Bulgaria Doing Business Guide

52

DOING BUSINESS GUIDE BULGARIA

Transcript of Bulgaria Doing Business Guide

DOING BUSINESS GUIDE BULGARIA

2 This Guide is prepared by Popov & Partners law firm, a member of TAGLaw

3

Introduction 4 WhyBulgaria? 4

Promotionofforeigninvestments 5Supportedsectors 5Investmentincentives 6Conditionsforinvestmentpromotion 7Minimuminvestmentthreshold 8Priorityinvestmentprojects 9

Taxandsocialsecuritylegislation 10Advantages 10Taxes 12Socialsecuritysystem 20

Tradelegislation 22 Legalandorganizationalformsforstructuringofabusiness 23

Limitedliabilitycompany(LTD/ООД) 24Lointstockcompany(LSC/АД) 24Jointstockspecialpurposeinvestmentcompany(JSSPIC/АДСИЦ) 25Cooperative 25Partnership(Consortium) 26Branch 26Representation 26Peculiaritiesinthestructuringofspecificbusinessactivities 27Otherformsofstartingabusinessthroughalocalpartner 27

MergersandAcquisitions 28Transformation 28Acquisitions 29Transferofacommercialenterprise 30Controlofmergersandacquisition 30AdministrativecostsofinvestmentinBulgaria 31

Commercialdisputes 32 Regulationofadvertising 33 Electroniccommerceandvirtualcurrency 33 Internationalmoneytransfers 34 Employmentrelationship 34

Requirementforstaffrecruitment 35Executionofemploymentcontracts 36Typesofemploymentcontractsandemploymentschemes 36Laying-offworkforce 37Labourexpenses 38Employmentfundingoptions 39

Realestateinvestmentregime 39 Investmentinruraldevelopment 40 Publicprocurementlegislation 41

Computerizationofthepublicprocurementprocedure 42Publicprocurementawardprocedures 42

Concessionlegislation 43Typesofconcessions 44Procedureforselectionofconcessionaire 44

Intellectualproperty 45Industrialproperty 45Copyright 47

ResidenceofforeignersintheRepublicofBulgaria 48TypesofresidenceofforeignersintheRepublicofBulgaria 49

CONTENT

4 This Guide is prepared by Popov & Partners law firm, a member of TAGLaw

BulgariaisacountryinSoutheasternEuropelocatedontheBalkan Peninsula, bordering on Greece and Turkey to thesouth, Macedonia and Serbia to the west, Romania to thenorthandtheBlackSeatotheeast.Bulgariaisaparliamentaryrepublic,memberoftheEuropeanUnion, NATO and the Council of Europe, one of thefoundersof theOrganization forSecurity andCooperationinEurope(OSCE).The population of the country is over 7 million people, as

61.8%ofitisatworkingage(25-64yearsold).ThecapitalofBulgariaisthecityofSofia.Withapopulationofmorethan2millionpeoplethecityconcentrates1/4oftheworkforceofthecountryand1/6oftheannualproductionor34.3%ofBulgaria‘sGDP.Inthecapitalcity16languageschools with business orientation are located as well as 18foreign language schoolswitha focus in the fieldof IT,21high schools, fromwhichmore than20 thousand studentsgraduateeveryyear.

Introduction

Why Bulgaria?Despite being an EU member since 8 years, Bulgaria isstill poorly recognizable as an investment destination.Nevertheless, in recent years, investor interest to Bulgaria ison the rise.Here are somemajor advantages thatmake thecountryfavourablefordoingbusinessbyforeigncompanies:Low taxes Bulgaria has the most favorable tax regime andthelowestcorporatetaxrateinEurope.ThecorporatetaxinBulgariaequals10%of theprofitof legalentities, regardlessofitsamount.Aflatrateof10percentisalsoapplicabletopersonal income taxation of individuals, irrespective of itsamount.

LowlabourcostbuthighlyskilledworkforceThe minimum salary in Bulgaria for the year 2016 is420 BGN (214 EUR). Employers in our country payan average hourly rate of 3.80 EUR. For comparison,the average level for all Member States is 24.60 EUR.The average salary of employees in some of the mostproductive sectors varies within the range between 295and 1012 EUR a month. Meanwhile, Bulgaria offersrelatively high-skilled labor. More than 66% of theeconomically active population have completed tertiaryor secondary specialized education.1 Typical is also theexcellent command of English and German as well asTurkish,Russianandotherlanguages.

GeographicandgeopoliticallocationBulgaria is strategically located in the centre of theBalkanPeninsulaandformspartofthesouthernborderof the EU with Turkey. This makes it an importantarea for four European transport corridors that crossthe country. The harbours on the Black Sea and the

Danube offer reliable and inexpensive transportationof goods and raw materials to and from the country.The remarkable nature of Bulgaria predisposes thedevelopment of sustainable sectors such as tourism(mountainandsea),agriculture,etc.

SecurebusinessenvironmentAcurrencyboardiseffectiveinBulgaria-fixedexchangerateofBGNtotheEUR,whicheliminatesthecurrencyrisk. The fixed rate is: 1.95583 BGN for 1 EUR. Theannualchangeininflationis-1.4%(2014).Thepoliticaland macroeconomic stability ensure good credit ratingandsecurebusinessenvironmentformakinginvestments.Bycomparing189countriesinitsreportontheeconomicprofileofBulgariafortheyear2015,theWorldBankputsitinthefirstcategoryintermsofeaseofbusiness(top38countries),surpassingtheneighbouringcountryRomaniaby10positions.

InnovationtechnologiesBulgarian government encourages technologicalinnovations in a number of economic sectors:Mechatronicsandcleantechnologies,ICTandinformatics,Industry for healthy living and biotechnology, newtechnologies in creative and recreational industries. Forthe implementationof innovations in these areas fundsareenvisagedundertwoOperationalProgrammesfortheperiod2014-2020:InnovationandCompetitivenessandScienceandeducationforsmartgrowth.

1AsperdataoftheNationalStatisticalInstitutefortheyear2014.

5

Supported sectors

Industry: manufacturing, including high-tech industries(chemicals,pharmaceuticalproductsandpharmaceuticalpreparations,computerandcommunicationequipment,electronic and optical products, electrical equipment,machinery and equipment, cars and other vehicles,medicalanddentalinstrumentsandsupplies;

Services: creating software products, activities in thefield of information technology, information services,accounting and auditing activities, tax consulting,professional activities, architectural and engineeringactivities, technical testing and analysis, researchand development, education, human healthcare andmedical&social care activities, warehousing and storage,administrative and ancillary office activities, call centreoperationsandbusinesssupportactivities;

Hotelaccommodationservices.

Promotion of foreign investments Bulgariaoffersanumberofadvantagestoforeigninvestors:

shorter administrative deadlines and individualadministrativeservice;

easedrulesonacquisitionofrightofownershiporlimitedrealrightsoverstateandmunicipalproperty;

financialsupport(stateaid);• taxrelief;• institutionalsupport.Themaximumintensityofstateaidforprojectswitheligiblecosts under € 50 million of large enterprises is determinedat 50% of the total investment costs - for investments infive regions of Bulgaria, and at 25% - for investments inthe Southwest region. These levels may be increased by 20percentagepoints for investmentsmadebysmallenterprisesandby10percentagepoints-bymedium-sizedenterprises.

Northwestern

Southwestern

Northeastern

Southeastern

North

Central

South central

6 This Guide is prepared by Popov & Partners law firm, a member of TAGLaw

Investment incentivesClassA ClassB Measuresimplementedforencouragementofinvestments

Shorterdeadlinesforadministrativeservice

Company „X“ is an investor holding a certificate class„A“ or „B“ for investment projects in the industrialsector. Central and local executive authorities provideadministrativeservices to thecompanywithintime linesthatarebyone-thirdshorterthanthoseprovidedforintherelevantregulations.

Acquisitionofownershiprightorrestrictedrealrightsoverpropertieswithouttenderorcompetition

Company„Y“,holdingacertificateclass„A“or„B“forinvestment,wantstobuyarealproperty-privatemunicipalproperty.Theinvestormaypurchasethepropertywithoutholdingofa tenderorcompetition,after evaluationanddecisionofthemunicipalcouncil.Basedonthedecisionthemayorissuesanorderandconcludesacontractwithcompany„Y“forsaleandpurchaseoftherealproperty.

Financialsupportfortrainingforvocationalqualificationsforthoseemployedinthenewjobs(onlyforinvestmentsinhigh-techactivitiesorinmunicipalitieswithhighunemploymentrate)

Company „Z“ invests in less-favoured area, creating 25new jobs for implementation of the investment project.Theremunerationreceivedbythenewlyemployedworkersis higher than the country-average for the economicactivitybeingperformed.The companyholds certificateclass„A“forinvestment,wherebyithastheopportunityto apply for financial support for training for acquiringprofessionalqualificationofnewstaff(100%ofthecosts).Oncetheinvestorhasfulfilledallconditions,theCouncilofMinistersmayallocate resources for financial supportfollowingaproposalbytheMinisterofEconomy.

Financialsupportforpartialreimbursementofinvestor-madesocialinsurancecontributions,supplementarypensioninsuranceandhealthinsurancefornewlyhiredemployeesfortheimplementationoftheinvestmentproject

The investor holding a certificate class „A“ or „B“ mayapplyforsupportforaperiodnotexceeding24monthsasof thecreationof the respective job.TheCouncilofMinisters allocates funds for partial reimbursement ofany costs incurred following a proposal of the MinisterofEconomy,aftertheinvestorhasfulfilledallconditionsprescribedbythelaw.Investments that are implemented in high-tech activitiesorwithin the administrativeboundariesof economicallydisadvantagedregionsareencouragedwithpriority.

Undercertainconditions,investorscanusethefollowinginvestmentincentives:

7

Conditions for investment promotion

Financialsupportfordevelopmentoftechnicalinfrastructureelements

Financialsupportfordevelopmentoftechnicalinfrastructureelementsfortwoprojectsinindustrialarea

FinancialassistanceisprovidedfollowingaproposalbytheMinisterofEconomytotheCouncilofMinisters,wherethe investor meets all the requirements described below,for implementationofmeasures topromote investment.Investmentswhichareimplementedinhigh-techactivitiesorwithin the administrativeboundariesof economicallydisadvantagedregionsareencouragedwithpriority.

