Business Performance - Bolsas y Mercados Españoles · Business Performance January–March 2016 -...

33

-1- April 2016 Business Evolution January – March 2016 Business Performance January–March 2016

Transcript of Business Performance - Bolsas y Mercados Españoles · Business Performance January–March 2016 -...

- 1 -

April 2016

Business Evolution January – March 2016

BusinessPerformance

January–March 2016

- 2 -

April 2016

Business Evolution January – March 2016

DisclaimerThis presentation, which is personal to the recipient, has been prepared and produced by Bolsas y Mercados Españoles, Sociedad Holding de Mercados

y Sistemas Financieros, S,A, (“BME”) solely for the benefit of investment analysis and may not be used for any purpose other than assessment of

investments concerning BME, Unless otherwise stated, BME is the source for all data contained in this presentation, Such data is provided as at the date

of this presentation and is subject to change without notice,

This presentation is strictly confidential and is being furnished to you solely for your information, It may not be reproduced, redistributed, passed on or

published, in whole or in part, to any other person for any other purpose, This presentation does not constitute or form part of, and should not be

construed as, an offer or invitation for the sale of or the subscription of, or a solicitation of any offer to buy or subscribe for, any securities, nor shall it or

any part of it or the fact of its distribution form the basis of, or be relied on in connection with, any offer, contract, commitment or investment decision

relating thereto, nor does it constitute a recommendation regarding the securities of BME,

Neither this presentation nor any copy of it may be taken, transmitted into or distributed in the United States, the United Kingdom, Canada, Australia or

Japan except by or on the express instructions of BME, The distribution of this presentation in other jurisdictions may also be restricted by law and

persons into whose possession this presentation comes should inform themselves about and observe any such restrictions,

This presentation is directed only at persons who (i) have professional experience in matters relating to investments falling within article 19(5) of the

Financial Services and Markets Act 2000 (financial promotion) order 2005 (“the order”); or (ii) are persons to whom it can otherwise lawfully be

distributed (all such persons together being referred to as “relevant persons”), This presentation must not be acted on, or relied on by, persons who are

not relevant persons,

The information in this presentation has not been independently verified, No representation or warranty, express or implied, is made as to, and no

reliance should be placed on, the fairness, accuracy or completeness of the information or opinions contained herein, None of BME, any of its

shareholders, or any of their respective subsidiary undertakings or affiliates or any of such person’s directors, officers or employees, advisers or other

representatives, accepts any liability whatsoever (whether in negligence or otherwise) arising, directly or indirectly, from the use of this presentation or

otherwise arising in connection therewith,

This presentation could include forward-looking statements, These forward-looking statements involve known and unknown risks, uncertainties and other

factors, which may cause our actual results, performance, achievements or industry results to be materially different from those expressed or implied by

these forward-looking statements, Forward-looking statements speak only as of the date of this presentation and BME expressly disclaim any obligation

or undertaking to release any update of, or revisions to, any forward-looking statements in this presentation as a result of any change in our expectations

or any change in events, conditions or circumstances on which these forward-looking statements are based,

