Canada Research Cara Operations Limited … · Cara Operations Limited September ... positioning...

36

Canada Research Published by Raymond James Ltd. Please read domestic and foreign disclosure/risk information beginning on page 32 and Analyst Certification on page 30. Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2 Cara Operations Limited September 29, 2015 CAO-TSX Company Report - Initiation of Coverage Kenric S. Tyghe MBA | 416.777.7188 | [email protected] Krisztina Katai (Associate) | 416.777.7060 | [email protected] Consumer & Retail A Chalet in the Mountains, and Runway for the Landing Recommendation We are initiating coverage of Cara Operations Ltd. (Cara) with an Outperform rating and a $38.00 target price. Cara’s turnaround under the new management team continues to gain traction, as highlighted by its stronger operating performance and recent acquisition activity (which we expect to accelerate). Same Restaurant Sales (SRS) growth continues to track higher (on relatively easy comps), as new marketing strategies resonate, which (on solid execution) is driving margin expansion. We expect that Cara will deliver strong (absolute and relative) revenue and EBITDA CAGRs of 12.1% and 16.3%, respectively, through our forecast window to 2017E, with potential acquisitions offering further upside as Cara flexes its under-levered balance sheet. Analysis While we are mindful of the risks associated with a turnaround play, we believe (based on recent performance) that the risk-adjusted opportunity is attractive. The team doesn’t need to hit it out of the park in order to win, but rather to consistently execute against its (relatively aggressive) game plan. Cara’s balance sheet supports both improving the health of the existing network and rapidly building out the network, positioning Cara to increase market share. The highly fragmented restaurant industry presents numerous sizeable and attractive potential acquisition targets, which offer upside to our estimates. The Canadian restaurant industry, in which Cara ranks third with a 3.4% share, grew at a 4.0% 10-year CAGR through 2014, despite the macro headwinds. The $50.4 bln (2014) Canadian Restaurant Industry grew at a 3.7% CAGR in the 5 years through 2009, with growth accelerating post the recession to 4.3% through 2014. We are conservatively modeling SRS growth at the low-end of Cara’s target range of 2.5%-4.0%, and modest EBITDA margin expansion through 2017E. Our 2016E EBITDA growth estimate of 17.8% to $122.1 mln is predicated on SRS growth of 2.4% (for 2016E revenue growth of 14.6% to $369.8 mln). Valuation We are initiating coverage of Cara with an Outperform rating and $38.00 target price. Our target price of $38.00 is based on 16.0x our 2016E EBITDA of $122.1 mln, for an imputed value of $37.52. Our EV/EBITDA based target price is well supported by our DCF valuation of $38.18. We believe Cara warrants a premium valuation relative to its fast casual peer group average of 14.2x 2016E EBITDA, given its relative EBITDA growth trajectory (and margin profile). See our Valuation & Recommendation section for details. EPS 1Q 2Q 3Q 4Q Full Revenues EBITDA Mar Jun Sep Dec Year (mln) (mln) 2014A C$0.18 C$0.23 C$0.12 C$(0.24) C$0.29 C$282 C$84 2015E 0.17A 0.31A 0.28 0.32 1.12 323 104 2016E 0.35 0.41 0.34 0.34 1.44 370 122 2017E 0.36 0.43 0.36 0.37 1.52 397 131 Source: Raymond James Ltd., Thomson One Outperform 2 C$38.00 target price Current Price ( Sep-25-15 ) C$33.00 Total Return to Target 16% 52-Week Range C$36.99 - C$29.52 Suitability Medium Risk/Growth Market Data Market Capitalization (mln) C$1,667 Current Net Debt (mln) C$64 Enterprise Value (mil.) C$1,731 Shares Outstanding (mln, f.d.) 51.0 10 Day Avg Daily Volume (000s) 11 Dividend/Yield C$0.37/1.1% Key Financial Metrics 2014A 2015E 2016E 2017E P/E N/M 29.6x 23.0x 21.7x EV/EBITDA 20.7x 16.7x 14.2x 13.2x Company Description Cara is a leading full-service restaurant franchisor and operator in Canada, with 827 restaurants under 10 banners. Cara operates a highly franchised system, with approximately 89% of restaurants franchised.

Transcript of Canada Research Cara Operations Limited … · Cara Operations Limited September ... positioning...

Canada Research Published by Raymond James Ltd.

Please read domestic and foreign disclosure/risk information beginning on page 32 and Analyst Certification on page 30. Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Cara Operations Limited September 29, 2015 CAO-TSX Company Report - Initiation of Coverage Kenric S. Tyghe MBA | 416.777.7188 | [email protected]

Krisztina Katai (Associate) | 416.777.7060 | [email protected]

Consumer & Retail

A Chalet in the Mountains, and Runway for the Landing

Recommendation We are initiating coverage of Cara Operations Ltd. (Cara) with an Outperform rating and a $38.00 target price. Cara’s turnaround under the new management team continues to gain traction, as highlighted by its stronger operating performance and recent acquisition activity (which we expect to accelerate). Same Restaurant Sales (SRS) growth continues to track higher (on relatively easy comps), as new marketing strategies resonate, which (on solid execution) is driving margin expansion. We expect that Cara will deliver strong (absolute and relative) revenue and EBITDA CAGRs of 12.1% and 16.3%, respectively, through our forecast window to 2017E, with potential acquisitions offering further upside as Cara flexes its under-levered balance sheet.

Analysis While we are mindful of the risks associated with a turnaround play, we believe

(based on recent performance) that the risk-adjusted opportunity is attractive. The team doesn’t need to hit it out of the park in order to win, but rather to consistently execute against its (relatively aggressive) game plan.

Cara’s balance sheet supports both improving the health of the existing network and rapidly building out the network, positioning Cara to increase market share. The highly fragmented restaurant industry presents numerous sizeable and attractive potential acquisition targets, which offer upside to our estimates.

The Canadian restaurant industry, in which Cara ranks third with a 3.4% share, grew at a 4.0% 10-year CAGR through 2014, despite the macro headwinds. The $50.4 bln (2014) Canadian Restaurant Industry grew at a 3.7% CAGR in the 5 years through 2009, with growth accelerating post the recession to 4.3% through 2014.

We are conservatively modeling SRS growth at the low-end of Cara’s target range of 2.5%-4.0%, and modest EBITDA margin expansion through 2017E. Our 2016E EBITDA growth estimate of 17.8% to $122.1 mln is predicated on SRS growth of 2.4% (for 2016E revenue growth of 14.6% to $369.8 mln).

Valuation We are initiating coverage of Cara with an Outperform rating and $38.00 target price. Our target price of $38.00 is based on 16.0x our 2016E EBITDA of $122.1 mln, for an imputed value of $37.52. Our EV/EBITDA based target price is well supported by our DCF valuation of $38.18. We believe Cara warrants a premium valuation relative to its fast casual peer group average of 14.2x 2016E EBITDA, given its relative EBITDA growth trajectory (and margin profile). See our Valuation & Recommendation section for details.

EPS 1Q 2Q 3Q 4Q Full Revenues EBITDA Mar Jun Sep Dec Year (mln) (mln)

2014A C$0.18 C$0.23 C$0.12 C$(0.24) C$0.29 C$282 C$84

2015E 0.17A 0.31A 0.28 0.32 1.12 323 104

2016E 0.35 0.41 0.34 0.34 1.44 370 122

2017E 0.36 0.43 0.36 0.37 1.52 397 131

Source: Raymond James Ltd., Thomson One

Outperform 2 C$38.00 target price

Current Price ( Sep-25-15 ) C$33.00 Total Return to Target 16% 52-Week Range C$36.99 - C$29.52 Suitability Medium Risk/Growth

Market Data Market Capitalization (mln) C$1,667 Current Net Debt (mln) C$64 Enterprise Value (mil.) C$1,731 Shares Outstanding (mln, f.d.) 51.0 10 Day Avg Daily Volume (000s) 11 Dividend/Yield C$0.37/1.1%

Key Financial Metrics 2014A 2015E 2016E 2017E

P/E N/M 29.6x 23.0x 21.7x

EV/EBITDA 20.7x 16.7x 14.2x 13.2x

Company Description Cara is a leading full-service restaurant franchisor and operator in Canada, with 827 restaurants under 10 banners. Cara operates a highly franchised system, with approximately 89% of restaurants franchised.

Canada Research | Page 2 of 36 Cara Operations Limited

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Table of Contents

Executive Summary ............................................................................................................................................. 4

Company Overview .............................................................................................................................................. 5

Investment Thesis ................................................................................................................................................ 8

Financial Analysis & Outlook................................................................................................................................ 18

Valuation & Recommendation ............................................................................................................................ 21

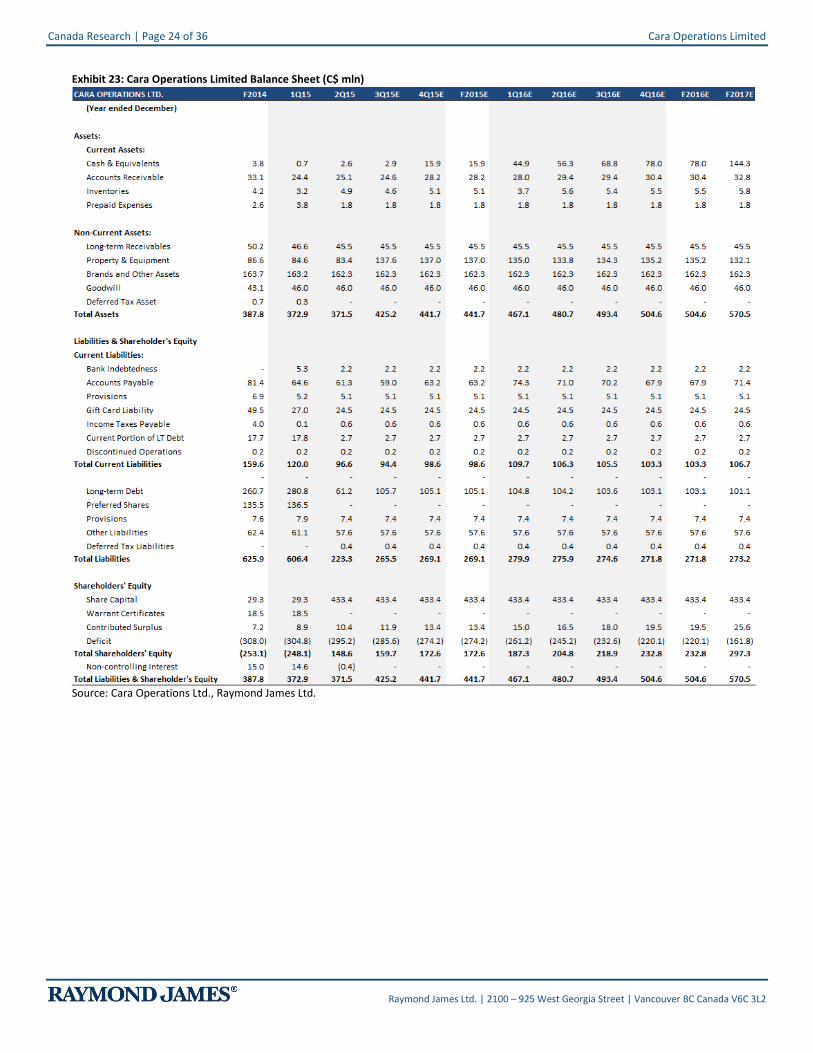

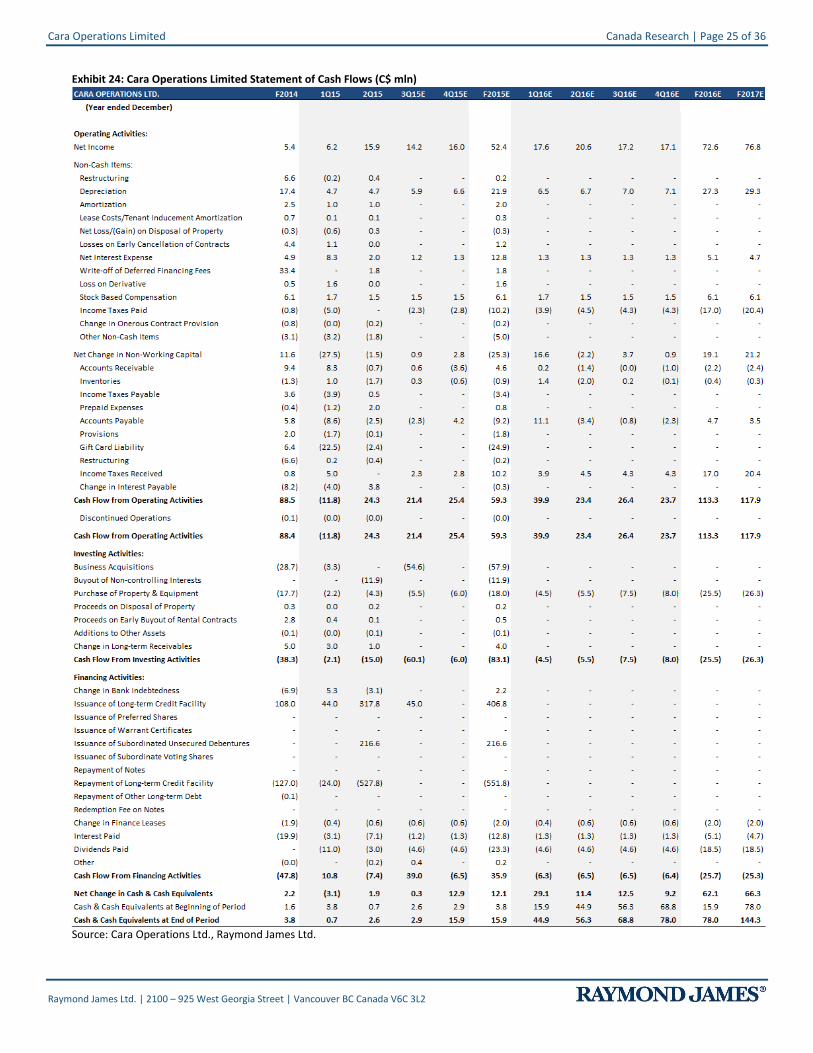

Appendix A: Financial Statements ....................................................................................................................... 23

Appendix B: Management & Board of Directors ................................................................................................. 26

Risks ..................................................................................................................................................................... 28

