B.V. Patel Institute of Business Management, Computer...

30

B.V. Patel Institute of Business Management, Computer & Information Technology, Uka Tarsadia University Question Bank 030100216: Managerial Accounting 1 Unit 1 Interpretation of Financial Statement Fill in the blanks. (1 mark) 1. Cost of Goods Sold = Opening Stock + _____________ +____________- Closing Stock 2. ___:___ is ideal Liquid Ratio 3. Operating ratio = 4. Current Assets – Current Liabilities = _______________. 5. Acid Test Ratio also known as________________. 6. Debt Equity Ratio = ---------- 7. Shareholders fund Rs. 75,000 and Reserve to Capital Ratio is 0.5 so capital is___________. 8. __: __ is ideal Current Ratio 9. Proprietary ratio also know as_____________. 10. Current Ratio is _____________, if Current Assets Rs. 200,000 and Working Capital Rs. 120,000 11. Formula of operating profit 12. Financial statements consider _____________ factors 13. Financial statements not consider _______________ factors 14. Balance sheet is _______________ 15. _________ form of balance sheet has two sides 16. _________ form of balance sheet has no sides 17. Fixed assets shown as _______________ in balance sheet 18. Provident fund is shown under _____________ head of balance sheet 19. Outstanding is shown under____________ head of balance sheet 20. Prepaid incomes is shown under ___________ head of balance sheet 21. Insurance co. a/c is shown under ___________ head of balance sheet 22. Prepaid expenditure shown under __________ head of balance sheet 23. Goodwill is ________ asset 24. Patent is ________ asset 25. Fictitious assets is not an asset but it is a ________________ 26. Preliminary expenditure is a ____________ asset

Transcript of B.V. Patel Institute of Business Management, Computer...

B.V. Patel Institute of Business Management, Computer & Information

Technology, Uka Tarsadia University

Question Bank 030100216: Managerial Accounting

1

Unit 1 Interpretation of Financial Statement

Fill in the blanks. (1 mark)

1. Cost of Goods Sold = Opening Stock + _____________ +____________- Closing Stock

2. ___:___ is ideal Liquid Ratio

3. Operating ratio =

4. Current Assets – Current Liabilities = _______________.

5. Acid Test Ratio also known as________________.

6. Debt Equity Ratio = ----------

7. Shareholders fund Rs. 75,000 and Reserve to Capital Ratio is 0.5 so capital is___________.

8. __: __ is ideal Current Ratio

9. Proprietary ratio also know as_____________.

10. Current Ratio is _____________, if Current Assets Rs. 200,000 and Working Capital Rs.

120,000

11. Formula of operating profit

12. Financial statements consider _____________ factors

13. Financial statements not consider _______________ factors

14. Balance sheet is _______________

15. _________ form of balance sheet has two sides

16. _________ form of balance sheet has no sides

17. Fixed assets shown as _______________ in balance sheet

18. Provident fund is shown under _____________ head of balance sheet

19. Outstanding is shown under____________ head of balance sheet

20. Prepaid incomes is shown under ___________ head of balance sheet

21. Insurance co. a/c is shown under ___________ head of balance sheet

22. Prepaid expenditure shown under __________ head of balance sheet

23. Goodwill is ________ asset

24. Patent is ________ asset

25. Fictitious assets is not an asset but it is a ________________

26. Preliminary expenditure is a ____________ asset

B.V. Patel Institute of Business Management, Computer & Information

Technology, Uka Tarsadia University

Question Bank 030100216: Managerial Accounting

2

27. Share issue expenditure is a ______________

28. Advertisement expenditure is a _____________ asset

29. Discount of Issue of Debentures is a __________asset

Briefly answer the following. (2 marks)

1. Determine the value of closing stock from the following details

Sales Rs. 6,00,000

Gross Profit 20% on sales

Stock velocity 4 Times

Closing stock was Rs. 10,000 in excess of opening stock

Ans.: Closing Stock: 115000

2. From the following information given below, calculate:

(a) Current liabilities and (b) Inventory

Current ratio: 2.5

Acid test: 1.7

Current assets: Rs. 250,000

Ans.: Current liabilities: Rs. 100,000 and Inventor: Rs. 80,000

3. Debtors velocity : 3 months

Sales Rs. 1,000,000 (includes 80% credit sales)

Find Debtors

Ans. Debtors Rs: 200,000

4. Debtors turnover ratio: 3 months

Gross profit to sales 25%

Gross Profit Rs. 4,00,000

Bill receivable Rs. 25,000

Calculate: (a) Sales (b) Sundry debtors

Ans. (a) Rs. 16,00,000 (b) Rs. 3,75,000

5. Shareholders fund Rs. 75000

Reserve to capital ratio 0.5

Fund Reserves and capital

Ans. Reserves Rs. 25,000 and Capital Rs. 50,000

B.V. Patel Institute of Business Management, Computer & Information

Technology, Uka Tarsadia University

Question Bank 030100216: Managerial Accounting

3

6. Determine the value of closing stock from the following details:

Sales Rs. 4,00,000

Gross Profit Ratio 10% on sales

Stock velocity 4 times

Closing stock was Rs. 10,000 in excess of opening stock

Ans.: Closing Stock: Rs. 95,000

7. Prepare a list of current assets from the following details:

Current Ratio: 2.5

Quick Ratio: 1.5

Working capital: Rs. 75,000

Bank Overdraft: Rs. 25,000

Cash in hand: Rs. 1,000

Ans. C.A total: Rs. 125,000; Cash in hand: Rs. 1,000; Stock: Rs. 50,000; other current

assets: Rs. 74,000

8. Cost of goods sold 12,00,000

Opening Stock 1,45,000

Closing stock 1,55,000

Find Purchase

Ans.: Purchase Rs. 12,10,000

9. Debtors velocity 3 Months

Bills Receivable Rs. 25000

Sales Rs. 16,00,000

Find out Debtors

Ans.: Debtors Rs. 375,000

10. Format of proprietary fund

Ans.: Proprietary fund = Share Capital + Reserves + Preference Shares + P & L A/c –

