Butterflies, Condors and Risk Limiting · PDF file• price of lower-strike call ... Buy 1...

46

www.OptionsEducation.org Butterflies, Condors and Risk‐Limiting Strategies December 17, 2013 | Joe Burgoyne, OIC 2 Options involve risks and are not suitable for everyone. Prior to buying or selling options, an investor must receive a copy of Characteristics and Risks of Standardized Options. Individuals should not enter into options transactions until they have read and understood the risk disclosure document, Characteristics and Risks of Standardized Options, available by calling 1-888-OPTIONS or by visiting OptionsEducation.org. Copies may be obtained by contacting your broker or The Options Industry Council at One North Wacker Drive, Chicago, IL 60606. In order to simplify the computations, commissions, fees, margin interest and taxes have not been included in the examples used in these materials. These costs will impact the outcome of all stock and options transactions and must be considered prior to entering into any transactions. Investors should consult their tax advisor about any potential tax consequences. Any strategies discussed, including examples using actual securities and price data, are strictly for illustrative and educational purposes only and are not to be construed as an endorsement, recommendation, or solicitation to buy or sell securities. Past performance is not a guarantee of future results. The Options Industry Council

Transcript of Butterflies, Condors and Risk Limiting · PDF file• price of lower-strike call ... Buy 1...

www.OptionsEducation.org

Butterflies, Condors and Risk‐Limiting StrategiesDecember 17, 2013 | Joe Burgoyne, OIC

2

Options involve risks and are not suitable for everyone. Prior to buying or selling options, an investor must receive a copy of Characteristics and Risks of Standardized Options. Individuals should not enter into options transactions until they have read and understood the risk disclosure document, Characteristics and Risks of Standardized Options, available by calling 1-888-OPTIONS or by visiting OptionsEducation.org. Copies may be obtained by contacting your broker or The Options Industry Council at One North WackerDrive, Chicago, IL 60606.

In order to simplify the computations, commissions, fees, margin interest and taxes have not been included in the examples used in these materials. These costs will impact the outcome of all stock and options transactions and must be considered prior to entering into any transactions. Investors should consult their tax advisor about any potential tax consequences.

Any strategies discussed, including examples using actual securities and price data, are strictly for illustrative and educational purposes only and are not to be construed as an endorsement, recommendation, or solicitation to buy or sell securities. Past performance is not a guarantee of future results.

The Options Industry Council

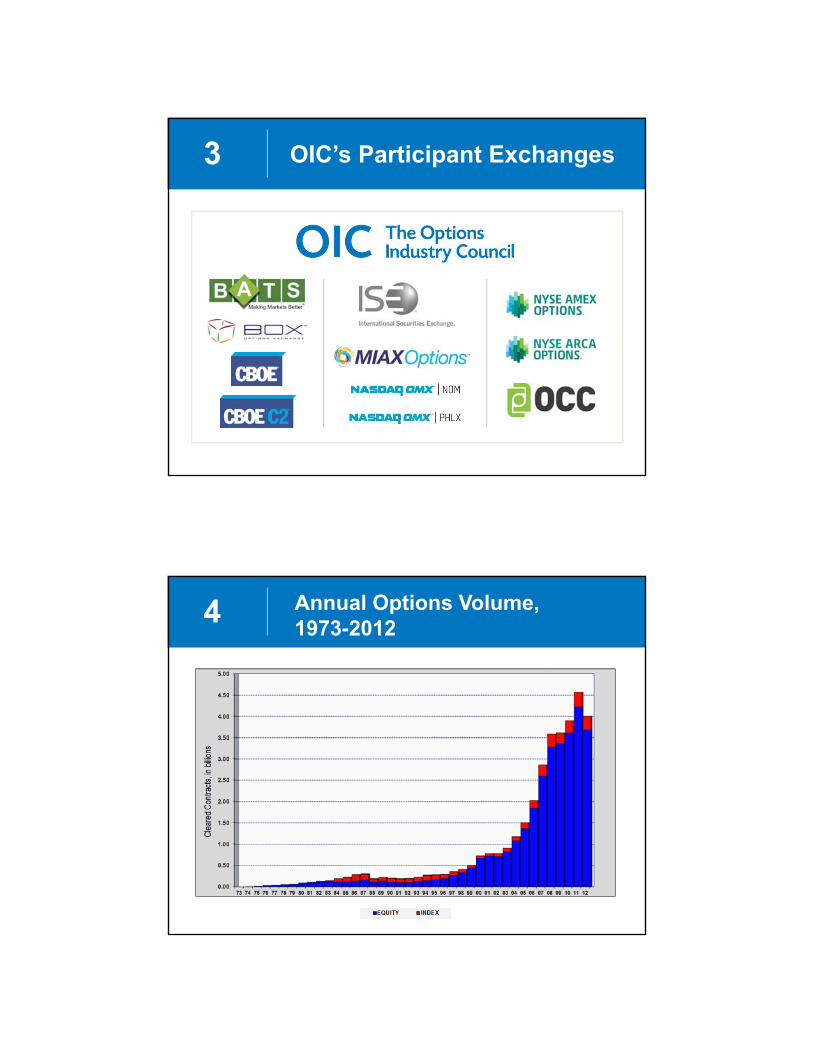

3 OIC’s Participant Exchanges

4 Annual Options Volume, 1973-2012

Cleared

Contracts

5 Slide Presentation

• Spread Basics

• Butterfly Spreads• call butterfly• iron butterfly

• Condor Spreads• call condor• iron condor

Spread Basics

7 Spread Basics

• Spread is a position with both long and short options• same underlying stock or ETF• all calls, all puts, or both calls and puts

• Long and short sides of spread are called “legs”• opening transactions• limits (hedges) risk of the other(s) to some degree

• Spreads can be bullish, bearish or neutral• depends on construction, not whether calls or puts

8 Spread Basics

• Spreads established at net debit or net credit• differential between leg prices

• Debit spread• long leg(s) cost more than received for short• investor paying net debit is “long” the spread

• Credit spread• more received for short leg(s) than paid for long• investor receiving net credit is “short” the spread

9 Spread Basics

• Focus on leg price differential• for pricing spread and/or trading in or out• after established to track profit or loss

• Investor may trade in or out with “spread order”• buy/sell legs simultaneously – as a unit• at net debit or net credit• orders away from market may be disseminated

but regarded as not held

10 Spread Basics

• Spreads can offer investors unique tradeoffs• limited loss potential ↔ limited profit potential• varying degrees• depends on spread construction

• For a given market forecast, spreads may offer• more acceptable risk versus reward ratios• higher percentage profits versus outright purchase

or sale of calls or puts

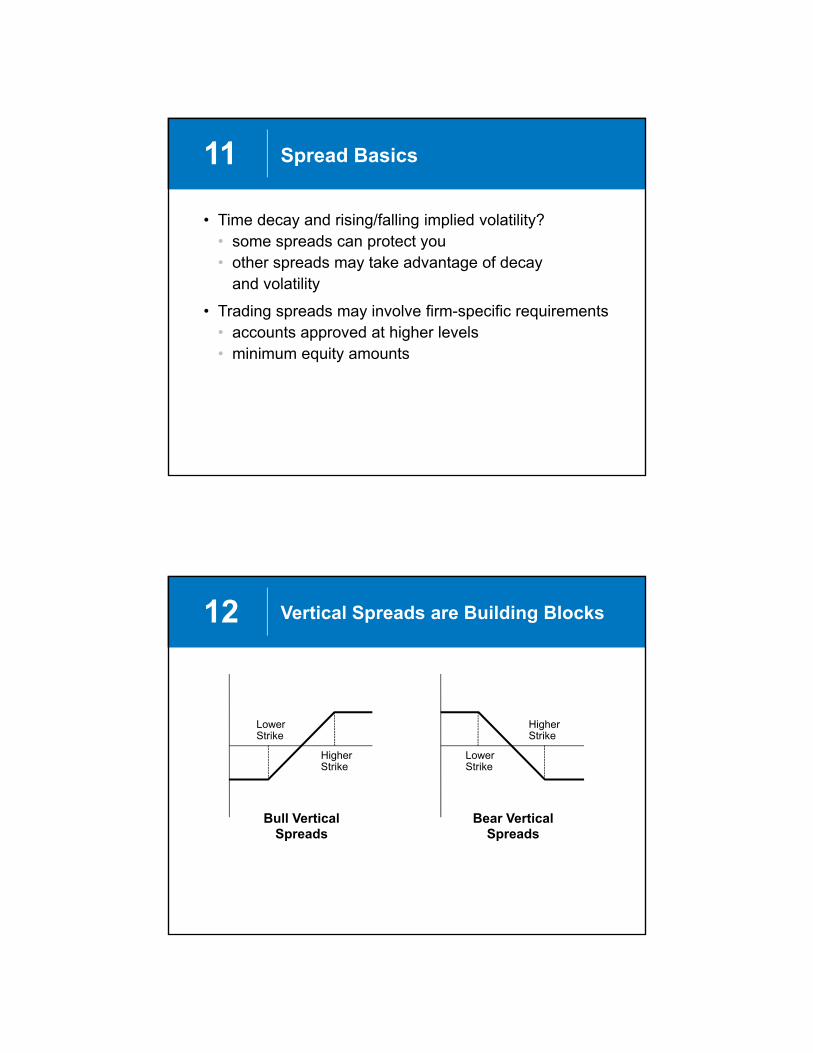

11 Spread Basics

• Time decay and rising/falling implied volatility?• some spreads can protect you• other spreads may take advantage of decay

and volatility

• Trading spreads may involve firm-specific requirements• accounts approved at higher levels• minimum equity amounts

