Brownstown Town Center Financial PPT 7.16.12 · POWERPOINT PRESENTATIONS ... The subject site was...

224

Brownstown Town Center Market and Financial Study Final Presentation Final Presentation Brownstown Downtown Development Authority | July 19, 2012

Transcript of Brownstown Town Center Financial PPT 7.16.12 · POWERPOINT PRESENTATIONS ... The subject site was...

Brownstown Town Center Market and Financial StudyFinal PresentationFinal Presentation Brownstown Downtown Development Authority | July 19, 2012

Page i E6-12962.00 July 17, 2012

TABLE OF CONTENTS

BACKGROUND AND OBJECTIVES ............................................................................................................................................ 1

SUBJECT SITE ANALYSIS .......................................................................................................................................................... 3

Subject Site Description ................................................................................................................................................ 3

Subject Site History and Development Status ........................................................................................................... 4

MARKET OVERVIEW ................................................................................................................................................................... 5

National Outlook ............................................................................................................................................................. 5

Regional Economic & Demographic Analysis ........................................................................................................... 7

For-Sale Local Competitive Market ............................................................................................................................. 8

For-Rent Local Competitive Market ............................................................................................................................ 9

Office .............................................................................. ........................................................................................ 9

Retail ............................................................................................................................................................. 10

CONCLUSIONS AND RECOMMENDATIONS ........................................................................................................................... 12

Option 1: Town Center Recommendations .............................................................................................................. 12

Option 2: Not Town Center Recommendations....................................................................................................... 14

CRITICAL ASSUMPTIONS ......................................................................................................................................................... 16

GENERAL LIMITING CONDITIONS ........................................................................................................................................... 18

BROWNSTOWN DDA

Page ii E6-12962.00 July 17, 2012

APPENDIX: SUPPORTING EXHIBITS

POWERPOINT PRESENTATIONS

MARKET STUDY

FINANCIAL STUDY

BROWNSTOWN DDA

Page 1 E6-12962.00 July 17, 2012

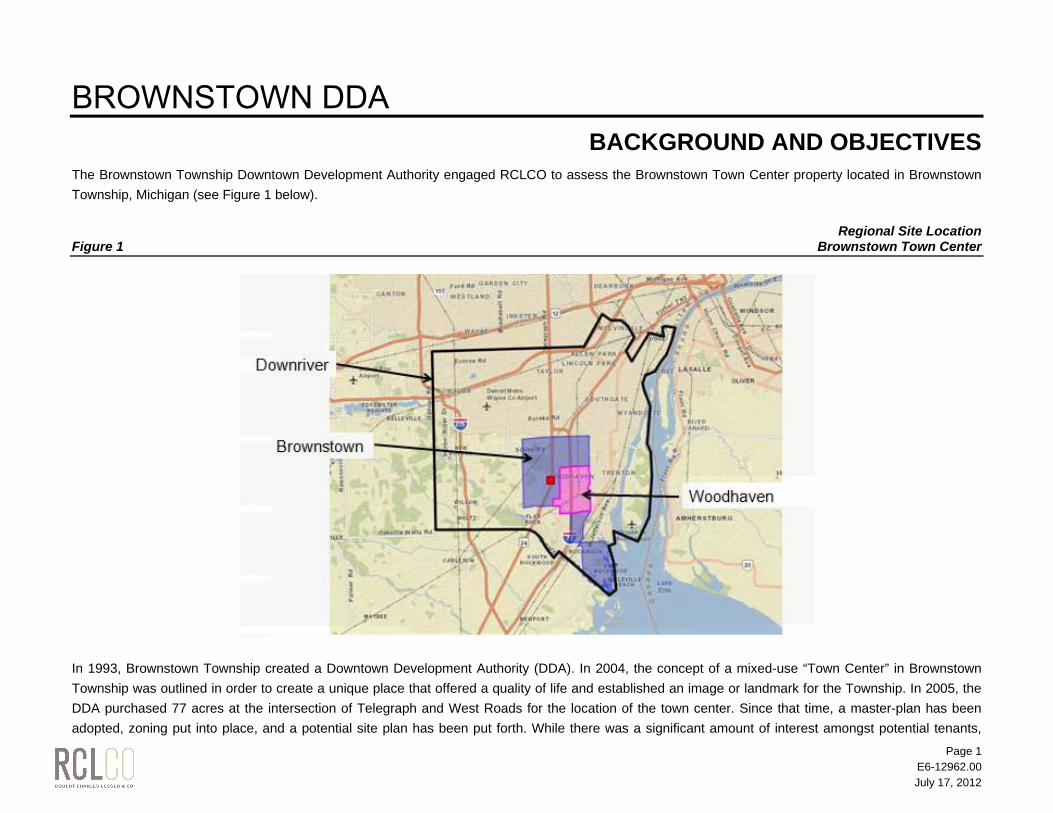

BACKGROUND AND OBJECTIVES The Brownstown Township Downtown Development Authority engaged RCLCO to assess the Brownstown Town Center property located in Brownstown Township, Michigan (see Figure 1 below). Regional Site Location Figure 1 Brownstown Town Center

In 1993, Brownstown Township created a Downtown Development Authority (DDA). In 2004, the concept of a mixed-use “Town Center” in Brownstown Township was outlined in order to create a unique place that offered a quality of life and established an image or landmark for the Township. In 2005, the DDA purchased 77 acres at the intersection of Telegraph and West Roads for the location of the town center. Since that time, a master-plan has been adopted, zoning put into place, and a potential site plan has been put forth. While there was a significant amount of interest amongst potential tenants,

BROWNSTOWN DDA

Page 2 E6-12962.00 July 17, 2012

until 2009, Telegraph Road was under construction making it a north/south road (as opposed to north bound only), hampering the ability to move forward on the project during the top of the last real estate cycle. RCLCO completed a market study and financial analysis to outline the market potential for the Town Center and the potential current value of the property. With the above in mind, the key objectives of this engagement were to:

Determine the timing of the different land uses within the town center;

Recommend the appropriate mix of land uses and total units/square feet;

Understand the future buyers, renters, tenant types, shoppers, and businesses that would likely locate and visit the town center; and

Prepare a financial analysis to clearly demonstrate the potential of the town center.

In order to assess the property, RCLCO completed the following tasks:

Visited the subject property and evaluated its condition and development potential

Compiled and analyzed economic and demographic information on the area to assess future growth drivers and the overall health and opportunities of the larger market

Estimated the demand for new apartments, single-family detached, retail, and office in the market and the site’s potential capture of that demand

Compiled data on the key competitive active and planned projects in the project’s competitive market area

Summarized the above and determined current and projected supply and demand trends, their influence on the timing of opportunities at the subject site, and the best candidate land-uses for the subject property among those evaluated for this engagement

Determined the likely absorption that could be achieved at the project through build-out

Analyzed all of the above and provided recommendations regarding timing of market entry, current and future end-user prices, and likely land values for the identified uses

Completed a financial analysis to determine the value of the land

BROWNSTOWN DDA

Page 3 E6-12962.00 July 17, 2012

SUBJECT SITE ANALYSIS Subject Site Description

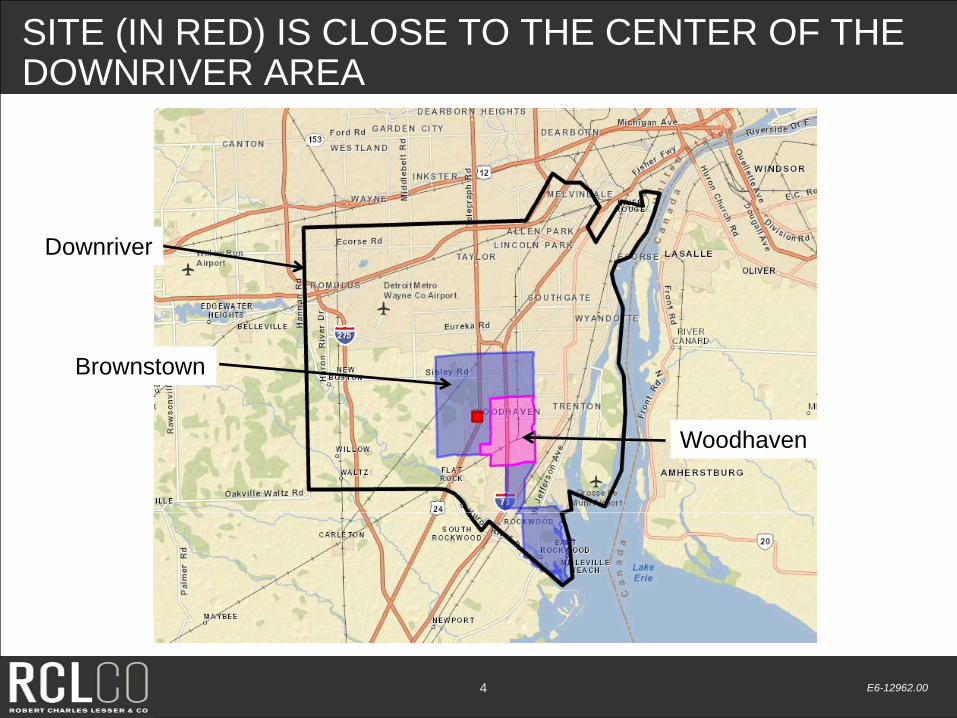

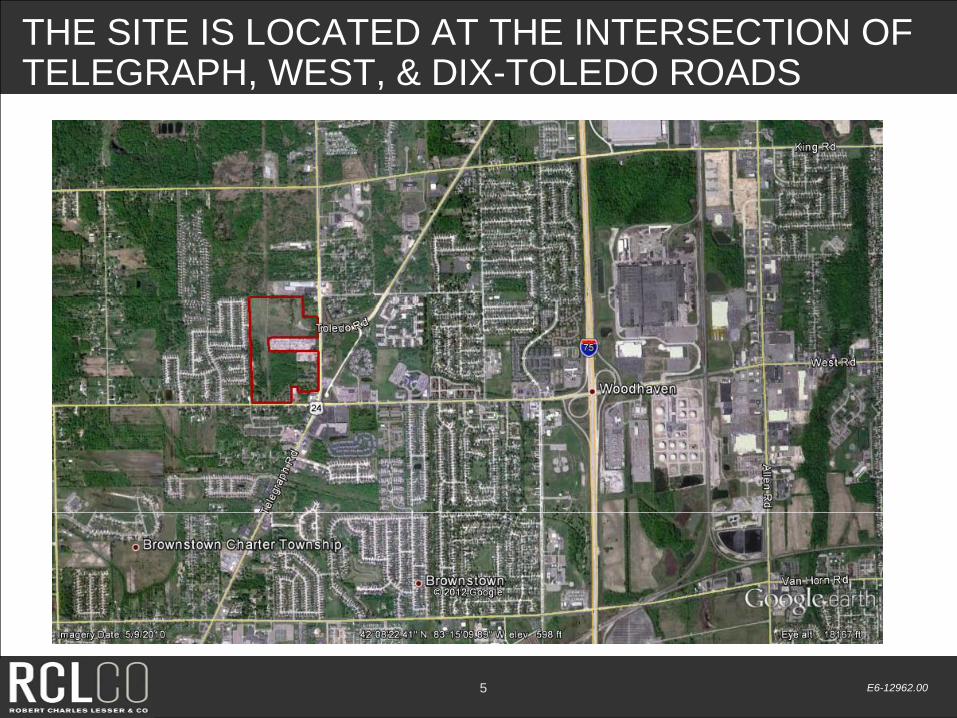

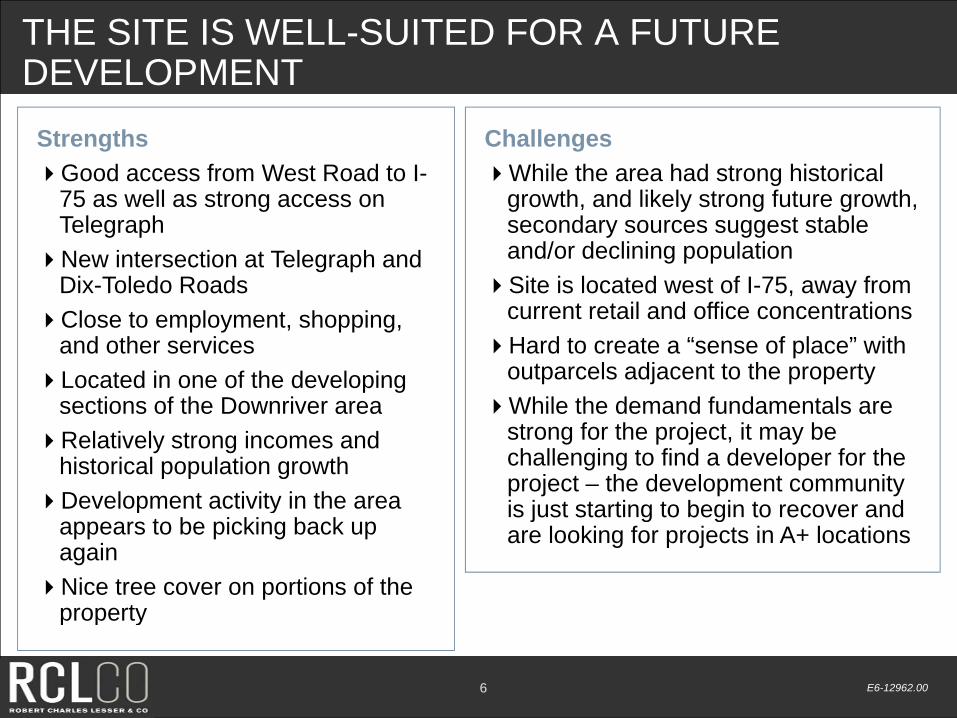

The subject site consists of approximately 77 acres of land zoned Town Center, located at the northwest intersection of Telegraph and West Roads. The site also has a signalized intersection at Telegraph and Dix-Toledo Roads. The site is well-located in Brownstown Township, an area that grew by almost 8,000 people between 2000 and 2010. Once the region begins to grow again, Brownstown is likely to be a recipient of the growth. The Southeastern Michigan Council of Governments (SEMCOG) predicts that Brownstown Township will grow by approximately 1,000 people by 2025. The site enjoys great access to both Telegraph and West Roads, and is, for the most part, surrounded by attractive land uses. A summary of strengths and weaknesses is provided in Figure 2. Strengths and Challenges Figure 2 Brownstown Town Center

STRENGTHS CHALLENGES

Good access from West Road to I-75 as well as strong access on Telegraph

New intersection at Telegraph and Dix-Toledo Roads Close to employment, shopping, and other services Located in one of the developing sections of the Downriver area Relatively strong incomes and historical population growth Development activity in the area appears to be picking back up again Nice tree cover on portions of the property

While the area had strong historical growth, and likely strong future

growth, secondary sources suggest stable and/or declining population Site is located west of I-75, away from the bulk of current retail and

office concentrations on West and Allen Roads Hard to create a “sense of place” with the RV storage facility within

the property boundaries While the demand fundamentals are strong for the project, it may be

challenging to find a developer for the project—the development community is just starting to begin to recover and are looking for projects in A+ locations

BROWNSTOWN DDA

Page 4 E6-12962.00 July 17, 2012

Subject Site History and Development Status The subject site was assembled in 2005 to develop the proposed Brownstown Town Center mixed-use project. A master-plan was created, zoning put into place, and a potential site plan developed. There had been a potential developer for the site. The proposed original site plan is shown in Figure 3 and includes the following uses south of the RV storage facility: 23 single-family lots, 56 apartments, 16 townhome units, and land for future development. North of the RV facility the plan included 4.5 acres of stormwater management, 12 acres of senior housing, 20 townhomes, a 50,000 square foot community center, a 26,000 square foot movie theater, and 97,000 square feet of other commercial. The movie theater located on another parcel on Allen Road, eliminates the market potential for a new theater on the property. Original Site Plan Figure 3 Brownstown Town Center

BROWNSTOWN DDA

Page 5 E6-12962.00 July 17, 2012

MARKET OVERVIEW National Outlook

The future success of the project is related to the local and regional outlook for real estate (typically related to the projected job and household growth) and the national outlook for real estate overall. RCLCO expects that residential real estate will bump along the bottom for the next 12 – 24 months, depending on geography—for example some markets in Texas are much farther along in their recovery. The most aggressive employment growth estimates, from Moody’s Analytics, forecast the return to pre-recession employment in 2014. While this results in an addition of six million jobs, the economy will not reach full employment due to increased population and labor force participation. RCLCO expects a slower recovery, with a return to pre-recession employment highs after 2015, and a return to full employment in 2016 or beyond. Regional and sector divergence are expected to continue. Threats to recovery include the price of oil and unrest in the Mideast, a further decline in the housing market, state and local government stress, the European sovereign debt crisis, weakening consumer confidence, and political deadlock. Based upon this national job outlook, housing starts will begin to rise in 2013 while lending standards and regulatory uncertainties loosen. In most markets “normal market conditions” will return in 2013/2014. Another key factor is the return of the Baby Boomers and Gen Y into the housing market starting in 2015 and continuing for 10 or more years. These generations have a significant impact on the underlying demand for real estate given their size and the timing of their entry or re-entry into the housing market. Real estate performance in the U.S. has been consistently cyclical, at least since records on commercial and residential pricing and volume have been tracked. “Peaks” and “valleys” may have different direct causes in every cycle, but consistently result from inevitable buy-side exuberance after a period of steady value increases and associated loosening of capital, particularly credit, resulting in skyrocketing pricing and excessive production. An event triggers an awakening of the market to the untenable situation in which it finds itself, and values, transaction, and production come to a standstill. The most recent real estate boom and bust was exceptionally severe, but very closely repeats patterns of earlier cycles. Figure 4 outlines the projected path of the real estate cycle over the next decade, including the timing for the following stages:

Bottom (2009 – 2012): The real estate bottom is characterized by real estate prices being below replacement costs; the bottom represents the ideal time to acquire existing assets.

Early Recovery (2011 – 2013): During the early recovery, prices begin to exceed replacement costs for many assets; the stage still offers numerous opportunities to acquire assets, as well as to reposition and develop those in preparation for subsequent phases.

BROWNSTOWN DDA

Page 6 E6-12962.00 July 17, 2012

Stability (2013 – 2014): Competition for assets becomes more difficult during the stable phase of the market; the market may offer select investment opportunities, but prices are increasing as cap rates compress.

Peak (2015 – 2016): At market peak, cap rates have compressed to the point that prices exceed reasonable net asset values for assets; the only purchasing opportunities will be highly opportunistic, otherwise, this represents the best opportunity to sell.

Downturn (2017): Investment activity is difficult during the downturn as it is impossible to know when the market will hit bottom and/or how low it will go; the downturn is a good time to start raising and committing funds to take advantage of low prices during the bottom.