Individualadministrativeservice

Company „W“holds a certificateof investmentprojectclass „A“ or „B“, which entitles it to receive individualadministrative service by Invest Bulgaria Agency. Theinvestor receives full and accurate information onthe time lines and charges, as well as assistance in theissuanceandreceiptofallthedocumentsrequiredfortheimplementationoftheinvestmentprojectandtherelatedbusinessoperations.

Thereisaprovisiontogranttaxexemptionsconstitutingstateaid.Theseareexpressedintheassignmentofcorporatetaxintheamountofupto100%oftheprofitsfromtheproductionactivity,beingcarriedout,includingproductionundertollingarrangement.2

2Withtheexceptionofproductsintheenergyandaeronauticsector

Investment incentives may be granted for investments intangible and intangible assets and the related jobs thatcumulativelyfulfillthefollowingconditions:

theyarerelatedtotheestablishmentofaneworexpansionofanexistingenterprise,withdiversificationofproductionorasignificantchangeintheoverallproductionprocess;

theyareexecutedintheeconomicactivitiesdesignatedforincentiveallotting(seeabove);

atleast80%ofthefuturerevenuesfromproducts(goodsand services) result from the implementation of thesupportedinvestment;

atleast40%oftheeligiblecostsarefinancedbyownorborrowedfunds;

thetimelimitforimplementationisuptothreeyears; theinvestmentisnotbelowthesetminimumamount; new jobs are created and maintained for a period of

minimumfiveyearsforlargeenterprisesandthreeyearsforsmallandmedium-sizedenterprisesintherespectivearea;

theinvestmentismaintainedintherespectiveareaforthesameperiod;

theacquiredassetsarenewandpurchasedundermarketconditionsbyindependentthirdparties.

Theconditionsforobtainingtaxreliefconstitutingstateaidareasfollows:

8 This Guide is prepared by Popov & Partners law firm, a member of TAGLaw

Conditions related tothe eligible costs, theinitial investment andthe assets, which arepartofit3

Thestateaid(intheformofassignedcorporatetax)isusedfortheacquisitionoftangibleandintangibleassets

Theinitialinvestmentismadewithinatimelimitofupto4years.

Theactivityrelatedtotheinitialinvestmentcontinuestobecarriedoutinthemunicipalityforatleastfiveyearsfollowingtheyearofcompletionoftheinvestment,astheincludedassetsmustbeusedonlyintheactivityoftheentityandshouldnotbeexpropriatedduringthisperiod

Atleast25percentoftheeligiblecostsforthetangibleandintangibleassetsincludedintheinitialinvestmentarefinancedbyownorborrowedfundsbythetaxpayer.

Production activity in the implementation of an initial investment project must be carried out onlyinmunicipalitieswhere thepreviousyearbefore theyear inwhichanapplication formforassistance issubmitted,thereisunemployment,byormorethan25percenthigherthanthenationalaverageforthesameperiod.MunicipalitiesaredeterminedbyorderoftheMinisterofFinance.

Throughoutthetaxperiodthetaxpayermustmaintainnotlessthan10jobs,asatleast50percentofthemshouldbedirectlyinvolvedintheproductionactivitybeingperformed.

Throughoutthetaxperiodnotlessthan30percentoftheemployeesaredomiciledinmunicipalitieswithlowunemploymentrate.

Specificities: Sector ClassA(million) ClassB(million)

Nospecificities(inthegeneralcase)Industrialsector 10millionBGN4 5millionBGN

Servicesector 3millionBGN 1.5millionBGN

Inmunicipalitieswithunemploymentratethatisequaltoorhigherthanthecountry-average

4millionBGN 2millionBGN

Inhigh-techactivitiesIndustrialsector 4millionBGN 2millionBGN

Servicesector 2millionBGN 1millionBGN

Specificities: Sector ClassA ClassB

Nospecificities(inthegeneralcase)Industrialsector

4millionBGNand150newjobs

2millionBGNand100newjobs

Servicesector1millionBGNand150newjobs

0.5millionBGNand100newjobs

Inmunicipalitieswithunemploymentratethatisequaltoorhigherthanthecountry-average

25newjobs 10newjobs

Inhigh-techactivitiesIndustrialsector 25newjobs 10newjobs

Servicesector 50newjobs 25newjobs

Dependingontheinvestmentamount,itmaybeassignedacertificateofclass:ClassAandClassB.Inaddition,aparticularinvestmentmaybedescribedas„priorityinvestmentproject“.InordertoobtainacertificateofclassAorclassBaninvestmentmustbeinacertainminimumamount:

Whenwiththeinvestmentprojectitisplannedtocreateandmaintainemployment,theminimumthresholdsareasfollows:

Minimum investment threshold

3Additionalconditionsareenvisagedwhentheinitialinvestmentispartofalargeinvestmentprojectorofasingleinvestmentproject.41EUR=1.95583BGN

9

Specificities: Sector Priorityinvestmentproject

Nospecificities(inthegeneralcase) 100millionBGNand150newjobs

Inmunicipalitieswithunemploymentequaltoorhigherthanthecountryaverageand/orhigh-techindustries 50millionBGNand100newjobs

Inhigh-techactivitiesorbasedonknowledgeandservices

Industrialsector 30millionBGNand100newjobs

Servicesector 20millionBGNand50newjobs

Constructionanddevelopmentof:

Industrial area –industrialpark 15millionBGNand15newjobs

Technologypark 15millionBGNand50newjobs

Priority investment projects „Priority“ are those investment projects which refer to allsectorsofeconomyand,inaccordancewiththerequirementslaiddownbyRegulation(EU)No.651/2014,areparticularlyimportantfortheeconomicdevelopmentoftheRepublicofBulgariaorfortheareasinthecountry.In respect of priority investment projects the legislatorenvisages all measures applicable to investment projectsof class A and class B, and furthermore, some additionalmeasuresarealsoembedded:

institutional support by an interdepartmental workinggroupforadministrativeassistance;

grantingofrightofuseorownershipofrealpropertiesforpriorityprojectsmaybeeffectedatpriceslowerthanthemarketones(butnotlowerthanthetaxassessment)andexemptionfromstampdutiesintheeventofchangingtheintendeduseoftheland);

additionalgrantforinvestmentsineducationandresearch(upto50%)andforinvestmentinmanufacturing(upto10%);

Themaincriteriaforissuanceofacertificateforsuchtypeofinvestmentprojectaretheminimuminvestmentamountandthegeneratedemployment:

The legislator envisages twooptions for reducing investment thresholds,provided that increased employment is ensured, asfollows:

Forevery50employeesexceedingtheprescribednumber-reducingthethresholdby10percent-forhigh-techservicesandtechnologyparks;

Forevery100employeesexceedingtheprescribednumber-reducingthethresholdby10percent-generally,inmunicipalitieswithhighunemploymentrate,high-techindustriesandfordevelopmentofindustrialzones.

10 This Guide is prepared by Popov & Partners law firm, a member of TAGLaw

Tax and social security legislation

ADVANTAGES

Bulgariantaxlegislationischaracterizedby:

1. favourabletaxratesandlowtaxburden(thelowestcorporatetaxinEU)and

2. taxpolicypredictability–legislativedevelopmentsinthesectorarelaunchedinaplannedmannerinlinewiththemeasuresoutlinedinthenationalstrategicdocuments(concepts,forecasts,plans,etc.)andonthebasisoftheinstructionsprovidedintherecommendationsoftheEuropeaninstitutions.Corporatetaxandflatincometaxwereintroducedatarateof10%intheyear2008,whichhasnotchangedeversincethen.Valueaddedtaxhasunalteredbasicrateof20%since1999.

Bulgarianlegislatorhasprovidedrelativelylargeamountoftaxbenefitsthataredirectlyaimedatstimulatinginvestmentandcreatingacompetitiveenvironmentforbusiness.

11

Taxrateoftheincomeofnaturalpersons

Corporatetaxrate

Denmark 52.2%

Denmark 24.5%

Greece 42%

Greece 26%

Italy 43%

Italy 27.5%

Luxembourg 40%

Luxembourg 21%

France 45%

France 15, 33.33%

Ireland 48%

Ireland 12.5%

Norway 39%

Norway 27%

England 45%

England 20-21%

Estonia 21%

Estonia 21%

Latvia 24%

Latvia 15%

Ukraine 15.7%

Ukraine 18%

Russia 13%

Russia 20%

Germany 45%

Germany 30-33%

Netherlands 52%

Netherlands 20, 25

Spain 47%

Spain 28%

Portugal 48%

Portugal 23%

Czech Republic 15%

Czech Republic 19%

Slovakia 19.25%

Slovakia 22%

Romania 16%

Romania 16%

Bulgaria 10%

Bulgaria 10%

Turkey 35%

Turkey 20%

Cyprus 35%

Cyprus 12.5%

Sweden 58%

Sweden 22%

12 This Guide is prepared by Popov & Partners law firm, a member of TAGLaw

Taxes

Taxtypes Objectoftaxation Taxbaseandrate

Directtaxes

Corporatetax

Theprofitoflocal(Bulgarian)legalentities;insomecasesnaturalpersons–soletraders,merchants,employeesworkingundermanagementcontracts;

TheprofitofforeignlegalentitiesfromaplaceofbusinessintheRepublicofBulgaria;

Reliefs/exemptionsareintroduced,suchas:

Assignmentofcorporatetax; Acceleratedtaxdepreciation

forcertaincategoriesofassets; Exemptionfromcorporate

taxofcollectiveinvestmentschemesandtransactionsinsharescarriedoutonstockexchange.

10%ofprofit

Alternativetax

This type of tax replaces thecorporate tax and it is levied inrespectof:

Gamblingactivities; Vesseloperationactivities

The rate is different and/or isaccruedondifferentbase:Gambling:

Gamblingdevices,casinos(taxrate: fixed amount per device,table, roulette, etc., as thefinally determined amount isbetween 500 – 22 000 BGNperquarterlyperiod)

Gamblinggames inwhichthebet is related to thepriceofatelephone or other electroniccommunication service (taxrate:15%ofprofits)

Revenue from ancillary andgamblingactivities–alternativetax on their value in theamountof12%

Taxonvesseloperations: Operatorsofvessels, chartered

vessels,vesselcharterers; Taxable amount per vessel

determined based on nettonnage;

Taxrate:10%

TAX TYPES AND BASIC APPLICABLE RATES:

13

Taxwithheldatsource

Income from dividends andliquidationshares;Income of foreign legal entities,when it is not earned through aplaceofbusinessinthecountry;Exemptions are introduced, as thefollowingaretaxexempt:Dividends and liquidation sharesdistributed

by resident legal entities infavourofnon-resident

legal entities (if not taxed intheirjurisdiction)and

resident legal entities that arenotmerchantsand

royalties paid to non-residentlegalentities.

