CAPITAL BUDGETING Involves decision to invest current funds of a business concern most effectively...

26

CAPITAL BUDGETING Involves decision to invest current funds of a business concern most effectively in long-term activities, in anticipation of an expected flow of future benefits over a series of years in future.

-

Upload

sara-rodgers -

Category

Documents

-

view

215 -

download

2

Transcript of CAPITAL BUDGETING Involves decision to invest current funds of a business concern most effectively...

CAPITAL BUDGETING

Involves decision to invest current funds of a business concern most effectively in long-term activities, in anticipation of an expected flow of future benefits over a series of years in future.

CAPITAL BUDGETING

Importance of Capital Budgeting:-

1. Long term implications for the firm

2. Involve committing large funds

3. They are irreversible decisions.

4. Among the most difficult decisions to make.

CAPITAL BUDGETING

Features of Capital Investment Decisions:-

1. Exchange of current funds for future benefits.

2. Funds invested in long-term assets

3. Future benefits will occur over a series of years.

CAPITAL BUDGETING

INVESTMENT EVALUATION CRITERIA:

INVOLVES:-

1. ESTIMATION OF CASH FLOWS.

2. ESTIMATION OF REQUIRED RATE OF RETURN

3. APPICATION OF A DECISION TECHNIQUE FOR MAKING THE CHOICE

CAPITAL BUDGETING

DECISION- TECHNIQUES:-

TRADITIONAL

1. PAY-BACK METHOD

2. AVERGE RATE OF RETURN(ARR)-

RETURN ON INVESTMENT METHOD

CAPITAL BUDGETING

DECISION-TECHNIQUES:-

DISCOUNTED-CASH FLOW(DCF)-

TIME-ADJUSTED METHODS

1. NET PRESENT VALUE METHOD(NPV)

2. INTERNAL RATE OF RETURN(IRR)

3. TERMINAL VALUE METHOD

4. PROFITABILITY INDEX

CAPITAL BUDGETING

SOME CAPITAL BUDGETING DECISIONS1. Mechanisation of a Division2. Replacing or modernising a process3. Mutually exclusive decisions in selecting a

machine4. Buy or Lease decisions-comparative

profitability5. Business expansion by capital investments.

CAPITAL BUDGETING

INVESTMENT DECISIONS:-PAY-BACK METHOD

PAY BACK PERIOD (PBP)= TOTAL CASH OUTFLOWS ANNUAL CASH FLOWS FROM OPERATIONS

If Rs. 60000 invested today yields annual cash inflow of Rs. 15000 for 6 years, the Pay Back Period= 60000/15000 = 4 years.

PROJECT WITH LEAST PBP IS ACCEPTED

CAPITAL BUDGETING

PAY BACK METHOD:-

LIMITATIONS:-

1. Does not give weightage to total earnings

2. Time value of money not recognised

MERITS:-

a. Very simple and popular.

b. Good in unstable conditions

CAPITAL BUDGETING

AVERAGE RATE OF RETURN(ROI)

METHOD :-

Average annual profit after Tax x 100

Average investment over the life of the product

Average Profit=Sum of Profits over the life of the asset / No. of years.

Average investment= Original Investment-scrap value / 2

CAPITAL BUDGETING

ARR METHOD:-

Advantages:-

Can be readily calculated

Simple in application

Entire stream of income is considered

Useful as a good performance evaluation

and control measure.

CAPITAL BUDGETING

ARR METHOD:-SHORTCOMINGS:-1. CASH FLOWS IGNORED2. TIME VALUE OF MONEY IGNORED3. AVERGE RETURNS vs. CURRENT

RETURNS4. LESS USEFUL FOR INVESTMENT

DECISIONS.

CASH BUDGETING

DISCOUNTED CASH FLOW METHODS:-NET PRESENT VALUE METHOD:-The difference between present value of cash

inflows and cash outflows. The firm’s opportunity cost of capital being the discount rate.