Cara Operations Limited Canada Research | Page 3 of 36

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

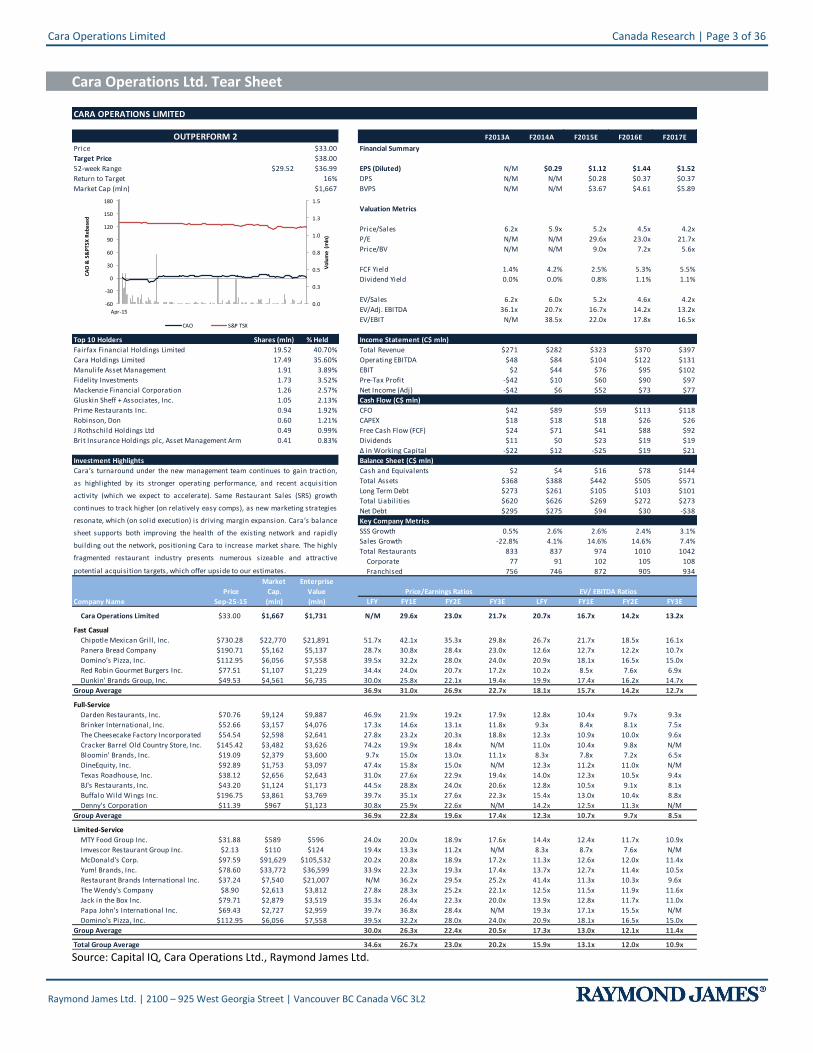

Cara Operations Ltd. Tear Sheet

CARA OPERATIONS LIMITED TSX:CAO

F2013A F2014A F2015E F2016E F2017E

Price $33.00 Financial Summary 12/31/2011 12/31/2013 12/31/2014 12/31/2015 12/30/2016 12/30/2017

Target Price $38.00

52-week Range $29.52 $36.99 EPS (Diluted) N/M $0.29 $1.12 $1.44 $1.52

Return to Target 16% DPS N/M N/M $0.28 $0.37 $0.37

Market Cap (mln) $1,667 BVPS N/M N/M $3.67 $4.61 $5.89

Valuation Metrics

Price/Sales 6.2x 5.9x 5.2x 4.5x 4.2x

P/E N/M N/M 29.6x 23.0x 21.7x

Price/BV N/M N/M 9.0x 7.2x 5.6x

FCF Yield 1.4% 4.2% 2.5% 5.3% 5.5%

Dividend Yield 0.0% 0.0% 0.8% 1.1% 1.1%

EV/Sales 6.2x 6.0x 5.2x 4.6x 4.2x

EV/Adj. EBITDA 36.1x 20.7x 16.7x 14.2x 13.2x

EV/EBIT N/M 38.5x 22.0x 17.8x 16.5x

18.9 18.9 47.0 50.5 50.5

Top 10 Holders Shares (mln) % Held Income Statement (C$ mln)

Fairfax Financial Holdings Limited 19.52 40.70% Total Revenue $271 $282 $323 $370 $397

Cara Holdings Limited 17.49 35.60% Operating EBITDA $48 $84 $104 $122 $131

Manulife Asset Management 1.91 3.89% EBIT $2 $44 $76 $95 $102

Fidelity Investments 1.73 3.52% Pre-Tax Profit -$42 $10 $60 $90 $97

Mackenzie Financial Corporation 1.26 2.57% Net Income (Adj) -$42 $6 $52 $73 $77

Gluskin Sheff + Associates, Inc. 1.05 2.13% Cash Flow (C$ mln)

Prime Restaurants Inc. 0.94 1.92% CFO $42 $89 $59 $113 $118

Robinson, Don 0.60 1.21% CAPEX $18 $18 $18 $26 $26

J Rothschild Holdings Ltd 0.49 0.99% Free Cash Flow (FCF) $24 $71 $41 $88 $92

Brit Insurance Holdings plc, Asset Management Arm 0.41 0.83% Dividends $11 $0 $23 $19 $19

Δ in Working Capital -$22 $12 -$25 $19 $21

Investment Highlights Balance Sheet (C$ mln)

Cash and Equivalents $2 $4 $16 $78 $144

Total Assets $368 $388 $442 $505 $571

Long Term Debt $273 $261 $105 $103 $101

Total Liabilities $620 $626 $269 $272 $273

Net Debt $295 $275 $94 $30 -$38

Key Company Metrics

SSS Growth 0.5% 2.6% 2.6% 2.4% 3.1%

Sales Growth -22.8% 4.1% 14.6% 14.6% 7.4%

Total Restaurants 833 837 974 1010 1042

Corporate 77 91 102 105 108

Franchised 756 746 872 905 934

Market

Price Cap.

Company Name Sep-25-15 (mln) LFY FY1E FY2E FY3E LFY FY1E FY2E FY3E1000 1001 1002 1003 1000 1001 1002 1003

Cara Operations Limited $33.00 $1,667 $1,731 TSX:CAO N/M 29.6x 23.0x 21.7x 20.7x 16.7x 14.2x 13.2x

Fast Casual

Chipotle Mexican Gril l , Inc. $730.28 $22,770 $21,891 CMG 51.7x 42.1x 35.3x 29.8x 26.7x 21.7x 18.5x 16.1x

Panera Bread Company $190.71 $5,162 $5,137 PNRA 28.7x 30.8x 28.4x 23.0x 12.6x 12.7x 12.2x 10.7x

Domino's Pizza, Inc. $112.95 $6,056 $7,558 DPZ 39.5x 32.2x 28.0x 24.0x 20.9x 18.1x 16.5x 15.0x

Red Robin Gourmet Burgers Inc. $77.51 $1,107 $1,229 RRGB 34.4x 24.0x 20.7x 17.2x 10.2x 8.5x 7.6x 6.9x

Dunkin' Brands Group, Inc. $49.53 $4,561 $6,735 DNKN 30.0x 25.8x 22.1x 19.4x 19.9x 17.4x 16.2x 14.7x

Group Average 36.9x 31.0x 26.9x 22.7x 18.1x 15.7x 14.2x 12.7x

Full-Service

Darden Restaurants, Inc. $70.76 $9,124 $9,887 DRI 46.9x 21.9x 19.2x 17.9x 12.8x 10.4x 9.7x 9.3x

Brinker International, Inc. $52.66 $3,157 $4,076 EAT 17.3x 14.6x 13.1x 11.8x 9.3x 8.4x 8.1x 7.5x

The Cheesecake Factory Incorporated $54.54 $2,598 $2,641 CAKE 27.8x 23.2x 20.3x 18.8x 12.3x 10.9x 10.0x 9.6x

Cracker Barrel Old Country Store, Inc. $145.42 $3,482 $3,626 CBRL 74.2x 19.9x 18.4x N/M 11.0x 10.4x 9.8x N/M

Bloomin' Brands, Inc. $19.09 $2,379 $3,600 BLMN 9.7x 15.0x 13.0x 11.1x 8.3x 7.8x 7.2x 6.5x

DineEquity, Inc. $92.89 $1,753 $3,097 DIN 47.4x 15.8x 15.0x N/M 12.3x 11.2x 11.0x N/M

Texas Roadhouse, Inc. $38.12 $2,656 $2,643 TXRH 31.0x 27.6x 22.9x 19.4x 14.0x 12.3x 10.5x 9.4x

BJ's Restaurants, Inc. $43.20 $1,124 $1,173 BJRI 44.5x 28.8x 24.0x 20.6x 12.8x 10.5x 9.1x 8.1x

Buffalo Wild Wings Inc. $196.75 $3,861 $3,769 BWLD 39.7x 35.1x 27.6x 22.3x 15.4x 13.0x 10.4x 8.8x

Denny's Corporation $11.39 $967 $1,123 DENN 30.8x 25.9x 22.6x N/M 14.2x 12.5x 11.3x N/M

Group Average 36.9x 22.8x 19.6x 17.4x 12.3x 10.7x 9.7x 8.5x.

Limited-Service

MTY Food Group Inc. $31.88 $589 $596 MTY 24.0x 20.0x 18.9x 17.6x 14.4x 12.4x 11.7x 10.9x

Imvescor Restaurant Group Inc. $2.13 $110 $124 TSX:IRG 19.4x 13.3x 11.2x N/M 8.3x 8.7x 7.6x N/M

McDonald's Corp. $97.59 $91,629 $105,532 MCD 20.2x 20.8x 18.9x 17.2x 11.3x 12.6x 12.0x 11.4x

Yum! Brands, Inc. $78.60 $33,772 $36,599 YUM 33.9x 22.3x 19.3x 17.4x 13.7x 12.7x 11.4x 10.5x

Restaurant Brands International Inc. $37.24 $7,540 $21,007 QSR N/M 36.2x 29.5x 25.2x 41.4x 11.3x 10.3x 9.6x

The Wendy's Company $8.90 $2,613 $3,812 WEN 27.8x 28.3x 25.2x 22.1x 12.5x 11.5x 11.9x 11.6x

Jack in the Box Inc. $79.71 $2,879 $3,519 JACK 35.3x 26.4x 22.3x 20.0x 13.9x 12.8x 11.7x 11.0x

Papa John's International Inc. $69.43 $2,727 $2,959 PZZA 39.7x 36.8x 28.4x N/M 19.3x 17.1x 15.5x N/M

Domino's Pizza, Inc. $112.95 $6,056 $7,558 DPZ 39.5x 32.2x 28.0x 24.0x 20.9x 18.1x 16.5x 15.0x

Group Average 30.0x 26.3x 22.4x 20.5x 17.3x 13.0x 12.1x 11.4x

Total Group Average 34.6x 26.7x 23.0x 20.2x 15.9x 13.1x 12.0x 10.9x

OUTPERFORM 2

Cara’s turnaround under the new management team continues to gain traction,

as highlighted by its stronger operating performance, and recent acquisition

activity (which we expect to accelerate). Same Restaurant Sales (SRS) growth

continues to track higher (on relatively easy comps), as new marketing strategies

resonate, which (on solid execution) is driving margin expansion. Cara’s balance

sheet supports both improving the health of the existing network and rapidly

building out the network, positioning Cara to increase market share. The highly

fragmented restaurant industry presents numerous sizeable and attractive

potential acquisition targets, which offer upside to our estimates.

Enterprise

Value

(mln)

Price/Earnings Ratios EV/ EBITDA Ratios

0.0

0.3

0.5

0.8

1.0

1.3

1.5

-60

-30

0

30

60

90

120

150

180

Apr-15

Vo

lum

e (

mln

)

CA

O &

S&

PT

SX

Re

ba

sed

CAO S&P TSX

Source: Capital IQ, Cara Operations Ltd., Raymond James Ltd.

Canada Research | Page 4 of 36 Cara Operations Limited

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Executive Summary

Turnaround Play Poised to Lever its Market Share

The $50.4 bln (2014) Canadian Restaurant Industry is fragmented, with the top 5 restaurant chains accounting for approximately 31% of the market and the next 195 largest chains accounting for 29% (the top 10 largest chains comprise 40% of restaurant industry sales). The restaurant industry grew at a 4.0% 10-year CAGR through 2014, with growth accelerating from 3.7% in the 5 years through 2009 to 4.3% through 2014, led by growth in limited-service (Harvey’s is Cara’s only limited-service banner). The 5-year full-service CAGR through 2014 was 3.9% versus limited-service of 4.7%, according to Statistics Canada.

Cara, with a 3.4% market share, is the third largest player in Canada behind Restaurant Brands International (13.6%) and McDonald’s (8.0%), with the balance sheet (and appetite) to make meaningful potential acquisitions through our forecast window. With 72% of its network in Ontario, Cara’s performance is closely tied to that of Ontario’s economic growth which, according to the Conference Board of Canada, is expected to outpace the national average for the first time since 2002 (approximately 16% of Cara’s network is in Western Canada).

Franchise Model – Asset Light, FCF Heavy

Cara’s transformation into a pure play restaurant operator began in 2004 with its privatization by the Phelan family, subsequent to which (i) a number of non-core (non-restaurant) assets were divested, and (ii) Cara began the transformation to a largely franchise-driven business model. Prior to its privatization in 2004, Cara’s model was 58% franchised versus 89% today. The capital-light business model shifts CAPEX (and operating costs) to franchisees, generating both strong FCF and ROE metrics, and lends itself to both organic (and acquisition) driven network growth (with attractive peer group relative economics).

While the franchise model supported (and continues to support) EBITDA margin expansion, it is significant cost cutting initiatives (which accelerated under new management) that have driven the marked increase in the EBITDA margins. In 2012, SG&A margins were 66.8% (on SG&A dollars of $233.9 mln), versus 57.7% in 2014.

New (Highly Qualified) Management Team to Drive Turnaround

The new management team has significant retail turnaround and food service experience. The three key members of the new team include the CEO (Mr. Bill Gregson), the CFO (Mr. Ken Grondin) and the President (Family Division) and Chief Development Officer (Mr. Ken Otto). During their tenures at The Brick, Mr. Gregson (who served as CEO from July 2009) and Mr. Grondin (who served as CFO from April 2011) led The Brick through a successful turnaround (and ultimate sale to Leon’s Furniture). Prior to joining The Brick, Mr. Gregson led a successful turnaround of Forzani Group Ltd., where he served as President and Chief Operating Officer.

