Building Financial Projections April 8, 2003 Charlie Tillett SM ‘91 508 358-7861...

51

-

Upload

lee-howard -

Category

Documents

-

view

217 -

download

0

Transcript of Building Financial Projections April 8, 2003 Charlie Tillett SM ‘91 508 358-7861...

Agenda

• Part 1• The Business Model

• Part 2• Building Your Financial Projections

Background

1991 MIT Sloan School of Management

Spring 1990 Third Place $10K Contest

Summer 1990 Intern - Boston Capital Ventures

‘91 to ‘00 CFO of NetScout Systems (NTCT)- VC financings of $6MM and

$45MM- IPO in August 1999

’00 to present Consulting CFO- Dot Com – Magazine

Subscriptions- Enterprise Software- Bomb Detection for checked

baggage

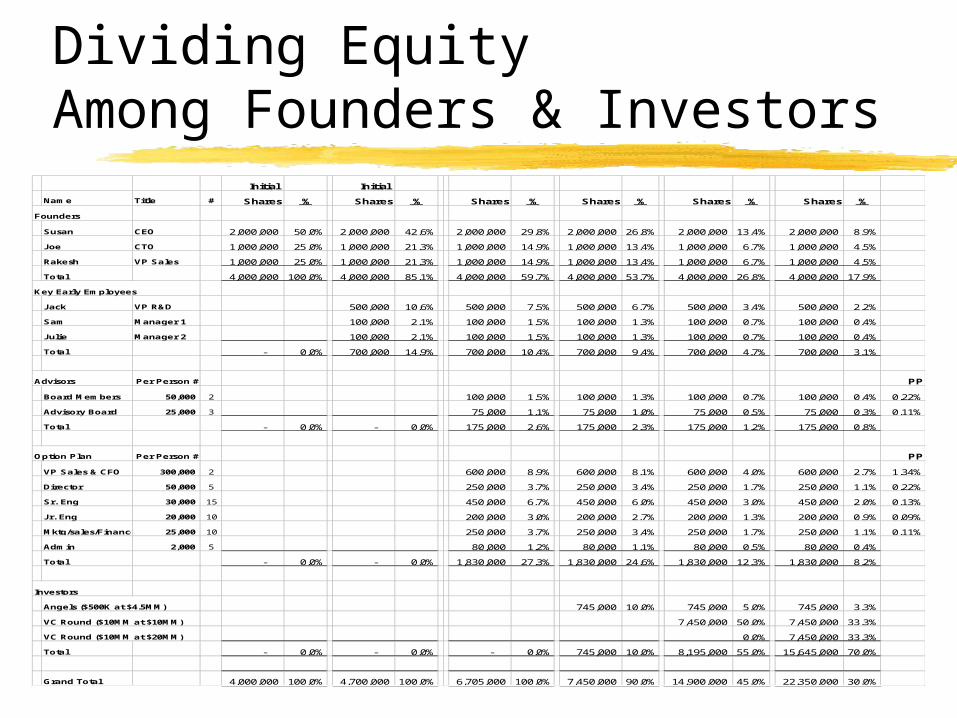

Dividing EquityAmong Founders & Investors

Initial Initial

Name Title # Shares % Shares % Shares % Shares % Shares % Shares %

Founders

Susan CEO 2,000,000 50.0% 2,000,000 42.6% 2,000,000 29.8% 2,000,000 26.8% 2,000,000 13.4% 2,000,000 8.9%

Joe CTO 1,000,000 25.0% 1,000,000 21.3% 1,000,000 14.9% 1,000,000 13.4% 1,000,000 6.7% 1,000,000 4.5%

Rakesh VP Sales 1,000,000 25.0% 1,000,000 21.3% 1,000,000 14.9% 1,000,000 13.4% 1,000,000 6.7% 1,000,000 4.5%

Total 4,000,000 100.0% 4,000,000 85.1% 4,000,000 59.7% 4,000,000 53.7% 4,000,000 26.8% 4,000,000 17.9%

Key Early Employees

Jack VP R&D 500,000 10.6% 500,000 7.5% 500,000 6.7% 500,000 3.4% 500,000 2.2%

Sam Manager 1 100,000 2.1% 100,000 1.5% 100,000 1.3% 100,000 0.7% 100,000 0.4%

Julie Manager 2 100,000 2.1% 100,000 1.5% 100,000 1.3% 100,000 0.7% 100,000 0.4%

Total - 0.0% 700,000 14.9% 700,000 10.4% 700,000 9.4% 700,000 4.7% 700,000 3.1%

Advisors Per Person # PP

Board Members 50,000 2 100,000 1.5% 100,000 1.3% 100,000 0.7% 100,000 0.4% 0.22%

Advisory Board 25,000 3 75,000 1.1% 75,000 1.0% 75,000 0.5% 75,000 0.3% 0.11%

Total - 0.0% - 0.0% 175,000 2.6% 175,000 2.3% 175,000 1.2% 175,000 0.8%

Option Plan Per Person # PP

VP Sales & CFO 300,000 2 600,000 8.9% 600,000 8.1% 600,000 4.0% 600,000 2.7% 1.34%

Director 50,000 5 250,000 3.7% 250,000 3.4% 250,000 1.7% 250,000 1.1% 0.22%

Sr. Eng 30,000 15 450,000 6.7% 450,000 6.0% 450,000 3.0% 450,000 2.0% 0.13%

Jr. Eng 20,000 10 200,000 3.0% 200,000 2.7% 200,000 1.3% 200,000 0.9% 0.09%

Mktg/sales/Finance 25,000 10 250,000 3.7% 250,000 3.4% 250,000 1.7% 250,000 1.1% 0.11%

Admin 2,000 5 80,000 1.2% 80,000 1.1% 80,000 0.5% 80,000 0.4%

Total - 0.0% - 0.0% 1,830,000 27.3% 1,830,000 24.6% 1,830,000 12.3% 1,830,000 8.2%

Investors

Angels ($500K at $4.5MM) 745,000 10.0% 745,000 5.0% 745,000 3.3%

VC Round ($10MM at $10MM) 7,450,000 50.0% 7,450,000 33.3%

VC Round ($10MM at $20MM) 0.0% 7,450,000 33.3%

Total - 0.0% - 0.0% - 0.0% 745,000 10.0% 8,195,000 55.0% 15,645,000 70.0%

Grand Total 4,000,000 100.0% 4,700,000 100.0% 6,705,000 100.0% 7,450,000 90.0% 14,900,000 45.0% 22,350,000 30.0%

Disclaimer - Charlie’s Rules-of-Thumb

• Focused on making attractive to investors

• Most relevant for technology-based companies

• May not apply to your industry or business model

• Most Common Business Plan Errors:• Revenue too high in year 4• Profit too high in year 4

What is a Business Model?

Boston Globe - January 9, 2003

• StorageNetworks replaced the CEO and eliminated 50% of its workforce as it struggles to find a new business model.

• Tried to build a national network of data-storage infrastructure available for lease but was hurt by customer reluctance to let outsiders handle their most sensitive data.

• Their new business model is focused on storage management software.

