Bunzl Business Case

24

Business Case May 2015

-

Upload

rick-mcmillen -

Category

Documents

-

view

118 -

download

0

Transcript of Bunzl Business Case

Business CaseMay 2015

About us

Bunzl is a growingand successful Group providing outsourcing solutions and value added distribution across the Americas, Europe and Australasia

Business Case May 2015 1

Source Consolidate Deliver

Business overview

2

Sales channel

Products

Sourcing

Footprint

Key facts

Financials

Business to business distribution

£6.2bn revenue in 2014

Wide range of non-food consumable products

From leading brand manufacturers

Own brands and unbranded products

Sourcing centre in Shanghai – no own manufacturing

c.15,000 employees (2014 year end)

International diversification: 28 countries, 4 continents

UK plc headquartered in London

Listed on LSE; FTSE 100; Support Services sector

Revenue growth: 10% (CAGR 04-14)

Adjusted operating profit growth*: 10% (CAGR 04-14)

Average annual cash conversion† of 97% (04-14)* Before intangible amortisation and acquisition related costs† Operating cash flow before acquisition related costs to operating profit before intangible amortisation and acquisition related costs

2004-2005 continuing operations only

Business Case May 2015

Benefits to customers:Supply Chain

Supported byan integratedIT platform

Customer

Global sourcing& procurement

International warehousing& distribution infrastructure

3

Consolidationof consumables

Range of delivery options

Business Case May 2015

Value proposition

In-house procurement andself distribution is costly

Bunzl applies its resourcesand expertise to reduce or eliminate many of the “hidden” costs of in-house procurement and self distribution

The benefits to customers area lower cost of doing business and reduced working capital and carbon emissions

Outsourcingadds value forour customers

4

Product cost

Inventory investment

Cash flow

Direct labour & overtime

Inventory finance cost

Expedited orders

Inbound freight

Purchase order administration

Inventory damage & shrinkage

Accounts payable admin

Storage space

Capital employed

Cost to acquire

Cost to process

Business Case May 2015

Market environment

5

Growing market sectors Fragmented competitors

Customer baseOutsourcing trend

Exposed to growing sectors including

– Foodservice – away from home

– Cleaning & hygiene – away from home

– Healthcare – demographics

– Safety – increased legislation

None do what we do, on our scale and across our markets

Bunzl’s national footprint provides competitive advantage

Strong customer base

Working with national and international leaders

Aligned with customer growth

Customers and manufacturers focusing on their core business

Multiple growth drivers

Business Case May 2015

Operatingmodel efficiencies

We constantly striveto make our business more efficient and environmentally friendly

Acquisition growth

Since 2004 we have announced 100 acquisitions with total spend of £1.9bn

Organic growth

By outsourcing to Bunzl the purchase, consolidation and delivery of a broad range of products our customers achieve efficiencies and savings

Consistent and proven strategy

ROIC

17.6%

6

High ROICdespite significant acquisition spend

Business Case May 2015

Key competitive advantages

7

A platform for growth

Unique

business

model

Strong

financial

discipline

Acquisition

strategy &

track record

Operational

focus

Experienced

management

Global

sourcing

Attractive

customer

markets

Balanced

business

portfolio

Business Case May 2015

Business model

One-stop-shopfor non-food consumables

8

Source

Consolidate

Deliver

Global suppliers

Low cost sources

Commodities

Own brands

Foodservice GroceryCleaning& hygiene

Retail Safety Healthcare

Individual ranges

to

Consolidated offer

to

Business Case May 2015

Attractive customer markets

28%

26%13%

12%

11%

7%3%

HealthcareDisposable healthcare consumables, including gloves, swabs, gowns and bandages and other healthcare related equipment to hospitals, care homes and other facilities serving the healthcare sector.

SafetyA complete range of personal protection equipment, including hard hats, gloves, boots, ear and eye protection and other workwear, to industrial and construction markets.

RetailGoods not for resale, including packaging and other store supplies and a full range of cleaning and hygiene products, to department stores, boutiques, office supply companies, retail chains and home improvement chains.

Cleaning & hygieneCleaning and hygiene materials, including chemicals and hygiene paper, to cleaning and facilities management companies and industrial and healthcare customers.

FoodserviceNon-food consumables, including food packaging, disposable tableware,guest amenities, catering equipment, cleaning products and safety items, to hotels, restaurants, contract caterers, food processors and the leisure sector.

GroceryGoods not for resale (items which are used but not actually sold), including food packaging, films, labels and cleaning and hygiene supplies, to grocery stores, supermarkets and retail chains.

OtherA variety of product ranges supplied to other end user markets such as government and education establishments.

