by Professor Hsieh Intermediate Financial Accounting Accounting for Income Taxes.

41

by Professor Hsieh Intermediate Financial Accounting Accounting for Income Taxes

-

date post

22-Dec-2015 -

Category

Documents

-

view

235 -

download

4

Transcript of by Professor Hsieh Intermediate Financial Accounting Accounting for Income Taxes.

by Professor Hsieh

Intermediate Financial Accounting

Accounting for Income Taxes

Accounting for Income Taxes2

Objectives of the Chapter To learn the permanent difference

between the financial income and taxable income.

To learn the temporary difference between the financial income and taxable income.

To learn the accounting treatment for the temporary difference and permanent difference.

Accounting for Income Taxes3

Permanent Difference versus Temporary DifferencePermanent Difference:

A difference between financial income and taxable income in an accounting period that will never be reversed in later accounting periods.

This difference does not require an interperiod tax allocation.

Accounting for Income Taxes4

Permanent Difference versus Temporary Difference (contd.)Examples of Permanent Difference

1. Revenue recognized for F/R (financial report) but not taxable.

a. Interest on municipal bonds.

b. Life insurance proceeds payable to a corporation upon the death of an insured employee

Accounting for Income Taxes5

Permanent Difference versus Temporary Difference (contd.)Examples (contd.)

2. Expense recognized for F/R but not tax deductible:

Life insurance premium paid for employees.

3. Expense is tax deductible but not recognized for F/R purpose:

Percentage depletion in excess of Cost Depletion.

Accounting for Income Taxes6

Permanent Difference versus Temporary Difference (contd.)Temporary Difference:

A difference between a taxable income and a financial income in an accounting period that will be reversed in later accounting periods.

This difference requires an intertperiod tax allocation.

Causes of Temporary Difference:

Different treatment between GAAP and IRC

Accounting for Income Taxes7

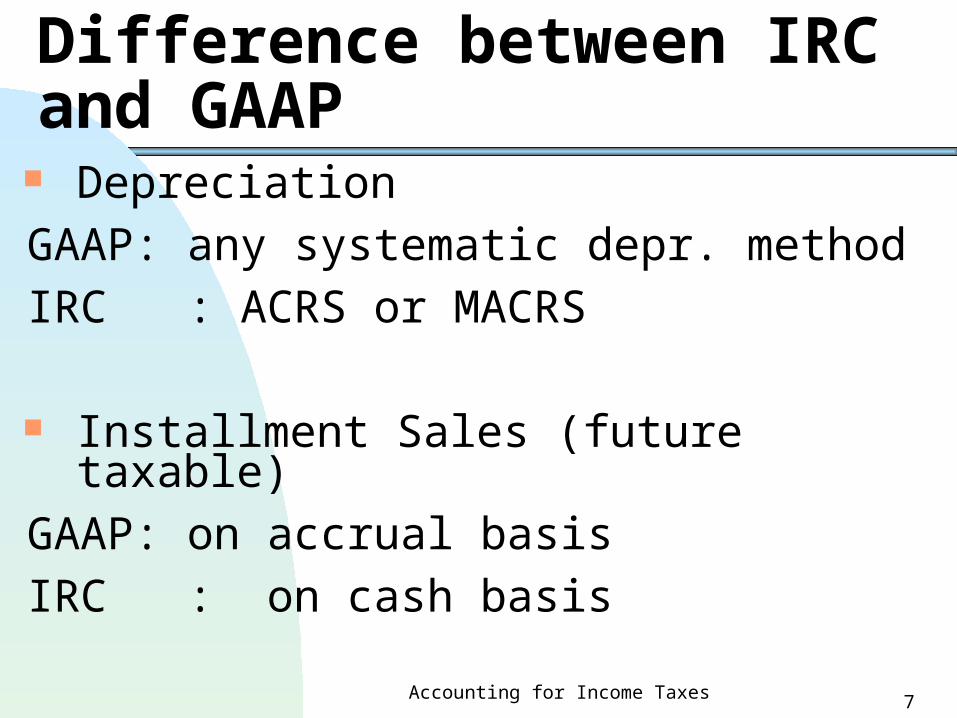

Difference between IRC and GAAP

Depreciation

GAAP: any systematic depr. method

IRC : ACRS or MACRS

Installment Sales (future taxable)

GAAP: on accrual basis

IRC : on cash basis

Accounting for Income Taxes8

Difference between IRC and GAAP (contd.)