The Business Model

• A Profit & Loss Statement that details your financial performance in percentage terms

• Assumes you reach critical mass

• Explains WHY your business will MAKE MONEY

• The complete business plan shows HOW!

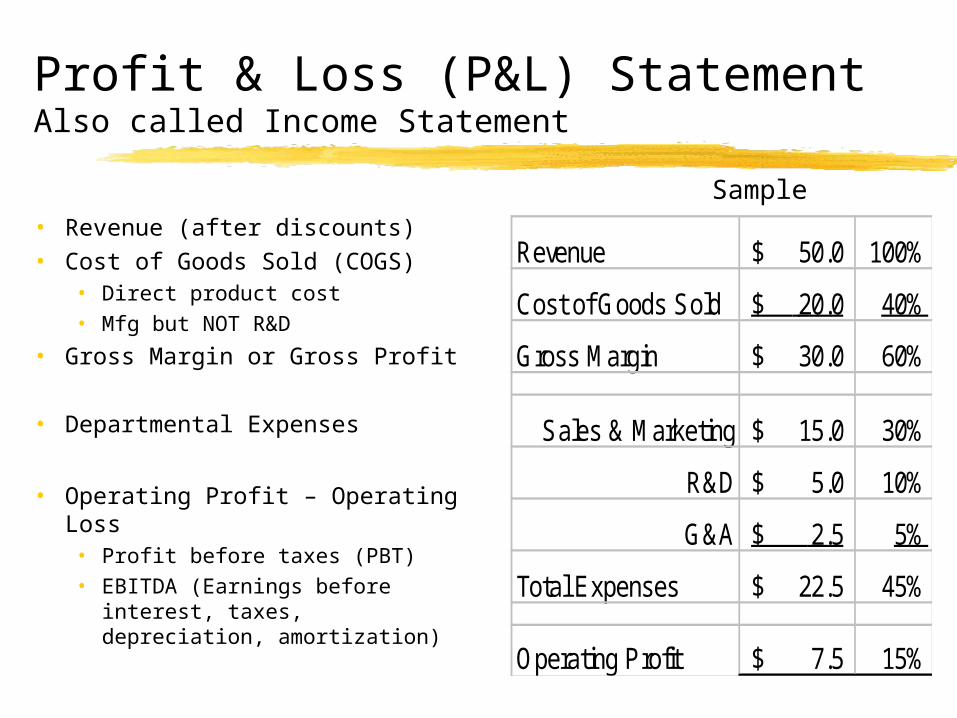

Profit & Loss (P&L) StatementAlso called Income Statement

• Revenue (after discounts)• Cost of Goods Sold (COGS)

• Direct product cost• Mfg but NOT R&D

• Gross Margin or Gross Profit

• Departmental Expenses

• Operating Profit – Operating Loss• Profit before taxes (PBT)• EBITDA (Earnings before

interest, taxes, depreciation, amortization)

Revenue 50.0$ 100%

Cost of Goods Sold 20.0$ 40%

Gross Margin 30.0$ 60%

Sales & Marketing 15.0$ 30%

R&D 5.0$ 10%

G&A 2.5$ 5%

Total Expenses 22.5$ 45%

Operating Profit 7.5$ 15%

Sample

Business Model Example“Typical” Data Communications Company

Sales 100%

Cost of Goods Sold (20% to 50%) 40%

Gross Margin 60%

Sales & Marketing (20% to 35%) 30%

R&D (10% to 15%) 10%

G&A (4% to 6%) 5%

Total Expenses 45%

Operating Profit (15%-25%) 15%

Actual Business ModelsQ3 ’98 and Q3 ’00

Cisco Cisco Sun Sun IBM IBM

Q3 '98 Q3 '00 Q3 '98 Q3 '00 Q3 '98 Q3 '00

Revenue 100% 100% 100% 100% 100% 100%

Cost of Goods Sold 35% 36% 50% 52% 60% 64%

Gross Margin 65% 64% 50% 48% 40% 36%

Sales & Marketing 19% 21% 22% 20% 17% 14%

R&D 12% 14% 10% 10% 7% 6%

G&A 3% 3% 6% 4% 4% 3%

Total Expenses 34% 38% 38% 34% 28% 23%

Operating Profit 31% 26% 12% 14% 12% 13%

Annual Revenue/Emp. 600,000$ 675,000$ 520,000$ 315,000$

Actual Business Models Q3 ’98 and Q3 ’00

Tech Data Tech Data Yahoo Yahoo Amazon Amazon

Q3 '98 Q3 '00 Q3 '98 Q3 '00 Q3 '98 Q3 '00

Revenue 100% 100% 100% 100% 100% 100%

Cost of Goods Sold 93% 95% 11% 13% 78% 74%

Gross Margin 7% 5% 89% 87% 22% 26%

Sales & Marketing 4% 3% 53% 36% 23% 22%

R&D 0% 0% 15% 9% 8% 11%

G&A 1% 1% 7% 6% 3% 4%

Total Expenses 5% 4% 75% 51% 34% 37%

Operating Profit 2% 1% 14% 36% -12% -11%

Annual Revenue/Emp. 2,000,000$ 250,000$ 400,000$ 400,000$ 300,000$

Case Study - CISCO Forecast – December 2002

FY '00 FY '01 FY '02 FY '03 FY '00 FY '01 FY '02 FY '03Actual Actual Forecast Forecast Actual Actual Forecast Forecast

Revenue 18.9$ 22.3$ 19.0$ 21.3$ 100% 100% 100% 100%

Cost of Goods Sold 6.7$ 9.2$ 7.7$ 7.8$ 35% 41% 41% 37%

Gross Margin 12.2$ 13.1$ 11.3$ 13.5$ 65% 59% 59% 63%

Sales & Marketing 3.9$ 5.3$ 4.3$ 4.4$ 21% 24% 23% 21%

R&D 2.7$ 3.8$ 3.3$ 3.4$ 14% 17% 17% 16%

G&A 0.7$ 0.7$ 0.6$ 0.7$ 4% 3% 3% 3%

Total Expenses 7.3$ 9.8$ 8.2$ 8.5$ 39% 44% 43% 40%

Operating Profit 4.9$ 3.3$ 3.1$ 5.0$ 26% 15% 16% 23%

Building YOUR Model

• Start with what you “know”• Your Cost of Goods Sold• R&D should end up at 10% to 20%• G&A should end up at 5% to 15%

• Target an operating profit of 15% to 20%

• Only remaining variable is Sales & Marketing

Building YOUR Model

• Verify your assumptions by looking at competitors or comparable companies

• You must be able to justify that:• You can meet a sales target of $X • With a Sales/Marketing budget of Y% of $X

