Capita retail banking report - Prioritising to prosper

9

Prioritising to prosper Choosing the right path to recovery in the retail banking sector

Transcript of Capita retail banking report - Prioritising to prosper

Prioritising to prosperChoosing the right path to recovery in the retail banking sector

Mark Record, Strategic Account Leader for financial services at Capita, sets out a roadmap to success for the sector in a post-pandemic world.

Reviewing priorities The first common theme is that strategic priorities are shifting. Many banks and other financial providers are reviewing the priorities that they set at the beginning of the year or even last year. Are they still important in today’s environment? What are the new opportunities and priorities needed to survive and thrive?

Many COOs and CFOs are focusing even more on strategic projects. However, their key digital transformation and automation efforts are now taking on a much broader scope as they seek to shift their business models and compete in ever-more challenging times. Some projects that were lower down the priority list are now an immediate need; something that was being implemented may now be postponed or is simply no longer relevant.

COVID-19 has certainly made companies conservative in certain areas of their business. In some respects, however, it has increased their appetite for risk when it comes to innovation. McKinsey published an article on this subject and talked about “finding a silver lining in the falling barriers to improvisation and experimentation and the permission to embrace innovative action instead of tinkering around the edges”. In its words, the pandemic is giving companies “a mandate to be bold”. While a crisis poses challenges, there are also opportunities that can pay off significantly.

A few key themes are emerging across many financial institutions and our clients are starting to think about how their world will look after the Coronavirus pandemic:

• How will they act differently? • How will they re-model their

businesses? • What help will they need?

Bad companies are destroyed by crisis, good companies survive them,

great companies are improved by them.”

Andy Grove (Source: .inc.com, 21 March 2016)

Real-time data is becoming pivotal in this ‘new normal’

The second common theme is the thirst for data and near real-time reporting. Every day the Government is probed on its data accuracy, for example the ‘R’ factor and track and tracing data. The need for accurate and trustworthy real-time data is now important to all of us, in all of our daily transactions.

Market and overall uncertainty have also resulted in leadership teams and boards requesting constant updates to scenario planning to reflect the ever-changing environment. I think that, for a lot of CEOs / CFOs / COOs, scenario-planning has been a hugely manual process, taking hundreds of people and, in some cases, many weeks, and they are now realising that their existing systems and processes are unable to provide constant trading statements and forecasts. Creating automated finance models that use a trusted set of accurate financial data is now an imperative: the market and investors will expect no less in the future.

Challenged with legacy technology and data quality issues, most banks are unable to achieve the desired returns on their modernisation initiatives. As a result, they might need to adopt a back-to-basics approach before they can fully reap the rewards from advanced technologies.

As a first step, institutions should tackle their technical debt, which is typically caused by past underspending and layering newer technologies on top of ageing infrastructure. Legacy systems are among the biggest barriers to bank growth.

2020 could be the year of ’build and migrate’, as banks continue to test ways to modernise their core systems. Establishing a new, parallel, cloud-native core banking platform is gaining traction as a strategy. This is because it is less risky, reduces time-to-market, brings results and allows core banking functions to be migrated over time.

The need for accurate and trustworthy real-time data is now important to all of us, in all of our daily transactions.

Cost reduction is a key focus because revenue is unpredictable

The third common theme is that many banks and financial services providers are seeking ways to significantly drive down their operating costs. This is because their revenue streams are unpredictable and are affected by forces beyond their control, such as interest rates and consumer behaviour.

The companies that are surviving, and in some cases thriving, have recurring revenue streams through licence fees and monthly / annual subscriptions. Recurring revenue models are going to be in a much better place than those that are focused on short-term cash or project-driven activity. The pandemic may accelerate an already existing shift towards business models that result in steady, more predictable revenue streams.

Banks are launching products with premium monthly plans that offer a variety of services in addition to perks and rewards. Will we see hard-hit sectors like airlines or retail try to come up with feasible subscription-based offerings to help them to come back from the brink, too?

A more aggressive approach to revenue management will be expected to track, manage and report on the progression of revenue in more detail as it moves through the contract lifecycle.

Advances in robotics and AI will start a wave of ‘re-shoring’ and localisation. And they’ll be the basis of new alliances between leading financial services and technology companies, to address key pressure points, reduce costs and mitigate risks.

