CA State Bar International

16

TAX STRATEGIES CROSS-BORDER M&A AND REORGANIZATIONS Roger Royse Royse Law Firm, PC Palo Alto, San Francisco, Los Angeles [email protected] www.rroyselaw.com www.rogerroyse.com Skype: roger.royse Twitter: Rroyse00 IRS Circular 230 Disclosure: To ensure compliance with the requirements imposed by the IRS, we inform you that any tax advice contained in this communication, including any attachment to this communication, is not intended or written to be used, and cannot be used, by any taxpayer for the purpose of (1) avoiding penalties under the Internal Revenue Code or (2) promoting, marketing or recommending to any other person any transaction or matter 2012 Annual Meeting of the California Tax Bar & California Tax Policy Conference Nov. 3, 2012 TAX STRATEGIES CROSS-BORDER M&A AND REORGANIZATIONS 1

-

Upload

roger-royse -

Category

Business

-

view

252 -

download

4

Transcript of CA State Bar International

1

TAX STRATEGIESCROSS-BORDER M&A AND REORGANIZATIONS

Roger RoyseRoyse Law Firm, PC

Palo Alto, San Francisco, Los [email protected]

www.rroyselaw.comwww.rogerroyse.com

Skype: roger.royseTwitter: Rroyse00

IRS Circular 230 Disclosure: To ensure compliance with the requirements imposed by the IRS, we inform you that any tax advice contained in this communication, including any attachment to this communication, is not intended or written to be used, and cannot be used, by any taxpayer for the purpose of (1) avoiding penalties under the Internal Revenue Code or (2) promoting, marketing or recommending to any other person any transaction or matter addressed herein.

2012 Annual Meeting of the California Tax Bar & California Tax Policy Conference

Nov. 3, 2012

TAX STRATEGIESCROSS-BORDER M&A AND REORGANIZATIONS

2

OVERVIEW OF TRANSACTIONS• Domestic Transactions

– Type A – Merger– Type B – Stock for Stock– Type C – Stock for Assets– Type D – Spin Off, Split Off, Split Up, and

Type D Acquisitive Reorganizations– Triangular Mergers

• Foreign Transactions– §367(a) – Outbound Transactions– §367(b) – Inbound and Foreign to Foreign

Transactions– §7874 – Anti-Inversion Rules– §338(g) Election

• Joint Ventures

3

TYPE A REORGANIZATIONSIRC §368(a)(1)(A) STATUTORY MERGER / CONSOLIDATION

Acquiror

Shareholders

Target Assets; Merger

Acquiror Stock; Boot

• Statutory Merger: Two or more corporations combine and only one survives (Rev. Rul. 2000-5)

• International A reorganizations are possible for transactions after Jan. 23, 2006. Reg. § 1.368-2(b)(1)(ii).

Target

4

TYPE B REORGANIZATIONSIRC §368(a)(1)(B) STOCK FOR STOCK

• Acquiror receives Target stock, resulting in control of Target, in exchange for Acquiror voting stock.

Acquiror

Target

Shareholders

Acquiror Stock

Target Stock (Control)

