Budget Methods and Practices -...

43

Budget Methods and Practices Anwar Shah [email protected] Workshop on Public Sector Governance in India IIPA, New Delhi, Octobr 30, 2007

Transcript of Budget Methods and Practices -...

Budget Methods and Practices

Anwar [email protected]

Workshop on Public Sector Governance in IndiaIIPA, New Delhi, Octobr 30, 2007

Outline• Budgetary Institutions and Processes

– Role of MOF– Fiscal Rules– Line Ministries– Cabinet– Parliament– Presidential vs Parliamentary system of government

• Issues in budget formulation– Macro-fiscal framework– Comprehensiveness– Multiyear budgeting– Participatory budgeting : potentials and pitfalls– Performance Budgeting

Outline ………………….2

• Performance Budgeting– What?– Why?– How?– Conclusions

Fiscal Framework

• Government ‘s resource envelope, borrowing stance and spending priorities

• Short and medium term objectives• Projections • Need a macro model – better done by a

think tank rather than in-house

Functions of Budgeting Systems

• Setting Priorities• Planning• Financial control over inputs• Management of operations• Accountability

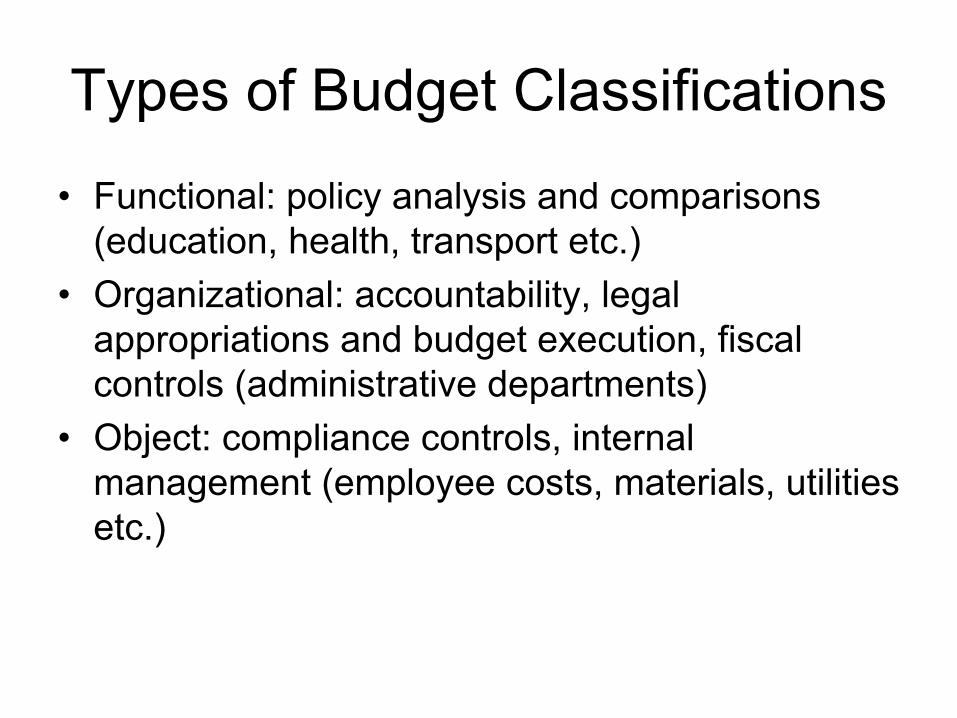

Types of Budget Classifications

• Functional: policy analysis and comparisons (education, health, transport etc.)

• Organizational: accountability, legal appropriations and budget execution, fiscal controls (administrative departments)

• Object: compliance controls, internal management (employee costs, materials, utilities etc.)

Budget Comprehensiveness

• What is to be included?• What works against comprehensiveness?

