Capital Allowances Made Simple 6 October · PDF file•What are capital allowances...

39

Capital Allowances Made Simple 6 October 2016

Transcript of Capital Allowances Made Simple 6 October · PDF file•What are capital allowances...

Capital Allowances Made Simple

6 October 2016

• What are capital allowances

• Who can claim and the benefit

• How to claim on different transactions

• Which properties qualify and which items

• Types of Capital Allowances

• Buying and selling

• Case studies

Contents

What are they?

• Government incentive for investment

• Legislation and case law

• Interpreted and applied by tax payers

• HMRC check claims

Current Position

• Favoured by Government, increase rates

• Complicated by trying to reduce abuse via legislation

• Increases the benefit

• HMRC lack of resources

Why are CAs important?

• Deduction against corporation or income tax

• Available where incur expenditure on commercial property

• Cash flow benefit

• Higher Equity / Lower L to V

• Only form of tax relief against property capital expenditure

How it WorksTax Return Without Capital

AllowancesWith CapitalAllowances

Rental income/Profit £1,000,000 £1,000,000Deduct allowable costs i.e. debt finance

(£500,000) (£500,000)

Capital Allowances 0 (£500,000)Profit subject to tax £500,000 0Tax to pay (@20%) £100,000 0

CAs in Tax Transparent Vehicles

• REITS / PAIFS• Don’t pay tax but legally must claim Capital Allowances• Used to reduce PID (amount must distribute to shareholders)

• Authorised Contractual Scheme (ACS)• Combine Funds / Encourage Onshore Investment• Offer SDLT & CGT exemptions• Complexities on calculating CAs on disposal of units and properties

Who can claim?YES

Institutions Listed Co'sPrivate Co's Overseas InvestorsPrivate Individuals Others

£58bn

NO

Pensions

£12bn

Who can claim? Common Misunderstandings

Traders, ie Retailers v Trading Stock

Capital Expenditure v P & L Expenditure

Overseas Companies v Overseas Properties

What Triggers Entitlement to Claim

Incur Capital Expenditure

Own Relevant Interest

Held as Investment

Capital Contribution

Make a Claim

Freehold vs Leasehold

Not Held as Trading

Capital Contribution Claims

• Know the legal position

• Who pays for what

• Structure agreement

Case StudyDrafted contract clause stated tenant (recipient) will get benefit. Invalid

Service Charges & Dilapidation Payments

• Claim if met by the service charge?

• Is the service charge taxed as income?

• Claim on receipt of a dilapidations payment?

Asset Management Budget

Landlord Tenant

Qualifying Property Types

Common Misconception / ErrorCan’t claim at all on ‘residential’ property

Typical Qualifying AmountsType Developments Acquisitions• Shopping Centre 30% - 60% 2% - 35%• Care Home 35% - 60% 6% - 35%• Office 35% - 50% 5% - 32%• Hotel 40% - 65% 2% - 35%• Car Dealership 25% - 40% 2% - 20%• Health Centre 30% - 45% 3% - 25%• Student Accommodation 7% - 15% 2% - 6%• Industrial Warehouse / Retail Parks 5% - 40% 1% - 30%• General Fit-outs / Refurbishments 55% - 95% n/a

Main Types of Allowances1. On reducing balance basis

18% Plant & Machinery8% Integral features & Thermal Insulation

2. In year of Expenditure (First Year Allowance)100% Annual Investment Allowance (£200,000)

Enhanced Capital AllowancesBusiness Premises Renovation Allowances

150% Land Remediation Relief

Examples of Plant & Machinery

18% writing down allowance pa

Examples of Integral Features

8% writing down allowance pa

Examples of Green Tax Incentives

100% or 8% writing down allowance pa

Business Premises Renovation Allowances• Many property owners unaware of

benefit• 100% tax relief on all expenditure• Includes most major cities• Vacant or part vacant propertywww.ukassistedareasmap.com

Ceases April 2017 - Funding must be committed

Land Remediation Relief 150%

• Developers & investors• Land in the UK• Contaminated at acquisition• No subsidy or contribution• Polluter cannot claim• Relevant interest in the land• Tax credit

Claim Prep/ Rebuild & Land Value

How to Make a Claim

Client ReviewPortfolio Report

Advice on Disposal Agree Claim with

HMRC

Collate DocumentsEntitlement to

ClaimSurveyIncur

Expenditure

Maximise Claims

• Incorporate incidental expenditure• Claim all associated professional fees• Not just M&E expenditure• Claim at the highest writing down allowances• Capital vs Revenue• Timing of the claim – “when expenditure is incurred”

Case Study – First Tier Tribunal

Expenditure: £30m

Claim Value: £6m

Client: Overseas Fund

Cash Saving: £1.2m (4%)

Case Study – Retail Refurbishment

Expenditure: RetailRefurbishment

Project Value: £13m

Client: UK REIT Plc

Cash Saving: £7m (£6.3m)

Buying and Selling

• What do I need to do and when?