12 Vertical Spreads are Building Blocks

Bull VerticalSpreads

Bear VerticalSpreads

LowerStrike

HigherStrike

LowerStrike

HigherStrike

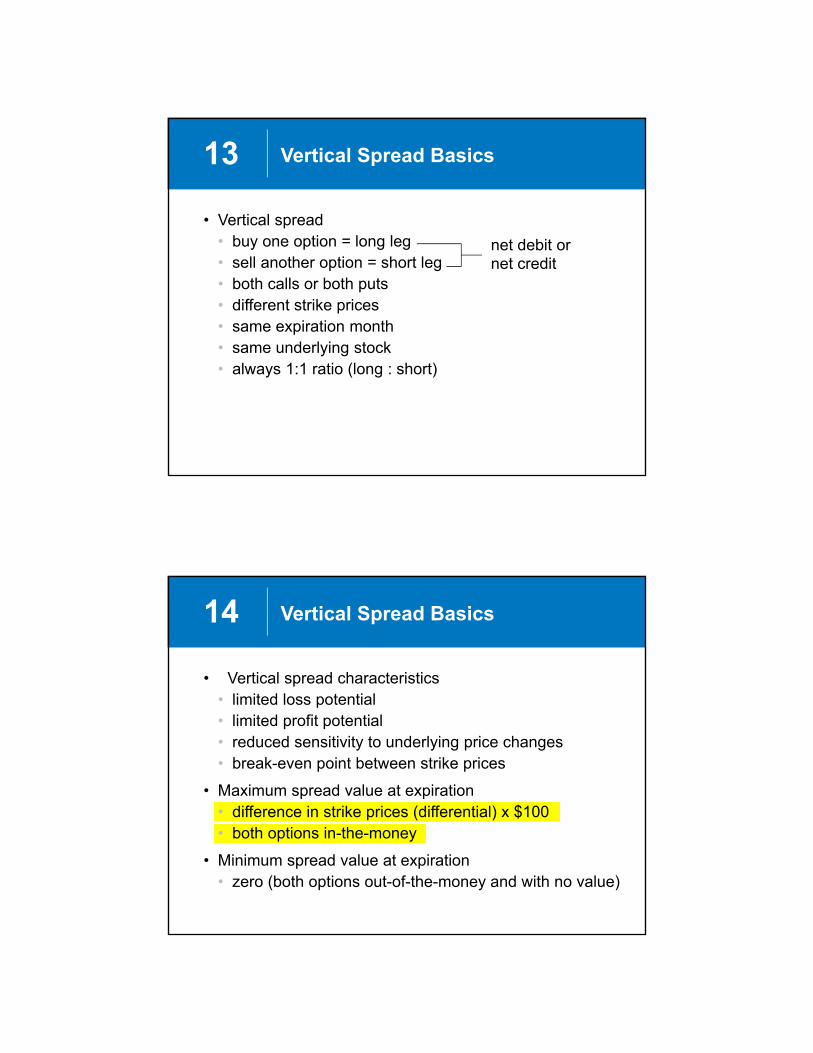

13 Vertical Spread Basics

• Vertical spread• buy one option = long leg• sell another option = short leg• both calls or both puts• different strike prices• same expiration month• same underlying stock• always 1:1 ratio (long : short)

net debit ornet credit

14 Vertical Spread Basics

• Vertical spread characteristics• limited loss potential• limited profit potential• reduced sensitivity to underlying price changes• break-even point between strike prices

• Maximum spread value at expiration• difference in strike prices (differential) x $100• both options in-the-money

• Minimum spread value at expiration• zero (both options out-of-the-money and with no value)

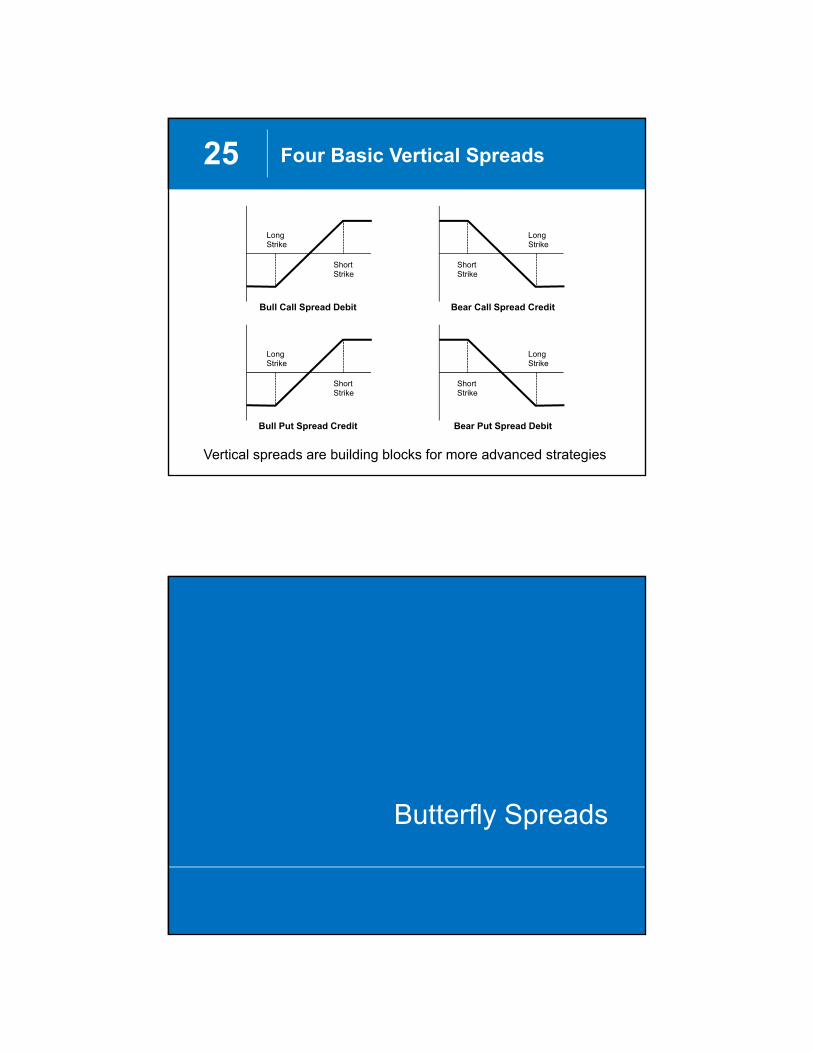

15 Four Basic Vertical Spreads

• Bull call spread• moderately bullish• debit spread• “long call spread”

• Bear call spread• moderately bearish• credit spread• “short call spread”

• Bear put spread• moderately bearish• debit spread• “long put spread”

• Bull put spread• moderately bullish• credit spread• “short put spread”

16 Debit Spread Characteristics

Bull Call Spreads and Bear Put Spreads

• Maximum loss• limited to net debit paid for spread

• Maximum profit potential• difference between strike prices – net debit paid

• Margin• net debit must be paid in full

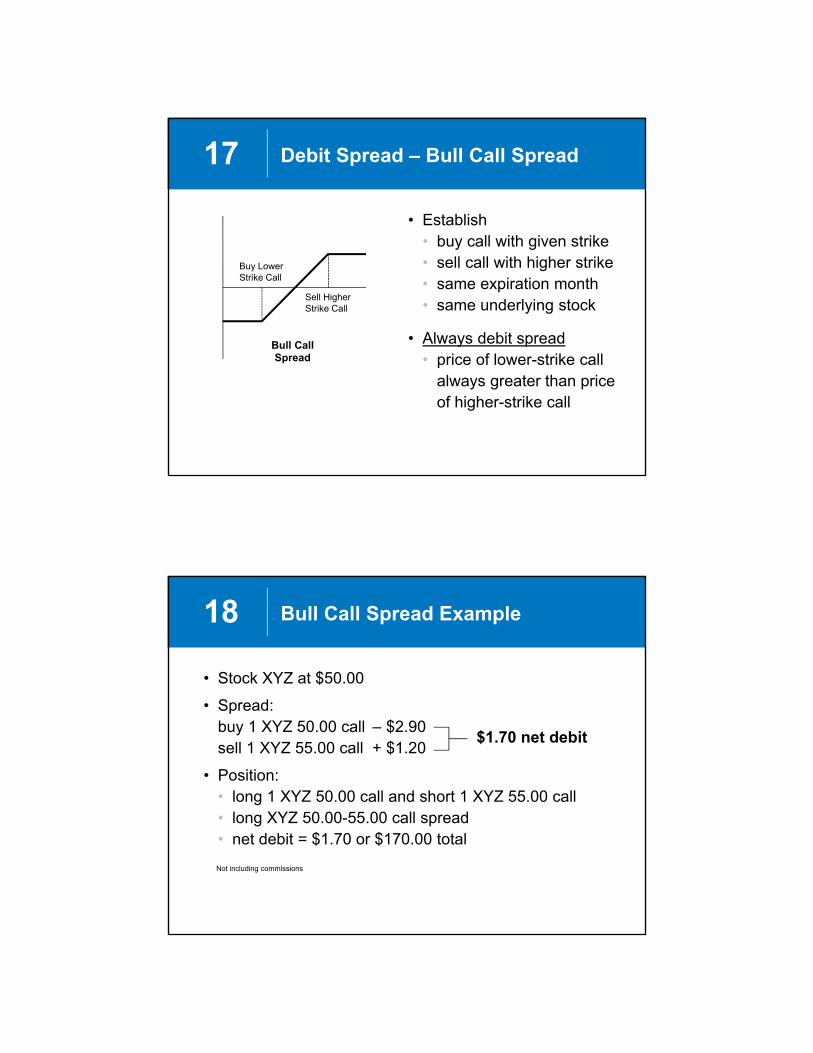

17 Debit Spread – Bull Call Spread

• Establish• buy call with given strike• sell call with higher strike• same expiration month• same underlying stock

• Always debit spread• price of lower-strike call

always greater than price of higher-strike call

Bull CallSpread

Buy Lower Strike Call

Sell Higher Strike Call

18 Bull Call Spread Example

• Stock XYZ at $50.00

• Spread:buy 1 XYZ 50.00 call – $2.90sell 1 XYZ 55.00 call + $1.20

• Position:• long 1 XYZ 50.00 call and short 1 XYZ 55.00 call• long XYZ 50.00-55.00 call spread• net debit = $1.70 or $170.00 total

Not including commissions

$1.70 net debit

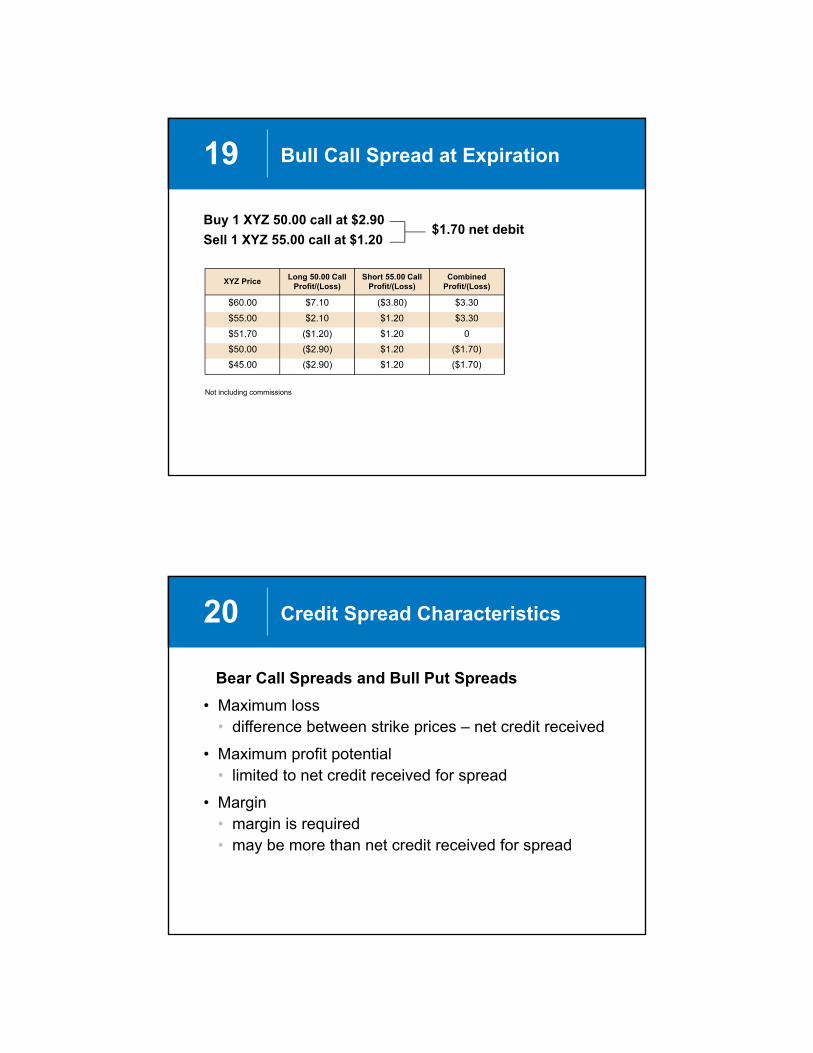

19 Bull Call Spread at Expiration

Buy 1 XYZ 50.00 call at $2.90

Sell 1 XYZ 55.00 call at $1.20$1.70 net debit

Long 50.00 CallProfit/(Loss)