Bottom (2018 – 2019)

Regions vary as do submarkets within regions which makes it critical to understand local market dynamics. Figure 4 National Real Estate Outlook

P=Price RC=Replacement Cost NAV=Net Asset Value

BROWNSTOWN DDA

Page 7 E6-12962.00 July 17, 2012

Regional Economic & Demographic Analysis The subject site is located in the Detroit-Warren-Livonia Metropolitan Statistical Area (MSA) that consists of Lapeer, Livingston, Macomb, Oakland, St. Clair, and Wayne Counties. This MSA was hit very hard during the recession, and while signs are positive for growth, it is one of the slower areas to recover in the nation. However, according to the Manpower Employment Outlook Survey from June 2012, “Detroit-Warren-Livonia, MI MSA employers expect to hire at a bullish pace during Quarter 3 2012. Among survey participants, the Detroit-Warren-Livonia, MI MSA employment outlook is the fifth best in the nation. From July to September, 27% of the companies interviewed plan to hire more employees, while 5% expect to reduce staff. Another 68% expect to maintain their current workforce levels and 0% are not certain of their hiring plans. This yields a Net Employment Outlook of 22%.” This is very positive for the region. Brownstown Town Center is located in Brownstown Township, which has just less than 1% of the households in the MSA and approximately 10% of the households in the Downriver Region (see Figure 1), which is Wayne County southwest of the City of Detroit (See Exhibits 2.1 and 2.2). The subject property is located within an area that has higher incomes than the rest of the Downriver area and the Detroit MSA overall (median household income of $53,000 in 2010 compared to $45,500 and $49,800 in Downriver and Detroit MSA respectively). The Detroit-Warren-Livonia MSA is expected to experience continued population decline from 2011 to 2020, according to ESRI and Economy.com, nationally recognized sources and SEMCOG, a locally recognized source (See Exhibit 2.3). However, after 2020, SEMCOG is projecting growth in the Detroit-Warren-Livonia MSA while Economy.com projects a continued decline. ESRI does not make projections out past 2016. However, SEMCOG is projecting Brownstown Township to continue to gain population throughout the entire time period. See Figure 5 below. Brownstown Township Population Projections Figure 5 SEMCOG 2040 Forecast

Change: 2010 - 20402010 2015 2020 2025 2030 2035 2040 Number %

Total Population 30,627 30,960 31,274 31,304 31,945 32,092 32,124 1,497 4.9%

Additional demographic and economic information is provided in Exhibits in Section 2.

BROWNSTOWN DDA

Page 8 E6-12962.00 July 17, 2012

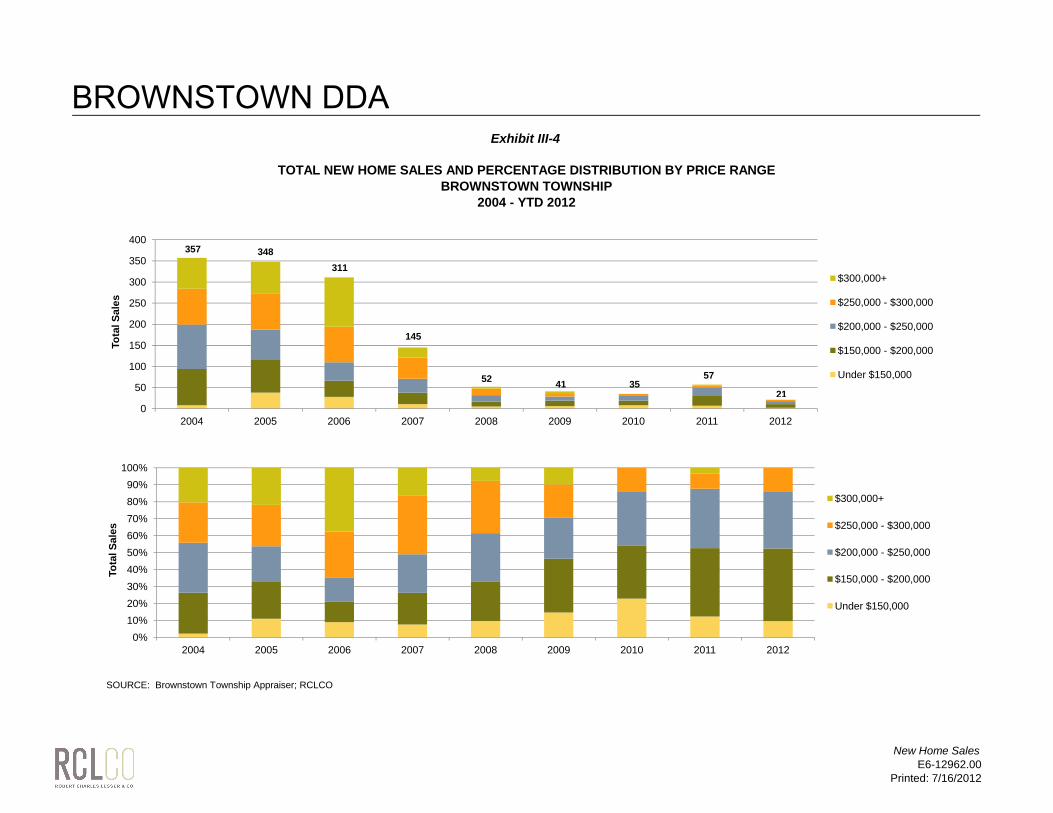

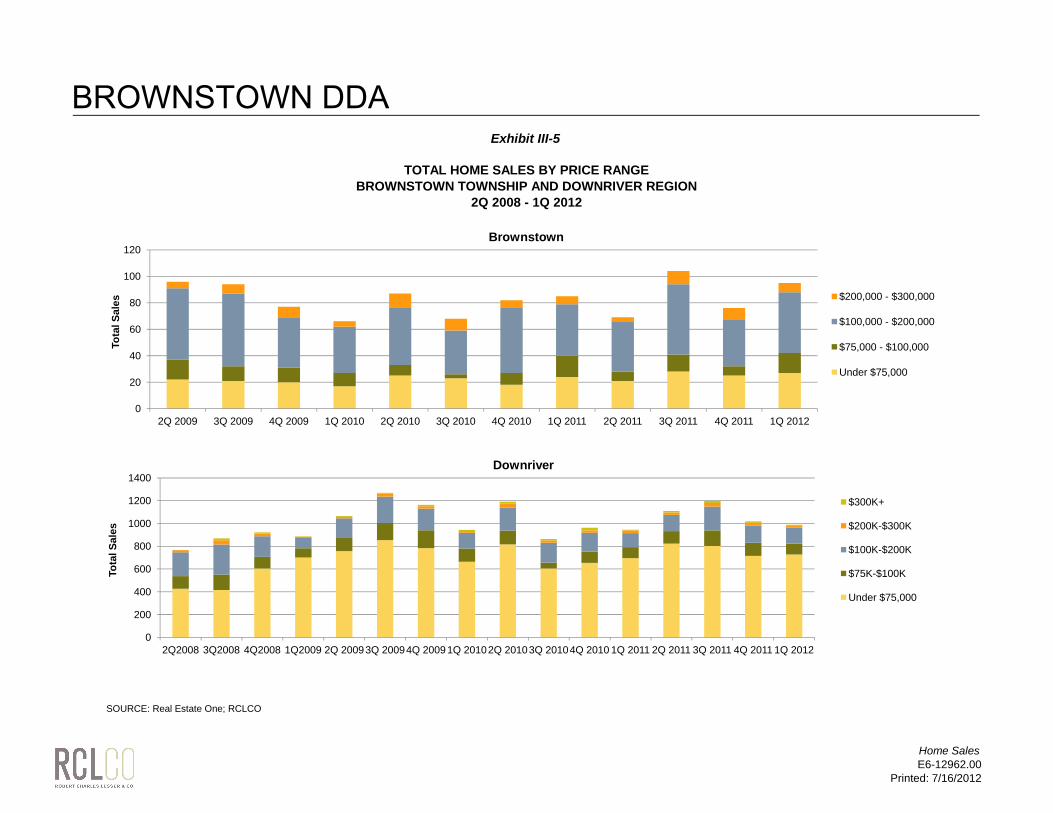

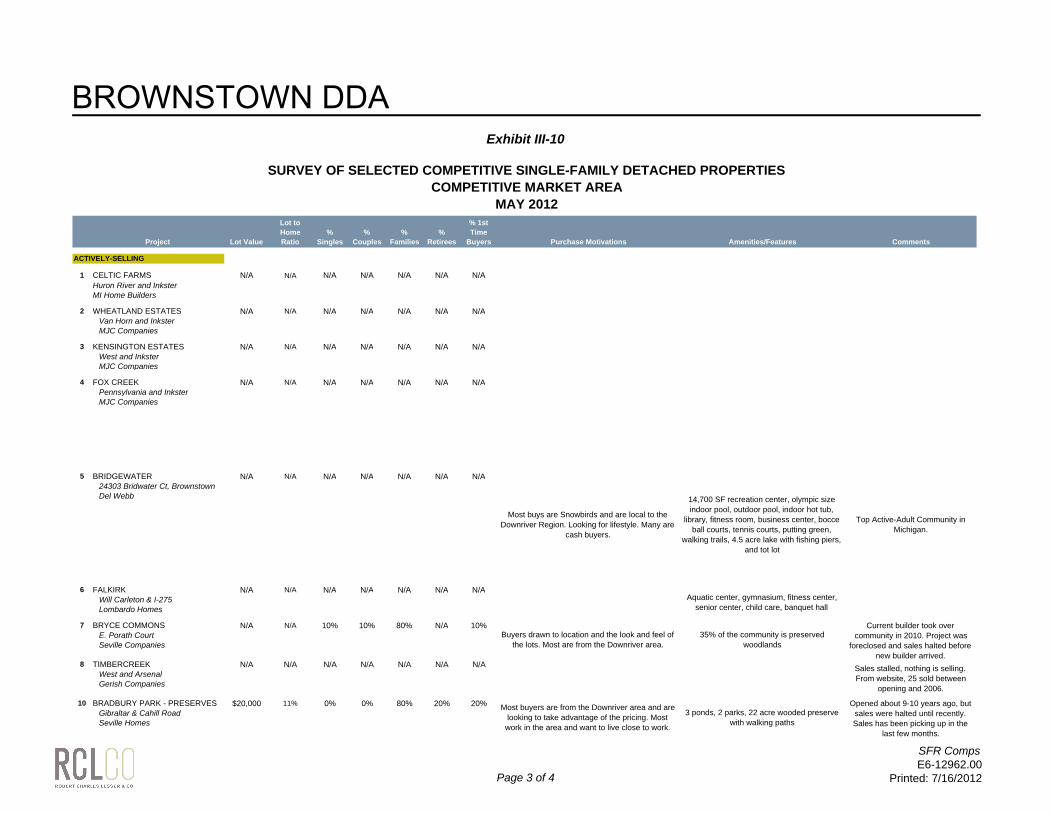

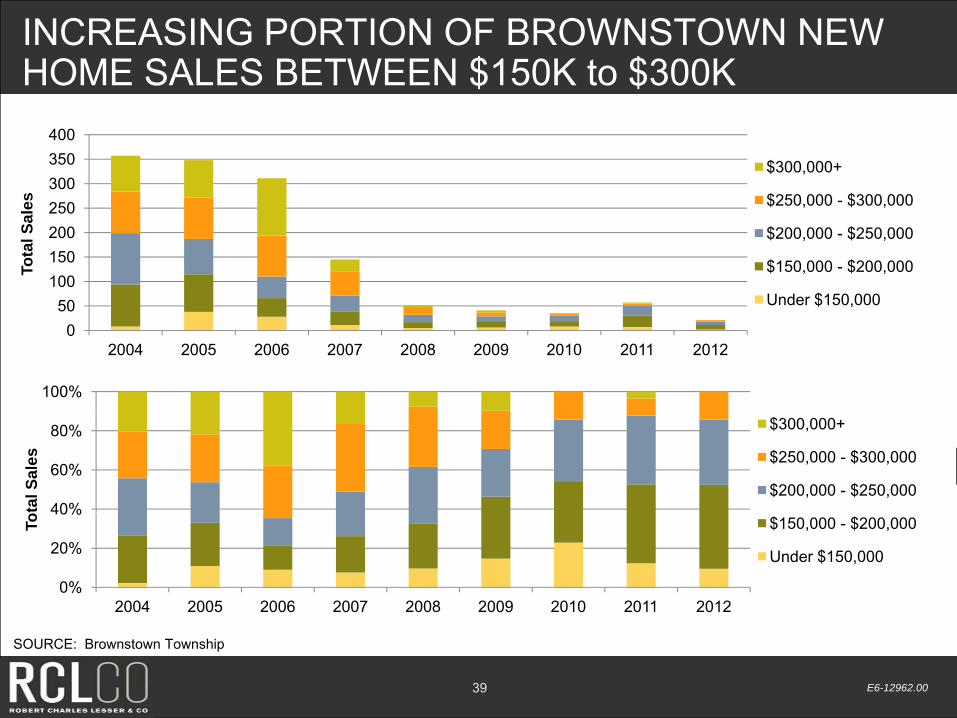

For-Sale Local Competitive Market From 2000 to 2005, average annual permits were approximately 19,000 annually in the Detroit-Warren-Livonia MSA. From 2006 to 2011 permits slid to an average of 4,000 per year with the lowest permitting year in 2009 with just 1,333 permits (see Exhibit 3.1). In terms of detached and attached housing units, from 2006 to 2011, approximately 88% of permits were for single-family homes (See Exhibit 3.1). Wayne County experienced a similar decline in the number of permits from a high of 6,317 in 2004 to a low of 288 in 2009. However, a larger percentage of permits were for multifamily from 2006 to 2011 (25%). See Exhibit 3.2. Permits in Brownstown have been down a considerable amount over the past few years, at an average of 44 per year from 2007 to 2011, compared to an average of 414 from 1995 to 2006 (See Exhibit 3.3). Like the rest of Detroit, the worst year was 2009. Each year since then the number of permits has slowly begun to increase. The majority of permits in Brownstown are for single-family detached housing (90%). As with many parts of the country, there are signs that the market is beginning to slowly recover. Job growth is projected to continue to increase which has an impact on demand for housing and retail. In addition, housing activity has picked up. During first quarter 2012, 21 new homes were sold in Brownstown, compared to 57 new homes overall sold in 2011. New home sales have been down significantly in the Township from an average of 300+ to under 60 the last few years (see Exhibit 3.4). However, this is likely to improve in the coming years. Total home sales have been fairly stable the last few years, with the majority of homes sold between $100,000 and $200,000 (see Exhibit 3.5). In order to determine what prices and absorptions are feasible in this market and at the subject site, RCLCO surveyed 14 nearby single-family detached communities and five attached communities (Exhibit 3.9 to 3.12). Not all of the new projects are actively selling as some have been dormant the last few years during the recession. Of those selling, the bulk of product is offered between $150,000 and $250,000 with an average home size range of 1,500 to 2,500 ($100/SF). The best selling project is Bridgewater, a Del Webb Active Adult Community, which is selling approximately 36 homes per year. Other projects reported that sales are picking back up as well. The attached products have yet to begin to recover. There is one actively selling project at Bradbury Park – The Coves with homes priced at $150,000. Other projects have foreclosures and re-sales on the market for $40,000 to $100,000 per unit. Overall, the market is projected to recover as inventories are burned off, demand returns, and new home activity continues. Anecdotal evidence suggests that builders are back in the market purchasing developed lots and traffic has increased in communities. Once the market recovers, Brownstown Township should again be a central location for new home activity in the Downriver area. The subject site is well located to capitalize on the market when it returns. It has good access to I-75, is near existing residential, and would provide residents with the opportunity to walk to retail. All of the residential exhibits are included in exhibit section three.

BROWNSTOWN DDA

Page 9 E6-12962.00 July 17, 2012

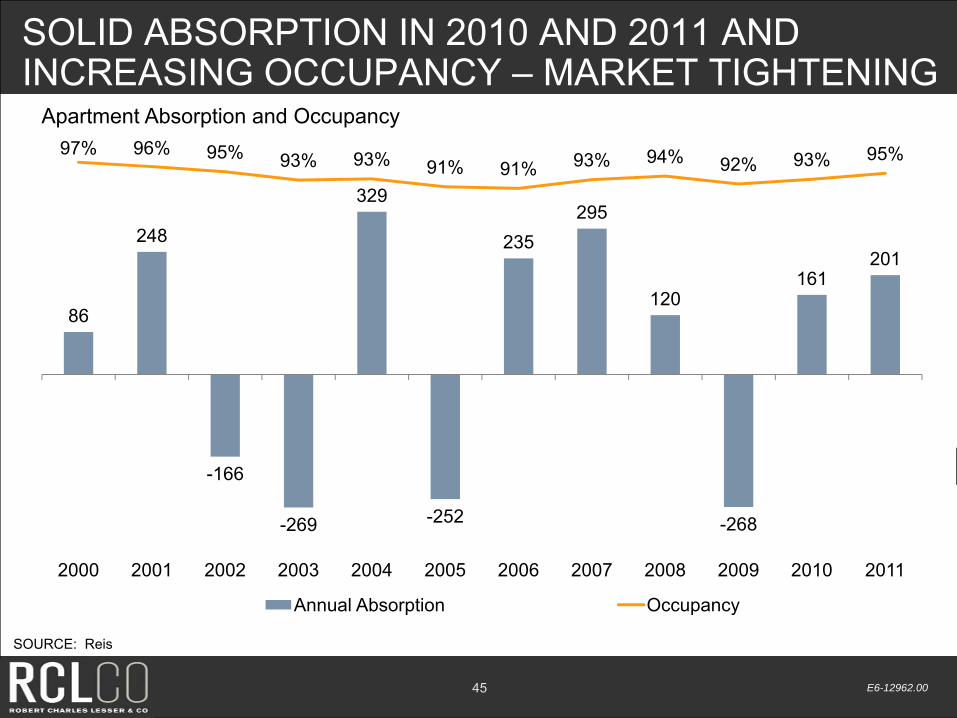

For-Rent Local Competitive Market The overall apartment market in Brownstown is healthy. Brownstown Township is part of the Reis Downriver/South Wayne apartment submarket. Overall effective rent has remained steady in the submarket, with an average of $682/month rent (see Exhibit 3.14). Very few apartments have been constructed in the submarket in the last ten years. Occupancy is high at 95%, and absorption is up (see Exhibit 3.16). In order to determine what rents and sizes are feasible in this market and at the subject site, RCLCO surveyed five of the newest competitive apartment projects and compiled information on their performance (see Exhibit 3.18 through 3.21). Rents for competitive apartment projects averaged $0.98, which is typically a rate barely sufficient to warrant new construction of garden-style product. The highest rent in the market is at Stratford Place Apartments in Brownstown Township at $1.02/SF. Occupancies were also very high at an average of 98%. Three of the projects were built in 2004, and none have been built since that time. Many of them reported recently raising rents, and they expect that trend to continue. Overall, the market is strong for apartments. The challenge has less to do with the supply side which is constrained, but with questions about the demand side. The depth of demand for higher-end apartments in Brownstown appears to be high enough to justify new construction. Exhibit 3.25 outlines the statistical demand RCLCO created for the subject property which suggests the demand for 225 new apartments with an 11% capture of the market. We believe the project could support 250 apartment units at just over $1.00/SF. The location and the walkability to retail would be a strong draw for renters.