– Tax expenditures– SOEs– Extra-budgetary and off-budget expenditures – Earmarked funds– External assistance– Contingent and non-contingent liabilities– Quasi-fiscal activities by central bank

Implications of a segmented budget

• Fiscal discipline• Allocative Efficiency• Technical/operational Efficiency• Integrity and Trust

Medium Term Expenditure Framework (MTEF)

• Multi-year budgetary planning to link annual budgets with medium term priorities

• Three year rolling expenditure and revenue plans

• Baseline and forward estimates• Annual reconciliations• Considerations: appropriate cost drivers

and log framework for service delivery

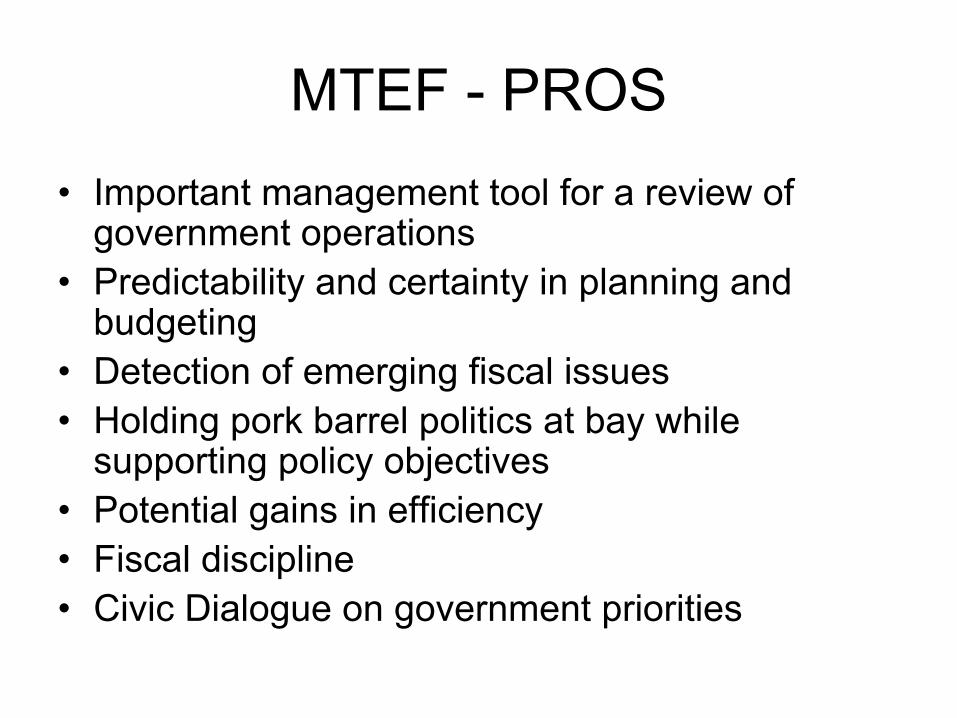

MTEF - PROS• Important management tool for a review of

government operations• Predictability and certainty in planning and

budgeting• Detection of emerging fiscal issues• Holding pork barrel politics at bay while

supporting policy objectives• Potential gains in efficiency• Fiscal discipline• Civic Dialogue on government priorities

MTEF - CONS• Costly paper exercise if dependence on

unpredictable external finance• Costly exercise with no real benefits if done

mechanically using incrementalism without a serious look at government operations

• Costly if no framework for fiscal discipline• Sense of entitlements• Resistance to change even in the presence of

major shocks• Ineffective if no oversight by parliaments and

citizens

Participatory budgeting• Merits

– Citizens’ review of government operations and priorities

– Bottom-up Government accountability – Easier for Local governments

• Demerits– Interest group capture– High transactions costs– Little impact when budgetary inflexibility– Little use when it is used for window-dressing

government programs and priorities

History of Budgeting• Early 1900s Line-item incremental budgeting for

financial control• Central agency for coordination of government

spending• Program budgeting in 1950s to link with

planning• Block vote budgeting in 1960s: aggregate

allocations• Zero based budgeting in 1970s to set priorities• Performance budgeting in 1990s to achieve

operational efficiency and to improve accountability for results

A comparative perspective on the two budgeting approachesFocus on Results

Increased Managerial Discretion and less control

Managers are accountable for what they achieve.

