Practice of capital budgeting Monty Hall game Incremental cash flows Puts and calls.

of 49

Upload

arun-s-bharadwajCategory

view

232download

18/13/2019 Capital Budgeting and Cash Flows

1/49

PROJECT APPRAISAL CRITERIA

8/13/2019 Capital Budgeting and Cash Flows

2/49

CAPITAL EXPENDITURES AND THEIR

IMPORTANCE

The basic characteristics of a capital expenditure (also

referred to as a capital investment or just project) is that

it involves a current outlay (or current and futureoutlays) of funds in the receiving a stream of benefits infuture

Importance stems from

Long-term consequences

Substantial outlays

Difficulty in reversing

8/13/2019 Capital Budgeting and Cash Flows

3/49

PROCESS

Identification of Potential Investment Opportunities

Assembling of Investment Proposals

Decision Making

Preparation of Capital Budget and Appropriations

Implementation

Performance Review

8/13/2019 Capital Budgeting and Cash Flows

4/49

PROJECT CLASSIFICATION

Mandatory Investments

Replacement Projects

Expansion Projects

Diversification Projects

Research and Development Projects

Miscellaneous Projects

8/13/2019 Capital Budgeting and Cash Flows

5/49

INVESTMENT CRITERIA

INVESTMENT

CRITERIA

DISCOUNTING

CRITERIA

NON-DISCOUNTING

CRITERIA

NET

PRESENTVALUE

BENEFIT

COSTRATIO

INTERNAL

RATE OFRETURN

PAYBACK

PERIODACCOUNTING

RATE OFRETURN

8/13/2019 Capital Budgeting and Cash Flows

6/49

PAYBACK PERIOD

Payback period is the length of time required to recover the initial

outlay on the projectCapital Project

Year Cash flow Cumulative cash flow

0 -100 -100

1 34 - 66

2 32.5 -33.53 31.37 - 2.13

4 30.53 28.40

Pros Cons

Simple Fails to consider the time valueof money

Rough and ready method Ignores cash flows beyond thefor dealing with risk payback period

Emphasises earlier cash inflows

8/13/2019 Capital Budgeting and Cash Flows

7/49

Payback The payback period of a project is the number of

years it takes before the cumulative forecastedcash flow equals the initial outlay.

The payback rule says only accept projects thatpayback in the desired time frame.

This method is flawed, primarily because itignores later year cash flows and the the present

value of future cash flows.

8/13/2019 Capital Budgeting and Cash Flows

8/49

PaybackExample

Examine the three projects and note the mistakewe would make if we insisted on only takingprojects with a payback period of 2 years or less.

502050018002000-C

58-2018005002000-B

2,624350005005002000-A

10%@NPVPeriod

PaybackCCCCProject 3210

+

+

8/13/2019 Capital Budgeting and Cash Flows

9/49

8/13/2019 Capital Budgeting and Cash Flows

10/49

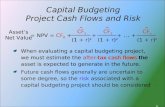

NET PRESENT VALUE

n CtNPV = Initial investment

t=1 (1 +rt )t

8/13/2019 Capital Budgeting and Cash Flows

11/49

NET PRESENT VALUE

The net present value of a project is the sum of the present value of all the cash

flows associated with it. The cash flows are discounted at an appropriate discount

rate (cost of capital)

