C-087 Syndicate Practices Handbook · SYNDICATE PRACTICES HANDBOOK The syndicate practices for the...

28

INVESTMENT DEALERS ASSOCIATION OF CANADA ASSOCIATION CANADIENNE DES COURTIERS EN VALEURS MOBILIÈRES Syndicate Practices Handbook August 1995

Transcript of C-087 Syndicate Practices Handbook · SYNDICATE PRACTICES HANDBOOK The syndicate practices for the...

INVESTMENT DEALERS ASSOCIATION OF CANADAASSOCIATION CANADIENNE DES COURTIERS EN VALEURS MOBILIÈRES

SyndicatePracticesHandbook

August 1995

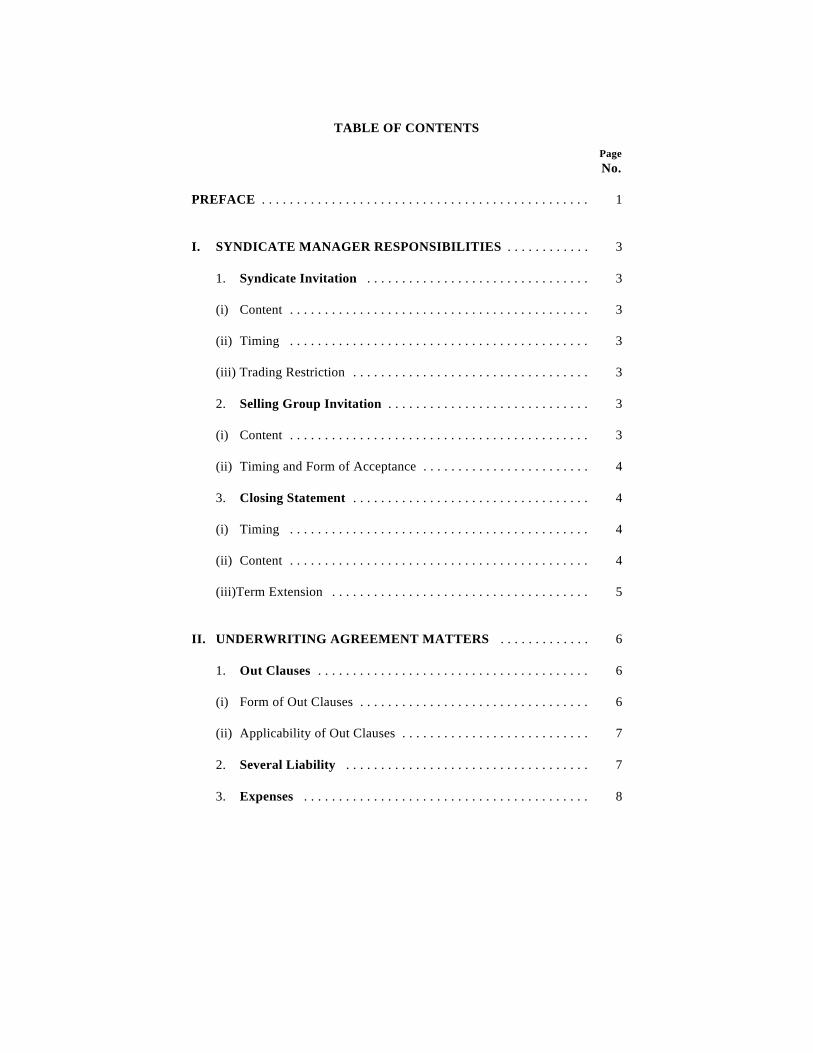

TABLE OF CONTENTS

PageNo.

PREFACE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

I. SYNDICATE MANAGER RESPONSIBILITIES . . . . . . . . . . . . 3

1. Syndicate Invitation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

(i) Content . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

(ii) Timing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

(iii) Trading Restriction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

2. Selling Group Invitation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

(i) Content . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

(ii) Timing and Form of Acceptance . . . . . . . . . . . . . . . . . . . . . . . . 4

3. Closing Statement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

(i) Timing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

(ii) Content . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

(iii)Term Extension . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

II. UNDERWRITING AGREEMENT MATTERS . . . . . . . . . . . . . 6

1. Out Clauses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

(i) Form of Out Clauses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

(ii) Applicability of Out Clauses . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

2. Several Liability . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

3. Expenses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

PageNo.

III. SYNDICATE MATTERS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

1. Liability Calculation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

2. Exempt List . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

3. Selling Group . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

4. Firm Sales and Oversales . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

5. Market Stabilization and Over-Allotment . . . . . . . . . . . . . . . . . 10

6. Marketing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

7. Repurchase by the Manager . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

8. Term . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

IV. MARKETING MATTERS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

1. Price Discipline . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

2. Exempt List . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

3. Distribution Statement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

4. Compliance with Securities Laws . . . . . . . . . . . . . . . . . . . . . . . 12

5. Advertising . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

6. Settlement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

V. ACCOUNTING MATTERS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

1. Price Structure and Definitions . . . . . . . . . . . . . . . . . . . . . . . . . 14

2. Management Fee . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

3. Syndicate Profit . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

4. Allowable Syndicate Expenses . . . . . . . . . . . . . . . . . . . . . . . . . 15

5. Payment of Underwriting Profits . . . . . . . . . . . . . . . . . . . . . . . . 16

VI. OTHER MATTERS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

1. Conflict Resolution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

2. Choice of Law . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

3. Examination . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

4. Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

1

SYNDICATE PRACTICES HANDBOOK

PREFACE

The Corporate Finance Committee of the Investment Dealers Association of Canada hasreviewed the current practices related to the formation and operation of underwritin gsyndicates for corporate debt, preferred share and equity financings. The Investmen tDealers Association is publishing these practices which have evolved over time int oinformal conventions in the interests of improving the efficiency of the underwritin gprocess.

For many corporate financings the underwriting pro cess has truncated in recent years froma typical two-month period between the inception of the deal and the closing to a three-week period in response to intense competitive pressures. The shortened timetable fo rcompleting a transaction has left little time to negotiate detailed agreements betwee nsyndicate group members (firms taking a share of the underwriting liability) and sellinggroup members (firms not taking a liability position but participating in the distribution ofthe offered securities). As a result underwriters have proceeded on the basis o funderstandings or practices as to how various syndicate matters are handled. The absenceof formal agreements among investment de aler participants in an underwriting transactionhas from time-to-time given rise to misunderstandings in respect of the details of th eunderwriting agreement and the responsibilities of syndic ate and selling group participants.The difficulties have been exacerbated by the frequency of large-sized underwriting soccurring on an accelerated timetable.

