Building Simple Continuous Reviews in ACL

29

Building Simple Continuous Reviews in ACL TM July 2, 2014 AuditNet and AuditSoftwareVideos.com Collaboration Brought to you by AuditSoftwareVideos.com and AuditNet ® , working together to provide: Practical audit software training Resource links Independent analysis Tools to improve audit software usage Today focused on providing practical data analysis training Page 1

-

Upload

jim-kaplan-cia-cfe -

Category

Data & Analytics

-

view

366 -

download

16

description

Continuous auditing and monitoring (“continuous reviews”) has been discussed for decades but implemented in moderation based on recent surveys. It comes down to how much are data analytics integrated into our audit processes initially to then become continuous. If a high degree of integration exists, then there is probably a good amount of continuous reviews happening in the organization already. However, most companies fall into the other camp and have not integrated analytics well enough or considered how to take full advantage of continuous reviews. This course will explain culturally what audit departments must do to embrace continuous reviews and how that can be integrated with ACL Desktop software techniques. Sample files and scripts will be provided to get you started down the road to continuous reviews. As regulatory changes sweep the globe, auditors, risk management, and compliance professionals are using more sophisticated tools, and methods. Using a live/video training library approach, we help companies of all sizes use audit and assurance software to improve business intelligence, increase efficiencies, identify fraud, test controls, and bottom line savings. AuditNet and Cash Recovery Partners Webinar recording available at auditsoftwarevideos.com and AuditNet.tv (registration required) Recording free to view. Sample Data Files for All Courses are available for $49 To purchase access to all sample data files, Excel macros and ACL scripts associated with the free training visit AuditSoftwareVideos.

Transcript of Building Simple Continuous Reviews in ACL

Building Simple Continuous Reviews in ACLTM

July 2, 2014

AuditNet and AuditSoftwareVideos.com Collaboration

Brought to you by AuditSoftwareVideos.com and AuditNet®, working together to provide:Practical audit software training

Resource links

Independent analysis

Tools to improve audit software usage

Today focused on providing practical data analysis training

Page 1

About Jim Kaplan, CIA, CFE

President and Founder of AuditNet®, the global resource for auditors (now available on Apple and Android devices)

Auditor, Web Site Guru,

Internet for Auditors Pioneer

Recipient of the IIA’s 2007 Bradford Cadmus Memorial Award.

Author of “The Auditor’s Guide to Internet Resources” 2nd Edition

Page 2

About AuditNet® LLC

• AuditNet®, the global resource for auditors, is available on the Web, iPad, iPhone and Android devices and features:

• Over 2,000 Reusable Templates, Audit Programs, Questionnaires, and Control Matrices

• Training without Travel Webinars focusing on fraud, audit software (ACL, IDEA, Excel), IT audit, and internal audit

• Audit guides, manuals, and books on audit basics and using audit technology

• LinkedIn Networking Groups

• Monthly Newsletters with Expert Guest Columnists

• Book Reviews

• Surveys on timely topics for internal auditors

Introductions

Page 3

Webinar Housekeeping

Page 4

This webinar and its material are the property of Cash Recovery Partners LLC. Unauthorized usage or recording of this webinar or any of its material is strictly forbidden. We are recording the webinar and you will be provided with a link to that recording as detailed below. Downloading or otherwise duplicating the webinar recording is expressly prohibited.

Webinar recording link will be sent via email within 5‐7 business days.

NASBA rules require us to ask polling questions during the Webinar and CPE certificates will be sent via email to those who answer ALL the polling questions

The CPE certificates and link to the recording

will be sent to the email address you registered with in GTW. We are not responsible for delivery problems due to spam filters, attachment restrictions or other controls in place for your email client.

Submit questions via the chat box on your screen and we will answer them either during or at the conclusion.

After the Webinar is over you will have an opportunity to provide feedback. Please complete the feedback questionnaire to help us continuously improve our Webinars

If GTW stops working you may need to close and restart. You can always dial in and listen and follow along with the handout.

Disclaimers

5

The views expressed by the presenters do not necessarily represent the views, positions, or opinions of AuditNet® or the presenters’ respective organizations. These materials, and the oral presentation accompanying them, are for educational purposes only and do not constitute accounting or legal advice or create an accountant‐client relationship.

While AuditNet® makes every effort to ensure information is accurate and complete, AuditNet® makes no representations, guarantees, or warranties as to the accuracy or completeness of the information provided via this presentation. AuditNet® specifically disclaims all liability for any claims or damages that may result from the information contained in this presentation, including any websites maintained by third parties and linked to the AuditNet® website

Any mention of commercial products is for information only; it does not imply recommendation or endorsement by AuditNet®

Richard B. Lanza, CPA, CFE, CGMA

• Over two decades of ACL and Excel software usage• Has written and spoken on the use of audit data analytics for

over 20 years.• Received the Outstanding Achievement in Business Award by

the Association of Certified Fraud Examiners for developing the publication Proactively Detecting Fraud Using Computer Audit Reports as a research project for the IIA

• Recently was a contributing author of:• Global Technology Audit Guide (GTAG #13) Fraud in an

Automated World – Institute of Internal Auditors.• Data Analytics – A Practical Approach - research whitepaper

for the Information System Accountability Control Association.

