CAIIB Super Notes: Corporate Banking: Module B: Investment Banking: Mergers and Acquisitions

48

CAIIB – Super-Notes © M S Ahluwalia Sirf Business Mergers and Acquisitions Module B: Investment Banking

-

Upload

ms-ahluwalia -

Category

Business

-

view

1.605 -

download

5

Transcript of CAIIB Super Notes: Corporate Banking: Module B: Investment Banking: Mergers and Acquisitions

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Mergers and Acquisitions

Module B: Investment Banking

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

CAIIB – SUPER NOTES

Corporate Banking: Mergers and Acquisitions

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Contents

Coverage:

1. Mergers

2. Types of Mergers

3. Acquisitions

4. Strategic Approach to Acquisitions

5. Acquisition and Organic Growth

6. Financing M &A

7. Corporate Restructuring

8. Types of Demerger, Divestitures

9. Merger Procedure

10. Valuation of a Merger: Determination of Share

Exchange Ratio

11. Mergers and Takeovers: Indian Scene

12. The changing international M&A landscape

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

MERGERS

1.

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Merger

• Coming together of two companies of roughly equal size, pooling

their resources into a single business

• Stockholders of both pre-merger companies have a share in

ownership of the merged entity and top management of both

companies continues to hold senior management positions after

the merger

• Control is the key test of distinction between a merger and an

acquisition

• There is nil/negligible exchange of cash

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

TYPES OF MERGERS

2.

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

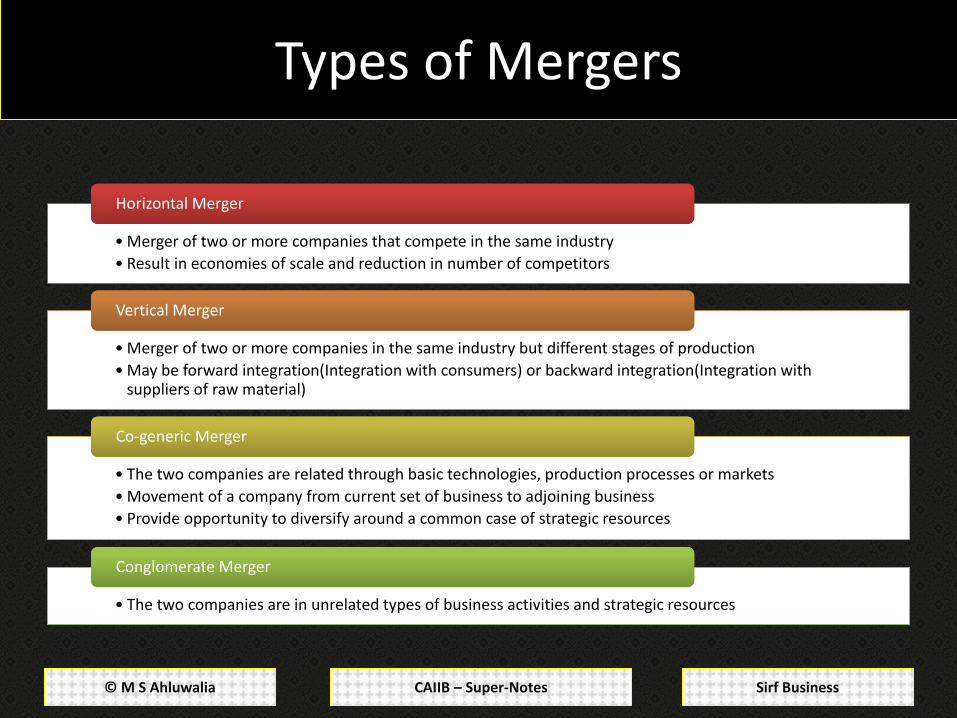

Types of Mergers

• Merger of two or more companies that compete in the same industry

• Result in economies of scale and reduction in number of competitors

Horizontal Merger Horizontal Merger

• Merger of two or more companies in the same industry but different stages of production

• May be forward integration(Integration with consumers) or backward integration(Integration with suppliers of raw material)

Vertical Merger Vertical Merger

• The two companies are related through basic technologies, production processes or markets

• Movement of a company from current set of business to adjoining business

• Provide opportunity to diversify around a common case of strategic resources

Co-generic Merger Co-generic Merger

• The two companies are in unrelated types of business activities and strategic resources

Conglomerate Merger Conglomerate Merger

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

ACQUISITIONS

3.