While Cara is a turnaround play (with aggressive, but in our opinion achievable, organic growth targets), we expect that potential acquisitions to complement the organic growth opportunity will (i) focus on markets outside of Ontario, and (ii) target solid (not troubled) banners, from which growth (and synergies) can be driven by levering Cara’s infrastructure.

Potential Acquisitions to Complement Organic Growth

Cara is, we believe, well positioned to continue to consolidate the highly fragmented Canadian restaurant industry, given its market share, track record of successful integration of acquisitions (Prime Restaurants and The Landing Group) to date, and under-levered balance sheet.

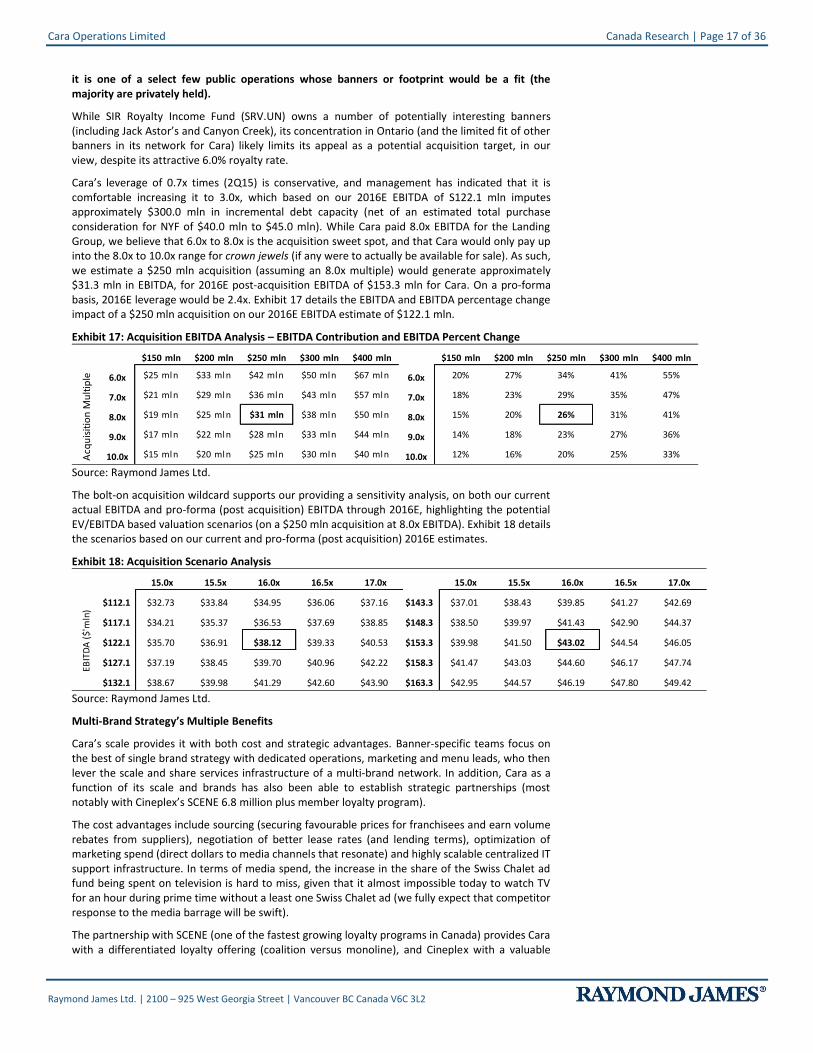

Cara’s leverage of 0.7x times (2Q15) is conservative, and management has indicated that it is comfortable increasing it to 3.0x (approximately $300.0 mln in incremental debt capacity). While Cara paid 8.0x EBITDA for the Landing Group, we believe that 6.0x – 8.0x is the acquisition sweet spot, and that Cara would only pay up into the 8.0x – 10.0x range for crown jewels. We estimate a $250 mln acquisition (on an 8.0x multiple) would generate approximately $31.3 mln in EBITDA (for a 26% 2016E EBITDA estimate increase from $122.1 mln to $153.3 mln). Exhibit 17 details our sensitivity analysis.

While we believe that a bolt-on acquisition of the likes of St-Hubert would bring immediate scale to Cara’s operations in Québec, a series of smaller tuck in acquisitions is equally probable. We detail some of what we believe are the more attractive targets in the report.

Cara Operations Limited Canada Research | Page 5 of 36

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Company Overview

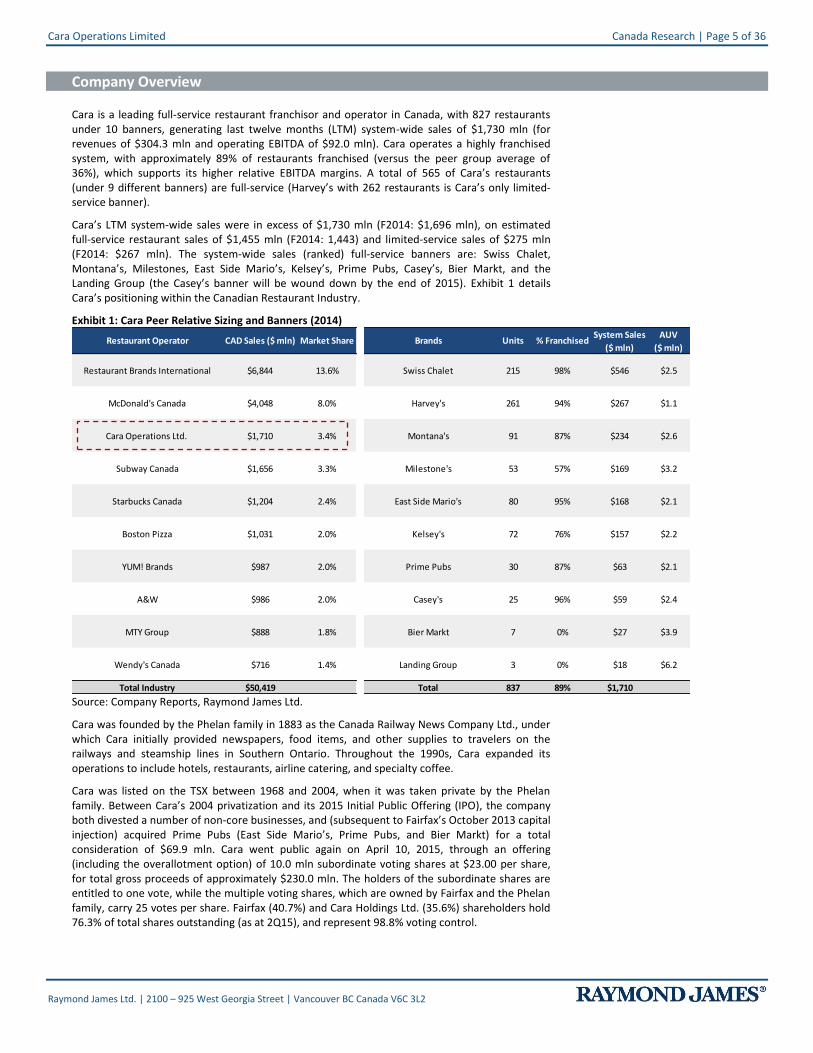

Cara is a leading full-service restaurant franchisor and operator in Canada, with 827 restaurants under 10 banners, generating last twelve months (LTM) system-wide sales of $1,730 mln (for revenues of $304.3 mln and operating EBITDA of $92.0 mln). Cara operates a highly franchised system, with approximately 89% of restaurants franchised (versus the peer group average of 36%), which supports its higher relative EBITDA margins. A total of 565 of Cara’s restaurants (under 9 different banners) are full-service (Harvey’s with 262 restaurants is Cara’s only limited-service banner).

Cara’s LTM system-wide sales were in excess of $1,730 mln (F2014: $1,696 mln), on estimated full-service restaurant sales of $1,455 mln (F2014: 1,443) and limited-service sales of $275 mln (F2014: $267 mln). The system-wide sales (ranked) full-service banners are: Swiss Chalet, Montana’s, Milestones, East Side Mario’s, Kelsey’s, Prime Pubs, Casey’s, Bier Markt, and the Landing Group (the Casey’s banner will be wound down by the end of 2015). Exhibit 1 details Cara’s positioning within the Canadian Restaurant Industry.

Exhibit 1: Cara Peer Relative Sizing and Banners (2014)

Restaurant Brands International $6,844 13.6% Swiss Chalet 215 98% $546 $2.5

McDonald's Canada $4,048 8.0% Harvey's 261 94% $267 $1.1

Cara Operations Ltd. $1,710 3.4% Montana's 91 87% $234 $2.6

Subway Canada $1,656 3.3% Milestone's 53 57% $169 $3.2

Starbucks Canada $1,204 2.4% East Side Mario's 80 95% $168 $2.1

Boston Pizza $1,031 2.0% Kelsey's 72 76% $157 $2.2

YUM! Brands $987 2.0% Prime Pubs 30 87% $63 $2.1

A&W $986 2.0% Casey's 25 96% $59 $2.4

MTY Group $888 1.8% Bier Markt 7 0% $27 $3.9

Wendy's Canada $716 1.4% Landing Group 3 0% $18 $6.2

Total Industry $50,419 Total 837 89% $1,710

% FranchisedSystem Sales

($ mln)

AUV

($ mln)Restaurant Operator CAD Sales ($ mln) Market Share Brands Units

Source: Company Reports, Raymond James Ltd.

Cara was founded by the Phelan family in 1883 as the Canada Railway News Company Ltd., under which Cara initially provided newspapers, food items, and other supplies to travelers on the railways and steamship lines in Southern Ontario. Throughout the 1990s, Cara expanded its operations to include hotels, restaurants, airline catering, and specialty coffee.

Cara was listed on the TSX between 1968 and 2004, when it was taken private by the Phelan family. Between Cara’s 2004 privatization and its 2015 Initial Public Offering (IPO), the company both divested a number of non-core businesses, and (subsequent to Fairfax’s October 2013 capital injection) acquired Prime Pubs (East Side Mario’s, Prime Pubs, and Bier Markt) for a total consideration of $69.9 mln. Cara went public again on April 10, 2015, through an offering (including the overallotment option) of 10.0 mln subordinate voting shares at $23.00 per share, for total gross proceeds of approximately $230.0 mln. The holders of the subordinate shares are entitled to one vote, while the multiple voting shares, which are owned by Fairfax and the Phelan family, carry 25 votes per share. Fairfax (40.7%) and Cara Holdings Ltd. (35.6%) shareholders hold 76.3% of total shares outstanding (as at 2Q15), and represent 98.8% voting control.

Canada Research | Page 6 of 36 Cara Operations Limited

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Fairfax Financial Holdings Limited made its initial $170 mln investment in Cara in October 2013, which consisted of $100 mln in cash and the vending into Cara of Prime Restaurants Inc., for a total consideration of $69.6 mln (net of $3.9 mln long-term debt retired). In November 2013, Fairfax purchased a 51% interest Keg Restaurants chain, which reported 2014 system-wide sales of $520.7 mln. On December 18, 2014, Cara acquired a 55% interest in the Landing Group for $18.3 mln and had an option to acquire the remaining 45% at any time until December 18, 2018 (on June 26, 2015 Cara purchased the remaining 45%).

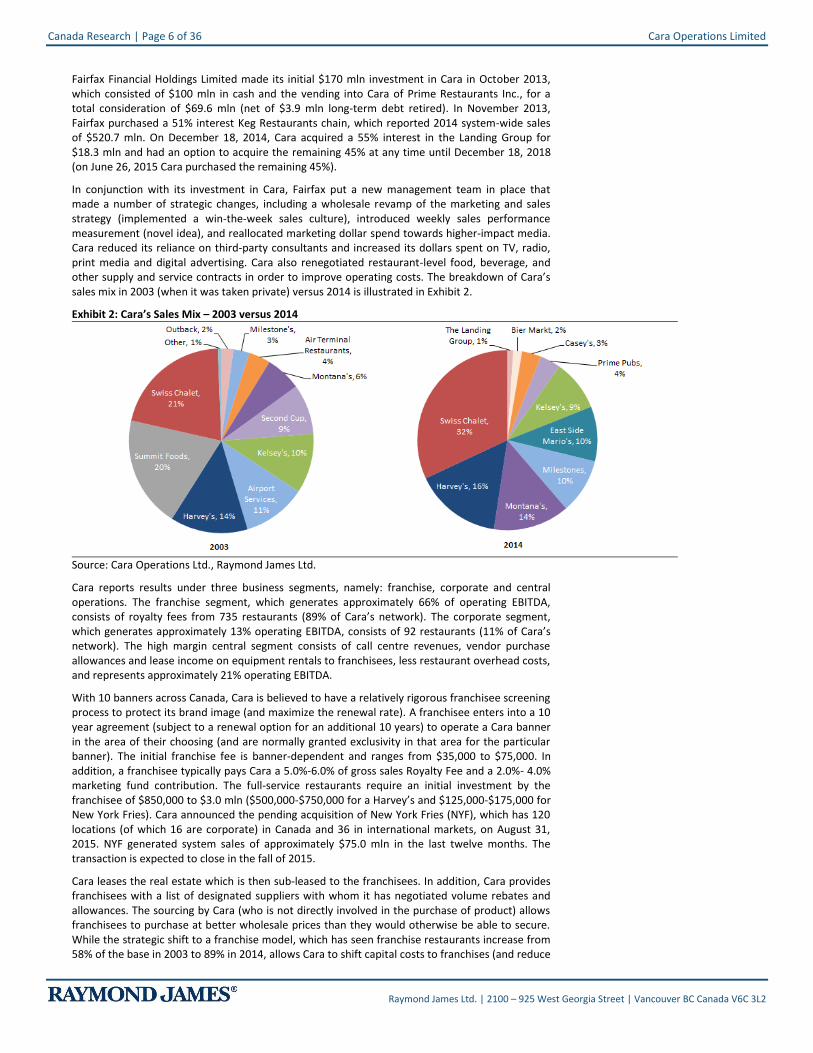

In conjunction with its investment in Cara, Fairfax put a new management team in place that made a number of strategic changes, including a wholesale revamp of the marketing and sales strategy (implemented a win-the-week sales culture), introduced weekly sales performance measurement (novel idea), and reallocated marketing dollar spend towards higher-impact media. Cara reduced its reliance on third-party consultants and increased its dollars spent on TV, radio, print media and digital advertising. Cara also renegotiated restaurant-level food, beverage, and other supply and service contracts in order to improve operating costs. The breakdown of Cara’s sales mix in 2003 (when it was taken private) versus 2014 is illustrated in Exhibit 2.

