Capital expenditure

16

Capital Expenditure A consumer company’s Case Study

-

Upload

imran-qadri -

Category

Economy & Finance

-

view

173 -

download

1

Transcript of Capital expenditure

Capital

ExpenditureA consumer company’s Case Study

Introduction to Case

1. Bank Manager

3. New Office – Human and Intellectual Capital

2. Looking for New Business Opportunities

4. Successfully set a Meeting with MD of HICL

Growth

Meeting Outcomes

4. Needs Medium Term Financing of 1.2 Million

5. Six years Old Business, going through rapid

expansion, with 95 employees,

6. From 3 different location to the new One

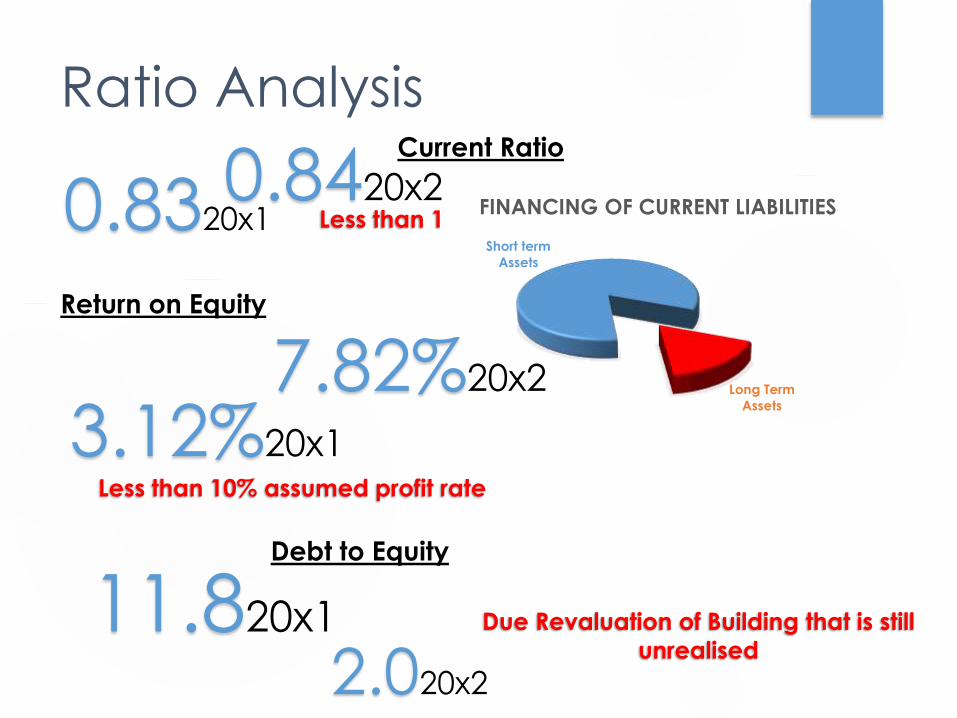

Ratio Analysis

HUMAN & INTELLECTUAL CAPITAL LIMITED

Ratios and Other Information

As at May 31 Year 20X1 Year 20X2 Year 20X2 (4 months to 30th Sep) 20X3 (12 months to 30 May)

Forecast Actual Forecast

Liquidity

Current ratio 0.83:1 0.84:1

Acid (Quick) test ratio 0.81:1 0.83:1 0.51:1 0.44:1

Efficiency

Credit given (days) 89 81 52 38

Credit taken (days) 83 90 70 69

Profitability

Gross profit margin (%) 28 32.9 35.7 34.3 36

Net profit margin (%) 1.3 3.8 9.7 5.6 6.3

Financial Structure

Gearing (%) (To compute the ratio)

Interest/finance charges cover (times) 4.4 4 7.3 3.6 5.2

Net working assets to sales (%) 3.2 6.1

Retained profit to sales (%) 1.1 2.1

11.8 2.0

Balance Sheet’s AnalysisTrend Analysis

0.00% 200.00% 400.00% 600.00% 800.00%1000.00%

Cash

Debtors

Stock

Total Current Assets

Total Fixed Assets

Total Assets

Bank overdraft

LT Debt current portion

Current Tax

Total Currrent Liabilities

Long term financing

Total Longterm Liabilities

Distributable reserves

Shareholders' funds

Total Liabilities & SHE

Trend Analysis

Revaluation Reserve

523,369in Shareholder Fund

Creditors

Hire Purchase

Bank overdraft

LT Debt current

portionCurrent Tax

Term liabilities

Hire Purchase

over 12 months

Long term

financingRevaluation

reserve

Distributable

reserves

Shareholders'

funds

COMMON SIZE ANALYSIS 20X2

Creditors

Hire Purchase

Bank overdraftLT Debt current

portion

Current Tax

Term liabilities

Hire Purchase

over 12 months

Long term

financing

Distributable

reserves

Shareholders'