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Acquisitions

• An acquisition or takeover occurs when one company acquires

from another either:

– A controlling interest in the company’s stocks

– A controlling interest in the business operation and its assets

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Joint Venture

• A business partnership in which two or more companies agree

to invest cash or other assets in a particular project or

business activity

• Partners establish a separate company in which they hold

stocks in proportion to their investment

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

STRATEGIC APPROACH TO ACQUISITIONS

4.

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

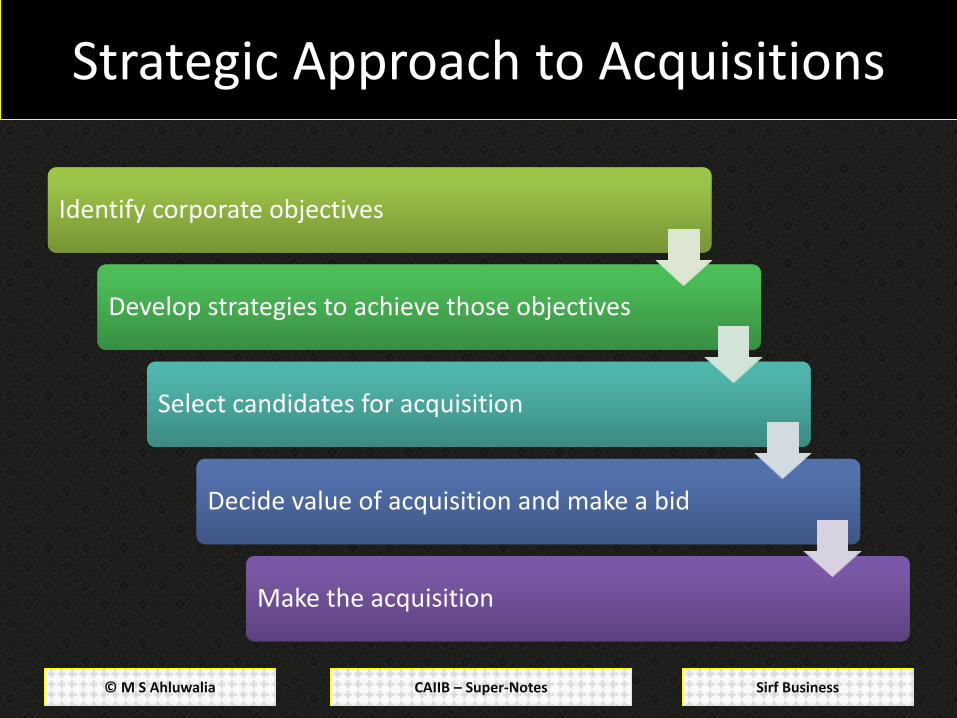

Strategic Approach to Acquisitions

Identify corporate objectives Identify corporate objectives

Develop strategies to achieve those objectives Develop strategies to achieve those objectives

Select candidates for acquisition Select candidates for acquisition

Decide value of acquisition and make a bid Decide value of acquisition and make a bid

Make the acquisition Make the acquisition

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Corporate Objectives

Market Leadership Market Leadership Technological

Leadership Technological

Leadership

Social Welfare (By providing quality

services and products)

Social Welfare (By providing quality

services and products)

Innovation Innovation Being the lowest

cost producer Being the lowest

cost producer

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

ACQUISITION AND ORGANIC GROWTH

5.

