c 2020 Giorgi Pertaia - ufdcimages.uflib.ufl.edu

85

APPLICATIONS OF CONDITIONAL VALUE AT RISK NORM AND BUFFERED PROBABILITY IN RISK MANAGEMENT By GIORGI PERTAIA A DISSERTATION PRESENTED TO THE GRADUATE SCHOOL OF THE UNIVERSITY OF FLORIDA IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF DOCTOR OF PHILOSOPHY UNIVERSITY OF FLORIDA 2020

Transcript of c 2020 Giorgi Pertaia - ufdcimages.uflib.ufl.edu

APPLICATIONS OF CONDITIONAL VALUE AT RISK NORM AND BUFFEREDPROBABILITY IN RISK MANAGEMENT

By

GIORGI PERTAIA

A DISSERTATION PRESENTED TO THE GRADUATE SCHOOLOF THE UNIVERSITY OF FLORIDA IN PARTIAL FULFILLMENT

OF THE REQUIREMENTS FOR THE DEGREE OFDOCTOR OF PHILOSOPHY

UNIVERSITY OF FLORIDA

2020

c© 2020 Giorgi Pertaia

2

I dedicate this to my beloved family.

3

ACKNOWLEDGEMENTS

I would like to thank my advisor, Prof. Stan Uryasev, for his outstanding guidance and

mentorship. Prof. Uryasev helped me significantly improve my knowledge and skills. He set the

research goals, patiently and rigorously checked, corrected and edited all my work, as well as,

provided very helpful guidelines for writing, structuring and improving projects and papers that I

worked on.

I grateful to Prof. Artem Prokhorov, Prof. Morton Lane, Mr. Matthew Murphy for their

collaboration on research papers and many insightful discussions. Also, I would like to thank

Viktor Kuzmenko, Alex Zrazhevsky and entire AORDA team for their help with numerical

studies.

I thank my family for their unconditional love, limitless support, understanding and

encouragement.

I would like to express special thanks to my teachers and mentors, Prof. Teimuraz

Toronjadze, Prof. Vakhtang Shelia and Prof. Jean-Philippe Richard, who were essential in my

education and taught me more than I thought I could learn.

I am thankful to my committee members, Prof. Panos Pardalos, Prof. Hongcheng Liu and

Prof. Banerjee Arunava for providing their expertise and support.

This research was partially supported by the DARPA EQUiPS program, grant SNL

014150709, Risk-Averse Optimization of Large-Scale Multiphysics Systems.

4

TABLE OF CONTENTSpage

ACKNOWLEDGEMENTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

LIST OF TABLES. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

LIST OF FIGURES. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

ABSTRACT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

CHAPTER

1 INTRODUCTION AND OPENING REMARKS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

2 FINITE MIXTURE FITTING WITH CVAR CONSTRAINTS . . . . . . . . . . . . . . . . . . . . . . . . . . 12

2.1 Motivation. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 122.2 Finite Mixture and CVaR-distances Between Distributions . . . . . . . . . . . . . . . . . . . . . . . . . 13

2.2.1 CVaR - norm of Random Variables . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 132.2.2 CVaR -distance. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

2.3 Distribution Approximation by a Finite Mixture . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 152.3.1 CVaR -distance Minimization . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 152.3.2 CVaR -constraint . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 162.3.3 Cardinality Constraint . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

2.4 Case Study: Fitting Mixture by minimizing CVaR-distance . . . . . . . . . . . . . . . . . . . . . . . . 19

3 OPTIMAL ALLOCATION OF RETIREMENT PORTFOLIOS . . . . . . . . . . . . . . . . . . . . . . . . . 25

3.1 Motivation. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 253.2 Notations. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 273.3 Model Formulation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 283.4 Special Case of General Formulation. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 333.5 Simulation of Return Sample Paths and Mortality Probabilities . . . . . . . . . . . . . . . . . . . . . 34

3.5.1 Historical Simulations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 343.5.2 Mortality Probabilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35

3.6 Case Study . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 363.6.1 Case Study Parameters . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 363.6.2 Optimal Portfolio. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 373.6.3 Expected Shortage Time for Different Cash Outflows . . . . . . . . . . . . . . . . . . . . . . . . 45

4 A NEW APPROACH TO CREDIT RATINGS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

4.1 Motivation. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 494.2 Credit Ratings and Probability of Exceedance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 524.3 Motivation for bPoE-based ratings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 544.4 bPoE Definition and Estimation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 584.5 bPoE Ratings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 604.6 Uncovered Call Options Investment Strategy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64

5

4.7 Application to Optimal Step-Up CDO Structuring . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 664.7.1 Optimal CDO Structuring with PoE-Based Ratings. . . . . . . . . . . . . . . . . . . . . . . . . . . 674.7.2 Optimal CDO Structuring with bPoE-Based Ratings . . . . . . . . . . . . . . . . . . . . . . . . . 71

5 SUMMARY AND CONCLUSION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 78

REFERENCES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 80

BIOGRAPHICAL SKETCH . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 85

6

LIST OF TABLESTables page

2-1 Parameters of normal distributions in the mixture fitted with EM. . . . . . . . . . . . . . . . . . . . . . . . 20

2-2 CVaRs of empirical distribution and normal mixture fitted by the EM algorithm . . . . . . . . . . 20

2-3 Weights of the mixture calculated with CVaR-distance minimization . . . . . . . . . . . . . . . . . . . . 21

2-4 CVaRs of empirical and mixture distributions, fitted with CVaR constraints . . . . . . . . . . . . . . 21

3-1 USA Mortality table for the year 2016 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

3-2 The list of assets in the retirement portfolio. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37

3-3 Average investment in assets, L = $ 10,000, optimistic out-of-sample paths . . . . . . . . . . . . . . 40

3-4 Average investment in assets, L = $ 30,000, optimistic out-of-sample paths . . . . . . . . . . . . . . 40

3-5 Average investment in assets, L = $ 50,000, optimistic out-of-sample paths . . . . . . . . . . . . . . 41

3-6 Average investment in assets, L = $ 70,000, optimistic out-of-sample paths . . . . . . . . . . . . . . 41

3-7 Average investment in assets, L = $ 90,000, optimistic out-of-sample paths . . . . . . . . . . . . . . 41

3-8 Average investment in assets, L = $ 10,000, pessimistic out-of-sample paths . . . . . . . . . . . . . 42

3-9 Average investment in assets, L = $ 25,000, pessimistic out-of-sample paths . . . . . . . . . . . . . 42

3-10 Average investment in assets, L = $ 30,000, pessimistic out-of-sample paths . . . . . . . . . . . . . 43

3-11 Average investment in assets, L = $ 50,000, pessimistic out-of-sample paths . . . . . . . . . . . . . 43

4-1 S&P global corporate average cumulative default rates (1981-2015) (%). . . . . . . . . . . . . . . . . 54

4-2 Revised ratings for buffered probability of default. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 63

4-3 PoE and bPOE constraint right hand sides and corresponding ratings.. . . . . . . . . . . . . . . . . . . . 73

4-4 Numerical results for CDO structuring problem with three types of risk constraints. . . . . . 74

4-5 Numerical results for Problem PoE and Problem bPoE with stressed scenarios.. . . . . . . . . . . 75

4-6 Solution of ”Problem PoE” with stressed scenarios . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 75

4-7 Solution of ”Problem bPoE” with stressed scenarios . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 75

7

LIST OF FIGURESFigures page

2-1 QQ plot of mixture with parameters calculated with EM . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

2-2 QQ plot of the mixture with parameters calculated by minimizing CVaR-distance . . . . . . . . 23

2-3 Analog of QQ plots, but CVaRs are plotted instead of the quantiles . . . . . . . . . . . . . . . . . . . . . . 24

3-1 Mortality probability graph . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35

3-2 Portfolio values for optimistic out-of-sample paths . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44

3-3 ETS values for the optimistic sample paths . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

3-4 ETS values for the pessimistic sample paths . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47

3-5 Relationship between expected estate value and the ETS, for the optimistic sample paths.. 48

4-1 Relationship between PoE and VaR. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 55

4-2 Loss distributions for two companies with equal PoE.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 56

4-3 Relationship between bPoE and CVaR.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 57

4-4 Relationship between bPoE and PoE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 63

4-5 CDO attachment and detachment points. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 68

4-6 Discounted CDO income compared to CDO payments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 76

8

Abstract of Dissertation Presented to the Graduate Schoolof the University of Florida in Partial Fulfillment of theRequirements for the Degree of Doctor of Philosophy

APPLICATIONS OF CONDITIONAL VALUE AT RISK NORM AND BUFFEREDPROBABILITY IN RISK MANAGEMENT

By

Giorgi Pertaia

August 2020Chair: Stan UryasevMajor: Industrial and Systems Engineering

This study targets various applications of Conditional Value at Risk (CVaR) and Buffered

Probability of Exceedance (bPoE) in risk management, financial engineering and statistical

analysis. Recent developments of CVaR-Norm and bPoE measure, allow supplementing existing

methodologies with more efficient and conservative measures of risk. This study explores 3

applications of these novel methodologies.

First part explores application of CVaR-Norm for finite mixture fitting with additional

constraints on the mixture tails. This approach focuses on a subset of the mixture parameters,

which allows to effectively solve the mixture fitting problem with additional constraints.

