12566217552161_Call Centers in India BPO Companies in India Call Centres in India

Call Center/BPO Industry in Colombia

May 2009

1. Call Center/BPO Industry in Colombia

• Competitive Operational Cost• Human Resources• Industry Maturity• Infrastructure• Business Environment

2. Services to investors

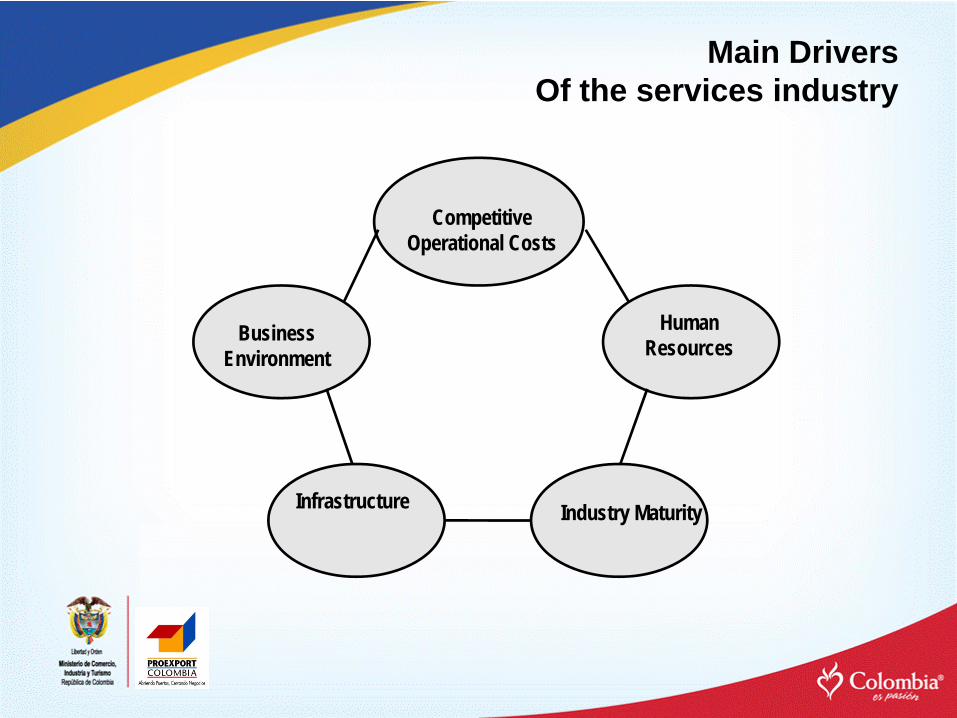

Main DriversOf the services industry

Human Resources Business

Environment

Industry MaturityInfrastructure

Competitive Operational Costs

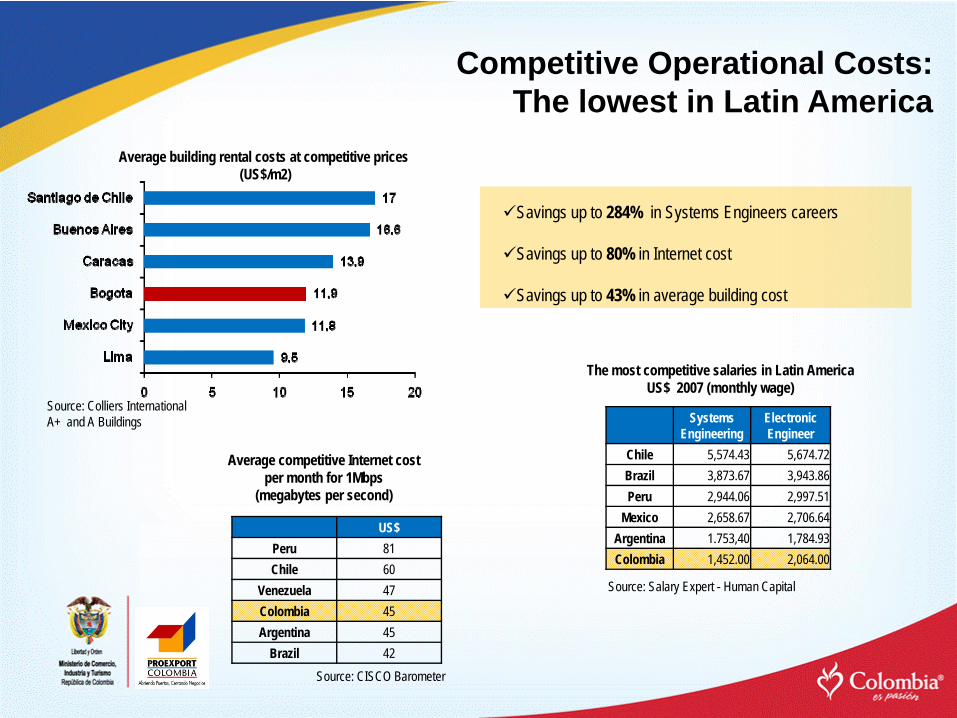

Savings up to 284% in Systems Engineers careers

Savings up to 80% in Internet cost

Savings up to 43% in average building cost

The most competitive salaries in Latin AmericaUS$ 2007 (monthly wage)

Source: Salary Expert - Human Capital

Average building rental costs at competitive prices (US$/m2)

Source: Colliers InternationalA+ and A Buildings

Average competitive Internet cost per month for 1Mbps

(megabytes per second)

Source: CISCO Barometer

Systems Engineering

Electronic Engineer

Chile 5,574.43 5,674.72Brazil 3,873.67 3,943.86Peru 2,944.06 2,997.51

Mexico 2,658.67 2,706.64Argentina 1.753,40 1,784.93Colombia 1,452.00 2,064.00

US$Peru 81Chile 60

Venezuela 47Colombia 45Argentina 45

Brazil 42

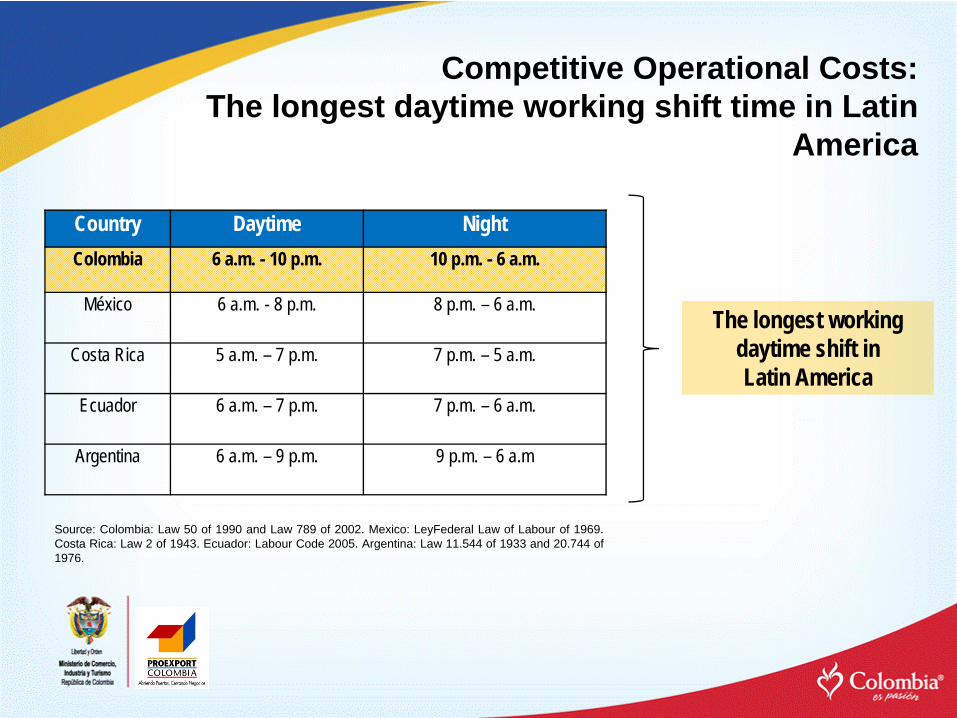

Competitive Operational Costs:The lowest in Latin America

Country Daytime NightColombia 6 a.m. - 10 p.m. 10 p.m. - 6 a.m.

México 6 a.m. - 8 p.m. 8 p.m. – 6 a.m.

Costa Rica 5 a.m. – 7 p.m. 7 p.m. – 5 a.m.

Ecuador 6 a.m. – 7 p.m. 7 p.m. – 6 a.m.

Argentina 6 a.m. – 9 p.m. 9 p.m. – 6 a.m

The longest working daytime shift in Latin America

Competitive Operational Costs: The longest daytime working shift time in Latin

America

Source: Colombia: Law 50 of 1990 and Law 789 of 2002. Mexico: LeyFederal Law of Labour of 1969.Costa Rica: Law 2 of 1943. Ecuador: Labour Code 2005. Argentina: Law 11.544 of 1933 and 20.744 of1976.