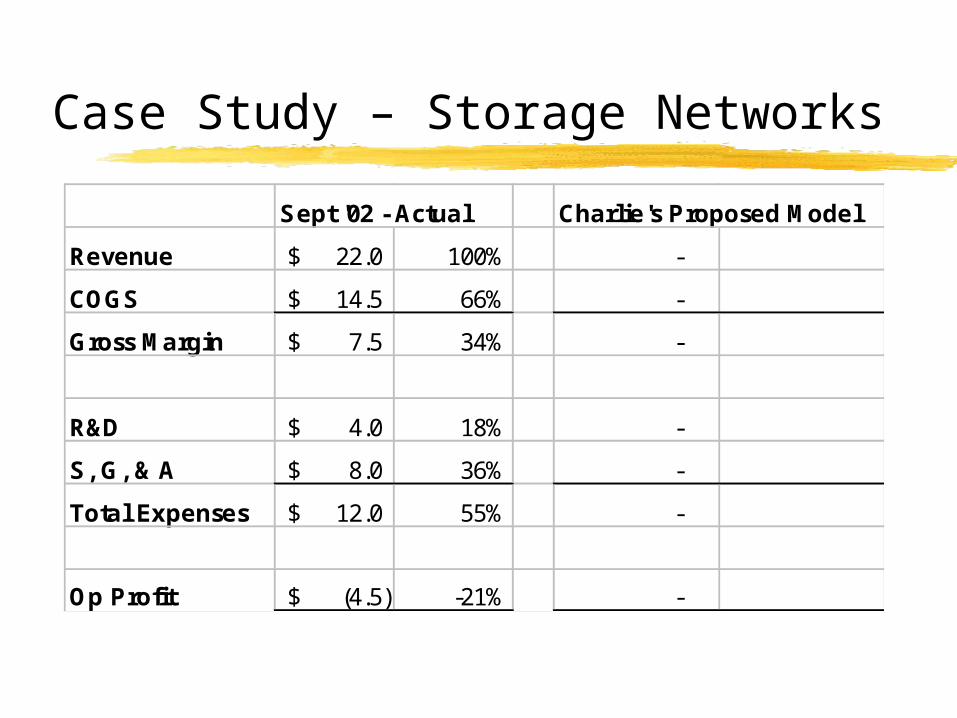

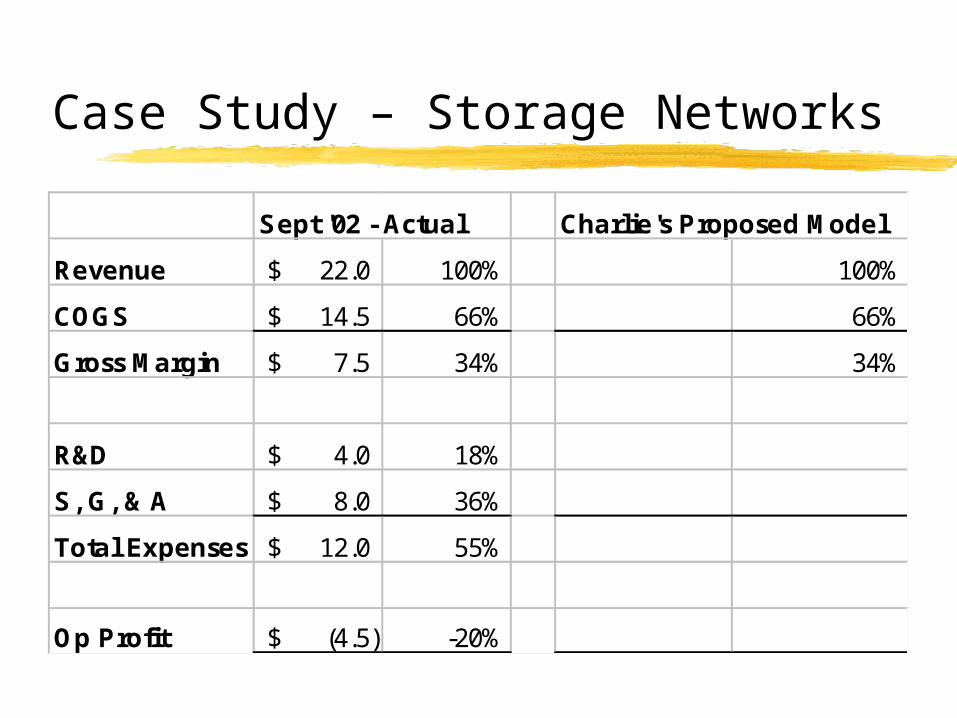

Case Study – Storage Networks

Sept '02 - Actual Charlie's Proposed Model

Revenue 22.0$ 100% -

COGS 14.5$ 66% -

Gross Margin 7.5$ 34% -

R&D 4.0$ 18% -

S, G, & A 8.0$ 36% -

Total Expenses 12.0$ 55% -

Op Profit (4.5)$ -21% -

Case Study – Storage Networks

Sept '02 - Actual Charlie's Proposed Model

Revenue 22.0$ 100% 100%

COGS 14.5$ 66% 66%

Gross Margin 7.5$ 34% 34%

R&D 4.0$ 18%

S, G, & A 8.0$ 36%

Total Expenses 12.0$ 55%

Op Profit (4.5)$ -20%

Case Study – Storage Networks

Sept '02 - Actual Charlie's Proposed Model

Revenue 22.0$ 100% 100%

COGS 14.5$ 66% 66%

Gross Margin 7.5$ 34% 34%

R&D 4.0$ 18% 4.0$

S, G, & A 8.0$ 36%

Total Expenses 12.0$ 55%

Op Profit (4.5)$ -20%

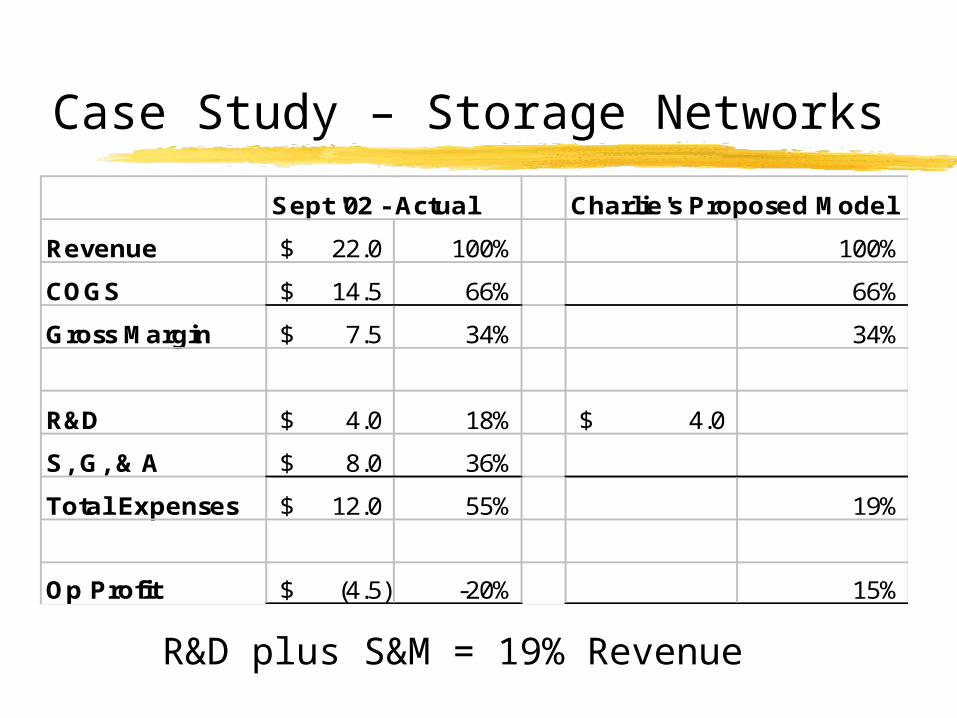

Case Study – Storage Networks

Sept '02 - Actual Charlie's Proposed Model

Revenue 22.0$ 100% 100%

COGS 14.5$ 66% 66%

Gross Margin 7.5$ 34% 34%

R&D 4.0$ 18% 4.0$

S, G, & A 8.0$ 36%

Total Expenses 12.0$ 55% 19%

Op Profit (4.5)$ -20% 15%

R&D plus S&M = 19% Revenue

Case Study – Storage Networks

R&D plus S&M = 19% Revenue

If we assume R&D = $4MM

then

Revenue = ($4 + S&M) / .19

S&M Revenue

6$ 53$

8$ 63$

10$ 74$

12$ 84$

