Fundraising Trends and the Next Generation of Canadian Giving

Upload

buck-caseyCategory

view

216download

1

Canadian Society of Association Executives

16 October, 2013

Successful Fundraising Strategies

Daniel P. Brunette

President, AFP Ottawa Chapter

Manager, Development and Donor Services,

Setting the stage Terminology Prime motivators The big questions The big mistakes Q&A Resources

Overview

Fundraising

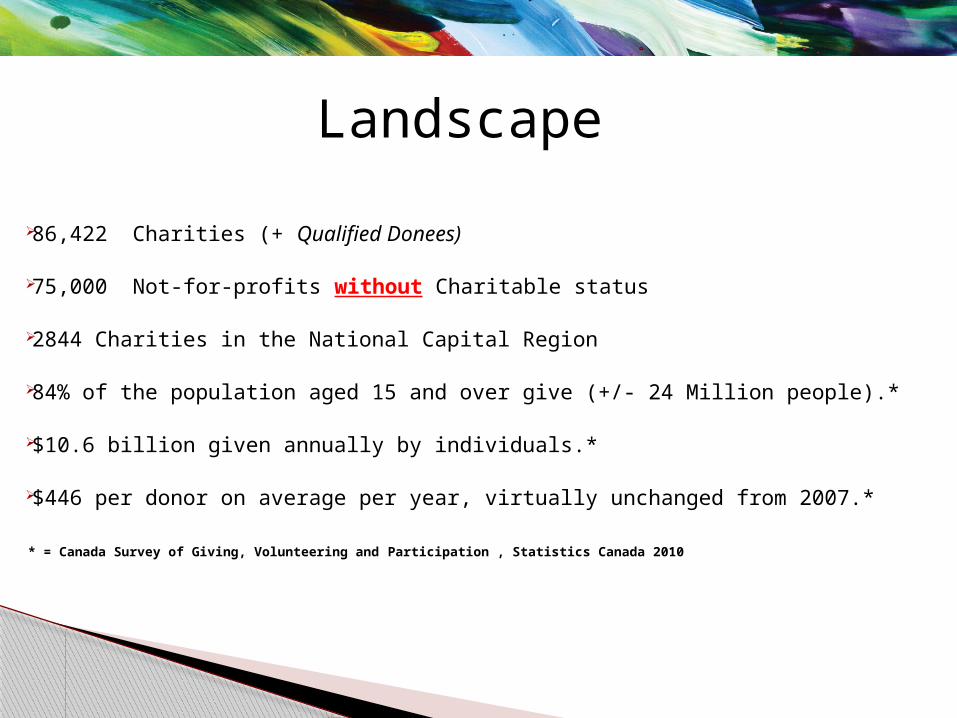

Landscape

86,422 Charities (+ Qualified Donees)

75,000 Not-for-profits without Charitable status

2844 Charities in the National Capital Region

84% of the population aged 15 and over give (+/- 24 Million people).* $10.6 billion given annually by individuals.*

$446 per donor on average per year, virtually unchanged from 2007.*

* = Canada Survey of Giving, Volunteering and Participation , Statistics Canada 2010

HR Council (Not-For-Profit Sector)

75% of Not-for-Profits have less than 10 employees

76% of Not-for-Profits Sector employees are women

89% self-identified as White or Caucasian

88% are satisfied with their job

30% (+/-) have been with their employer 10 +years

Landscape…Continued

Source of Funds

Individuals & Families Private and Public Foundations Other Qualified Donees Government Employee Groups Associations/Clubs Corporations / Businesses (Philanthropy vs. Sponsorship)

Why people give…

Compassion for those in need (89%)

Personal belief in a cause and desire to help (85%)

Desire to contribute to their communities (79%)

Personally affected by an organization’s cause (61%)

Religious obligations or beliefs (29%)

Income tax credit (23%).

Top reason people do not give… They are not asked!!!

