BURSA MALAYSIA BERHADbursa.listedcompany.com/misc/slides_20110517.pdf · Serve High Income...

42

Invest Malaysia New York Dato’ Tajuddin Atan, CEO 17 – 18 May 2011 BURSA MALAYSIA BERHAD Destination of choice for listings and investments in the region

Transcript of BURSA MALAYSIA BERHADbursa.listedcompany.com/misc/slides_20110517.pdf · Serve High Income...

Invest Malaysia New YorkDato’ Tajuddin Atan, CEO

17 – 18 May 2011

BURSA MALAYSIA BERHADDestination of choice for listings and investments in the region

Part I

Transforming Malaysia:

Drive for Private Sector Growth

3

Malaysian Market Liberalisation

Country

Recognition

& Competitiveness

Free Capital Mobility

& Improved Access to

Capital Market

New Economic Model - high value & high income

Increasing private sector role in driving business

Creating a conducive environment for entrepreneurship

Focus on developing Human Capital & Innovation

4th for Investor Protection

(World Bank)

10th for Resilience in crisis

(Sevcorp Int’l Business Confidence

Survey)

25th amongst 134 countries for

Corporate Governance Framework

(World Economic Forum)

10th on World Competitiveness

Scoreboard 2010

(IMD World Competitiveness Yearbook)

Access for Foreign Participation No restrictions on international

investments in Malaysia.

Free to repatriate capital, profits and

income.

Liberalised entry and ownership for

foreign players in the capital market.

Foreign Listings

3

4

Liberalising Access for Foreign Participation

Foreign shareholding for stockbroking firms, Islamic banks investment banks & insurance companies raised to 70%

New licenses for foreign brokers

30% bumi equity in 27 services subsectors dropped

Global players present in all segments of the Malaysian Capital Market

30% bumi equity for new IPOs liberalised

More foreign IPOs in the pipeline

Investors

Issuers

Participants

4

Sound Macro Environment

• Projected 5% - 6% for 2011F(Source: BNM)

GDP Growth

• > 90% of assets are RM denominated

• Non-performing loan at 2.3% @ end Feb 2011

(Source: BNM)

Strong Banking Sector & Ample

Liquidity

• Overnight policy rate: 3.0%Conducive Domestic Interest

Rates

• Modest 2.5% - 3.5% for 2011F(Source: BNM)

Manageable Inflation

• 2011F at RM 114.2 billion(Source: MOF)

Strong Current Account in the

Region

• > USD130 billion @ 29 April 2011(Source: BNM)

Healthy International Reserves

5

9. Create regional

champions

10. Global Islamic

Finance Hub

6

Changing Financial Services Landscapeunder the Economic Transformation Program (ETP)

1. Revitalise equity

markets

2. Deepen and

broaden bond

markets

3. Transforms DFIs

4. Create integrated

payment eco-

systems

Strengthen the

Core

Go on the

Offensive

5. Insure our

population

6. Develop private

pension industry

7. Spur growth of

wealth

management

8. Accelerate asset

management

Four Strategic Thrusts & Ten EPPs Identified to Grow Incremental Gross

National Income by RM28.8 billion by 2020

Note: Bursa Malaysia to co-lead item 1 and action/play a part in item 2/4/10 Entry Point Projects

alongside MoF, BNM, SC and other key organisations/ agencies/ companies.

Serve High Income

Population

Seed New

Growth

6

7

Bursa Malaysia’s Report Card Case for Change under the Economic Transformation Program (ETP)

Case for Change: Low liquidity as well as scale and growth

Aspirations: Vibrant Capital Markets that attracts quality listings

and investors

Revitalise the Equity Markets

1. Building Quality:

• Launched the Sustainability Programme

2. Enhancing Efficiency:

• Internet trading for futures products

3. Improving Liquidity:

• New CBBCs/ETFs/REITs issued

• Derivatives product migration to CME

Globex

4. Internationalising our Market:

• CME strategic partnership. CME’s KL Hub

is now a gateway for trading derivatives

products,

• Upgraded FTSE Advanced Emerging

Market Status

Status : Completed

1. Building Quality

• Enhancing standard of CG and

• Market engagement and education

2. Enhancing Efficiency

• Issuing of dual licenses

3. Improving Liquidity

• Increasing Proprietary Day Traders in the

market

4. Internationalising our Market

• Increased visibility through ASEAN

Exchanges

• Expanding reach and profile of Islamic

market

Status : Ongoing

7

na

5,000

8

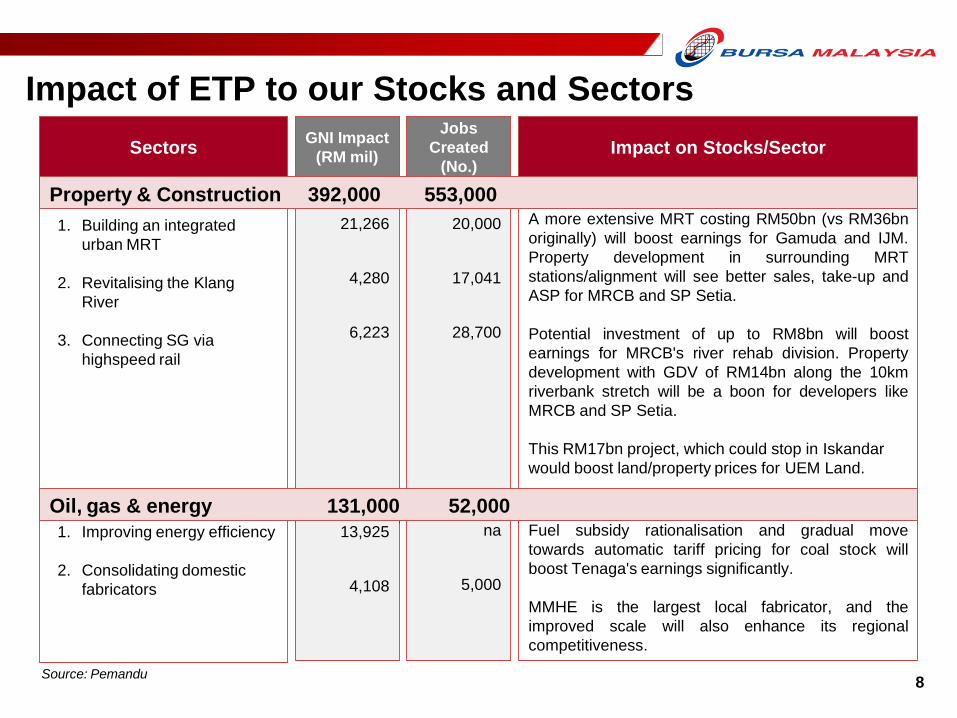

A more extensive MRT costing RM50bn (vs RM36bn

originally) will boost earnings for Gamuda and IJM.

