By: CA.Gaurav Garg. Section 92 E “Every person who has entered into an international transaction...

31

AUDIT & DOCUMENTATION ORGANISED BY: BARODA BRANCH OF ICAI JAN 19, 2013 By: CA.Gaurav Garg

-

Upload

alberta-collins -

Category

Documents

-

view

214 -

download

0

Transcript of By: CA.Gaurav Garg. Section 92 E “Every person who has entered into an international transaction...

AUDIT & DOCUMENTATION

ORGANISED BY:BARODA BRANCH OF ICAIJAN 19, 2013

By: CA.Gaurav Garg

Form 3CEB…

Section 92 E“Every person who has entered into an international transaction or specified domestic transaction during a previous year shall obtain a report from an accountant and furnish such report on or before the specified date in the prescribed form duly signed and verified in the prescribed manner by such accountant and setting forth such particulars as may be prescribed”

Section 271BAIf any person fails to furnish a report from an accountant as required by section 92E the Assessing Officer may direct that such person shall pay, by way of penalty, a sum of one hundred thousand rupees.

..Form 3CEB..

Applicable on all type of Assessee who has entered into specified domestic transaction

Value of Specified domestic transaction should not be less than 5cr in aggregate

Accountant means Chartered Accountant in practice Specified date shall have the same meaning as

assigned to “due date” in Explanation 2 below sub-section (1) of section 139 i.e. 30th day of November of the assessment year

..Form 3CEB..

Scope of examination under section 92E of the Act

The Accountant’s Report has got two parts Form 3CEB, &, Annexure to Form 3CEB

Annexure to Form 3CEB has again two parts Part A – Clause 1 to 6 – Particulars of the tax payers Part B – Clause 7 – Particulars of AEs

- Clause 8 – 13 – Information about various transactions

..Form 3CEB..

Scope of examination under section 92E of the Act

Form 3CEB Para 1

“*I/we have examined the accounts and records of ……………….. (name and address of the assessee with PAN) relating to the specified domestic transactions entered into by the assessee during the previous year ending on 31st March, ……….”

..Form 3CEB..

The scope of examination envisaged by section 92E is restricted to such examination of accounts and records of the taxpayer relating to the international transaction entered into by the assessee during the previous year under examination

Ensuring completeness of the listing of international transactions is the responsibility of the taxpayer

MRL should be obtained from the client

..Form 3CEB..

Scope of examination under section 92E of the Act

Guidance Note on Transfer Pricing issued by the ICAI

“36.9 Ensuring completeness of the listing of international transactions is the responsibility of the assessee….”

“36.10 The accountant should obtain a written representation from the assessee providing him with the name, address, legal status and country of tax residence of each of the enterprises with whom international transactions have been entered into by the assessee, and association linkages among them.”

..Form 3CEB..

Scope of examination under section 92E of the Act

Form 3CEB Para 2 “2. In *my/our opinion proper information and documents as are prescribed have been kept by the assessee in respect of the international transaction(s) entered into so far as appears from *my/our examination of the records of the assessee”.

..Form 3CEB..

The Accountant needs to give opinion on Ensuring completeness of the listing of international

transactions is the responsibility of the taxpayer MRL should be obtained from the client

..Form 3CEB..

Scope of examination under section 92E of the Act

Guidance Note on Transfer Pricing issued by the ICAI

“36.12…… It should however be noted that the accountant is not responsible for the content of the transactions and documentation maintained by the assessee.”

“36.13….If any document is not maintained, then the accountant should suitably qualify his report or disclose the same in his report depending upon the facts and circumstances of each case. The accountant should state the qualification in the report making it comprehensive and self explanatory…”

..Form 3CEB..

Scope of examination under section 92E of the Act Form 3CEB Para 2

“3. The particulars required to be furnished under section 92E are given in the Annexure to this Form. In *my/our opinion and to the best of my/our information and according to the explanations given to *me/us, the particulars given in the Annexure are true and correct”.

..Form 3CEB..

Scope of examination under section 92E of the Act

Guidance Note on Transfer Pricing issued by the ICAI

“36.16… As mentioned above, the particulars should be obtained from the assessee, duly authenticated, which should be reviewed by the accountant. In case of any negative remark or qualification about this matter, the same should be properly reported.”

..Form 3CEB..

