Calidda conference call 3T 13

18

Results and Key Developments 3Q 2013 Strictly Private and Confidential

-

Upload

empresa-de-energia-de-bogota -

Category

Investor Relations

-

view

65 -

download

5

Transcript of Calidda conference call 3T 13

Results and Key Developments

3Q 2013

Strictly Private and Confidential

Results and Key Developments – 3Q 2013

32

I. Key Developments

II. Operational Performance

III. Commercial Performance

IV. Financial Performance and Key Metrics

V. Questions and answers session

VI. Disclaimer

VII. Annexes

(i) Strong Sponsorship with Optimal Experience

(ii) Experienced and Proven Management Team & Board

Results and Key Developments – 3Q 2013

33

I. Key Developments

II. Operational Performance

III. Commercial Performance

IV. Financial Performance and Key Metrics

V. Questions and answers session

VI. Disclaimer

VII. Annexes

(i) Strong Sponsorship with Optimal Experience

(ii) Experienced and Proven Management Team & Board

Key Developments

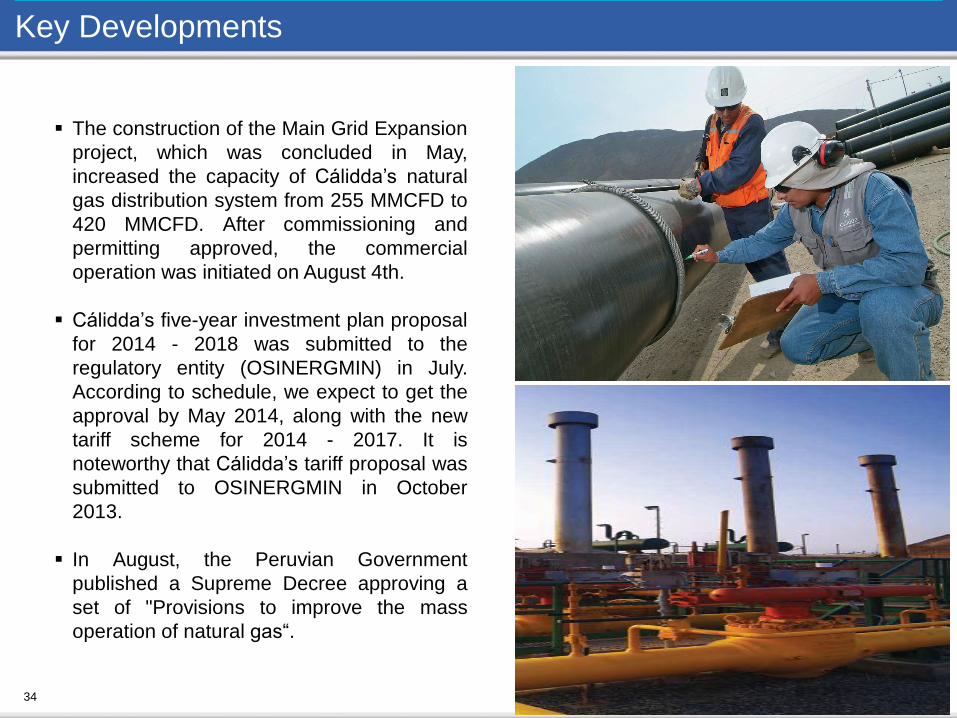

The construction of the Main Grid Expansion

project, which was concluded in May,

increased the capacity of Cálidda’s natural

gas distribution system from 255 MMCFD to

420 MMCFD. After commissioning and

permitting approved, the commercial

operation was initiated on August 4th.

Cálidda’s five-year investment plan proposal

for 2014 - 2018 was submitted to the

regulatory entity (OSINERGMIN) in July.

According to schedule, we expect to get the

approval by May 2014, along with the new

tariff scheme for 2014 - 2017. It is

noteworthy that Cálidda’s tariff proposal was

submitted to OSINERGMIN in October

2013.

In August, the Peruvian Government

published a Supreme Decree approving a

set of "Provisions to improve the mass

operation of natural gas“.

34

Results and Key Developments – Q3 2013

35

I. Key Developments

II. Operational Performance

III. Commercial Performance

IV. Financial Performance and Key Metrics

V. Questions and answers session

VI. Disclaimer

VII. Annexes

(i) Strong Sponsorship with Optimal Experience

(ii) Experienced and Proven Management Team & Board

Operational Performance

Network

Capital Expenditures

Infrastructure

Network Expansion

36

273 303 359 387 404

701 1,020

1,465

2,163

2,690

974

1,324

1,824

2,550

3,094

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2009 2010 2011 2012 Q3 2013

km

Steel Network Polyethylene Network Total

Over Q3 2013, Cálidda’s distribution network was

expanded by 237km, reaching a total of 3,094km of

underground pipelines.