Property development in surrounding MRT

stations/alignment will see better sales, take-up and

ASP for MRCB and SP Setia.

Potential investment of up to RM8bn will boost

earnings for MRCB's river rehab division. Property

development with GDV of RM14bn along the 10km

riverbank stretch will be a boon for developers like

MRCB and SP Setia.

This RM17bn project, which could stop in Iskandar

would boost land/property prices for UEM Land.

21,266

4,280

6,223

GNI Impact

(RM mil)

Jobs

Created

(No.)Impact on Stocks/SectorSectors

20,000

17,041

28,700

Fuel subsidy rationalisation and gradual move

towards automatic tariff pricing for coal stock will

boost Tenaga's earnings significantly.

MMHE is the largest local fabricator, and the

improved scale will also enhance its regional

competitiveness.

Source: Pemandu

Impact of ETP to our Stocks and Sectors

13,925

4,108

Oil, gas & energy 131,000 52,000

1. Building an integrated

urban MRT

2. Revitalising the Klang

River

3. Connecting SG via

highspeed rail

1. Improving energy efficiency

2. Consolidating domestic

fabricators

Property & Construction 392,000 553,000

Impact of ETP to our Stocks and Sectors (contd.)

GNI Impact

(RM mil)

Jobs

Created

(No.)Impact on Stocks/SectorSectors

Source: Pemandu 9

1. Broadband for all

2. Extending broadband reach

3. Extending regional telco

1,600

10,000

5,858

10,172

13,711

5,813

Enhances growth for TM, Maxis, Digi and Axiata

as players move towards quad play.

Increased market cap and trading velocity will

improve earnings for Bursa and stockbrokers.

Higher overseas contributions from Malaysian

banks. E.g CIMB, Maybank and RHB.

Stronger contributions for Banks with Islamic

arms.

1. A duty free shopping

destination

2. Improves rates, mix and

quality of hotels

3. Enhance connectivity to

medium-haul markets

This will improve productivity and revenue for

Sime, IOI, KLK and Genting Plant.1. Improving FFB yields

2. Increasing oil extraction

dates

3. Developing oleo derivatives

Palm Oil 125,000 42,000

Improves yield and load factor for Air Asia, as

well as hotel occupancy and yields for Genting

group.

Financial Services 121,000 275,000

1. Revitalising capital market

2. Developing regional

champions

3. Global hub for Islamic

Finance

3,325

5,564

7,242

8,598

(8,524)

11,644

7,838

5,528

3,310

3,325

5,564

7,242

Tourism 67,000 497,000

Comms, Content & Infra 36,000 43,000

7,155

3,135

1,220

2,160

2,688

2,289

Capital Market

StakeholdersDRIVERS

MOF, PEMANDU, BNM, SC, Bursa Malaysia

Our Assets PEOPLE MARKET FRAMEWORK LOCATION

Our Strengths

1) Stable Political

Environment

2) Multicultural:

Historical ties with

China,India, Indonesia and

the Developed World

3) New Corporate

Champions:

Highly educated business

leaders

4) Good Infrastructure & No

Barriers:

Open access & Business

friendly

5) Healthy Credit Market:

Globally respected agencies

in place

6) Expanding capital market:

QDII, US SEC Recognition &

FTSE Advance Emerging

Economy Status

7) Young Demographics:

Malaysia is situated at the

heart of ASEAN’s 590

million people. With a

population of 28 mil,

Malaysia’s labor force

stands high at 64%. Only

5% of population is above

age 65.

8) Abundant Resources:

Commodity Rich, Ample

Land

Our StoryThe Exchange is a conduit to ASEAN as many Malaysian companies

have regional growth and footprint.

Regional Champions

Strength of Our Market

Crossing Borders

10

Regional Champions

ASEAN’s leading bank franchise with over 1,000 branches, the largest in the region.Presence in CIMB Niaga (Indonesia), CIMB Thai (Thailand) and consumer banking franchise in

Singapore and Cambodia.

AirAsia is Asia’s largest low cost carrier with over 130 routes linking three continents. Regional presence with holdings in PT Indonesia AirAsia, Thai AirAsia, AirAsia Philippines Inc etc.

One of Malaysia’s largest and most diversified construction groups Successful infrastructure projects in China, Argentina, India & Vietnam

Axiata has over 150 million mobile subscribers in Asia.Controlling interests in mobile operators in Malaysia, Indonesia, Sri Lanka, Bangladesh & Cambodia

with significant strategic stakes in India, Singapore and Iran.

One of the world’s leading integrated leisure and entertainment resortGlobal presence including Australia, the Americas, the Philippines and the UK

Leading integrated palm oil player and largest vegetable oil based oleochemical

manufacturer in Asia

Serving global markets in more than 65 countries

11

Regional Champions

Some of our companies are global leaders in their respective fields and others are making mark

around the region. They grow by leveraging on the country’s assets and pro-business policies.

These companies now spearhead Malaysia’s emergence as a dynamic advancing economy.

The world's largest rubber glove manufacturer Top Glove exports to more than 900 customers in over 180 countries through its sales and marketing

offices in Malaysia, the United States and Germany.

The Public Bank Group's regional network has been expanded to 109 branches in

countries outside of Malaysia. Banking operations presence in Hong Kong and China, Cambodia, Vietnam, Laos and Sri Lanka.

The leading integrated petrochemicals producer in Malaysia and one of the largest in

Southeast Asia.Production capacity in eastern Peninsular Malaysia as well as manufacturing complexes in Gurun,

Bintulu, Labuan and Vung Tau, Vietnam.

The world largest palm oil producer, and diversified multinational involved in property,

motors, industrial equipment and energy & utilities, with healthcare as a growing

business.

Workforce of over 100,000 employees in over 20 countries.

One of Malaysia’s leading banking group with a growing presence in South East Asia The Group has expanded internationally, with over 1,750 branches and offices in 14 countries and

serving over 18 million customers.

12

Ride Wave of Market Reform

Malaysia houses some of the biggest regional

players in ASEAN. With conducive macro

environment and the Economic Transformation in

full motion, more companies are positioned to take

giant leaps towards Malaysia’s 2020 high-income

economy aspiration.