funds

20X1

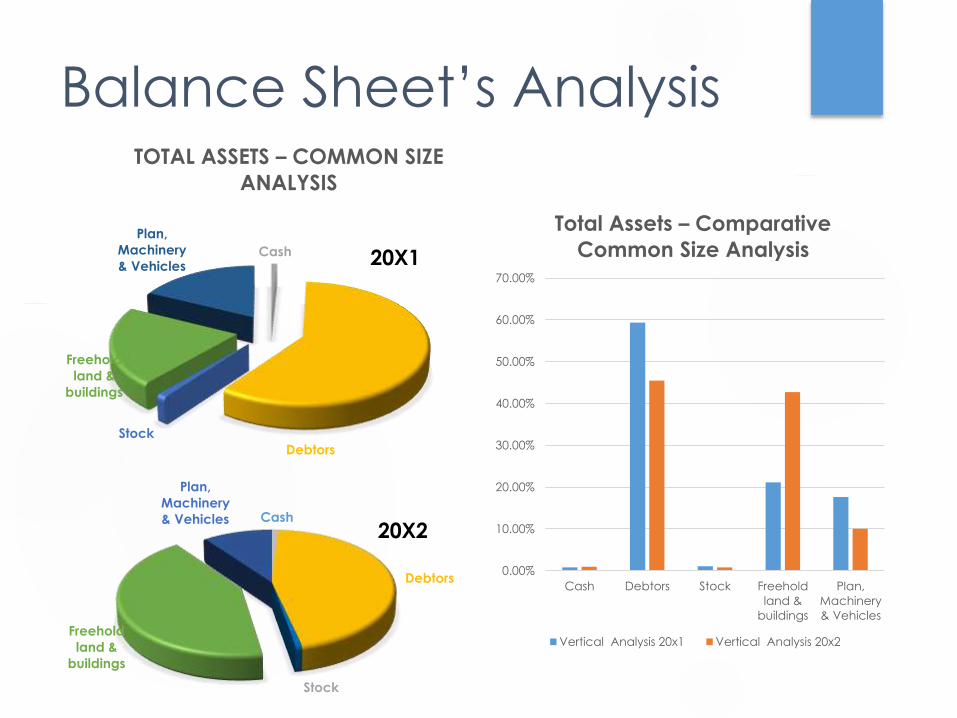

Balance Sheet’s Analysis

Cash

Debtors

Stock

Freehold

land &

buildings

Plan,

Machinery

& Vehicles

TOTAL ASSETS – COMMON SIZE

ANALYSIS

Cash

Debtors

Stock

Freehold

land &

buildings

Plan,

Machinery

& Vehicles20X2

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

Cash Debtors Stock Freehold

land &

buildings

Plan,

Machinery

& Vehicles

Total Assets – Comparative

Common Size Analysis

Vertical Analysis 20x1 Vertical Analysis 20x2

20X1

Balance Sheet’s Analysis

0.00% 10.00% 20.00% 30.00% 40.00% 50.00% 60.00%

Creditors

Hire Purchase

Bank overdraft

LT Debt current portion

Current Tax

Term liabilities

Hire Purchase over 12 months

Long term financing

Revaluation reserve

Distributable reserves

Shareholders' funds

Common size Analysis - Total Liabilities Comparative

Common size Analysis 20x2 Common size Analysis 20x1

Income Statement

HUMAN & INTELLECTUAL CAPITAL LTD

Profit & Loss Account Summary

12 months to May 31 Year 20X1 Year 20X2

4 months to 30th Sep Year 20X2

4 months to 30th Sep 20X2

20X3 (12 months to 30 May)

Adjusted Calculation

Forecast Actual Forecast

Sales2,685,374 5,234,983 2,433,000 2,111,842 7,398,000

Profit after tax34,549 198,829 235,000 119,136 466,000 236,244

Interest (Finance

charge) 10,097 65,193 37,266 45,304 111,700 135,795

Depreciation38,429 45,267 16,800 16,800 54,000

Directors' remuneration47,298 63,663 20,000 20,000 85,000

Tax @ 30% Assume14,784 98,932

EBITDA97,859 408,221 289,066 181,240 631,700

EBIT59,430 362,954 272,266 164,440 577,700

Expected Interest260,795

Interest Coverage with EBIT1.3917

Int Cov with EBITDA1.5653

Ratio Analysis

Return on Equity

Current Ratio

0.8320x10.8420x2

3.12%20x1

7.82%20x2

Less than 1

Less than 10% assumed profit rate

Short term

Assets

Long Term

Assets

FINANCING OF CURRENT LIABILITIES

Debt to Equity

11.820x1

2.020x2

Due Revaluation of Building that is still

unrealised

Agreement in PrinciplesProposed Loan Calculations

1. $1.25 Million Loan Principle

2. At 10% Profit Margin, Total Payable in 5 years

$ 1.875 Million

3. First Year debt repayment

$ 115,871 Interest

$ 318,706 Installment

4. Adjusted Expected Interest payment for 20x3

$ 260,795 Adjusted Exp + New Facility

Agreement in PrinciplesInterest Coverage Ratio for 20X3 with New Loan

Interest

1. 362,954 EBIT 20X3 & 408,221 EBITD 20X3

2. 362,954/260,795 IC

3. IC = 1.39 or 1.56 i.e < 2

Agreement in Principles

“YES”, subject to certain conditions

Past 3 Years Audited Accounts

5 year Projected Mgmt Accounts

130% Collateral/Charge

Other Facilities

Bai Inah Cash Line (OD) Financing - i

(2nd contract)

Customer Bank

Asset (owned

by the Bank)

Customer applies financing from the bank

2. When ownership of the asset transferred to

customer ,simultaneously the asset is sold back

to the Bank at a price equivalent to financing

amount and the Bank pays on cash basis to

customer as principal limit of Cash Line, made

available in customer’s Wadiah Current Account

1. Bank sells their asset at a selling price (financing

amount plus profit margin) on deferred term.

(1st contract)

Customer pays profit for utilized amount on

monthly basis. Profit on unutilized portion is

rebated

Other Facilities

Customer

Seller/

Supplier

Bank

Buyer1. Sells on credit term

2. Presents the debt (invoices) and

bank purchases the debt arising

from the sale transaction and

pays the Bank on maturity

3. Settles the

purchase price

on or before

maturity date

Bai Al Dayn Working Capital Financing i (BWCF)