Capital Project

Year Cash flow Discount factor (15%) Presentvalue

0 -100.00 1.000 -100.00

1 34.00 0.870 29.58

2 32.50 0.756 24.57

3 31.37 0.658 20.64

4 30.53 0.572 17.46

5 79.90 0.497 39.71

Sum = 31.96

Pros Cons

Reflects the time value of money Is an absolute measure and not a relative

Considers the cash flow in its entirely measure

Squares with the objective of wealth maximisation

8/13/2019 Capital Budgeting and Cash Flows

12/49

NPV

8/13/2019 Capital Budgeting and Cash Flows

13/49

PROPERTIES OF THE NPV RULE

NPVs ARE ADDITIVE

INTERMEDIATE CASH FLOWS ARE INVESTED AT

COST OF CAPITAL

NPV CALCULATION PERMITS TIME-VARYINGDISCOUNT RATES

NPV OF A SIMPLE PROJECT AS THE DISCOUNT

RATE

8/13/2019 Capital Budgeting and Cash Flows

14/49

BENEFIT COST RATIO

PVB

Benefit-cost Ratio :BCR =

I

PVB = present value of benefits

I = initial investment

To illustrate the calculation of these measures, let us consider a project which is being evaluatedby a firm that has a cost of capital of 12 percent.

Initial investment : Rs 100,000

Benefits: Year 1 25,000

Year 2 40,000Year 3 40,000

Year 4 50,000

The benefit cost ratio measures for this project are:

25,000 40,000 40,000 50,000

(1.12) (1.12)2 (1.12)3 (1.12)4

BCR = = 1.145

100,000

Pros Cons

Measures benefit per buck Provides no means for aggregation

+ + +

8/13/2019 Capital Budgeting and Cash Flows

15/49

Discount rate

Net Present Value

INTERNAL RATE OF RETURN

The internal rate of return (IRR) of a project is the discount rate that

makes its NPV equal to zero. It is represented by the point of intersectionin the above diagram

Net Present Value Internal Rate of Return

Assumes that the Assumes that the netdiscount rate (cost present value is zero

of capital) is known.

Calculates the net Figures out the discount rate

present value, given that makes net present value zero

the discount rate.

8/13/2019 Capital Budgeting and Cash Flows

16/49

IRR

8/13/2019 Capital Budgeting and Cash Flows

17/49

NPV & IRR

8/13/2019 Capital Budgeting and Cash Flows

18/49

PROBLEMS WITH IRR

NON-CONVENTIONAL CASH FLOWS

MUTUALLY EXCLUSIVE PROJECTS

LENDING VS. BORROWING

DIFFERENCES BETWEEN SHORT-TERM AND

LONG-TERM INTEREST RATES

8/13/2019 Capital Budgeting and Cash Flows

19/49

Internal Rate of ReturnPitfall 1 - Lending or Borrowing? With some cash flows the NPV of the project increases

s the discount rate increases. This is contrary to the normal relationship between NPV

and discount rates.

364%50500,1000,1364%50500,1000,1

%10@Project 10

++

+++

B

A

NPVIRRCC

8/13/2019 Capital Budgeting and Cash Flows

20/49

Internal Rate of ReturnPitfall 2 - Multiple Rates of Return Certain cash flows can generate NPV=0 at two different discount rates.

The following cash flow generates NPV= 0 at both IRR% of (-44%)and +11.6%.

600

NPV

300

0

-30

-600

Discount

Rate

IRR=11.6%

IRR=-44%

8/13/2019 Capital Budgeting and Cash Flows

21/49

IRR

8/13/2019 Capital Budgeting and Cash Flows

22/49

Internal Rate of Return

Pitfall 2 - Multiple Rates of Return

It is possible to have a zero IRR and a positive NPV

339500,2000,3000,1

%10@Project 210

++++ NoneC

NPVIRRCCC

8/13/2019 Capital Budgeting and Cash Flows

23/49

8/13/2019 Capital Budgeting and Cash Flows

24/49

Internal Rate of ReturnPitfall 3 - Mutually Exclusive Projects

8/13/2019 Capital Budgeting and Cash Flows

25/49

Profitability Index When resources are limited, the profitability

index (PI) provides a tool for selecting amongvarious project combinations and alternatives

A set of limited resources and projects can yieldvarious combinations.

The highest weighted average PI can indicatewhich projects to select.