Warranty Expense (future deductible)

GAAP: accrual basis (estimated and recognized at the end of each period)

IRC : cash basis (tax deductible when paid)Bad Debt Expense (future deductible)

GAAP: estimated and recognized at the end of each period.

IRC : tax deductible when accounts defaulted.

Accounting for Income Taxes9

Temporary Difference: an example

Depreciation method:

For tax filing purpose: ACRS, 4-year life For financial reporting purpose: straight-line method, 5-year life

The asset was purchased on 1/1/x1 with a cost of $10,000 and a zero residual value.

Accounting for Income Taxes10

Temporary Difference: an example (contd.)Financial depr. expense vs. tax depr.: Year S-L method

Depr. exp.Tax Depr.exp.

20x1 $2,000 $2,500a

20x2 $2,000 $3,750b

20x3 $2,000 $1,875c

20x4 $2,000 $1,250d

20x5 $2,000 $ 625

Accounting for Income Taxes11

Temporary Difference: an example (contd.)a. $10,000*50% *0.5 = 2,500b. $7,500*50% = 3,750 c. $3,750*50% = 1,875 d. $1,875*50% = 937.5 < (1,875/1.5 =1,250)

Accounting for Income Taxes12

Temporary Difference: an example (contd.)Assuming a 30% tax rate, the following table presents the annual temporary difference and the deferred tax liability:

Annual temp. diff.

Cum. Temp.diff

Ending deferred T/L

Beg. Deferred T/L

Change in defer. Liam.

500 500 150 0 150

1,750 2,250 675 150 525

(125) 2,125 637.5 675 (37.5)

(750) 1,375 412.5 637.5 (225)

(1,375) 0 0 412.5 (412.5)

Accounting for Income Taxes13

Temporary Difference: an example (contd.) T-account of the deferred tax liability

Deferred Tax Liability

20x3….. 37.5 150……..20x1

20x4…. 225 525……..20x2

20x5…. 412.5

0…..20x5

Accounting for Income Taxes14

Interperiod Income Tax Allocation

Example A: the following information is available for the year ended 12/31/x1: Accounting income = $10,400 Taxable income = $ 9,000 (AI > TI) Tax Rate = 30% The difference of $1,400 is resulting from using ACRS for I/T filing while using S-L for F/R purposes. This difference will be reversed as follows:

Accounting for Income Taxes15

Interperiod Income Tax Allocation

Reversed Amount (F/R depr.>Tax Depr.)

20x1 $500 20x2 700 20x3 200 Total 1,400

Tax payable for 20x1 = >

9,000 *30% =$2,700

Accounting for Income Taxes16

Interperiod Income Tax Allocation (contd.) Alternative Accounting Treatments

I. No Allocation of Deferred I/T Liam.

Income Tax Exp. 2,700 Income Tax Payable 2,700

II. With Allocation (comply with the matching principle) – Deferred Approach(APB No. 11)

Income Tax Expense 3,120 Income Tax Payable 2,700

Deferred Income Tax Liam. 420*

Accounting for Income Taxes17

Interperiod Income Tax Allocation (contd.) Alternative Accounting Treatments (contd.)

III.With Allocation- Liability Approach (SFAS 109)

Income Tax Expense 3,120 Income Tax Payable 2,700 Deferred Income Tax Liam. 420**

Accounting for Income Taxes18

Interperiod Income Tax Allocation (contd.) * Deferred tax lia. is calculated as income

tax exp. minus income tax payable.