Not applicable to foreign legalentitiesthat

areresidentsintheEU/EEA Furtherexemptions:interestson

bondsand other securities (if listed in the

EU/EEA), interest on loansgrantedbyforeignlegalpersons

5%ofincomefromdividendsandliquidationshares;10 % of income of foreign legalentities, when it is not earnedthrough a place of business in thecountry

Taxonexpenses

Businessentertainmentexpenses

SocialexpensesrelatedtoLifeinsurance,companycars,mealvouchers.

10%oftheexpenditureamount

Personalincometax

IncomeoflocalnaturalpersonsfromsourcesintheRepublicofBulgariaandabroad;

Income of foreign naturalpersons from sources in theRepublicofBulgaria;

Exemptions/reliefs areintroduced,asthefollowingaretaxexempt:

Income from exchange forcertain categories of movableandimmovableproperty;

Income from disposal offinancialinstruments;

Income from distribution inthe form of equity in businesscompanies (new shares, stocks,etc.), as well as acquisition ofstocks and shares, receivedagainstnon-cashcontributions;

Incomederivedfromrent,leaseor other onerous provision ofagriculturalland;

Indemnifications, scholarships,etc.

10%oftheincome,irrespectiveofitsamountTaxableincomeincludes:

Incomefromemployment Income from sole-trader

activities Income from other economic

activities – the tax is in theamountof10%,asbeforetaxesthe income is reduced by thefollowing recognized statutoryexpenses: 60 % for registeredfarmers; 40 % for certainagriculturalactivities,authorshipand license fees, craft activity;25%for freelanceoccupationsandnon-employment relations.Thus,theamountmayactuallybebroughtdownto4%.

Rent Transferofrealestateproperty-

differencebetweenthepurchaseand sale price (minus tenpercentofexpenses)

Cashprizes Final tax on amounts paid

transferstonon-residentnaturalpersons

14 This Guide is prepared by Popov & Partners law firm, a member of TAGLaw

Indirecttaxes

Valueaddedtax

Taxablesupplyofgoodsorserviceforconsideration;

Intra-Communityacquisitionwithplaceofperformanceinthecountry;

Importsofgoods

20 % of the value of the supply/serviceReducedtaxrate:

9 % tax is levied on provisionof hotel and similaraccommodationservices,aswellas vacation accommodationand letting places for campinggrounds and recreationalvehiclesparkinglots;

Suppliesatzerorate: internationaltransportofgoods

(to non-EU/EEA countries),international transport ofpassengers, maintenance andsupplies to international aircarriers/vessels, supply relatedto the processing of goods,delivery of gold to the centralbank, delivery related to dutyfree trade, supply of servicesprovidedbyagents,brokersandotherintermediaries

Exemptsupplies: Related to healthcare, social

care, education, sports, culture,religion, disposition of certaincategoriesoflandandbuildings,financialandinsuranceservices,gambling, postal stamps andservices

Taxoninsurancepremiums

Insurance premiums on insurancecontracts,except:

Lifeinsurance; Insurance of goods during

internationaltransportation; Insuranceofaircraftandvessels

2%ofthevalueoftheinsurancepremium

Exciseduty

Alcoholandalcoholicbeverages; Tobaccoproducts; Energyproductsandelectricity.

Exemptions/reliefsareintroduced: Refund of paid excise duty on

alcohol and alcoholic beverageswhenusedformedicalpurposes,productiontests/processesorforscientificpurposes/research;

Zeroexcisedutyonelectricityforhouseholdsandoncoalandcokeinsalestonaturalpersons;

Reduced rate of excise duty onnatural gas used as motor fueland beer produced by smallindependentbreweries

The excise rate is different foreach specific type of goods and isexplicitly regulated in the ExciseDutiesandTaxWarehousesAct:

Alcoholandalcoholicbeverages– fixed rates based on theamount of ethyl alcohol; forwine-zeroexcisedutyrate;

Tobacco products – fixedrates, based on the number orweight/flatrateof23%ofthepurchasepriceofcigarettes;

energyproducts-fixedratesperlitre/gigawattJaul/MWh

15

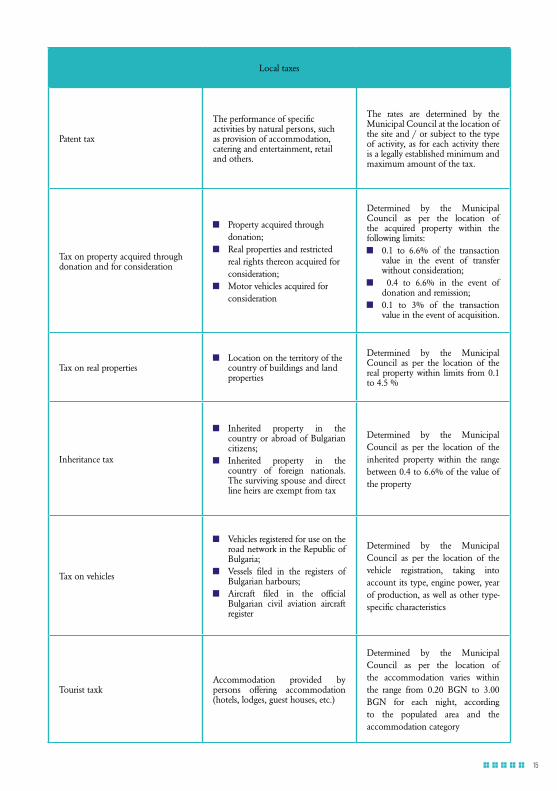

Localtaxes

Patenttax

Theperformanceofspecificactivitiesbynaturalpersons,suchasprovisionofaccommodation,cateringandentertainment,retailandothers.

The rates are determined by theMunicipalCouncilatthelocationofthesiteand/orsubjecttothetypeofactivity,asforeachactivitythereisalegallyestablishedminimumandmaximumamountofthetax.

Taxonpropertyacquiredthroughdonationandforconsideration

Propertyacquiredthroughdonation;

Realpropertiesandrestrictedrealrightsthereonacquiredforconsideration;

Motorvehiclesacquiredforconsideration

Determined by the MunicipalCouncil as per the location ofthe acquired property within thefollowinglimits:

0.1 to 6.6% of the transactionvalue in the event of transferwithoutconsideration;

0.4 to 6.6% in the event ofdonationandremission;

0.1 to 3% of the transactionvalueintheeventofacquisition.

Taxonrealproperties Locationontheterritoryofthe

countryofbuildingsandlandproperties

Determined by the MunicipalCouncil as per the location of therealpropertywithin limits from0.1to4.5%

Inheritancetax

Inherited property in thecountryorabroadofBulgariancitizens;

Inherited property in thecountry of foreign nationals.Thesurvivingspouseanddirectlineheirsareexemptfromtax

Determined by the MunicipalCouncil as per the location of theinherited property within the rangebetween0.4to6.6%ofthevalueoftheproperty

Taxonvehicles

VehiclesregisteredforuseontheroadnetworkintheRepublicofBulgaria;

Vessels filed in the registers ofBulgarianharbours;

Aircraft filed in the officialBulgarian civil aviation aircraftregister

Determined by the MunicipalCouncil as per the location of thevehicle registration, taking intoaccountitstype,enginepower,yearofproduction,aswellasothertype-specificcharacteristics

TouristtaxкAccommodation provided bypersons offering accommodation(hotels,lodges,guesthouses,etc.)

Determined by the MunicipalCouncil as per the location ofthe accommodation varies withinthe range from 0.20 BGN to 3.00BGN for each night, accordingto the populated area and theaccommodationcategory

16 This Guide is prepared by Popov & Partners law firm, a member of TAGLaw

DECLARING AND PAYMENT OF DIRECT TAXES- BASIC RULES

Subjecttothetypeofthepayabletaxitisenvisagedtodeclaresametotherelevantcompetentauthoritybysubmittingtaxreturnsasperformwithinsettimelimits.Forthetwotypesofmaindirecttaxesthesearerespectively-March31inthenextyearforcorporatetaxand30Aprilinthenextyearforincometaxofnaturalpersons.Proceduresforthesubmissionoftaxreturnsandpaymentfollowgenerallyestablishedforms,andareperformedmostlyelectronically.

VAT REGISTRATION, SUBMISSION OF RETURNS, VAT PAYMENT AND REFUND

ForthemainindirecttaxinBulgaria-VATregistrationisenvisaged.Forentitiesestablishedinthecountry,theregistrationisoftwotypes-mandatoryoroptional,dependingonthetypeofsuppliesandtheirvalue.Aseparateregistrationregimeisintroducedforforeignentitiesnotestablishedinthecountry,astheirregistrationmaybeexecutediftheprerequisitesspecifiedinthetablearepresent:

ProcedureforVATregistration-accomplishedbysubmittinganapplicationformtothecompetentbodyat itsofficeorelectronically.Withinsevendaysanexaminationofthegroundsforregistrationisperformedasadeedisissuedtoexecuteorrejecttheregistration.Ashorterthree-daytermisenvisagedinthepresenceofspecificgroundsforregistration,savetheturnoverspecifiedintheabovetable.Forforeignentitiesregistrationisarrangedbyanaccreditedrepresentative.

PaymentofVAT-thetaxpayableforeachtaxperiodispaidbytheregisteredsubjectfortherelevanttaxperiod,basedonthetaxreturnssubmittedbythe14thdayofthemonthfollowingthetaxperiod.

Mandatoryregistrationofentitiesestablishedintherepublicofbulgaria

Optionalregistration Registrationofforeignentity

Generalgroundforregistration:

Uponachievedtaxableturnoverof50,000BGNinaperiodnotlongerthanthepreceding12consecutivemonthsbeforethecurrentmonth

Specificgroundsforregistration:

upontransformation,uponperformanceofservicesthetaxonwhichispayablebytherecipient,distancesellingofgoodsintra-Communityacquisition

Any entity, irrespective whetherestablished within the territoryof Bulgaria or not, for whichthe conditions for mandatoryregistration are not present, isentitledtooptionalregistration

AforeignentitymustregisterforVATifithasapermanentestablishment (office, branchoffice) on the territory ofBulgaria, for carrying outeconomic activity and ifit is eligible to mandatoryregistration (availability oftaxable turnover) or optionalregistrationand/orperformscertain categoriesof supplies,regardlessofturnover,deliveryofgoodswhicharemountedor installed in the countrybyoronitsbehalf;provisionof telecommunicationservices, radio and televisionbroadcasting or electronicservices to non-taxablepersons established in thecountry; distance selling ofgoods; intra-Communityacquisition;

A foreign entity, which doesnot have a permanent site,butperformstaxablesupplieswithplaceofperformance inthe country, except those forwhich the tax is payable bytherecipient.

