©Cambridge Business Publishing, 2010 Single Economic Entity Consolidated statements present...

55

©Cambridge Business Publishing, ©Cambridge Business Publishing, 2010 2010 Single Economic Entity Consolidated statements present financial performance and status of consolidated companies as a single economic entity Intercompany transactions must be removed Two types of intercompany sales/transfers Downstream sale/transfer Occurs when the parent sells to a subsidiary Upstream sale/transfer Occurs when a subsidiary sells to a parent 1 Often used to enhance supply chain efficiencies

-

date post

21-Dec-2015 -

Category

Documents

-

view

218 -

download

0

Transcript of ©Cambridge Business Publishing, 2010 Single Economic Entity Consolidated statements present...

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Single Economic Entity

Consolidated statements present financial performance and status of consolidated companies as a single economic entity Intercompany transactions must be removed

Two types of intercompany sales/transfers Downstream sale/transfer

Occurs when the parent sells to a subsidiary

Upstream sale/transfer Occurs when a subsidiary sells to a parent

1

Often used to enhance supply chain efficiencies

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Eliminating Intercompany Transactions

Why eliminate intercompany revenues and expenses? Do not arise out of transactions with outside

parties Must avoid overstatement of consolidated

revenues and expenses Also eliminate related intercompany

receivables and payables Eliminate gains and losses on

intercompany asset transfers Since gains and losses are not ‘confirmed’

by outside party transactions, assets held at end of period must be adjusted

2

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Eliminating Entries3

Eliminate current year’s equity method entries

Eliminate subsidiary’s beginning-of-year stockholders’ equity account balances

Revalue the subsidiary’s assets and liabilities as of the beginning of the year

Recognize current year write-offs of the subsidiary’s asset and liability revaluations

Recognize the noncontrolling interest in net income

Eliminate the effects of upstream and downstream intercompany transactions

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

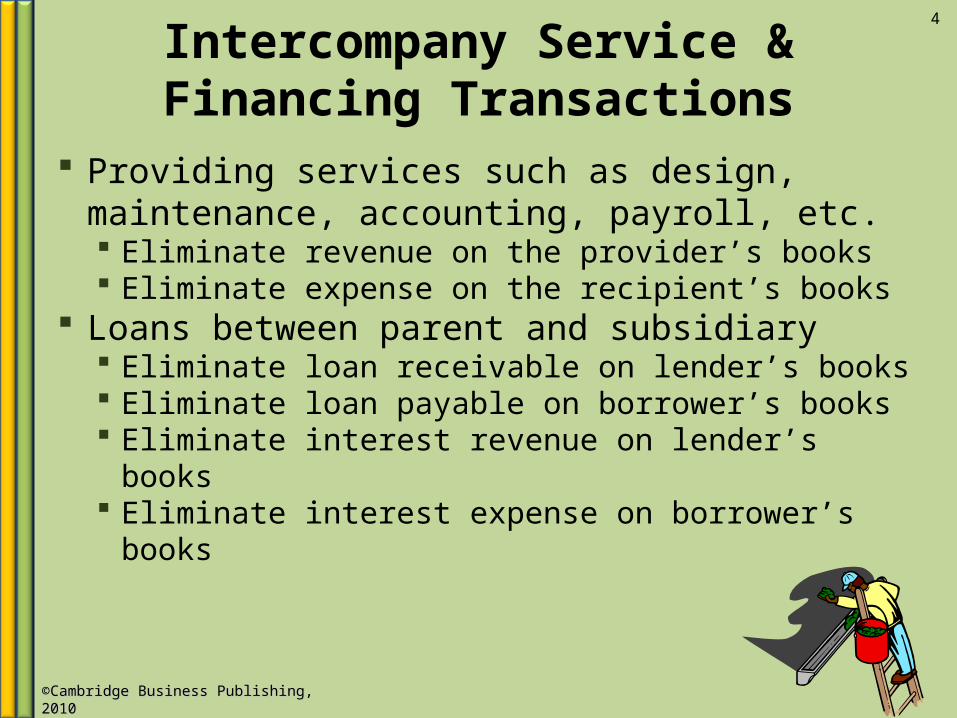

Intercompany Service & Financing Transactions

Providing services such as design, maintenance, accounting, payroll, etc. Eliminate revenue on the provider’s books Eliminate expense on the recipient’s books

Loans between parent and subsidiary Eliminate loan receivable on lender’s books Eliminate loan payable on borrower’s books Eliminate interest revenue on lender’s books Eliminate interest expense on borrower’s

books

4

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Eliminating Intercompany Service Transactions Example

Parrish Shoe Factory is a subsidiary of Jordan Athleticwear. In 2010, Jordan provides design services costing $650,000 to Parrish and bills Parrish $900,000. At year-end, Parrish still owes Jordan $100,000.

5

Balances at December 31, 2010: Jordan ParrishBalance Sheet: Accounts receivable $100,000 - Accounts payable - $100,000Income Statement: Design revenue 900,000 - Design expense 650,000 900,000

To eliminate the intercompany receivable/payable:(I) Accounts payable 100,000

Accounts receivable 100,000

To eliminate the intercompany service revenue/expense:(I) Design revenue 900,000

Design expense 900,000

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Eliminating Intercompany Loan Transactions Example

Parrish Shoe Factory is a subsidiary of Jordan Athleticwear. In 2010, Jordan loans $1,000,000 to Parrish. Interest on the loan totals $50,000, and is accrued and paid.

6

Balances at December 31, 2010:

To eliminate the intercompany loan principal:

To eliminate the intercompany interest revenue/expense:

Jordan ParrishBalance Sheet: Loan receivable $1,000,000 $ - Loan payable - 1,000,000Income Statement: Interest revenue 50,000 - Interest expense - 50,000

(I) Loan payable 1,000,000 Loan receivable 1,000,000

(I) Interest revenue 50,000 Interest expense 50,000

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Intercompany Profits

Result from transferred assets from one affiliate to the other

Per ARB 51, profits not yet confirmed by further sale to outside parties must be eliminated Both upstream and downstream transactions i.e., not considered to be arm’s-length transactions

Confirmed profits require no elimination

7

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Eliminating Intercompany Profits Example

Parrish Shoe Factory is a subsidiary of Jordan Athleticwear. In 2010, Jordan sells land to Parrish for $1,400,000 that had an original cost of $1,000,000. Prior to consolidation, Jordan shows a gain of $400,000 on its books while Parrish carries the land at $1,400,000.