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

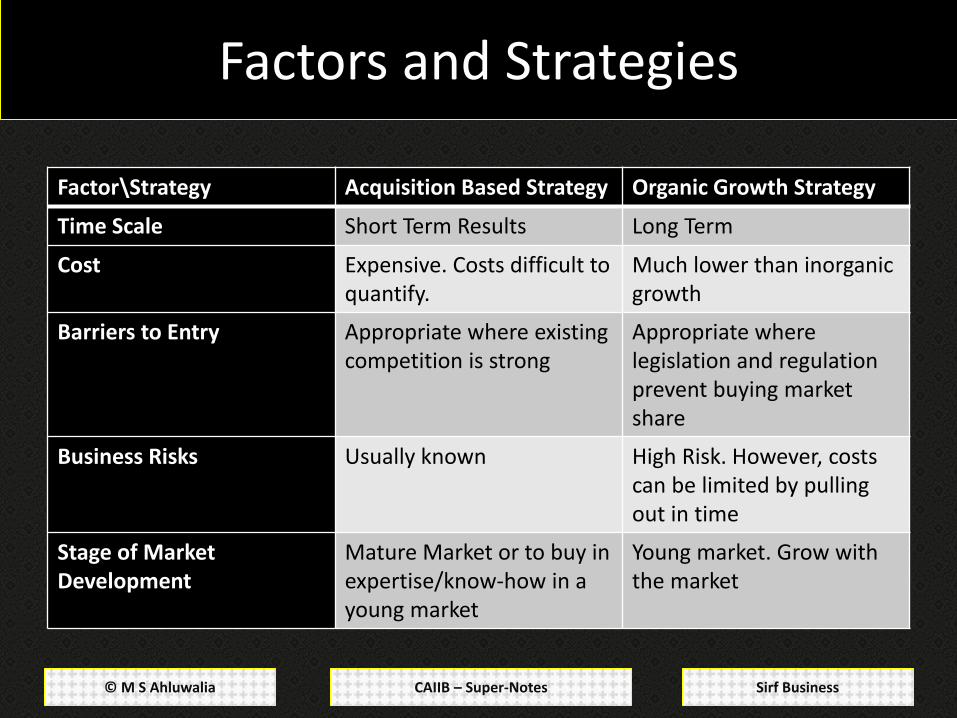

Factors and Strategies

Factor\Strategy Acquisition Based Strategy Organic Growth Strategy

Time Scale Short Term Results Long Term

Cost Expensive. Costs difficult to quantify.

Much lower than inorganic growth

Barriers to Entry Appropriate where existing competition is strong

Appropriate where legislation and regulation prevent buying market share

Business Risks Usually known High Risk. However, costs can be limited by pulling out in time

Stage of Market Development

Mature Market or to buy in expertise/know-how in a young market

Young market. Grow with the market

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Aggressive and Defensive Strategies

Aggressive Strategy Aggressive Strategy

• To improve market position

Defensive Strategy Defensive Strategy

• To survive in a changing industry

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Techniques to avoid Hostile Takeover Bid

• The unfriendly bidder

Black Knight Black Knight

• Friendly investor

• May also be the investor in a struggling entity to prevent it from falling

White Knight White Knight

• Enters hostile takeover bid, however, more favourable than the Black Knight

Grey Knight Grey Knight

• Similar to a White Knight. However, only exercises a significant minority stake

White Squire White Squire

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Hostile Firm’s Counter-strategies

• Make an offer more lucrative than the White Knight’s offer.

• NL Strategy:

– Wait for the white knight to complete the takeover process

– Take over the white knight

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

FINANCING M &A

6.

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Financing M &A

Cash Cash Bank

Financing Bank

Financing

Hybrids (Cash & Debt)

Hybrids (Cash & Debt)

Factoring Factoring

Recent years have seen the rise of specialist M&A firms which only provide consultancy services and do not provide financing

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

CORPORATE RESTRUCTURING

7.

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Forms of Corporate Restructuring

Corporate Restructuring

Corporate Restructuring

Expansion Expansion

Amalgamation Amalgamation

Absorption Absorption

Tender Offer Tender Offer

Asset Acquisition

Asset Acquisition

Joint Venture Joint Venture

Contraction Contraction

Demerger Demerger

Spin Off Spin Off

Equity Carve out

Equity Carve out

Split Off Split Off

Split Up Split Up

Divestitures Divestitures

Asset Value Asset Value

Corporate Control

Corporate Control

Going Private Going Private

Equity buyback Equity

buyback

Anti Takeover Anti Takeover

Leveraged Buyouts

Leveraged Buyouts

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

TYPES OF DEMERGER, DIVESTITURES

8.

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Types of Demerger, Divestitures

•Division of company into wholly owned subsidiary of the parent company

•Shares of subsidiary are distributed amongst the shareholders of the parent company on pro-rata basis

•Split off: The shareholders are given shares of the spun off company in lieu of the parent company’s shares

•Equity Carve Out: Only difference from Spin Off being that some part of equity is offered to the public

Spin Off Spin Off

•Company is split into various companies such that parent company ceases to exist

Split Up Split Up

•Sale of segment of a company for cash or for securities to an outside party. Based on principle of ‘antergy’.

