Business Interruption Losses - Pennock Acheson Nielsen Devaney

18

Pennock Acheson Nielsen Devaney Pennock Acheson Nielsen Devaney

Transcript of Business Interruption Losses - Pennock Acheson Nielsen Devaney

Pennock Acheson Nielsen DevaneyPennock Acheson Nielsen Devaney

Presentation OutlinePresentation Outline

1. Overview of Business Interruption Coverage

2. Key Financial Information and Terms

3. Calculating Business Interruption Losses

S / Q ti4. Summary / Questions

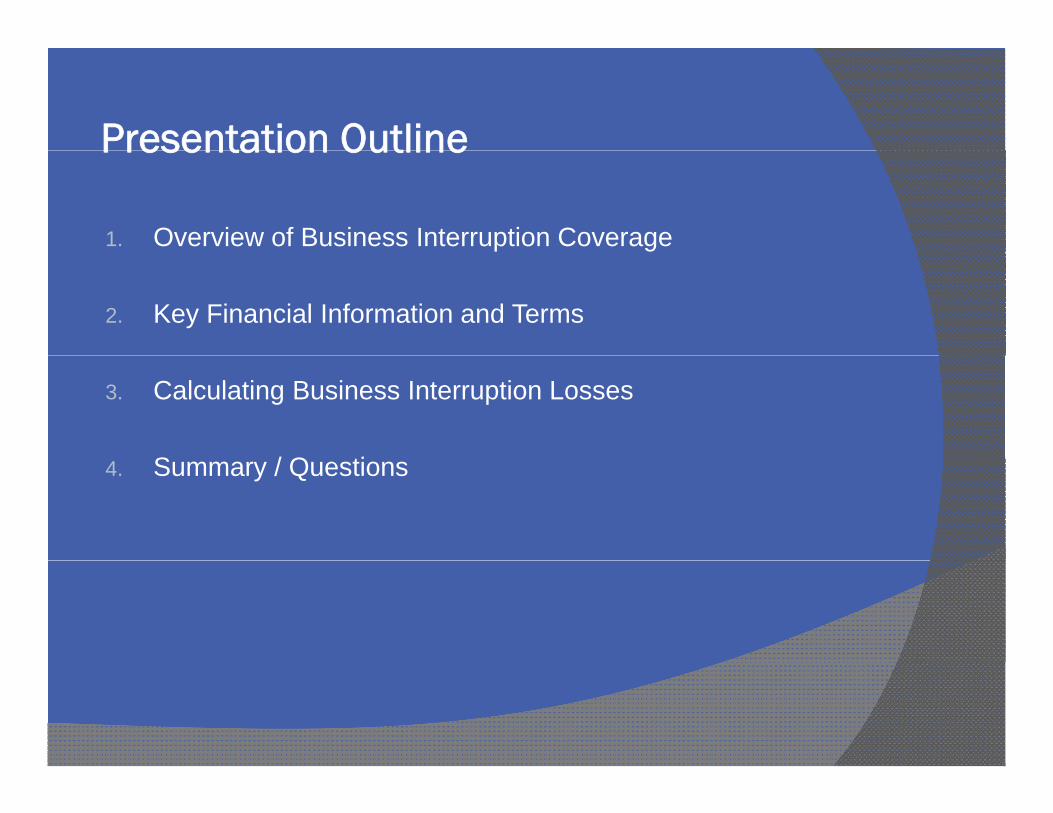

Overview of Business Interruption Coverage

What is Business Interruption Insurance?

Business interruption (“BI”) insurance is a type of coverage that is intended to restore a business to the same financial position as if a loss event had not occurred

Typically triggered by physical damage to property or forced shutdown of business operations E g Fire flood theft vandalism accident etc E.g. Fire, flood, theft, vandalism, accident, etc.

