Budget 2015 16 - exhilarating possibilities

38

Copyright © 2015 Aureus Law Partners. All rights reserved.

-

Upload

abhishek-dutta -

Category

Business

-

view

1.289 -

download

2

Transcript of Budget 2015 16 - exhilarating possibilities

Copyright © 2015 Aureus Law Partners. All rights reserved.

Copyright © 2015 Aureus Law Partners. All rights reserved.

Union Budget 2015-16Exhilarating Possibilities

Copyright © 2015 Aureus Law Partners. All rights reserved.

4

Introduction & Background

The Economic Survey presented by the FM indicated positive growth in diverse sectors of the Indian economy. TheEconomic Survey forecast a GDP growth of 8.1 to 8.5 percent of the Indian economy for the financial year 2015-16.

The survey indicated that the following factors could play a decisive role in shaping economic growth in India:

• Easing the cost of doing business in India, which includes improvement to tax administration

• Focus on prioritization of unskilled labour

• Overhaul of the subsidy regime by creation of a fiscal space for rationalization of subsidies

• Restructuring of all PPP contracts

• Adherence to the medium-term fiscal deficit target of 3 percent of GDP

• Expenditure control with growth recovery and introduction of GST will ensure that medium-term targets are met

• Shift from public consumption to public investment while continuing focus on private investments

The aforesaid predictions had been made at the back of heartening data outlined in the following slide

Copyright © 2015 Aureus Law Partners. All rights reserved.

5

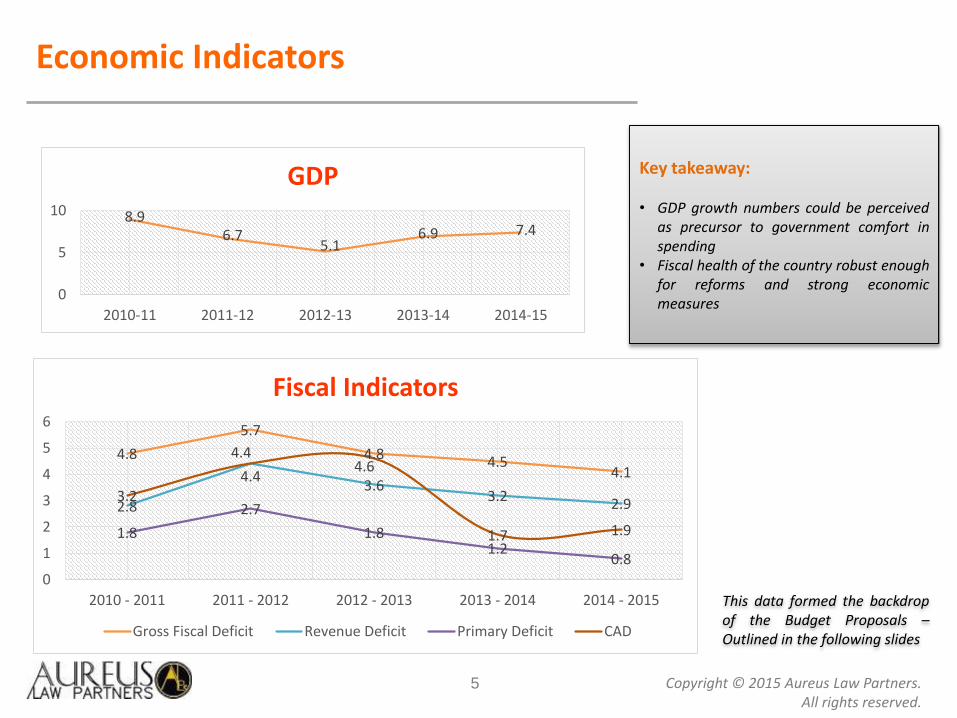

Economic Indicators

8.96.7

5.16.9 7.4

0

5

10

2010-11 2011-12 2012-13 2013-14 2014-15

GDP

4.8

5.7

4.8 4.54.1

2.8

4.43.6

3.2 2.9

1.8

2.7

1.81.2

0.8

3.2

4.44.6

1.7 1.9

0

1

2

3

4

5

6

2010 - 2011 2011 - 2012 2012 - 2013 2013 - 2014 2014 - 2015

Fiscal Indicators

Gross Fiscal Deficit Revenue Deficit Primary Deficit CAD

Key takeaway:

• GDP growth numbers could be perceivedas precursor to government comfort inspending

• Fiscal health of the country robust enoughfor reforms and strong economicmeasures

This data formed the backdropof the Budget Proposals –Outlined in the following slides

Copyright © 2015 Aureus Law Partners. All rights reserved.