Invest in Our Growth Story

GROWTH

13

Part II

Bursa Malaysia:

Conduit to Malaysian Growth

15

Diversified OfferingsStrong Niche In Islamic and Commodities

10 Derivatives Products:

Commodity futures

Equity futures

Equity options

Financial futures

Sukuk

Shari’ah compliant

equities

i-REITS

i-ETFs

Bursa Suq Al-Sila’

TRADING CLEARING SETTLEMENT DEPOSITORY

2 Markets:

Main Market : 840 cos

ACE Market : 116 cos

Market Cap @ 30 Apr 11 :

RM1,310 bil (USD442 bil)

Products : Shares, REITs,

Warrants, ETFs, CBBCs,

Loans & Bonds

Focus :

Drive Liquidity &

Vibrancy

Focus :

Leverage On Existing

Strategic Partnership

Focus :

Attract International

Investors & Issuers

SECURITIES DERIVATIVES ISLAMIC OFFERINGS OTHERS

Bond Market

Electronic trading

platform for :

Government Bonds

Corporate Bonds

Non-ringgit securities

Sukuk Listing

Offshore Market

LISTING

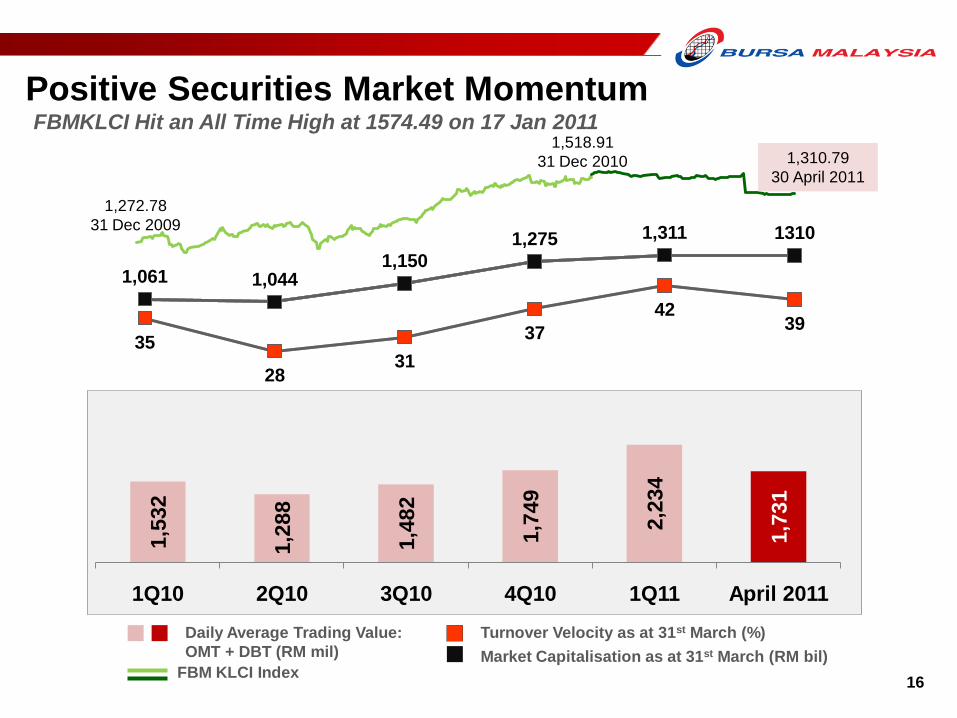

1,061 1,0441,150

1,275 1,311 1310

35

2831

37

4239

1,518.91

31 Dec 2010 1,310.79

30 April 2011

Positive Securities Market MomentumFBMKLCI Hit an All Time High at 1574.49 on 17 Jan 2011

1,5

32

1,2

88

1,4

82

1,7

49

2,2

34

1,7

31

1Q10 2Q10 3Q10 4Q10 1Q11 April 2011

Daily Average Trading Value:

OMT + DBT (RM mil)

Turnover Velocity as at 31st March (%)

Market Capitalisation as at 31st March (RM bil)FBM KLCI Index

1,272.78

31 Dec 2009

16

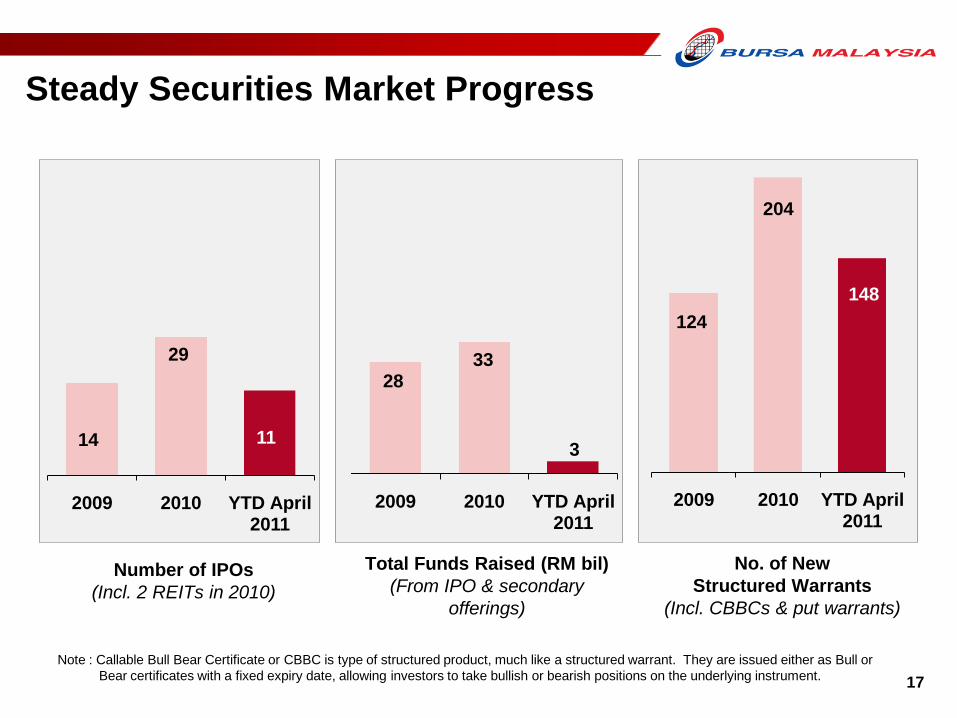

14

29

11

2009 2010 YTD April 2011

2833

3

2009 2010 YTD April 2011

124

204

148

2009 2010 YTD April 2011

Steady Securities Market Progress

No. of New

Structured Warrants

(Incl. CBBCs & put warrants)

Number of IPOs

(Incl. 2 REITs in 2010)

Total Funds Raised (RM bil)

(From IPO & secondary

offerings)

Note : Callable Bull Bear Certificate or CBBC is type of structured product, much like a structured warrant. They are issued either as Bull or