• Who should be aware of CAs and who should address the CAs?

• What are the angles?

• The seller says there are no allowances to pass across? What next?

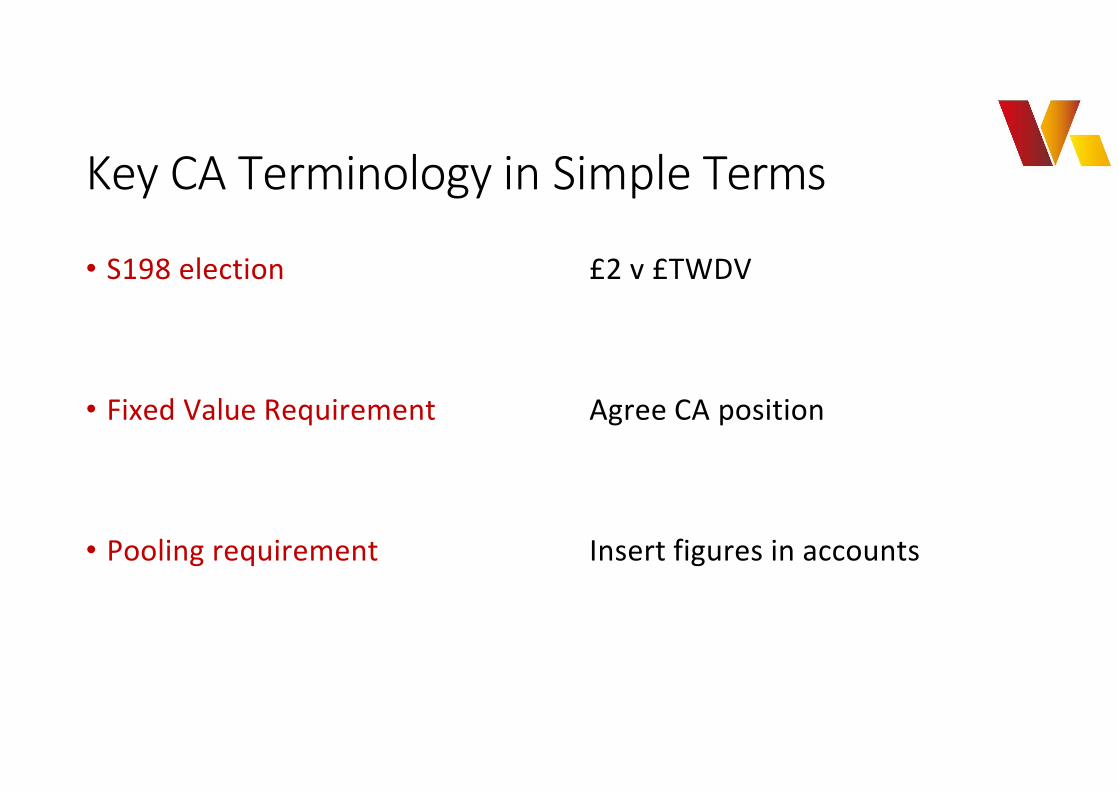

Key CA Terminology in Simple Terms

• S198 election £2 v £TWDV

• Fixed Value Requirement Agree CA position

• Pooling requirement Insert figures in accounts

Acquisitions – Legal entitlement?

• Vendor – tax payer / pension / LA / offshore?

• Freehold / Leasehold Acquired?

• CPSEs

• Prior Owners Claim History

• Contract Wording – HOT stage?