6

Budget 2014-15: The Big Picture

High Spot observations for 2015-16

• Forecast of world trade growth down from 5.3 percent to 4 percent

• CAD expected to be below 1.3 percent of GDP

• Decline in manufacturing activities from 18 percent to 17 percent of GDP – ‘Make in India’ to provide boost

• Focus on ‘Ease of Doing Business’ in India and increased infrastructure spend

Economic Management

• Reduced fiscal space for the Centre after allocation of 42 percent of share of divisible pool of taxes to States

• Increased need of public investment and building infrastructure space

• Plugging leakages in existing subsidies to ensure direct transfer of benefits

• Enabling technology start up eco systems to develop the IT space with newer ideas

• Reinforcement of commitment to introduce GST by April 2016

Copyright © 2015 Aureus Law Partners. All rights reserved.

7

Budget 2014-15: The Big Picture (Cont’d…)

Tax Administration

• Creation of a globally competitive tax regime to focus on high investment, higher growth and job creation withreduction of exemptions and litigation

• Roadmap to curb the use of black money in the economy through appropriate legislations thereby leading tohigher tax collections

• Enforcement and legal construct of exchanging information between CBDT and CBEC through leverage oftechnology

Regulatory environment

• eBiz portals set up during the last year integrated 14 regulatory permissions at one source

• Appointment of an Expert Committee to prepare a draft legislation for replacing the multiple prior permissions set-up to a pre-existing regulatory mechanism

• Proposal to merge FMC with SEBI to better regulate commodity forward markets

• Introduction of Public Contract (Resolution of Disputes) Bill to streamline disputes in public contracts

Copyright © 2015 Aureus Law Partners. All rights reserved.

8

Policy Proposals

Infrastructure

• Establishment of National Investment and Infrastructure Fund and ensuring annual flow of INR 20,000 Crore to the same

• Introduction of tax free infrastructure bonds in rail, road and irrigation sectors

• Revisiting and revitalizing PPP models

• Converting existing ports in the public sector into companies to attract investments

• DMIC corridor to start work on basic infrastructure

Start up businesses

• Establishing SETU – a techno-financial facilitation programme aiming to aid start up businesses particularly the technology driven areas

Power Projects

• Setting up of five new 4000 MW Ultra Mega Power Projects

• Launch of prior clearances and linkages before award by way of an auction

Copyright © 2015 Aureus Law Partners. All rights reserved.

9

Enabling legislative environment mooted

RBI – Management of Public Debt

• Proposal to set up PDMA to manage domestic and external debt, currently managed by the RBI

• Consequent amendments proposed in the RBI Act whereby RBI may govern public debt, if notified by the Central Government

Increase in powers of SEBI

• FMC proposed to be merged with the SEBI. Accordingly, it is proposed to repeal the FCRA

• The recognized associations under the FCRA proposed to be recognized as stock exchanges

FEMA Regulations – Amendments in Capital Account Transactions

• Central Government may now specify any class or classes of capital account transactions, not involving debt instruments, which are permissible

• Deletion of Section 6 (3) of the FEMA which empowered RBI to prohibit, restrict or regulate transfer or issue of foreign securities, borrowing and lending in foreign exchange, import/export or holding of currency or currency notes etc.

Copyright © 2015 Aureus Law Partners. All rights reserved.

10

Enabling legislative environment mooted (Cont’d …)

FEMA Regulations (continued …)

• Central Government to be empowered with making regulations relating to Capital Account Transactions.Regulations made by RBI under Sections 6 and 47 to continue until amended or rescinded by the CentralGovernment

• FEMA allows an Indian resident to acquire, hold, own, possess or transfer any foreign exchange, foreign securityor any immoveable property situated outside India, only in accordance with its provisions. Authorized Officer isproposed to be empowered to seize value equivalent of such foreign exchange, foreign security or immovableproperty situated in India

Prevention of Money Laundering Act

• The definition of ‘proceeds of crime’ under PMLA to be amended to enable attachment and confiscation ofequivalent asset in India where the asset located abroad cannot be forfeited

• Value involved in offences under Part B of the Schedule increased from INR 30 lakhs to INR 1 Crore or more

Copyright © 2015 Aureus Law Partners. All rights reserved.

Tax Proposals & Changes

Copyright © 2015 Aureus Law Partners. All rights reserved.

12

Direct Tax Proposals

Personal taxation

• No change in rates of personal income tax

• Levy of Surcharge at the rate of 10 percent on individuals having income exceeding INR 1 Crore and 12 percent in certain specific cases

• Deduction under Section 80C of the IT Act for investment in Sukanya Samriddhi Scheme

• Deduction under Section 80D of the IT Act increased to INR 25,000 on health insurance premium

• Deduction under Section 80CCC of the IT Act on account of contribution to a pension fund of LIC or IRDA approved insurer increased from INR 1 lakh to INR 1.5 lakhs

• Deduction under Section 80CCD of the IT Act on account of contribution by the employee to NPS increased from INR 1 lakh to INR 1.50 lakhs

• Deduction on account of interest on loan in respect of self-occupied house property raised from INR 1.5 lakhs to INR 2 lakhs

• Central Government vested with powers to specify those cases where TAN would not be required. This provision may be effectuated for certain specific cases such as one time purchase of immovable property by individuals or HUFs

Copyright © 2015 Aureus Law Partners. All rights reserved.