- 3 -

April 2016

Business Evolution January – March 2016

Index

A. Results

B. Business Units

C. Financials

D. Business Drivers

- 4 -

April 2016

Business Evolution January – March 2016

Index

A. Results

B. Business Units

C. Financials

D. Business Drivers

- 5 -

April 2016

Business Evolution January – March 2016

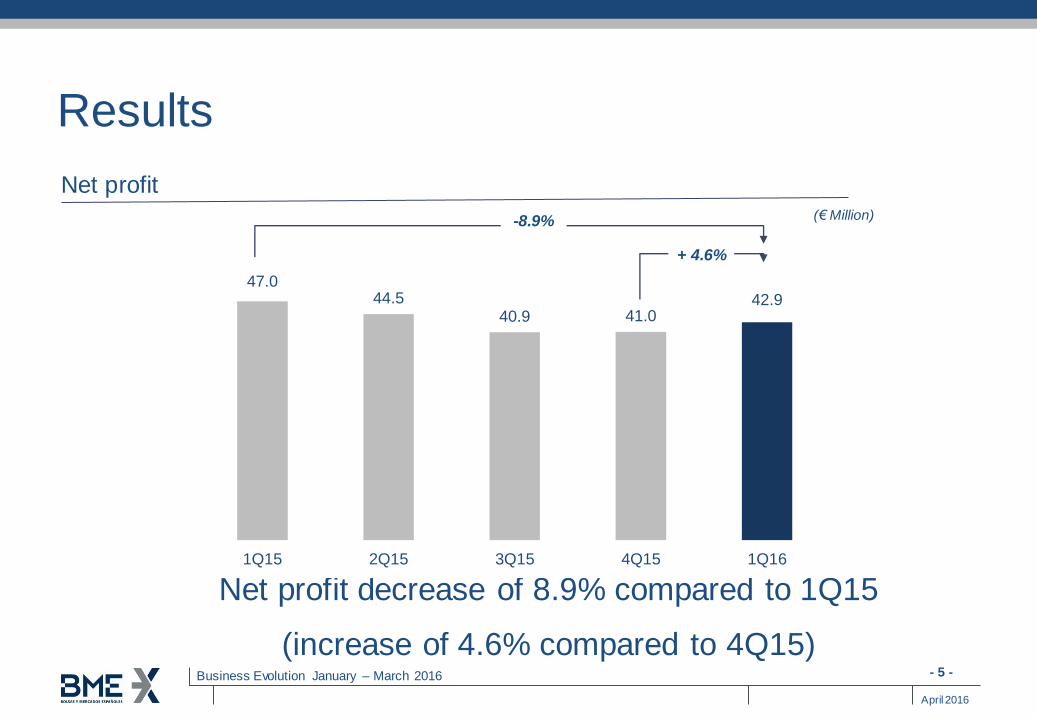

Results

Net profit

Net profit decrease of 8.9% compared to 1Q15

(increase of 4.6% compared to 4Q15)

-8.9% (€ Million)

47.044.5

40.9 41.042.9

1Q15 2Q15 3Q15 4Q15 1Q16

+ 4.6%

- 6 -

April 2016

Business Evolution January – March 2016

Results

Net profit

A comparison with an outstanding 1T15

-8.9%(€ Million)

35.533.0

42.2

47.042.9

1Q12 1Q13 1Q14 1Q15 1Q16

- 7 -

April 2016

Business Evolution January – March 2016

Solid operating leverage

Costs Revenues Revenues not linked to volumes Ratio

- 8 -

April 2016

Business Evolution January – March 2016

Key ratios benchmarking

• Efficiency • ROE

- BME´s data as of 31/03/2016

- Average peer Group figures are calculated using last results published and not taking account