17

Country CorporateTax Taxontheincomeofnaturalperson

Bulgaria 10% 10%

Romania

16%,to3%formicro-enterpriseshavingturnoverbelow65.000EURandzerotaxforsomestatecompanies

16%,24%ofincomeover100.000EUR,receivedfromgambling

CzechRepublic 19%(5%inspecialcases)15%7%-additionalrateforincomeexceeding46060EURperannum

Germany Between30and33%(dependingontheprovince)

Progressivetaxationatratesofupto45%

TheNetherlands 20%or25%(forprofitsexceeding200.000EUR)

Progressivetaxationatratesofup52%

RefundofVAT-proceduresareinplaceforrefundofVATforsubjectsregisteredinBulgaria,asataxrefundcountryandforsubjectsnotestablished/notregisteredontheterritoryofthetaxrefundstate:

• ForVATregisteredsubjectsinBulgariaapossibilityisprovidedbyinitiativeofthecompetentauthoritiesoruponsubmittedwrittenrequestifataxforrefundingisformed,itmaybeoffset,deductedorrefunded.ThetimelimitsforcompletionoftheentireprocedureandforVATrefundingmaycontinueupto90days,andifthetaxrelatestoinvestmentprojects,thetimelimitis30days;

• Forsubjects,whicharenotestablished/notregisteredinthestateofrefundbutwhichareestablishedinanothercountry-EUmember,aprocedureforVATrefundisintroducedcoveringtwomaingroups:

RefundofVATchargedinBulgariatotaxablesubjects,whicharenotestablished/registeredinBulgaria,butareestablishedand registered forVAT in anotherEUMember State, for goodspurchased, services received and importsmadeon theterritoryofBulgaria;

RefundofVATchargedinotherEUMemberStatetotaxablesubjectsestablishedinBulgariaandregisteredforVATforgoodspurchased,servicesreceivedorimportperformedontheterritoryofanotherEUMemberState,inwhichtheyareregistered/established.

Theproceduretakesplaceentirelyelectronically,basedonforms.Forthefirstgroupofsubjectstherefundmaytakebetween4and8months,whileforthesecondgroupthetimelimitissetdependingontheproceduresintherelevantMemberState,inwhichthetaxhasbeencharged.

ESTABLISHMENT AND COLLECTION OF LIABILITIES Bulgarianinstitutionshaveelaboratedcapabilitiesforelectronicdeclaringandpaymentofpublicliabilities(taxesandsocial

insurance contributions) accessiblemainly through thewebsiteof theNationalRevenueAgency/НАП.The competentsupervisoryauthoritieshavethepower,despitethedeclaredinformation,tomakeacheckand/oraudit,asaresultofwhichtoestablishthesameordifferentamountofliabilities.TheestablishmentiscarriedoutbytheNationalRevenueAgency,theCustomsAgencyorbythemunicipality,dependingonthetypeofliability.

Bulgarianlegislationallowsfortheprotectionofpersonsinrespectofwhomvariousobligationsareestablishedbasedontaxassessmentnotice.Appeal is envisaged following theadministrativeprocedures andaccordingly - two instancecourtproceedings.

THE LOW TAX RATES of the main direct taxes in Bulgaria and selected EU countries are evidenced by the followingcomparativetable:

18 This Guide is prepared by Popov & Partners law firm, a member of TAGLaw

Ireland

12.5 % - general case, for incomefromtradeoperations25 % -for non-trade income andinvestmentincome33%-capitalgains

Progressivetaxationatratesbetween21.5 % and 48 %, includingthe mandatory social insurancecontributionsaswell

Luxembourg20 % or 21 % (for profits over15.000EUR)

Progressive taxation at rates of upto40%

Slovakia 21% 19%(25%forannualincomeover35.000EUR)

Estonia 21% 21%

AVOIDANCE OF DOUBLE TAXATIONConsideringthepossibilityuponrealizationofincomebyaforeignentitytobereacheddoubletaxation(imposingidenticalintypeandscopetaxesintwoormorecountriesonthesameincome),Bulgariaappliestheprinciplesofavoidingdoubletaxation.Asaresult,ifaneffectiveconventionorotherinternationalagreementtowhichBulgariaisapartyisinplace,andifitcontainsprovisionsotherthanthoselaiddowninthenationallaw,theprovisionsoftheconvention/agreementshallapply.CurrentlyBulgariaisapartytoalmost70doubletaxationconventions.

SignatorystateDateofsigningtheagreement/Effectivedate

Taxonincomefromdividends(%)

Taxonincomefrominterest(%)

Taxonincomefromlicensepayments(%)

Albania 01.07.1999 5/15 10 10

Algeria 11.04.2005 10 0/10 10

Armenia 01.12.1995 5/10 10 10

Austria 03.02.2011 0/5 0/5 0/5

Azerbaijan 01.01.2009 8 0/7 5/10

Bahrain 06.10.2010 5 5 5

Belarus 17.02.1998 10 10 10

Belgium 30.12.1988/1993 10 0/10 5

GreatBritain 28.12.1987 10 0 0

Vietnam 04.10.1996 15 0/10 15

Germany 21.12.2010 5/15 5 5

Georgia 01.07.1999 10 0/10 10

Greece 27.06.2001 10 10 10

Denmark 27.03.1989 5/15 0 0

Egypt 11.05.2004 10 12.5 12.5

Estonia 01.01.2009 0/5 0/5 5

Zimbabwe 29.01.1990 10/20 0/10 10

Israel 31.12.2002 10/7.5-12.5 0/5/10 7.5-12.5

India 23.06.1995 15 0/15 15/20

Indonesia 25.05.1992/1993 15 0/10 10

Italy 10.06.1991 10 0 5

Iran 29.06.2006 7.5 0/5 5

19

Ireland 05.01.2001 5/10 0/5 10

Spain 14.06.1991 5/15 0 0

Jordan 19.12.2008 10 0/10 10

Canada 25.10.2001 10/15 0/10 0/10

Kazakhstan 24.07.1998 10 0/10 10

Qatar 23.12.2010 0 3 5

Cyprus 03.01.2001 5/10 0/7 10

China 25.05.1990/2003 10 10 7/10

Kuwait 23.02.2004 0/5 0/5 10

Latvia 18.08.2004 5/10 0/5 5/7

Lebanon 10.11.2001 5 0/7 5

Lithuania 27.12.2006 0/10 0/10 10

Luxembourg 15.03.1994 5/15 0/10 5

Macedonia 24.09.1999 5/15 0/10 10

Malta 01.01.1988 0-30 0 10

Morocco 06.12.1999 7/10 10 10

Moldova 24.03.1999 5/15 0/10 10

Mongolia 17.02.2003 10 0/10 10

Netherlands 11.05.1994 5/15 0 0/5

Norway 01.04.1989 15 0 0

UAE 01.01.2009 5 2 5

Poland 10.05.1995 10 0/10 5

Portugal 18.07.1996 10/15 0/10 10

Romania 12.09.1995 10/15 0/15 15

Russia 24.04.1995 15 0/15 15

USA 15.12.2008 0/5/10 0/5/10 5

Slovakia 02.05.2001 10 0/10 10

Slovenia 04.05.2004 5/10 0/5 5/10

NorthKorea 07.01.2000 10 0/10 10

Singapore 26.12.1997 0/5 0/5 5

Syria 04.10.2001 10 0/10 18

Serbia 10.01.2000 5/15 10 10

Thailand 13.02.2001 10 0/10/15 5/15

Turkey 17.09.1997 10/15 0/10 10

Hungary 07.09.1995 10 0/10 10

Uzbekistan 21.10.2004 10 0/10 10

Ukraine 03.10.1997 5/15 0/10 10

Finland 21.04.1986 10 0 0/5

France 01.06.1988 5/15 0 5

Croatia 30.07.1998 5 5 0

Montenegro 10.01.2000 5/15 10 10

CzechRepublic 02.07.1999 10 0/10 10

Sweden 28.12.1988 10 0 5

Switzerland 18.10.2013 0/10 0/5 5

SouthAfrica 27.10.2004 5/15 0/5 5/10

SouthKorea 22.06.1995 5/10 0/10 5

Japan 09.08.1991 10/15 0/10 10

20 This Guide is prepared by Popov & Partners law firm, a member of TAGLaw

Social security system

Unlike other countries, Bulgarian social security systemdistributestheburdenofpaymentofcontributionsbetweenthe employer and the employee. Furthermore, typical ratesarerelativelylow,expressedasapercentageofthegrossbasicsalaryofemployeesuptoacertainmaximumamount.Themaximum insurable income is determined annually by law(for2015and2016-2,600BGN),whichservesasthebasisfordeterminingcontributions,regardlessoftheactualincomethathasbeenreceived.SocialsecuritysysteminBulgariadividesinsuranceintotwomaintypes-socialandhealthinsurance,combiningelementsofmandatoryinsuranceandoptionsforvoluntaryinsurance.

