California, USA October 2009cesonoma.ucdavis.edu/files/27763.pdf · Olive oil storage Vertical...

20

1 ‘Australia’s premier olive company’ Introduction to Olive Oil Production Olive Oil Processing Course California, USA ‐ October 2009 • Public unlisted company. • Established in 1997. • 85 shareholders, 110 employees. • Head Office Based in Lara, Vic. • Australia’s leading vertically integrated olive oil company.

Transcript of California, USA October 2009cesonoma.ucdavis.edu/files/27763.pdf · Olive oil storage Vertical...

1

‘Australia’s premier olive company’

Introduction to Olive Oil Production

Olive Oil Processing Courseg

California, USA ‐ October 2009

• Public unlisted company.

• Established in 1997.

• 85 shareholders, 110 employees.

• Head Office Based in Lara, Vic.

• Australia’s leading vertically

integrated olive oil company.

2

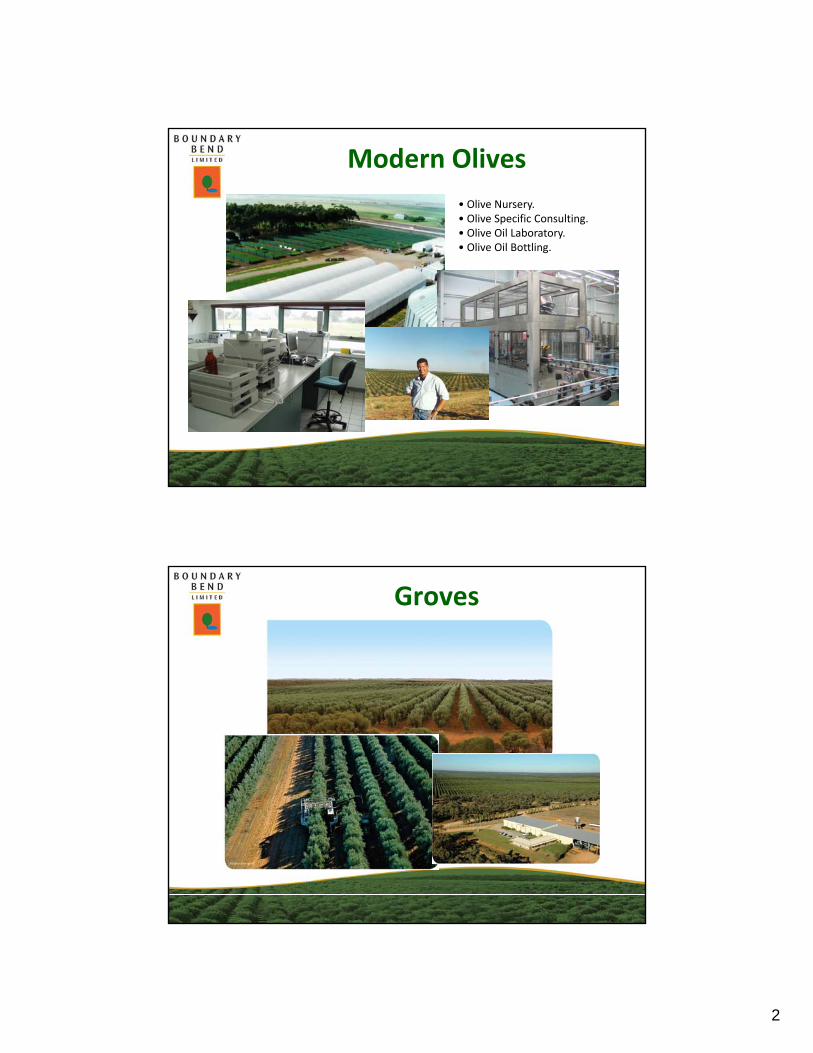

Modern Olives• Olive Nursery.• Olive Specific Consulting.• Olive Oil Laboratory.• Olive Oil Bottling• Olive Oil Bottling.