Bear certificates with a fixed expiry date, allowing investors to take bullish or bearish positions on the underlying instrument. 17

Increasing Interest in the Derivatives MarketFCPO open interest hits all-time high at 112,921 contracts on May 9

23,8

89

22,5

17

25,1

11

24,2

55

36,7

85

31,9

00

1Q10 2Q10 3Q10 4Q10 1Q11 April 2011

128,988

114,820 113,565

132,151 136,202

151,812

Daily Average Contracts 1Q11 1Q10 Δ% 4Q10 Δ%

FCPO 25,606 15,794 62 17,030 50

FKLI 10,274 7,316 40 7,065 45

Daily Average Contracts (Units) Open Positions

18

19

Strengthen

Equity Market

Expand

Derivatives

Market

Widen &

Internationalise

Islamic Market

TO REMAIN COMPETITIVE IN THE REGION

Key Focus for 2011

• Increasing PDTs

• Collaboration of

ASEAN Exchanges

• More BSAS

Participants

• Dual licensing

• New Derivatives

Clearing System

Other initiatives will be updated as we progress throughout the year

19

37

5 55

3

44

4

46

5

48

2 64

0

72

2

69

5 84

9 11

06

87

0

82

4 11

01 12

94

37

983

266

138

20

Securities Market Highlights

FBMKLCI Index & No. of PLCs

Finance

Consumer Products

Industrial Products

Infrastructure Project Cos.

Trading/Services

Diverse Sectors & Products

ETFs

REITs

Loans

Main Market

Call Warrants

ACE Market

14

As at 30 April 2011

5

13 New Listings YTD 15 May 2011

Average Market Capitalisation

Total Listed Companies

FMBKLCI Index

Construction

Plantation571.96

(1 Jan 1998)

1,310.79

(30 Apr 2011)

42%

28%

10%

7%

5%5%

3%

20

736 758798 816

865906

96310211027

987 977 960 957 956

21

Derivatives Market Highlights

25% Equity Stake in

Bursa Malaysia

Derivatives (BMD)

Licensing of FCPO

Prices to CME

Technology

Partnership

BMD will partner

CME in ASEAN in

market and

technology

development

Joint product

development and

marketing

Human capital

development

Strengthen

Malaysia’s position

as the global price

benchmark for CPO

Ensure price

discovery for palm

oil remains in

Malaysia

Global distribution of

Malaysian derivatives

products via Globex

TPs connected directly

to CME Globex® and

are able to trade CME

products*

TPs can now market

Malaysian derivatives

products in the US

Completed acquisition

and group

restructuring of BMD

CME USD Palm Oil

Contract launched 24

May 2010

Migrations of BMD’s products

to CME Globex® trading

platform in September 2010

* Subject to them having a clearing relationship with a CME Clearing Futures Commission Merchant (FCM)

21

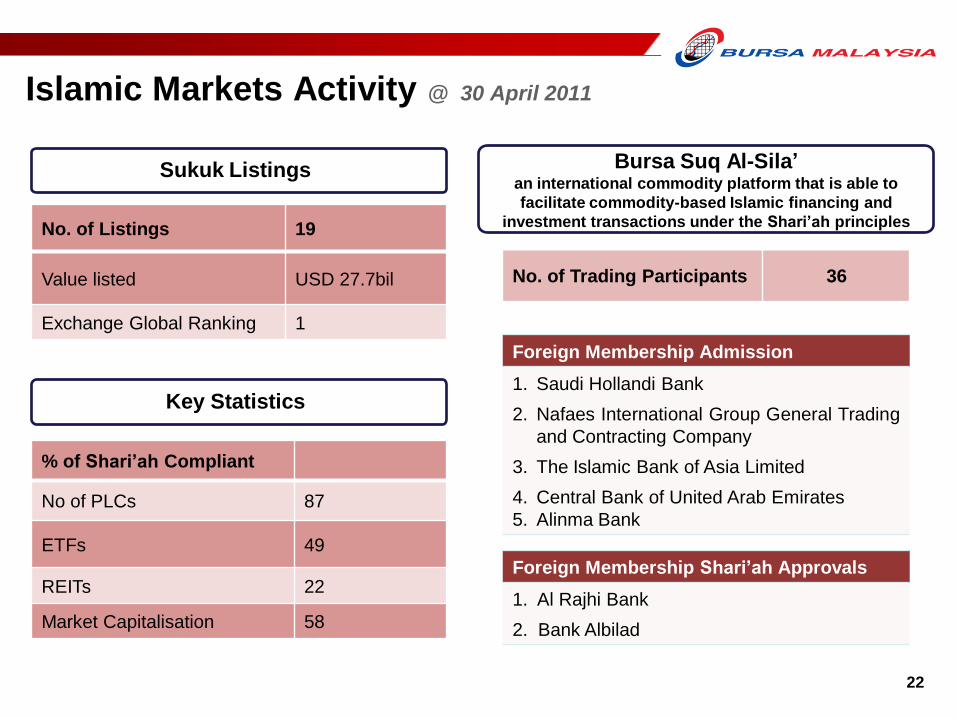

22

Bursa Suq Al-Sila’an international commodity platform that is able to

facilitate commodity-based Islamic financing and

investment transactions under the Shari’ah principles No. of Listings 19

Value listed USD 27.7bil

Exchange Global Ranking 1

Sukuk Listings

Foreign Membership Admission

1. Saudi Hollandi Bank

2. Nafaes International Group General Trading

and Contracting Company

3. The Islamic Bank of Asia Limited

4. Central Bank of United Arab Emirates

5. Alinma Bank

Foreign Membership Shari’ah Approvals

1. Al Rajhi Bank

2. Bank Albilad

% of Shari’ah Compliant

No of PLCs 87

ETFs 49

REITs 22

Market Capitalisation 58

Key Statistics

No. of Trading Participants 36

Islamic Markets Activity @ 30 April 2011

22

Solid

Foundation

People, Sound Regulatory Framework, Technologies

Strong Stakeholders’ Support

Five

Strategic

ThrustsRevitalising

the market

Improving the

Ecosystems

Development

of world class

workforce.

