Camel

33

INDIAN INSTITUTE OF PLANNING AND MANAGEMENT NEW DELHI “FINANCIAL PERFORMANCE OF PUBLIC SECTOR BANKS VERSUS PRIVATE SECTOR BANKS” SUBMITTED TO: SUBMITTED BY: 1

Transcript of Camel

INDIAN INSTITUTE OF PLANNING AND MANAGEMENT NEW DELHI

“FINANCIAL PERFORMANCE OF PUBLIC SECTOR BANKS VERSUS PRIVATE SECTOR BANKS”

SUBMITTED TO:

SUBMITTED BY:

1

ABSTRACT

The banking sector has been undergoing a complex, but comprehensive phase of

restructuring since 1991, with a view to make it sound, efficient, and at the same time

forging its links firmly with the real sector for promotion of savings, investment and

growth. Although a complete turnaround in banking sector performance is not

expected till the completion of reforms, signs of improvement are visible in some

indicators under the CAMEL framework. Under this bank is required to enhance

capital adequacy, strengthen asset quality, improve management, increase earnings

and reduce sensitivity to various financial risks. The almost simultaneous nature of

these developments makes it difficult to disentangle the positive impact of reform

measures. Keeping this in mind, signs of improvements and deteriorations are

discussed for the three groups of scheduled banks in the following sections.

CAMELS Framework

Supervisory framework, consistent with international norms, covers risk-monitoring

factors for evaluating the performance of banks. This framework involves the

analyses of six groups of indicators reflecting the health of financial institutions. The

indicators are as follows:

CAPITAL ADEQUACY

ASSET QUALITY

MANAGEMENT SOUNDNESS

EARNINGS & PROFITABILITY

LIQUIDITY

SENSITIVITY TO MARKET RISK

The whole banking scenario has changed in the very recent past on the

recommendations of Narasimham Committee. Further BASELL II Norms were

introduced to internationally standardize processes and make the banking industry

more adaptive to the sensitive market risks. The fact that banks work under the most

volatile conditions and the banking industry as such in the booming phase makes it an

interesting subject of study. Amongst these reforms and restructuring the CAMELS

2

Framework has its own contribution to the way modern banking is looked up on now.

The attempt here is to see how various ratios have been used and interpreted to reveal

a banks performance and how this particular model encompasses a wide range of

parameters making it a widely used and accepted model in today’s scenario.

Performance Analysis of Nationalized Banks in India an Application of Camel

Model using different parameters:

(A)CAPITAL ADEQUACY:

Capital adequacy ratio is defined as

where Risk can either be weighted assets ( ) or the respective national regulator's

minimum total capital requirement. If using risk weighted assets,

≥ 8%.

The percent threshold (8% in this case, a common requirement for regulators

conforming to the Basel Accords) is set by the national banking regulator.

Two types of capital are measured: tier one capital, which can absorb losses without a

bank being required to cease trading, and tier two capital, which can absorb losses in

the event of a winding-up and so provides a lesser degree of protection to depositors.

CAMEL RATING

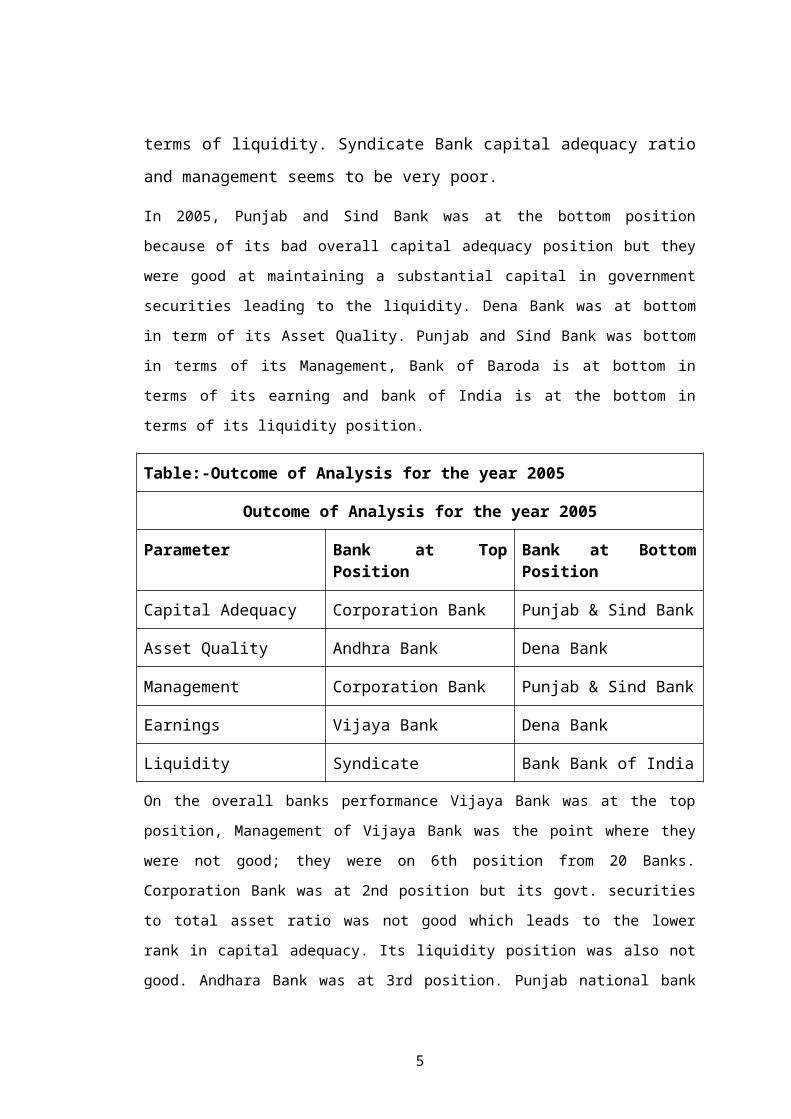

Financial year 2005 (From Annexure I A & B 2005)

In the financial year ending March 2005, based on the total score obtain from five

parameters (CAMEL), Vijaya Bank was at the top position in terms of Capital

Adequacy, but its Total Advance to Total asset ratio is not good. Andhara Bank was

at the top in terms of Asset quality, Corporation Bank was at the top on the basis of

Management. Vijaya Bank was at the top in terms of Earnings but Vijaya Bank’s

noninterest income to total asset was very low and syndicate bank was at the top in

3

terms of liquidity. Syndicate Bank capital adequacy ratio and management seems to

be very poor.

In 2005, Punjab and Sind Bank was at the bottom position because of its bad overall capital

adequacy position but they were good at maintaining a substantial capital in government

securities leading to the liquidity. Dena Bank was at bottom in term of its Asset Quality.

Punjab and Sind Bank was bottom in terms of its Management, Bank of Baroda is at bottom

in terms of its earning and bank of India is at the bottom in terms of its liquidity position.

Table:-Outcome of Analysis for the year 2005

Outcome of Analysis for the year 2005

Parameter Bank at Top Position Bank at Bottom Position

Capital Adequacy Corporation Bank Punjab & Sind Bank

Asset Quality Andhra Bank Dena Bank

Management Corporation Bank Punjab & Sind Bank

Earnings Vijaya Bank Dena Bank

Liquidity Syndicate Bank Bank of India

On the overall banks performance Vijaya Bank was at the top position, Management of

Vijaya Bank was the point where they were not good; they were on 6th position from 20

Banks. Corporation Bank was at 2nd position but its govt. securities to total asset ratio was

not good which leads to the lower rank in capital adequacy. Its liquidity position was also not

good. Andhara Bank was at 3rd position. Punjab national bank was at 4th position but they

were lacking in maintaining the liquidity quality ratios, and Indian bank was at 5th position.

Table: Overall Performance of the Banks in the Year 2005

Overall Performance of the Banks in the Year 2005

Vijaya Bank 1 Punjab & Sind Bank 16

Corporation Bank 2 Bank of India 17

Andhra Bank 3 Bank of Baroda 18

4

Punjab National Bank 4 Dena Bank 19

Indian Bank 5 Central Bank of India 20

In 2005, Central Bank of India was at bottom most position following the Dena bank,

Bank of Baroda, Bank of India, Punjab and Sind Bank respectively. Bank of India

was still good at maintaining the Management ratios. Punjab and Sind bank too had

good earnings and liquidity rankings but were lacking in other elements.

SBI being the largest public sector bank & SBI had very good in Capital Adequacy,

Earnings and Liquidity rankings but its Asset quality was bad in terms of NPA and its

Management ranking was also not good in year 2005.