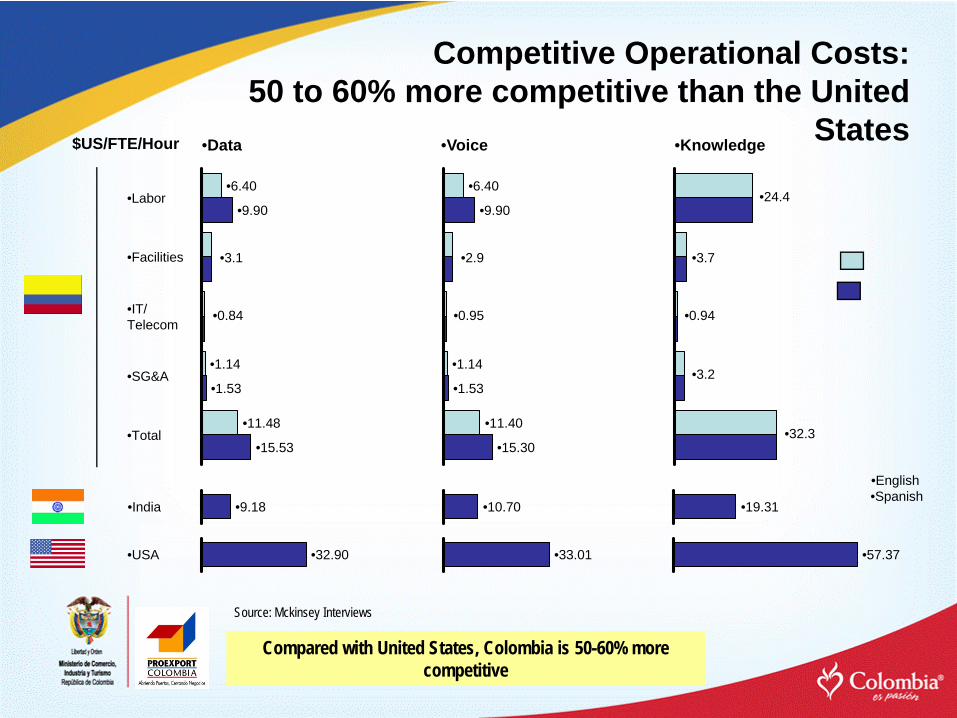

Competitive Operational Costs:50 to 60% more competitive than the United

States

Compared with United States, Colombia is 50-60% more competitive

Source: Mckinsey Interviews

•Data •Voice •Knowledge

•15.53

•1.53

•9.90

•6.40•Labor

•Facilities

•IT/Telecom

•1.14•SG&A

•11.48•Total

•32.90•USA

•9.18•India

•15.30

•1.53

•9.90

•6.40

•1.14

•11.40

•33.01

•10.70

•57.37

•19.31•Spanish•English

•3.1

•0.84

•2.9

•0.95

•3.7

•0.94

$US/FTE/Hour

•24.4

•3.2

•32.3

Source: Manpower

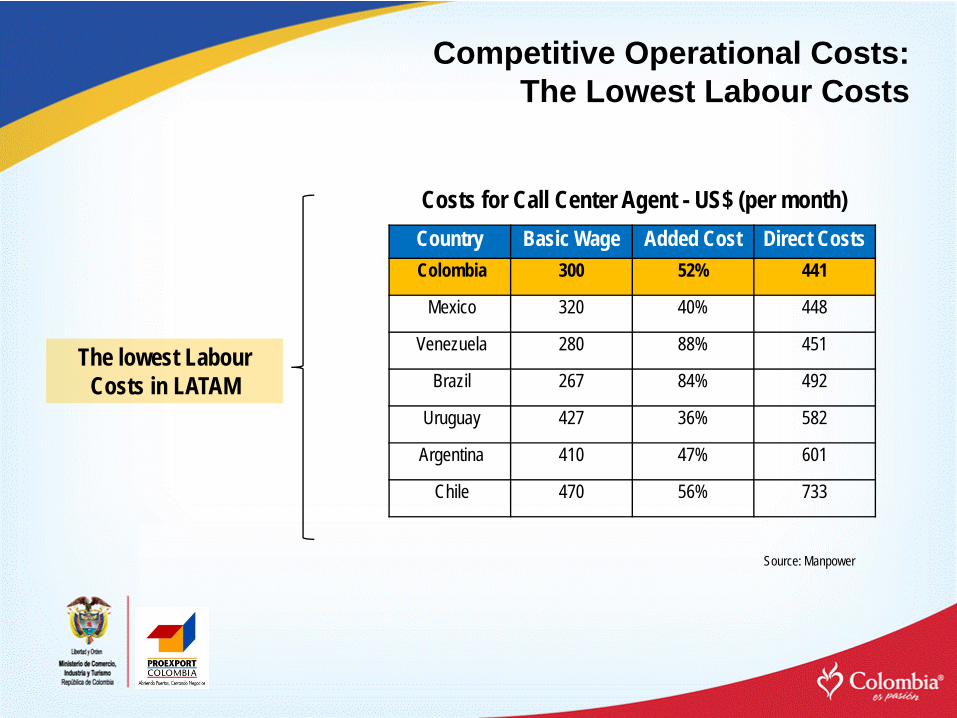

Costs for Call Center Agent - US$ (per month)

The lowest Labour Costs in LATAM

Country Basic Wage Added Cost Direct Costs Colombia 300 52% 441

Mexico 320 40% 448

Venezuela 280 88% 451

Brazil 267 84% 492

Uruguay 427 36% 582

Argentina 410 47% 601

Chile 470 56% 733

Competitive Operational Costs:The Lowest Labour Costs

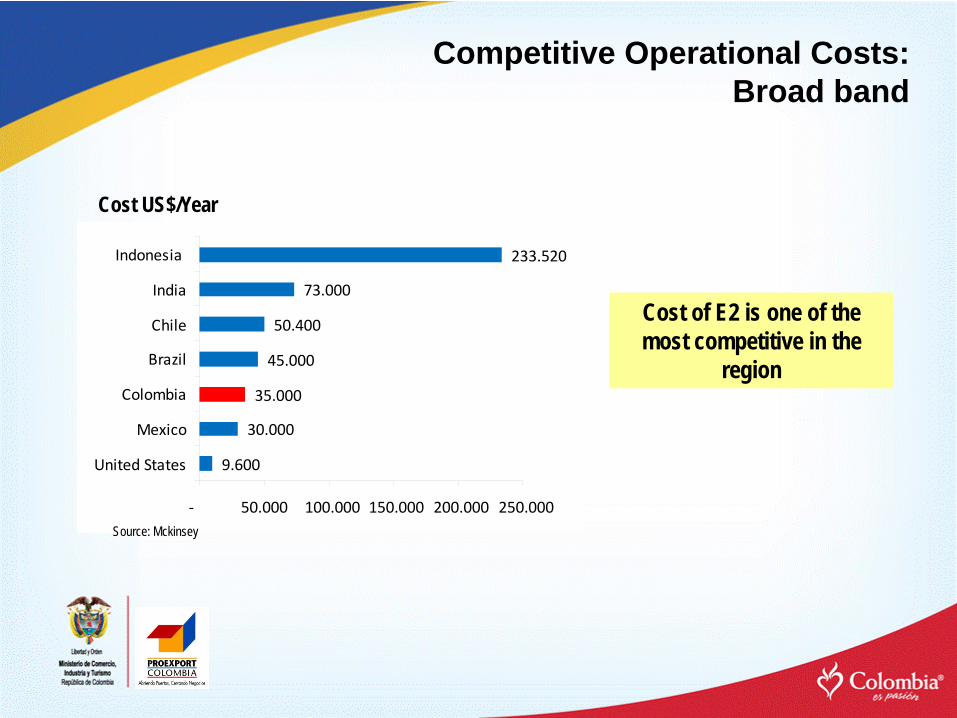

Competitive Operational Costs:Broad band

9.600

30.000

35.000

45.000

50.400

73.000

233.520

‐ 50.000 100.000 150.000 200.000 250.000

United States

Mexico

Colombia

Brazil

Chile

India

Indonesia

Cost of E2 is one of the most competitive in the

region

Cost US$/Year

Source: Mckinsey

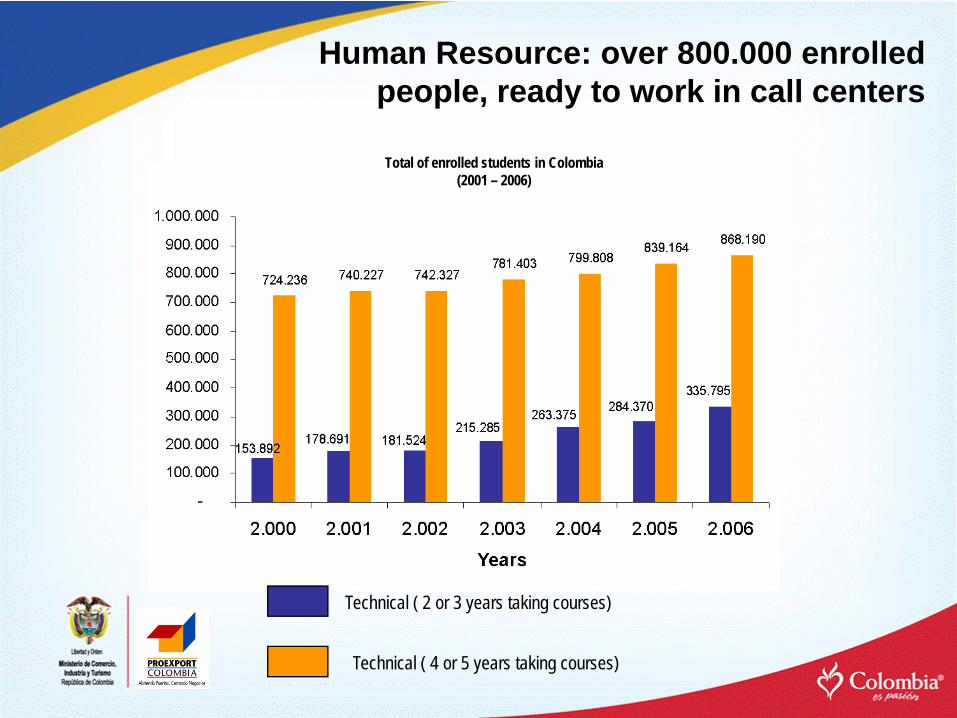

Total of enrolled students in Colombia(2001 – 2006)