13

Direct Tax Proposals (Cont’d…)

Corporate taxation

• Possible reduction of corporate tax rate from 30 percent to 25 percent over the next four years. However, no specific provision in this regard in the Finance Bill as of date

• Surcharge to be levied at the rate of 7 percent on domestic companies having income exceeding INR 1 crore to INR 10 crore

• Surcharge at the rate of 12 percent on domestic companies having income exceeding INR 10 crore

• Surcharge on foreign companies to continue at the rate of 2 percent if the income exceeds INR 1 crore and 5 percent if income exceeds INR 10 crore

• All the above to have a marginal relief clause

Taxation regime

• Applicability of GAAR deferred by two years. GAAR proposed to be applicable for income of the financial year 2017-18 and subsequent years. No application of GAAR on investments made upto March 31, 2017

• It is stated that DTC would not be implemented separately as most provisions already provided in the IT Act

Copyright © 2015 Aureus Law Partners. All rights reserved.

14

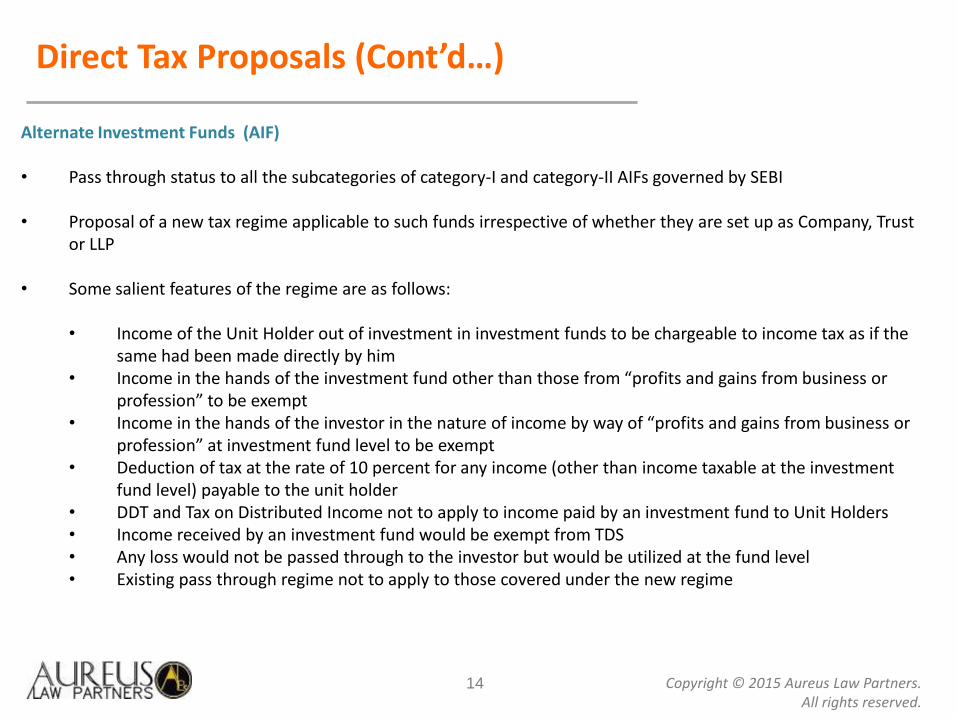

Direct Tax Proposals (Cont’d…)

Alternate Investment Funds (AIF)

• Pass through status to all the subcategories of category-I and category-II AIFs governed by SEBI

• Proposal of a new tax regime applicable to such funds irrespective of whether they are set up as Company, Trust or LLP

• Some salient features of the regime are as follows:

• Income of the Unit Holder out of investment in investment funds to be chargeable to income tax as if the same had been made directly by him

• Income in the hands of the investment fund other than those from “profits and gains from business or profession” to be exempt

• Income in the hands of the investor in the nature of income by way of “profits and gains from business or profession” at investment fund level to be exempt

• Deduction of tax at the rate of 10 percent for any income (other than income taxable at the investment fund level) payable to the unit holder

• DDT and Tax on Distributed Income not to apply to income paid by an investment fund to Unit Holders • Income received by an investment fund would be exempt from TDS• Any loss would not be passed through to the investor but would be utilized at the fund level • Existing pass through regime not to apply to those covered under the new regime

Copyright © 2015 Aureus Law Partners. All rights reserved.

15

Direct Tax Proposals (Cont’d…)

Off Shore Funds and ‘Business Connection’

• Recognition that in case of off-shore funds, the presence of a fund manager in India may create sufficient nexusto create a business connection in India, even if the fund manager is an independent person. Location of the fundmanager in India may tax the investment made by fund manager outside India due to such business connection

• In order to change the above anomaly Section 9A is proposed in the Finance Bill

• Fund management activity carried out by an eligible fund through an eligible fund manager not constitute abusiness connection in India, subject to detailed conditions including conditions regarding holding structure andbusiness connection requirements

New taxation regime prescribed for Business Trusts

• Finance Act 2014 provided for a pass through status to REIT and InvIT. Further, there was a deferred capital gains tax liability in the hands of the sponsor of SPV, on transfer of shares to the Business Trust. Such capital gains apply at the time of disposal of units of Business Trust

• However, due to the levy of STT the preferential capital gains regime available to Unit Holders was not available to sponsors at the time of transfer of units. Also, the deferral of capital gains places the sponsor at a disadvantageous position vis-à-vis direct listing of shares of the SPV

Copyright © 2015 Aureus Law Partners. All rights reserved.