8/13/2019 Capital Budgeting and Cash Flows

26/49

Profitability Index

Investment

NPVIndexityProfitabil =

8/13/2019 Capital Budgeting and Cash Flows

27/49

Profitability Index

121555

1620552153010

%10@Project 210

++

++

++

C

BA

NPVCCC

121555

1620552153010

%10@Project 210

++

++

++

C

BA

NPVCCC

8/13/2019 Capital Budgeting and Cash Flows

28/49

Profitability Index

2.4125C

3.2165B2.12110A

IndexityProfitabil($)NPV($)InvestmentProject

2.4125C

3.2165B2.12110A

IndexityProfitabil($)NPV($)InvestmentProject

Cash Flows ($ millions)

8/13/2019 Capital Budgeting and Cash Flows

29/49

Profitability IndexProj NPV Investment PI

A 230,000 200,000 1.15

B 141,250 125,000 1.13C 177,600 160,000 1.11

D 162,000 150,000 1.08

Select projects with highest Weighted AvgPI

WAPI (BD) = 1.13(125) + 1.08(150) + 0.0 (25)(300) (300) (300)

= 1.01

8/13/2019 Capital Budgeting and Cash Flows

30/49

Profitability IndexProj NPV Investment PI

A 230,000 200,000 1.15

B 141,250 125,000 1.13C 177,600 160,000 1.11

D 162,000 150,000 1.08

Select projects with highest Weighted AvgPI

WAPI (BD) = 1.01WAPI (A) = 0.77

WAPI (BC) = 1.06

8/13/2019 Capital Budgeting and Cash Flows

31/49

Multi Period

121555

162055

2153010

%10@Project 210

++

++

++

C

B

A

NPVCCC

121555

162055

2153010

%10@Project 210

++

++

++

C

B

A

NPVCCC

4.0

136040%10@Project 210

PI

D

NPVCCC

+

4.0

136040%10@Project 210

PI

D

NPVCCC

+

8/13/2019 Capital Budgeting and Cash Flows

32/49

Linear Programming Maximize Cash flows or NPV

Minimize costs

Example

Max NPV = 21Xn + 16 Xb + 12 Xc + 13 Xdsubject to

10Xa + 5Xb + 5Xc + 0Xd

8/13/2019 Capital Budgeting and Cash Flows

33/49

INVESTMENT APPRAISAL

IN PRACTICE

Over time, discounted cash flow methods have gained in

importance and internal rate of return is the mostpopular evaluation method.

Firms typically use multiple evaluation methods.

Accounting rate of return and payback period are

widely employed as supplementary evaluation methods.

8/13/2019 Capital Budgeting and Cash Flows

34/49

CFO Decision Tools

Profitability

Index, 12%

Payback, 57%

IRR, 76%

NPV, 75%

Book rate of

return, 20%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Survey Data on CFO Use of Investment Evaluation Techniques

SOURCE: Graham and Harvey, The Theory and Practice of Finance: Evidence from the Field,

Journal of Financial Economics

8/13/2019 Capital Budgeting and Cash Flows

35/49

Be consistent in how you handle inflation!!Use nominal interest rates to discount

nominal cash flows.

Use real interest rates to discount real cash

flows.

You will get the same results, whether youuse nominal or real figures

InflationINFLATION RULE

8/13/2019 Capital Budgeting and Cash Flows

36/49

InflationExample

You own a lease that will cost you 8,000 nextyear, increasing at 3% a year (the forecastedinflation rate) for 3 additional years (4 years

total). If discount rates are 10% what is thepresent value cost of the lease?

1 + real interest rate = 1+nominal interest rate1+inflation rate

8/13/2019 Capital Budgeting and Cash Flows

37/49

InflationExample - nominal figures

Year Cash Flow PV @ 10%1 8000

2 8000x1.03 = 82408000x1.03 = 8240

8000x1.03 = 8487.20

80001.10

2

3

=

=

=

=

7272 73

6809 923 6376 56

4 5970 78429 99

8240

1 10

8487 20

1 10

8741 82

1 10

2

3

4

.

..

.$26, .

.