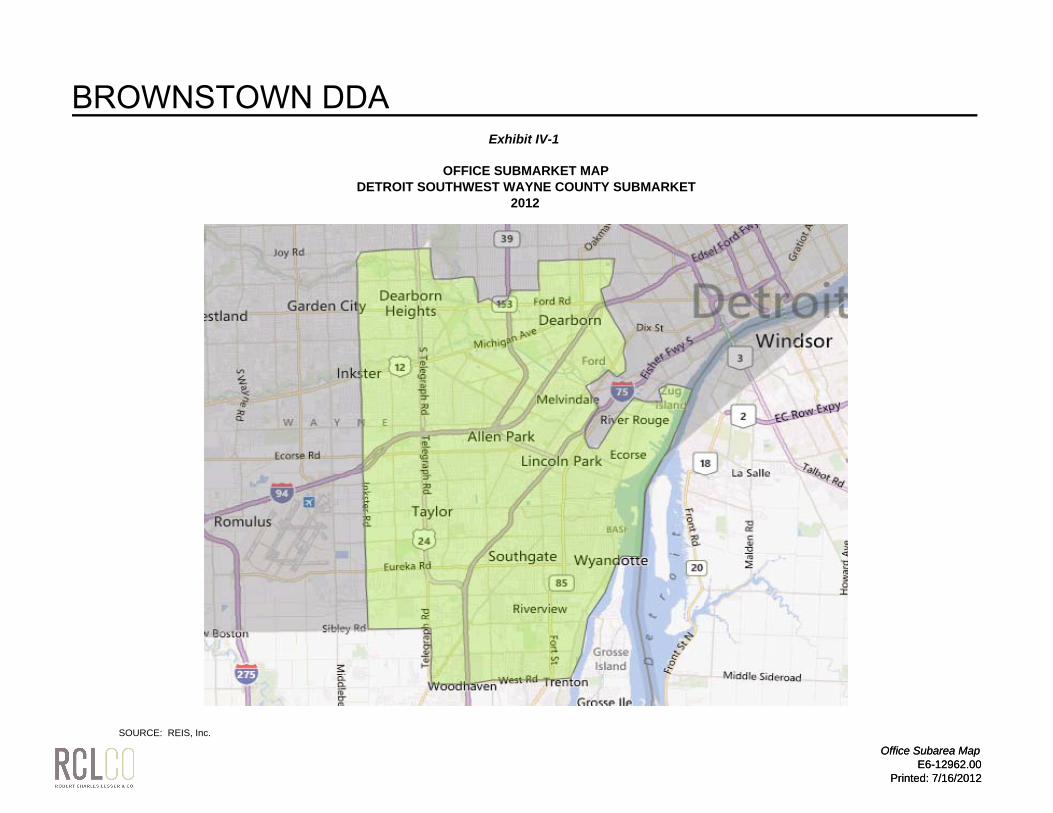

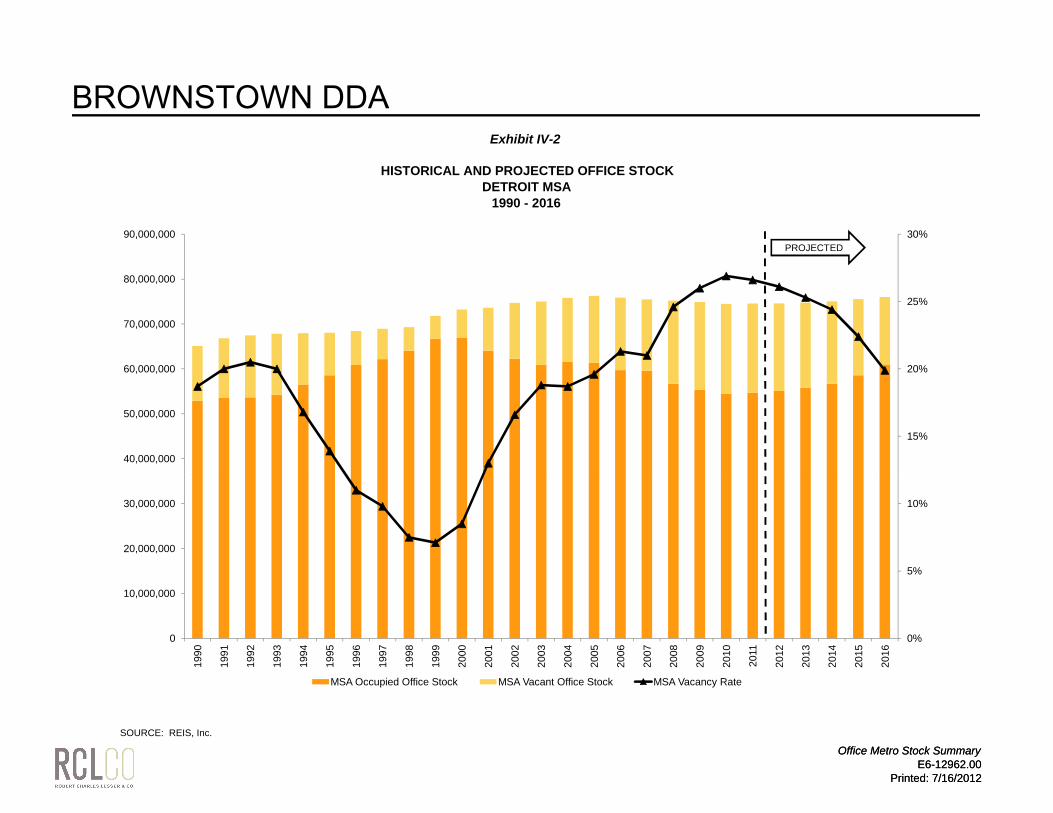

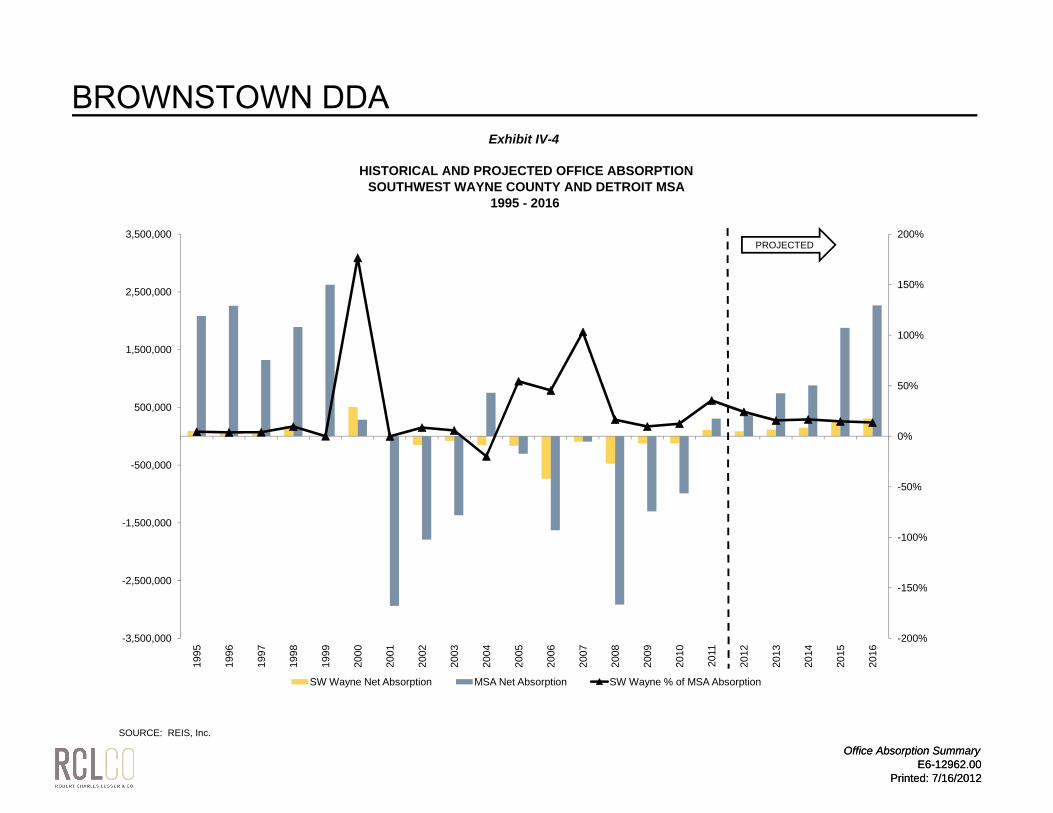

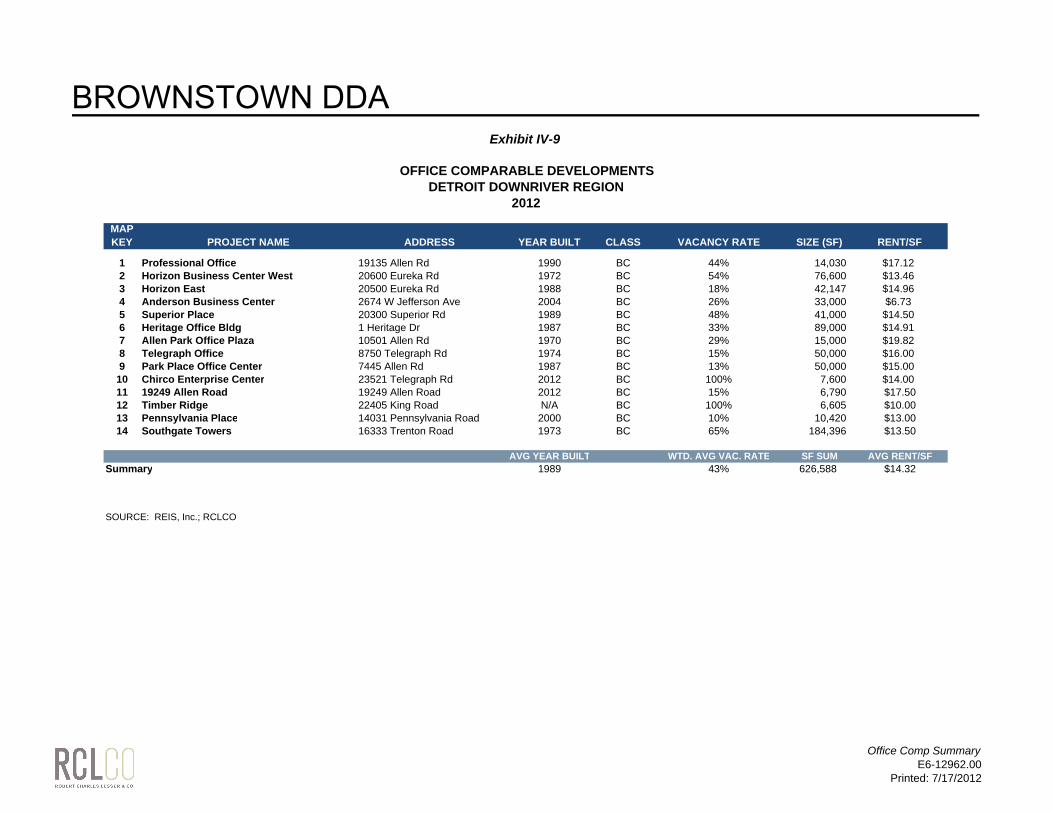

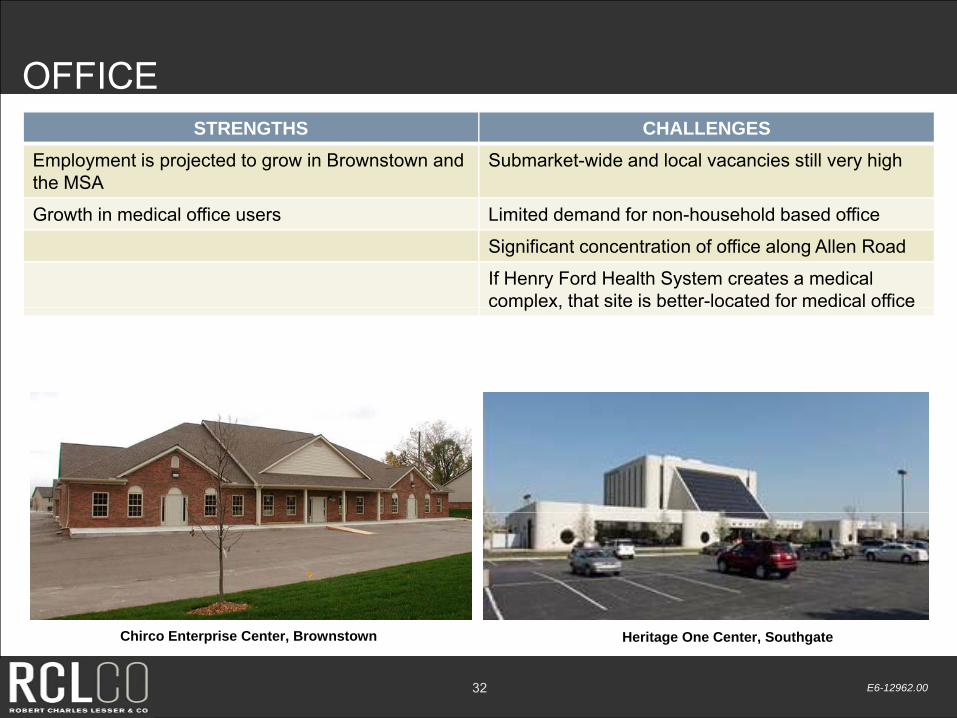

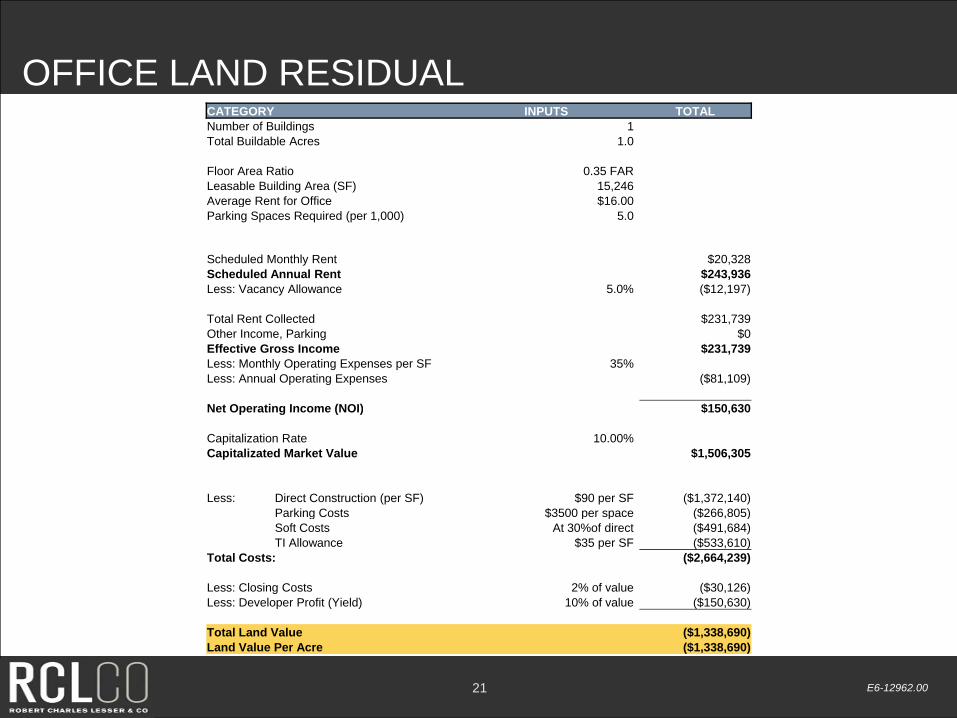

Office The office market is relatively weak. The subject site is located in the Reis Detroit Southwest Wayne County Submarket (Exhibit 4.1). Office absorption has been negative in the last few years with the exception of 2011. Going forward, absorption is projected to improve as the economy continues to recover (Exhibit 3.3). Rental rates have dropped from a high of over $20/SF in 2000 to just under $14/SF in 2012. It appears that rental rates have stabilized, but are not expected to grow significantly by 2016 (see Exhibit 4.5). The standard Class A and Class B office market is located north of Brownstown Township, primarily in the Dearborn area of Downriver. Office in Brownstown Township is primarily related to household needs (such as doctors, accountants, etc.). RCLCO examined information on 14 different office buildings/centers in the Downriver area (see Exhibits 4.8 and 4.9). These centers represent approximately 630,000 square feet of office space. The majority of office space closest to the subject site is located along Allen Road. Occupancies in the market vary, based primarily on the age and condition of the centers (0% – 90% occupied) with an average weighted occupancy of 57%. Rents range from $6.73/SF to $19.82/SF, with most around $14/SF.

BROWNSTOWN DDA

Page 10 E6-12962.00 July 17, 2012

The demand for office is generally weak in the overall market as the economy continues to recover. Typical office demand is based upon employment growth. As employment continues to grow in the market, so will the demand for office space, however, there is a significant amount of vacancy in the overall market that needs to be absorbed as well. The statistical demand completed by RCLCO suggests the total demand for approximately 50,000 square feet of office at the subject site (see Exhibit 4.12). Overall the opportunity in the market for office is limited. There is a significant amount of available space in the market, and the area is not a standard office market. In a true town center configuration, the site could be a good location for small, local office users (dentist, accountant, photographer, lawyer, architect) and medical office—perhaps partnering with Henry Ford Health System.