Scope of examination under section 92E of the Act

Guidance Note on Transfer Pricing issued by the ICAI

“36.17 The accountant must limit his scope of work and the review procedures to the extent certified in Form No.3CEB. For e.g. in the Annexure the method which has been used to determine the arm’s length price needs to be stated. In this context the accountant is only required to ensure that the method stated as being used to determine the arm’s length price by the assessee has actually been used and it is not the accountant’s responsibility to ensure that the method so used is the most appropriate method as prescribed by the Board.”

..Form 3CEB..

Scope of examination under section 92E of the Act

Annexure to Form 3CEB 13 Clauses Clause 1 – Name of the assessee Clause 2 – Address Clause 3 – Permanent account number Clause 4 – Status Clause 5 – Previous year ended Clause 6 – Assessment year

..Form 3CEB..

Scope of examination under section 92E of the Act

Annexure to Form 3CEB Clause 7 – List of the associated enterprises with whom the assessee

has international transactions S.No Particulars

a. Name of associated enterprise.

b. Nature of relationship with the associated enterprise as referred to in section 92 A(2).

c. Brief description of the business carried on by the associated enterprise.

..Form 3CEB..

Clause 8 – Particulars in respect of transactions in tangible property.▪ A - Purchase/sale of raw material, consumables or

any other supplies for assembling/processing/manufacturing of goods/articles from/to AE

S.No Particulars

a. Name and address of the AE with whom the international transaction has entered into.

b. Description of transaction and quantity purchased /sold

c. Total amount paid/received or payable/receivable in the transaction

(i) as per books of account.(ii) as computed by the assessee having regard to the

arm’s length price.

d. Method used for determining the ALP

..Form 3CEB..

B. If the assessee has entered into any international transaction in respect of purchase/sale of traded/finished goods, then:S.No Particulars

a. Name and address of the AE with whom the international transaction has entered into.

b. Description of transaction and quantity purchased /sold

c. Total amount paid/received or payable/receivable in the transaction

(i) as per books of account.(ii) as computed by the assessee having regard to the

arm’s length price.

d. Method used for determining the ALP

..Form 3CEB..

C. purchase/sale of any other tangible movable/immovable property or lease of such property, then:S.No Particulars

a. Name and address of the AE with whom the international transaction has entered into.

b. Description of property and nature of transaction.

c. Number of units of each category of movable/immovable property involved in the transaction.

d. Total amount/lease rent paid/received or payable/receivable in respect of each transaction of purchase/sale or lease provided/entered into:

(i) as per books of account.(ii) as computed by the assessee having regard to the

arm’s length price.

e. Method used for determining the ALP

..Form 3CEB..

Clause 9 – Particulars in respect of intangible property▪ Purchase/sale/use of intangible property such as know-

how, patents, copyrights, licenses etc, then:

S.No Particulars

a. Name and address of the AE with whom the international transaction has entered into.

b. Description of intangible property and nature of transaction.

c. Total amount paid/received or payable/receivable for purchase/sale/use of each category of intangible property:

(i) as per books of account.(ii) as computed by the assessee having regard to the

arm’s length price.

d. Method used for determining the ALP

..Form 3CEB..

Clause 10 – Particulars in respect of providing services▪ In respect of services such as financial, administrative,

technical, commercial services, etc, then:

S.No Particulars

a. Name and address of the AE with whom the international transaction has entered into.

b. Description of services provided/availed of/from the AE.

c. Total amount paid/received or payable/receivable for the services provided/taken:

(i) as per books of account.(ii) as computed by the assessee having regard to the

arm’s length price.

d. Method used for determining the ALP

..Form 3CEB..