.

.

.

.

8/13/2019 Capital Budgeting and Cash Flows

38/49

InflationExample - real figures

Year Cash Flow [email protected]%1 = 7766.99

2 = 7766.99= 7766.99

= 7766.99

80001.03

7766.991.068

8240

1.03

8487.20

1.03

8741.82

1.03

2

3

4

=

=

=

=

7272 73

6809 923 637656

4 5970 7826 429 99

7766 99

1 068

7766 99

1 068

7766 99

1 068

2

3

4

.

.

.

.

.

.

.

.

.

.

= $ , .

8/13/2019 Capital Budgeting and Cash Flows

39/49

Equivalent Annual CostEquivalent Annual Cost - The cost per

period with the same present value as thecost of buying and operating a machine.

8/13/2019 Capital Budgeting and Cash Flows

40/49

Equivalent Annual CostEquivalent Annual Cost - The cost per

period with the same present value as thecost of buying and operating a machine.

Equivalent annual cost =present value of costs

annuity factor

8/13/2019 Capital Budgeting and Cash Flows

41/49

Example

Given the following costs of operating two

machines and a 6% cost of capital, select thelower cost machine using equivalent annual cost

method.

Year

Machine 1 2 3 4 PV@6% EAC

A 15 5 5 5 28.37 10.61

B 10 6 6 21.00 11.45

Equivalent Annual Cost

8/13/2019 Capital Budgeting and Cash Flows

42/49

Timing Even projects with positive NPV may be

more valuable if deferred. The actual NPV is then the current value

of some future value of the deferredproject.

tr

t

)1(

dateofasvaluefutureNet

NPVCurrent +=

8/13/2019 Capital Budgeting and Cash Flows

43/49

TimingExample

You may harvest a set of trees at anytime overthe next 5 years. Given the FV of delaying the

harvest, which harvest date maximizes current

NPV?

9.411.915.420.328.8in valuechange%109.410089.477.564.450(1000s)FVNet

543210

YearHarvest

8/13/2019 Capital Budgeting and Cash Flows

44/49

8/13/2019 Capital Budgeting and Cash Flows

45/49

TimingExample - continued

You may harvest a set of trees at anytime over the next 5 years.Given the FV of delaying the harvest, which harvest date maximizescurrent NPV?

5.581.10

64.41yearinharvestedif ==NPV

67.968.367.264.058.550(1000s)NPV

543210

YearHarvest

8/13/2019 Capital Budgeting and Cash Flows

46/49

Fluctuating Load Factors

$30,00015,0002machinestwoofcostoperatingPV

$15,0001,500/.10pachinepercostoperatingPV$1,5007502machinepercostOperating

units750machineperoutputAnnual

MachinesOldTwo

=

=

=

8/13/2019 Capital Budgeting and Cash Flows

47/49

Fluctuating Load Factors

$27,000500,132machinestwoofcostoperatingPV

$13,500750/.106,000pachinepercostoperatingPV

$7507501machinepercostOperating

000,6$machinepercostCapital

units750machineperoutputAnnual

MachinesNewTwo

=

=+

=

8/13/2019 Capital Budgeting and Cash Flows

48/49

Fluctuating Load Factors

000,26..$..............................machinestwoofcostoperatingPV

$16,000.10/000,16,000$10,000,000/.101machinepercostoperatingPV

$1,000000,11$1,0005002machinepercostOperating

000,6$0machinepercostCapital

units1,000units500machineperoutputAnnual

MachineNewOneMachineOldOne

=+=

==

What To Discount

8/13/2019 Capital Budgeting and Cash Flows

49/49

What To Discount Cash Flows.not accounting

income/expenses

Estimate Cash Flows on an Incremental

BasisDo not confuse average with incremental

payoffs

Beware of allocated overhead costsInclude all incidental effects

Do not forget working capital requirements

Include opportunity costs

Forget sunk costs

Treat inflation consistently

Post Tax