Socialsecurityincludes:• State Social Security (SSS) comprising four funds:

„General Disease and Maternity“ (GDM), „Pensions“,„Occupational accidents and occupational disease“(OAOD)and„Unemployment“-12.8%to17.3%

• Supplementaryobligatorypensioninsurance(SOPI)-5%;• Voluntarysocialinsurance

Healthinsuranceincludes:• Obligatoryhealthinsurance(OHI)–8%• Voluntaryhealthinsurance;

21

Fund/Coveredrisk

Employmentagreement Employmentagreement

*grosssalarypermonth–1000BGN**recognizedstatutoryexpenses–n/a***insurableearnings–1000BGN(contributionsarebasedonthelatter)

*grosssalarypermonth–100000BGN**recognizedstatutoryexpenses–n/a***insurableearnings–2600BGN(contributionsarebasedonthelatter)

Total%contribution%contributionbytheemployer

%contributionbytheemployee

Total%contribution

%contributionbytheemployer

%contributionbytheemployee

SSS 17.3% 9.8% 7.5% 17.3% 9.8% 7.5%

SOPI 5% 2,8% 2.2% 5% 2,8% 2.2%

OAOD

0.4%(between0.4%and1.1%dependingontheeconomicactivity)

0.4% n/a 0.4% 0.4% n/a

OHI 8% 4.8% 3.2% 8% 4.8% 3.2%

Totalin% 30.7% 17.8% 12.9% 30.7% 17.8% 12.9%

TotalinBGN

Totalamountofinsurancecontributions*

Contributionbytheemployer

Contributionbytheemployee

Totalamountofinsurancecontributions*

Contributionbytheemployer

Contributionbytheemployee

307BGN*theemployerdeductsadditionally10%inadvance,amountingto87.10BGNinthiscase

178BGN 129BGN

798,20BGN*theemployerdeductsadditionally10%inadvance,amountingto9966,46BGNinthiscase

462,80BGN 335,40BGN

Totalexpenditurefortheemployer–salaryandcontributionsattheexpenseoftheemployer

1178BGNTotalexpenditurefortheemployer–salaryandcontributionsattheexpenseoftheemployer

100462,80BGN

Netamountreceivedbytheemployeeafterdeductionofthesocialsecuritycontributionsand10%tax

783.90BGNNetamountreceivedbytheemployeeafterdeductionofthesocialsecuritycontributionsand10%tax

89698,14BGN

Fund/Coveredrisk

Freelanceagreement Freelanceagreement

*grossremunerationpermonth–1000BGN**recognizedstatutoryexpenses–25%/250BGN***insurableearnings–750BGN(determinedafterreducingtheamountwiththerecognizedstatutoryexpenses,asthecontributionsarebasedontheresultingamount)

*grossremunerationpermonth–100000BGN**recognizedstatutoryexpenses–25%/25000BGN***insurableearnings–2600BGN(thecontributionsarebasedonthelatter)

Total%contribution%contributionbytheemployer

%contributionbytheemployee

Total%contribution

%contributionbytheemployer

%contributionbytheemployee

SSS 12.8% 7.1% 5.7% 12.8% 7.1% 5.7%

SOPI 5% 2,8% 2.2% 5% 2,8% 2.2%

OAOD n/a n/a n/a n/a n/a n/a

OHI 8% 4.8% 3.2% 8% 4.8% 3.2%

Totalin% 25.8% 14.7% 11.1% 25.8% 14.7% 11.1%

TotalinBGN

Totalamountofinsurancecontributions*

contributionbytheemployer

contributionbytheemployee

Totalamountofinsurancecontributions

contributionbytheemployer

contributionbytheemployee

193.50BGN*theemployerdeductsadditionally10%inadvance,amountingto66.68BGNinthiscase

110.25BGN 83.25BGN

670,80*theemployerdeductsadditionally10%inadvance,amountingto7471,14BGNinthiscase

382,20BGN 288,60BGN

Totalexpenditurefortheemployer–remunerationandcontributionsattheexpenseoftheemployer

1110.25BGNTotalexpenditurefortheemployer–remunerationandcontributionsattheexpenseoftheemployer

100382,20BGN

Netamountreceivedbytheemployeeafterdeductionofthesocialsecuritycontributionsand10%tax

850.07BGNNetamountreceivedbytheemployeeafterdeductionofthesocialsecuritycontributionsand10%tax

92340,26BGN

Examplesof allocationof the social securityburden and the resultingnet remunerationunder employment agreement andfreelanceagreement:

*Similarparametersapplyalsotoagreementsonmanagementandcontrolofalegalentity,asthedifferenceisthatnocontributionforOAODispayable.

22 This Guide is prepared by Popov & Partners law firm, a member of TAGLaw

Trade legislationMAIN ADVANTAGES:

Diverse and flexible legal forms for structuring of abusiness;

ElectronicBusinessRegister(includingaffordableservicesinEnglishlanguageaswell:http://www.brra.bg/Default.ra);

Short time limits for registration of a new company -withinaday;

Lowregistrationfees; Lowminimumcapitalforalimitedliabilitycompanyas

comparedtootherEuropeancountries:

BusinesscompaniesariseasofthemomentoftheirfilingintheTradeRegisterattheRegistryAgency. Theentireprocedureforelaborationofthedocuments,paymentofthecapital,submissionoftheapplicationforregistration

andthefilingofthenewcompanytakesaboutoneweek

Country Bulgaria Germany France Estonia Romania

Legal form of the company

Limited liability company (LTD/ООД)

Gesellschaft mit beschränkter Haftung (GmbH)

Société à Responsabilité Limitée (SARL)

Private Limited Company (osaühing or OÜ)

Societate cu rãspundere limitatã (Limited Liability Company)

Minimumcapital 1.06€ 12500€ 1.00€ 2500€ RON200(45.37€)

Thus, for a freelance agreement with a value of 100 000 BGN per month, the total tax and social insurance burden is in the amount of 8 141.94 BGN, as all the remaining amount is received directly by the person:

7.4%Tax

Social insurance

contributions

Net income to be

received

0.7%

91.9%

23

Themostcommonlyusedformsforstructuringofabusinessarethelimitedliabilitycompanyandthejoint-stockcompany,anditsspecificvarieties.

Legal and organizational forms for structuring of a business

Legalform MinimumcapitalLiabilityofthemembers,partners,shareholdersforobligationsofthelegalentity

Taxreliefs

Generalpartnership(GP/СД)

NoAll members have unlimitedliability

NO

Limitedpartnership(LP/КД)

NoA part of the partners haveunlimited liability, while othershavelimitedliability

NO

Limitedliabilitycompany(LTD/ООД)

2BGN

Limited liability of all partnersup to the amount of theircontributions in the capital ofthecompany;participationinthemanagement.Thepartnermaybeonlyone,as thisdoesnotchangeitsrights,obligationsandliability.

NO

Jointstockcompany(Jcs/АД)

50000BGN

Liability for the obligationsassumed by the Jsc companyup to the amount of the sharessubscribed in the capital of thecompany. The shareholder maybe only one when this does notchange its rights, obligations andliability.

NO

Partnershiplimitedbyshares(PLS/КДА)

A part of the partners haveunlimited liability and others areshareholders

NO

Cooperative NoThe liability of the cooperativemembers if up to the amount oftheirsharecontributions

YES

24 This Guide is prepared by Popov & Partners law firm, a member of TAGLaw

Limited liability company (LTD/ООД)

Joint stock company (JSC/АД)

LTD is an appropriate form for structuringboth small andmedium-sized enterprises and larger-scale businesses. Thecompany share in aLTD isnotmaterializedona security.LTDmaybeestablishedbyonepersononly.AmajoradvantageofLTDisthelimitedliabilityofallpartnersto the extent of their contributions in the capital. Alsoattractiveisthelowminimumcapitalforitsestablishment-2BGNcapital(about1Euro),therelativelylowexpensesforitsestablishmentandsubsequentadministration.

Unlike LTD, in the case of a JSC against the capitalcontributions shareholders receive shares - securitiesmaterializing the ownership and membership rights. Thesharesareindivisibleandhaveequalvalue.JSC is the preferred form for structuring larger capitalinvestments. The procedure for acquiring a shareholdingis reduced to theobligation to make a capital contributionagainstwhichtheshareholderreceivessharesPublicofferingof

sharesispossible,aswellastheissuanceofbondstobeofferedbothpubliclyandtocertainpersons.JSC is a flexible legal form facilitating the transfer andpledging of shares, application of flexible models to attractadditionalfunding,variousformsofrestrictionsandprivilegesfordifferentclassesofshares.ThemaincharacteristicsofJSCcompanyandofLTDcompanymaybepresentedinacomparativemannerasfollows:

LTD/ООД JSC/АД

MinimumnumberoffoundersOne(SinglememberLTD)ormorenaturalpersonsorlegalentities

One(SinglememberJSC)ormorenaturalpersonsorlegalentities

Maximumnumberofpartners/shareholders

Unlimited Unlimited

Minimumregisteredcapital 2BGN

50000BGN(forcertaintypeofJSCsomerequirementsareinplaceforahigherminimumamountofthecapital)

Minimumshareamount 1BGN 1BGN

Minimumamountofthecapitaltobepaidupuponincorporation

Theminimumcapitalestablishedunderthelaw/Intheeventthatthecompanyisregisteredwithacapitalhigherthantheminimumestablishedunderthelaw–atleast70%ofthecapitalmustbepaidup

Notlessthan25%oftheparvalueorthevalueenvisagedinthearticlesofassociationforissuanceofeachshare

25

Joint stock special purpose investment company (JSSPIC/АДСИЦ)JSSPICisaninstrumentofthecapitalmarket toencouragesmall and medium investors, providing them with theopportunity to participate in large and profitable projects.Thesecompaniesarepublicly tradedonthestockexchangeand invest the generated funds in projects related to realpropertiesandreceivablesinBulgaria.Theprincipalactivitiesof about 90% of the JSSPIC 's investments are in realproperties,whiletheremaining10%compriseinvestmentsinreceivables.SpecificrequirementsareinplaceinrespectoftheassociationandfunctioningofJSSPIC.

Acooperativeisanassociationbetweencapablenaturalpersons,whomustbeatleastseven.Unlikebusinesscompanies,ithasvariablecapitalandvariablenumberofmembers.Thecooperativeistheonlyformofcommercialassociation,

which is supported by the state. Cooperatives are exemptfrom any expenses related to their start-up, transformationand termination. Opportunities are provided for reduction,assignmentandexemptionfromcorporatetax

TimelimitforpaymentSet under the memorandum ofassociation, however not exceedingtwoyears

Set under articles of association, butnotexceedingtwoyears.

ObjectsofbusinessAll types of activities that are notprohibitedbythelaw.

All types of activities that are notprohibitedbythelaw.

Corporatebodies

Generalmeeting,manager(managers)/In case of a single member LTD/ЕООД the sole owner of the capitalmanagesandrepresents thecompanyinpersonor throughamanager thathe has designated. If the owner is alegal entity, its manager or a persondesignated by him manages thecompany.