XYZ Price

$60.00

$55.00

$51.70

$7.10

$2.10

($1.20)

($3.80)

$1.20

$1.20

$3.30

$3.30

0

Short 55.00 CallProfit/(Loss)

CombinedProfit/(Loss)

$50.00 ($2.90) $1.20 ($1.70)

$45.00 ($2.90) $1.20 ($1.70)

Not including commissions

20 Credit Spread Characteristics

Bear Call Spreads and Bull Put Spreads

• Maximum loss• difference between strike prices – net credit received

• Maximum profit potential• limited to net credit received for spread

• Margin• margin is required• may be more than net credit received for spread

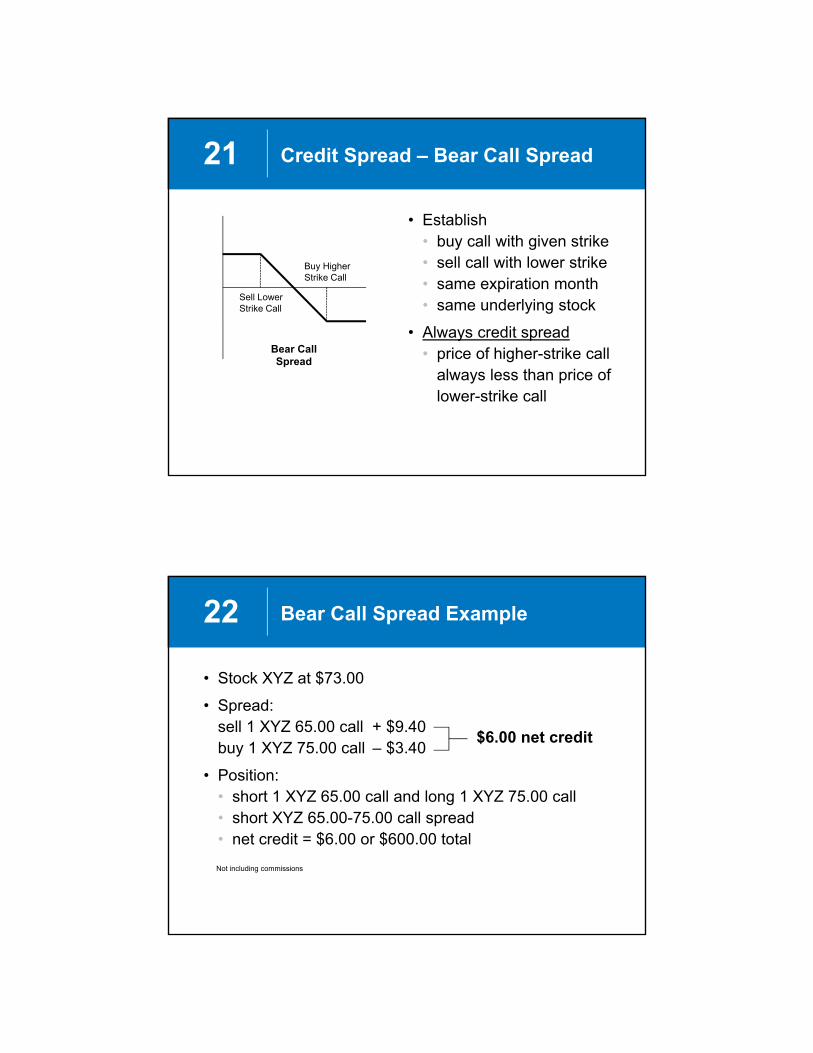

21 Credit Spread – Bear Call Spread

• Establish• buy call with given strike• sell call with lower strike• same expiration month• same underlying stock

• Always credit spread• price of higher-strike call

always less than price of lower-strike call

Bear CallSpread

Buy Higher Strike Call

Sell Lower Strike Call

22 Bear Call Spread Example

• Stock XYZ at $73.00

• Spread:sell 1 XYZ 65.00 call + $9.40buy 1 XYZ 75.00 call – $3.40

• Position:• short 1 XYZ 65.00 call and long 1 XYZ 75.00 call• short XYZ 65.00-75.00 call spread• net credit = $6.00 or $600.00 total

Not including commissions

$6.00 net credit

23 Bear Call Spread at Expiration

Sell 1 XYZ 65.00 call at $9.40

Buy 1 XYZ 75.00 call at $3.40$6.00 net credit

Long 75.00 CallProfit/(Loss)

XYZ Price

$80.00

$75.00

$71.00

$1.60

($3.40)

($3.40)

($5.60)

($0.60)

$3.40

($4.00)

($4.00)

0

Short 65.00 CallProfit/(Loss)

CombinedProfit/(Loss)

$70.00 ($3.40) $4.40 $1.00

$65.00

$60.00

($3.40)

($3.40)

$9.40

$9.40

$6.00

$6.00

Not including commissions

24 Time Decay and Volatility

For All Vertical SpreadsBull or Bear ↔ Debit or Credit

• Effect of time decay depends on stock price versus strikes• between strikes → effect generally minimal• closer to long strike → losses should increase at faster rate

as time passes• closer to short strike → profits should increase at faster rate

as time passes

• Effect of changing volatility depends on • whether one or both legs are in-the-money• amount of time until expiration

25 Four Basic Vertical Spreads

Bull Call Spread Debit Bear Call Spread Credit

LongStrike

ShortStrike

ShortStrike

LongStrike

Bull Put Spread Credit Bear Put Spread Debit

LongStrike

ShortStrike

ShortStrike

LongStrike

Vertical spreads are building blocks for more advanced strategies

Butterfly Spreads

27 Long Butterfly Basics

• Long butterfly spread – to establish• buy 1 option with lowest strike• sell 2 options with middle strike• buy 1 option with highest strike

• All calls or all puts• same underlying stock• same expiration month• same strike price increment• always 1:2:1 ratio (long to short to long)

3 option seriesAlways net debit

28 Long Butterfly Basics

• Investor’s position• long 1 lowest strike → wing• short 2 middle strike → body• long 1 highest strike → wing

• Investor is long butterfly• has purchased butterfly for net debit

• Composition = two vertical spreads• 1 bull spread and 1 bear spread• 1 debit spread and 1 credit spread

• Profit potential and loss potential both limited

29 Long Butterfly Basics

• Neutral strategy

• Expectations for underlying• trade in a range before expiration• stabilize around middle (short) strike at expiration

• Motivations• profit from time decay• profit from decreasing implied volatility

• Investor wants to profit from stable underlying market• unwilling to accept risk of short straddle

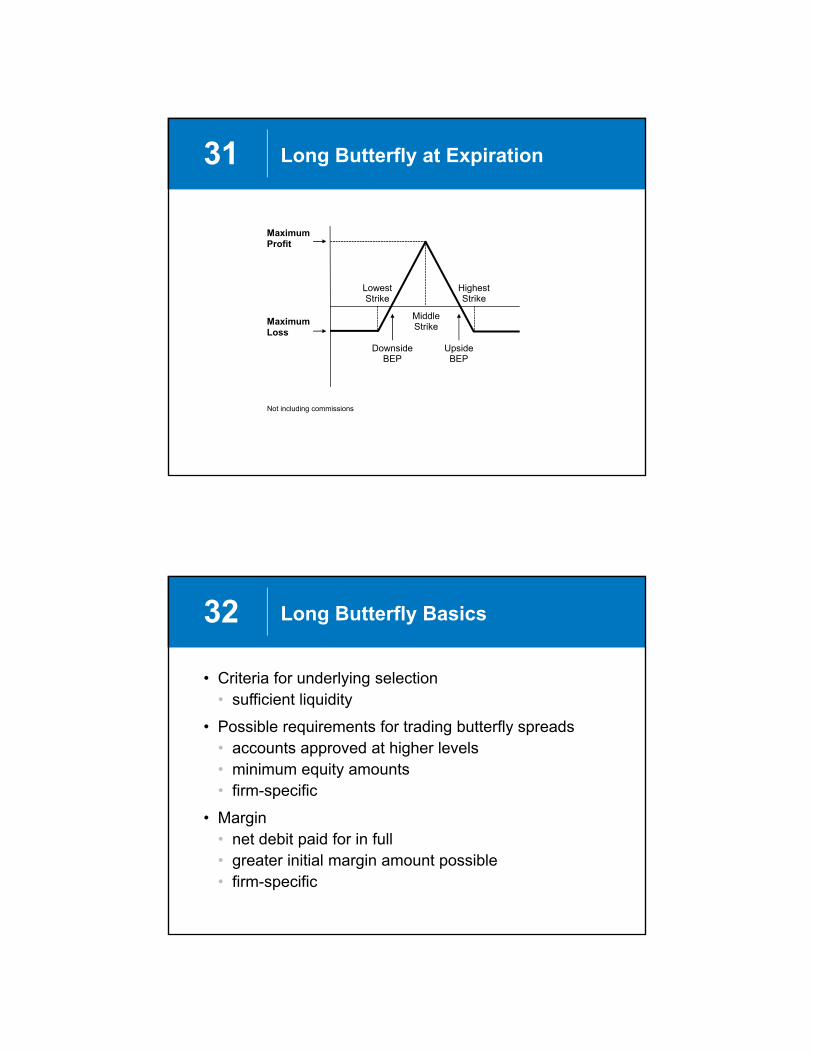

30 Long Butterfly at Expiration

• Maximum profit limited• strike difference – net debit paid for spread• if underlying closes at middle (short) strike

• Maximum loss limited• net debit paid for spread• if underlying at or below lowest strike• if underlying at or above highest strike

• Break-even points• downside → lowest strike + net debit paid• upside → highest strike – net debit paid

