Canada’s Position in the Global Wine Market Insight... · Canada’s Position in the Global Wine...

33

Stefano Pallotti Vilma Pumi Head of Credit Analyst Canada’s Position in the Global Wine Market A look at the broader market Rabobank International March 2012

Transcript of Canada’s Position in the Global Wine Market Insight... · Canada’s Position in the Global Wine...

Stefano Pallotti Vilma PumiHead of Credit Analyst

Canada’s Position in the Global Wine Market

A look at the broader market

Rabobank InternationalMarch 2012

Current Trends in the Global Wine Market

I Global supply trends

II Production developments by region

III Global demand analysis- where will growth come from?

- The UK

- Germany

- - The US

- China

IV Canada’s position in the world market

Summary

What’s happening in the rest of the world?

The Global Wine Market

Global Supply

In 2008, Chile and Australia had particularly large harvests (Aus +27%)

In 2009, both Chile and Australia drop pricing on bulk wine to make room in tanks for incoming harvest

California grape prices drop, bottled imports drop, California shipments flat!

Does the rest of the world matter?

Chilean and Aus imports add 14 million cases-Average pricing declines 36%

Total US market grows 2%, but…

Bottled imports decline

California shipments flat

Volume Volume $/ Case

2008 2009 % Growth % Growth

Chile & Aus Bulk Imports 3569.3 17939.2 403% -36%

Total Bottled Imports 69355.6 68366.1 -1% -12%

Total Imports 94948.7 105760.1 11% -22%

Total US Wine Market 316800 322800 2% n.a

California Wine Shipments 196400 196700 0.0% n.a.

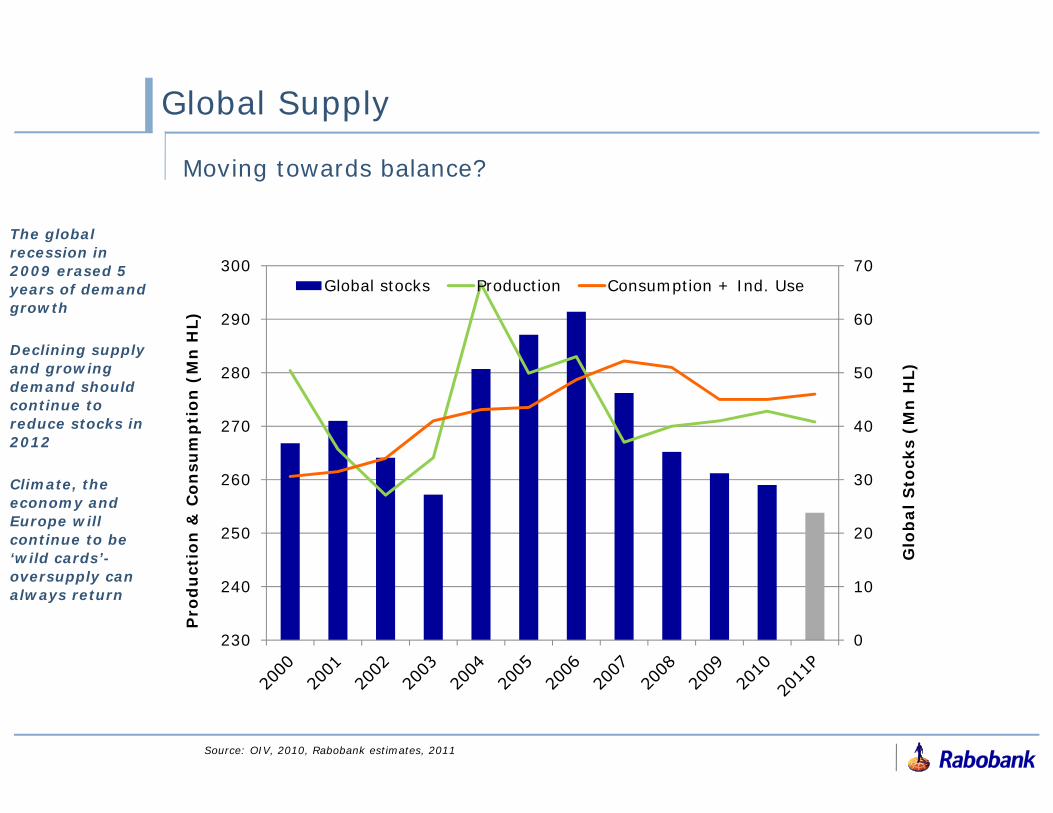

Global Supply

Moving towards balance?