14$ 95$

16$ 105$

Case Study – Storage Networks

Sept '02 Charlie's Proposed Model

Revenue 22.0$ 100% 63.0$ 100%

COGS 14.5$ 66% 41.6$ 66%

Gross Margin 7.5$ 34% 21.4$ 34%

R&D 4.0$ 18% 4.0$ 6%

S, G, & A 8.0$ 36% 8.0$ 13%

Total Exp. 12.0$ 55% 12.0$ 19%

Op Profit (4.5)$ -20% 9.4$ 15%

Case Study – Storage Networks

Sept '02 Charlie's Proposed Model

Revenue 22.0$ 100% 105.0$ 100%

COGS 14.5$ 66% 69.3$ 66%

Gross Margin 7.5$ 34% 35.7$ 34%

R&D 4.0$ 18% 4.0$ 4%

S, G, & A 8.0$ 36% 16.0$ 15%

Total Exp. 12.0$ 55% 20.0$ 19%

Op Profit (4.5)$ -20% 15.7$ 15%

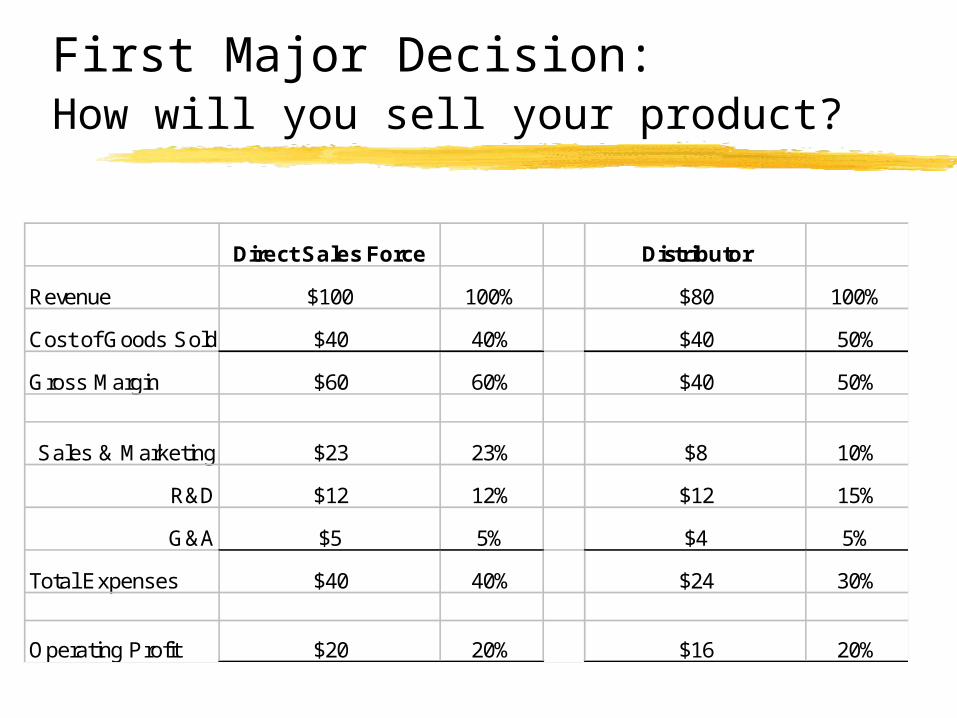

First Major Decision:How will you sell your product?

Direct Sales Force Distributor

Revenue $100 100% $80 100%

Cost of Goods Sold $40 40% $40 50%

Gross Margin $60 60% $40 50%

Sales & Marketing $23 23% $8 10%

R&D $12 12% $12 15%

G&A $5 5% $4 5%

Total Expenses $40 40% $24 30%

Operating Profit $20 20% $16 20%

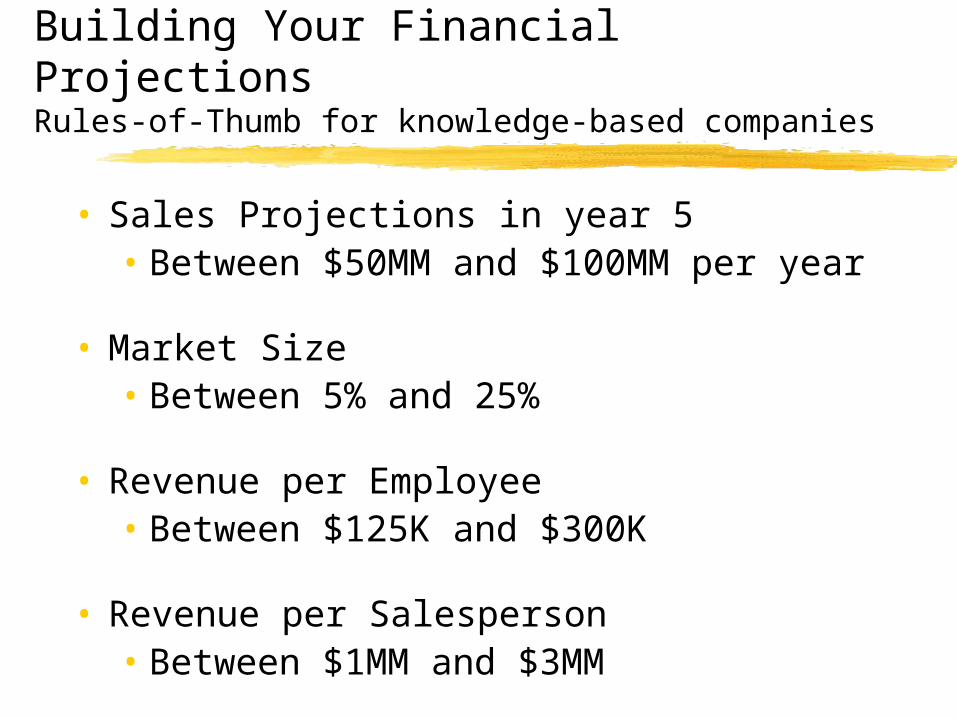

Building Your Financial ProjectionsRules-of-Thumb for knowledge-based companies

• Average employee salary will be $70K to $80K

• Employee benefits will add 15%

• Initially, salaries will be 60% to 75% of non-COGS expense• Remainder will be rent, utilities, supplies, phones, travel