General meeting of the shareholders;Board of directors (one-tier system)or managing board and supervisoryboard(two-tiersystem).InasinglememberJSC/ЕАДthesoleownerofthecapitalresolvestheissueswithin thecompetenceof thegeneralmeeting

AssociationdocumentMemorandum of association orConstituentinstrument

Articlesofassociation

Cooperative

26 This Guide is prepared by Popov & Partners law firm, a member of TAGLaw

Branch

Representation

The branch is a structural territorial subdivision locatedoutsidethedomicileofthemerchant.ThebranchofaforeignentityisenteredintheTradeRegister.Theentryofabranchofaforeignmerchantdoesnotcreateanewlegalentity.Theforeignmerchantisapartytothelegalrelationships in which it participates through the branchregistered in Bulgaria and is liable with all its property forany assumed obligations. However, the branch must keepcompanybooksasanindependentmerchant.Fortaxpurposes,thebranchistreatedasanindependenttaxsubjectwithaplaceofbusinessinBulgaria

ForeignpersonswhocarryoutcommercialactivitiesmayopentraderepresentationsinBulgaria.Theestablishmentofatraderepresentationhasasobjectivetheperformanceofnon-profitactivitiessuchaspreparationofpromotions,organizationandholdingofexhibitions,advertising,providinginformationtothemarket,studyofcompetition,etc.The trade representation is not a legal entity and is notentitledtoconductbusiness.However, it is subject toentryin the Unified Register of Business Subjects Bulstat. ThecompetentauthorityistheBulgarianChamberofCommerceand Industry (BCCI) as the trade representation offices aresubjecttoenteringintheUnifiedTradeRegisterofBCCI.Thetransactionsbeingcarriedoutby the trade representation inthecountryonbehalfoforundertheauthorityoftheforeign

entity are regarded as independent business and are subjecttotaxation.Registrationofatraderepresentationmayberequestedbyanyforeign entitywhohas the right to conductbusinessundertheirnationallegislation.In order to facilitate the procedure BCCI provides fullterritorial coverage through representatives in the regionalchambers of commerce and industry that receive on thespotdocuments for registrationof trade representationsandofficiallysendthemforregistrationinSofia.TheregistrationdocumentsforatraderepresentationofaforeignentitymaybesubmittedelectronicallythroughthewebsiteofBCCIbyusinganelectronicsignature.

Partnership (Consortium)The so-called partnership or consortium is not anindependentlegalentityandnotamerchant.It isaspecificcontractualassociationof twoormorepersonsforcarryingoutjointactivities.Similarly to business companies, the partners in theconsortium can negotiate and make property and cashcontributionstoachievetheir jointobjective.Contributionsare common property of the partners, as well as all that isacquired by the consortium. Each partner is entitled torequestandreceivetheirshareofthecommonpropertyofthecompanyuponwithdrawal fromitoruponits termination.Gainsandlossesofthepartnershiparedistributedamongthepartnersprorata to their share, if it isnotagreedotherwise

underthecontract.TheconsortiumisnotregisteredintheCommercialRegisterandforitsterminationnoliquidationisneeded.ThecontractisregisteredintheBULSTATregisteronamandatorybasis.This type of company is a form that is often used forparticipationinpublicprocurementprocedures,asitdoesnotbindthepartnerswiththeestablishmentofanewlegalentityandallowstheuseofresourcesofthepartnerstomeetspecificcriteria. It is possible to form a partnership with a foreignentitythatdoesnothavebusinessoperationsinBulgaria.InBulgaria it ispossible to establish aEuropeancompany,butinpracticethisformisseldomused.

27

Peculiarities in the structuring of specific business activities Forcarryingoutcertaintypesofactivitiesspecificregulationsaresetforthinrespectofthestructuringthroughaparticularlegalform,mostoften-LTDandJSC.Someofthemarediscussedbelow:

Activity/Typeofcompany/ Minimumrequiredcapital Admissibleformsofthebusinesscompany

Bankingactivity 10000000BGN Jointstockcompany

InsurancecompanyBetween1100000and3500000BGNdependingonthescopeoftheinsuranceactivity

Jointstockcompany,cooperative,aswellasinsurerfromathirdcountrythroughabranchregisteredundertheCommerceAct.

Financialinstitution 1000000BGNLimitedliabilitycompany,jointstockcompanyorpartnershiplimitedbyshares.

InvestmentintermediaryBetween100000and1500000BGN–dependingonthescopeoftheactivitiesthatitperforms

Limitedliabilitycompanyorjointstockcompany.

Marketoperator5000000BGN–capitalwhichthemarketoperatormusthaveavailableatanytime.

Jointstockcompany

Pensioninsurancecompanies

5000000BGN–thepensioninsurancecompanymusthaveavailableequityintheamountof2500000BGNatanytime

Jointstockcompany

Jointstockspecialpurposeinvestmentcompany

500000BGN Jointstockcompany

PaymentinstitutionBetween40000BGNand250000BGN

Limitedliabilitycompanyorjointstockcompany

Electronicmoneycompany 700000BGNLimitedliabilitycompanyorjointstockcompany

Activityasanoperatorofapaymentsystemwithsettlementfinality

5000000BGNcapital,50%ofwhichshallbepaidascashcontribution.

Jointstockcompany

Other forms of starting a business through a local partner Apartfromtheaforementionedformsofacquiringabusiness,itispossibleforaforeigninvestortostartanactivityinthelocalmarketalsothroughalocalbusinesspartner,byemployingthefamiliarformsofbusinesscooperation:

Traderepresentationagreement; Franchisingagreement; Exclusiveornon-exclusivedistributionagreement; Othercontractualformsofcollaboration

28 This Guide is prepared by Popov & Partners law firm, a member of TAGLaw

Mergers and acquisitions

Transformation

Bulgarianlegislationprovidesinvestorswithdifferentlegalformsforacquisitionandreorganizationofabusiness:

ThemainformsoftransformationinBulgariaare: takeover,merger, division and separation. Their regulation isharmonizedinlinewiththeEUlegislation.

Takeover-aprocedureinwhichtheentirepropertyofoneormorebusinesscompaniespasstoanexistingcompany,which becomes their legal successor. The transformingcompaniesarewoundupwithoutliquidation

Merger-aprocedureinwhichtheentirepropertyoftwoormorebusinesscompaniespassestoanewlyestablishedcompany, which becomes their legal successor. Thetransforming companies are wound up withoutliquidation.

Division - a procedure in which the entire property ofabusiness companypasses to twoormore companies,whichbecomeitslegalsuccessorsfortherespectivepart.The company being transferred is wound up withoutliquidation. The companies to which the property ofthe company being transformed passes may include:existingcompaniesindivisionthroughacquisition,newlyestablishedcompaniesindivisionthroughincorporation;as well as existing and newly established companiessimultaneously.

Separation - a procedure in which part of the propertyof a company passes to one or more companies, which

become its legal successors for that part of the property.The company being transformed is not wound up.The companies to which a part of the property of thetransformingcompanypassesmaybeexistingcompaniesupon separation through acquisition, newly establishedcompaniesuponseparationthroughincorporation,aswellasexistingandnewlyestablishedcompaniessimultaneously.

The transformation is performed in accordance withtransformationagreement/plan,whichregulatesthemannerinwhichthetransformationwillbecarriedout.A report by the governing bodies of the transformingcompanies is also elaborated, containing detailed economicandlegalrationaleonwhichthetransformationisbased.A check of the transformation is performed by a certifiedauditor, unless all the partners or shareholders in thetransforming and acquiring companies have expressed theirconsentinwriting.The whole procedure until the entry of the transformationlasts approximately between 1 and 6 months, dependingonthe formof transformation, thenumberof transformingcompanies, thenumberofnewlyemergingsubjectsandtheneedforpermissionfromtheCommissionforProtectionofCompetition.Inordertoprotectcreditors,thereceivingornewlyestablishedcompany manages separately the property of each of thetransformingcompaniesforaperiodofsixmonthsasofthedateofentryofthetransformation.

29

Acquisitions

ACQUISITION OF SHARES IN JSC

ACQUISITION OF COMPANY SHARES IN LTDTheacquisitionofaninterestinLTDiseffectedthroughtransferofcompanyshares,aswellasthroughtheconclusionofanagreementonsale(themostfrequentcase)andthroughbarter,donationandothertransfertransactionsandmethods,includingthroughcapitalincrease.Thetransferofcompanysharesiscarriedoutbytheexecutionofawrittenagreementwithnotarizedsignatures.Whensharesare being transferred between partners, the consent of theotherpartnersisnotnecessary.Whenthecompanysharesaresoldtoathirdparty,thenanapprovalbytheGeneralMeetingofthepartnersisneeded.ThetransferofsharesshallbeenteredintheTradeRegister,astheadmissionofapartnershallhaveeffectasofitsentryintheTradeRegister.

The sale of shares is the most commonly used method totransfershares.Another frequently used option for acquisition of ashareholdingisbyincreasingitscapitalandissuingnewsharestobesubscribedbytheacquirer.Subject to a transfer may be all types of shares, but themethodisdifferent:

Registeredshares-uponsubscriptionofregisteredsharestemporarycertificatesareissued,whicharereplacedwithshares only when the full value of the shares is paid.Registered shares are transferredby endorsement, as thetransfer must be entered in the Book of Shareholders.

Registeredsharesmaybeacquiredalsobeforepaymentoftheirparorissuevalue;

Bearer shares - what is special about them is that it isnot recorded who their first owner is. Bearer shares areacquiredwiththeirsimpledeliveryandacceptance.Unlikeregistered shares, bearer shares may not be transferredbeforetheirparorissuevalueisfullypaid.

Dematerialized shares - in dematerialized shares tangiblecarrierismissing,astheyarealwaysissuedasregisteredshares.Thetransferofdematerializedsharesisperformedthroughassignment, as the issue and disposal of dematerializedsharesshallberecordedinaspecialbookofdematerializedshares,whichiskeptattheCentralDepository.