Technical ( 2 or 3 years taking courses)

Technical ( 4 or 5 years taking courses)

Human Resource: over 800.000 enrolled people, ready to work in call centers

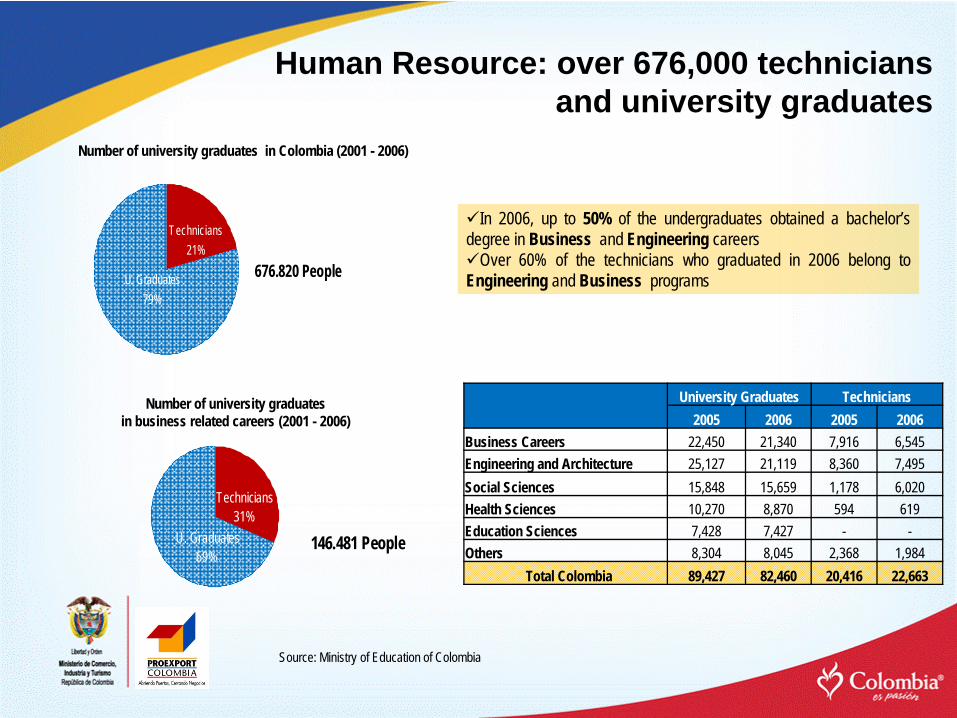

Human Resource: over 676,000 technicians and university graduates

Number of university graduates in Colombia (2001 - 2006)

In 2006, up to 50% of the undergraduates obtained a bachelor’sdegree in Business and Engineering careers

Over 60% of the technicians who graduated in 2006 belong toEngineering and Business programs

Source: Ministry of Education of Colombia

Number of university graduates in business related careers (2001 - 2006)

University Graduates Technicians2005 2006 2005 2006

Business Careers 22,450 21,340 7,916 6,545Engineering and Architecture 25,127 21,119 8,360 7,495Social Sciences 15,848 15,659 1,178 6,020Health Sciences 10,270 8,870 594 619Education Sciences 7,428 7,427 - -Others 8,304 8,045 2,368 1,984

Total Colombia 89,427 82,460 20,416 22,663

U. Graduates 79%

Technicians 21%

676.820 People

Technicians 31%

U. Graduates 69%

146.481 People

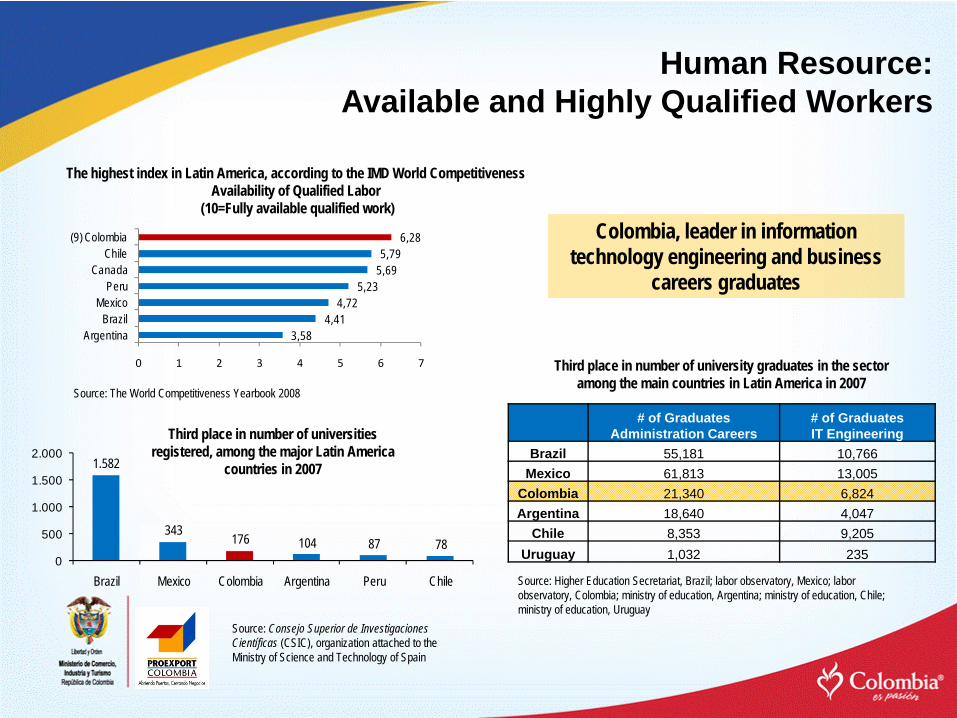

Human Resource:Available and Highly Qualified Workers

3,584,41

4,725,23

5,695,79

6,28

0 1 2 3 4 5 6 7

ArgentinaBrazil

MexicoPeru

CanadaChile

(9) Colombia

1.582

343 176 104 87 780

500

1.000

1.500

2.000

Brazil Mexico Colombia Argentina Peru Chile

Third place in number of universities registered, among the major Latin America

countries in 2007

Source: Consejo Superior de Investigaciones Científicas (CSIC), organization attached to the Ministry of Science and Technology of Spain

Source: The World Competitiveness Yearbook 2008

# of GraduatesAdministration Careers

# of GraduatesIT Engineering

Brazil 55,181 10,766Mexico 61,813 13,005

Colombia 21,340 6,824Argentina 18,640 4,047

Chile 8,353 9,205Uruguay 1,032 235

Source: Higher Education Secretariat, Brazil; labor observatory, Mexico; labor observatory, Colombia; ministry of education, Argentina; ministry of education, Chile; ministry of education, Uruguay

The highest index in Latin America, according to the IMD World CompetitivenessAvailability of Qualified Labor

(10=Fully available qualified work) Colombia, leader in information

technology engineering and business careers graduates

Third place in number of university graduates in the sector among the main countries in Latin America in 2007

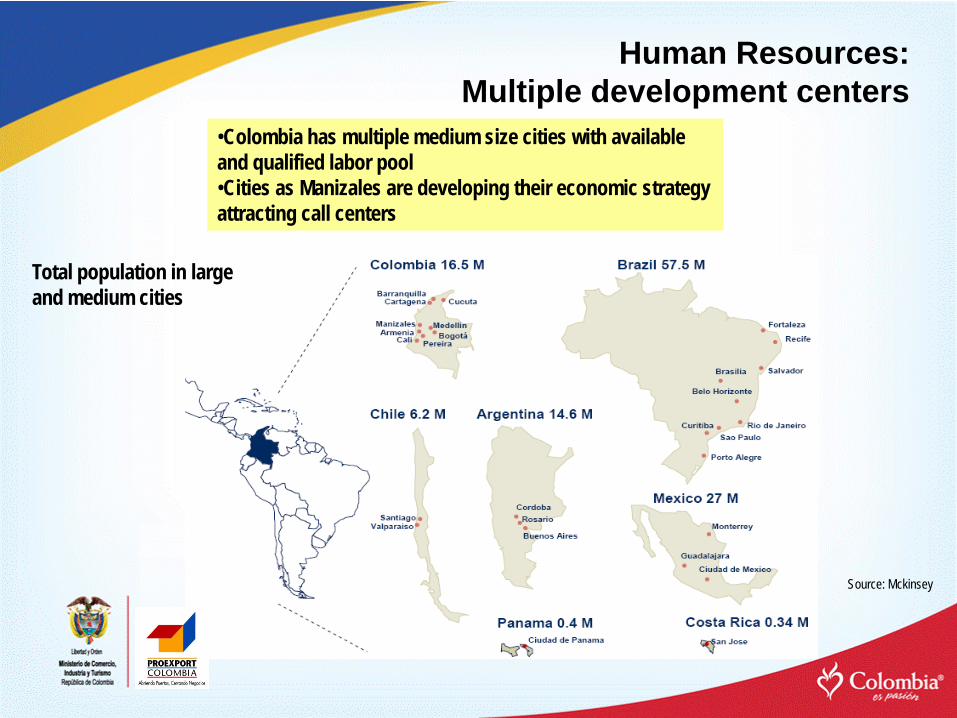

Human Resources:Multiple development centers

•Colombia has multiple medium size cities with available and qualified labor pool•Cities as Manizales are developing their economic strategy attracting call centers

