better access to more liquid domestic and offshore

markets, which can help in hedging currency mismatches. However, hedging markets in

Chart 39Chart 39Chart 39Chart 39 Chart 40Chart 40Chart 40Chart 40

Others -22.4%

CA Surplus Countries- 25.6%

South Africa, Turkey, Indonesia, India & Brazil -23.2%

Russia -10.4%

China - 10%

Hong Kong -8.5%

EMEMEMEM Corporate Bond Corporate Bond Corporate Bond Corporate Bond ---- Country BreakdownCountry BreakdownCountry BreakdownCountry Breakdown

Source: Market Vectors, IIF.

GCC -12.8%

Financials -40%

Energy - 22%

Utilities -8.3%

Communications - 8.1%

Basic Materials-7.6%

Consumer -6.4% Other -

7.6%

Source: Market Vectors, IIF.

EMEMEMEM Corporate Bond Corporate Bond Corporate Bond Corporate Bond ---- Industry BreakdownIndustry BreakdownIndustry BreakdownIndustry Breakdown

The impact of a The impact of a The impact of a The impact of a stronger U.S. stronger U.S. stronger U.S. stronger U.S. dollar is likely to dollar is likely to dollar is likely to dollar is likely to vary considerably.vary considerably.vary considerably.vary considerably.

iif.com © Copyright 2015. The Institute of International Finance, Inc. All rights reserved.

page 19 CAPITAL FLOWS TO EMERGING MARKETS | MAY 28, 2015

most EMs are not well developed, with high associated costs continuing to

discourage many firms from hedging FX risk. As noted by the BIS, one big issue is

the lack of liquidity in hedging markets, particularly in times of stress. Given that

exposures are typically hedged with more liquid short-term contracts in an attempt

to reduce hedging costs, it becomes harder to roll over these contracts as swap

dealers become less willing to sell protection (as seen during the 2013 taper

tantrum and the oil price shock of H2 2014). In some countries, like Brazil, central

banks with ample reserves may step in to provide currency hedges to corporates at

times of stress. However, the expectation of such behavior can also serve to

discourage development of private hedging markets.

■ Higher riskHigher riskHigher riskHigher risk: Specific sectors in some countries are at higher risk due to high levels of

USD exposure and/or a lack of natural hedges and access to derivatives markets. In

particular, firms in the consumer and real estate sectors with local currency revenues

and FX expenses seem to be more exposed to currency risks. This may pose

particular problems for these sectors in countries with economic/political

vulnerabilities (see pages 10-12).

Against this backdrop, with EM corporate issuers facing a diverse set of risks, careful

attention to credit selection is warranted by investors. While broad valuation measures

(e.g., EMBIG spreads) continue to look attractive relative to those in comparable asset

classes (and relative to their long-run averages), bottom-up analysis of currency and

refinancing risks will be increasingly important in an environment of rising U.S. rates.

One big issue is One big issue is One big issue is One big issue is the lack of the lack of the lack of the lack of liquidity in liquidity in liquidity in liquidity in hedging markets, hedging markets, hedging markets, hedging markets, particularly in particularly in particularly in particularly in times of stress. times of stress. times of stress. times of stress.

iif.com © Copyright 2015. The Institute of International Finance, Inc. All rights reserved.