The global recession in 2009 erased 5 years of demand growth

Declining supply and growing demand should continue to reduce stocks in 2012

Climate, the economy and Europe will continue to be ‘wild cards’-oversupply can always return

Source: OIV, 2010, Rabobank estimates, 2011

0

10

20

30

40

50

60

70

230

240

250

260

270

280

290

300Global stocks Production Consumption + Ind. Use

Pro

du

ctio

n &

Co

nsu

mp

tio

n (

Mn

HL)

Glo

bal

Sto

cks

(Mn

HL)

Global Oversupply

The reduction of oversupply is supporting bulk wine prices

Source: Ciatti Wine Brokers

Average bulk wine prices are gradually improvingPricing improvements seen across a diverse range of regionsPricing improvements seen across a diverse range of varietals

‘Cabernet Sauvignon: Price/lt. of bulk wine by country, Sept 2010- Dec 2011

Generic White: Price/lt. of bulk wine by country, Sept 2010- Dec 2011

0.00

0.50

1.00

1.50

2.00

2.50

Sep-10

Dec-10

Mar-11

Jun-11

Sep-11

Dec-110.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

Australia(AUD)

Italy(EUR)

Spain(EUR)

Sep-10

Dec-10

Mar-11

Jun-11

Sep-11

Dec-11

Bulk wine prices generally on the rise…

… but “be careful with ‘averages’”

The International Market

Easing of oversupply creates other pressures

Rising grape prices raise input costsWeak economies in major consumer markets create pricing pressureMargin pressure the story of 2012, particularly by- Producers with strong currencies (Chile, Australia)- Suppliers dependent on spot market- Markets with tightest supplies (US)

Index of Chilean Cab. Sauv Prices- Internal bulk market vs. Average bottled export prices in Chilean Pesos (CLP), 2007- 2011

050

100150200250300350400450

Jan-0

7

Apr-

07

Jul-

07

Oct

-07

Jan-0

8

Apr-

08

Jul-

08

Oct

-08

Jan-0

9

Apr-

09

Jul-

09

Oct

-09

Jan-1

0

Apr-

10

Jul-

10

Oct

-10

Jan-1

1

Apr-

11

Jul-

11

Oct

-11

Cab. Sauv. Domestic bulk price Cab. Sauv. Btld export price

Input Costs

Sales Price

Exports of key competitors

Production Developments

Competitiveness of Producers

Currency fluctuationsWeakness of the USD and GBP create pricing pressure for many suppliers (Aus., Chile, South Africa, etc.)

Country (or regional) image/ Perception of qualityImage as a wine supplier is built over time- often tied with the broader image of the countryCountry image will vary from market to market

Regional supply/ demand balanceExcess production results in increasing sales of bulk at lower pricesOngoing/ structural oversupply erodes the country-image, lower perceived quality

Factors that influence pricing

Italy

Export dynamo

Developments:

2011 harvestdown 14% from 2010-Italian bulk wine prices on the rise-Italy becoming a major importer of Spanish bulk wine