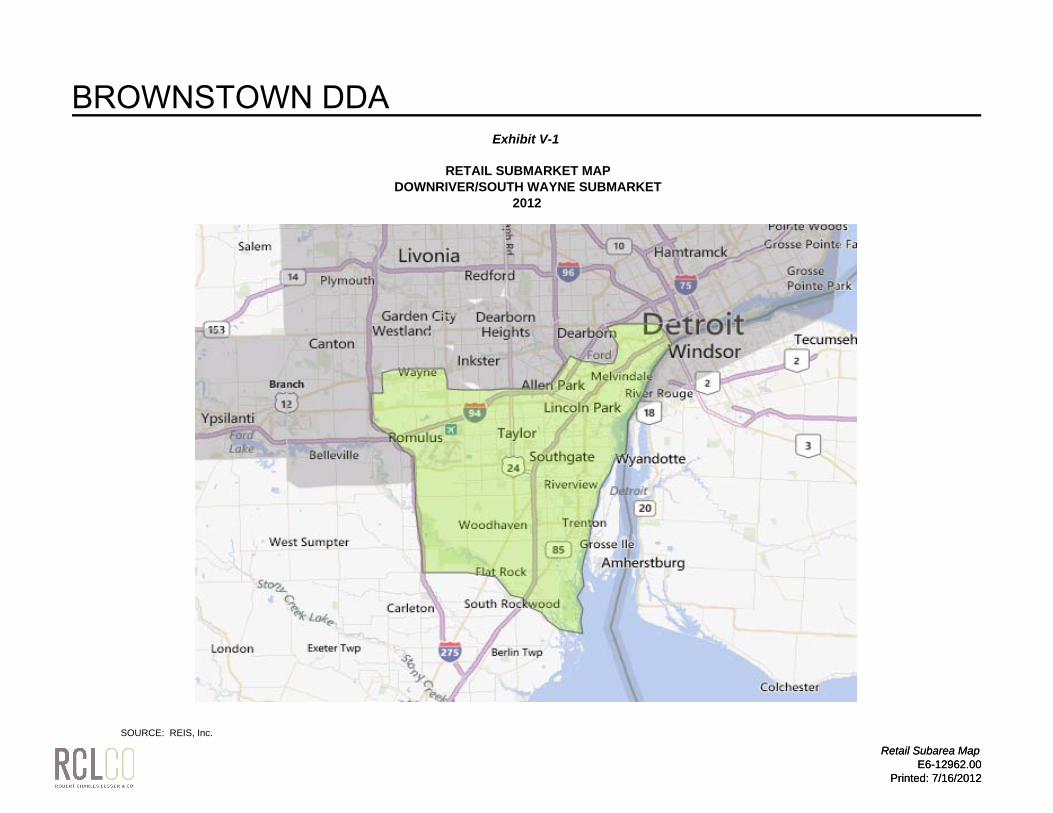

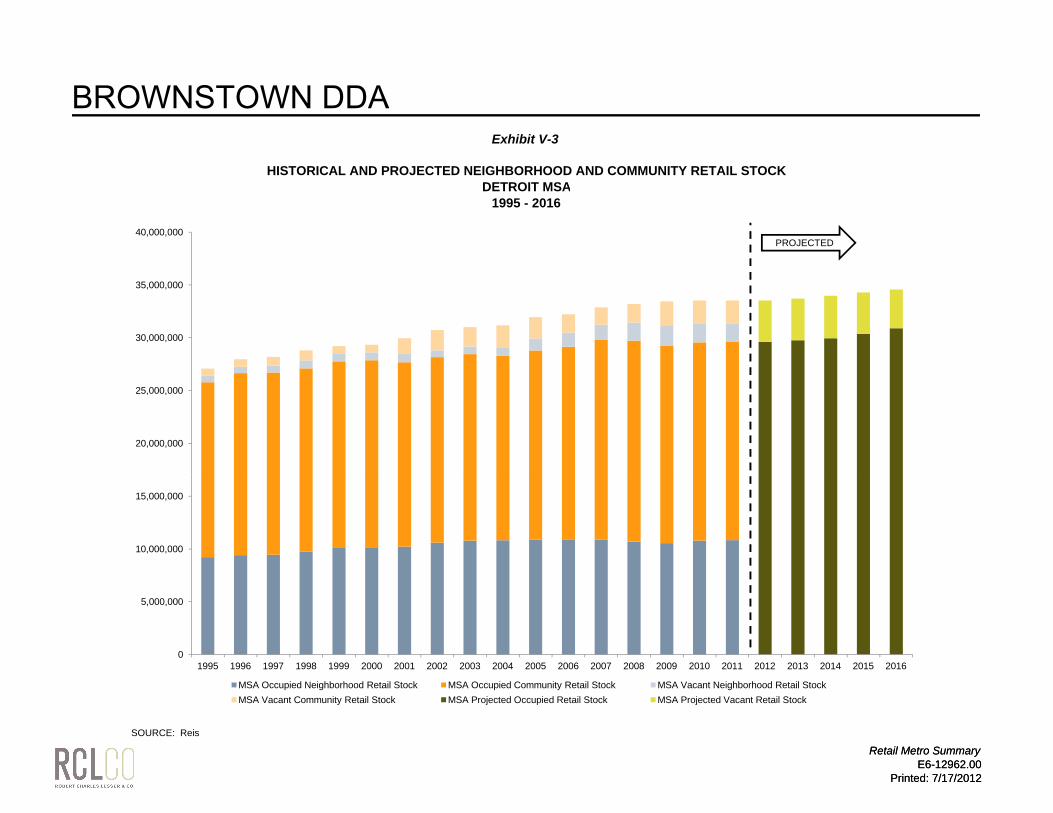

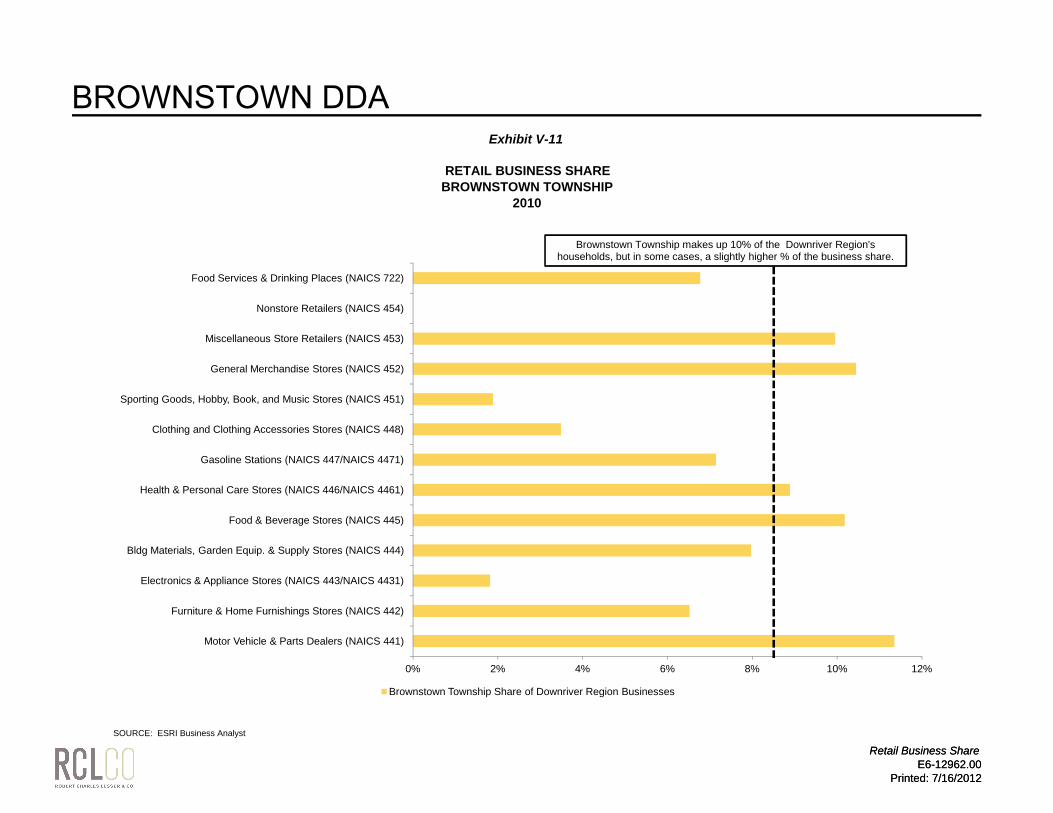

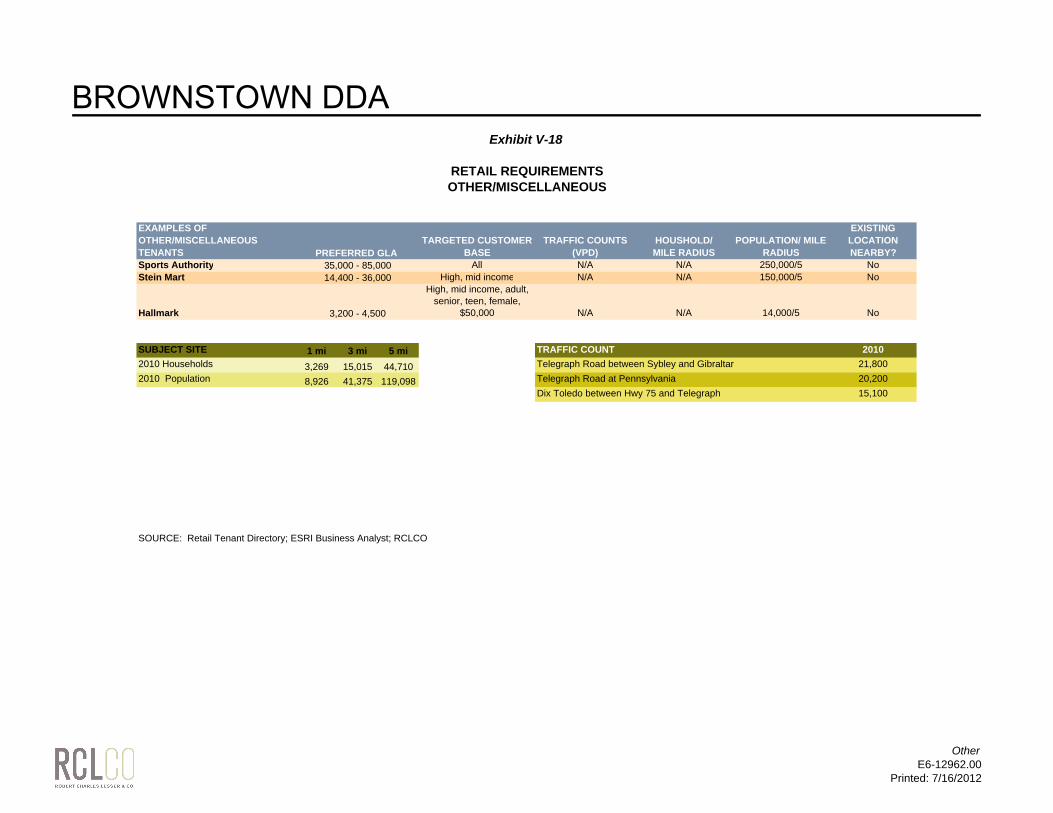

Retail The subject site is located in the Reis Downriver/South Wayne Submarket (Exhibit 5.1). Rental rates have been relatively stable for community1 and neighborhood 2 retail at approximately $14/SF for community retail and $15/SF for neighborhood retail. Both types of retail have relatively high vacancy rates (24% for community and 15% for neighborhood). See Exhibit 5.5. Traffic counts near the subject site are strong with approximately 20,000 cars per day on Telegraph Road (see Exhibit 5.6). The retail market is primarily saturated; however, many of the establishments and shopping centers in the area are in need of renovation and could likely be outperformed by new retail. RCLCO examined information on 30 different shopping centers in the Downriver area (see Exhibits 5.9 and 5.10). These centers represent 3.6 million square feet of retail space. The major centers closest to the subject site are concentrated along Eureka Road and West and Allen Roads. Occupancies in the market vary, based primarily on the age and condition of the centers (36% – 100% occupied) with an average weighted occupancy of 83%. Non-anchor rents range from $10/SF to $25/SF, with most at $15/SF. There is a lot of retail leakage both in the Township and within the Downriver Region for retail. This suggests that residents of the area shop outside of the market for many of their retail needs. This was anecdotally confirmed by talking to residents, business owners, and brokers in the market. The highest leakage within Brownstown Township is for Food Services & Drinking Places, General Merchandise Stores, Clothing, and Motor Vehicles & Parts Dealers.

1 One of the several standard classes of shopping centers recognized by The Urban Land Institute. The community shopping center usually has a junior department store or a

discount store as the major tenant. The community shopping center is typically about 150,000 square feet of store area but ranges from 100,000 square feet to 450,000 square feet. 2 The smallest type of shopping center, comprising 30,000 to 100,000 square feet. It provides for the sale of convenience goods (food, drugs, and sundries) and personal services

that meet the daily needs of an immediate neighborhood trade area. A supermarket is the principal tenant.

BROWNSTOWN DDA

Page 11 E6-12962.00 July 17, 2012

Therefore, although the demand for new space based upon new household growth is somewhat limited by the current economic climate, there is an opportunity to capture some of the retail dollars that are leaving the market. Overall the opportunity in the market for retail is mixed—it is heavily dependent upon the site. The subject site represents a good opportunity for retail. It is at the intersection of two major roads, and with the correct land plan, could capitalize on the intersection, even with the gas station on the corner. If the town center is located on the northern portion of the property at the intersection of Telegraph and Dix-Toledo, it will be necessary to have strong anchors and to create a reason for people to be there. The better location for retail is at West and Telegraph Roads. All of the retail information is included in exhibits in section four.

BROWNSTOWN DDA

Page 12 E6-12962.00 July 17, 2012

CONCLUSIONS AND RECOMMENDATIONS The subject property is well-suited for a development. It is located along a major intersection of Telegraph and West Roads, as well as the intersection of Telegraph and Dix-Toledo Roads. It is adjacent to an established residential neighborhood and enjoys good access to nearby retail and amenities. In addition, it is located adjacent to the Ice Box, an ice skating facility which draws in a large number of users, and close to the Township property. Based upon our analysis, RCLCO provided the Township with two sets of recommendations, one for a town center that roughly followed the initial site plan, and another scenario based upon moving the retail to the intersection of Telegraph and West Roads without a public and/or civic space.

Option 1: Town Center Recommendations The site has the potential to become a mixed-use town center. However, it will be challenging given the economic climate to create a vertically mixed-use town center. Rents are not high enough to justify this type of construction and developers have a hard time financing vertical mixed-use projects. Traffic counts are not as high as the concentration of retail along Allen and West Road, but similar to other town center locations, suggesting enough traffic for retailers to consider the site. In addition, the area is already a proven retail site with retail in the area (Kroger-anchored shopping center and CVS-anchored center across Telegraph). If a town center were created, it would be horizontally mixed (the land uses next to each other), but not vertically mixed (the uses on top of each other). In this scenario, it will be critical to find a key anchor for the town center. This anchor could be a large anchor retail tenant (furniture store, home furnishing store, specialty food store), a collection of restaurants, civic space (park, library, etc.), a strong connection to Ice Box with new soccer fields, and/or a YMCA (another partnering opportunity with Henry Ford Health System). The key would be to have something of scale that would attract other tenants as well as shoppers to the town center. Other key success factors include:

The development should be characterized by civic/other anchors, superior place making, enhanced internal connectivity, pedestrian access to parks and commercial uses, and strong transportation accessibility, and visibility

It is key to create and deliver an experience that the market values and that generates premiums. This includes walking linkages between the uses

Integration of civic uses will create the distinction of a public center, rather than a private development, contributing to a true “town center”

BROWNSTOWN DDA

Page 13 E6-12962.00 July 17, 2012

Civic or other anchor components should be developed in conjunction with or prior to private development to form the “core” or “beach” of the development

Site should be master-planned in anticipation of future uses to create a well-integrated development at build-out

Utilize the largest, open space to create the commercial core at the northern end of the property

Need to have strong entrance off of Dix-Toledo and strong anchors

The single-family detached on the site will buffer the existing single-family to the west

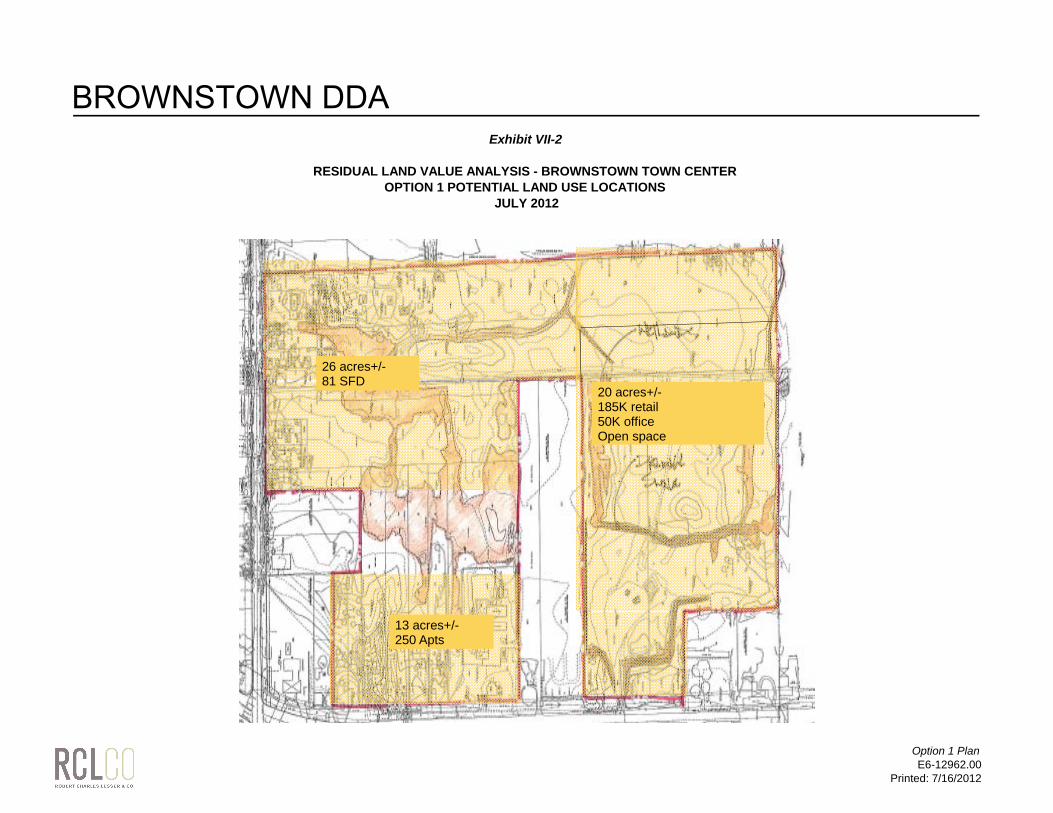

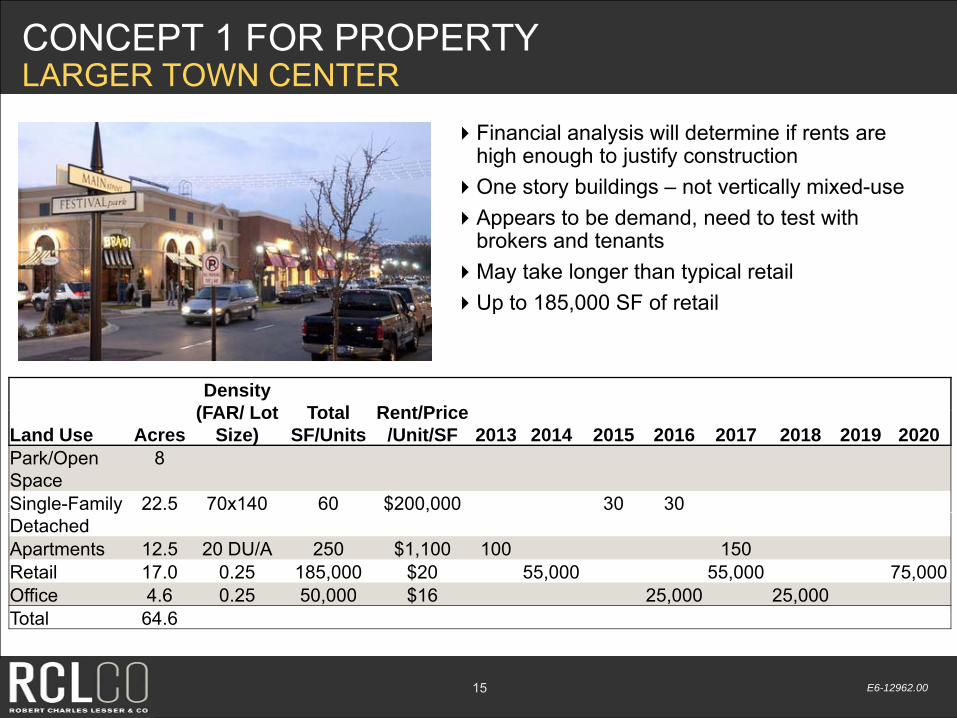

This program would allow for future expansion into the RV storage area as a mix of uses Figure 6 shows the potential location of the various land uses in Option 1. The original detailed program is shown in Exhibit 1.1. The modified program (based upon the results of the financial model) and the results of the financial model are provided in Exhibit 7.1. The financial model suggests the property is worth approximately $5 million, depending on the amount of infrastructure that needs to be included to sell it, it could be closer to $4 million.