As of Q3 2013, Cálidda has built 17km of steel high

pressure network and 527km of polyethylene

secondary network.

As of Q3 2013, Cálidda has invested USD 61 MM

in the expansion of its distribution network.

According to Cálidda’s five-year investment plan

proposal for 2014 - 2018, subject to approval by

OSINERGMIN, we expect capital expenditures for

the expansion of the distribution network to amount

up to USD 500 MM by the end of such period.

48 33 31

63 56

3 53

33

5 51

33

84

96

61

0

20

40

60

80

100

120

2009 2010 2011 2012 Q3 2013

MM

US

D

Secondary Network Main Network

Results and Key Developments – Q3 2013

37

I. Key Developments

II. Operational Performance

III. Commercial Performance

IV. Financial Performance and Key Metrics

V. Questions and answers session

VI. Disclaimer

VII. Annexes

(i) Strong Sponsorship with Optimal Experience

(ii) Experienced and Proven Management Team & Board

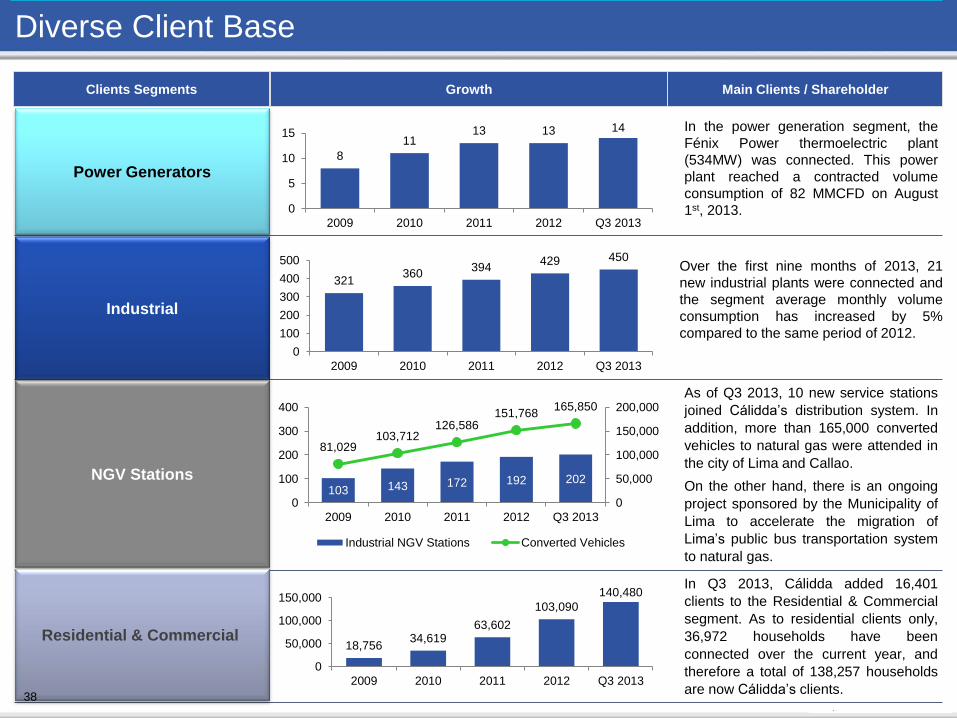

In the power generation segment, the

Fénix Power thermoelectric plant

(534MW) was connected. This power

plant reached a contracted volume

consumption of 82 MMCFD on August

1st, 2013.

Over the first nine months of 2013, 21

new industrial plants were connected and

the segment average monthly volume

consumption has increased by 5%

compared to the same period of 2012.

As of Q3 2013, 10 new service stations

joined Cálidda’s distribution system. In

addition, more than 165,000 converted

vehicles to natural gas were attended in

the city of Lima and Callao.

On the other hand, there is an ongoing

project sponsored by the Municipality of

Lima to accelerate the migration of

Lima’s public bus transportation system

to natural gas.

In Q3 2013, Cálidda added 16,401

clients to the Residential & Commercial

segment. As to residential clients only,

36,972 households have been

connected over the current year, and

therefore a total of 138,257 households

are now Cálidda’s clients.