Export prices recovering from 2009- supported by weak euro

Ontario’s largest import competitor by volume

Source: Union Italiani Vini, 2011

€ 2.00

€ 2.10

€ 2.20

€ 2.30

€ 2.40

€ 2.50

€ 2.60

€ 2.70

0

500

1,000

1,500

2,000

2,500

Packaged still Bulk still Average Price- Bottled

Exp

ort

Vo

lum

e-

Millio

n l

iters

Avera

ge P

rice

btl

d-

€/

lt

Australia

Can it recover its “Premium” image

Developments:Particularly hurt by strengthening AUD, oversupplyImage-erosion in some markets due to ongoing oversupplySlow, steady reduction of vineyard areaStrong participation in emerging markets

FTA:Current- Chile, US, Singapore, Thailand, NZ, Philippines, VietnamPending- China, Japan, Korea, India

Source: Australian Wine & Brandy Corporation, 2011

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

0

100

200

300

400

500

600

700

800

900

Bottled Bulk Avg Value- Btld

Exp

ort

Vo

lum

e-

Millio

n l

iters

Avera

ge P

rice

btl

d-

$/

lt

France

The French Paradox

Developments:

Export volumes and pricing recovering from abysmal 2009

Export growth being led by highest priced segments (Champagne, Bordeaux & Burgundy)

2011 harvest +11% (bulk wine prices declining)

No. 3 import in Ontario

China has been a boon, but is a double edged sword

Source: FEVS, 2011

€4.00

€4.20

€4.40

€4.60

€4.80

€5.00

€5.20

€5.40

-

200

400

600

800

1,000

1,200

1,400

1,600

2007 2008 2009 2010 2011e

Volume (Mn. Lt) Avg Value (€/lt.)

Exp

ort

Vo

lum

e-

Millio

n l

iters

Avera

ge P

rice

-€

/lt

USA

A very different reality

DevelopmentsLarge, attractive domestic market & weak currency set U.S. suppliers apartExports represent a small % of production (17%) but opportunisticPricing for bottled wine exports has improved

FTA:Current- NAFTA, DR-CAFTA, Australia, Chile, Israel, Peru, SingaporePending- Korea

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

$4.50

$5.00

0

50

100

150

200

250

300

350

400

450

500

2005 2006 2007 2008 2009 2010 2011e

Avera

ge V

alu

e (

US

$/

litr

e F

OB

)

Exp

ort

Vo

lum

e (

ML)

Bulk

Bottled

Avg Value - Bottled(RHS)

Argentina

Rising star

Developments:Country-image continues to improve with Malbec

Adverse weather affects production in recent years, reduces bulk wine exports

Inflation now the major concern-affecting bottled exports

Next steps after Malbec?

FTA:Current-MERCOSUR, Israel

Source: INV, 2011

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

0

50

100

150

200

250

300

350

400

450

2005 2006 2007 2008 2009 2010 2011e

Packaged Bulk Avg Price- pckgd

Exp

ort

Vo

lum

e-

Millio

n l

iters

Avera

ge P

rice

btl

d-

$/

lt

Where are exporters finding growth?

Global Demand

Major Global Wine Import Markets

Who’s growing, who’s not?

Of the world’s largest wine import markets, only three show sustained growth

Source: IWSR/WDR, 2010

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

Signs of life?

Germany

Signs of life?

Germany

German marketOld World suppliers dominate import market (@75% share of imports)PL makes up @ 50% of wine sales70% of wine sold were valued at <€3.00/ liter; 95% <€4.99/ literGrowth occurring at the <€1.50/ liter AND €3.00- €4.99/ liter

Share of Imports

Avg Import Price (€/l)

Italy 43.3% € 1.20

France 15.8% € 2.53

Spain 14.9% € 1.17

South Africa 4.80% € 0.99

Chile 3.10% € 1.08

US 2.70% € 1.14

Australia 2.30% € 1.25

Price Segment Mkt Share

> € 0.99 14.20%

€1.00-1.49 9.50%

€1.50- 1.99 22.40%

€2.00-2.99 24.50%

€3.00- 4.99 23.80%

€5.00+ 5.60%

Source: Euromonitor 2011

Will profitability recover?