If Positive (> 0) = ACCEPTIf Negative (< 0) = REJECT

CAPITAL BUDGETING

PV OF FUTURE CASH INFLOWS=

s

(1 + r)^n

Where s = Cash inflow expected

r = rate of interest

n = no. of years.

i.e. S = P (1+ r)^n

CAPITAL BUDGETING

NPV METHOD:-

MERITS:-

1. Considers all cash flows.

2. True measure of profitability

3. Time value of money reckoned

4. Consistent with wealth maximisation principle

CAPITAL BUDGETING

NPV METHOD:-

DE-MERITS:-

1. TEDIOUS ESTIMATES

2. DISCOUNT RATE-COMPUTATION

3. SENSITIVE TO DISCOUNT RATES

STILL REGARDED AS MOST EFFECTIVE

CAPITAL BUDGETING

IRR METHOD( YIELD METHOD): IRR is the discount rate which equates the

present value of an investment’s cash inflows and outflows.

IF IRR > K(COST)-----ACCEPT IF IRR = K(COST)-----MAY ACCEPT IF IRR < K(COST)-----REJECT IF IRR = K, NPV = 0

CAPITAL BUDGETING

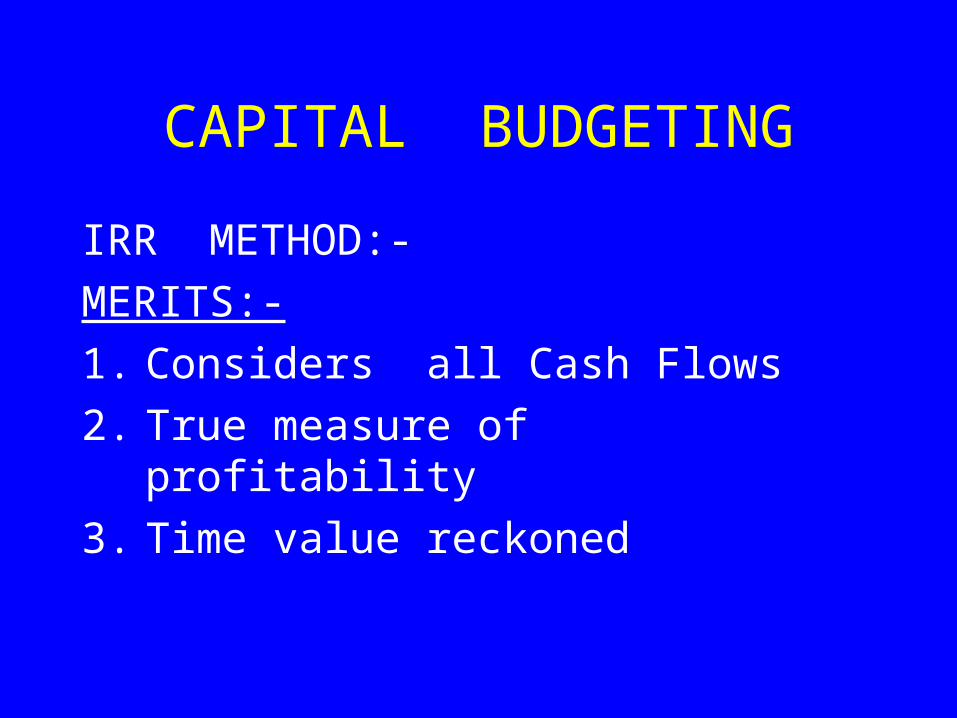