Improvement of

efficiency &

productivity

Inter-

nationalising

the Market

A preferred Partner in Asia for Fund Raising,

Trading and Investment

Vision

1 2 3 4 5

23

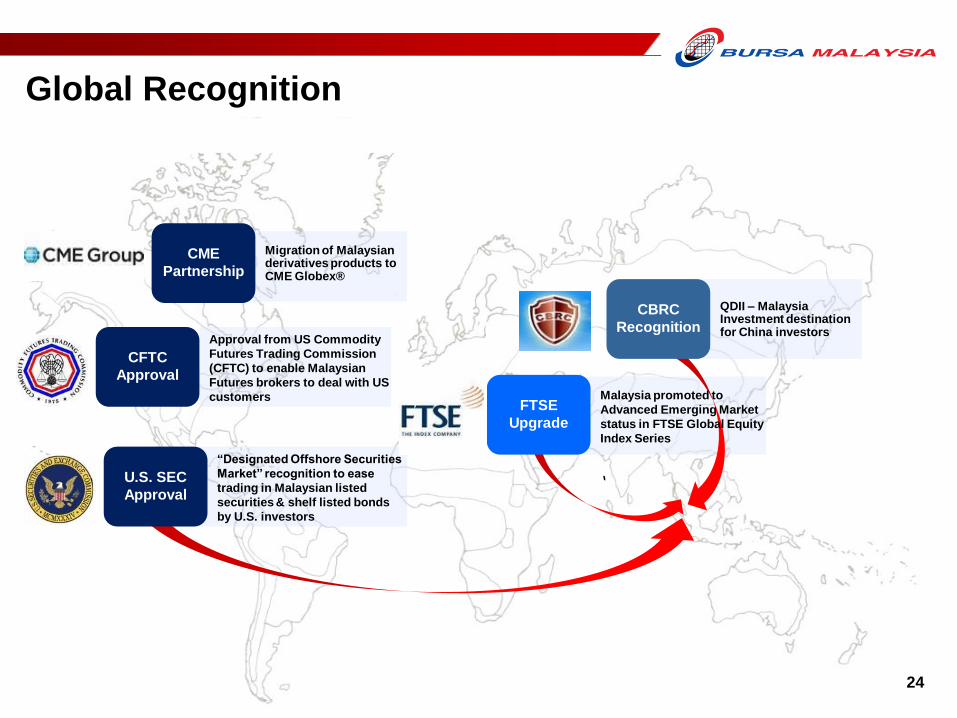

Setting Priorities and Areas for Growth

Global Recognition

Migration of Malaysian derivatives products to CME Globex®

QDII – Malaysia Investment destination for China investors

CBRC

Recognition

FTSE

Upgrade

CFTC

Approval

U.S. SEC

Approval

“Designated Offshore Securities

Market” recognition to ease

trading in Malaysian listed

securities & shelf listed bonds

by U.S. investors

CME

Partnership

Malaysia promoted to

Advanced Emerging Market

status in FTSE Global Equity

Index Series

24

Approval from US Commodity

Futures Trading Commission

(CFTC) to enable Malaysian

Futures brokers to deal with US

customers

25

Positive Prospect & Outlook

Barring any adverse developments, we expect improved level of activity in our markets

and financial results for the financial year ending 31 December 2011.

Potential Market

Catalysts

Acceleration in the implementation of various economic transformation

programmes.

Greater M&A activities & government transformation programmes.

Prospects for further divestments by government-linked companies.

Bursa remains committed in ensuring markets continues to be sustainable and vibrant

despite increasing volatility from external factors.

Malaysia’s strong economic fundamentals.

Liberalisation efforts by the government.

Sustained domestic corporate earnings growth attracting portfolio inflows.

Strong and Solid

System

Progressive

Developmental

Efforts

We continue to invest in the development of the capital market and the

regulatory environment.

And at the same time, putting a close watch on our expenditure.

25

Financial Review

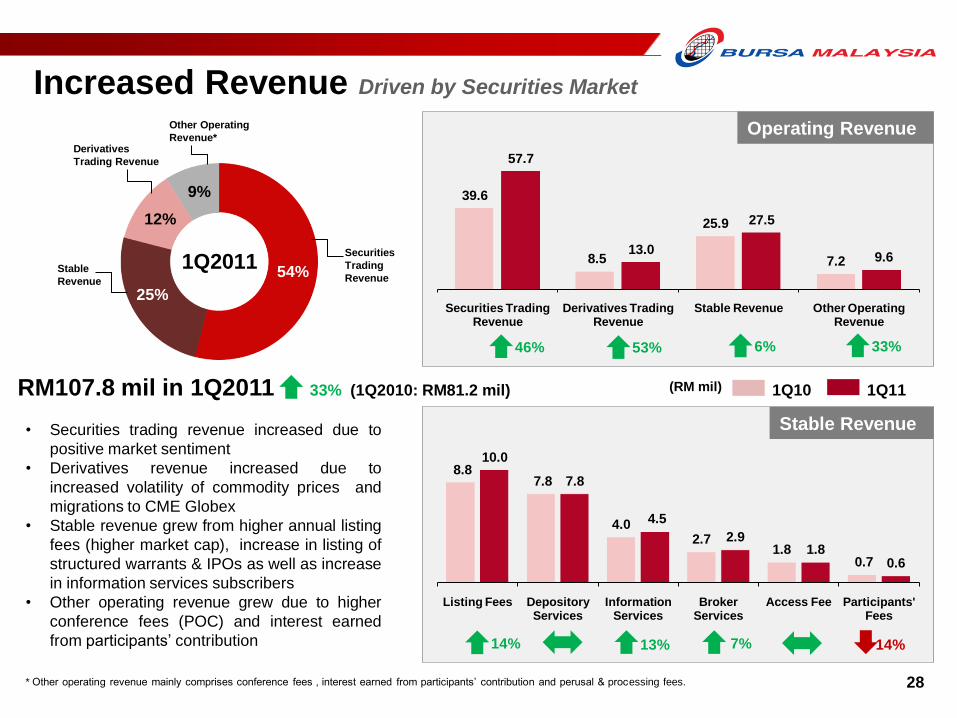

Improved Financial Performance 27

Increased Revenue 28

Higher Operating Expenses 29

Sustainable Performance Ratios 30

Dividend Payout 31

Strong Reserves 32

26

Improved Financial Performance

Operating Revenue

(RM mil)

Other Income

(RM mil)

81.2 1

07.8

1Q10 1Q11

6.9 8.3

1Q10 1Q11

48.4 5

7.8

1Q10 1Q11

29.0

41.9

1Q10 1Q11

5.3

7.6

1Q10 1Q11

Operating Expenses

(RM mil)

PAT

(RM mil)

Earnings Per Share

(sen)

33%

20%

19%

44%

43%

27

1Q10

54%

25%

12%

9% 39.6

8.5

25.9

7.2

57.7

13.0

27.5

9.6

Securities Trading Revenue

Derivatives Trading Revenue

Stable Revenue Other Operating Revenue

8.8 7.8

4.02.7

1.80.7

10.0

7.8

4.5

2.91.8

0.6

Listing Fees Depository Services

Information Services

Broker Services

Access Fee Participants' Fees

Operating Revenue

Increased Revenue Driven by Securities Market

28* Other operating revenue mainly comprises conference fees , interest earned from participants’ contribution and perusal & processing fees.