Intangible Assets – Fictitious Assets

11. Enlist eight current liabilities

12. Formula of operating profit

B.V. Patel Institute of Business Management, Computer & Information

Technology, Uka Tarsadia University

Question Bank 030100216: Managerial Accounting

4

13. Write four limitations of financial statements

14. Explain inflation as one of the limitation of financial statements

15. Explain convention of conservatism as a limitation of financial statements

16. Enlist four tangible assets

17. Enlist four intangible assets

18. List any four current assets

19. Define Fixed assets

20. Define Current assets

21. Define Current liabilities

22. List any four current liabilities

23. List any four Non-current liabilities

24. Enlist any four Fictitious assets

25. Explain Fictitious assets

26. Define Ratio

27. Explain intangible assets

28. Explain deferred expenditures

29. Give mode of expression of the ratio with example

30. What are the steps in ratio analysis?

31. Enlist any four importance of ratio analysis.

32. Enlist any four limitations of ratio analysis.

33. Enlist any four limitations of current ratio

34. Enlist ratios in which Creditors (Short term), Investors and Money Lenders are interested?

35. Enlist ratios in which Shareholders, creditors, purchasers and employees are interested?

36. Enlist solvency ratio

37. Enlist Profitability ratio

38. Enlist Activity ratio

39. Enlist Earning ratio

40. Write the formula of quick ratio along with signification of it

B.V. Patel Institute of Business Management, Computer & Information

Technology, Uka Tarsadia University

Question Bank 030100216: Managerial Accounting

5

41. Tamil and co. sells goods on cash as well as credit (thought not on deferred installment

terms). The following particular are extracted from their books of accounts for the calendar

year 2012

Rs.

Total Gross Sales

Cash Sales (included in above)

Sales Returns

Total Debtors for sales as on 31.12.2012

Bills Receivable on 31.12.2012

Provision for doubtful debts on 31.12.2012

Total creditors on 31.12.2012

Calculate the average collection period

1,00,000

20,000

7,000

9,000

2,000

1,000

10,000

Ans. Average Collection period 55 Days

42. Calculate stock turnover ratio: Opening Stock Rs. 20,000, Closing stock Rs. 10,000,

Purchases Rs. 50,000, Wages Rs. 3,000, Carriage Inward Rs. 2,000 and Freight outward Rs.

5,000

Ans. Average Stock Rs. 15,000 and Stock Turnover Ratio 4.3 times

43. Calculate opening debtors and closing debtors in the following case: Cash sales Rs.

1,00,000, Cost of goods sold Rs. 3,00,000, Gross profit Rs. 1,00,000, Debtors turnover ratio

3 times and closing debtors were Rs. 1,00,000 in excess of opening debtors

Ans. Average Debtors Rs. 300,000, Opening Debtors Rs. 50,000 and Closing stock Rs.

1, 50,000

44. A trading company purchases goods on cash as well as on credit terms. The following

particular are available:

Rs.

Total purchases

Cash purchases

Purchases at the end

Creditors at the end

Bills payable at the end

Reserve for discount on creditors

5,81,000

30,000

51,000

1,05,000

60,000

10,000

Calculate average payment period

Ans. Average payment period 119 days, not credit purchase Rs. 500,000 and Accounts

payable Rs. 165,000.

B.V. Patel Institute of Business Management, Computer & Information

Technology, Uka Tarsadia University

Question Bank 030100216: Managerial Accounting

6

45. Calculate working capital Turnover ratios from the following:

Rs.

Current Assets

Current Liabilities

Credit Sales

Cash sales

Sales returns

6,00,000

1,20,000

12,00,000

2,60,000

20,000

Ans. Working Capital Turnover Ratio 3 times

46. Calculate working capital Turnover Ratio from the following.

Rs.

Capital Employed

Net Fixed assets

Cost of goods sold

Gross Profit

6,00,000

4,00,000

20,00,000

4,00,000

Ans. Working Capital Turnover Ratio 12 times

47. Calculate Fixed Assets Turnover Ratio from the following.

Rs.

Capital Employed

Working Capital

Cost of goods sold

Gross Profits

2,00,000

40,000

6,40,000

1,60,000

Ans. Fixed Turnover Ratio 5 times

48. From the following information calculate current ratio

Particulars Rs. Particulars Rs.

Share capital

(1,00,000 shares of Rs. 1 each)

Profit & Loss A/c

General reserve

Development Rebate Reserve

Land & Building

Plant & Machinery

Stock in trade

1,00,000

15,000

20,000

10,000

70,000

1,75,000

1,00,000

Bank Overdraft (Short term)

Sundry creditors

Bills payable

Sundry Debtors

Bills Receivable

Cash at bank

2,00,000

50,000

25,000

50,000

5,000

20,000

Ans. Current Assets Rs. 1,75,000, Current Liabilities Rs. 2,75,000. Current Ratio 0.64:1

49. Determine the value of closing stock from the following details

Sales Rs. 6,00,000

B.V. Patel Institute of Business Management, Computer & Information

Technology, Uka Tarsadia University

Question Bank 030100216: Managerial Accounting

7

Gross Profit 20% on sales

Stock velocity 4 Times

Closing stock was Rs. 10,000 in excess of opening stock

Ans.: Closing Stock: 115000

50. From the following information given below, calculate:

(b) Current liabilities and (b) Inventory

Current ratio: 2.5

Acid test: 1.7

Current assets: Rs. 2,50,000

Ans.: Current liabilities: Rs. 100,000 and Inventor: Rs. 80,000

51. Debtors velocity : 3 months

Sales Rs. 10,00,000 (includes 80% credit sales)