Second part develops a multistage portfolio selection model with CVaR constraints. This

model proposes a novel approach of expected estate maximization for a retiree, while

guaranteeing specific cash outflows from the portfolio over multiple time periods.

The third part explores applications of bPoE for credit risk analysis and financial

engineering. This methodology proposes to supplement Probability of Exceedance (PoE) based

credit ratings with bPoE based ratings. bPoE based ratings have 2 major advantages compared to

existing PoE based methodologies. Firstly, bPoE provides a more conservative risk measure

compared to optimistic PoE measure, since bPoE is sensitive to the heaviness ot the distribution

tail. Secondly, bPoE based ratings can be used for financial engineering since bPoE function has

remarkable mathematical properties compared to usual PoE measure, that allows development of

very efficient optimization algorithms.

9

CHAPTER 1INTRODUCTION AND OPENING REMARKS

First part of this thesis explores applications of CVaR norm in finite mixture fitting with

additional constraints on tail of the mixture. Standard methods of fitting finite mixture models

take into account the majority of observations in the center of the distribution. This paper

considers the case where the decision maker wants to make sure that the tail of the fitted

distribution is at least as heavy as the tail of the empirical distribution. For instance, in nuclear

engineering, where probability of exceedance (PoE) needs to be estimated, it is important to fit

correctly tails of the distributions. The goal of this paper is to supplement the standard

methodology and to assure an appropriate heaviness of the fitted tails. We consider a new

Conditional Value-at-Risk (CVaR) distance between distributions, that is a convex function with

respect to weights of the mixture. We have conducted a case study demonstrating efficiency of the

approach. Weights of mixture are found by minimizing CVaR distance between the mixture and

the empirical distribution. We have suggested convex constraints on weights, assuring that the tail

of the mixture is as fat as the tail of empirical distribution.

The second part of the thesis develops a multistage portfolio selection model for retirement

portfolios. A retiree with a savings account balance, but without a pension is confronted with an

important investment decision that has to satisfy two conflicting objectives. Without a pension the

function of the savings is to provide post-employment income to the retiree. At the same time,

most retirees will want to leave an estate to their heirs. Guaranteed income can be acquired by

investing in an annuity. However, that decision takes funds away from investment alternatives that

might grow the estate. The decision is made even more complicated because one does not know

how long one will live. A long life expectancy may suggest more annuities, and short life

expectancy could promote more risky investments. However there are very mixed opinions about

either strategy. This paper develops a stochastic programming model to frame this complicated

problem. The objective is to maximize expected terminal net worth (the estate), subject to CVaR

constraints on target income shortfalls. The CVaR constraints on cash outflow shortage, are

applied each year of the portfolio investment horizon. Case study was conducted using two

10

variations of the model. The parameters used in this case study correspond to typical retirement

situation. The results of the case study show that if the market forecasts are pessimistic, it is

optimal to invest in annuity.

The third part of the thesis develops a credit rating system based on a novel measure of risk

called the Buffered Probability of Exceedance (bPoE). Credit ratings are fundamental in assessing

the credit risk of a security or debtor. The failure of the Collateralized Debt Obligation (CDO)

ratings during the financial crisis of 2007-2008 and the massive undervaluation of corporate risk

leading up to the crisis resulted in review of rating approaches. Yet the fundamental metric that

guides the construction of credit ratings has not changed. This paper proposes a new methodology

based on a buffered probability of exceedance. The new approach offers a conservative risk

assessment, with substantial conceptual and computational benefits. The new approach is

illustrated using several examples of structuring step-up CDO.

11

CHAPTER 2FINITE MIXTURE FITTING WITH CVAR CONSTRAINTS

2.1 Motivation

Finite mixtures (or mixture distributions) allow to model complex characteristics of a

random variable. They are frequently used in the cases where data are not normally distributed.

For example, finite mixtures are well suited for modeling heavy tails. Another application of

finite mixtures is to model multi-modal random variables.

The ability to model heavy tails is important in risk management and financial engineering.

Finite mixtures are frequently used in these fields to model a wide variety of random variables.

For example, paper [1]estimates Value-at-Risk (VaR) for a heavy-tailed return distribution using a

finite mixture. Paper [2] models asset prices with a log-normal mixture. Paper [3] models the

error distribution of the GARCH(1,1) with a finite mixture, the resulting model is called

NM-GARCH.

Finite mixtures are also frequently used in machine learning for clustering and classification

of the data. For example, paper [4] uses the Gaussian mixture models for image classification.

Expectation Maximization (EM) is a popular algorithm for fitting mixture models. In

general, EM solves a nonconvex optimization problem with respect to parameters of the mixture.

The original EM algorithm, as defined in [5], does not allow for additional constraints in the

problem. There exist modifications of original EM algorithm with different constraints. For

example [6] presents a modified EM algorithm that can handle linear equality constraints on the

parameters. Papers [7] and [8] presents modification of EM algorithm that can handle linear

equality and inequality constraints and linear and nonlinear equality constraints respectfully.

This article derives a new methodology for fitting mixture models with constraints on length

of the tails of the mixture distribution. The methodology is based on the concept of Conditional

Value at Risk (CVaR) distance between distributions. In finance, CVaR is also called Expected

Shortfall (ES). This paper deals with the weights of the individual distributions in the mixture and

imposes CVaR constraints on the tails of the mixture. The resulting problem is a convex

minimization problem. We also formulate a problem with cardinality constraints on the number of

12

nonzero weights in the mixture. In this case, the resulting problem is mixed-integer minimization

problem with convex objective function and convex constraints on CVaRs of the fitted mixture .

We present a case study that illustrates a method of fitting a normal (Gaussian) mixture such that

the resulting tales of the mixture are at least as heavy as the tails of the empirical distribution.

2.2 Finite Mixture and CVaR-distances Between Distributions

Let F1(x,θ1), . . . ,Fm(x,θm) be a set of cumulative distribution functions (CDFs), where

x ∈ R and θi is the parameter set of a distribution Fi. The CDF of the mixture of

F1(x,θ1), . . . ,Fm(x,θm) is defined as follows.

Definition 1. Let p = (p1, . . . , pm)T be the column vector of weights of the mixture, p≥ 0 and

pT 1 = 1, the CDF of a finite mixture is defined as

Fp,θ (x) =m

∑j=1

p jFj(x,θ j). (2-1)

In this definition, θ = (θ1, . . . ,θm) is the vector of parameters. Further, we will omit θ from

Fp,θ (x) and write the CDF of the mixture as Fp(x). Normal distributions are usually used for

construction of finite mixtures.

2.2.1 CVaR - norm of Random Variables

We denote the CVaR of a random variable (r.v.) X at the the confidence level α ∈ [0,1) by

CVaRα(X),

CVaRα(X) = minC

(C+

11−α

E[X−C]+), (2-2)

where [x]+ = max(x,0), C ∈ R and E is an expectation operator. if X is a continuous random

variable then

CVaRα(X) = E(X |X > qα(X))

13

where qα(X) is the α quantile of X

qα(X) = infx ∈ R | P(X > x)≤ 1−α

with P denoting probability. Additionally, It can be shown that CVaR0(X) = E(X). CVaRα(X) is

a convex measure of risk with respect to X and satisfies coherent risk measure properties proposed

by Artzner in [9]. For a comprehensive analysis of the CVaRα(X) risk-measure see [10], [11].

We denote by ‖X‖α the CVaRα -norm of X at the confidence level α ∈ [0,1),

‖X‖α = CVaRα(|X |). (2-3)

CVaRα -norm is the expectation of 1−α largest absolute values of X . The CVaRα -norm for the

deterministic case was introduced in [12] and for the stochastic case in [13]. CVaRα -norm

satisfies the following standard properties:

1. If ‖X‖α = 0⇒ X ≡ 0 almost surely (a.s.),

2. ‖λX‖α = |λ |‖X‖α for any λ ∈ R (positive homogeneity),

3. ‖X +Y‖α ≤ ‖X‖α +‖Y‖α for any r.v.s X ,Y , defined on the same probability space

(Ω,µ,F ) (triangle inequality).

2.2.2 CVaR -distance

This section introduces the concept of CVaRα -distance between distributions. The

CVaRα -distance was defined by Pavlikov and Uryasev [14] in the context of discrete distributions.

A distance function on a set V is defined as a map d : V ×V 7→ R satisfying the following

conditions ∀x,y ∈V :

1. d(x,y)≥ 0 (non-negativity axiom);

2. d(x,y) = 0 if and only if x = y (identity of indiscernibles);

3. d(x,y) = d(y,x) (symmetry);

4. d(x,y)≤ d(x,z)+d(z,y) (triangle inequality).

14

Assume that there are two r.v.s Y and Z, with corresponding CDFs, F(x) and G(x). Assume

also that there is some auxiliary r.v. H with CDF W (x). We define a new r.v. XW , representing the

difference between F(x) and G(x), as

XW (F,G) = F(H)−G(H).

Note, that the auxiliary r.v. H may coincide with one of the r.v.s Y and Z, i.e., W (x) may be equal

to F(x) or G(x).

CVaRα distance at some confidence level α ∈ [0,1), between distributions of two r.v.s

Y and Z with corresponding CDFs FY and GZ is defined as

dWα (F,G) = ‖XW (F,G)‖α , (2-4)

where H is an auxiliary r.v. with CDF WH .