8

To eliminate the unconfirmed intercompany profit and reduce the land to original acquisition cost:

(I) Gain on sale of land 400,000 Land 400,000

• Land in consolidated balance sheet will be $1,000,000• Gain of $400,000 remains in Jordan’s retained earnings• Land remains at $1,400,000 on Parrish’s books

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

If Subsidiary Has Noncontrolling Interest

Elimination of intercompany profits arising in downstream sales must be made Affects only the controlling interest in consolidated

income No effect on subsidiary’s income No effect on any noncontrolling interest in income

Elimination of intercompany profits arising in upstream sales must be made Affects both controlling and noncontrolling

interests in consolidated net income Elimination of profit shared between controlling

and noncontrolling interests

9

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Equity Method Income Effects

Affects equity method income accrual Due to unconfirmed intercompany gains and

losses on upstream and downstream sales Parent’s share of unconfirmed intercompany

gains (losses) is deducted (added) to its share of subsidiary’s reported net income

Because unconfirmed profits are eliminated in consolidation

10

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Equity Method Effects of Unconfirmed Intercompany Profits

11

Effects of Unconfirmed Intercompany Profits

Equity in Net IncomeNoncontrolling Interest in

Net Income

Downstream transactions

Remove all unconfirmed profit

No effect

Upstream transactions

Remove parent's share of unconfirmed profit

Remove noncontrolling interest's share of unconfirmed profit

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Equity Method ExampleJordan Athleticwear acquires 80% of Parrish Shoe Factory on January 1, 2010. During 2010, Jordan sells merchandise costing $380,000 to Parrish for $400,000, which Parrish still holds at year-end.

12

$20,000 profit unconfirmed until Parrish

sells to an outside customer

Equity in Income of Parrish

Deduct $20,000 to remove downstream intercompany profit

Suppose Parrish sells the merchandise to Jordan, and Jordan holds the merchandise at year-end.

$20,000 profit unconfirmed until Jordan sells to an

outside customer

Jordan’s Equity in Income

Deduct Jordan’s 80% share of unconfirmed profit ($16,000 )to remove upstream intercompany profit

Noncontrolling Interest in Net Income

Deduct noncontrolling interest’s 20% share of unconfirmed profit ($4,000)

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

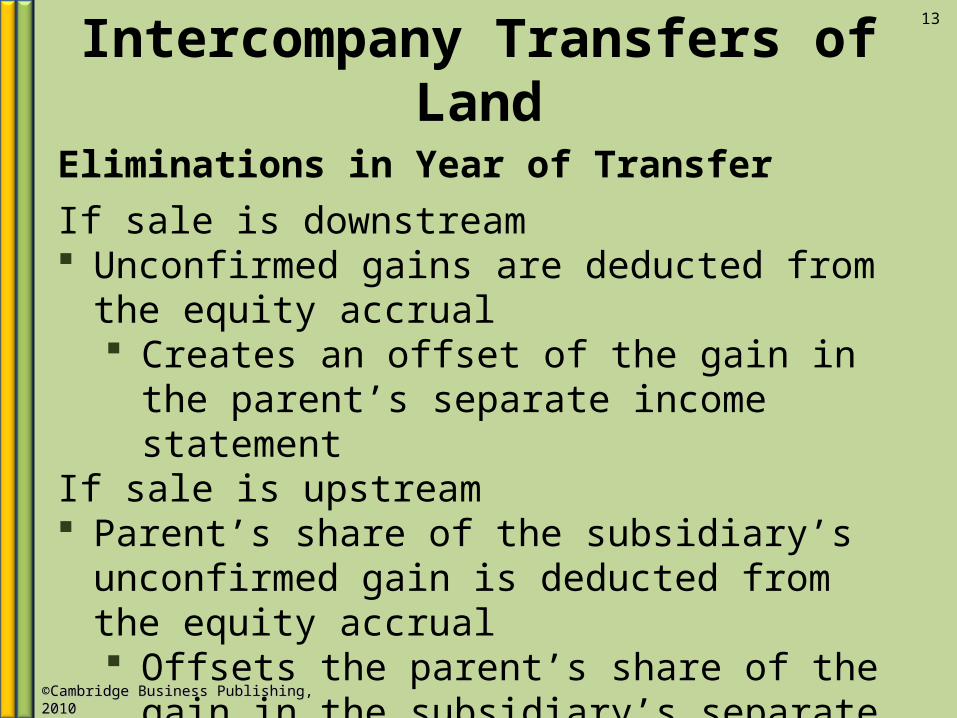

Intercompany Transfers of Land

Eliminations in Year of Transfer

13

If sale is downstream Unconfirmed gains are deducted from the equity

accrual Creates an offset of the gain in the parent’s

separate income statementIf sale is upstream Parent’s share of the subsidiary’s unconfirmed

gain is deducted from the equity accrual Offsets the parent’s share of the gain in the

subsidiary’s separate income statement

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Intercompany Transfers of Land –Year of Transfer Example

14

In 2010, one affiliate sells land costing $2,000,000 to the other affiliate for $2,300,000. The buying affiliate holds the land at year-end.

Consolidation eliminating entry, year of transferTo eliminate the unconfirmed intercompany profit and reduce the land to original acquisition cost (same entry, downstream or upstream):

(I) Gain on sale of land 300,000 Land 300,000

Effects of $300,000 Unconfirmed Intercompany Profit in Year of Transfer

Equity in Net

Income20% Noncontrolling

Interest in Net IncomeDownstream transfer Subtract $300,000 No effectUpstream transfer Subtract $240,000 Subtract $60,000

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Intercompany Transfers of Land –Subsequent Years

Sold Upstream in a Prior Period

15

Must eliminate the unconfirmed gain from subsidiary’s beginning retained earnings

Facilitates elimination of the investment account against the parent’s share of the subsidiary’s stockholders’ equity