5

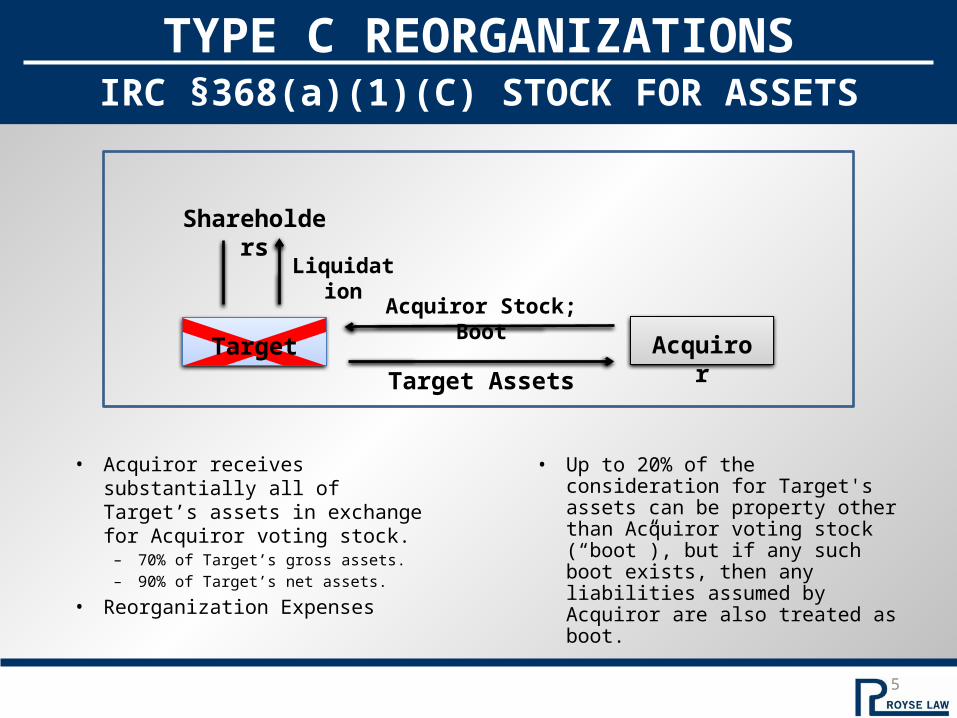

TYPE C REORGANIZATIONSIRC §368(a)(1)(C) STOCK FOR ASSETS

Target Assets

• Acquiror receives substantially all of Target’s assets in exchange for Acquiror voting stock.– 70% of Target’s gross assets.– 90% of Target’s net assets.

• Reorganization Expenses

• Up to 20% of the consideration for Target's assets can be property other than Acquiror voting stock (“boot”), but if any such boot exists, then any liabilities assumed by Acquiror are also treated as boot.

Acquiror

Shareholders

Acquiror Stock; Boot

Liquidation

Target

6

TYPE D REORGANIZATIONSIRC §§355, 368(a)(1)(D) DIVISIVE REORGANIZATION

T1

Shareholders

• Active Business Requirement• “Spin Off”; “Split Off”; “Split Up”

T1 Stock; Control

T1, T2 Stock

T2Assets

T2 Stock; Control

Assets

Transferor

7

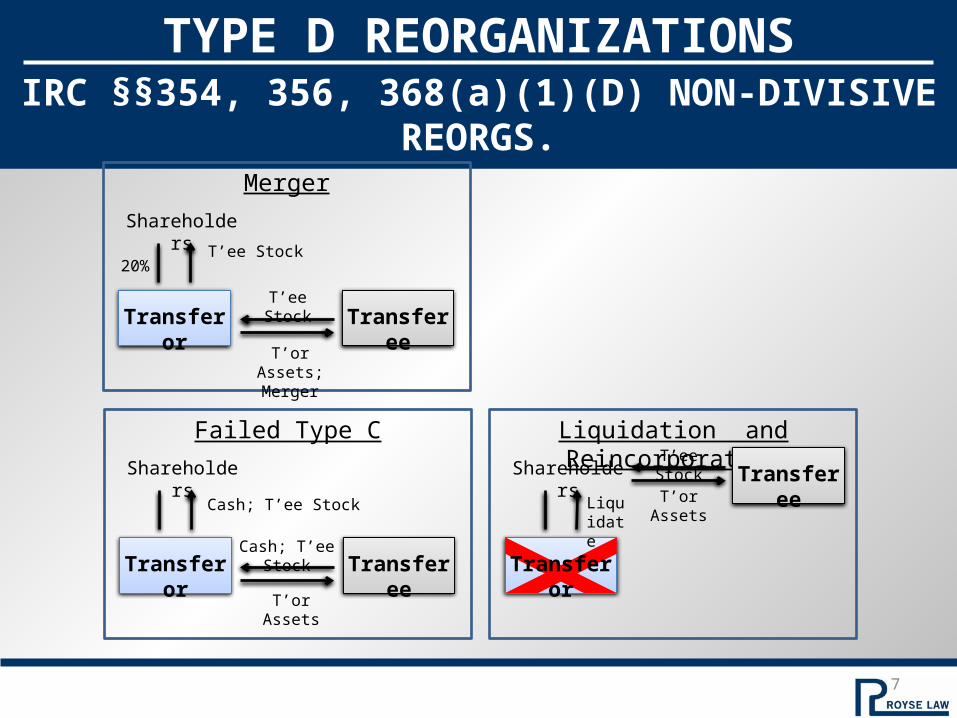

TYPE D REORGANIZATIONSIRC §§354, 356, 368(a)(1)(D) NON-DIVISIVE REORGS.