2.3 Distribution Approximation by a Finite Mixture

2.3.1 CVaR -distance Minimization

This section presents a method of approximating CDF F with the mixture Fp , by finding

weights p in the mixture. Other parameters of the mixture (such as mean and variance in case of

Gaussian mixtures) are assumed to be estimated using EM or maximum likelihood. The objective

is to minimize the CVaRα distance (2-4) between F and Fp . It will be shown later in the paper,

that the resulting problems of fitting the mixture, are convex programming problems. In this

section, only two types of constraints are considered. The first type of constraints, simply assures

that each element of vector p is positive, and the second type of constraints assures that the

elements of p sum to 1. The CVaRα constraints will be added in the next section.

We approximate CDF F(x) with the mixture Fp(x) by finding weights p in the following

minimization problem:

15

minp

dWα (F,Fp)

s.t. (2-5)

pT 1 = 1

p≥ 0

Further we prove that, function Q(p) = dWα (F,Fp) is a convex function of weights p.

Proposition 2.3.1. Q(p) = dWα (F,Fp) is a convex function of p.

Proof. Let λ ∈ [0,1]. From the definition of Fp(x) and properties of CVaR norm:

Q(λ p+(1−λ )p) = dWα (F,Fλ p+(1−λ )p) = ‖XW (F,Fλ p+(1−λ )p)‖α =

= ‖F(H)−Fλ p+(1−λ )p(H)‖α = ‖F(H)−m

∑j=1

(λ p j +(1−λ )p j)Fj(H)‖α =

= ‖λ [F(H)−m

∑j=1

p jFj(H)]+(1−λ )[F(H)−m

∑j=1

p jFj(H)]‖α ≤

≤ λ‖F(H)−m

∑j=1

p jFj(H)‖α +(1−λ )‖F(H)−m

∑j=1

p jFj(H)‖α =

= λQ(p)+(1−λ )Q(p).

The idea of using the CVaRα - norm to fit the finite mixtures, was first explored by V.

Zdanovskaya and S. Uryasev in an unpublished report.

2.3.2 CVaR -constraint

This section adds CVaRα constraints to the problem (2-5). The CVaRα constraints ensure a

specified heaviness of the tail. For example, if some portfolio loss distribution is approximated by

a mixture, CVaRα constraints guarantee that CVaRα of the fitted mixture will be greater than or

equal to the specified threshold.

Let Xp be a r.v. having CDF of the mixture of distributions Fp(x), defined by (2-1).

16

Proposition 2.3.2. CVaRα(Xp) is a concave function of p.

Proof. Using the definition of CVaRα and X

CVaRα(Xλ p+(1−λ )p) = minC

(C+

11−α

∫R

[x−C

]+dFλ p+(1−λ )p(x))=

= minC

(C+

11−α

∫R

[x−C

]+d

(m

∑j=1

(λ p j +(1−λ )p j)Fj(x)

))=

= minC

(C+

11−α

m

∑j=1

(λ p j +(1−λ )p j)∫R

[x−C

]+dFj(x)

).

Let

z j(C) =1

1−α

∫R

[x−C

]+dFj(x),

then

CVaRα(Xλ p+(1−λ )p) = minC

(C+

m

∑j=1

(λ p j +(1−λ )p j)z j(C)

)=

= minC

(λ [C+

m

∑j=1

p jz j(C)]+(1−λ )[C+m

∑j=1

p jz j(C)]

)≥

≥ λ minC

(C+

m

∑j=1

p jz j(C)

)+(1−λ )min

C

(C+

m

∑j=1

p jz j(C)

)=

= λCVaRα(Xp)+(1−λ )CVaRα(Xp).

Again, we are given the random variable Y and its distribution F that we want to ap-

proximate with the mixture distribution Fp. The goal is to construct a mixture Fp such that,

CVaRα(k)(Xp)≥ CVaRα(k)(Y ), where Xp is a r.v. with distribution Fp and α(k) ∈ α1, ...,αK is

some set of confidence levels. Adding CVaRα constraints to the problem (2-5) we have,

17

minp

dWα (F,Fp) (2-6)

s.t.

CVaRα(k)(Xp)≥ CVaRα(k)(Y ), k = 1, . . . ,u

pT 1 = 1

p≥ 0

The objective function in (2-6) is convex and the feasible region is the intersection of convex sets,

thus (2-6) is a convex optimization problem.

2.3.3 Cardinality Constraint

In certain applications, it might be important to limit the number of distributions in the fitted

mixture, or otherwise, the number of nonzero weights in the mixture. This section presents a

variant of model (2-5) with constraints on the maximum number of nonzero weight in p. Initially,

a mixture with m distributions if fitted to the data, using some standard method, for example

maximum likelihood. Next, the problem (2-5) is solved with additional constraint that only

M ≤ m weights in p are allowed to be nonzero.

Let us denote

card(p) =m

∑i=1

g(pi), where g(pi) =

1 if pi > 0

0 if pi ≤ 0.

Problem (2-5) with cardinality constraint is rewritten as

minp

dWα (F,Fp) (2-7)

s.t.

card(p)≤M

(2-8)

18

pT 1 = 1

p≥ 0

Equivalently:

minp

dWα (F,Fp) (2-9)

s.t.m

∑j=1

r j ≤M

r j ∈ 0,1, j = 1, . . . ,m

p j ≤ r j, j = 1, . . . ,m

pT 1 = 1,

p≥ 0.

Problem (2-9) is a mixed integer programming problem (MIP) and can be solved using standard

MIP solvers.

2.4 Case Study: Fitting Mixture by minimizing CVaR-distance

This section solves problem (2-6) that fits the finite mixture to an empirical CDF. The

empirical cumulative distribution for some sample Y = y1, . . . ,yn is defined as,

Fn(Y ) =1n

n

∑i=1

1y≥yi, (2-10)

where n is the number of observations and 1∗ is an indicator function. This case study uses the

data considered in the research paper [15] and the corresponding case study [16]. Portfolio

Safeguard (PSG) version 2.3 is used to solve the optimization problems and MATLAB for

plotting and data management. The case study codes and data are posted in [17]. We used PSGs

precoded CVaR function to set the constraints on the mixture. In this case study, the

CVaRα -distance with α = 0 is considered. The distributions in the mixture are chosen to be

19

Normal (Gaussian) and therefore the resulting mixture is the Gaussian mixture

Fp(x) =m

∑j=1

p jΦ(x,µi,σi), (2-11)

where Φ(x,µi,σi) is a normal CDF with mean µi and standard deviation σi. Parameters µi and σi

are estimated with EM algorithm. The estimated parameters of the mixture are in Table 2-1.

Table 2-1. Parameters of normal distributions in the mixture fitted with EM.j µ j σ j p j1 0.0020 0.0014 0.19702 0.0100 0.0046 0.18823 0.0344 0.0144 0.23824 0.0583 0.0206 0.25815 0.0957 0.0365 0.1185

For the mixture with parameters in Table 2-1 and the empirical distribution, we have

calculated CVaR0.9, CVaR0.95, CVaR0.99 and CVaR0.995, see Table 2-2.

Table 2-2. CVaRs of empirical distribution and normal mixture fitted by the EM algorithm.CVaRα(k)(Xp) is the CVaR of mixture with confidence α(k) and CVaRα(k)(Y ) is theCVaR of empirical distribution. The entries in “Difference” column areCVaRα(k)(Xp)−CVaRα(k)(Y ).

k α(k) CVaRα(k)(Xp) CVaRα(k)(Y ) Difference1 90% 0.1118 0.1115 0.00022 95% 0.1300 0.1292 0.00073 99% 0.1626 0.1666 -0.00404 99.5% 0.1735 0.1814 -0.0079

Table 2-2 column “α(k)” contains confidence levels. In the column “CVaRα(k)(X)” are

CVaRs of the mixture and column “CVaRα(k)(Y )” contains CVaRs of the empirical distribution.

The column labeled as “Difference” shows the difference between CVaR of mixture and CVaR of

empirical distribution (CVaRα(k)(Xp)−CVaRα(k)(Y )).

20

Further, the CVaR distance, as given in Problem (2-6), is minimized with respect to the

weights. CVaRs of the mixture are constrained to be greater or equal to the empirical CVaRs

minp

dWα (Fn,Fp) (2-12)

s.t. CVaRα(k)(Xp)≥ CVaRα(k)(Y ), k = 1, . . . ,u

pT 1 = 1

p≥ 0

Optimal weights of the mixture, obtained by solving (2-12), are given in Table 2-3.

Table 2-3. Weights of the mixture calculated with CVaRα -distance minimization (2-6).j p j1 0.19362 0.29113 0.12264 0.20715 0.1857objective 0.030791

The CVaRs for the resulting mixture are shown in Table 2-4, alongside the CVaRs for the

corresponding empirical distribution.

Table 2-4 shows that CVaR constraints are satisfied, i.e. CVaRα(k)(X) ≥ CVaRα(k)(Y ),

k = 1, . . . ,4. However only the CVaR with α = 99.5% is active (CVaR99.5%(X) =

CVaR99.5%(Y ) = 0.1814), for other CVaRs the inequality is strict.

