by L. Brad Harvey A practicum thesis submitted to Johns ... · A practicum thesis submitted to...

46

1816 NORTH CLARK STREET HOTEL CASE STUDY by L. Brad Harvey A practicum thesis submitted to Johns Hopkins University in conformity with the requirements for the degree of Master of Science in Real Estate Baltimore, Maryland December 16, 2010

Transcript of by L. Brad Harvey A practicum thesis submitted to Johns ... · A practicum thesis submitted to...

1816 NORTH CLARK STREET HOTEL

CASE STUDY

by L. Brad Harvey

A practicum thesis submitted to Johns Hopkins University in conformity with the requirements for the degree of Master of Science in Real Estate

Baltimore, Maryland December 16, 2010

Case Study – 1816 North Clark Street Hotel/ December, 2010

Hotel Case Study – December 2010 L. Brad Harvey

Table of Contents

Summary ....................................................................................................................................................... 2

The Hotel ....................................................................................................................................................... 4

Location Map ................................................................................................................................................ 5

Typical Floor Plate ......................................................................................................................................... 6

Background on Case ...................................................................................................................................... 7

Property Description ..................................................................................................................................... 8

Market Description and Performance ........................................................................................................ 10

Hotel Demand Drivers ................................................................................................................................. 14

Leasing Plan ................................................................................................................................................. 15

Financial Analysis ........................................................................................................................................ 20

Sources ........................................................................................................................................................ 21

Uses ............................................................................................................................................................. 22

Capital Markets ........................................................................................................................................... 23

Case Study Assignment ............................................................................................................................... 29

Appendix: Loan Summary ........................................................................................................................... 30

Appendix: Property Condition Report ........................................................................................................ 32

Appendix: Revenue Assumptions ............................................................................................................... 33

Appendix: Expense Assumptions ................................................................................................................ 34

Appendix: Net Operating Income Proforma ............................................................................................... 35

Appendix: Proforma Percentage Allocations .............................................................................................. 36

Appendix: Occupancy Analysis.................................................................................................................... 37

Appendix: Competitive Analysis ................................................................................................................. 38

Appendix: STR Report ................................................................................................................................. 39

Bibliography ................................................................................................................................................ 45

Case Study – 1816 North Clark Street Hotel/ December, 2010

Hotel Case Study – December 2010 L. Brad Harvey

Summary The 1816 N Clark Street Case Study is on a stalled renovation project on an existing hotel located in Chicago’s Lincoln Park neighborhood. And while the case study could be looked at from a few different angles in this case study you are working for the construction lender who has a substantial investment in the project and must determine the best option to preserve it. The renovation is not complete, mechanics liens exist, there is an unhappy restaurant tenant operating on the first floor, and the project is under control of an SEC appointed receiver. In the spring of 2008 the Lincoln Park Hotel, located at 1816 North Clark Ave in Chicago, was nearing completion when the sponsor ran out of money. The construction work was over 90% complete and the FF&E was either in storage or had been ordered. A temporary occupancy certificate inspection had been performed by the city and while it was not awarded the findings could have been easily fixed. The general contractor estimated that had the funds been available they could have had a TCO within 90 days. Another 30 days would have been needed to furnish the rooms and the hotel could have been open in August. (Kleese, 2008) The following happened instead. On August 11, 2008, the United States Securities and Exchange Commission ("SEC") filed charges against Steven Byers, Joseph Shereshevsky, Wextrust Capital, LLC ("Wextrust") and four affiliated Wextrust entities, alleging that the defendants conducted a massive Ponzi‐type scheme from 2005 or earlier that raised approximately $255 million from approximately 1,200 investors, most of whom were members of the Orthodox Jewish Community. The SEC also sought and obtained emergency relief to freeze the defendants' assets and place the Wextrust entities under the control of a receiver to safeguard assets. The Court appointed Timothy J. Coleman as Temporary Receiver for the Wextrust entities. The United States Attorney's Office for the Southern District of New York has filed a criminal complaint against Steven Byers and Joseph Shereshevsky. (Wextrust SEC website, 2008) This has become an all too common problem in real estate projects that were in construction and not completed when the market began to fall in 2008. Many lenders and investors are faced with similar problems every day in the current marketplace. This property not only has construction risk and market risk but there is also risk associated with local lien laws and the SEC receiver. Though the latter may not be common on all stressed projects, a lender or potential investor must understand the receiver’s position much like they would a borrower’s position. A Receiver is put in place by the judge to protect the interest of those who have invested in the Ponzi scheme and is tasked with recouping as much of the investment as possible. In the case of Wextrust, the Receiver’s first order of business was to freeze all Wextrust assets and hire someone to value the portfolio of real estate assets. The amount of time before the project will be released by the courts is an unknown and any analysis of this property must account for potential delays the Receiver and judge

Case Study – 1816 North Clark Street Hotel/ December, 2010

Hotel Case Study – December 2010 L. Brad Harvey

may pose while completing their underwriting. Much like a property in a judicial foreclosure or bankruptcy, the time you must account for before being able to take control of the property is a difficult assumption. On top of that a title report has indicated that there are approximately $3.3 million in mechanics liens on the project placed by subcontractors and the general contractor for work that is complete. The major trade contracts are not currently complete so none of their work is warranted. While negotiating a reduction to the total amount outstanding may be an option, getting lien holders back in the hotel to complete their work is a top priority. Negotiations with contractors could be further strained by the fact that the lender is a comingled fund and many of their investors are union pension funds that require work to be performed by union tradesmen. The lender must also take steps to protect its investment in the hotel. Dealing with the Receiver can be tedious and this does not help an unfinished construction project. The longer it sits partially complete the more the value of the property could deteriorate. By the third quarter of 2008 the Chicago hospitality market was still strong. The future, however, is not as rosy as companies across the country have begun to reduce travel expenditures. The financial model that accompanies the case study provides a basic analysis cost to complete, required rates of return for interested parties, waterfall scenarios, and use market date from a STR report. These options include but are not limited to taking‐back the building, constructing, stabilizing, and selling. In addition, the analysis will be performed and analyzed to consider finishing construction and holding the property in portfolio until such time it is best to divest the asset. In researching this case study many conversations arose with individuals who have knowledge of this projects construction, the original Wextrust business plan, as well as the Chicago hospitality market. The most extensive conversations were with those who have experience in dealing with SEC appointed receivers. Remember the job of the receiver is to squeeze as much value as possible, in this case, out of each Wextrust real estate asset. Data and information specific to the hospitality market came from STR reports and information from appraisal firms like HVS and Cushman Wakefield. The following case study is based on the issues the lender faced once the sponsor was arrested and the project was under the control of the receiver. This exercise will require the reader to determine which scenario they believe will recoup the greatest value using the information and the model provided while taking into consideration the risk of each possible scenario. Factors that will need to be taken into consideration include cost‐to‐complete, hospitality market, historical tax credits, and the complexities of an SEC appointed receiver.

Case Study – 1816 North Clark Street Hotel/ December, 2010

Hotel Case Study – December 2010 L. Brad Harvey

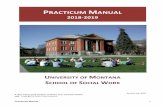

The Hotel Geographic Location: Chicago, IL Asset Type: Non‐flagged hotel Current Status: Held by an SEC

appointed Receiver. First lien holder is a commingled pension fund. Property is nonoperational less a 2500 square foot restaurant which provides (type of rent). Further, some advertising income comes from advertising along the side of the hotel.

Project Size: Asset Summary

• The Hotel is a 95,000 square foot, 194 key.

• The Hotel also has two meeting/conference rooms (totaling 1,250 square feet), a 650 square foot pre‐function area, a rooftop garden terrace and penthouse unit, administrative offices, the Perennial Restaurant, and a fitness facility.

• Hotel is in the midst of an incomplete renovation project which began in October 2006 and stalled in March 2008.

• Current estimates are $6 million to complete the remaining construction. A significant portion of the cost‐to‐complete is $3.3 million in liens.

• The Hotel qualified and received Historic Tax Credits through a RTC partnership structure designed to accept such credits.

• The hotel has no designated parking but can be contracted out with public and private parking lots close to the property.

Case Study – 1816 North Clark Street Hotel/ December, 2010

Hotel Case Study – December 2010 L. Brad Harvey

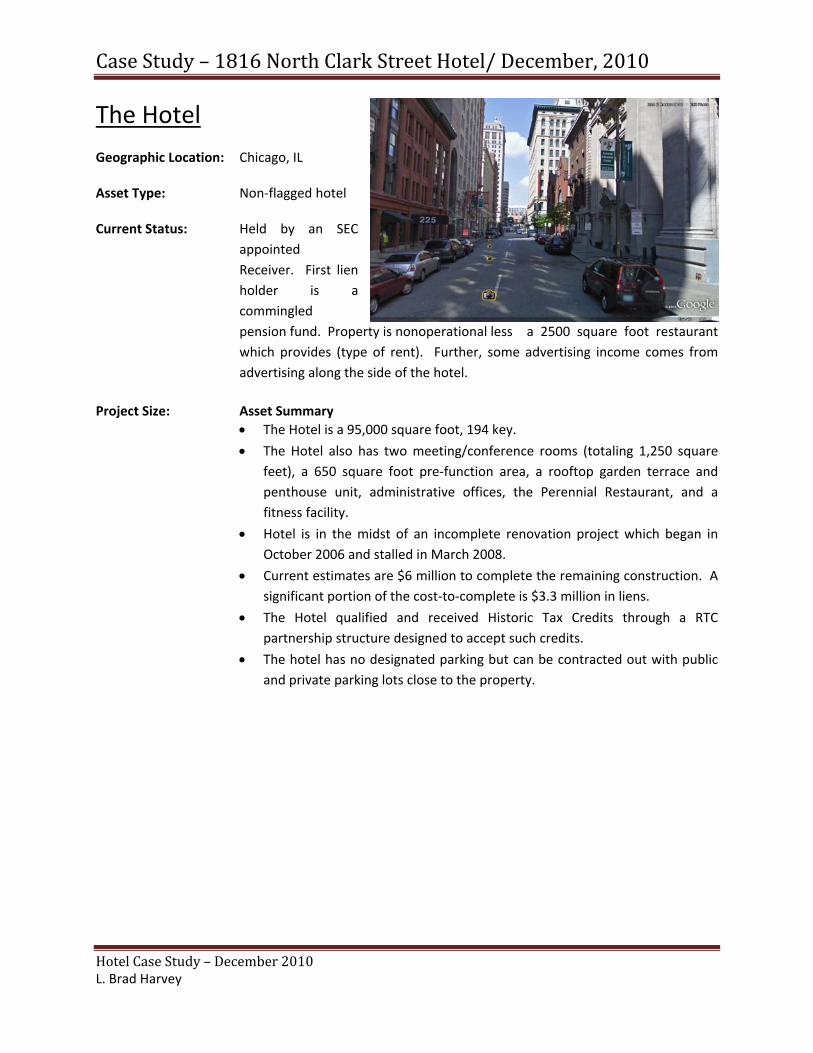

Location Map

Case Study – 1816 North Clark Street Hotel/ December, 2010

Hotel Case Study – December 2010 L. Brad Harvey

Typical Floor Plate

Case Study – 1816 North Clark Street Hotel/ December, 2010

Hotel Case Study – December 2010 L. Brad Harvey

Background on Case On August 11, 2008, the United States Securities and Exchange Commission ("SEC") filed civil charges against Steven Byers, Joseph Shereshevsky, Wextrust Capital, LLC ("Wextrust") and four affiliated Wextrust entities, alleging that the defendants have conducted a massive Ponzi‐type scheme, starting in 2005 or earlier, that raised approximately $255 million from approximately 1,200 investors. On the same date, the SEC also sought and obtained emergency relief to freeze the defendants' assets and place all entities connected with the defendants, including Gold Coast Investors LLC, the equity holder of the Hotel, under the control of the receiver. The Court appointed Timothy J. Coleman, a partner with the law firm of Dewey & LeBoeuf, LLP as Receiver for the Wextrust entities. The United States Attorney's Office for the Southern District of New York has filed a criminal complaint against Steven Byers and Joseph Shereshevsky. Since August 11, there has been frequent contact with the Receiver and his colleagues in an attempt to resolve issues connected with this loan, in particular, securing the funds needed to release mechanics liens of approximately $3.2 million and complete the Hotel renovation. As there was a significant “mixing” of funds by the defendants, determining which Wextrust entity truly owned the property has been extremely problematic for the receiver. As noted earlier, the Hotel is not operating, but is incurring ongoing expenses to maintain, including taxes and utilities. In addition, the general contractor has warned of a number of conditions that could significantly damage the property if not attended to. As noted, in addition to the construction work that remains to be completed, there are a number of permits that must be obtained before the Hotel can operate, e.g. certificate of occupancy. Accordingly, the Lender (a co‐mingled fund that has the senior debt position on the property) has been stressing to the Receiver the immediate need to resolve the issues before the value of the Hotel is significantly reduced. Legal counsel has advised that court approval is required to bring foreclosure proceedings, and that the process would be time consuming. Thus, although the Lender has contacted the Receiver and mentioned their willingness and ability to seek foreclosure if it appeared that our investors interests were best served by taking such action as a fiduciary on their behalf, they have also made it clear that they are willing to work with the Receiver so long as it moves promptly to resolve the matter. The Lender has been advised by counsel that the Receiver has now brought an emergency request for relief to the court to enable the Receiver to use all funds in the receivership freely, without regard to their source, which would, among other things, enable the Receiver to apply the resources needed to preserve the value of the Hotel. The property was built in 1928 as a hotel and has remained a hotel since. Updates were performed in the early 1990’s as the hotel changed management and became a Days Inn Hotel. In 2005 the property was purchased by Goldcoast with the intentions of turning the hotel into an independent boutique hotel.