Not including commissions

31 Long Butterfly at Expiration

Not including commissions

Maximum Profit

DownsideBEP

Maximum Loss

UpsideBEP

LowestStrike

MiddleStrike

HighestStrike

32 Long Butterfly Basics

• Criteria for underlying selection• sufficient liquidity

• Possible requirements for trading butterfly spreads• accounts approved at higher levels• minimum equity amounts• firm-specific

• Margin• net debit paid for in full• greater initial margin amount possible• firm-specific

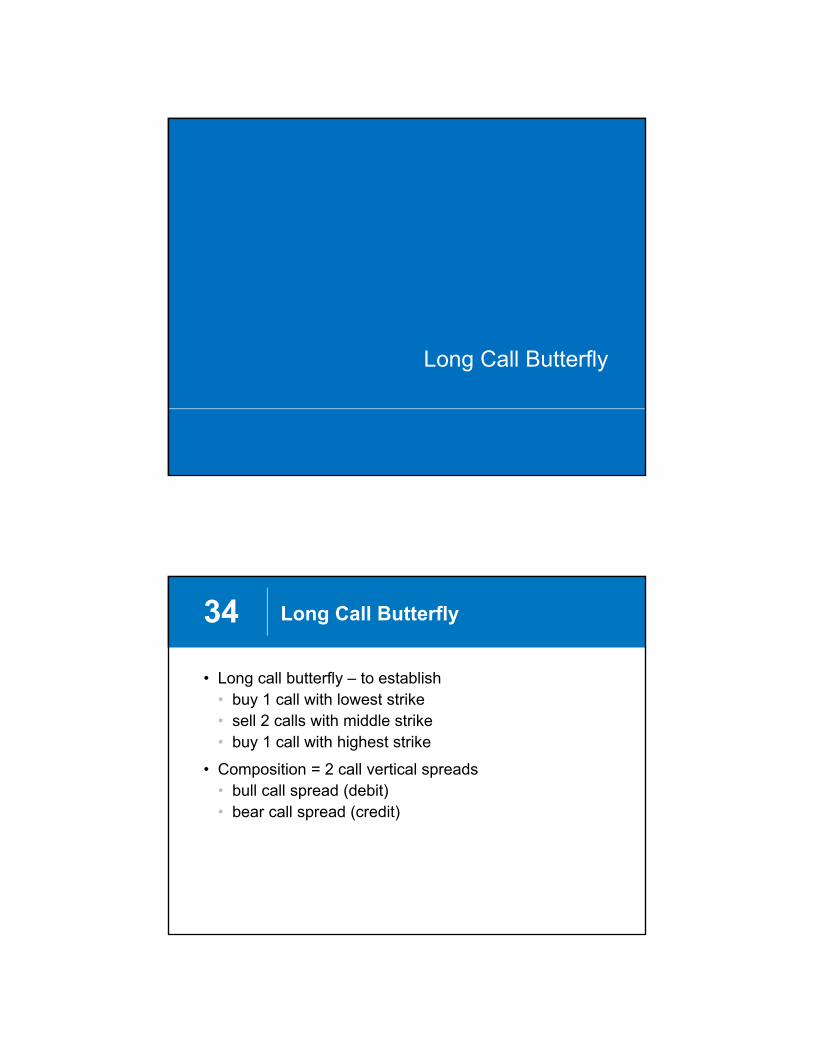

Long Call Butterfly

34 Long Call Butterfly

• Long call butterfly – to establish• buy 1 call with lowest strike• sell 2 calls with middle strike• buy 1 call with highest strike

• Composition = 2 call vertical spreads• bull call spread (debit)• bear call spread (credit)

35 Long Call Butterfly

Long Call Butterfly

Long1 Call

Short2 Calls

Long1 Call

Bull Call

LongCall

ShortCall

Bear Call

ShortCall

LongCall

36

XYZ 55.00 call

XYZ 60.00 call

XYZ 65.00 call

XYZ 70.00 call

XYZ 75.00 call

Available 60-day calls

$7.30

$4.10

$2.00

$0.85

$0.30

Long Call Butterfly Example

• Stock XYZ currently at $61.00

• Spread:Buy 1 XYZ 60.00 call – $4.10Sell 2 XYZ 65.00 calls + $2.00Buy 1 XYZ 70.00 call – $0.85

net cost: – $0.95 debit

• XYZ 60.00-65.00-70.00 call butterfly purchased for $0.95 or $95.00 total

Not including commissions

37 Long Call Butterfly Example

Buy 1 XYZ 60.00 call at $4.10Sell 2 XYZ 65.00 calls at $2.00Buy 1 XYZ 70.00 call at $0.85

• Downside break-even point• lowest strike + net debit paid• $60.00 + $0.95 = $60.95

• Upside break-even point• highest strike – net debit

paid• $70.00 – $0.95 = $69.05

$0.95 net debit

Not including commissions

38 Long Call Butterfly Example

Buy 1 XYZ 60.00 call at $4.10Sell 2 XYZ 65.00 calls at $2.00Buy 1 XYZ 70.00 call at $0.85

• Maximum profit• strike difference – net debit paid• $5.00 – $0.95 = $4.05, or $405.00 total

• Maximum loss• net debit paid• $0.95, or $95.00 total

$0.95 net debit

Not including commissions

39 Long Call Butterfly Example

Buy 1 XYZ 60.00 call at $4.10Sell 2 XYZ 65.00 calls at $2.00Buy 1 XYZ 70.00 call at $0.85

Long 160.00 Call

Profit/(Loss)XYZ Price

$70.00

$69.05

$67.00

$5.90

$4.95

$2.90

($6.00)

($4.10)

0

($0.85)

($0.85)

($0.85)

($0.95)

0

$2.05

$4.05

$2.05

0

($0.95)

Short 265.00 Calls

Profit/(Loss)

Long 170.00 Call

Profit/(Loss)

$65.00 $0.90 $4.00 ($0.85)

$63.00

$60.95

$60.00

($1.10)

($3.15)

($4.10)

$4.00

$4.00

$4.00

($0.85)

($0.85)

($0.85)

Not including commissions

CombinedProfit/(Loss)

$0.95 net debit

40

Not including commissions

Max Profit$405.00

↓BEP$60.95

Max Loss$95.00

↑BEP$69.05

6065

70

Long Call Butterfly Example

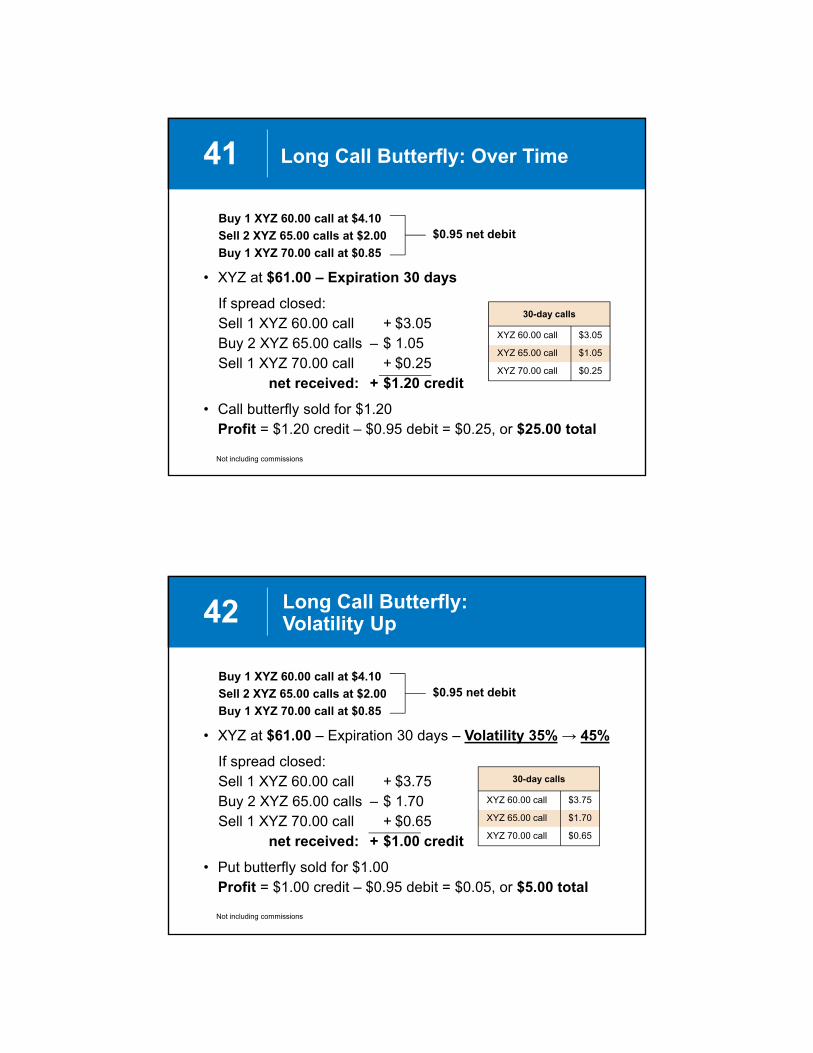

41 Long Call Butterfly: Over Time

Buy 1 XYZ 60.00 call at $4.10

Sell 2 XYZ 65.00 calls at $2.00

Buy 1 XYZ 70.00 call at $0.85

• XYZ at $61.00 – Expiration 30 days

If spread closed:Sell 1 XYZ 60.00 call + $3.05Buy 2 XYZ 65.00 calls – $ 1.05Sell 1 XYZ 70.00 call + $0.25

net received: + $1.20 credit

• Call butterfly sold for $1.20Profit = $1.20 credit – $0.95 debit = $0.25, or $25.00 total

Not including commissions

XYZ 60.00 call

XYZ 65.00 call

XYZ 70.00 call

30-day calls

$3.05

$1.05

$0.25

$0.95 net debit

42

Buy 1 XYZ 60.00 call at $4.10

Sell 2 XYZ 65.00 calls at $2.00

Buy 1 XYZ 70.00 call at $0.85

• XYZ at $61.00 – Expiration 30 days – Volatility 35% → 45%

If spread closed:Sell 1 XYZ 60.00 call + $3.75Buy 2 XYZ 65.00 calls – $ 1.70Sell 1 XYZ 70.00 call + $0.65

net received: + $1.00 credit

• Put butterfly sold for $1.00Profit = $1.00 credit – $0.95 debit = $0.05, or $5.00 total

Not including commissions

XYZ 60.00 call

XYZ 65.00 call

XYZ 70.00 call

30-day calls

$3.75

$1.70

$0.65

Long Call Butterfly:Volatility Up

$0.95 net debit

43

Buy 1 XYZ 60.00 call at $4.10

Sell 2 XYZ 65.00 calls at $2.00

Buy 1 XYZ 70.00 call at $0.85

• XYZ at $61.00 – Expiration 30 days – Volatility 35% → 25%

If spread closed:Sell 1 XYZ 60.00 call + $2.35Buy 2 XYZ 65.00 calls – $ 0.50Sell 1 XYZ 70.00 call + $0.05

net received: + $1.40 credit

• Put butterfly sold for $1.40Profit = $1.40 credit – $0.95 debit = $0.45, or $45.00 total

Not including commissions

XYZ 60.00 call

XYZ 65.00 call

XYZ 70.00 call

30-day calls

$2.35

$0.50

$0.05

Long Call Butterfly:Volatility Down

$0.95 net debit

44 Early Assignment for Dividend

• XYZ has risen• short calls now in-the-money

• Early assignment possible before dividend• on or just before ex-dividend date

• You might expect early assignment when• expiration is relatively near• dividend greater than short calls’ time value

• Action• to avoid assignment, close the spread

45 Butterflies in General

• Call or put butterflies• behavior and profit/loss profiles much the same• choose suitable risk/reward that current

premiums offer

• Unless all options expiring worthless, position will generally need to be totally or partially closed before expiration

• Since position is combination of 2 vertical spreads, you might consider exiting profitable spread before expiration and let unprofitable spread expire.