Table 2-4. CVaRs of empirical distribution and normal mixture fitted by minimizing CVaRdistance with CVaR constraints. CVaRα(k)(Xp) is the CVaR of mixture with confidenceα(k) and CVaRα(k)(Y ) is the CVaR of empirical distribution. The entries in“Difference” column are CVaRα(k)(Xp)−CVaRα(k)(Y ).

k α(k) CVaRα(k)(X) CVaRα(k)(Y ) Difference1 90% 0.126 0.1115 0.01452 95% 0.1428 0.1292 0.01363 99% 0.1715 0.1666 0.00494 99.5% 0.1814 0.1814 0.0000

21

Figure 2-1. QQ plot of mixture with parameters calculated with EM. “X” axis shows quantiles ofthe mixture and “Y” axis shows quantiles of the empirical distribution.

The quantile-quantile (QQ) plots are used to visually compare quantiles of empirical

distribution and quantiles of fitted mixture. QQ plots graph the quantiles of one distribution

against quantiles of another distribution (pair of quantiles are evaluated for the same probability).

If the two distributions are identical, the points (pairs of quantiles) will form a straight line with 0

intercept and 45 degree slope.

Figure 2-1 shows the QQ plot for the mixture fitted with just EM algorithm. The quantiles

of empirical distribution are on “Y” axis and quantiles of fitted mixture are on “X” axis. The

mixture is fitted well in the center of the distribution, since in the center, the mixture quantiles and

empirical quantiles form a straight line with 45 degree slope. However, the points corresponding

to the quantiles of the right tails are above the 45 degree line, i.e. the mixture fited with just EM

algorithm has thinner tails than the empirical distribution (mixture quantiles are smaller for the

same probability values). Figure 2-2 shows the QQ plot for the mixture fitted with the CVaR

constraints. In this case, the quantiles on tails are closer to the empirical, however the quantiles

towards center are below the line, indicating that quantiles in the center of the mixture are larger

than corresponding quantiles in the empirical distribution.

22

Figure 2-2. QQ plot of the mixture with parameters calculated by minimizing CVaR-distance asdefined in (2-12). “X” axis shows quantiles of the mixture and “Y” axis showsquantiles of empirical distribution.

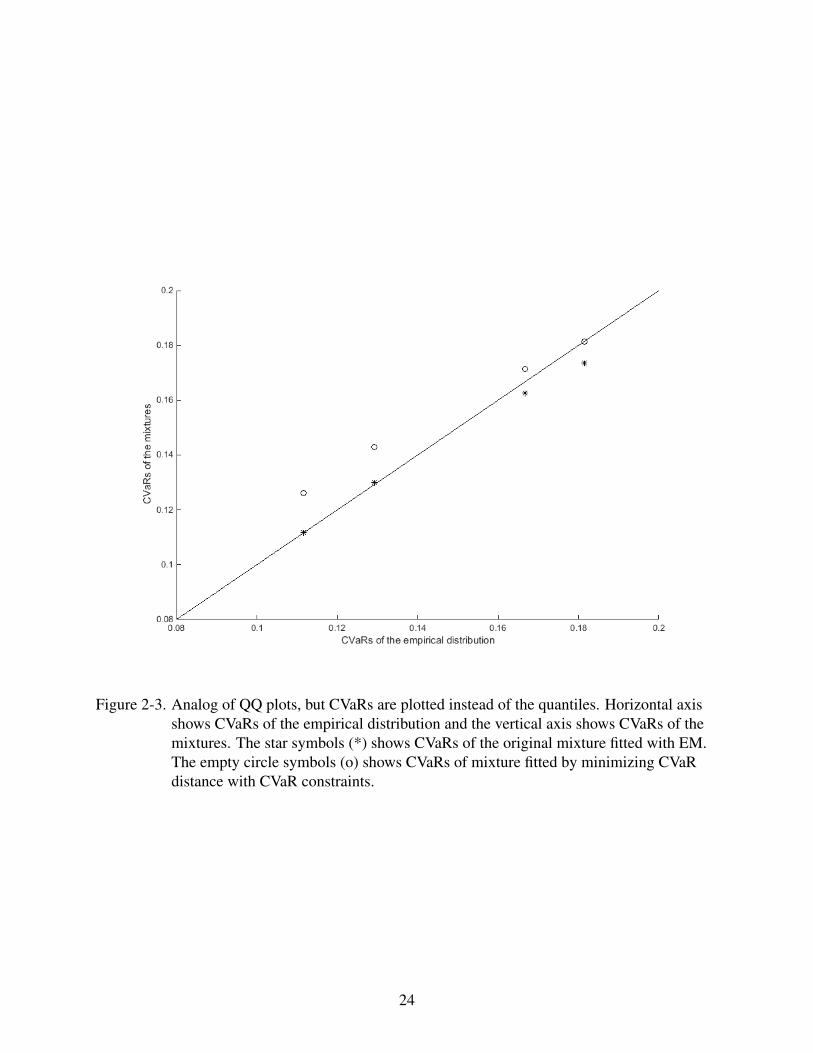

Similar to QQ plots we show CVaR to CVaR plot, which graphs two distribution CVaRs

against each other (evaluated for the same α values). The idea behind CVaR to CVaR plot is

identical to QQ plots.

Figure 2-3 shows CVaR to CVaR plot of the mixture fitted with EM and mixture fitted with

CVaR constraints. The CVaRs of the mixture fitted with CVaR constraints are heavier or equal to

the empirical CVaRs. In Figure 2-3 the points corresponding to the CVaRαs are above the line,

except for the last point, that is on the line. This indicates that only the last CVaRα constraint

(α(4) = 99.5%) is active and other CVaRs are heavier (larger) than specified in the right hand

side of the constraints.

23

Figure 2-3. Analog of QQ plots, but CVaRs are plotted instead of the quantiles. Horizontal axisshows CVaRs of the empirical distribution and the vertical axis shows CVaRs of themixtures. The star symbols (*) shows CVaRs of the original mixture fitted with EM.The empty circle symbols (o) shows CVaRs of mixture fitted by minimizing CVaRdistance with CVaR constraints.

24

CHAPTER 3OPTIMAL ALLOCATION OF RETIREMENT PORTFOLIOS

3.1 Motivation

The problem of selecting optimal portfolios for retirement has unique features that are not

addressed by more commonly used portfolio selection models used in trading. One distinct

feature of a retirement portfolio is that it should incorporate the life span of an investor. The

planning horizon depends on the age of investor, or more specifically, on a conditional life

expectancy. Another important feature is to guarantee, in some sense, that the individual will be

able to withdraw some amount of money every year from a portfolio by selling some predefined

amount of assets without injecting external funds. Finally, one of the questions that the models

tries to answer is, in what situation is it beneficial to invest in annuity instead of more risky assets.

Most of portfolio optimization literature considers portfolios focusing on risk minimization

with some budget and expected profit constraints. The famous mean-variance (or Markowitz)

portfolio [18] minimizes portfolio variance with constraints on the expected return. There are

many directions that extend the original mean-variance portfolio and deal with its shortcomings.

One direction is to substitute variance with some other risk measures. Variance does not

distinguish positive and negative portfolio returns, however investors are mostly concerned only

with negative returns. [11, 10] and [19] used Conditional Value-at Risk (CVaR) instead of the

variance. CVaR is a convex function of its random variable and therefore problems involving

CVaR can be solved efficiently in many cases. Another important risk measure, which is

frequently used in trading, is drawdown. Drawdown can be optimized with convex and linear

programming, see [20], [21] and [22]. Other extension of the portfolio theory focuses on dynamic

models. In dynamic models the decision to invest is made over time. The dynamic models can be

of two types, continuous-time and discrete-time (multistage) models. In continuous time, the

decision to invest is made continuously and in discrete-time, the investment decisions take place

on specific time moments. For the continuous-time portfolio selection see [23, 24]. For

discrete-time stochastic control model see [25]. A comprehensive literature review on dynamic

models is given in [26]. Multistage models can be formulated as stochastic optimization

25

problems. [27] and [28] developed a general multistage approach for modeling financial planning

problems. [29] and [30] use stochastic programming to solve dynamic cash flow matching and

asset/liability management problems, respectively. In general, it is very hard to solve multistage

stochastic optimization problems formulated with scenario trees, due to the size of the problem

(number of variables) growing beyond tractable bounds. It should be mentioned that calibration

of such trees is a difficult non-convex optimization problem.

In order to avoid the dimensionality problems, [31] models the investment decisions as

linear functions that remain same across all scenarios and produce the investment decision based

on previous performance of the asset.

Takano and Gotoh in [32] model the investment decisions with kernel method, resulting in

the nonlinear control functions depending upon returns of instruments.

We follow ideas of [32] and model multistage portfolio decision process using the kernel

method. The investment horizon is 35 years, starting from the retirement of the investor at the age

of 65. The objective is to maximize the discounted expected terminal wealth subject to constraints

on cash outflows from the portfolio. We generate multiple sample paths of assets prices,

simulated using historical data. for every sample path, the discounted weighted portfolio value is

calculated, where the probabilities of death are used as weights. The probability of death is

calculated from the U.S. mortality tables. The investor wants to have predetermined cash outflows

obtained by selling a portion of the portfolio. Risk of shortage of this cash outflows is managed

by penalizing the cash outflow shortage in the objective function. Furthermore, the monotonicity

constraints are imposed on the cash outflows from the portfolio. Without the monotonicity

constraint the model might not provide the necessary cash outflow on certain periods and instead,

reinvest that amount to increase the expected estate value.