IRR METHOD:-

MERITS:-

1. Considers all Cash Flows

2. True measure of profitability

3. Time value reckoned

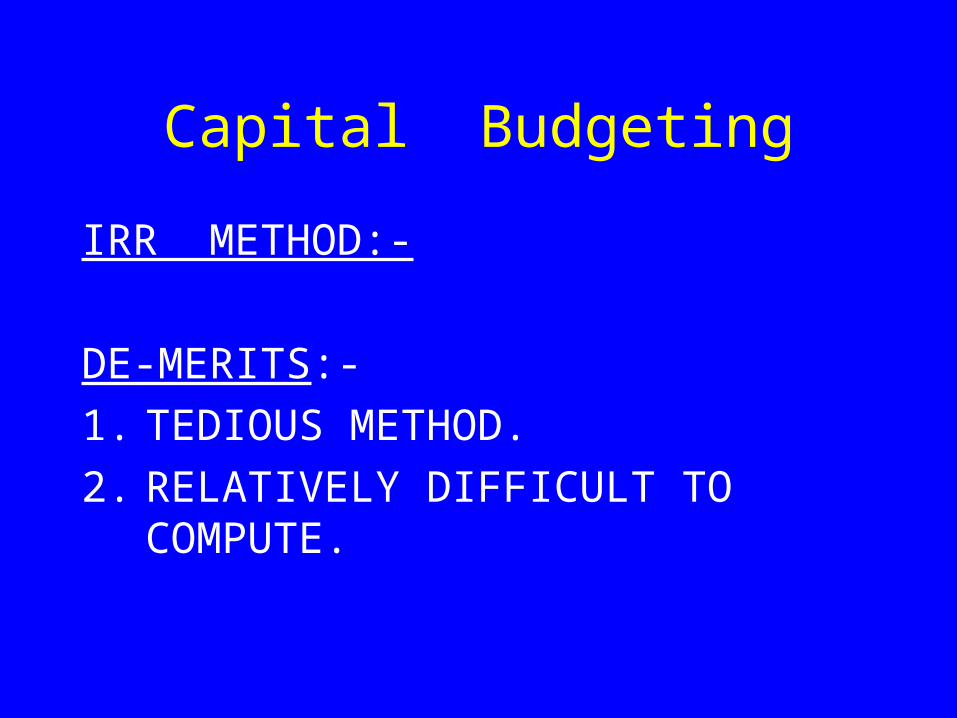

Capital Budgeting

IRR METHOD:-

DE-MERITS:-

1. TEDIOUS METHOD.

2. RELATIVELY DIFFICULT TO COMPUTE.

CAPITAL BUDGETING

NPV vs IRR:-

INTERPOLATION METHOD:-

When one comes across two rates of NPV-

One positive NPV & One negative NPV

IRR by Interpolation:-

Lower rate + NPV at Lower rate x rate differential.

Absolute difference of both NPVs

CAPITAL BUDGETING

IRR by INTERPOLATION-

e.g.:-

At 10% say NPV of cash flows = Rs. 200( +)

At 12% say NPV pf cash flows = Rs. 210( -)

IRR = 10% + 200 x ( 12-10)

(200 + 210)

10% + 0.98 = 10.98%

CAPITAL BUDGETING

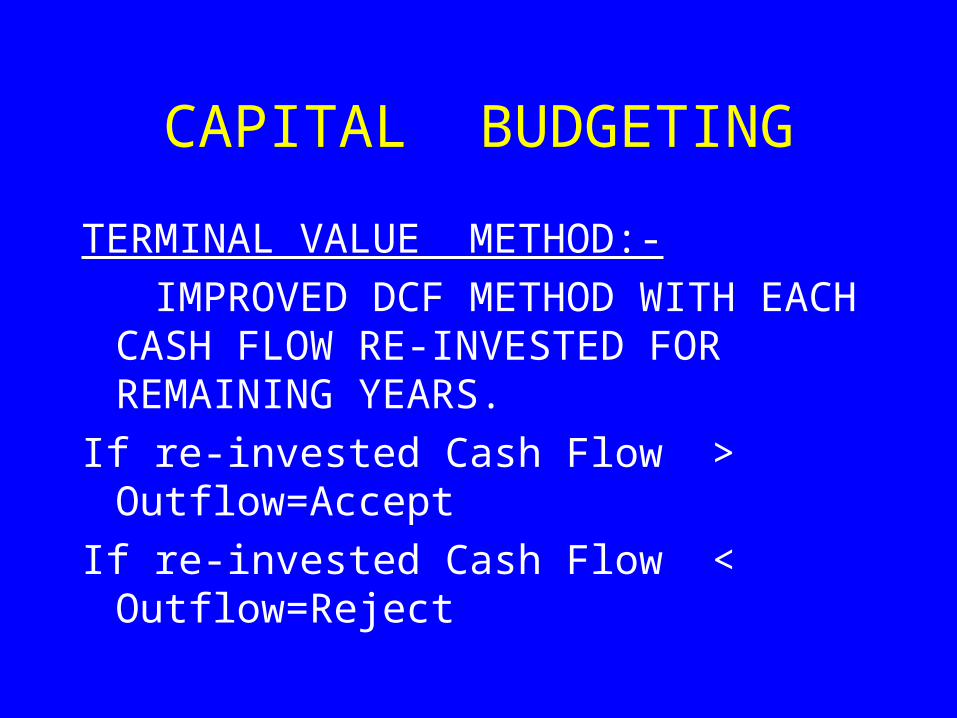

TERMINAL VALUE METHOD:-

IMPROVED DCF METHOD WITH EACH CASH FLOW RE-INVESTED FOR REMAINING YEARS.