16

Direct Tax Proposals (Cont’d…)

New taxation regime for Business Trusts (continued …)

• Accordingly any income in the nature of long term capital gain arising from transfer of units of a business trust which were acquired in consideration for exchange of shares of a SPV on which STT has been paid would not be included in the total income of the sponsor

• Pass through benefit proposed to be granted to rental income directly received by REIT

• The amendments in relation to business trust to come into effect from April 1, 2016

Royalty and FTS in case of non-residents

• Rate of tax on Royalty and FTS reduced from 25 percent to 10 percent from April 1, 2016

Indirect Transfer Provisions explained

• Concept of derivation of “substantial value” from assets located in India had remained unexplained. The same has been explained to mean at least 50 percent of the FMV of all the assets owned by the company or entity should be represented by the assets located in India

• The indirect transfer provisions would not apply if the value of Indian assets does not exceed INR 10 crore

• Principle of proportionality to apply in computing the tax. However, determinants of proportionality to be prescribed separately via rules

Copyright © 2015 Aureus Law Partners. All rights reserved.

17

Direct Tax Proposals (Cont’d…)

Indirect Transfer Provisions explained (Cont’d …)

• Further rationalisation measures include:• Exemption to the transferor (who directly owns the asset in India) if he neither holds the right of

management or control nor holds voting power / share capital interest in excess of 5 percent of the total voting power / share capital

• In case of indirect holding, similar provisions prevail along with a rider that neither the transferor nor its associated entities should exercise such control

• Amalgamation and demergers to be treated as exceptions, subject to detailed terms and conditions

• Reporting obligation cast upon the Indian entity if any offshore transaction results in modification of ownership structure or control either directly or indirectly, failing which penalties would be leviable

Threshold limit for domestic transfer pricing

• Amendment is proposed to Section 92BA of the IT Act to increase the threshold limit for applicability of transfer pricing regulations to specified domestic transactions from INR 5 Crore to INR 20 Crore

Abolition of Wealth Tax

• Wealth tax levied under the Wealth Tax Act, 1957 is proposed to be abolished. Additional Surcharge on high net worth individuals to be levied

Copyright © 2015 Aureus Law Partners. All rights reserved.

18

Direct Tax Proposals (Cont’d…)

Rationalisation in respect of charitable institutions

• Provision regarding advancement of ‘any other object of general public utility’ not to qualify as charitable purpose if such object involves carrying on of any activity in the nature of trade, commerce or business for a cess, fee or any other consideration.

• Exception to this general rule being:• Such activity is undertaken in the course of actual carrying out of such advancement of any other object of

general public utility• The aggregate receipts from such activities do not exceed 20 percent of total receipts

Taxability of interest paid by branch office of foreign banks in India

• Any interest payable by the branch office of a foreign bank having a PE in India to any other entity including itself outside India to be deemed to accrue or arise in India

• Such offices to be considered as separate entities • Such interest payments to be chargeable to tax in India

Incentives for the State of Andhra Pradesh and Telangana

• Deduction of 15 percent of the cost of new assets acquired and installed by the taxpayer to be allowed in Andhra Pradesh and Telangana. Investment allowance of 35 percent also provided for such new assets

• Assets are required to be held for a minimum of 5 years

Copyright © 2015 Aureus Law Partners. All rights reserved.

19

Direct Tax Proposals (Cont’d…)

Miscellaneous

• Exemption granted to Core Settlement Guarantee fund of Clearing Corporations arising out of contributions received, investment made and penalties imposed by the Clearing Corporation

• Proposed to provide tax neutrality on transfer of units of a scheme of a Mutual Fund under the process of consolidation of schemes of Mutual Funds as per SEBI Regulations

• Provision of mechanism to pre-empt repetitive appeals by the revenue on the same question of law year after year

• Amendment in Section 115 JB of the IT Act to exclude income from transactions in securities held by a Foreign Institutional Investor from the chargeability of MAT

• Residency status of a company proposed to be determined through the test of ‘place of effective management’. If the place of effective management of a company is at any time of the year in India, it shall be considered a resident company

• Extension of period of applicability of reduced rate of tax at 5 percent in respect of interest income of foreign investors (FIIs and QFIs) from corporate bonds and government securities from May 31, 2015 to June 30, 2017

• Proposed amendment to section 80JJAA of the IT Act to provide tax benefit to a ‘person’ rather than a ‘company’ deriving profits from manufacture of goods in a factory and paying wages to new regular workmen

Copyright © 2015 Aureus Law Partners. All rights reserved.