Exhibit 2: Cara’s Sales Mix – 2003 versus 2014

Source: Cara Operations Ltd., Raymond James Ltd.

Cara reports results under three business segments, namely: franchise, corporate and central operations. The franchise segment, which generates approximately 66% of operating EBITDA, consists of royalty fees from 735 restaurants (89% of Cara’s network). The corporate segment, which generates approximately 13% operating EBITDA, consists of 92 restaurants (11% of Cara’s network). The high margin central segment consists of call centre revenues, vendor purchase allowances and lease income on equipment rentals to franchisees, less restaurant overhead costs, and represents approximately 21% operating EBITDA.

With 10 banners across Canada, Cara is believed to have a relatively rigorous franchisee screening process to protect its brand image (and maximize the renewal rate). A franchisee enters into a 10 year agreement (subject to a renewal option for an additional 10 years) to operate a Cara banner in the area of their choosing (and are normally granted exclusivity in that area for the particular banner). The initial franchise fee is banner-dependent and ranges from $35,000 to $75,000. In addition, a franchisee typically pays Cara a 5.0%-6.0% of gross sales Royalty Fee and a 2.0%- 4.0% marketing fund contribution. The full-service restaurants require an initial investment by the franchisee of $850,000 to $3.0 mln ($500,000-$750,000 for a Harvey’s and $125,000-$175,000 for New York Fries). Cara announced the pending acquisition of New York Fries (NYF), which has 120 locations (of which 16 are corporate) in Canada and 36 in international markets, on August 31, 2015. NYF generated system sales of approximately $75.0 mln in the last twelve months. The transaction is expected to close in the fall of 2015.

Cara leases the real estate which is then sub-leased to the franchisees. In addition, Cara provides franchisees with a list of designated suppliers with whom it has negotiated volume rebates and allowances. The sourcing by Cara (who is not directly involved in the purchase of product) allows franchisees to purchase at better wholesale prices than they would otherwise be able to secure. While the strategic shift to a franchise model, which has seen franchise restaurants increase from 58% of the base in 2003 to 89% in 2014, allows Cara to shift capital costs to franchises (and reduce

Cara Operations Limited Canada Research | Page 7 of 36

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

working capital requirements), Cara does provide franchisee relief for less profitable restaurants. New franchisees start at full royalty rates.

While Cara currently has approximately 36 pre-qualified candidates from whom it has received deposits of $1.5 mln, we believe the more interesting stats are: (i) management’s confidence in its ability to refresh the franchisee pool, (ii) that approximately 50% of the interest is coming from existing franchisees (speaking to increased brand resonance supporting underlying restaurant performance), and (iii) that new franchisees (or franchisee investor groups) must include a seasoned operator with a minimum 10% equity interest in the venture.

A key target for Cara is to reduce franchisee support in order to drive an increase in the effective royalty rate from 3.7% in 2014 to a target of 5.0% through 2020, which will necessitate a further improvement in overall network health and profitability. New York Fries franchisees typically pay a 6.0% royalty rate on sales, versus Cara’s effective 3.9% in 2Q15. While NYF’s effective royalty (given franchisee support) is modestly below 6.0%, it is expected to boost Cara’s royalty rate. Exhibit 3 details key banners by format (limited- or full-service). The upscale casual Bier Markt and Landing Group are corporate owned.

Exhibit 3: Overview of Key Cara Banners by Format and Areas of Focus

Average

ChequeUnder $8.50 $8 to $12 $8 to $12 $12 to $30 $20 to $50 $50+

Brands Area of Focus

Limited-Service Restaurants

Quick Service

Restaurants

Fast Casual

Restaurants

Full -Service Restaurants

Midscale

Restaurants

Casual-Dining

Restaurants

Upscale Casual-

Dining Restaurants

Fine Dining

Restaurants

Source: Cara Operations Ltd., Raymond James Ltd.

While Cara has a national footprint, 72% of its restaurants are concentrated in Ontario, with population density per Cara restaurant of 22,846 versus Atlantic Canada at 55,161, Western Canada at 85,001 and Québec at 135,021. Management is targeting growth outside of Ontario, particularly in Western Canada and Québec, to build out the Cara network which (excluding potential bolt-on acquisitions) we expect will be led by Swiss Chalet and Harvey’s. Exhibit 4 below details Cara’s restaurant network.

Exhibit 4: Cara’s Restaurant Network (as of 2Q15)

Source: Cara Operations Ltd., Raymond James Ltd.

Canada Research | Page 8 of 36 Cara Operations Limited

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Investment Thesis

Leading Canadian Restaurant Operator; Overview of Canadian Restaurant Landscape

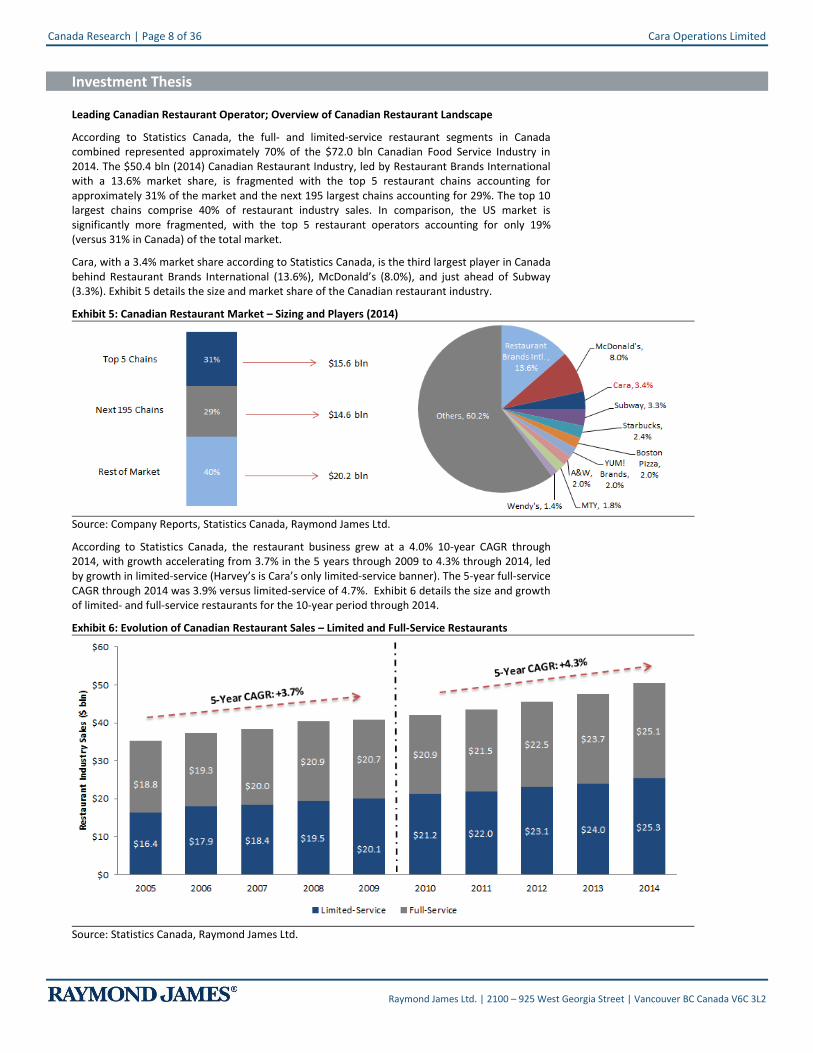

According to Statistics Canada, the full- and limited-service restaurant segments in Canada combined represented approximately 70% of the $72.0 bln Canadian Food Service Industry in 2014. The $50.4 bln (2014) Canadian Restaurant Industry, led by Restaurant Brands International with a 13.6% market share, is fragmented with the top 5 restaurant chains accounting for approximately 31% of the market and the next 195 largest chains accounting for 29%. The top 10 largest chains comprise 40% of restaurant industry sales. In comparison, the US market is significantly more fragmented, with the top 5 restaurant operators accounting for only 19% (versus 31% in Canada) of the total market.

Cara, with a 3.4% market share according to Statistics Canada, is the third largest player in Canada behind Restaurant Brands International (13.6%), McDonald’s (8.0%), and just ahead of Subway (3.3%). Exhibit 5 details the size and market share of the Canadian restaurant industry.

Exhibit 5: Canadian Restaurant Market – Sizing and Players (2014)

Source: Company Reports, Statistics Canada, Raymond James Ltd.

According to Statistics Canada, the restaurant business grew at a 4.0% 10-year CAGR through 2014, with growth accelerating from 3.7% in the 5 years through 2009 to 4.3% through 2014, led by growth in limited-service (Harvey’s is Cara’s only limited-service banner). The 5-year full-service CAGR through 2014 was 3.9% versus limited-service of 4.7%. Exhibit 6 details the size and growth of limited- and full-service restaurants for the 10-year period through 2014.

Exhibit 6: Evolution of Canadian Restaurant Sales – Limited and Full-Service Restaurants

Source: Statistics Canada, Raymond James Ltd.

Cara Operations Limited Canada Research | Page 9 of 36

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

In the 10-year period through 2014, the correlation between real GDP and full-service restaurant sales was a strong 0.6, with limited-service (lower average cheque) restaurants necessarily faring better in periods of economic weakness. In limited-service restaurants, the average cheque is under $8.50 versus full-service where the average cheque is in the range of $8.00 to $50.00. In the last 10 years, full-service restaurant sales have only decreased in one year (2009), while limited-service restaurant sales have not experienced a sales decline in any year. Between 2006-2008, both full-service and limited-service restaurant sales were robust, growing at CAGRs of 3.8% and 4.4%, respectively, which slowed through 2010 (the recession and early recovery) to 4.3% and 0.2%. The full-service pendulum swung as the recovery gathered momentum, with a robust 4.6% CAGR in the 2010-2014 period (versus 4.5% at limited-service restaurants).

As highlighted, both Cara and its peer group benefited from favourable underlying macro trends through 2014, which supported positive Same Restaurant Sales (SRS) trends. Cara reported SRS sales of 2.6% (versus a target of 2.5%-4.0%) in 2014, driven largely by particularly strong 4Q14 SRS of 4.8%. In addition, Cara bested its key full-service peers in the market, despite what was an impressive acceleration through 2014 by SIR Royalty Corp. (SRV.UN) operated Jack Astor’s and Boston Pizza Royalties Income Fund (BPF.UN) owned Boston Pizza. The performance of Cara, SIR Royalty, and BP Royalty banners is in sharp contrast to that of Brinker International (EAT) operated Olive Garden, which had a tough 2014 posting an SRS decrease of -2.4%. Through 2Q15, Jack Astor’s has stalled (posting negative SRS growth), while Cara has managed to maintain positive comps, and Olive Garden continues to build momentum (albeit on easy comps). Exhibit 7 details Cara’s SRS performance relative to Canadian full-service restaurant sales through 2Q15.

Exhibit 7: SRS Performance versus Canadian Full-Service Restaurant Sales

Source: Cara Operations Ltd., Raymond James Ltd.

While the correlation between the broader macro backdrop necessarily plays into consumer sentiment and the propensity to eat out, it is to the performance of the Ontario economy that Cara is most highly leveraged. Approximately 72% of Cara’s footprint is based in Ontario. According to the Conference Board of Canada, Ontario’s (oil consuming) GDP growth in 2015, bolstered by strong exports (on higher US growth) and consumer spending (cost savings from lower gas prices), is expected to outpace the national average of 1.1% (BOC, July 15, 2015 – MPR) for the first time since 2002.

We believe that Cara’s organic national unit growth plans are most likely to be led by Swiss Chalet and Harvey’s in the short- to medium-term, given the relative economics of franchise versus corporate. Ontario is home to 161 Swiss Chalet and 180 Harvey’s, which represent 57.3% of the Ontario base and 41.4% on the National base. Management believes that the Swiss Chalet banner has the potential to essentially double sales from the current $546 mln to $1.0 bln over the longer term. The Ontario-focused Bier Markt and Landing restaurants require heavy absolute and relative CAPEX, and site selection is that much harder (there are a very finite number of markets in which either concept will work well). As a point of reference, we are regulars at Harpers Landing (Oakville), and while we like the concept (and execution is generally solid) there is nothing particularly special or differentiated about the concept, experience or menu, in our opinion.

Canada Research | Page 10 of 36 Cara Operations Limited

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Franchise Model – Asset Light, FCF Heavy

Cara’s transformation into a pure play restaurant operator began in 2004 with its privatization (resulting in leverage of 3.7x EBITDA at the time of its privatization) by the Phelan family, subsequent to which (i) a number of non-core (non-restaurant) assets were divested, and (ii) Cara began the transformation to a largely franchise-driven business model.

The divested assets included the airline catering and logistics business (Cara Airport Services), the food service distribution business (Summit), the air terminal restaurants (ATR), the specialty coffee business (Second Cup) and select restaurant banners (Outback). The proceeds from the divestitures were not used to pay down debt, but to further invest in the business, resulting in a higher cost base (new head office, new data centre, new stores). The financial crisis exacerbated the challenges and by 2012 debt-to-EBITDA was 7.1x.

Prior to its privatization in 2004, Cara’s model was 58% franchised versus 89% today. The capital-light business model shifts CAPEX (and operating costs) to franchisees, generating both strong FCF and ROE metrics, and lends itself to both organic (and acquisition) driven network growth (with attractive peer group relative economics).