Iron Butterfly

47 Iron Butterfly

• Iron butterfly – to establish• buy 1 put with lowest strike• sell 1 put with middle strike• sell 1 call with middle strike• buy 1 call with highest strike

• Composition – 2 ways to look at it• bull put spread (credit) + bear call spread (credit)• short straddle (credit) + long strangle (debit)

• Spread always established for net credit• margin requirement (firm specific)

48 Iron Butterfly

Iron Butterfly

Long1 Put

Short 1 PutShort 1 Call

Long1 Call

Bull Put

LongPut

ShortPut

Bear Call

ShortCall

LongCall

49

XYZ 60.00 put

XYZ 65.00 put

XYZ 70.00 put

XYZ 70.00 call

XYZ 75.00 call

XYZ 80.00 call

60-day options

$0.60

$1.75

$3.80

$4.10

$2.20

$1.05

Iron Butterfly Example

• Stock XYZ currently at $70.00

• Spread:Buy 1 XYZ 60.00 put – $0.60Sell 1 XYZ 70.00 put + $3.80Sell 1 XYZ 70.00 call + $4.10Buy 1 XYZ 80.00 call – $1.05

net received: + $6.25 credit

• XYZ 60.00-70.00-80.00 iron butterfly established for $6.25 credit, or $625.00 total

Not including commissions

50 Iron Butterfly Example

Buy 1 XYZ 60.00 put at $0.60 Sell 1 XYZ 70.00 put at $3.80

Sell 1 XYZ 70.00 call at $4.10 Buy 1 XYZ 80.00 call at $1.05

• Downside break-even point• middle strike – net credit received• $70.00 – $6.25 = $63.75

• Upside break-even point• middle strike + net credit received• $70.00 + $6.25 = $76.25

$6.25net credit

Not including commissions

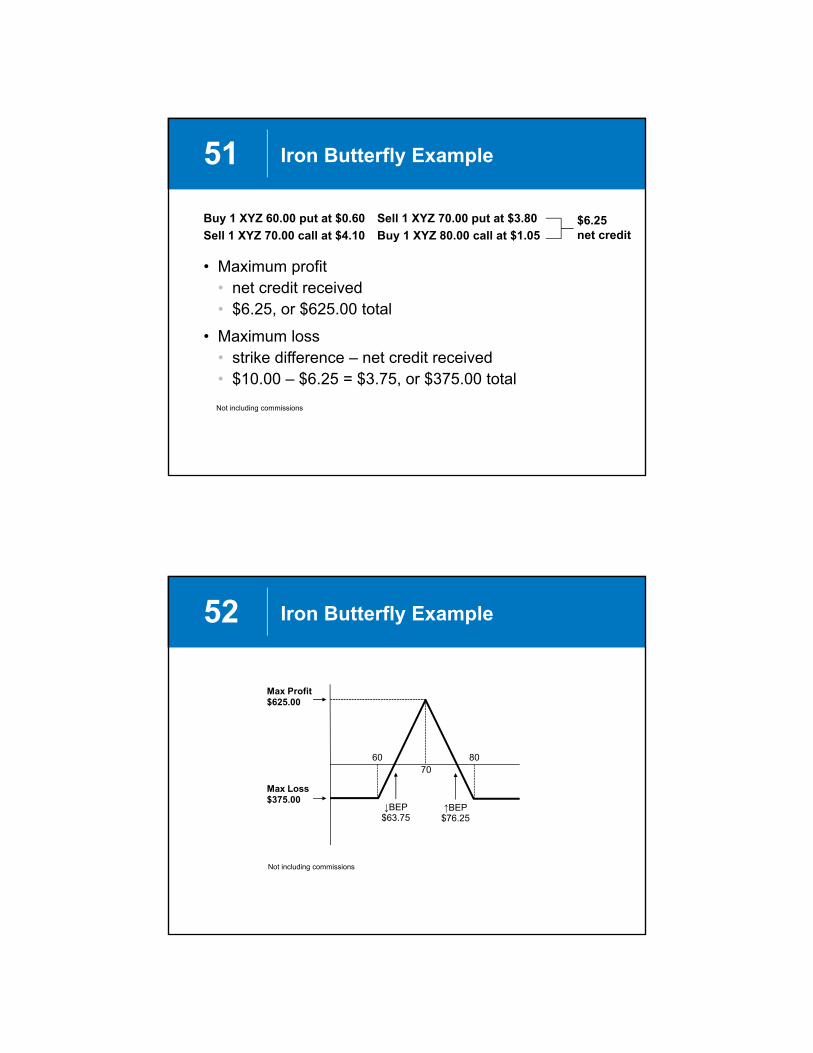

51 Iron Butterfly Example

Buy 1 XYZ 60.00 put at $0.60 Sell 1 XYZ 70.00 put at $3.80

Sell 1 XYZ 70.00 call at $4.10 Buy 1 XYZ 80.00 call at $1.05

• Maximum profit• net credit received• $6.25, or $625.00 total

• Maximum loss• strike difference – net credit received• $10.00 – $6.25 = $3.75, or $375.00 total

$6.25net credit

Not including commissions

52

Not including commissions

Max Profit$625.00

↓BEP$63.75

Max Loss$375.00

↑BEP$76.25

6070

80

Iron Butterfly Example

53 Iron Butterfly: Over Time

Buy 1 XYZ 60.00 put at $0.60 Sell 1 XYZ 70.00 put at $3.80

Sell 1 XYZ 70.00 call at $4.10 Buy 1 XYZ 80.00 call at $1.05

• XYZ at $70.00 – Expiration 30 days

If spread closed:Sell 1 XYZ 60.00 put + $0.15Buy 1 XYZ 70.00 put – $2.70Buy 1 XYZ 70.00 call – $2.85Sell 1 XYZ 80.00 call + $0.35

net paid: – $5.05 debit

• Iron butterfly closed for $5.05 debitProfit = $6.25 credit – $5.05 debit = $1.20, or $120.00 total

Not including commissions

XYZ 60.00 put

XYZ 70.00 put

XYZ 70.00 call

XYZ 80.00 call

30-day options

$0.15

$2.70

$2.85

$0.35

$6.25net credit

54 Iron Butterfly: Volatility Up

Buy 1 XYZ 60.00 put at $0.60 Sell 1 XYZ 70.00 put at $3.80

Sell 1 XYZ 70.00 call at $4.10 Buy 1 XYZ 80.00 call at $1.05

• XYZ at $70.00 – Expiration 30 days – Volatility 35% → 45%

If spread closed:Sell 1 XYZ 60.00 put + $0.45Buy 1 XYZ 70.00 put – $3.50Buy 1 XYZ 70.00 call – $3.70Sell 1 XYZ 80.00 call + $0.80

net paid: – $5.95 debit

• Iron butterfly closed for $5.95 debitProfit = $6.25 credit – $5.95 debit = $0.30, or $30.00 total

Not including commissions

XYZ 60.00 put

XYZ 70.00 put

XYZ 70.00 call

XYZ 80.00 call

30-day options

$0.45

$3.50

$3.70

$0.80

$6.25net credit

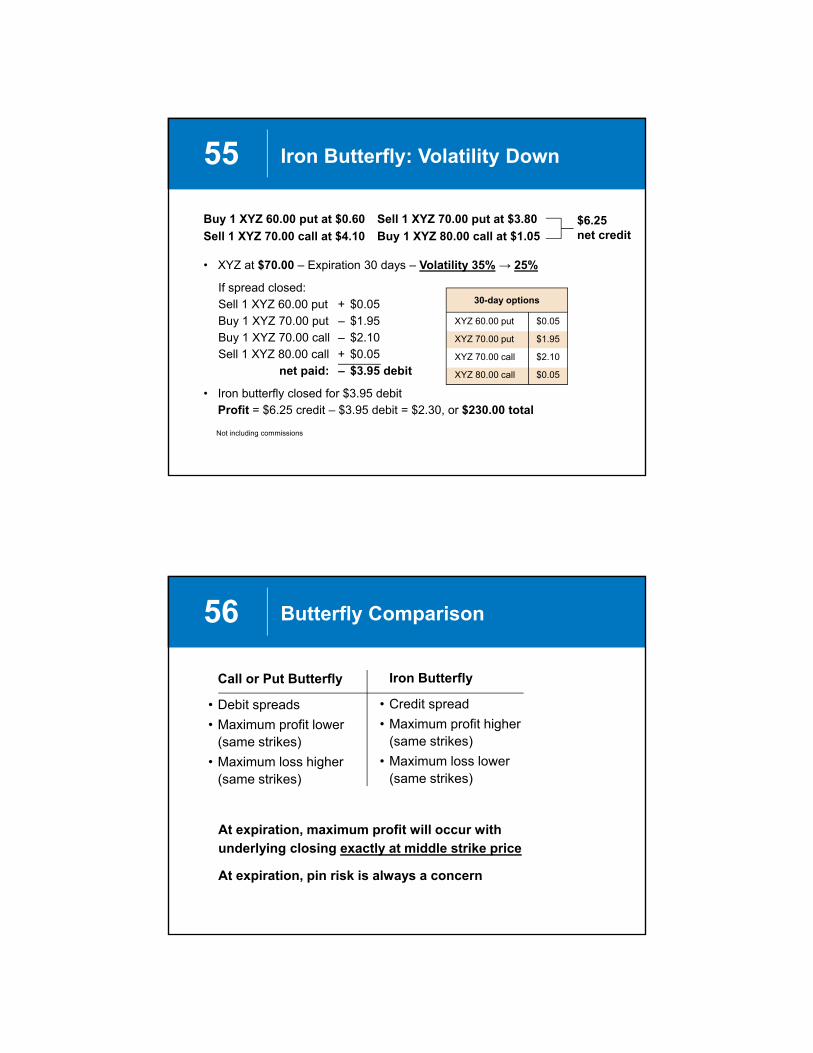

55 Iron Butterfly: Volatility Down

Buy 1 XYZ 60.00 put at $0.60 Sell 1 XYZ 70.00 put at $3.80

Sell 1 XYZ 70.00 call at $4.10 Buy 1 XYZ 80.00 call at $1.05

• XYZ at $70.00 – Expiration 30 days – Volatility 35% → 25%

If spread closed:Sell 1 XYZ 60.00 put + $0.05Buy 1 XYZ 70.00 put – $1.95Buy 1 XYZ 70.00 call – $2.10Sell 1 XYZ 80.00 call + $0.05

net paid: – $3.95 debit

• Iron butterfly closed for $3.95 debitProfit = $6.25 credit – $3.95 debit = $2.30, or $230.00 total