20

Service Tax

Rate rejigs

• Service tax rate increased from 12.36 percent (inclusive of cesses) to 14 percent. Education cesses not to apply on the revised rate, which would come into force from a date to be notified

• “Swachh Bharat Cess” at the rate of 2 percent to apply on value of taxable service

Revision in the negative list

• Following services removed from negative list and made taxable:• Amusement parks• Entertainment event of concerts, non-recognized sporting events, pageants, music concerts and award

functions, if admission charges are more than INR 500(These services though removed from the negative list, are proposed to be included in the Mega Exemption Notification – hence, they would not attract service tax till)

• All services provided by Government or local authority to business entities to be taxable, unless specifically exempted

• Service by way of carrying out any processes for production or manufacture of alcoholic liquor for human consumption made taxable

• Changes in negative list effective from a date to be notified after enactment of the Finance bill, 2015

Copyright © 2015 Aureus Law Partners. All rights reserved.

21

Service Tax (Cont’d…)

Exemptions withdrawn/restricted (effective from April 1, 2015)

• Construction services provided to government to be exempt only for the construction of: • a historical monument, archaeological site or remains of national importance, archaeological excavation or

antiquity• a canal, dam or other irrigation work• a pipeline, conduit or plant for

• water supply • water treatment, or • sewerage treatment or disposal.

• Exemption to services provided by performing artist in folk or classical art form limited only to such cases where amount charged is upto INR 1 lakh per performance

• Exemption withdrawn on the following services provided by:• Mutual fund agent to a mutual fund or asset management company• Distributor to a mutual fund or asset management company • Selling or marketing agent of lottery tickets to a distributor of lottery• Departmentally run public phone, guaranteed public telephone operating only local calls and free telephone

at airport and hospital where no bills are issued

Copyright © 2015 Aureus Law Partners. All rights reserved.

22

Service Tax (Cont’d…)

New exemptions (with effect from April 1, 2015)

• Following services are exempted from service tax • Operation of Common Effluent Treatment Plant• Pre-conditioning, pre- cooling, ripening, waxing, retail packing, labeling of fruits and vegetables• Admission to a museum, zoo, national park, wild life sanctuary and a tiger reserve • Transport of goods for export by road from inland container depot, container freight station or factory to a

land customs station • Service provided by way of exhibition of movie by an exhibitor/theatre owner to the distributor or

association of persons consisting of exhibitor as one of its member• Life insurance services provided by way of Varishtha Pension Bima Yogna• All ambulance services provided to patients

Copyright © 2015 Aureus Law Partners. All rights reserved.

23

Service Tax (Cont’d…)

Reverse charge mechanism (with effect from April 1, 2015)

• Recipient of services to pay 100 percent of the service tax in the following case:• Manpower supply and security services when provided by individual, HUF, partnership firm to a body

corporate• Service provided by mutual fund agents, mutual fund distributors and lottery agents• Service provided by a person involving an aggregator in any manner

Abatement scheme (effective from April 1, 2015)

• A uniform abatement of 70 percent prescribed for transport of goods and passengers by rail provided that cenvatcredit on inputs, capital goods and input services has not been taken

• Abatement of 70 percent prescribed for services provided by goods transport agency in relation to transportation of goods and transportation of goods in a vessel

• Abatement of 60 percent and 40 percent prescribed for transport of passengers by air in economy class and other than economy class respectively

• Abatement scheme on chit services withdrawn

Copyright © 2015 Aureus Law Partners. All rights reserved.

24

Service Tax (Cont’d…)

Key revenue enhancement measures

• Definition of the term Government tightened. May lead to several exclusions including municipal corporations

• “Consideration” defined to include reimbursements and expenses, with allowed exclusions per rules framed

• Lottery and chits specifically brought under the definition of services. Service tax to apply on these activities upon enactment of Finance Act

Miscellaneous

• Where service tax has been self assessed in the return and the same has not been paid either in full or in part then such tax to be recovered along with interest as per modes of recovery prescribed under Section 87 without service of notice

• Revision proceedings prescribed under central excise laws allowed in matters involving rebate of service tax

• Aggregator model made taxable – “defined as a person who owns and manages a web based software application and by means of the application and a communication device, enables a potential customer to connect with persons providing service of a particular client under the brand name or trade name of the aggregator” (With effect from March 1, 2015)

Copyright © 2015 Aureus Law Partners. All rights reserved.

25

Service Tax (Cont’d…)

Key Changes in Service Tax Rules, 1994

• Provision for issuing digitally signed invoices are being added along with the option of presentation of records in electronic form

• Consequent to the upward revision in Service Tax rate, the composition rate on specified services, namely, life insurance service, air travel agent services, money changing services provided by banks or authorized dealers, and service provided by lottery distributor and selling agent, is proposed to be revised proportionately, with effect from April 1, 2015

Copyright © 2015 Aureus Law Partners. All rights reserved.

