Business Management 410 Marriott School of Management Fall 2009 Brian Boyer.

34

Business Management 410 Marriott School of Management Fall 2009 Brian Boyer

-

Upload

jasmin-arnold -

Category

Documents

-

view

216 -

download

0

Transcript of Business Management 410 Marriott School of Management Fall 2009 Brian Boyer.

Business Management 410

Marriott School of Management

Fall 2009

Brian Boyer

Objectives

What is optimal portfolio allocation? Given market conditions, what is the “best” way to

combine financial assets into a portfolio?

What determines asset prices? What characteristics of a financial asset

determines its price in equilibrium?

Not a personal finance course!

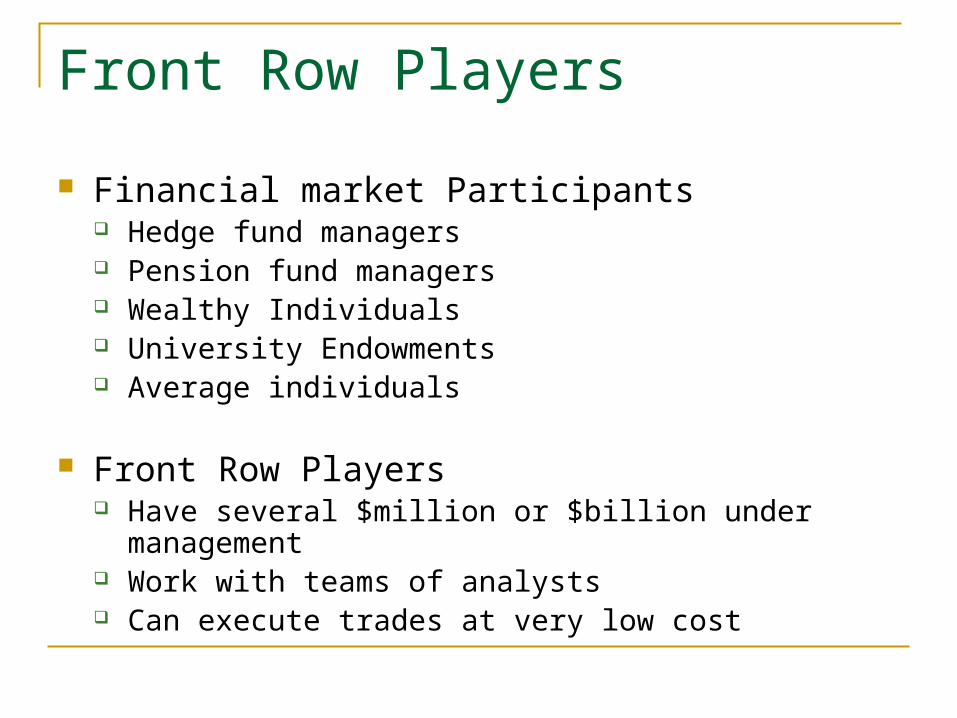

Front Row Players

Financial market Participants Hedge fund managers Pension fund managers Wealthy Individuals University Endowments Average individuals

Front Row Players Have several $million or $billion under management Work with teams of analysts Can execute trades at very low cost

Example

Rewards will be highest for those managing large portfolios.

Suppose research will yield a guaranteed increase in return of 0.1% over the next year

Suppose you have $10,000 invested You get $10 woo-hoo!

Now suppose you have $10 billion invested You get $1 million

CFA Exam CFA: Charted Financial Analyst

Pass Level I, Level II, and Level III exams At least four years of acceptable professional experience

Curriculum: Ethical and Professional Standards Quantitative Methods Economics Financial Statement Analysis Corporate Finance Analysis of Fixed-Income Investments Analysis of Equity Investments Analysis of Derivatives Analysis of Alternative Investments Portfolio management

Teaching Assistants

Bryce Bailey

Matthew Cox

Nathan Leishman

My History

Grew up in Central California BYU after high school Mission in Sao Paulo Brazil Undergrad at BYU (economics) Federal Reserve in D.C. (two years) PhD at University of Michigan

Married with three children

What have your heard about this class?

What do you hope to get out of investments this semester?