Figure 6 Option 1, Potential Site Plan

BROWNSTOWN DDA

Page 14 E6-12962.00 July 17, 2012

Option 2: Not Town Center Recommendations The site is well-suited for a variety of land uses. In addition to the Town Center option above, RCLCO considered an option that did not mix the land uses or create a town center, but broke the development into three different parcels (although someone could buy and develop all of them). In this scenario, each land use would be optimized for location as well as size. This program is less risky than the town center option. Key considerations and means to success of this scenario include the following:

Retail would be along Telegraph and West Roads. It will be important to have a land plan that demonstrates the visibility of the retail from the intersection with the existing gas station

The single-family detached would occupy the largest portion of the property and create a community of scale. Ideally, it would be walkable to the retail and to the Brownstown Township Recreation Campus

Garden-style apartment complex along West Road taking advantage of the wetlands and location off West Road, close to the retail

Provide walking linkages between land uses

Would allow for future expansion into RV storage area as a mix of uses

Additional frontage on Telegraph for commercial—this could be either stand-alone retail (restaurant or bank) or a small office building Figure 7 shows the potential location of the various land uses in Option 2. The original detailed program is shown in Exhibit 1.1. The modified program (based upon the results of the financial model) and the results of the financial model are provided in Exhibit 7.2. The financial model suggests the land is worth approximately $5 million, or $4.5 million, depending on the amount of costs necessary to improve land prior to selling. This is similar to Option 1. However, this scenario is less risky given the type of development and location of land uses.

BROWNSTOWN DDA

Page 15 E6-12962.00 July 17, 2012

Figure 7 Option 2, Potential Site Plan

BROWNSTOWN DDA

Page 16 E6-12962.00 July 17, 2012

CRITICAL ASSUMPTIONS Our conclusions are based on our analysis of the information available from our own sources and from the client as of the date of this report. We assume that the information is correct, complete, and reliable. We made certain assumptions about the future performance of the global, national, and local economy and real estate market, and on other factors similarly outside either our control or that of the client. We analyzed trends and the information available to us in drawing these conclusions. However, given the fluid and dynamic nature of the economy and real estate markets, as well as the uncertainty surrounding particularly the near-term future, it is critical to monitor the economy and markets continuously and to revisit the aforementioned conclusions periodically to ensure that they stand the test of time. We assume that the economy and real estate markets are close to bottoming out for the current cycle, and that they will grow at a stable and moderate rate starting in 2011, more or less in a straight line on average for the duration of the analysis period (to 2020 and beyond). However, history tells us that stable and moderate growth patterns are not sustainable over extended periods of time, and that the economy is cyclical and that the real estate markets are typically highly sensitive to business cycles. Further, it is very difficult to predict when the current economic and real estate downturns will end, and what will be the shape and pace of growth once they are recovered. With the above in mind, we assume that the long term average absorption rates and price changes will be as projected, realizing that most of the time performance will be either above or below said average rates. Our analysis does not take into account the potential impact of future economic shocks on the national and/or local economy, and does not necessarily account for the potential benefits from major "booms,” if and when they occur. Similarly, the analysis does not necessarily reflect the residual impact on the real estate market and the competitive environment of such a shock or boom. Also, it is important to note that it is difficult to predict changing consumer and market psychology. For all the reasons outlined, we recommend the close monitoring of the economy and the marketplace, and updating this analysis as appropriate. Further, the project and investment economics should be “stress tested” to ensure that potential fluctuations in revenue and cost assumptions resulting from alternative scenarios regarding the economy and real estate market conditions will not cause failure.

In addition, we assume that once the current cycle is over, the following will occur in accordance with current expectations:

Economic, employment, and household growth.

BROWNSTOWN DDA

Page 17 E6-12962.00 July 17, 2012

Other forecasts of trends and demographic and economic patterns, including consumer confidence levels.

The cost of development and construction.

Tax laws (i.e., property and income tax rates, deductibility of mortgage interest, and so forth).

The availability and cost of capital and mortgage financing for real estate developers, owners and buyers, at levels present in the market before the most recent run up (i.e., early 2000s levels).

Competitive projects will be developed as planned (active and future) and that a reasonable stream of supply offerings will satisfy real estate demand.

Major public works projects occur and are completed as planned.

Should any of the above change, this analysis should probably be updated, with the conclusions reviewed accordingly (and possibly revised).

BROWNSTOWN DDA

Page 18

E6-12962.00 July 17, 2012

GENERAL LIMITING CONDITIONS Reasonable efforts have been made to ensure that the data contained in this study reflect accurate and timely information and are believed to be reliable. This study is based on estimates, assumptions, and other information developed by RCLCO from its independent research effort, general knowledge of the industry, and consultations with the client and its representatives. No responsibility is assumed for inaccuracies in reporting by the client, its agent, and representatives or in any other data source used in preparing or presenting this study. This report is based on information that to our knowledge was current as of the date of this report, and RCLCO has not undertaken any update of its research effort since such date. Our report may contain prospective financial information, estimates, or opinions that represent our view of reasonable expectations at a particular time, but such information, estimates, or opinions are not offered as predictions or assurances that a particular level of income or profit will be achieved, that particular events will occur, or that a particular price will be offered or accepted. Actual results achieved during the period covered by our prospective financial analysis may vary from those described in our report, and the variations may be material. Therefore, no warranty or representation is made by RCLCO that any of the projected values or results contained in this study will be achieved. Possession of this study does not carry with it the right of publication thereof or to use the name of "Robert Charles Lesser & Co." or "RCLCO" in any manner without first obtaining the prior written consent of RCLCO. No abstracting, excerpting, or summarization of this study may be made without first obtaining the prior written consent of RCLCO. This report is not to be used in conjunction with any public or private offering of securities or other similar purpose where it may be relied upon to any degree by any person other than the client without first obtaining the prior written consent of RCLCO. This study may not be used for any purpose other than that for which it is prepared or for which prior written consent has first been obtained from RCLCO.

APPENDIX: SUPPORTING EXHIBITS

BROWNSTOWN DDA

Page i E6-12962.00 July 17, 2012

LIST OF EXHIBITS

I. RECOMMENDATIONS

Exhibit I-1 Recommendations; Brownstown Town Center; June 2012

II. SOCIOECONOMICS

Exhibit II-1 Location Map; Brownstown Township, Woodhaven, and Downriver Region

Exhibit II-2 Comparative Socioeconomic Characteristics; Brownstown Township, Woodhaven, Downriver Region, and Detroit MSA; 2000 – 2016

Exhibit II-3 Projected Population Growth; Wayne County Excluding Detroit; 2000 – 2035

Exhibit II-4A Households by Age and Income; Brownstown Township, MI; 2010

Exhibit II-4B Households by Age and Income; Woodhaven, MI; 2010

Exhibit II-4C Households by Age and Income; Downriver Region, MI; 2010

Exhibit II-5 Household Shares; Downriver Region, Brownstown Township, and Woodhaven; 2000 – 2015

Exhibit II-6 Housing Unit Trends; Downriver Region, Brownstown Township, and Woodhaven; 2000 – 2015

Exhibit II-7A Compound Annual Growth Rates; Downriver Region, Brownstown Township, and Woodhaven; 2000 – 2015

Exhibit II-7B Household Shares; Downriver Region, Brownstown Township, and Woodhaven; 2000 – 2015

Exhibit II-8 Population 25+ by Educational Attainment; Brownstown Township, Woodhaven, Downriver Region, and Detroit MSA; 2010

Exhibit II-9 Inbound and Outbound Migration; Wayne County, MI; 2010

BROWNSTOWN DDA

Page ii E6-12962.00 July 17, 2012

Exhibit II-10 Place of Employment by Zip Code; Residents Living in Brownstown Township; 2010

Exhibit II-11 Place of Residence by Zip Code; Employees Working in Brownstown Township; 2010

Exhibit II-12 Projected Employment Growth; Wayne County Excluding Detroit; 2000 – 2035

Exhibit II-13 Household Annual Growth Rate by Block Group; Brownstown Township, MI; 2000 – 2010

Exhibit II-14 Household Annual Growth Rate by Block Group; Brownstown Township, MI; 2010 – 2015

Exhibit II-15 Household Density by Block Group; Brownstown Township, MI; 2010

Exhibit II-16 Median Household Income by Block Group; Brownstown Township, MI; 2010

Exhibit II-17 Median Age by Block Group; Brownstown Township, MI; 2010

Exhibit II-18 Median Home Values by Block Group; Brownstown Township, MI; 2010

Exhibit II-19 Employment Density by Block Group; Brownstown Township, MI; 2010

Exhibit II-20 Percent of Rent Occupied Housing Units by Block Group; Brownstown Township, MI; 2010

Exhibit II-21 Number of Employees; Brownstown Township, MI; 2010

Exhibit II-22 Shopping Centers; Brownstown Township, MI; 2010

III. RESIDENTIAL

Exhibit III-1A Historical Single-Family and Multifamily Permits; Detroit MSA; 1990 – YTD 2012

Exhibit III-1B Historical Single-Family and Multifamily Permits; Wayne County, MI; 1990 – YTD 2012

Exhibit III-1C Historical Single-Family and Multifamily Permits; Brownstown Township, MI; 1990 – YTD 2012

Exhibit III-2 Multifamily Share of Permits; Detroit MSA, Wayne County, and Brownstown Township; 1990 – 2011

Exhibit III-3 Geographic Share of Permits; Brownstown Township, Wayne County, and Detroit MSA; 1990 – 2011

BROWNSTOWN DDA

Page iii E6-12962.00 July 17, 2012

Exhibit III-4 Total New Home Sales and Percentage Distribution by Price Range; Brownstown Township; 2004 – YTD 2012

Exhibit III-5 Total Home Sales by Price Range; Brownstown Township and Downriver Region; 2Q 2008 – 1Q 2012

Exhibit III-6 Inventory Analysis of Vacant Developed Lots; Brownstown Township; May 25, 2012

Exhibit III-7 Brownstown Total Home Sales by Price Range as a Percent of the Downriver Region; Brownstown Township and Downriver Region; 2Q 2009 – 1Q 2012

Exhibit III-8 Percentage Breakdown of Home Sales by Price Range; Brownstown Township and Downriver Region; 2Q 2009 – 1Q 2012

Exhibit III-9 For-Sale Communities Map; Detroit Downriver Region; 2012

Exhibit III-10 Summary of Selected Competitive Single-Family Detached Properties; Competitive Market Area; May 2012

Exhibit III-11 Home Price to Unit Size Relationship; Comparable Single-Family Projects; May 2012

Exhibit III-12 Survey of Selected Competitive Attached Properties; Competitive Market Area; May 2012

Exhibit III-13 RESI Submarket Map; Downriver/South Wayne Submarket

Exhibit III-14 Effective Rents; Downriver/South Wayne Submarket; 2000 – 2011

Exhibit III-15 Annual Completions; Downriver/South Wayne Submarket; 2000 – 2011

Exhibit III-16 Annual Absorption and Occupancy Rate Trends; Downriver/South Wayne Submarket; 2000 – 2011

Exhibit III-17 Effective Rent and Occupied Inventory Trends; Downriver/South Wayne Submarket; 2000 – 2011

Exhibit III-18 Map of Competitive Apartment Projects; Detroit Downriver Region, MI; May 2012

Exhibit III-19 Summary of Apartment Market Comparables; Detroit Downriver Region, MI; May 2012

Exhibit III-20 Effective Base Rent to Unit Size Relationship; Competitive Apartments; May 2012

Exhibit III-21 Effective Base Rent to Unit Size Relationship by Unit Type; Competitive Apartments; May 2012

BROWNSTOWN DDA

Page iv E6-12962.00 July 17, 2012

Exhibit III-22 Summary of Older Apartment Developments; Detroit Downriver Region, MI; May 2012

Exhibit III-23 Distribution of Gross Rent; Brownstown Township; 2010

Exhibit III-24 Distribution of Gross Rent; Detroit Downriver Region; 2010

Exhibit III-25 Annual Rental Demand Potential; Detroit Downriver Region

Exhibit III-26 Annual New Home Demand Potential; Detroit Downriver Region and Brownstown Town Center; 2011 – 2016

IV. OFFICE

Exhibit IV-1 Office Submarket Map; Detroit Southwest Wayne County Submarket; 2012

Exhibit IV-2 Historical and Projected Office Stock; Detroit MSA; 1990 – 2016

Exhibit IV-3 Historical and Projected Office Stock; Detroit Southwest Wayne County Submarket; 1995 – 2016

Exhibit IV-4 Historical and Projected Office Absorption; Southwest Wayne County and Detroit MSA; 1995 – 2016

Exhibit IV-5 Effective Rate and Vacancy Rate; Southwest Wayne County and Detroit MSA; 1995 – 2016

Exhibit IV-6 Ratio of Asking Rent to Effective Rent; Southwest Wayne County and Detroit MSA; 1995 – 2016

Exhibit IV-7 Number of Employees; Brownstown Township, MI; 2010

Exhibit IV-8 Comparable Office Developments Map; Detroit Downriver Region; 2012

Exhibit IV-9 Office Comparable Developments; Detroit Downriver Region; 2012

Exhibit IV-10 Business Summary – Number of Businesses; Brownstown Township; 2010

Exhibit IV-11 Business Share; Brownstown Township, MI; 2010

Exhibit IV-12 Office Demand; Brownstown Township; 2012 – 2025

BROWNSTOWN DDA

Page v E6-12962.00 July 17, 2012

V. RETAIL

Exhibit V-1 Retail Submarket Map; Downriver/South Wayne Submarket; 2012

Exhibit V-2 Historical and Projected Neighborhood and Community Retail Stock; Detroit Downriver Submarket; 2000 – 2016

Exhibit V-3 Historical and Projected Neighborhood and Community Retail Stock; Detroit MSA; 1995 – 2016

Exhibit V-4 Submarket Share of Metro Area Retail Stock; Downriver Submarket and Detroit MSA; 2000 – 2016

Exhibit V-5 Historical Effective Rents and Vacancy Rates; Detroit Downriver Submarket; 2000 – 2011

Exhibit V-6 Average Daily Traffic Counts; Detroit Downriver Region; 2010

Exhibit V-7 Grocery and General Merchandise Retail Map; Brownstown Township, MI; 2012

Exhibit V-8 1-, 3-, and 5-Mile Ring; Brownstown Township, MI; 2012

Exhibit V-9 Retail Comparables Map; Detroit Downriver Region; 2012

Exhibit V-10 Neighborhood Center and Community Center Retail Comparables; Brownstown Township, MI; 2012

Exhibit V-11 Retail Business Share; Brownstown Township; 2010

Exhibit V-12 Retail Surplus and Leakage; Brownstown Township and Downriver Region; 2010

Exhibit V-13 Retail Requirements; Grocery Stores

Exhibit V-14 Retail Requirements, Furniture and Electronics

Exhibit V-15 Retail Requirements, Health and Professional Care

Exhibit V-16 Retail Requirements, Department Store

Exhibit V-17 Retail Requirements, Clothing Store

Exhibit V-18 Retail Requirements, Other/Miscellaneous

BROWNSTOWN DDA

Page vi E6-12962.00 July 17, 2012

Exhibit V-19 Retail Requirements, Limited Service Restaurants

Exhibit V-20 Retail Requirements, Full Service Restaurants

Exhibit V-21 Retail Demand Based on Current Unmet Demand by Supply of Retail in Trade Areas; Brownstown Township, MI; 2010

VI. CASE STUDIES

Exhibit VI-1 Summary of Investment Criteria from Steiner and Associates; Compared to Brownstown Town Center; May 2012

Exhibit VI-2 Community Case Studies; Town Center Case Studies; May 2012

VII. FINANCIAL MODEL

Exhibit VII-1 Financial Analysis – Option 1; Brownstown Town Center; July 2012

Exhibit VII-2 Residual Land Value Analysis – Brownstown Town Center; Option 1 Potential Land Use Locations; July 2012

Exhibit VII-3 Financial Analysis – Option 2; Brownstown Town Center; July 2012

Exhibit VII-4 Residual Land Value Analysis – Brownstown Town Center; Option 2 Potential Land Use Locations; July 2012

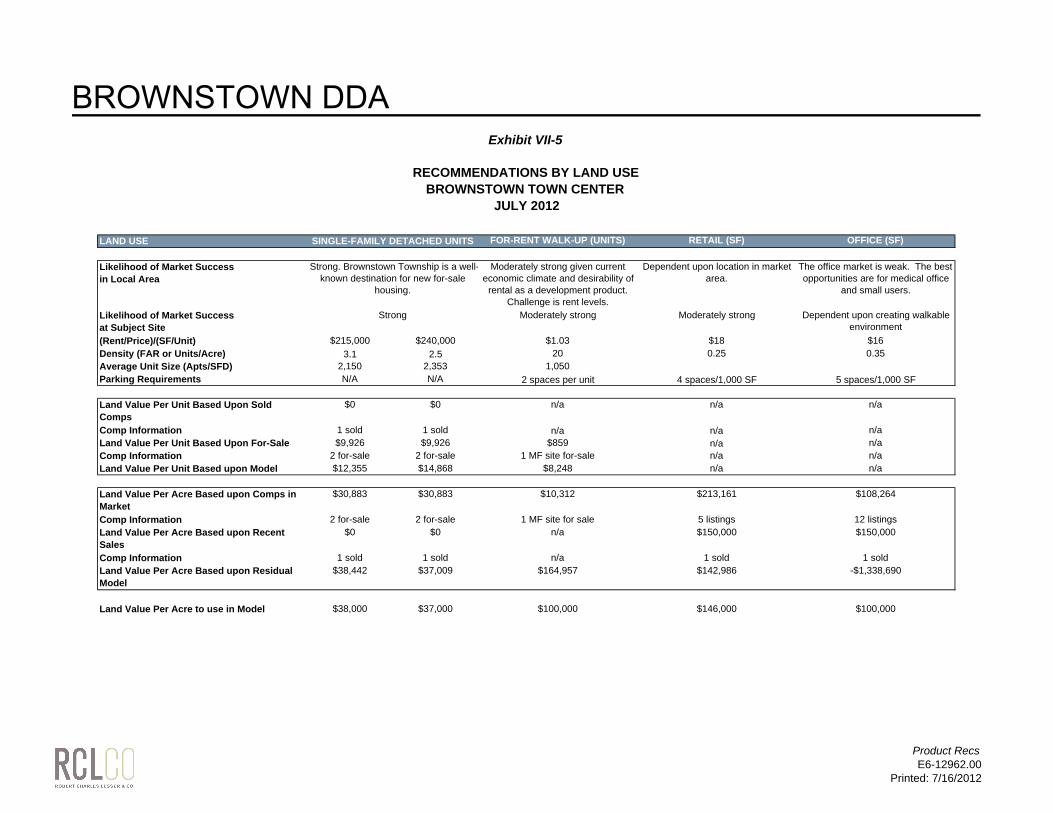

Exhibit VII-5 Recommendations by Land Use; Brownstown Town Center; July 2012

Exhibit VII-6 Residual Land Value Analysis – Brownstown Town Center; Single-Family Detached; July 2012