Failed Type CShareholders

Transferor Transferee

Cash; T’ee Stock

Cash; T’ee Stock

T’or Assets

MergerShareholders

Transferor Transferee

T’ee Stock

T’ee Stock

T’or Assets; Merger

20%

Liquidation and ReincorporationShareholders Transferee

Liquidate

T’or Assets

T’ee Stock

Transferor

8

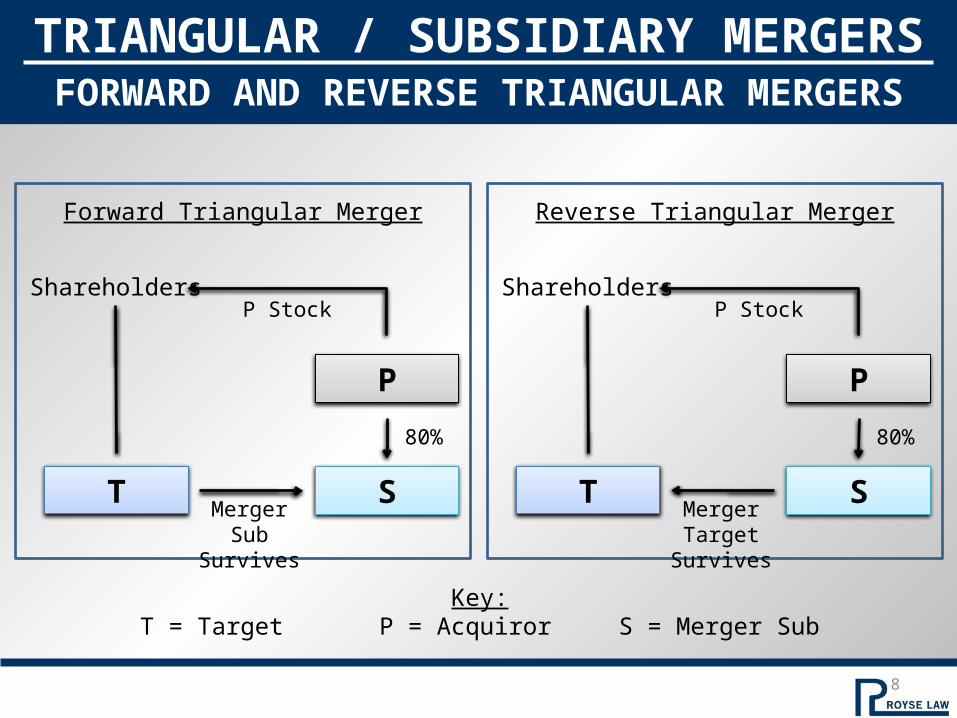

TRIANGULAR / SUBSIDIARY MERGERSFORWARD AND REVERSE TRIANGULAR MERGERS

T

P

S

Shareholders

80%

MergerSub Survives

Key:T = Target P = Acquiror S = Merger Sub

P Stock

Forward Triangular Merger

T

P

S

Shareholders

80%

MergerTarget Survives

P Stock

Reverse Triangular Merger

9

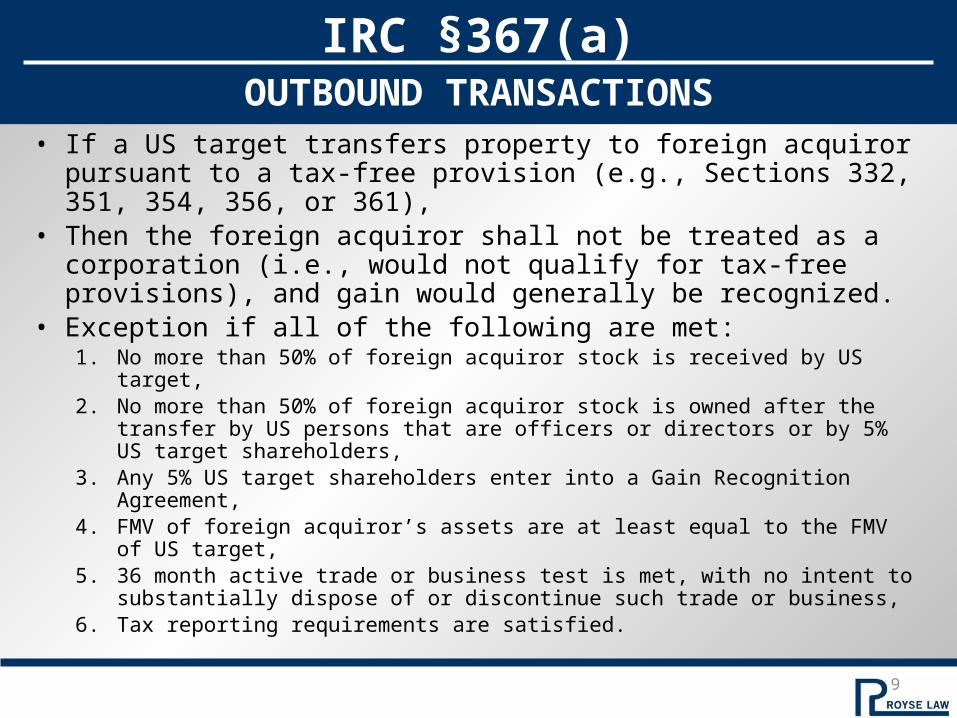

• If a US target transfers property to foreign acquiror pursuant to a tax-free provision (e.g., Sections 332, 351, 354, 356, or 361),

• Then the foreign acquiror shall not be treated as a corporation (i.e., would not qualify for tax-free provisions), and gain would generally be recognized.

• Exception if all of the following are met:1. No more than 50% of foreign acquiror stock is received by US target,2. No more than 50% of foreign acquiror stock is owned after the transfer by US

persons that are officers or directors or by 5% US target shareholders,3. Any 5% US target shareholders enter into a Gain Recognition Agreement,4. FMV of foreign acquiror’s assets are at least equal to the FMV of US target,5. 36 month active trade or business test is met, with no intent to substantially

dispose of or discontinue such trade or business,6. Tax reporting requirements are satisfied.