• UNLESS you have extraordinary marketing!!!• Will reduce to 50% to 55% over time

• If you know your staffing plan, you can make a good

estimate of each department’s expenses

Building Your Financial ProjectionsRules-of-Thumb for knowledge-based companies

• Sales Projections in year 5• Between $50MM and $100MM per year

• Market Size• Between 5% and 25%

• Revenue per Employee• Between $125K and $300K

• Revenue per Salesperson• Between $1MM and $3MM

Cash Flow Projections Happiness is a positive cash flow

• Burn Rate• Your monthly operating loss plus capital expenditures

• Cash Flow Projection• Cumulative operating losses excluding depreciation• Plus cumulative capital expenses

• To determine the total cash required • Generally you look at your cumulative operating losses

plus cumulative capital expenses as of the month that you reach breakeven

VC Observations

• VCs don’t expect you to spend you own money BUT they expect you to spend money as though it were your own

• VCs don’t want their entrepreneurs to starve BUT they want them to be hungry

Financial DataPresentation Suggestions

• Steady, consistent revenue growth• No hockey sticks

• Steady, consistent evolution of your model

• Show % next to quarterly & yearly columns

• Show pre-tax only

• Don’t allocate G&A expenses

• Show depreciation expenses on a separate line

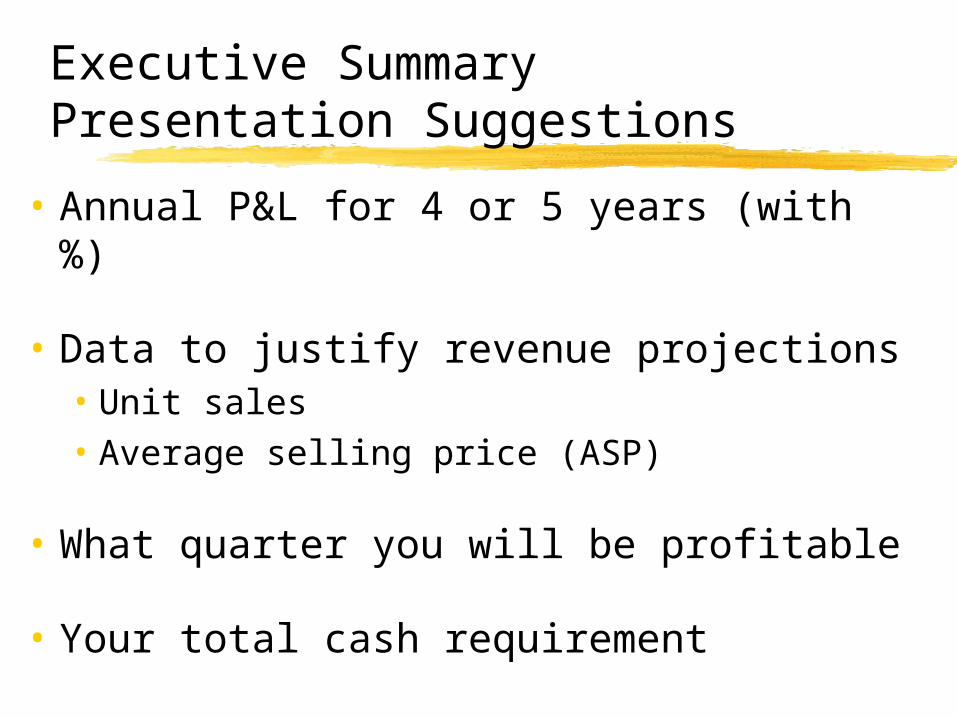

Executive SummaryPresentation Suggestions

• Annual P&L for 4 or 5 years (with %)

• Data to justify revenue projections• Unit sales• Average selling price (ASP)

• What quarter you will be profitable

• Your total cash requirement

Full Business PlanPresentation Suggestions

• Page 1: Annual P&L for 4 years

• Page 2 & 3: Quarterly P&L for all 4 years

• Page 4: Quarterly Staffing plan for 4 years

• Page 5: Quarterly cash flow for 4 years

End Result - Profit and Loss Statement

P & L by Year

Source Year 1 Year 2 Year 3 Year 4

Revenue

Model 1 P&L By Qtr 1,275,000$ 100% 10,500,000$ 88% 33,750,000$ 82% 37,500,000$ 50%

Model 2 P&L By Qtr -$ 0% 1,400,000$ 12% 5,250,000$ 13% 27,500,000$ 36%

Model 3 P&L By Qtr -$ 0% -$ 0% 2,400,000$ 6% 10,500,000$ 14%

Total Revenue 1,275,000$ 100% 11,900,000$ 100% 41,400,000$ 100% 75,500,000$ 100%

COGS P&L By Qtr 425,000$ 33% 3,920,000$ 33% 13,385,000$ 32% 23,200,000$ 31%

Gross Margin 850,000$ 67% 7,980,000$ 67% 28,015,000$ 68% 52,300,000$ 69%

Expenses

Engineering P&L By Qtr 1,326,625$ 104% 3,475,275$ 29% 7,212,188$ 17% 12,205,975$ 16%

Marketing P&L By Qtr 710,750$ 56% 1,810,750$ 15% 3,239,350$ 8% 5,300,000$ 7%

Sales P&L By Qtr 1,214,250$ 95% 3,466,500$ 29% 7,171,500$ 17% 12,393,500$ 16%

G&A P&L By Qtr 964,575$ 76% 1,817,750$ 15% 3,117,000$ 8% 5,308,500$ 7%

Operating Exp. 4,216,200$ 331% 10,570,275$ 89% 20,740,038$ 50% 35,207,975$ 47%

Operating Profit (3,366,200)$ -264% (2,590,275)$ -22% 7,274,963$ 18% 17,092,025$ 23%