of goodwill impairment charges

37.8%

19.7%

BME Average PeerGroup

32.6%

46.4%

BME Average PeerGroup

- 9 -

April 2016

Business Evolution January – March 2016

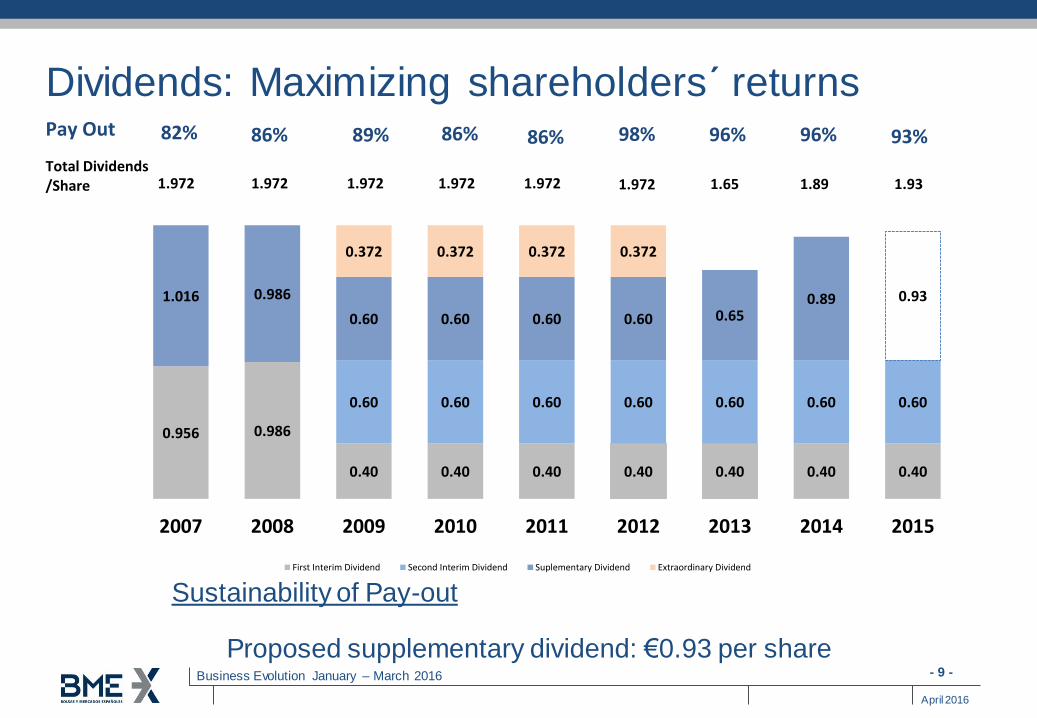

Dividends: Maximizing shareholders´ returns

Sustainability of Pay-out

Proposed supplementary dividend: €0.93 per share

0.956 0.986

0.40 0.40 0.40 0.40 0.40 0.40 0.40

0.60 0.60 0.60 0.60 0.60 0.60 0.60

1.016 0.986

0.60 0.60 0.60 0.60 0.650.89 0.93

0.372 0.372 0.372 0.372

2007 2008 2009 2010 2011 2012 2013 2014 2015

First Interim Dividend Second Interim Dividend Suplementary Dividend Extraordinary Dividend

1.972 1.972Total Dividends /Share

Pay Out 82% 86%

1.9721.9721.972

89% 86% 86%

1.972

98%

1.65

96%

1.89

96%

1.93

93%

- 10 -

April 2016

Business Evolution January – March 2016

Index

A. Results

B. Business Units

C. Financials

D. Business Drivers

- 11 -

April 2016

Business Evolution January – March 2016

Business Areas

Consolidated Revenues

1Q 2016 - %

EBITDA

1Q 2016 - %

Equity44.5%

Settlement24.2%

Clearing5.0%

Information 13.8%

Derivatives3.7%

Fixed Income

2.9%

IT & Consulting

5.9%

Equity45.9%

Settlement26.4%

Clearing3.2%

Information 16.1%

Derivatives2.9%

Fixed Income 1.8%

IT & Consulting

3.7%

- 12 -

April 2016

Business Evolution January – March 2016

261 262

222 218

198

56.2 56.046.3 50.3 51.5

17.7

15.6 14.814.1

15.6

1Q15 2Q15 3Q15 4Q15 1Q16

Mile

s d

e m

illo

ne

s

94

81 8689

8489

97

62 63

80

7068

74

61 63

27.2

13.016.1

29.4

10.915.7

22.5

9.7 14.0

21.615.2 13.5

23.0

13.0 15.4

6.9

5.35.5

5.7

4.4

5.4

5.44.4

5.0 5.2

4.3 4.6 5.2

5.55.0

1/15 2/15 3/15 4/15 5/15 6/15 7/15 8/15 9/15 10/15 11/15 12/15 1/16 2/16 3/16

Equity Market

Equity (Turnover, number of trades and number of shares traded

Revenue in line with 4Q15

Turnover (€ Bill.) Shares (Bill.) Trades (Mill.)

Thousands of € 1Q 2016 1Q 2015 %

Revenues 35,862 43,654 -17.8%

Expenses (9,762) (9,432) 3.5%

EBITDA 26,100 34,222 -23.7%

- 13 -

April 2016

Business Evolution January – March 2016

• Listing activity

Investment flows channeled through the Exchange (€ Million)

• Investment flows have slowed the pace

compared to the first half of 2015. Amounted to €3.3 billion, of which €886 million were in scrip dividend.

• Issuers return to market acess activity with

Telepizza, Dominion and Parques Reunidos IPOs in April.