page 20 CAPITAL FLOWS TO EMERGING MARKETS | MAY 28, 2015

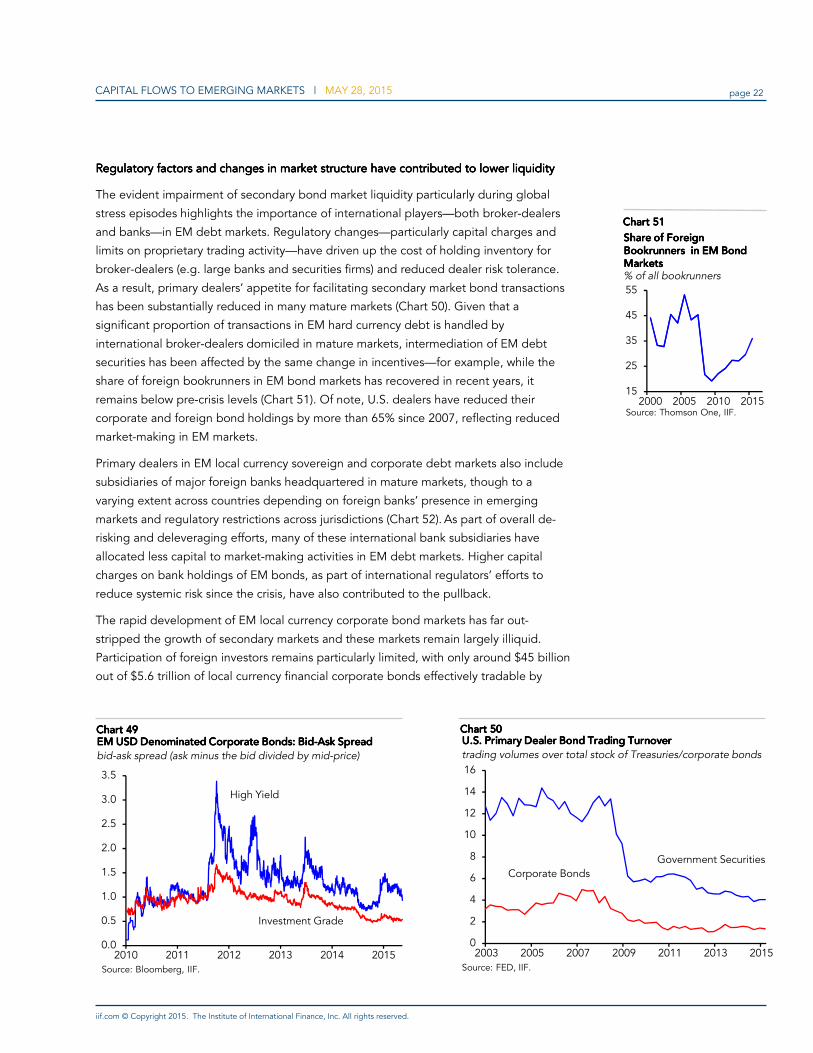

SECONDARY MARKET LIQSECONDARY MARKET LIQSECONDARY MARKET LIQSECONDARY MARKET LIQUIDITY IN EMERGING MARKETSUIDITY IN EMERGING MARKETSUIDITY IN EMERGING MARKETSUIDITY IN EMERGING MARKETS————HOW BAD IS ITHOW BAD IS ITHOW BAD IS ITHOW BAD IS IT? ? ? ?

The landscape of portfolio debt investment in emerging markets has evolved

considerably since the 2008 global crisis. The EM debt universe has more than doubled

from $6.5 trillion in 2007 to $13.5 trillion in 2014, supported by robust appetite for EM

debt securities related to the hunt for yield in a low-rate environment (Chart 41).1 Another

contributing factor has been the rapid pace of market development in recent years,

including development of local currency bond markets and capital markets infrastructure

more broadly. However, this robust expansion has also been associated with new

vulnerabilities, including a rapid rise in non-financial corporate indebtedness (see

previous section) and an increasing concern about the lack of liquidity, as market-making

capacity has not kept pace with growth in market capitalization.

Although secondary bond market liquidity more broadly has been under periodic

scrutiny since the onset of the 2008 crisis, the full extent of liquidity risk in EM bond

markets was not on most radar screens until the 2013 taper tantrum. The sharp

retrenchment in foreign portfolio flows into EM debt markets during the summer of 2013

was associated with a surge in EM asset price volatility and a decline in liquidity (Charts

42 and 43).

Notional trading activity in EM debt markets remains below pre-crisis levels (Chart 43)

and has lagged the growth in market capitalization. Hard currency sovereign bond

turnover ratio has more than halved since the crisis (Chart 45). Moreover, trading

volumes in both local currency and corporate debt markets have failed to keep pace with

the surge in bond issuance in recent years and turnover in these two markets is only

around 50% and 25% of the turnover in hard-currency sovereign bonds, respectively.

Available data suggest that the decline in sovereign turnover ratios has been widespread

across a range of both mature and emerging markets, but has been more pronounced in

emerging markets. Brazil and Hong Kong have recorded the largest drop among the

0

2

4

6

8

10

12

14

1998 2002 2006 2010 2014

Hard Currency Corporate

Local Currency Corporate

Hard Currency Sovereign

Local Currency Sovereign

EmergingEmergingEmergingEmerging Market Debt MarketsMarket Debt MarketsMarket Debt MarketsMarket Debt Markets$ trillion

Source: BIS, IIF.

Chart 41Chart 41Chart 41Chart 41

2

4

6

8

10

12

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2012 2013 2014 2015

Fund Flows

Volatility of yields*

EM Local Currency Bond Fund Flows EM Local Currency Bond Fund Flows EM Local Currency Bond Fund Flows EM Local Currency Bond Fund Flows $ billion percent, 180-days volatility

Source: Bloomberg, EPFR, IIF; *Volatilty of CEMBI yields

Chart 43Chart 43Chart 43Chart 43

1. Our sample includes Argentina, Brazil, China, Taiwan (China), Chile, Colombia, Croatia, Czech Republic, Hungary, India, Indonesia, Israel,

South Korea, Malaysia, Mexico, Pakistan, Peru, Philippines, Poland, Russia, Saudi Arabia, South Africa, Thailand, and Turkey.

3.5

5.0

6.5

8.0

May 12 Nov 13 May 15

BidBidBidBid----Ask Spreads for EM Ask Spreads for EM Ask Spreads for EM Ask Spreads for EM Local Currency Gov't BondsLocal Currency Gov't BondsLocal Currency Gov't BondsLocal Currency Gov't Bondsbps, 10-yr bonds

Source: Bloomberg, IIF.

Chart 42Chart 42Chart 42Chart 42

1

2

3

4

5

6

7

2002 2006 2010 2014

HC corp. HC gov't.LC bonds