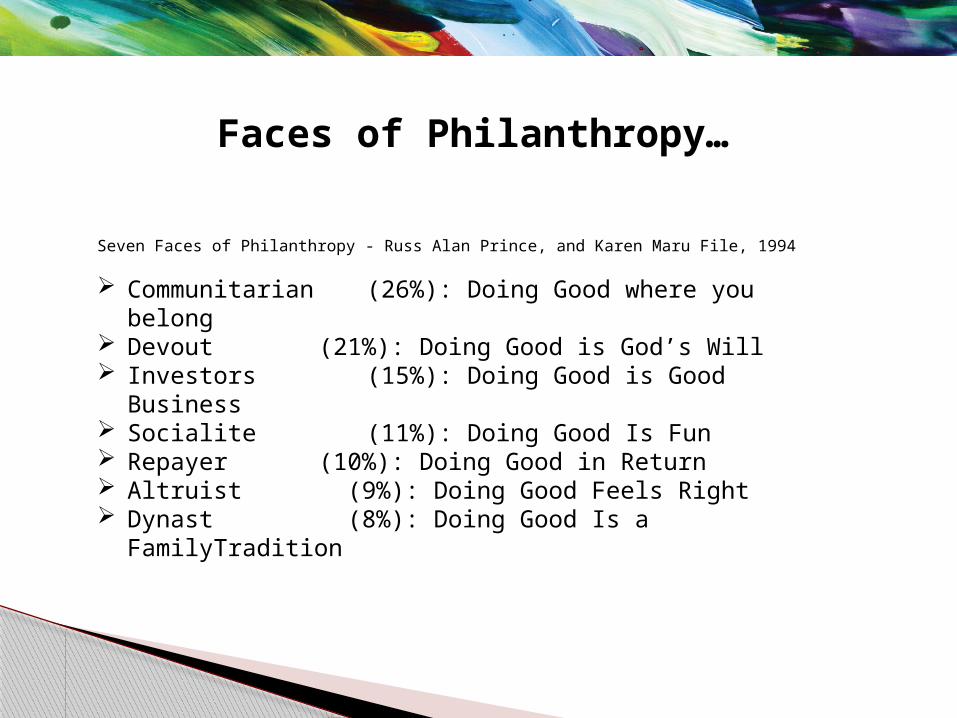

Faces of Philanthropy…

Seven Faces of Philanthropy - Russ Alan Prince, and Karen Maru File, 1994

Communitarian (26%): Doing Good where you belong

Devout (21%): Doing Good is God’s Will Investors (15%): Doing Good is Good

Business Socialite (11%): Doing Good Is Fun Repayer (10%): Doing Good in Return Altruist (9%): Doing Good Feels Right Dynast (8%): Doing Good Is a FamilyTradition

Where does the $10.6B go?

Universities and Colleges 1%

Arts and Culture 1 % Law, advocacy and politics 1%

Development and Housing 1%

Other Groups 1%

Sports and Recreation 2%

Education & Research 3%

Environment 3%

Grant making, Fundraising & voluntarism 6%

Hospital 6%

International Aid 8%

Social Services 11%Health 15%

Disaster relief 20%

Religion 40%

Philanthropic Giving Pyramid

Why fundraise? Operations

Core programming

Special Projects

Grantmaking

Endowments /Investment Funds /Reserves

Partnerships

How do you do it? (Continued)

Revenue Generation – Fundraising -Philanthropy

How do you do it?Revenue Generation / Fundraising / Philanthropy

Membership fees

Membership categories

Membership “top up” donation

Cross promotion within communications

Job postings

Sponsorships

Event fees conference, trade shows, cross promotion, price differentials)

How do you do it? (Continued)

Revenue Generation – Fundraising -Philanthropy

Cash gifts (receiptable or non receiptable)

Cost Reduction

In-Kind gifts

Legacy Gifts

3rd party events

Foundation model

Other

What is important?

Value Proposition / Case for Support

Information Management

Process management

The Elevator Pitch

Subject matter knowledge

Audience knowledge

The ask (Right person, right time, right way, right amount)

Ethics & Transparency

Relationships

The Fundraising Cycle

Suspects

Prospects

Discovery

NO!

No…for now

Maybe

Stewardship Yes!

Ask

Cultivation

Thank you

C apacityA ffinityT imeframe &P ersonal notesL inks to people and cause A ffluence indicatorsT ype of gifts T ype of philanthropist/member E njoyable things /HobbiesR ed Flags

Useful Information

◦ Memberships◦ court ordered transfer of property to a charity;◦ the payment of a basic fee for admission to an event or

to a program;◦ the payment of membership fees that convey the right to

attend events, receive literature, receive services, or be eligible for entitlements of any material value that exceeds 80% of the value of the payment;

◦ a payment for a lottery ticket or other chance to win a prize

◦ the purchase of goods or services from a charity;◦ Advantage or consideration exceeds 80% of the value of

the donation;

Common Mistakes#1 Improper issuance of Tax Receipts

◦ Advantage or consideration exceeds 80% of the value of the donation;

◦ a gift in kind for which the fair market value cannot be determined;

◦ donations provided in exchange for advertising/sponsorship;

◦ gifts of services (for example, donated time, labour);◦ gifts of promises (for example, gift certificates

donated by the issuer)◦ pledges;◦ loans of property;◦ use of a timeshare; and the lease of premises.

Common Mistakes – #1 Improper issuance of Tax Receipts

#2 Lack of planning (Strategic, Funding etc)

#3 Failure to keep good records

#4 Ineffective Board or lack of governance

#5 Failure to invest in talent/expertise◦ CRA, PIPEDA, CNCA etc

Common mistakes

Pre & post meeting discussions Research profiles at the meeting Crisis Management Plan CRA Filing and Compliance Personal Information Protection and Electronic

Documents Act (PIPEDA) Canada Not-For-Profit Corporation Act (CNCA) Etc…

Learn from them!

Horror story examples

Pro-Bono work

Delegates and/or ambassadors

Professional Advisors to Charities or Community causes

Speaker Bureau of key influencers / Speakers

Advocacy efforts for the NFP Sector

College and University Clubs

Mentorship programs

Other “value added” approaches

1-Luck is when planning meets opportunity (Seneca –Greek philosopher)

2-What’s your Iowa? (Betsy Myers)

3-“Don’t fear the reaper…” (Blue Oyster Cult)

4- Play where the puck will be. (Wayne Gretzky)

5-Two certainties in life, death and taxes…Philanthropy can help with both.

And...

***The HBB (hit by a bus) rule overrules ***

Quotable quotes to ponder

Association of Fundraising Professionals: www.afpnet.org

Canada Revenue Agency: www.cra-arc.gc.ca/charitylists/

Charity Village: www.charityvillage.com

Imagine Canada: www.sectorsource.ca/

CFRE Reading List: www.cfre.org/pdf/CFRE-Reading-List.pdf

Global Philanthropy: www.globalphilanthropy.ca

Resources

AFP Ottawa Chapter Officec/o Jessica HarrisThe Willow Group

1485 Laperriere AvenueOttawa, ON K1Z 7S8

Phone: 613-590-1412E-mail: [email protected]