Case Study – 1816 North Clark Street Hotel/ December, 2010

Hotel Case Study – December 2010 L. Brad Harvey

After operating the property for two years under the Days Inn flag the new owner used this time to determine which systems needed to be updated as well as gaining a better understanding of the existing room layouts. Updates included mechanical systems and bringing the project compliant with ADA.

Property Description The Hotel is a 12‐story property originally constructed in 1928, and has undergone several renovations including extensive work in 1997 and the current suspended overhaul. The Hotel contains approximately 95,000 square feet of gross building area. This upscale lodging facility containing 194 keys, two meeting/conference rooms totaling 1,250 square feet, a 650 square foot pre function area, a rooftop garden terrace with an unmatched view of Lake Michigan and penthouse unit, administrative offices, Perennial restaurant, a fitness facility, and typical office facilities required to run a hotel of this size and magnitude. Guest rooms are provided on floors 3 through 12 with one penthouse guestroom suite located on floor 13. The basement provides a second kitchen and central mechanical rooms. Parking is provided by off‐site public garages and street‐metered parking throughout the neighborhood. Renovation Status The Hotel has undergone a full building renovation with construction reportedly commencing in October 2006 and ending in March 2008 short of the project completion date due to the financing being in default. Currently the Hotel is vacant with the exception of the ground floor restaurant tenant. When the renovation stopped it was estimated to be approximately 95 percent complete with punch list construction items remaining. None of the warranties for the work are valid. Interviews with the construction engineer found that there were several incomplete or problematic building condition items brought up in addition to punch list items, such as façade work, persisting mold, and rusty window frames. The renovation building permit was issued October 17, 2006 by the City of Chicago’s Building Department. A construction consultants retained by Lender to evaluate the existing building condition, state in their December 2008 Opinion of Probable Costs Report that various disciplines have been signed off as Final, but not all construction disciplines were signed as Final. A Partial Certificate of Occupancy was issued by the City of Chicago Building Department dated June 10, 2008 for Floor 1 Lobby and Base Building Retail and Commercial Spaces. Currently Perennial, the restaurant tenant, occupies the building. Please refer to the summary of property condition report in the Appendix section of this report for further permitting and construction related details. Lien Status There are approximately $3.3 million in total liens outstanding on the Hotel, of which $3.2million is from the General Contractor. A new $100,000 lien was recently filed by the mold remediation specialist for unpaid work. The construction consultant is confident the liens can be negotiated down by

Case Study – 1816 North Clark Street Hotel/ December, 2010

Hotel Case Study – December 2010 L. Brad Harvey

approximately 25% with the General Contractor. It is also the consultant’s opinion that if the General Contractor is paid off he will be interested in returning to finish the job. Note that a reduction in lien payoff may be problematic as investors in the Lender are union pension funds. Union labor has been used to complete all work on the hotel and therefore a reduction in liens could be problematic at best. Further note that liens accrue interest at a regulatory rate of 10% in Illinois. Therefore, the General Contractor, who is well capitalized, can afford to wait as there is a belief in a final settlement. Tax Credits The Hotel’s ownership is held through a credit pass‐through lease structure set up by Wextrust to facilitate the syndication of federal rehabilitation tax credits, or “RTCs.” The RTC investor provided for a 10 percent income tax credit for qualified expenditures or “QREs” related to the substantial rehabilitation of a qualified rehabilitated building. In this transaction, TCC formed an operating company as the “Master Tenant” in order to enter into a master lease with Gold Coast Investors, LLC, the borrowing entity with $1,062,188 of equity intended for the purchase of furniture, fixtures and marketing expenses. They also committed to contributing additional equity of $326,827 upon completion and delivery of a cost certification and $245,120 once the project has operated at breakeven for a period of six months. The Master Tenant is not a member in the Borrowing entity. Under the current circumstances, the Lender must consider if it wants to continue with the syndication of the RTCs and, if not, how to unwind the structure. The major disadvantage of this structure is the credit pass‐through lease will need to be in place for at least 60 months from the date the building rehab is placed in service, or else some or all of the RTCs may be recaptured. A future buyer or joint venture partner will have to buy the Hotel (or portion of the Hotel), subject to the Master Lease, potentially limiting the salability of the fee simple. During the 60‐month period, the buyer of the fee simple cannot be a tax exempt entity such as a state entity, REIT or pension fund. There are further complications for the Lender if this structure stays in place:

1. TCC will share in a portion of the project’s cash flow with a nominal $5,000 asset management fee and an annual preferred return on its capital contribution of 3percent,

2. The Lender will have to step into Wextrust’s place and operate the Hotel according to the multi‐tiered syndication structure, and

3. TCC will most likely insist on certain rights that could result in a loss of operational autonomy for the Lender including consent to sell the Hotel that could result in the termination of the Master Lease.

Perennial Restaurant Approximately 3,200 square feet of restaurant and lounge space is leased to Perennial Restaurant, operated by Richard Katz of the RK Group. This restaurant is critically acclaimed and extremely popular with patrons. At the moment the only meal the restaurant serves is dinner. RK Group is owed $100,000 for tenant improvement work to the restaurant in addition to $150,000 owed to them for work they were required to do utilizing union labor. Currently Perennial is not paying rent, as their lease does not

Case Study – 1816 North Clark Street Hotel/ December, 2010

Hotel Case Study – December 2010 L. Brad Harvey

require rent to be paid until the Hotel opens. The restaurant has proven so profitable Richard Katz believes if he were paying rent at this time he would already be paying percentage rent.

Market Description and Performance National Hospitality and Tourism Outlook The national recession has hit the hospitality sector hard, pushing down occupancy and forcing more property owners to cut daily rates to boost demand. National occupancy, according to Marcus & Millichap’s Q2 2009 Hospitality Research, states that conditions are expected to remain weak over the remainder of 2009 as persistent job losses discourage leisure travel and cost conscious businesses cut trips. Revenue per available room (RevPAR) is a performance indicator that reflects trends in both occupancy and the average daily rate (ADR). This source also cites a year to date national occupancy rate of approximately 54 percent, with the national ADR sliding to under $100 and RevPAR declining by double digits. Negatively impacted by the decline in business travel, tight capital markets and weakening of operating fundamentals, hotel asset values have fallen in the past 12 months. The recent bankruptcy filing of Extended Stay Hotels could be a harbinger of future additional distress in this asset class. The delinquency rates on loans backed by hotel properties is anticipated to rise as falling room rates exert downward pressure on property owners. Marcus & Millichap opined that the early 2003 lodging property delinquency rate of 8.4 percent could potentially be reached again in the next several quarters as cash flows continue to decrease, particularly with properties purchased in 2006 and 2007. National Supply Outlook Supply trends are related to the availability and cost of financing, as financing is one of the greatest barriers to entry for new hotel development. New hotels are coming online at a brisk pace. Currently there are approximately 159,000 hotel rooms under construction nationally, including more than 75,000 rooms affiliated with national full‐service brands. Since the third quarter of last year construction financing has become less available and projects have been removed from the pipeline. The weakening of hospitality fundamentals plus constraints on capital has forced the pipeline of planned projects to contract 22 percent from one year ago to 520,000 rooms. (Note: 159,000 (in construction) versus 520,000 (planned, construction not started) rooms) Marcus and Millichap report there is a growing sentiment among hotel analysts and national brands that the industry is passing through the worst phase of the down turn, and conditions may start to stabilize soon.

Case Study – 1816 North Clark Street Hotel/ December, 2010

Hotel Case Study – December 2010 L. Brad Harvey

Source: Smith Travel Research, Inc.

Employment Effects on the Hospitality Industry According to Economy.com the office using employment sector has fallen by 900,000 positions year to date for 2009 and is down nearly 2 million workers during the recession. Employment losses erode hotel room demand as consumers reduce spending on discretionary purchases such as travel and vacations. Businesses have drastically cut travel budgets. The drop in office employees has adversely affected hospitality occupancy during the Tuesday through Thursday period. So far this year, occupancy has averaged approximately 55 percent on these days, compared with 64 percent in the corresponding time frame in 2008. Future Hospitality Forecast STR projects that at the end of 2009, supply will be up 3.0 percent, demand will be down 5.5 percent, occupancy will decline 8.4 percent, average daily rate will drop 9.7 percent, and revenue per available room will be down 17.1 percent. The outlook for 2010 looks slightly better than 2009, but nationally the industry still is expected to end 2010 with decreases in all three key metrics. Occupancy is projected to end 2010 with a 0.6‐percent decrease, ADR is forecasted to end the year with a 3.4‐percent decrease, and RevPAR is expected to end with a 4.0‐percent decrease in occupancy. With talk of improvement in the overall U.S. economy and a relative stabilization of transient leisure demand, there seems to be light at the end of the tunnel. A key indicator for recovery might be demand in group and transient business travel as the conference season begins. This is the greatest demand group in the Chicago market due to McCormick Place and Navy Pier. Although it is likely leisure demand will lead the hotel industry recovery, stronger‐than‐expected performance in group business would be a welcomed addition. Chicago Hospitality Market History The number of rooms in Chicago has increased by approximately 10,463 units from 1987 through the present, or about 38 percent. Most of this development occurred in two distinct periods of industry expansion. Between year‐end 1987 and 1993, the citywide hotel inventory increased by nearly 6,300 rooms, representing a supply increase of approximately 22.6 percent over the six‐year period. The hotel room supply decreased by roughly 2,000 rooms between year‐end 1993 and 1997. A slower, but longer‐lasting, expansion period extended from year‐end 1997 through 2005, when the hotel inventory grew by almost 4,500 rooms. Supply declined slightly between year‐end 2005 and 2007. A third cycle of supply

Metrics Absolute % ChangeHotels 51,459 2.7%Room Supply 4.8mm 3.2%Room Demand 2.2mm ‐8.0%Occupancy 54.6% ‐10.9%ADR $98.66 ‐8.7%RevPAR $53.97 ‐18.7%Room Revenue $45.7B ‐16.1%

US Market Key Hospitality Statistics June 2009 YTD

Case Study – 1816 North Clark Street Hotel/ December, 2010

Hotel Case Study – December 2010 L. Brad Harvey

growth began when several new hotels opened in 2008, increasing supply by nearly 1,900 rooms in 2008.