Not including commissions

XYZ 60.00 put

XYZ 70.00 put

XYZ 70.00 call

XYZ 80.00 call

30-day options

$0.05

$1.95

$2.10

$0.05

$6.25net credit

56 Butterfly Comparison

At expiration, maximum profit will occur with

underlying closing exactly at middle strike price

At expiration, pin risk is always a concern

Call or Put Butterfly

• Debit spreads

• Maximum profit lower (same strikes)

• Maximum loss higher (same strikes)

Iron Butterfly

• Credit spread

• Maximum profit higher (same strikes)

• Maximum loss lower (same strikes)

Condor Spreads

58 Long Condor Basics

• Long condor spread – to establish• buy 1 option with lowest strike• sell 1 option with higher strike• sell 1 option with higher strike• buy 1 option with highest strike

• All calls or all puts• same underlying stock• same expiration month• same strike price increment• always 1:1:1:1 ratio (long to short to short to long)

Four strikesAlways net debit

59 Long Condor Basics

• Investor’s position• long 1 lowest strike → wing• short 1 higher strike → body• short 1 higher strike → body• long 1 highest strike → wing

• Investor is long condor• has purchased condor for net debit

• Composition = two vertical spreads• 1 bull spread and 1 bear spread• 1 debit spread and 1 credit spread

• Profit potential and loss potential both limited

60 Long Condor Basics

• Neutral strategy

• Expectations for underlying• trade in a range before expiration• stabilize and close within a range at expiration

• Motivations• profit from time decay• profit from decreasing implied volatility

• Investor wants to profit from stable underlying market• unwilling to accept risk of short strangle

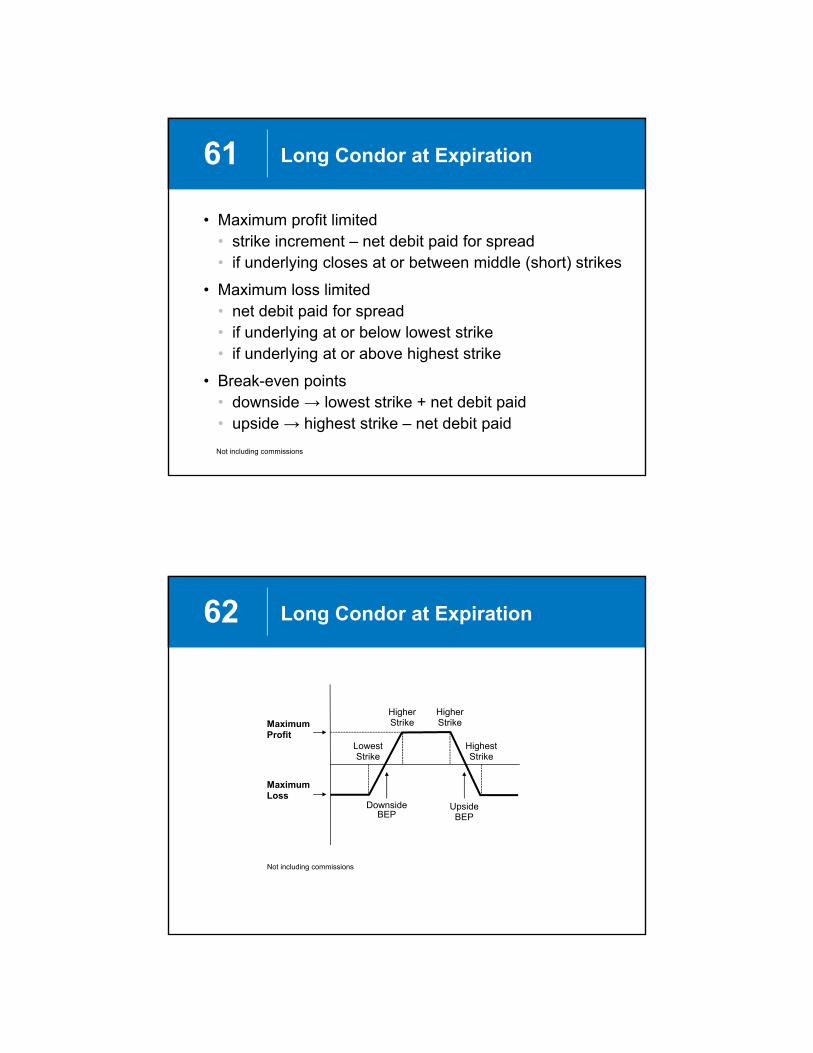

61 Long Condor at Expiration

• Maximum profit limited• strike increment – net debit paid for spread• if underlying closes at or between middle (short) strikes

• Maximum loss limited• net debit paid for spread• if underlying at or below lowest strike• if underlying at or above highest strike

• Break-even points• downside → lowest strike + net debit paid• upside → highest strike – net debit paid

Not including commissions

62 Long Condor at Expiration

Not including commissions

Maximum Profit

DownsideBEP

Maximum Loss

UpsideBEP

LowestStrike

HighestStrike

HigherStrike

HigherStrike

63 Long Condor Basics

• Criteria for underlying selection• higher priced stocks/ETFs → more available strikes• sufficient liquidity

• Possible requirements for trading condor spreads• accounts approved at higher levels• minimum equity amounts• firm-specific

• Margin• net debit paid for in full• greater initial margin amount possible• firm-specific

Long Call Condor

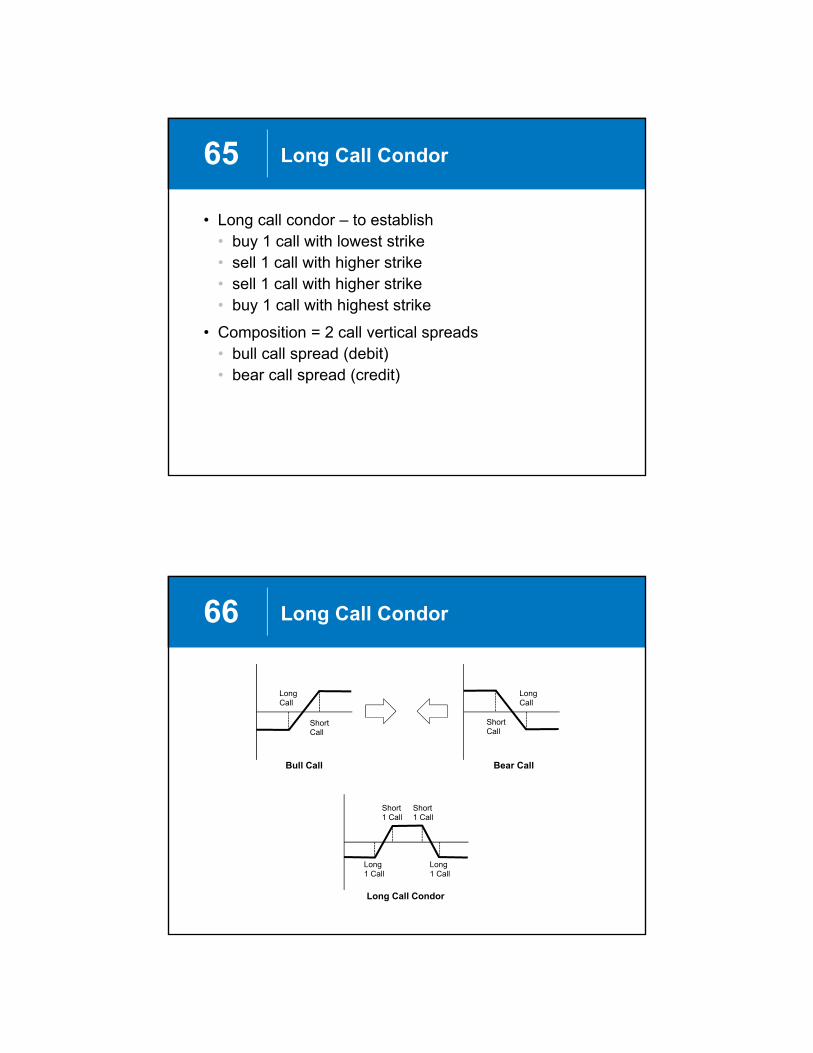

65 Long Call Condor

• Long call condor – to establish• buy 1 call with lowest strike• sell 1 call with higher strike• sell 1 call with higher strike• buy 1 call with highest strike

• Composition = 2 call vertical spreads• bull call spread (debit)• bear call spread (credit)

66 Long Call Condor

Long Call Condor

Long1 Call

Long1 Call

Short1 Call

Short1 Call

Bull Call

LongCall

ShortCall

Bear Call

ShortCall

LongCall

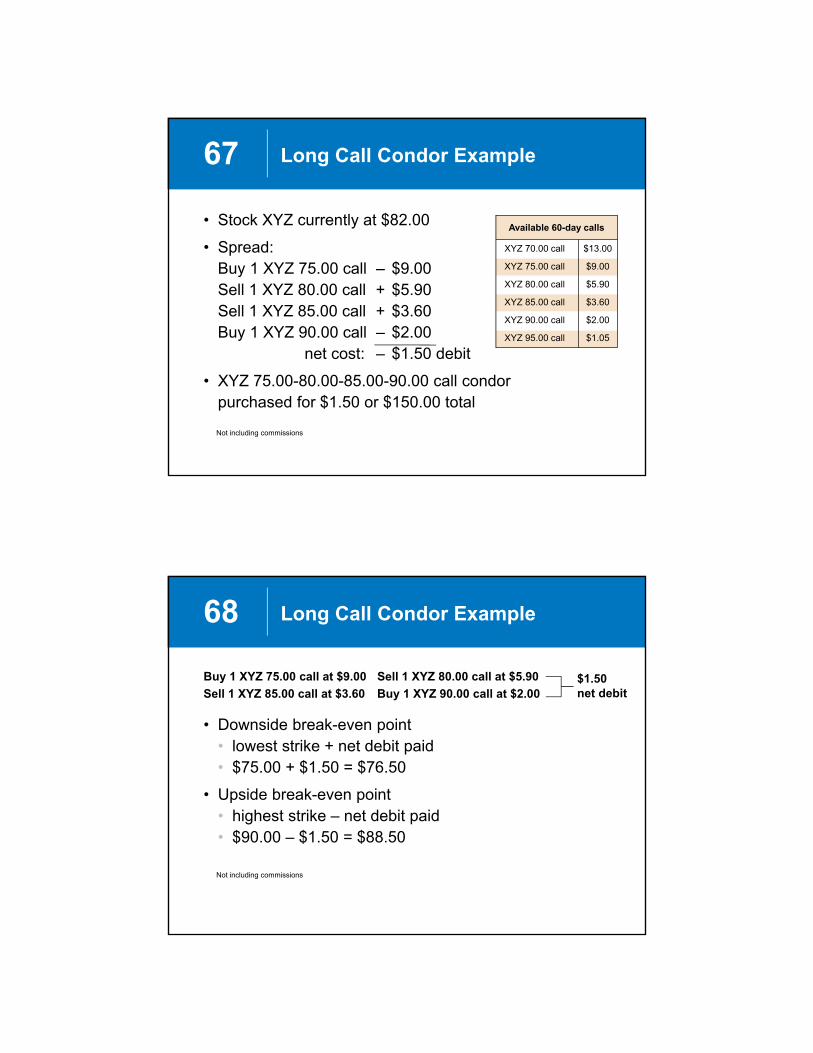

67

XYZ 70.00 call

XYZ 75.00 call

XYZ 80.00 call

XYZ 85.00 call

XYZ 90.00 call

XYZ 95.00 call

Available 60-day calls

$13.00

$9.00

$5.90

$3.60

$2.00

$1.05

Long Call Condor Example

• Stock XYZ currently at $82.00

• Spread:Buy 1 XYZ 75.00 call – $9.00Sell 1 XYZ 80.00 call + $5.90Sell 1 XYZ 85.00 call + $3.60Buy 1 XYZ 90.00 call – $2.00