We conducted a case study corresponding to a typical investment decision upon retirement,

in order to reveal the conditions leading to investments in annuities. Two types of asset return

sample paths are considered. First type assumes that the asset returns will be similar to the

historically observed rates of the asset. The second type of sample paths assumes the future asset

26

returns will be significantly lower. These sample paths are created by subtracting 12% from the

historical returns of all assets. The case study shows that for the first type of sample paths, where

rates are similar to the ones observed in the past, investment in the annuities is not optimal.

However, in the case when the asset growth rates are significantly lower, the model invests only in

the annuities.

3.2 Notations

We start with introduction of notations

• N := number of assets available for investments,

• S := number of sample paths,

• T := portfolio investment horizon,

• rsi,t := rate of return of asset i = 1, . . . ,N during period t = 1, . . . ,T in sample path

s = 1, . . . ,S; we will call rate of return by just return and denote the vector of returns by

rst = (rs

1,t , . . . ,rsN,t) ,

• vsm,t = rs

m, . . . ,rst−1 := set of returns observed from period m, until the end of period

t−1 (not including the returns rst ) for sample path s,

• dst := discount factor at time t for sample path s; discounting is done using inflation rate

ρst , ds

t = 1/(1+ρst )

t ,

• pt := probability that a person will die at the age 65+ t (conditional that he is alive at the

age of 65),

• yi := vector of control variables for investment adjustment function,

• f (vst ,yi) := investment adjustment function defining how much investment is made in

each sample path s in asset i at the end of period t,

• G(yi) := regularization function of control parameters,

• K(vsm,t ,v

km,t) := kernel function, k = 1, . . . ,S,

• xsi,t := investment amount to i-th asset at the end of time period t for sample path s,

• xi := investments to i-th asset at time t = 0,

27

• usi,t := adjustment (change in position) of asset i at the beginning of period t for sample

path s,

• Rsi,t := cash outflow resulting from selling an asset i at the end of time t for sample path s,

• V0 := portfolio value at time t = 0 (initial investment),

• V st := portfolio value at time t for sample path s,

• z := investment in annuity at time t = 0(in dollars),

• Ast := yield of annuity at the end of time period t for sample path s,

• L := amount of money that the investor is planing to withdraw as each time t,

• λ := regularization coefficient, λ > 0,

• κt := penalty for the cash flow shortage at time t,

• α := upper bound on sum of absolute adjustments each year, expressed as a fraction of

the portfolio.

3.3 Model Formulation

This section develops a model for optimization of a retirement portfolio. We consider a

portfolio including stock indices, bond indices, and an annuity. The annuity pays amount Ast z at

the end of each period t and does not contribute funds to the expected estate value. Annuity is

bought at time t = 0 and can not be bought or sold after that moment. It is also assumed that the

tax rate is zero (tax free environment).

Given initial investments in assets xi, the dynamics of investments in stocks and bonds are

as follows

xsi,1 = (1+ rs

i,1)xi, (3-1)

xsi,t = (1+ rs

i,t)(xsi,t−1 +us

i,t−1−Rsi,t−1) t = 2, . . . ,T.

Variables usi,t and Rs

i,t control how much is invested at the end of each period in each asset. usi,t is a

position adjustments for asset i at the end of time t for sample path s. Rsi,t is cash outflow from the

28

portfolio, generated from selling asset i at time t for sample path s. The variable usi,t is defined as

usi,t = f (vs

t ,yi), (3-2)

where vst is a set of returns for all assets, up to time t, for sample path s, and yi are some

parameters defining the function f . Therefore, usi,t , are some nonlinear functions of previous

returns of assets. The explicit form of function f is not specified in this section. The only

requirement on function f is that it should be linear in yi, i.e.

f (vst ,γ1y1

i + γ2 y2i ) = γ1 f (vs

t ,y1i )+ γ2 f (vs

t ,y2i ),

where γ1,γ2 ∈ R. Also, it should be noted that the function f does not change with t, however it

takes input vst that depends both on t and s, therefore the position adjustments depend on t and s.

The linearity of f with respect to yi is introduced to formulate the portfolio optimization problem

as a convex programming problem.

The total asset adjustments must sum to 0, this is expressed as a constraint,

N

∑i=1

usi,t = 0 . (3-3)

In addition to (3-3) the sum of absolute adjustments (over each asset i) in each period t and

sample path s is constrained to be less than or equal to some fraction α of the portfolio value in

the previous year of the same sample path,

N

∑i=1|us

i,t | ≤ αV st−1. (3-4)

Constraint (3-4) serves as additional regularization on the adjustments. Without constraint (3-4)

the values of usi,t can potentially be very large in absolute value but cancel out due to opposite

signs and still satisfy (3-3).

The value of the portfolio at the end of time period t for sample path s equals,

V st =

N

∑i=1

xsi,t . (3-5)

29

The objective is to maximize expected estate value of the portfolio. The expected estate value is

the weighted average of the discounted expected portfolio values for each sample path, where the

probabilities of death pt are used as weights. For every sample path s the portfolio value V st , at the

end of time period t, is discounted to time 0 using discounting coefficients dst , defined by

inflation, therefore,

discounted estate value for sample path s =T

∑t=1

ptdst V

st . (3-6)

By averaging over sample paths we obtain the expected estate value,

1S

S

∑s=1

T

∑t=1

ptdst V

st . (3-7)

In order to avoid over-fitting the data, we included the regularization term G(yi), defined for every

instrument i. The total regularization term is

N

∑i=1

G(yi) . (3-8)

The total cash outflow from selling the assets in the portfolio equals

cash flow from portfolio =N

∑i=1

Rsi,t .

The amount of money that the investor receives from the portfolio and annuity at the end of time

period t for sample path s equals Ast z+∑

Ni=1 Rs

i,t . If Ast z+∑

Ni=1 Rs

i,t < L then there is a shortage of

cash outflow and the resulting amount is penalized in the objective. Let κtTt=1 be some

decreasing sequence of positive numbers, the following function is a penalty term of cash outflow

shortages in the objectiveT

∑t=1

κt

[L−As

t z−N

∑i=1

Rsi,t

]+, (3-9)

where [∗]+ = max∗,0. To illustrate why it is important that κtTt=1 is a decreasing sequence,

consider the case where all κt are equal. Also, lets assume that there is a shortage of cash outflow,

equal to the amount w, at some year t > 0. Because, κt are all equal in (3-9), it does not make a

difference for that penalty term if there is a shortage equal to w/t during every year until t, or just

30

a single shortage of w at time t. However, if the amount of w/t is reinvested before time t in the

portfolio, it will(probably) increase in value by the time t and therefore, it will increase the

expected estate value of the portfolio. So, if κtTt=1 is not a decreasing sequence, the model will

try to incur penalty as soon as possible, even if there are enough funds in the portfolio at that

earlier date, and reinvest that shortage amount in the portfolio. Therefore the penalty from

parameters κt should outweigh any possible benefits from reinvesting at earlier dates. A simple

formula for κt is κt = κ(1+ r)T−t , where κ > 1 is some constant and r is some percentage that it

is significantly greater than the average growth rate of any asset considered in the portfolio.

Alternative to (3-9), it is possible to formulate the cash outflow requirement as a constraint

for each time t and sample path s

Ast z+

N

∑i=1

Rsi,t ≥ L. (3-10)

However constraint (3-10) may be violated on some sample paths, where the sampled rates of

returns for assets are particularly low and portfolio value shrinks to 0. Therefore, a better way of

imposing cash outflow requirements as a constraint would be to impose it as CVaR constraint. Let

X be some random variable. Imposing the CVaR constraint assures that the cash outflow

requirement (3-10) will be satisfied most of the time (around 100(1−α/2) percent of the cash

outflow payments will be fully paid). The CVaRα cash outflow requirement is

minζt

(ζt +

1S(1−αt)

S

∑s=1

[−

N

∑i=1

Rsi,t−As

t z−ζt

]+)≤−lt . (3-11)

The CVaRα(X) constraint is less likely to become infeasible since it allows cash outflows to be

less than required amount, on a small percentage sample paths. However, if the confidence

interval is very large and the cash outflow requirements are very high compared to the initial

investment, the CVaRα(X) constraints will become infeasible.

The model includes constraints on monotonicity of the cash outflows from the portfolio

N

∑i=1

Rsi,t−1 ≥

N

∑i=1

Rsi,t . (3-12)

31

Without the monotonicity constraints, the model might not provide necessary cash outflows at the

end of certain years and instead, reinvest that amount to increase the expected estate value of the

portfolio. The monotonicty constraint ensures that the cash outflow shortage occurs only in years

where the portfolio value drops below the cash outflow amount at the end of the previous year.

We minimize the objective function, containing expected costs with minus sign,

regularization term with penalty coefficient λ > 0 and cash outflow shortage with penalty κt

−1S

S

∑s=1

T

∑t=1

ptdst V

st +λ

N

∑i=1

G(yi)+T

∑t=1

κt

[L−As

t z−N

∑i=1

Rsi,t

]+. (3-13)

The explicit form of function G is not defined in this section, however, it is assumed that the

function G(y) is a convex function in y. This is important to formulate the problem as a convex

optimization. The resulting objective function (3-13) is a convex function in yi and linear in V st .