The syndicate practices have been developed by the Corporate F inance Committee to makeIDA Member firms more aware of the conventional practices before an underwritin gtransaction takes place. These practices will provide IDA Member firms with a bette runderstanding of their responsibilities in syndicate and selling groups, particularly i nrapidly structured financings.

The practices in the attached document should not be interpreted as a priori and requiredconditions for an underwriting transaction. IDA Member firms participating as syndicateand selling group members, and corporate issuers, can structure corporate financings a sthey see fit. This document is simply to provide a reference for syndicate managers t oindicate to syndicate and selling group members possible differences from the norma lpractice.

The IDA practices document has been prepared by a worki ng group of the Capital MarketsCommittee, chaired by Jim Hinds, Wood Gundy Inc. Oth er members of the working groupinclude George Ratner, Richardson Greenshields of Canada Limited; Ron Lloyd, RB CDominion Securities Inc.; Paul Allison, Nesbitt Burns Inc.; Brian Porter, ScotiaMcLeodInc.; John Warren, Borden & El liot and Ian Russell, Investment Dealers Association. Theworking group has incorporated the comments and suggestions which have been pu tforward by all member firm representatives of the Capital Markets Committee. The IDABoard of Directors has approved the publication of these underwriting practices.

2

SYNDICATE PRACTICES HANDBOOK

The syndicate practices for the formation and operation of underwriting syndicates will bereviewed on an annual basis, to reflect revised practices in the underwriting business andchanges in the regulatory environment. The first review is scheduled for December 1995.Any comments or suggestions should be directed to Ian C.W. Russell, Vice-President ,Capital Markets, Investment Dealers Association of Canada, Suite 1600, 121 King StreetWest, Toronto, Ontario M5H 3T9.

3

SYNDICATE PRACTICES HANDBOOK

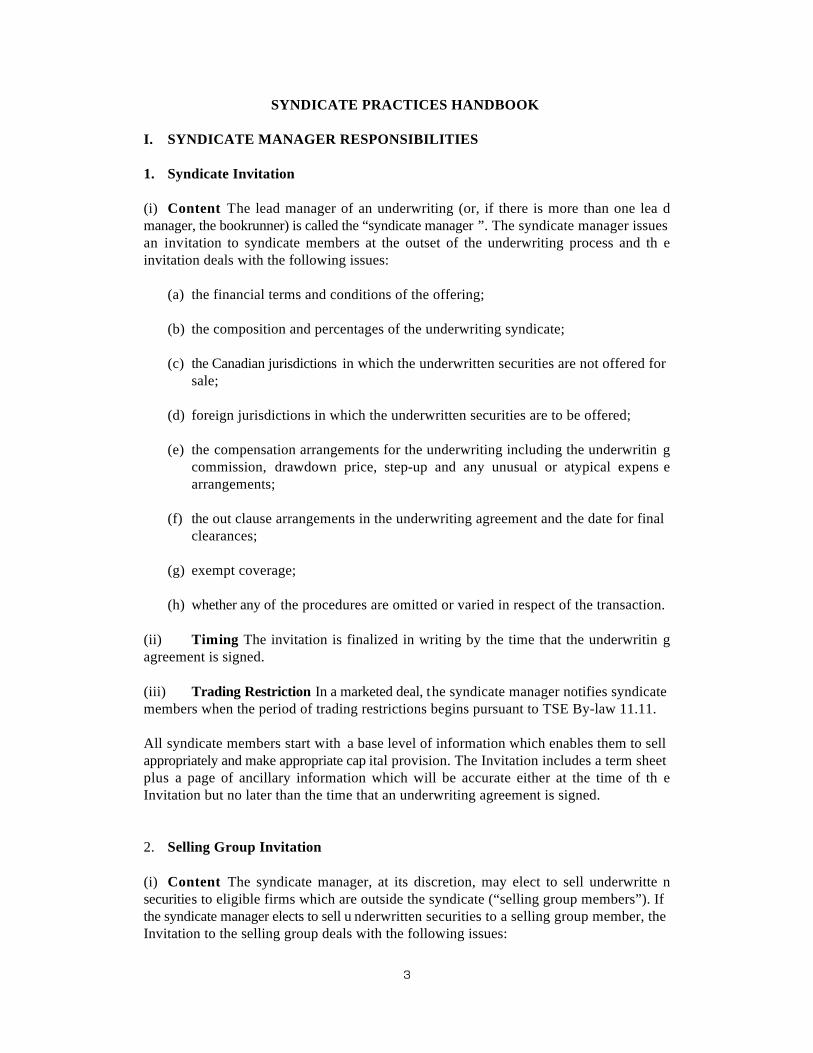

I. SYNDICATE MANAGER RESPONSIBILITIES

1. Syndicate Invitation

(i) Content The lead manager of an underwriting (or, if there is more than one lea dmanager, the bookrunner) is called the “syndicate manager ”. The syndicate manager issuesan invitation to syndicate members at the outset of the underwriting process and th einvitation deals with the following issues:

(a) the financial terms and conditions of the offering;

(b) the composition and percentages of the underwriting syndicate;

(c) the Canadian jurisdictions in which the underwritten securities are not offered forsale;

(d) foreign jurisdictions in which the underwritten securities are to be offered;

(e) the compensation arrangements for the underwriting including the underwritin gcommission, drawdown price, step-up and any unusual or atypical expens earrangements;

(f) the out clause arrangements in the underwriting agreement and the date for finalclearances;

(g) exempt coverage;

(h) whether any of the procedures are omitted or varied in respect of the transaction.

(ii) Timing The invitation is finalized in writing by the time that the underwritin gagreement is signed.

(iii) Trading Restriction In a marketed deal, the syndicate manager notifies syndicatemembers when the period of trading restrictions begins pursuant to TSE By-law 11.11.

All syndicate members start with a base level of information which enables them to sellappropriately and make appropriate cap ital provision. The Invitation includes a term sheetplus a page of ancillary information which will be accurate either at the time of th eInvitation but no later than the time that an underwriting agreement is signed.