Find Debtors

Ans. Debtors Rs: 2,00,000

52. Debtors turnover ratio: 3 months

Gross profit to sales 25%

Gross Profit Rs. 4,00,000

Bill receivable Rs. 25,000

Calculate: (a) Sales (b) Sundry debtors

Ans. (a) Rs. 16,00,000 (b) Rs. 3,75,000

53. Shareholders fund Rs. 75000

Reserve to capital ratio 0.5

Fund Reserves and capital

Ans. Reserves Rs. 25,000 and Capital Rs. 50,000

54. Determine the value of closing stock from the following details:

Sales Rs. 4,00,000

Gross Profit Ratio 10% on sales

Stock velocity 4 times

Closing stock was Rs. 10,000 in excess of opening stock

Ans.: Closing Stock: Rs. 95,000

B.V. Patel Institute of Business Management, Computer & Information

Technology, Uka Tarsadia University

Question Bank 030100216: Managerial Accounting

8

55. Prepare a list of current assets from the following details:

Current Ratio: 2.5

Quick Ratio: 1.5

Working capital: Rs. 75,000

Bank Overdraft: Rs. 25,000

Cash in hand: Rs. 1,000

Ans. C.A total: Rs. 1,25,000; Cash in hand: Rs. 1,000; Stock: Rs. 50,000; Other

current assets: Rs. 74,000

56. Cost of goods sold 12,00,000

Opening Stock 1,45,000

Closing stock 1,55,000

Find Purchase

Ans.: Purchase Rs. 12,10,000

57. Debtors velocity 3 Months

Bills Receivable Rs. 25000

Sales Rs. 16,00,000

Find out Debtors

Ans.: Debtors Rs. 3,75,000

B.V. Patel Institute of Business Management, Computer & Information

Technology, Uka Tarsadia University

Question Bank 030100216: Managerial Accounting

9

Answer the following (limit 250 words). (5 marks)

1. State the Purpose and mode of determining the following ratios: (i) Inventory ratios (ii)

Debtors Ratios and (iii) Operating Ratios

2. State the significance of accounting ratios in the analysis of financial statements

3. What is meant by Ratio Analysis? Discuss its objects and limitations

4. What are turnover ratios? Discuss their significance

5. What are the limitations on Ratio Analysis?

6. Discuss some of the importance ratios usually worked from financial statement showing

how they would be useful to higher management?

B.V. Patel Institute of Business Management, Computer & Information

Technology, Uka Tarsadia University

Question Bank 030100216: Managerial Accounting

10

Unit-2 Fund Flow Statement

Fill in the blanks. (1 mark)

1. Proposed Dividend is a current _______________.

2. Net working capital: in the Year 2009- Rs. 1,00,000 and in the Year 2010 Rs. 1,10,000. It is

______________.

3. Capital in the year 2010 was Rs. 50,000 and in the year 2011 was Rs. 1,00,000. It is

______________.

4. Increase in current assets result in __________________.

5. Increase in current liabilities result in _______________.

6. Decrease in both current assets and current liabilities by the same amount, there is

_____________ .(Impact/ No impact on flow of fund)

7. Increase in current assets and non-current liabilities. There is _________________.

(Impact/ No impact on flow of fund)

8. Sold building for cash. There is ____________ .(Impact/ No impact on flow of fund)

9. Bill accepted by us. There is _____________. (Impact/ No impact on flow of fund)

10. Machinery purchase by issuing share. There is ____________ .(Impact/ No impact on flow

of fund)

11. Fixed Assets in the year 2009 was Rs.100,000 and in the year 2012 was Rs.95,000. It is a

___________ of fund (Source or Application)

12. Long term loan in the year 2009 was Rs. 88,000 and in the year 2010 was Rs. 82,000. It is a

_______________ of fund (Source or Application)

13. Increase in working capital goes to ______________ side of Fund of flow statement

14. Total of credit side of P&L Adjustment account is higher than debit side, so it is

___________________.

15. P & L a/c Rs. 10,000 on Liabilities side, so it is ________________.(Profit / Loss)

B.V. Patel Institute of Business Management, Computer & Information

Technology, Uka Tarsadia University

Question Bank 030100216: Managerial Accounting

11

Briefly answer the following. (2 marks)