If re-invested Cash Flow > Outflow=Accept

If re-invested Cash Flow < Outflow=Reject

CAPITAL BUDGETING

PROFITABILITY INDEX:-

Present Value of Cash Inflows

Present Value of Cash Outflows

It is a relative measure and provides solution for projects requiring initially different levels of investment

APPLY WHEN NPV IS SAME IN 2 CASES

CAPITAL BUDGETING

PROFITABILITY INDEX FOR PROJECT APPRAISAL

Project-A Project-B Project-C

Cash Outflows 10000 20000 40000

PV –Inflows 14000 25000 52000

NPV 4000 5000 12000

RANKING III II I

P. INDEX 1.40 1.25 1.30

RANKING BY PI I III II

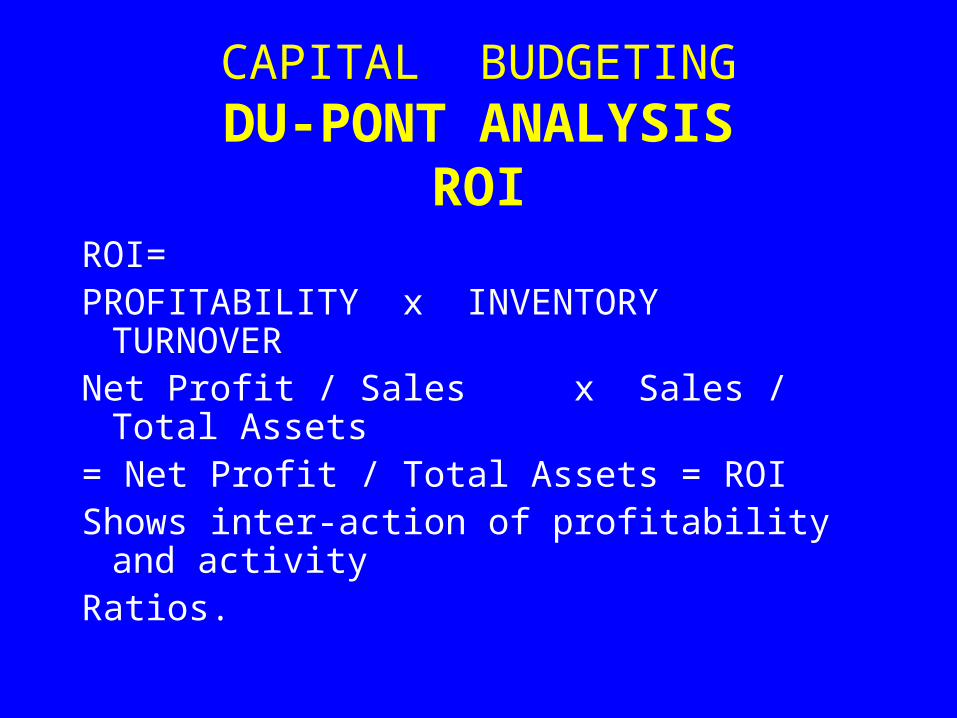

CAPITAL BUDGETINGDU-PONT ANALYSIS

ROIROI= PROFITABILITY x INVENTORY

TURNOVERNet Profit / Sales x Sales / Total Assets= Net Profit / Total Assets = ROIShows inter-action of profitability and activityRatios.

CAPITAL BUDGETINGDU-PONT ANALYSIS

ROIIt shows that performance can be improved

Either by-

(a) Generating more sales volume per rupee of investment. OR

(b) Increasing the profit margin per rupee of sales.

A CENTRAL MEASURE OF OVERALL PROFITABILITY AND OPERATIONAL EFFICIENCY