• Cost Recovery – Turning Your Accounts Payable Department into a Profit Center – Wiley and Sons.

Please see full bio at www.richlanza.com

Learning Objectives

Why it is important to development continuous monitoring applications in key areas of your business to reduce audit time while increase audit quality. Integrating analytics in all areas of the audit process from audit planning to follow up. Outline an effective data request process to ensure complete and accurate extractions of data every time. Discuss auto-normalization techniques of data to speed the reporting process. See how analytics can maximize the annual audit plan and better ensure focus is placed on organizational risk. Understand how to develop Excel / CSV export routines that auto-export data from ACL at the end of processing. Pros and cons of specific software tools when implementing data analytics and continuous reviews.Understand some common approaches to overcoming obstacles to planning data analytics based on case studies from companies and survey attendees themselves.

Page 7

Continuous Audit / Continuous Monitoring -Why It’s Important and Audit Software Integration

Page 8

Analytic Command Center“Auditor in a Can”

Page 9

Top Audit Software Implementation Practices

Page 10

Audit Analytic Best Practices

Automate the data import and normalization process Develop Excel macros to improve client provided data quickly

Automate the data extraction, file cleansing, and data validation

Everyone is different with their data – so normalize

Reduce false positives in the final reports Prioritize the likelihood of findings

Use mathematical scoring

Document, save, and possibly videotape your work plan Audit logs in software, flowcharts, and documents take minutes to

develop to the hours to later remember what was done

Video editing (Camtasia) can be used to show how to run applications for future auditors

Page 11

Think Prevention vs. Future Detection Identify issues earlier in their lifecycle Build a aura of deterrence within procure to pay

Build a Continuous Review Process Technology Minimal staff time / external assistance

Keep Improving the Model Model on identified frauds Remove false positives to isolate interesting events

Best Practice Approach on Fraud - Find It Before It Finds You

Data Marts and Server Benefits

Centralized data and backups

Audit knowledge is saved in one place Remove the “Learn and Leave” dilemma facing companies

Security and user management

Better data than the business units

Faster processing for large data sets

Page 13

Data Marts and Server Reality

Most audit areas don’t require it Data is only needed once a year or more for some audits

Data extraction routines can be saved by IT and audit

Server speed is not needed for majority of audits

Sometimes difficult to explain the ROI to I.T. if smaller “example” audits are not completed first High initial cost of a sledgehammer for hanging a picture

May turn off management to all data analytics

Page 14

Value of ACL Scripting

Useful for routine tasksCan be for periodic audit stepsAlso can assist in importing similar data

• For example, OPEN FILE 1, EXTRACT RECORD, OPEN FILE 2, EXTRACT RECORD, etc.

Build the quality in once “Set it and forget it”

Learn how ACL works behind the scenesValue of learning ACL for DOS

Page 15

Making it Continuous

Does not make sense for every audit area Makes sense for general ledger in all companies

Find willing business units who want to self-review

Start small, roll out audit applications, and have a management plan that does NOT include audit except for business requirement changes

Audit can have access and should periodically “kick the tires”

Page 16

Polling Question 1

Polling Question Displayed during the Webinar

Effective Data Request Process andAuto-Normalization

Page 18

20

There’s Gold In That Data

Taken from the 2007 Buyer’s Guide to Audit, Anti-Fraud, and Assurance Software

Data Request is Sent Prior…..11/14/12 Webinar

Page 2111/14/12

Top 10 Data Import Mistakes

1. Not knowing what is possible within the tool to import and normalize data

2. Asking for data before understanding reporting needs

3. Not including knowledgeable system professionals to assist in or review the extract

4. Forgetting to run statistics on amount/date fields5. Not summarizing text code fields (including

invoice numbers to find E+ issues)