Exhibit VII-7 Residual Land Value Analysis – Brownstown Town Center; Garden-Style Apartments; July 2012

Exhibit VII-8 Residual Land Value Analysis – Brownstown Town Center; Retail; July 2012

Exhibit VII-9 Residual Land Value Analysis – Brownstown Town Center; Office ; July 2012

BROWNSTOWN DDA

I. RECOMMENDATIONS

BROWNSTOWN DDA

Exhibit I-1

RECOMMENDATIONSBROWNSTOWN TOWN CENTER

JUNE 2012

Site Acres 78.04Wetland/Drainage Swale 11.23Developable Acres 66.81

Land Use Option 1

Land Use AcresDensity

(FAR/Lot Size)Total

SF/UnitsRent/Price

/Unit/SF 2013 2014 2015 2016 2017 2018 2019 2020Park/Open Space 8Single-Family Detached 22.5 70x140 60 $200,000 30 30Apartments 12.5 20 Units/Acre 250 $1,100 100 150Retail 17.0 0.25 185,000 $20 55,000 55,000 75,000Office 4.6 0.25 50,000 $16 25,000 25,000Total 64.6

Land Use Option 2

Land Use AcresDensity

(FAR/Lot Size)Total

SF/UnitsRent/Price/

Unit/SF 2013 2014 2015 2016 2017 2018 2019 2020Park/Open Space 8Single-Family Detached 32.6 80x150 71 $225,000 30 30 11Apartments 12.5 20 Units/Acre 250 $1,100 100 150Retail 13.8 0.25 150,000 $20 55,000 55,000 40,000Office 0.0 0.25 0 $16Total 66.9

Old PlanApartments & THs 10 7.2 72Single-Family Detached 14 80-150 23Senior Hsg 12 0.1 37,000Townhomes 2.5 8.0 20Community Center 4.4 0.2 50,000Commercial 15.1 0.2 123,000

58Acres

North of RV 32East of Wetland 12West of Wetland,Behind RV 23Wetlands 11Total 78

SOURCE: RCLCORecs

E6-12962.00Printed: 7/16/2012

BROWNSTOWN DDA

II. SOCIOECONOMICS

BROWNSTOWN DDA

Exhibit II-1

LOCATION MAPBROWNSTOWN TOWNSHIP, WOODHAVEN, AND DOWNRIVER REGION

DOWNRIVER REGION

BROWNSTOWNTOWNSHIP

WOODHAVEN

SOURCE: ESRI Business Analyst; RCLCO

WOODHAVEN

MapE6-12962.00

Printed: 7/16/2012

BROWNSTOWN DDA

Exhibit II-2

COMPARATIVE SOCIOECONOMIC CHARACTERISTICS BROWNSTOWN TOWNSHIP, WOODHAVEN, DOWNRIVER REGION, AND DETROIT MSA

2000 - 2016

BROWNSTOWN DOWNRIVERCHARACTERISTIC TOWNSHIP WOODHAVEN REGION DETROIT MSA

2000 Population (Census) 28,463 12,530 358,447 4,452,5572010 Population (Census) 36,179 12,875 357,259 4,296,2502011 Population (ESRI) 36,242 12,897 355,191 4,267,7312016 Population (ESRI) 35,489 12,493 341,467 4,183,875

Pop. Growth Rate, 2000 - 2010 2.4% 0.3% 0.0% -0.4%Pop. Growth Rate, 2011 - 2016 -0.4% -0.6% -0.8% -0.4%

2000 Households (Census) 10,411 4,708 140,515 1,696,9432010 Households (Census) 13,440 5,159 141,759 1,682,1112011 Households (ESRI) 13,435 5,163 140,805 1,670,9492016 Households (ESRI) 13,224 5,074 136,046 1,647,685

Household Growth Rate, 2000 - 2010 2.6% 0.9% 0.1% -0.1%Household Growth Rate, 2011 - 2016 -0.3% -0.3% -0.7% -0.3%

2011 Household Size 2.70 2.50 2.52 2.55

2011 Per Capita Income $24,286 $28,930 $23,215 $26,2302011 Median Household Income $53,434 $57,146 $45,526 $49,7922011 Average Household Income $64,958 $71,352 $58,005 $66,156

2.4%ANNUAL POPULATION GROWTH RATES, 2000-2016

SOURCE: ESRI Business Analyst; RCLCO

2.6%

-0.3%

0.9%

-0.3%

0.1%

-0.7%-0.1% -0.3%

2000-2010 2011-2016

ANNUAL HOUSEHOLD GROWTH RATES, 2000-2016

Brownstown Township Woodhaven Downriver Detroit MSA

-0.4%

0.3%

-0.6%0.0%

-0.8%-0.4% -0.4%

2000-2010 2011-2016

Brownstown Township Woodhaven Downriver Detroit MSA

Pop and HHsE6-12962.00

Printed: 7/16/2012

BROWNSTOWN DDA

Exhibit II-3

PROJECTED POPULATION GROWTHWAYNE COUNTY EXCLUDING DETROIT

2000 - 2035

1,000

1,050

1,100

1,150

1,200

opul

atio

n (T

hous

ands

)

NOTE: Historical Data per SEMCOG. Economy.com projection based on growth rate for Wayne County.

SOURCE: ESRI Business Analyst; Economy.com; SEMCOG; RCLCO

850

900

950

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

Po

SEMCOG ESRI ECONOMY.COM

Population Proj.E6-12962.00

Printed: 7/16/2012

BROWNSTOWN DDA

Exhibit II-4A

HOUSEHOLDS BY AGE AND INCOMEBROWNSTOWN TOWNSHIP, MI

2010

PROFESSIONALS EMPTY NESTERS RETIREESUNDER 25 25-34 35-44 45-54 55-64 65-74 75 AND OVER TOTAL

INCOME RANGE TOTAL PCT. TOTAL PCT. TOTAL PCT. TOTAL PCT. TOTAL PCT. TOTAL PCT. TOTAL PCT. TOTAL PCT.

Less than $25,000 152 32% 178 8% 195 8% 149 6% 264 12% 323 29% 318 46% 1,579 14%$25,000 - $34,999 64 13% 165 8% 122 5% 108 4% 215 10% 164 15% 97 14% 935 8%$35,000 - $49,999 149 31% 433 20% 283 12% 336 13% 295 13% 243 22% 107 15% 1,846 16%$50,000 - $74,999 54 11% 702 33% 798 33% 726 28% 615 28% 150 14% 61 9% 3,106 27%$75,000 - $99,999 14 3% 398 18% 492 21% 567 22% 273 12% 93 8% 44 6% 1,881 16%

$100,000 - $149,999 26 5% 221 10% 372 16% 579 22% 398 18% 60 5% 20 3% 1,676 14%$150,000 - $199,999 18 4% 23 1% 126 5% 111 4% 122 6% 44 4% 39 6% 483 4%$200,000 - $249,999 3 1% 20 1% 3 0% 10 0% 22 1% 15 1% 8 1% 81 1%$250,000 - $499,999 0 0.0% 12 1% 1 0% 9 0% 9 0% 4 0% 0 0% 35 0%$500,000 and above 0 0.0% 0 0% 0 0% 0 0% 0 0% 0 0% 0 0% 0 0%

TOTAL 480 100% 2,152 100% 2,392 100% 2,595 100% 2,213 100% 1,096 100% 694 100% 11,622 100%Percent of Total 4% 19% 21% 22% 19% 9% 6% 100%

27%

HOUSEHOLDS BY INCOME

21%22%

19%

HOUSEHOLDS BY AGE

SOURCE: ESRI Business Analyst; RCLCO

22%

16% 16%14%

5%

Less than $35,000

$35,000-$49,999

$50,000-$74,999

$75,000-$99,999

$100,000-$149,999

$150,000 and above

4%

19% 19%

9%

6%

Under 25 25-34 35-44 45-54 55-64 65-74 75 and over

Brownstwn AxIE6-12962.00

Printed: 7/16/2012

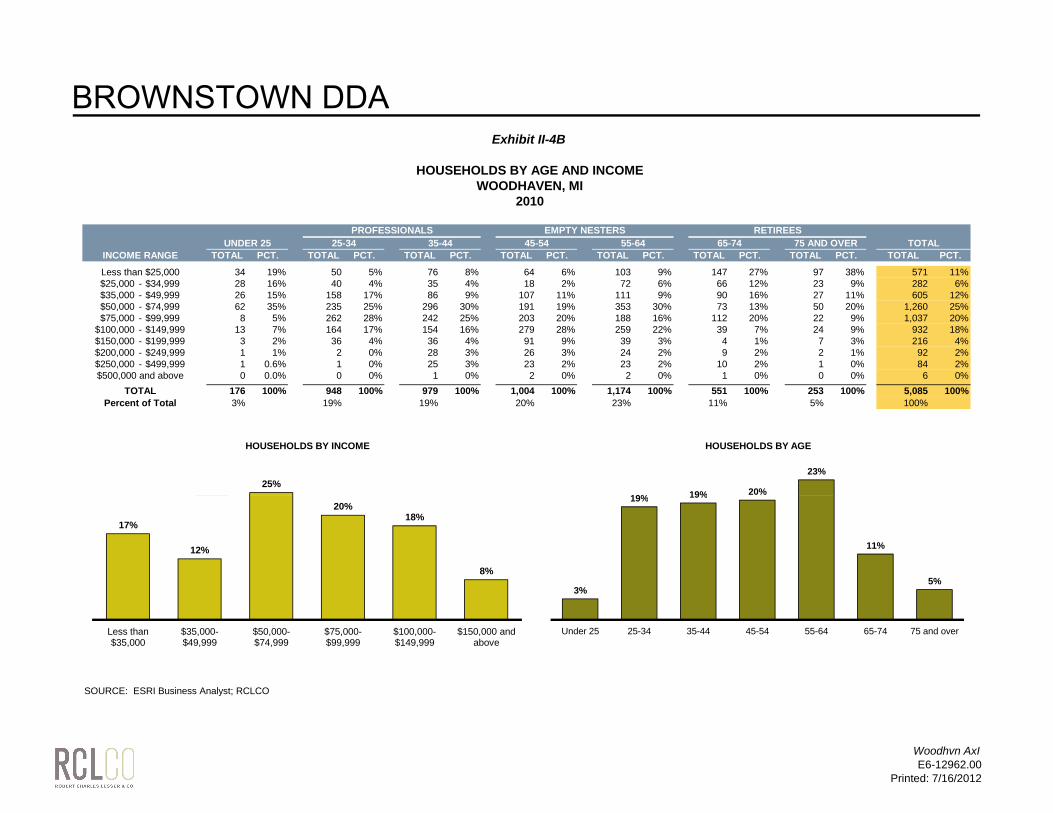

BROWNSTOWN DDA

Exhibit II-4B

HOUSEHOLDS BY AGE AND INCOMEWOODHAVEN, MI

2010

PROFESSIONALS EMPTY NESTERS RETIREESUNDER 25 25-34 35-44 45-54 55-64 65-74 75 AND OVER TOTAL

INCOME RANGE TOTAL PCT. TOTAL PCT. TOTAL PCT. TOTAL PCT. TOTAL PCT. TOTAL PCT. TOTAL PCT. TOTAL PCT.

Less than $25,000 34 19% 50 5% 76 8% 64 6% 103 9% 147 27% 97 38% 571 11%$25,000 - $34,999 28 16% 40 4% 35 4% 18 2% 72 6% 66 12% 23 9% 282 6%$35,000 - $49,999 26 15% 158 17% 86 9% 107 11% 111 9% 90 16% 27 11% 605 12%$50,000 - $74,999 62 35% 235 25% 296 30% 191 19% 353 30% 73 13% 50 20% 1,260 25%$75,000 - $99,999 8 5% 262 28% 242 25% 203 20% 188 16% 112 20% 22 9% 1,037 20%

$100,000 - $149,999 13 7% 164 17% 154 16% 279 28% 259 22% 39 7% 24 9% 932 18%$150,000 - $199,999 3 2% 36 4% 36 4% 91 9% 39 3% 4 1% 7 3% 216 4%$200,000 - $249,999 1 1% 2 0% 28 3% 26 3% 24 2% 9 2% 2 1% 92 2%$250,000 - $499,999 1 0.6% 1 0% 25 3% 23 2% 23 2% 10 2% 1 0% 84 2%$500,000 and above 0 0.0% 0 0% 1 0% 2 0% 2 0% 1 0% 0 0% 6 0%

TOTAL 176 100% 948 100% 979 100% 1,004 100% 1,174 100% 551 100% 253 100% 5,085 100%Percent of Total 3% 19% 19% 20% 23% 11% 5% 100%

25%

HOUSEHOLDS BY INCOME

19% 19% 20%

23%

HOUSEHOLDS BY AGE

25%

HOUSEHOLDS BY INCOME

19% 19% 20%

23%

HOUSEHOLDS BY AGE

SOURCE: ESRI Business Analyst; RCLCO

17%

12%

20%18%

8%

Less than $35,000

$35,000-$49,999

$50,000-$74,999

$75,000-$99,999

$100,000-$149,999

$150,000 and above

3%

19% 19%

11%

5%

Under 25 25-34 35-44 45-54 55-64 65-74 75 and over

17%

12%

20%18%

8%

Less than $35,000

$35,000-$49,999

$50,000-$74,999

$75,000-$99,999

$100,000-$149,999

$150,000 and above

3%

19% 19%

11%

5%

Under 25 25-34 35-44 45-54 55-64 65-74 75 and over

Woodhvn AxIE6-12962.00

Printed: 7/16/2012

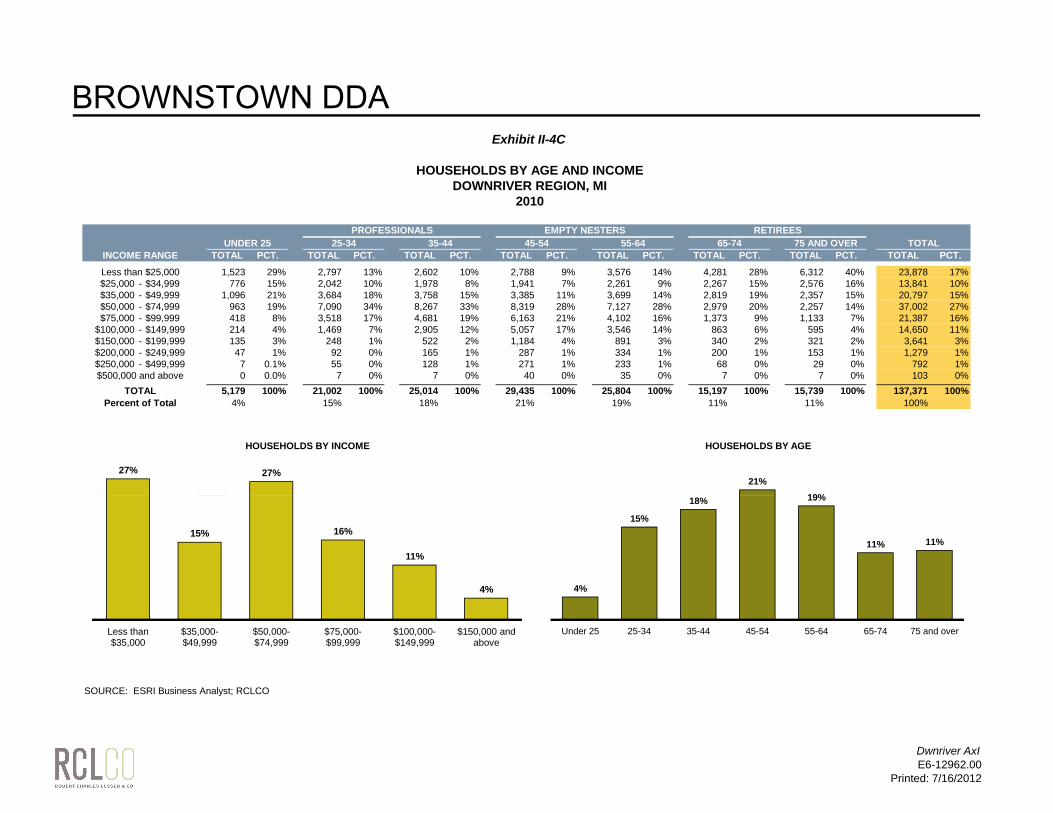

BROWNSTOWN DDA

Exhibit II-4C

HOUSEHOLDS BY AGE AND INCOMEDOWNRIVER REGION, MI

2010

PROFESSIONALS EMPTY NESTERS RETIREESUNDER 25 25-34 35-44 45-54 55-64 65-74 75 AND OVER TOTAL

INCOME RANGE TOTAL PCT. TOTAL PCT. TOTAL PCT. TOTAL PCT. TOTAL PCT. TOTAL PCT. TOTAL PCT. TOTAL PCT.