26

Customs

Rationalization measures

• It has been clarified that the exemption to automatic cash dispensers extended to parts of such machines as well

• The period of validity of bank guarantee to be furnished in case the mega power status of a project is provisional enhanced to 66 months

• It has been clarified that if a certificate has been obtained under the import rules for availing of concessional rate of BCD on bulk drugs then an additional certificate under the excise rules for claiming concessional rate of CVD would not be required

• CVD and SAD exemption available on specified goods imported for use by Security Printing and Minting Corporation of India Limited has been withdrawn

• Concessional customs duties available on specified goods used in the manufacture of electrically operated vehicles and hybrid motor vehicles has been extended upto March 31, 2016

• A resident firm (i.e. a partnership, proprietorship, LLP and one person company) has been specified as a class of person that can now apply for advance ruling

Copyright © 2015 Aureus Law Partners. All rights reserved.

27

Customs (Cont’d…)

Rate revision

• Additional duty on MS and HSD has been increased from INR 2 per litre to INR 6 per litre

• Certain key rate revisions notified are as under:

• Export duty on ilmenite (26140020) reduced from 5 percent to 2.5 percent • Consequential amendment pursuant to removal of Education and SHE Cess has been made by removal of

the said cesses in respect of all goods on which these cesses were being applied • BCD rates on several industrial inputs and chemicals such as styrene, ethylene di-chloride, vinyl chloride

monomate etc. reduced to 2 percent, while on certain others, the BCD rates reduced to 2.5 percent • SAD on naphtha, ethylene dichloride (EDC), vinyl chloride monomer (VCM) and styrene monomer (SM) for

manufacture of excisable goods reduced from 4 percent to 2 percent• BCD on sulphuric acid used in manufacture of fertilizers reduced to 5 percent• BCD on metallurgical coke increased to 5 percent from 2.5 percent

• Several rate regimes for electronic hardware have been notified, with key amongst them being:

• All goods except populated printed circuit boards used in the manufacture of ITA Bound Items exempted from SAD

• All items used in the manufacture of tablet computers and their sub-parts fully exempted from BCD, CVD and SAD

• Basic Customs Duty on ‘metal parts’ for use in the manufacture of electrical insulators reduced from 10 percent to 7.5 percent

Copyright © 2015 Aureus Law Partners. All rights reserved.

28

Customs (Cont’d…)

Rate revision

• Several rate regimes for electronic hardware have been notified, with key amongst them being:

• BCD on goods used in the manufacture of insulated wires and cables reduced from 10 percent to 7.5 percent

• BCD on magnetron of upto 1 KW for use in the manufacture of domestic microwave ovens reduced to Nil• BCD on zeolite, ceria zirconia compounds and cerium compounds for use in the manufacture of washcoats,

used in manufacture of catalytic converters reduced from 7.5 percent to 5 percent • BCD on specified components for use in the manufacture of specified CNC lathe machines and machining

centres reduced from 7.5 percent to 2.5 percent • BCD on certain items used in manufacture of Refrigerator compressors reduced from 7.5 percent to 5

percent • Black Light Unit Module used in manufacture of LCD/LED TV panels and (OLED) TV panels to attract Nil BCD • CVD and SAD fully exempted on specified raw materials [battery, titanium, palladium wire, eutectic wire,

silicone resins and rubbers, solder paste, reed switch, diodes, transistors, capacitors, controllers, coils (steel), tubing (silicone)] for use in the manufacture of pacemakers

• SAD on inputs for use in the manufacture of LED drivers and MCPCB for LED lights, fixtures and lamps to be exempt

• BCD on Digital Still Image Video Camera capable of recording video with minimum resolution of 800x600 pixels, at minimum 23 frames per second, for at least 30 minutes in a single sequence, using the maximum storage (including the expanded) capacity and parts and components for use in the manufacture of such cameras is being reduced to Nil

Copyright © 2015 Aureus Law Partners. All rights reserved.

29

Customs (Cont’d…)

Rate revision

• Automotive sector

• BCD on Commercial Vehicles increased to 20 percent. However, BCD on such vehicles in CKD condition and electrically operated vehicles of heading 8702 including those in CKD condition will continue to be at 10 percent

• Concessional customs duties of Nil BCD, 6 percent CVD and Nil SAD on specified goods for use in the manufacture of Electrically operated vehicles and Hybrid motor vehicles to continue

• Renewables

• Evacuated Tubes with three layers of solar selective coating for use in the manufacture of solar water heater and system to attract Nil BCD

• BCD on Active Energy Controller for use in the manufacture of Renewable Power System Inverters reduced to 5 percent, subject to certification by MNRE

Copyright © 2015 Aureus Law Partners. All rights reserved.

30

Excise

Education cesses abolished coupled with increase in rate

• Education Cess and SHE Cess leviable abolished• Median rate of 12 percent enhanced to 12.5 percent

Specific rate revisions

• Duty of excise on waters, including mineral waters and aerated waters falling under Chapter sub-heading 2202 10has been increased from 12 percent to 18 percent.

• Duty of excise on cigarettes has been increased by 25 percent for cigarettes of length not exceeding 65 mm and by15 percent for cigarettes of other lengths. Further, increase in duty rates is also proposed on cigars, cheroots andcigarillos.