Financial year 2006 (From Annexure II A & B 2006)

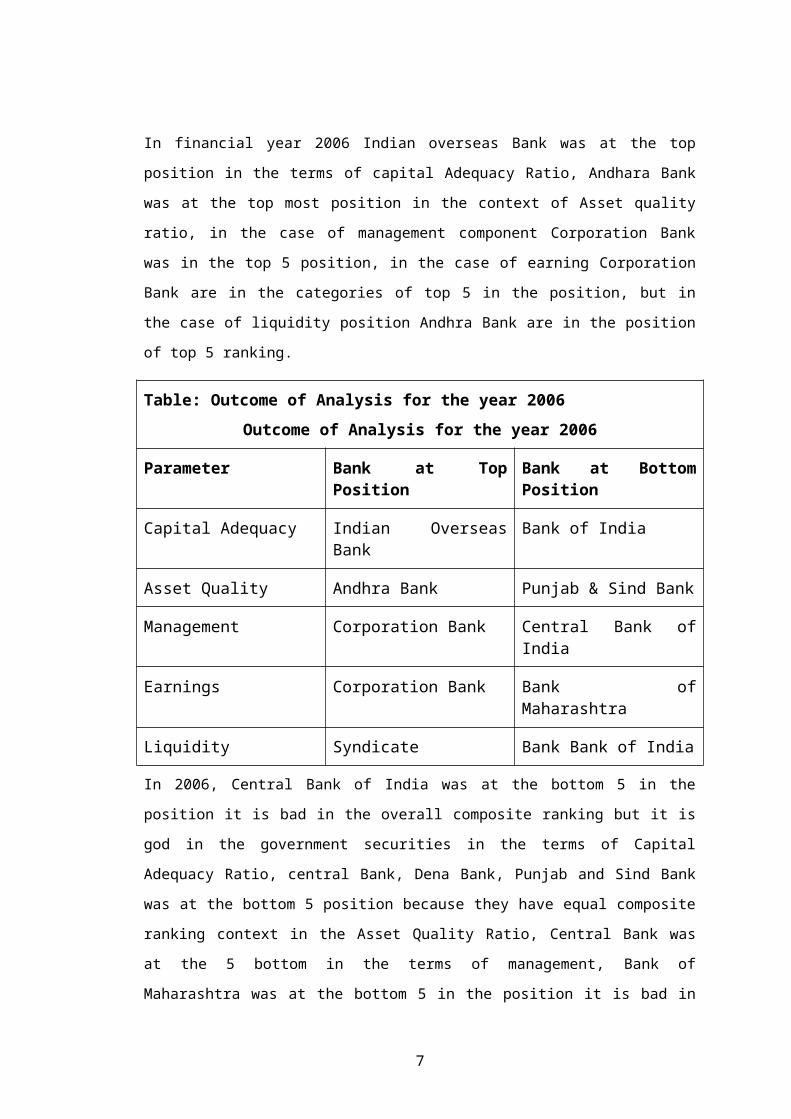

In financial year 2006 Indian overseas Bank was at the top position in the terms of capital

Adequacy Ratio, Andhara Bank was at the top most position in the context of Asset quality

ratio, in the case of management component Corporation Bank was in the top 5 position, in

the case of earning Corporation Bank are in the categories of top 5 in the position, but in the

case of liquidity position Andhra Bank are in the position of top 5 ranking.

Table: Outcome of Analysis for the year 2006

Outcome of Analysis for the year 2006

Parameter Bank at Top Position Bank at Bottom Position

Capital Adequacy Indian Overseas Bank Bank of India

Asset Quality Andhra Bank Punjab & Sind Bank

Management Corporation Bank Central Bank of India

Earnings Corporation Bank Bank of Maharashtra

Liquidity Syndicate Bank Bank of India

In 2006, Central Bank of India was at the bottom 5 in the position it is bad in the overall

composite ranking but it is god in the government securities in the terms of Capital

Adequacy Ratio, central Bank, Dena Bank, Punjab and Sind Bank was at the bottom 5

position because they have equal composite ranking context in the Asset Quality Ratio,

Central Bank was at the 5 bottom in the terms of management, Bank of Maharashtra was at

5

the bottom 5 in the position it is bad in the composite ranking but god in dividend payout

ratio and interest income to total income in the terms of earning, central Bank was at the

bottom 5 in position in the terms of liquidity.

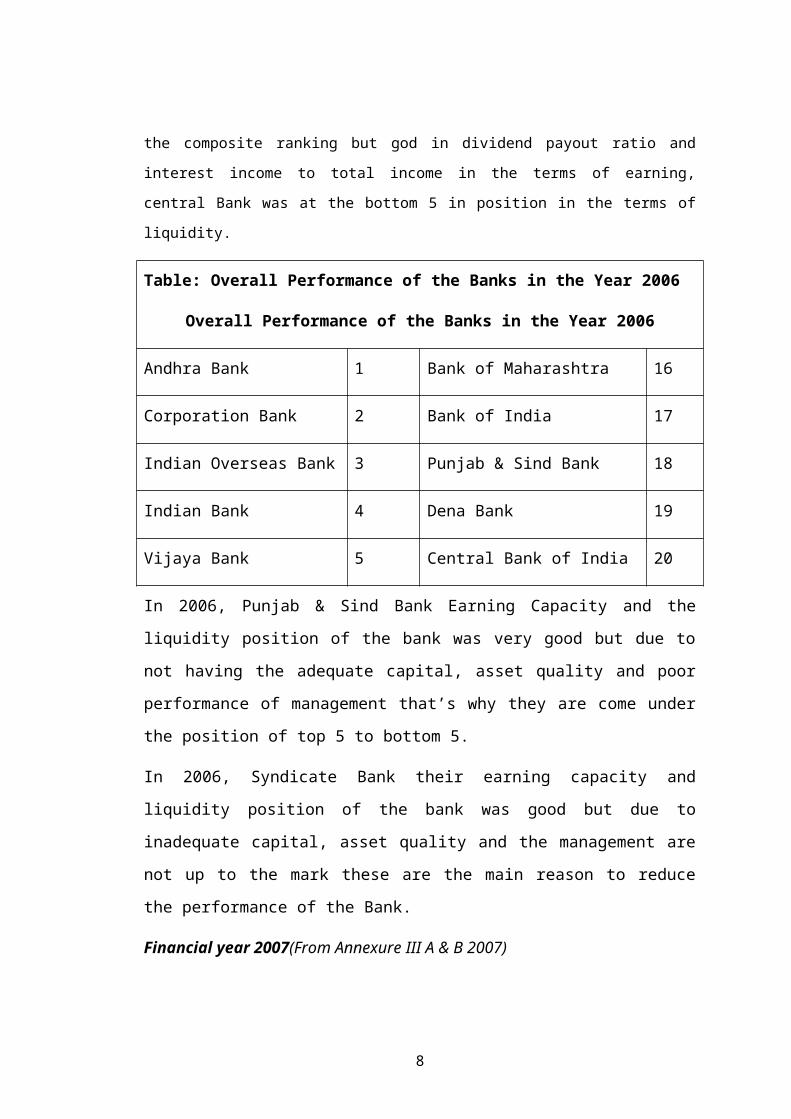

Table: Overall Performance of the Banks in the Year 2006

Overall Performance of the Banks in the Year 2006

Andhra Bank 1 Bank of Maharashtra 16

Corporation Bank 2 Bank of India 17

Indian Overseas Bank 3 Punjab & Sind Bank 18

Indian Bank 4 Dena Bank 19

Vijaya Bank 5 Central Bank of India 20

In 2006, Punjab & Sind Bank Earning Capacity and the liquidity position of the bank

was very good but due to not having the adequate capital, asset quality and poor

performance of management that’s why they are come under the position of top 5 to

bottom 5.

In 2006, Syndicate Bank their earning capacity and liquidity position of the bank was

good but due to inadequate capital, asset quality and the management are not up to the

mark these are the main reason to reduce the performance of the Bank.

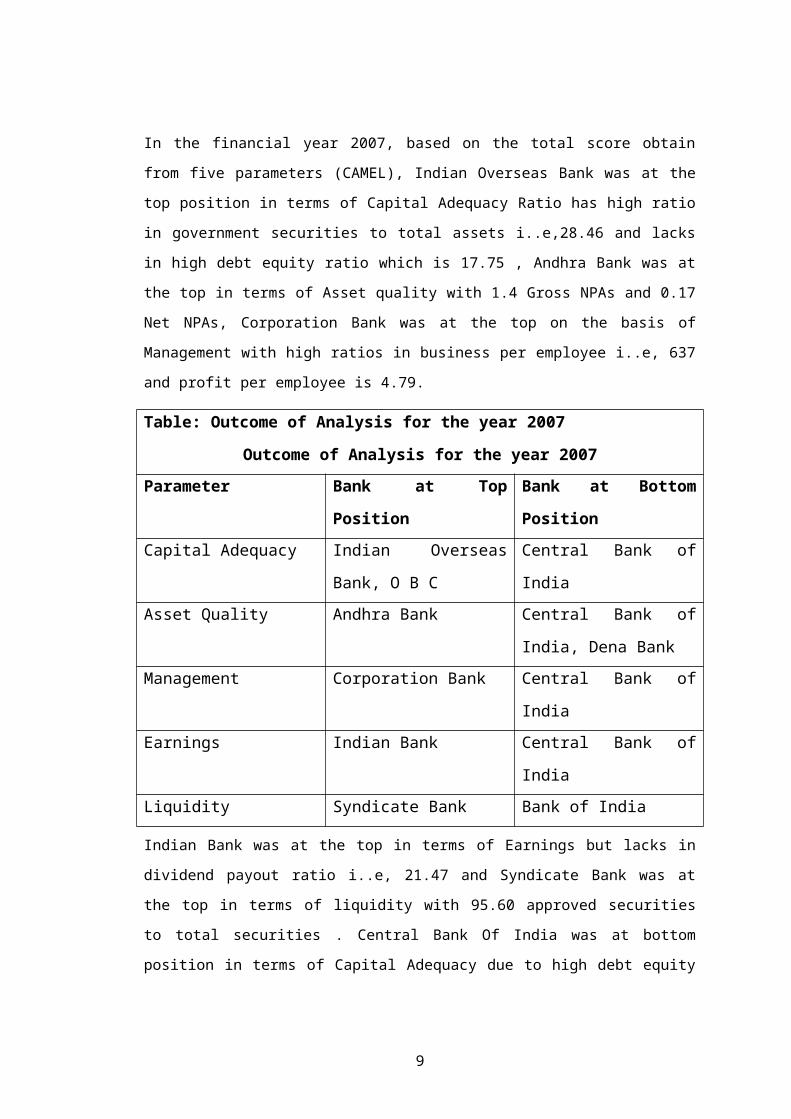

Financial year 2007(From Annexure III A & B 2007)