PB

Focus on Control

No Managerial Discretion

Managers are accountable for what and how they spend on inputs.

Line-Item

Zero-based Budgeting?ZBB refers to a budgeting system

where every item of expenditure has to be fully justified again every year.Reality: impossible to implement Developing country – wages and salaries sometimes can reach 70% of the budget which is outside of the control of budget officials

International Experience: discontinued practice-- Impractical technique -- Too costly to administer

Performance Budgeting: What?

A system of budgeting that presents the purpose and objectives for which funds are required, the costs of the programs proposed for achieving these objectives, and outputs to be produced or services to be rendered under each program.

Strict Definition: A system of budgeting that explicitly links each increment in allocated resources to an increment in outputs and outcomes.

Objectives

Programs

Measures and Report Performance

Management and Planning Decisions

Allocation Decisions

Program Budgeting

Performance Management

Performance Budgeting

Transformation: from Line-Item Budgeting to PB

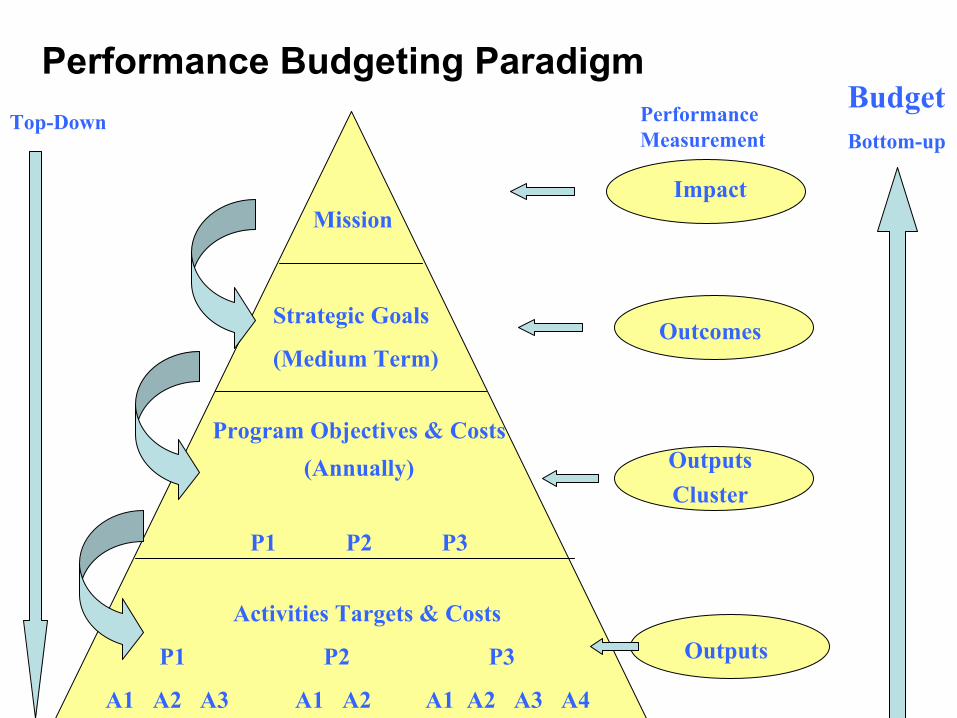

Performance Budgeting Paradigm

Mission

Strategic Goals

(Medium Term)

Program Objectives & Costs(Annually)

P1 P2 P3

Activities Targets & Costs

P1 P2 P3

A1 A2 A3 A1 A2 A1 A2 A3 A4

Performance Measurement

Impact

Outcomes

OutputsCluster

Outputs

BudgetBottom-up

Top-Down

Performance Budgeting Results Chain Application in Education

Enrollments, student-teacher ratio, class size

Educational spending by age, sex, urban/rural; spending by level; teachers, staff, facilities, tools, books