9Business Case May 2015

c.75% resilient Grocery FoodserviceCleaning & hygiene Healthcare

2014 FY Revenue

Typical Products

10

A broad range of non-food consumable products

Business Case May 2015

Balanced business portfolio

11

Geographic balance

Our markets are at different stages of maturity

National footprints

International brands and local products

Regional diversification

Customer markets balance

Six market sectors with numerous sub-sectors

Products and markets – specialist distributors

Direct to customer or through a sub-distributor

Diversified by geography and sector

55%

19%

17%

9% North America

Continental Europe

UK & Ireland

Rest of the World

Business Case May 2015

2014 FY Revenue

Operational focus

12

Hands on management with clear customer focus

Full P&L and working capital responsibility

Aligned incentive measurement with profit and ROCE

Decentralised operating structure

Investing

Majority of capex spend on IT systems and warehouse facilities

Robust IT and systems strategy e.g. warehouse management

Order systems and vehicle routing

Continually evaluating and upgrading our warehousing

Sharing best practice across all business areas

Business Case May 2015

Global sourcing

13

+Own brands

Commodities

Low cost sources

Eco-friendly products

SourcingPreferred suppliers

Business Case May 2015

Acquisition strategy

14

Key acquisition parameters

Acquisition types

Business to business

Consolidated “not-for-resale” product offering

Resilient and growing markets

Fragmented customer base

Scope for further consolidation and synergies

Small % of total customer spend

Opportunity for “own label” products

Attractive financial returnsRetention of managers and customers is key

Anchor

– New geographies

– New markets

Bolt-on – existing geography and market

– Extending product range

– Consolidating markets

Extracting value

Purchasing synergies

Warehouse & distribution efficiencies

Back office integration

Customer overlays

Product range extensions

Sharing best practice

Investment in infrastructure

Business Case May 2015

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Number of

acquisitions7 7 9 8 7 2 9 10 13 11 17

Committed

acquisition

spend (£m)

302 129 162 197 123 6 126 185 277 295 211

Annualised

acquisition

revenue (£m)

430 270 386 225 151 27 154 204 518 281 223

Acquisition growth

15

04-05 continuing operations only

Average annual acquisition spend over the last 3 years

£261m

Business Case May 2015

2014

Geographic expansion timeline

16

1997*

7 countries

2003*

12 countries

2015

28 countries

2008

23 countries

2005*

18 countries

Revenue

2010

North America Continental Europe UK & Ireland Rest of the world

2005*

* Continuing operations only

Business Case May 2015

Experienced management

17

Experienced executive directors and management team

Brian May

Finance Director

Michael Roney

Chief ExecutivePatrick Larmon

President and

CEO North

America

Celia Baxter

Director of Group

Human

Resources

Paul Hussey

General Counsel

& Company

Secretary

Paul Budge

Managing

Director UK &

Ireland

Andrew Mooney

Director of

Corporate

Development

Frank van Zanten

Managing

Director

Continental

Europe

Rodrigo

Mascarenhas

Managing

Director Latin

America

Kim Hetherington

Managing

Director

Australasia

Business Case May 2015

Strong financial discipline

18

High return on capital

Strong balance sheet

Low working capital requirements

Low capex

High free cash flow yield

Uniform financial reporting system

Return on operating capital: 57.7% Return on invested capital (pre-tax): 17.6%

(2014)

Net debt/EBITDA 1.9x year end 2014

Average working capital to sales at 10% in 2014

Average of £23m p.a. over past 3 years

Operating cash flow† to adjusted operating profit* average of 97% 2004 - 2014

Across all geographies

†Before acquisition related costs

*Before intangible amortisation and acquisition related costs

Growing dividend stream

Dividend per share CAGR of 10% since 2004

Business Case May 2015

Cash conversion*

19

93% 95%92%

103%

92%

102%

93%

110%

93%

102%

95%

04 05 06 07 08 09 10 11 12 13 14

* Operating cash flow before acquisition related costs to adjusted operating profit

