Building for the future - nordea.com · 116 154 166 166 166 64 64 64 163 82 115 82 239 178 137 ......

26

Sanford C. Bernstein Pan-European Strategic Decisions Conference 18 September 2014 Christian Clausen, President and Group CEO Building for the future

Transcript of Building for the future - nordea.com · 116 154 166 166 166 64 64 64 163 82 115 82 239 178 137 ......

Sanford C. Bernstein Pan-European Strategic Decisions Conference

18 September 2014

Christian Clausen, President and Group CEO

Building for the future

Headline lower line

Sub-head line

Single medium chart axis

Right content border

Slide bottom border

Left border Right border Left content border

Comment text box top

Content and chart border

Small chart axis

Sub-head line

Small chart top

Small chart axis

Left and right small lower comments top border

Single medium chart toptop

Heading

Primary chart colours

Sub-head

Content lines (Non-Nordea)

Small chart top

76 116 154

166 166 166

64 64 64

163 82

115

239 178 137

119 154 188

175 80 70

233 170

0

217 217 217

Page numbers 166 166 166

Secondary chart/diagram colours (Non-Nordea)

185 205 229

217 217 217

Other chart and ornamental colours

239 241 204

211 157 155

204 102

0

127 127 127

82 82 82

217 217 217

Comments 76 116 154

166 166 166

This presentation contains forward-looking statements that reflect management’s current

views with respect to certain future events and potential financial performance. Although

Nordea believes that the expectations reflected in such forward-looking statements are

reasonable, no assurance can be given that such expectations will prove to have been

correct. Accordingly, results could differ materially from those set out in the forward-looking

statements as a result of various factors.

Important factors that may cause such a difference for Nordea include, but are not limited

to: (i) the macroeconomic development, (ii) change in the competitive climate, (iii) change

in the regulatory environment and other government actions and (iv) change in interest rate

and foreign exchange rate levels.

This presentation does not imply that Nordea has undertaken to revise these forward-

looking statements, beyond what is required by applicable law or applicable stock

exchange regulations if and when circumstances arise that will lead to changes compared

to the date when these statements were provided.

Disclaimer

2 •

0

96

161

225

106

3

1

144

163

163

153

111

175

80

70

127

127

127

233

170

0

163

82

115

103

172

206

239

178

137

117

204

208

204

199

178

211

157

155

182

185

186

242

206

134

206

159

182

Primary Colours Extra Colours

76

116

154

Chart Colours 119

154

188

166

166

166

191

191

191

127

127

127

204

102

0

0

96

161

Nordea was created with the vision that the Nordic

region was one market and to establish a pan-Nordic

platform

Nordic ideas

3 •

Nordea has established a pan-Nordic platform… … and is the largest financial services group in the region

Today, Nordea is the largest financial services group in

the Nordic and Baltic Sea region

11 million customers

Distribution power through 800 locations and

over 7 million Netbank customers

Financially strong with a CET1 capital ratio of

15.2%

AA credit rating

EUR ̴ 41bn in market cap and a top-10 European

retail bank

The relationship bank business model

has delivered 14

0

96

161

225

106

3

1

144

163

163

153

111

175

80

70

127

127

127

233

170

0

163

82

115

103

172

206

239

178

137

117

204

208

204

199

178

211

157

155

182

185

186

242

206

134

206

159

182

Primary Colours Extra Colours

5 76

116

154

Chart Colours 166

166

166

191

191

191

127

127

127

204

102

0

0

96

161

119

154

188

Nordea has a unique position in the Nordics…

Note: Illustration excludes, Baltic's (406,700 total customers) and Russia (67,000 total customers)

1: Ranking in Nordic region

Sweden

Norway

Finland

Denmark

Relationships

(m)

Market

position

Superior customer franchise Global capabilities on par with

international peers1

Relationships

(‘000s)

52 #1-2

Total

Nordea 10.5 #1 540 #1

Capital Markets

Asset

Management

Life &

Pension

Private Banking

#1

#1

#1

#1

Retail Customers Corporates & Institutions

4.1 #2-3

1.0 #2

3.2 #1-2

1.8 #2

238 #1-2

88 #2

125 #1

Market

position

…with a resiliant relationship bank business model

Nordea is the most

diversified Nordic bank…

…with low-volatility

earnings growth…

…and low funding costs

Nordea Peer 1 Peer 2 Peer 3 Peer 4 Peer 5

Largest market contribution1

Nordea Peer 1 Peer 2 Peer 3 Peer 4 Peer 5

Earnings volatility2 Funding cost3

Nordea Peer 1-18

Notes:

1) Credit portfolio by geographical area

2) Net income volatility 2008-2013. Compared to Nordic peers

3) Five year Senior CDS spread. Compared to European peers

6 •

2015 plan update 14

Headline lower line

Sub-head line

Single medium chart axis

Right content border

Slide bottom border

Left border Right border Left content border

Comment text box top

Content and chart border

Small chart axis

Sub-head line

Small chart top

Small chart axis

Left and right small lower comments top border

Single medium chart toptop

Heading

Primary chart colours

Sub-head

Content lines (Non-Nordea)

Small chart top

76 116 154

166 166 166

64 64 64

163 82

115

239 178 137

119 154 188

175 80 70

233 170

0

217 217 217

Page numbers 166 166 166

Secondary chart/diagram colours (Non-Nordea)

185 205 229

217 217 217

Other chart and ornamental colours

239 241 204

211 157 155

204 102

0

127 127 127

82 82 82

217 217 217

Comments 76 116 154

166 166 166

The 2015 plan – an update

Nordea market commitments Key initiatives and levers

Strong capital generation and

increased payout ratio in 2014 and 2015

while maintaining a strong capital base

To reach a ROE of 13% at the required

CET1 ratio taking prevailing low interest

rates into account

Delivering low-volatility results

based on a well diversified and resilient

business model

Capital initiative to improve the CET1 ratio

Initiatives for income generation

Efficiency initiatives of ~EUR 900m

5% lower cost base 2015 vs. 2013

Low-risk profile and low volatility

8 •

Headline lower line

Sub-head line

Single medium chart axis

Right content border

Slide bottom border

Left border Right border Left content border

Comment text box top

Content and chart border

Small chart axis

Sub-head line

Small chart top

Small chart axis

Left and right small lower comments top border

Single medium chart toptop

Heading

Primary chart colours

Sub-head

Content lines (Non-Nordea)

Small chart top

76 116 154

166 166 166

64 64 64

163 82

115

239 178 137

119 154 188

175 80 70

233 170

0

217 217 217

Page numbers 166 166 166

Secondary chart/diagram colours (Non-Nordea)

185 205 229

217 217 217

Other chart and ornamental colours

239 241 204

211 157 155

204 102

0

127 127 127

82 82 82

217 217 217

Comments 76 116 154

166 166 166

11 689 12 821

14 313

17 766 19 103

20 677 21 961

23 112 23 172

2006 2007 2008 2009 2010 2011 2012 2013 H1/14

1 882 3 715

5 868 7 180 8 675

10 261 12 017 13 399 14 066

1 271

2 568

3 087 4 093

5 261

6 309

7 679

9 413 10 263

3 153

6 283

8 955

11 273

13 936

16 570

19 696

22 812 24 329

2006 2007 2008 2009 2010 2011 2012 2013 H1/14

Strong capability to generate capital

COMMON EQUITY TIER 1 CAPITAL*, EURm

CAPITAL GENERATION**, EURm

• Doubled the capital base in 7 years

• Increased CET 1 ratio from 6.8% to

15.2%

COMMENTS

Acc. retained equity

Acc. Dividend incl. accrued dividend , EUR 850m***, for H1/14

Dividend payout (accrued dividend for H1/14)

CET 1 capital

* Basel 2.5 until FY 2013. Basel 3 from 2014

** Dividend included in the year profit was generated. Excluding rights issue

(EUR 2 495m in 2009).

*** Assumes a 56% payout ratio 9 •

Headline lower line

Sub-head line

Single medium chart axis

Right content border

Slide bottom border

Left border Right border Left content border

Comment text box top

Content and chart border

Small chart axis

Sub-head line

Small chart top

Small chart axis

Left and right small lower comments top border

Single medium chart toptop

Heading

Primary chart colours

Sub-head

Content lines (Non-Nordea)

Small chart top

76 116 154

166 166 166

64 64 64

163 82

115

239 178 137

119 154 188

175 80 70

233 170

0

217 217 217

Page numbers 166 166 166

Secondary chart/diagram colours (Non-Nordea)

185 205 229

217 217 217

Other chart and ornamental colours

239 241 204

211 157 155

204 102

0

127 127 127

82 82 82

217 217 217

Comments 76 116 154

166 166 166

2,860 3,240

Income holding up

• Lending margins up 7 bps

YoY (RB)

• Lending margins up 16 bps

YoY (WB)

• Continued strong inflow of

household customers

~ 45,600 new (externally

recruited) Gold and

Premium customers (RB)