Required Materials

Essentials of Investments, Bodie, Kane, and Marcus, 7th Edition

Business Statistics, Downing and Clark, 4th Edition

Fool’s Gold, Gillian Tett

Financial Calculator

Laptop with Excel including the analysis toolpack

Workload We will use a lot of math.

Working knowledge of algebra is required.

Expectation: Six hours per week out of class

Homework Sets (15% of Grade) Wall Street Survivor Trading Game

Quizes (15% of Grade) Wall Street Journal and Economist reading assignments.

Exams Exam 1: 20% of grade Exam 2: 20% of grade Exam 3: 30% of grade

Tour of class web page.

Syllabus

Review Syllabus.

Make a formula sheet as you go along. No notes allowed on exams The formula sheet will help you prepare for exams

Investments: Background and IssuesBKM: Chapter 1

Financial Markets and Assets

Financial asset: a claim to a stream of future cash flows.

Financial Market: a location or mechanism by which buyers and sellers get together and trade financial assets.

Financial Markets and Assets

Firms

Households and Institutional Investors

Goodsand

Services

Types of Financial Markets

Direct Search Markets

Brokered Markets

Dealer Markets

Auction Markets

Types of Financial Instruments Reading BKM Chapter 2.1-2.3

Returns: Review

Key Ideas Calculating Returns Present Value and Future Value Returns and Compounding Returns to a portfolio

Measuring Performance: Price, Payoff, and Return 1 Share of Cisco Stock

You buy it now for $100 In three months you sell it for $110

1 Share of Apache Stock You buy it now for $200 In three months you sell it for $215

What is the correct “measuring stick?” Payoff: what you get at the end of the investment Profit: payoff minus price Return:

Returns

Returns are the “growth rate” of your investment

Investment in Cisco “grew” by 10% (110/100-1)

Investment in Apache “grew” by 7.5%

Instead of buying Apache for $200 buy two shares of Cisco for the same price Profit is $20

Gross Returns Gross returns measure what you get back as a

percentage of the initial investment.

Gross returns are simply payoff/price

Gross return from buying Cisco: 110/100 = 110% By investing in Cisco, you get back 110% of what you initially

invested. Gross returns above 100% are good Gross returns below 100% are bad

Net Returns

Net returns are growth rates.

Net returns are simply payoff/price - 1

Net return from buying Cisco: 110/100 - 1 = 10% Or 10/100 = 10% Your investment grows by 10%.

Net returns above 0 are good Net returns below 0 are bad

Growth rates and Future Value Example: Investment with net return of 5% per year. Initial Investment: $100

After first year, what is the value of investment?

After second year, what is the value of investment?

After third year, what is the value of investment?

10505.1100

25.11005.110005.1105 2

76.11505.110005.125.110 3

Future Value

In general: FV=P0(1+r)n

P0= initial principal invested r = net return on investment N = number of time periods

Financial Calculator N=number of time periods PV = -initial principal (remember “-” sign) r = net return on investment pmt=coupons paid before end of each period (0)

Present Value

Suppose you are given the choice of two flows Choice #1: Receive $X now Choice #2: Receive $100 two years from now

The present value of the cash flow from choice #2 is the amount, $X, that would make you indifferent between the two choices.

Present Value

Case #1: Suppose the cash flow from choice #2 is risk free Risk-free accounts pay a net return of 4.5% per year If you get $X now, you can invest it risk free and in