The UK

UK

Government policies affect consumptionExcise tax on wine +34% since 2005, VAT increased from 17.5% to 20% in 2011- Taxes make up 54% of retail price of a bottle of wineAusterity measures affect consumer demand

Retailer consolidation increases pricing pressure on suppliers

Can profitability recover in the World’s largest import market?

The UK had been the most attractive export market for many suppliers

Pricing has now become unattractive or unsustainable for many suppliers

Most suppliers exiting or reducing exposure to the UK market

Source: IWSR/WDR, 2010

UK Wine Imports and excise tax per bottle, 2005- 2011e

£0.00

£0.50

£1.00

£1.50

£2.00

£2.50

£3.00

1,050

1,100

1,150

1,200

1,250

1,300

1,350

1,400

Avera

ge E

xci

se P

aid

(G

BP

/L)

Vo

lum

e (

ML)

SparklingStill <15% abv

Wine imports down 8% from 2007

Australian suppliers have seen average income/ case decline by @ 65% since 2002 due to:- Excise tax increase- Currency

Still attractive for exporters?

The US

22

Source: Gomberg-Fredrikson

US market grew 4.5% in 2011, reaching 345 million cases (@ 3.1 bn. Lt.)Domestic wine (@65% market share) facing supply constraintsConsumers return to premiumization, discounting activity abatingImported wine growing at a faster rate, as California production has not kept pace with consumption

The US

Current Situation

US consumption has increased by over 100 mncases between 2001- 2011

Over past decade, most growth has occurred at higher price points ($9+)

Pricing pressure during 2008-2010

Encouraging market growth in 2010 and 2011

Discounting/ promotions becoming less aggressive

0

50

100

150

200

250

300

350

400

200,000

250,000

300,000

350,000

400,000

450,000

500,000

550,000

Existing NewSource: Gomberg-Fredrikson

US wine consumption (mn cases), 2001- 2011 California wine grape acreage, 2002- 2010