30 This Guide is prepared by Popov & Partners law firm, a member of TAGLaw

Transfer of a Commercial Enterprise

Control of Mergers and Acquisition

Commercialenterpriseisadistinctsetofrights,obligationsandfactualrelationsarisingasaresultofthebusinesscarriedoutbythetrader.Therightsincludethetitleandalllimitedrights in rem over all the trader‘s movable and immovableproperty, claims, share interest, rights to inventions,trademarks, licenses, etc. The obligations include all loansandothercontractualandnon-contractualobligationoftherespective trader, forming the liabilities of the commercialenterprise.Thefactualrelationsincludethetrader‘srelationswiththirdparties,builtonthebasisofthetrader‘spersonalqualities(customers,businesscontactswithpartners)andtheorganization, established in the enterprise (including know-how),etc.The transfer of the commercial enterprise is carried outby entering into a sale contract (most commonly) andthroughexchange,donation,contributionandothertransfertransactionsandprocesses.The sale of the commercial enterprise is carried out byexecuting a contract in writing with notarized signatures,whereas the transferor is imposed the obligation to notifytheircreditorsanddebtorsofthetransfer.The transferofanenterprise isconsidereda supplyexemptfromtaxundertheprovisionsoftheVATAct.The transfer of a commercial enterprise is subject to

The Commission for Protection of Competition (CPC) isthe specialized regulator responsible for the implementationof the Community competition law in Bulgaria. TheCommissioncarriesoutbothex-ante,andex-postcontrolonthecompliancewiththecompetitionrules.The ex-ante control carried out by the CPC applies to alltypesofbusinesstransfertransactions,includingtransactionswithstocksorsharesincommercialandholdingcompanies,transfer of enterprises or parts thereof, acquisitions,mergersandother formsof business combinationor acquisitionofcontrol thereof. Such a control is exercised even when therelevant business combination takes place outside Bulgaria,buthasaneffectonthelocalmarket.Before acquiring control on an enterprise or group ofenterprises, the acquirer should notify the CPC and ask

for permission to perform the concentration. Notificationobligationexists ifthecombinedturnoveroftheenterprisesinvolved in the transaction for the previous financial yearexceedsBGN25,000,000andintheeventthat:

the turnover of each of at least two of the enterprisesinvolved in the concentration in Bulgaria during theprecedingfinancialyearexceedsBGN3,000,000,or

theturnoveroftheenterprisebeingacquiredinBulgariaduring the preceding financial year exceeds BGN3,000,000.

TheCommissionwillpermittheconcentrationifitdoesnotleadtoestablishingorstrengtheningofadominantpositionwhichwouldsignificantlyimpedetheeffectivecompetitionintherelevantmarket.Thedecisionissubjecttoappealincourt.

registration with the Commercial Register. Before filing anapplication, the transferor is required to notify the relevantterritorialdirectorateoftheNationalRevenueAgency.The creditor protection rules provide for the joint liabilityof the transferor of the enterprise for the liabilities ofthe enterprise jointly with the successor equivalent withthe proportion of the rights acquired. The successor willseparatelymanage the commercial enterprise transferred foraperiodof6monthsasfromtheregistrationofthetransfer.

31

Administrative Costs of Investment in BulgariaTheadministrativecostsassociatedwiththeestablishmentoracquisitionofabusinessinBulgariagenerallydependinsizeon the type of investment, the nature of business activitiesto be carried out, whether they concern a new business orinvestment in the acquisition of an existing one. However,theusualadministrativecostsofsettingupanewbusinessarequitelow.Forexample:

Typeofservice Beneficiary FeeinEuro

RegistrationofanewLimitedLiabilityCompany(OOD)/SingleMemberLimitedLiabilityCompany(EOOD)

CommercialRegister 28.12

RegistrationofanewJointStockCompany(AD)/SingleMemberJointStockCompany(EAD) CommercialRegister 92.03

Registrationofcapitalincrease CommercialRegister 15.33

Registrationoftransformation CommercialRegister 46.01

Registrationoftransferofenterprise CommercialRegister 20.45

Registrationofrepresentation BulgarianChamberofCommerceandIndustry 120

Considerationofanapplicationforpermissionforenterpriseconcentration

CommissionforProtectionofCompetition 1022

Permissionforconcentration(onlyifavailable) CommissionforProtectionofCompetition

0.1%oftheturnoveroftheenterprises,butnotmorethan€30,677.

BeforeinvestinginanexistingbusinessinBulgaria,werecommendyoutoengagespecialistsforcarryingoutfinancial,legalandtechnicalduediligenceofthetargetedbusiness.

32 This Guide is prepared by Popov & Partners law firm, a member of TAGLaw

Commercial Disputes

Bulgarian legislation provides for a specific procedure fordealing with commercial disputes, in order to accelerate theirconsideration.Allthedocumentaryevidenceonthecaserelatingtothecommercialoperationunderreviewisexpeditiouslysuppliedtroughtheso-called„doubleexchangeofpapers“procedure.Alongwith thestatecourts,anumberofarbitrationcourtsoperate in Bulgaria expeditiously dealing with commercialdisputes.Compared with the state system of justice, arbitration hasa number of features that can be considered advantages,including:

Single-instanceproceedings; Participationoftheparties intheprocessofstructuring

bythedeterminingauthority; Thenegotiatingpartiesmay choosewhether to initiate

an ad hoc arbitration at the chosen location or to use theinstitutionalarbitrationcourt.

ThehearingusuallytakesplaceinBulgarian,butifanyofthepartiesisdomiciledorresidingabroad,theymayagreeto

useanotherlanguage5.Thedeterminingauthorityappointsatranslatorforthenon-Bulgarianspeakingparty.AmongthemostcommonlyusedcourtsofarbitrationarethecourtsofarbitrationattheBulgarianChamberofCommerceandIndustryandtheBulgarianIndustrialAssociation.The averagedurationof civil cases inBulgaria is about12months in the first instance,which isamongthe lowest inEurope.Thearbitrationproceedingsaresignificantlyfaster–theyusuallyendwithunappealabledecisionwithin9to12monthsfromtheinitiationofthearbitration.Anadvantageforbusinesses is theoption to initiate a so-called „writsofexecution“ where the creditor may obtain an enforceabletitle through a facilitatedprocedure.Thedurationof theseproceedingsincourtsoutsideSofiatypicallyrangesbetween3daysand1month incaseofdefendant‘spassivity.Withthe introduction of e-Justice, the duration of civil andcommercialtrialsisexpectedtobefurtherreduced.TheaveragelengthofadministrativeproceedingsinBulgariais one of the shortest: between 3 and 5 months in first-instancecases.6

5AccordingtotheRegulationsofCourtsofArbitrationattheBulgarianChamberofCommerceandIndustry(BCCI)6EUJusticeScoreboard2015

33

Regulation of Advertising

Electronic Commerce and Virtual Currency

Bulgarianlegislationsetsstandardsforadvertisingtoprotectconsumersfrommisleadingadvertisementsandsomegroupsinvolved in the preparation of advertising communicationsuch as minor actors. The legislator provides for thepropriety and relevance of the advertising communicationwith the responsible and professional tone expected by theBulgariansociety.Thelawprovidesthatthecontrolovertheserequirementstobeexercisedthroughself-regulation.The Bulgarian Association of Advertisers, the BulgarianAssociationofCommunicationsAgenciesandtheAssociationof Bulgarian Broadcasters have established the National

Council forSelf-Regulation (NCSR).NCSRaims to supporttheoperationsoftheadvertisingindustrytohighprofessionalandethicallevel.NCSRhassetupandmonitorstheobservanceoftheCodeofEthicsforrulesandbestpracticesinthefieldof advertising communication. In violation of these rules,NCSRmayorderthesuspensionofcertainadvertising.Iftheadvertisingisnotsuspended,thelawprovidesforcertainfines.Furthermore, NCSR offers the Copy Advice service, whichinvolvesreview,approvalandrecommendationsonthecontentof advertising campaigns before their official broadcast toensuretheircompliancewiththeCodeofEthics.

The requirements of the Bulgarian legislation concerningthe implementation of electronic commerce comply withthe European legal framework. The Electronic CommerceAct, harmonizing the European framework with Directive2000/31/EC(ElectronicCommerceDirective).The specificobligations of the suppliers are related to the provision ofpriorinformation,additionalrequirementsforcontractingbyelectronic means. It specifically regulates the liability of theserviceprovidersoftheinformationsocietyandtheapplicablelawinconcludingsuchcontracts.According to the European Banking Authority, virtualcurrency is a typeofunregulateddigitalmoney that isnotissuedandguaranteedbytheCentralBankandthatcanactasameansofpayment.Inrecentyears,BitcoinvirtualcurrencyhasbeenalsoestablishedinBulgaria,thuscreatingconditionsfor a new generation of decentralized, peer-to-peer virtualcurrencies–oftenreferredtoas„cryptocurrencies“.According to the opinion of the Bulgarian National Bank,Bitcoinvirtualcurrencyisnotalegaltender.Theacquisition,trading and payment operations using Bitcoin are notgovernedbythenationallawandarenotsubjecttolicensingorregistration.Given the nature of Bitcoin and the other similarcryptocurrencies, they could represent and/or serve as anunderlyingassetofderivativefinancialinstruments.

34 This Guide is prepared by Popov & Partners law firm, a member of TAGLaw

Banks in Bulgaria offer cross-border money transfers in allcurrencies to/from countries around the world through awide network of correspondents. Usually outgoing transfersaremadewithin1workingday,andavalue-dateofthesamedayisalsopossible.Mostbanksoffertheoptionofreceivingandmakingforeigncurrencypaymentsindifferentcurrencies

withoutrequiringthecustomertomaintainacurrentaccountin the respective currency. The bank commissions forpaymentsinforeigncurrencyarehigherthanthoseestablishedforpaymentsinBGN–0.10%to0.40%,dependingonthevaluedate,andminimumthresholds(atleastEUR10)havebeenset.7

International Money Transfers

Employment RelationshipCurrently, in Bulgaria there is a detailed legal arrangementof the relationship involved in the provision of workforceprovidingforahighlevelofemployees‘rightsprotection.

Thisarrangementhasthefollowingadvantages:

Opportunity for flexible work organization (differenttypesofworkinghoursandmethodsofcalculation)andemploymentschemes,including:

• 8workinghours.Part-timeworkisalsopossible,aswellas working time with variable duration and unilateralextensionofworkinghoursupto12hours;

• Therearefixed-termcontractsforprojectsandtemporaryworkforamaximumdurationof36months,contractsfor homeworking, contracts for part-time employment,contractswithdurationof1calendardayforagriculturaloperations,etc.;

• Staff leasing contracts make up a widely used model,includinginthesectorsofICTandbusinessprocessandservicesoutsourcing;

• 50-hour working week is allowed for no more than 2monthsayearincaseofaseasonalincreaseofwork;

7AccordingtotariffsofRaiffeisenbankandUnicredit

35

Requirement for StaffRecruitment

Bulgaria 214 € Germany 1473 € Estonia 390 € France 1458 € Romania 218 €

Prerequisitesforachievinggoodeducationalstructureandlevelofthelabourforceandemploymenthavebeenestablished–theprocessofdualtraininglegallyestablished,opportunitiesareprovidedforongoingqualificationandre-qualificationofemployees;

Relativelylowlabourcosts–Bulgariaisthecountrywiththelowestminimumwage.Despitethetrendtowardsincreasingtheminimumwage,itisstillsignificantlybelowtheaverageintheEuropeanUnion(€214.00permonthand€1.27perhour).