Page 22

Top 10 Data Import Mistakes

6. Lack of hardcopy information for review in relation to imported data

7. Not validating field totals to batch totals

8. Using report files vs. fixed length system files

9. Getting data in Excel vs. a more raw format

10.Lack of understanding of the various data types

Page 23

Clear Data Request

Accounts Payable Data Request.doc

Data Import ModuleFrom Excel

Import Script Code.xlsx

Polling Question 2

Polling Question Displayed during the Webinar

Maximize the Audit Plan and Building an Organizational Viewpoint

Page 27

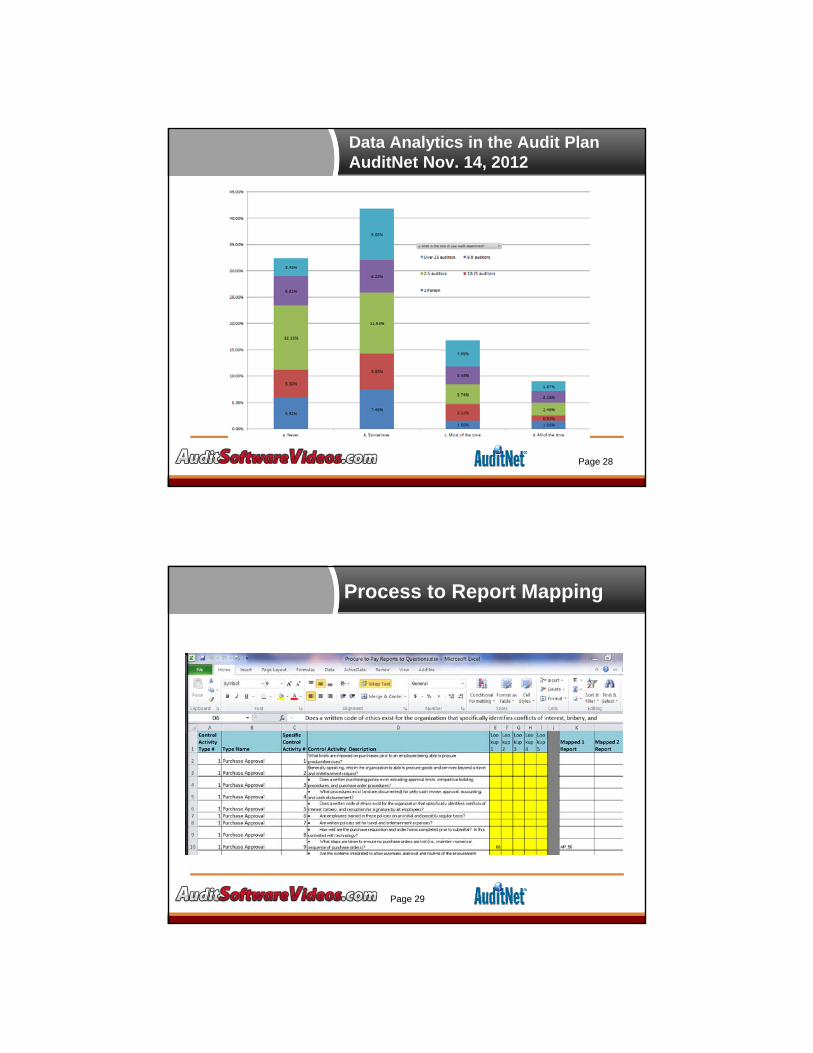

Data Analytics in the Audit PlanAuditNet Nov. 14, 2012

Page 28

Process to Report Mapping

Page 29

Mapping Data and Objectives

30

Query Viewpoints

Query T&E Reports

Unmatched query of cardholders to an active employee masterfile

Cards used in multiple states (more than 2) in the same day Cards processing in multiple currencies (more than 2) in the

same day Identify cards that have not had activity in the last six

months Cardholders that have more than one card Extract any cash back credits processed through the card Extract declined card transactions and determine if they are

frequent for certain cards

Data Mining T&E - It’s The Trends…Right?

Trend categories (meals, hotel, airfare, other)

Trend by person and title

Trend departments

Trend vendors

Trend in the type of receipts

Trend under limits (company policy)

33

Transactional Score Benefits

The best sample items (to meet your attributes) are selected based on the severity given to each attribute. In other words, errors, as you define them, can be mathematically calculated.

Instead of selecting samples from reports, transactions that meet multiple report attributes are selected (kill more birds with one stone). Therefore a 50 unit sample can efficiently audit:

38 duplicate payments

22 round invoices

18 in sequence invoices

….and they are the best given they are

mathematically the most “severe”.

34

Pick Items Rare in Several Ways

Don’t choose just ANY weekend invoice

Choose an UNUSUAL weekend invoice

Large weekend invoices are the rarest kind (i.e., only 2 percent of large invoices)

The odds of finding a recoverable error go up AND since the invoice is large, the value recovered goes up too!

Page 35

Summaries on Various Perspectives

36

Summarize by

dimensions (and sub

dimension) to pinpoint

within the cube the

crossover between the top

scored location, time, and

place of fraud based on

the combined judgmental

and statistical score

ALL TIES BACK TO THE

ORIGINAL ANALYTIC

APPROACH

Combining the ScoresACL Code

Page 37

Obtain data at least once a year for use in the planning exercise Basic data may all that is needed from key systems and locations

Run a series of tests across each location’s data Consider focusing on general ledger given its broad exposure to the

business Consider using risk scoring in a consistent fashion across the

company

Prototype a few local audit toolkits each year Most cost effective way to develop and ACL is cheaper than almost

any other development platform for finance/audit professionals Identify “low hanging fruit” for cost savings and improvements.