04 - 05 continuing operations only

90%

Average cash conversion* of

funds growing dividend and acquisitions

97%

Business Case May 2015

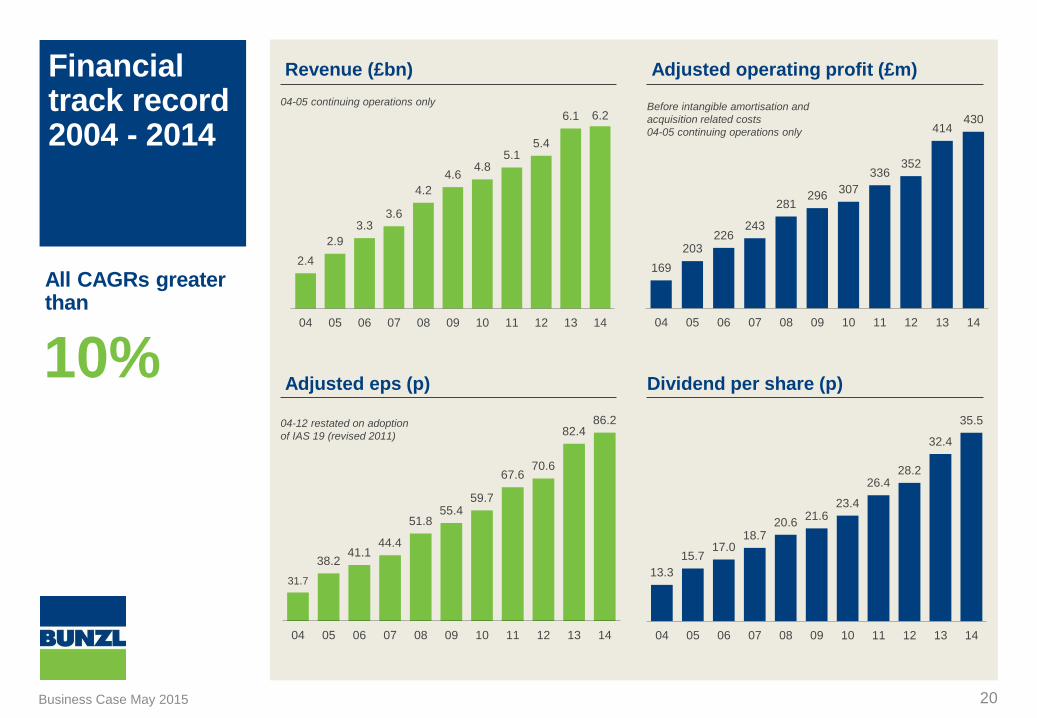

Revenue (£bn)Financial track record 2004 - 2014

20

2.4

2.9

3.33.6

4.2

4.64.8

5.15.4

6.1 6.2

04 05 06 07 08 09 10 11 12 13 14

31.7

38.241.1

44.4

51.855.4

59.7

67.670.6

82.486.2

04 05 06 07 08 09 10 11 12 13 14

Adjusted eps (p)

Adjusted operating profit (£m)

Dividend per share (p)

All CAGRs greater than

04-05 continuing operations only

04-12 restated on adoption

of IAS 19 (revised 2011)

169

203226

243

281296

307

336352

414430

04 05 06 07 08 09 10 11 12 13 14

Before intangible amortisation and

acquisition related costs

04-05 continuing operations only

13.3

15.717.0

18.720.6

21.623.4

26.428.2

32.4

35.5

04 05 06 07 08 09 10 11 12 13 14

10%

Business Case May 2015

Business case summary

21

Clear strategy for growth

Entering new markets/product groups Expansion/penetration of established

markets Strong operational focus

Attractive business model

Strong business model

Clear value added for customers and suppliers

Recurring revenues “Big in the middle”

Attractive markets

Resilient and growing markets Multiple growth drivers Fragmented with opportunity to

consolidate

Balanced portfolio

Product diversification Geographical presence Independence from customers and

suppliers

Robust financial performance

Consistent revenue and earnings growth High cash generation Cash reinvested at high return on capital Strong and growing dividend stream

Business Case May 2015

Contacts

22

Bunzl plc+44 20 7725 5000

Michael Roney – Chief ExecutiveBrian May – Finance Director

Business Case May 2015

Disclaimer

23

No representation or warranty (express or implied) of any nature can be given, nor is any

responsibility or liability of any kind accepted, by Bunzl plc with respect to the completeness or

accuracy of the content of or omissions from this presentation.

This presentation is for information purposes only and does not constitute and shall not be deemed

to constitute an offer document or an offer in respect of securities or an invitation to purchase or

subscribe for any securities in any jurisdiction. Persons in a jurisdiction other than the United

Kingdom should ensure that they inform themselves about and observe any relevant securities laws

in that jurisdiction in respect of this presentation.

The presentation does not constitute an offer of securities for sale in the United States. None of the

securities described in the presentation have been registered under the U.S. Securities Act of 1933.

Such securities may not be offered or sold in the United States except pursuant to an exemption

from such registration.

This presentation contains forward-looking statements. They are subject to risks and uncertainties

that might cause actual results and outcomes to differ materially from the expectations expressed in

them. You are cautioned not to place undue reliance on such forward-looking statements which

speak only as of the date hereof. Bunzl undertakes no obligation to revise or update any such

forward-looking statements.

Where this presentation is being communicated as a financial promotion it will only be made to and

directed at: (i) those persons who have professional experience in matters relating to investments

falling within Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion)

Order 2005 (the “Order”); (ii) those persons falling within Article 49 of the Order; or (iii) to persons

outside of the United Kingdom only where permitted by applicable law (all such persons together

being referred to as “relevant persons”) and must not be acted on or relied on by persons who are

not relevant persons.

Business Case May 2015