23

Source: Gomberg-Fredrikson Report, Rabobank analysis, 2011

The US

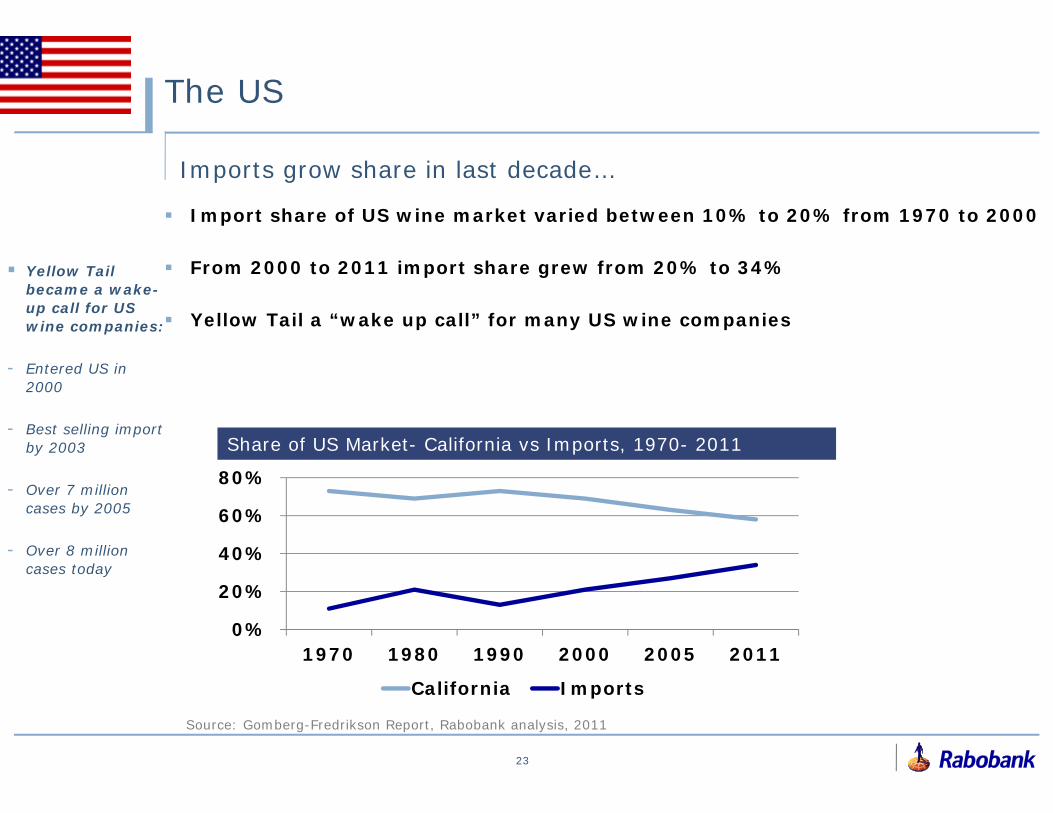

Imports grow share in last decade…

0%

20%

40%

60%

80%

1970 1980 1990 2000 2005 2011

California Imports

Share of US Market- California vs Imports, 1970- 2011

Yellow Tail became a wake-up call for US wine companies:

- Entered US in 2000

- Best selling import by 2003

- Over 7 million cases by 2005

- Over 8 million cases today

Import share of US wine market varied between 10% to 20% from 1970 to 2000

From 2000 to 2011 import share grew from 20% to 34%

Yellow Tail a “wake up call” for many US wine companies

24

The US

… but US wineries are now import protagonists US wineries have incorporated imported wines by:

Importing foreign brands to enhance their portfolio

Eliminating appellation for lower-priced brands to use cheaper imported wines

Use imported wines in traditional California brands for key varietals

Creating new brands using various import sources

The miracle we’ve been waiting for?

China

China

A big nation with a growing thirst for the good lifeChanging preferences of the developing middle class & younger generations

The luxury appeal of imported winesChinese consumers are highly motivated by image & status

The miracle we’ve been waiting for?

Growth rates of wine 2005-2010:

22% vol. 26% val(Euromonitor, 2011)

Imported wine represents 10% of volumes and growing fast

0

200

400

600

800

1,000

1,200

1,400

1,600

2005 2006 2007 2008 2009 2010

Millio

ns

lt

+170%

Wine sales in China, 2005- 2010

Source: China Customs, 2011 Source: China Customs, 2011

Competitive outlook for imported wines

China

-

2

4

6

8

10

12

14

16

18

2004 2005 2006 2007 2008 2009 2010

Vo

lum

e (

mil

lio

n 9

L c

ase

s)

Bottled wine imports

France Australia

Italy Chile

Spain USA

Others

+61%

-

2

4

6

8

10

12

14

16

18

2004 2005 2006 2007 2008 2009 2010

Vo

lum

e (

mil

lio

n 9

L c

ase

eq

uiv

ale

nts

)

Bulk wine imports

Chile Spain

Australia Italy

France USA

Others

+71%

Relative prices of imported wines

China

Generally strong pricing in the Chinese marketSignificant variations among suppliers

France maintains a dominant position and strong pricingAustralia achieves above-average pricesMost others are mainly bulk suppliersIn spite of attractive growth and pricing, the Chinese market remains problematic and a “Black Box”

No national distributorsLack of protection for brandsEtc.