Source: Mckinsey

Total population in large and medium cities

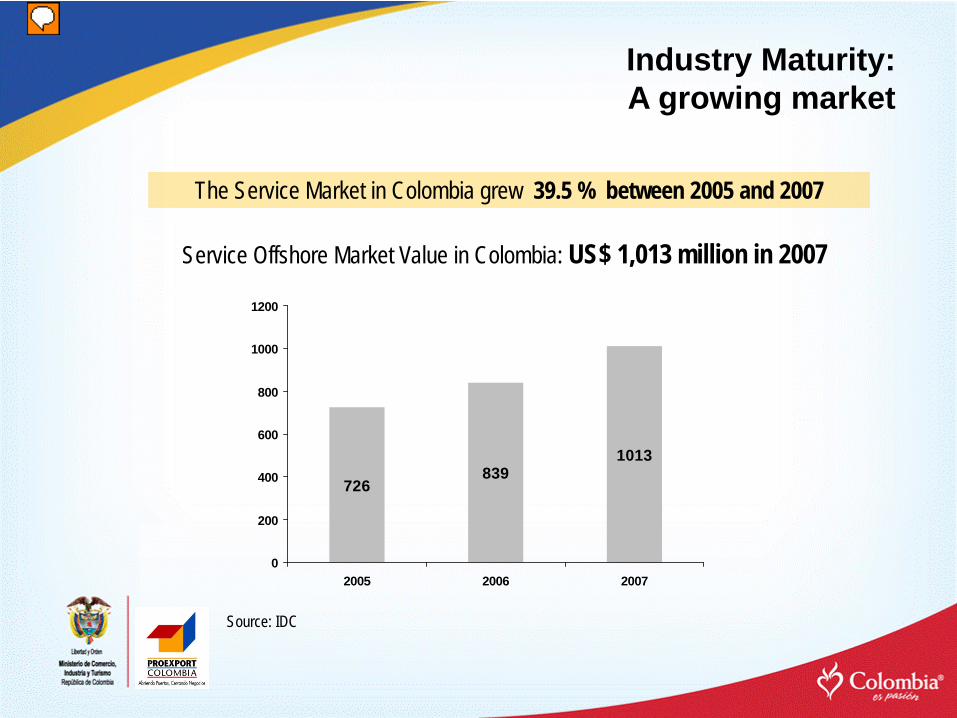

The Service Market in Colombia grew 39.5 % between 2005 and 2007

Industry Maturity:A growing market

Service Offshore Market Value in Colombia: US$ 1,013 million in 2007

Source: IDC

726839

1013

0

200

400

600

800

1000

1200

2005 2006 2007

Source: IDC

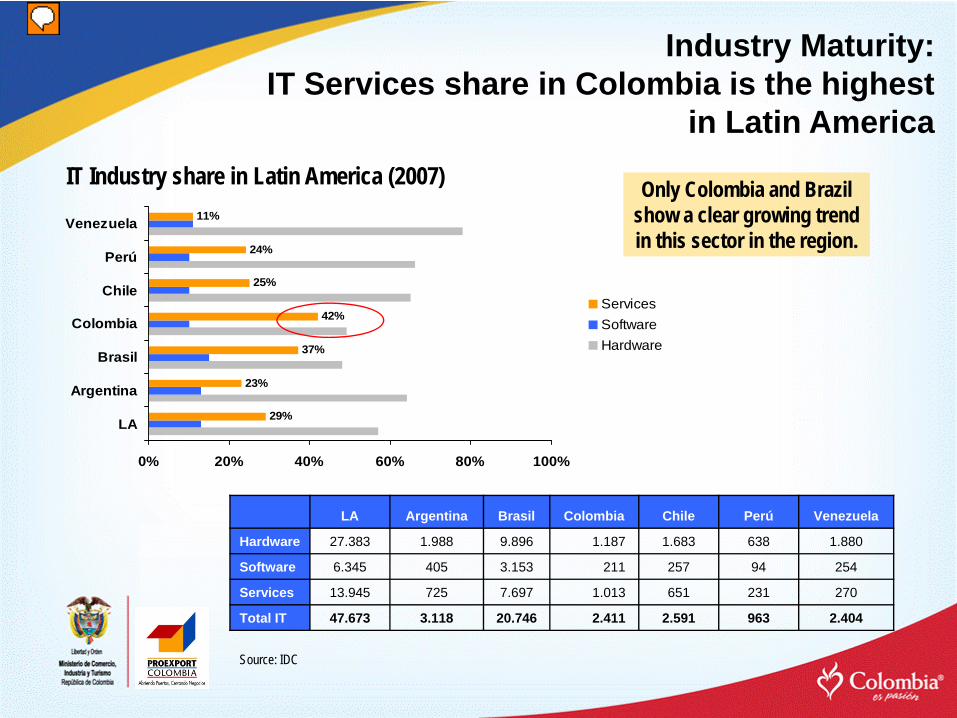

Only Colombia and Brazil show a clear growing trend in this sector in the region.

IT Industry share in Latin America (2007)

Industry Maturity:IT Services share in Colombia is the highest

in Latin America

29%

23%

37%

42%

25%

24%

11%

0% 20% 40% 60% 80% 100%

LA

Argentina

Brasil

Colombia

Chile

Perú

Venezuela

ServicesSoftwareHardware

LA Argentina Brasil Colombia Chile Perú Venezuela

Hardware 27.383 1.988 9.896 1.187 1.683 638 1.880

Software 6.345 405 3.153 211 257 94 254

Services 13.945 725 7.697 1.013 651 231 270

Total IT 47.673 3.118 20.746 2.411 2.591 963 2.404

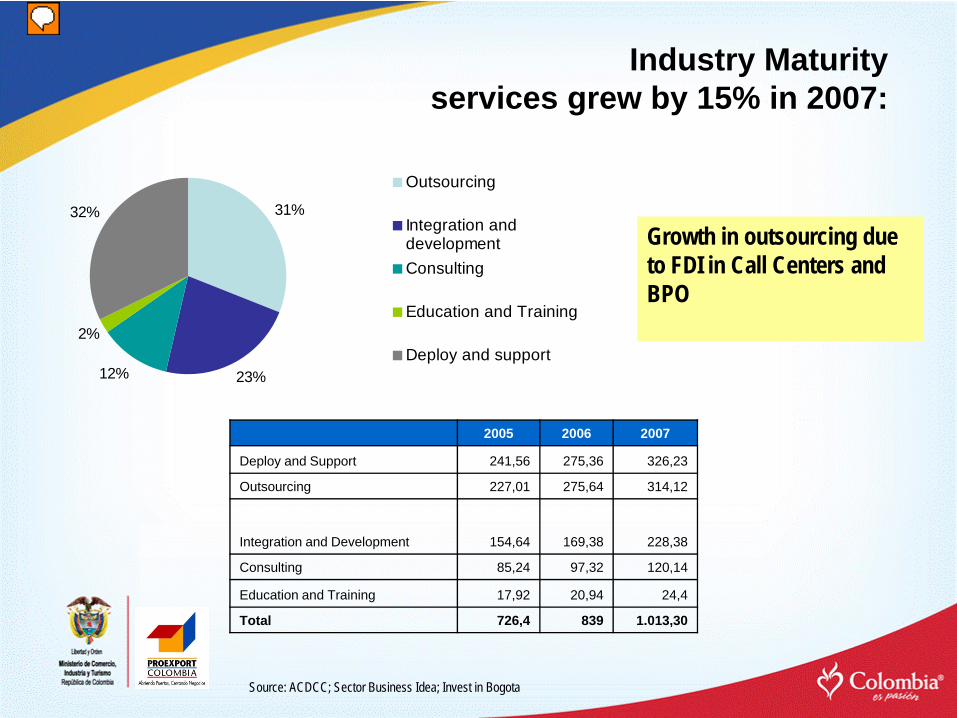

Growth in outsourcing due to FDI in Call Centers and BPO

Industry Maturityservices grew by 15% in 2007:

Source: ACDCC; Sector Business Idea; Invest in Bogota

31%

23%12%

2%

32%

Outsourcing

Integration anddevelopmentConsulting

Education and Training

Deploy and support

2005 2006 2007

Deploy and Support 241,56 275,36 326,23

Outsourcing 227,01 275,64 314,12

Integration and Development 154,64 169,38 228,38

Consulting 85,24 97,32 120,14

Education and Training 17,92 20,94 24,4

Total 726,4 839 1.013,30

Source: ACDCC; Sector Business Idea; Invest in Bogota

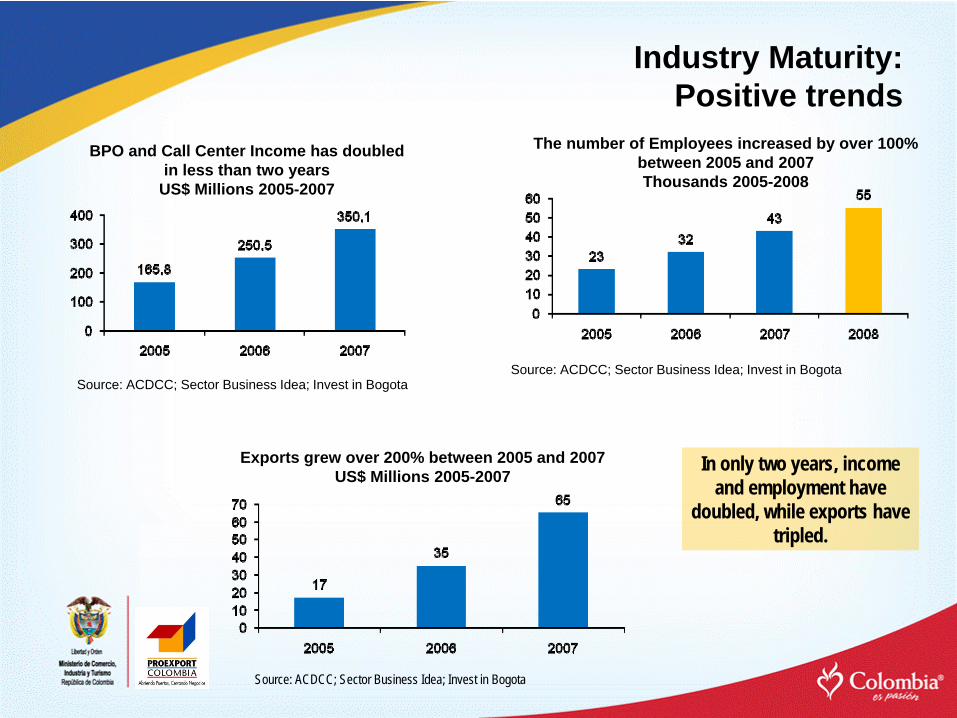

BPO and Call Center Income has doubledin less than two years

US$ Millions 2005-2007

The number of Employees increased by over 100% between 2005 and 2007Thousands 2005-2008

Exports grew over 200% between 2005 and 2007US$ Millions 2005-2007

Source: ACDCC; Sector Business Idea; Invest in Bogota

Source: ACDCC; Sector Business Idea; Invest in Bogota

In only two years, income and employment have

doubled, while exports have tripled.

Industry Maturity:Positive trends

Source: CCIT

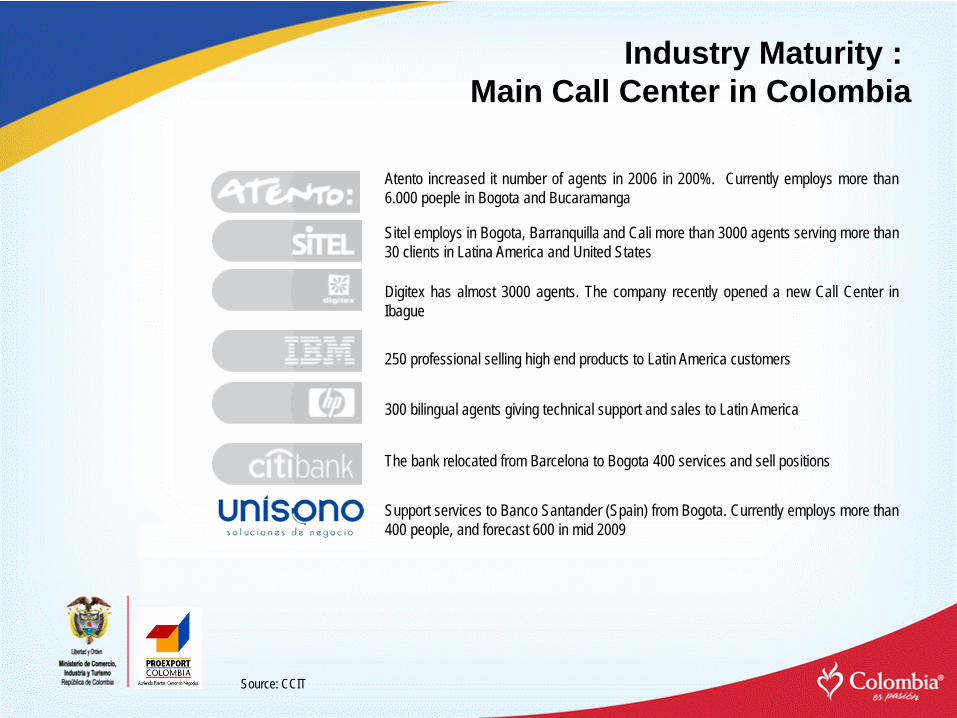

Industry Maturity : Main Call Center in Colombia

Atento increased it number of agents in 2006 in 200%. Currently employs more than6.000 poeple in Bogota and Bucaramanga

Sitel employs in Bogota, Barranquilla and Cali more than 3000 agents serving more than30 clients in Latina America and United States

Digitex has almost 3000 agents. The company recently opened a new Call Center inIbague

250 professional selling high end products to Latin America customers

300 bilingual agents giving technical support and sales to Latin America

The bank relocated from Barcelona to Bogota 400 services and sell positions

Support services to Banco Santander (Spain) from Bogota. Currently employs more than400 people, and forecast 600 in mid 2009

Source: CCIT

Industry Maturity : Main Service’s companies

The Spanish multinational supplier of technology for the travel and tourismindustry, has opened an operation in Bogota to source the Americas

From Bogota, the U.S. firm begins to provide design services for its globalcustomers.

Since 1986, the pioneer in the world of outsourcing in Bogota serves awide range of companies from different sectors.

Since 2002, this Mexican multinational IT service provider is present inBogota with its third largest operation in America.

In Bogota this multinational expands its global footprint in response to localcustomers.

Launched recently operation center in Bogota, which plans to increase itspresence in Latin America and improve the level of customer satisfactiontoday.

From Bogota, 200 consultants providing IT services to America at theCenter for Managed Services largest multinational in this region.

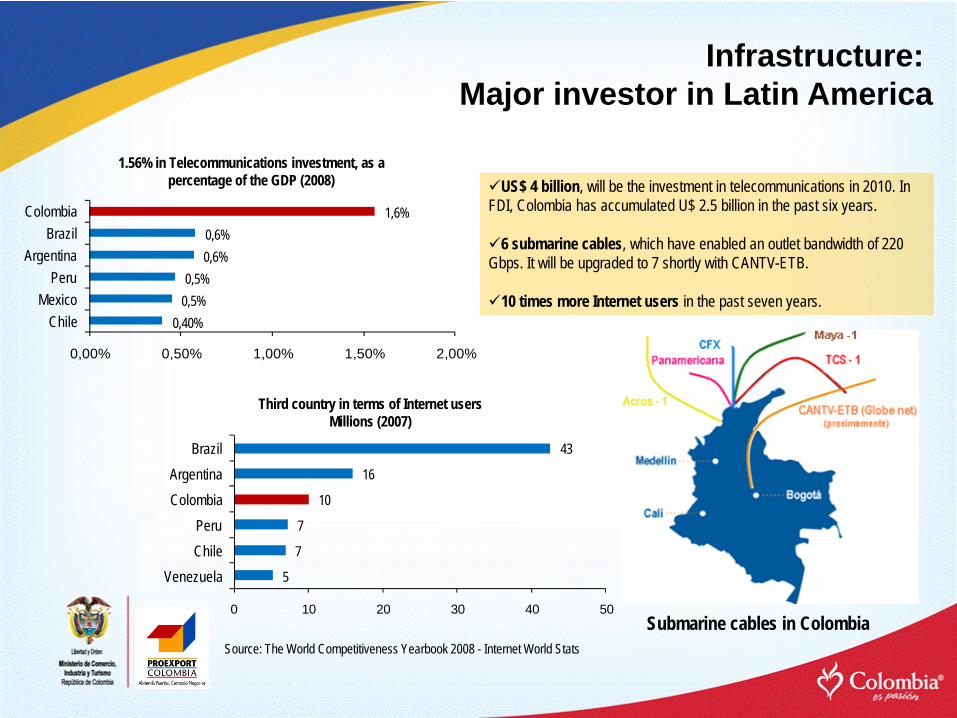

Infrastructure: Major investor in Latin America

Source: The World Competitiveness Yearbook 2008 - Internet World Stats

1.56% in Telecommunications investment, as a percentage of the GDP (2008) US$ 4 billion, will be the investment in telecommunications in 2010. In

FDI, Colombia has accumulated U$ 2.5 billion in the past six years.