1Q2011

46% 6% 33%53%

RM107.8 mil in 1Q2011 33% (1Q2010: RM81.2 mil)

• Securities trading revenue increased due to

positive market sentiment

• Derivatives revenue increased due to

increased volatility of commodity prices and

migrations to CME Globex

• Stable revenue grew from higher annual listing

fees (higher market cap), increase in listing of

structured warrants & IPOs as well as increase

in information services subscribers

• Other operating revenue grew due to higher

conference fees (POC) and interest earned

from participants’ contribution

Stable Revenue

(RM mil) 1Q11

14% 7%13%

Other Operating

Revenue*

Securities

Trading

RevenueStable

Revenue

Derivatives

Trading Revenue

14%

28

`

45%

17%

9%

12%

4%

2%11%

29

21.5

11.1

4.83.6

2.50.5

4.4

25.9

9.9

5.46.8

2.61.0

6.2

• Other OPEX comprises administrative expenses, CDS consumables & other miscellaneous expenses..

1Q2011

Staff Cost

Depreciation & Amortisation

(D & A)

Market Development

Technology Charges

Building Management Costs

Professional Fees

Other OPEX

Higher Operating Expenses Talent Investment for Future Growth

(RM mil) 1Q10 1Q11

RM57.8 mil in 1Q2011 19% (1Q2010: RM48.4 mil)

Staff Cost D&A Market

DevelopmentTechnology

Charges

Building

Management

Costs

Professional

Fees

Other OPEX

20% 11% 12% 40%89% 3% 100%

• Higher staff costs due to increased headcount as well as talent attraction &

development.

• Higher technology charges due to Globex service fee charged by CME (RM3 mil) for

the use of Globex electronic trading platform which commenced in September 2010.

• Operating expenses increase was further attributable to a write off of computer

software, the postage hike in July 2010 which raised the cost of CDS consumables,

higher market development expenses and higher consultancy fees.

29

`

33.0

54.0

13.1

36.1

55.6

18.6

Net Profit Margin Operating EBITDA Margin

Return on Equity

30

Sustainable Performance Ratios

(%)

9%

1Q10 1Q11

42%3%

30

31 31

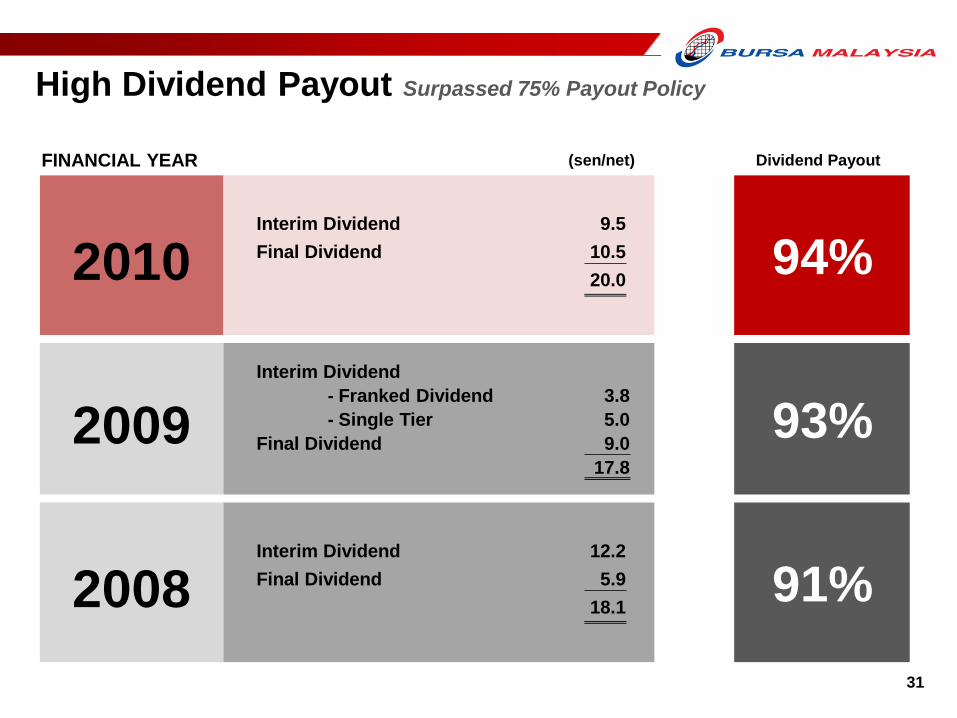

High Dividend Payout Surpassed 75% Payout Policy

(sen/net) Dividend Payout

2010 94%

FINANCIAL YEAR

2009

Interim Dividend 9.5

Final Dividend 10.5

20.0

Interim Dividend

- Franked Dividend 3.8

- Single Tier 5.0

Final Dividend 9.0

17.8

2008 91%Interim Dividend 12.2

Final Dividend 5.9

18.1

93%

`

870

886

1Q10 1Q11

(RM mil)

504

594

1Q10 1Q11

32

Strong Reserves

Shareholders’ Fund

Financial Resources

Available for Use

(RM mil)