In the financial year 2007, based on the total score obtain from five parameters (CAMEL),

Indian Overseas Bank was at the top position in terms of Capital Adequacy Ratio has high

ratio in government securities to total assets i..e,28.46 and lacks in high debt equity ratio

which is 17.75 , Andhra Bank was at the top in terms of Asset quality with 1.4 Gross NPAs

and 0.17 Net NPAs, Corporation Bank was at the top on the basis of Management with high

ratios in business per employee i..e, 637 and profit per employee is 4.79.

Table: Outcome of Analysis for the year 2007

Outcome of Analysis for the year 2007

Parameter Bank at Top Position Bank at Bottom Position

6

Capital Adequacy Indian Overseas Bank, O

B C

Central Bank of India

Asset Quality Andhra Bank Central Bank of India,

Dena Bank

Management Corporation Bank Central Bank of India

Earnings Indian Bank Central Bank of India

Liquidity Syndicate Bank Bank of India

Indian Bank was at the top in terms of Earnings but lacks in dividend payout ratio i..e, 21.47

and Syndicate Bank was at the top in terms of liquidity with 95.60 approved securities to

total securities . Central Bank Of India was at bottom position in terms of Capital Adequacy

due to high debt equity ratio with 33.38, Asset Quality, Management, Earning Quality. Bank

of India was at bottom position in terms of Liquidity.

Table: Overall Performance of the Banks in the Year 2007

Overall Performance of the Banks in the Year 2007

Indian Overseas Bank 1 Bank of Baroda 16

Corporation Bank 2 United Bank of India 17

Andhra Bank 3 Bank of Maharashtra 18

O B C 3 Dena Bank 18

Canara Bank 5 Central Bank of India 20

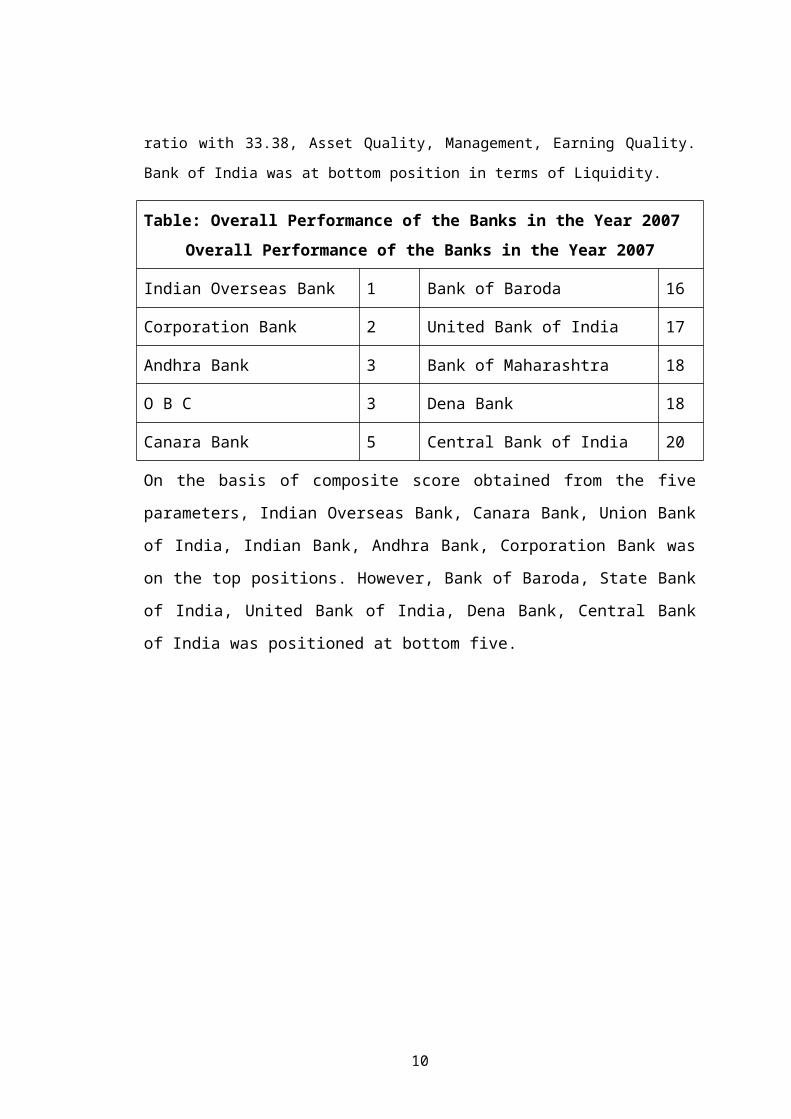

On the basis of composite score obtained from the five parameters, Indian Overseas

Bank, Canara Bank, Union Bank of India, Indian Bank, Andhra Bank, Corporation

Bank was on the top positions. However, Bank of Baroda, State Bank of India, United

Bank of India, Dena Bank, Central Bank of India was positioned at bottom five.

7

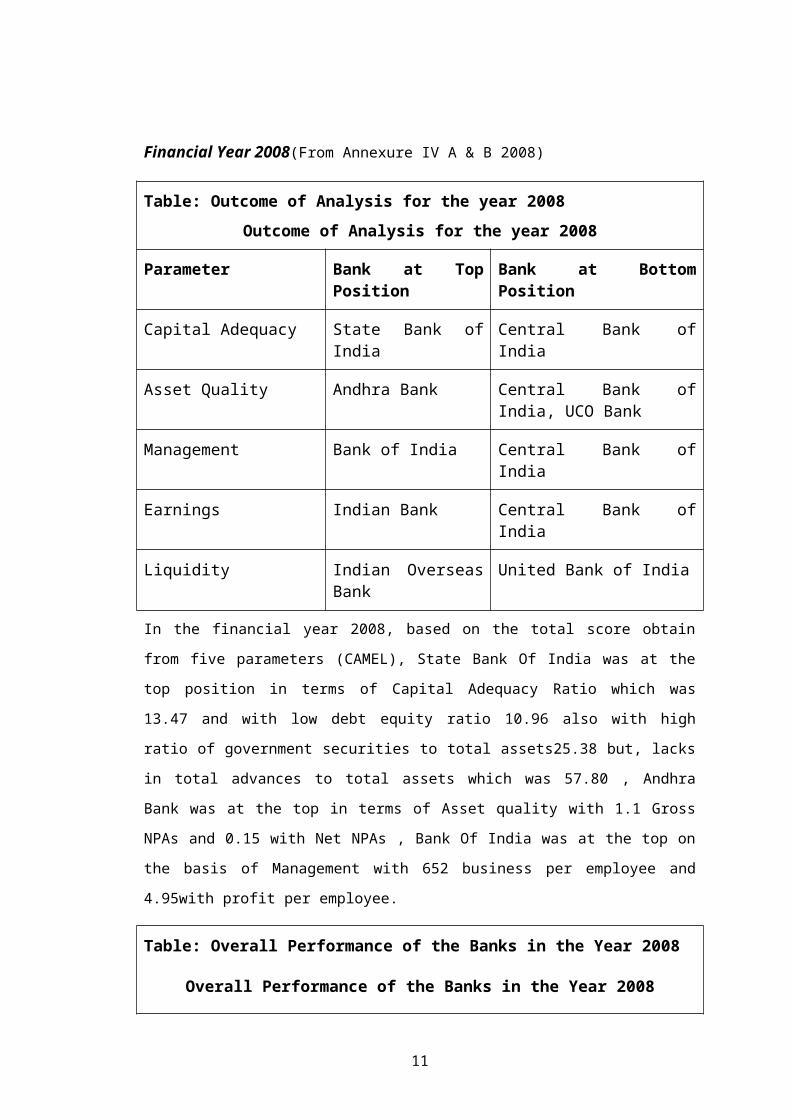

Financial Year 2008(From Annexure IV A & B 2008)

Table: Outcome of Analysis for the year 2008

Outcome of Analysis for the year 2008

Parameter Bank at Top Position Bank at Bottom Position

Capital Adequacy State Bank of India Central Bank of India

Asset Quality Andhra Bank Central Bank of India, UCO Bank

Management Bank of India Central Bank of India

Earnings Indian Bank Central Bank of India

Liquidity Indian Overseas Bank United Bank of India

In the financial year 2008, based on the total score obtain from five parameters (CAMEL),

State Bank Of India was at the top position in terms of Capital Adequacy Ratio which was

13.47 and with low debt equity ratio 10.96 also with high ratio of government securities to

total assets25.38 but, lacks in total advances to total assets which was 57.80 , Andhra Bank

was at the top in terms of Asset quality with 1.1 Gross NPAs and 0.15 with Net NPAs , Bank

Of India was at the top on the basis of Management with 652 business per employee and

4.95with profit per employee.