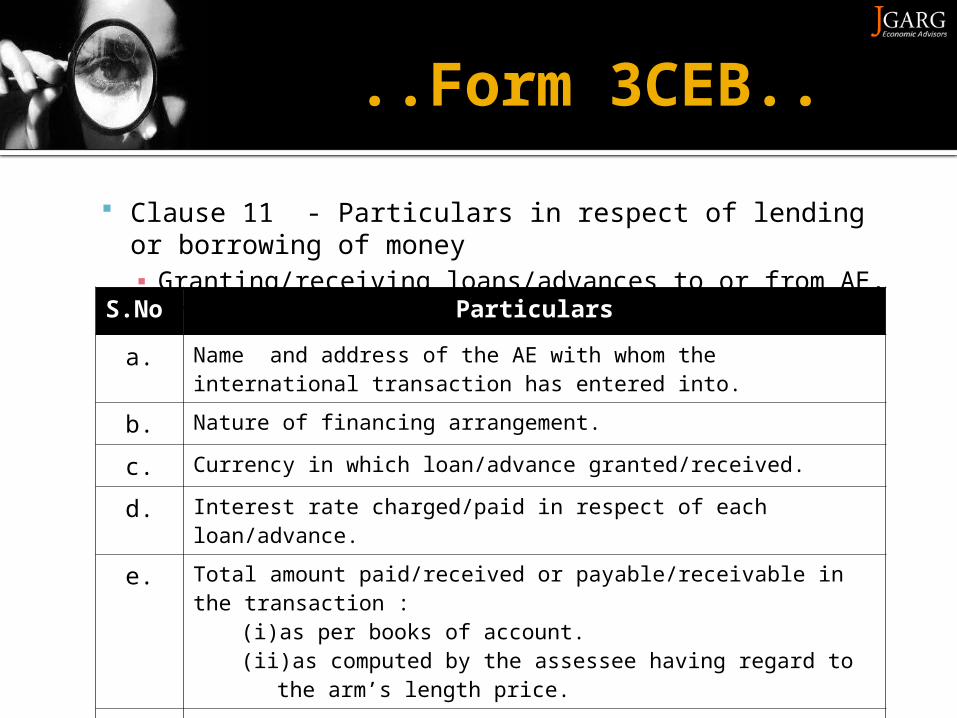

Clause 11 - Particulars in respect of lending or borrowing of money▪ Granting/receiving loans/advances to or from AE, then

S.No Particulars

a. Name and address of the AE with whom the international transaction has entered into.

b. Nature of financing arrangement.

c. Currency in which loan/advance granted/received.

d. Interest rate charged/paid in respect of each loan/advance.

e. Total amount paid/received or payable/receivable in the transaction :

(i) as per books of account.(ii) as computed by the assessee having regard to the

arm’s length price.

f. Method used for determining the ALP

…Form 3CEB

Clause 12 – Particulars in respect of mutual agreement or arrangement.▪ Mutual agreement or arrangement for the allocation or

apportionment of, or any contribution to, any cost or expense incurred or to be incurred in connection with a benefit, service or facility provided or to be provided to any or more of such enterprises:S.No Particulars

a. Name and address of the AE with whom the international transaction has entered into.

b. Description of such mutual agreement or arrangement.

c. Total amount paid/received or payable/receivable in each such transaction:

(i) as per books of account.(ii) as computed by the assessee having regard to the

arm’s length price.

d. Method used for determining the ALP

…Form 3CEB

Clause 13- Particulars in respect of any other transactions▪ Any other international transaction not specifically

referred to above, with AE

S.No Particulars

a. Name and address of the AE with whom the international transaction has entered into.

b. Description of the transaction.

c. Total amount paid/received or payable/receivable in each such transaction:

(i) as per books of account.(ii) as computed by the assessee having regard to the

arm’s length price.

d. Method used for determining the ALP

Transfer Pricing Documentation

25

TP Documentation… Refer section 92D of the Act read with Rule 10D of

the Rules Types of Documents

Enterprise - wise

Transaction specific

Computation related

26

…TP Documentation… Enterprise-wise documents

Ownership structure of the taxpayer Profile of the Group Name of Associated Enterprises, address,, legal

status, country of tax residence, ownership linkage and business

Business of the taxpayer, description of industry

27

…TP Documentation… Transaction-specific documents

Description of transaction Functional Asset & Risk Analysis Industry / market condition, forecasts/ budget, financial

estimates Uncontrolled transactions and comparability analysis

Computation related Most appropriate method Assumptions and adjustments if any Arm’s length price

28

…TP Documentation… Section 92 D of the Act read with Rule 10E of the Rules

Should be prepared on contemporaneous basis Should be kept and maintained for 8 years from the

end of the relevant assessment year No fresh documentation required for continuing

transactions unless there is some significant change which can have impact on pricing

29

Sufficiency

Reasonableness

AccuracyContemporaneous

Regulation

…TP Documentation…

Open House?

Thank You

CA. Gaurav GargJGarg Economic

Advisors

Email: [email protected]

Mobile: +91 9899994934

www.jgarg.com

13 Nov 2011