Depreciation P&L By Qtr 144,833$ 427,333$ 593,000$ 608,167$

EBIT (3,511,033)$ (3,017,608)$ 6,681,963$ 16,483,858$

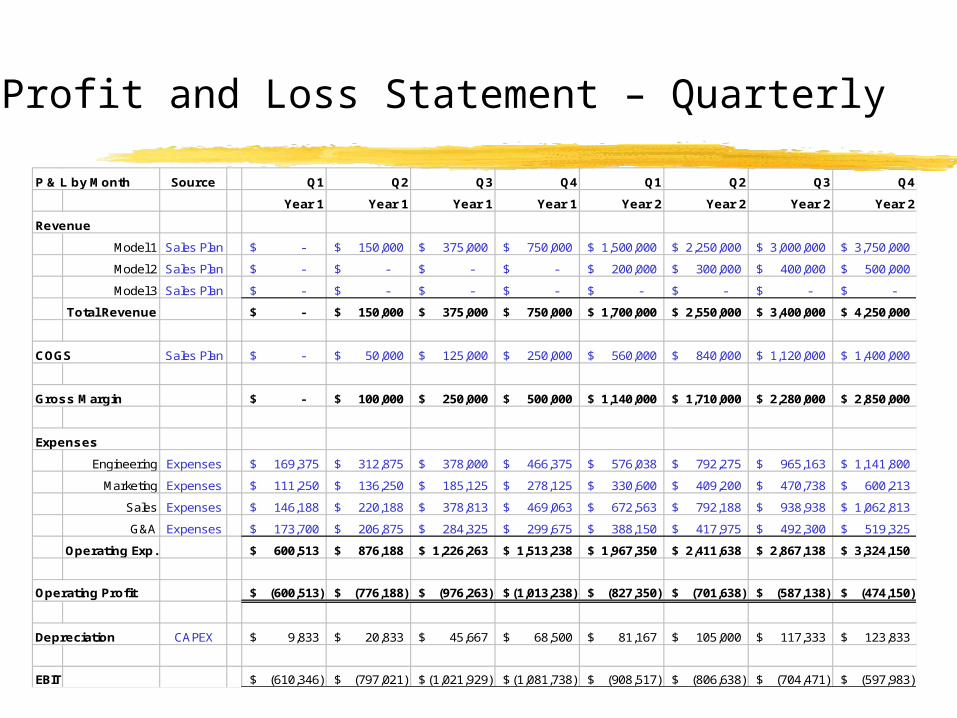

Profit and Loss Statement – Quarterly

P & L by Month Source Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

Year 1 Year 1 Year 1 Year 1 Year 2 Year 2 Year 2 Year 2

Revenue

Model 1 Sales Plan -$ 150,000$ 375,000$ 750,000$ 1,500,000$ 2,250,000$ 3,000,000$ 3,750,000$

Model 2 Sales Plan -$ -$ -$ -$ 200,000$ 300,000$ 400,000$ 500,000$

Model 3 Sales Plan -$ -$ -$ -$ -$ -$ -$ -$

Total Revenue -$ 150,000$ 375,000$ 750,000$ 1,700,000$ 2,550,000$ 3,400,000$ 4,250,000$

COGS Sales Plan -$ 50,000$ 125,000$ 250,000$ 560,000$ 840,000$ 1,120,000$ 1,400,000$

Gross Margin -$ 100,000$ 250,000$ 500,000$ 1,140,000$ 1,710,000$ 2,280,000$ 2,850,000$

Expenses

Engineering Expenses 169,375$ 312,875$ 378,000$ 466,375$ 576,038$ 792,275$ 965,163$ 1,141,800$

Marketing Expenses 111,250$ 136,250$ 185,125$ 278,125$ 330,600$ 409,200$ 470,738$ 600,213$

Sales Expenses 146,188$ 220,188$ 378,813$ 469,063$ 672,563$ 792,188$ 938,938$ 1,062,813$

G&A Expenses 173,700$ 206,875$ 284,325$ 299,675$ 388,150$ 417,975$ 492,300$ 519,325$

Operating Exp. 600,513$ 876,188$ 1,226,263$ 1,513,238$ 1,967,350$ 2,411,638$ 2,867,138$ 3,324,150$

Operating Profit (600,513)$ (776,188)$ (976,263)$ (1,013,238)$ (827,350)$ (701,638)$ (587,138)$ (474,150)$

Depreciation CAPEX 9,833$ 20,833$ 45,667$ 68,500$ 81,167$ 105,000$ 117,333$ 123,833$

EBIT (610,346)$ (797,021)$ (1,021,929)$ (1,081,738)$ (908,517)$ (806,638)$ (704,471)$ (597,983)$

Sales and COGS Forecast

Sales Plan Source Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

Year 1 Year 1 Year 1 Year 1 Year 2 Year 2 Year 2 Year 2

Unit Sales

Model 1 Input - 20 50 100 200 300 400 500

Model 2 Input - - - - 20 30 40 50

Model 3 Input - - - - - - - -

Total Units - 20 50 100 220 330 440 550

Revenue

Model 1 7,500$ -$ 150,000$ 375,000$ 750,000$ 1,500,000$ 2,250,000$ 3,000,000$ 3,750,000$

Model 2 10,000$ -$ -$ -$ -$ 200,000$ 300,000$ 400,000$ 500,000$

Model 3 15,000$ -$ -$ -$ -$ -$ -$ -$ -$

Total Revenue -$ 150,000$ 375,000$ 750,000$ 1,700,000$ 2,550,000$ 3,400,000$ 4,250,000$

Cost of Goods Sold

Model 1 2,500$ -$ 50,000$ 125,000$ 250,000$ 500,000$ 750,000$ 1,000,000$ 1,250,000$

Model 2 3,000$ -$ -$ -$ -$ 60,000$ 90,000$ 120,000$ 150,000$

Model 3 3,500$ -$ -$ -$ -$ -$ -$ -$ -$

Total COGS To P&L -$ 50,000$ 125,000$ 250,000$ 560,000$ 840,000$ 1,120,000$ 1,400,000$

Staffing Plan

Staffing Plan Staffing Staffing Staffing Staffing Staffing Staffing Staffing Staffing

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

Year 1 Year 1 Year 1 Year 1 Year 2 Year 2 Year 2 Year 2

Engineering

CTO Input 1 1 1 1 1 1 1 1

Programmer Input 4 8 10 12 15 20 25 30

Tech Writer Input - 1 1 2 2 4 4 4

Other Input - - - - - - - -

Total Eng 5 10 12 15 18 25 30 35

Marketing

VP Marketing Input 1 1 1 1 1 1 1 1

Product Manager Input 1 1 2 2 3 3 4 4

Mar-Com Input - - 1 1 2 2 2 2

Other Input 1 1 1 2 2 2 3 3

Total Mktg 3 3 5 6 8 8 10 10

Salary Expenses

Staffing Plan Annual Expense Expense Expense Expense Expense Expense Expense Expense

Salary Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

Year 1 Year 1 Year 1 Year 1 Year 2 Year 2 Year 2 Year 2

Benefits/COLA -> 115% 115% 115% 115% 117% 119% 121% 123%

Engineering

CTO Input 150,000$ 43,125$ 43,125$ 43,125$ 43,125$ 43,875$ 44,625$ 45,375$ 46,125$

Programmer Input 75,000$ 86,250$ 172,500$ 215,625$ 258,750$ 329,063$ 446,250$ 567,188$ 691,875$

Tech Writer Input 60,000$ -$ 17,250$ 17,250$ 34,500$ 35,100$ 71,400$ 72,600$ 73,800$

Other Input 80,000$ -$ -$ -$ -$ -$ -$ -$ -$

Total Eng To Dept Exp 129,375$ 232,875$ 276,000$ 336,375$ 408,038$ 562,275$ 685,163$ 811,800$

Marketing

VP Marketing Input 125,000$ 35,938$ 35,938$ 35,938$ 35,938$ 36,563$ 37,188$ 37,813$ 38,438$

Product Manager Input 95,000$ 27,313$ 27,313$ 54,625$ 54,625$ 83,363$ 84,788$ 114,950$ 116,850$

Mar-Com Input 75,000$ -$ -$ 21,563$ 21,563$ 43,875$ 44,625$ 45,375$ 46,125$

Other Input 80,000$ 23,000$ 23,000$ 23,000$ 46,000$ 46,800$ 47,600$ 72,600$ 73,800$