Source: FESE (Federation of European Stock Exchanges)

Equity Market

11,089 11,770

5,455 5,2313,217

4,389 2,917

626157

37

1Q15 2Q15 3Q15 4Q15 1Q16

New shares issued of listed companies New listings (IPOs)

- 14 -

April 2016

Business Evolution January – March 2016

14.013.1

11.1

13.7

11.8

1Q15 2Q15 3Q15 4Q15 1Q16

1,447 1,446 1,457 1,455 1,464

832 840 768 772 718

1Q15 2Q15 3Q15 4Q15 1Q16

2,286 2,225 2,227 2,1822,279

Par Value registered in FI Market value registered in Equity

Securities under custody: Volumes

(€ Billion)

Settlement & Registration

Settlement: Number of trades settled

(Million of trades)

The stability of registration softens the effect of lower volumes

Thousands of € 1Q 2016 1Q 2015 %

Revenues 19,490 21,718 -10.3%

Expenses (4,463) (4,947) -9.8%

EBITDA 15,027 16,771 -10.4%

- 15 -

April 2016

Business Evolution January – March 2016

150156

150 152 154

4.43.5 3.6 3.1

4.0

1Q15 2Q15 3Q15 4Q15 1Q16

Subscribers (Thousand) P.Quote (Mill.)

Information

Information: Subscribers to primary market sources (Average for the period

in thousands of subscribers and millions of accesses per quote)

Core growth and Infobolsa adquisition

Thousands of € 1Q 2016 1Q 2015 %

Revenues 11,100 9,415 17.9%

Expenses (1,914) (807) 137.2%

EBITDA 9,186 8,608 6.7%

- 16 -

April 2016

Business Evolution January – March 2016

5,993

3,854 4,053

9,190 9,187

1Q15 2Q15 3Q15 4Q15 1Q16

245,892

210,543

141,121125,714 124,418

1Q15 2Q15 3Q15 4Q15 1Q16

Turnover BME Clearing REPO (€ Million) Volume (Mwh) traded in Energy market (Thousand)

Clearing

negative effect on income (REPO segment) offset by cost reduction

Thousands of € 1Q 2016 1Q 2015 %

Revenues 4,041 4,435 -8.9%

Expenses (2,237) (2,523) -11.3%

EBITDA 1,804 1,912 -5.6%

- 17 -

April 2016

Business Evolution January – March 2016

1,862 1,921

854 897

1,782

1,014

1Q15 1Q16

Derivatives

(Thousand of contracts)

Growth in IBEX® Futures not enough to offset rest of products

Stock derivatives contracts tradedIndex derivatives contracts traded

IBEX 35® Futures MiniIBEX 35® Futures IBEX 35® Options Stock Futures Stock Options

(Thousand of contracts)

Thousands of € 1Q 2016 1Q 2015 %

Revenues 3,020 3,159 -4.4%

Expenses (1,361) (1,274) 6.8%

EBITDA 1,659 1,885 -12.0%

3,6603,312

5,0474,829

1Q15 1Q16

- 18 -

April 2016

Business Evolution January – March 2016

126,894

93,083 91,647

73,100

119,962

1Q15 2Q15 3Q15 4Q15 1Q16

Fixed income

AIAF – Volume admitted (Million €)

• Public Debt trading in the quarter improved

19.2% over the previous year to €33.5 billion.

• The primary fixed income market has recovered compared to previous quarters. Issuances for the

first quarter amounted to €120 billion, 5.5% lower compared to 1Q15.

• Alternative Fixed Income Market, MARF, continues its growth path. The volume issued in the first quarter reached 482 million, multiplying

by more than 6 times one year ago issuances.