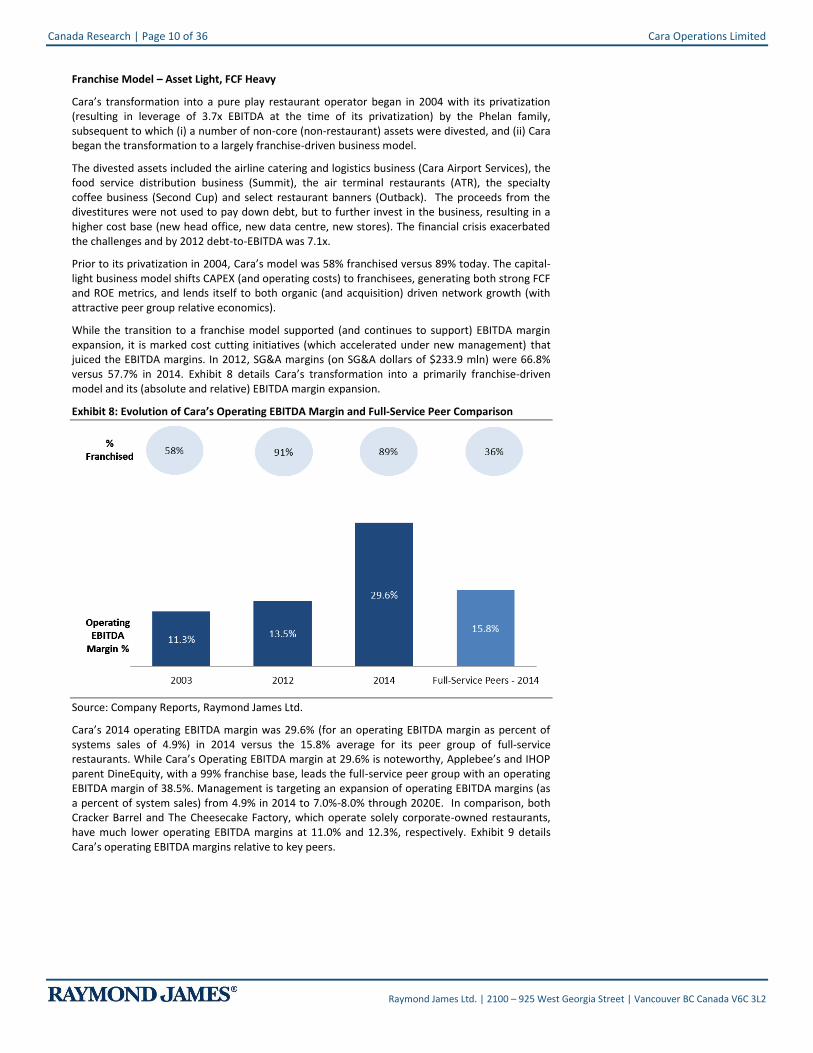

While the transition to a franchise model supported (and continues to support) EBITDA margin expansion, it is marked cost cutting initiatives (which accelerated under new management) that juiced the EBITDA margins. In 2012, SG&A margins (on SG&A dollars of $233.9 mln) were 66.8% versus 57.7% in 2014. Exhibit 8 details Cara’s transformation into a primarily franchise-driven model and its (absolute and relative) EBITDA margin expansion.

Exhibit 8: Evolution of Cara’s Operating EBITDA Margin and Full-Service Peer Comparison

Source: Company Reports, Raymond James Ltd.

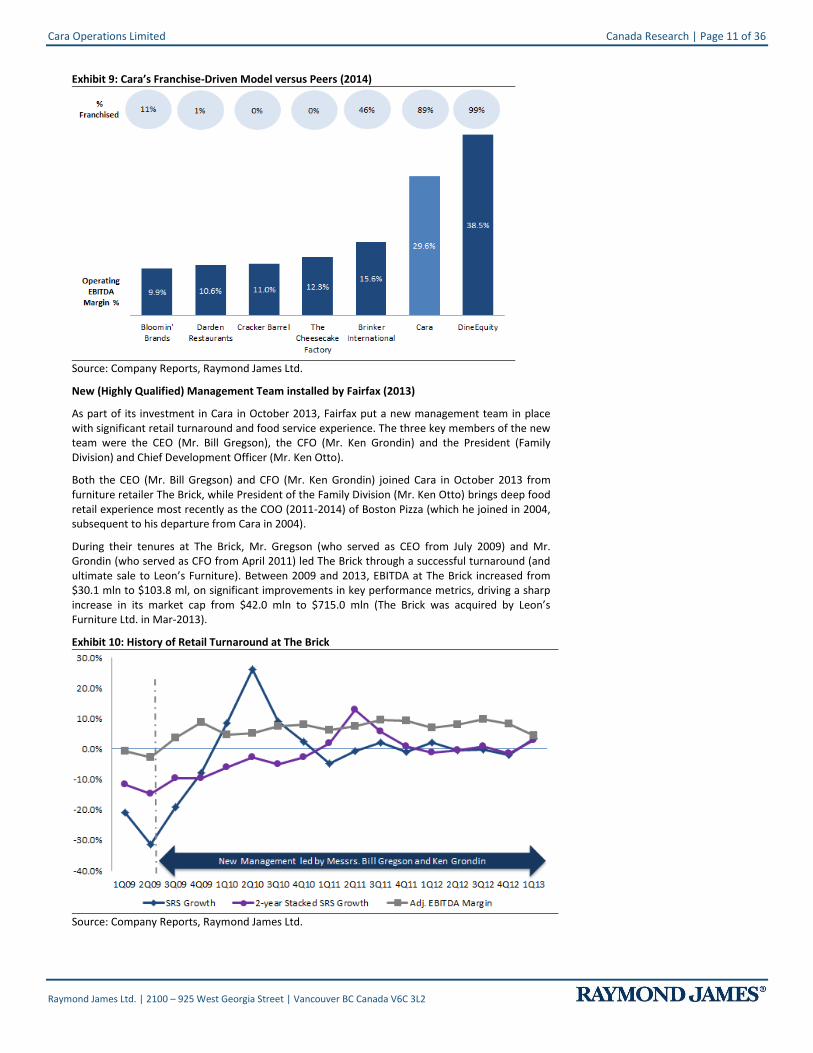

Cara’s 2014 operating EBITDA margin was 29.6% (for an operating EBITDA margin as percent of systems sales of 4.9%) in 2014 versus the 15.8% average for its peer group of full-service restaurants. While Cara’s Operating EBITDA margin at 29.6% is noteworthy, Applebee’s and IHOP parent DineEquity, with a 99% franchise base, leads the full-service peer group with an operating EBITDA margin of 38.5%. Management is targeting an expansion of operating EBITDA margins (as a percent of system sales) from 4.9% in 2014 to 7.0%-8.0% through 2020E. In comparison, both Cracker Barrel and The Cheesecake Factory, which operate solely corporate-owned restaurants, have much lower operating EBITDA margins at 11.0% and 12.3%, respectively. Exhibit 9 details Cara’s operating EBITDA margins relative to key peers.

Cara Operations Limited Canada Research | Page 11 of 36

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Exhibit 9: Cara’s Franchise-Driven Model versus Peers (2014)

Source: Company Reports, Raymond James Ltd.

New (Highly Qualified) Management Team installed by Fairfax (2013)

As part of its investment in Cara in October 2013, Fairfax put a new management team in place with significant retail turnaround and food service experience. The three key members of the new team were the CEO (Mr. Bill Gregson), the CFO (Mr. Ken Grondin) and the President (Family Division) and Chief Development Officer (Mr. Ken Otto).

Both the CEO (Mr. Bill Gregson) and CFO (Mr. Ken Grondin) joined Cara in October 2013 from furniture retailer The Brick, while President of the Family Division (Mr. Ken Otto) brings deep food retail experience most recently as the COO (2011-2014) of Boston Pizza (which he joined in 2004, subsequent to his departure from Cara in 2004).

During their tenures at The Brick, Mr. Gregson (who served as CEO from July 2009) and Mr. Grondin (who served as CFO from April 2011) led The Brick through a successful turnaround (and ultimate sale to Leon’s Furniture). Between 2009 and 2013, EBITDA at The Brick increased from $30.1 mln to $103.8 ml, on significant improvements in key performance metrics, driving a sharp increase in its market cap from $42.0 mln to $715.0 mln (The Brick was acquired by Leon’s Furniture Ltd. in Mar-2013).

Exhibit 10: History of Retail Turnaround at The Brick

Source: Company Reports, Raymond James Ltd.

Canada Research | Page 12 of 36 Cara Operations Limited

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Prior to joining The Brick, Mr. Gregson led a successful turnaround of Forzani Group Ltd., where he served as President and Chief Operating Officer. Under his leadership, Forzani’s EBITDA grew from negative $3.0 mln in 1997 to $123.0 mln in 2008, while market capitalization increased from $11.0 mln to $551.0 mln.

The employment inducements, options awarded (and vesting periods) required to secure the services of this team, are we believe worth noting. While the options expire on the 8

th anniversary

of the grant (for expiry dates that range between October 31, 2021 and September 8, 2022), and generally vest on a pro-rata annual basis over the life of the option, the options issued under the Legacy Share Option Plan are subject to accelerated vesting provisions. In terms of the accelerated vesting provision, 50% of Mr. Gregson’s initial option tranches vest on October 31, 2015, with the balance vesting on October 31, 2016. Additionally, the majority of Mr. Grondin’s options vest on October 31, 2016. Exhibit 11 details the existing options and their vesting dates.

Exhibit 11: Summary of Select Employment Inducements

# of Options Exercise Price Expiry Date

William D. Gregson 1,075,268 $0.01 Oct-31-2021 50% of Tranche Oct-31-2015

2,419,354 $8.51 Oct-31-2021 50% of Tranche Oct-31-2016

Kenneth J. Grondin 241,935 $8.51 Oct-31-2021 Oct-31-2016

26,440 $8.51 Dec-04-2022 Dec-04-2017

Kenneth Otto 215,052 $8.51 Sep-08-2022 Sep-08-2017

Vesting Date

Source: Cara Operations Ltd., Raymond James Ltd.

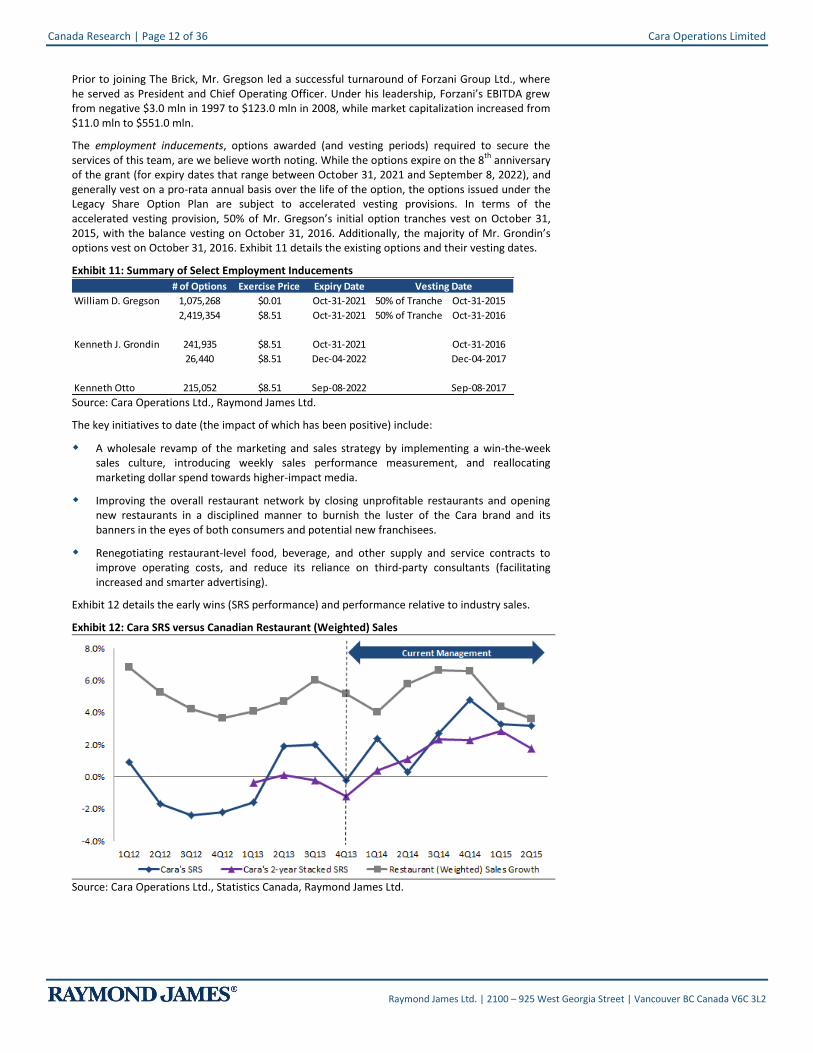

The key initiatives to date (the impact of which has been positive) include:

A wholesale revamp of the marketing and sales strategy by implementing a win-the-week sales culture, introducing weekly sales performance measurement, and reallocating marketing dollar spend towards higher-impact media.

Improving the overall restaurant network by closing unprofitable restaurants and opening new restaurants in a disciplined manner to burnish the luster of the Cara brand and its banners in the eyes of both consumers and potential new franchisees.

Renegotiating restaurant-level food, beverage, and other supply and service contracts to improve operating costs, and reduce its reliance on third-party consultants (facilitating increased and smarter advertising).

Exhibit 12 details the early wins (SRS performance) and performance relative to industry sales.

Exhibit 12: Cara SRS versus Canadian Restaurant (Weighted) Sales

Source: Cara Operations Ltd., Statistics Canada, Raymond James Ltd.