Choosing the right priorities will be critical

What could be on the must-do list for 2020 / 21? I’ve spoken to a number of executive clients and board members, and here is my starter-for-10 priority list:

Improving customer experience through trusted data, APIs and AI will become critical to:• improving personalisation• improving fraud detection• improving complex back-office functions

such as risk management• improving fulfilment and obliterating processes and all at much lower cost

Updating your IT operating model to serve your customers better• Greater adoption of the ecosystem model. Mobile banking brought everyday banking

on the move, now ecosystems integrate our everyday lives with banking. They bring many elements of modern platform services such as cloud, explainable AI and open APIs together into one seamless journey

• Spend time giving your team real purpose so that they deliver greater value• Does your current operating model enable effective software development from home?

Does it support agility and collaboration?

1

2

Moving to trusted and real-time data and de-fragmenting customer, operational and corporate data • Is it time to truly tackle those legacy issues and create normalised ‘golden sources’

of data? • Fragmented data is usually the true root cause of poor customer service

and experience, ineffiency, increased risks and out-of-date reporting

Establishing true and effective partnering• Helping clients to build their knowledge and seconding capabilities will become

more important• Aligning interests and avoiding self-interest• Take stock of your partners. Who has stuck with you in this crisis and been willing

to ignore the contract and do the right thing?

3

4

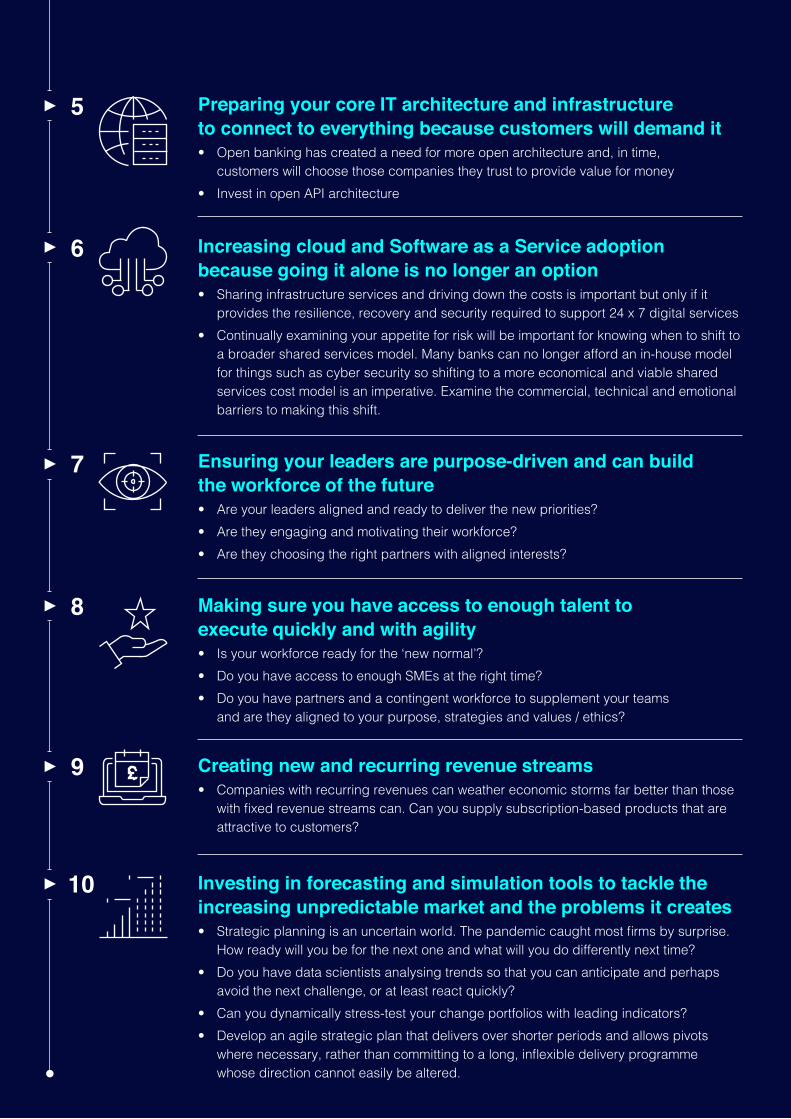

Preparing your core IT architecture and infrastructure to connect to everything because customers will demand it• Open banking has created a need for more open architecture and, in time,

customers will choose those companies they trust to provide value for money• Invest in open API architecture

Ensuring your leaders are purpose-driven and can build the workforce of the future• Are your leaders aligned and ready to deliver the new priorities?• Are they engaging and motivating their workforce?• Are they choosing the right partners with aligned interests?