Sold Downstream In subsequent years, must add back the

unconfirmed gain to the investment account No adjustment to retained earnings because

downstream transfers have no effect on subsidiary’s income

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

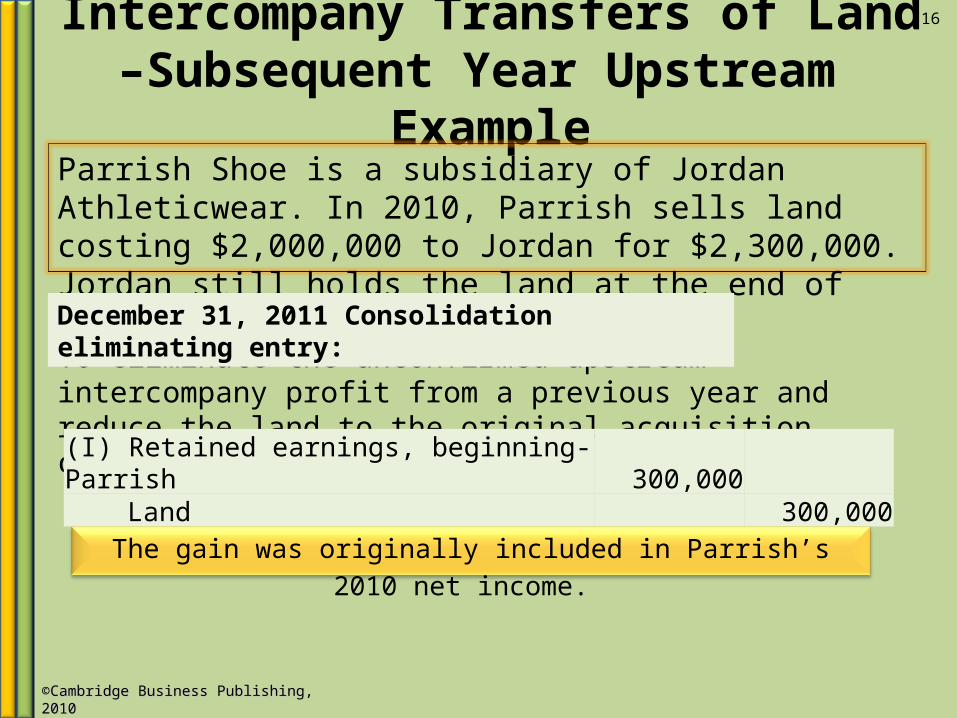

Intercompany Transfers of Land –Subsequent Year Upstream Example

Parrish Shoe is a subsidiary of Jordan Athleticwear. In 2010, Parrish sells land costing $2,000,000 to Jordan for $2,300,000. Jordan still holds the land at the end of 2011.

16

To eliminate the unconfirmed upstream intercompany profit from a previous year and reduce the land to the original acquisition cost:

December 31, 2011 Consolidation eliminating entry:

(I) Retained earnings, beginning-Parrish 300,000 Land 300,000

The gain was originally included in Parrish’s 2010 net income.

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

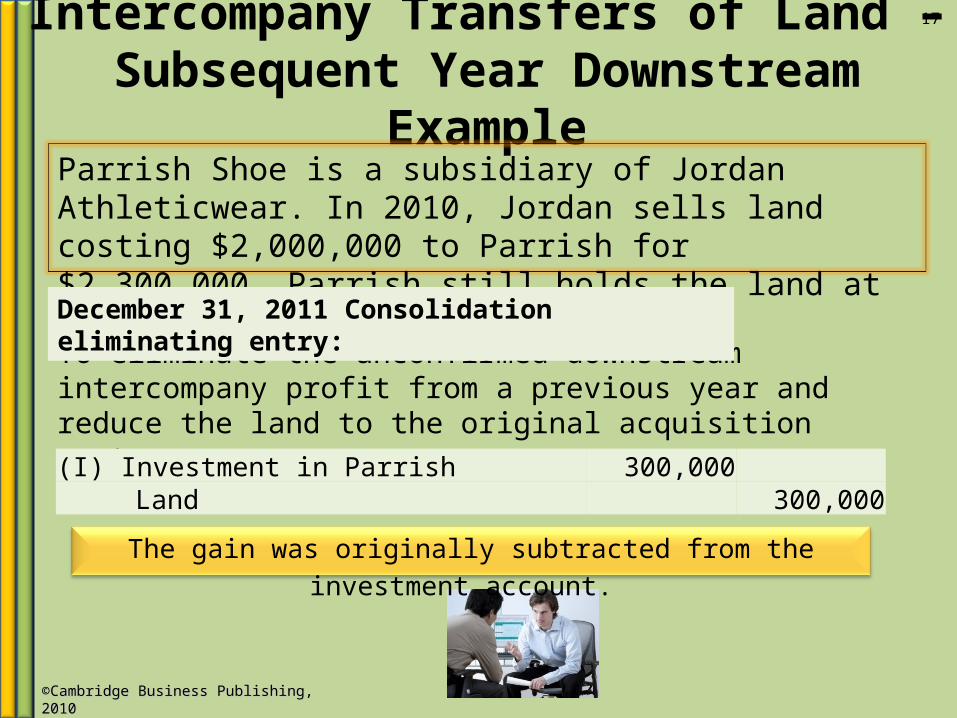

Intercompany Transfers of Land –Subsequent Year Downstream Example

Parrish Shoe is a subsidiary of Jordan Athleticwear. In 2010, Jordan sells land costing $2,000,000 to Parrish for $2,300,000. Parrish still holds the land at the end of 2011.

17

To eliminate the unconfirmed downstream intercompany profit from a previous year and reduce the land to the original acquisition cost:

December 31, 2011 Consolidation eliminating entry:

(I) Investment in Parrish 300,000 Land 300,000

The gain was originally subtracted from the investment account.

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Intercompany Transfers of Land –Year of Sale to Outside Party

Requires that the original intercompany gain be recognized in consolidated net income in the year of sale to outside party

Upstream Entry transfers the original gain out of the

subsidiary’s retained earnings and into current income

Downstream Entry adds the gain back to the investment

account from which it was previously deducted via the equity method income accrual and recognizes it as current income

18

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Intercompany Transfers of Land –Year of Sale to Outside Party Example

Assume the land was sold in 2012 for $3 million. The original cost to the consolidated entity was $2 million, requiring a consolidated gain of $1 million to be reported. The selling entity carries the land at $2,300,000, and reports a gain of $700,000.