• Further strengthened

customer service model

with enhanced focus on

business potential, cross-

selling and ancillary income

(WB)

• Strengthened capital

markets position

• Strong performance in

Equities, with increasing

market shares

• Participated in three IPOs

and a number of capital

raisings

• Continued growth in AuM,

up 14% YoY

Re-pricing New customers Ancillary income

538

708

10 •

NCI DEVELOPMENT, EURm

CAGR +7%

Q2/10 Q2/14

LENDING RE-PRICING DEVELOPMENT PB AND GOLD CUSTOMERS, thousands

Q2/10 Q2/14 Q2/10 Q2/14

29 bps

CAGR +3%

Reductions in Nordea Life & Pension

Other

Increased Offshoring

Capital Markets savings

Reduced external spend

Insourcing of IT services

Branch closures and reduced cash handling

Moderated expansion plans in Wealth area

HQ programme

Streamlining & automation

11 •

Efficiency iniatives are in place to achieve the

5% cost reduction by end-2015

25%

17%

15%

10%

10%

6%

6%

4%

4%

3%

% of total cost

efficiency iniatives

Headline lower line

Sub-head line

Single medium chart axis

Right content border

Slide bottom border

Left border Right border Left content border

Comment text box top

Content and chart border

Small chart axis

Sub-head line

Small chart top

Small chart axis

Left and right small lower comments top border

Single medium chart toptop

Heading

Primary chart colours

Sub-head

Content lines (Non-Nordea)

Small chart top

76 116 154

166 166 166

64 64 64

163 82

115

239 178 137

119 154 188

175 80 70

233 170

0

217 217 217

Page numbers 166 166 166

Secondary chart/diagram colours (Non-Nordea)

185 205 229

217 217 217

Other chart and ornamental colours

239 241 204

211 157 155

204 102

0

127 127 127

82 82 82

217 217 217

Comments 76 116 154

166 166 166

Improved credit quality

TOTAL NET LOAN LOSSES, bps

• Ten year average of 16 bps

reached for first time since Q3/11

• Continued improvement in

Denmark

• Net reversals in Shipping

• Stable credit quality in other

areas

COMMENTS

12 •

-70.0

-60.0

-50.0

-40.0

-30.0

-20.0

-10.0

0.0

10.0

20.0

30.0

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 Q2/14

16 bps

Headline lower line

Sub-head line

Single medium chart axis

Right content border

Slide bottom border

Left border Right border Left content border

Comment text box top

Content and chart border

Small chart axis

Sub-head line

Small chart top

Small chart axis

Left and right small lower comments top border

Single medium chart toptop

Heading

Primary chart colours

Sub-head

Content lines (Non-Nordea)

Small chart top

76 116 154

166 166 166

64 64 64

163 82

115

239 178 137

119 154 188

175 80 70

233 170

0

217 217 217

Page numbers 166 166 166

Secondary chart/diagram colours (Non-Nordea)

185 205 229

217 217 217

Other chart and ornamental colours

239 241 204

211 157 155

204 102

0

127 127 127

82 82 82

217 217 217

Comments 76 116 154

166 166 166

13 •

Lower costs

RoE – strong underlying business performance

Excluding restructuring charge in Q2/14

Business

performance

External

factors Q2 2014 Q2 2013

11.6%

13.0%

12.0%

+1.4% -1.0%

Re-pricing

Ancillary

income

Lower

loan losses

Capital

increase

Other Volumes

Interest

rates

Headline lower line

Sub-head line

Single medium chart axis

Right content border

Slide bottom border

Left border Right border Left content border

Comment text box top

Content and chart border

Small chart axis

Sub-head line

Small chart top

Small chart axis

Left and right small lower comments top border

Single medium chart toptop

Heading

Primary chart colours

Sub-head

Content lines (Non-Nordea)

Small chart top

76 116 154

166 166 166

64 64 64

163 82

115

239 178 137

119 154 188

175 80 70

233 170

0

217 217 217

Page numbers 166 166 166

Secondary chart/diagram colours (Non-Nordea)