two years get

For you to be indifferent between the two choices

2)045.1(X

100)045.1( 2 X

Present Value

Doing some algebra

91.57 is the “present value” of the cash flow from choice #2

57.91)045.1(

100

100)045.1(

2

2

X

X

Present Value

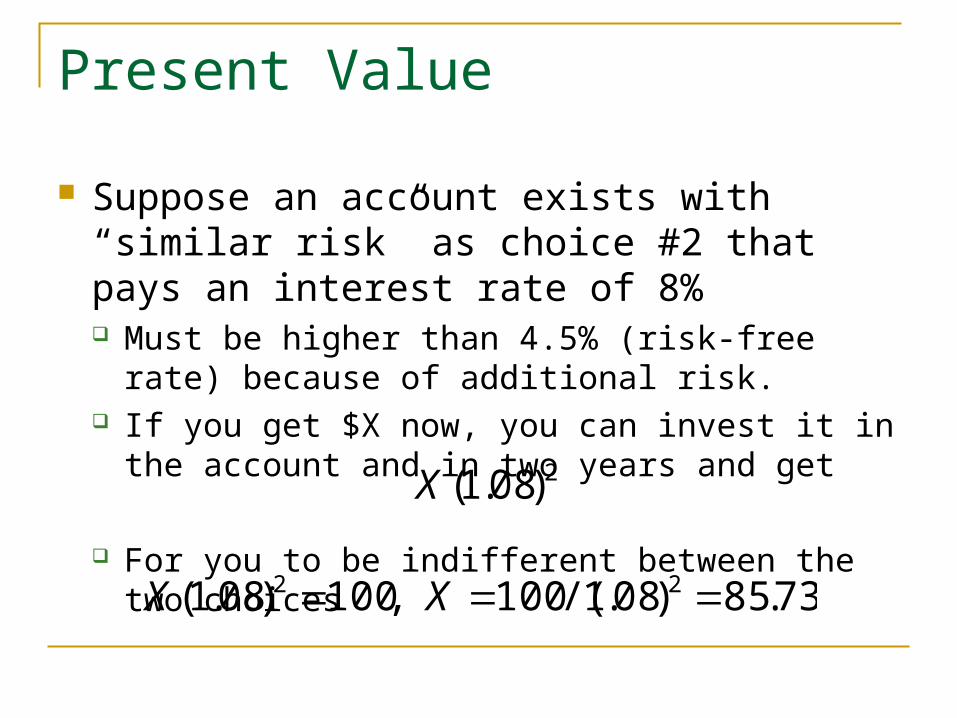

Case #2 What if the cash flow from investment #2 is not risk-

free? That is, on average you expect to get paid $100, but it could be more or less.

Choice #1: Receive $X now Choice #2: Receive $100 two years from now with

some uncertainty.

Present Value

Suppose an account exists with “similar risk” as choice #2 that pays an interest rate of 8% Must be higher than 4.5% (risk-free rate) because

of additional risk. If you get $X now, you can invest it in the account

and in two years and get

For you to be indifferent between the two choices

2)08.1(X

73.85)08.1/(100,100)08.1( 22 XX

Present Value

In general:

FV= payoff at the end of year n r = return on investment of similar risk as FV N = number of time periods until money is received

Financial Calculator N=number of time periods FV=payoff r = net return on investment of similar risk as payoff pmt=coupons paid before end of each period (0)

0 (1 )nFV

Pr

Present Value of an Annuity

Annuity: A constant stream of payments that last forever.

PV = pmt/r

Example: What is the PV of a stream of payments that pays $10 every year for ever? Assume rate of return is 10%. PV=10/.10 = $100

Growth Rates and Time

Net returns (growth rates) are attached to a unit of time.

How can we transform growth rates to different units of time?

Example: Account pays 1% per month What is the growth rate per year? Hint: the answer is not 12%!

Growth Rates and Time

If I invest $1 in this account the money has grown to

Over one year, the net return is

A monthly growth rate of 1% is equivalent to an annual growth rate of 12.68%

1268.101.11 12

%68.1211

1268.1

Growth Rates and Time

Example: Account pays 24% per 2 years What is the growth rate per year? Hint: the answer is not 12%!

Let rA = the annual growth rate If I invest $1 in this account in two years I have

24.1)1(1 2 Ar

Growth Rates and Time

Solving for rA gives us

24.1)1(1 2 Ar

%35.111)24.1(

)24.1()1(2/1

2/1

A

A

r

r

![Cheryl Boyer CV - Kansas State University · management practices: Guide for Producing Nursery Crops. 3rd Ed. SNA, Acworth, GA. [Authorship is listed alphabetically] • Boyer, C.](https://static.fdocuments.in/doc/165x107/5f5d9115c6c58963863faab4/cheryl-boyer-cv-kansas-state-university-management-practices-guide-for-producing.jpg)