2. Selling Group Invitation

(i) Content The syndicate manager, at its discretion, may elect to sell underwritte nsecurities to eligible firms which are outside the syndicate (“selling group members”). Ifthe syndicate manager elects to sell u nderwritten securities to a selling group member, theInvitation to the selling group deals with the following issues:

4

SYNDICATE PRACTICES HANDBOOK

(a) the financial terms and conditions of the offering;

(b) the Canadian jurisdictions where the securities are not qualified for sale;

(c) the drawdown price;

(d) the date for final clearances;

(e) whether any of the procedures are omitted or varied in respect of the transaction;

(f) the allotment to the selling group member.

(ii) Timing and Form of Acceptance The selling group invitation is finalized in writingby the time that the receipt for the final prospectus has been issued. Confirmation of thenumber of underwritten securities may be made in the selling group Invitation or orally.

This procedure replaces the lengthy an d repetitive selling group agreements which may ormay not be prepared at present.

3. Closing Statement

(i) Timing At closing, the syndicate manager sends out a statement to syndicat emembers, setting forth the information below to the extent that it is then known. If th esyndicate is extended or if a greenshoe option is still alive, the syndicate manager sendsout a further statement containing final information at the end of the extension period orgreenshoe exercise or expiry.

(ii) Content The Closing Statement contains the following information to the extent thatit is known:

(a) name and sale amount to each exempt institution (reference is made to III. 2.);

(b) aggregate sales to the Selling Group (reference is made to III. 1.);

(c) aggregate sales to syndicate members;

(d) whether the syndicate is long, or whether over-allotment or market stabilizationactivities have been liquidated, whether there was a greenshoe and whether it hasbeen exercised, has expired or remains an option and an estimate of the cost o rprofit of each of these activities;

(e) an estimate of expenses of the offering;

(f) identification of any atypical sales, confirmation problems, settlement problemsor unusual expenses.

5

SYNDICATE PRACTICES HANDBOOK

(iii) Term Extension The syndicate manager may elect to extend the term of th esyndicate for a period not exceeding the longer of 60 days past closing of the underwritingor the expiry of any greenshoe option. Notice to that effect may be made in the ClosingStatement. Reference is made to III. 8.

6

SYNDICATE PRACTICES HANDBOOK

II. UNDERWRITING AGREEMENT MATTERS

1. Out Clauses

(i) Form of Out Clauses Set out below is the form of disaster out clause specified inIDA Regulation 100.5 together with a form of market out clause and rating change ou tclause:

“disaster out clause” means a provision substantially in the following form:

The obligations of the Underwriter (or any of them) to purchase (the Securities) underthis agreement may be terminated by the Underwriter (or any of them) at its option bywritten notice to that effect to the Company at any time prior to the Closing if thereshould develop, occur or come into effect or existence any event, action, state ,condition or major financial occurrence of national or inte rnational consequence or anylaw or regulation which in the opinion of the Underwriter seriously adversely affects,or involves, or will seriously adversely affect, or involve, the financial markets or thebusiness, operations or affairs of the Company and its subsidiaries taken as a whole;

“market out clause” means a provision substantially in the following form:

If, after the date hereof and prior to the T ime of Closing, the state of financial marketsin Canada or elsewhere where it is plan ned to market the Securities is such that, in thereasonable opinion of the Underwriters (or any of them), the Securities cannot b emarketed profitably, any Underwriter shall be entitled, at its option, to terminate it sobligations under this agreement by notice to that effect given to the Company at orprior to the Time of Closing;

“material change out” clause means a provision substantially in the following form:

If, after the date hereof and prior to the Time of Closin g, there shall occur any materialchange or change in a material fact which, in the reasonable opinion of th eUnderwriters (or any of them), would be expected to have a significant adverse effecton the market price or va lue of the Securities, any Underwriter shall be entitled, at itsoption, to terminate its obligations under this agreement by written notice to tha teffect, given to the Company at or prior to the Time of Closing;

“rating change out” clause means a provision substantially in the following form:

If, after the date hereof and prior to the Time of Closing, there shall occur a change inthe generic rating applicable to the Securities or any of the securities of the Companyby one of the statistical rating org anizations or if one of such organizations shall placeany of the securities of the Company on credit watch any Underwriter shall be entitled,at its option, to terminate its o bligations under this agreement by written notice to thateffect, given to the Company at or prior to the Time of Closing.

7

SYNDICATE PRACTICES HANDBOOK

(ii) Applicability of Out Clauses Different practices concerning out clauses hav eevolved depending upon the type of secu rity being underwritten -- debt, preferred share orequity -- and the process by which the deal is done -- bought or marketed. Common to allis the presence of a disaster out clause. Out clauses may or may not be present in atransaction depending upon the type of security offered. Set out below is the curren tCanadian practice with respect to out clauses:

Marketed Deal Bought Deal

Common Equity Disaster, Market, Disaster andsecurities and Material

Material Change Change

Preferred Shares Disaster, Market Disaster, MaterialMaterial Change and Change and RatingRating Change Change

Debt Securities Disaster, Material Disaster, MaterialChange and Rating Change and RatingChange Change

For greater certainty, “equity” securities include convertible debentures and non -retractable convertible preferred shares. For greater certainty, “marketed” deals are thosein which a preliminary prospectus has been filed before an underwriting agreement ha sbeen signed; agency deals are deemed to be marketed deals.

The IDA Regulations have for a number of years prescribed reduced levels of margin forMembers with respect to underwriting obligations if the relevant underwriting agreementcontains a “disaster out clause” in prescribed form. Similarly margin is able to be reducedif the underwriting agreement permits an underwriter to terminate its commitment t opurchase in the event of unsalability due to market conditions -- i.e. a market out.

2. Several Liability

Underwriting agreements generally contain a provision sub stantially in the following form:

“The obligation of the Underwriters to purchase the Securities at the Time of Closingshall be several and not joint and the liability of each of the Underwriters shall b elimited to the following percentages of the Securities to be purchased at that time:

No Underwriter shall be obligated to take up and pay for any of the Securities to bepurchased by it unless the other Underwriters simultaneously take up and pay for thepercentage of Securities set out opposite their names above.