185 205 229

217 217 217

Other chart and ornamental colours

239 241 204

211 157 155

204 102

0

127 127 127

82 82 82

217 217 217

Comments 76 116 154

166 166 166

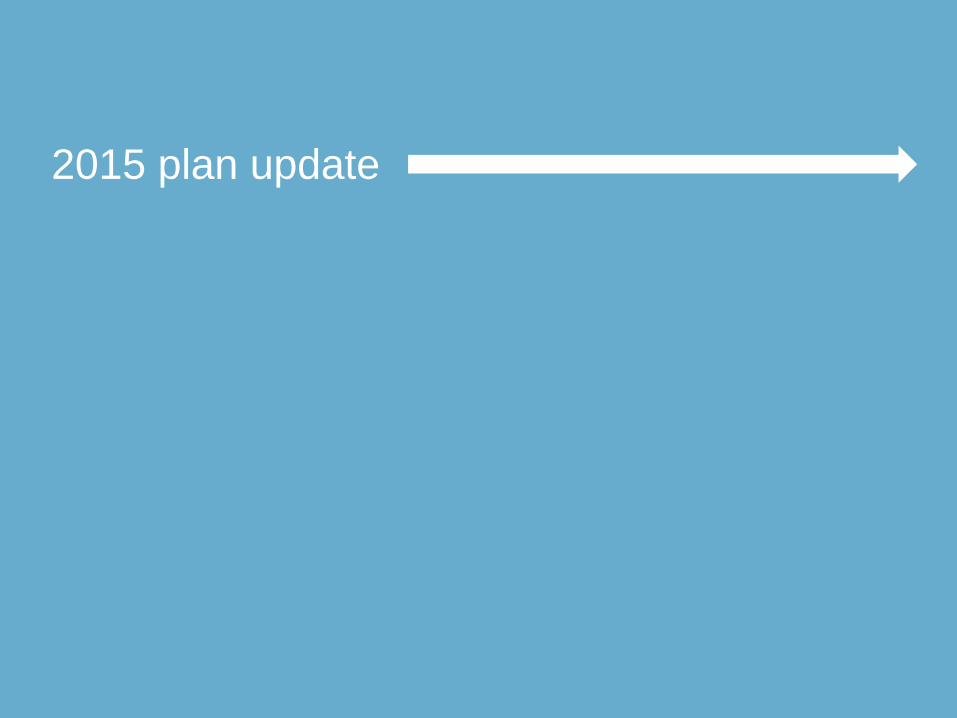

Progress in summary

• CET 1 capital ratio up 60 bps to 15.2%

PROGRESS ON NORDEA FINANCIAL PLAN 2015 IN Q2/14

CET1 capital ratio

Risk Exposure Amount

Income growth

Costs

Loan losses

RoE

P

• Total efficiencies of EUR 24bn of which 6bn in

the quarter

• Income holding up

• Cost programme delivering according to plan

• Loan loss ratio down to 16 bps

• RoE up 60 bps to 12.0%* P

P

P

P

(P)

14 • *Excluding restructuring charge in Q2/14

Banking Russia and Finland 14

16 •

Banking Russia operations

COMMENTS

• Limited share of Group operations

• 3% of income

• 2% of credit exposure

• Majority of lending is towards large

Russian corporates

• 600 Nordic customers

• Largest sector exposure

towards materials, real estate,

utilities, energy and

construction

• Largest currency exposure

towards USD (66%)

• RUB exposure funded locally via

deposits, USD and EUR exposure

funded via the Group

• Maturity of USD and EUR

funding has been prolonged

BANKING RUSSIA OPERATIONS

Nordea Bank

Russia Total

% of

Group Total

Total income 260 2.6

Operating profit 161 3.9

Nordea Bank

Russia Total

% of

Group Total

Lending corporates 5.6 3.0

Lending households 0.5 0.3

Total lending 6.1 1.8

Impaired loans gross 0.023 0.3

FY 2013, EUR MILLION

Q2 2014, EUR BILLION

Nordea actions regarding sanctions

17 •

• Task force in place since March 2014

• We monitor the development closely

• As of mid July, sanctions were extended from individuals and entities to specific

sectors – adding complexity

• Nordea follows OFAC (US), EU sanctions and Sectoral sanctions in all entities

• For non-sanction entities, business continues with existing customers

• No intention to increase business or market share

• Nordea is fully compliant with all regulatory requirements that apply to our operations

18 •

COMMENTS

• Finnish economy in undergoing the

longest downturn in 150 years

• Central and local government deficits

are large challenges

• Decline in the exports to Russia might

prolong the downturn, as Russia is

one of the largest export partners

(10% of exports)

• There are however some positive

trends which could have a positive

impact on exports

Macroeconomic view in Finland

Longest downturn in 150 years

Positive trends emerging

Index 2007=100

19 •

Finnish credit portfolio remains stable

PD development COMMENTS

Loan losses, Banking Finland, EURm

-5

0

5

10

15

20

25

30

0.000.200.400.600.801.001.201.401.601.80

20

11

Q1

20

11

Q2

20

11

Q3

20

11

Q4

20

12

Q1

20

12

Q2

20

12

Q3

20

12

Q4

20

13

Q1

20

13

Q2

20

13

Q3

20

13

Q4

20

14

Q1

20

14

Q2

Corporate

Household

• 22% of Nordea's total loan portfolio

• Average Corporate PD has gone down

as new lending is increasingly to better

rating classes

• Household average PD has increased

slightly over the last two years

• Loan losses are not showing an

increased trend despite the

macroeconomic situation

• The direct effect of Russian sanctions

and counter sanctions are hitting only

a few industries whose share of

Nordea’s lending book is very limited.