Cara Operations Limited Canada Research | Page 13 of 36

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

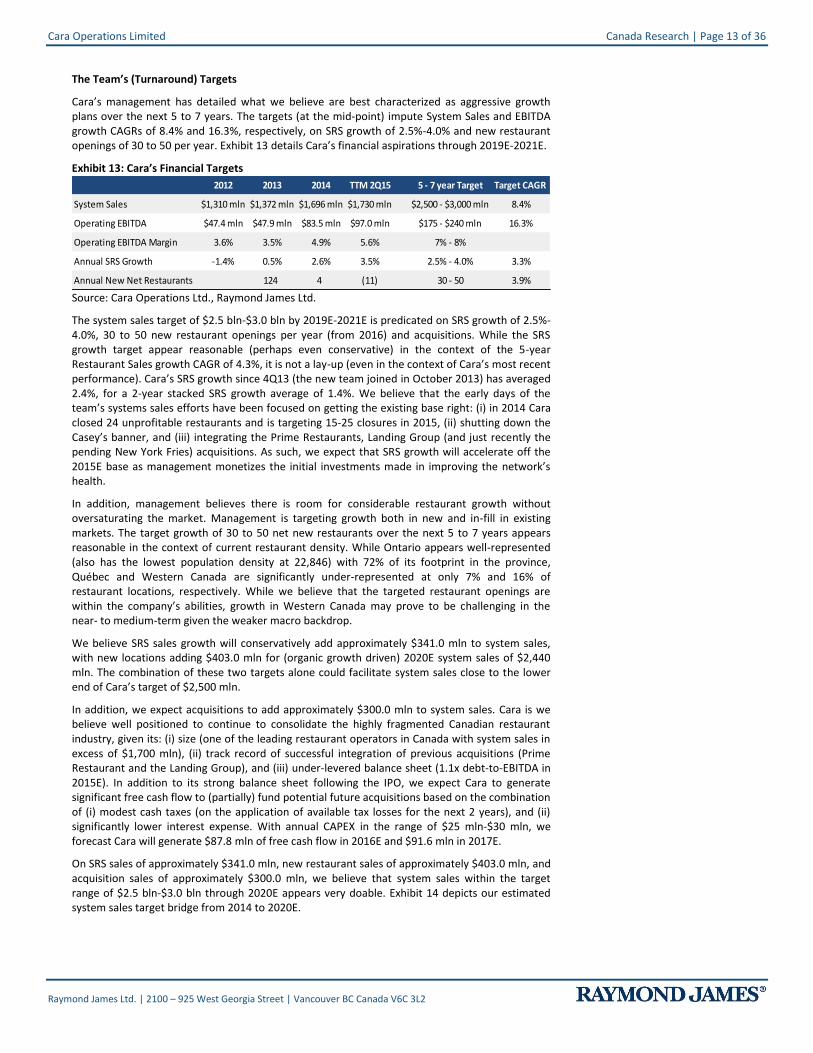

The Team’s (Turnaround) Targets

Cara’s management has detailed what we believe are best characterized as aggressive growth plans over the next 5 to 7 years. The targets (at the mid-point) impute System Sales and EBITDA growth CAGRs of 8.4% and 16.3%, respectively, on SRS growth of 2.5%-4.0% and new restaurant openings of 30 to 50 per year. Exhibit 13 details Cara’s financial aspirations through 2019E-2021E.

Exhibit 13: Cara’s Financial Targets

2012 2013 2014 TTM 2Q15 5 - 7 year Target Target CAGR

System Sales $1,310 mln $1,372 mln $1,696 mln $1,730 mln $2,500 - $3,000 mln 8.4%

Operating EBITDA $47.4 mln $47.9 mln $83.5 mln $97.0 mln $175 - $240 mln 16.3%

Operating EBITDA Margin 3.6% 3.5% 4.9% 5.6% 7% - 8%

Annual SRS Growth -1.4% 0.5% 2.6% 3.5% 2.5% - 4.0% 3.3%

Annual New Net Restaurants 124 4 (11) 30 - 50 3.9%

Source: Cara Operations Ltd., Raymond James Ltd.

The system sales target of $2.5 bln-$3.0 bln by 2019E-2021E is predicated on SRS growth of 2.5%-4.0%, 30 to 50 new restaurant openings per year (from 2016) and acquisitions. While the SRS growth target appear reasonable (perhaps even conservative) in the context of the 5-year Restaurant Sales growth CAGR of 4.3%, it is not a lay-up (even in the context of Cara’s most recent performance). Cara’s SRS growth since 4Q13 (the new team joined in October 2013) has averaged 2.4%, for a 2-year stacked SRS growth average of 1.4%. We believe that the early days of the team’s systems sales efforts have been focused on getting the existing base right: (i) in 2014 Cara closed 24 unprofitable restaurants and is targeting 15-25 closures in 2015, (ii) shutting down the Casey’s banner, and (iii) integrating the Prime Restaurants, Landing Group (and just recently the pending New York Fries) acquisitions. As such, we expect that SRS growth will accelerate off the 2015E base as management monetizes the initial investments made in improving the network’s health.

In addition, management believes there is room for considerable restaurant growth without oversaturating the market. Management is targeting growth both in new and in-fill in existing markets. The target growth of 30 to 50 net new restaurants over the next 5 to 7 years appears reasonable in the context of current restaurant density. While Ontario appears well-represented (also has the lowest population density at 22,846) with 72% of its footprint in the province, Québec and Western Canada are significantly under-represented at only 7% and 16% of restaurant locations, respectively. While we believe that the targeted restaurant openings are within the company’s abilities, growth in Western Canada may prove to be challenging in the near- to medium-term given the weaker macro backdrop.

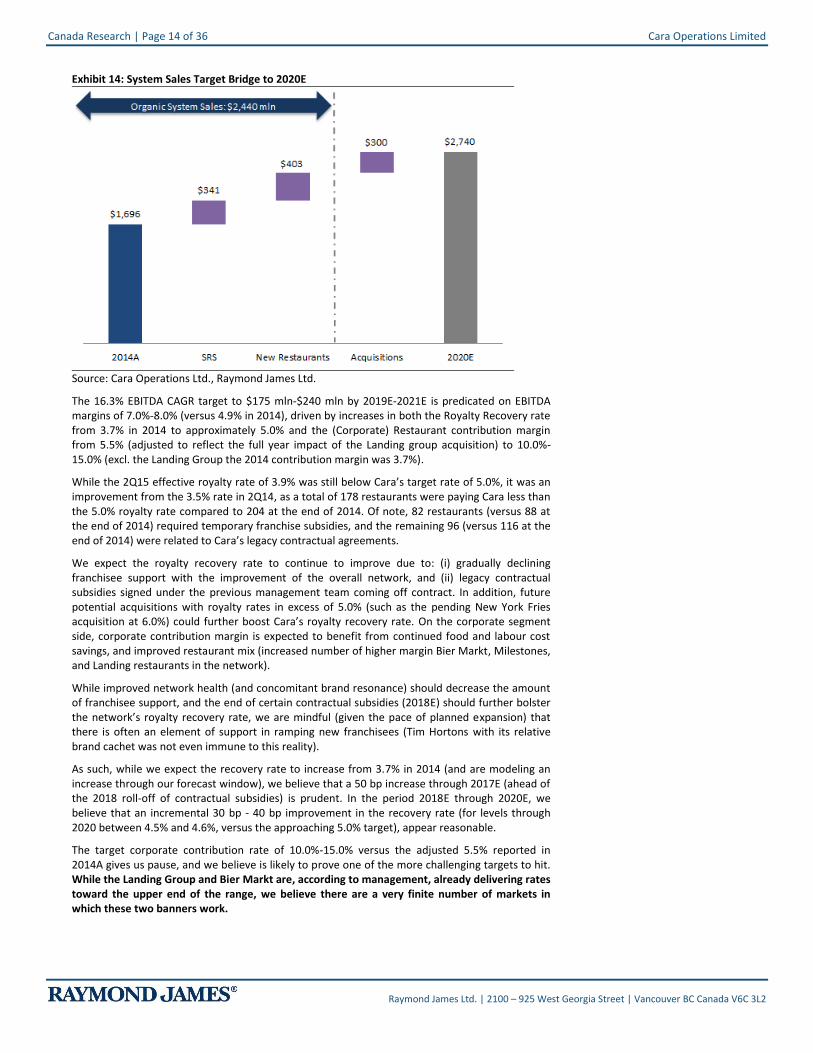

We believe SRS sales growth will conservatively add approximately $341.0 mln to system sales, with new locations adding $403.0 mln for (organic growth driven) 2020E system sales of $2,440 mln. The combination of these two targets alone could facilitate system sales close to the lower end of Cara’s target of $2,500 mln.

In addition, we expect acquisitions to add approximately $300.0 mln to system sales. Cara is we believe well positioned to continue to consolidate the highly fragmented Canadian restaurant industry, given its: (i) size (one of the leading restaurant operators in Canada with system sales in excess of $1,700 mln), (ii) track record of successful integration of previous acquisitions (Prime Restaurant and the Landing Group), and (iii) under-levered balance sheet (1.1x debt-to-EBITDA in 2015E). In addition to its strong balance sheet following the IPO, we expect Cara to generate significant free cash flow to (partially) fund potential future acquisitions based on the combination of (i) modest cash taxes (on the application of available tax losses for the next 2 years), and (ii) significantly lower interest expense. With annual CAPEX in the range of $25 mln-$30 mln, we forecast Cara will generate $87.8 mln of free cash flow in 2016E and $91.6 mln in 2017E.

On SRS sales of approximately $341.0 mln, new restaurant sales of approximately $403.0 mln, and acquisition sales of approximately $300.0 mln, we believe that system sales within the target range of $2.5 bln-$3.0 bln through 2020E appears very doable. Exhibit 14 depicts our estimated system sales target bridge from 2014 to 2020E.

Canada Research | Page 14 of 36 Cara Operations Limited

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Exhibit 14: System Sales Target Bridge to 2020E

Source: Cara Operations Ltd., Raymond James Ltd.

The 16.3% EBITDA CAGR target to $175 mln-$240 mln by 2019E-2021E is predicated on EBITDA margins of 7.0%-8.0% (versus 4.9% in 2014), driven by increases in both the Royalty Recovery rate from 3.7% in 2014 to approximately 5.0% and the (Corporate) Restaurant contribution margin from 5.5% (adjusted to reflect the full year impact of the Landing group acquisition) to 10.0%-15.0% (excl. the Landing Group the 2014 contribution margin was 3.7%).

While the 2Q15 effective royalty rate of 3.9% was still below Cara’s target rate of 5.0%, it was an improvement from the 3.5% rate in 2Q14, as a total of 178 restaurants were paying Cara less than the 5.0% royalty rate compared to 204 at the end of 2014. Of note, 82 restaurants (versus 88 at the end of 2014) required temporary franchise subsidies, and the remaining 96 (versus 116 at the end of 2014) were related to Cara’s legacy contractual agreements.

We expect the royalty recovery rate to continue to improve due to: (i) gradually declining franchisee support with the improvement of the overall network, and (ii) legacy contractual subsidies signed under the previous management team coming off contract. In addition, future potential acquisitions with royalty rates in excess of 5.0% (such as the pending New York Fries acquisition at 6.0%) could further boost Cara’s royalty recovery rate. On the corporate segment side, corporate contribution margin is expected to benefit from continued food and labour cost savings, and improved restaurant mix (increased number of higher margin Bier Markt, Milestones, and Landing restaurants in the network).

While improved network health (and concomitant brand resonance) should decrease the amount of franchisee support, and the end of certain contractual subsidies (2018E) should further bolster the network’s royalty recovery rate, we are mindful (given the pace of planned expansion) that there is often an element of support in ramping new franchisees (Tim Hortons with its relative brand cachet was not even immune to this reality).

As such, while we expect the recovery rate to increase from 3.7% in 2014 (and are modeling an increase through our forecast window), we believe that a 50 bp increase through 2017E (ahead of the 2018 roll-off of contractual subsidies) is prudent. In the period 2018E through 2020E, we believe that an incremental 30 bp - 40 bp improvement in the recovery rate (for levels through 2020 between 4.5% and 4.6%, versus the approaching 5.0% target), appear reasonable.

The target corporate contribution rate of 10.0%-15.0% versus the adjusted 5.5% reported in 2014A gives us pause, and we believe is likely to prove one of the more challenging targets to hit. While the Landing Group and Bier Markt are, according to management, already delivering rates toward the upper end of the range, we believe there are a very finite number of markets in which these two banners work.

Cara Operations Limited Canada Research | Page 15 of 36

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

In addition, squeezing the underperforming banners (given the Milestones and Kelsey’s heavy 2014 contribution rate excluding the Landing Group of 3.7%) is not without material risk, given both the competitive and brand positioning of these banners within the market. The adjusted 2014 contribution rate including the Landing Group was 5.5%. The reality is that while staffing and food costs are the two biggest cost containment levers, they are also the most sensitive. In the restaurant business (and particularly given the plethora of choices in the highly fragmented Canadian restaurant industry), any noticeable deterioration in either the food quality or service experience will relatively quickly impact traffic (and chatter). These things matter (hugely), and there is a higher cost (and sensitivity) to diluting the dining experience, versus the retail experience.

While we are mindful that if there is a team in the restaurant business that could pull off what we characterize as a fine line balancing act, this is the team. We believe that in order to hit the SRS target growth of 2.5%-4.0% contribution rates will be closer to the low end (10%) of the 10.0%-15.0% target range through 2020E.

The Landing Group and Bier Markt’s key competitors (who also dominate the segment in the key Western Canadian market) are the Fuller brothers-owned Earls, Joey and Saltlik chains (the Fuller family retains an interest in Cactus Club, with co-founder Richard Jaffray) and the Gaglardi family-owned Moxie’s chain (Milestones was previously owned by the Gaglardi family). Mr. Stan Fuller (CEO of Earls Restaurants) was on record stating that Ontario is a major thrust and that the problem is now finding premium locations with the right landlords. We lived in Vancouver for a number of years and are intimately familiar with Cactus Club (but have also spent more than our fair share of time and dollars at Joey’s and Earls).

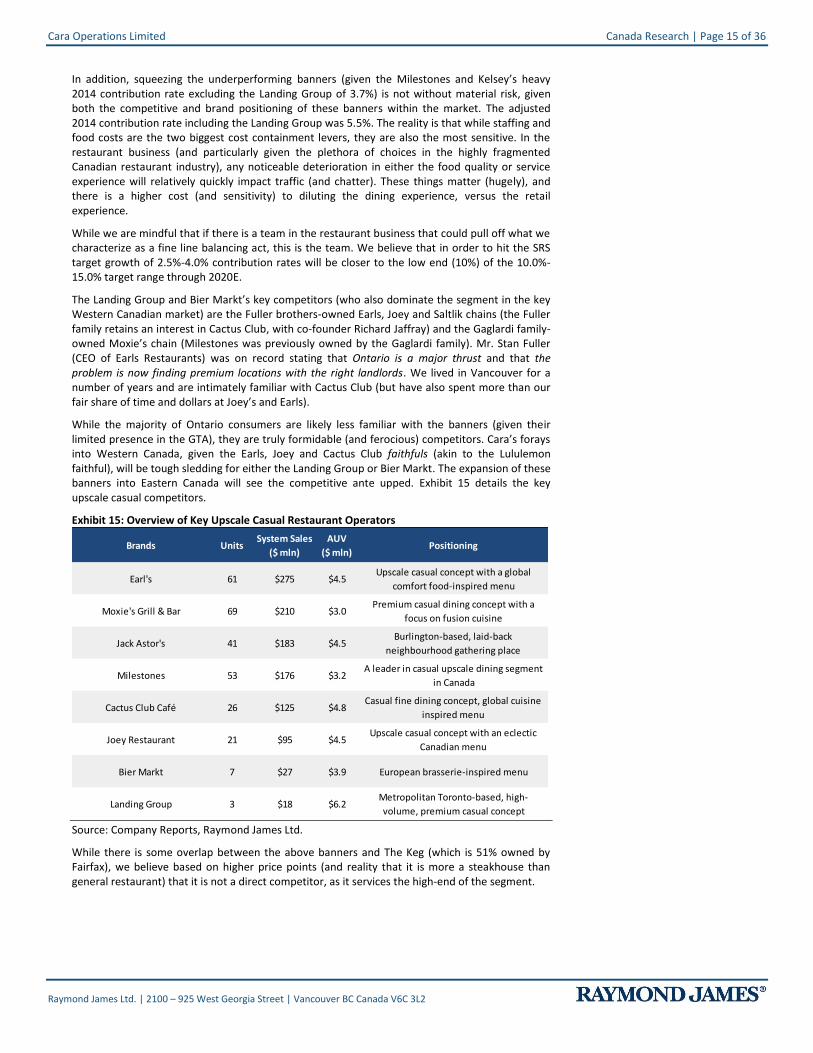

While the majority of Ontario consumers are likely less familiar with the banners (given their limited presence in the GTA), they are truly formidable (and ferocious) competitors. Cara’s forays into Western Canada, given the Earls, Joey and Cactus Club faithfuls (akin to the Lululemon faithful), will be tough sledding for either the Landing Group or Bier Markt. The expansion of these banners into Eastern Canada will see the competitive ante upped. Exhibit 15 details the key upscale casual competitors.