Diverse Client Base

Power Generators

Industrial

NGV Stations

Clients Segments Growth Main Clients / Shareholder

Residential & Commercial

8

11 13 13 14

0

5

10

15

2009 2010 2011 2012 Q3 2013

321 360

394 429 450

0

100

200

300

400

500

2009 2010 2011 2012 Q3 2013

103 143 172 192 202

81,029 103,712

126,586 151,768

165,850

0

50,000

100,000

150,000

200,000

0

100

200

300

400

2009 2010 2011 2012 Q3 2013

Industrial NGV Stations Converted Vehicles

18,756 34,619

63,602

103,090

140,480

0

50,000

100,000

150,000

2009 2010 2011 2012 Q3 2013

38

Commercial Performance

Network Efficiency

Penetration Rate

39

19,188

35,133

64,181

103,724

141,146

93,761

125,849

173,531

244,317

297,345

20%

28%

37%

42%

47%

0%

10%

20%

30%

40%

50%

0

100,000

200,000

300,000

400,000

2009 2010 2011 2012 Q3 2013

Total Clients Potential Clients* Penetration Rate

(*) Clients who are adjacent to Cálidda's distribution network.

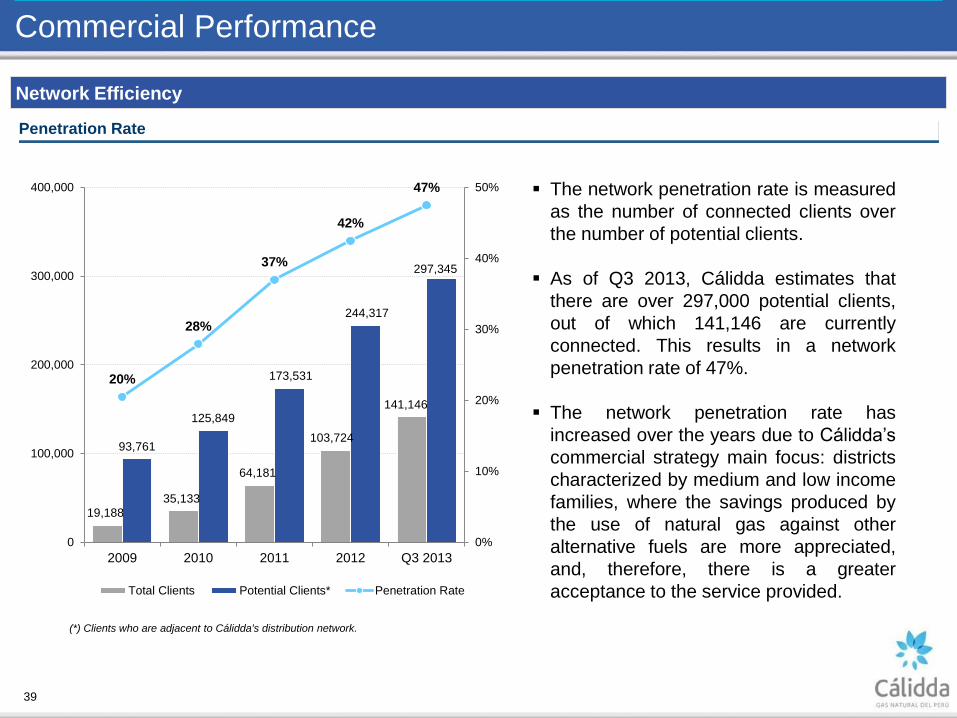

The network penetration rate is measured

as the number of connected clients over

the number of potential clients.

As of Q3 2013, Cálidda estimates that

there are over 297,000 potential clients,

out of which 141,146 are currently

connected. This results in a network

penetration rate of 47%.

The network penetration rate has

increased over the years due to Cálidda’s

commercial strategy main focus: districts

characterized by medium and low income

families, where the savings produced by

the use of natural gas against other

alternative fuels are more appreciated,

and, therefore, there is a greater

acceptance to the service provided.

8,896

11,757

14,738

18,052

13,266 14,943

2009 2010 2011 2012 Q3 2012 Q3 2013

28,377

52,146

103,897

116,346

88,658 81,319

2009 2010 2011 2012 Q3 2012 Q3 2013

305

464

694

1,068

773

1,005

2009 2010 2011 2012 Q3 2012 Q3 2013

22,152

26,856

31,659 32,735

24,613 25,935

2009 2010 2011 2012 Q3 2012 Q3 2013

Accumulated Volume Consumption by Client Segment

NGV Stations (MMCF) Residential & Commercial (MMCF)

Industrial (MMCF) Power Generators (MMCF)

40

Results and Key Developments – Q3 2013

41

I. Key Developments

II. Operational Performance

III. Commercial Performance

IV. Financial Performance and Key Metrics

V. Questions and answers session

VI. Disclaimer

VII. Annexes

(i) Strong Sponsorship with Optimal Experience

(ii) Experienced and Proven Management Team & Board

Financial Performance

(1) LTM: Last Twelve Months.