“Loss of profits” as an insurable risk was first implemented in 1797

Purchased by the insured as an add-on to an existing insurance policy

Overview of Business Interruption Coverage

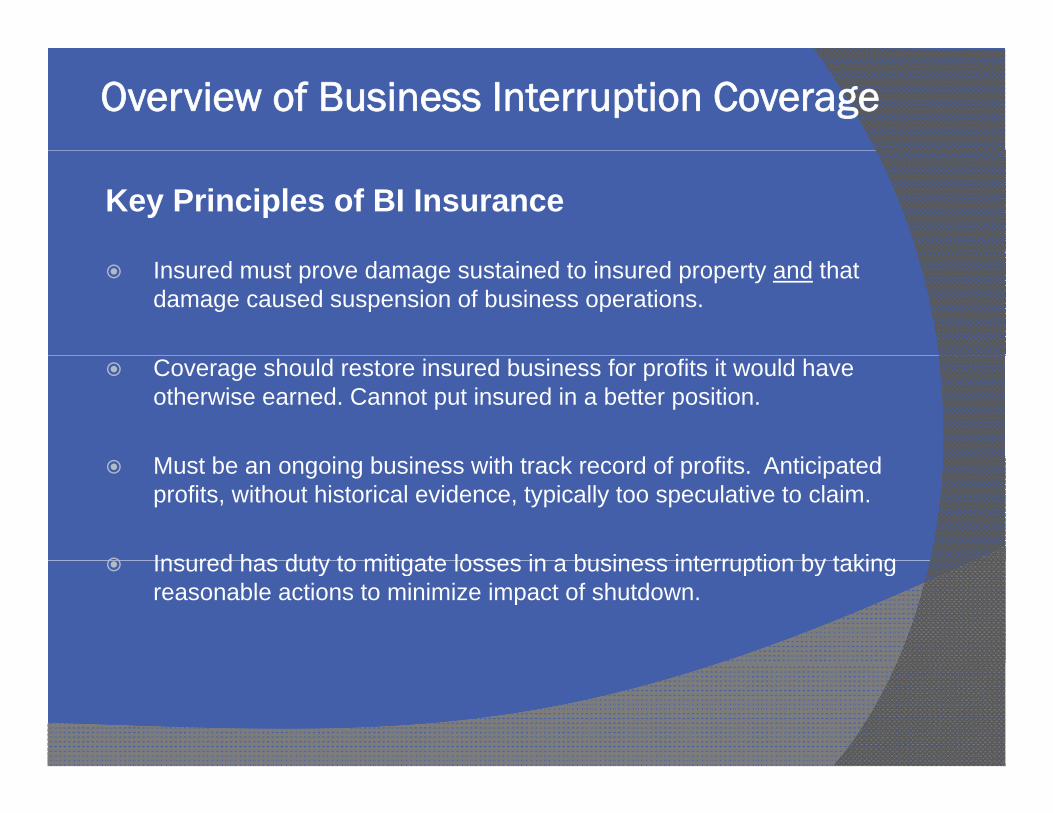

Key Principles of BI Insurance

Insured must prove damage sustained to insured property and that damage caused suspension of business operations.

Coverage should restore insured business for profits it would have otherwise earned. Cannot put insured in a better position.

M t b i b i ith t k d f fit A ti i t d Must be an ongoing business with track record of profits. Anticipated profits, without historical evidence, typically too speculative to claim.

Insured has duty to mitigate losses in a business interruption by taking Insured has duty to mitigate losses in a business interruption by taking reasonable actions to minimize impact of shutdown.