Source: STR, Inc Day of the Week Analysis RevPAR ($) 2007 and 2008 In 2007 the hotel industry peaked, setting records for the highest occupancy, ADR, and RevPAR levels achieved since 1987, the earliest year for which city wide data records are available. The effects of the national recession negatively affected hotel performance in 2008, when occupancy fell from 74 percent to 71 percent. In 2008, ADR surpassed that of 2007, with an average ADR of $187.6. Nonetheless, increases in ADR were not able to counteract the effect of lower occupancies, resulting in a 2008 RevPAR of $133.0, approximately $4.2 below the RevPAR of2007. According to STR, by year‐end 2008 there were 38,256 hotel rooms in Chicago, reflecting a significant increase from the 36,381 hotel rooms at year‐end of 2007. After relatively little supply growth in Chicago between 2003 and 2007, supply increased by 5.2 percent in 2008, thereby exacerbating the negative effects of the economic recession. STR also noted that demand has increased in 16 of the last 22 years in Chicago, while supply has increased in 15 of these years. However, the current economic recession and tightened credit markets are severely limiting the pipeline of new supply expected to take place in the Chicago market during the next several years. Although future group bookings at McCormick Place and across the Chicago hotel industry show further deterioration of demand through 2009, near term advance bookings for transient demand in Chicago show an improvement this summer versus last summer. HVS Hospitality Consultants conducted a study of the Chicago market along with interviews with hotel managers that indicate that the Chicago hotel industry will continue to struggle through 2009, with a probable recovery in mid to late 2010. It is HVS’s opinion that this may lead to growth in hotel demand for 2011 and 2012 that exceeds supply growth. HVS is predicting that overall hotel performance is likely to continue to decline year‐over‐year in the near‐term through the end of 2009, but should flatten in 2010, and see growth in 2011 and 2012. Peak Month and Days of the Chicago Hospitality Market The late spring months of May and June and early fall months of September and October represent the high seasons for the Chicago hotel industry. During those times of the year, meeting and group demand often peaks, and both commercial and leisure demand levels are also strong. While high occupancies are also attained in July and August, ADR levels during that two‐month period are well below those attained in the peak months. According to STR, the market’s low season includes the winter months of

Sun Mon Tue Wed Thu Fri Sat Total YearJul 06 ‐ Jun 07 87.74 99.97 105.47 103.57 99.70 117.26 130.17 106.33Jul 07 ‐ Jun 08 86.48 100.44 104.69 98.18 96.94 116.59 131.93 104.97Jul 08 ‐ Jun 09 73.02 81.69 84.75 84.09 84.00 101.43 116.81 89.39

Total 82.30 93.89 98.01 95.08 93.39 111.60 126.20 100.07

Day of the Week Analysis RevPAR ($)

Case Study – 1816 North Clark Street Hotel/ December, 2010

Hotel Case Study – December 2010 L. Brad Harvey

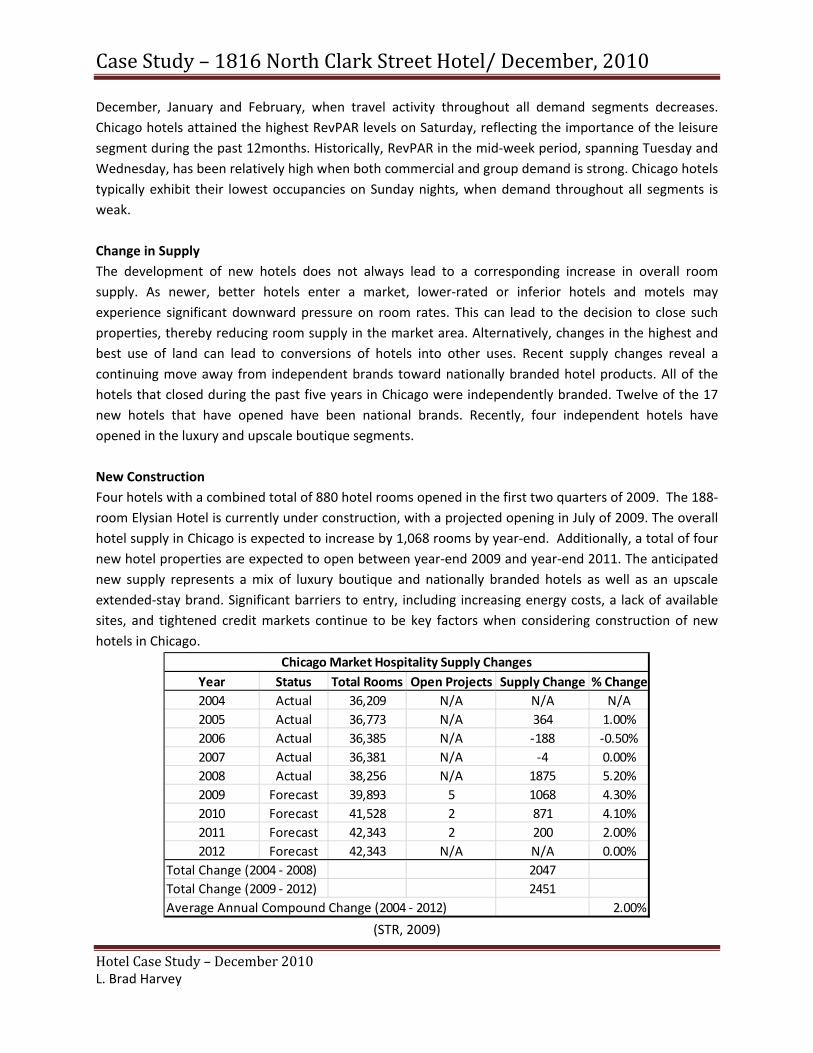

December, January and February, when travel activity throughout all demand segments decreases. Chicago hotels attained the highest RevPAR levels on Saturday, reflecting the importance of the leisure segment during the past 12months. Historically, RevPAR in the mid‐week period, spanning Tuesday and Wednesday, has been relatively high when both commercial and group demand is strong. Chicago hotels typically exhibit their lowest occupancies on Sunday nights, when demand throughout all segments is weak. Change in Supply The development of new hotels does not always lead to a corresponding increase in overall room supply. As newer, better hotels enter a market, lower‐rated or inferior hotels and motels may experience significant downward pressure on room rates. This can lead to the decision to close such properties, thereby reducing room supply in the market area. Alternatively, changes in the highest and best use of land can lead to conversions of hotels into other uses. Recent supply changes reveal a continuing move away from independent brands toward nationally branded hotel products. All of the hotels that closed during the past five years in Chicago were independently branded. Twelve of the 17 new hotels that have opened have been national brands. Recently, four independent hotels have opened in the luxury and upscale boutique segments. New Construction Four hotels with a combined total of 880 hotel rooms opened in the first two quarters of 2009. The 188‐room Elysian Hotel is currently under construction, with a projected opening in July of 2009. The overall hotel supply in Chicago is expected to increase by 1,068 rooms by year‐end. Additionally, a total of four new hotel properties are expected to open between year‐end 2009 and year‐end 2011. The anticipated new supply represents a mix of luxury boutique and nationally branded hotels as well as an upscale extended‐stay brand. Significant barriers to entry, including increasing energy costs, a lack of available sites, and tightened credit markets continue to be key factors when considering construction of new hotels in Chicago.

(STR, 2009)

Year Status Total Rooms Open Projects Supply Change % Change2004 Actual 36,209 N/A N/A N/A2005 Actual 36,773 N/A 364 1.00%2006 Actual 36,385 N/A ‐188 ‐0.50%2007 Actual 36,381 N/A ‐4 0.00%2008 Actual 38,256 N/A 1875 5.20%2009 Forecast 39,893 5 1068 4.30%2010 Forecast 41,528 2 871 4.10%2011 Forecast 42,343 2 200 2.00%2012 Forecast 42,343 N/A N/A 0.00%

Total Change (2004 ‐ 2008) 2047Total Change (2009 ‐ 2012) 2451Average Annual Compound Change (2004 ‐ 2012) 2.00%

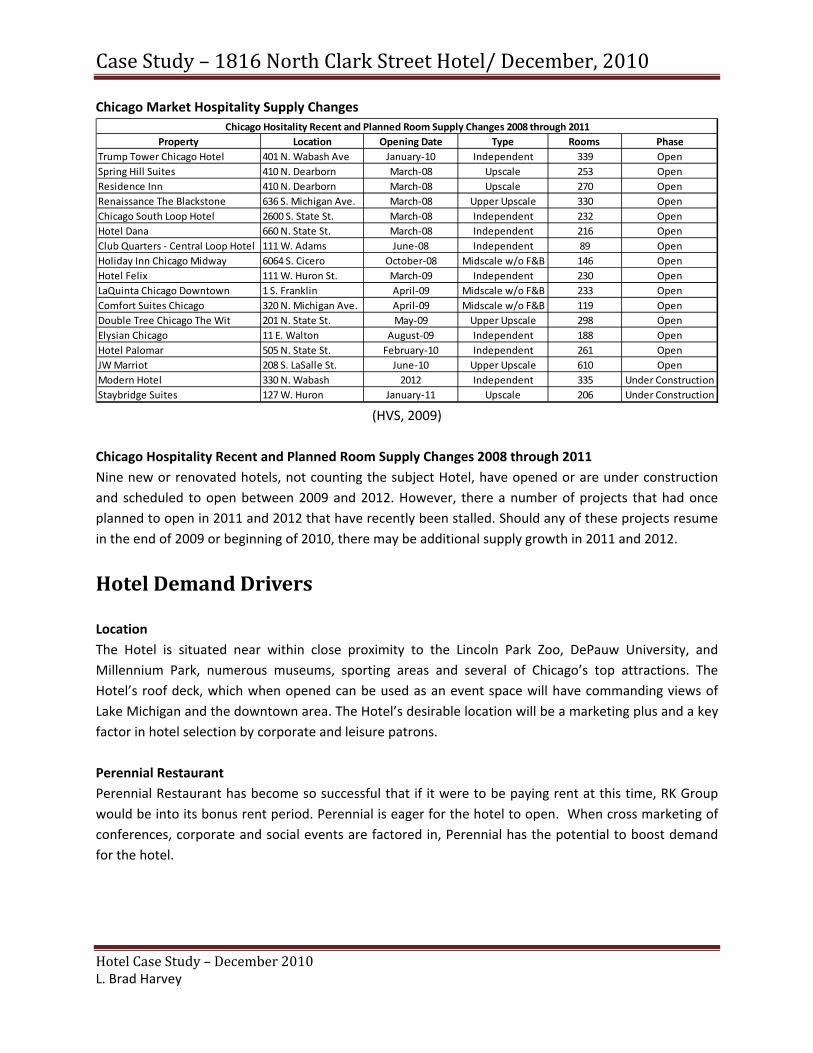

Chicago Market Hospitality Supply Changes

Case Study – 1816 North Clark Street Hotel/ December, 2010

Hotel Case Study – December 2010 L. Brad Harvey

Chicago Market Hospitality Supply Changes

(HVS, 2009)

Chicago Hospitality Recent and Planned Room Supply Changes 2008 through 2011 Nine new or renovated hotels, not counting the subject Hotel, have opened or are under construction and scheduled to open between 2009 and 2012. However, there a number of projects that had once planned to open in 2011 and 2012 that have recently been stalled. Should any of these projects resume in the end of 2009 or beginning of 2010, there may be additional supply growth in 2011 and 2012.

Hotel Demand Drivers Location The Hotel is situated near within close proximity to the Lincoln Park Zoo, DePauw University, and Millennium Park, numerous museums, sporting areas and several of Chicago’s top attractions. The Hotel’s roof deck, which when opened can be used as an event space will have commanding views of Lake Michigan and the downtown area. The Hotel’s desirable location will be a marketing plus and a key factor in hotel selection by corporate and leisure patrons. Perennial Restaurant Perennial Restaurant has become so successful that if it were to be paying rent at this time, RK Group would be into its bonus rent period. Perennial is eager for the hotel to open. When cross marketing of conferences, corporate and social events are factored in, Perennial has the potential to boost demand for the hotel.