Groves

3

Production

Processing & Marketing

4

What is olive oil?

Olive oil is the oil obtained solely from the fruit of the olive tree (Olea europaea L.), to the exclusion of oils obtained using solvents or re‐esterification processes and of any mixturesolvents or re esterification processes and of any mixture

with oils of other kinds.

Transversal view of an oliveDetail of cells in the olive flesh

What is olive oil?

Olive Oil CompositionSaponifiable

mattermatter98.5%

Minor components

1.5%

5

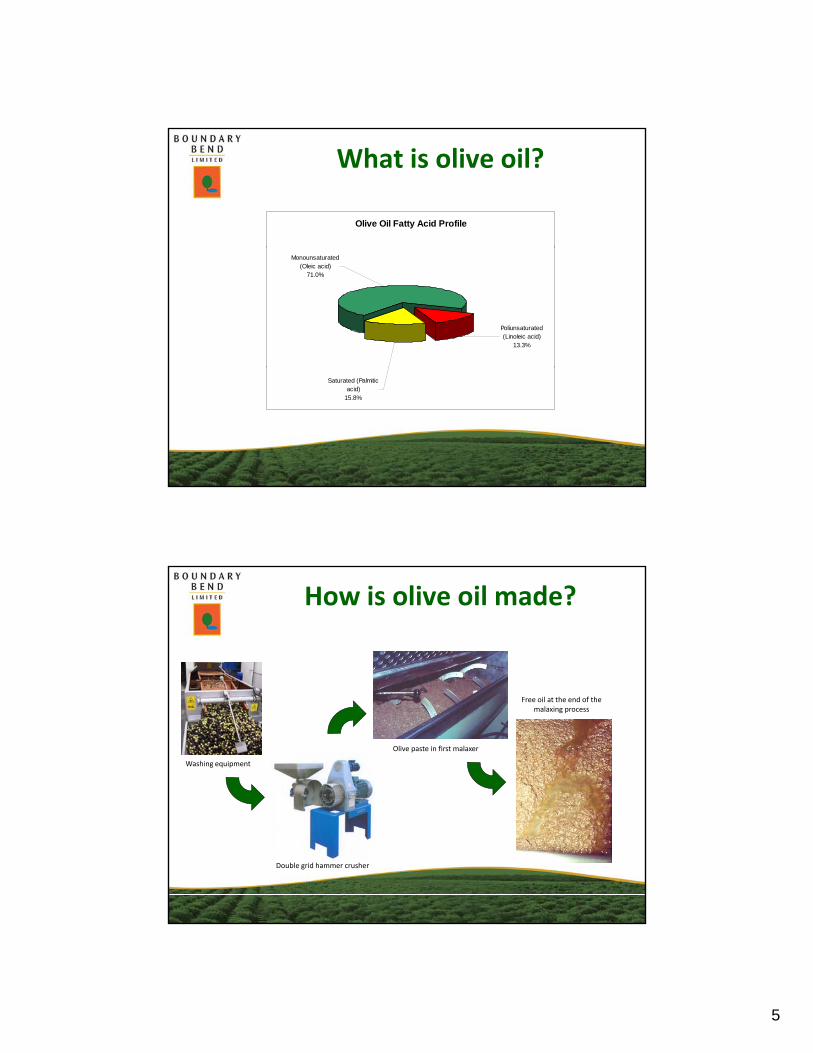

What is olive oil?

Olive Oil Fatty Acid Profile

Monounsaturated (Oleic acid)

71.0%

Poliunsaturated (Linoleic acid)

13.3%

Saturated (Palmitic acid)

15.8%

How is olive oil made?

Washing equipment

Olive paste in first malaxer

Free oil at the end of the malaxing process

Double grid hammer crusher

6

How is olive oil made?

Decanter separating olive oil from paste

Olive oil storage

Vertical separators clarifying the oil

Are all olive oils the same?