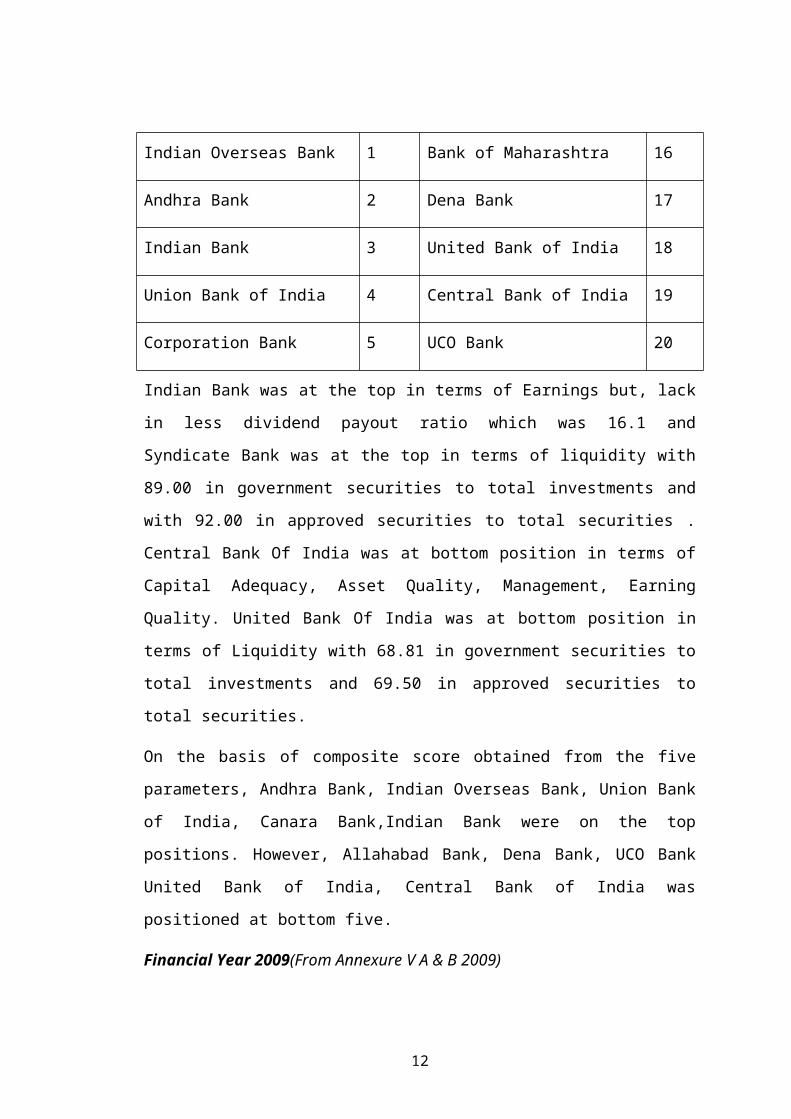

Table: Overall Performance of the Banks in the Year 2008

Overall Performance of the Banks in the Year 2008

Indian Overseas Bank 1 Bank of Maharashtra 16

Andhra Bank 2 Dena Bank 17

Indian Bank 3 United Bank of India 18

Union Bank of India 4 Central Bank of India 19

Corporation Bank 5 UCO Bank 20

8

Indian Bank was at the top in terms of Earnings but, lack in less dividend payout ratio

which was 16.1 and Syndicate Bank was at the top in terms of liquidity with 89.00 in

government securities to total investments and with 92.00 in approved securities to

total securities . Central Bank Of India was at bottom position in terms of Capital

Adequacy, Asset Quality, Management, Earning Quality. United Bank Of India was

at bottom position in terms of Liquidity with 68.81 in government securities to total

investments and 69.50 in approved securities to total securities.

On the basis of composite score obtained from the five parameters, Andhra Bank,

Indian Overseas Bank, Union Bank of India, Canara Bank,Indian Bank were on the

top positions. However, Allahabad Bank, Dena Bank, UCO Bank United Bank of

India, Central Bank of India was positioned at bottom five.

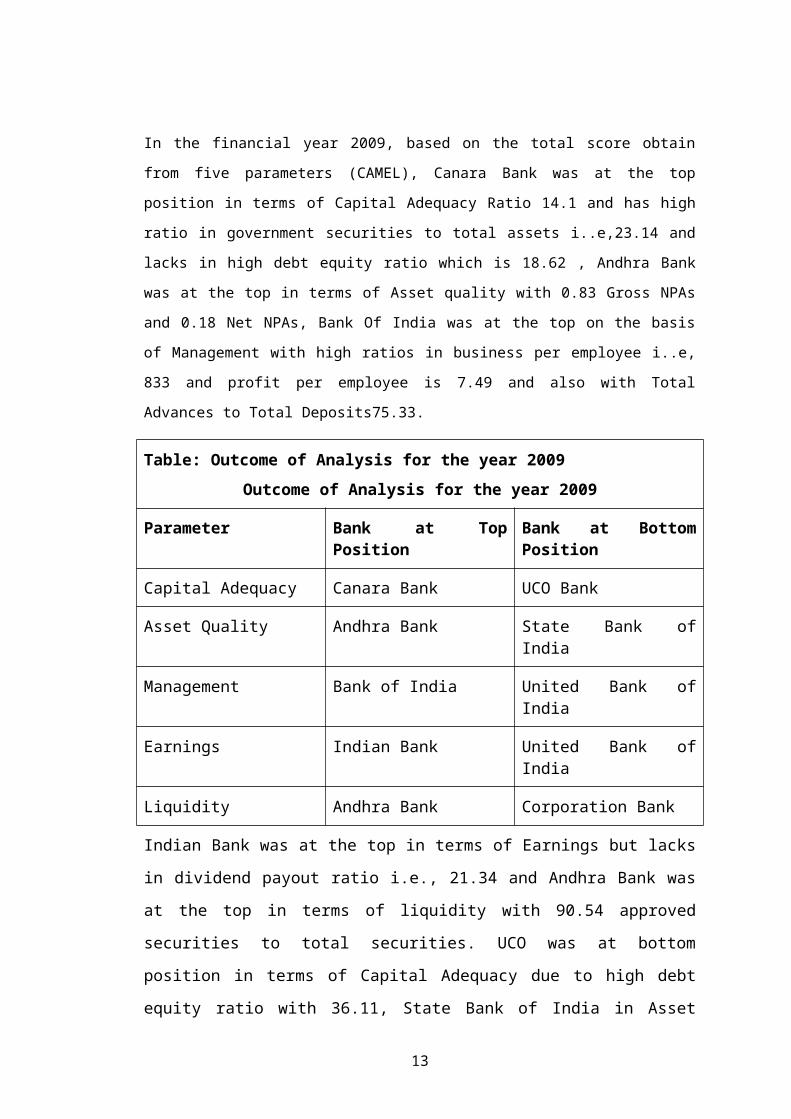

Financial Year 2009(From Annexure V A & B 2009)

In the financial year 2009, based on the total score obtain from five parameters (CAMEL),

Canara Bank was at the top position in terms of Capital Adequacy Ratio 14.1 and has high

ratio in government securities to total assets i..e,23.14 and lacks in high debt equity ratio

which is 18.62 , Andhra Bank was at the top in terms of Asset quality with 0.83 Gross NPAs

and 0.18 Net NPAs, Bank Of India was at the top on the basis of Management with high

ratios in business per employee i..e, 833 and profit per employee is 7.49 and also with Total

Advances to Total Deposits75.33.

Table: Outcome of Analysis for the year 2009

Outcome of Analysis for the year 2009

Parameter Bank at Top Position Bank at Bottom Position

Capital Adequacy Canara Bank UCO Bank

Asset Quality Andhra Bank State Bank of India

Management Bank of India United Bank of India

Earnings Indian Bank United Bank of India

Liquidity Andhra Bank Corporation Bank

Indian Bank was at the top in terms of Earnings but lacks in dividend payout ratio i.e.,

21.34 and Andhra Bank was at the top in terms of liquidity with 90.54 approved

9

securities to total securities. UCO was at bottom position in terms of Capital

Adequacy due to high debt equity ratio with 36.11, State Bank of India in Asset

Quality, United Bank of India in Management and Earning Quality Ratio. Corporation

Bank was at bottom position in terms of Liquidity.