Creating new and recurring revenue streams • Companies with recurring revenues can weather economic storms far better than those

with fixed revenue streams can. Can you supply subscription-based products that are attractive to customers?

Increasing cloud and Software as a Service adoption because going it alone is no longer an option• Sharing infrastructure services and driving down the costs is important but only if it

provides the resilience, recovery and security required to support 24 x 7 digital services • Continually examining your appetite for risk will be important for knowing when to shift to

a broader shared services model. Many banks can no longer afford an in-house model for things such as cyber security so shifting to a more economical and viable shared services cost model is an imperative. Examine the commercial, technical and emotional barriers to making this shift.

Making sure you have access to enough talent to execute quickly and with agility• Is your workforce ready for the ‘new normal’? • Do you have access to enough SMEs at the right time?• Do you have partners and a contingent workforce to supplement your teams

and are they aligned to your purpose, strategies and values / ethics?

Investing in forecasting and simulation tools to tackle the increasing unpredictable market and the problems it creates• Strategic planning is an uncertain world. The pandemic caught most firms by surprise.

How ready will you be for the next one and what will you do differently next time?• Do you have data scientists analysing trends so that you can anticipate and perhaps

avoid the next challenge, or at least react quickly?• Can you dynamically stress-test your change portfolios with leading indicators? • Develop an agile strategic plan that delivers over shorter periods and allows pivots

where necessary, rather than committing to a long, inflexible delivery programme whose direction cannot easily be altered.

5

7

9

6

8

10

Here at Capita, we’re already demonstrating the importance of effective partnerships, for banks and their customers:

Taking increased and calculated risksTo deliver on these rapidly changing priorities, you have to increase your appetite for risk. This pandemic has taught us that we can’t wait 10 years for a vaccine. The pharmaceutical industry globally is having to find new risk processes and the agility to tackle the demand for quick results. Of course, moving quickly doesn’t mean moving recklessly. Leaders need to learn quickly about what works and what doesn’t. In fact, fail fast and recover quickly might become the new way of working.

ScalingHunt out the barriers to scaling fast. Where are the key issues? A great source of data is your customer complaints. Examine these closely as they will tell you where the scale issues exist. Listen very carefully to these complaints and tackle the true root causes, not just the symptoms.

Seek out the right partnersAs Mckinsey says in its article about digital strategy, ”don’t go it alone”. Seek out trusted partners that match your values, ethics and interests. Look close to home first. Some of these partners might already exist in your company, in other teams or departments, and have more to offer if given the chance. You might find them eager to take more risks, be more transparent and share their data with you. Choosing the right partners with deep skills, experience and knowledge that is lacking or overstretched in your own company will help to reduce risk and improve performance.

Do fewer things better and fasterKeep things simple and don’t become overstretched. Doing less has been happening naturally during the pandemic but don’t be too eager to overstretch now that things are opening up more. Make sure that you prioritise viable activities and continually re-test this viability. Avoid complexity wherever possible.

At The Co-operative Bank, we have been focusing on helping our customers

through the challenges presented by COVID-19. With thousands of mortgage payment deferral requests to process each week, when we previously processed just a handful, it was essential that our mortgage service partner Capita was flexible, agile and focused. In true partnership, we have delivered for our customers and, as a result, our two organisations have worked more closely and our partnership has become stronger.”

Chris Davis, Chief Operating Officer at The Co-operative Bank

In summary

In April 2020, the World Economic Forum (WEF) listed five vital lessons of the Coronavirus pandemic . In the article, it says that:

Reading the report, I was struck by the WEF’s statement on ethics, diversity and responsibility:

However we choose to move forward from the pandemic, maintaining and delivering on strong values and ethics will be just as important as, if not more important than, the themes and priorities outlined in this article. We have to truly embrace inclusion and diversity and corporate and environmental responsibility as we deliver on our ‘new normal’ business model. Otherwise we will be ignoring the lessons we are currently being taught.

The promise of digital medicine is the promise of the Fourth Industrial

Revolution, where the tools of artificial intelligence transform all professions. At the same time, healthcare is the ultimate argument for the difficult lesson: that the digital future cannot simply make the wealthy healthier. Digital medicine gives us an unparalleled opportunity to address the social determinants of health and provide access to everyone in their own neighbourhoods.”

We need an early warning system for future crises

Digital access must be seen as a utility, like electricity

and plumbing

Creative partnerships and the digital economy can

create a better world for us

To learn more about how Capita can help you, please visit our website or speak to your Account Director today.