How Canada should view itself in the context of the global market

Implications for the Canadian Wine Industry

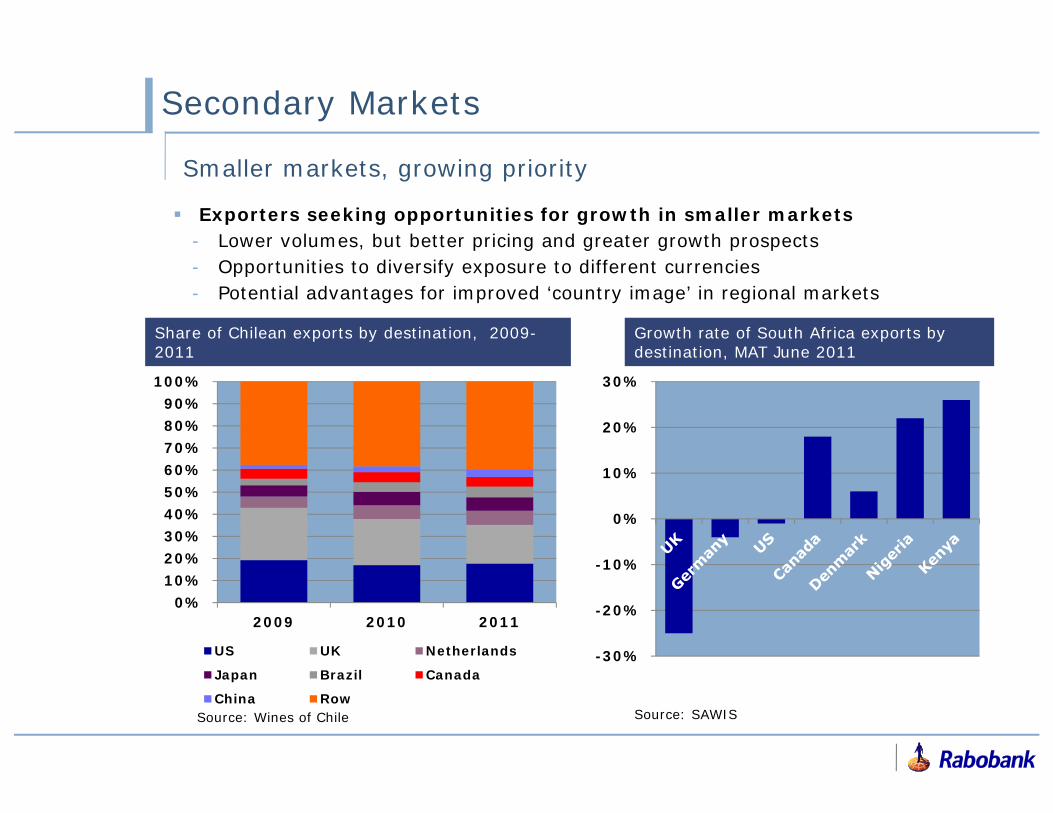

Secondary Markets

Exporters seeking opportunities for growth in smaller markets- Lower volumes, but better pricing and greater growth prospects- Opportunities to diversify exposure to different currencies- Potential advantages for improved ‘country image’ in regional markets

Smaller markets, growing priority

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2009 2010 2011

US UK Netherlands

Japan Brazil Canada

China Row

-30%

-20%

-10%

0%

10%

20%

30%

Share of Chilean exports by destination, 2009-2011

Growth rate of South Africa exports by destination, MAT June 2011

Source: SAWISSource: Wines of Chile

Canada

Opportunities:Sixth largest wine importer in the worldTotal wine consumption (@ 400 mn lt.) has grown 30% over past 5 yearsStrong average pricingValue growth has been outpacing volume growth

Challenges:Relatively small marketAccess (LCBO, SAQ)FragmentedMarketing costs

Exporters increasingly prioritizing Canada as a target market

Canada

Canada’s position in the global wine market…

Canadian Wine Market

International suppliers increasingly prioritizing Canada as a key export market

Canada’s Competitive Positioning

Ontario growers versus foreign competitors in the Canadian market

Who to watch

France facing excess supply

Australia looking to replace dependence on US, UK

US enjoys strong export pricing to Canada

Chile (esp. Concha y Toro) emphasizing Canadian market

Source: LCBO, Rabobank analysis, 2011

LCBO Wine Sales and Average Price per Liter by Source

Source Vol (Mn Lt.)

Canada 34

Italy 19.8

Australia 14

France 10.8

US 12.4

Argentina 8.8

Chile 7.2

Spain 2.6

South Africa 3.5