Thousands of € 1Q 2016 1Q 2015 %

Revenues 2,325 2,504 -7.1%

Expenses (1,274) (1,271) 0.2%

EBITDA 1,051 1,233 -14.8%

- 19 -

April 2016

Business Evolution January – March 2016

IT & Consulting

Market access

Alternative

Financial communication/Outsourcing

London Hubs

Proximity/Colocation

Virtual desks/Contingency/Call Centers

Highway Bulk Payment/Regis-TR®

Thousands of € 1Q 2016 1Q 2015 %

Revenues 4,797 4,630 3.6%

Expenses (2,709) (2,794) -3.0%

EBITDA 2,088 1,836 13.7%

- 20 -

April 2016

Business Evolution January – March 2016

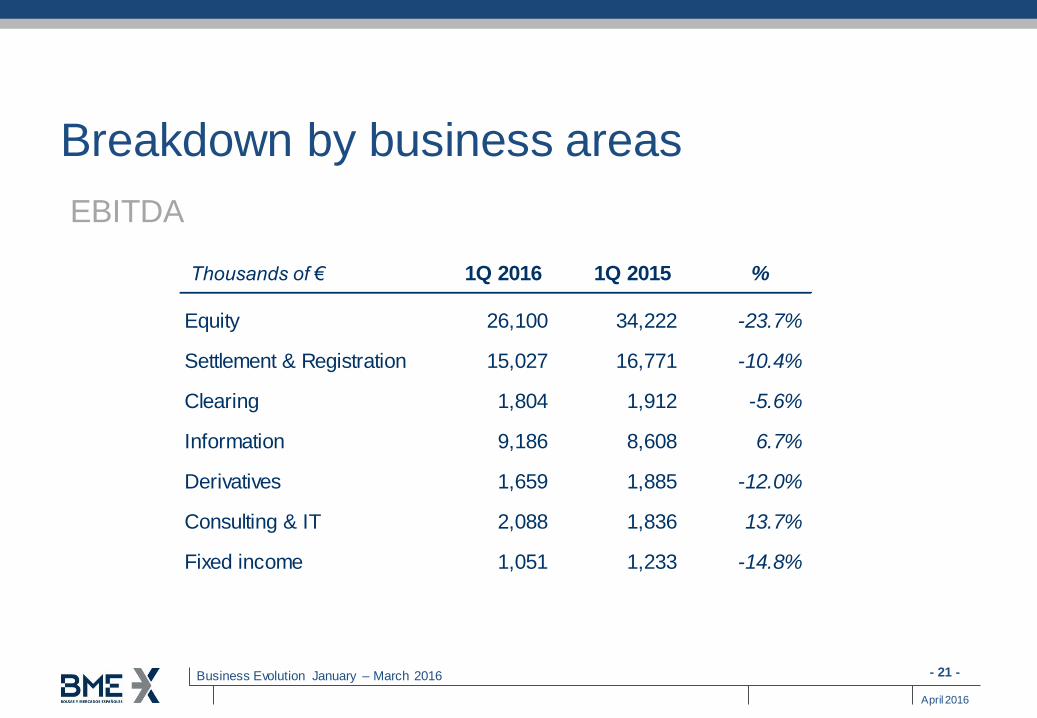

Breakdown by business areas

Revenues

Thousands of € 1Q 2016 1Q 2015 %

Equity 35,862 43,654 -17.8%

Settlement & Registration 19,490 21,718 -10.3%

Clearing 4,041 4,435 -8.9%

Information 11,100 9,415 17.9%

Derivatives 3,020 3,159 -4.4%

Consulting & IT 4,797 4,630 3.6%

Fixed income 2,325 2,504 -7.1%

- 21 -

April 2016

Business Evolution January – March 2016

Breakdown by business areas

EBITDA

Thousands of € 1Q 2016 1Q 2015 %

Equity 26,100 34,222 -23.7%

Settlement & Registration 15,027 16,771 -10.4%

Clearing 1,804 1,912 -5.6%

Information 9,186 8,608 6.7%

Derivatives 1,659 1,885 -12.0%

Consulting & IT 2,088 1,836 13.7%

Fixed income 1,051 1,233 -14.8%

- 22 -

April 2016

Business Evolution January – March 2016

Index

A. Results

B. Business Units

C. Financials

D. Business Drivers

- 23 -

April 2016

Business Evolution January – March 2016

Balance sheet

as of March, 31st

(Thousands of €)2016 2015

Goodwill 88,718 80,619

Other non-current assets 88,233 88,193

Cash and cash equivalents 229,268 251,929

Current financial assets 121,118 100,167

Non-Group current financial assets 23,395,894 36,133,238

Other current assets 101,035 98,504

Total assets 24,024,266 36,752,650

Owners' Equity 478,254 467,002

Non-current liabilities 20,215 18,344

Current liabilities 23,525,585 36,267,304

Total equity and liabilities 24,024,266 36,752,650

- 24 -

April 2016

Business Evolution January – March 2016

P/L

Thousands of € 1Q 2016 1Q 2015 %

Revenues 82,135 93,048 -11.7%

Expenses (26,791) (26,767) 0.1%

EBITDA 55,344 66,281 -16.5%

EBIT 53,865 64,718 -16.8%

Financial results 2,534 225 1,026.2%

Share of profit (loss) of associates 111 66 68.2%

EBT 56,510 65,009 -13.1%

Net Profit 42,864 47,035 -8.9%

- 25 -

April 2016

Business Evolution January – March 2016

EBITDA 1Q 2016/2015[€ Mill.] Net Profit 1Q 2016/2015 [€ Mill.]

Comparison with 1Q 2015