Property Location Opening Date Type Rooms PhaseTrump Tower Chicago Hotel 401 N. Wabash Ave January‐10 Independent 339 OpenSpring Hill Suites 410 N. Dearborn March‐08 Upscale 253 OpenResidence Inn 410 N. Dearborn March‐08 Upscale 270 OpenRenaissance The Blackstone 636 S. Michigan Ave. March‐08 Upper Upscale 330 OpenChicago South Loop Hotel 2600 S. State St. March‐08 Independent 232 OpenHotel Dana 660 N. State St. March‐08 Independent 216 OpenClub Quarters ‐ Central Loop Hotel 111 W. Adams June‐08 Independent 89 OpenHoliday Inn Chicago Midway 6064 S. Cicero October‐08 Midscale w/o F&B 146 OpenHotel Felix 111 W. Huron St. March‐09 Independent 230 OpenLaQuinta Chicago Downtown 1 S. Franklin April‐09 Midscale w/o F&B 233 OpenComfort Suites Chicago 320 N. Michigan Ave. April‐09 Midscale w/o F&B 119 OpenDouble Tree Chicago The Wit 201 N. State St. May‐09 Upper Upscale 298 OpenElysian Chicago 11 E. Walton August‐09 Independent 188 OpenHotel Palomar 505 N. State St. February‐10 Independent 261 OpenJW Marriot 208 S. LaSalle St. June‐10 Upper Upscale 610 OpenModern Hotel 330 N. Wabash 2012 Independent 335 Under ConstructionStaybridge Suites 127 W. Huron January‐11 Upscale 206 Under Construction

Chicago Hositality Recent and Planned Room Supply Changes 2008 through 2011

Case Study – 1816 North Clark Street Hotel/ December, 2010

Hotel Case Study – December 2010 L. Brad Harvey

A New Leaf Also located across the street from the Subject at 1820 North Wells Street is A New Leaf, a wedding and event venue run by one of Chicago’s premier florists and event designers. The space is a unique place to hold an event, with an outdoor court yard and an award‐winning multilevel interior of exposed brick, "suspended" concrete staircases and modern metalwork throughout. A New Leaf books up for weddings over 12 months in advance and in the past has referred wedding parties, wedding guests and event attendees to the Hotel as a place to stay. A New Leaf is a demand generator for the Hotel due to its location and expected upper middle hotel range upon completion of the renovation. Fortune Ranked Companies and Business Travel The primary marketing organization for the Chicago hotel industry is the Chicago Convention and Tourism Bureau (CCTB). One of the organization’s primary goals is to attract large out‐of‐town groups, requiring large blocks of hotel rooms, to Chicago. The Chicago hotel industry depends significantly on these “citywide” events and other group‐oriented room nights sold by the CCTB. Even hotels that primarily target transient corporate or leisure travelers benefit from large volumes of demand in the group segment because fewer rooms are available to serve transient guests when certain hotels commit their rooms to large groups. By aligning the hotel with the CCTB and positioning it as a well located downtown mid‐size boutique, the hotel may capture some of the future transient travel. Meeting and convention demand, as well as business travel demand relies heavily on the region’s corporate presence. Fortune Magazine tracks the largest companies in each state and city. In 2007 and 2008, 20 companies located in the City of Chicago finished within the Fortune 1000, an increase from the 19 Fortune 1,000 in 2006. Harley Davidson and Willis Insurance recently moved their headquarters to Chicago, and Miller Brewing Company, in 2008, moved its headquarters to Chicago. To mitigate the negative effect of the economic recession, the CCTB has undertaken a new marketing campaign aimed at local Fortune 500 companies, in an effort to maximize the number of events held in Chicago by local companies. The CCTB is also trying to capitalize on the public criticism of meetings and events held at resort and luxury destinations, promoting Chicago as “the common‐sense choice in uncommon times.” The Hotel’s location near the Central Business District in the downtown submarket in addition to working with the CCTB on bookings can help capture Chicago business travel demand. (HVS, 2009)

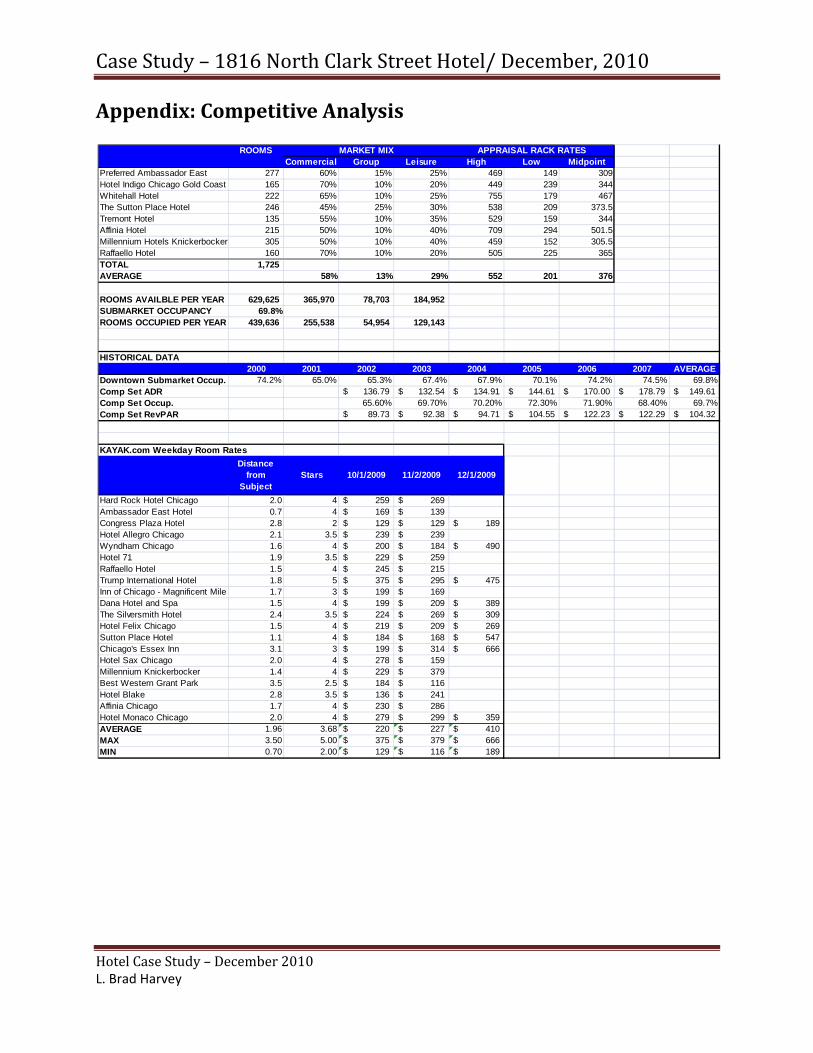

Leasing Plan National hospitality market has been harmed by the decline in business travel, constricted capital/financing markets and weakened operating fundamentals. STR (Smith Travel Resources) projects that at the end of 2009, supply will be up 3.0%, demand will be down 5.5%, occupancy will decline 8.4%, average daily rate will drop 9.7%, and revenue per available room will be down 17.1%. The outlook for 2010 looks slightly better. HVS Hospitality Consultants predict the Chicago hotel industry will continue

Case Study – 1816 North Clark Street Hotel/ December, 2010

Hotel Case Study – December 2010 L. Brad Harvey

to struggle through 2009, with a probable recovery in mid to late 2010. It is HVS’s opinion that this may lead to growth in hotel demand for 2011 and 2012 that exceeds supply growth. Recommended Amenities and Services for the Hotel (Silfen, 2010) Based on surveying the comparative set and the greater Chicago hospitality market, the following additional revenue streams were found at competing hotels. • Pet services for dogs under 25lbs. An amenity that seems to be common in the Chicago boutique hospitality market is offering overnight facilities for the dogs of guests. • Room Service. The Days Inn Lincoln Park North is a popular hotel with leisure travelers in the Lincoln Park neighborhood that does not provide room service for guests. In order to stand out and maintain an upscale service oriented image, Hotel should offer hotel guests the option of ordering from room service. • Roof top lounge with dining. With Perennial Restaurant as a tenant, Hotel has the opportunity to differentiate itself as a destination for both out of town guests and locals. • Outsource spa services to a local provider. The Hotel should formalize an agreement with a local spa that will provide in‐room spa services for guests that request services. • Valet parking. Due to Chicago’s urban setting almost all mid to upper range hotels offer valet parking with little or no self‐parking for guests. • Rooms packages with local event spaces for social functions. Formalize an arrangement with the event space across the street, A New Leaf, for bulk room discounts to wedding and social events. This type of arrangement could smooth out lumpy occupancy rates from business travelers. Chicago MSA The Hotel is located at 1816 North Clark Street in Chicago, Illinois. It is within the geographical and statistical boundaries of Cook County and the Chicago Combined Statistical Area (CSA).The Chicago CSA, combines the metropolitan areas of Chicago, Michigan City (in Indiana), and Kankakee (in Illinois). This area represents the extent of the labor market pool for the entire region. Consisting of nine counties and encompassing 5,065 square miles, the Chicago CSA is located along the southwestern shore of Lake Michigan in northeastern Illinois. (STR, 2009) Population The Chicago CSA is the third largest in the United States, behind New York and Los Angeles, with an estimated population of nearly 9.334 million people. Within a 300‐mile radius of Chicago lies 17% of the US population. The City of Chicago has 2.8 million people, is the largest incorporated area within the Chicago CSA and is the seat of Cook County. According to Woods & Poole, Economics, the Chicago CSA is

Case Study – 1816 North Clark Street Hotel/ December, 2010

Hotel Case Study – December 2010 L. Brad Harvey

expected to continue its gains both in population and employment, growing by 1.795 million persons and gaining 1.583 million jobs by2025. As of the 2000 census, there are 1.1 million households and 632,558 families residing within the City of Chicago. More than half the population of the state of Illinois lives in the Chicago metropolitan area. The population density of the city was 12,750 people per square mile, making it one of the nation's most densely populated cities. There were 1.2 million housing units at an average density of 5,075 per square mile. The median income for a household in the city was $38,625, and the median income for a family was $42,724. About 16.6% of families and 19.6% of the population lived below the poverty line. (HVS, 2009) Transportation Hub Chicago is a major transportation hub in the United States. Chicago is located at the junction office major interstate highways in addition to an extensive interstate system linked by both federal and state highways. The City is also well known for its extensive mass transportation system which includes suburban commuter trains, city and regional bus routes, subway and elevated train lines in the city. It is an important component in global distribution, as it is the third largest inter‐modal port in the world after Hong Kong and Singapore. Additionally, it is the only city in North America in which six Class I railroads meet. The Chicago Region Environmental and Transportation Efficiency (CREATE) initiative is using about $1.5 billion in private railroad, state, local, and federal funding to improve rail infrastructure in the region to reduce freight rail congestion by about one third. This is also expected to have a positive impact on passenger rail and road congestion, as well as create new green space. (HVS, 2009) Chicago Airports Chicago benefits from one of the world’s busiest airports; O’Hare International Airport served approximately 70.8 million passengers in 2008. The O’Hare Modernization Program (“OMP”) will spend $6.6 billion to reconfigure O’Hare’s runways to significantly increase capacity and reduce delays in all weather conditions at O’Hare International Airport. Federal approvals and funding are already in place for the program. Construction began in 2007 and three phases of development are planned through 2011. In 2005, O'Hare was the world's busiest airport by aircraft movements and the second busiest by total passenger traffic. Midway International Airport, on Chicago’s southwest side, served an additional 17.3 million passengers in 2008. Both O'Hare and Midway are owned and operated by the City of Chicago. Chicago is the world headquarters for United Airlines, the world's second‐largest airline by revenue‐passenger kilometers and the city is the second largest hub for American Airlines. Midway airport serves as a major 'focus city' for Southwest Airlines, the world's largest low‐cost airline. Rail Service Chicago is the largest hub of passenger rail service in the nation. Many Amtrak long distance services originate from Union Station. Such services terminate in New York, Seattle, Portland, New Orleans, San Francisco, Los Angeles, San Antonio, and Washington, D.C. Amtrak also provides a number of short‐haul