IRC §367(a)OUTBOUND TRANSACTIONS

10

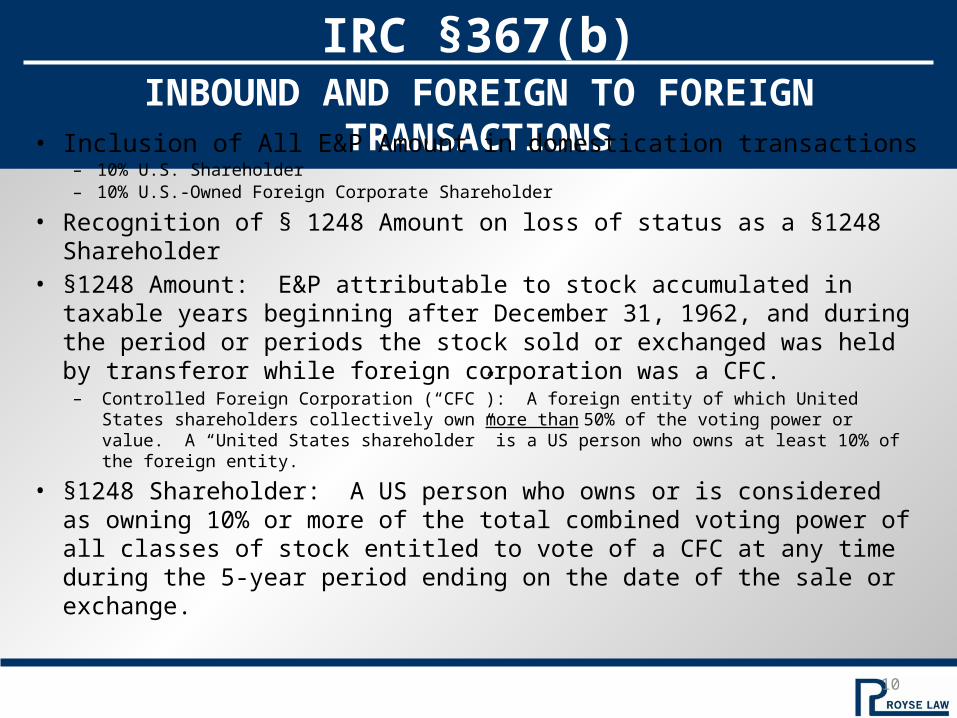

IRC §367(b)INBOUND AND FOREIGN TO FOREIGN TRANSACTIONS

• Inclusion of All E&P Amount in domestication transactions – 10% U.S. Shareholder– 10% U.S.-Owned Foreign Corporate Shareholder

• Recognition of § 1248 Amount on loss of status as a §1248 Shareholder• §1248 Amount: E&P attributable to stock accumulated in taxable years

beginning after December 31, 1962, and during the period or periods the stock sold or exchanged was held by transferor while foreign corporation was a CFC.– Controlled Foreign Corporation (“CFC”): A foreign entity of which United States shareholders

collectively own more than 50% of the voting power or value. A “United States shareholder” is a US person who owns at least 10% of the foreign entity.

• §1248 Shareholder: A US person who owns or is considered as owning 10% or more of the total combined voting power of all classes of stock entitled to vote of a CFC at any time during the 5-year period ending on the date of the sale or exchange.

11

• Seller of Controlled Foreign Corporation (CFC) must treat as dividend gain to extent of E&P

• §1248 inclusion carries foreign tax credits• §1248 amount determined at year end and pro rated

based on day count, so post closing events can have an effect on the §1248 amount

• Controlled Foreign Corporations (“CFCs”)– A foreign entity is classified as a CFC if it has “United States

Shareholders” who collectively own more than 50% of the voting power or value of the company. For the purposes of the CFC rules, a “United States Shareholder” is defined as US persons holding at least a 10% interest in the foreign corporation.