6 submarine cables, which have enabled an outlet bandwidth of 220 Gbps. It will be upgraded to 7 shortly with CANTV-ETB.

10 times more Internet users in the past seven years.

5

7

7

10

16

43

0 10 20 30 40 50

VenezuelaChilePeru

ColombiaArgentina

Brazil

0,40%0,5%0,5%

0,6%0,6%

1,6%

0,00% 0,50% 1,00% 1,50% 2,00%

ChileMexico

PeruArgentina

BrazilColombia

Third country in terms of Internet usersMillions (2007)

Submarine cables in Colombia

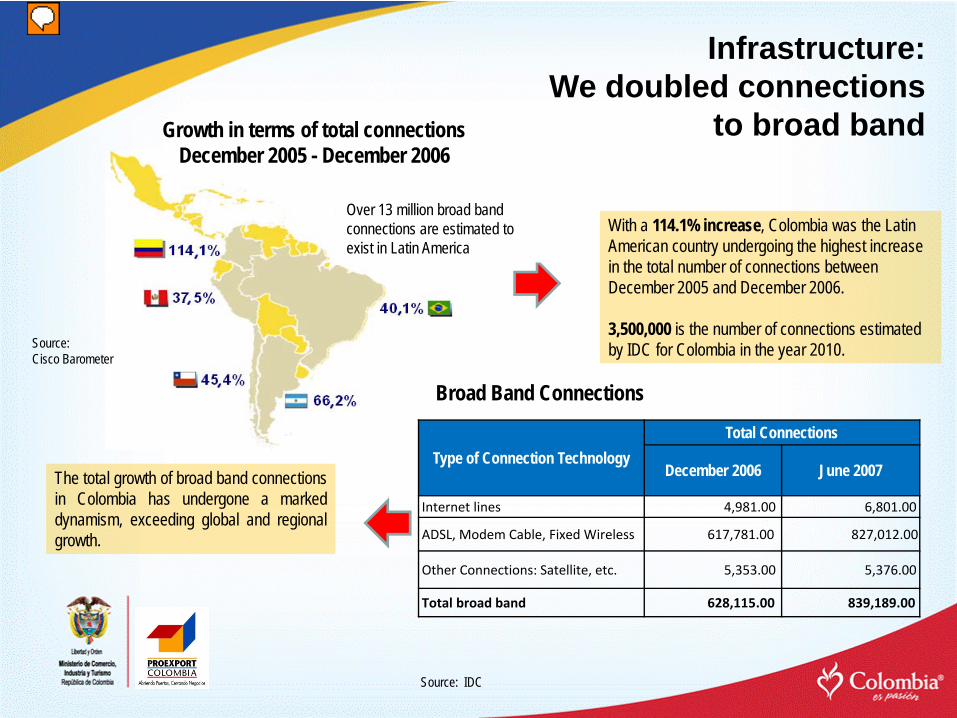

The total growth of broad band connectionsin Colombia has undergone a markeddynamism, exceeding global and regionalgrowth.

With a 114.1% increase, Colombia was the Latin American country undergoing the highest increase in the total number of connections between December 2005 and December 2006.

3,500,000 is the number of connections estimated by IDC for Colombia in the year 2010.

Source: IDC

Source: Cisco Barometer

Growth in terms of total connections December 2005 - December 2006

Infrastructure:We doubled connections

to broad band

Broad Band Connections

Type of Connection TechnologyTotal Connections

December 2006 June 2007

Internet lines 4,981.00 6,801.00

ADSL, Modem Cable, Fixed Wireless 617,781.00 827,012.00

Other Connections: Satellite, etc. 5,353.00 5,376.00

Total broad band 628,115.00 839,189.00

Over 13 million broad band connections are estimated to exist in Latin America

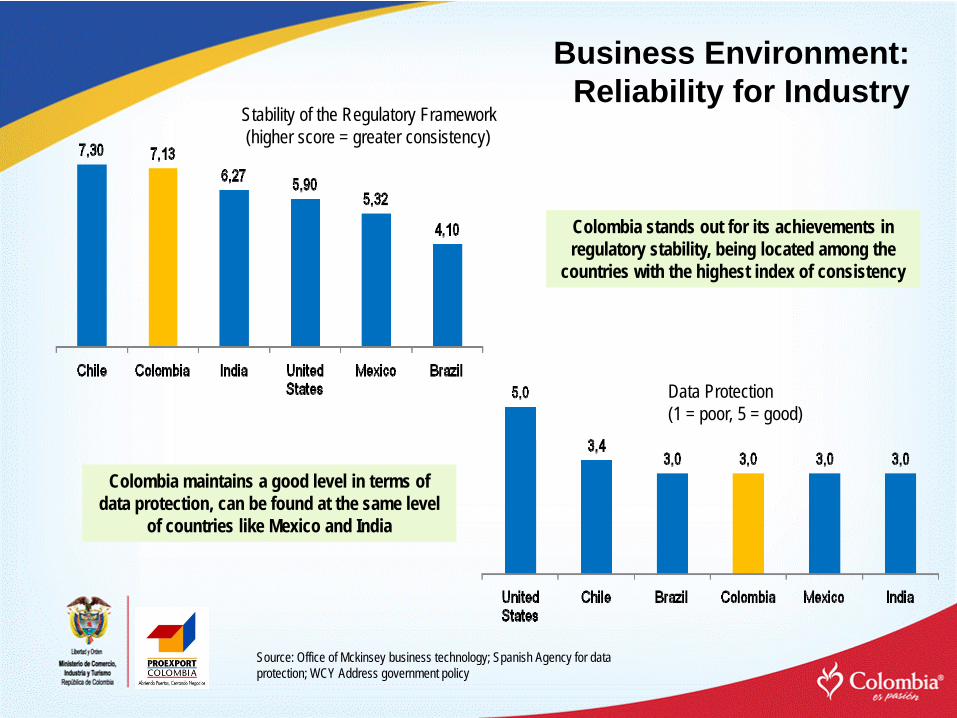

Business Environment:Reliability for Industry

Stability of the Regulatory Framework (higher score = greater consistency)

Data Protection (1 = poor, 5 = good)

Source: Office of Mckinsey business technology; Spanish Agency for data protection; WCY Address government policy

Colombia stands out for its achievements in regulatory stability, being located among the

countries with the highest index of consistency

Colombia maintains a good level in terms of data protection, can be found at the same level

of countries like Mexico and India

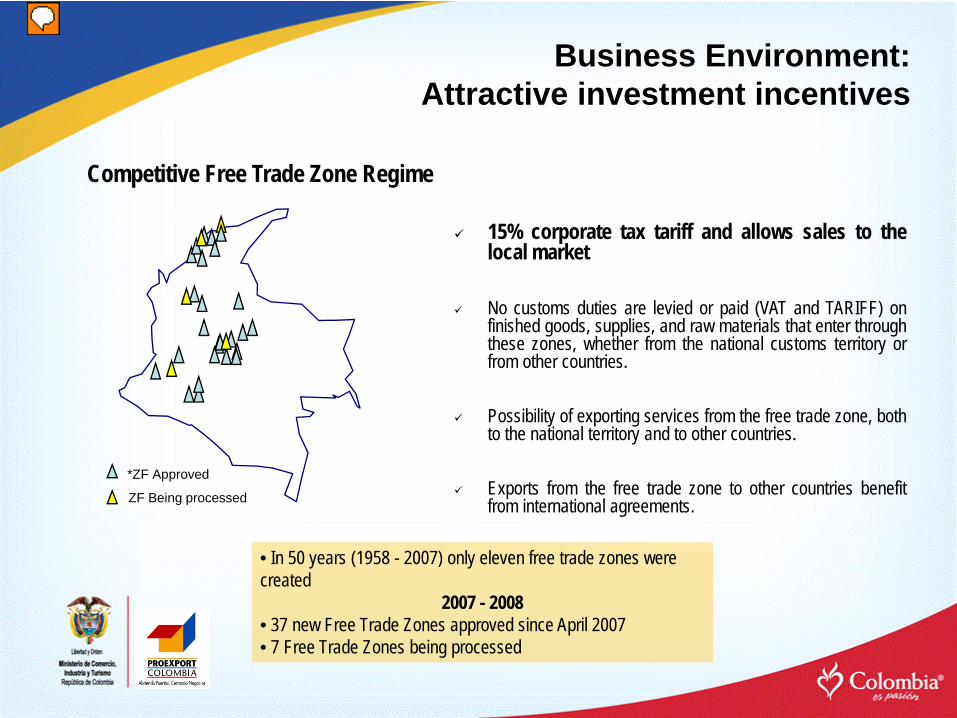

ZF Being processed

*ZF Approved

15% corporate tax tariff and allows sales to thelocal market

No customs duties are levied or paid (VAT and TARIFF) onfinished goods, supplies, and raw materials that enter throughthese zones, whether from the national customs territory orfrom other countries.

Possibility of exporting services from the free trade zone, bothto the national territory and to other countries.

Exports from the free trade zone to other countries benefitfrom international agreements.