Overview of Business Interruption Coverage

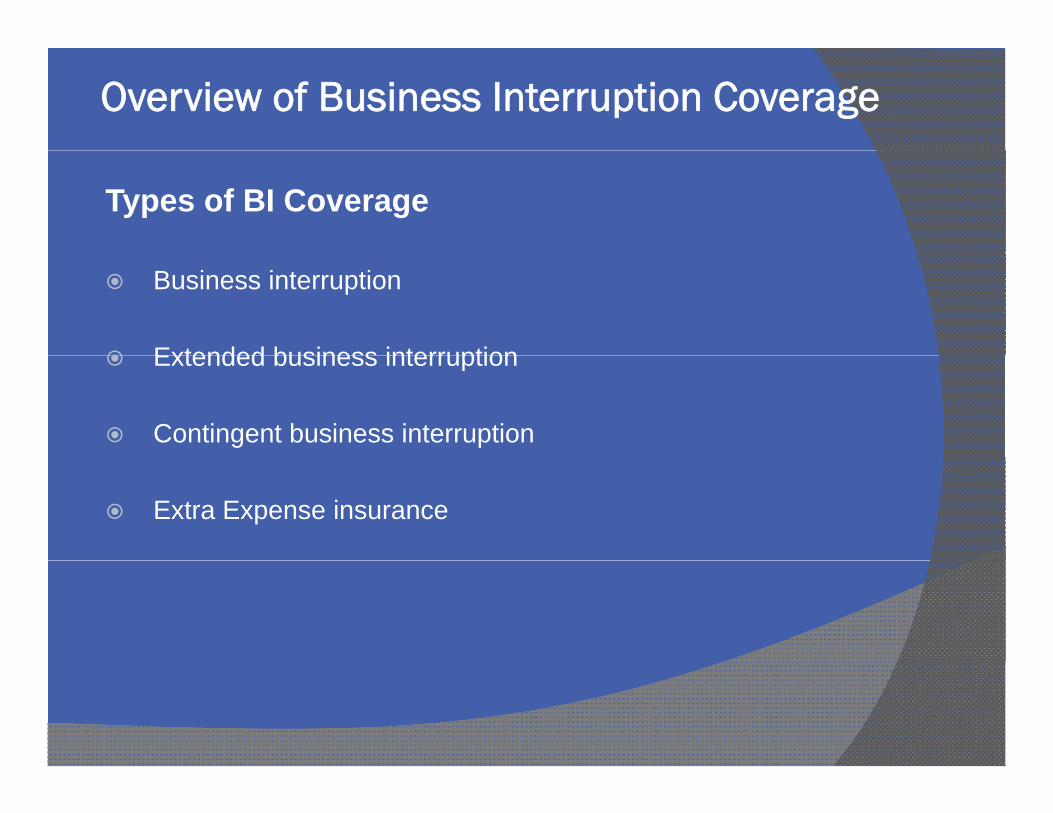

Types of BI Coverage

Business interruption

Extended business interruption Extended business interruption

Contingent business interruption

Extra Expense insurance

Overview of Business Interruption Coverage

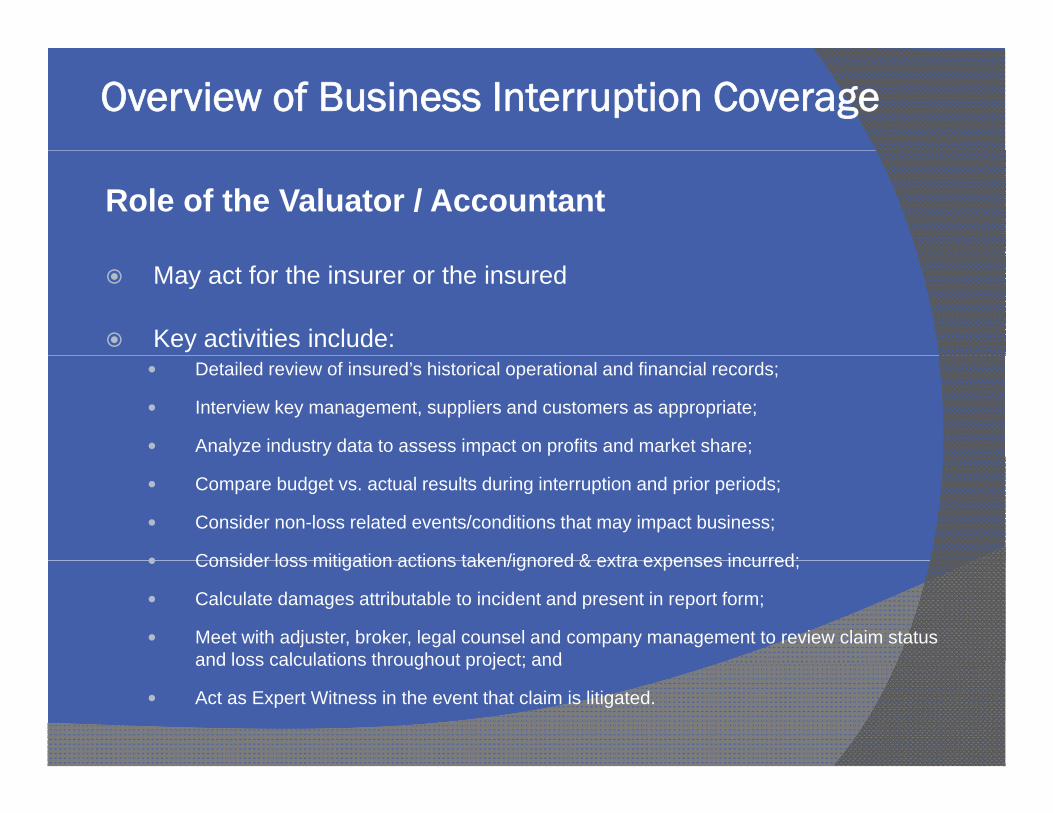

Role of the Valuator / Accountant

May act for the insurer or the insured

Key activities include: Detailed review of insured’s historical operational and financial records;

Interview key management, suppliers and customers as appropriate;

Analyze industry data to assess impact on profits and market share;

Compare budget vs. actual results during interruption and prior periods;

Consider non-loss related events/conditions that may impact business;

Consider loss mitigation actions taken/ignored & extra expenses incurred; Consider loss mitigation actions taken/ignored & extra expenses incurred;

Calculate damages attributable to incident and present in report form;

Meet with adjuster, broker, legal counsel and company management to review claim status and loss calculations throughout project; andand loss calculations throughout project; and

Act as Expert Witness in the event that claim is litigated.

Key Financial Information and Terms

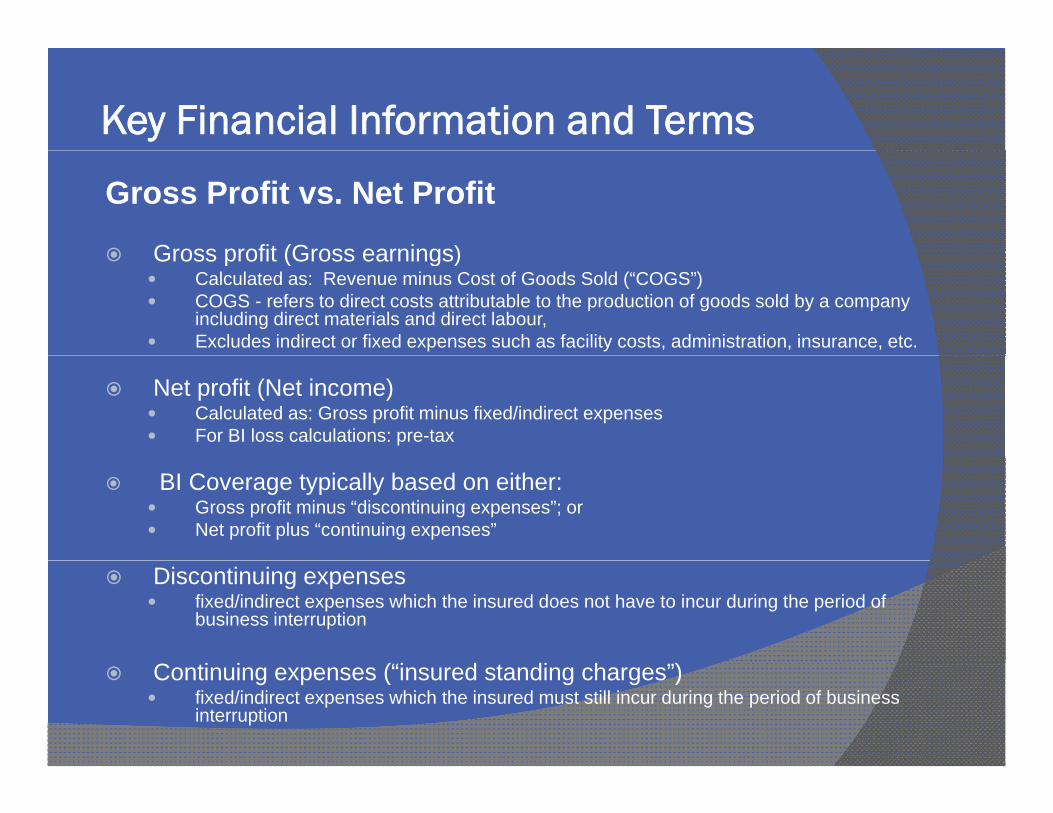

Gross Profit vs. Net Profit

Gross profit (Gross earnings) Gross profit (Gross earnings) Calculated as: Revenue minus Cost of Goods Sold (“COGS”) COGS - refers to direct costs attributable to the production of goods sold by a company

including direct materials and direct labour, Excludes indirect or fixed expenses such as facility costs, administration, insurance, etc.