Total Mktg To Dept Exp 86,250$ 86,250$ 135,125$ 158,125$ 210,600$ 214,200$ 270,738$ 275,213$

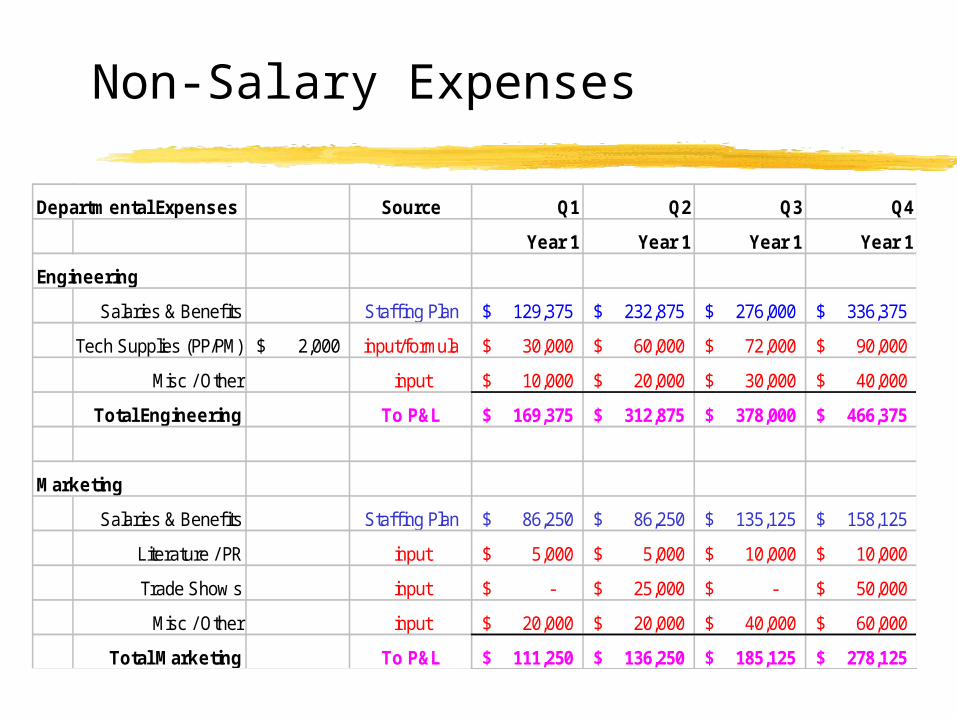

Non-Salary Expenses

Departmental Expenses Source Q1 Q2 Q3 Q4

Year 1 Year 1 Year 1 Year 1

Engineering

Salaries & Benefits Staff ing Plan 129,375$ 232,875$ 276,000$ 336,375$

Tech Supplies (PP/PM) 2,000$ input/formula 30,000$ 60,000$ 72,000$ 90,000$

Misc / Other input 10,000$ 20,000$ 30,000$ 40,000$

Total Engineering To P&L 169,375$ 312,875$ 378,000$ 466,375$

Marketing

Salaries & Benefits Staff ing Plan 86,250$ 86,250$ 135,125$ 158,125$

Literature / PR input 5,000$ 5,000$ 10,000$ 10,000$

Trade Show s input -$ 25,000$ -$ 50,000$

Misc / Other input 20,000$ 20,000$ 40,000$ 60,000$

Total Marketing To P&L 111,250$ 136,250$ 185,125$ 278,125$

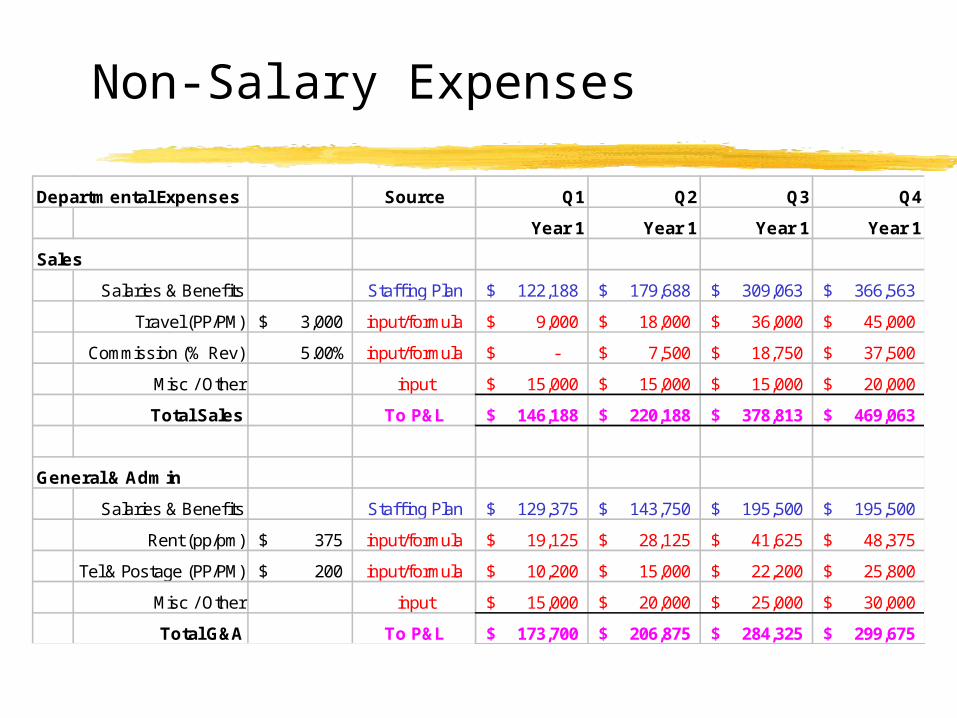

Non-Salary Expenses

Departmental Expenses Source Q1 Q2 Q3 Q4

Year 1 Year 1 Year 1 Year 1

Sales

Salaries & Benefits Staff ing Plan 122,188$ 179,688$ 309,063$ 366,563$

Travel (PP/PM) 3,000$ input/formula 9,000$ 18,000$ 36,000$ 45,000$

Commission (% Rev) 5.00% input/formula -$ 7,500$ 18,750$ 37,500$

Misc / Other input 15,000$ 15,000$ 15,000$ 20,000$

Total Sales To P&L 146,188$ 220,188$ 378,813$ 469,063$

General & Admin

Salaries & Benefits Staff ing Plan 129,375$ 143,750$ 195,500$ 195,500$

Rent (pp/pm) 375$ input/formula 19,125$ 28,125$ 41,625$ 48,375$

Tel & Postage (PP/PM) 200$ input/formula 10,200$ 15,000$ 22,200$ 25,800$

Misc / Other input 15,000$ 20,000$ 25,000$ 30,000$

Total G&A To P&L 173,700$ 206,875$ 284,325$ 299,675$

Profit and Loss Statement - Quarterly

P & L by Month Source Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

Year 1 Year 1 Year 1 Year 1 Year 2 Year 2 Year 2 Year 2

Revenue

Model 1 Sales Plan -$ 150,000$ 375,000$ 750,000$ 1,500,000$ 2,250,000$ 3,000,000$ 3,750,000$