IRC §1248SUBPART F INCOME

12

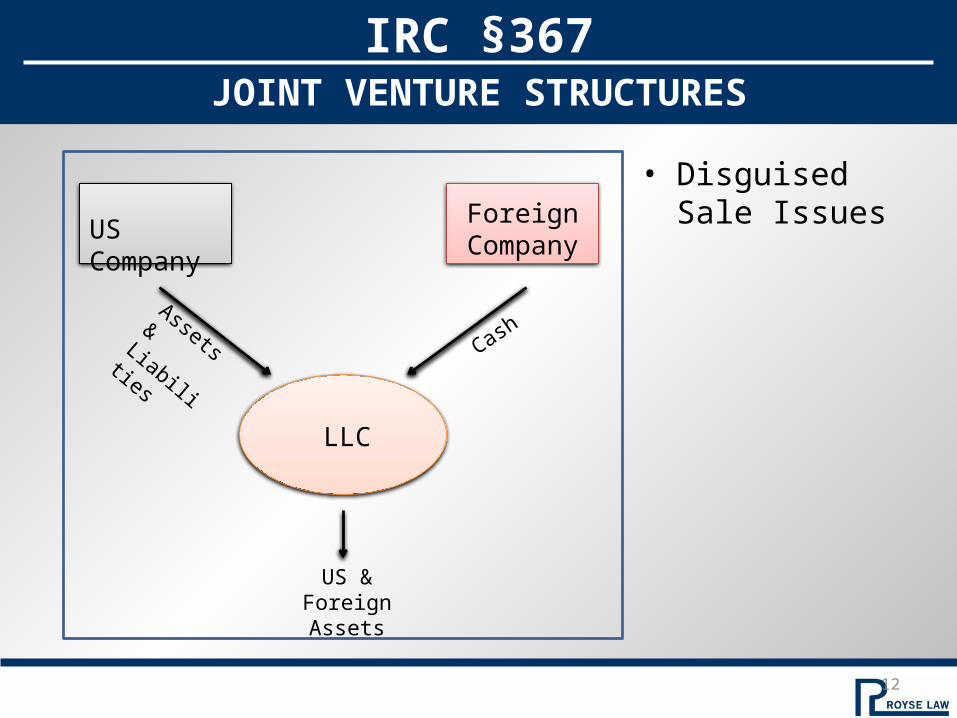

• Disguised Sale IssuesUS Company Foreign

Company

LLC

Assets & Liabilities

Cash

US & Foreign Assets

IRC §367JOINT VENTURE STRUCTURES

13

• The IRS may tax outbound reorganization and/or tax foreign acquiror as a U.S. taxpayer:– If ownership of former U.S. target shareholders in foreign acquiror is 80% or more

then foreign acquiror is treated as a U.S. company – If ownership continuity is between 60 and 80%, then the foreign acquiror is NOT

treated as a U.S. company, but U.S. tax attributes cannot be used to offset gains– 20% excise tax on stock-based compensation upon certain corporate inversion

transactions.

• Exception:– Companies with “substantial business activities” in the foreign jurisdiction; prior

facts and circumstances test compares activities of company in foreign jurisdiction with activities of company globally.

– New proposed regulations (REG-107889-12, T.D. 9592) require group employees, group assets, and group income located or derived in foreign country of incorporation to equal at least 25% of worldwide group employees, assets, and income. The “group income” definition makes this threshold very difficult in some cases.

IRC §7874ANTI-INVERSION RULES

14

• The US acquiror of a foreign-owned, foreign target may make a §338(g) election, which steps up basis and eliminates E&P and foreign tax credits.

• The target may be able to offset §338(g) gains with net operating losses.

• The acquiror of a US target with a foreign subsidiary may make a §338(g) election with regard to both the US target and the foreign subsidiary, triggering deemed sales of the target’s stock in the subsidiary and the subsidiary’s assets and a §1248 dividend.

IRC §338(g)STOCK PURCHASE AS ASSET ACQUISITION ELECTION

15

Connecting founders with investors.

Providing business, tax, and personal finance ideas to founders and executives.

Offering legal document templates and more.

www.RoyseUniversity.com

www.RoyseLink.com

www.rroyselaw.com/ijuris_login_jp.html

ADDITIONAL RESOURCES

16

www.rroyselaw.comTwitter: RoyseLaw

PALO ALTO1717 Embarcadero Road

Palo Alto, CA 94306

LOS ANGELES1150 Santa Monica Blvd.

Suite 1200Los Angeles, CA 90025

SAN FRANCISCO135 Main Street

12th FloorSan Francisco, CA 94105

![AMERICAN BAR ASSOCIATION & INTERNATIONAL BAR … · [AMERICAN BAR ASSOCIATION & INTERNATIONAL BAR ASSOCIATION] AFFIDAVIT OF OBLIGATION INTERNATIONAL COMMERCIAL LIEN (This is a verified](https://static.fdocuments.in/doc/165x107/5f15d353e4731c257a32dad2/american-bar-association-international-bar-american-bar-association-.jpg)

![AMERICAN BAR ASSOCIATION & INTERNATIONAL BAR ASSOCIATION · PDF file15.10.2015 · [AMERICAN BAR ASSOCIATION & INTERNATIONAL BAR ASSOCIATION] AFFIDAVIT OF OBLIGATION INTERNATIONAL](https://static.fdocuments.in/doc/165x107/5a9e216b7f8b9a420a8e06ec/american-bar-association-international-bar-association-american-bar-association.jpg)

![AMERICAN BAR ASSOCIATION & INTERNATIONAL …...[AMERICAN BAR ASSOCIATION & INTERNATIONAL BAR ASSOCIATION] AFFIDAVIT OF OBLIGATION INTERNATIONAL COMMERCIAL LIEN (This is a verified](https://static.fdocuments.in/doc/165x107/5f15d35de4731c257a32db06/american-bar-association-international-american-bar-association-.jpg)