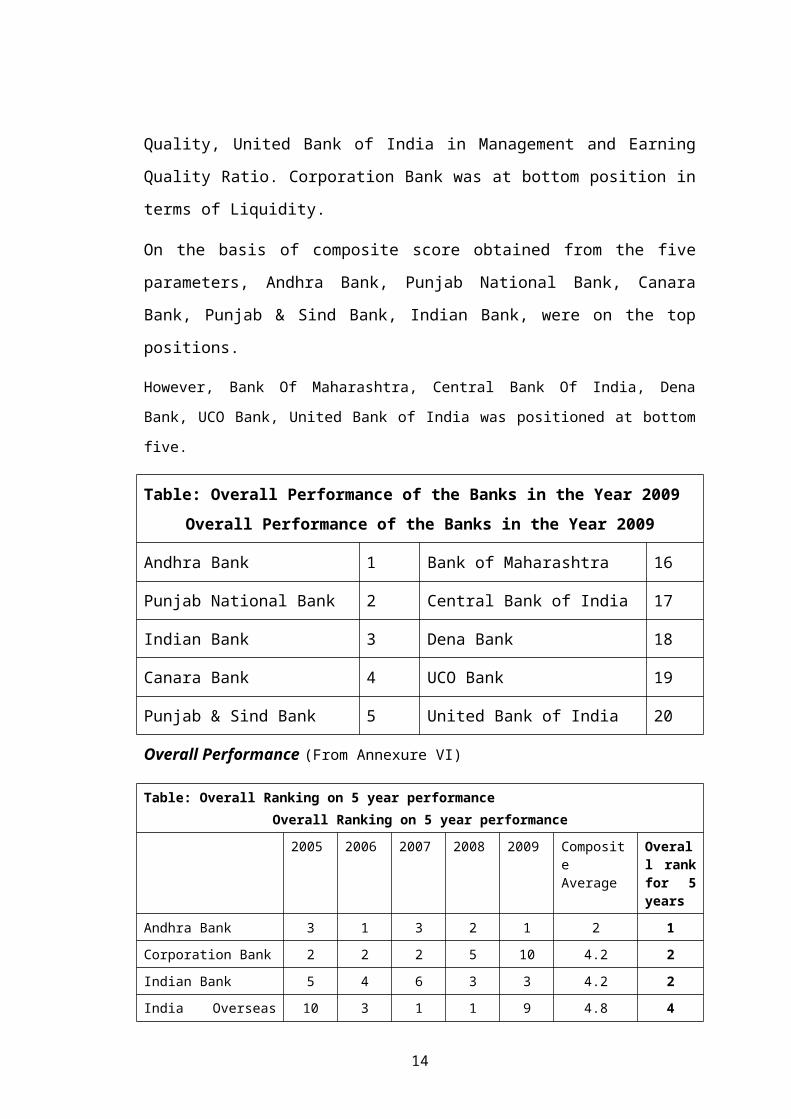

On the basis of composite score obtained from the five parameters, Andhra Bank,

Punjab National Bank, Canara Bank, Punjab & Sind Bank, Indian Bank, were on the

top positions.

However, Bank Of Maharashtra, Central Bank Of India, Dena Bank, UCO Bank, United Bank

of India was positioned at bottom five.

Table: Overall Performance of the Banks in the Year 2009

Overall Performance of the Banks in the Year 2009

Andhra Bank 1 Bank of Maharashtra 16

Punjab National Bank 2 Central Bank of India 17

Indian Bank 3 Dena Bank 18

Canara Bank 4 UCO Bank 19

Punjab & Sind Bank 5 United Bank of India 20

Overall Performance (From Annexure VI)

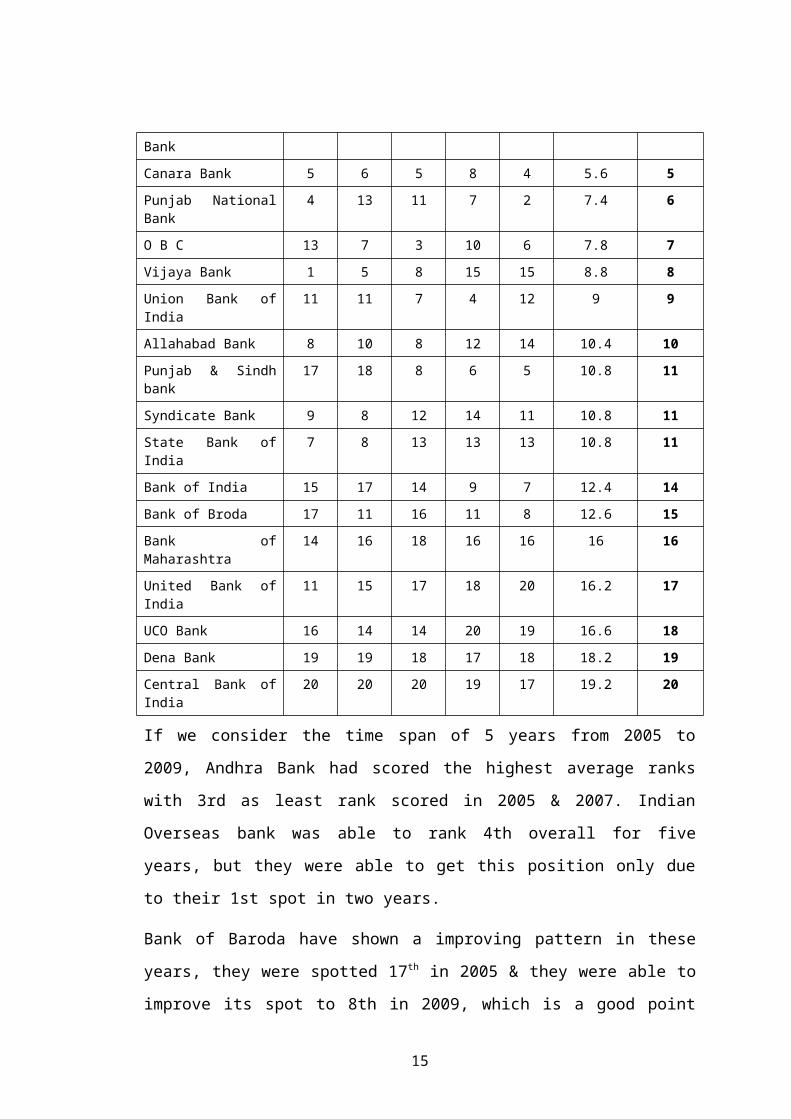

Table: Overall Ranking on 5 year performance

Overall Ranking on 5 year performance

2005 2006 2007 2008 2009 Composite Average

Overall rank for 5 years

Andhra Bank 3 1 3 2 1 2 1

Corporation Bank 2 2 2 5 10 4.2 2

Indian Bank 5 4 6 3 3 4.2 2

India Overseas Bank 10 3 1 1 9 4.8 4

Canara Bank 5 6 5 8 4 5.6 5

Punjab National Bank 4 13 11 7 2 7.4 6

O B C 13 7 3 10 6 7.8 7

Vijaya Bank 1 5 8 15 15 8.8 8

Union Bank of India 11 11 7 4 12 9 9

Allahabad Bank 8 10 8 12 14 10.4 10

10

Punjab & Sindh bank 17 18 8 6 5 10.8 11

Syndicate Bank 9 8 12 14 11 10.8 11

State Bank of India 7 8 13 13 13 10.8 11

Bank of India 15 17 14 9 7 12.4 14

Bank of Broda 17 11 16 11 8 12.6 15

Bank of Maharashtra 14 16 18 16 16 16 16

United Bank of India 11 15 17 18 20 16.2 17

UCO Bank 16 14 14 20 19 16.6 18

Dena Bank 19 19 18 17 18 18.2 19

Central Bank of India 20 20 20 19 17 19.2 20

If we consider the time span of 5 years from 2005 to 2009, Andhra Bank had scored

the highest average ranks with 3rd as least rank scored in 2005 & 2007. Indian

Overseas bank was able to rank 4th overall for five years, but they were able to get

this position only due to their 1st spot in two years.

Bank of Baroda have shown a improving pattern in these years, they were spotted 17 th

in 2005 & they were able to improve its spot to 8th in 2009, which is a good point for

the bank Canara Bank has shown a consistent position in all these years, Canara Bank

have been spotted around average ranks ranging between 4 to 8 & so the overall rank

for 5 years is 5th & same was the case with Allahabad Bank with overall rank of 10

for 5 years.

Punjab & Sind Bank has also shown a substantial growth, by raising its position of

17th in 2005 to 8th in 2007 & 5th in 2009, but due to bad position in previous years it

was able to rank only 11th in overall performance ranking same was the case with

Bank of India which was at 15th rank in 2007 & later in 2009 they were spotted at 7 th

rank.

Performance of Vijaya Bank has been declining year by year, they were at 1st

position in 2005 but later on they were at 15th in 2009.

Position of State Bank of India has shown a mixed results, we came to know that even

though it is a biggest bank in India but SBI has not availed good ranks over the time

period, they were just near the top five banks in 2005 & 2006 at 7th & 8th rank

respectively but later on in all SBI was able to get only 13th in all years. So overall

rank of SBI was just 11th rank.