19

Upstream - To include in current consolidated net income the previously recorded upstream gain now confirmed through external sale:

(I) Retained earnings, beginning-Parrish 300,000 Gain on sale of land 300,000

Downstream - To include in current consolidated net income the previously recorded downstream gain now confirmed through external sale:

(I) Investment in Parrish 300,000 Gain on sale of land 300,000

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Intercompany Transfers of Land –Year of Sale to Outside Party Example

Assume the land was sold in 2012 for $3 million. The original cost to the consolidated entity was $2 million, requiring a consolidated gain of $1 million to be reported. The selling entity carries the land at $2,300,000, and reports a gain of $700,000.

20

Effects of $300,000 Unconfirmed Intercompany Profit in Year of Sale to Outside Party

Equity in Net

Income20% Noncontrolling

Interest in Net Income

Downstream transfer Add $300,000 No effect

Upstream transfer Add $240,000 Add $60,000

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Intercompany Transfers of Inventory

Elimination of intercompany revenues and expenses required

Unconfirmed gains or losses may exist If intercompany transfer price differs from cost,

and Goods remain in the affiliated entity at year-end

Unconfirmed gain is part of ending or beginning inventory balance Eliminated by adjusting cost of goods sold

21

Eliminating intercompany profit in ending inventoryEliminating intercompany profit in ending inventory

Eliminating intercompany profit in beginning inventory

Eliminating intercompany profit in beginning inventory

Decreases cost of goods soldIncreases cost of goods sold

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

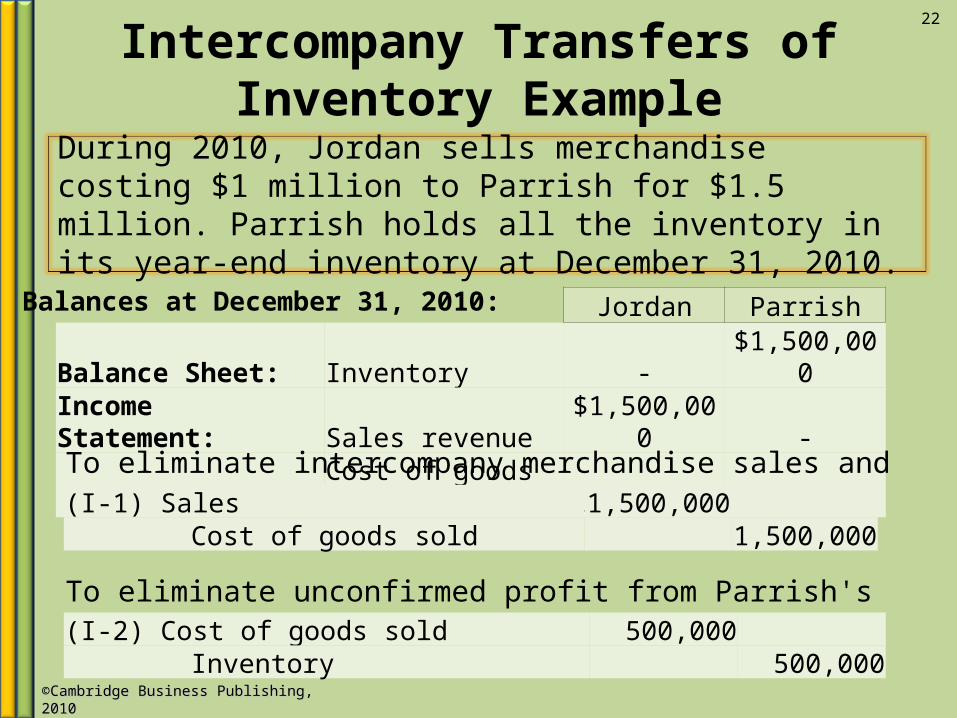

Intercompany Transfers of Inventory Example

During 2010, Jordan sells merchandise costing $1 million to Parrish for $1.5 million. Parrish holds all the inventory in its year-end inventory at December 31, 2010.

22

Jordan ParrishBalance Sheet: Inventory - $1,500,000Income Statement: Sales revenue $1,500,000 -

Cost of goods sold 1,000,000 -

Balances at December 31, 2010:

To eliminate intercompany merchandise sales and purchases:

To eliminate unconfirmed profit from Parrish's ending inventory:

(I-1) Sales 1,500,000 Cost of goods sold 1,500,000

(I-2) Cost of goods sold 500,000 Inventory 500,000

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Intercompany Transfers of Inventory Example

During 2010, Jordan sells merchandise costing $1 million to Parrish for $1.5 million. Parrish sells all the inventory for $1.8 million during 2010.

23

Jordan ParrishBalance Sheet: Inventory - - Income Statement: Sales revenue $1,500,000 $1,800,000

Cost of goods sold 1,000,000 1,500,000

Balances at December 31, 2010:

To eliminate intercompany merchandise sales and purchases:

The profit is confirmed, so no other elimination is needed.

(I) Sales 1,500,000 Cost of goods sold 1,500,000

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Unconfirmed Profit in Ending Inventory

Same whether upstream or downstream i.e., whether the parent or subsidiary holds the

inventory

Adjustments required for parent’s equity income accrual and noncontrolling interest in net income

24

Eliminating intercompany profit in ending inventoryEliminating intercompany profit in ending inventory Increases cost of goods sold

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Unconfirmed Profit in Ending Inventory Example

Assume merchandise priced at $5 million is sold to an affiliate during 2010. The buyer’s ending inventory includes $840,000 purchased from the seller. The seller’s markup is 20% of cost.

25

To eliminate intercompany merchandise sales and purchases.

To eliminate unconfirmed profit from the buyer’s ending inventory: $840,000 – ($840,000 ÷ 1.2) = $140,000

(I-1) Sales 5,000,000 Cost of goods sold 5,000,000

(I-2) Cost of goods sold 140,000 Inventory 140,000

Eliminations are the same whether upstream or downstream.

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Unconfirmed Profit in Ending Inventory Example

Assume merchandise priced at $5 million is sold to an affiliate during 2010. The buyer’s ending inventory includes $840,000 purchased from the seller. The seller’s markup is 20% of cost.