Case Study – 1816 North Clark Street Hotel/ December, 2010

Hotel Case Study – December 2010 L. Brad Harvey

services throughout Illinois and toward nearby Milwaukee, Indianapolis, Saint Louis, and Detroit. Nine interstate highways run through Chicago and its suburbs. Regional Transit The Regional Transportation Authority (RTA) coordinates the operation of the three service boards: CTA, Metra, and Pace. The Chicago Transit Authority (CTA) handles public transportation in the city of Chicago and a few adjacent suburbs. The CTA operates an extensive network of buses and a rapid transit elevated and subway system known as the 'L' (for "elevated"), with lines designated by colors. These rapid transit lines also serve both Midway Airport and O'Hare Airport. The CTA's rail lines consist of the Red, Blue, Green, Orange, Brown, Purple, Pink, and Yellow lines. A new subway/elevated line, the Circle Line, is also in the planning stages by the CTA. Local Economy Chicago has the third largest gross metropolitan product in the nation, approximately $506 billion according to 2007 estimates. Chicago and its surrounding metropolitan area are home to the second largest labor pool in the United States with approximately 4.25 million workers. The city has also been rated as having one of the most balanced economies in the United States, due to its high level of diversification. Business The Great Chicago area is home to 48 Fortune 1,000 companies. Chicago was named the fourth most important business center in the world in the MasterCard Worldwide Centers of Commerce Index. Additionally, the Chicago metropolitan area recorded the greatest number of new or expanded corporate facilities in the United States for six of the past seven years. In 2008, Chicago placed 16th on the UBS list of the world's richest cities. Financial Center Chicago is a major world financial center, with the second largest central business district in the U.S. The city is the headquarters of the Federal Reserve Bank of Chicago. The city is also home to three major financial and futures exchanges, including the Chicago Stock Exchange, the Chicago Board Options Exchange, and the Chicago Mercantile Exchange, which includes the former Chicago Board of Trade. Further the Chicago Mercantile Exchange is known for its virtual monopoly on Treasury Futures making it a financial hub for the short‐ and mid‐term. Also, as Dodd‐Frank has mandated a greater use of clearing houses, Chicago will become ever more important as a financial center due to the Chicago Mercantile Group. McCormick Place McCormick Place is the largest convention center in the United States, offering 2.7 million square feet of exhibition space. The convention center consists of four major buildings: the North and South Buildings, the Lakeside Center, and the newly opened McCormick West Building. Originally built in 1960, McCormick Place has been an important factor in making Chicago one of the world’s premier

Case Study – 1816 North Clark Street Hotel/ December, 2010

Hotel Case Study – December 2010 L. Brad Harvey

destinations for major conventions and tradeshows. The West Building opened in July, 2007. This most recent expansion of the convention center offers an additional 460,000 square feet of exhibition space, a 100,000‐square‐foot ballroom, and 250,000 square feet of additional meeting space in 61 rooms. The new facility targets midsized conventions and tradeshows, which allows Chicago to host multiple conventions simultaneously during periods of peak demand. Since the expansion of McCormick Place in 2007, the number of events hosted at the convention center increased significantly. The new West Building allows McCormick Place to host smaller conventions and meetings that historically have not been booked in Chicago, as well as simultaneous conventions and tradeshows. In 2008, McCormick Place hosted 108 events, drawing slightly greater total attendance than in 2007. McCormick Place continues to be a key indicator for the Chicago hotel industry. According to Chicago Crain’s Business, overall attendance at events is down this year. Given an economic recovery within a few years, McCormick Place will continue to represent one of the biggest single demand generators for hotels in the city.

Recreation City residents enjoy dozens of cultural institutions, historical sites and museums. There are more than 200 theaters, nearly 200 art galleries, and More than 7,300 restaurants in Chicago. Making use of its abundant resources, Chicago has a heritage for hosting major international, national, regional, and local events that include commerce, culture, entertainment, politics, and sports. Magnificent Mile The Magnificent Mile is located along North Michigan Avenue from the Chicago River to Lake Shore Drive. The area has a high concentration of the city's major media firms and advertising agencies, including the Chicago Tribune newspaper. The Magnificent Mile is a unique urban area and a well‐known theater capital that features 450 prestigious shops, fine dining, and numerous museums and galleries. Lincoln Park Area The Lincoln Park area has a lot to offer hotel guests. The neighborhood and hotel are within walking distance of the Lincoln Park Zoo, The Notebaert Nature Museum, Lake Michigan & Chicago Beaches, Wrigley Field, Diversey Driving Range, Halsted Street, and world renowned hospitals such as the Children's Memorial Hospital. There is a wide offering of retail including Aveda, Bally's Total Fitness,

Magnificent Mile

Case Study – 1816 North Clark Street Hotel/ December, 2010

Hotel Case Study – December 2010 L. Brad Harvey

Borders, Bath & Body Works, Best Buy, Borders, Chipotle, Cost Plus World Market, Express, Jamba Juice, Landmark Theatres, Nine West, Panera, Petsmart, Starbucks, T.J. Maxx, The Body Shoppe, The Counter Burger, Victoria's Secret, and The Vitamin Shoppe. Nearby is the Chicago Loop, Millennium Park, The Field Museum, The Art Institute, Museum of Contemporary Art and other famous cultural institutions, McCormick Place, Navy Pier, the Merchandise Mart and more. (HVS, 2009)

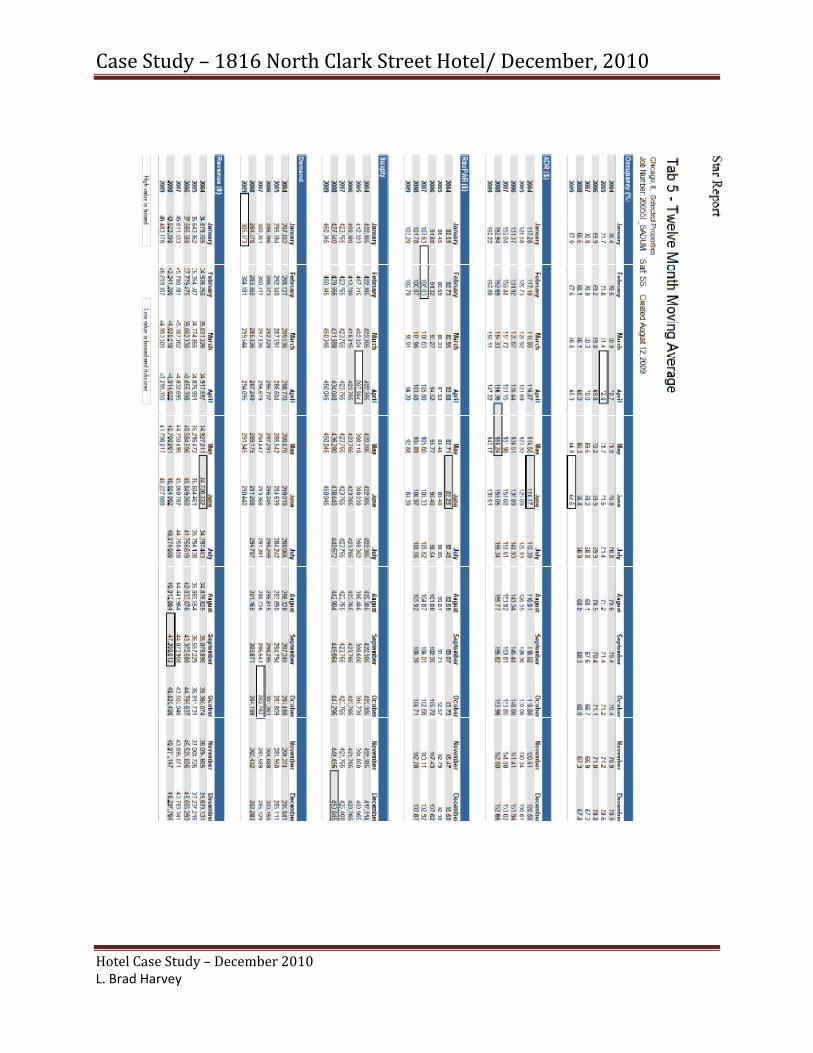

Financial Analysis Revenues In order to properly evaluate and forecast Hotel revenues, a Historical Trend Report was ordered from STR Global, obtaining precise revenue and occupancy data. Given the significant period of inactivity for the Hotel, it was decided that historical operating data was irrelevant, and that completion of the renovation would most likely change the hotel’s booking class. The Historical Trend Reports draws upon data from the past six years, tracking occupancy, average daily rate, revenue per available room, supply, demand and revenue. These detailed reports include raw absolute values, year over year percentage changes and rolling 12 month analyses. Please view the full report in the Appendix section of this report.

(STR, 2009)

Expenses “Undistributed Expenses” accounts for marketing, property operations and management, utilities, administration and general overhead. The expense per room which became the midpoint of the competitive cost set was selected. “Fixed Expenses” reflect Property Taxes and Insurance. A third party insurance consultant projected estimated coverage costs. Property taxes were a bit more complicated. Current property tax bills reflect an annualized tax bill of $60,000 per annum. Based on the Chicago property tax assessment and rates annual property taxes are estimated in the range of $215,000 per annum. Lastly, “Expenses” reflect variable operating expenses and margins reflect the midpoint of the competitive set. (HVS, 2009) In the appendix is an example run of the case study using the model and assumptions taken from the STR report.

Year Occupancy ADR RevPAR Supply Demand Revenue2003 71.1% $117.84 $83.73 422,305 300,051 35,358,860$ 2004 70.9% $120.56 $85.50 417,314 295,941 35,679,131$ 2005 70.6% $130.61 $92.18 403,965 285,111 37,237,216$ 2006 70.8% $151.94 $107.62 423,765 300,155 45,606,293$ 2007 67.3% $153.02 $102.92 425,408 286,129 43,783,141$ 2008 67.4% $152.66 $102.87 450,045 303,283 46,297,764$

Case Study – 1816 North Clark Street Hotel/ December, 2010

Hotel Case Study – December 2010 L. Brad Harvey

Sources While the current economy has reduced the number of capital sources, there are still a number of participants in the hospitality arena. A potential investor’s required rate of return and the amount of control they would like to have in the project will play a major role in the direction the Lender will take with the hotel. Hotel Operator Developer (JV, potential buyer) Since the news about SEC appointed receiver has hit the papers many hoteliers have been calling the Lender expressing interest in the hotel. Based on the questions they are asking they have no idea of the status of the building. While many operators may have access to the capital to purchase the property most have expressed interest in a joint venture should Lender decide to take the property back. Their basic structure requires the Lender to hold a fixed rate mortgage and receive a preferred rate of return on the net income plus a % of the sale proceeds. The Lender will need to consider if this option provides the greatest possibility for return. Another concern will be gaining comfort in the ability of the operator to fund the remaining development. This is best mitigated by requiring the monies needed to complete construction to be put in escrow in an account controlled by the Lender. Private Equity, Hospitality REIT (buyer) In addition to hotel operators, many private equity and hospitality REITs have expressed interest in an outright purchase of the note. This option will provide the Lender with immediate funds, but possibly bring the lowest return possible. On the positive side it will remove the Lender from any future liability of the property and provide funds that can be put to work on another project. Traditional lender: commercial, life insurance Company (debt provider to Lender) A traditional lender is an option should the Lender decide to complete the hotel and hire a hotel manager to operate once the renovation is complete. A traditional lender is an option for permanent financing once the hotel is opened and has established an operating history. Traditional lenders such as a commercial bank or life insurance company at this time are very cautious about hospitality. Construction financing for hotels does not currently exist and even purchase money or refinance mortgages on operating properties is not easy. Expect no more than 50% loan to value and a very conservative debt service coverage ratio.

Case Study – 1816 North Clark Street Hotel/ December, 2010

Hotel Case Study – December 2010 L. Brad Harvey

Uses The funds required to complete the project will be first applied to the $3.3 million in mechanic liens on the property. While many could be fought it will be in the best interest of the project to negotiate with the contractors whose services will be needed to complete the construction. At this time very little of the work is warranted by the contractors since they have not completed their contract. Below is a projected budget and completion timeline. The property condition report in the appendix will provide more detail on the specific work required. In addition you will find an analysis of discretionary items that may need attention depending on the hotel market niche selected.