Net profit (Net income) Calculated as: Gross profit minus fixed/indirect expenses For BI loss calculations: pre-tax

BI Coverage typically based on either: Gross profit minus “discontinuing expenses”; or Net profit plus “continuing expenses”

Discontinuing expenses fixed/indirect expenses which the insured does not have to incur during the period of

business interruption

C i i (“i d di h ”) Continuing expenses (“insured standing charges”) fixed/indirect expenses which the insured must still incur during the period of business

interruption

Key Financial Information and Terms

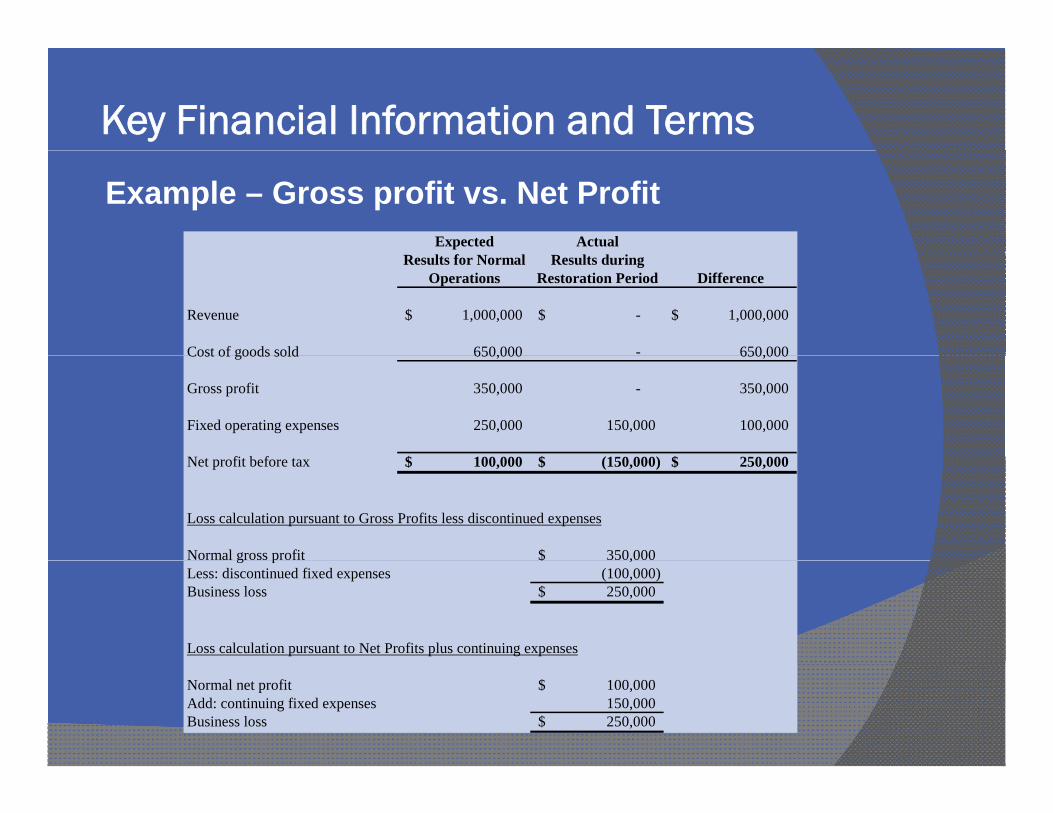

Example – Gross profit vs. Net Profit

Valve manufacturing business sustains a fire to their main production facility. The facility must be completely closed for one month for repairs.

During a typical month, the company would generate a 35% gross profit on sales of $1 million. The company’s typical monthly fixed expenses are $250,000.

During period of restoring the facility, the company generated no revenue and incurred $150,000 of fixed expenses ($100,000 of normal fixed

t i d d t i f ti )expenses were not incurred due to suspension of operations).

Assume nil Extra Expenses for purposes of this example.

Key Financial Information and Terms

Example – Gross profit vs. Net ProfitExpected Actual

Results for Normal Results duringOperations Restoration Period Difference

Revenue 1,000,000$ -$ 1,000,000$

Cost of goods sold 650,000 - 650,000Cost of goods sold 650,000 650,000

Gross profit 350,000 - 350,000

Fixed operating expenses 250,000 150,000 100,000

N t fit b f t 100 000$ (150 000)$ 250 000$Net profit before tax 100,000$ (150,000)$ 250,000$

Loss calculation pursuant to Gross Profits less discontinued expenses

Normal gross profit 350,000$ g p ,$Less: discontinued fixed expenses (100,000) Business loss 250,000$

Loss calculation pursuant to Net Profits plus continuing expenses

Normal net profit 100,000$ Add: continuing fixed expenses 150,000 Business loss 250,000$