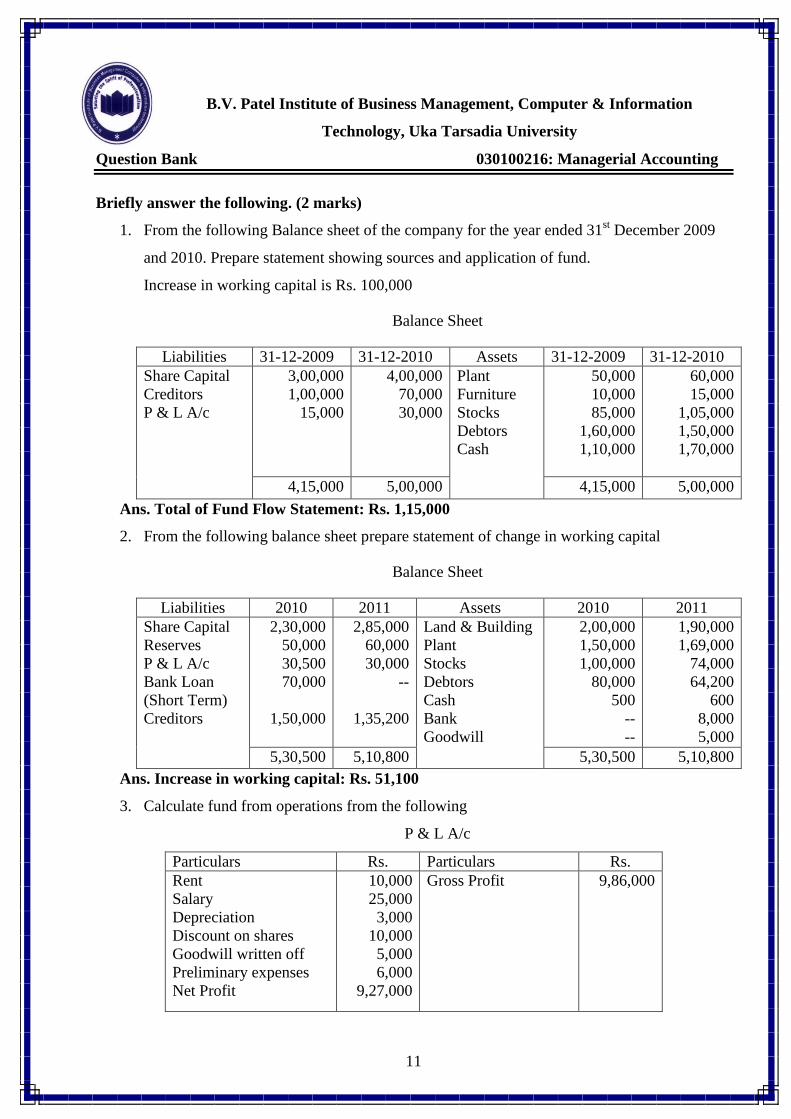

1. From the following Balance sheet of the company for the year ended 31st December 2009

and 2010. Prepare statement showing sources and application of fund.

Increase in working capital is Rs. 100,000

Balance Sheet

Liabilities 31-12-2009 31-12-2010 Assets 31-12-2009 31-12-2010

Share Capital

Creditors

P & L A/c

3,00,000

1,00,000

15,000

4,00,000

70,000

30,000

Plant

Furniture

Stocks

Debtors

Cash

50,000

10,000

85,000

1,60,000

1,10,000

60,000

15,000

1,05,000

1,50,000

1,70,000

4,15,000 5,00,000 4,15,000 5,00,000

Ans. Total of Fund Flow Statement: Rs. 1,15,000

2. From the following balance sheet prepare statement of change in working capital

Balance Sheet

Liabilities 2010 2011 Assets 2010 2011

Share Capital

Reserves

P & L A/c

Bank Loan

(Short Term)

Creditors

2,30,000

50,000

30,500

70,000

1,50,000

2,85,000

60,000

30,000

--

1,35,200

Land & Building

Plant

Stocks

Debtors

Cash

Bank

Goodwill

2,00,000

1,50,000

1,00,000

80,000

500

--

--

1,90,000

1,69,000

74,000

64,200

600

8,000

5,000

5,30,500 5,10,800 5,30,500 5,10,800

Ans. Increase in working capital: Rs. 51,100

3. Calculate fund from operations from the following

P & L A/c

Particulars Rs. Particulars Rs.

Rent

Salary

Depreciation

Discount on shares

Goodwill written off

Preliminary expenses

Net Profit

10,000

25,000

3,000

10,000

5,000

6,000

9,27,000

Gross Profit 9,86,000

B.V. Patel Institute of Business Management, Computer & Information

Technology, Uka Tarsadia University

Question Bank 030100216: Managerial Accounting

12

9,86,000 9,86,000

Ans. Fund from operations Rs. 9,51,000

4. From the following information, find out funds from operations:

2010 2011

Reserves 1,000 1,250

Goodwill 500 250

Provision for depreciation (plant) 500 600

Preliminary Expenses 300 200

P & L A/c 1,500 2,000

Ans. Fund from Operations Rs. 1,200

5. Examine the impact of the following transactions on the funds flow:

i. Cash collected from debtors

ii. Purchase of machinery by issue of debentures

iii. Old furniture the book value of Rs. 5000 discarded and written of in the profit and

loss account

Ans.: None of the transactions will affect funds flow

6. State the reason whether the following transactions result in the increase or decrease of

working capital or do not affect the working capital: (Each question is different so can ask

separately)

i. Advance income tax paid Rs. 50,000. Ans. Decrease

ii. Preliminary expenses written off Rs. 5,000. Ans. No effect

iii. A company issued 10,000 shares of Rs.10 each at par and fully paid up. Ans.:

Increase

iv. Debentures for Rs. 100,000 are converted into Equity shares. Ans.: No effect

v. Cash paid to creditors Rs. 30,000. Ans.: No effect

vi. Fixed assets purchased by issue of shares for Rs. 100,000. Ans.: No effect

vii. Bill receivable Rs. 10,000 discounted for Rs. 9,500. Ans.: Decrease

viii. Bills payable accepted and issued to creditors Rs. 40,000. Ans.: No effect

B.V. Patel Institute of Business Management, Computer & Information

Technology, Uka Tarsadia University

Question Bank 030100216: Managerial Accounting

13

ix. Building was purchased for Rs.150,000/-. Ans.: Decrease

x. Investments were sold for Rs. 50,000. Ans.: Increase

7. Enlist eight item added back to the net profit

Answer the following (limit 250 words). (5 marks)

1 What is a „fund flow statement‟? Examine its managerial uses.

2 „A funds flow statement is a better substitute for an income statement‟. Discuss

3 Explain the various concepts of funds in the context of funds flow analysis.

4 What do you understand by funds flow statements? How are they prepared? What are their

uses?

5 What are the chief advantages of funds flow statement? Also describe its limitations

6 Distinguish between statement showing change in working capital, and fund flow statement

7 Distinguish between income statement and funds flow statement

8 Short Notes: Applications of funds

9 Short Notes: Importance of funds flow statement

10 Short Notes: Statement of changes in financial position

11 Distinguish between: fund flow statement and a balance sheet

B.V. Patel Institute of Business Management, Computer & Information

Technology, Uka Tarsadia University

Question Bank 030100216: Managerial Accounting

14

Unit 3 Budgetary Control

Answer the following. (1 mark)

1 Define budget.

2 Office overhead is Rs. 12,000 (60 % variable), Find out Fixed cost.

3 Factory Overheads is Rs. 30 (40% fixed), Find out Variable cost.

4 Overheads are Rs. 5 per unit (60% fixed) for 40% capacity level, what would be the

Overheads (variable) per unit for 90% capacity level?