Revenues 1Q 2016/2015 Costs 1Q 2016/2015

Margins

[€ Mill.] [€ Mill.]

- 11.7% + 0.1%

- 16.5% - 8.9%

82.1 93.0

1Q 2016 1Q 2015

26.8 26.8

1Q 2016 1Q 2015

55.3 66.3

1Q 2016 1Q 2015

42.9 47.0

1Q 2016 1Q 2015

- 26 -

April 2016

Business Evolution January – March 2016

32.6% 28.8%

1Q16 1Q15

49.7%41.4%

1Q16 1Q15

65.6%69.6%

1Q16 1Q15

Efficiency & ProfitabilityROE Evolution EBIT/Revenues Ratio Evolution

% ROE % EBIT/Revenues

% Cost/EBIT % Efficiency

Cost/EBIT Ratio Evolution Efficiency Ratio Evolution

37.8%42.7%

1Q16 1Q15

- 27 -

April 2016

Business Evolution January – March 2016

Index

A. Results

B. Business Units

C. Financials

D. Business Drivers

- 28 -

April 2016

Business Evolution January – March 2016

Business drivers: Highly liquid market • Spanish blue-chips are of the most liquid stocks in the EMU

Source: Bloomberg 1) As of 31/03/16

RK

1Q16

40.8

36.1

36.0

32.2

30.8

30.4

28.4

28.4

26.2

26.2

23.1

16.9

15.4

1

2

3

4

5

6

7

8

9

10

16

24

30

0.66

0.58

0.58

0.52

0.50

0.49

0.46

0.46

0.42

0.42

0.37

0.27

0.25

3.09%

5.22%

3.35%

1.79%

4.10%

2.03%

3.59%

1.10%

3.43%

4.20%

2.15%

1.73%

1.56%

Company

Daily avg. 1Q16Relative weight at

EuroStoxx50 (%)1)Turnover (€ Biilion) Turnover (€ Biilion)

- 29 -

April 2016

Business Evolution January – March 2016

• Quality of spreads and best market impact for Spanish stocks

Business drivers: Highly liquid market

Source: Market annual and monthly reports

After a period of high volatility,

which caused an increase inspreads, again have becomenarrowed:

– The IBEX 35® and IBEX®

Medium Cap spread reachedagain values near their lows.

– IBEX® Small Cap achieved

record mimimum levels in thebid-ask spread with animprovement of 6 basis

points from a year earlier,reflecting greater market

depth and liquidity in thesesecurities.

Horq. Media (%)Horq. Media (%)

0.240%

0.235%

0.238%

0.258%

0.255%

0.277%

0.282%

0.261%

0.257%

0.268%

0.281%

0.302%

0.239%

0.052%

0.054%

0.057%

0.061%

0.057%

0.063%

0.065%

0.061%

0.061%

0.070%

0.072%

0.077%

0.064%

201503

201504

201505

201506

201507

201508

201509

201510

201511

201512

201601

201602

201603

Horq. Media (%)

0.75%

0.74%

0.85%

0.84%

0.71%

0.82%

0.91%

0.88%

0.80%

0.87%

0.96%

0.98%

0.69%

- 30 -

April 2016

Business Evolution January – March 2016

• Distribution by markets of business volume of the IBEX 35® companies (2008 – 2015)