net cost: – $1.50 debit

• XYZ 75.00-80.00-85.00-90.00 call condor purchased for $1.50 or $150.00 total

Not including commissions

68 Long Call Condor Example

Buy 1 XYZ 75.00 call at $9.00 Sell 1 XYZ 80.00 call at $5.90

Sell 1 XYZ 85.00 call at $3.60 Buy 1 XYZ 90.00 call at $2.00

• Downside break-even point• lowest strike + net debit paid• $75.00 + $1.50 = $76.50

• Upside break-even point• highest strike – net debit paid• $90.00 – $1.50 = $88.50

Not including commissions

$1.50net debit

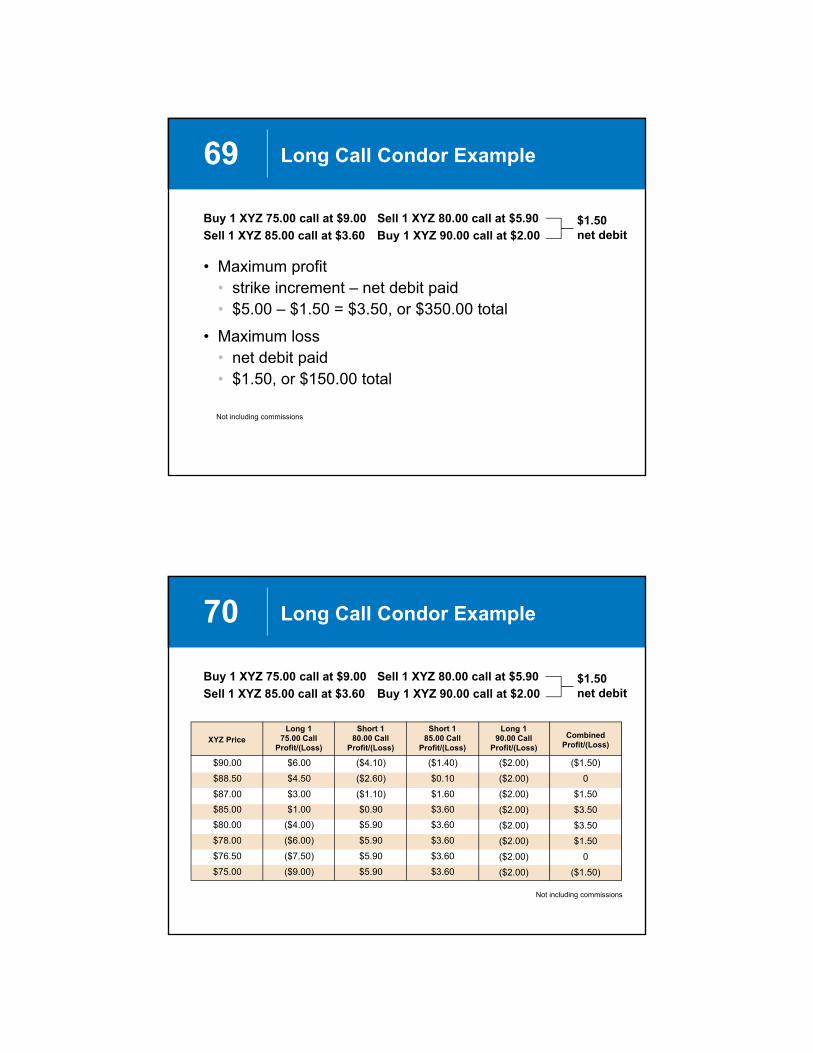

69 Long Call Condor Example

Buy 1 XYZ 75.00 call at $9.00 Sell 1 XYZ 80.00 call at $5.90

Sell 1 XYZ 85.00 call at $3.60 Buy 1 XYZ 90.00 call at $2.00

• Maximum profit• strike increment – net debit paid• $5.00 – $1.50 = $3.50, or $350.00 total

• Maximum loss• net debit paid• $1.50, or $150.00 total

Not including commissions

$1.50net debit

70 Long Call Condor Example

Buy 1 XYZ 75.00 call at $9.00 Sell 1 XYZ 80.00 call at $5.90

Sell 1 XYZ 85.00 call at $3.60 Buy 1 XYZ 90.00 call at $2.00

Long 175.00 Call

Profit/(Loss)XYZ Price

$90.00

$88.50

$87.00

$6.00

$4.50

$3.00

($4.10)

($2.60)

($1.10)

($1.40)

$0.10

$1.60

($2.00)

($2.00)

($2.00)

($2.00)

($2.00)

($2.00)

($2.00)

($2.00)

Short 180.00 Call

Profit/(Loss)

Short 185.00 Call

Profit/(Loss)

$85.00 $1.00 $0.90 $3.60

$80.00

$78.00

$76.50

$75.00

($4.00)

($6.00)

($7.50)

($9.00)

$5.90

$5.90

$5.90

$5.90

$3.60

$3.60

$3.60

$3.60

Not including commissions

Long 190.00 Call

Profit/(Loss)

($1.50)

0

$1.50

$3.50

$3.50

$1.50

0

($1.50)

CombinedProfit/(Loss)

$1.50net debit

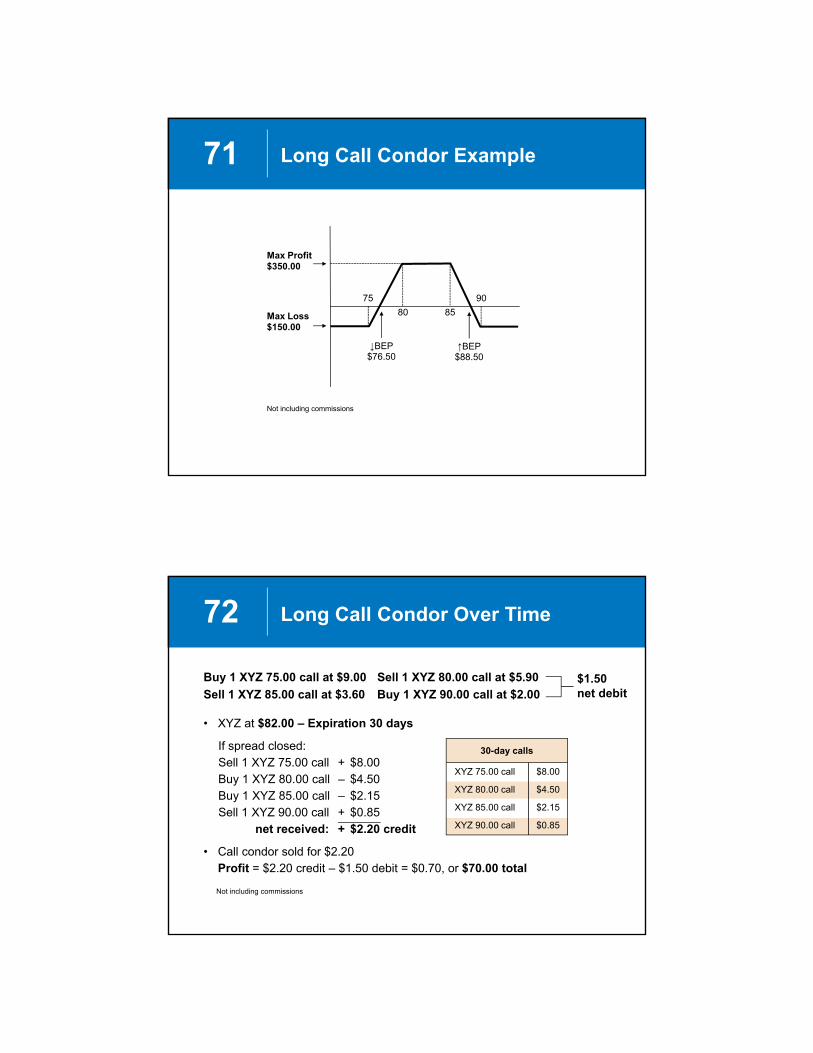

71 Long Call Condor Example

Not including commissions

Max Profit$350.00

Max Loss$150.00

75 90

↓BEP$76.50

↑BEP$88.50

80 85

72 Long Call Condor Over Time

Buy 1 XYZ 75.00 call at $9.00 Sell 1 XYZ 80.00 call at $5.90

Sell 1 XYZ 85.00 call at $3.60 Buy 1 XYZ 90.00 call at $2.00

• XYZ at $82.00 – Expiration 30 days

If spread closed:Sell 1 XYZ 75.00 call + $8.00Buy 1 XYZ 80.00 call – $4.50Buy 1 XYZ 85.00 call – $2.15Sell 1 XYZ 90.00 call + $0.85

net received: + $2.20 credit

• Call condor sold for $2.20Profit = $2.20 credit – $1.50 debit = $0.70, or $70.00 total

Not including commissions

XYZ 75.00 call

XYZ 80.00 call

XYZ 85.00 call

XYZ 90.00 call

30-day calls

$8.00

$4.50

$2.15

$0.85

$1.50net debit

73

Buy 1 XYZ 75.00 call at $9.00 Sell 1 XYZ 80.00 call at $5.90

Sell 1 XYZ 85.00 call at $3.60 Buy 1 XYZ 90.00 call at $2.00

• XYZ at $82.00 – Expiration 30 days – Volatility 35% → 45%

If spread closed:Sell 1 XYZ 75.00 call + $8.60Buy 1 XYZ 80.00 call – $5.30Buy 1 XYZ 85.00 call – $3.00Sell 1 XYZ 90.00 call + $1.60

net received: + $1.90 credit

• Call condor sold for $1.90Profit = $1.90 credit – $1.50 debit = $0.40, or $40.00 total