5 Give one example of semi variable cost.

6 Is there any difference between a forecast and a budget?

7 In variable cost what amount remain same for the next year calculation?

8 In fixed cost what amount remain same for the next year calculation?

9 Overheads are Rs. 5 per unit (60% fixed) for 40% capacity level, what would be the

Overheads (variable) per unit for 70% capacity level?

10 Which cost has a special significance in the preparation of flexible budget?

Briefly answer the following. (2 marks)

1 Define budgetary control.

2 What do you mean by Semi-variable cost?

3 Write any two advantages of preparing budget.

4 The following budget estimates are available from a factory working at 50% of its capacity:

Variable expenses Rs. 60,000

Semi –variable expense Rs. 20,000

Fixed expenses Rs. 10,000

B.V. Patel Institute of Business Management, Computer & Information

Technology, Uka Tarsadia University

Question Bank 030100216: Managerial Accounting

15

Prepare a budget for 75% of the capacity assuming that semi- variable expenses increase by

10% for every 25%.

5 Write any two objectives of budgeting.

6 Write down any two characteristics of budgetary control.

7 The following budget estimates are available from a factory working at 50% of its capacity:

Variable expenses Rs. 30,000

Semi –variable expense Rs. 10,000

Fixed expenses Rs. 5,000

Prepare a budget for 75% of the capacity assuming that semi- variable expenses increase by

10% for every 25%.

Answer the following (limit 250 words). (5 marks)

1 Write a brief note “Zero base budgeting”

2 Explain advantages and disadvantages of Budgetary control.

3 A factory engaged in manufacturing plastic buckets is working to 40% capacity and

produces 10,000 buckets per month. The present cost break-up for one bucket is as

under:

Material –Rs.10

Labour – Rs. 3

Overhead – Rs. 5 (60% fixed)

The selling price is Rs. 20 per bucket. If it is decided to work the factory at 50% capacity

the selling price falls by 3%. At 90% capacity the selling price falls by 5% accompanied by

a similar fall in the price of material.

You are required to prepare a statement showing the profit at 50% and 90% capacities and

also calculate the break-even points at these capacity productions.

4 You are given the following details of Hero Ltd., at 50% production level:

Production 200 units

B.V. Patel Institute of Business Management, Computer & Information

Technology, Uka Tarsadia University

Question Bank 030100216: Managerial Accounting

16

Raw materials Rs. 60 per unit

Wages 50% of materials

Direct expenses 50% of wages

Factory overheads Rs. 30,000 (40% fixed)

Administrative overheads Rs. 40,000 (50% fixed)

Prepare flexible budget at 60%, 80% and 100% level.

5 A department of company X attains sales of Rs. 6,00,000 at 80% of its normal capacity

and its expenses are given below :

Administration costs:

Office salaries Rs. 90,000

General expenses 2% of sales

Depreciation Rs. 7,500

Rates and taxes Rs. 8,750

Selling costs

Salaries 8% of sales

Travelling expenses 2% of sales

Sales office 1% of sales

General expenses 1% of sales

Distribution costs

Wages Rs. 15,000

Rent 1% of sales

Other expenses 4% of sales

Draw up flexible administration, selling and distribution costs budget, operating at 90%,

100% and 110% of normal capacity.

6 With the following data for a 60% activity, prepare a budget for production at 80%

and 100% activity.

Production at 60% activity- 600 units

Materials Rs. 100 per unit

Labour Rs. 40 per unit

Expenses Rs. 10 per unit

B.V. Patel Institute of Business Management, Computer & Information

Technology, Uka Tarsadia University

Question Bank 030100216: Managerial Accounting

17

Factory expenses Rs. 40,000 (40% fixed)

Administration expenses Rs. 30,000 (60% fixed)

7 The expenses budgeted for production of 10,000 units in a factory are furnished

below:

Particulars Rs. Per unit

Materials 70

Labour 25

Variable overheads 20

Fixed overheads (Rs. 1,00,000) 10

Variable expenses (direct) 5

Selling expenses (10% fixed) 13

Distribution expenses (20% fixed) 7

Administration expenses (Rs. 50,000) 5

Assuming that the administration expenses are rigid for all levels of production,

prepare a budget for the production of 6,000 and 8,000 units.

8 The cost of an article at the capacity level of 5,000 units is given under A below:

For a variation of 25% in capacity above or below this level, the individual expenses vary

as indicated under B below:

Particulars A B (%)

Material cost 25,000 100 (variable)

Labour cost 15,000 100(variable)

Power 1,250 80(variable)

Repairs and maintenance 2,000 75(variable)

Stores 1,000 100(variable)

Inspection 500 20(variable)

Administration overheads 5,000 25(variable)

Selling overheads 3,000 50(variable)

Depreciation 10,000 100(variable)

Total 62,750

Cost per unit 12.55

Prepare the flexible budget at 4,000 units and 6,000 units.

B.V. Patel Institute of Business Management, Computer & Information

Technology, Uka Tarsadia University

Question Bank 030100216: Managerial Accounting

18

9 The cost of an article at a capacity level of 10,000 units is given under A below: for a

variation in capacity above or below this level, the individual expenses vary as

indicated in B below:

Particulars A (Rs.) B (%)

Material cost 50,000 (100% varying)

Labour 30,000 (100% varying)

Power 3,000 (80% varying)

Repairs and maintenance 3,500 (80% varying)

Stores 2,000 (100% varying)

Inspection 800 (25% varying)

Depreciation 10,000 (100% varying)

Administration overhead 3,600 (25% varying)

Selling overhead 4,500 (50% varying)

Total 1,07,400

Cost per unit 10.74

Find out the unit cost of the product under each individual expense at production

level of 8,000 units and 12,000 units.

10 A factory is currently working to 50% capacity and produces 10,000 units. Estimate

the profits of the company when it workers to 60% and 80% capacity.

At 60% working raw material cost increases by 20% and selling price falls by 5%

At 50% capacity working the product costs Rs. 180 per unit and is sold at Rs. 200 per unit.,

The unit cost of Rs. 180 is made up as follows.