Improve quantity, quality, and access to education services

Program objectives Inputs Intermediate inputs

Winners and losers from government programs

Informed citizenry, civic engagement, enhanced international competitiveness

Literacy rates, supply of skilled professionals

Achievement scores, graduation rates, drop-out rates

Outputs Outcomes Impact Reach

Performance Measures Used in Performance Budgeting

• Cost: Inputs/resources used to produce outputs• Output: Quantity and quality of goods and services

produced. • Outcome: Progress in achieving program objectives• Impact: Program goals• Reach: People who benefit or are hurt by a program• Quality: Measure of service such as timeliness,

accessibility, courtesy, accuracy• Productivity: Output by work hour• Efficiency: Cost per unit of output• Satisfaction: Rating of services by users

Citizen-centered performance budgeting

• Budget format to follow closely service delivery format and also to include a performance report and net worth assessment

• Citizens charter and sunshine rights• Citizen inputs in budget process to be formalized

at all stages– Formulation: Town Hall meeting on the previous

year’s performance and new proposals. Comments on Porto Allegre and Belo Horizonte, Bolivia

– Review and execution: Formal process for complaints– Post: Compliance and feedback reports.

Performance Management Framework is a pre-requisite for the success of PB

• Letting managers manage: operational flexibility and freedom – few rules more discretion

• Making managers manage. Accountability for results. Contracts/work program agreements based upon pre-specified output and performance targets and budgetary allocations

new civil service framework• Activity based costing, accrual accounting,

capital charging• Subsidiarity principle• Competitive service delivery and benchmarking• Incentives for cost efficiency (including capital

use)

Performance Budgeting: Why?

Why pursue PBB?

• Enhance communication between budget actors

• Promote management in government agencies

• Improve public services delivery• Facilitate more informed budgetary

decision-making• Achieve higher transparency and

accountability

Performance Budgeting: How?

International Experiences

Theory to Reality

Diversification in Implementation

Alternate approaches• PB with Fuzzy New Public Management (Letting

Managers Manage, competition, voice and choice, informal agreements): USA, Netherlands, Australia, Uganda, Mongolia, South Africa (small steps towards PB).

• PB with New Public Management (Making Managers Manage, stronger competition, voice and choice, formal contracts or agreements ): New Zealand, Malaysia (?), Singapore (?)

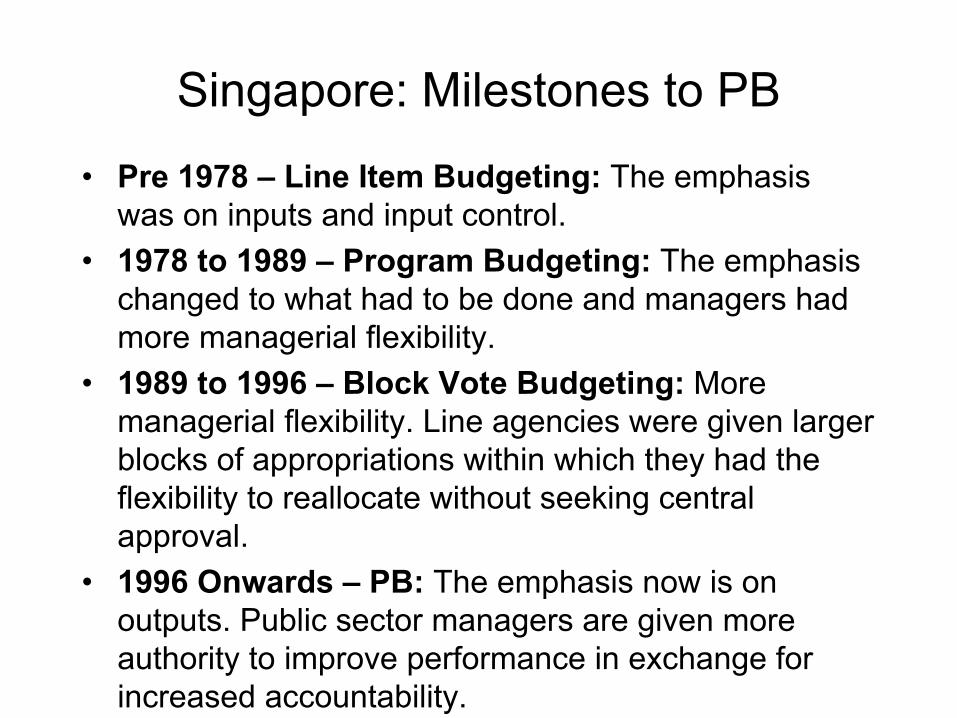

Singapore: Milestones to PB

• Pre 1978 – Line Item Budgeting: The emphasis was on inputs and input control.