Less than $25,000 1,523 29% 2,797 13% 2,602 10% 2,788 9% 3,576 14% 4,281 28% 6,312 40% 23,878 17%$25,000 - $34,999 776 15% 2,042 10% 1,978 8% 1,941 7% 2,261 9% 2,267 15% 2,576 16% 13,841 10%$35,000 - $49,999 1,096 21% 3,684 18% 3,758 15% 3,385 11% 3,699 14% 2,819 19% 2,357 15% 20,797 15%$50,000 - $74,999 963 19% 7,090 34% 8,267 33% 8,319 28% 7,127 28% 2,979 20% 2,257 14% 37,002 27%$75,000 - $99,999 418 8% 3,518 17% 4,681 19% 6,163 21% 4,102 16% 1,373 9% 1,133 7% 21,387 16%

$100,000 - $149,999 214 4% 1,469 7% 2,905 12% 5,057 17% 3,546 14% 863 6% 595 4% 14,650 11%$150,000 - $199,999 135 3% 248 1% 522 2% 1,184 4% 891 3% 340 2% 321 2% 3,641 3%$200,000 - $249,999 47 1% 92 0% 165 1% 287 1% 334 1% 200 1% 153 1% 1,279 1%$250,000 - $499,999 7 0.1% 55 0% 128 1% 271 1% 233 1% 68 0% 29 0% 792 1%$500,000 and above 0 0.0% 7 0% 7 0% 40 0% 35 0% 7 0% 7 0% 103 0%

TOTAL 5,179 100% 21,002 100% 25,014 100% 29,435 100% 25,804 100% 15,197 100% 15,739 100% 137,371 100%Percent of Total 4% 15% 18% 21% 19% 11% 11% 100%

27% 27%

HOUSEHOLDS BY INCOME

21%19%

HOUSEHOLDS BY AGE

27% 27%

HOUSEHOLDS BY INCOME

21%19%

HOUSEHOLDS BY AGE

SOURCE: ESRI Business Analyst; RCLCO

15% 16%

11%

4%

Less than $35,000

$35,000-$49,999

$50,000-$74,999

$75,000-$99,999

$100,000-$149,999

$150,000 and above

4%

15%

18% 19%

11% 11%

Under 25 25-34 35-44 45-54 55-64 65-74 75 and over

15% 16%

11%

4%

Less than $35,000

$35,000-$49,999

$50,000-$74,999

$75,000-$99,999

$100,000-$149,999

$150,000 and above

4%

15%

18% 19%

11% 11%

Under 25 25-34 35-44 45-54 55-64 65-74 75 and over

Dwnriver AxIE6-12962.00

Printed: 7/16/2012

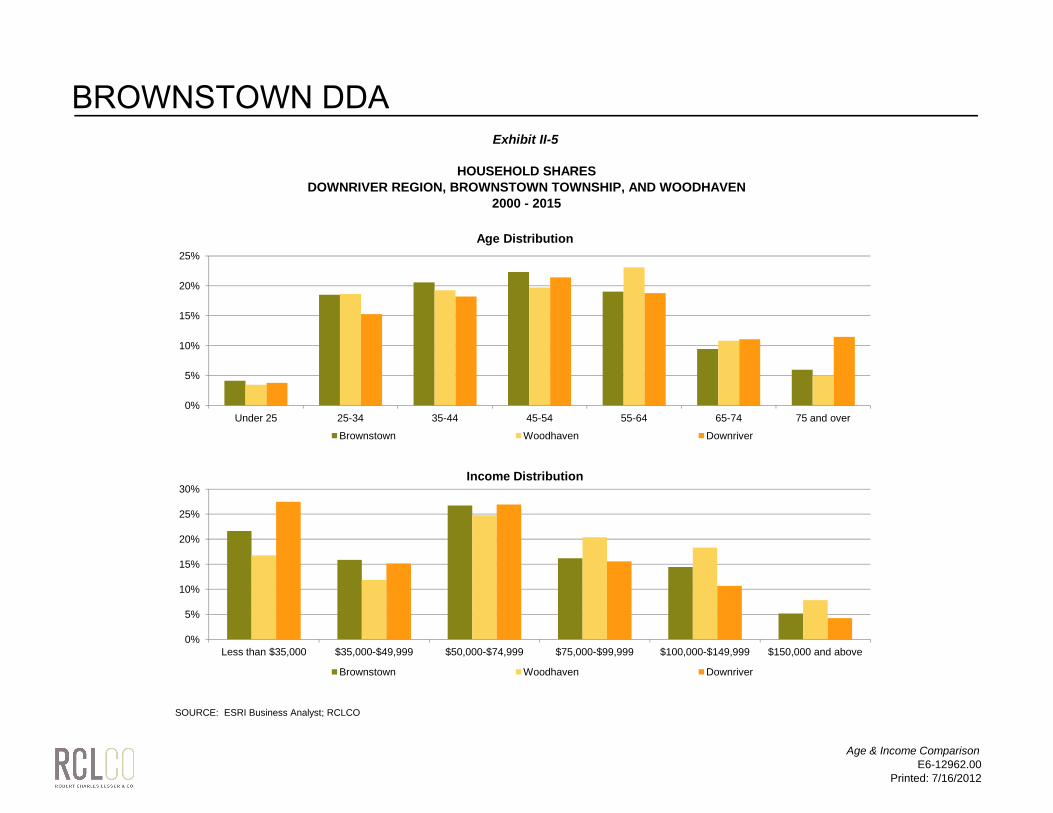

BROWNSTOWN DDA

Exhibit II-5

HOUSEHOLD SHARESDOWNRIVER REGION, BROWNSTOWN TOWNSHIP, AND WOODHAVEN

2000 - 2015

0%

5%

10%

15%

20%

25%

Under 25 25-34 35-44 45-54 55-64 65-74 75 and over

Age Distribution

Brownstown Woodhaven Downriver

30%Income Distribution

SOURCE: ESRI Business Analyst; RCLCO

0%

5%

10%

15%

20%

25%

Less than $35,000 $35,000-$49,999 $50,000-$74,999 $75,000-$99,999 $100,000-$149,999 $150,000 and above

Brownstown Woodhaven Downriver

Age & Income ComparisonE6-12962.00

Printed: 7/16/2012

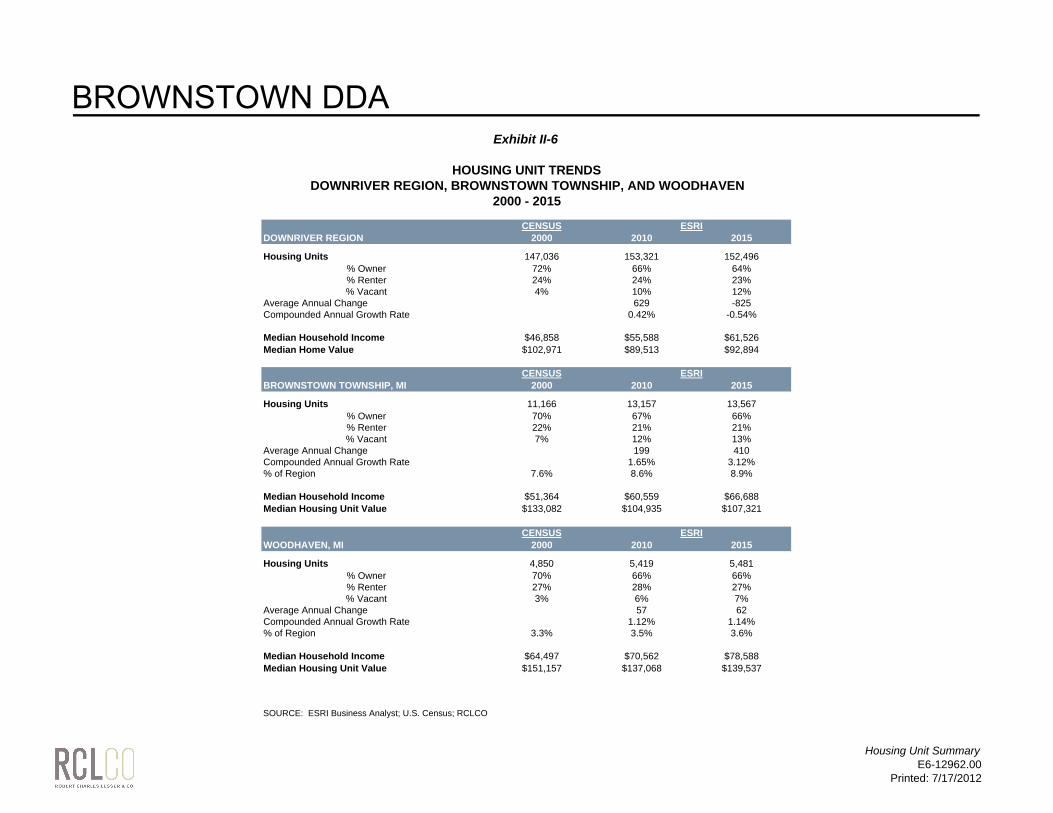

BROWNSTOWN DDA

CENSUSDOWNRIVER REGION 2000 2010 2015

Housing Units 147,036 153,321 152,496% Owner 72% 66% 64%% Renter 24% 24% 23%% Vacant 4% 10% 12%

Average Annual Change 629 -825Compounded Annual Growth Rate 0.42% -0.54%

Median Household Income $46,858 $55,588 $61,526Median Home Value $102,971 $89,513 $92,894

CENSUSBROWNSTOWN TOWNSHIP, MI 2000 2010 2015

Housing Units 11,166 13,157 13,567% Owner 70% 67% 66%% Renter 22% 21% 21%% Vacant 7% 12% 13%

Average Annual Change 199 410Compounded Annual Growth Rate 1.65% 3.12%% of Region 7.6% 8.6% 8.9%

Median Household Income $51,364 $60,559 $66,688Median Housing Unit Value $133,082 $104,935 $107,321

CENSUSWOODHAVEN, MI 2000 2010 2015

Housing Units 4,850 5,419 5,481% Owner 70% 66% 66%% Renter 27% 28% 27%% Vacant 3% 6% 7%

Average Annual Change 57 62Compounded Annual Growth Rate 1.12% 1.14%% of Region 3.3% 3.5% 3.6%

Median Household Income $64,497 $70,562 $78,588Median Housing Unit Value $151,157 $137,068 $139,537

SOURCE: ESRI Business Analyst; U.S. Census; RCLCO

ESRI

ESRI

Exhibit II-6

HOUSING UNIT TRENDSDOWNRIVER REGION, BROWNSTOWN TOWNSHIP, AND WOODHAVEN

2000 - 2015

ESRI

Housing Unit SummaryE6-12962.00

Printed: 7/17/2012

BROWNSTOWN DDA

Exhibit II-7A

COMPOUND ANNUAL GROWTH RATESDOWNRIVER REGION, BROWNSTOWN TOWNSHIP, AND WOODHAVEN

2000 - 2015

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

$90,0002000 2010 2015

Downriver Region Median Income Brownstown Township Median Income Woodhaven Median Income

$160,000.002000 2010 2015

SOURCE: ESRI Business Analyst; U.S. Census; RCLCO

$0.00

$20,000.00

$40,000.00

$60,000.00

$80,000.00

$100,000.00

$120,000.00

$140,000.00

Downriver Region Median HV Brownstown Township Median HV Woodhaven Median HV

HU and Income GraphsE6-12962.00

Printed: 7/17/2012

BROWNSTOWN DDA

Exhibit II-7B

HOUSEHOLD SHARESDOWNRIVER REGION, BROWNSTOWN TOWNSHIP, AND WOODHAVEN

2000 - 2015

72% 66% 64%

24% 24% 23%

4% 10% 12%

0%

20%

40%

60%

80%

100%2000 2010 2015

Downriver Region Vacant % Downriver Region Renter % Downriver Region Owner %

70% 67% 66%

22% 21% 21%

7% 12% 13%

40%

60%

80%

100%2000 2010 2015

SOURCE: ESRI Business Analyst; U.S. Census; RCLCO

0%

20%

Brownstown Vacant % Brownstown Renter % Brownstown Owner %

70% 66% 66%

27% 28% 27%

3% 6% 7%

0%

20%

40%

60%

80%

100%2000 2010 2015

Woodhaven Vacant % Woodhaven Renter % Woodhaven Owner %

HU Split GraphsE6-12962.00

Printed: 7/17/2012

BROWNSTOWN DDA

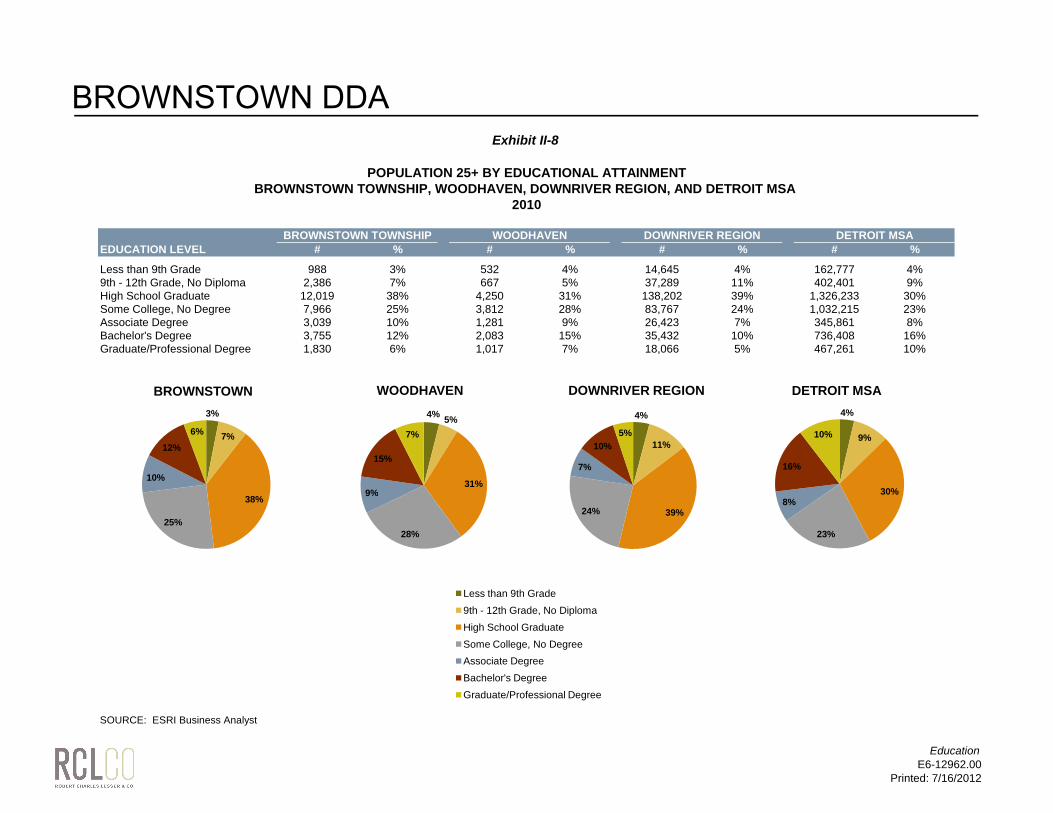

Exhibit II-8

POPULATION 25+ BY EDUCATIONAL ATTAINMENTBROWNSTOWN TOWNSHIP, WOODHAVEN, DOWNRIVER REGION, AND DETROIT MSA

2010

EDUCATION LEVEL # % # % # % # %

Less than 9th Grade 988 3% 532 4% 14,645 4% 162,777 4%9th - 12th Grade, No Diploma 2,386 7% 667 5% 37,289 11% 402,401 9%High School Graduate 12,019 38% 4,250 31% 138,202 39% 1,326,233 30%Some College, No Degree 7,966 25% 3,812 28% 83,767 24% 1,032,215 23%Associate Degree 3,039 10% 1,281 9% 26,423 7% 345,861 8%Bachelor's Degree 3,755 12% 2,083 15% 35,432 10% 736,408 16%Graduate/Professional Degree 1,830 6% 1,017 7% 18,066 5% 467,261 10%

BROWNSTOWN TOWNSHIP WOODHAVEN DOWNRIVER REGION DETROIT MSA

3%

7%

10%

12%6%

BROWNSTOWN 4% 5%

31%9%

15%

7%

WOODHAVEN

4%

11%

7%

10%5%

DOWNRIVER REGION4%

9%

30%

16%

10%

DETROIT MSA

SOURCE: ESRI Business Analyst

38%

25%28%

9%

39%24%

23%

8%

Less than 9th Grade9th - 12th Grade, No DiplomaHigh School GraduateSome College, No DegreeAssociate DegreeBachelor's DegreeGraduate/Professional Degree

EducationE6-12962.00

Printed: 7/16/2012

BROWNSTOWN DDA

Exhibit II-9

INBOUND AND OUTBOUND MIGRATIONWAYNE COUNTY, MI

2010

SOURCE: IRS; US Census; RCLCO

MigrationE6-12962.00

Printed: 7/16/2012

BROWNSTOWN DDA

Exhibit II-10

PLACE OF EMPLOYMENT BY ZIP CODERESIDENTS LIVING IN BROWNSTOWN TOWNSHIP

2010

TOTAL EMPLOYEES

500+

250 - 499

100 - 249

Less than 100

SOURCE: U.S. Census; MapPoint

Where Residents WorkE6-12962.00

Printed: 7/16/2012

BROWNSTOWN DDA

Exhibit II-11

PLACE OF RESIDENCE BY ZIP CODEEMPLOYEES WORKING IN BROWNSTOWN TOWNSHIP

2010

TOTAL RESIDENTS

250+

100 - 249

Less than 100

SOURCE: U.S. Census; MapPoint

Where Emp. LiveE6-12962.00

Printed: 7/16/2012

BROWNSTOWN DDA

Exhibit II-12

PROJECTED EMPLOYMENT GROWTHWAYNE COUNTY EXCLUDING DETROIT

2000 - 2035

580

585

590

595

600

605

610

ploy

men

t (Th

ousa

nds)

NOTE: Historical Data per SEMCOG. Economy.com projection based on growth rate for Wayne County.

SOURCE: ESRI Business Analyst; Economy.com; SEMCOG; RCLCO

560

565

570

575

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

Emp

SEMCOG ECONOMY.COM

Employmt Proj.E6-12962.00

Printed: 7/16/2012

BROWNSTOWN DDA

Exhibit II-13

HOUSEHOLD ANNUAL GROWTH RATE BY BLOCK GROUPBROWNSTOWN TOWNSHIP, MI

2000 - 2010

SOURCE: Esri Business Analyst

HH Growth 2000-2010E6-12962.00

Printed: 7/16/2012

BROWNSTOWN DDA

Exhibit II-14

HOUSEHOLD ANNUAL GROWTH RATE BY BLOCK GROUPBROWNSTOWN TOWNSHIP, MI

2010 - 2015

SOURCE: Esri Business Analyst

HH Growth 2010-2015E6-12962.00

Printed: 7/16/2012

BROWNSTOWN DDA

Exhibit II-15

HOUSEHOLD DENSITY BY BLOCK GROUPBROWNSTOWN TOWNSHIP, MI

2010

Density = Housholds/Square MileSOURCE: Esri Business Analyst

HH Density 2010E6-12962.00

Printed: 7/16/2012

BROWNSTOWN DDA

Exhibit II-16

MEDIAN HOUSEHOLD INCOME BY BLOCK GROUPBROWNSTOWN TOWNSHIP, MI

2010

SOURCE: Esri Business Analyst

Med HH Inc 2010E6-12962.00

Printed: 7/16/2012

BROWNSTOWN DDA

Exhibit II-17

MEDIAN AGE BY BLOCK GROUPBROWNSTOWN TOWNSHIP, MI

2010

SOURCE: Esri Business Analyst

Med Age 2010E6-12962.00

Printed: 7/16/2012

BROWNSTOWN DDA

Exhibit II-18

MEDIAN HOME VALUES BY BLOCK GROUPBROWNSTOWN TOWNSHIP, MI

2010

SOURCE: Esri Business Analyst

Med HV 2010E6-12962.00

Printed: 7/16/2012

BROWNSTOWN DDA

Exhibit II-19

EMPLOYMENT DENSITY BY BLOCK GROUPBROWNSTOWN TOWNSHIP, MI

2010

Density = Employees/Square MileSOURCE: Esri Business Analyst

Employment Density 2010E6-12962.00

Printed: 7/16/2012

BROWNSTOWN DDA

Exhibit II-20

PERCENT OF RENTER OCCUPIED HOUSING UNITS BY BLOCK GROUPBROWNSTOWN TOWNSHIP, MI

2010

SOURCE: Esri Business Analyst

Renter Percentage 2010E6-12962.00

Printed: 7/16/2012

BROWNSTOWN DDA

Exhibit II-21

NUMBER OF EMPLOYEESBROWNSTOWN TOWNSHIP, MI

2010

SOURCE: Esri Business Analyst

Business CentersE6-12962.00

Printed: 7/16/2012

BROWNSTOWN DDA

Exhibit II-22

SHOPPING CENTERSBROWNSTOWN TOWNSHIP, MI

2010

SOURCE: Esri Business Analyst

Retail CentersE6-12962.00

Printed: 7/16/2012

BROWNSTOWN DDA

III. RESIDENTIAL

BROWNSTOWN DDA

Exhibit III-1A

HISTORICAL SINGLE-FAMILY AND MULTIFAMILY PERMITSDETROIT MSA

1990 - YTD 2012

10,841 10,56212,089 12,801

14,743 15,51017,157 16,322

17,950 17,224 16,06514,009 15,208 16,334 17,399

13,631

7,468

3,8331,937 1261 2,430 2,854

638

4,6362,976

26622,654

3,679 3,276

3,7942,837

4,3803,355

3,248

3,5573,826

3,5664,409

2,761

1,452

492

65372

780504

354

YTDLAND USE 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 1

RESIDENTIAL-BUILDING PERMITSSingle-Family 10,841 10,562 12,089 12,801 14,743 15,510 17,157 16,322 17,950 17,224 16,065 14,009 15,208 16,334 17,399 13,631 7,468 3,833 1,937 1261 2,430 2,854 638Multifamily 4,636 2,976 2662 2,654 3,679 3,276 3,794 2,837 4,380 3,355 3,248 3,557 3,826 3,566 4,409 2,761 1,452 492 653 72 780 504 354TOTAL 15,477 13,538 14,751 15,455 18,422 18,786 20,951 19,159 22,330 20,579 19,313 17,566 19,034 19,900 21,808 16,392 8,920 4,325 2,590 1,333 3,210 3,358 992