When looking at the option to hold and complete the project assumptions must be made for cost associated with the hotel opening and marketing. Should it be decided that the hotel needs to be rebranded this to will need to be analyzed and included in the underwriting.

Completion Timeline (Days)Control of Property 30Length of Completion 90Days to Stabilize 365Days Remaining in 2009 -343

BudgetLien Payment 3,200,000$ Perennial Restaurant 250,000$ Property Tax 60,000$ Electric 100,000$ Furniture 140,000$ Setup & Storage 230,000$ Accountant 15,000$ Lawyer Fees 100,000$ Portfolio Group 25,000$ Gettys 25,000$ Consultant Fees, Expens 75,000$ Structure 475,102$ Construction Costs 1,250,000$ Sign Income (30,000)$ Receiver 30,000$ Total Budget 5,945,000$

COMPLETION DETAILS

Case S

Hotel CasL. Brad Ha

CapitaThe threelargest aseven giveIncome w A discussimarket foperformafrom a hi2008. For the pNational Cthe worsthistory fonew year‐

The raw delevated, continuesmid‐2003

tudy – 18

se Study – Dearvey

al Markee main assetssset class wasen the huge dwill eclipse Rea

ion of commeor residentiance by 16 moistoric perspe

period endingCase‐Shiller It year‐over‐yeor the Case‐Sh‐over‐year pr

data with Futthe values ps to indicate t.

816 Nort

ecember 201

ets s in the U.S. s real estate destruction inal Estate as th

ercial real estal is 400% gonths. This isective, indica

g September ndex, Compoear price chahiller index. Oice change lo

(Staiger

ures values hprovide a beathe market w

th Clark S

10

economy arbut currentlyn asset valueshe largest ass

tate cannot breater than important asates a signific

2008, the yosite‐20, weranges, for theOther than laows.

r, Commercia

has experiencarish forecastill not bottom

Street Ho

re Fixed Incoy, at the end s for real estaset class in 20

begin withoutcommercial s the peak of cant fall in c

ear‐over‐yeae 17.15% ande eleventh (1ast month, th

al and Residen

ced minimal tt for pricing tm prior to 1st

otel/ Dec

me, Real Estof 2008, Fixate. Current 009.

t an overviewand is a leathe residentiommercial p

r residential d 17.43%, re11th) straight e DC MSA ha

ntial Data, 20

trading for 20trends in the quarter 2011

cember, 2

ate and Equied Income anpredictions a

w of residentiaading indicatial market warices beginni

price changespectively. Pmonth, nati

as, for close t

010)

009 productsDC‐MSA. Th1, returning t

2010

ities. In 200nd Real Estatare that that

al real estatetor of commas July 2006 wing fourth qu

es for DC anPlease note, tonally in recoo a year, ach

. While remahe Futures mo pricing simi

06 the te are Fixed

. The mercial which, uarter

d the this is orded hieved

aining market ilar to

Case S

Hotel CasL. Brad Ha

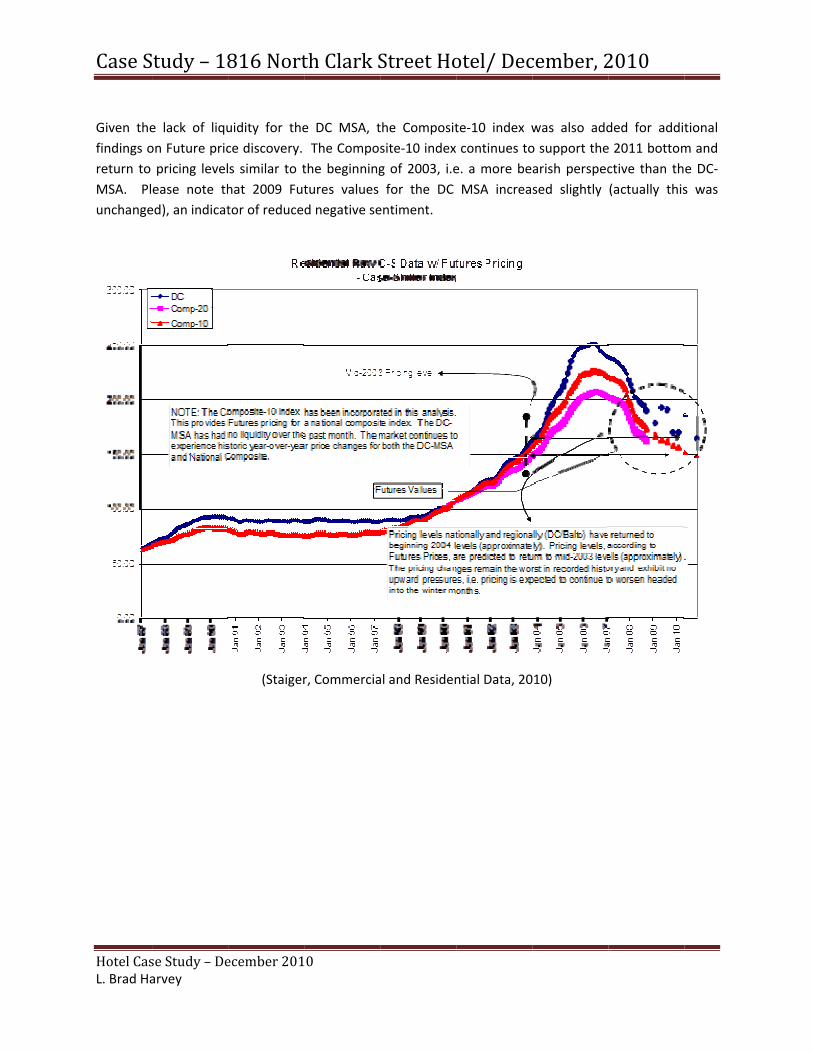

Given thefindings oreturn to MSA. Plunchange

tudy – 18

se Study – Dearvey

e lack of liquon Future pricpricing levelease note thed), an indicat

816 Nort

ecember 201

uidity for thece discovery. s similar to that 2009 Futtor of reduce

(Staiger

th Clark S

10

e DC MSA, t The Composthe beginningtures values d negative se

r, Commercia

Street Ho

the Compositsite‐10 index g of 2003, i.efor the DC

entiment.

al and Residen

otel/ Dec

te‐10 index wcontinues to

e. a more beMSA increa

ntial Data, 20

cember, 2

was also addo support thearish perspecsed slightly

010)

2010

ded for addite 2011 bottomctive than th(actually this

tional m and e DC‐s was

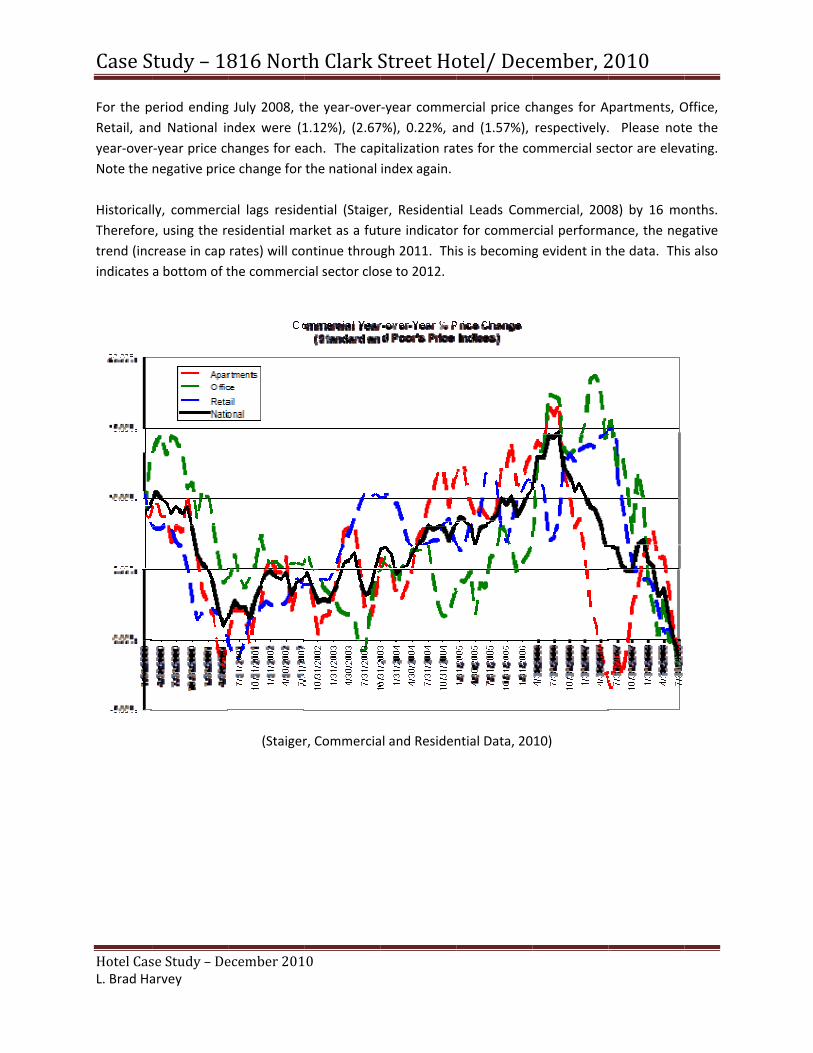

Case S

Hotel CasL. Brad Ha

For the pRetail, anyear‐overNote the HistoricalThereforetrend (incindicates

tudy – 18

se Study – Dearvey

eriod endingnd National inr‐year price cnegative pric

ly, commercie, using the recrease in cap a bottom of t

816 Nort

ecember 201

g July 2008, tndex were (1hanges for eae change for

ial lags residesidential marates) will cothe commerc

(Staiger

th Clark S

10

he year‐over1.12%), (2.67ach. The capthe national

ential (Staigearket as a futontinue throucial sector clos

r, Commercia

Street Ho

r‐year comme7%), 0.22%, apitalization ratindex again.

er, Residentiature indicatorgh 2011. Thise to 2012.

al and Residen

otel/ Dec

ercial price chand (1.57%), tes for the co

al Leads Comr for commeris is becoming

ntial Data, 20

cember, 2

hanges for Arespectively.ommercial se

mmercial, 200rcial performag evident in t

010)

2010

Apartments, O. Please notctor are elev

08) by 16 moance, the negthe data. Thi

Office, te the ating.

onths. gative s also

Case S

Hotel CasL. Brad Ha

The Staignational commerc(Staiger, R The Grapindex witforecasts these pre

tudy – 18

se Study – Dearvey

ger predictivecommercial ial market mResidential Le

hic below deth the predicrelated to indictive mode

816 Nort

ecember 201

e equation wpricing is de

mid‐2012 witheads Commer

emonstrates cted future ndividual comels being deve

(Staiger

th Clark S

10

which quantifepicted belowh capitalizatircial, 2008)

Composite‐2prices for co

mmercial asseeloped by SBA

r, Commercia

Street Ho

fies the 16 mw. The Staion rates risin

20 residentialommercial inet classes as wA, LLC).

al and Residen

otel/ Dec

month lead iiger Equationng rapidly ov

l overlaying tn red. Futurwell as regio

ntial Data, 20

cember, 2

in residentian predicts thver the next

the National re analyses ions (several m

010)

2010

l composite‐he bottom o12 – 18 mo

commercial intend to prmonths away

20 to of the onths.

price rovide from

Case S

Hotel CasL. Brad Ha

CommerMidwestexperien

tudy – 18

se Study – Dearvey

cial Year‐ov, and retail cing an elev

816 Nort

ecember 201

ver‐Year pricstrengthen

vation in cap

(Staiger

th Clark S

10

ce Change aned this moitalization ra

r, Commercia

Street Ho

as of Augusnth, albeit ates due to t

al and Residen

otel/ Dec

st 2008. Oslightly. Apthe shadow

ntial Data, 20

cember, 2

nly the Midpartments, acondominiu

010)

2010

d Atlantic Soas expectedum market.