Virgin Oils

• Extra virgin (≤0.8% acidity & no defects).• Virgin (≤2.0% acidity & slight defects).• Lampante oil (>2.0% & not suitable for direct human consumptiondirect human consumption

Refined Oils

EVOO or VOO

Olive Oil or Pure Olive Oil

Pomace Oils

7

Fats & oils in the world

World fats and oils consumption 2004/05 (133.7 Millions of Tonnes)

Corn1.6%

Coconut2.4%

Palmiste

Sesame0.6%

Palm22.7%

Soybean25.1%

Olive2.1%

Lineseed0.5%

Castor0.4%

Lard11.6%

Butter4.9% Fish oil

0.8%

Palmiste2.7%

Cotton seed3.3%

Peanut3.7%

Sunflower6.9%

Canola11.0%

Present

Areas Main Countries Population Litres/capita

Great variability in consumption

EC Producers Spain/Italy/Greece 186.6 10.17

EC Non Producers Germany/UK 247.9 0.60

North Africa & Middle East Tunisia/Turkey/Syria 357.7 1.07

Other Producers Australia/USA 503.4 0.64

Other Non Producers Brazil/Canada/Japan 654.7 0.26

Others China/India/Indonesia 4,755.7 0.01

TOTAL 6,706.0 0.44

Source: IOC/US Census Bureau

8

Present

Country Yields (% of world) Yields (litres/ha)

Great variability in production

Spain 38.6% 482.6

Italy 22.8% 483.0

Greece 13.6% 400.8

Turkey 4.3% 218.2

Tunisia 6.2% 119.0

BBL (in 2008) 0.2% 1,692.3

Average 318.2

Source: IOC/FAO

The Future

P t 2007/08 2020 Annual 2020 Vs.

Analysis of consumption growing trends

Parameter 2007/08 2020 Growth 2020 2007/08

Consumption (x 1000 Tn) 2,927 4,117 2.88% 4,117 -1,295.90

Population (x 1M) 6,706 7,659 1.11% 3,336 -515.72

Consumption per capita (l/person/year) 0.44 0.54 1.68%

Source: IOC/US Census Bureau

9

The Future

At current

Developments required to satisfy expected growing demand

Parameter At current average yields At 10 Tn/ha

Current Growth 4,320,000 has 785,000 has

Population Growth 1,715,000 has 313,000 has

International Olive Oil Industry

10

Past and present

EC prohibited planting olives

Greece joins the EC

Subsidies Implemented Production aids increased

No more subsidies for trees planted after May 1998

Spain joins the EC

Sources: IOC & EC report on Olive Oil

p

International Olive Oil Industry

Source: Boundary Bend Marketing

11

International Olive Oil Industry

Source Boundary Bend Marketing

If we are going to run out of oil, why prices are at historical low???

• Olive oil was not part of the soft commodities boom.

• Significant concentration of oil trading companies. Atomised offer (> 20,000

processing plants) and concentrated demand (< 10 buyers).

• Adulteration and new refining techniques.

12

Not part of soft commodities boom

Source: IOC/IMF

Large buyers dominate

Price performance of SOS share price

Source: Madrid Stock Exchange

13

Large buyers dominate

Source: PoolRed/Mercacei/FACUA

Large buyers dominate

Source: Mercacei/FACUA

14

Olive Oil Quality and Authenticity

Olive Oil Quality and Authenticity

Olive oil€ 3.52/l

EVOO (No Italian)

€ 3.59/lEVOO (Italian)

€ 4.65/lPremium (Bari & Tuscan)

€ 7.19 - 9.97/lPremium (Boutique)

€ 50.38/l

Prices from Coop Supermarket, Perugia, Italy (September 2005) & Faraway foods (September 2006)

15

Olive Oil Quality and Authenticity

Olive Oil Quality and Authenticity

7.30 Report:

“I t d li il lit d ti ”“Imported olive oil quality under scrutiny”

16

How and why olive oil is adulterated

Seed oils (canola sunflower etc )

Food service OO and ELOO, and spray cans(canola, sunflower, etc.)