Annual Change -- -1,939 1,213 704 2,967 364 2,165 -1,792 3,171 -1,751 -1,266 -1,747 1,468 866 1,908 -5,416 -7,472 -4,595 -1,735 -1,257 1,877 148MF as % of Total 30% 22% 18% 17% 20% 17% 18% 15% 20% 16% 17% 20% 20% 18% 20% 17% 16% 11% 25% 5% 24% 15%

1 YTD 2012 through March.

SOURCE: U.S. Department of Housing and Urban Development; RCLCO

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

SINGLE-FAMILY MULTIFAMILY

Permits - MSAE6-12962.00

Printed: 7/16/2012

BROWNSTOWN DDA

Exhibit III-1B

HISTORICAL SINGLE-FAMILY AND MULTIFAMILY PERMITSWAYNE COUNTY, MI

1990 - YTD 2012

1,874 2,058 2,090 2,1902,676 2,795 3,100 3,113 3,347 3,124 2,939 3,006

3,388 3,7294,211

3,138

2,056

919524 264 470 476 93

1,257 7691094 1,185

1,101 743

1,293661

1,5021,063 1,143 1,255

1,454

1,909

2,106

1,436

378

176 37124 265 229 0

YTDLAND USE 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 1

RESIDENTIAL-BUILDING PERMITSSingle-Family 1,874 2,058 2,090 2,190 2,676 2,795 3,100 3,113 3,347 3,124 2,939 3,006 3,388 3,729 4,211 3,138 2,056 919 524 264 470 476 93Multifamily 1,257 769 1094 1,185 1,101 743 1,293 661 1,502 1,063 1,143 1,255 1,454 1,909 2,106 1,436 378 176 371 24 265 229 0TOTAL 3,131 2,827 3,184 3,375 3,777 3,538 4,393 3,774 4,849 4,187 4,082 4,261 4,842 5,638 6,317 4,574 2,434 1,095 895 288 735 705 93

Annual Change -- -304 357 191 402 -239 855 -619 1,075 -662 -105 179 581 796 679 -1,743 -2,140 -1,339 -200 -607 447 -30MF as % of Total 40% 27% 34% 35% 29% 21% 29% 18% 31% 25% 28% 29% 30% 34% 33% 31% 16% 16% 41% 8% 36% 32%

1 YTD 2012 through March.

SOURCE: U.S. Department of Housing and Urban Development; RCLCO

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

SINGLE-FAMILY MULTIFAMILY

Permits - WayneE6-12962.00

Printed: 7/16/2012

BROWNSTOWN DDA

Exhibit III-1C

HISTORICAL SINGLE-FAMILY AND MULTIFAMILY PERMITSBROWNSTOWN TOWNSHIP, MI

1990 - YTD 2012

40 67 54 52

165

274 305253

315

451

330413

356 347 385

237 262

58 25 25 35 56 82

0 0 0

0

0 160

56

22

96

64

64

388261

2444

66 0 9 0 0

YTDLAND USE 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 1

RESIDENTIAL-BUILDING PERMITSSingle-Family 40 67 54 52 165 274 305 253 315 451 330 413 356 347 385 237 262 58 25 25 35 56 8Multifamily 2 0 0 0 0 0 16 0 56 22 96 64 64 388 261 24 44 6 6 0 9 0 0TOTAL 42 67 54 52 165 274 321 253 371 473 426 477 420 735 646 261 306 64 31 25 44 56 8

Annual Change -- 25 -13 -2 113 109 47 -68 118 102 -47 51 -57 315 -89 -385 45 -242 -33 -6 19 12MF as % of Total 5% 0% 0% 0% 0% 0% 5% 0% 15% 5% 23% 13% 15% 53% 40% 9% 14% 9% 19% 0% 20% 0%

1 YTD 2012 through March.

SOURCE: U.S. Department of Housing and Urban Development; RCLCO

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

SINGLE-FAMILY MULTIFAMILY

Permits - BrownstownE6-12962.00

Printed: 7/16/2012

BROWNSTOWN DDA

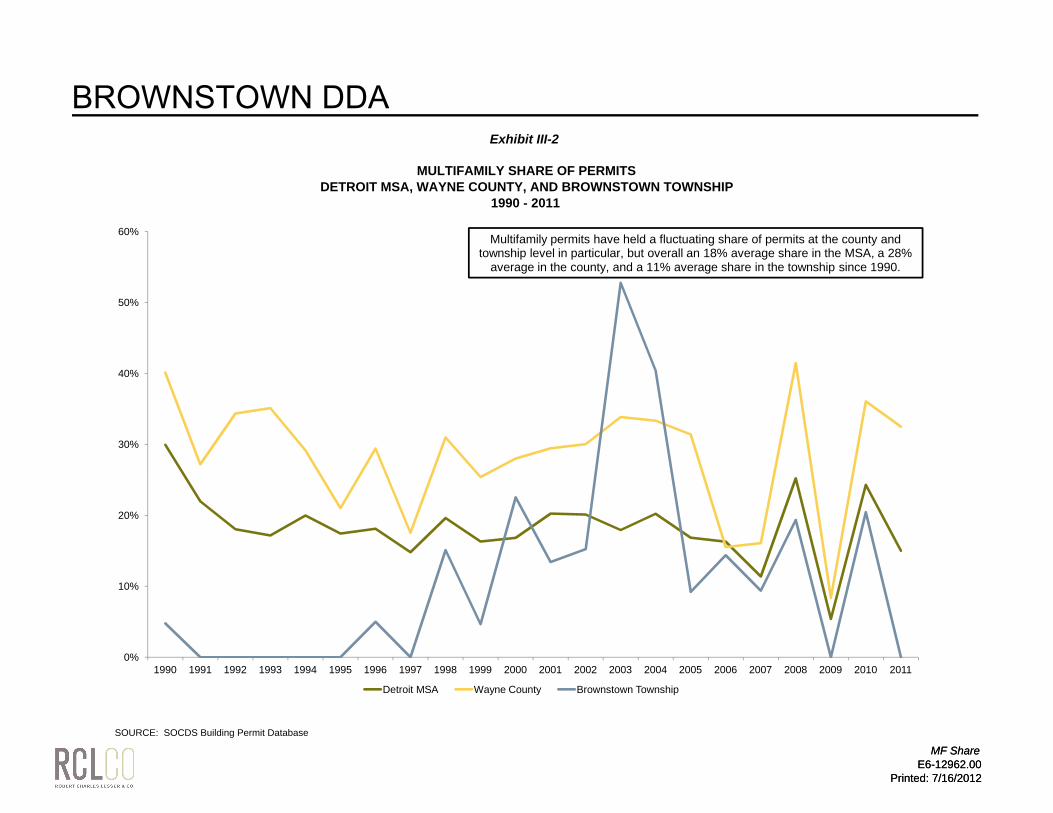

Exhibit III-2

MULTIFAMILY SHARE OF PERMITSDETROIT MSA, WAYNE COUNTY, AND BROWNSTOWN TOWNSHIP

1990 - 2011

30%

40%

50%

60%Multifamily permits have held a fluctuating share of permits at the county and

township level in particular, but overall an 18% average share in the MSA, a 28% average in the county, and a 11% average share in the township since 1990.

MF ShareE6-12962.00

Printed: 7/16/2012

SOURCE: SOCDS Building Permit Database

0%

10%

20%

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Detroit MSA Wayne County Brownstown Township

MF ShareE6-12962.00

Printed: 7/16/2012

BROWNSTOWN DDA

Exhibit III-3

GEOGRAPHIC SHARE OF PERMITSBROWNSTOWN TOWNSHIP, WAYNE COUNTY, AND DETROIT MSA

1990 - 2011

15%

20%

25%

30%

35%

40%

45%

50%Wayne County permits hold an increasing share of the MSA's

permits; Brownstown Township also has an increasing share of the County's permits from 1990 to 2011.

Geographic SharesE6-12962.00

Printed: 7/16/2012

SOURCE: SOCDS Building Permit Database

0%

5%

10%

15%

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011Wayne Co. % of MSA Brownstown Township % of County Linear (Wayne Co. % of MSA) Linear (Brownstown Township % of County)

Geographic SharesE6-12962.00

Printed: 7/16/2012

BROWNSTOWN DDA

Exhibit III-4

TOTAL NEW HOME SALES AND PERCENTAGE DISTRIBUTION BY PRICE RANGEBROWNSTOWN TOWNSHIP

2004 - YTD 2012

0

50

100

150

200

250

300

350

400

2004 2005 2006 2007 2008 2009 2010 2011 2012

Tota

l Sal

es

$300,000+

$250,000 - $300,000

$200,000 - $250,000

$150,000 - $200,000

Under $150,000

90%100%

$300 000

357 348311

145

52 41 3557

21

SOURCE: Brownstown Township Appraiser; RCLCO

0%10%20%30%40%50%60%70%80%

2004 2005 2006 2007 2008 2009 2010 2011 2012

Tota

l Sal

es

$300,000+

$250,000 - $300,000

$200,000 - $250,000

$150,000 - $200,000

Under $150,000

New Home SalesE6-12962.00

Printed: 7/16/2012

BROWNSTOWN DDA

Exhibit III-5

TOTAL HOME SALES BY PRICE RANGEBROWNSTOWN TOWNSHIP AND DOWNRIVER REGION

2Q 2008 - 1Q 2012

0

20

40

60

80

100

120

2Q 2009 3Q 2009 4Q 2009 1Q 2010 2Q 2010 3Q 2010 4Q 2010 1Q 2011 2Q 2011 3Q 2011 4Q 2011 1Q 2012

Tota

l Sal

es

Brownstown

$200,000 - $300,000

$100,000 - $200,000

$75,000 - $100,000

Under $75,000

1400Downriver

SOURCE: Real Estate One; RCLCO

0

200

400

600

800

1000

1200

2Q2008 3Q2008 4Q2008 1Q2009 2Q 20093Q 20094Q 20091Q 20102Q 20103Q 20104Q 2010 1Q 2011 2Q 2011 3Q 2011 4Q 2011 1Q 2012

Tota

l Sal

es

$300K+

$200K-$300K

$100K-$200K

$75K-$100K

Under $75,000

Home SalesE6-12962.00

Printed: 7/16/2012

BROWNSTOWN DDA

Exhibit III-6

INVENTORY ANALYSIS OF VACANT DEVELOPED LOTSBROWNSTOWN TOWNSHIP

MAY 25, 2012

Single-Family Subdivision

Vacant Platted

Lots YearBrownstown

New Home Sales

Year End Remaining Inventory

Year End Remaining Inventory

W/O DelWebb2004 357

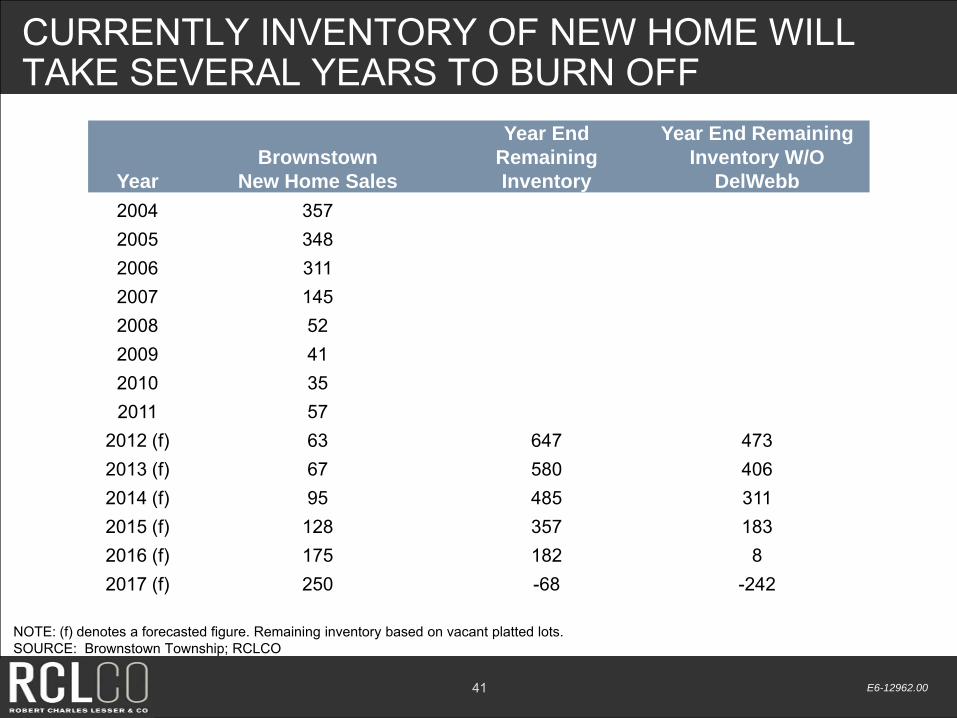

Bonks Bay 11 2005 348Bridgewater -- Del Webb 174 2006 311Bryce Commons 44 2007 145Cambridge Meadows 13 2008 52Cattail Creek 3 2009 41Crystal Crossing 30 2010 35Flowers Creek 0 2011 57Forest Heights 0 2012 63 647 473Fox Creek 95 2013 67 580 406Huron Pointe 21 2014 95 485 311Kensington Estates 0 2015 128 357 183Meadow Brook Village 0 2016 175 182 8Oakwood Estates 2 2017 250 -68 -242Pheasant Run 5Prairie Creek 93Oak Leaf 10Riverfront Estates 0River Valley 0ySilver Creek 12Smith Creek 0Spring Gate 0Stefano Meadows 0Timber Creek 117Wellington Estates 74Whispering Heights 4Woodcreek Meadows 8Woodland Heights 0Woodside Village 0Wheatland Estates 15Total 731

SOURCE: Brownstown Township; RCLCO

InventoryE6-12962.00

Printed: 7/17/2012

BROWNSTOWN DDA

Exhibit III-7

BROWNSTOWN TOTAL HOME SALES BY PRICE RANGE AS A PERCENT OF THE DOWNRIVER REGIONBROWNSTOWN TOWNSHIP AND DOWNRIVER REGION

2Q 2009 - 1Q 2012

40%

50%

60%

70%

80%

90%

Perc

ent o

f Sal

es

Under $75,000

$75K-$100K

$100K-$200K

$200K-$300K

SOURCE: Real Estate One; RCLCO

0%

10%

20%

30%

2Q 2009 3Q 2009 4Q 2009 1Q 2010 2Q 2010 3Q 2010 4Q 2010 1Q 2011 2Q 2011 3Q 2011 4Q 2011 1Q 2012

BT as % of DRE6-12962.00

Printed: 7/16/2012

BROWNSTOWN DDA

Exhibit III-8

PERCENTAGE BREAKDOWN OF HOME SALES BY PRICE RANGEBROWNSTOWN TOWNSHIP AND DOWNRIVER REGION

2Q 2009 - 1Q 2012

0%10%20%30%40%50%60%70%80%90%

100%

2Q 2009 3Q 2009 4Q 2009 1Q 2010 2Q 2010 3Q 2010 4Q 2010 1Q 2011 2Q 2011 3Q 2011 4Q 2011 1Q 2012

Perc

ent o

f Sal

es

BROWNSTOWN

$200,000 - $300,000

$100,000 - $200,000

$75,000 - $100,000

Under $75,000

90%100%

DOWNRIVER

SOURCE: Real Estate One; RCLCO

0%10%20%30%40%50%60%70%80%90%

2Q2008 3Q2008 4Q2008 1Q2009 2Q 20093Q 20094Q 20091Q 20102Q 20103Q 20104Q 2010 1Q 2011 2Q 2011 3Q 2011 4Q 2011 1Q 2012

Perc

ent o

f Sal

es

$300K+

$200K-$300K

$100K-$200K

$75K-$100K

Under $75,000

Home sales %E6-12962.00

Printed: 7/16/2012

BROWNSTOWN DDA

MAP KEY PROJECT NAME

AVG.PRICE

AVG.$/SF

SINGLE-FAMILY DETACHED

1 CELTIC FARMS $182,400 $822 WHEATLAND ESTATES $264,950 $1233 KENSINGTON ESTATES $280,400 $1134 FOX CREEK $212,400 $1065 BRIDGEWATER $222,740 $1086 FALKIRK $205,400 $937 BRYCE COMMONS $224,450 $948 TIMBERCREEK $202,500 $909 BRADBURY PARK - PRESERVES $187,400 $9210 PRAIRIE CREEK 1 $168,400 $8711 ROLLING RIDGE N/A N/A12 OAKWOOD FARMS N/A N/A13 CYRSTAL CROSSING N/A N/A14 HURON POINTE $229,999 $89

Exhibit III-9

FOR SALE COMMUNITIES MAPDETROIT DOWNRIVER REGION

2012

35 8

7

10

4

3

5

4

For-Sale Comp MapE6-12962.00

Printed: 7/16/2012

ATTACHED/CONDOMINIUMS

1 BRADBURY PARK - THE COVES $150,000 $942 PINE ARBOR CONDOMINIUMS N/A N/A3 PARKLANE TOWNHOMES N/A N/A4 TRENTON GRANDE N/A N/A5 DOVES POINTE N/A N/A

SOURCE: Google Maps; RCLCO

12

35 8

6

9

11

13

14

1

2

12

For-Sale Comp MapE6-12962.00

Printed: 7/16/2012

BROWNSTOWN DDA

1/1/2012

Project Year Open

Total Active Units Units Sold

Units Sold YTD 2012

2011 Hist. Annual

Absorption

2012 Annual

AbsorptionLot Front

Size

Average Home Price

AverageHome Price

Price Change

ACTIVELY-SELLING

1 CELTIC FARMS N/A 46 N/A N/A N/A N/A N/A $169,900 - $194,900 $182,400 N/A - N/A N/A N/A 1,900 - 2,635 $89 - $74Huron River and InksterMI Home Builders

2 WHEATLAND ESTATES N/A 46 N/A 1 N/A 2 N/A $189,900 - $340,000 $264,950 $234,900 - $429,900 $332,400 -20% 1,720 - 2,493 $110 - $136Van Horn and InksterMJC Companies

3 KENSINGTON ESTATES N/A 69 N/A N/A 1 N/A N/A $209,900 - $350,900 $280,400 N/A - N/A N/A N/A 1,624 - 3,614 $129 - $97West and InksterMJC Companies