Key Financial Information and Terms

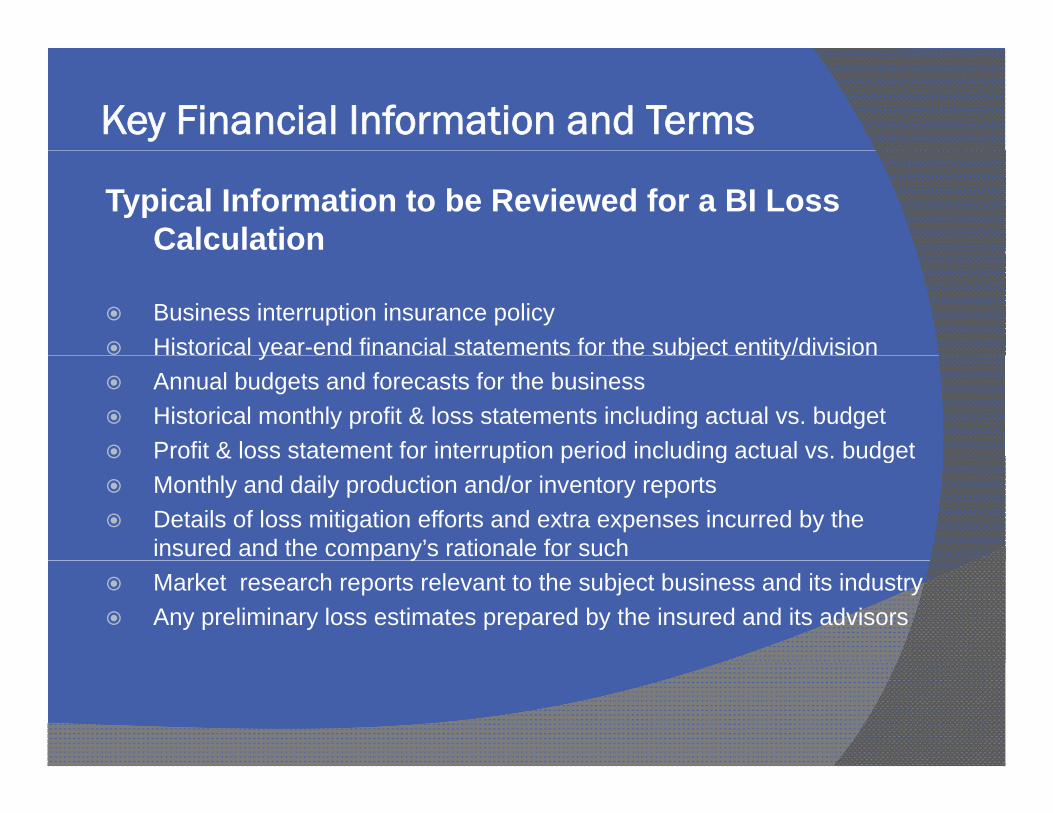

Typical Information to be Reviewed for a BI Loss Calculation

Business interruption insurance policy Historical year-end financial statements for the subject entity/divisiony j y Annual budgets and forecasts for the business Historical monthly profit & loss statements including actual vs. budget Profit & loss statement for interruption period including actual vs. budget Profit & loss statement for interruption period including actual vs. budget Monthly and daily production and/or inventory reports Details of loss mitigation efforts and extra expenses incurred by the

insured and the company’s rationale for suchp y Market research reports relevant to the subject business and its industry Any preliminary loss estimates prepared by the insured and its advisors

Key Financial Information and Terms

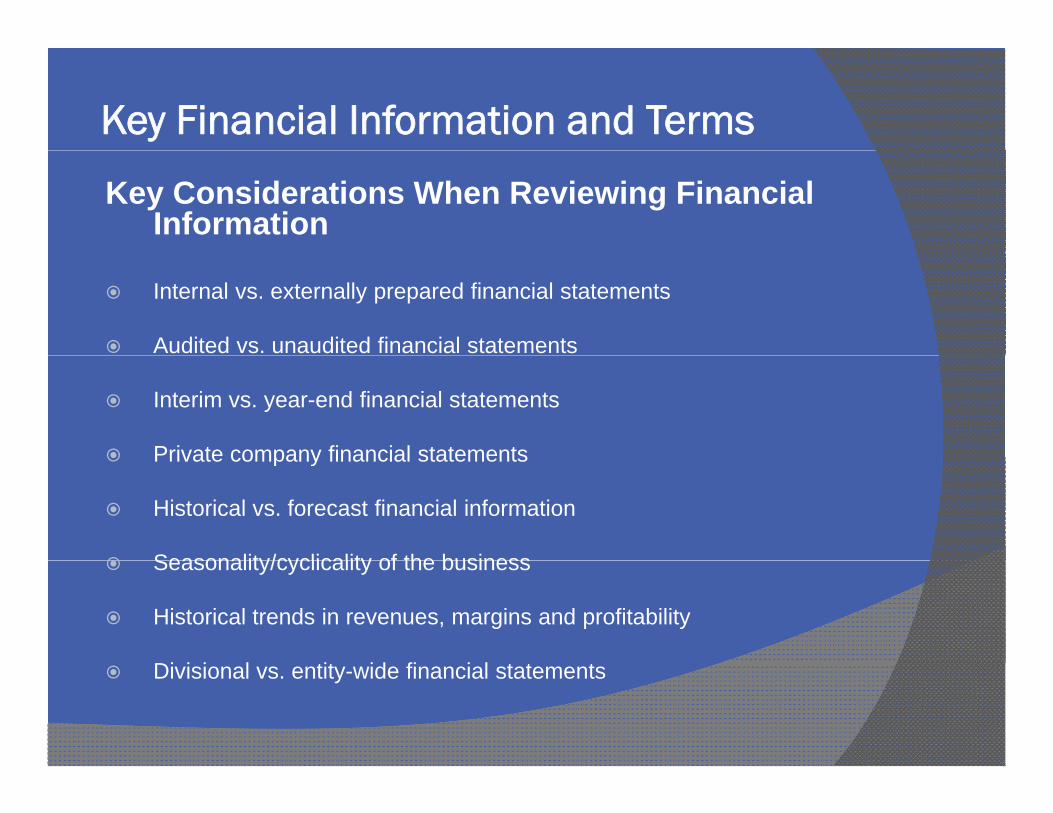

Key Considerations When Reviewing Financial Information

Internal vs. externally prepared financial statements

Audited vs. unaudited financial statements

Interim vs. year-end financial statements

Private company financial statements Private company financial statements

Historical vs. forecast financial information

Seasonality/cyclicality of the business Seasonality/cyclicality of the business

Historical trends in revenues, margins and profitability

Di i i l tit id fi i l t t t Divisional vs. entity-wide financial statements

Calculating Business Interruption Losses

Does BI Coverage Apply to an Event?