8

SYNDICATE PRACTICES HANDBOOK

If one or more of the Underwriters shall fail to purchase its or their applicabl epercentage of the total number of Securities at the Time o f Closing for any reason eachof the other Underwriters (the “Remaining Underwriters”) shall be relieved of it sobligations hereunder provide d that, notwithstanding the provisions of this section theRemaining Underwriters may, but sha ll not be obligated to, purchase the total numberof Securities in such proportion as may be agreed upon by t he Remaining Underwritersand the Remaining Underwriters shall have the right, by notice to the Company t opostpone the Time of Closing by not more than 72 hours to effect such purchase .Nothing in this section shall oblige the Company to sell to the Underwriters less thanall of the Securities or shall relieve from liability to the Company any Underwrite rwho shall be in default.”

It is Canadian practice that the obligation of each underwriter to purchase securities fromthe issuer is several as opposed to joint.

3. Expenses

Expense arrangements as between the issuer and the syndicate as set forth in th eunderwriting agreement are substantially as set out below.

All expenses of or incidental to th e creation, issue, delivery and sale of the securities shallbe borne by the issuer, including, with out limitation, the cost of any institutional and retailroadshows, expenses payable in conn ection with the qualification of the securities for saleto the public, the fees and expenses of the issuer's counsel, all advertising expenses, al lcosts incurred in connection with the preparation, printing and delivery of the prospectusand any prospectus amendme nt including commercial copies thereof and of the definitivecertificates representing the securities and any stock exchange listing fees. The fees anddisbursements of the underwriters' counse l and the underwriters' “out-of-pocket” expenses(other than those referred to above) shall be borne by the underwriters except that th eunderwriters will be reimbursed by the issuer for the underwriters' reasonable fees ,disbursements and expenses (including the fees and disbursements of the underwriters 'counsel) if the underwriting is not completed other than by reason of a default by th eunderwriters.

9

SYNDICATE PRACTICES HANDBOOK

III. SYNDICATE MATTERS

1. Liability Calculation

The liability of each member of the syndicate for the underwritten securities is calculatedas follows:

Size of underwriting

less: sales to the exempt list (reference is made to 2. below)

less: sales to selling group members

less: oversales by syndicate members

times: syndicate member's percentage

less: firm sales by the syndicate member

equals: syndicate member's liability

2. Exempt List

The syndicate manager, together with such other syndicate members as it shall determineat its discretion is authorized to offer the underwritten securities on behalf of the syndicateto certain purchasers (the “exempt list”) several lists of which are attached as Exhibit 1.Separate examples of exempt lists are included for preferred share and equity securitiestransactions. Any institutional account included on the exempt list is removed at its option.The syndicate manager at its discretion designates additional accounts to be covered on anexempt basis in the Invitation.

Sales to the exempt list, if any, are for the account of the syndicate as described i nparagraph 1. above.

3. Selling Group

Reference is made to I. 2. for selling group sales, ie. s ales by firms which are not syndicatemembers. Such sales are made at the drawdown price.

4. Firm Sales and Oversales

Where appropriate, the syndicate manager makes u nderwritten securities available for saleby syndicate members to individual, international and institutional purchasers which arenot on the exempt list at a price to the syndicate members equal to the drawdown price.Allotments made by the syndicate manager and accepted by the syndicate member ar ecalled “firm sales”.

10

SYNDICATE PRACTICES HANDBOOK

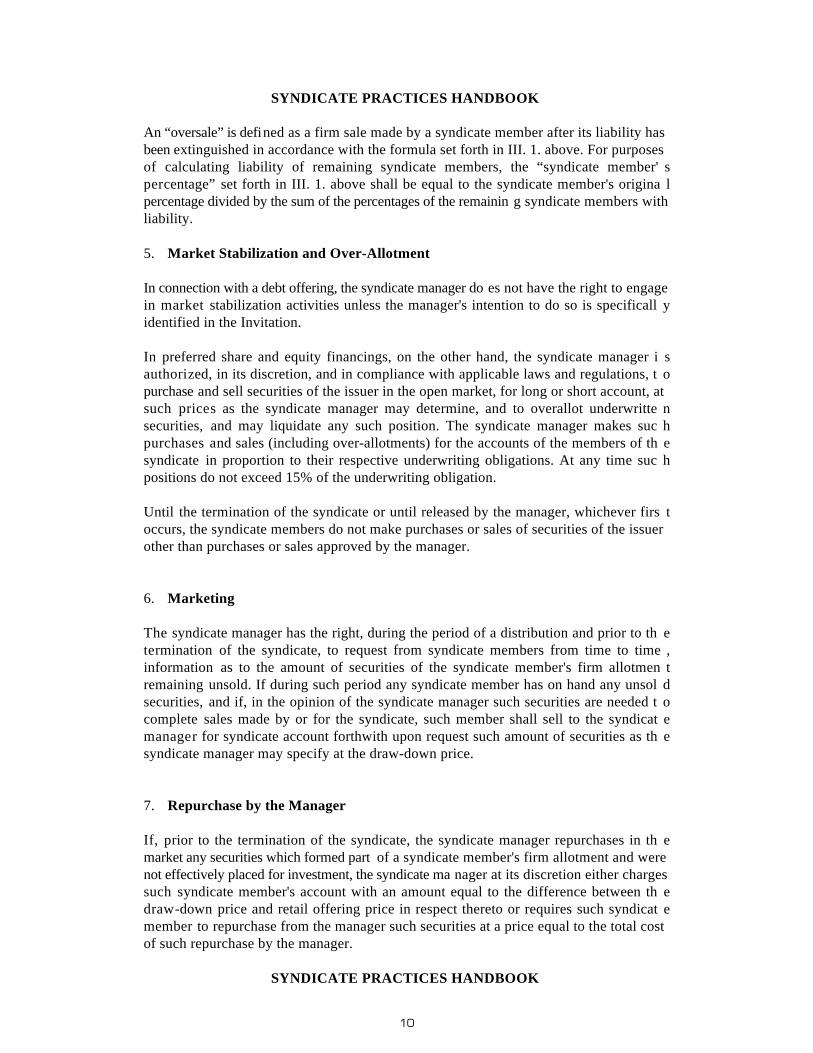

An “oversale” is defined as a firm sale made by a syndicate member after its liability hasbeen extinguished in accordance with the formula set forth in III. 1. above. For purposesof calculating liability of remaining syndicate members, the “syndicate member' spercentage” set forth in III. 1. above shall be equal to the syndicate member's origina lpercentage divided by the sum of the percentages of the remainin g syndicate members withliability.