26

Effect of $140,000 unconfirmed profit in ending inventory:

Equity in Net

Income20% Noncontrolling

Interest in Net IncomeDownstream transfer Subtract $140,000 No effectUpstream transfer Subtract $112,000 Subtract $28,000

20% × $140,000 = $28,000

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Unconfirmed Profit in Beginning Inventory

Consolidated cost of goods sold is overstated by the previous year’s unconfirmed profits Must eliminate these gains by transferring into

current year income and reduce cost of goods sold

Adjustments required for parent’s equity income accrual and noncontrolling interest in net income

27

Eliminating intercompany profit in beginning inventoryEliminating intercompany

profit in beginning inventory Decreases cost of goods sold

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Unconfirmed Profit in Beginning Inventory Example

Assume merchandise priced at $5 million is sold to an affiliate during 2010. The buyer’s ending inventory includes $840,000 purchased from the seller. The seller’s markup is 20% of cost.

28

Downstream: Parrish’s beginning inventory includes $840,000 purchased from Jordan. To eliminate intercompany merchandise sales and purchases:

Upstream: Jordan’s beginning inventory includes $840,000 purchased from Parrish. To eliminate unconfirmed profit from beginning inventory:

(I) Investment in Parrish 140,000 Cost of goods sold 140,000

(I) Retained earnings, beginning - Parrish 140,000 Cost of goods sold 140,000

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Unconfirmed Profit in Beginning Inventory Example

Assume merchandise priced at $5 million is sold to an affiliate during 2010. The buyer’s ending inventory includes $840,000 purchased from the seller. The seller’s markup is 20% of cost.

29

Effect of $140,000 unconfirmed profit in ending inventory:

Equity in Net

Income20% Noncontrolling

Interest in Net IncomeDownstream transfer Add $140,000 No effectUpstream transfer Add $112,000 Add $28,000

20% × $140,000 = $28,000

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Intercompany Profits and Inventory Cost Flow Assumptions

Eliminating entries apply to any cost flow assumption

Elimination of profit from beginning inventory assumes beginning inventory is sold and profit confirmed

But if beginning inventory is not sold, it appears in ending inventory and elimination of profit from ending inventory corrects that assumption

30

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Intercompany Transfers of Depreciable Assets

Intercompany gains and losses are confirmed when Asset is sold to an outside party or Asset depreciates

Portion of gain equal to excess depreciation is ‘confirmed’

Objectives of eliminations Eliminate the unconfirmed intercompany gain or loss Eliminate the difference between depreciation

expense recorded by purchasing entity and the amount based on original acquisition cost, i.e. excess depreciation

Restate the asset and accumulated depreciation accounts so that they are based on cost

31

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Eliminations in Year of Transfer for Depreciable Assets Example

On January 2, 2010, Jordan sells equipment with a 10-year remaining life and an original cost of $5 million to Parrish for $4,500,000. Accumulated depreciation on the transfer date was $2 million.

32

Jordan’s gain = $4,500,000 – ($5,000,000 – $2,000,000) = $1,500,000Parrish’s depreciation = $4,500,000/10 = $450,000

Balances on 2010 statements: Jordan ParrishBalance Sheet, December 31, 2010 Equipment (remaining on Parrish's books) $ - $4,500,000 Accumulated depreciation - 450,0002010 Income Statement Depreciation expense 450,000 Gain on sale of equipment 1,500,000 -

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Eliminations in Year of Transfer for Depreciable Assets Example continued

33

December 31, 2010 consolidation eliminating entries:

To eliminate unconfirmed gain on intercompany transfer of equipment:(I-1) Gain on sale of equipment 1,500,000

Equipment 1,500,000

(I-2) Accumulated depreciation 150,000 Depreciation expense 150,000

(I-3) Equipment 2,000,000 Accumulated depreciation 2,000,000

To eliminate the excess annual depreciation expense recorded by the purchasing affiliate: $1,500,000 ÷ 10 = $150,000

To restate the assets and accumulated depreciation accounts to their original acquisition cost basis. The amount of adjustment is equal to the accumulated depreciation at the date of transfer:

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Effects in Year of Transfer for Depreciable Assets

Effect of $1,500,000 unconfirmed gain on intercompany transfer of depreciable assets in year of transfer:

34

Equity in Net Income20% Noncontrolling

Interest in Net Income

Downstream transferSubtract $1,500,000

Add $150,000No effect

Upstream transferSubtract $1,200,000

Add $120,000Subtract $300,000

Add $30,000

The $1,500,000 unconfirmed gain as of the date of transfer is confirmed by reducing depreciation expense by $150,000 in each of

the asset’s 10 years of remaining life.

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

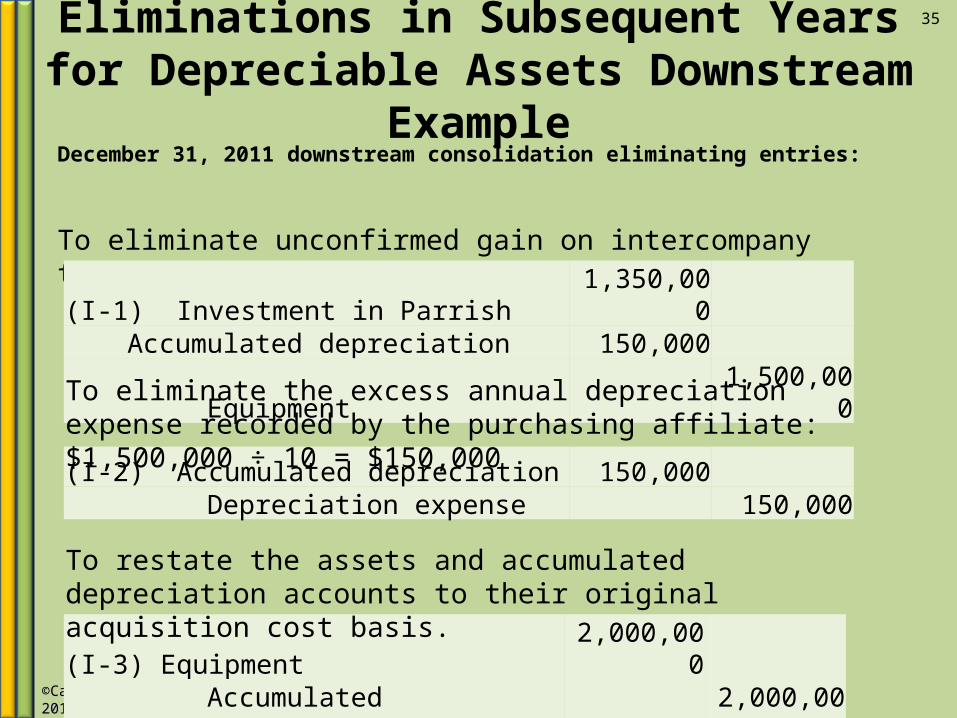

Eliminations in Subsequent Years for Depreciable Assets Downstream Example

35

December 31, 2011 downstream consolidation eliminating entries:

To eliminate unconfirmed gain on intercompany transfer of equipment:(I-1) Investment in Parrish 1,350,000

Accumulated depreciation 150,000 Equipment 1,500,000

(I-2) Accumulated depreciation 150,000 Depreciation expense 150,000

(I-3) Equipment 2,000,000 Accumulated depreciation 2,000,000

To eliminate the excess annual depreciation expense recorded by the purchasing affiliate: $1,500,000 ÷ 10 = $150,000

To restate the assets and accumulated depreciation accounts to their original acquisition cost basis.

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Eliminations in Subsequent Years for Depreciable Assets Upstream Example

36

December 31, 2011 upstream consolidation eliminating entries:

To eliminate unconfirmed gain on intercompany transfer of equipment:(I-1) Retained earnings, beg.- Parrish 1,350,000

Accumulated depreciation 150,000 Equipment 1,500,000

(I-2) Accumulated depreciation 150,000 Depreciation expense 150,000

(I-3) Equipment 2,000,000 Accumulated depreciation 2,000,000

To eliminate the excess annual depreciation expense recorded by the purchasing affiliate: $1,500,000 ÷ 10 = $150,000

To restate the assets and accumulated depreciation accounts to their original acquisition cost basis.

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Effects in Subsequent Years for Depreciable Assets

Effect of $1,500,000 unconfirmed gain on intercompany transfer of depreciable assets during the subsequent year, 2011:

37

Equity in Net Income20% Noncontrolling

Interest in Net Income

Downstream transfer Add $150,000 No effect

Upstream transfer Add $120,000 Add $30,000

The $1,500,000 unconfirmed gain as of the date of transfer is confirmed by reducing depreciation expense by

$150,000 in each of the asset’s 10 years of remaining life.

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Comprehensive IllustrationAdonis Corp. acquired 90% of the voting stock of Reelok Company, on January 2, 2007 at a cost of $27,830,000. Other data:

38

Reelock’s book value at date of acquisition $2,000,000Estimated fair value of noncontrolling interest 2,170,000Plant and equipment with 10-year remaining life undervalued by 7,000,000Long-term debt with a 4-year remaining term overvalued by 400,000Previously unreported identifiable intangibles: Order backlog with a 2-year life 1,000,000 Favorable leaseholds with a 5-year life 3,000,000

Calculation of goodwill:

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

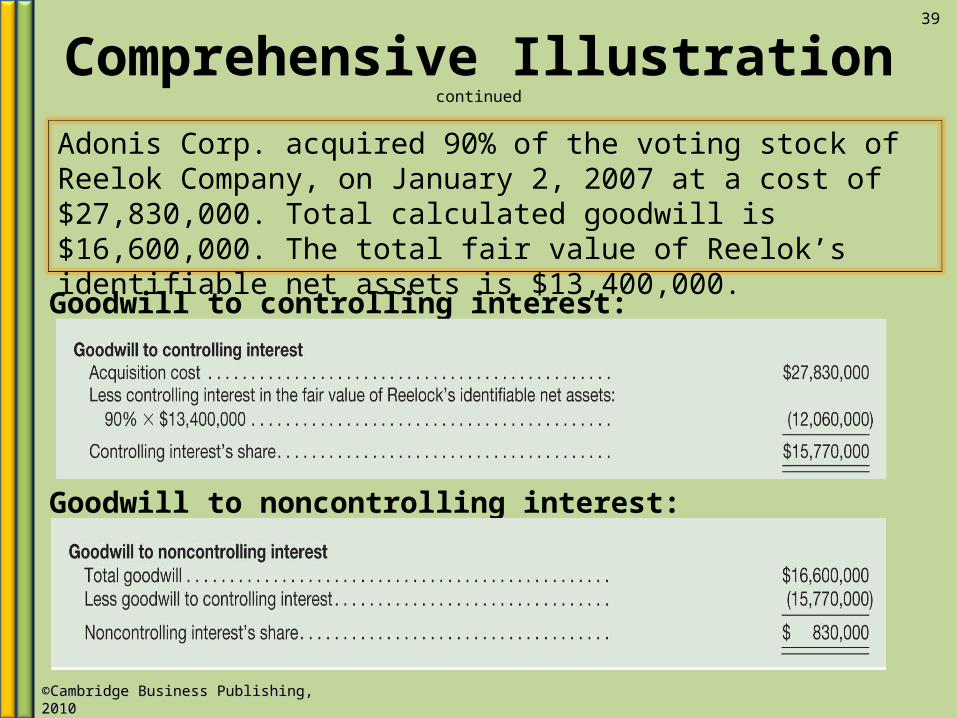

Comprehensive Illustration continued

Adonis Corp. acquired 90% of the voting stock of Reelok Company, on January 2, 2007 at a cost of $27,830,000. Total calculated goodwill is $16,600,000. The total fair value of Reelok’s identifiable net assets is $13,400,000.

39

Goodwill to controlling interest:

Goodwill to noncontrolling interest:

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Comprehensive Illustration continued

40

Adonis Corp.’s intercompany transactions during 2010:

Sale of land in 2008 costing $5 million by Reelock to Adonis for $5.5 million; Sale in 2010 by Adonis to outside firm for $6.5 millionReelock sells merchandise to Adonis at a 20% markup on sales. Adonis’ January 1, 2010 inventory balance includes $400,000 of merchandise purchased from Reelock, and its December 31, 2010 inventory includes $450,000 purchased from Reelock.