11

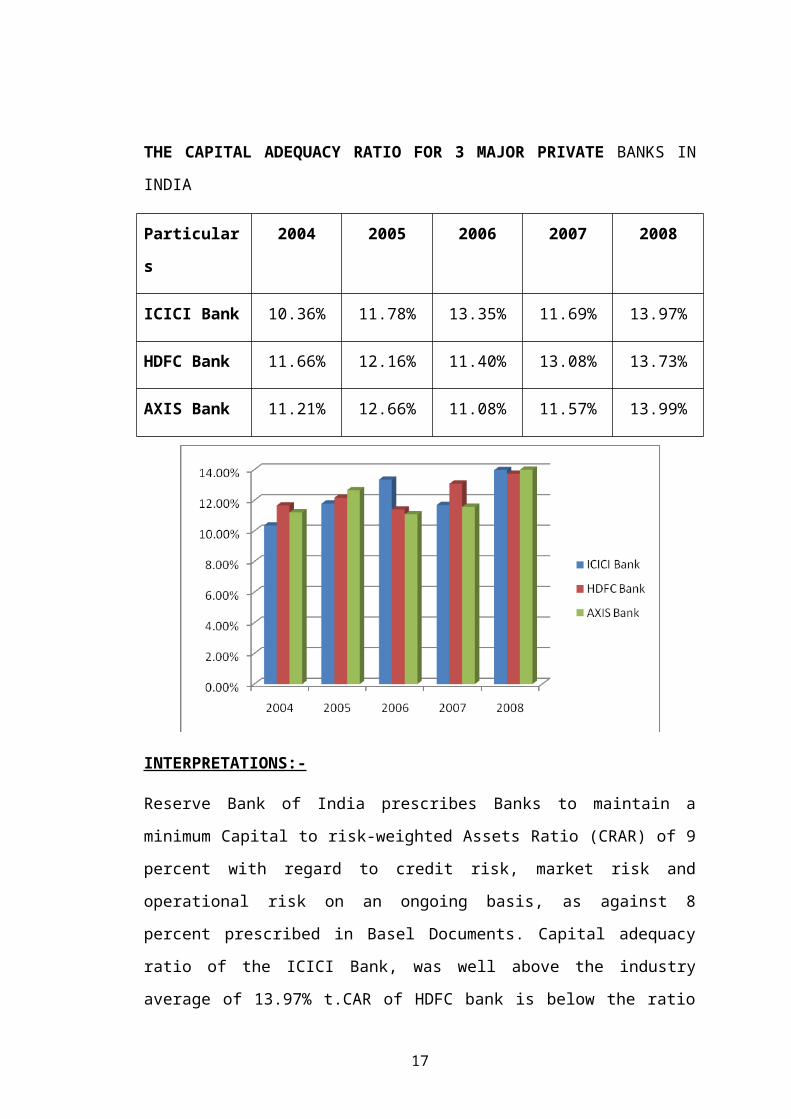

THE CAPITAL ADEQUACY RATIO FOR 3 MAJOR PRIVATE BANKS IN

INDIA

Particulars 2004 2005 2006 2007 2008

ICICI Bank 10.36% 11.78% 13.35% 11.69% 13.97%

HDFC Bank 11.66% 12.16% 11.40% 13.08% 13.73%

AXIS Bank 11.21% 12.66% 11.08% 11.57% 13.99%

INTERPRETATIONS:-

Reserve Bank of India prescribes Banks to maintain a minimum Capital to risk-

weighted Assets Ratio (CRAR) of 9 percent with regard to credit risk, market risk and

operational risk on an ongoing basis, as against 8 percent prescribed in Basel

Documents. Capital adequacy ratio of the ICICI Bank, was well above the industry

average of 13.97% t.CAR of HDFC bank is below the ratio of ICICI bank. HDFC

Bank’s total Capital Adequacy stood at 13.6% as of March 31, 2008. The Bank

adopted the Basel 2 framework as of March 31, 2009 and the CAR computed as per

Basel 2 guidelines stands higher against the regulatory minimum of 9.0%.And the

capital adequacy ratio of Axis bank is the highest among the three banks and it is

12

above the industry average, which shows the improvement from the last 5 years.

Higher the ratio the banks are in a comfortable position to absorb losses.

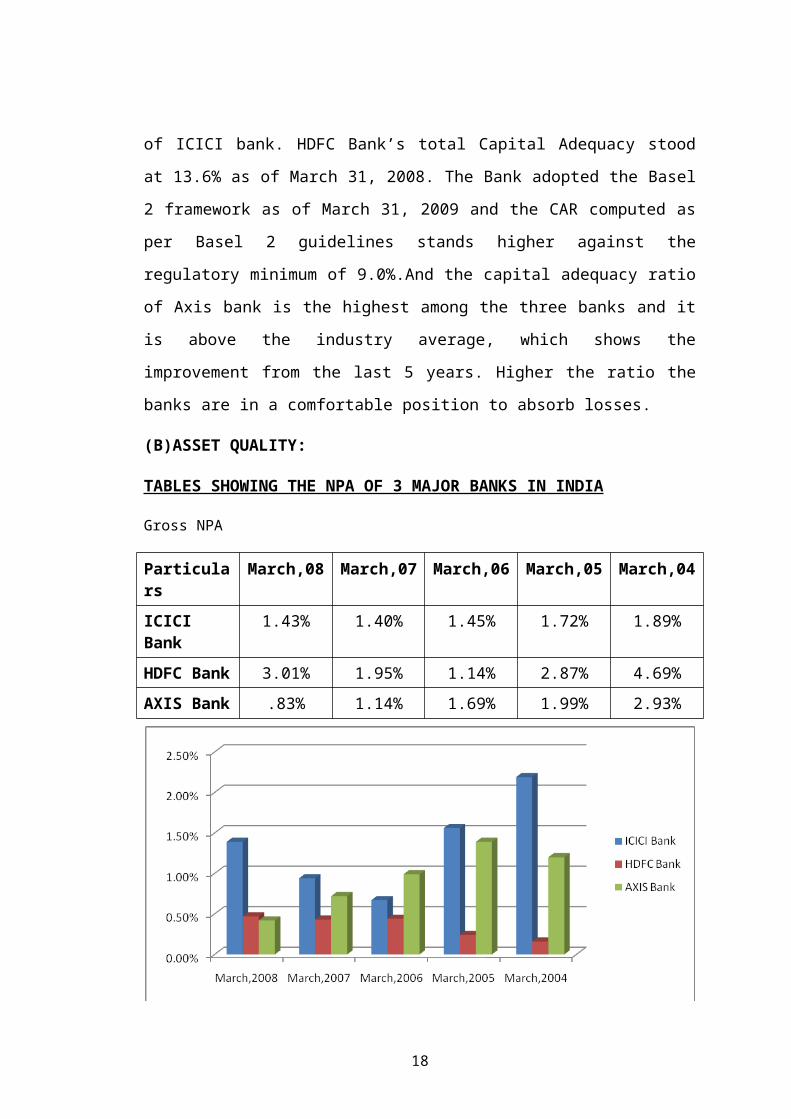

(B)ASSET QUALITY:

TABLES SHOWING THE NPA OF 3 MAJOR BANKS IN INDIA

Gross NPA

Particulars March,08 March,07 March,06 March,05 March,04

ICICI Bank 1.43% 1.40% 1.45% 1.72% 1.89%

HDFC Bank 3.01% 1.95% 1.14% 2.87% 4.69%

AXIS Bank .83% 1.14% 1.69% 1.99% 2.93%

Net NPA

Particulars March, 08 March, 07 March, 06 March, 05 March, 04

ICICI Bank 1.39% .94% .67% 1.56% 2.19%

HDFC Bank .47% .43% .44% .24% .16%

AXIS Bank .42% .72% .99% 1.39% 1.20%

13

INTERPRETATIONS:

Above ratios show the highest NPA of ICICI bank from the last 5 years among the 3

banks. HDFC Bank’s asset quality is the best in the Indian banking sector despite the

bank sustaining aggressive growth for the past several quarters. The bank has

maintained its net NPAs at 0.47% as at end FY08. It has continued to make general

provisions and holds specific general provisions on its standard customer assets that

are higher than regulatory requirements. Axis bank is also approaching to this level.