outh, d, are

Case S

Hotel CasL. Brad Ha

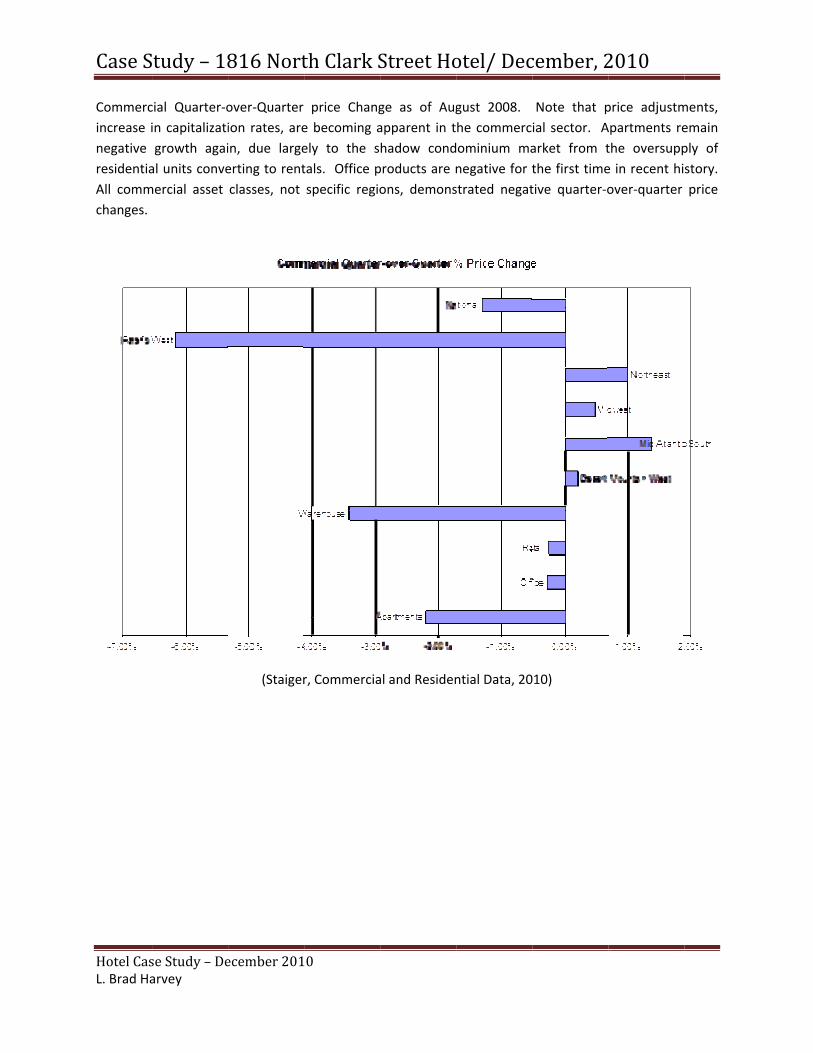

Commercincrease inegative residentiaAll commchanges.

tudy – 18

se Study – Dearvey

cial Quarter‐oin capitalizatigrowth agaial units convemercial asset

816 Nort

ecember 201

over‐Quarter ion rates, arein, due largeerting to rentclasses, not

(Staiger

th Clark S

10

price Change becoming aely to the stals. Office pspecific regio

r, Commercia

Street Ho

ge as of Augapparent in thadow condproducts are nons, demons

al and Residen

otel/ Dec

gust 2008. he commercominium manegative for tstrated negat

ntial Data, 20

cember, 2

Note that pial sector. Aarket from tthe first timetive quarter‐o

010)

2010

price adjustmApartments rethe oversuppe in recent hiover‐quarter

ments, emain ply of story. price

Case Study – 1816 North Clark Street Hotel/ December, 2010

Hotel Case Study – December 2010 L. Brad Harvey

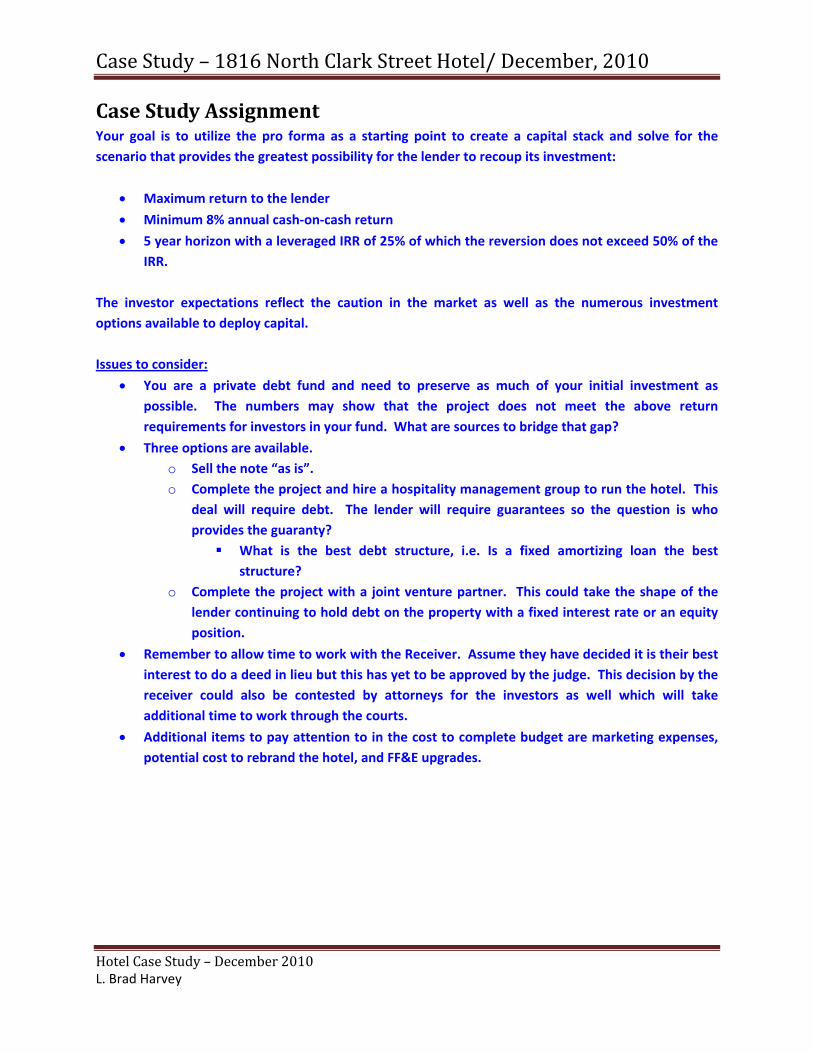

Case Study Assignment Your goal is to utilize the pro forma as a starting point to create a capital stack and solve for the scenario that provides the greatest possibility for the lender to recoup its investment:

• Maximum return to the lender

• Minimum 8% annual cash‐on‐cash return

• 5 year horizon with a leveraged IRR of 25% of which the reversion does not exceed 50% of the IRR.

The investor expectations reflect the caution in the market as well as the numerous investment options available to deploy capital. Issues to consider:

• You are a private debt fund and need to preserve as much of your initial investment as possible. The numbers may show that the project does not meet the above return requirements for investors in your fund. What are sources to bridge that gap?

• Three options are available. o Sell the note “as is”. o Complete the project and hire a hospitality management group to run the hotel. This

deal will require debt. The lender will require guarantees so the question is who provides the guaranty?

What is the best debt structure, i.e. Is a fixed amortizing loan the best structure?

o Complete the project with a joint venture partner. This could take the shape of the lender continuing to hold debt on the property with a fixed interest rate or an equity position.

• Remember to allow time to work with the Receiver. Assume they have decided it is their best interest to do a deed in lieu but this has yet to be approved by the judge. This decision by the receiver could also be contested by attorneys for the investors as well which will take additional time to work through the courts.

• Additional items to pay attention to in the cost to complete budget are marketing expenses, potential cost to rebrand the hotel, and FF&E upgrades.

Case Study – 1816 North Clark Street Hotel/ December, 2010

Hotel Case Study – December 2010 L. Brad Harvey

Appendix: Loan Summary I. LOAN PROFILE • Loan: The Loan is secured by a Payment Guaranty Agreement and a Completion Guaranty

Agreement, each dated December 22, 2005, from WexTrust Equity Partners, LLC, formerly known as Wexford Equity Partners, LLC, an Illinois limited liability company , in favor of Lender. Twenty‐Seven Million Six Hundred Thousand and 00/100 Dollars ($27,600,000.00).

• Interest Rate: Proceeds of the Loan bear interest at an amount equal to Prime Rate floating

plus one percent (1%), per annum, adjusted on a daily basis; provided, however, that at no time during the term of the Loan shall the Interest Rate be less than seven and three‐quarter percent (7 3/4 %) per annum; provided, further, in no event shall the Interest Rate exceed two percent (2%) over the stated Interest Rate at the Closing Date.

• Default Rate: In the event of any default, the Interest Rate shall be equal to five percent (5%)

in excess of the then‐applicable Interest Rate, but shall not at any time exceed the highest rate permitted by law.

• Maturity Date: The term of the Loan, subject to the Borrower’s right to extend, is 36 months.

The original Maturity Date is December 22, 2008. • Loan Extension: The Borrower was eligible to extend the loan term for up to two (2), three (3)

month period if the Loan was performing and in balance as defined by the construction loan documents.

• Equity: Borrower contributed Six Million and 00/100 Dollars ($6,000,000.00) of equity towards

the Project prior to Closing. • Out of Balance: The construction loan documents provide that if the Lender determines, in its

sole discretion, that the Loan is “out of balance” and that there are insufficient funds in the budget to complete the Project, the Borrower has ten (10) days to deposit sufficient funds with the lender or take other corrective action approved by Lender to bring the Loan “in balance”.

• Union Labor Requirement: Each Contractor, and any subcontractor (to any degree) of a

Contractor performing work on the project (A) shall be bound by and be a signatory to a collective bargaining agreement with a labor organization which is affiliated with the Building and Construction Trades Department of the AFL‐CIO. So long as the Loan is in effect, service workers employed in the Mortgaged Property will be covered by a collective bargaining

Case Study – 1816 North Clark Street Hotel/ December, 2010

Hotel Case Study – December 2010 L. Brad Harvey

agreement with an AFL‐CIO affiliated union whose jurisdiction covers the type of work being performed. The failure to comply with the provisions of this subparagraph shall constitute an immediate Event of Default. Borrower is bound by, and is a signatory to a neutrality agreement with the local UNITE‐HERE union.

• Default: A notice of Default was delivered by Lender to Borrower. The construction loan

documents provide for a number of remedies upon default, including, without limitation, the right to (i) declare the entire balance of the Loan immediately due; (ii) institute a proceeding for foreclosure; (iii) cause the Project to be sold; (iv) file for specific performance; (v) apply for the appointment of a receiver; (vi) collect all rents due to Borrower; and (vii) take all other actions permitted under the UCC.

Case Study – 1816 North Clark Street Hotel/ December, 2010

Hotel Case Study – December 2010 L. Brad Harvey

Appendix: Property Condition Report Necessary Items ‐ $432,000

A. Site Scope ‐ $50,000 B. Superstructure and Substructure Scope ‐ $5,000 C. Exterior Scope (walls, windows, roof) ‐ $125,000 D. Interior Scope ‐ $190,000 E. M/E/P Life Safety Scope ‐ $62,000

Discretionary Items

A. Window Replacement ‐ $210,000 – Update existing windows with new aluminum windows B. Roof Replacement ‐ $120,000 – Install a new system with insulation, and

reinstall/reconstruction the plastic wood decks C. Carpet Replacement ‐ $600,000 – Remove existing carpet and underlayment in corridors and

guestrooms from the third floor through the penthouse. D. Vinyl Wall Covering ‐ $1,200,000 – Remove and replace existing wall coverings from corridors

and guestrooms from the third floor through the penthouse. E. Popcorn Ceiling Replacement ‐ $1,220,000 – Remove existing popcorn ceilings and replace with

a smooth ceiling in guestrooms from the third floor through the penthouse. F. Corridor Ceiling Replacement ‐ $170,000 – Remove existing ceiling and replace with new lay‐in

acoustical tile ceiling from the third floor through the penthouse G. PTAC Unit Replacement ‐ $640,000 – Remove and replace units in guestrooms from the third

floor through the penthouse.