Model 2 Sales Plan -$ -$ -$ -$ 200,000$ 300,000$ 400,000$ 500,000$

Model 3 Sales Plan -$ -$ -$ -$ -$ -$ -$ -$

Total Revenue -$ 150,000$ 375,000$ 750,000$ 1,700,000$ 2,550,000$ 3,400,000$ 4,250,000$

COGS Sales Plan -$ 50,000$ 125,000$ 250,000$ 560,000$ 840,000$ 1,120,000$ 1,400,000$

Gross Margin -$ 100,000$ 250,000$ 500,000$ 1,140,000$ 1,710,000$ 2,280,000$ 2,850,000$

Expenses

Engineering Expenses 169,375$ 312,875$ 378,000$ 466,375$ 576,038$ 792,275$ 965,163$ 1,141,800$

Marketing Expenses 111,250$ 136,250$ 185,125$ 278,125$ 330,600$ 409,200$ 470,738$ 600,213$

Sales Expenses 146,188$ 220,188$ 378,813$ 469,063$ 672,563$ 792,188$ 938,938$ 1,062,813$

G&A Expenses 173,700$ 206,875$ 284,325$ 299,675$ 388,150$ 417,975$ 492,300$ 519,325$

Operating Exp. 600,513$ 876,188$ 1,226,263$ 1,513,238$ 1,967,350$ 2,411,638$ 2,867,138$ 3,324,150$

Operating Profit (600,513)$ (776,188)$ (976,263)$ (1,013,238)$ (827,350)$ (701,638)$ (587,138)$ (474,150)$

Depreciation CAPEX 9,833$ 20,833$ 45,667$ 68,500$ 81,167$ 105,000$ 117,333$ 123,833$

EBIT (610,346)$ (797,021)$ (1,021,929)$ (1,081,738)$ (908,517)$ (806,638)$ (704,471)$ (597,983)$

CAPEX & Cash Flow Projection

Cash Flow Source Q1 Q2 Q3 Q4

Year 1 Year 1 Year 1 Year 1

Beginning Cash Input (Beginning only) -$ 4,281,488$ 3,273,300$ 1,849,038$

Gross Margin From P&L Quarterly -$ -$ 100,000$ 250,000$

Expenses From P&L Quarterly (600,513)$ (876,188)$ (1,226,263)$ (1,513,238)$

Investment Input 5,000,000$ -$ -$ -$

Capital Expense From P&L CAPEX (118,000)$ (132,000)$ (298,000)$ (274,000)$

Change in Cash 4,281,488$ (1,008,188)$ (1,424,263)$ (1,537,238)$

Ending Balance 4,281,488$ 3,273,300$ 1,849,038$ 311,800$

Capital Expenses Q1 Q2 Q3 Q4

Year 1 Year 1 Year 1 Year 1

Employee Workstations (PP) 4,000$ 68,000$ 32,000$ 48,000$ 24,000$

Prototype Expenses Input 50,000$ 100,000$ 250,000$ 250,000$

118,000$ 132,000$ 298,000$ 274,000$

Cumulative CAPEX 118,000$ 250,000$ 548,000$ 822,000$

Depreciation

Depreciation Charge 9,833$ 20,833$ 45,667$ 68,500$

Real World Expenses

• See $50K Web Site for more detail

PART 2 - Dividing the Pie

• Address two fundamental questions:How much of my company should the VCs get?How much of my company should employees

get?

• “The Formula”• Conceptual Framework for Stock Ownership• Some Real-World Examples & Advice

Valuation – “The Formula”VC % = VC$ / (pre-money + VC$)

VC Ownership % assumes only 1 round of financing

Example 1 Example 2 Example 3 Example 4

Pre-Money ($MM) 10$ 10$ 15$ 15$ plus Investment ($MM) 5$ 10$ 5$ 10$

equals Post-Money ($MM) 15$ 20$ 20$ 25$

Investment ($MM) 5$ 10$ 5$ 10$

divided by Post-Money ($MM) 15$ 20$ 20$ 25$

equals VC Ownership (see note below) 33% 50% 25% 40%

Founder's Shares in MM 1.00 1.00 1.00 1.00 Newly Issued VC Shares in MM 0.50 1.00 0.33 0.67

Total Shares in MM 1.50 2.00 1.33 1.67

YourCompany.COM

Let’s assume a pre-money value of $10MM

Stage 1 - Before any funding (pre-money)

Founder

VC

Employees

YourCompany.COM

Stage 2 – Assume $10MM raised at a $10MM pre-money valuation would yield a post-money valuation of $20MM)

The WRONG* way to look at it:

Founder

VC

Employees

* WRONG because the post-money pie is shown as the same size as the pre-money pie

YourCompany.COM

Stage 2 – Same example

The RIGHT way to look at it

Founder

VC

Employees

Founder

VC

Employees

Original Company ($10MM Pre-Money) $10MM Cash in Bank (Money)

YourCompany.COM

Pie represents both “original company” and new cash

Founder

VC

Employees

Stage 2 – Same exampleCombine the two and the “post-money” pie is twice as large

YourCompany.COM

Think of issuing stock to employees in the same way

Stage 2 – Another way to look at the same example.Your holdings are the same but the company is twice as large

VC

Founder

Employees

Raising money in stages

All at once Round 1 Round 2

Pre-Money 5 5 16plus Investment 5 3 4

equals Post-Money 10 8 20

Investment 5 3 4divided by Post-Money 10 8 20

equals Dilution 50% 38% 20%

Your Shares 100 50% 100 63% 100 50%VC Shares - Round 1 100 50% 60 38% 60 30%VC Shares - Round 2 40 20%

Total Shares 200 100% 160 100% 200 100%

Some Observations on VCs

• What do VCs want? Return on investment of:• Three to five times (300%-500%)• Within 4 to 6 years

• Therefore: • Your company’s post-money value must increase 3 to 5

times• Prefer management with a track record• Average investment is $5+ million• By the liquidity event, VCs want to make sure that founders

hold at least 10% to 20% of the equity• Round 1 financings are in the range of 25% to 50% • This allows for additional dilution in round 2 & 3• They will also build in an option pool of 10% to 20%

Employee Equity – Real World Examples

• Create the right number of shares – 10MM to 20MM• Equity by Position – very general guidelines

CEO – 5% to 10%Other VPs – 1% to 2.5%First Level Managers - .2% to .3%Scale down other levels of employees from hereSlight premium for technical hires

• Early stage companies may have to exceed these guidelines

• 4 year vesting, 25% after 1 year then 6.25% per quarter

VC Funding Recommendations

• Create more VC interest to increase the valuation• Research VC Firms. Approach one appropriate

for:• Your business stage• Your business size• Your industry

• There’s more than valuation: • Advice & council• How will they react when things go bad?

Random Advice

• Build a GREAT team• Technology, Marketing. Sales, Finance

• Get a good lawyer before you:• Negotiate with VCs• Grant stock or options

• A Big-5 accountant adds to your credibility• Write this down – Section 83(b) of IRS tax code• Build relationships with investment community (VCs

& investment bankers) BEFORE you need them