Further we provide the general model formulation.

minus

i,t ,Rsi,t ,

V0,V st ,yi,

xsi ,x

si,t ,z

− 1S

S

∑s=1

T

∑t=1

ptdst V

st +λ

N

∑i=1

G(yi)+T

∑t=1

κt

[L−As

t z−N

∑i=1

Rsi,t

]+(3-14)

s.t.

xsi,1 = (1+ rs

i,1)xi i = 1, . . . ,N; s = 1, . . . ,S

xsi,t = (1+ rs

i,t)(xsi,t−1 +us

i,t−1−Rsi,t−1) i = 1, . . . ,N; t = 2, . . . ,T ; s = 1, . . . ,S

N

∑i=1

xi =V0− z

V st =

N

∑i=1

xsi,t t = 1, . . . ,T ; s = 1, . . . ,S

N

∑i=1

usi,t = 0 t = 1, . . . ,T ; s = 1, . . . ,S

32

N

∑i=1

Rsi,t ≤

N

∑i=1

Rsi,t−1 t = 2, . . . ,T ; s = 1, . . . ,S

usi,t = f (vs

m,t ,yi) i = 1, . . . ,N; t = 1, . . . ,T ; s = 1, . . . ,S

N

∑i=1|us

i,t | ≤ αV st−1 t = 2, . . . ,T ; s = 1, . . . ,S

N

∑i=1|us

i,1| ≤ α(V0− z)

z≥ 0

Rsi,t ≥ 0

xi ≥ 0 i = 1, . . . ,N

xsi,t ≥ 0 i = 1, . . . ,N; t = 1, . . . ,T ; s = 1, . . . ,S

3.4 Special Case of General Formulation

This section presents a special case of the general problem formulation. We picked

functions G(yi) and f (rst ,yi) similar to the model developed in [32].

Let m > 0 be some integer and Km(vst ,v

kt ) be the kernel function defined as follows

K(vsm,t ,v

km,t) = exp

(− σ

m

N

∑i=1

t−1

∑l=t−m−1

(rki,l− rs

i,l)2), (3-15)

where σ > 0 is some constant. The parameter m controls how many previous years of information

is used by the kernel function to calculate the portfolio adjustments. Given (3-15), the control

function f (vst ,yi) is defined as

f (vst ,yi) =

S

∑j=1

y ji K(vs

m,t ,vjm,t), where yi = (y1

i , . . . ,ySi ). (3-16)

Function (3-16) is linear in yi. By substituting (3-16) in constraint (3-2), we get the following

adjustment functions

usi,t =

S

∑j=1

y ji K(vs

m,t ,vjm,t) i = 1, . . . ,N; t = 1, . . . ,T ; s = 1, . . . ,S. (3-17)

33

We use L2 norm as the regularization function G(yi),

G(yi) = ||yi||22 =S

∑s=1

(ysi )

2. (3-18)

Substituting (3-18) in the objective, gives

−1S

T

∑t=1

S

∑s=1

ptdst V

st +λ

N

∑i=1||yi||22 +

T

∑t=1

κt

[L−As

t z−N

∑i=1

Rsi,t

]+. (3-19)

This model can be reduced to convex quadratic problem by linearizing (3-9). Other

formulations are also possible. For example using L1 norm instead of L2 norm in (3-18) leads to

a linear programming formulation after linearization of (3-9). Another variation of this model

could be linear (with respect to rates rsi,t) adjustment functions instead of the nonlinear kernel

adjustment functions. Linear investment adjustments will lead to a lower expected estate value.

However the dimensionality of the problem will be reduced significantly, because the problem

size (the number of parameters to be optimized) will increase linearly with the number of sample

paths, instead of quadratically, with kernel functions.

3.5 Simulation of Return Sample Paths and Mortality Probabilities

3.5.1 Historical Simulations

We simulate return sample paths of considered investment instruments for T years in the

future. The simulations are based on end-of-year data of N assets over T years. Let t ∈ 1, . . . , T

be a year index for a historical dataset and ri,t be a historical return of asset i. The returns of the

indices are represented as the N× T matrix,

r1,1 r2,1, . . . , rN,1

r1,2 r2,2, . . . , rN,2

. . . . . . . . . . . .

r1,T r2,T , . . . , rN,T

(3-20)

We generate return sample paths using the historical simulation method. The historical simulation

method samples a random row from the matrix (3-20) and uses this row as a possible future

realization of returns of instruments. Therefore the future simulation of returns is just sampling of

34

the matrix (3-20) with replacement. Each such sample represents a future dynamics of return of

the assets. Note that the simulation method samples entire row from matrix (3-20), therefore the

correlations among assets are maintained in the random sample.

3.5.2 Mortality Probabilities

Let τ be a random variable that denotes an age of death of the investor. The probability that

an investor dies in time interval [t−1, t) since retirement at the age 65 is defined as follows

pt = P(t +64 < τ ≤ t +65 | τ > 65), t = 1, . . . ,T.

It is possible to calculate pt using the mortality table of USA. Mortality tables give a

conditional probability of death at some age, given that person is alive at year earlier of that age.

We use the mortality Table 3-1, which gives probability pt that t +64 < τ ≤ t +65, conditional

that τ > t +64,

pt = P(t +64 < τ ≤ t +65|τ > t +64), t = 1, . . . ,T.

It can be shown that

60 70 80 90 100 110 120

Age

0

0.01

0.02

0.03

0.04

0.05

Pro

babili

ty

Male

Female

Figure 3-1. Mortality probability graph. Probabilities that person dies while he/she is t +64 yearsold (t = 1, . . . ,T ), conditional that he/she is alive at the age of 65.

35

Table 3-1. USA Mortality table for the year 2016 with probabilities of death for male and femaleUSA citizens. This table can be found at US Social Security website:https://www.ssa.gov/oact/STATS/table4c6.html

Age p(age) Male p(age) Female65 0.0158 0.009866 0.0170 0.0107. . . . . . . . .119 0.8820 0.8820

pt =

pt , if t = 1

pt ∏t−1j=1(1− p j), if t = 2, . . . ,T

Figure 3-1 shows pt as the function of age t .

3.6 Case Study

3.6.1 Case Study Parameters

This case study considers a typical retirement situation in USA. Two variants of future asset

return sample paths are considered. These two variants correspond to an optimistic and

pessimistic projections regarding the future market dynamics. In the optimistic case, the future

returns over 35 years, for all instruments, are sampled from the historical returns over the recent

30 years. In the pessimistic case, the market is assumed to enter into a stagnation, similar to the

Japaneses market, which has approximately zero cumulative return for the recent 30 years. In the

pessimistic case, 12% is subtracted from each asset return, every year for every sample path.

Here are parameters of the model, which correspond to the retirement conditions in USA.

• The retiree is 65 years old.

• Investment horizon is 35 years.

• Portfolio is re-balanced at the end of each year.

• Retiree is a male (mortality probabilities for males are used in objective function).

• $500,000 is available for investment at time t = 0.

• Yearly inflation rate is 3% during the entire investment horizon.

• Yearly rate of return of annuity is 5%.

36

• Adjustment rules use kernel functions with parameter σ = 1.

• λ = 100

• κt = 2 ·1.2(35−t)

• α = 20%

• m = 5

There are 10 stock and bond indexes available for investment, see Table 3-2.

Table 3-2. The list of assets in the retirement portfolio.Index Name Index AbbreviationBarclays Muni FI-MUNIBarclays Agg FI-INVGRDRussell 2000 USEQ-SMRussell 2000 Value USEQ-SMVALRussell 2000 Growth USEQ-SMGRTHS&P 500 USEQ-LGS&P 400 Mid Cap USEQ-MIDS&P Citi 500 Value USEQ-LGVALS&P Citi 500 Growth USEQ-LGGRTHMSCI EAFE NUSEQ

For each index, 30 years of yearly returns (from 1985, to 2015) are used to create future

return sample paths. Each sample path includes 35 yearly returns, sampled from the 30 year

historical dataset (see the Historical Simulation method in Section 3.5). 200 sample paths are

generated for both, optimistic and pessimistic cases. 100 sample paths out of 200, for both

optimistic and pessimistic datasets, are used to find optimal investment rules in the model.

Therefore, the model is fitted on 3500 data points (asset returns) sampled from historical

observations. The remaining 100 sample paths, not included in the optimization, are used for

evaluating the out-of-sample performance of the model.

3.6.2 Optimal Portfolio

The considered optimization problems are reduces to Quadratic Programming, by

linearizing function (3-9) in the objective. Gurobi version 8.1.0 and Pyomo version 5.5.0 are used

for solving th resulting quadratic programming problem. The following case study link contains

37

the corresponding code:

http://uryasev.ams.stonybrook.edu/index.php/research/testproblems/financial engin

eering/case-study-retirement-portfolio-selection/.

The coefficients of the adjustment functions yi, are obtained by solving the quadratic

optimization problem corresponding to the optimal portfolio problem (3-14). Next, the

adjustment values for the out-of-sample dataset are evaluated, according to the formula (3-16).

The adjustment functions, for end of the time moment t, take previous m rates of returns of all

assets in the portfolio, observed in time interval [t−m, t−1] and produce an asset adjustment for

that time moment. Note that returns that go into these functions are different for each sample

path, therefore the adjustment values will be different for each sample path as well.