Diversified market

Source: Interim Reports from listed companies obtained from CNMV

Spain EU OCDE Rest

20%

20%

24%

- 31 -

April 2016

Business Evolution January – March 2016

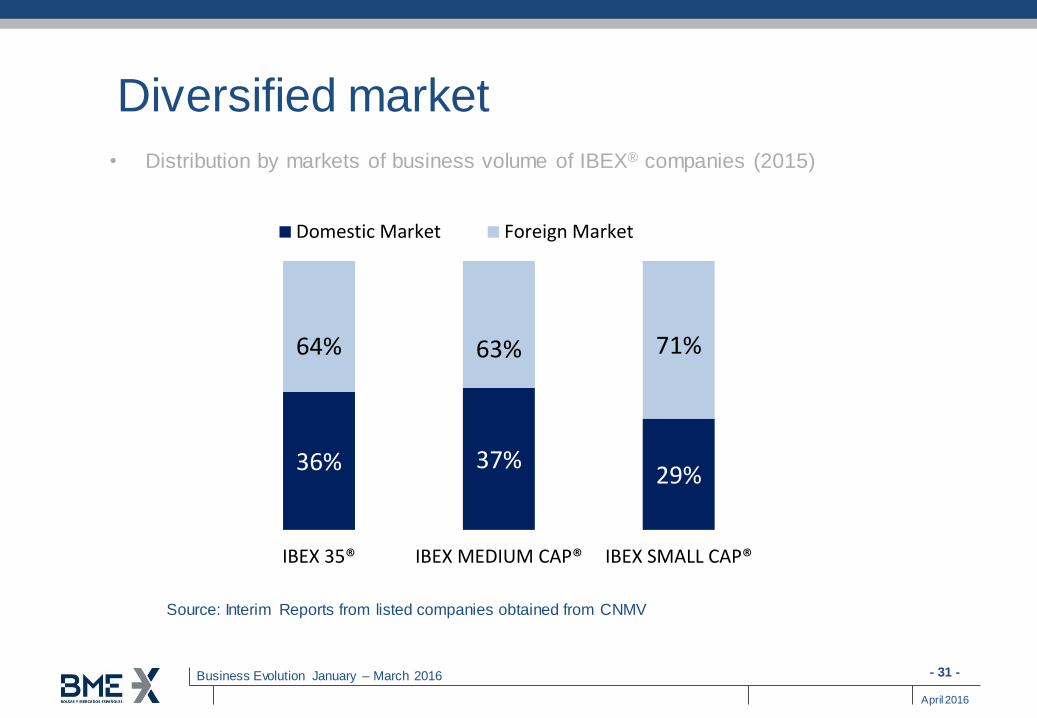

• Distribution by markets of business volume of IBEX® companies (2015)

Diversified market

Source: Interim Reports from listed companies obtained from CNMV

36% 37%29%

64% 63% 71%

IBEX 35® IBEX MEDIUM CAP® IBEX SMALL CAP®

Domestic Market Foreign Market

- 32 -

April 2016

Business Evolution January – March 2016

Growth projects “core” and “non-core”

Progress report

Listing/Trading

• Opportunity for financing companies

through the markets

• Funds Platform

Clearing

• Expansion of clearing

activities

• EMIR: OTC

instruments, new

segments

• Share infrastructure

with othermarkets/platforms

• Equity Segment

Settlement

• T2S conection.

Conection hub forpayment and

securities.

• Portfolio of Services

related to Post-Trading Reform and additional

European regulation.

Market Data

• LATAM project

• Growth in Regis TR®

activities

• New obligations in

compliance reporting(Mifid2)

• Enrichment of the value chain in all their links

Products/services “non-core”

• Open Finance Visual Trader Infobolsa Consulting

• Technology Compliance SIR/SICAM

- 33 -

April 2016

Business Evolution January – March 2016

Q&A

![Instructiva Para Fese 2008 Sis j Go[1]](https://static.fdocuments.in/doc/165x107/5571fc4e497959916996f5b3/instructiva-para-fese-2008-sis-j-go1.jpg)