Considerations for Overall Audit Planning

Normalize and test general ledger data consistently on all locations

Most internal audit shops obtain general ledger data quarterly for their external auditors anyway – no excuse

G/L data is the lifeblood of the organization

Planning will improve as focus can be placed on key accounts, entries, timeframes, enterers, etc. and will guide future data extracts

Most systems post in detail (even down to inventory movements) which can allow detailed review of subledgers….using G/L data

Identify savings, better ideas,…and fraud

Fraud has been the focus and we should still test for it

Savings in cost recoveries can now become more of a focus

Better ideas leveraged through technology

• Efficiency (to help a faster close)

• Revenue and business enhancement

Key Mantras of G/L Analytic Auditing

Journal Entry Surveillance System (“J.E.S.S”) Overall Review Objectives

Model “normal” account behavior

Identify unusual changes in activity

• Over time

• By account sequence

• In amount

• In value (I/S, B/S, Net effect)

• In enterers behavior or words entered

• Key concern accounts

Detect unusual journal entries based on past risk factors and expected schemes

Monitor unauthorized enterers

Reconcile GL activity to trial balance figures (completeness) and financial statements

Profit Opportunities Outweigh Analytic Costs

Accounts PayableAudit Fee BenchmarkingAdvertising AgencyDocument FleetFreightHealth BenefitsLeaseMediaOrder to Cash

Proactive Fraud DetectionProject FraudReal Estate DepreciationSales & Use Tax / VAT / R&D taxStrategic SourcingTelecomTravel and EntertainmentUtilities

Cost Recovery Opportunity Tests

A/P and G/L Review Factors Accounts that are sole sourced Accounts that have too many vendors Categories that map to the “recovery

list” Assess to industry cost category

benchmarks Top 100 vendors Trend analysis over time Trend analysis by vendor (scatter

graph)

Polling Question 3

Polling Question Displayed during the Webinar

Auto-Workpaper Export Routines

Page 44

Polling Question 4

Polling Question Displayed during the Webinar

Pros and Cons of Tools When Implementing Continuous Analytics & Overcoming Obstacles

Page 46

Most Popular Audit Software Products

ACL / AX

ActiveData for Excel

Arbutus Software

IDEA

Microsoft Access

Microsoft Excel

TopCaats

Tool Selection Considerations

Core processing features

Advanced features

Advanced data import

Scripting

Ease of use

Training / Customer Support / User Groups

Years in business / Company sustainability

Workpaper system integration

Proposal Decision Analysis

Page 49

http://www.caseware.com/products/idea#_research_reports

Use data analytics on almost every audit Brainstorm the use data analytics in the audit planning process

Drop an audit and instead plan 10% for “data fun” across all audits / Understand the process and benchmark it for future reviews

Make it part of annual objectives to use the product

Find cost savings to pay for the usage & Track it & Promote it Risk assess the general ledger – stratify by month by account J/E risk

scores

Search for cost recovery opportunities

Sell the need for increased software and education• Also sell the cost/benefit of ACL to other development platforms

(especially for prototyping).

Overcoming Obstacles

Page 50

Plan on education and make it routine Meet every three weeks on analytics – no matter what

Build a team of champions to coach the team

Get everyone else involved…..even if it is with Excel to start

Make it part of annual objectives to learn the product

Establish data channels to all (material) parts of the organization Have more freedom to extract data as needed

Obtain quarterly feeds of data

Obtain data from all locations once a year for audit planning

Overcoming Obstacles

Page 51

Polling Question #5

Page 52

Polling Question Displayed during the Webinar

Questions?

Any Questions?Don’t be Shy!

Page 53

In the Queue

Sampling in Excel and Other Simple Add-In Products – Aug 13

ACL Basic/Intermediate Scripting – Sept 10

Financial Statement Analysis to Journal Reviews With Excel Tools – Oct 7

AuditSoftwareVideos.com

Videos accessible for FREE subscriptions

Repeat video and text instruction as much as you need

Sample files, scripts, and macros in ACL™, Excel™, etc. available for purchase

Bite-size video format (3 to 10 minutes)

Page 55

>> Professionally produced videos by instructors with over 20 years experience in ACL™, Excel™ , and more

Thank You!

Jim KaplanAuditNet® LLC

1-800-385-1625Email:[email protected]://www.auditnet.org

Richard B. Lanza, CPA, CFE, CGMACash Recovery Partners, LLC

Phone: 973-729-3944Cell: 201-650-4150Fax: 973-270-2428

Email: [email protected]://www.richlanza.com

Page 56