Divestiture Divestiture

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Motives behind Divestitures

Dismantling Conglomerates

Dismantling Conglomerates

Abandoning Core Business

Abandoning Core Business

Changing Strategies Changing Strategies

Adding value by selling into a

better fit

Adding value by selling into a

better fit

Large additional investment

required

Large additional investment

required

Harvest past successes

Harvest past successes

Discard unwanted business from

prior acquisitions

Discard unwanted business from

prior acquisitions

Finance prior acquisitions done

before LBO

Finance prior acquisitions done

before LBO

Ward Off Takeover Ward Off Takeover

Meeting Regulatory

Requirements

Meeting Regulatory

Requirements

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Divestitures

Benefits

• Shedding Excess Flab

• Effective Market Regulation

• Financial Support

Issues

• Market Reactions

• Government Interventions

Asset Sale: Sale of tangible assets of a company to generate cash. Slump Sale: A partial sell off involving the sale of a business unit or plant of one firm to another.

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Corporate Controls

•Listed company is converted to private by buying back all unlisted shares

Going Private Going Private

•Reduction in equity capital by buying back some portion of the outstanding shares of the company

•Increases promoter’s percentage share

Equity Buyback Equity Buyback

•Various measures resorted to by companies to prevent hostile takeovers

Anti-Takeover Defenses Anti-Takeover Defenses

•Raising of capital from the market or institutions by the management to acquire a company on the strength of its assets

Leveraged Buyouts Leveraged Buyouts

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Amalgamation

• A legal process by which two or more companies are to be

absorbed or blended with another.

• The amalgamating companies lose their existence and a new

entity is formed

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Takeover

• A series of transactions whereby a person, individual, group of

individuals or a company acquires control over the assets of a

company, either directly by becoming owner of those assets

or indirectly by obtaining control of management of the

company

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Takeover Bid

• An offer to acquire enough shares of a company to gain voting control of the

company

• For taking over the control and management affairs of a listed company by

acquiring its controlling interest

Typ

es

Typ

es

Negotiated Bid Negotiated Bid

•Also called Friendly Merger

•Management/Owners of both firms sit together and negotiate the deal

Tender Offer Tender Offer

•Acquiring firm approaches the shareholders of the target firm directly to sell their shareholding to the acquiring firm at a fixed price

Hostile Takeover Bid Hostile Takeover Bid

•Also called Raid

•Acquiring firm without the knowledge and consent of the management of the target firm, may unilaterally pursue the efforts to gain a controlling interest in the target firm

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

MERGER PROCEDURE

9.

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Merger Procedure

Examination of Object Clauses Examination of Object Clauses

Intimation to Stock Exchanges

Intimation to Stock Exchanges

Approval of the draft amalgamation

proposal by the respective boards

Approval of the draft amalgamation

proposal by the respective boards

Application to the National Company

Law Tribunal (NCLT)

Application to the National Company

Law Tribunal (NCLT)

Dispatch of notice to shareholders and

creditors

Dispatch of notice to shareholders and

creditors

Holding of meeting of Shareholders and

creditors

Holding of meeting of Shareholders and

creditors

Petition to the NCLT for confirmation and

passing of NCLT orders

Petition to the NCLT for confirmation and

passing of NCLT orders

Filing the order with the Registrar

Filing the order with the Registrar

Transfer of Assets and Liabilities

Transfer of Assets and Liabilities

Issue of Shares and Debentures

Issue of Shares and Debentures

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

VALUATION OF A MERGER: DETERMINATION OF SHARE EXCHANGE RATIO

10.

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Valuation Methods

Net Asset Value (NAV) Method

Net Asset Value (NAV) Method

• NAV is sum total of value of assets after removing liabilities other than preference shares

• NAV is divided by fully diluted equity to get NAV per share

Yield Value Method Yield Value Method

• Also called profit earning capacity method

• Assessment of future maintainable profits of the business

• The above divided by appropriate capitalisation rates give the true value of business

• The above divided by equity value gives value per share

Market Value Method Market Value Method

• For listed companies

• The average of high or low values and closing prices over a specified period is taken as the representative value per share

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Supreme Court Guidelines

• Regard should be had to price of shares prevailing in the stock market

• Profit earning capacity (yield method) or dividend declared by the

company (dividend method) should be considered. Golden mean may be

found in case of differing values

• In computing yields, abnormal expenses will be added back to calculate

‘yield’

• If lower dividend or profits are due to temporary reasons, then estimate of

share value before the setback and proportionate fall in price of quoted

shares of companies which have suffered similar reverses should be

considered

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Reverse Merger

• When a healthy company merges with a small or a sick company

• Reasons:

– Transferor company gets advantage of carry forward of losses without any

conditions

– If transferee company is listed the transferor company gets advantages of

listed company without following strict norms of listing

• Transfer of assets under the amalgamation scheme is exempt from

Capital Gains Tax

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

MERGERS AND TAKEOVERS: INDIAN SCENE

11.