In order to calculate the portfolio values on the out-of-sample data, the cash outflows Rsi,t

are required. The model does not provide the cash outflow Rsi,t for the out-of-sample paths, as

those values are calculated for the in-sample paths. Therefore, it is unclear what values of Rsi,t

should be use in the out-of-sample paths. Additionally, despite the constraint on positivity of asset

positions in the in-sample optimization problems, a small portion of the assets may be allocated to

short positions in out-of-sample runs. Usually, the retirement portfolios do not have short

positions, since it is considered a risky strategy and therefore not suitable for a risk averse retiree

investors. Next, we show how to circumvent these problems for the out of sample datasets.

Let Ps,t+ and Ps,t

− be the total dollar investment in long and short positions, in a portfolio at

the end of time period t for sample path s,

Ps,t+ =

N

∑i=1

[xsi,t ]

+ ,

Ps,t− =

N

∑i=1

[−xsi,t ]

+.

The cash outflows are calculated as follows

Rsi,t =

L[xs

i,t−1]+

Ps,t−1+

if Ps,t−1+ > L

xsi,t−1 otherwise

(3-21)

38

So the cash outflows originate only from the long positions and are proportional to Ps,t−1+ .

All short positions, at the end of time period t for sample path s, are set to 0. As a result, the

amount of money equal to Ps,t− has to be subtracted from the remaining (long) part of the portfolio.

To shrink the portfolio by Ps,t− , each long asset position is reduced in a proportion to Ps,t

+ . Thus,

the new positions xsi,t are

xsi,t =

0, if xs

i,t ≤ 0

xsi,t−

xsi,t

Ps,t+

Ps,t− , otherwise.

Tables 3-3 through 3-7 show the average (over sample paths) investments in assets over

time for optimistic out-of-sample paths, corresponding to the model (3-14), with the minimum

cash flows requirements L ∈ $10,000;$30,000; . . . ,$90,000. Tables 3-8,3-9 and 3-10 show the

average (over sample paths) investments in assets over time for pessimistic out-of-sample paths,

corresponding to the model (3-14), with the minimum cash flows requirements

L ∈ $10,000;$25,000;$30,000;$50,000. Tables 3-8,3-9 and 3-10, show that, in the

pessimistic case, for L = $10,000, the model invests 30% of funds in the annuity and for

L = $25,000, 100% of investment goes into the annuities. However for L = $30,000 the model

decreases the annuity investment to 56%. As for L = $50,000 (and higher) nothing is invested in

the annuities and the model selects the stock/bond indexes. The Figure 3-2 shows the average

(taken over sample paths) portfolio values through time, constructed using the adjustment

functions, corresponding to the model (3-14) with the minimum cash flows requirements of

L ∈ $10,000;$30,000; . . . ,$90,000. However in the optimistic sample paths, the model does

not invest in annuities at any minimum cash outflow requirement L.

39

Table 3-3. Average investment in assets, L = $ 10,000, optimistic out-of-sample paths (inthousand dollars). Average is taken over sample paths.

Asset Investment t=0 t=5 t=10 t=15 t=20 t=25 t=30 t=35Annuity 0 0 0 0 0 0 0 0FI-MUNI 0 0 0 0 0 0 0 0FI-INVGRD 0 3 4 6 7 11 16 25USEQ-SM 0 0 0 0 0 0 0 0USEQ-SMVAL 0 28 54 104 171 360 635 1,177USEQ-SMGRTH 0 1 1 2 4 7 13 19USEQ-LG 0 0 0 0 0 0 0 0USEQ-MID 500 779 1,475 2,791 4,993 10,593 20,183 36,797USEQ-LGVAL 0 0 0 0 0 0 0 0USEQ-LGGRTH 0 4 8 15 30 72 139 380NUSEQ 0 50 80 153 268 444 762 1,186

Table 3-4. Average investment in assets, L = $ 30,000, optimistic out-of-sample paths (inthousand dollars). Average is taken over sample paths.

Asset Investment t=0 t=5 t=10 t=15 t=20 t=25 t=30 t=35Annuity 0 0 0 0 0 0 0 0FI-MUNI 0 0 0 0 0 0 0 0FI-INVGRD 3 34 44 51 64 95 138 194USEQ-SM 0 0 0 0 0 0 0 0USEQ-SMVAL 69 28 57 105 192 366 592 1,121USEQ-SMGRTH 0 1 2 4 7 14 27 42USEQ-LG 0 0 0 0 0 0 0 0USEQ-MID 402 612 1,025 1,818 3,136 6,642 12,574 22,657USEQ-LGVAL 0 0 0 0 0 0 0 0USEQ-LGGRTH 25 30 54 102 181 448 920 2,594NUSEQ 0 45 69 124 209 365 628 996

40

Table 3-5. Average investment in assets, L = $ 50,000, optimistic out-of-sample paths (inthousand dollars). Average is taken over sample paths.

Asset Investment t=0 t=5 t=10 t=15 t=20 t=25 t=30 t=35Annuity 0 0 0 0 0 0 0 0FI-MUNI 0 7 7 7 7 10 14 21FI-INVGRD 330 244 202 206 246 328 492 680USEQ-SM 0 0 0 0 0 0 0 0USEQ-SMVAL 57 137 194 281 424 693 1,163 1,875USEQ-SMGRTH 0 0 0 0 0 0 0 0USEQ-LG 0 0 0 0 0 0 0 0USEQ-MID 36 47 58 84 108 224 416 820USEQ-LGVAL 0 0 0 0 0 0 0 0USEQ-LGGRTH 77 65 66 92 157 386 857 2,515NUSEQ 0 33 35 74 104 154 255 349

Table 3-6. Average investment in assets, L = $ 70,000, optimistic out-of-sample paths (inthousand dollars). Average is taken over sample paths.

Asset Investment t=0 t=5 t=10 t=15 t=20 t=25 t=30 t=35Annuity 0 0 0 0 0 0 0 0FI-MUNI 0 0 0 0 0 0 0 0FI-INVGRD 195 117 67 40 32 35 44 56USEQ-SM 0 0 0 0 0 0 0 0USEQ-SMVAL 46 66 67 48 43 65 99 132USEQ-SMGRTH 0 0 0 0 0 0 0 0USEQ-LG 0 0 0 0 0 0 0 0USEQ-MID 107 118 73 69 88 170 320 596USEQ-LGVAL 0 0 0 0 0 0 0 0USEQ-LGGRTH 136 92 77 90 142 350 748 2,300NUSEQ 16 67 48 35 42 78 162 300

Table 3-7. Average investment in assets, L = $ 90,000, optimistic out-of-sample paths (inthousand dollars). Average is taken over sample paths.

Asset Investment t=0 t=5 t=10 t=15 t=20 t=25 t=30 t=35Annuity 0 0 0 0 0 0 0 0FI-MUNI 0 0 0 0 0 0 0 0FI-INVGRD 65 54 17 6 5 5 6 7USEQ-SM 0 0 0 0 0 0 0 0USEQ-SMVAL 70 83 51 30 29 46 76 115USEQ-SMGRTH 0 0 0 0 0 0 0 0USEQ-LG 0 0 0 0 0 0 0 0USEQ-MID 164 85 30 28 33 67 133 302USEQ-LGVAL 0 0 0 0 0 0 0 0USEQ-LGGRTH 140 107 56 48 76 204 439 1,522NUSEQ 61 58 26 12 9 14 23 42

41

Table 3-8. Average investment in assets, L = $ 10,000, pessimistic out-of-sample paths (inthousand dollar). Average is taken over sample paths.

Asset Investment t=0 t=5 t=10 t=15 t=20 t=25 t=30 t=35Annuity 147 147 147 147 147 147 147 147FI-MUNI 0 0 0 0 0 0 0 0FI-INVGRD 1 3 3 2 2 2 1 1USEQ-SM 0 0 0 0 0 0 0 0USEQ-SMVAL 2 3 2 3 2 1 1 0USEQ-SMGRTH 0 0 0 1 0 0 0 0USEQ-LG 0 0 0 0 0 0 0 0USEQ-MID 350 350 360 378 384 355 311 303USEQ-LGVAL 0 0 0 0 0 0 0 0USEQ-LGGRTH 0 4 7 7 7 5 5 4NUSEQ 0 4 4 3 3 3 2 2

Table 3-9. Average investment in assets, L = $ 25,000, pessimistic out-of-sample paths (inthousand dollar). Average is taken over sample paths.

Asset Investment t=0 t=5 t=10 t=15 t=20 t=25 t=30 t=35Annuity 500 500 500 500 500 500 500 500FI-MUNI 0 0 0 0 0 0 0 0FI-INVGRD 0 0 0 0 0 0 0 0USEQ-SM 0 0 0 0 0 0 0 0USEQ-SMVAL 0 0 0 0 0 0 0 0USEQ-SMGRTH 0 0 0 0 0 0 0 0USEQ-LG 0 0 0 0 0 0 0 0USEQ-MID 0 0 0 0 0 0 0 0USEQ-LGVAL 0 0 0 0 0 0 0 0USEQ-LGGRTH 0 0 0 0 0 0 0 0NUSEQ 0 0 0 0 0 0 0 0

42

Table 3-10. Average investment in assets, L = $ 30,000, pessimistic out-of-sample paths (inthousand dollar). Average is taken over sample paths.