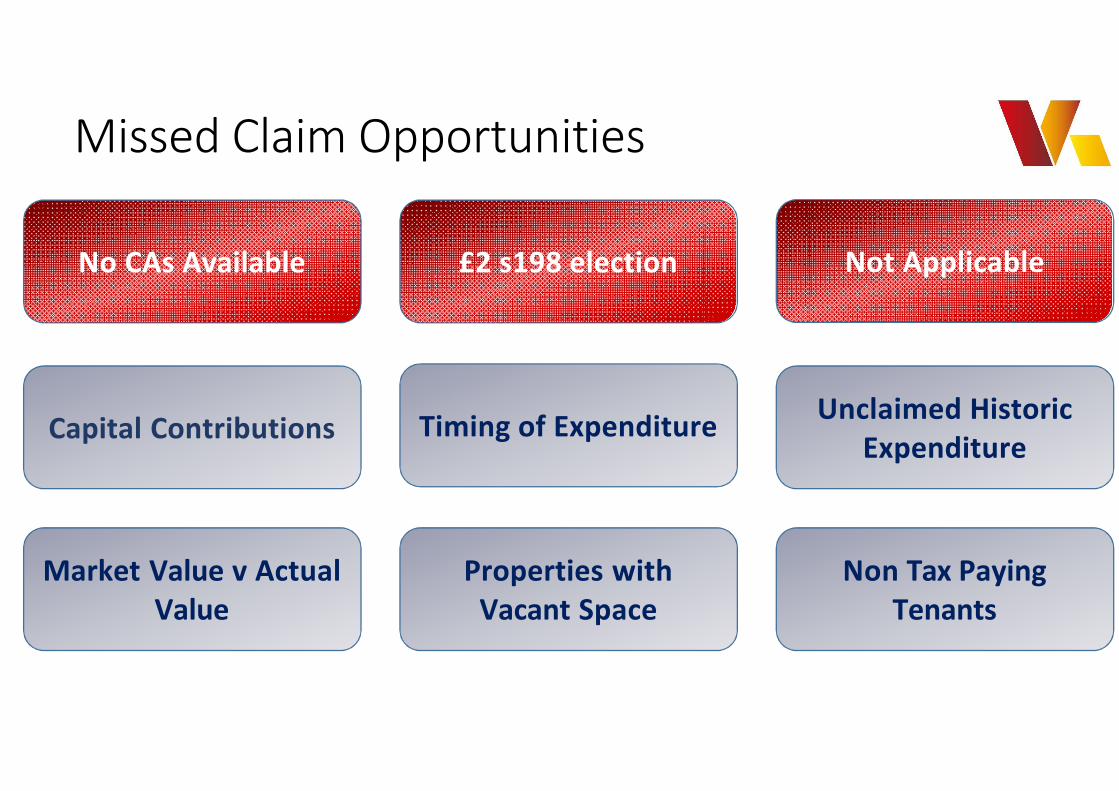

Missed Claim Opportunities

Capital ContributionsTiming of ExpenditureCapital Contributions

Market Value v Actual Value

Non Tax Paying Tenants

Properties with Vacant Space

£2 s198 election

Unclaimed Historic Expenditure

Not ApplicableNo CAs Available

Case Study – Hotel AcquisitionExpenditure: Hotel

Value: £6.7m

Client: Private Investor

Cash Saving: £360,000 (5.4%)

Case Study – Industrial AcquisitionExpenditure: Industrial

Value: £2.3m

Client: Private Equity Investor

Cash Saving: £144k (6%)With £2 s198

Case Study – Shopping Centre AcquisitionExpenditure: Shopping Centre

Value: £23m

Client: Overseas Investor

Cash Saving: £850k (3.7%)Receivership Deal

Case Study – Office AcquisitionExpenditure: Office

Value: £5,000,000

Client: Overseas Investor

Cash Saving: £310,000 (6%)

Company Acquisitions

• Review for unclaimed historic expenditure

• Capital Contributions

• Capex reconciliations

Common Misconception / ErrorTime restriction to review historic expenditure

Surely all clients claim CAs….Don’t understand benefit

Think it is too late / No record of costs

Loss making or low tax rate

‘Too much effort’

Perception need to own property

Client assumes accountant or someone addressing it

Capital Allowances

Accountant

QS

Lawyer

Client

Capital Allowances – 2016 / 2017?