**Deferred tax lia.is calculated based on the reversed amount in the future times the future tax rate. If the future tax rate remains at 30%, the deferred tax lib. Is $420. Otherwise, the deferred tax lib. will not be $420 (see the example next).

Accounting for Income Taxes19

Interperiod Income Tax Allocation (contd.)—Example BExample B: The taxable income of 20x1 = $9,000 The accounting income of 20x1 =$10,400

Partial Income statement: Pretax financial income $10,400 Less: additional accelerated depr. Deducted for I/T (1,400) Taxable Income $9,000

Accounting for Income Taxes20

Interperiod Income Tax Allocation (contd.)—Example B (contd.)At the beg. of 20x1, the deferred I/T has a balance of $0 (due to 20x1 is the first year of occurrence of difference in depr.) and the current tax rate is 30%.

There is no expectation of tax rate changes in the future.

Accounting for Income Taxes21

Interperiod Income Tax Allocation (contd.)—Example B (contd.)The financial depr. exp. will exceed the taxable depr. by the following amount in the next three years:

a&b: assumed numbers.

Year Acc.Depr.a Tax depr.b Diff.

20x2 $1,000 $500 $50020x3 1,000 300 70020x4 1,000 800 200

Accounting for Income Taxes22

Interperiod Income Tax Allocation (contd.)—Example B (contd.)The following table shows the annual temporary difference, accumulative temporary diff. and deferred liability (tax rate = 30%):

Year Temp. Diff Accu.

Temp. DiffEnd. Defer. I/T lia.

Beg. Defer. I/T lia.

Change in def. I/T lia.

20x1 $1,400 $1,400 $420 $0 420

20x2 (500) 900 270 420 (150)

20x3 (700) 200 60 270 (210)

20x4 (200) 0 0 60 (60)

Accounting for Income Taxes23

Interperiod Income Tax Allocation (contd.)—Example B (contd.)T-account of Deferred income tax lia.

Deferred I/T Liam.

20x2…..150 420…….20x1 20x3…..210 20x4….. 60

0 (bal)20x4

Accounting for Income Taxes24

Interperiod Income Tax Allocation (contd.)—Example B (contd.)J.E. (for 20x1) (based on APB No.11; the deferred approach)Income Tax Expense 3,120a Income Tax Payable 2,700 b Deferred Income Tax Liam. ? c