5. Market Stabilization and Over-Allotment

In connection with a debt offering, the syndicate manager do es not have the right to engagein market stabilization activities unless the manager's intention to do so is specificall yidentified in the Invitation.

In preferred share and equity financings, on the other hand, the syndicate manager i sauthorized, in its discretion, and in compliance with applicable laws and regulations, t opurchase and sell securities of the issuer in the open market, for long or short account, atsuch prices as the syndicate manager may determine, and to overallot underwritte nsecurities, and may liquidate any such position. The syndicate manager makes suc hpurchases and sales (including over-allotments) for the accounts of the members of th esyndicate in proportion to their respective underwriting obligations. At any time suc hpositions do not exceed 15% of the underwriting obligation.

Until the termination of the syndicate or until released by the manager, whichever firs toccurs, the syndicate members do not make purchases or sales of securities of the issuerother than purchases or sales approved by the manager.

6. Marketing

The syndicate manager has the right, during the period of a distribution and prior to th etermination of the syndicate, to request from syndicate members from time to time ,information as to the amount of securities of the syndicate member's firm allotmen tremaining unsold. If during such period any syndicate member has on hand any unsol dsecurities, and if, in the opinion of the syndicate manager such securities are needed t ocomplete sales made by or for the syndicate, such member shall sell to the syndicat emanager for syndicate account forthwith upon request such amount of securities as th esyndicate manager may specify at the draw-down price.

7. Repurchase by the Manager

If, prior to the termination of the syndicate, the syndicate manager repurchases in th emarket any securities which formed part of a syndicate member's firm allotment and werenot effectively placed for investment, the syndicate ma nager at its discretion either chargessuch syndicate member's account with an amount equal to the difference between th edraw-down price and retail offering price in respect thereto or requires such syndicat emember to repurchase from the manager such securities at a price equal to the total costof such repurchase by the manager.

SYNDICATE PRACTICES HANDBOOK

11

8. Term

The syndicate ceases at the close of business on t he closing date of the underwriting unlessthe syndicate is extended by the syndicate manager by notice to the syndicate members asreferred to in I. 3.(iii). The syndicate manager has the right by notice to the syndicat emembers to extend any syndicate for a p eriod not exceeding 60 days, except in the case ofa greenshoe, in which event the maximum term extension is the expiry of the greenshoe.Further extensions of term require the agreement of each syndicate member.

The term of the syndicate does not affect obligations which are intended to survive closing;in particular, the timing payment of syndicate profits is as set forth in V. 3.

The termination provision assists in t he timely disposition of syndicate remnants, either ofunsold new issue positions or associated market stabilization positions. The syndicat emanager tries to clean up positions at closing; failing which, it automatically extends for60 days after; failing which it either achieves consent from the syndicate to hold it togetheror breaks it up.

12

SYNDICATE PRACTICES HANDBOOK

IV. MARKETING MATTERS

1. Price Discipline

Unless the syndicate manager agrees otherwise, all transactions in the underwritte nsecurities during the term of the syndicate by any syndicate member or selling grou pmember with any purchaser take place at the public offering price. No firm withholds fromsale to the public underwritten securities in order to make sales at higher prices durin gsome later time frame.

Transfers within the syndicate of firm allotments or sales to selling group members ar emade at the drawdown price.

2. Exempt List

Syndicate members and selling group members do not offer the underwritten securities tothose on the exempt list during the term of the syndicate.

3. Distribution Certificate

Each syndicate member and selling group member is required to complete a distributioncertificate to be delivered to the syndicate ma nager within 14 days of the closing date. Thedistribution certificate indicates the number of securities sold in each province or territory,as more fully set forth in Exhibit 2.

4. Compliance with Securities Laws

Each syndicate member and sellin g group member represents and warrants that it will notoffer for sale, or solicit an offer to buy any of the underwri tten securities in any jurisdictionwhere it is not legally qualified to do business and that it will distribute the securities incompliance with applicable securities laws.

5. Advertising

Each syndicate member and selling group member agrees not to advertise the offerin gwithout the syndicate manager's consent.

Unless a syndicate member has notified the manager in writing to the contrary, th esyndicate manager may include the name of the syndicate member in such advertisementin the style appearing on the signature page of the prospectus.

6. Settlement

Unless specifically identified otherwise in the Invitation, the syndicate manager uses theNew Issue Distribution Service of CDS for an underwriting. Syndicate members an dselling group members are participants in CDS.

13

SYNDICATE PRACTICES HANDBOOK

The syndicate manager ensures that underwritten securities will be available for deliveryat the principal office of the transfer agent identified in the prospectus in Toronto an dMontreal. Each syndicate member and selling group member advises the transfer agent ofsplits and registrations for redelivery in a timely fashion. Failing timely receipt of suc hadvice by the syndicate manager, all shares are delivered to such syndicate member o rselling group member in Toronto.