Equity in net income

$450,000

$72,000

($81,000)

Noncontrolling interest in net

income

$50,000

$8,000

($9,000)

Upstream

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

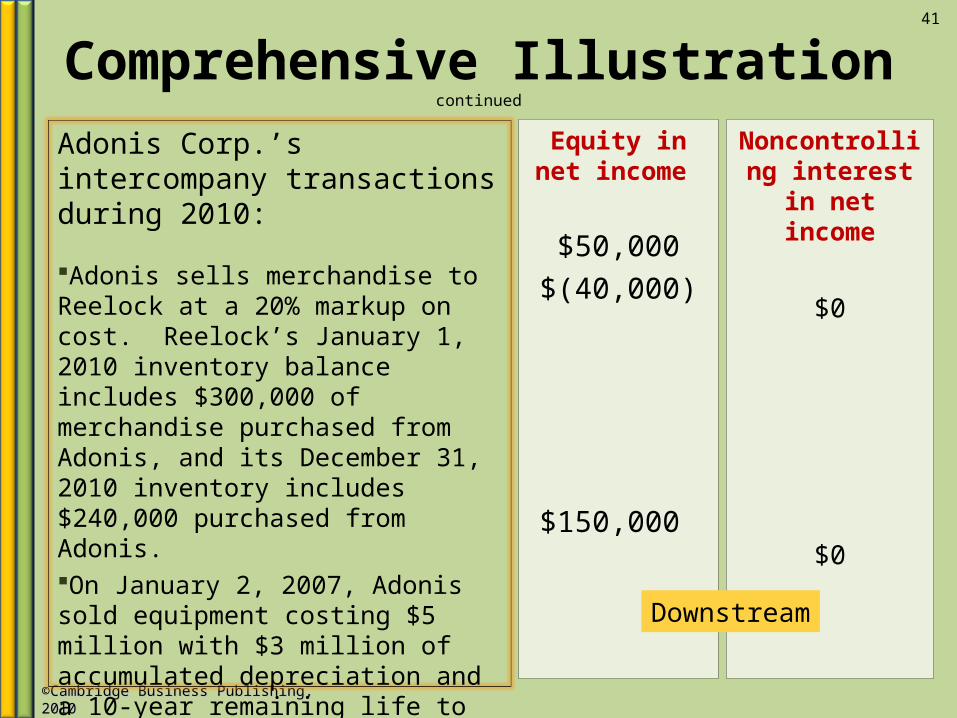

Comprehensive Illustration continued

41

Adonis Corp.’s intercompany transactions during 2010:

Adonis sells merchandise to Reelock at a 20% markup on cost. Reelock’s January 1, 2010 inventory balance includes $300,000 of merchandise purchased from Adonis, and its December 31, 2010 inventory includes $240,000 purchased from Adonis. On January 2, 2007, Adonis sold equipment costing $5 million with $3 million of accumulated depreciation and a 10-year remaining life to Reelock for $3.5 million. Reelock holds the equipment at year-end.

Equity in net income

$50,000

$(40,000)

$150,000

Noncontrolling interest in net

income

$0

$0

Downstream

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Comprehensive Illustration continued

Adonis Corp. acquired 90% of the voting stock of Reelok Company, on January 2, 2007 at a cost of $27,830,000. Total calculated goodwill is $16,600,000. Reelock’s reported income for 2010 is $2,000,000.

42

2010 Equity in net income and noncontrolling interest in income:

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Comprehensive Illustration continued

Elimination C

The equity in net income of Reelock, reported on Adonis’ books, totals $951,000. Reelock declared and paid no dividends in 2010.

43

To eliminate equity in net income on the parent's books and restore the investment account to its beginning-of-year value:

(C) Equity in income of Reelock 951,000 Investment in Reelock 951,000

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Comprehensive Illustration continued

Adjustments for Intercompany Transactions

44

To recognize the confirmed gain on the upstream land sales.

(I-1) Retained earnings, January 1 500,000 Gain on sale of land 500,000

In 2008, Reelock sold land costing $5 million to Adonis for $5.5 million. In 2010, Adonis sold the land to a real estate investment firm for $6.5 million.

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Comprehensive Illustration continued

Adjustments for Intercompany Transactions

Total 2010 retail sales by Reelock to Adonis were $3 million. Adonis’ January 1, 2010 inventory balance includes $400,000 in merchandise purchased from Reelock. Total 2010 retail sales by Adonis to Reelock were $2 million. Reelock sells to Adonis at a 20% markup on sales.

45

To eliminate intercompany sales and purchases: $3,000,000 + $2,000,000 = $5,000,000

(I-2) Sales revenue 5,000,000 Cost of goods sold 5,000,000

To recognize the confirmed upstream profit in beginning inventory: $400,000 × 20% = $80,000(I-3) Retained Earnings, January 1 80,000

Cost of goods sold 80,000

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Comprehensive Illustration continued

Adjustments for Intercompany TransactionsAdonis sells to Reelock at a 20% markup on cost. Reelock’s January 1, 2010 inventory includes $300,000 in merchandise purchased from Adonis.

46

To recognize the confirmed downstream profit in beginning inventory: $300,000 – ($300,000 ÷ 1.2) = $50,000

(I-4) Investment in Reelock 50,000

Cost of goods sold 50,000

(I-5) Cost of goods sold 130,000 Current assets 130,000

To eliminate the unconfirmed upstream and downstream profit in ending inventory: ($450,000 × 20%) + ($240,000 – ($240,000/1.2)) = $130,000

Reelock’s December 31, 2010 inventory includes $240,000 purchasedfrom Adonis (20% markup on cost). Adonis’ December 31, 2010 inventory includes $450,000 purchased from Reelock (20% markup on sales).

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Comprehensive Illustration continued

Adjustments for Intercompany Transactions

On January 2, 2007, Adonis sold equipment costing $5 million with $3 million accumulated depreciation, and a 10-year remaining life, straight-line, to Reelock for $3.5 million. Reelock still holds the equipment at year-end.

47

(I-6) Investment in Reelock 1,050,000 Accumulated depreciation 450,000

Plant and equipment 1,500,000

To remove the unconfirmed beginning-of-year profit on downstream sale of equipment: Total gain = $3,500,000 – ($5,000,000 - $3,000,000) = $1,500,000 Unconfirmed gain = $1,500,000 – [($1,500,000 ÷ 10) × 3 years] = $1,050,000

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Comprehensive Illustration continued

Adjustments for Intercompany Transactions

On January 2, 2007, Adonis sold equipment costing $5 million with $3 million accumulated depreciation, and a 10-year remaining life, straight-line, to Reelock for $3.5 million. Reelock still holds the equipment at year-end.