Conventionally refined olive oil

Deodorisedolive oil

spray cans

Food service EVOO, organic OO and spray cans

Supermarket EVOO

IOC & Codex

DGF & AEV

Inadequate Best Before Date or no BBD at all

All oils

DGF & AEV

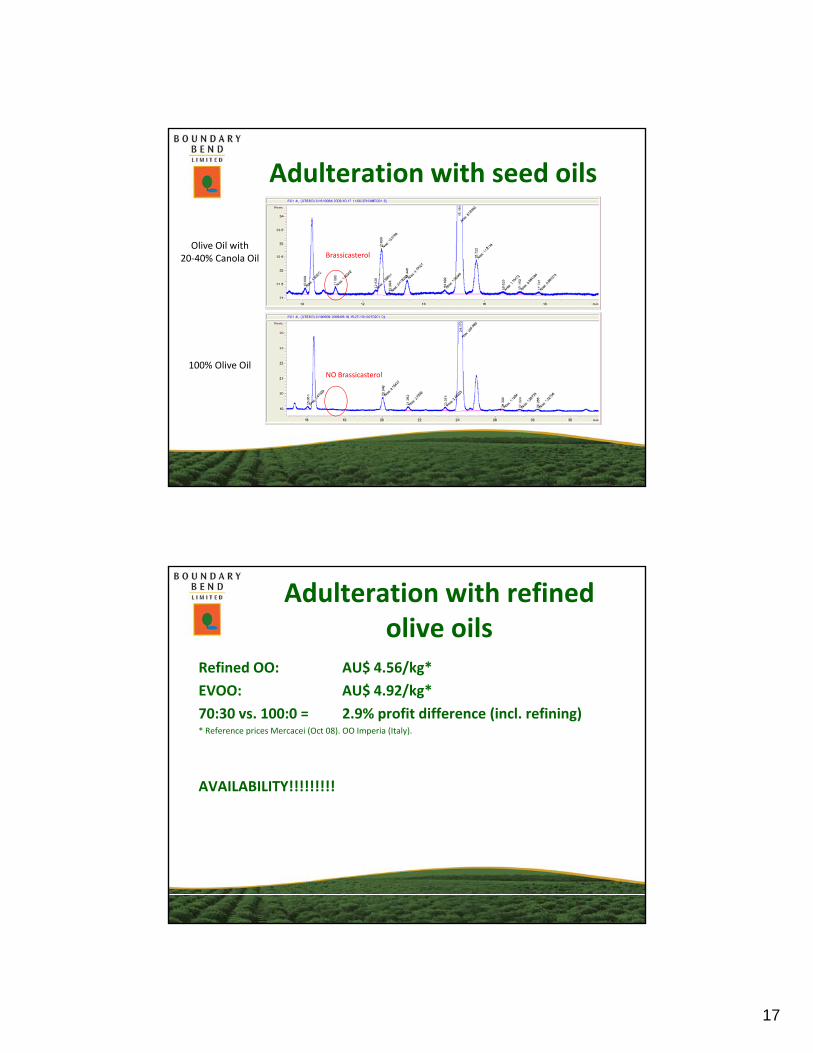

Adulteration with seed oils

Refined OO: AU$ 4.56/kg*

Canola oil: AU$ 1 72/kg*Canola oil: AU$ 1.72/kg

70:30 vs. 100:0 = 18.7% profit difference* Reference prices Mercacei (Oct 08). OO Imperia (Italy); Canola (Nederland)