• Excise duty on cut tobacco has been increased from INR 60 per kg to INR 70 per kg• Tariff rate of excise duty on specific types of cements falling under Chapter sub-heading 2523 29 has been increased

from INR 900 per tonne to INR 1000 per tonne

• Petroleum product remain unaffected

• Tariff rate of excise duty on HSD increased from 14 percent plus INR 5 per litre to 14 percent plus INR 15 perlitre

• Additional duty of Excise on MS and HSD has been increased from INR 2 per litre to INR 6 per litre.• Even though the Finance Bill, 2015 has revised the AED and CENVAT rate, the effective rate of petrol and

diesel (both branded and unbranded) remains unchanged

Copyright © 2015 Aureus Law Partners. All rights reserved.

31

Excise (Cont’d…)

Sector wise rate revisions

• Automotive sector• Excise duty on chassis for ambulances reduced from 24 percent to 12.5 percent

• Electronics sector• Excise duty on wafers for manufacture of IC modules for smart cards reduced to 6 percent• Excise duty on inputs for use in the manufacture of LED drivers and MCPCB for LED lights, fixtures and

lamps, reduced to 6 percent• Pacemakers exempted• LED lights or fixtures including LED lamps converted to MRP products• Mobile phones and tablet computers to be charged to 12.5 percent duty with credit, with an option to pay

1 percent duty without availing cenvat credit

• Renewable energy• Excise duty on pig iron SG grade and Ferro-silicon-magnesium for manufacture of Cast components of wind

operated electricity generators has been fully exempted• Nil excise duty structure without CENVAT credit or 12.5 percent with CENVAT credit has been prescribed for

solar water heater and system• Excise duty on round copper wire and tin alloys used in manufacture of solar PV cells has been fully exempted

• Consumer goods• Excise duty on leather footwear of Retail Sale Price more than INR 1000 per pair reduced to 6 percent

Copyright © 2015 Aureus Law Partners. All rights reserved.

32

Excise (Cont’d…)

• Miscellaneous• The period of validity of bank guarantee to be furnished in case the ultra mega power and mega power

status of a project is provisional enhanced to 42 months and 66 months respectively• The standard rate of clean energy cess increased to INR 300 per tonne. Effective rate of Clean Energy Cess

increased from INR 100 per tonne to INR 200 per tonne• Specific retrospective amendment made to rationalise duty paid on railways and tramway track

construction material

Amendment to the Rules:

• Application for registration or de-registration or amendment of the registration application to be filed online onthe website www.aces.gov.in

• In case of sale of business transferee to get himself registered afresh• Cancelation of registration certificate only after providing opportunity to the taxpayer

Copyright © 2015 Aureus Law Partners. All rights reserved.

33

Cenvat Credit

Rationalization of credit mechanism with respect of job worker

• Cenvat credit provisions relating to job workers rationalised with the following amendments: • Full credit on inputs and 50 percent credit on capital goods allowed to be taken immediately on

receipt of inputs at the premises of job worker• Inputs being sent to multiple job workers successively made eligible for cenvat credit availment

subject to the condition that the resultant products are received by the principal manufacturer / service provider within 180 days

• Similar provisions allowed in respect of capital goods also as long as the capital goods are received within 2 years of dispatch to job worker

• In case inputs or capital goods are not received within the stipulated time frame, the cenvat credit taken on receipt of inputs and capital goods to be reversed

Time for availment of cenvat credit

• Clarification has been made in respect of time for availment of cenvat credit in respect of partial reverse charge. Cenvat credit for services on which partial reverse charge arises to be available upon payment of service tax by the recipient. It is unclear if the service tax paid by the service provider would be allowed for immediate availment. Consequent amendments made in relation to reversal provisions (if payment not made within 3 months) as well. This provision to be effected from April 1, 2015

• Time limit for availment of credit extended by 6 months to 1 year

Copyright © 2015 Aureus Law Partners. All rights reserved.

34

Cenvat Credit (Cont’d…)

Miscellaneous

• “Export goods” have been defined specifically to mean those goods which are to be taken to a place outside India. However, the term “export goods” has not been specifically used in the CCR

• For the purposes of rule 6 of CCR, definition of “exempted goods” or “final goods” to include non excisable goods cleared for a consideration from the factory. Value of non-excisable goods to be the invoice value or as may be reasonably determined where not available consistent with principles of valuation under excise

• Further clarity brought about to include an importer (First stage/second stage dealer) allowed to issue cenvatable invoice as a person on whose invoice cenvat credit may be claimed by a Taxpayer

• Power of suspension of registration and imposing restriction on utilization of cenvat credit granted to Central Government in case of importers as well

Copyright © 2015 Aureus Law Partners. All rights reserved.