Competitive Free Trade Zone Regime

• In 50 years (1958 - 2007) only eleven free trade zones were created

2007 - 2008• 37 new Free Trade Zones approved since April 2007• 7 Free Trade Zones being processed

Business Environment:Attractive investment incentives

VAT Exemption for Services provided abroad• The service exports from Colombia can be exempt of the VAT if they meet the following

requirements:– The service is provided from Colombia.– The service is provided to a consumer (company) that has no type of operation within

Colombia.– Register the service provision agreement before the Colombian Industry, Commerce

and Tourism Ministry.

Business Environment:Attractive investment incentives

• This tax benefit allows the investor to import capital goods that will be used to export services, with complete or partial exemption of custom duties and postpone the payment of VAT.

• This tax benefit requires that the investor exports 150% of the FOB value of the productive assets imported under the Especial Import – Export Mechanism.

• The investor must provide an insurance policy or global bank guaranty o 20% of the FOB value of the productive assets imported under the Plan.

Business Environment:Attractive investment incentives

Special Import – Export Mechanism

• The services related with research and technology that can apply to the tax benefit are the following:

– Computer services and other related– Research and development services – Telecommunication Services

• The Division of Especial Programs will approve or reject the “Especial Import – Export Mechanism” tax benefit program within 10 days from the filing of the application and will notify the applicant.

• Colombia through the Law 170 of 1994, adopted the Agreement that created the World Trade Organization WTO and with it the General Agreement on Trade in Services (GATS).

Special Import – Export Mechanism

Business Environment:Attractive investment incentives

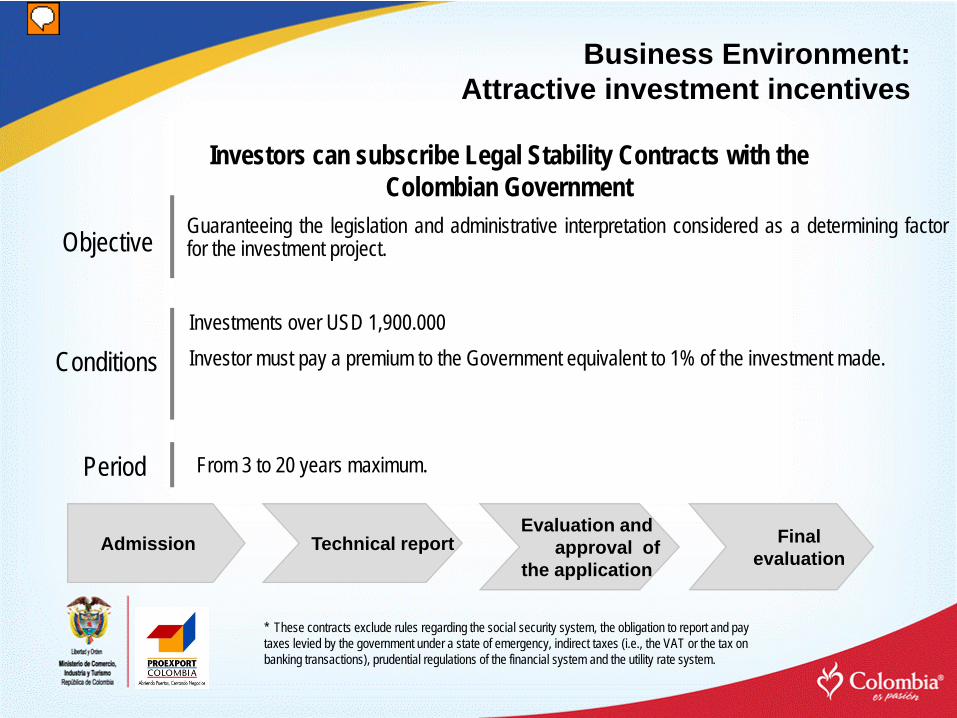

Investments over USD 1,900.000Investor must pay a premium to the Government equivalent to 1% of the investment made.

* These contracts exclude rules regarding the social security system, the obligation to report and pay taxes levied by the government under a state of emergency, indirect taxes (i.e., the VAT or the tax on banking transactions), prudential regulations of the financial system and the utility rate system.

Period

Admission Technical reportEvaluation and

approval of the application

Final evaluation

Objective Guaranteeing the legislation and administrative interpretation considered as a determining factorfor the investment project.

Conditions

From 3 to 20 years maximum.

Investors can subscribe Legal Stability Contracts with the Colombian Government

Business Environment:Attractive investment incentives

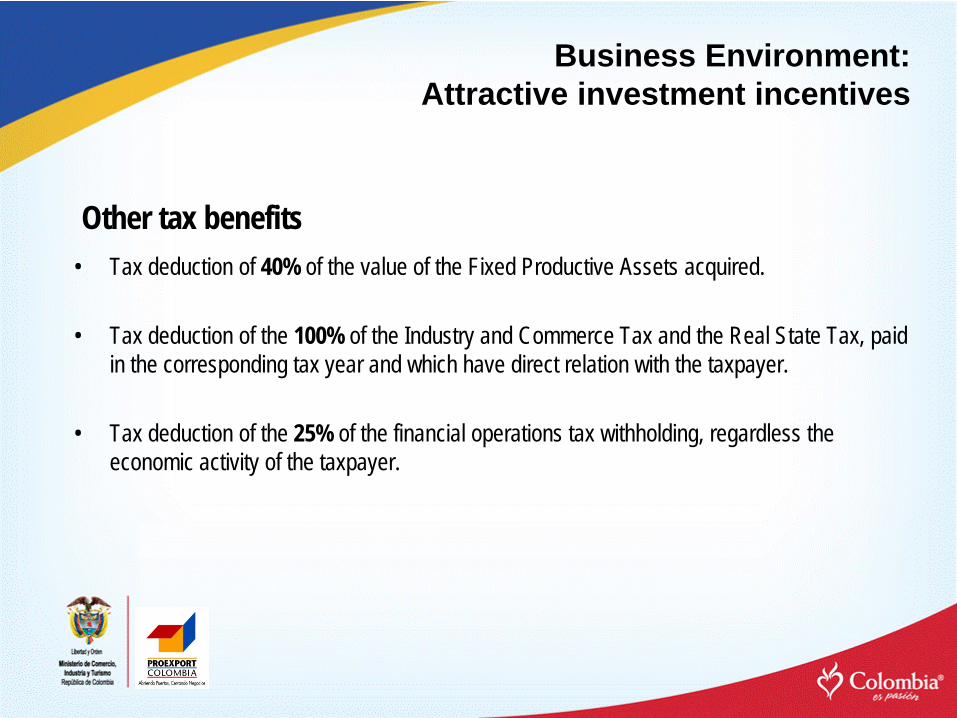

• Tax deduction of 40% of the value of the Fixed Productive Assets acquired.

• Tax deduction of the 100% of the Industry and Commerce Tax and the Real State Tax, paid in the corresponding tax year and which have direct relation with the taxpayer.

• Tax deduction of the 25% of the financial operations tax withholding, regardless the economic activity of the taxpayer.

Other tax benefits

Business Environment:Attractive investment incentives

Success StoryCITIBANK

“The talent, preparation and skills for customer service that distinguishes Colombians, have been fundamental for us to feel comfortable to move

our customer service and collection operations to Colombia” Sergio de Horna, Citibank President Spain

• From Bogotá, Citibank shared services operation provides:– Outbound

• Collection • Product sales

– Inbound• Product support for clients• Customer service

• Provides services to 12 different countries• Overall Citibank's operation employees over 2.000 people

Success StoryUNISONO - SANTANDER

“"Colombia is one of the countries with big potential due to it’s economic growth, labor cost and government support to the sector. Now we have an

additional motivation: We are special trade zone”Ana Isabel Iglesias, Unisono President Colombia

• From Bogotá, Unisono provides services for Banco Santander (Spain) with more than 600 agents who attend corporative and customers from Spain.

• Outsourcing of sales and customer service operation

Key qualitative factors in IT Services

• Service oriented people• Macroeconomic and political stability better than other countries in Latin America• Neutral accent

WHY COLOMBIA• Cheaper than Mexico• Better service attitude than Argentina• Is not saturated as Costa Rica or Uruguay