Material Rs. 100

Labour Rs. 30

Factory overhead Rs. 30 (40% fixed)

Administrative overhead Rs. 20 (50% fixed)

At 50% capacity:

Factory overhead Rs. 30 per unit.

Fixed cost is 40% of Rs. 30 or Rs. 12 per unit.

Production – 10,000 units.

B.V. Patel Institute of Business Management, Computer & Information

Technology, Uka Tarsadia University

Question Bank 030100216: Managerial Accounting

19

Total fixed factory overhead – 10,000 × 18 or Rs. 1,80,000

Administrative overhead – Rs. 20 per unit.

Fixed cost is 50% of Rs. 10 per unit.

Total fixed administrative overhead – 10,000 × 10 or Rs. 1,00,000

It may be noted that the fixed overhead will normally remain constant up to 100% capacity,

increase in raw material cost and decrease in selling price are to be calculated with

reference to the figure given 50% capacity usage.

11 The expenses budgeted for production of 10,000 units in a factory are given below:

Rs. Per unit

Materials 70

Labour 25

Variable overheads 20

Fixed overheads (1,00,000) 10

Variable overheads (Direct) 5

Selling expenses (10% fixed) 13

Administration expenses (Rs. 50,000) 5

Distribution expenses (20% fixed) 7

155

Prepare a budget of the production (a) 8,000 units (b) 6,000 units. Assume that the

administration expenses are rigid for all levels of production.

12 Draw up a flexible budget for overhead expenses on the basis of the following data

and determine the overhead rates at 70%, 80% and 90% capacity levels.

At 80% capacity (Rs.)

Variable overheads:

Indirect labor 12,000

Indirect material 4,000

Semi- variable overheads:

Power (30% fixed and 70% variable) 20,000

Repairs and maintenance (60% fixed) 2,000

Fixed overheads:

B.V. Patel Institute of Business Management, Computer & Information

Technology, Uka Tarsadia University

Question Bank 030100216: Managerial Accounting

20

Depreciation 11,000

Insurance 3,000

Others 10,000

Total overheads 62,000

124,000 hours

13 With the following data for a 60% activity, prepare a budget for production at 80%

and 100% activity. Production at 60% activity: 600 units.

Materials Rs. 100 per unit

Labour Rs. 40 per unit

Expenses Rs. 10 per unit

Factory expenses Rs. 40,000 (40% fixed)

Administration expenses Rs. 30,000 (60% fixed)

14 From the following forecasts of income and expenditure prepare a cash budget for the

three months commencing 1st June, when the bank balance was Rs. 1, 00,000.

Month Sales (Rs.) Purchase

(Rs.)

Wages

(Rs.)

Factory Exp.

(Rs.)

Adm. & Selling

Exp. (Rs.)

April 80,000 41,000 5,600 3,900 10,000

May 76,500 40,500 5,400 4,200 14,000

June 78,500 38,500 5,400 5,100 15,000

July 90,000 37,000 4,800 5,100 17,000

August 95,000 35,000 4,700 6,000 13,000

A sales commission of 5% on sales, due two months after sales, is payable in addition to

selling expenses. Plant valued at Rs. 65,000 will be purchased and paid for in August, and

the dividend for the last financial year of Rs. 15,000 will be paid in July. There is a two

month credit period allowed to customers and received from suppliers.

15 A company expects to have Rs. 37,500 cash in hand on 1st April, and requires you to

prepare an estimate of cash position during the three months, April, May and June.

The following information is supplied to you:

Month Sales

(Rs.)

Purchase

(Rs.)

Wages

(Rs.)

Factory

Exp. (Rs.)

Office Exp.

(Rs.)

Selling Exp.

(Rs.)

February 75,000 45,000 9,000 7,500 6,000 4,500

March 84,000 48,000 9,750 8,250 6,000 4,500

April 90,000 52,500 10,500 9,000 6,000 5,250

May 120,000 60,000 13,500 11,250 6,000 6,570

B.V. Patel Institute of Business Management, Computer & Information

Technology, Uka Tarsadia University

Question Bank 030100216: Managerial Accounting

21

June 135,000 60,000 14,250 14,000 7,000 7,000

Other information:

1. Period of credit allowed by suppliers 2 month.

2. 20% of sales is for cash and period of credit allowed to customers for credit is one

month.

3. Delay in payment of all expenses- 1month.

4. Income tax of Rs. 57,500 is due to be paid on June 15 th.

5. The company is to pay dividends to shareholders and bonus to workers of Rs. 15,000

and Rs. 22,500 respectively in the month of April

6. Plant has been ordered to be received and paid in May. It will cost Rs.120,000.

16 Prepare a cash budget for the three months ending 30th June from the following

information.

Month Sales Materials Wages Overheads

February 14,000 9,600 3,000 1,700

March 15,000 9,000 3,000 1,900

April 16,000 9,200 3,200 2,000

May 17,000 10,000 3,600 2,200

June 18,000 10,400 4,000 2,300

(a) 10% of the sales are on cash. 50% of the credit sales are collected next month and the

balance in the following month.

(b) Lag in payment:- materials 2 months, wages ¼ month, overheads ½ month.

(c) Cash and bank balance on 1st April is expected to be Rs. 6,000.

(d) Other information:

1. Plant and machinery will be installed in February at a cost of Rs. 96,000. The

monthly installments of Rs. 2,000 are payable from April onwards.

2. Dividend @5% on preference share capital of Rs. 2, 00,000 will be paid on 1st June.

3. Advanced to be received for sale of vehicles Rs. 9,000 in June.

4. Dividend from investments amounting to Rs. 1,000 is expected to be received in

June.

5. Income-tax to be paid in June Rs. 2,000.

B.V. Patel Institute of Business Management, Computer & Information

Technology, Uka Tarsadia University

Question Bank 030100216: Managerial Accounting

22

17 Ram Ltd. produces 12,000 scooters at present at 60% production capacity. If the

company produces at 80% and 90% production capacity, what would be the profit?