• 1978 to 1989 – Program Budgeting: The emphasis changed to what had to be done and managers had more managerial flexibility.

• 1989 to 1996 – Block Vote Budgeting: More managerial flexibility. Line agencies were given larger blocks of appropriations within which they had the flexibility to reallocate without seeking central approval.

• 1996 Onwards – PB: The emphasis now is on outputs. Public sector managers are given more authority to improve performance in exchange for increased accountability.

Singapore: PB Framework• Government departments managed as

Autonomous Agencies• Macro Incremental Factor• Targets and output plans• Funding linked to output levels• Operational and financial autonomy• Capital charging including office use,

interdepartmental charging• 3-year development block vote• New Civil Service Framework

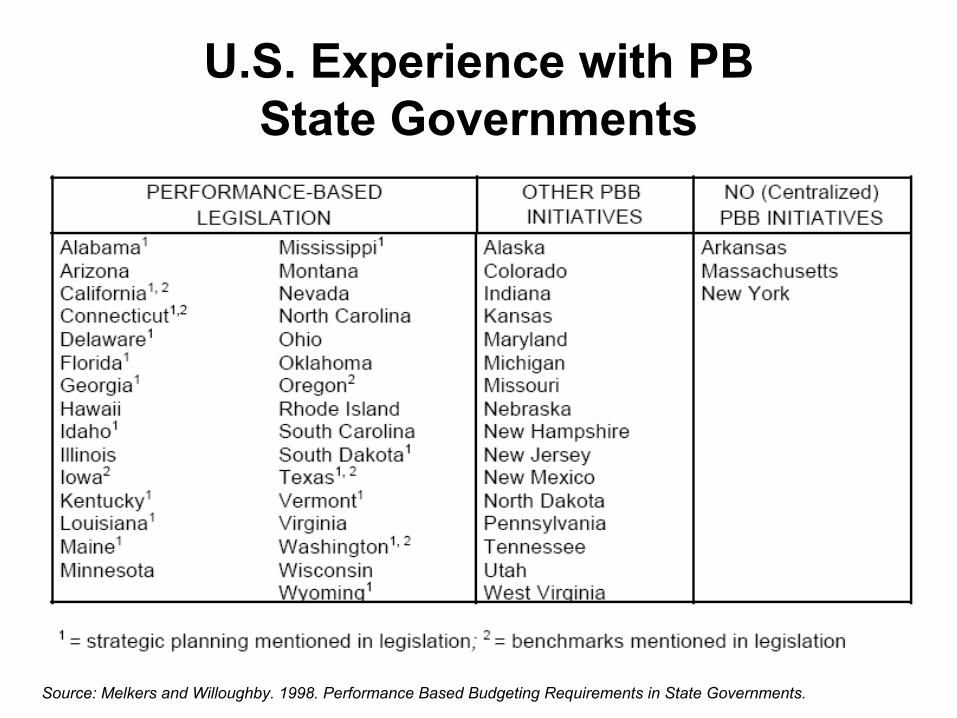

U.S. Experience with PB State Governments

Source: Melkers and Willoughby. 1998. Performance Based Budgeting Requirements in State Governments.

U.S. Experience with PB State Governments

• line-item budget 27 states• program budget 10 states• Half-way to PB 10 states• PB Michigan & Texas

Source: Hager, G. & Hobson, A. June 2001. Performance-Based Budgeting.

Texas State

Source: Hager, G. & Hobson, A. June 2001. Performance-Based Budgeting.