a: $10,400 (accounting income)*30% b. $9,000 (taxable income)*30%

c. ?= 3,120-2,700

Accounting for Income Taxes25

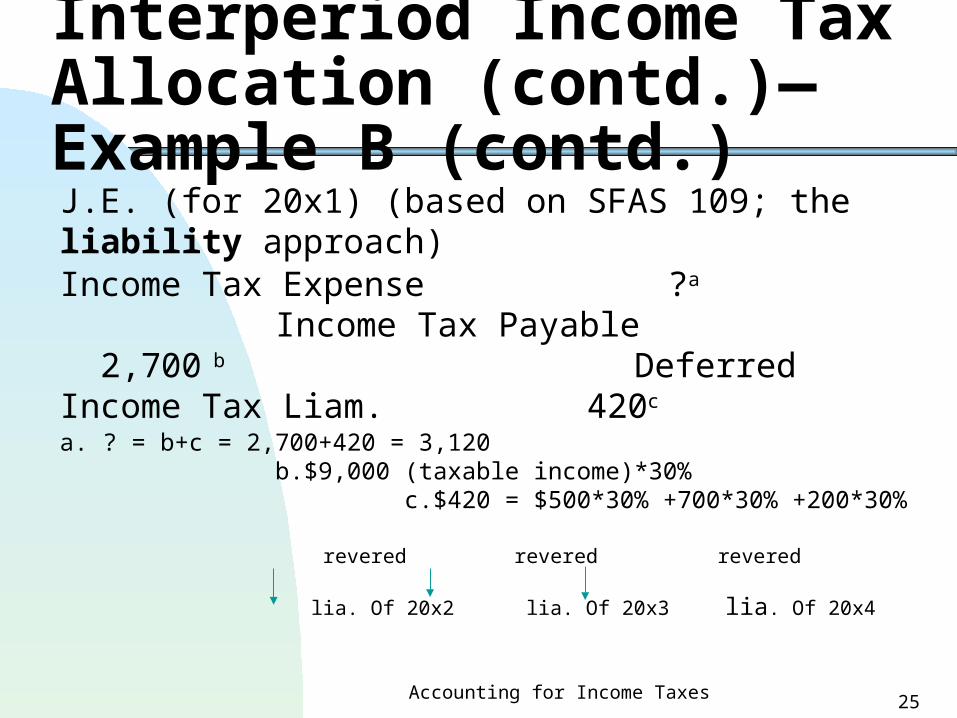

Interperiod Income Tax Allocation (contd.)—Example B (contd.)J.E. (for 20x1) (based on SFAS 109; the liability approach)Income Tax Expense ?a

Income Tax Payable 2,700 b Deferred Income Tax Liam. 420c

a. ? = b+c = 2,700+420 = 3,120 b.$9,000 (taxable income)*30% c.$420 = $500*30% +700*30% +200*30%

revered revered revered

lia. Of 20x2 lia. Of 20x3 lia. Of 20x4

Accounting for Income Taxes26

Interperiod Income Tax Allocation (contd.)—Example B (contd.)Note c is also presented in the following table:

a. Due to future taxable income > future acc. Income. It is a result of future tax depr. < future acc. Depr. b. Future expected tax rate should be used. Example B assumed all future tax rates remain at 30%.

20x2 20x3 20x3 Total

Futurea taxable amount

$500 $700 $200 $1,400

I/T Rate 30%b 30% 30%Defer. Liam. reversed

$150 $210 $60 $420

Accounting for Income Taxes27

Interperiod Income Tax Allocation (contd.)—Example B (contd.)

Assuming taxable income of 20x2,20x3 and 20x4 are $7,000, $6,000 and $8,000, respectively, journal entries of income tax for those year are as follows (all future tax rate remains at 30%) (follow SAFS 109):20x2 Deferred I/T Liam. 150 a I/T Expense ? b

I/T Payable 2,100c

a. See the previous table for year 20x2 b. income tax expense = $2,100 –150 c. taxable income 7,000*30%

Accounting for Income Taxes28

Interperiod Income Tax Allocation (contd.)—Example B (contd.)20x3 Deferred I/T Liam. 210 a I/T Expense ? b

I/T Payable 1,800c

20x4 Deferred I/T Liam. 60 d I/T Expense ? e

I/T Payable 2,400f

a. See the previous table for year 20x3 b. income tax expense = $1,800 –210 c. taxable income 6,000*30%d. See the previous table for year 20x4 e. income tax expense = $2,400 –60 f. taxable income 8,000*30%

Accounting for Income Taxes29

Interperiod tax Allocation with Different Expected Tax RateUsing the same information as in Example B except the tax rates are expected to change in the future as follows: 20x1 = 30% (the current year) 20x2 = 40% 20x3 = 40% 20x4 = 40%The ending bal. of the deferred I/T lia. for year 20x1 would be $$560 instead of $420 as in Example B when future rate states at 30%.

Accounting for Income Taxes30

Interperiod tax Allocation with Different Expected Tax Rate (cont.)The computation of the ending balance of deferred I/T lia. For 20x1 is as follows:

20x2 20x 3 20x4 TotalTaxable amount $500 $700 $200 $1,400I/T rate 40% 40% 40% 40%

Reversed tax lia. $200 $280 $80 $560

Accounting for Income Taxes31

Interperiod tax Allocation with Different Expected Tax Rate (cont.)Journal Entry for 20x1 is as follows based on a 40% expected tax rate for 20x2 to 20x4:

Income Tax Expense ?a Income Tax Payable 2,700 b Deferred Income Tax Liam. 560c

a. ? = b+c = 2,700+560 = 3,260 b.$9,000 (taxable income)*30% c.$560 = $500*40% +700*40% +200*40% or as shown in the previous table