Exhibit 15: Overview of Key Upscale Casual Restaurant Operators

Brands UnitsSystem Sales

($ mln)

AUV

($ mln)Positioning

Earl's 61 $275 $4.5Upscale casual concept with a global

comfort food-inspired menu

Moxie's Grill & Bar 69 $210 $3.0Premium casual dining concept with a

focus on fusion cuisine

Jack Astor's 41 $183 $4.5Burlington-based, laid-back

neighbourhood gathering place

Milestones 53 $176 $3.2A leader in casual upscale dining segment

in Canada

Cactus Club Café 26 $125 $4.8Casual fine dining concept, global cuisine

inspired menu

Joey Restaurant 21 $95 $4.5Upscale casual concept with an eclectic

Canadian menu

Bier Markt 7 $27 $3.9 European brasserie-inspired menu

Landing Group 3 $18 $6.2Metropolitan Toronto-based, high-

volume, premium casual concept Source: Company Reports, Raymond James Ltd.

While there is some overlap between the above banners and The Keg (which is 51% owned by Fairfax), we believe based on higher price points (and reality that it is more a steakhouse than general restaurant) that it is not a direct competitor, as it services the high-end of the segment.

Canada Research | Page 16 of 36 Cara Operations Limited

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Acquisition Tally, Talk and Targets

With the successful acquisition (and integration) of both Prime Pubs and the Landing Group (and the New York Fries acquisition pending) highlighting management’s integration capabilities, focus necessarily remains on the acquisition opportunity (we estimate that acquisitions will need to add at least $300 mln to system sales through 2020E to achieve targets of $2.5 bln to $3.0 bln). The Prime Pubs (which generated approximately $300 mln systems sales) acquisition for a total of $69.6 mln (net of $3.9 mln long-term debt retired), saw East Side Mario’s, Prime Pubs, and Bier Markt vended into Cara on October 31, 2013, and was followed by the Landing Group acquisition. On December 18, 2014, Cara acquired a 55% interest in the Landing Group (with an option to acquire the remaining 45% on an agreed upon formula through 2018) for $18.3 mln. While the purchase option on the 45% ran through 2018, Cara purchased the remaining 45% on June 26, 2015 on an effective 8.0x EBITDA multiple. On August 31, 2015, Cara announced the acquisition of New York Fries (NYF). NYF has 120 (of which 16 are corporate) locations in Canada and 36 in international markets and generated system sales of approximately $75.0 mln in the last twelve months.

The combination of Cara’s strong balance sheet and the imperative that is a more balanced network (expansion we believe will be concentrated in Western Canada and Québec markets) makes relatively large scale acquisitions a priority. We are hard pressed to believe that any of the upscale casual crown jewels (Earls, Joey, Cactus Club) of Western Canada (or even Moxie’s) would be up for sale (much less on multiples that would be accretive). With growth in Western Canada more likely to be organic, in our view, Québec is the focus market for acquisitions. In Québec, approximately 89% of Cara’s 54 restaurants are Harvey’s. The single Bier Markt restaurant in Québec opened on January 3, 2014 on the old Queue de Cheval site on the corner of René-Lévesque and Drummond.

While we believe that a bolt-on acquisition of the likes of St-Hubert, would bring immediate scale to Cara’s operations in Québec, a series of smaller tuck in acquisitions is equally probable. We believe that chains the likes of Jimmy the Greek (50 restaurants) and Nando’s (29 restaurants) would make for interesting tuck-in acquisitions.

St-Hubert (controlled by the Léger family) has more than 115 locations (94% of which are in Québec) and generated restaurant sales of approximately $405 mln in 2014 (a decrease from its estimated 2010 sales of $420 mln) and retail sales of $285 mln, for total revenues of an estimated $690 mln. While St-Hubert recently went through a challenging time with the resignation of its CEO, Mr. Robert Depatie, on May 13, 2015 after only 3 months on the job (Mr. Depatie resigned as CEO of Québecor on April 28, 2014), there are no indications to date that Mr. Léger would be interested in selling a majority stake.

Imvescor operates 4 banners: Bâton Rouge (operating in Québec, Ontario and Nova Scotia), Mikes and Scores (primarily in Québec), Pizza Delight (primarily in Atlantic Canada) and a solid retail product portfolio. Through its 234 locations (of which 56% are in Québec), Imvescor generated 2014 system sales of $376.0 mln, revenues of $47.2 mln (97% of restaurants are franchised), and operating EBITDA of $16.0 mln.

Exhibit 16: Imvescor Restaurant Group Targets

2014 2018E Target

Revenue $47.2 mln 14% - 18%

SRS Growth -2.7% 3.0% - 5.0%

Restaurant Count 234 10 net additions

Restaurant Freshness Factor 47% 80%

Operating EBITDA $16.0 mln $20.0 mln

Note: 2018 targets are Imvescor estimates

Source: Imvescor Group, Raymond James Ltd.

Despite a challenged top line over the last 5 years, Imvescor has managed to maintain a royalty recovery rate of 4.7% in 2014. Imvescor banners each generate a different royalty rate: Pizza Delight 6.0%, Mikes 5.0%-6.0%, Scores 3.0%-4.0%, and Bâton Rouge 5.0%. Imvescor’s LTM operating EBITDA through 2Q15 was $15.2 mln. While we do not believe that Cara is necessarily interested in acquiring a turnaround play, applying a 6.0x-8.0x multiple imputes a valuation of $91 mln-$122 mln. We believe it’s worth highlighting this low probability acquisition scenario as

Cara Operations Limited Canada Research | Page 17 of 36

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

it is one of a select few public operations whose banners or footprint would be a fit (the majority are privately held).

While SIR Royalty Income Fund (SRV.UN) owns a number of potentially interesting banners (including Jack Astor’s and Canyon Creek), its concentration in Ontario (and the limited fit of other banners in its network for Cara) likely limits its appeal as a potential acquisition target, in our view, despite its attractive 6.0% royalty rate.

Cara’s leverage of 0.7x times (2Q15) is conservative, and management has indicated that it is comfortable increasing it to 3.0x, which based on our 2016E EBITDA of S122.1 mln imputes approximately $300.0 mln in incremental debt capacity (net of an estimated total purchase consideration for NYF of $40.0 mln to $45.0 mln). While Cara paid 8.0x EBITDA for the Landing Group, we believe that 6.0x to 8.0x is the acquisition sweet spot, and that Cara would only pay up into the 8.0x to 10.0x range for crown jewels (if any were to actually be available for sale). As such, we estimate a $250 mln acquisition (assuming an 8.0x multiple) would generate approximately $31.3 mln in EBITDA, for 2016E post-acquisition EBITDA of $153.3 mln for Cara. On a pro-forma basis, 2016E leverage would be 2.4x. Exhibit 17 details the EBITDA and EBITDA percentage change impact of a $250 mln acquisition on our 2016E EBITDA estimate of $122.1 mln.

Exhibit 17: Acquisition EBITDA Analysis – EBITDA Contribution and EBITDA Percent Change

31.25 $150 mln $200 mln $250 mln $300 mln $400 mln $150 mln $200 mln $250 mln $300 mln $400 mln

6.0x $25 mln $33 mln $42 mln $50 mln $67 mln 6.0x 20% 27% 34% 41% 55%

7.0x $21 mln $29 mln $36 mln $43 mln $57 mln 7.0x 18% 23% 29% 35% 47%

8.0x $19 mln $25 mln $31 mln $38 mln $50 mln 8.0x 15% 20% 26% 31% 41%

9.0x $17 mln $22 mln $28 mln $33 mln $44 mln 9.0x 14% 18% 23% 27% 36%

10.0x $15 mln $20 mln $25 mln $30 mln $40 mln 10.0x 12% 16% 20% 25% 33%Acq

uis

itio

n M

ult

iple

Source: Raymond James Ltd.

The bolt-on acquisition wildcard supports our providing a sensitivity analysis, on both our current actual EBITDA and pro-forma (post acquisition) EBITDA through 2016E, highlighting the potential EV/EBITDA based valuation scenarios (on a $250 mln acquisition at 8.0x EBITDA). Exhibit 18 details the scenarios based on our current and pro-forma (post acquisition) 2016E estimates.

Exhibit 18: Acquisition Scenario Analysis

##### 15.0x 15.5x 16.0x 16.5x 17.0x ##### 15.0x 15.5x 16.0x 16.5x 17.0x

$112.1 $32.73 $33.84 $34.95 $36.06 $37.16 $143.3 $37.01 $38.43 $39.85 $41.27 $42.69

$117.1 $34.21 $35.37 $36.53 $37.69 $38.85 $148.3 $38.50 $39.97 $41.43 $42.90 $44.37

$122.1 $35.70 $36.91 $38.12 $39.33 $40.53 $153.3 $39.98 $41.50 $43.02 $44.54 $46.05

$127.1 $37.19 $38.45 $39.70 $40.96 $42.22 $158.3 $41.47 $43.03 $44.60 $46.17 $47.74

$132.1 $38.67 $39.98 $41.29 $42.60 $43.90 $163.3 $42.95 $44.57 $46.19 $47.80 $49.42

EBIT

DA

($'

mln

)

Source: Raymond James Ltd.

Multi-Brand Strategy’s Multiple Benefits

Cara’s scale provides it with both cost and strategic advantages. Banner-specific teams focus on the best of single brand strategy with dedicated operations, marketing and menu leads, who then lever the scale and share services infrastructure of a multi-brand network. In addition, Cara as a function of its scale and brands has also been able to establish strategic partnerships (most notably with Cineplex’s SCENE 6.8 million plus member loyalty program).

The cost advantages include sourcing (securing favourable prices for franchisees and earn volume rebates from suppliers), negotiation of better lease rates (and lending terms), optimization of marketing spend (direct dollars to media channels that resonate) and highly scalable centralized IT support infrastructure. In terms of media spend, the increase in the share of the Swiss Chalet ad fund being spent on television is hard to miss, given that it almost impossible today to watch TV for an hour during prime time without a least one Swiss Chalet ad (we fully expect that competitor response to the media barrage will be swift).

The partnership with SCENE (one of the fastest growing loyalty programs in Canada) provides Cara with a differentiated loyalty offering (coalition versus monoline), and Cineplex with a valuable

Canada Research | Page 18 of 36 Cara Operations Limited

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

new coalition member (supporting the perceived value of the SCENE currency, which supports member engagement in the program) as roughly 60% of Cara restaurants are within 5 km of a Cineplex theatre.

Financial Analysis & Outlook

2Q15 Results Summary

Cara’s 2Q15 system sales increased 4.6% from $417.8 mln to $437.0 mln, while revenue increased a strong 16.6% from $69.4 mln to $80.9 mln. Cara’s top-line growth was driven by SRS increase of 3.2% (on an easy 0.3% comp), and a greater number of corporate restaurants from the addition of the Landing Group (which more than offset the TTM through 2Q15 net closure of 11 restaurants).

Cara’s revenue increased a strong 16.6% from $69.4 mln to $80.9 mln, reflecting SRS growth of 3.2% and a greater number of corporate restaurants from the addition of the Landing Group. Cara’s relatively strong SRS increase marked the 6

th consecutive quarterly SRS

increase, reflecting the continued momentum of its strategic initiatives.

Operating EBITDA margin performance was noteworthy, increasing a strong 124 bp to 6.5% (of total system sales). The strong operating EBITDA margin expansion reflects food and labour cost savings at its corporate restaurants and increased (higher volume and margin) corporate restaurants in Cara’s mix.

While Cara added 6 new restaurants during the quarter (22 new openings in the TTM period), it closed 16 restaurants (36 closed in the TTM period), bringing its total footprint to 827. While the net restaurant count decreased year-to-date, Cara remains committed to the opening of 14 net new restaurants in 2015E, with a targeted 30 to 40 openings partially offset by the closure of 15 to 25 restaurants.

System Sales and Revenue

Cara’s system sales increased 4.6% from $417.8 mln to $437.0 mln, while total revenue increased a robust 16.6% from $69.4 mln to $80.9 mln, reflecting SRS growth of 3.2% and increased corporate restaurants from the addition of the Landing Group. While store count decreased during the TTM through 2Q15 period, Cara’s restaurant mix includes a greater number of higher volume corporate-owned restaurants such as Bier Markt and the Landing Group which, combined with SRS growth of 3.2%, drove the top-line growth.

Operating EBITDA

Cara’s operating EBITDA increased 29.2% from $22.0 mln to $28.4 mln, for an operating EBITDA margin (% of total system sales) of 6.5%. The strong 124 bp margin increase reflects the combination of food and labour cost savings at corporate restaurants, and increased higher margin corporate restaurants in the mix.

Corporate segment contribution was $8.1 mln in 2Q15, for a contribution margin of 13.3%, which was a significant improvement over the $2.8 mln contribution (5.7% contribution margin) in the year-ago period. The improvement in corporate segment profitability was primarily driven by food and labour cost savings, and improved restaurant mix (greater higher margin corporate-owned restaurants in Cara’s mix).