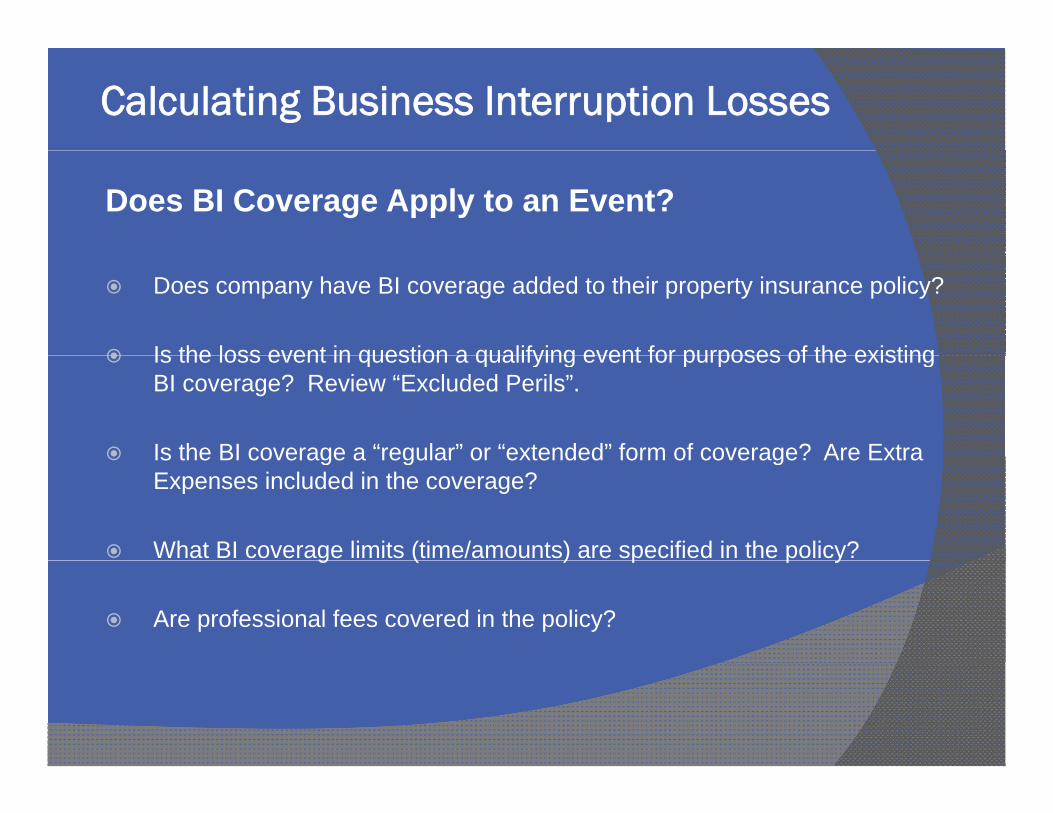

Does company have BI coverage added to their property insurance policy?

Is the loss event in question a qualifying event for purposes of the existing Is the loss event in question a qualifying event for purposes of the existing BI coverage? Review “Excluded Perils”.

Is the BI coverage a “regular” or “extended” form of coverage? Are Extra Is the BI coverage a regular or extended form of coverage? Are Extra Expenses included in the coverage?

What BI coverage limits (time/amounts) are specified in the policy?g ( ) p p y

Are professional fees covered in the policy?

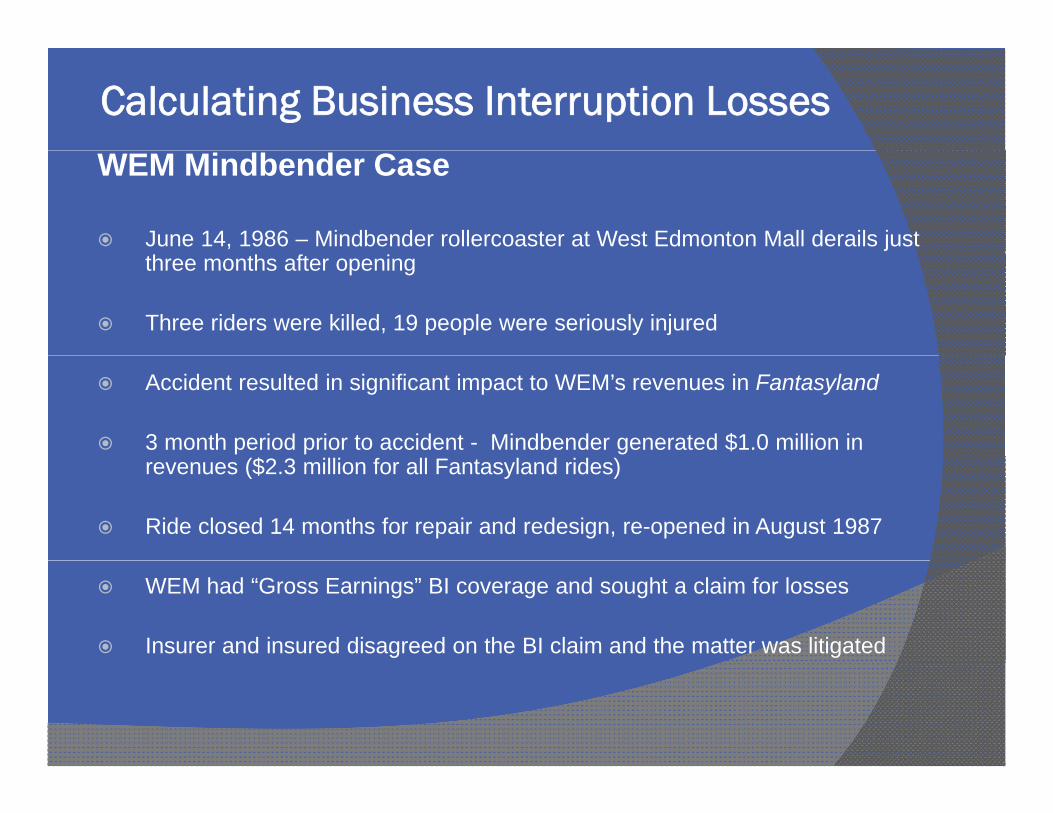

Calculating Business Interruption LossesWEM Mindbender Case

June 14, 1986 – Mindbender rollercoaster at West Edmonton Mall derails just three months after opening

Three riders were killed, 19 people were seriously injured

Accident resulted in significant impact to WEM’s revenues in Fantasyland

3 month period prior to accident - Mindbender generated $1.0 million in ($2 3 illi f ll F l d id )revenues ($2.3 million for all Fantasyland rides)