Montgomery Country, Maryland … 1

Public Works and Transportation Highway Services

Programs: Resurfacing Program Mission: To resurface the Country’s roads on a seven year cycle to assure an aesthetically pleasing, adequately maintained, functional roadway surface

Program Measures FY99 Actual

FY00 Actual

FY01 Actual

FY02 Budget

FY02 Actual

FY03 Approved

Outcomes: Lower maintenance cost and better safety

Outputs: Percentage of roads needing resurfacing that were resurfaced (assuming a 7-year cycle) Lane miles resurfaced

77

300

79

309

76

296

64

248

39

152

42

162Service Quality: Effective resurfacing cycle (years)

9.1

8.8

9.2

11.0

18.0 16.9

Efficiency: Average cost per lane-mile resurfaced ($)

4,483

5,706

5,115

5,109

5,099 5,230

Inputs: Expenditure ($000) Workyears

1,345

1,763

1,514

1,267

775 847

Source: Office of Management and Budget, Montgomery Country. Montgomery Measures Up! For the Year 2002

Montgomery Country, Maryland … 2

Montgomery Country, Maryland … 3

Fairfax County, Virginia … Police Patrol Services (1)

Fairfax County, Virginia … Police Patrol Services (2)

Fairfax County, Virginia … Fire and Rescue (1)

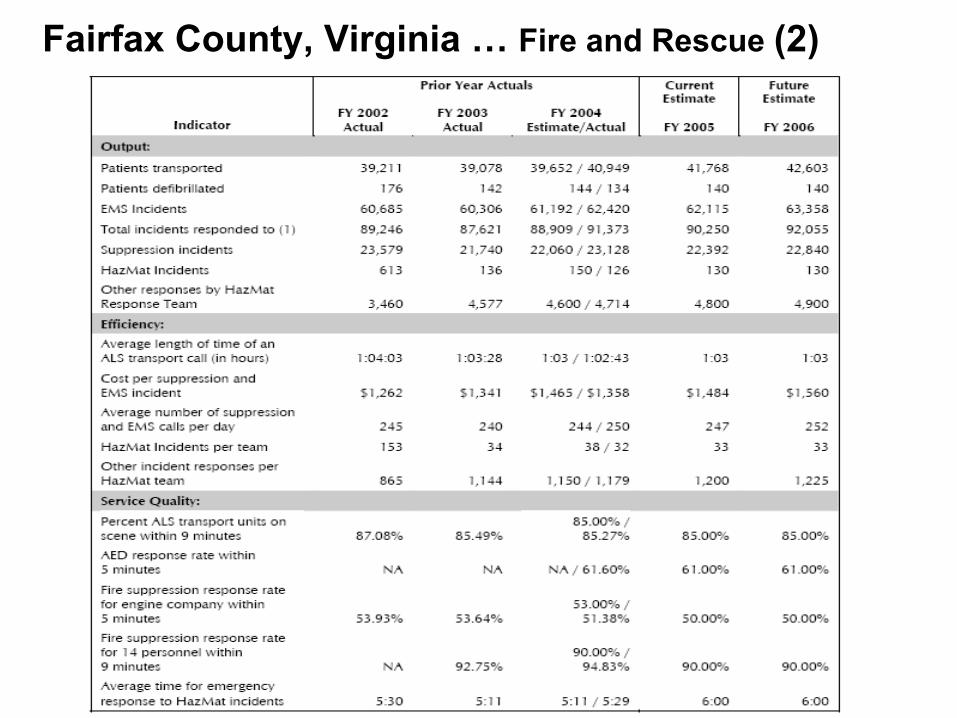

Fairfax County, Virginia … Fire and Rescue (2)

Fairfax County, Virginia … Fire and Rescue (3)

Conclusions• Performance budgeting must be an integral

element of a broader reform package to bring about performance culture. In the absence of an incentive environment for better performance and accountability for results, the introduction of performance budgeting will not lead to better performance.

• Managerial accountability must be on outputs and not on outcomes as the latter are influenced by external factors. Outcomes however should be monitored.

• Transparency of the budget and citizens’evaluation of outputs helpful in improving budgetary outcomes.