35

Rationalization of penalty provisions

Service tax, Excise and Customs

Service tax and ExcisePayment within 30 days of

Notice Order

In case of intent to evade Base penalty would be 100 percent of the tax amount

15 percent of service tax/duty

25 percent of service tax/duty

In case of no intent to evade Base penalty would be 10 percentof the tax amount

No penalty 25 percent of penalty

CustomPayment within 30 days of

Notice Order

In case of intent to evade Base penalty would be 10 percent of the tax amount

15 percent of duty 25 percent of the penalty

Transitional provision introduced such that till the time that the Finance Act is notified, the aforesaid options may be exercised by the taxpayer subject to the notice not having been issued or if issued, order not having been passed. In such cases, penalty not to exceed 50 percent the tax / duty

Also specified, that in case of any modification to the order in an appellant proceeding, the penalty shall also stand appropriately modified

Copyright © 2015 Aureus Law Partners. All rights reserved.

36

Looking ahead upon 2015-16

Union budget has envisaged the creation of an institutional and regulatory framework for the future. Emphasis hasbeen given to increasing investment in infrastructure sector, providing roadmap for transforming the indirect and directtax regime, rationalization of subsidies and prioritizing job creation in the Indian economy. New measures such asstartup entrepreneur’s funds, GST rollout, attempts to deal with black money and deferral of GAAR should support thecause of ‘Ease of Doing Business in India’. A roadmap to revamp the tax regime by lowering corporate tax rates andphasing out of exemptions over the next four years is a welcome step towards the revival of growth and investmentregime.

Union Budget 2015-16 has made mostly rationalization changes via its tax proposals. These don’t seem to be indicativeof a larger term vision except perhaps the changes in service tax and excise duty rates.

More important to us are the various amendments / changes made to the associated legislations such as the FEMA Actand FCRA which could perhaps provide the central government with unprecedented authority in terms of foreigninvestment. If structural changes can be suitably implemented, then the next steps of the government in delivering the‘double digit growth promise’ would be a reality.

In conclusion, we hope that you have enjoyed this presentation, and found it to be useful. Your comments would behelpful to us in making this endeavour better, and we hope to hear from you.

Thank you,

Aureus Law Partners

Copyright © 2015 Aureus Law Partners. All rights reserved.

37

Glossary

AAR Authority for Advance RulingADR American Depositary ReceiptAIF Alternate Investment FundsALP Arm's Length PriceAMT Alternate Minimum TaxAPA Advance Pricing AgreementBCD Basic Custom DutyCAD Current Account DeficitCBDT Central Board of Direct TaxesCBEC Central Board of Excise and CustomsCCR Cenvat Credit Rules, 2004CKD Complete Knock DownCRR Cash Reserve RatioCSR Corporate Social ResponsibilityCVD Countervailing DutyDDT Dividend Distribution Tax

DMIC Delhi-Mumbai Industrial CorridorDTA Domestic Tariff AreaDTC Direct Tax CodeEC Educational Cess

EOU Export Oriented UnitsEVA Ethylene Vinyl Acetate

FCRA Foreign Contribution Regulation Act, 2010

FDI Foreign Direct InvestmentFEMA Foreign Exchange Management Act, 1999

FII Foreign Institutional InvestorFIPB Foreign Investment Promotion BoardFM Finance Minister

FMC Forward Markets ContractsFMV Fair Market ValueFTS Fee for Technical ServicesFY Financial Year

GAAR General Anti-avoidance RulesGDP Gross Domestic ProductGDR Global Depositary ReceiptGFD Gross Fiscal DeficitGST Goods and Services TaxGTA Goods Transport AgencyHSD High Speed DieselHUF Hindu Undivided FamilyIFRS International Financial Reporting Standards

Ind AS Indian Accounting StandardsINR Indian National Rupees

InvIT Infrastructure Investment TrustsIRDA Insurance Regulatory and Development Authority

IT Information Technology

Copyright © 2015 Aureus Law Partners. All rights reserved.

38

Glossary

IT Act Income Tax ActLED Light Emitting DiodeLIC Life Insurance CorporationLLP Limited Liability PartnershipLNG Liquefied Natural GasMAT Minimum Alternate TaxMS Motor SpiritMW Mega WattsNHAI National Highway Authority of IndiaNPS National Pension SchemePD Primary Deficit

PDMA Public Debt Management AgencyPMLA Prevention of Money Laundering Act, 2002PNG Petroleum & Natural GasPPP Public Private PartnershipPSF Polyester staple fibrePSL Priority Sector LendingPSU Public Sector UndertakingPSY Polyester filament yarnPV PhotovoltaicQFI Qualified Finanncial InstitutionalRBI Reserve Bank of IndiaRD Revenue Deficit

REIT Real Estate Investment TrustRO Reverse OsmosisSAD Special Additional DutySEBI Securities and Exchange Board of IndiaSEZ Special Economic Zone

SHEC Secondary and Higher Education CessSLR Statutory Liquidity RatioSPV Special Purpose VehicleSTT Securities Transaction TaxTDS Tax Deduction at SourceTPO Transfer Pricing OfficerUN United NationsUS The United States of America

USD US DollarsVCM Vinyl Chloride Monomer