• Business Premises Renovation Allowances (BPRA)

• Authorised Contractual Scheme

• Energy Efficiency Requirements / Lease Breaks

2016 / 2017 – Authorised Contractual Scheme

• Tax Transparent Fund Structure; Multiple Funds under one umbrella

• Taxed at investor level; CGT doesn’t apply to fund or non UK investors

• Value of UK ACS funds likely to exceed £250 billion by 2017*

• Pension Funds – Future Capital Allowances claims

• Complexities calculating CA values* According to survey of Financial professionals undertaken by Northern Trust

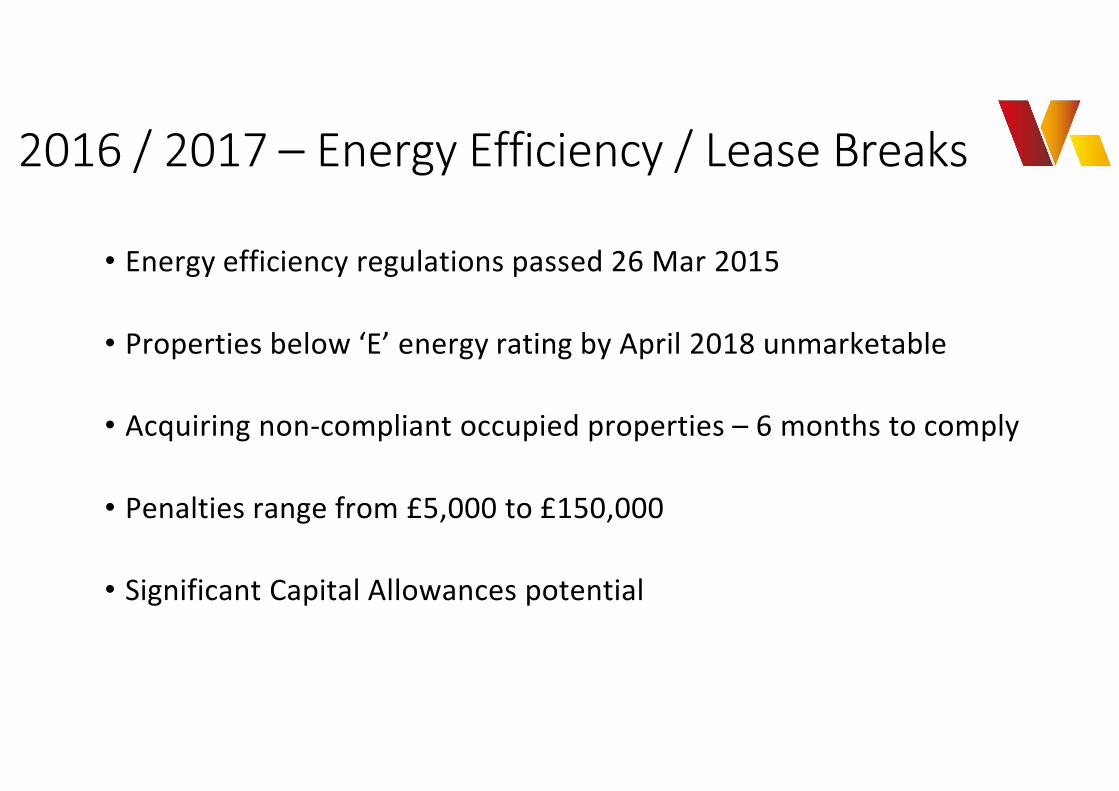

2016 / 2017 – Energy Efficiency / Lease Breaks

• Energy efficiency regulations passed 26 Mar 2015

• Properties below ‘E’ energy rating by April 2018 unmarketable

• Acquiring non-compliant occupied properties – 6 months to comply

• Penalties range from £5,000 to £150,000

• Significant Capital Allowances potential

Concluding Note• Agent Family Trusts, Private Investors, Occupiers often not advised

• QS / PM If no one asks for Cost Information no one is claiming!

• Lawyer Ensure contracts cover CAs adequately

• Accountant Valuing Land / Buildings / CAs; Ancillary costs

• Investor Never assume no allowances available without checking

• Occupier Check claims have been made on all expenditure

Clive CurdDip Prop Invest, MRICS, [email protected]: 0203 7937 154Mob: 07502 376 973

Nolan MastersMRICS, ATT, BSc (Hons)[email protected]: 0203 7714 315Mob: 07502 376 204

David GibsonMRICS, ATT, BSc (Hons)[email protected]: 0203 7714 316Mob: 07502 376 957

46 Blandford Street, W1U 7HTTelephone: 0203 1300 293www.veritasadvisory.co.uk