Ride closed 14 months for repair and redesign, re-opened in August 1987

WEM had “Gross Earnings” BI coverage and sought a claim for losses

Insurer and insured disagreed on the BI claim and the matter was litigated

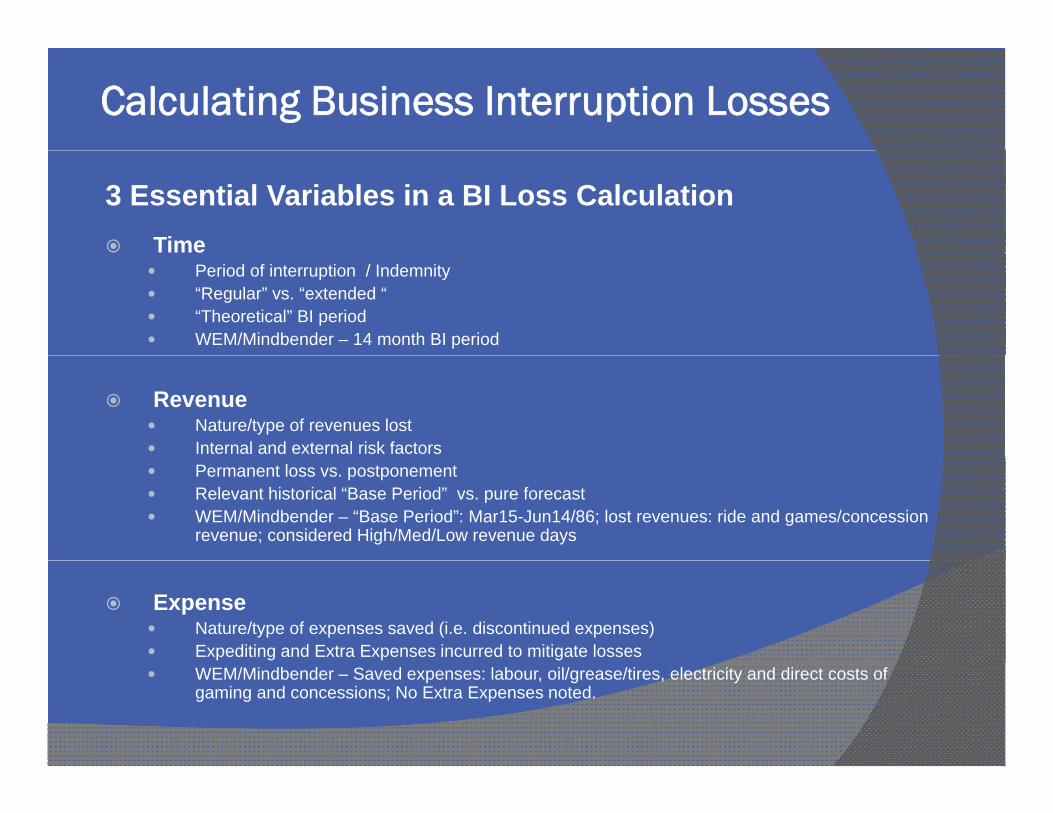

Calculating Business Interruption Losses

3 Essential Variables in a BI Loss Calculation Time

Period of interruption / Indemnity “Regular” vs. “extended “ “Theoretical” BI period WEM/Mindbender – 14 month BI period

Revenue Nature/type of revenues lost Internal and external risk factors Permanent loss vs. postponement Relevant historical “Base Period” vs. pure forecast WEM/Mindbender – “Base Period”: Mar15-Jun14/86; lost revenues: ride and games/concession

revenue; considered High/Med/Low revenue days

Expense Nature/type of expenses saved (i.e. discontinued expenses) Expediting and Extra Expenses incurred to mitigate losses WEM/Mindbender – Saved expenses: labour, oil/grease/tires, electricity and direct costs of

gaming and concessions; No Extra Expenses noted.