The expected direct impact on the

loan portfolio is minor

Banking business model undergoing change 14

0

96

161

225

106

3

1

144

163

163

153

111

175

80

70

127

127

127

233

170

0

163

82

115

103

172

206

239

178

137

117

204

208

204

199

178

211

157

155

182

185

186

242

206

134

206

159

182

Primary Colours Extra Colours

0

96

161

225

106

3

1

144

163

163

153

111

175

80

70

127

127

127

233

170

0

163

82

115

Primary Colours

76

116

154

Chart Colours 166

166

166

191

191

191

127

127

127

204

102

0

0

96

161

119

154

188

103

172

206

239

178

137

117

204

208

204

199

178

211

157

155

182

185

186

242

206

134

206

159

182

Extra Colours

21

SEPA End-date

Securities Law

Directive

FTT

Recovery & Resolution

for FMIs

Liikanen

Structural Reform

Shadow Banking

MiFID II / MiFIR

EMIR

Short Selling

CSD regulation

PRIPs

Investor Compensation

schemes

Dodd-Frank Act

Living

Wills

Banking Union

Basel III

CRD IV / CRR

Leverage Ratio

AIFMD UCITS V

Fundamental

Review of the

Trading Book

Banking

Recovery & Resolution

Directive

Long-term

Financing

Transparency

Directive

NSFR

Corporate

Governance

Data Protection Deposit

Guarantee

Schemes

Payments package

(PSD II) Volcker Rule

FATCA

Prospectus

Directive

Coherence of

legislation

“EU FATCA”

Solvency II

4th AML

Directive Bank Account

Mortgage

Directive

Remuneration

MAD

& OUR CUSTOMERS

ELTIF

MMFs

Benchmarks

Regulation

IMD 2

IORP II

Credit Rating

Agencies

Regulation

Insurance

Guarantee

Scheme

UCITS VI

The banking sector is currently affected by 48 new regulations

Technology-driven development of banking business

Transactions at branches, million

38

30

19

2009 2011 2013

Transactions in the mobile bank, million

0

6

17

2009 2011 2013

22 •

0

96

161

225

106

3

1

144

163

163

153

111

175

80

70

127

127

127

233

170

0

163

82

115

103

172

206

239

178

137

117

204

208

204

199

178

211

157

155

182

185

186

242

206

134

206

159

182

Primary Colours Extra Colours

23 76

116

154

Chart Colours 166

166

166

191

191

191

127

127

127

204

102

0

0

96

161

119

154

188

We change everything we do...

Balance sheet

Products and services

Production

Customer contacts

• More capital

• More liquidity

• Longer funding

• Online 24/7

• More digital, less

physical

• Capital-light products

• Customer data for

tailored services

• Mobile bank

• More efficient

• More flexible

• Adapted to regulations

and stable

0

96

161

225

106

3

1

144

163

163

153

111

175

80

70

127

127

127

233

170

0

163

82

115

103

172

206

239

178

137

117

204

208

204

199

178

211

157

155

182

185

186

242

206

134

206

159

182

Primary Colours Extra Colours

24 76

116

154

Chart Colours 166

166

166

191

191

191

127

127

127

204

102

0

0

96

161

119

154

188

...to shape the future relationship bank

Future relationship bank

A sustainable business model in the framework of the

new regulations

ROE clearly above cost of capital

Fully loaded balance sheet

2015 plan

Relationship strategy Values & leadership

Convincing

message to the capital

market

Strong brand with clear

customer

commitments

Customer

centricity

GREAT CUSTOMER

EXPERIENCES

Agility Scale

Simplification Key enabler for Nordea enhancing our strengths

More value to customers Easier to deal with, more competent, more relevant, more innovative ...

25 •

Simplification also enhances our strengths and supports great

customer experiences

Sanford C. Bernstein Pan-European Strategic Decisions Conference

18 September 2014

Christian Clausen, President and Group CEO

Building for the future