Accounting for Income Taxes32

Interperiod tax Allocation with Different Expected Tax Rate (cont.)What if at the end of 20x2, the tax rate has been increased to 45% (instead of 40% as expected at the end of 20x1), the deferred liability at the end of 20x1 should have been $625a rather than $560 as using the 40% expected rate.The following adjusting entry should be prepared on 12/31/20x2: a. $500*45%+700*45%+200*45% = $625

Accounting for Income Taxes33

Interperiod tax Allocation with Different Expected Tax Rate (cont.)12/31/20x2

Loss on Adjustment of Deferred Taxes 65 a Deferred I/T Liam. 65

a. $625-560 = $65

Accounting for Income Taxes34

Interperiod tax Allocation – Example CThe following is a reconciliation of a pretax financial income with a taxable income for 20x3:Financial Income $3,000Add: estimated warranty exp. deducted for financial reporting in excess of actual warranty exp. deducted for I/T (a future

deductible) 100 Less:Additional accelerated depr. deducted for I/T (a future taxable) (150) Taxable Income $2,950

Accounting for Income Taxes35

Interperiod tax Allocation – Example C (contd.)No expectation of tax changes in the future and the current tax rate is 30%. The beginning balance of deferred income tax lia. account is $495 due to the first year of depr. exp. difference occurred in 20x1.

Accounting for Income Taxes36

Interperiod tax Allocation – Example C (contd.)Additional information regarding depr. exp. Lib. as follows:

a. 20x3 is the current year.

year Difference of tax depr. And financial depr.

20x1 $800 (tax dep>fin. Dep)20x2 860 (tax dep>fin. Dep)20x3a 150 (tax dep>fin. Dep)20x4 (300) (fin.dep > tax dep)

20x5 (300) (fin.dep > tax dep) 20x6 (1,200) (fin.dep >taxdep)Total 0

Accounting for Income Taxes37

Interperiod tax Allocation – Example C (contd.)The followings are projections regarding the temporary differences for years 20x4 to 20x6(future years):

a. Tax warranty cost in excess of financial warranty cost b. Financial depr. exp. In excess of tax depr. exp.

year Diff. In warranty amounta

Diff. In depr. amountb

20x4 $50 $ 30020x5 30 30020x6 20 1,200Total $100 $1,800

Accounting for Income Taxes38

Interperiod tax Allocation – Example C (contd.)J.E. for the current year 20x3 (SFAS 109):

I/T Exp. ?a

Deferred I/T assets 30b

I/T Payable 885c

Deferred I/T Liam. 45d a. $885+45-30 = $900 b. $50*30%+30*30%+20%30% = 100*30% =$30 c. $2,950*30% = $885 d. (800+850+150)*30% - $495 = $540-495 = $45

Accounting for Income Taxes39

Interperiod tax Allocation – Example C (contd.)T-accounts of deferred tax lia. And deferred tax assets:

Deferred I/T Asset Deferred I/T Liam. beg. bal. 0 495..beg.bal. Adj. Of 20x3 30 45..adj.Of 20x3

30a 540b

a. $50*30%+30*30%+20%30% = 100*30% =$30 b.(800+850+150)*30% =1,800*30% =$540

Accounting for Income Taxes40

Interperiod tax Allocation – Example C (contd.)Presentation of selected accounts on I/S:

Pretax Income $3,000 I/T exp. (900) Net Income $2,100

Presentation of selected accounts on B/S:

Current Assets: Current Lia.:

Deferred Tax Assets 30 I/T Payable 885 Deferred Tax Lia. 540

Accounting for Income Taxes41

Interperiod tax Allocation – Example C (contd.)Had APB No. 11 been followed (the deferred approach), the following entry will be prepareda:

I/T Exp. (3,000*30%) 900

I/T Payable (2,950*30%) 885

Deferred I/T Liam. (900-885) 15

a. This treatment is NOT acceptable.