48

(I-7) Accumulated depreciation 150,000 Operating expenses 150,000

To recognize the confirmed profit (excess depreciation) on downstream sale of equipment: $1,500,000 ÷ 10 = $150,000

(I-8) Plant and equipment 3,000,000 Accumulated depreciation 3,000,000

To restate the asset and accumulated depreciation accounts to their original acquisition cost basis:

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Comprehensive Illustration continued

Adjustments for Intercompany Transactions

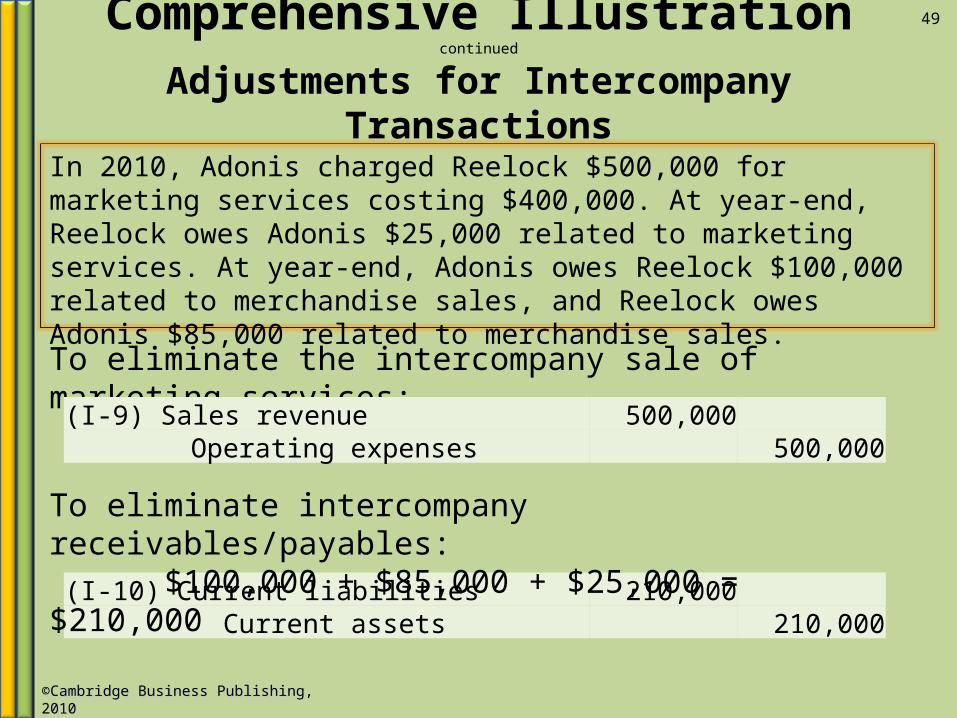

In 2010, Adonis charged Reelock $500,000 for marketing services costing $400,000. At year-end, Reelock owes Adonis $25,000 related to marketing services. At year-end, Adonis owes Reelock $100,000 related to merchandise sales, and Reelock owes Adonis $85,000 related to merchandise sales.

49

To eliminate the intercompany sale of marketing services:

(I-9) Sales revenue 500,000 Operating expenses 500,000

(I-10) Current liabilities 210,000 Current assets 210,000

To eliminate intercompany receivables/payables: $100,000 + $85,000 + $25,000 = $210,000

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Comprehensive Illustration continued

Elimination E

Reelock’s January 1, 2010 capital stock balance was $1,400,000 and its retained earnings was $8,600,000. Entry I-1 reduced Reelock’s retained earnings by $500,000 and entry I-3 reduced it by $80,000.

50

To eliminate the subsidiary's beginning-of-year capital stock account and the remainder of its beginning retained earnings account against the beginning-of-year book value portion of the investment account, and recognize the beginning-of-year book value of the noncontrolling interest: $8,600,000 – $500,000 – $80,000 = $8,020,000

(E) Capital stock 1,400,000 Retained earnings, January 1 8,020,000

Investment in Reelock (90%) 8,478,000 Noncontrolling interest in Reelock (10%) 942,000

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Comprehensive Illustration continued

Elimination R

Reelock’s assets and liabilities were fairly reported except for plant and equipment undervalued by $7 million; long-term debt overvalued by $400,000; and previously unreported identifiable intangibles: order backlog for $1 million and favorable leaseholds for $3 million. Accumulated goodwill impairment for 2007-2009 was $1 million.

51

To revalue Reelock's net assets as of the beginning of the year and allocate the revaluations to the controlling interest: ($7,000,000 + $1,200,000 + $100,000 – $2,100,000) = $6,200,000 (90% × $6,200,000) + (95% × $15,600,000) = $20,400,000 (10% × $6,200,000) + (5% × $15,600,000) = $1,400,000

(R) Plant and equipment 7,000,000 Identifiable intangibles 1,200,000 Long-term debt 100,000 Goodwill 15,600,000

Accumulated depreciation 2,100,000Investment in Reelock 20,400,000Noncontrolling interest in Reelock 1,400,000

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Comprehensive Illustration continued

Elimination O

Reelock’s assets and liabilities were fairly reported except for plant and equipment undervalued by $7 million; long-term debt overvalued by $400,000; and previously unreported identifiable intangibles: order backlog for $1 million and favorable leaseholds for $3 million. Goodwill impairment is $200,000 for 2010.

52

To write off the revaluations for the current year: $7,000,000 ÷ 10 = $700,000 $3,000,000 ÷ 5 = $600,000 $400,000 ÷ 4 = $100,000

(O) Operating expenses 1,600,000 Accumulated depreciation 700,000Identifiable intangibles 600,000Long-term debt 100,000Goodwill 200,000

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Comprehensive Illustration continued

Elimination N

The noncontrolling interest in Reelock’s net income for 2010 is $99,000. Reelock declared and paid no dividends in 2010.

53

To recognize the noncontrolling interest in the subsidiary's income:

(N) Noncontrolling interest in net income 99,000 Noncontrolling interest in Reelock 99,000

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Comprehensive Illustration continued

Consolidation Working Paper, December 31, 2010

54

Exhibit 6.1

©Cambridge Business Publishing, 2010©Cambridge Business Publishing, 2010

Comprehensive Illustration continued

Consolidated Balance Sheet, Dec. 31, 2010

55