17

Adulteration with seed oils

Olive Oil withBrassicasterol

Olive Oil with 20‐40% Canola Oil

100% Olive OilNO Brassicasterol

100% Olive Oil

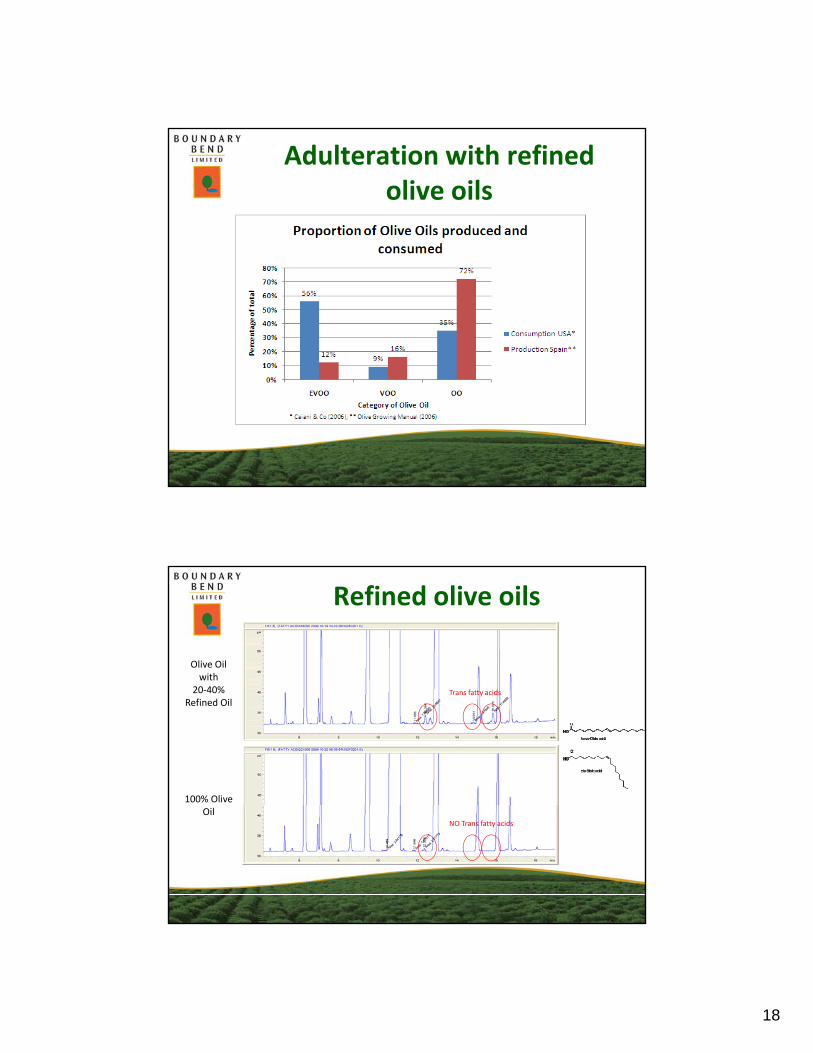

Adulteration with refined olive oils

Refined OO: AU$ 4.56/kg*

$ /k *EVOO: AU$ 4.92/kg*

70:30 vs. 100:0 = 2.9% profit difference (incl. refining)* Reference prices Mercacei (Oct 08). OO Imperia (Italy).

AVAILABILITY!!!!!!!!!

18

Adulteration with refined olive oils

Refined olive oils

Olive Oil with

20‐40% Refined Oil

100% Olive

Trans fatty acids

OilNO Trans fatty acids

19

Soft Column Refining

Not heated

80°C 60 min

120°C 60 min

160°C 60 min

DGF Methods

20

Adulterations

Recent Australian Market study (Modern • Minimum 20% higher prices for high

quality EVOO.Olives – Jan 2009)

q y

• 35,000,0000 litres (O/S oil in Oz) x

83% (Not EVOO) x 20% (Price

premium) x AU$ 5.00/litre =

AU$ 29,000,000/year

OOr

17,500 ha of new groves

Proposed Changes

![[flavouring] Extra Virgin Olive Oil - Delizio · [flavouring] Extra Virgin Olive Oil Naturally obtained from the fi rst pressing of the olive by mechanical means, Extra Virgin olive](https://static.fdocuments.in/doc/165x107/5f0ba1707e708231d43173ba/flavouring-extra-virgin-olive-oil-delizio-flavouring-extra-virgin-olive-oil.jpg)