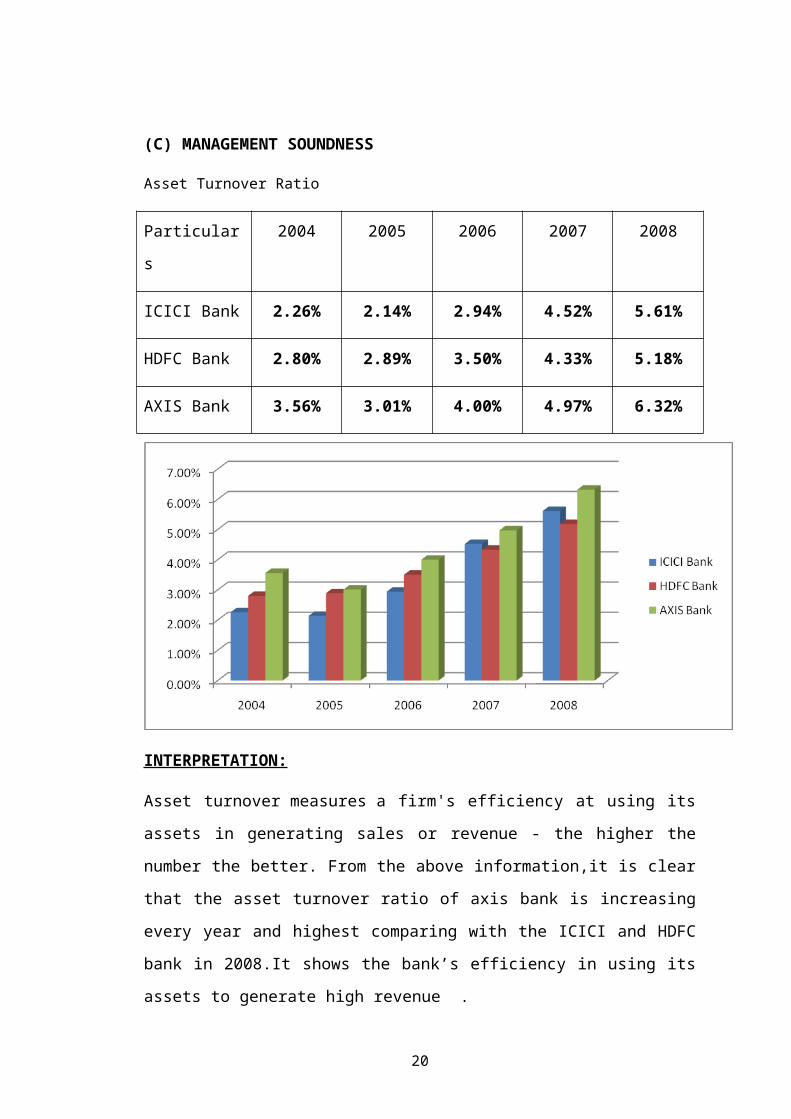

(C) MANAGEMENT SOUNDNESS

Asset Turnover Ratio

Particulars 2004 2005 2006 2007 2008

ICICI Bank 2.26% 2.14% 2.94% 4.52% 5.61%

HDFC Bank 2.80% 2.89% 3.50% 4.33% 5.18%

AXIS Bank 3.56% 3.01% 4.00% 4.97% 6.32%

14

INTERPRETATION:

Asset turnover measures a firm's efficiency at using its assets in generating sales or

revenue - the higher the number the better. From the above information,it is clear that

the asset turnover ratio of axis bank is increasing every year and highest comparing

with the ICICI and HDFC bank in 2008.It shows the bank’s efficiency in using its

assets to generate high revenue .

15

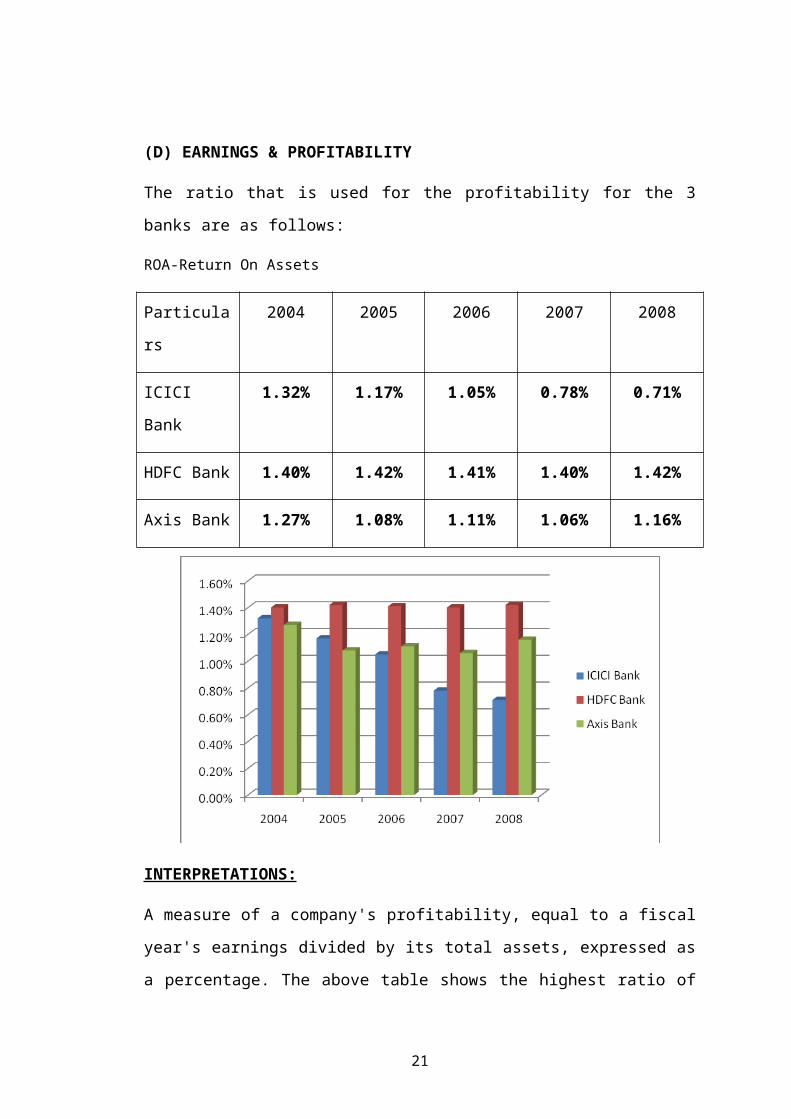

(D) EARNINGS & PROFITABILITY

The ratio that is used for the profitability for the 3 banks are as follows:

ROA-Return On Assets

Particulars 2004 2005 2006 2007 2008

ICICI Bank 1.32% 1.17% 1.05% 0.78% 0.71%

HDFC Bank 1.40% 1.42% 1.41% 1.40% 1.42%

Axis Bank 1.27% 1.08% 1.11% 1.06% 1.16%

INTERPRETATIONS:

A measure of a company's profitability, equal to a fiscal year's earnings divided by its

total assets, expressed as a percentage. The above table shows the highest ratio of

HDFC Bank for the last 5 years.ROA of ICICI bank is falling every year .And Axis

Bank has maintained almost the same level of the ratio for the last 5 years.

16

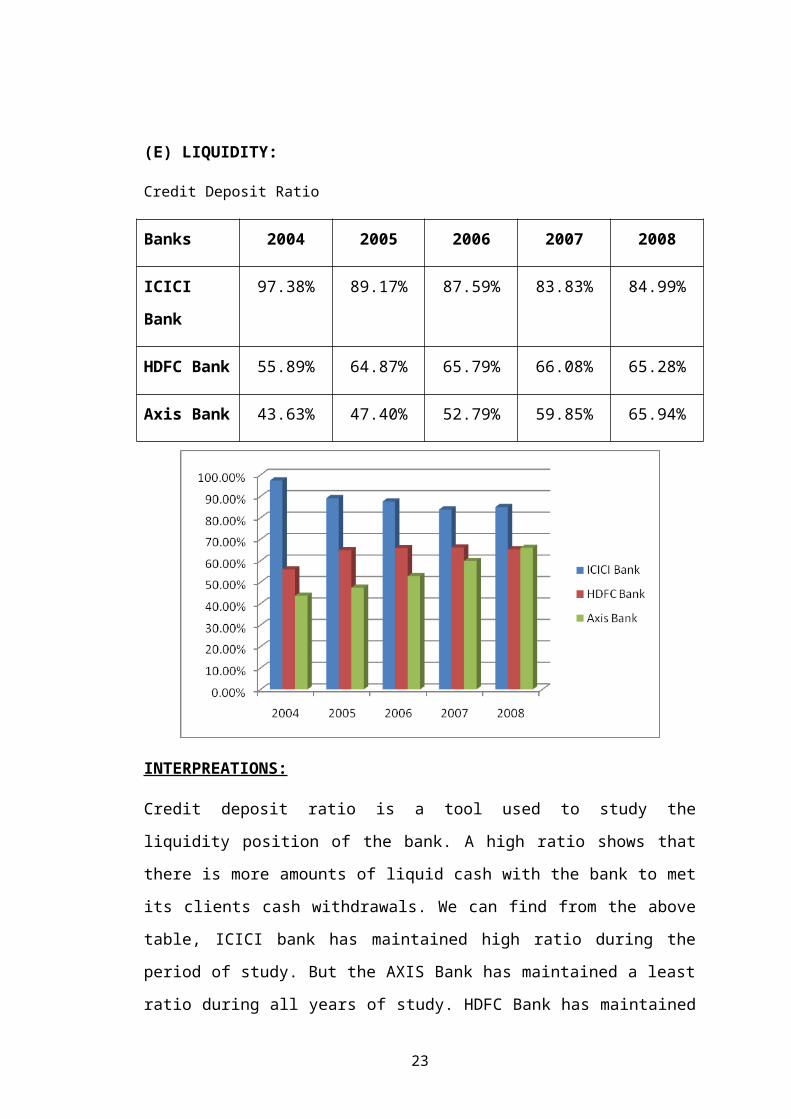

(E) LIQUIDITY:

Credit Deposit Ratio

Banks 2004 2005 2006 2007 2008

ICICI Bank 97.38% 89.17% 87.59% 83.83% 84.99%

HDFC Bank 55.89% 64.87% 65.79% 66.08% 65.28%

Axis Bank 43.63% 47.40% 52.79% 59.85% 65.94%

INTERPREATIONS:

Credit deposit ratio is a tool used to study the liquidity position of the bank. A high

ratio shows that there is more amounts of liquid cash with the bank to met its clients

cash withdrawals. We can find from the above table, ICICI bank has maintained high

ratio during the period of study. But the AXIS Bank has maintained a least ratio

during all years of study. HDFC Bank has maintained the cdr ratio lower than ICICI

but higher than Axis bank.But in 2008 CDR of Axis bank was more than HDFC bank.