14

SYNDICATE PRACTICES HANDBOOK

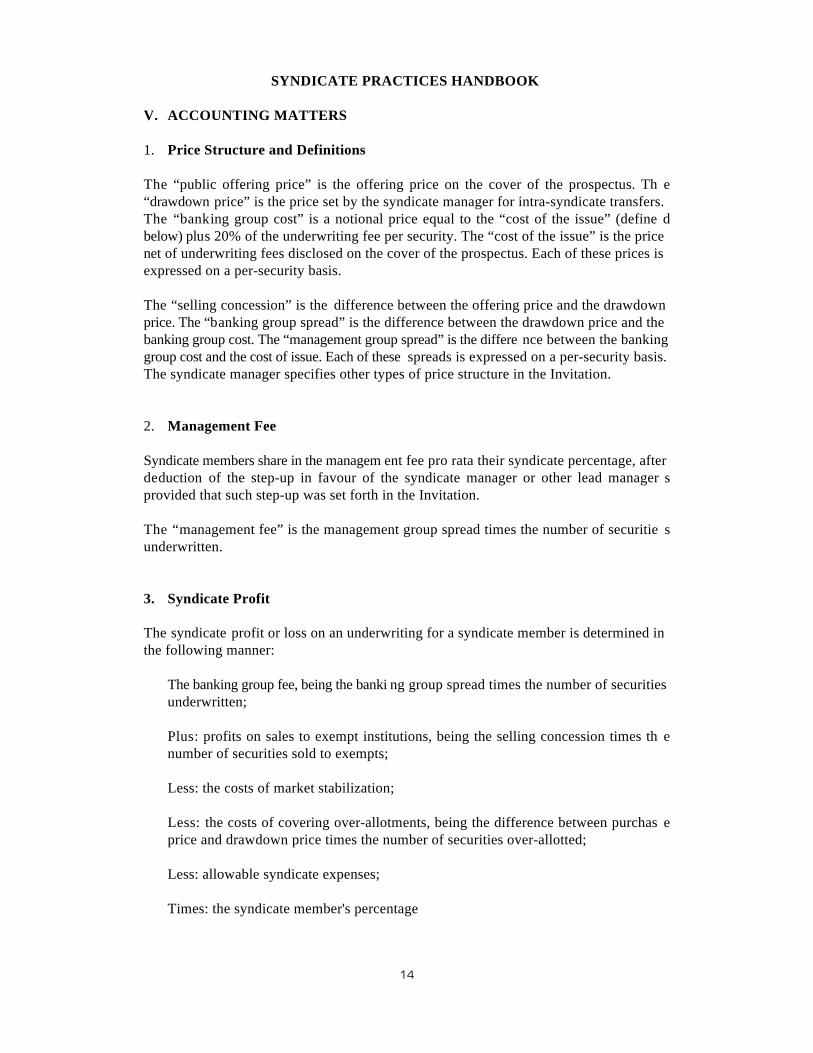

V. ACCOUNTING MATTERS

1. Price Structure and Definitions

The “public offering price” is the offering price on the cover of the prospectus. Th e“drawdown price” is the price set by the syndicate manager for intra-syndicate transfers.The “banking group cost” is a notional price equal to the “cost of the issue” (define dbelow) plus 20% of the underwriting fee per security. The “cost of the issue” is the pricenet of underwriting fees disclosed on the cover of the prospectus. Each of these prices isexpressed on a per-security basis.

The “selling concession” is the difference between the offering price and the drawdownprice. The “banking group spread” is the difference between the drawdown price and thebanking group cost. The “management group spread” is the differe nce between the bankinggroup cost and the cost of issue. Each of these spreads is expressed on a per-security basis.The syndicate manager specifies other types of price structure in the Invitation.

2. Management Fee

Syndicate members share in the managem ent fee pro rata their syndicate percentage, afterdeduction of the step-up in favour of the syndicate manager or other lead manager sprovided that such step-up was set forth in the Invitation.

The “management fee” is the management group spread times the number of securitie sunderwritten.

3. Syndicate Profit

The syndicate profit or loss on an underwriting for a syndicate member is determined inthe following manner:

The banking group fee, being the banki ng group spread times the number of securitiesunderwritten;

Plus: profits on sales to exempt institutions, being the selling concession times th enumber of securities sold to exempts;

Less: the costs of market stabilization;

Less: the costs of covering over-allotments, being the difference between purchas eprice and drawdown price times the number of securities over-allotted;

Less: allowable syndicate expenses;

Times: the syndicate member's percentage

15

SYNDICATE PRACTICES HANDBOOK

Less: the costs of liquidating the long position, being the difference between ultimatedisposal price (including age ncy commissions, if any) and the drawdown prices timesthe number of securities held for the liability account of the individual syndicat emember according to the calculation set forth in III. 1.

4. Allowable Syndicate Expenses

The following expenses are incurred and paid by the syndicate manager on behalf of thesyndicate:

(a) all fees charged by the Canadian Depository for Secur ities for the use of their NewIssue Distribution System (NIDS) for settling a new issue;

(b) Investment Dealers Association of Canada levies charged on public and privatelyplaced offerings;

(c) all fees charged by legal counsel for the underwriters;

(d) all travel expenses (airfares, hotel, meals, etc.) for Member firm employees andprofessionals engaged by syndicate members involved in carrying out du ediligence responsibilities proxim ate to the offering. Travel expenses include visitsto issuer offices, location of operations and offices of related companies;

(e) the cost of all printing, photocopying, courier, telephone and facsimile charge srelated to the offering;

(f) the cost of advertising in newspapers and other media;

(g) the cost of all financing charges incurred on behalf of the syndicate by the lea dmanager, including (1) over-certification charges in connection with settling withthe issuer at closing, and (2) carrying costs associated with market stabilizatio nand unsold new issue security positions and late settlement of exempt sales;

(h) the cost of meals, meeting rooms and related expenses in carrying out syndicateresponsibilities including “road show” expenses (audio visual equipment ,presentation costs and ancillary expenses) not borne by the issuer;

(i) the cost of all entertainment, such as the closing dinner, related to the offering;

(j) the cost of all gift and mementos related to the offe ring provided to representativesof the issuer and members of the underwriting syndicate; and

(k) any miscellaneous charges related to the offering such as secretarial overtime, cabfares, etc.

16

SYNDICATE PRACTICES HANDBOOK

For greater certainty the following expenses are not considered proximate to the offering:expenses in connection with regular coverage or entertainment of the account an dextraordinary presentation expenses.

5. Payment of Underwriting Profits

Following is the schedule for payment of underwriting profits:

(a) the management fee is paid on the closing date;

(b) the selling concession is paid to syndicate members and selling group members bysettling with the members at the draw-down price on closing date on fir mallotments; and

(c) the syndicate profits are paid in two instalments. An interim payment amountingto 75% of the estimated syndicate profits is paid within 25 business days of th eclosing date and the final payment is made within 120 days of the closing date.

17

SYNDICATE PRACTICES HANDBOOK

VI. OTHER MATTERS

Syndicate arrangements include the following provisions:

1. Conflict Resolution

Except as noted below any dispute arising out of these arrangements and which the partiescannot resolve shall be decided by each side agreeing to be bound by the decision of a nindependent syndicate manager of their choice; if they cannot agree on one independentsyndicate manager, then each side shall nominate one independent syndicate manager andthe two independent managers shall ag ree on a third and the majority decision of the threeshall be determinative.

2. Choice of Law

The agreement evidencing the syndicate a rrangements shall be governed by and construedin accordance with the laws of the Province of Ontario and the laws of Canada applicabletherein.