Relativelylowminimumamountofpaidannualleave:20workingdaysperyear.Forcomparison,theminimumamountofpaidannualleaveinSpainis30calendardays,inGermany–24workingdays,Estonia–28workingdays,Italy–30days,Austria–between30and36workingdays.

The employer is entitled to terminate the employment contract with immediate effect and without reason during theprobationaryperiod(6months);

Absenceoftradeunionsofworkersinmostbusinesssectors.

Comparative table of the minimum gross salary in 5 EU member States, randomly selected

Statutory minimum of the monthly salary

AnyemployerstartingbusinessinBulgariaisboundbycertainmandatoryrequirementsbeforeenteringintoanemploymentcontractwithanemployee

todevelopandapproveInternalLabourRegulations,whichregulateatintercompanyleveltheissuesoforderanddiscipline,governingtheimplementationofworktasksintheenterprise;

todevelopandapproveRulesforWages,whichlaydowntherulesforwagearrangement,wagepaymentsystems,allocationoffundsforwages,determiningtheminimumbasicsalariesbypositions,etc.;

toenterintoacontractwiththeoccupationalhealthservice; toensurethemaintenanceofrecordsforinitialandperiodicinstruction.

36 This Guide is prepared by Popov & Partners law firm, a member of TAGLaw

Execution of Employment Contracts

Types of Employment Contracts and Employment Schemes

Bulgarianlegislationrequiresthattheemploymentcontractbeconcludedinwritingandcontaincertainminimumrequisites.TheemployerisrequiredtoregistertheemploymentcontractsexecutedwiththerespectiveterritorialdirectorateoftheNationalRevenueAgencybeforetheemployeecommenceswork.

Permanent employment contract – executed for anindefinite period and creates the most stable and long-term mutual commitment between the parties to theemploymentrelationship.

Fixed-term employment contract – executed for a fixedperiodunderthefollowingcircumstances:

• foraspecifiedperiod,whichmaynotexceed3years;• untilthecompletionofthespecificjob;• toensurereplacementofanemployeewhoisabsentfrom

work;• forapositionoccupiedfollowingacompetition—forthe

timewhilethepositionisvacantuntilthecompletionofthecompetition;

• for a fixed term, when such term is established for therelevantentity.

The fixed-term employment contract may not be extendedmorethantwice,wherethetotaldurationmaynotexceed3years.

Homeworking,distanceworking–allowsforflexibilityforbothemployersandemployeeswithrespect tobusinessstructuringandperformanceofjobduties.

Employment contract with a condition of performingworkbyanundertakingwhichprovidestemporarywork– allows for the implementation of the so-called „staffrenting“service.Theemployeesexecuteanemploymentcontractwithanemployerwhowaspreviouslyregisteredas a company that provides temporary work. Thus,the employees are sent to another entity, where theyactually work, but without entering into employmentrelationswith thecompanywhere theywork.This typeof contracts may only be concluded for a fixed periodendingeitherwiththecompletionofcertainwork(projectwork),orwiththereplacementoftheemployee.

Contractforextrawork–thistypeofcontractrequirestheavailabilityofanotherprimaryemploymentrelationship.Such contracts may be executed both for work for thesameemployerundertheprimaryemploymentcontract,andforworkwithanotheremployer.

37

Laying-off Workforce

Thepresenceof the above reasons shouldbedulydocumentedby the employer.The employee is entitled to challenge thedismissalwithterminationnoticeincourt.Intheeventthatthecourtfindsthattheterminationisnotsufficientlyobjectivelygrounded,thecourtmayorderthatthelaid-offemployeeshouldbereinstated.

Terminationwithnotice-theemployerisentitledtoterminatetheemploymentrelationshipinthefollowingcircumstancesonly:

• Uponclosingoftheenterpriseorpartthereoforreductionofthestaff;

• Uponreductionofthevolumeofwork;• Incaseofstoppageformorethan15workingdays;• Whentheemployeelacksqualitiestoeffectivelyperform

thejoborwhentheemployeedoesnothavetherequirededucationorqualificationstoperformthework;

• Uponrefusaloftheemployeestofollowtheentityoritssubsidiarywheretheyworkwhenthebusinessmovestoanotherlocations;

• Whenthepositionoccupiedbytheemployeeshouldbereleasedtorestoreanillegallydismissedemployeewhohaspreviouslyoccupiedthesameposition;

• Uponentitlementtoapensionorwhentheemploymentrelationship has commenced after the employee hasacquiredandexercisedtheirrighttoapension;

• Upon changing the performance requirements for theposition,iftheemployeefailstocomplywiththem;

• Upon objective inability to perform the employmentcontract;

• Duetotheexecutionofacontractformanagementoftheenterprise.

38 This Guide is prepared by Popov & Partners law firm, a member of TAGLaw

Terminationwithoutnotice–theemployerisrequiredtoindicateaspecificlegalbasisforsuchtermination.Theemployeeisentitledtodisputetheexistenceofthespecifiedlegalbasisandappealtheterminationincourt.Theemployermayusethisprocedureforterminationofemploymentwhentheemployee:

TerminationofEmploymentattheInitiativeoftheEmployeragainstaCompensationUponterminationonthisbasis,thecompensationmaynotbelessthan4grosswages.

Labour legislation in Bulgaria provides for several paymentsystemsatwork:

accordingtoduration; accordingtotheoutput; mixedsystem.

To labour expenses should be supplemented with otherexpenses which constitute additional remuneration.The following should be considered as such additionalremuneration:

expensesforovertime; expensesfornightwork; expensesforemploymentatthedisposaloftheemployer; expenses foracquired lengthof serviceandprofessional

experience.

• isarrestedforexecutionofsentence;• isdeprivedbyacourtjudgementorbyanadministrative

procedureoftherighttopracticeaprofessionortooccupythepositiontowhichtheemployeewasappointed;

• isdeprivedofthequalificationdegree, iftheconclusionof the employment contract was made in view of thequalificationdegreeacquired;

• is deleted from the records of the professional

organizations;• refuses to take the suitable position offered in case of

vocationalrehabilitation;• isdismissedfordisciplinaryreasons;• failstonotifyoftheexistenceofincompatibilitywiththe

workperformed,existenceofsuchanincompatibilityorconflictofinterestestablishedunderthePreventionandDisclosureofConflictsofInterestAct.

The employermay terminate the employment contractwithoutnotice and isnot required toprovide reasons for such act,providedthatthecontractwasconcludedforaprobationaryperiodinfavouroftheemployer,whichperiodmaynotbelongerthan sixmonths.During theprobationaryperiod, thepartieshave all rights andobligations aswith the final employmentcontract.

Labour Expenses

MINIMUM WAGE

270 BGN 290 BGN 310 BGN 340 BGN 360 BGN 380 BGN 420 BGN

Relevant part of the social security contributions of the employees is borne by the employer. Generally, the social securitycontributionsamountto30%ofthewageandalmost60%ofthecontributionisbornebytheemployer.

01.01.2012 -

30.04.2012

01.05.2012-

31.12.2012

01.01.2013 -

31.12.2013

01.01.2014 -

31.12.2014

01.01.2015 -

30.06.2015

01.07.2015-

31.12.2015

01.01.2016 -

present

39

Employment Funding Options

Real Estate Investment Regime

Promotionofemploymentandtheprovisionofnewjobs isapriority inthe labour legislationoftheEuropeanUnionandBulgaria. EU funds allocated for the employment in Bulgaria are available through the Operational Programme „HumanResources Development“ (OP HRD), where employers and organizations are entitled independently to apply with projectsprovidedthattheymeetcertaincriteria.

AccordingtotheBulgarianlegislation,realestatetransactionsbetweenindividualsareperformedbymeansofanotarydeedexecutedbyaregisterednotarypublic.Afterissuingthedeed,thetransactionissubjecttoregistrationandaftertheregistrationtherealrightisconsideredtobetransferred.

AcertainsetofdocumentsissuedbytheBulgarianauthorities,theauthoritiesofthecountriesoforiginofthepersons,declarationoforiginofthefundsusedforthepaymentoftheprice,declarationoflackofpublicobligationsofthetransferor,etc.,shouldbesubmittedtothenotarypublic.

Thecostsfortheacquisitionofrealestatevarydependingonthespecificmunicipalitywheretheacquiredrealestateislocated,thetypeoftransactionandotherfactors.ThefollowingtableshowsthebasictaxesandfeesfortheacquisitionofrealestateregulatedbythelawsofBulgaria.

Tax/fee Amount

ValueAddedTax 0or20%(dependingontherealestate/seller)

Taxonrealestateacquisitionforvalue 1.3%to3%(indifferentmunicipalities)

Feeforregistrationofthetransaction0.1%onthehigherofthefollowingtwovalues:a)priceofthetransferredrightagreedbetweentheparties,andb)taxvaluationoftherealestate

NotaryfeeDependingonthevalueofthetransaction,butnotmorethanEUR3,070,excludingVAT

40 This Guide is prepared by Popov & Partners law firm, a member of TAGLaw

OwnershipofagriculturallandcanbeacquiredbyforeignindividualsandforeignlegalentitiesthathaveresidedorexistedintheRepublicofBulgariaformorethan5years.AnexceptionisprovidedforlegalentitiesregisteredundertheBulgarianlegislationforlessthan5years,providedthattheirpartners,associationmembersorjointstockcompanyfoundershaveresidedorestablishedintheRepublicofBulgariaformorethan5years.Thefollowingentitiesmaynotacquireandownpropertyonagriculturalland:

commercialcompanieswherethemembersorshareholdersareconstituteddirectlyorindirectlyascompaniesregisteredinlistedpreferentialtaxregimejurisdictions;

commercialcompanieswherethemembersorshareholdersareforeignersandforeignlegalentities(notapplicablefornationalsofEUmemberstatesorpartiestotheEEAAgreement,tonationalsofcountrieswithwhichtherelevantinternationaltreatywassignedandincaseofinheritancebylaw);