Calculating Business Interruption Losses

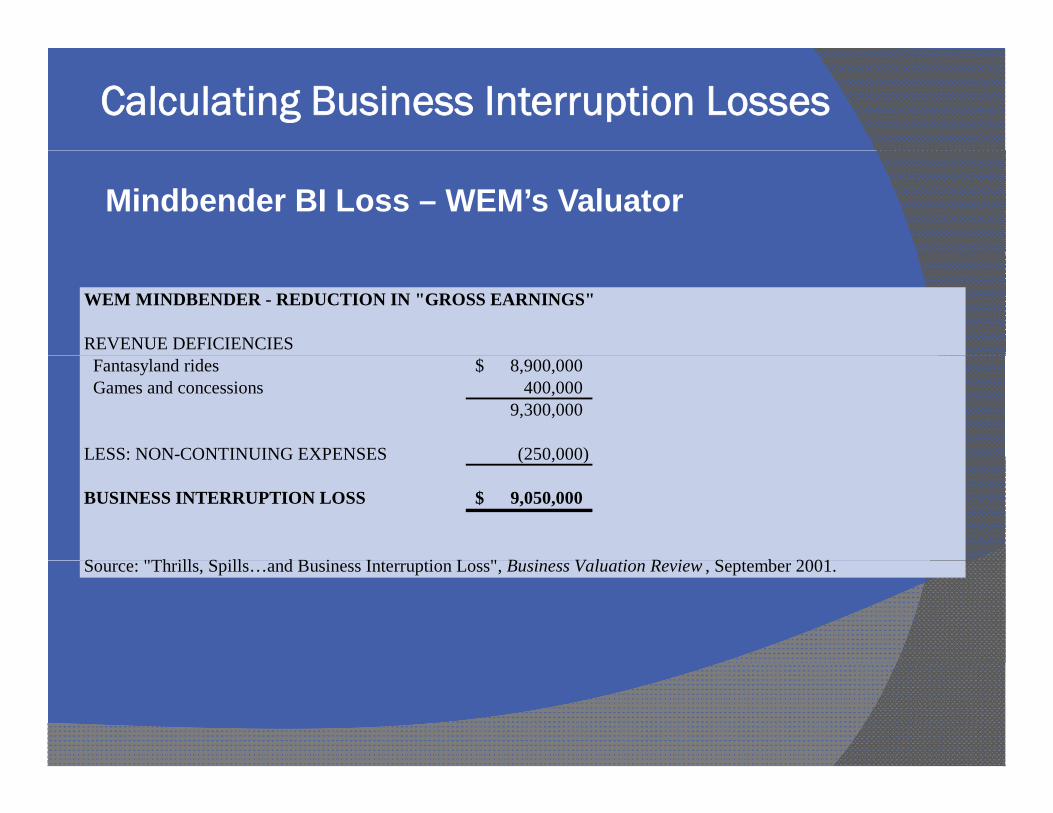

Mindbender BI Loss – WEM’s Valuator

WEM MINDBENDER - REDUCTION IN "GROSS EARNINGS"

REVENUE DEFICIENCIES Fantasyland rides 8,900,000$ Games and concessions 400,000

9,300,000

LESS: NON-CONTINUING EXPENSES (250,000)LESS: NON CONTINUING EXPENSES (250,000)

BUSINESS INTERRUPTION LOSS 9,050,000$

S "Th ill S ill d B i I i L " B i V l i R i S b 2001Source: "Thrills, Spills…and Business Interruption Loss", Business Valuation Review , September 2001.

Calculating Business Interruption Losses

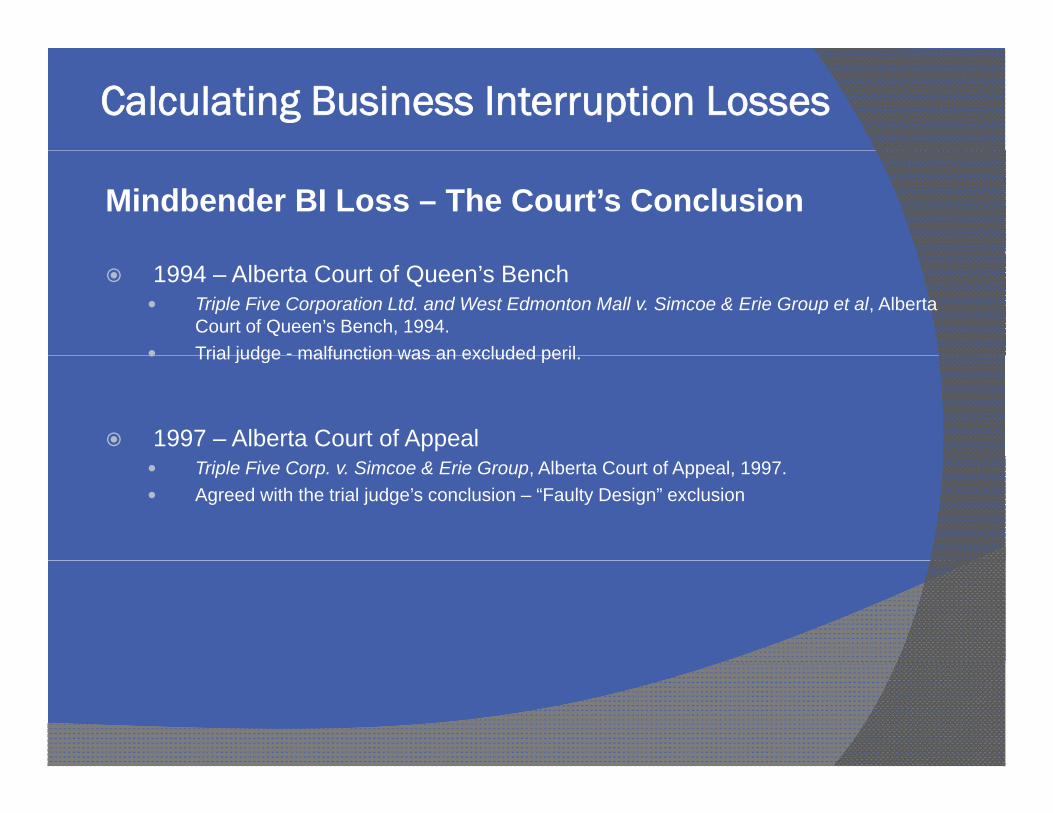

Mindbender BI Loss – The Court’s Conclusion

1994 – Alberta Court of Queen’s Bench Triple Five Corporation Ltd. and West Edmonton Mall v. Simcoe & Erie Group et al, Alberta

Court of Queen’s Bench, 1994. Trial judge - malfunction was an excluded peril Trial judge malfunction was an excluded peril.

1997 – Alberta Court of Appeal Triple Five Corp. v. Simcoe & Erie Group, Alberta Court of Appeal, 1997. Agreed with the trial judge’s conclusion – “Faulty Design” exclusion

Summary

Proper consideration of applicability of BI coverage is critical first step b f d t ki l l l tibefore undertaking a loss calculation

Three key variables in any BI loss calculation: Time, Revenue, Expense

Determination of BI loss is not an exact science; many factors to consider and weigh into a given analysis

Involvement of valuator or accountant important where significant financial information needs to be reviewed and complex analysis is required

Don’t ride a roller coaster in its first year of operation!

QUESTIONS? QUESTIONS?

Contact InformationContact Information

Pennock Acheson Nielsen DevaneyChartered Accountants

Trevor Philippon CA CBV Peter Blasetti CATrevor Philippon, CA, CBV Peter Blasetti, CADirector, Financial Advisory Services Senior ManagerPhone: 780-420-3368 Phone: 780-496-7774Email: [email protected] [email protected]: [email protected] [email protected]

Allan Barwick, CMAPartnerPhone: 780-496-7774Email: [email protected]