3. Examination

Each syndicate member including th e syndicate manager shall agree to permit a charteredaccountant selected by the syndicate manager to examine the syndicate member's recordsrelating to sales of the securities which are the subject of the distribution to determin ewhether the offering terms or business practices set out in the syndicate arrangements arebeing or have been complied with and to report the results of such examination o rexaminations to the syndicate or syndicate manager, as the case may be.

4. Information

The syndicate manager shall provide to a syndicate member on request timely oral reportsof the status of the offering containing the information prescribed in III. 1.

Exhibit 1

PUBLIC OFFERING: ONE-WAY EXEMPT LIST

Type Equity Preferred

A.B.R.P.C.U.M. (Montreal Police) PF X

Aetna Insurance INS X X

AGF Management Ltd. MM X X

Air Canada PF X

Alberta Teachers PF X

Alberta Treasury P X

Alcan PF X

Allied Capital MM X X

Altamira Management Ltd. MM X X

American International Group (AIG) INS X

AMI Partners Inc. MM X X

Assurance Vie Desjardins INS X X

Bank of Canada PF X

Bank of Montreal BK X X

Bank of Nova Scotia BK X X

Batterymarch MM X

Berghuis Investment Counsel MM X X

Beutel Goodman & Co. Ltd. MM X X

Bimcor MM X X

Bisset & Associates MM X

Bloom Investment MM X X

Bluewater MM X

Bolton Tremblay Inc. MM X X

Bonavista (formerly Confed) MM X

BPI Capital MM X

C.F.G. Heward InvestmentManagement Limited MM X

Caisse de Depot et Placementsdu Quebec PF X X

Canada Life Assurance Company INS X X

Canada Life InvestmentManagement MM X

Canada Trust Company TC X X

Canadian BroadcastingCorporation PF X

2

PUBLIC OFFERING: ONE-WAY EXEMPT LIST

Type Equity Preferred

Canadian GeneralInvestments/Meighan's Assoc. MM X X

Canadian Imperial Bank of Commerce BK X X

Canadian National RailwayCompany PF X

Canadian Pacific Limited PF X

Canadian ReinsuranceCompany Limited INS X X

Canagex Limited MM X X

Capital Guardian/Capital Re US X

Cavaleti Investments Limited MM X

CIBC Trust TC X X

Citadel Life AssuranceCompany INS X X

Citibank US X

Citibank Canada BK X X

CMHC Pension PF X

Co-Operators InsuranceAssociation INS X X

Connor, Clark & Lunn MM X X

Conseillers Financiere St.Laurent MM X

Cote 100 MM X

Credit Suisse Canada BK X X

CREF US X

Crown Life Insurance Company INS X X

Delaney Capital MM X

Dominion Life AssuranceCompany INS X X

Domtar PF X

Dorchester Investments MM X

Dustan Waschell InvestmentManagement MM X X

E-L Financial Corporation INS X X

Eaton's PF X

Economical Mutual INS X X

Elliott & Page Ltd. MM X

F.W. Thompson Co. Ltd. MM X

3

PUBLIC OFFERING: ONE-WAY EXEMPT LIST

Type Equity Preferred

Fidelity US X

Fidelity Canada MM X

Fonds de la Solidarite PF X X

Foyston, Gordon & Payne MM X

General Accident INS X X

Gestion Sodagep MM X

Global Strategy MM X

Gluskin Sheff MM X

Goodman & Co. MM X X

Grantham Mayo US X

Great West Life Assurance INS X XCompany

Greystone (formerly ICS) MM X

Groupe Commerce MM X X

Gryphon Investments MM X X

Guarantee Company of INS X XNorth America

Guardian Capital MM X

Guardian Insurance INS X XCompany of Canada

Hamblin Watsa Investment MM X XCounsel

Hodgson, Roberton, Laing & MM X XCo.

Holdron Moreault MM X

Hong Kong Bank of Canada BK X X

Hospitals of Ontario Pension PF XPlan (HOPP)

Howson Tattersall MM X

Hudson's Bay Company PF X

Hughes, King MM X X

Hydro-Quebec PF X

I.A. Michael/ ABC Funds MM X

IDS Financial US X

Independent Order of INS XForesters

Insurance Corporation of INS XBritish Columbia

Investors Group MM X X

4

PUBLIC OFFERING: ONE-WAY EXEMPT LIST

Type Equity Preferred

Ivy Funds MM X

J.R. Senecal Ltd. MM X

Jarislowsky Fraser & Co. Ltd. MM X X

Jim Pattison Group MM X X

Jones Heward Investment MM X XManagement Inc.

Knight, Bain, Seath & Holbrook MM X X

Laketon Investment MM X XManagement

Lancaster Financial MM X X

Laurentian Bank of Canada BK X X

Leith Wheeler MM X

Letko Brousseau MM X

Lincluden Management MM X

London Life Insurance Company INS X X

M.K. Wong MM X X

M.S. Lamont MM X

MacKenzie Financial MM X XCorporation

Magnavista MM X

Managed Investments MM X

Manufacturers Life Insurance INS X XCompany

Maritime Life Assurance INS X XCompany

Marquest Investment Capital MM X X

Martin Lucas & Seagram MM X X

Maxima Investment MM X

McLean Budden Limited MM X

Mentor Capital Management MM X

Merrill Lynch Asset US XManagement

Montrusco Associes Inc. MM X X

MTA MM X

Mu-Cana MM X

Mulvihill & Associates MM X X

Mutual Life Assurance Co. of INS X XCanada

NatCan MM X

5

PUBLIC OFFERING: ONE-WAY EXEMPT LIST

Type Equity Preferred

National Bank of Canada BK X X

National Life Assurance Co. of INS X XCanada

National Trust TC X X

Ontario Hydro Pension Fund PF X

Ontario Municipal Employees PF XRetirement System

Ontario Teachers Pension Fund PF X

Oppenheimer US X

Pembroke Management MM X X

PEMP, Conseilliers en MM X XPlacements

Phillips, Hager & North Ltd. MM X

Polar Capital MM X

Province of British Columbia P X

Province of Manitoba P X

Province of New Brunswick P X

Province of Nova Scotia P X

Province of Saskatchewan P X

Prudential Insurance Company INS X Xof America

Prudential Portfolio Managers MM X(PPM)