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Mergers and Takeovers: Indian Scene

• The concept was not popular and kept a low profile till 1990

due to regulatory and prohibitory provisions of the MRTP Act,

1969

• Most of the provisions of the Act have been repealed which

has resulted in a spate of mergers and acquisitions in the

country

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Motives of Merger

Synergies through

consolidation

Synergies through

consolidation

Operating Synergy

Operating Synergy

Financial Synergy Financial Synergy

Managerial Synergy

Managerial Synergy

Sales Synergy Sales Synergy

Diversification Diversification

Accelerated Growth

Accelerated Growth

Increased Market Power

Increased Market Power

Purchase of Assets at Bargain

Price

Purchase of Assets at Bargain

Price

Reduction in Tax Liability

Reduction in Tax Liability

Economies of Scale

Economies of Scale

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Choosing Target Firm

• Choice depends on the motive:

– If motive is undervaluation, the target firm must be undervalued

– If motive is diversification, the target firm will be unrelated business

Etc.

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Valuing Target Firm

• Status Quo Valuation: Firm’s value with existing investing, financing and

dividend policies

• Value of Corporate Control = Value of firm optimally managed – Value of firm

with current management

• Value of Operational Synergy:

– What form is the synergy expected to take?

– When will the synergy start affecting cash flows?

• Value of Financial Synergy:

– Tax Benefit

– Increase in debt capacity

– Better use for excess cash or cash slack

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Structuring the Acquisition

How much to pay?

•Based on:

•Market Price of the target firm, if publically traded

•Relative scarcity of the specialised resources

•Presence of other bidders for the target firm

How much to pay?

•Based on:

•Market Price of the target firm, if publically traded

•Relative scarcity of the specialised resources

•Presence of other bidders for the target firm

How to pay?

•Debt vs. Equity

•Cash vs. Stock

•Availability of Cash on hand

•Perceived value of the stock

•Tax Factors

How to pay?

•Debt vs. Equity

•Cash vs. Stock

•Availability of Cash on hand

•Perceived value of the stock

•Tax Factors

Accounting Treatment of the Deal Accounting Treatment of the Deal

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Exogenous factors affecting Mergers

Anti Trust Anti Trust Arbitrage Arbitrage Currencies Currencies Deregulation Deregulation

Experts Experts Hostile Bids Hostile Bids Labour Labour LBO funds LBO funds

Markets Markets Taxes Taxes

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

THE CHANGING INTERNATIONAL M&A LANDSCAPE

12.

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Cross Border Mergers

How should the transaction be

financed?

How should the transaction be

financed?

How are the customs and the cultures of the

parties different?

How are the customs and the cultures of the

parties different?

How do the applicable laws

govern the transaction?

How do the applicable laws

govern the transaction?

What level of due diligence is

appropriate?

What level of due diligence is

appropriate?

Are there any significant anti-trust or non-competition

issues?

Are there any significant anti-trust or non-competition

issues?

Are there any significant tax or currency issues?

Are there any significant tax or currency issues?

Management Management Customers Customers

Vendors Vendors Problems involving

places Problems involving

places Legal Issues Legal Issues

Fact

ors

to

be

con

sid

ered

Fa

cto

rs t

o b

e co

nsi

der

ed

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Post Merger Task Force

• Composed of a representative group from both sides of the

transaction. The members should be credible and respected

by people belonging to both sides

• Formed after the due diligence process

• Purpose is to uncover, evaluate, and resolve post-merger

problems

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Do you have any questions or queries or some feedback to give?

Just mark an email to [email protected]

CAIIB – Super-Notes © M S Ahluwalia Sirf Business For more Super-Notes: Click Here

M S Ahluwalia, amongst other things, is a visual artist, blogger,

blog designer and of course an MBA and Banker from New

Delhi, India.

To know more about him you may visit his blog-site: Estudiante De La Vida