(2) Financial Debt is net of amortized costs.

(3) Interests do not include debt prepayment penalties (USD8MM). 42

Revenues

In US$ MM

5.8% 3.0% 2.4% 3.1% 2.3% 5.2%

11.4% 15.8% 23.8% 25.9% 26.2%

30.2% 12.4%

27.0%

36.0% 34.2% 35.5% 28.2%

27.8%

19.2%

15.4% 15.1% 14.8% 14.5% 39.2%

32.4% 20.0% 18.5% 18.1% 17.1%

3.5% 2.6% 2.4% 3.2% 3.0% 4.7%

2009 2010 2011 2012 Q3 2012 Q3 2013

Residential &CommercialIndustrial

NGVStationsPowerGeneratorsInstallationServicesOthers

Total Adjusted Revenues1 By Client Segment

43 64 103 125

90 103

116 125

201

245

176 194 160

188

304

370

266 297

2009 2010 2011 2012 Q3 2012 Q3 2013

Distribution & Others Pass-through & IFRIC 12

2

(1) Total Adjusted Revenues exclude Pass-through and IFRIC 12 revenues.

(2) Installation services include revenues from connection fees and facility’s financing.

2009 2010 2011 2012 Q3 2012 Q3 2013 LTM1 Set-13

Total Revenues 160 188 304 370 266 297 401

Pass-through & IFRIC 12 116 125 201 245 176 194 263

Distribution & Others 43 64 103 125 90 103 137

EBITDA 19 29 59 64 48 51 67

Adjusted EBITDA Margin 44.5% 46.5% 57.6% 51.6% 53.6% 49.3% 48.5%

Financial Debt2 75 114 166 196 196 318 318

Cash 16 24 27 45 42 122 122

Interests3 5 8 10 12 9 8 12

(MM USD)

Key Metrics

Interest Coverage1 Debt and Net Debt / EBITDA

EBITDA (MM USD) & Adj. EBITDA Margin (%) FFO / Net Debt

43

20.9% 20.2%

28.9% 28.3%

11.5%

2009 2010 2011 2012 Q3 2013

19

29

59 64 67

44.5% 46.1% 57.6%

51.6% 48.5%

2009 2010 2011 2012 Q3 2013

EBITDA Adjusted EBITDA Margin

3.5x 3.8x

5.8x 5.5x 5.6x

2009 2010 2011 2012 Q3 2013

3.9x 3.9x

2.8x 3.0x

4.8x

3.1x 3.1x

2.3x 2.3x

2.9x

2009 2010 2011 2012 Q3 2013

Debt / EBITDA Net Debt / EBITDA

(1) Ratio does not include debt prepayment penalties (USD8MM).

Results and Significant Developments – Q3 2013

44

I. Key Developments

II. Operational Performance

III. Commercial Performance

IV. Financial Performance and Key Metrics

V. Questions and answers session

VI. Disclaimer

VII. Annexes

(i) Strong Sponsorship with Optimal Experience

(ii) Experienced and Proven Management Team & Board

Disclaimer

45

The information provided here is for informational and illustrative purposes only and is not, and does

not seek to be, a source of legal or financial advice on any subject. This information does not constitute

an offer of any sort and is subject to change without notice.

Cálidda and its Shareholders expressly disclaim any responsibility for actions taken or not taken based

on this information. Neither Cálidda nor its Shareholders accept any responsibility for losses that might

result from the execution of the proposals or recommendations herein presented. Neither Cálidda nor

its Shareholders are responsible for any content that may originate with third parties. Cálidda or its

Shareholders may have provided, or might provide in the future, information that is inconsistent with the

information herein presented.