Franchise segment contribution was $14.7 mln, for a 3.9% contribution margin, versus $12.9 mln and 3.5%, respectively. The improvement in franchise contribution margin primarily reflects increased royalty income and a reduction in franchise subsidies. The effective net royalty rate stood at 3.9% at the end of 2Q15, an improvement from the 3.5% effective rate in the year-ago quarter, as a total of 178 restaurants (24% of franchise base) were paying Cara a royalty rate of less than 5.0%, versus 204 in 2014 (27% of franchise base).

EPS

Cara’s EPS was $0.31 (up from $0.23 in 2Q14), on net income of $15.9 mln and an effective tax rate of 6.6%.

Cara Operations Limited Canada Research | Page 19 of 36

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Model and Estimates

We expect system sales CAGR of 10.1% from $1,696.0 mln in 2014 to $2,263.1 mln in 2017E, revenue growth of 12.1% from $281.8 mln to $397.3 mln, and operating EBITDA growth of 16.3% from $83.5 mln to $131.3 mln (versus Cara’s targeted system sales and operating EBITDA CAGRs of 8.4% and 16.3%, respectively), as Cara continues to pursue its 5 to 7 year targets.

On system sales growth of 5.2% to $1,784.8 mln, our 2015E revenue is $322.8 mln (growth of 14.6%), for operating EBITDA of $103.6 mln. We expect system sales growth in 2016E to accelerate sharply to 18.9% (system sales of $2,122.8 mln), for revenue of $369.8 mln and operating EBITDA of $122.1 mln. In 2017E, we expect system sales growth of 6.6% for system sales of $2,263.1 mln, revenue of $397.3 mln, and operating EBITDA of $131.3 mln. We are initiating with 2015E EPS of $1.12, 2016E EPS of $1.44, and 2017E EPS of $1.52.

The combination of the tailwinds from the initial investments made in improving the network’s overall health, and focus on improved restaurant mix (higher-margin corporate restaurants, such as Bier Markt, Milestones, and Landing), is expected to facilitate solid performance through our forecast window. While Cara’s results have significantly improved in 2014, the company has yet to realize the full benefits of its operational turnaround, as a number of initiatives are still in early stage.

While sales in Western Canada experienced some softness given the challenging macro backdrop, Cara’s network in the East continues to see solid sales momentum. Importantly, recall that Cara has the greatest exposure to Ontario’s economy, where GDP growth in 2015 is expected to outpace the national average for the first time since 2002 (driven by strong exports and consumer spending). Our earnings forecasts are based on the following assumptions:

2015 Estimates

System Sales: System sales of $1,784.8 mln reflect corporate segment system sales of $226.4 mln and franchise segment system sales of $1,558.1 mln. Total revenue of $322.8 mln reflects a 14.6% increase from the prior year, driven by SRS growth of 2.6% and the addition of 134 new restaurants (includes the pending New York Fries acquisition).

Operating EBITDA: Operating EBITDA margin improvement from 4.9% of system sales to 5.8% (operating EBITDA of $103.6 mln), reflecting our expectations of continued food and labour cost savings at corporate restaurants.

Corporate Segment: Corporate segment contribution margin of 9.2%, versus the long-term targeted contribution margin of 10.0%-15.0%. Cara expects to improve corporate restaurant profitability through lower operating costs, such as sourcing, marketing, and labour.

Franchise Segment: Franchise segment contribution margin of 3.9%, an improvement from the 3.7% contribution margin in 2014. The contribution margin should increase gradually as the effective royalty rate (currently at 3.7%) will increase closer to the standard 5.0% rate as temporary and historical contractual franchisee subsidy support is decreased as overall network health improves.

EPS: EPS of $1.12, which is predicated on our expectations of net income of $52.4 mln and an effective tax rate of 12.9%.

2016 Estimates

System Sales: System sales growth of 18.9% from $1,784.8 mln to $2,122.8 mln, on corporate segment system sales of $258.2 mln and franchise segment system sales of $1,864.3 mln. Total revenue of $369.8 mln reflects a 14.6% increase from 2015E, reflecting our expectations of SRS growth of 2.4% and the addition of 36 new restaurants (which is toward the low end but within Cara’s targeted annual restaurant additions of 30 to 50).

Operating EBITDA: Essentially flat operating EBITDA margin of 5.8% of system sales. Our operating EBITDA estimate of $122.1 mln is toward the low end of Cara’s targeted range of $175 mln-$240 mln over the next 5 to 7 years.

Corporate Segment: Corporate segment contribution margin of 9.4%, for corporate segment contribution of $24.3 mln, reflecting the continued improvement of corporate restaurant profitability on cost savings.

Canada Research | Page 20 of 36 Cara Operations Limited

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Franchise Segment: Franchise segment contribution margin improvement of 15 bp, from 3.9% in 2015E to 4.1% in 2016E. The contribution margin should continue to increase gradually with the increase of the effective royalty rate closer to the standard 5.0%, as temporary and historical contractual franchisee subsidy support is decreased as overall network health improves.

EPS: EPS growth of 28.8% to $1.44, which is predicated on our $72.6 mln net income expectation and effective tax rate of 19.0%.

2017 Estimates

System Sales: System sales of $2,263.1 mln reflect corporate segment system sales of $274.0 mln and franchise segment system sales of $1,988.9 mln. Total revenue of $397.3 mln reflects a 7.4% increase from the prior year, driven by SRS growth of 3.1% and the addition of 32 new restaurants (at the lower end of Cara’s targeted 30 to 50 net new restaurant openings).

Operating EBITDA: Essentially flat operating EBITDA margin of 5.8% (operating EBITDA of $131.3 mln), reflecting our expectations of continued food and labour cost savings at corporate restaurants.

Corporate Segment: Corporate segment contribution margin of 9.8%, which remains on track to achieving the long-term targeted range of 10.0% -15.0%. Corporate restaurant profitability is expected to continue to improve driven by lower operating costs, namely sourcing, marketing, and labour.

Franchise Segment: Franchise segment contribution margin of 4.3%, an improvement from the 4.1% contribution margin in 2016E. The contribution margin is expected to continue to increase gradually as the effective royalty rate increases closer to the standard 5.0% rate as temporary and historical contractual franchisee subsidy support is decreased as overall network health improves.

EPS: EPS of $1.52, which is predicated on our expectations of net income of $76.8 mln and an effective tax rate of 21.0%.

Cara Operations Limited Canada Research | Page 21 of 36

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

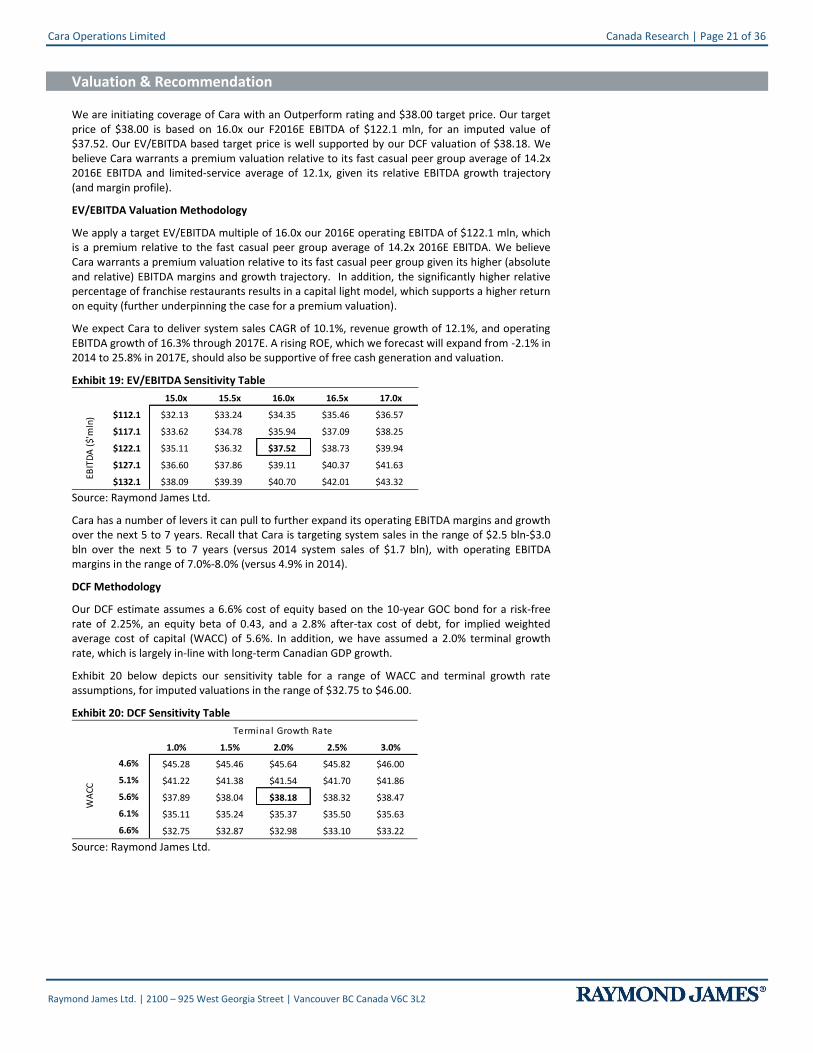

Valuation & Recommendation

We are initiating coverage of Cara with an Outperform rating and $38.00 target price. Our target price of $38.00 is based on 16.0x our F2016E EBITDA of $122.1 mln, for an imputed value of $37.52. Our EV/EBITDA based target price is well supported by our DCF valuation of $38.18. We believe Cara warrants a premium valuation relative to its fast casual peer group average of 14.2x 2016E EBITDA and limited-service average of 12.1x, given its relative EBITDA growth trajectory (and margin profile).

EV/EBITDA Valuation Methodology

We apply a target EV/EBITDA multiple of 16.0x our 2016E operating EBITDA of $122.1 mln, which is a premium relative to the fast casual peer group average of 14.2x 2016E EBITDA. We believe Cara warrants a premium valuation relative to its fast casual peer group given its higher (absolute and relative) EBITDA margins and growth trajectory. In addition, the significantly higher relative percentage of franchise restaurants results in a capital light model, which supports a higher return on equity (further underpinning the case for a premium valuation).

We expect Cara to deliver system sales CAGR of 10.1%, revenue growth of 12.1%, and operating EBITDA growth of 16.3% through 2017E. A rising ROE, which we forecast will expand from -2.1% in 2014 to 25.8% in 2017E, should also be supportive of free cash generation and valuation.

Exhibit 19: EV/EBITDA Sensitivity Table

37.52$ 15.0x 15.5x 16.0x 16.5x 17.0x

$112.1 $32.13 $33.24 $34.35 $35.46 $36.57

$117.1 $33.62 $34.78 $35.94 $37.09 $38.25

$122.1 $35.11 $36.32 $37.52 $38.73 $39.94

$127.1 $36.60 $37.86 $39.11 $40.37 $41.63

$132.1 $38.09 $39.39 $40.70 $42.01 $43.32

EBIT

DA

($'

mln

)

Source: Raymond James Ltd.

Cara has a number of levers it can pull to further expand its operating EBITDA margins and growth over the next 5 to 7 years. Recall that Cara is targeting system sales in the range of $2.5 bln-$3.0 bln over the next 5 to 7 years (versus 2014 system sales of $1.7 bln), with operating EBITDA margins in the range of 7.0%-8.0% (versus 4.9% in 2014).

DCF Methodology

Our DCF estimate assumes a 6.6% cost of equity based on the 10-year GOC bond for a risk-free rate of 2.25%, an equity beta of 0.43, and a 2.8% after-tax cost of debt, for implied weighted average cost of capital (WACC) of 5.6%. In addition, we have assumed a 2.0% terminal growth rate, which is largely in-line with long-term Canadian GDP growth.

Exhibit 20 below depicts our sensitivity table for a range of WACC and terminal growth rate assumptions, for imputed valuations in the range of $32.75 to $46.00.

Exhibit 20: DCF Sensitivity Table

3,818% 1.0% 1.5% 2.0% 2.5% 3.0%

4.6% $45.28 $45.46 $45.64 $45.82 $46.00

5.1% $41.22 $41.38 $41.54 $41.70 $41.86

5.6% $37.89 $38.04 $38.18 $38.32 $38.47

6.1% $35.11 $35.24 $35.37 $35.50 $35.63

6.6% $32.75 $32.87 $32.98 $33.10 $33.22

Terminal Growth Rate

WA

CC

Source: Raymond James Ltd.

Canada Research | Page 22 of 36 Cara Operations Limited

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Exhibit 21: Peer Group Comparison Shrs Market 1000 1001 1002 1003

Price O/S Cap.

Company Name 9/25/2015 (mln) (mln) LFY FY1E FY2E FY3E LFY FY1E FY2E FY3E LFY FY1E FY2E FY3E LFY FY1E FY2E FY3E

Cara Operations Limited $33.00 50.5 $1,667 $0.29 $1.12 $1.44 $1.52 112.2 29.6 23.0 21.7 $84 $104 $122 $131 20.7 16.7 14.2 13.2

Fast Casual LAST 1000 1001 1002 1003

Chipotle Mexican Grill , Inc. $730.28 31.5 $23,029 14.13 17.36 20.67 24.50 51.7 42.1 35.3 29.8 $828 $1,022 $1,200 $1,376 26.7 21.7 18.5 16.1

Panera Bread Company $190.71 26.6 $5,070 6.64 6.19 6.71 8.31 28.7 30.8 28.4 23.0 $401 $396 $414 $470 12.6 12.7 12.2 10.7

Domino's Pizza, Inc. $112.95 56.7 $6,406 2.86 3.51 4.04 4.70 39.5 32.2 28.0 24.0 $378 $438 $479 $528 20.9 18.1 16.5 15.0

Red Robin Gourmet Burgers Inc. $77.51 14.3 $1,110 2.25 3.23 3.74 4.50 34.4 24.0 20.7 17.2 $121 $146 $163 $178 10.2 8.5 7.6 6.9

Dunkin' Brands Group, Inc. $49.53 102.5 $5,077 1.65 1.92 2.24 2.55 30.0 25.8 22.1 19.4 $364 $416 $448 $493 19.9 17.4 16.2 14.7

Group Average 36.9 31.0 26.9 22.7 18.1 15.7 14.2 12.7

Full-Service LAST 1000 1001 1002 1003