2%

18%

`

`

The Company has sufficient financial resources to cover its Clearing

Guarantee Fund commitment, CAPEX and working capital requirements. 32

Additional Information

Board of Directors & Shareholdings Structure 34

Securities Market Trading Activity 35

Securities Market Trading Participation 36

Securities Market Foreign Ownership 37

Peer Comparison for 1Q 2011 38

Bursa’s Potential To Grow Its Velocity 39

Derivatives Market Activity 40

Derivatives Market Demography 41

Sound Macro Environment 40

34

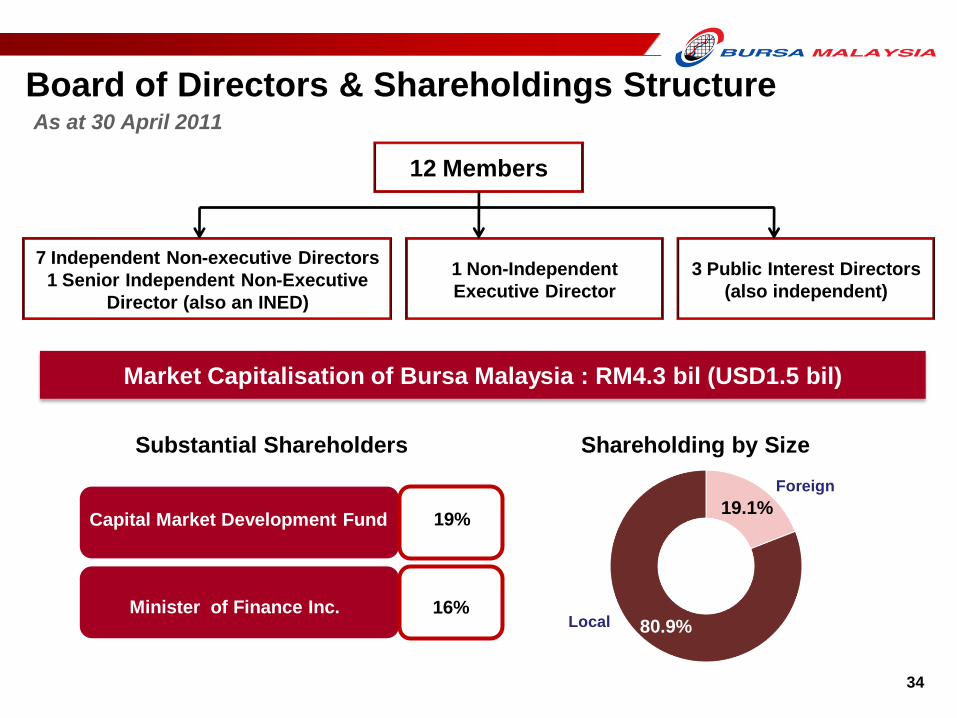

Board of Directors & Shareholdings StructureAs at 30 April 2011

12 Members

7 Independent Non-executive Directors

1 Senior Independent Non-Executive

Director (also an INED)

1 Non-Independent

Executive Director

3 Public Interest Directors

(also independent)

19.1%

80.9%

Foreign

Local

Substantial Shareholders Shareholding by Size

Minister of Finance Inc.

Capital Market Development Fund

16%

19%

Market Capitalisation of Bursa Malaysia : RM4.3 bil (USD1.5 bil)

34

1,924

497

805 911

350 472

748 874

718

1,019

2,179

1,181 1,129 1,403

2,032

-

400

800

1,200

1,600

2,000

2,400

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 YTD Apr

2011

RM mil

Annual DATV & Velocity57%

31%40% 39%

20%23%

34% 32%

25%

34%

53%

34% 34% 33%39%

68%

54%50%

41%46%

31%25%

32%

23%

48%

36%

28%

35%

28%31%

37%42%

2,610 2,303

2,069 1,751

1,907

1,187

823 854 615

1,490 1,266

1,099 1,435 1,209

1,387

1,566

2,161

-

400

800

1,200

1,600

2,000

2,400

2,800

1Q07 2Q07 3Q07 4Q07 1Q08 2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10 4Q10 1Q11

RM mil

Securities Market Trading Activity

Quarterly DATV & Velocity

Daily Average Trading Value (RM mil) Turnover Velocity

Daily Average Trading Value (RM mil) Turnover Velocity

35

346

806

283 373 378

569

34 37

24

3326 28

66 63 76 67 74 72

2006 2007 2008 2009 2010 YTD April 2011

Securities Market Trading Participation

From 2006 to 2009, the statistics were based on Brokers’ submission. From 2010 onwards statistics were based on Bursa’s internal system.

65 6358

73 7377

35 37 42 27 27 23

2006 2007 2008 2009 2010 YTD April 2011

Retail

(%)

Institutions

(%)Local

(%)

Foreign

(%)

Retail DATV

(RM mil)Foreign DATV

(RM mil)

357

806

496

305393

467

Retail vs Institutions Foreign vs Local

36

37

Securities Market Foreign Ownership

7.8%

1.9%

0.9%

0.4%

0.1%

13.2%

Singapore

Hong Kong

UK

USA

Mid-East

Others

25.8%

74.2%

Foreign Ownership by Nationality

Foreign Nominees

Based on Market Capitalisation

(as at month end)

26.5

25.7

24.1

21.7

20.9

20.7

20.7

20.9

20.4

20.4

20.6

20.8

21.8

21.9

22.0

21

.4

Mar

2011

%

1.6%China / Taiwan

37

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

Colo

mbo S

E

Shanghai S

E

Kore

a E

xchange

Thaila

nd S

E

Hong K

ong

Austr

alia

n S

E

Shenzhen S

E

Indonesia

SE

Phili

ppin

e S

E

Sin

gapore

…

Osaka S

E

Tokyo S

E G

roup

Taiw

an S

E C

orp

.

National S

tock …

Bom

bay S

E

-6

-4

-2

0

2

4

Shanghai S

E

Kore

a

Austr

alia

Thaila

nd

Hong K

ong

Shenzhen S

E

Indonesia

Osaka

Taiw

an

Colo

mbo

Sin

gapore

National S

E I

ndia

Bom

bay S

E

Tokyo S

E

Peer Comparison for 1Q 2011

Funds Raised

Asian Benchmark Index Growth % Asian Market Capitalisation Growth %

Source: World Federation Exchanges (WFE)

Mala

ysia

2%

Mala

ysia

2%

USD909 mil

Mala

ysia

0

5

10

15

20

25

30

Shenzhen S

E

Shanghai S

E

Hong K

ong …

Tokyo S

E G

roup

Sin

gapore

…

Austr

alia

n S

E

National S

tock …

Indonesia

SE

Thaila

nd S

E

Kore

a E

xchange

Taiw

an S

E C

orp

.

Colo

mbo S

E

Phili

ppin

e S

E

Bom

bay S

E

Osaka S

E

Billion

38

London SE

39

Hong Kong Exchanges

262%

182%

127%

126%

115%

106%

87%

75%

71%

58%

55%

50%

47%

38%

31%

16%

Source: World Federation Exchanges (WFE)

YTD April 2011

Philippine SE

Bursa Malaysia

Indonesia SE

Singapore SE

The Stock Exchange of Thailand

National Stock Exchange India

Taiwan SE Corp.