Not including commissions

XYZ 75.00 call

XYZ 80.00 call

XYZ 85.00 call

XYZ 90.00 call

30-day calls

$8.60

$5.30

$3.00

$1.60

Long Call Condor:Volatility Up

$1.50net debit

74

Buy 1 XYZ 75.00 call at $9.00 Sell 1 XYZ 80.00 call at $5.90

Sell 1 XYZ 85.00 call at $3.60 Buy 1 XYZ 90.00 call at $2.00

• XYZ at $82.00 – Expiration 30 days – Volatility 35% → 25%

If spread closed:Sell 1 XYZ 75.00 call + $7.50Buy 1 XYZ 80.00 call – $3.60Buy 1 XYZ 85.00 call – $1.25Sell 1 XYZ 90.00 call + $0.30

net received: + $2.95 credit

• Call condor sold for $2.95Profit = $2.95 credit – $1.50 debit = $1.45, or $145.00 total

Not including commissions

XYZ 75.00 call

XYZ 80.00 call

XYZ 85.00 call

XYZ 90.00 call

30-day calls

$7.50

$3.60

$1.25

$0.30

Long Call Condor:Volatility Down

$1.50net debit

75 Early Assignment for Dividend

• XYZ has risen• short call(s) now in-the-money

• Early assignment possible before dividend• on or just before ex-dividend date

• You might expect early assignment when• expiration is relatively near• dividend greater than short call’s(s’) time value

• Action• to avoid assignment, close the spread

76 Condors in General

• Call or put condors• behavior and profit/loss profiles much the same • choose suitable risk/reward that current

premiums offer

• Unless all options expiring worthless, position will generally need to be totally or partially closed before expiration

• Since position is combination of 2 vertical spreads, you might consider exiting profitable spread before expiration and let unprofitable spread expire

Iron Condor

78 Iron Condor

• Iron condor – to establish• buy 1 put with lowest strike• sell 1 put with higher strike• sell 1 call with higher strike• buy 1 call with highest strike

• Composition – 2 ways to look at it• bull put spread (credit) + bear call spread (credit)• short strangle (credit) + long wider strangle (debit)

• Spread always established for net credit• margin requirement (firm specific)

79 Iron Condor

Iron Condor

Long1 Put

Long1 Call

Short1 Put

Short1 Call

Bull Put

LongPut

ShortPut

Bear Call

ShortCall

LongCall

80

XYZ 50.00 put

XYZ 60.00 put

XYZ 65.00 put

XYZ 70.00 call

XYZ 75.00 call

XYZ 80.00 call

60-day options

$0.10

$1.30

$3.10

$2.30

$1.10

$0.45

Iron Condor Example

• Stock XYZ currently at $66.00

• Spread:Buy 1 XYZ 60.00 put – $1.30Sell 1 XYZ 65.00 put + $3.10Sell 1 XYZ 70.00 call + $2.30Buy 1 XYZ 75.00 call – $1.10

net received: + $3.00 credit

• XYZ 60.00-65.00-70.00-75.00 iron condor established for $3.00 credit, or $300.00 total

Not including commissions

81 Iron Condor Example

Buy 1 XYZ 60.00 put at $1.30 Sell 1 XYZ 65.00 put at $3.10

Sell 1 XYZ 70.00 call at $2.30 Buy 1 XYZ 75.00 call at $1.10

• Downside break-even point• short put strike – net credit received• $65.00 – $3.00 = $62.00

• Upside break-even point• short call strike + net credit received• $70.00 + $3.00 = $73.00

Not including commissions

$3.00net credit

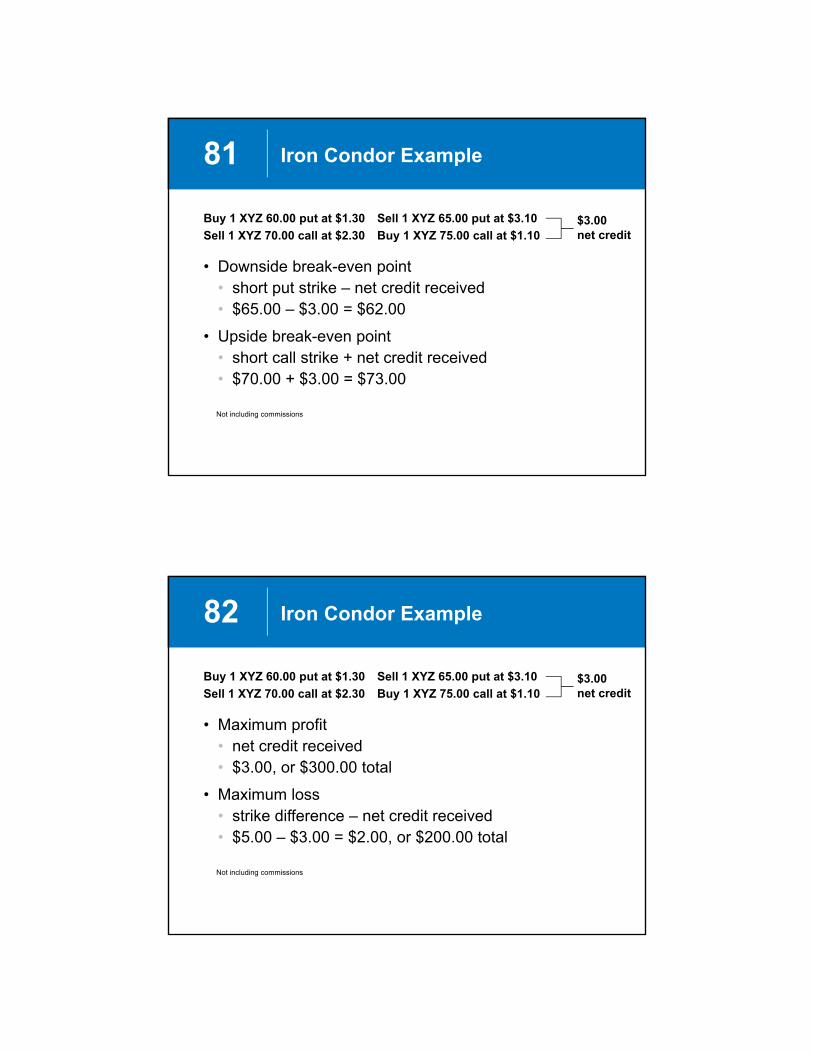

82 Iron Condor Example

Buy 1 XYZ 60.00 put at $1.30 Sell 1 XYZ 65.00 put at $3.10

Sell 1 XYZ 70.00 call at $2.30 Buy 1 XYZ 75.00 call at $1.10

• Maximum profit• net credit received• $3.00, or $300.00 total

• Maximum loss• strike difference – net credit received• $5.00 – $3.00 = $2.00, or $200.00 total

Not including commissions

$3.00net credit

83 Iron Condor Example

Not including commissions

Max Profit$300.00

Max Loss$200.00

60 75

↓BEP$62.00

↑BEP$73.00

65 70

84 Iron Condor: Over Time

Buy 1 XYZ 60.00 put at $1.30 Sell 1 XYZ 65.00 put at $3.10

Sell 1 XYZ 70.00 call at $2.30 Buy 1 XYZ 75.00 call at $1.10

• XYZ at $66.00 – Expiration 30 days

If spread closed:Sell 1 XYZ 60.00 put + $0.55Buy 1 XYZ 65.00 put – $2.10Buy 1 XYZ 70.00 call – $1.25Sell 1 XYZ 75.00 call + $0.35

net paid: – $2.45 debit

• Iron condor closed for $2.45 debitProfit = $3.00 credit – $2.45 debit = $0.55, or $55.00 total

Not including commissions

XYZ 60.00 put

XYZ 65.00 put

XYZ 70.00 call

XYZ 75.00 call

30-day options

$0.55

$2.10

$1.25

$0.35

$3.00net credit

85 Iron Condor: Volatility Up

Buy 1 XYZ 60.00 put at $1.30 Sell 1 XYZ 65.00 put at $3.10

Sell 1 XYZ 70.00 call at $2.30 Buy 1 XYZ 75.00 call at $1.10

• XYZ at $66.00 – Expiration 30 days – Volatility 35% → 45%

If spread closed:Sell 1 XYZ 60.00 put + $1.05Buy 1 XYZ 65.00 put – $2.85Buy 1 XYZ 70.00 call – $1.90Sell 1 XYZ 75.00 call + $0.80

net paid: – $2.90 debit

• Iron condor closed for $2.90 debitProfit = $3.00 credit – $2.90 debit = $0.10, or $10.00 total

Not including commissions

XYZ 60.00 put

XYZ 65.00 put

XYZ 70.00 call

XYZ 75.00 call

30-day options

$1.05

$2.85

$1.90

$0.80

$3.00net credit

86 Iron Condor: Volatility Down

Buy 1 XYZ 60.00 put at $1.30 Sell 1 XYZ 65.00 put at $3.10

Sell 1 XYZ 70.00 call at $2.30 Buy 1 XYZ 75.00 call at $1.10

• XYZ at $66.00 – Expiration 30 days – Volatility 35% → 25%

If spread closed:Sell 1 XYZ 60.00 put + $0.20Buy 1 XYZ 65.00 put – $1.35Buy 1 XYZ 70.00 call – $0.60Sell 1 XYZ 75.00 call + $0.10

net paid: – $1.65 debit

• Iron condor closed for $1.65 debitProfit = $3.00 credit – $1.65 debit = $1.35, or $135.00 total

Not including commissions

XYZ 60.00 put

XYZ 65.00 put

XYZ 70.00 call

XYZ 75.00 call

30-day options

$0.20

$1.35

$0.60

$0.10

$3.00net credit

87 Condor Comparison

Call or Put Condor

• Debit spreads

• Maximum profit lower (same strikes)

• Maximum loss higher (same strikes)

Iron Condor

• Credit spread

• Maximum profit higher (same strikes)

• Maximum loss lower (same strikes)

At expiration, maximum profit will occur with underlying

closing at or between the two middle strike prices

At expiration, pin risk is always a concern

88 Iron Butterfly vs. Iron Condor

Iron Butterfly at Expiration

• Maximum loss generally lower

• Maximum profit (net credit) generally higher

• Maximum profit at singlestrike price (middle)

Iron Condor at Expiration

• Maximum loss generally higher

• Maximum profit (net credit) generally lower

• Maximum profit within range of strike prices (middle two)

89 In Conclusion

• Butterflies and condors (including iron versions)• neutral strategies• tradeoff for limited loss potential → limited profit potential• opportunity to sell options with limited risk

• Probability of maximum profit at expiration• butterfly lower• condor higher

• Margin, as well as account approval, may be required to trade these strategies

90 For More Information

www.OptionsEducation.org

1‐888‐OPTIONS

Thank youfor attending

www.OptionsEducation.org

Thank you for attending.