17

FINDINGS, RECOMMENDATIONS & SUGGESTIONS

This study investigates the performance of the nationalized banks through the help of

the CAMEL model. For the purpose, a sample of 20 nationalized banks is taken. For

the CAMEL Analysis, the data of five years, i.e., from 2004-05 to 2008-09, has been

used. After making an analysis of the CAMEL parameters, all the banks were first

individually ranked for each ratio on a single parameter. Then the composite some of

each bank for each parameter was arrived at by taking an average of the individual

ranks achieved by the banks for each ratio in a single parameter. Then, all the banks

for each parameter were ranked in the proper order i.e., ascending/descending based

on the parameter.

According to the model, there are various parameters which tell us about the

performance of the banks in comparison to other banks. These parameters are

CCapital Adequacy, A- Asset Quality, M-management, E- Earnings and L- Liquidity.

There are various ratios in all of these parameters for example in Capital Adequacy

the various ratios are Capital Adequacy Ratio, Debt/Equity, Advances/Assets and

Government Securities/Investment.

The analysis was done, by calculating each of the ratios individually for the five

financial years and then ranking the banks on the basis of their performance in

comparison to other banks. Then, the ratios of the various parameters on a particular

year were combined with each year and group average was calculated. After that,

group rank was calculated which was again in comparison to other banks. When, all

the ratios of all the parameters of all the years were calculated, the next step was to

find the best performing bank for each year.

The ranks of all parameters of a year were combined and then a composite rank was

calculated. This process of calculating composite rank was repeated for all the next

financial years too. The composite rank was calculated by adding up the ranks of all

the parameters for that year and dividing by five. After that, again the banks were

ranked using the rank formula in Microsoft excel sheet, in comparison to other ranks.

Here, the bank which had the least composite average was the best and so was ranked

the best that is 1st.

18

Economic development of any country is mainly influenced by the growth of the

banking industry in that country. The banking industry has gone through innumerable

twists and turns in the post independence era. The banking industry in India is

growing at a fast pace. Increased economic activity coupled with de-regulation has

further strengthened the position of Indian bank. The growth has not been restricted to

any specific sector, all sectors (public sector, private sector and foreign) have shown

good growth.

CAMEL provides a measurement of a bank’s current overall financial, managerial,

and operational and compliance performance. It is a diagnostic model and

management tool that measures capital adequacy, asset quality, management, earnings

and liquidity of Financial Institutions. During the course of the rating procedure,

attention is focused on the financial strength and payment capacity of the Financial

Institution based on its historical trends, typically going back five years, and

compared against its peers.

Overall performance ranking table shows that Andhra Bank had scored the highest

average ranks with 3rd as least rank scored in 2005 & 2007. Indian Overseas bank

was able to rank 4th overall for five years, but they were able to get this position only

due to their 1st spot in two out of five years.

Bank of Baroda have shown a improving pattern in these years, they were spotted 17 th

in 2005 & they were able to improve its spot to 8th in 2009, which is a good point for

the bank, they were able to attain such a growth improving itself on all parameters of

CAMEL model.

Canara Bank has shown a consistent position in all these years, Canara Bank have

been spotted around average ranks ranging between 4 to 8 & so the overall rank for 5

years is 5th & same was the case with Allahabad Bank with overall rank of 10 for 5

years.

Punjab & Sind Bank has also shown a substantial growth, by raising its position of

17th in 2005 to 8th in 2007 & 5th in 2009, but due to bad position in previous years it

was able to rank only 11th in overall performance ranking same was the case with

Bank of India which was at 15th rank in 2007 & later in 2009 they were spotted at 7 th

rank.

19

Performance of Vijaya Bank has been declining year by year, they were at 1st

position in 2005 but later on they were at 15th in 2009. Decreasing Asset Quality

ratios & Management ratios were the main reason for the fall in their rank.

Position of State Bank of India has shown a mixed results, we came to know that even

though it is a biggest bank in India but SBI has not availed good ranks over the time

period, they were just near the top five banks in 2005 & 2006 at 7th & 8th rank

respectively but later on in all SBI was able to get only 13th in all years. So overall

rank of SBI was just 11th rank. Asset quality was the main are that has to be focused

by the SBI for improving its position.

In bottom five Central Bank of India was on the last position i.e. 20th rank, following

the other banks like Dena Bank, UCO, and United & Bank of Maharashtra.

The capital adequacy ratio of all the three private sector banks is above the minimum

requirements and above the industry average. HDFC Bank has maintained a standard

for the NPA’s in the period of 2004-2008. AXIS has shown remarkable decrease in

NPA’s in the same period. But the NPA of ICICI bank is increasing every year.

Professional approach that has been adopted by the banks in the recent past is in right

direction & also it is the right decision. HDFC has shown a good growth record for its

ROA. But ICICI Bank has gone down in its performance with negative growth.

AXIS’s performance has been average. Banks should maintain quality securities with

good liquidity to meet contingencies. ICICI Bank is fulfilling this requirement by

maintaining highest credit deposit ratio. All banks have ventured into many financial

areas and are in the league of Universal Banking. They have also become sensitive to

customer needs.

RECOMMENDATIONS:

Allahabad Bank need to improve its Earning, Liquidity position as they have

been ranked 10th on overall performance for 5 years, but these are the two

parameters were the bank is lacking.

Bank of Baroda & Bank of India both need to improve its investments in

government & approved securities, as this was the parameter where bank was

not able to outperform.

20

Bank of Maharashtra should decrease its debt equity ratio so as to attract new

investors & also decrease fixed charge on bank’s earnings.

Canara Bank should improve their advancing techniques, as they are lacking

in controlling their net NPAs & also all ratios considered under Earnings

parameter need be raised.

Corporation bank has shown a declining trend in its Capital adequacy ranks,

specially its Government securities to total assets ratio is very low, which also

reduced the liquidity. So we recommend Corporation bank to improve its

Government Securities holdings.

State Bank of India, which is the largest bank of Indian banking industry, is

performing good under the capital adequacy parameter in all years but the

main are of concern for the bank is the Asset quality & the Management where

they have been ranked 15th in Asset quality in all years & 11th in

Management. So we recommend the body to improve its NPAs position

In Punjab & Sind Bank, debt equity ratio is continuously rising over the years

which are not good so they have to increase equity or reduce debts in their

capital structure.

United Bank of India has comparatively less total advance to total asset ratio.

So, bank has to give more advances in order to earn more interest. But they

should have to also keep in mind the credit worthiness of the customers.

Indian Overseas Bank need to improve its asset quality ratio, as its rank has

been going down year by year, so they must make necessary arrangements to

make sure that they have lower NPAs or should work on more careful

advancing activities.

Vijaya Bank should improve its earning capacity ratios, as its operating profit

to average working fund is very low, which also hinders its management

quality. The Liquidity position of the bank has also not been so good, Vijaya

Bank need to increase its holdings in government securities.

The banks should adapt themselves quickly to the changing norms.

21

The system is getting internationally standardized with the coming of

BASELL II accords so the Indian banks should strengthen internal processes

so as to cope with the standards.

The banks should maintain a 0% NPA by always lending and investing or

creating quality assets which earn returns by way of interest and profits.

The banks should find more avenues to hedge risks as the market is very

sensitive to risk of any type.

Have good appraisal skills, system, and proper follow up to ensure that banks

are above the risk.

SUGGESTIONS FOR FURTHER RESEARCH

Research on which industries are best suited for the use of the CAMELS

Framework.

Research on how other variables can be added or how variables can be

selected to suit the industry needs.

Research on why the CAMELS Framework can not be used as a tool of

performance evaluation.

Websites Visited

http://www.stock-picks-focus.com/hdfc-bank.html

http://www.stock-picks-focus.com/axis-bank.html

http://www.stock-picks-focus.com/icici-bank.html

http://www.basel2implementation.com/pillars.htm

http://www.icicibank.com

http:// www.hdfcbank.com

http:// www.axisbank.com

http://www.allbankingsolutions.com/camels.htm

http://www.shkfd.com.hk/glossary/eng/RA.htm

"http://www.wikinvest.com/wiki/CAPITAL_ADEQUACY_RATIO"

22

http://www.answers.com/topic/basel-ii

http://chestofbooks.com/finance/banking/English-Manual/Chapter-I-The-

Origin-And-Uses-Of-Banks.html

http://www.allbankingsolutions.com/CAMEL.htm Accessed on 27/2/2010

23