Competitive Operational Cost

Human Resource

Industry Maturity

Infrastructure

Business Environment

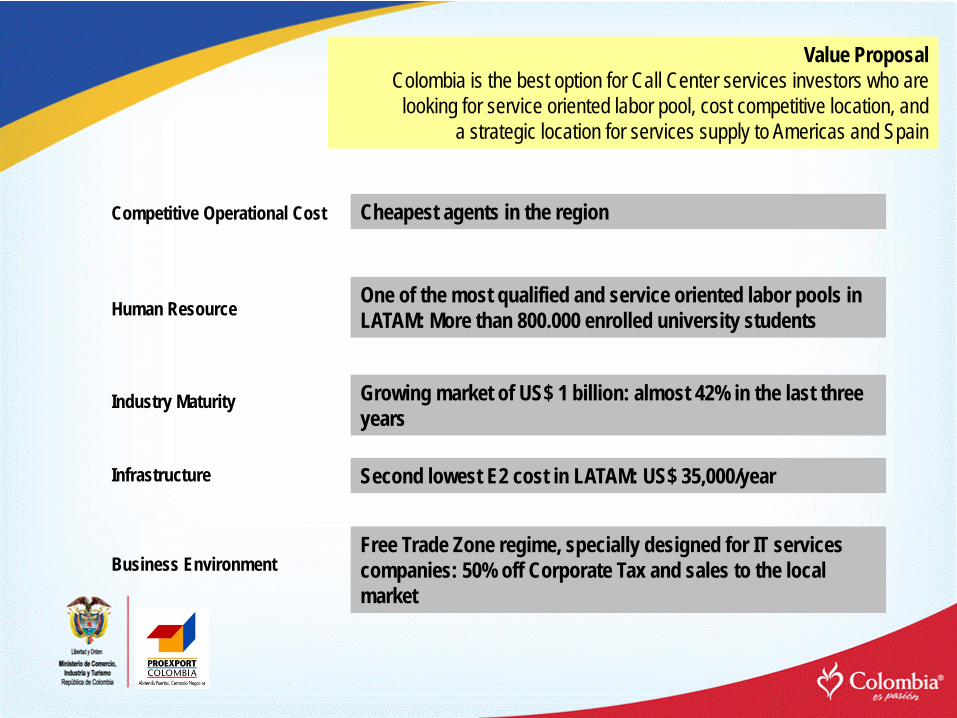

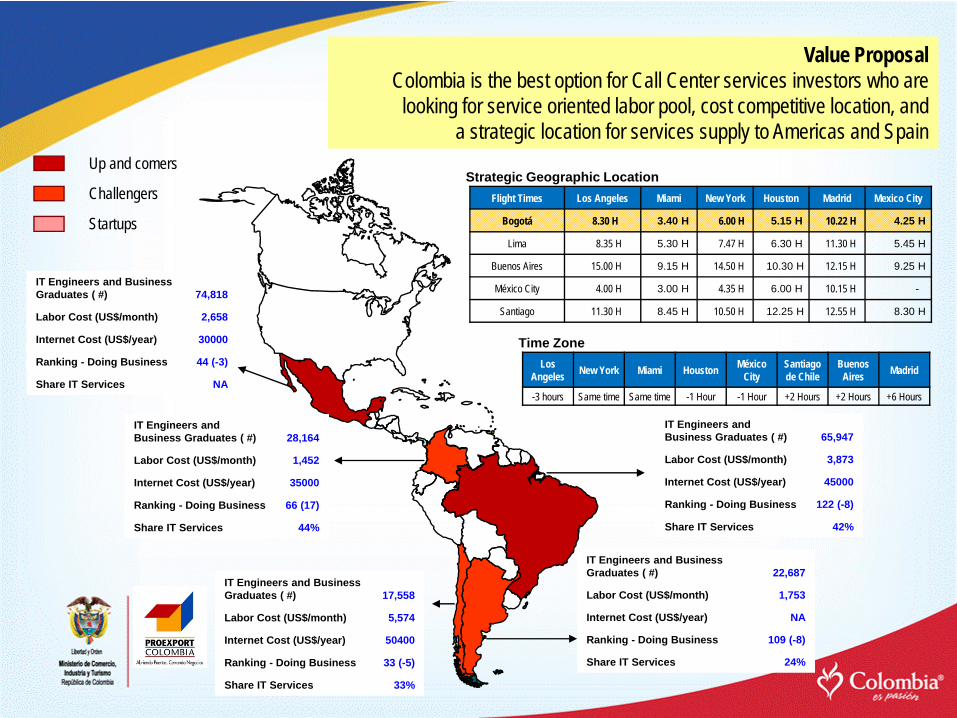

Value Proposal Colombia is the best option for Call Center services investors who are

looking for service oriented labor pool, cost competitive location, and a strategic location for services supply to Americas and Spain

One of the most qualified and service oriented labor pools in LATAM: More than 800.000 enrolled university students

Cheapest agents in the region

Growing market of US$ 1 billion: almost 42% in the last three years

Second lowest E2 cost in LATAM: US$ 35,000/year

Free Trade Zone regime, specially designed for IT services companies: 50% off Corporate Tax and sales to the local market

Flight Times Los Angeles Miami New York Houston Madrid Mexico City

Bogotá 8.30 H 3.40 H 6.00 H 5.15 H 10.22 H 4.25 H

Lima 8.35 H 5.30 H 7.47 H 6.30 H 11.30 H 5.45 H

Buenos Aires 15.00 H 9.15 H 14.50 H 10.30 H 12.15 H 9.25 H

México City 4.00 H 3.00 H 4.35 H 6.00 H 10.15 H -

Santiago 11.30 H 8.45 H 10.50 H 12.25 H 12.55 H 8.30 H

Los Angeles New York Miami Houston México

CitySantiago de Chile

Buenos Aires Madrid

-3 hours Same time Same time -1 Hour -1 Hour +2 Hours +2 Hours +6 Hours

Time Zone

Strategic Geographic Location

IT Engineers and Business Graduates ( #) 28,164

Labor Cost (US$/month) 1,452

Internet Cost (US$/year) 35000

Ranking - Doing Business 66 (17)

Share IT Services 44%

IT Engineers and Business Graduates ( #) 74,818

Labor Cost (US$/month) 2,658

Internet Cost (US$/year) 30000

Ranking - Doing Business 44 (-3)

Share IT Services NA

IT Engineers and Business Graduates ( #) 22,687

Labor Cost (US$/month) 1,753

Internet Cost (US$/year) NA

Ranking - Doing Business 109 (-8)

Share IT Services 24%

IT Engineers and Business Graduates ( #) 65,947

Labor Cost (US$/month) 3,873

Internet Cost (US$/year) 45000

Ranking - Doing Business 122 (-8)

Share IT Services 42%

IT Engineers and Business Graduates ( #) 17,558

Labor Cost (US$/month) 5,574

Internet Cost (US$/year) 50400

Ranking - Doing Business 33 (-5)

Share IT Services 33%

Challengers

Up and comers

Startups

Value Proposal Colombia is the best option for Call Center services investors who are

looking for service oriented labor pool, cost competitive location, and a strategic location for services supply to Americas and Spain

1. Call Center/BPO Industry in Colombia

• Competitive Operational Cost• Human Resources• Industry Maturity• Infrastructure• Business Environment

2. Services to investors

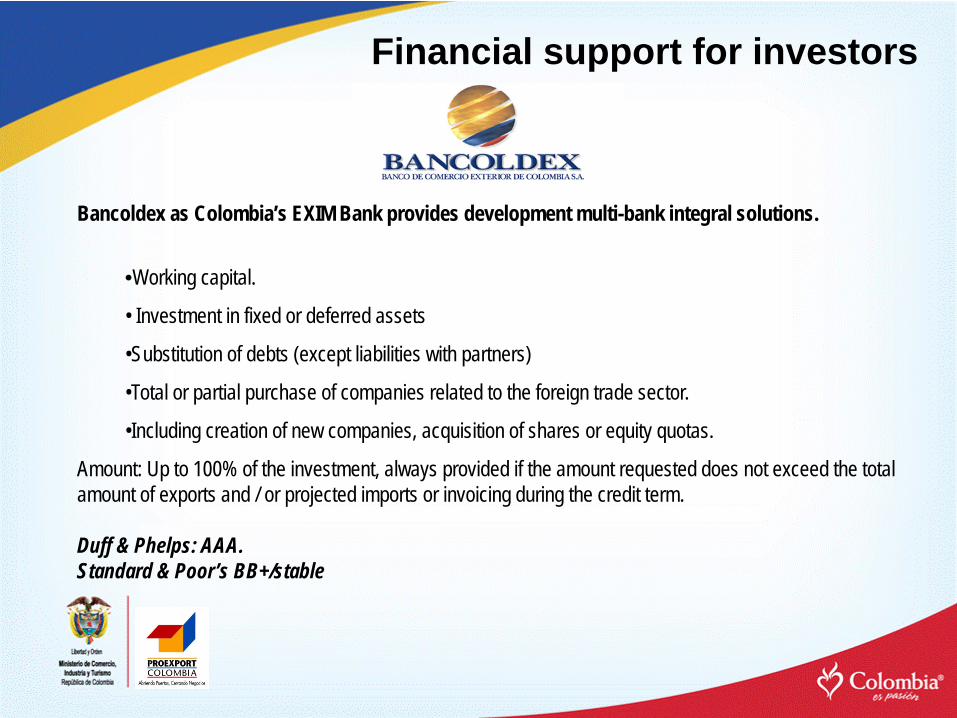

Bancoldex as Colombia’s EXIM Bank provides development multi-bank integral solutions.

•Working capital.

• Investment in fixed or deferred assets

•Substitution of debts (except liabilities with partners)

•Total or partial purchase of companies related to the foreign trade sector.

•Including creation of new companies, acquisition of shares or equity quotas.

Amount: Up to 100% of the investment, always provided if the amount requested does not exceed the total amount of exports and / or projected imports or invoicing during the credit term.

Duff & Phelps: AAA.Standard & Poor’s BB+/stable

Financial support for investors

Tailor made information request

Contacts with public and private sectors

Set up of agendas when investors decide to visit to Colombia

Aftercare services for investors that are already established in the country

Assessment and improvement of business climate

Proexport: Investment Promotion Agency offers world class services to

foreign investors

Proxeport’s overseas offices