Tokyo SE

NYSE Euronext (Europe)

Australian SE

Shanghai SE

Korea Exchange

NYSE Euronext (US)

Shenzhen SE

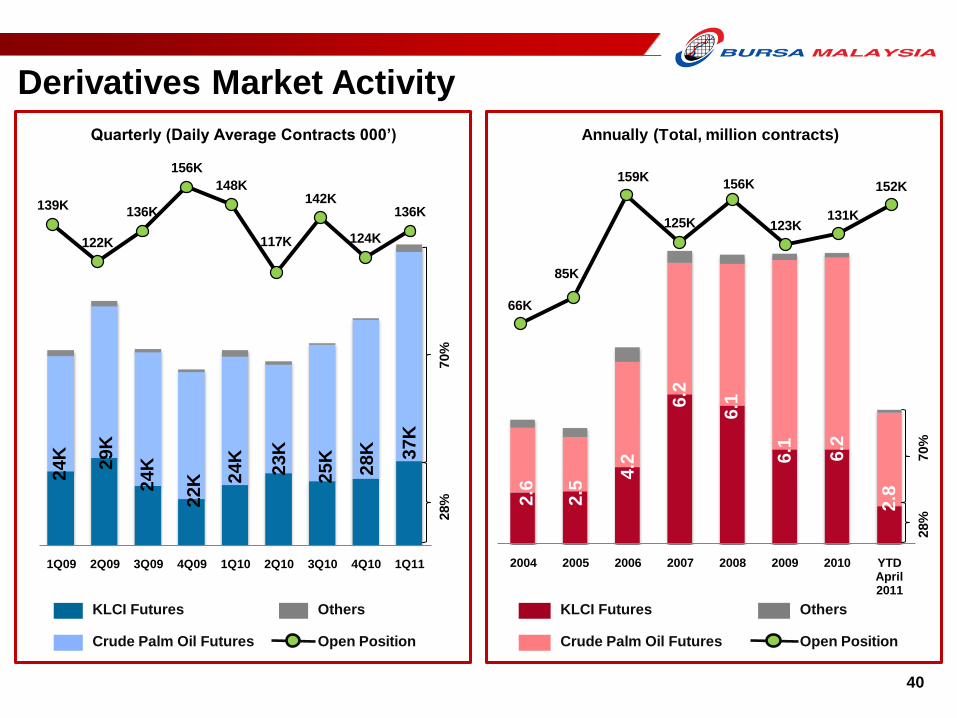

Bursa’s Potential To Grow Its Velocity

139K

122K

136K

156K

148K

117K

142K

124K

136K

1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10 4Q10 1Q11 2004 2005 2006 2007 2008 2009 2010 YTD April 2011

66K

85K

159K

125K

156K

123K131K

152K

40

Derivatives Market Activity

2.6

2.5

4.2

6.1

6.1 6.2

Annually (Total, million contracts)

KLCI Futures

Crude Palm Oil Futures Open Position

Others

28%

24K

29K

24K

70%

Quarterly (Daily Average Contracts 000’)

KLCI Futures

Crude Palm Oil Futures Open Position

Others

22K

2.8

24K

28%

70%

25K

23K

28K 37K

6.2

40

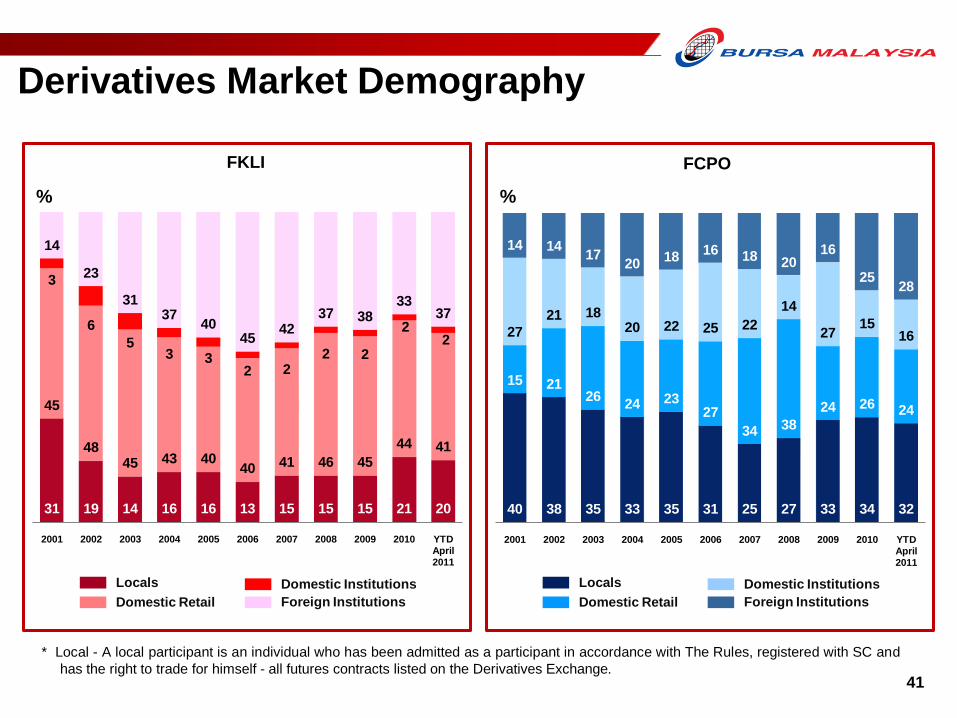

Derivatives Market Demography

* Local - A local participant is an individual who has been admitted as a participant in accordance with The Rules, registered with SC and

has the right to trade for himself - all futures contracts listed on the Derivatives Exchange.

31 19 14 16 16 13 15 15 15 21 20

45

4845 43 40

40 41 46 45

44 41

3

6

53 3

2 22 2

22

14

23

3137

4045

4237 38

3337

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 YTD April 2011

%

FKLI

Locals

Domestic Retail

Domestic Institutions

Foreign Institutions

40 38 35 33 35 31 25 27 33 34 32

15 2126

24 2327

34 38

24 26 24

27

21 1820 22 25 22

14

2715

16

14 1417

2018

16 18 2016

2528

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 YTD April 2011

%

FCPO

Locals

Domestic Retail

Domestic Institutions

Foreign Institutions

41

KOAY LEAN LEE

603-2034 7306

Disclaimer :

Bursa Malaysia and its Group of Companies (the Company) reserve all proprietary rights to the contents of this Presentation.

Whilst the Company endeavours to ensure that the contents in the presentation booklet are accurate, complete or have been obtained from sources believed

by the Company to be accurate and reliable, neither the Company nor the Presenter make any warranty, express or implied, nor assume any legal liability or

responsibility for the accuracy, completeness or currency of the contents of this Presentation.

In no event shall the Company be liable for any claim, howsoever arising, out of or in relation to this presentation booklet to the recipient of this presentation

booklet and/or to any other third party.

© Bursa Malaysia 2011

INTAN DIYANA TAJUDIN

603-2034 7049

INVESTOR RELATIONS CONTACT INFORMATION

E-mail : [email protected]

Fax : 603-2026 3684

MUHAMMAD ALI

603-2034 7673

![Setia Insight Nov07-Part1[1]](https://static.fdocuments.in/doc/165x107/577d26f61a28ab4e1ea2ab8e/setia-insight-nov07-part11.jpg)