Asset Investment t=0 t=5 t=10 t=15 t=20 t=25 t=30 t=35Annuity 282 282 282 282 282 282 282 282FI-MUNI 0 0 0 0 0 0 0 0FI-INVGRD 43 15 1 0 0 0 0 0USEQ-SM 0 0 0 0 0 0 0 0USEQ-SMVAL 35 18 2 0 0 0 0 0USEQ-SMGRTH 0 0 0 0 0 0 0 0USEQ-LG 0 0 0 0 0 0 0 0USEQ-MID 61 33 4 1 0 0 0 0USEQ-LGVAL 0 0 0 0 0 0 0 0USEQ-LGGRTH 54 27 3 0 0 0 0 0NUSEQ 24 11 1 0 0 0 0 0

Table 3-11. Average investment in assets, L = $ 50,000, pessimistic out-of-sample paths (inthousand dollar). Average is taken over sample paths.

Asset Investment t=0 t=5 t=10 t=15 t=20 t=25 t=30 t=35Annuity 0 0 0 0 0 0 0 0FI-MUNI 0 0 0 0 0 0 0 0FI-INVGRD 67 32 6 1 0 0 0 0USEQ-SM 0 0 0 0 0 0 0 0USEQ-SMVAL 95 64 24 6 3 1 0 0USEQ-SMGRTH 0 0 0 0 0 0 0 0USEQ-LG 0 0 0 0 0 0 0 0USEQ-MID 148 105 42 13 5 1 0 0USEQ-LGVAL 0 0 0 0 0 0 0 0USEQ-LGGRTH 128 85 30 8 3 1 0 0NUSEQ 62 37 13 3 1 0 0 0

43

0 5 10 15 20 25 30 35Years

0

5

10

15

20

25

30

35

40

Averag

e Po

rtfolio Value

(in million

s of d

ollars) L = 10K

L = 30KL = 50KL = 70KL = 90K

Figure 3-2. Portfolio values for optimistic out-of-sample paths. The average(over sample paths)portfolio value for the optimistic out-of-sample dataset, constructed using adjustmentfunctions, corresponding to model (3-14) with minimum cash outflow requirementsL ∈ $10,000;$30,000; . . . ,$90,000

44

3.6.3 Expected Shortage Time for Different Cash Outflows

When the investor demands higher cash outflows from the portfolio, the expected estate

value of the portfolio will decrease. Further, with higher cash outflow demands, there are higher

chances that there will not be enough money in the portfolio, at some point, to finance any

outflows.

To measure the cash outflow shortage resulting from the different values of L, the following

measure, named Expected Shortage Time (or ETS) is defined

ET S(L) =1S

S

∑s=1

T

∑t=1

pt(T − t)

(L−∑

Tt=1 Rs

i,t

)+L

ETS is measured in years and calculates the amount of time the retiree will spend without the

necessary cash outflow L, i.e. the number of years he/she will expect to be on Social Security.

The parameters of the case study are used to construct the ETS values for the optimistic and

pessimistic cases. ETS is calculated on the in-sample data, for the cash outflow values of

L ∈ $10,000;$15,000; . . . ;$100,000. The resulting ETS values are shown on Figures 3-3 and

3-4 for optimistic and pessimistic sample paths respectively.

The Figure 3-3 shows that, in the optimistic sample paths, the retiree can have cash outflows

up to $50,000, without expecting any shortages given an average life span. For the values of L

greater than $50,000, the ETS grows roughly linearly. For L = $100,000 the retiree will spend

most of his expected life without necessary cash outflow, because the portfolio can not provide

this much cash outflow, given the initial investment of $500,000.

It should be noted that, in the pessimistic case, if L≤ $25,000 the annuities can fully cover

the cash flow requirements and therefore ETS = 0. However, if L > $25,000 the investment in the

annuities can no longer cover the cash outflow requirements. Even if the entire initial investment

goes into the annuities, it will provide only A · z = 5% ·$500,000 = $25,000. Therefore, for L

values higher than $25,000, the model starts to invest in stock and bond indexes and the ETS is

greater than 0.

45

For the pessimistic sample paths, if the cash flow requirement is L = $100,000 the ETS is

almost equal to the life expectancy of the retiree. This happens because, on most pessimistic

sample paths, the portfolio shrinks to 0 in a 3 or 4 years for L = $100,000. However, if

L = $30,000, on the pessimistic sample paths, the retiree still has relatively small ETS values of

around 3 year.

Higher values of expected estate result in lower values of ETS. Figure 3-5 illustrates the

relationship between expected estate and ETS relationship for the case of optimistic sample paths.

Figure 3-5 is constructed by solving problem (3-14) for cash outflow values of

L ∈ $10,000;$15,000; . . . ;$100,000 and plotting the resulting values of ETS and expected

estate.

20 40 60 80 100Required Cash Flow (in thousands of dollars)

0

1

2

3

4

5

6

7

8

Years

Figure 3-3. ETS values for the optimistic sample paths. Required cash flowsL ∈ $20,000;$30,000; . . . ;$100,000

46

20 40 60 80 100Required Cash Flow (in thousands of dollars)

0

2

4

6

8

10

12Ye

ars

Figure 3-4. ETS values for the pessimistic sample paths. Required cash flowsL ∈ $10,000;$15,000; . . . ;$100,000

Another way to illustrates these relationships is a trade-off between the expected estate (3-7)

and the ETS. Figure 3-5 illustrates the relationship between expected estate and ETS for the set of

optimistic sample paths. Figure 3-5 is constructed by solving problem (3-14) for cash outflow

values of L = $10,000;$15,000; . . . ;$100,000 and plotting the resulting values of ETS and

expected estate. Each marker dot on the curve is a different level of target cash flow (lowest on

the left). When the cash outflow requirements are low, then the expected estate is high – around

$2 million with a $20,000 target - and the expected number of years without cash flow is very low

– or zero. Of course, existence will be close to Social Security standards, but the heirs will be

happy. As the cash outflow requirement rises to around $50,000 to $60,000 per year, the expected

estate drops below $500,000 and one can expect to spend almost a year on social security. At

higher target levels the expected estate drops even further and the time on Social Security rises.

To be clear, these are expected levels. In any specific sample path, once the portfolio goes to zero

no further cash is available for distribution, however long one lives. On the other hand, in very

fortuitous sample paths, portfolio values may not dip to zero for a very long time.

47

0 1 2 3 4 5 6 7 8ETS

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5Ex

pected

Estate Va

lue

Figure 3-5. Relationship between expected estate value and the ETS, for the optimistic samplepaths.

48

CHAPTER 4A NEW APPROACH TO CREDIT RATINGS

4.1 Motivation

At the height of the financial crisis of 2008, American International Group, Inc. (AIG), once

the largest insurance company in the US, was rescued from bankruptcy by a US government

bailout worth $85 bn [see, e.g., 33]. This was part of the Troubled Asset Relief Program (TARP)

that cost the US taxpayer in excess of $245 bn. What caused the companies that enjoyed stable

AAA credit ratings to fail abruptly and what role did credit ratings play in the failure?

Early post-crisis literature focused on issues of risk mispricing caused by using dependence

models that fail to accommodate realistic tail behavior of joint defaults and on issues around

structured finance where loan securitization obscured the true riskiness of the collateral. For

example, [34] and [35] provide two different perspectives at how securitized risky debt was

repackaged as virtually risk-free. What is common in the two papers is that they show how rating

agencies were simply unfamiliar with assessing creditworthiness of financial instruments that

cannot be ascribed to a single company and instead involve a pool of loans, bonds and mortgages

from various sources. Thus, the subsequent issues of claims – known as synthetic instruments –

against those assets, were not supported by a robust methodology for pricing their riskiness.

[34] make the point that the new developments in structured finance amplified errors in risk

assessment, while [35] shows that the commonly used dependence assumption known as the

Gaussian copula was inappropriate. As a result, relatively minor imprecisions in credit risk

estimation could have led to variations in default risk of the synthetic securities that were large

enough to cause an AAA-rated security to default with a high probability.

Moreover, [36] looked at a large number of mortgage-backed securities (MBS), collaterized

debt obligations (CDO) and other structured finance securities and found empirical evidence that

higher credit ratings were closely associated with higher MBS prices after controlling for a large

set of security fundamentals. They report that, in terms of value, 80 to 90 percent of sub-prime

MBS initially received AAA ratings but were in effect 6-10 rating notches lower1. This offers

1Rating agencies commonly use 21-22 notch scales, from AAA to C or AAA to D.

49

support for the widely held belief that more conservative credit ratings would have muted the

crisis by making credit more expensive and providing a more reliable information about synthetic

instruments to less informed investor. [37] describe the various conflicts of interest that may have

added to the inability or unwillingness of credit rating agencies to do that.

Moody’s, Standard and Poor’s and Fitch Group – the three major credit rating agencies

known as the Big Three – have evolved since then. They are now more mindful of joint tail risk

and synthetic instruments are hardly new any more. More recent papers on this topic focus on

how credit rating inflation is affected by competition between agencies, by regulation of the

industry and by the business cycle [see, e.g., 38, 39, 40, 41, 42, 43, 44, 45]. For example, [38] find

evidence that credit ratings are inflated during the boom periods and [45] present a model where

ratings quality is counter-cyclical. It is noteworthy that the “boom bias” in these papers does not

result from changes in legislation or competitive pressures surrounding rating agencies. Rather it

comes from the rating agencies’ incentive conflicts.