At 80% production capacity, the cost of raw material increases by 5% and sales price is

reduced by 2%. At 90% production capacity. The cost of raw material increases 8.33% and

sale price is reduced by 3%. At 60% production capacity, the cost of production per unit of

scooter is Rs. 22,000 and it is sold at Rs. 25,000 per unit. The cost analysis of Rs. 22,000

per unit is as under:

Raw material Rs. 12,000

Wages Rs. 2,000

Factory overhead expenses Rs. 5,000 (60% fixed)

Administrative overhead expenses Rs. 3,000 (80% fixed)

18 Patel Ltd. is expected to have Rs. 25,000 in its bank account on 1st April, 2006.

Prepare a cash budget for three months ending 30th June, 2006:

Month Sales purchases Salary Office expenses Selling expenses

February 50,000 30,000 6,000 9,000 3,000

March 56,000 32,000 6,500 9,500 3,000

April 60,000 35,000 7,000 10,000 3,500

May 80,000 40,000 9,000 11,500 4,500

June 90,000 40,000 9,500 12,500 4,500

Additional information:

(1) 20% sales are on cash basis.

(2) Credit sales to be collected in the next month.

(3) Suppliers are paid in the second month, following the month of purchases.

(4) Workers salary to be paid on the 7th

of each month.

(5) Administrative/office expenses have a time lag of one month.

(6) Selling expenses to be paid in the next month.

(7) Dividend of Rs. 10,000 and bonus to workers of Rs. 15,000 to be paid in May.

(8) Income tax of Rs. 25,000 to be paid in June.

B.V. Patel Institute of Business Management, Computer & Information

Technology, Uka Tarsadia University

Question Bank 030100216: Managerial Accounting

23

19 Prepare a flexible budget at 80% and 100% production capacity from the following

information of ABC Ltd. for three months ending on 31st March, 2010:

Fixed expenses:

Salaries Rs. 63,000

Rent and taxes Rs. 42,000

Depreciation on machinery Rs. 52,500

Office expenses Rs. 66,750

Semi- variable expenses: (at 50% capacity)

plant maintenance Rs. 18,750

indirect labour Rs. 74,250

salesmen‟s salaries and expenses Rs. 21,750

sundry expenses Rs. 19,500

Variable expenses : (at 50% capacity)

Material Rs. 1,80,000

Labour Rs. 1,92,000

Salesmen‟s commission Rs. 28,500

Semi variable expenses remain constant between 40% and 70% capacity, increase by 10%

between 70% and 85% capacity and increase by 15% between 85% and 100% capacity.

Sales at 80% capacity are Rs. 10,20,000 and at 100% capacity Rs. 12,75,000.

20 You are given the following details of Gajanan Ltd., at 50% production level:

Production 200 units

Raw materials Rs. 60 per unit

Wages – 50% of materials

Direct expenses – 50% of wages

Factory overheads – Rs. 30,000 (40% fixed)

Administrative overheads – Rs. 40,000 (50% fixed)

Prepare flexible budget at 60%, 80% and 100% level.

21 A company is expecting to have Rs. 25,000 cash in hand on 1st April 2010 and it

requires you to prepare an estimate of cash position during the three months, April to

June 2010. The following information is supplied to you.

Month Sales Purchases Wages Expenses

February 70,000 40,000 8,000 6,000

B.V. Patel Institute of Business Management, Computer & Information

Technology, Uka Tarsadia University

Question Bank 030100216: Managerial Accounting

24

March 80,000 50,000 8,000 7,000

April 92,000 52,000 9,000 7,000

May 100,000 60,000 10,000

B.V. Patel Institute of Business Management, Computer & Information

Technology, Uka Tarsadia University

Question Bank 030100216: Managerial Accounting

25

Unit-4 Cost Volume profit Analysis

Answer the following. (1 mark)

1. What is Break Even Point?

2. Give the formula of Marginal cost.

3. What is Contribution?

4. From the following data, calculate Break Even Point.

Variable cost per unit Rs. 12, Selling price per unit Rs. 18 and Fixed expenses Rs. 60,000

5. Give full form of PVR.

6. Which formula used to find out sales volume?

7. Give the formula of Margin of safety.

8. Which formula used to find out Break Even Point (in Rs.)?

9. Which formula used to find Fixed Cost?

10. What is Angle of incidence?

Briefly answer the following. (2 marks)

1. Define Marginal costing.

2. What do you mean by Differential cost?

3. If the PVR ratio is 68% and fixed overheads for the period is Rs. 40,000; what would be the

volume of sales to derive a profit of Rs. 20,000.

4. A company produces and sells 100 units per month at Rs. 20. Marginal cost per unit is Rs.

12 and fixed costs are Rs. 300 per month. It is proposed to reduce the selling price by 20%.

Find the additional sales required to earn the same profit as before.

5. The sales and profit during the two periods were as follows:

Period I – sales Rs. 20,00,000 and Profit Rs. 2,00,000

Period II – sales Rs. 30,00,000 and Profit Rs. 4,00,000

Calculate profit volume ratio; sales volume to earn a profit of Rs. 5, 00,000.

6. From the following particulars, calculate the sales required to earn a profit of Rs. 1, 20,000.

Sales Rs. 600,000 Variable cost Rs. 375,000 Fixed cost Rs. 1,80,000

7. Find the profit from the following data :

B.V. Patel Institute of Business Management, Computer & Information

Technology, Uka Tarsadia University

Question Bank 030100216: Managerial Accounting

26

Sales Rs. 80,000 Marginal cost Rs. 60,000 Break-even point 60,000 sales

8. From the following data, calculate the margin of safety.

Sales Rs. 10,00,000 fixed expenses Rs. 3,00,000 profit Rs. 2,00,000

9. You are given the data of Akash Ltd. for the year ended 30-3-07:

Sales 100,000 units of Rs. 10 each

Variable cost per unit Rs. 6

Fixed cost per annum Rs. 300,000

Calculate margin of safety.

10. From the following particulars, find the selling price per unit if Break Even Point is to be

brought down to 9,000 units.