Case Study – 1816 North Clark Street Hotel/ December, 2010

Hotel Case Study – December 2010 L. Brad Harvey

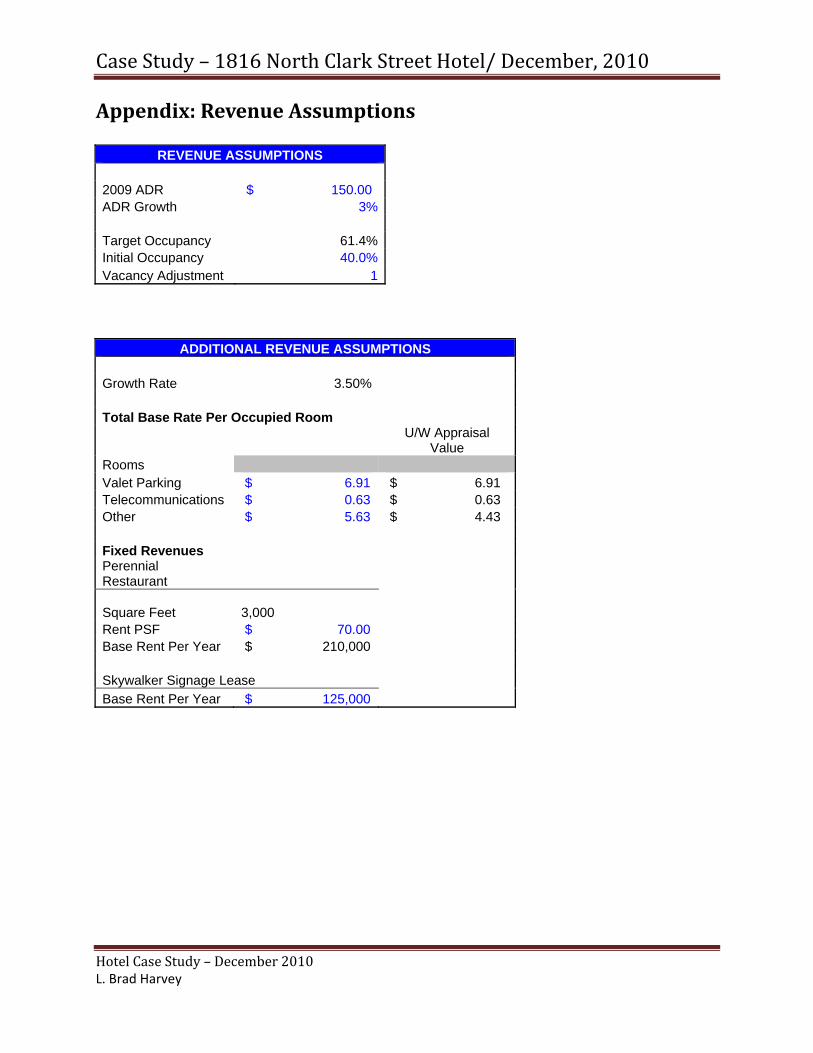

Appendix: Revenue Assumptions

REVENUE ASSUMPTIONS 2009 ADR $ 150.00 ADR Growth 3% Target Occupancy 61.4%Initial Occupancy 40.0%Vacancy Adjustment 1

ADDITIONAL REVENUE ASSUMPTIONS Growth Rate 3.50% Total Base Rate Per Occupied Room

U/W Appraisal

Value Rooms Valet Parking $ 6.91 $ 6.91 Telecommunications $ 0.63 $ 0.63 Other $ 5.63 $ 4.43 Fixed Revenues Perennial Restaurant

Square Feet

3,000 Rent PSF $ 70.00 Base Rent Per Year $ 210,000 Skywalker Signage Lease Base Rent Per Year $ 125,000

Case Study – 1816 North Clark Street Hotel/ December, 2010

Hotel Case Study – December 2010 L. Brad Harvey

Appendix: Expense Assumptions

UNDISTRIBUTED EXPENSES Growth Rate 3.50% Total Base Rate Per Available Room Marketing $ 4,000 Property O & M $ 2,500 Utilities $ 2,600 A & G $ 5,000 Percent of Revenue Management Fee 5%Franchise Fees

EXPENSES Growth Rate 3.50% Total Base Pct Per Year Rooms 28.0%Valet Parking 90.0%Telecommunications 141.0%Other 85.0% Total Base Rate Per Year Rooms $ 1,400,000 Valet Parking $ 190,000 Telecommunications $ 30,000 Other $ 150,000

FIXED EXPENSES Growth Rate 3.50% Total Base Rate Per Year Property Taxes $ 215,000 Insurance $ 140,000 Percent of Revenue Replacement Reserve 3%

Case Study – 1816 North Clark Street Hotel/ December, 2010

Hotel Case Study – December 2010 L. Brad Harvey

Appendix: Net Operating Income Proforma

0 1 2 3 4 5 6 7 8 9 102009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Days Per Year 1 (98) 365 366 365 365 365 366 365 365 365 Rooms 194 194 194 194 194 194 194 194 194 194 194 Available Rooms 194 (19,012) 70,810 71,004 70,810 70,810 70,810 71,004 70,810 70,810 70,810 Days in Stabilization 1 (98) 365 97 - - - - - - - Remaining Days to Stabilize 364 462 97 - - - - - - - - Stabilized Year FALSE FALSE FALSE FALSE TRUE FALSE FALSE FALSE FALSE FALSE FALSE

Occupancy 40% 45% 51% 56% 61% 62% 63% 63% 64% 65% 65%

Occupied Rooms 78 (8,621) 35,890 39,782 43,457 43,892 44,330 44,896 45,222 45,674 46,130 ADR 150.00 154.50 159.14 163.91 168.83 173.89 179.11 184.48 190.02 195.72 201.59 RevPAR 60.00 70.05 80.66 91.84 103.61 107.79 112.13 116.65 121.35 126.24 131.33

RevenueRooms 11,640 (1,331,879) 5,711,435 6,520,703 7,336,685 7,632,354 7,939,937 8,282,547 8,592,791 8,939,081 9,299,326 Valet Parking 536 (12,158) 232,634 252,392 269,973 274,918 279,992 286,488 290,539 296,021 301,648 Restaurant Lease 575 210,000 210,000 210,000 210,000 210,000 210,000 210,000 210,000 210,000 210,000 Signage Lease 342 125,000 125,000 125,000 125,000 125,000 125,000 125,000 125,000 125,000 125,000 Telecommunications 49 (5,432) 22,614 25,066 27,381 27,655 27,931 28,288 28,493 28,778 29,066 Other Income 437 90,293 181,756 193,312 204,575 209,594 214,768 220,342 225,598 231,267 237,111 Total Revenue 13,580 (924,176) 6,483,439 7,326,472 8,173,614 8,479,521 8,797,628 9,152,665 9,472,422 9,830,147 10,202,151

Departmental ExpensesRooms (3,663) 384,210 (1,529,561) (1,637,259) (1,740,854) (1,805,050) (1,871,625) (1,945,984) (2,012,267) (2,086,522) (2,163,530) Valet Parking (509) 40,242 (205,284) (216,009) (225,513) (232,190) (239,089) (247,029) (253,581) (261,191) (269,055) Telecommunications (78) 8,133 (32,061) (33,950) (35,680) (36,639) (37,629) (38,757) (39,705) (40,794) (41,917) Other Income (399) 6,154 (158,827) (166,029) (172,656) (178,154) (183,838) (190,143) (195,793) (202,077) (208,576) Total Departmental Expenses (4,649) 438,740 (1,925,733) (2,053,247) (2,174,704) (2,252,033) (2,332,181) (2,421,912) (2,501,346) (2,590,584) (2,683,078)

Departmental Profit 8,931 (485,436) 4,557,706 5,273,225 5,998,910 6,227,487 6,465,447 6,730,754 6,971,075 7,239,562 7,519,073

Undistributed ExpensesMarketing (2,126) (795,012) (814,689) (835,056) (856,134) (877,951) (900,531) (923,902) (948,091) (973,126) (999,037) Property Operations & Maintenance (1,329) (496,883) (509,181) (521,910) (535,084) (548,720) (562,832) (577,439) (592,557) (608,204) (624,398) Utilities (1,382) (516,758) (529,548) (542,786) (556,487) (570,668) (585,345) (600,536) (616,259) (632,532) (649,374) A & G (2,658) (993,765) (1,018,362) (1,043,819) (1,070,168) (1,097,439) (1,125,664) (1,154,878) (1,185,113) (1,216,407) (1,248,797) Management Fee (679) 46,209 (324,172) (366,324) (408,681) (423,976) (439,881) (457,633) (473,621) (491,507) (510,108) Total Undistributed Expenses (8,173) (2,756,209) (3,195,952) (3,309,894) (3,426,555) (3,518,754) (3,614,255) (3,714,388) (3,815,641) (3,921,776) (4,031,714)

Gross Operating Profit 757$ (3,241,645)$ 1,361,754$ 1,963,331$ 2,572,355$ 2,708,733$ 2,851,193$ 3,016,366$ 3,155,434$ 3,317,786$ 3,487,359$

Fixed ExpensesProperty Taxes (589) 59,746 (230,313) (239,027) (246,717) (255,353) (264,290) (274,289) (283,114) (293,023) (303,279) Insurance (384) 38,905 (149,972) (155,646) (160,653) (166,276) (172,096) (178,607) (184,353) (190,806) (197,484) Replacement Reserve (407) 27,725 (194,503) (219,794) (245,208) (254,386) (263,929) (274,580) (284,173) (294,904) (306,065) Total Fixed Expenses (1,380) 126,376 (574,788) (614,467) (652,579) (676,014) (700,314) (727,477) (751,640) (778,733) (806,827)

Net Operating Income (623) (3,115,268) 786,966 1,348,863 1,919,776 2,032,719 2,150,878 2,288,889 2,403,795 2,539,053 2,680,532

Case Study – 1816 North Clark Street Hotel/ December, 2010

Hotel Case Study – December 2010 L. Brad Harvey

Appendix: Proforma Percentage Allocations

0 1 2 3 4 5 6 7 8 9 102009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Occupancy 40% 45% 51% 56% 61% 62% 63% 63% 64% 65% 65%

RevenueRooms 85.7% 144.1% 88.1% 89.0% 89.8% 90.0% 90.3% 90.5% 90.7% 90.9% 91.2%Valet Parking 3.9% 1.3% 3.6% 3.4% 3.3% 3.2% 3.2% 3.1% 3.1% 3.0% 3.0%Restaurant Lease 4.2% -22.7% 3.2% 2.9% 2.6% 2.5% 2.4% 2.3% 2.2% 2.1% 2.1%Signage Lease 2.5% -13.5% 1.9% 1.7% 1.5% 1.5% 1.4% 1.4% 1.3% 1.3% 1.2%Telecommunications 0.4% 0.6% 0.3% 0.3% 0.3% 0.3% 0.3% 0.3% 0.3% 0.3% 0.3%Other Income 3.2% -9.8% 2.8% 2.6% 2.5% 2.5% 2.4% 2.4% 2.4% 2.4% 2.3%Total Revenue 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0%

Departmental Expenses (Percent of Item Revenue)Rooms 31.5% 28.8% 26.8% 25.1% 23.7% 23.6% 23.6% 23.5% 23.4% 23.3% 23.3%Valet Parking 93.5% 262.1% 88.7% 86.8% 85.4% 86.0% 86.7% 87.3% 88.1% 88.7% 89.4%Telecommunications 157.3% 148.5% 141.7% 136.2% 131.8% 133.7% 135.6% 137.6% 139.6% 141.6% 143.8%Other Income 91.3% -6.8% 87.4% 85.9% 84.4% 85.0% 85.6% 86.3% 86.8% 87.4% 88.0%Total Departmental Expenses 34.2% 46.6% 29.7% 28.1% 26.7% 26.6% 26.6% 26.5% 26.4% 26.4% 26.3%

Departmental Income 65.8% 53.4% 70.3% 71.9% 73.3% 73.4% 73.4% 73.5% 73.6% 73.6% 73.7%