Reitman's PF X X

River Road/Paloma Partners US X

Royal Bank Investment MM X XManagement

Royal Bank of Canada BK X X

Royal Insurance Company of INS XCanada

RT Capital MM X

S.T.C.U.M. (Montreal Transport) PF X

Sagit Management MM X

Sceptre Investment Counsel MM X XLimited

Scotia Investment Management MM X X

Scudder Stevens & Clark US X

Seaboard Life Insurance INS X X

Seamark MM X

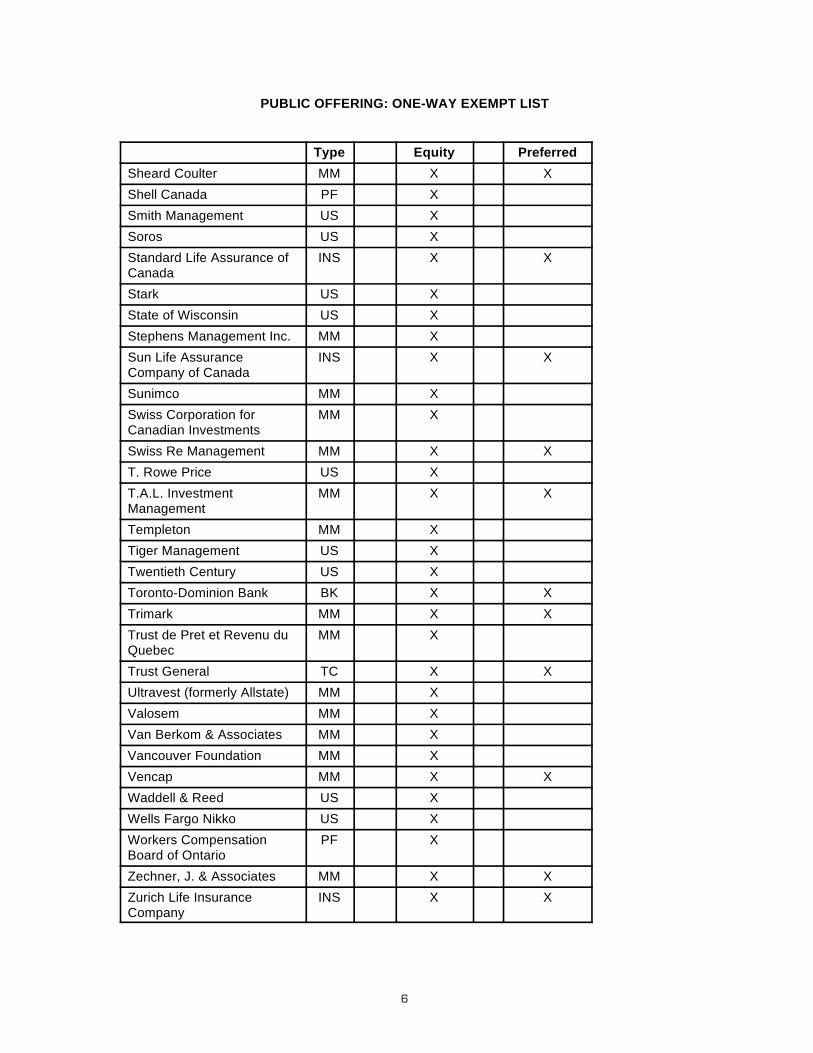

6

PUBLIC OFFERING: ONE-WAY EXEMPT LIST

Type Equity Preferred

Sheard Coulter MM X X

Shell Canada PF X

Smith Management US X

Soros US X

Standard Life Assurance of INS X XCanada

Stark US X

State of Wisconsin US X

Stephens Management Inc. MM X

Sun Life Assurance INS X XCompany of Canada

Sunimco MM X

Swiss Corporation for MM XCanadian Investments

Swiss Re Management MM X X

T. Rowe Price US X

T.A.L. Investment MM X XManagement

Templeton MM X

Tiger Management US X

Twentieth Century US X

Toronto-Dominion Bank BK X X

Trimark MM X X

Trust de Pret et Revenu du MM XQuebec

Trust General TC X X

Ultravest (formerly Allstate) MM X

Valosem MM X

Van Berkom & Associates MM X

Vancouver Foundation MM X

Vencap MM X X

Waddell & Reed US X

Wells Fargo Nikko US X

Workers Compensation PF XBoard of Ontario

Zechner, J. & Associates MM X X

Zurich Life Insurance INS X XCompany

PUBLIC OFFERING: ONE-WAY EXEMPT LIST

Code:BK — BankINS — Insurance Co.MM — Money Management and OthersP — ProvincePF — Pension FundTC — Trust CompanyUS — United States

Exhibit 2

DISTRIBUTION CERTIFICATE

[NAME OF DEAL]

[DEAL DESCRIPTION]

To: [Syndicate Manager][Investment Dealer] Due Date: [mm/dd/yy]

In accordance with the syndicate and/or selling group arrangements formed in conjunction with theabove issue, we hereby certify that we have completed distribution of this issue to the public andthat the distribution with respect to our allotment is as stated in the following table. In compiling thislist we have indicated that province in which the customer resides and not the location of our salesoffice. We understand that this distribution certificate is to be returned to you immediately followingour completion of distribution to the public.

Analysis ofSales

# of Size of # ofPurchasers Lots Shares

1 — 99100 — 499500 — 999

1,000 — 1,9992,000 — 2,9993,000 — 3,9994,000 — 4,999

over 5,000Totals

NUMBER OF NUMBER OFSALES SALES

British Columbia

Alberta

Saskatchewan

Manitoba

Ontario

Quebec

New Brunswick

Nova Scotia

P.E.I.

Newfoundland

U.S.A.

Other/International

Totals 0 0

![Henderson v Merrett Syndicates [1994] 3 WLR 761](https://static.fdocuments.in/doc/165x107/577cc1781a28aba711932aad/henderson-v-merrett-syndicates-1994-3-wlr-761.jpg)

![Index [researchonline.jcu.edu.au] · joint venture see Joint venture overview .... 16.2 partnership see Partnership sole trader see Sole trader syndicates see Syndicates trading trust](https://static.fdocuments.in/doc/165x107/5e1f645778460e348e4c4e11/index-joint-venture-see-joint-venture-overview-162-partnership-see-partnership.jpg)