Variable cost per units Rs. 75

Fixed expenses Rs. 270,000

Selling price per unit Rs. 100

11. A company earned a profit of Rs. 30,000 during the year. If the marginal cost and selling

price of a product are Rs. 8 and Rs. 10 per unit respectively, find margin of safety.

12. From the following information of a company, find out PVR, break even point and margin

of safety.

Sales Rs. 500,000

Variable costs Rs. 300,000

Fixed costs Rs. 90,000

13. Sales 10,000 units @ Rs.25 per unit, variable cost Rs. 15 per unit, Fixed cost Rs. 100,000.

Find out the sales for earning a profit of Rs. 50,000.

Answer the following (limit 250 words). (5 marks)

1. Explain the significance of Marginal costing.

2. Explain: Key factor, PV ratio and Margin of safety.

3. The sales turnover and profit during two years were as follows :

Year Sales (Rs.) Profit (Rs.)

2003 1,50,000 20,000

2004 1,70,000 25,000

B.V. Patel Institute of Business Management, Computer & Information

Technology, Uka Tarsadia University

Question Bank 030100216: Managerial Accounting

27

Calculate :

a. P/V Ratio

b. Break –even point

c. The sales required to earn a profit of Rs. 40,000

d. Profit when sales are Rs. 2,50,000

e. Margin of Safety at a profit of Rs. 50,000.

4. The trading results of Raja & Co. for the last two quarters are :

The quarter ended Sales Profit

June Rs. 25,000 Rs. 5,000

September Rs. 37,500 Rs. 10,000

Calculate

a. Profit – Volume Ratio

b. Fixed Costs

c. Break –even Sales Volume

d. Sales to earn a profit Rs. 7,500

e. Profit when sales are Rs. 20,000.

5. Margin of safety ratio is 20%, P/V Ratio is 60%, Fixed cost = Rs.30,000. Find out :

a. B.E.P sales

b. Actual total sales for the year

c. Variable cost for the year

d. Profit for the year

6. A company budgets for production of 1,50,000 units. The variable cost per unit is Rs.

14 and fixed cost is Rs. 2 per unit. The company fixes its selling price to fetch a profit

of 5% of cost.

a. What is the breakeven point?

b. What is the profit volume ratio?

c. If it reduces its selling price by 5% how does the revised selling price affect the break

even and profit volume ratio?

B.V. Patel Institute of Business Management, Computer & Information

Technology, Uka Tarsadia University

Question Bank 030100216: Managerial Accounting

28

d. If a profit increase of 10% is desired more than the budget, what should be the sale at

the reduced price?

7. From the following information relating to a firm, you are required to find out:

(a) Contribution

(b) Break-even point in units

(c) Margin of safety

(d) Profit

Total fixed costs Rs. 4,500

Total variable costs Rs. 7,500

Total sales Rs. 15,000

Units sold 5,000 units

Also calculate the volume of sales to earn profit of Rs. 6,000.

8. Raj corporation Ltd. has prepared the following budget estimates for the year 2010:

Sales units 15,000

Fixed expenses Rs. 34,000

Sales value Rs. 150,000

Variable costs Rs. 6 per unit

You are required to:

a. Find the P/V ratio, break-even point and margin of safety.

b. Calculate the revised P/V ratio, break- even point and margin of safety in each of

the following cases:

i. Decrease of 10% in selling price.

ii. Increase of 10% in variable costs.

iii. Increase of sales volume by 2,000 units

iv. Increase of Rs. 6,000 in fixed costs.

9. The following is the information of Jaydeep Ltd.:

Year Sales Profit

2006-07 Rs. 1,00,000 Rs. 10,000

2007-08 Rs. 1,20,000 Rs. 14,000

Calculate :

B.V. Patel Institute of Business Management, Computer & Information

Technology, Uka Tarsadia University

Question Bank 030100216: Managerial Accounting

29

(1) P/V Ratio

(2) Profit /loss when sales are Rs. 90,000 and 40,000

(3) Sales to earn profit of Rs. 20,000

(4) Break – even point

10. A company manufacturing a single article sells it at Rs. 10 per unit. The variable cost

is Rs. 6 per unit and fixed cost is Rs. 4,000 per annum. Calculate:

(1) The P/V Ratio

(2) The break – even sales

(3) The margin of safety if total sales are Rs. 15,000.

(4) The sales required to earn a profit of Rs. 5,000.

(5) The amount of profit when sale is Rs. 15,000

11. A company had incurred fixed expenses of Rs. 4, 50,000 with sales of Rs. 15,00,000

and earned a profit of Rs. 3,00,000 during the first half year. In the second half, it

suffered a loss of Rs. 1, 50,000.

Calculate:

(a) The profit volume ratio, break- even point and margin of safety for the first half

year.

(b) Expected sales-volume for the second half year assuming that selling price and

fixed expenses remained unchanged during the second half year.

(c) The break- even point and margin of safety for the whole year.

12. From the following data calculate:

(1) Break Even point in units and rupees.

(2) Profit when sales are Rs. 1,00,000 and Rs. 80,000

(3) Sales when it is desired to earn a profit of Rs. 30,000. The data given is as follows:

Fixed cost Rs. 40,000, Variable cost Rs. 2 per unit and Selling price Rs. 10 per unit

13. Lambodhar Enterprises has prepared a budget of 10,000 units. The selling price is

fixed to earn 25% profit on sales. The total fixed cost and variable cost per unit are

Rs. 60,000 and Rs. 24 per unit respectively. Find out:

(1) BEP (units and Rs.)

(2) New BEP (units) and PVR, if S.P. is reduced by 20%.

B.V. Patel Institute of Business Management, Computer & Information

Technology, Uka Tarsadia University

Question Bank 030100216: Managerial Accounting

30

(3) Profit on sales of 6,000 units at S.P. of Rs. 36 per unit

(4) Sales to earn a profit of Rs. 10,000

(5) S.P per unit if BEP is 3000 units