Strong Sponsorship with Optimal Experience

Controlling Shareholder – 60% Ownership in Cálidda

Shareholder – 40% Ownership in Cálidda

Leading energy holding company with interests across the electricity and

natural gas sectors in Colombia, Peru and Guatemala

– Founded in 1896, controlled by the Distrito de Bogotá since 1956 with a 76.2%

ownership stake

– Leader in the Energy Sector: major player in the transmission and distribution of

electricity and natural gas

– International presence: Colombia, Peru and Guatemala

One of the largest natural gas distribution and transportation companies in

Colombia

– Founded in 1974 by the government of Colombia. Currently controlled by Grupo Aval

– Only vertically-integrated natural gas company in Colombia

– Major player in the gas distribution sector in Colombia through Gases de Occidente,

Surtigas and Gases del Caribe

– Participation in the power distribution in Colombia and telecommunications sector in

Panama and Costa Rica

– International Presence: Panama, Peru and Costa Rica

– EEB has 15.6% stake in Promigas

Controlling Investments

Non Controlling Investments

Controlling Investments

Non Controlling Investments

Strong Shareholder Commitment to Cálidda

– Injected USD 35 MM in November 2012 and another USD 25 MM in February 2013 as equity.

– Provided a USD 47 MM intercompany subordinated loan to Cálidda.

– In May 2013, capital was increased through the capitalization of retained earnings (USD 62.2 MM).

46

Experienced and Proven Management Team & Board

Cálidda’s management team and board have a successful track record in the oil and gas sector

Board of Directors

Management Team

47

ChiefOperating

Officer

JorgeMonterroza

Years in industry:16 years

Years at Cálidda:2 years

Chief Executive OfficerAdolfo Heeren

Years in Industry: 16 YearsYears at Cálidda: 2 years

ChiefCommercial

Officer

CarlosCerón

Years in industry:16 years

Years at Cálidda:2 years

ChiefProcurement

Officer

PatriciaPazos

Years in industry:16 years

Years at Cálidda:8 years

ChiefFinancialOfficer

JaimeQuintana

Years in industry:7 years

Years at Cálidda:2 years

Chief Human Resources

Officer

RosarioJiménez

Years in industry:4 years

Years at Cálidda:4 years

ChiefExternal Affairs Officer

TaniaSilva

Years in industry:2 years

Years at Cálidda:1 years

ChiefLegal and Regulatory

Officer

AmadeoArrarte

Years in industry:11 years

Years at Cálidda:9 years

ChiefStrategy Officer

TatianaRivas

Years in industry:5 years

Years at Cálidda:5 years

ChiefInternal Auditor

CarolinaHernández

Years in industry:7 years

Years at Cálidda:5 years

PresidentSandra Stella

Fonseca Arenas

18 years of working experience in the

energy sector

Former Executive Director of the Energy and Gas Regulation

Commission in Colombia

Luis BetancurEscobar

Served as Director of Fondo Financiero Desarrollo Urbano

President of Colombia's

restructuring of the Energy and Gas

Regulatory Commission

Jose Elias Melo Acosta

President of Corporación Financiera

Colombiana S.A

Minister of Colombia's Treasury and Public Credit and Labor and

Social Security departments.

Antonio CeliaMartínez-Aparicio

President ofPromigas

Served on the board of directors of various companies in the

natural gas sector.

Manuel GuillermoCamargo Vega

Management positions in distribution and

transportation utilities of natural gas and

project experience in transportation of crude

oil and natural gas.

José MiguelAcosta Suárez

CIA and CCSA

Former Comptrollerof Consorcio

Transmantaro. Over 30 years of experience

in technical, administrative,

financial and internal audit departments.

Luis ErnestoMejía Castro

Director ofPromigas

Minister of Mines and Energy and Vice

Minister of Hydrocarbons and

Mines.

48

For more information about Cálidda, please contact our Investor Relations team:

http://calida.com.pe/inversionistas/

http://www.grupoenergiadebogota.com.co

Jaime Quintana

CFO

+51 1 625 7310

jaime.quintana@Cálidda.com.pe

Rafael Andrés Salamanca Rodriguez

Investor Relations Advisor

+57 1 326 8000 – ext. 1675

Antonio Angarita

Investor Relations Officer

+57 1 326 8000 – ext. 1546

Mathius Sersen

Finance Director

+51 1 625 7390

mathius.sersen@Cálidda.com.pe

Investor Relations

![3T]caP[[h ]Tgc [TeT[ 3T[TQaPcT - Novotel Sydney Central · 3t[tqapct 3t]cap[[h 5if(spwf$pdlubjm1bdlbhf qfsqfstpo ipvsdbobqft ipvstpgcfwfsbhft $pdlubjm1bdlbhf qfsqfstpo ipvstpgefmjdjpvt{dbobqft{](https://static.fdocuments.in/doc/165x107/5f6aa72c2199805f6a1a97e5/3tcaph-tgc-tet-3ttqapct-novotel-sydney-central-3ttqapct-3tcaph-5ifspwfpdlubjm1bdlbhf.jpg)